What’s hot, what’s new? Andrew Lowe ING Australia November 2006

What’s hot, what’s new? Andrew Lowe ING Australia November 2006.

Dec 17, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

What’s hot, what’s new?

Andrew Lowe

ING Australia

November 2006

What’s hot, what’s new?

• Contribution limits

• Tax-free benefits

• Contribution splitting

• Transition to retirement

• Life insurance via superannuation

• Superannuation death benefits

• Employer ETPs

• Social security and aged care

Budget consultation outcome

• Consultation ended on 9 October 2006– Over 1500 submissions on superannuation

proposals received

• Government issued its response on 5 September 2006

• All outstanding proposals require safe legislative passage and may be subject to change

Taxable contributions cap

• Proposal effective 1 July 2007• Replaces age based deduction limits• Annual cap of $50,000 (indexed) per person

– If aged 50 or more, a transitional limit of $100,000 applies up to and including 2011/12

• Not a ‘deduction limit’• No $5,000 + 75% formula • New time limit on 82AAT notices• Revised penalties apply for breaching

Taxable contributions cap

• Surplus taxable contributions ‘effectively’ taxed at highest MTR– 31.5% personal tax liability on top of 15% contributions tax

– May request release of super to pay for tax liability

– ATO discretion available for inadvertent breaches

• Surplus contributions also counts towards post-tax contributions limits

Post-tax contributions caps

* Can bring forward next two years entitlements if under age 65 (3-year averaging)

10

May

20

06

No limit $1,000,000 limit $150,000 per financial year limit*

1 J

uly

20

07

Post-tax contributions caps

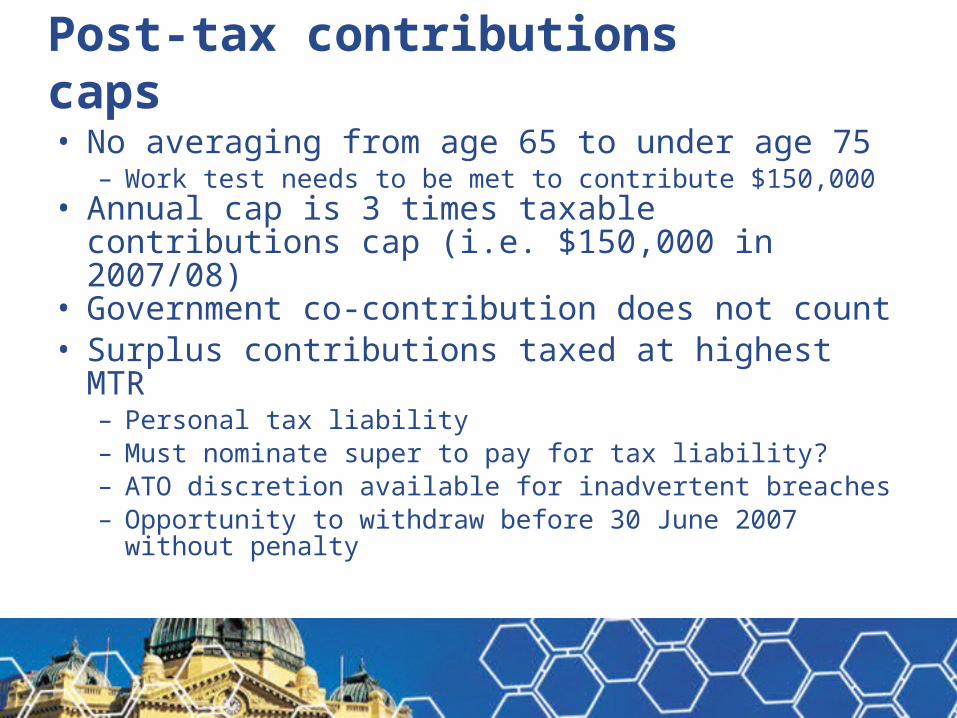

• No averaging from age 65 to under age 75– Work test needs to be met to contribute $150,000

• Annual cap is 3 times taxable contributions cap (i.e. $150,000 in 2007/08)

• Government co-contribution does not count• Surplus contributions taxed at highest MTR

– Personal tax liability– Must nominate super to pay for tax liability?– ATO discretion available for inadvertent breaches– Opportunity to withdraw before 30 June 2007 without

penalty

3-year averaging

Year Scenario A Scenario B Scenario C Scenario D

1 -

2 $450,000

3 -

4 -

$150,000

$450,000

-

-

$350,000

-

$100,000

$150,000 (or up to $450,000)

$450,000

-

-

$150,000(or up to $450,000)

• Annual limit works on a ‘use it or lose it’ basis

Post-tax contributions caps

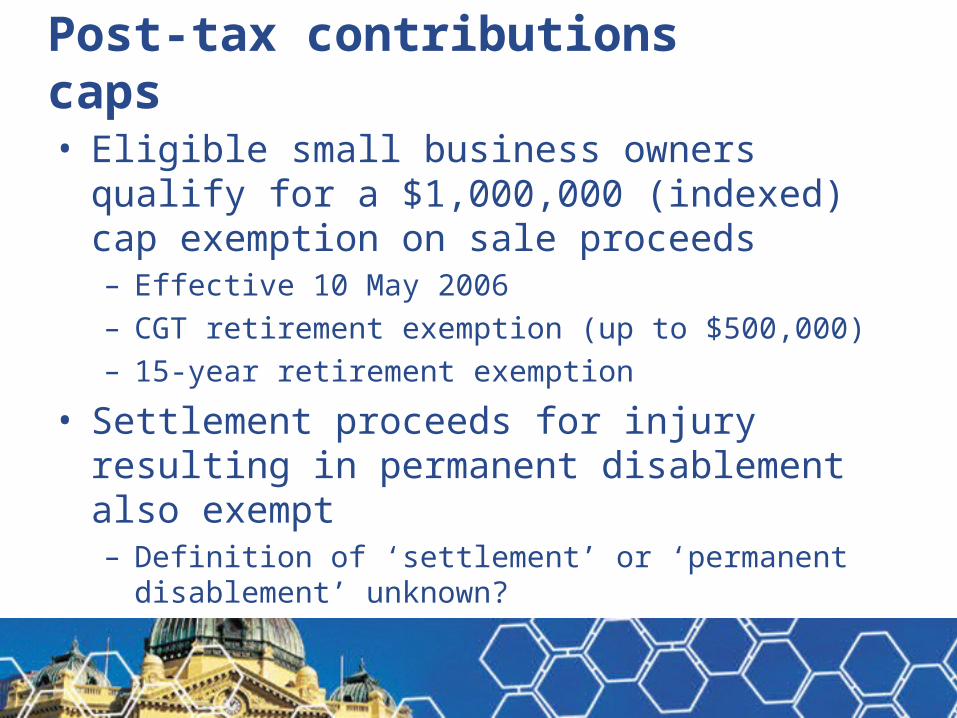

• Eligible small business owners qualify for a $1,000,000 (indexed) cap exemption on sale proceeds– Effective 10 May 2006

– CGT retirement exemption (up to $500,000)

– 15-year retirement exemption

• Settlement proceeds for injury resulting in permanent disablement also exempt– Definition of ‘settlement’ or ‘permanent disablement’

unknown?

RBLs abolished

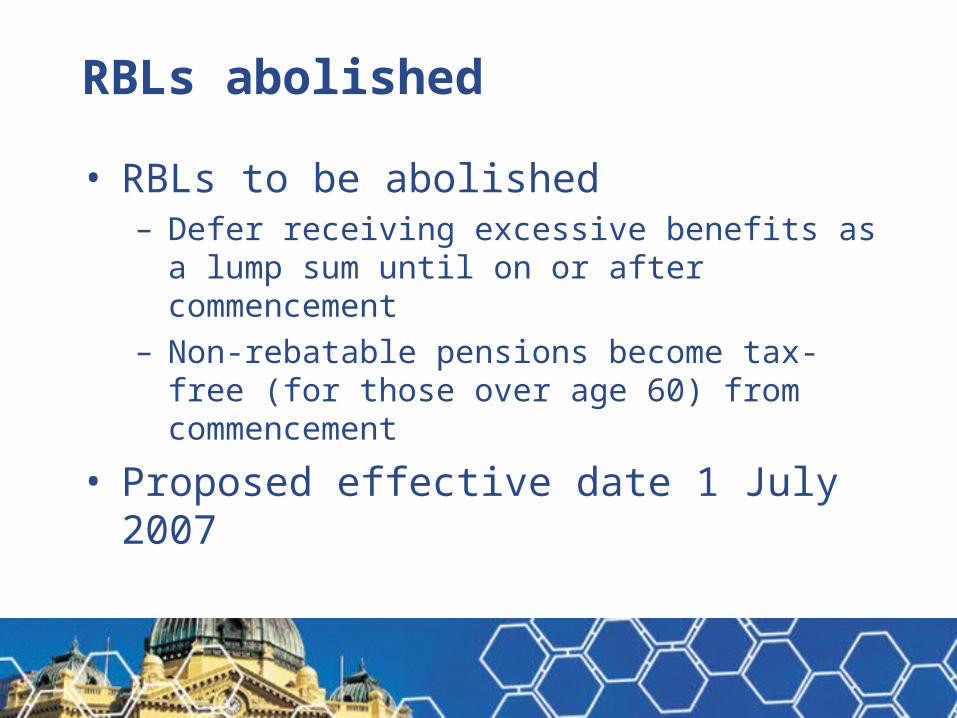

• RBLs to be abolished– Defer receiving excessive benefits as a lump sum until

on or after commencement

– Non-rebatable pensions become tax-free (for those over age 60) from commencement

