What We Know of the Youth Market Analysis of Core Tourism Statistics Produced by Tourism New Zealand, Insights – March 2012

What We Know of the Youth Market Analysis of Core Tourism Statistics Produced by Tourism New Zealand, Insights – March 2012.

Dec 17, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

What We Know of the Youth Market

Analysis of Core Tourism Statistics

Produced by Tourism New Zealand, Insights – March 2012

Key FindingsThe youth sector generates $1.8 billion in tourism expenditure

60 per cent of the NZs youth market originate from Australia as either Australians or visitors to Australia.

Youth travellers do more activities in New Zealand than all tourists

Over half of all youth tourists do some form of adventure tourism while in New Zealand

Youth tourists stay for longer periods of time in New Zealand than other tourists

Almost 80 per cent of youth are not backpackers

The Value of the Youth Market

Total ExpenditureTotal Expenditure

For the year ended March 2012 the youth market* generated $1.8 billion in tourism expenditure. This represents 32% of total international tourism expenditure in New Zealand.

Average Expenditure

In the year ended March 2012 the youth market* spent an average of $2,877 per trip to New Zealand. The average for all tourists is $2,360 or $517 less per trip than the youth market.

Length of Stay

For the year ended June 2012 the youth market* stayed for an average of 29.2 days in New Zealand. The average for allvisitors to New Zealand is 19.4 days.

*Includes 15 to 29 year olds1International Visitor Survey – YE Mar 20122International Travel and Migration Statistics – YE Jun 2012

$1.8 billion1 Sample: 1,708

$2,877 per trip1 Sample: 1,708

29.2 days2

Holiday ExpenditureAverage Expenditure

Over the last three years the youth holiday market* spent an average of $2,593 per trip to New Zealand. The average for all tourists over this period of time is $2,846, or $253 more per trip than the youth holiday segment.

Length of Stay

For the year ended June 2012 the youth holiday market* stayed for an average of 25.3 days in New Zealand. The average for allholiday visitors to New Zealand is 16.1 days.

Length of Stay – Less Working Holiday Visa Tourists

For the year ended June 2012 the youth holiday market* less working holiday visa tourists stayed for an average of 21 days in New Zealand. The average for all holiday visitors less working holiday visas is 16 days.

*Includes 15 to 29 year olds1International Visitor Survey – Average of YE Mar 2010 to 20122International Travel and Migration Statistics – YE Jun 2012

$2,593 per trip1 Sample:

2,758

25.3 days2

21 days2

Holiday InteractionAverage Number of Regions VisitedYouth 4.9All 4.2

Average Number of Activities DoneYouth 11.9All 10.5

International Visitor Survey – YE Dec 2009 - 2011 (15 – 29 year olds)

Which Youth Markets Are The Most Valuable?

Youth Arrivals

International Travel and Migration Statistics – YE Dec 2011 (18 – 29 year olds)

0

50,000

100,000

150,000

200,000

250,000

Aust

ralia UK

USA

Ger

man

yCh

ina

Fran

ceJa

pan

Cana

daIn

dia

Kore

aM

alay

sia

Net

herla

nds

Irela

ndSi

ngap

ore

Switz

erla

ndSw

eden

Braz

ilTa

iwan

Sout

h Af

rica

Arge

ntina

Arriv

als

Youth Arrivals - YE Jun 2012

020,00040,00060,00080,000

100,000120,000

Aust

ralia UK

USA

Ger

man

yCh

ina

Fran

ceJa

pan

Cana

daIn

dia

Net

herla

nds

Mal

aysi

aSi

ngap

ore

Irela

ndKo

rea

Swed

enSw

itzer

land

Taiw

anD

enm

ark

Arge

ntina

Aust

ria

Arriv

als

Youth Arrivals 2011 - HolidayYE Jun 12

Youth Total Stay Days

International Travel and Migration Statistics – YE Jun 2012 (18 – 29 year olds)