• Proposed effective date 1 July 2007

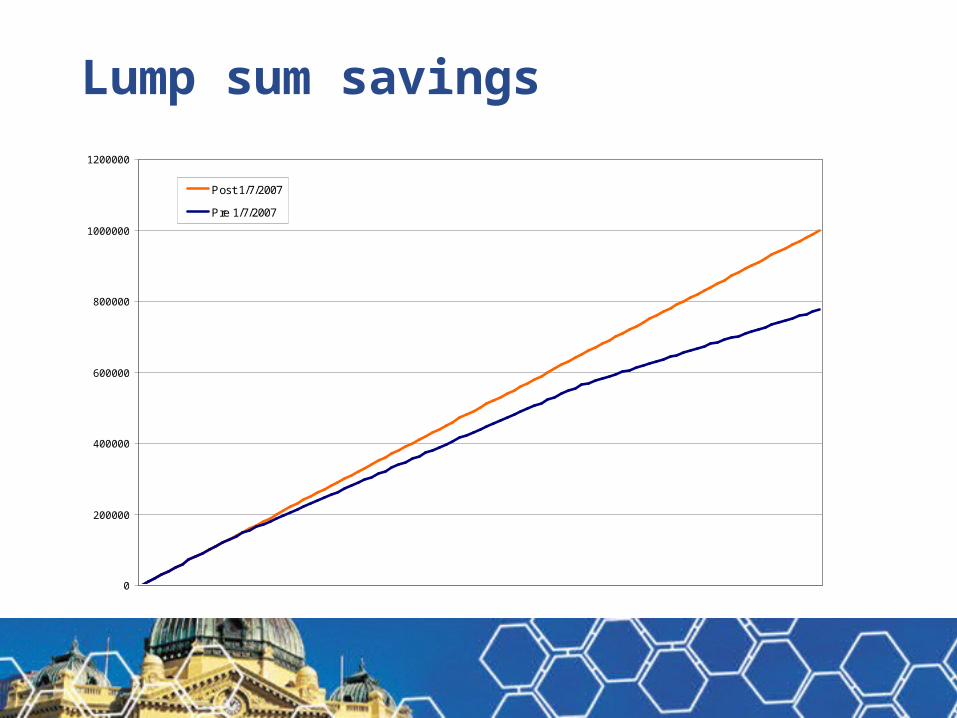

Lump sum savings

0

200000

400000

600000

800000

1000000

1200000

Post 1/7/2007

Pre 1/7/2007

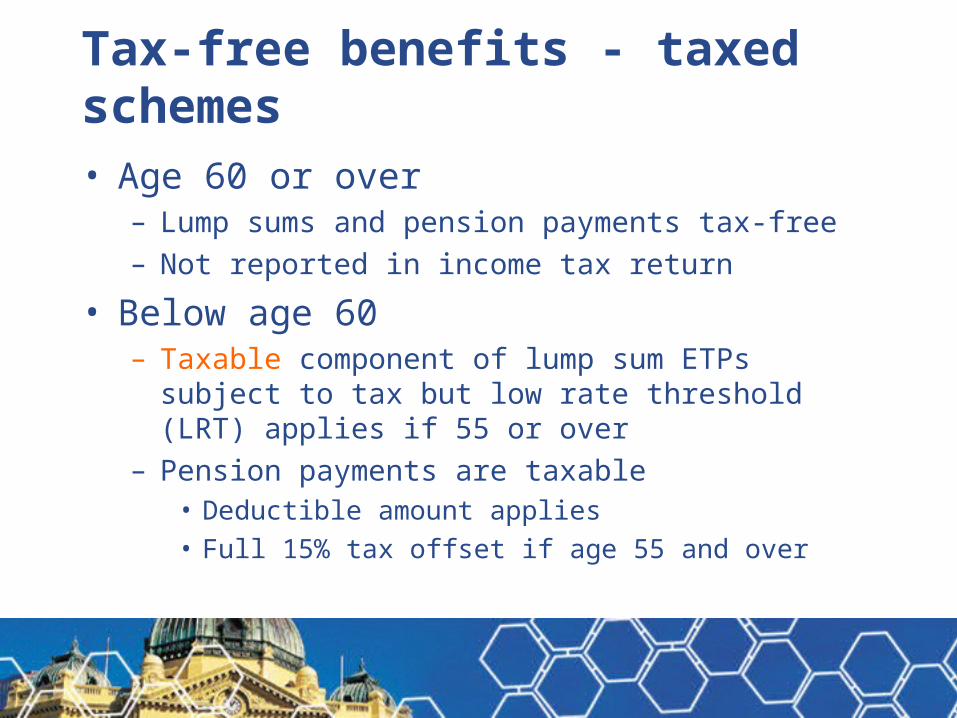

Tax-free benefits - taxed schemes

• Age 60 or over– Lump sums and pension payments tax-free

– Not reported in income tax return

• Below age 60– Taxable component of lump sum ETPs subject to

tax but low rate threshold (LRT) applies if 55 or over

– Pension payments are taxable• Deductible amount applies

• Full 15% tax offset if age 55 and over

Tax effective debt reduction

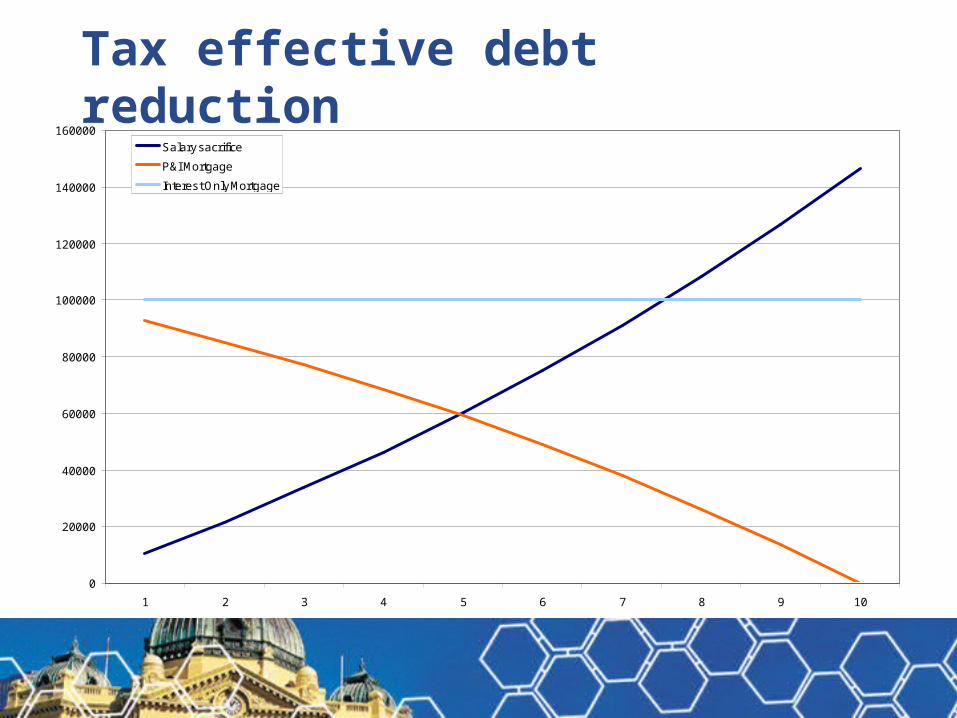

• Tom (50) is planning to retire at age 60

• He derives an annual salary of $100,000– 41.5% marginal tax rate

• Tom has a balance of $100,000 remaining on his home loan– Interest rate of 7.5% pa

– Remaining term of 10 years

– Current principal and interest repayments of $14,176 pa

Tax effective debt reduction

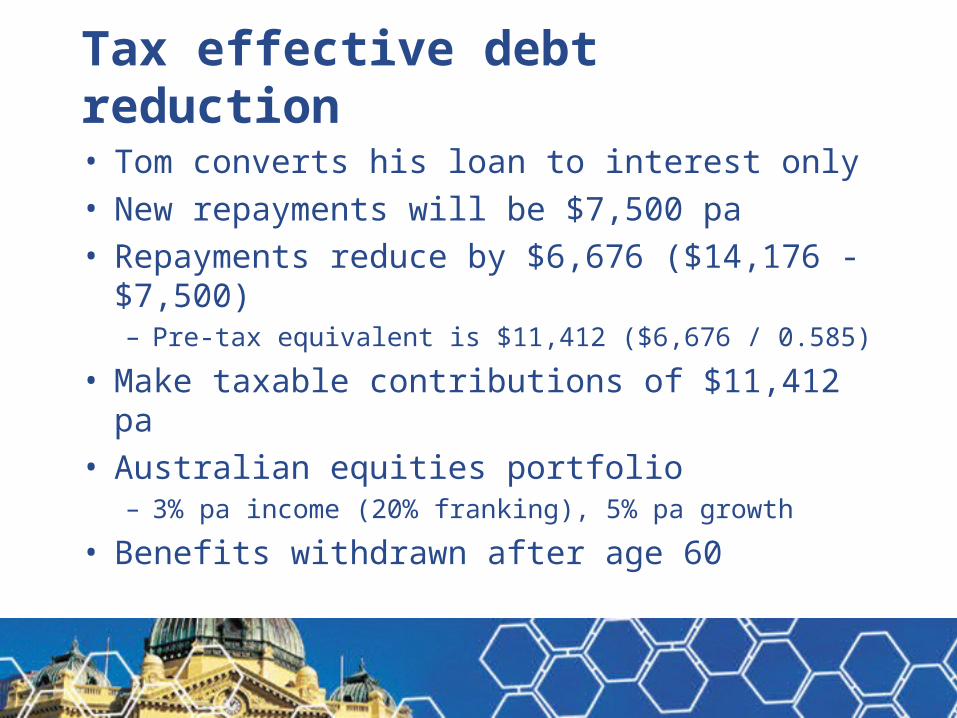

• Tom converts his loan to interest only

• New repayments will be $7,500 pa

• Repayments reduce by $6,676 ($14,176 - $7,500)– Pre-tax equivalent is $11,412 ($6,676 / 0.585)

• Make taxable contributions of $11,412 pa

• Australian equities portfolio– 3% pa income (20% franking), 5% pa growth

• Benefits withdrawn after age 60

Tax effective debt reduction

0

20000

40000

60000

80000

100000

120000

140000

160000

1 2 3 4 5 6 7 8 9 10

Salary sacrifice

P&I Mortgage

Interest Only Mortgage

Tax effective debt reduction

• After 10 year Tom withdraws his superannuation benefit of $146,376 and repays his mortgage of $100,000

• Tom has accrued an extra $46,376 after all taxes with no impact on his disposable income

• Variations of this strategy are possible– Establishing a line of credit against equity in home to

finance living expenses while maximising superannuation salary sacrificing opportunities

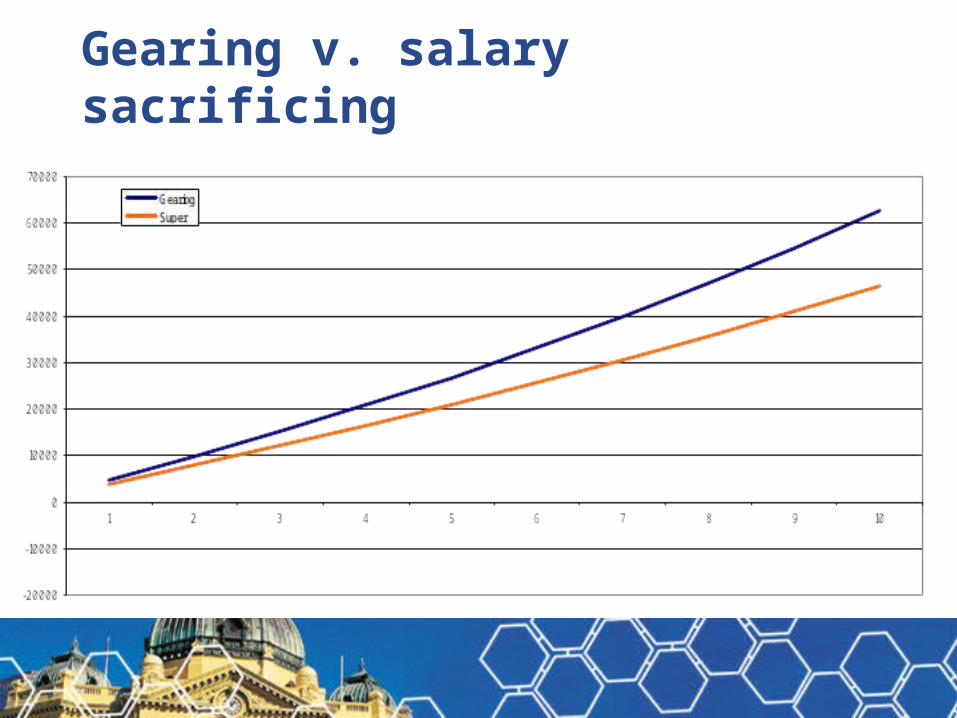

Gearing v. salary sacrificing

• An adviser has a number of clients who are looking to aggressively grow their savings for retirement

• Which is best?– Borrow to invest; or

– Salary sacrifice into super

• Beware, too many variables to determine end outcome

Gearing v. salary sacrificing

• Gearing assumptions– 41.5% MTR

– Borrow $100,000 (100% LVR) at 7.5% pa

– Equity portfolio• 3% pa income (25% franking)

• 6% pa growth

– Net of tax positions shown on redemption• 50% CGT discount applied

Gearing v. salary sacrificing

• Salary sacrifice assumptions– 41.5% MTR– Annual net cost of gearing alternative is grossed-up and

salary sacrificed into super• Cash flows are matched under both scenarios

– Equity portfolio (as per gearing)– Net of tax positions shown on withdrawal

• 15% tax on contributions• Earnings taxed at a combination of 15% and 10%• Benefits received tax-free from age 60

Gearing v. salary sacrificing

Gearing v. salary sacrificing

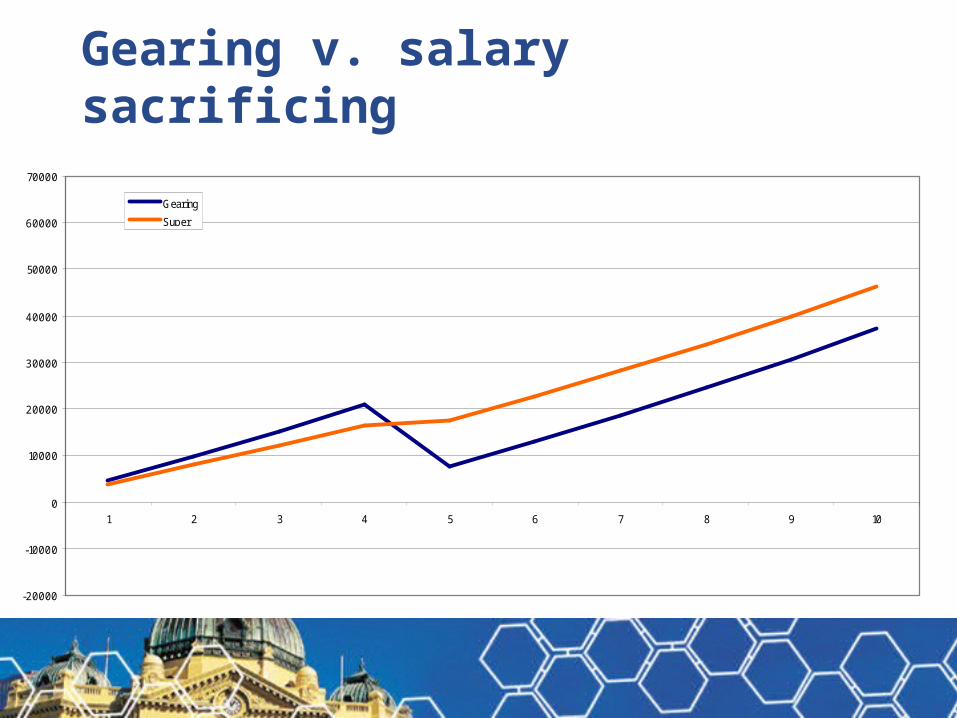

• What if in year 5, the equity portfolio under both alternatives return -10%?

• 3% income (25% franking)

• -13% capital

Gearing v. salary sacrificing

-20000

-10000

0

10000

20000

30000

40000

50000

60000

70000

1 2 3 4 5 6 7 8 9 10

Gearing

Super

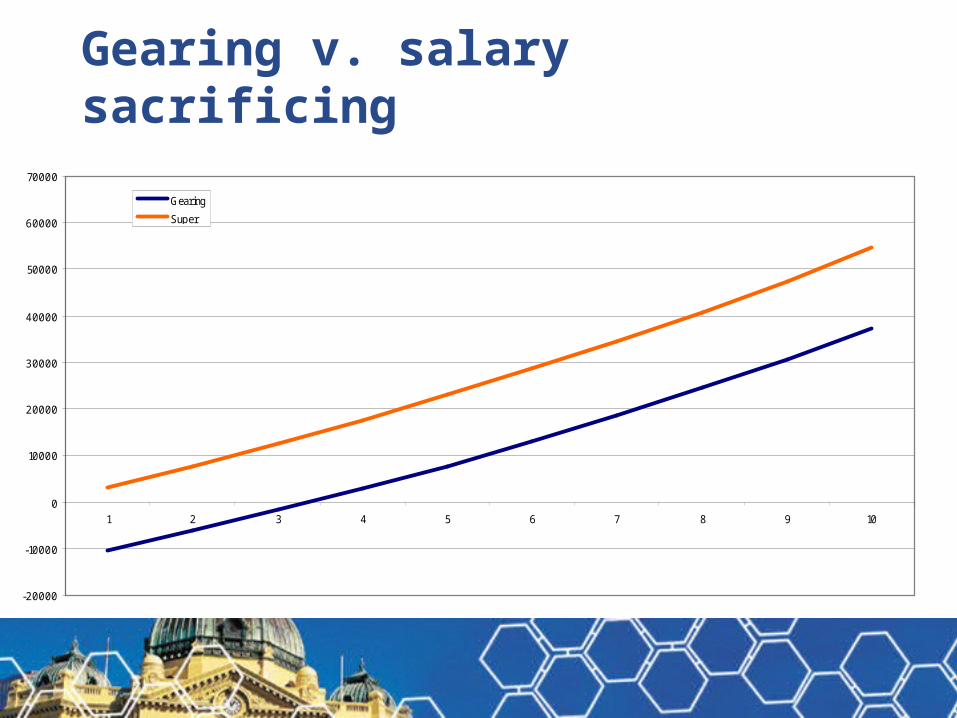

Gearing v. salary sacrificing

• What if the -10% investment returns happened in year 1 instead?