0500,000

1,000,0001,500,0002,000,0002,500,0003,000,000

Aust

ralia UK

Ger

man

yU

SAFr

ance

Chin

aCa

nada

Japa

nN

ethe

rland

sKo

rea

Indi

aSw

itzer

land

Mal

aysi

aIre

land

Swed

enBr

azil

Vanu

atu

Phili

ppin

es Fiji

Arge

ntina

Tota

l Sta

y D

ays

Youth Total Stay Days

0200,000400,000600,000800,000

1,000,0001,200,0001,400,000

Aust

ralia

Ger

man

yU

KU

SAFr

ance

Net

herla

nds

Cana

daSw

itzer

land

Irela

ndSw

eden

Mal

aysi

aCh

ina

Japa

nIs

rael

Kore

aDe

nmar

kAr

genti

naCz

ech

Repu

blic

Aust

riaSi

ngap

ore

Tota

l Sta

y D

ays

Youth Stay Days - Holiday

Pure Holiday Visitors

The graph above shows total stay days for the youth segment for pure holiday visitors. This is holiday visitors with all those arriving on a work visa removed from the data series.

*Australians do not need a visa to enter New Zealand so are not included within this segment

International Travel and Migration Statistics – YE Jun 2012 (18 – 29 year olds)

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

Aust

ralia UK

Ger

man

y

USA

Fran

ce

Net

herla

nds

Switz

erla

nd

Cana

da

Isra

el

Irela

nd

Swed

en

Chin

a

Japa

n

Denm

ark

Kore

a

Aust

ria

Indi

a

Mal

aysi

a

Sing

apor

e

Tota

l Sta

y D

ays

Total Stay Days - Holiday (Visitor Only)

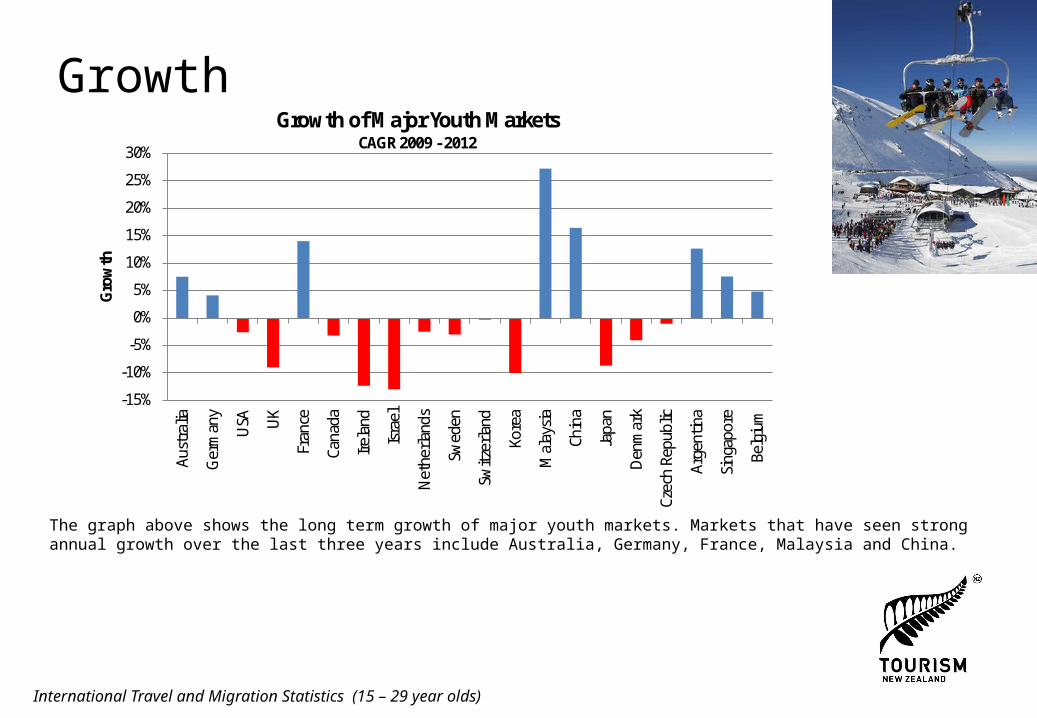

Growth

The graph above shows the long term growth of major youth markets. Markets that have seen strong annual growth over the last three years include Australia, Germany, France, Malaysia and China.