Gearing v. salary sacrificing

-20000

-10000

0

10000

20000

30000

40000

50000

60000

70000

1 2 3 4 5 6 7 8 9 10

Gearing

Super

Gearing v. salary sacrificing

• In an increasing market, gearing generally provides higher potential returns than superannuation

• Gearing produces more volatility in asset values

• Gee, what a revelation!

Superannuation contribution splitting

• Maximise two low rate thresholds

• Protection against legislative risk

• Financial independence

• Effectively doubles a person’s post-tax contributions limits

• Spouse turns 60 or preservation age sooner– Salary sacrifice & pension strategy (eg. TTR)

• Asset protection (bankruptcy)?

• Social security assets test

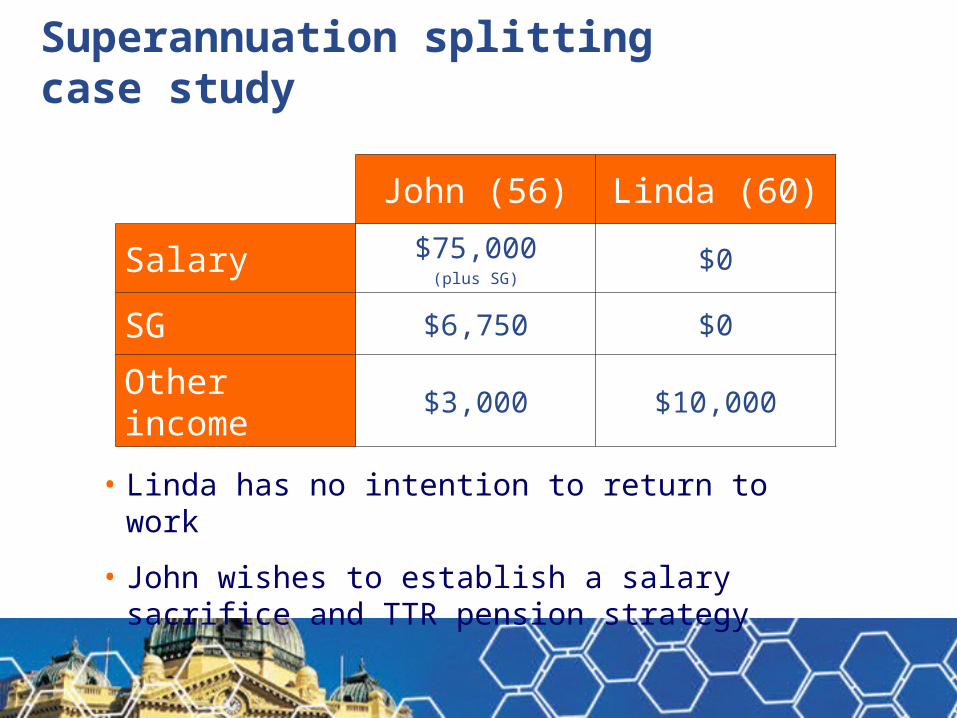

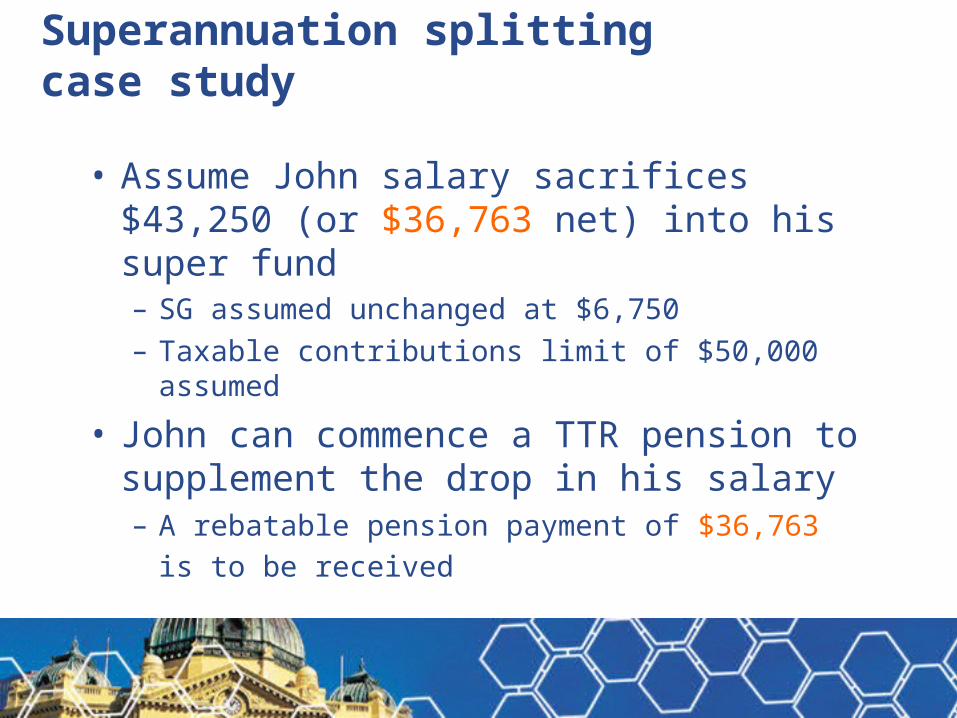

Superannuation splitting case study

John (56) Linda (60)

Salary $75,000(plus SG)

$0

SG $6,750 $0

Other income $3,000 $10,000

• Linda has no intention to return to work

• John wishes to establish a salary sacrifice and TTR pension strategy

• Assume John salary sacrifices $43,250 (or $36,763 net) into his super fund– SG assumed unchanged at $6,750

– Taxable contributions limit of $50,000 assumed

• John can commence a TTR pension to supplement the drop in his salary– A rebatable pension payment of $36,763 is to be

received

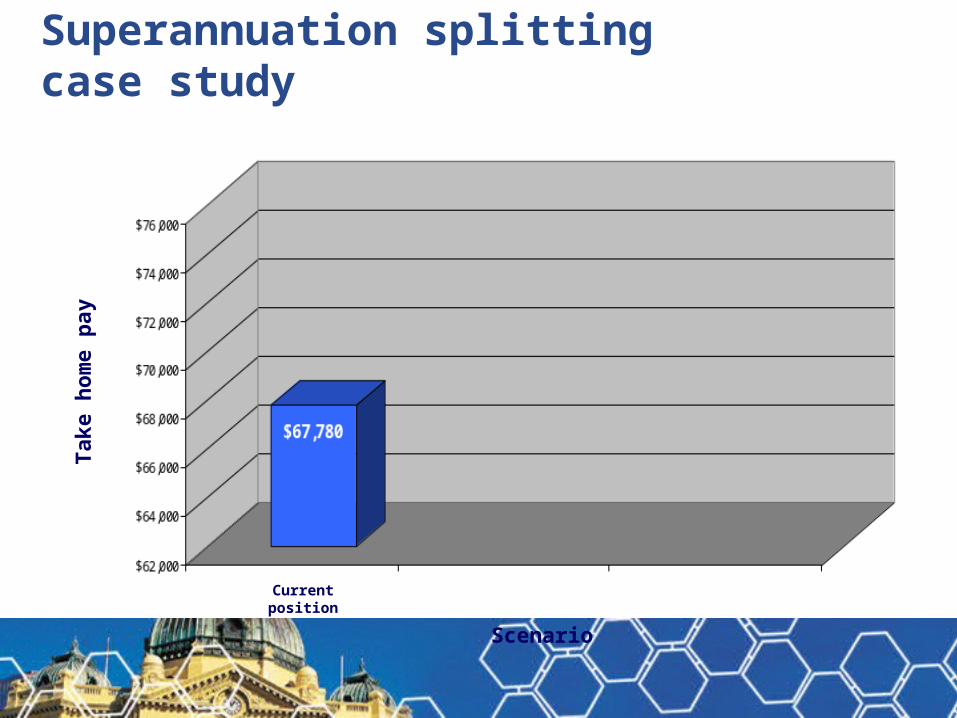

Superannuation splitting case study

Tak

e h

om

e p

ay

Current position

Scenario

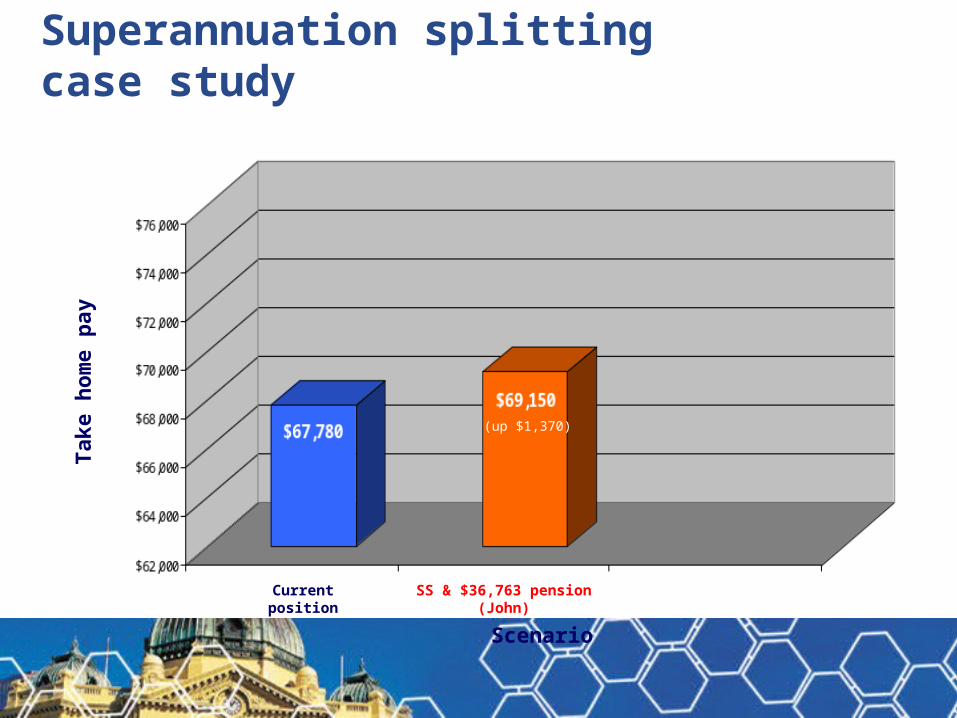

Superannuation splitting case study

Tak

e h

om

e p

ay

Current position SS & $36,763 pension (John)

Scenario

(up $1,370)

Superannuation splitting case study

• Is John better off establishing a TTR pension, or is Linda better off establishing a pension instead (disregard tax-free pension earnings)?

• Can contributions splitting help?

Linda, as the pension payments are tax-free from age 60 and no 10% maximum payment applies.

Not now as Linda is permanently retired.However, a carefully implemented medium-to-long term contributions splitting strategy may be vital in the lead up to retirement to ensure people like Linda have enough super to establish their pension.

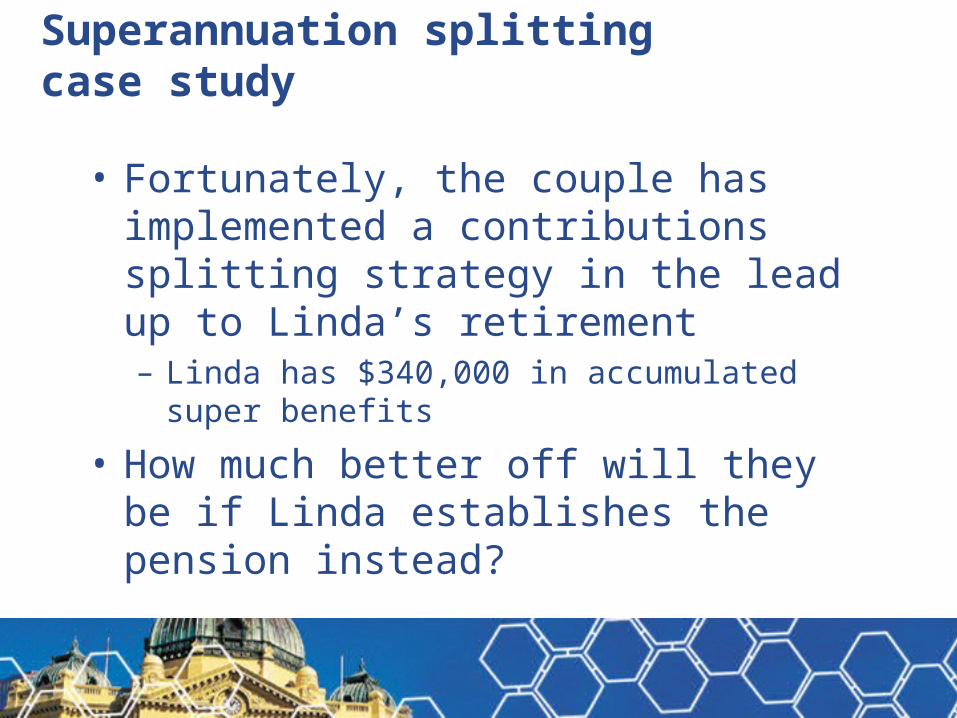

Superannuation splitting case study

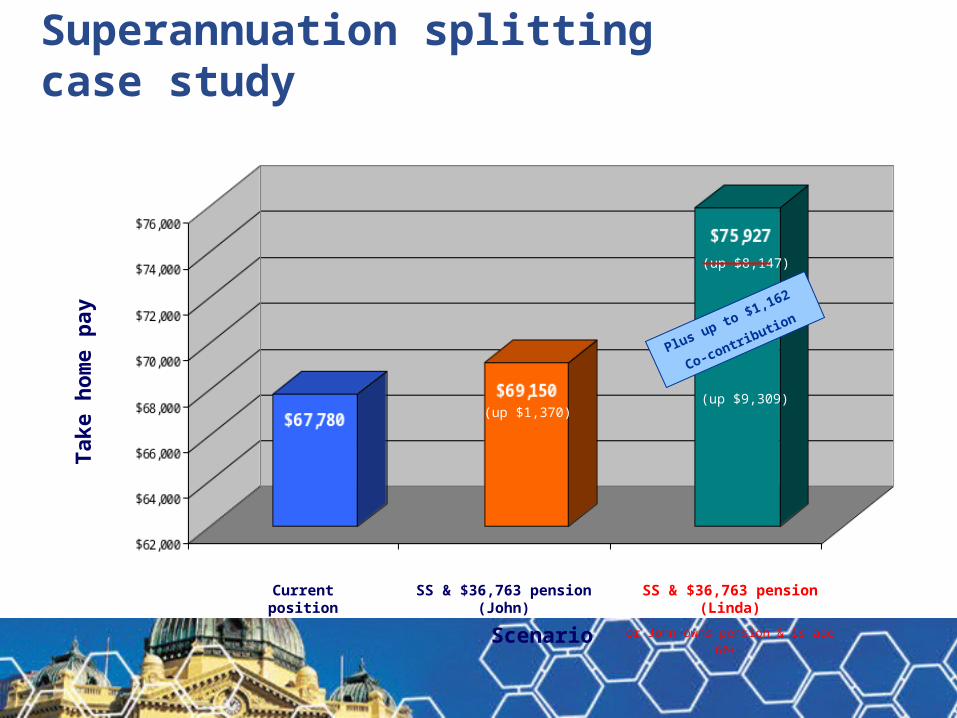

• Fortunately, the couple has implemented a contributions splitting strategy in the lead up to Linda’s retirement– Linda has $340,000 in accumulated super benefits

• How much better off will they be if Linda establishes the pension instead?

Superannuation splitting case study

Tak

e h

om

e p

ay

Current position SS & $36,763 pension (John) SS & $36,763 pension (Linda)

or John owns pension & is age 60+

Scenario

(up $1,370)

(up $8,147)

Plus up to $1,162

Co-contributio

n

(up $9,309)

Superannuation splitting case study

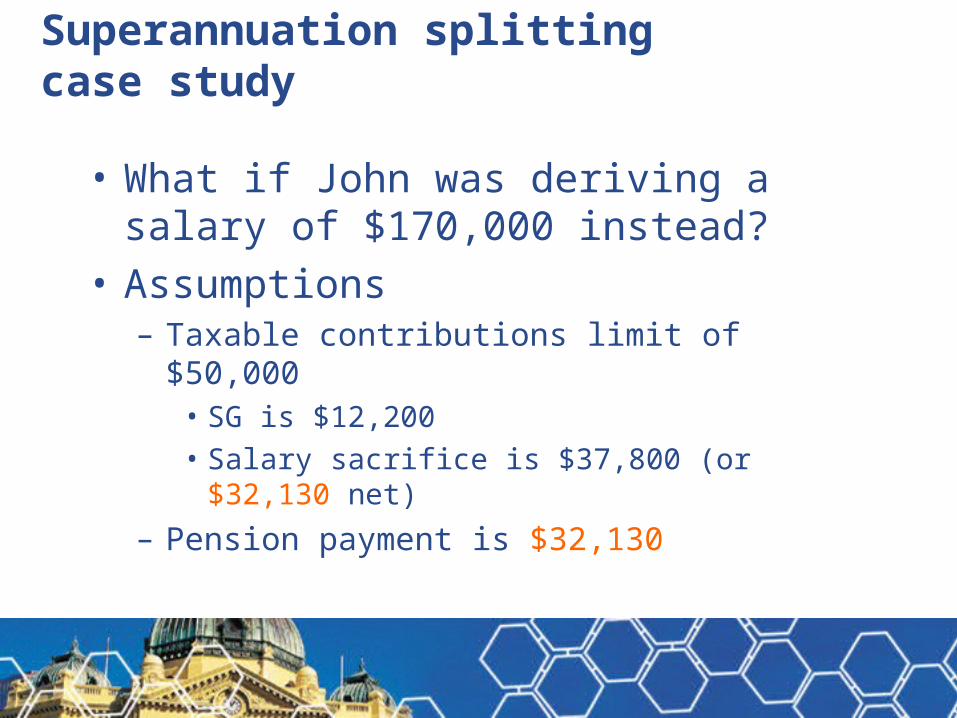

• What if John was deriving a salary of $170,000 instead?