International Travel and Migration Statistics (15 – 29 year olds)

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

Aust

ralia

Ger

man

y

USA U

K

Fran

ce

Cana

da

Irela

nd

Isra

el

Net

herla

nds

Swed

en

Switz

erla

nd

Kore

a

Mal

aysi

a

Chin

a

Japa

n

Den

mar

k

Czec

h Re

publ

ic

Arge

ntina

Sing

apor

e

Belg

ium

Gro

wth

Growth of Major Youth MarketsCAGR 2009 - 2012

Major Youth Markets

The top four youth markets based on arrivals and total stay days include:

#1 Australia#2 UK#3 Germany#4 USA

Following this are:

FranceNetherlandsSwitzerlandCanadaIsraelIrelandSweden

Youth Profile

Purpose of Visit - Arrivals

The Youth segment has a higher share of holiday visitors than New Zealand’s average. Not surprisingly the youth segment is made up of less business and conference arrivals than average and more education arrivals.

Taking holiday arrivals only, the youth segment makes up 23% of New Zealand’s holiday arrivals.

International Travel and Migration Statistics – YE Jun 2012 (18 – 29 year olds)

47%

32%

10%

2%2%

4%

3%

Purpose of Visit - All

Holiday

VFR

Business

Conferences

Education

52%

28%

5%

1%5%

6%

3%

Purpose of Visit - Youth

Holiday

VFR

Business

Conferences

Education

Purpose of Visit – Total Stay Days

Holiday accounts for 45% of the youth segments days spent in New Zealand, which is more than the New Zealand average (39%).

The youth segment makes up 36% of New Zealand’s holiday total stay days. The youth holiday segment generates 7.1 million total stay days, which as a comparison is more than Australia which generates 5.1 million holiday total stay days.

International Travel and Migration Statistics – YE Jun 2012 (18 – 29 year olds)

45%

18%5%0%

18%

11%

3%

Purpose of Visit - Youth

Holiday

VFR

Business

Conferences

Education

Other

39%

35%

5%1%

9%

8%

3%

Purpose of Visit - All

Holiday

VFR

Business

Conferences

Education

Other

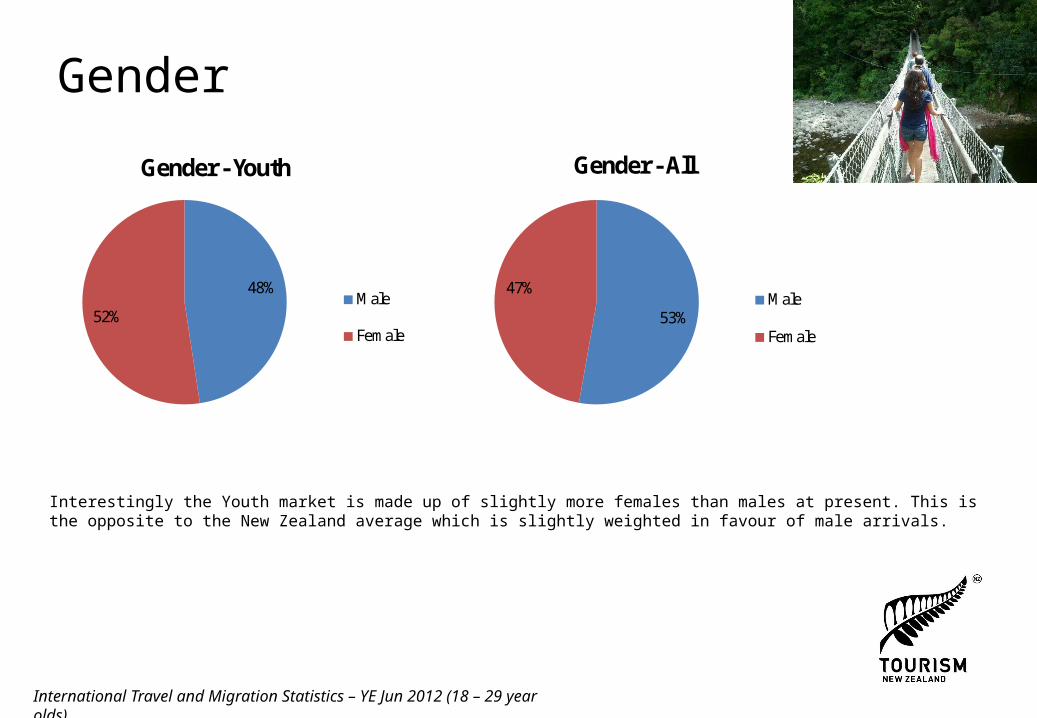

Gender

Interestingly the Youth market is made up of slightly more females than males at present. This is the opposite to the New Zealand average which is slightly weighted in favour of male arrivals.

International Travel and Migration Statistics – YE Jun 2012 (18 – 29 year olds)

48%

52%

Gender - Youth

Male

Female53%

47%

Gender - All

Male

Female

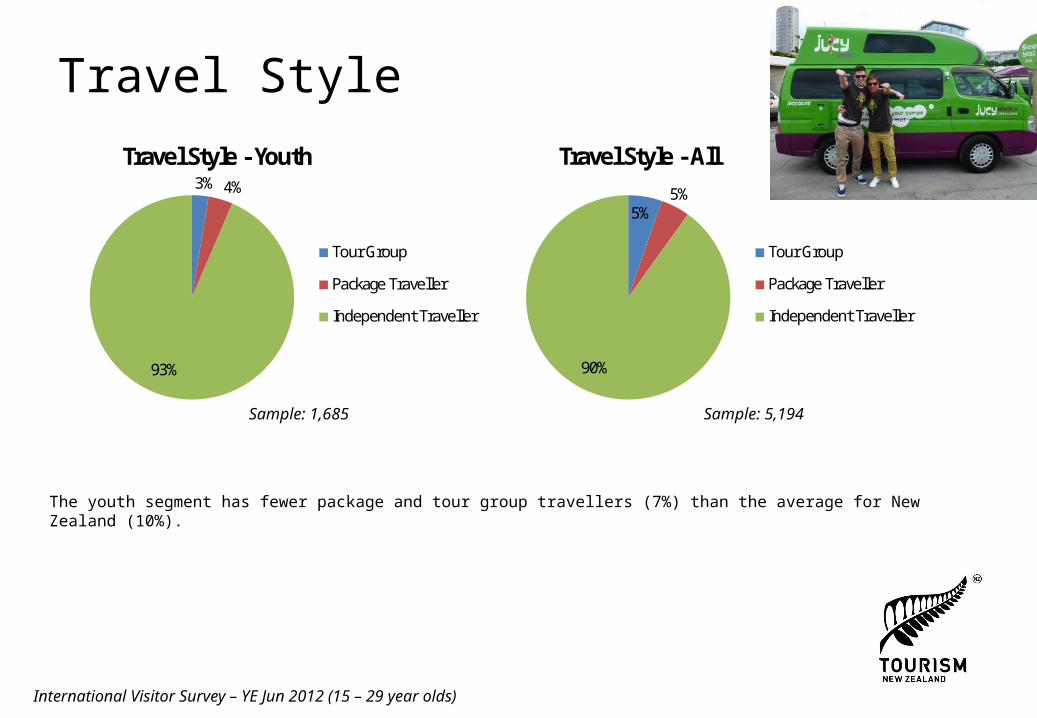

Travel Style

The youth segment has fewer package and tour group travellers (7%) than the average for New Zealand (10%).

International Visitor Survey – YE Jun 2012 (15 – 29 year olds)

Sample: 1,685 Sample: 5,194

3% 4%

93%

Travel Style - Youth

Tour Group

Package Traveller

Independent Traveller

5%5%

90%

Travel Style - All

Tour Group

Package Traveller

Independent Traveller

i-SITE

Youth travellers (40%) are more likely to visit an i-SITE than the average for New Zealand (34%).

International Visitor Survey – YE Jun 2012 (15 – 29 year olds)

Sample: 1,685 Sample: 5,194

40%

59%

1%Visited an i-SITE - Youth

Yes

No

Don't Know

34%

65%

1%Visited an i-SITE - All

Yes

No

Don't Know

Backpackers

Not surprisingly the youth segment has a higher ratio of backpackers (19%) than the average for New Zealand (8%).

Despite this difference between the groups, non-backpackers still make up the vast majority (81%) of the youth segment.