• Assumptions– Taxable contributions limit of $50,000

• SG is $12,200

• Salary sacrifice is $37,800 (or $32,130 net)

– Pension payment is $32,130

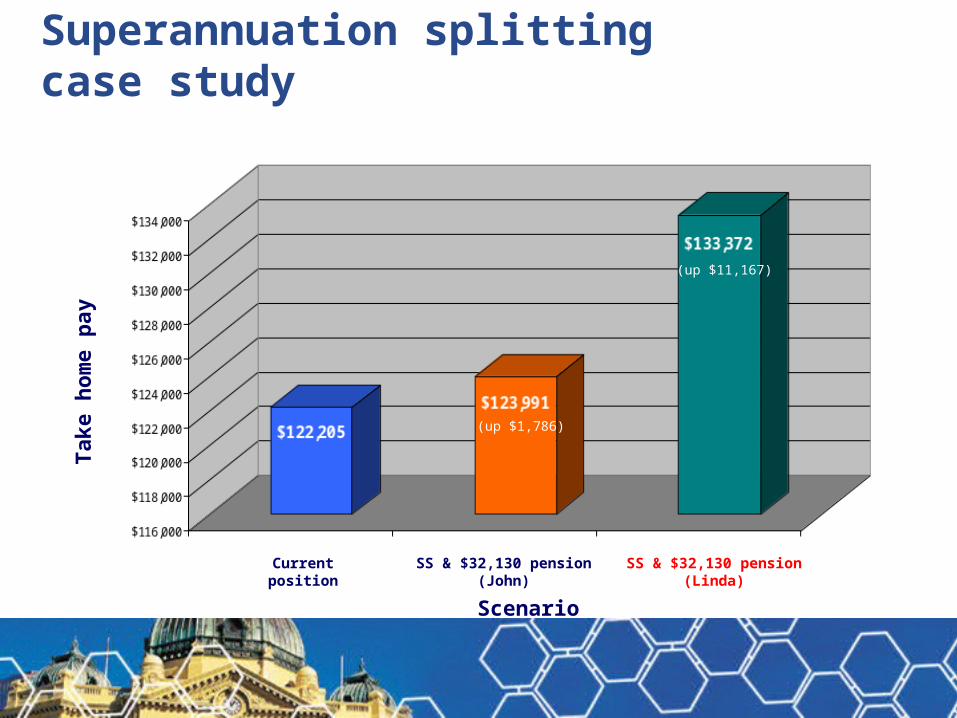

Superannuation splitting case study

Tak

e h

om

e p

ay

Current position SS & $32,130 pension (John) SS & $32,130 pension (Linda)

Scenario

(up $1,786)

(up $11,167)

Superannuation splitting case study

Tax effective life insurance planning

• Funding life insurance via superannuation can be tax effective but requires a comprehensive analysis of the taxation and other consequences of receiving benefit proceeds

• With the Government’s proposed superannuation reforms due to take effect from 1 July 2007, optimal funding arrangements may change

Types of cover

• Types of cover available through superannuation include:

• Death

• TPD

• Income protection

• Trauma?

• Taxation of life insurance proceeds received through superannuation:– Death benefits

• Dependants

• Non-dependants

– TPD• Post-June 94 invalidity component

Tax effective life insurance planning

Tax effective life insurance planning

• Insurance proceeds paid as a lump sum to a dependant– Tax free within deceased’s Pension RBL ($1,356,291

or higher transitional RBL)

– Excess taxed at 39.5%/48.5%

Budget strategy update

• Government has proposed that RBLs are to be abolished from 1 July 2007– From 1 July 2007 we will see uncapped amounts of

death cover held via superannuation

• Government has proposed caps on deductible and undeducted contributions from 9 May 2006– Life insurance remains a way of getting substantial

assets into superannuation to fund tax effective income streams for beneficiaries

Tax effective life insurance planning

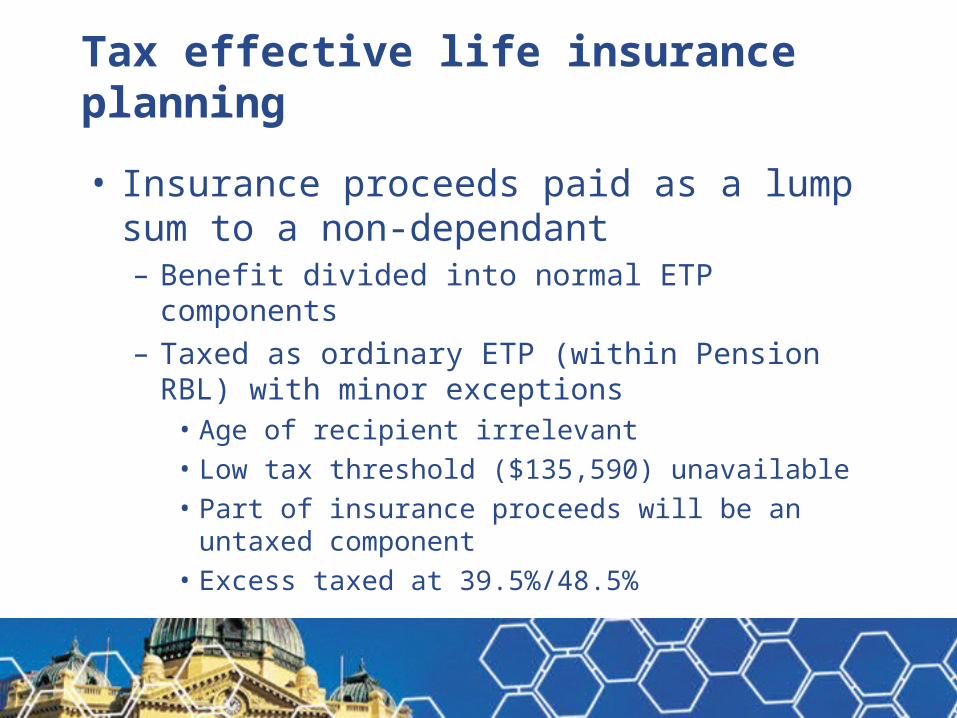

• Insurance proceeds paid as a lump sum to a non-dependant– Benefit divided into normal ETP components

– Taxed as ordinary ETP (within Pension RBL) with minor exceptions

• Age of recipient irrelevant

• Low tax threshold ($135,590) unavailable

• Part of insurance proceeds will be an untaxed component

• Excess taxed at 39.5%/48.5%

Death benefits• Reversionary pension payments exempt from

tax if deceased was at least 60 • Non-dependants (tax law) must receive death

benefits as a lump sum – Exempt component is tax-free– Taxable component generally up to 16.5% (may be

partly taxed at up to 31.5% if includes death cover)

• Death benefit pensions paid to a child– Pension must cease by 25th birthday (unless child

is permanently disabled)– Pension balance cashed tax-free on cessation

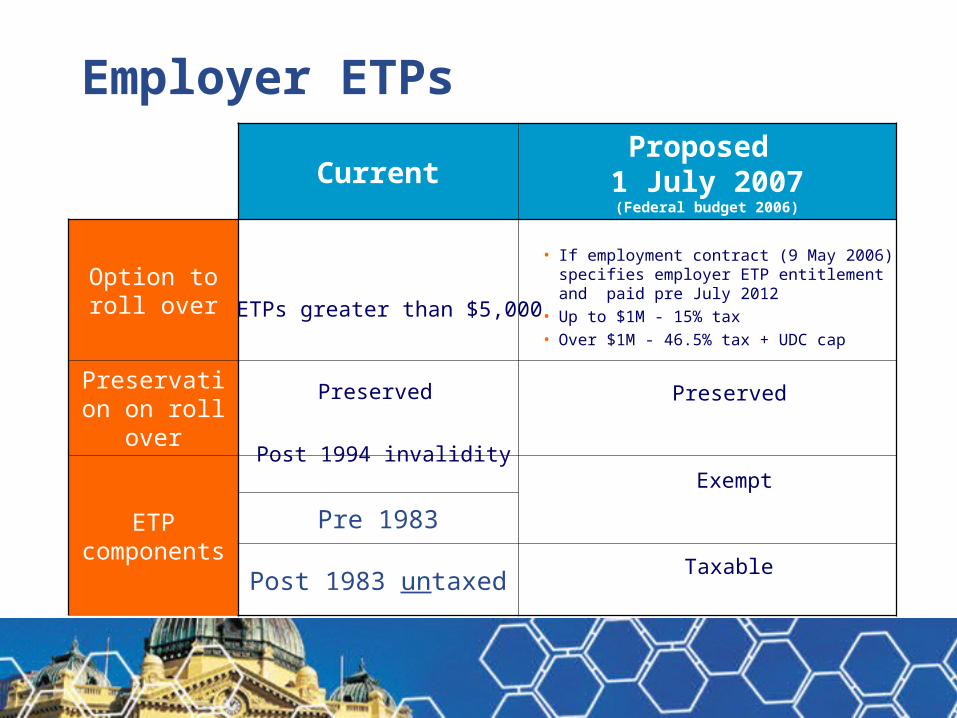

Employer ETPs

CurrentProposed

1 July 2007(Federal budget 2006)

Option to roll over

Preservation on roll over

ETP components

Pre 1983

Post 1983 untaxed

ETPs greater than $5,000

Preserved

• If employment contract (9 May 2006) specifies employer ETP entitlement and paid pre July 2012