International Visitor Survey – YE Jun 2012 (15 – 29 year olds)

Sample: 1,685 Sample: 5,194

19%

81%

Backpacker - Youth

Backpacker

Non-Backpacker

8%

92%

Backpacker - All

Backpacker

Non-Backpacker

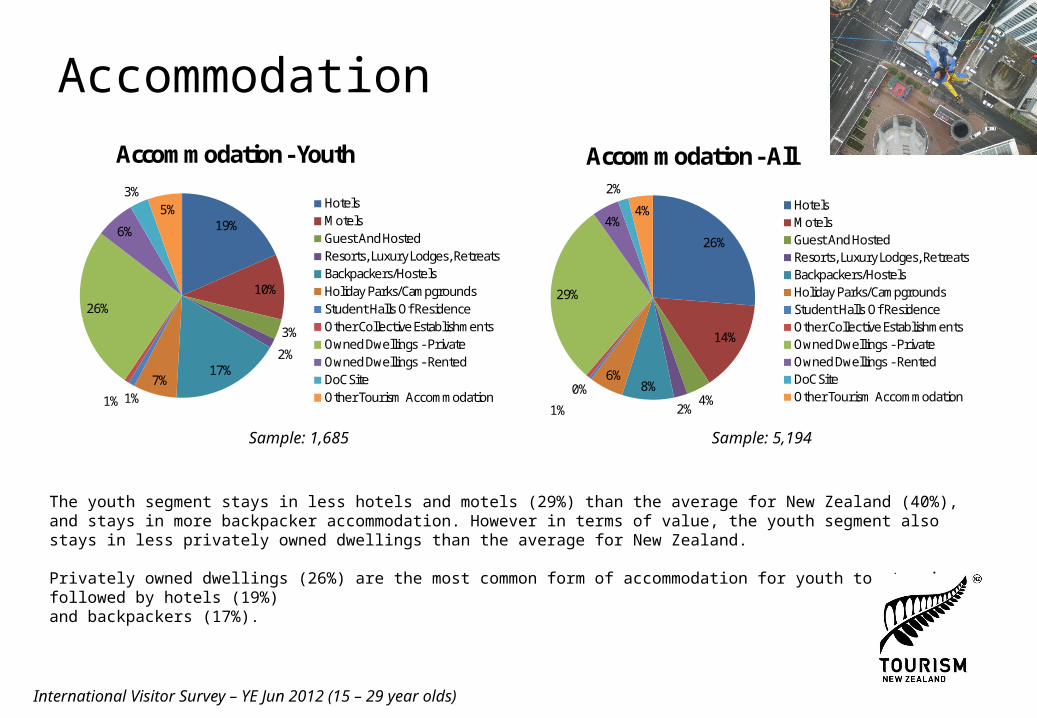

Accommodation

The youth segment stays in less hotels and motels (29%) than the average for New Zealand (40%), and stays in more backpacker accommodation. However in terms of value, the youth segment also stays in less privately owned dwellings than the average for New Zealand.

Privately owned dwellings (26%) are the most common form of accommodation for youth to stay in, followed by hotels (19%)and backpackers (17%).

International Visitor Survey – YE Jun 2012 (15 – 29 year olds)

19%

10%

3%

2%17%

7%1%1%

26%

6%

3%5%

Accommodation - Youth

HotelsMotelsGuest And HostedResorts, Luxury Lodges, RetreatsBackpackers/HostelsHoliday Parks/CampgroundsStudent Halls Of ResidenceOther Collective EstablishmentsOwned Dwellings - PrivateOwned Dwellings - RentedDoC SiteOther Tourism Accommodation

26%

14%

4%2%

8%6%

0%

1%

29%

4%

2%

4%

Accommodation - All

HotelsMotelsGuest And HostedResorts, Luxury Lodges, RetreatsBackpackers/HostelsHoliday Parks/CampgroundsStudent Halls Of ResidenceOther Collective EstablishmentsOwned Dwellings - PrivateOwned Dwellings - RentedDoC SiteOther Tourism Accommodation

Sample: 1,685 Sample: 5,194

Dual Destination

The youth segment has a very similar number of dual destination arrivals as the New Zealand average.