• Up to $1M - 15% tax• Over $1M - 46.5% tax + UDC cap

Preserved

Exempt

Taxable

Post 1994 invalidity

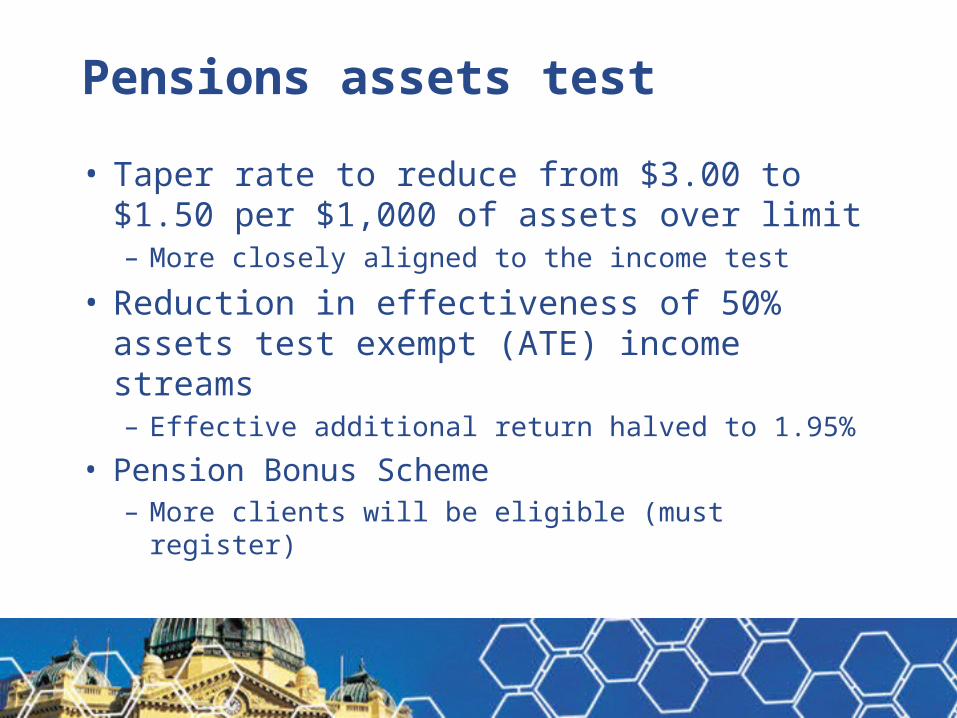

Pensions assets test

• Taper rate to reduce from $3.00 to $1.50 per $1,000 of assets over limit– More closely aligned to the income test

• Reduction in effectiveness of 50% assets test exempt (ATE) income streams– Effective additional return halved to 1.95%

• Pension Bonus Scheme – More clients will be eligible (must register)

Pensions assets test

Family situationAsset free

limit

Cut-out limit

Estimated cut-out limit on 20/09/2007

Single homeowner $161,500 $330,000

Single non-homeowner $278,500 $447,000

Couple homeowner $229,000 $509,500

Couple non-homeowner $346,000 $626,500

Illness separated couple homeowner $229,000 $566,000

Illness separated couple non-homeowner $346,000 $683,000

$526,500

$647,000

$838,500

$959,000

$956,000

$1,076,500

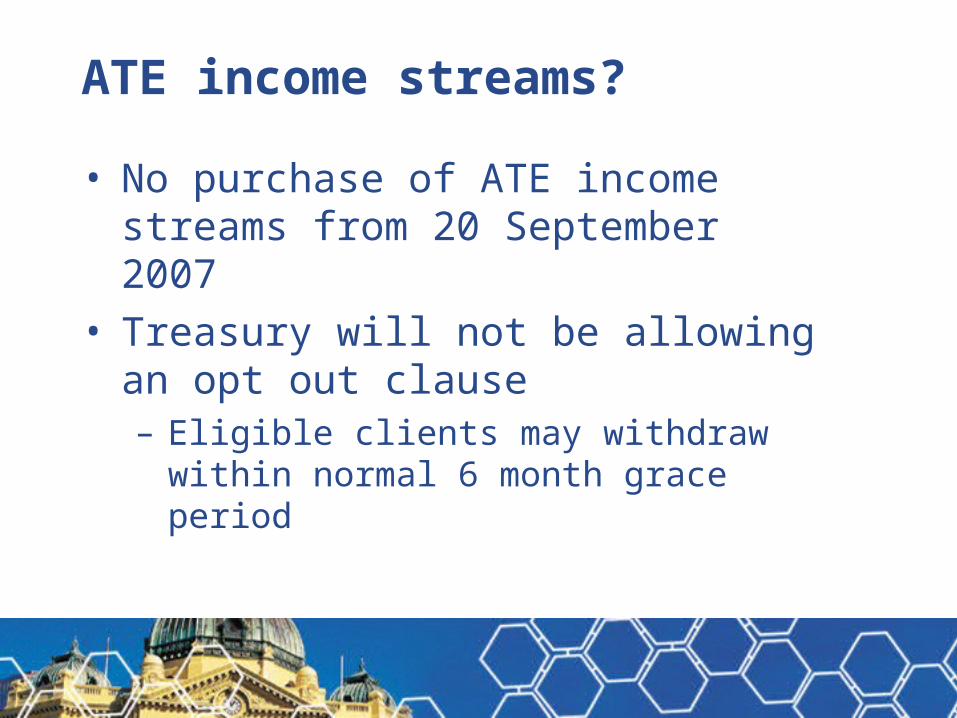

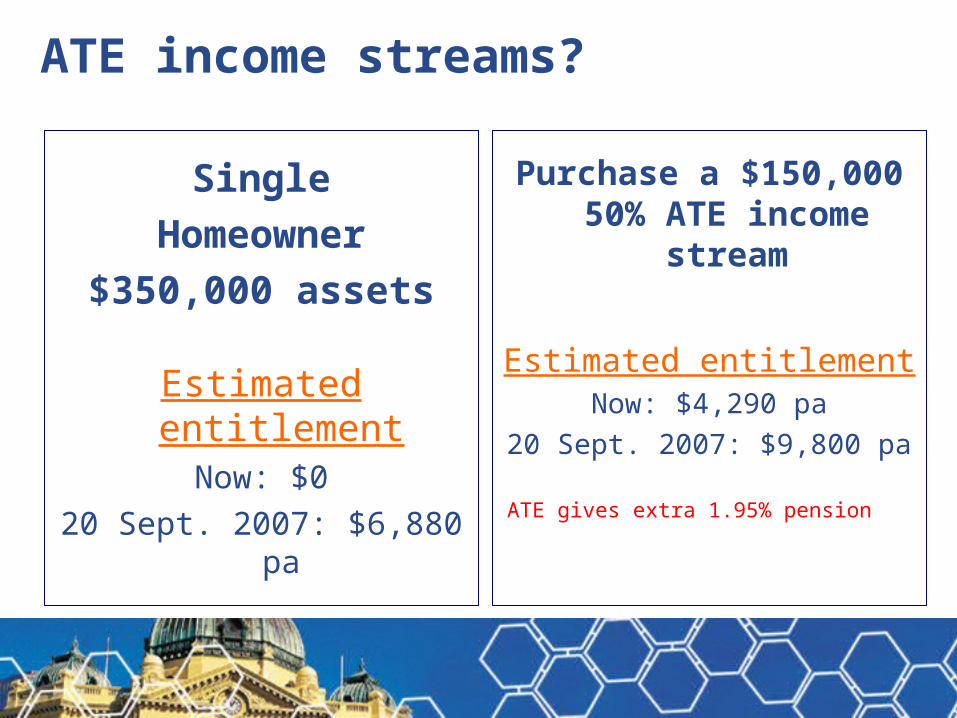

ATE income streams?

• No purchase of ATE income streams from 20 September 2007

• Treasury will not be allowing an opt out clause– Eligible clients may withdraw within normal 6

month grace period

ATE income streams?

Single

Homeowner

$350,000 assets

Estimated entitlementNow: $0

20 Sept. 2007: $6,880 pa

Purchase a $150,000 50% ATE income

stream

Estimated entitlementNow: $4,290 pa

20 Sept. 2007: $9,800 pa

ATE gives extra 1.95% pension

Aged care

• For aged care residents entering facility from 1 January 2007, assessable assets for accommodation bond or accommodation charge purposes to be brought in line with Centrelink assets test– Deprived assets

• If gifted on or after 10 May 2006

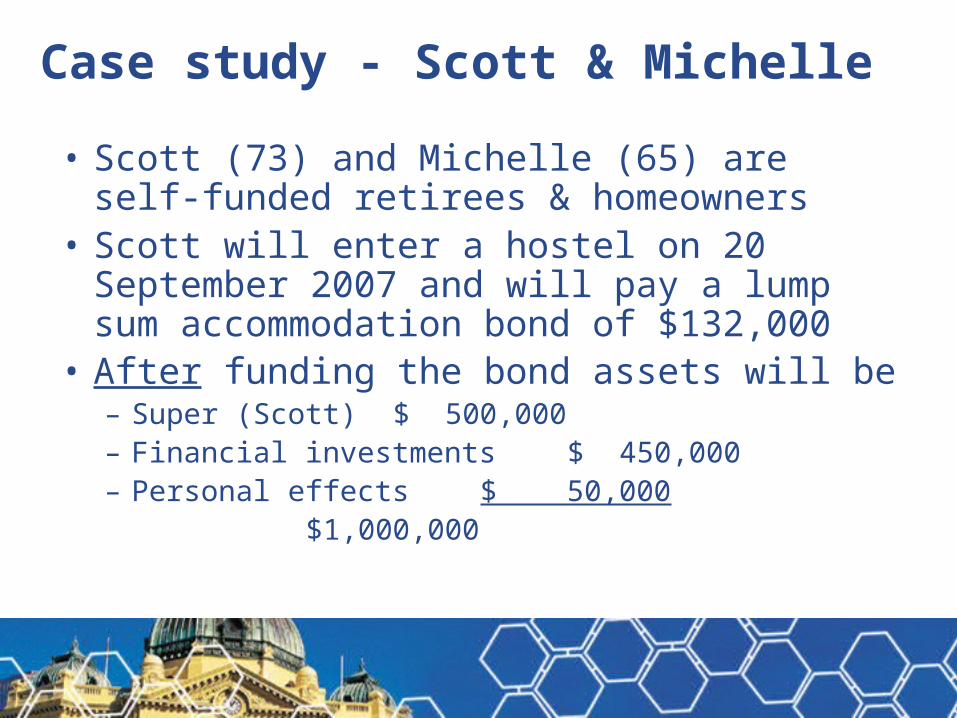

Case study - Scott & Michelle

• Scott (73) and Michelle (65) are self-funded retirees & homeowners

• Scott will enter a hostel on 20 September 2007 and will pay a lump sum accommodation bond of $132,000