International Visitor Survey – YE Mar 2012 (15 – 29 year olds)

Sample: 1,685 Sample: 5,194

36%

64%

Dual Destination - Youth

Visited Another Country

No Other Countries Visited

35%

65%

Dual Destination - All

Visited Another Country

No Other Countries Visited

People Travelled With

Slightly more youth travel by themselves than the New Zealand average. Also youth are much more likely to travel with friends than the New Zealand average.

Half of all youth travellers travel by themselves, with the addition of 14 per cent that are travelling with friends this mean around 64 percent of youth are singles.

International Visitor Survey – YE Mar 2012 (15 – 29 year olds)

50%

18%

11%

14%

2%1%

0%3%

1%

0%0%

Travelled With - Youth

Travelled AlonePartner/SpouseFamily/WhanauFriendsBusiness AssociatesFamily And FriendsOther CouplesTour GroupSchool Group/Student GroupSpecial Interest GroupOther

46%

22%

13%

7%

4% 1%0%

5%

1%

1% 0%

Travelled With - All

Travelled AlonePartner/SpouseFamily/WhanauFriendsBusiness AssociatesFamily And FriendsOther CouplesTour GroupSchool Group/Student GroupSpecial Interest GroupOther

Sample: 1,685 Sample: 5,194

Activities and Attractions

This index shows firstly which activities youth travellers over index on compared to all tourists, and secondly the percent of youth travellers that undertake particular activities (see percent in brackets on y axis).

Youth travellers over index on a wide range of activities due to their propensity to do more activities while in New Zealand compared to all tourists. Youth travellers do 14.1 activities on average while in New Zealand vs. 13.7 activities on average for all tourists.

Of particular interest is the fact that youth travellers over index on adventure activities. Youth are almost three times more likely to go sky diving and bungy jumping than regular tourists, and are twice as likely to do snow sports, caving, rafting, horse trekking and climbing. 50.3 per cent of youth travellers do some form of adventure tourism while in New Zealand where only 32.9 per cent of all tourists do some form of adventure tourism.

International Visitor Survey – YE Mar 2010 - 2012 (15 – 29 year olds)

100% 150% 200% 250% 300% 350%

Working Holiday (5%)Sky Diving/Parachuting (9%)

Education/Language School (9%)Bungy Jumping (11%)

Snow Sports (11%)Caving (1%)

Canoeing, Kayaking, Rafting (14%)Horse Trekking/Riding (4%)

Climbing (2%)Hunting/Shooting (1%)

Entertainment (47%)Nth Is National Parks (1%)

Paraponting (1%)Motor Sports (3%)

Cycle Sports (5%)Sporting Event (5%)

Theme And Leisure Parks (8%)Swimming (10%)

Performing Arts (3%)Food And Wine Festival (1%)

Whale Watching (4%)Fishing (6%)

Dolphin Watching (7%)Other Scenic/Natural Attractions (59%)

Golf (3%)Volcanic/Geothermal Attractions (31%)

Boating (30%)Other Wildlife Encounters (9%)

Walking And Trekking (80%)Museums And Galleries (28%)

Zoos/Wildlife/Marine Parks (11%)Other Major Events (4%)

Shopping (81%)

Youth Activity Index

Sample: 5,350

Regional Visitation

The youth market generally has a similar regional visitation profile as all visitors. Two clear differences are that youth generally visit more regions than average and also youth are slightly less likely to visit Auckland than all visitors.

International Visitor Survey – YE Mar 2012 (15 – 29 year olds)

Sample: 1,685

0%10%20%30%40%50%60%70%80%90%

Perc

ent o

f Tou

rists

Regional Visitation

Youth

Total

Queenstown

As part of a separate analysis it was found international tourists that visit Queenstown were highly over-represented by youth travellers.

International Visitor Survey – YE Dec 2011International Travel and Migration Survey – YE Dec 2011

1%4%

35%

17%

10%14% 13%

4%0% 0%

0%

5%

10%

15%

20%

25%

30%

35%

40%

Under 10 Years

10 - 19 Years

20 - 29 Years

30 - 39 Years

40 - 49 Years

50 - 59 Years

60 - 69 Years

70 - 79 Years

80 - 89 Years

90 Years and

Over

Arr

ival

sAge Profile of Queenstown International Tourists

Age of Australian Ski MarketThe ski market is much younger than the total of all Australian holiday tourists. Almost two thirds of the Australian ski market are aged between 15 and 34.