• After funding the bond assets will be – Super (Scott) $ 500,000– Financial investments $ 450,000– Personal effects $ 50,000

$1,000,000

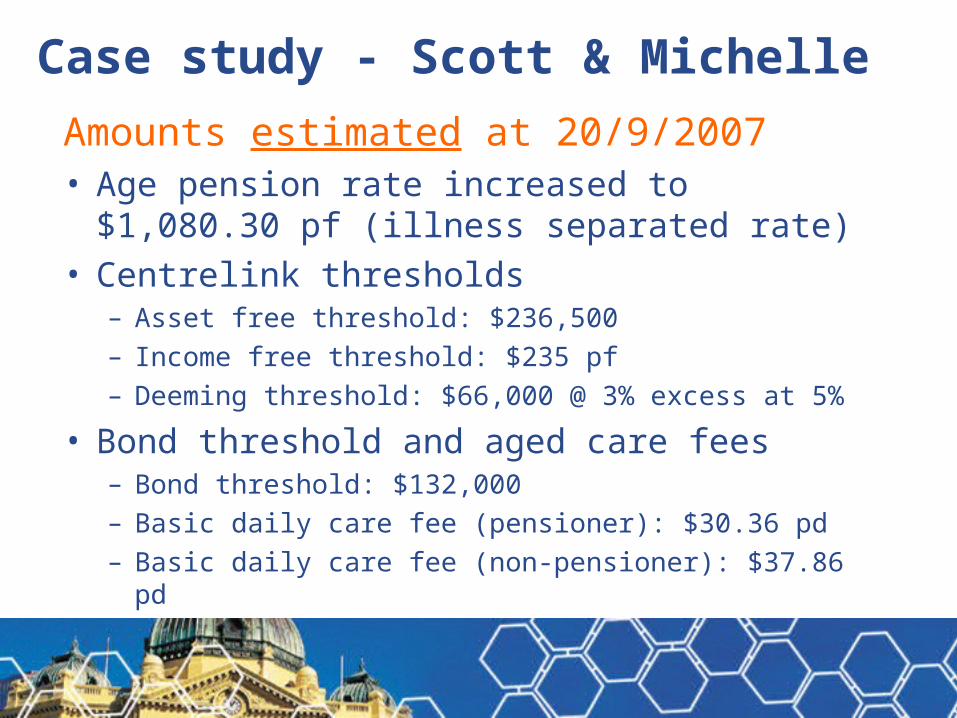

Case study - Scott & Michelle

Amounts estimated at 20/9/2007• Age pension rate increased to $1,080.30 pf (illness

separated rate)• Centrelink thresholds

– Asset free threshold: $236,500

– Income free threshold: $235 pf

– Deeming threshold: $66,000 @ 3% excess at 5%

• Bond threshold and aged care fees– Bond threshold: $132,000

– Basic daily care fee (pensioner): $30.36 pd

– Basic daily care fee (non-pensioner): $37.86 pd

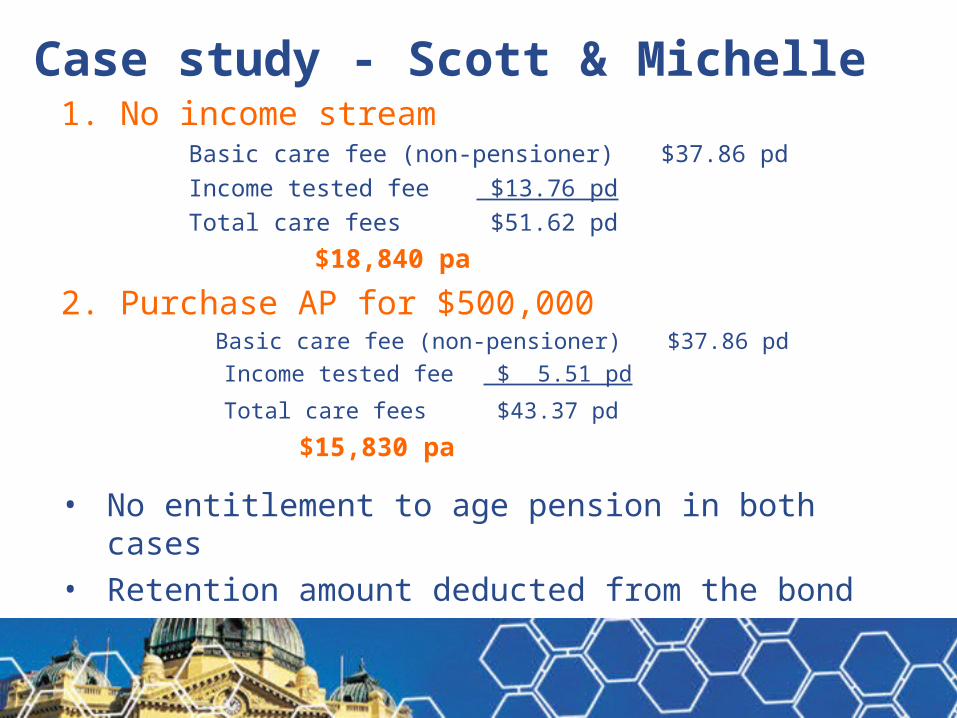

Case study - Scott & Michelle1. No income stream

Basic care fee (non-pensioner) $37.86 pd

Income tested fee $13.76 pd

Total care fees $51.62 pd

$18,840 pa

2. Purchase AP for $500,000 Basic care fee (non-pensioner) $37.86 pd

Income tested fee $ 5.51 pd

Total care fees $43.37 pd

$15,830 pa

• No entitlement to age pension in both cases

• Retention amount deducted from the bond

Case study - Scott & Michelle

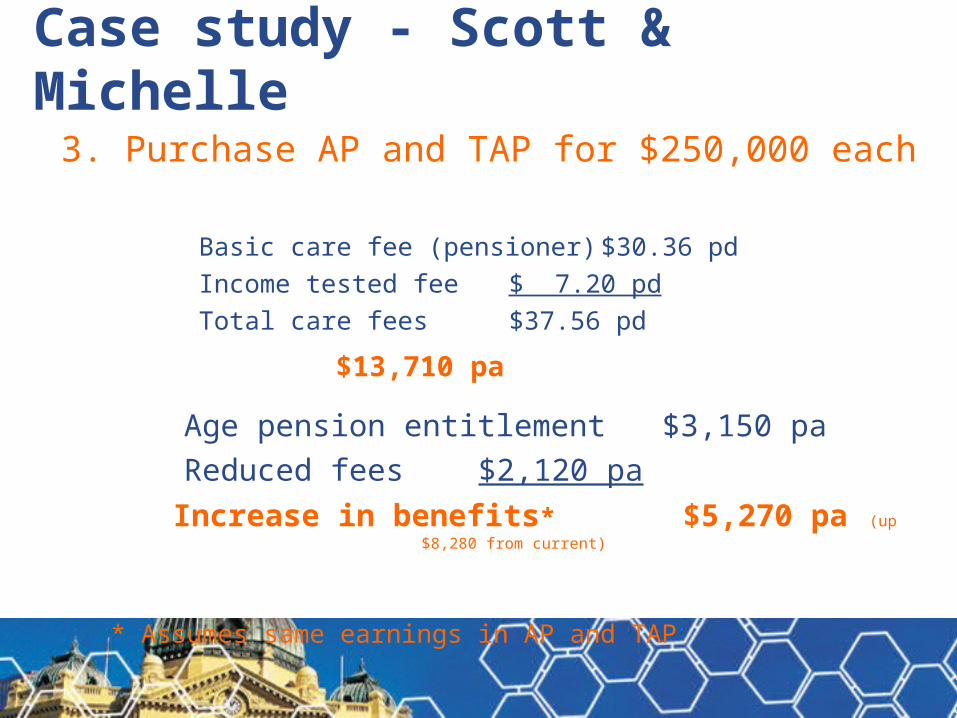

3. Purchase AP and TAP for $250,000 each Basic care fee (pensioner) $30.36 pd

Income tested fee $ 7.20 pd

Total care fees $37.56 pd

$13,710 pa

Age pension entitlement $3,150 pa

Reduced fees $2,120 pa

Increase in benefits* $5,270 pa (up $8,280 from current)

* Assumes same earnings in AP and TAP

What’s hot, what’s new?

• Contribution limits

• Tax-free benefits

• Contribution splitting

• Transition to retirement

• Life insurance via superannuation

• Superannuation death benefits

• Employer ETPs

• Social security and aged care

Disclaimer

This information is a summary based on ING’s understanding of the relevant legislation. It is only intended to be general financial product advice. It is general in nature and may not be relevant to individual circumstances. You should not do or refrain from doing anything in reliance on this information without obtaining suitable professional advice. You should consider any relevant Product Disclosure Statement before making any decision about whether to acquire any product. ING Product Disclosure Statements are available on request by calling ING or by visiting our website, www.ing.com.au.

Related Documents

![[Nhom 11] [Lowe]](https://static.cupdf.com/doc/110x72/577c831f1a28abe054b3afc3/nhom-11-lowe.jpg)