0%

5%

10%

15%

20%

25%

30%

35%

15 to 24 25 to 34 35 to 44 45 to 54 55 to 64 65+

Perc

ent o

f Arr

ival

s

Ski Australia All Australia

Source: International Visitor Survey: YE March 09 to 12

Australia as a Source Market

Australia As A Source Market

532,869

311,223

Total Youth Arrivals - 2011

Non Australian Residents

221,646Australian

Residents*

*Australian Residents are classed in NZ arrivals as people that have lived in Australia for 12 months or more

95,234Arrive in New Zealand

after visiting and spending time in

Australia

60% of the youth market originate from Australia as either Australians or visitors to Australia.

Australia as a Source Market

532,869221,646

Total Youth Arrivals - 2011

Australian Residents*42% of total

youth

*Australian Residents are classed in NZ arrivals as people that have lived in Australia for 12 months or more

123,645Australian Residents

and Australian Citizens

23% of total

youth

70,320Australian Residents

but NZ Citizens

13% of total

youth

28,061Australian Residents

but not Aust or NZ Citizens5% of total

youth

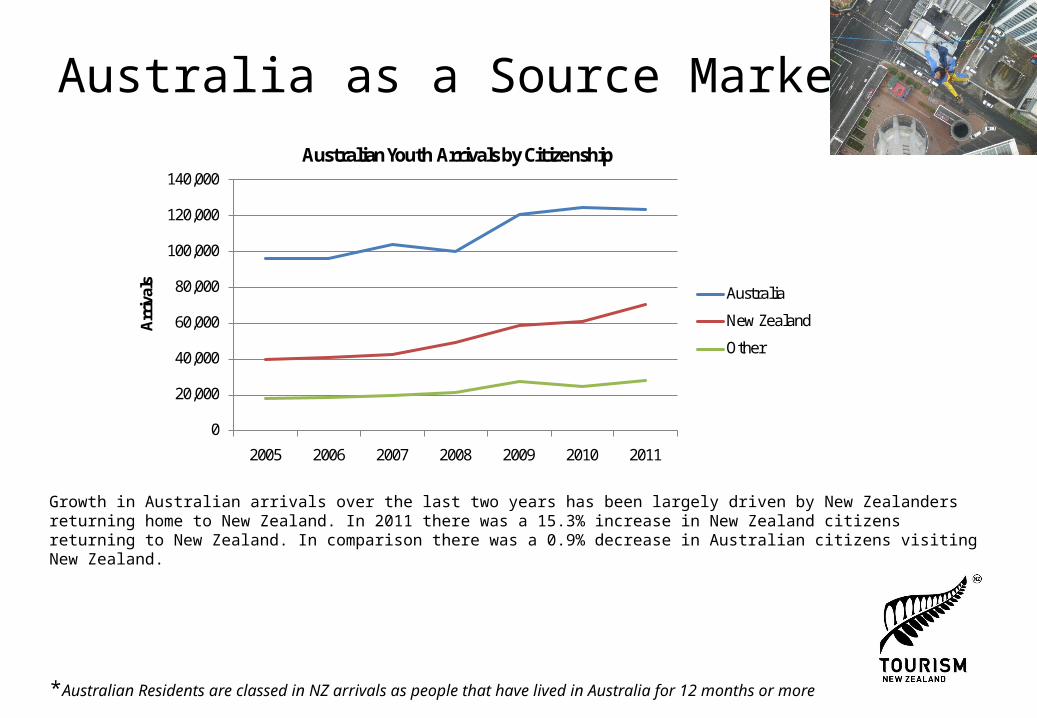

Australia as a Source Market

*Australian Residents are classed in NZ arrivals as people that have lived in Australia for 12 months or more

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

2005 2006 2007 2008 2009 2010 2011

Arr

ival

sAustralian Youth Arrivals by Citizenship

Australia

New Zealand

Other

Growth in Australian arrivals over the last two years has been largely driven by New Zealanders returning home to New Zealand. In 2011 there was a 15.3% increase in New Zealand citizens returning to New Zealand. In comparison there was a 0.9% decrease in Australian citizens visiting New Zealand.

Related Documents