What is Economics?

What is Economics?. Definition: study of how individuals & societies make choices about ways to use scarce resources to fulfill their wants.

Dec 24, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

What is Economics?

What is Economics?

• Definition: study of how individuals & societies make choices about ways to use scarce resources to fulfill their wants

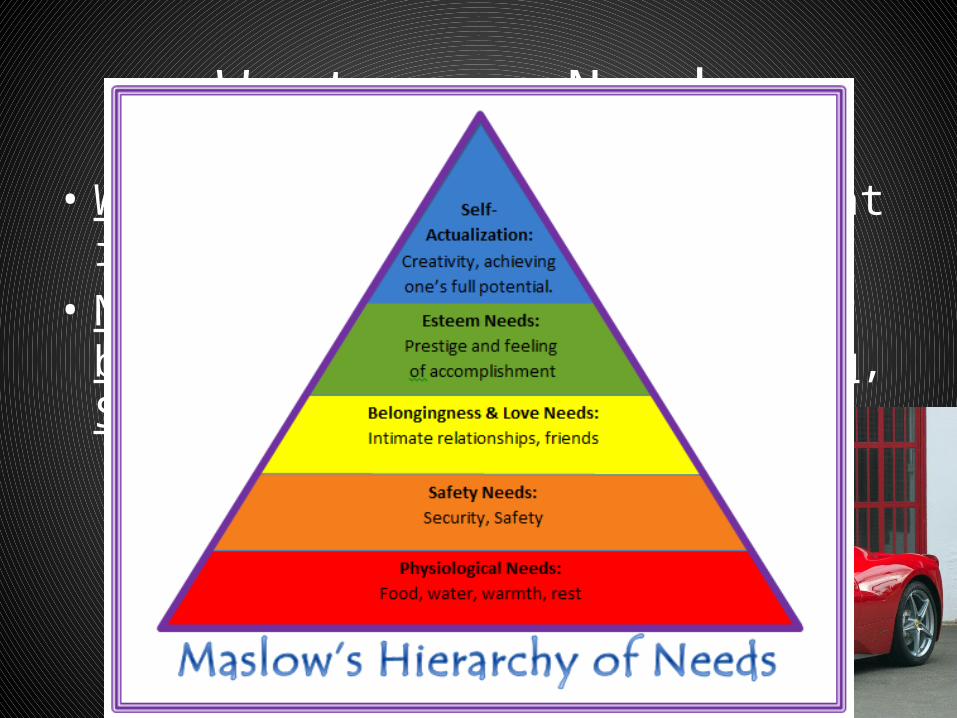

Wants vs. Needs

• Wants: anything other than what is needed for basic survival

• Needs: things required for basic survival (Food, Clothing, Shelter)

Wants vs. Needs

• Example: In 1901, people discovered oil in Texas – but they were actually looking for water. Disappointed, they offered to trade the oil for water at a ratio of 1:1 (1 barrel of oil for each barrel of water).

Problem of Scarcity

• Scarcity is THE fundamental problem in economics

• Maintains that all resources are limited• People will compete for these limited

resources• Scarcity exists because people cannot satisfy

their every want

Factors of Production

• Definition: what goes into producing a product• 4 Factors of Production:1. Capital: previously manufactured goods used to

make other goods & services2. Entrepreneurship: ability of individuals to start

new businesses & develop new products; Risk-taker; lemonade stand example

3. Land: natural resources & surface land & water4. Labor: human effort directed toward production

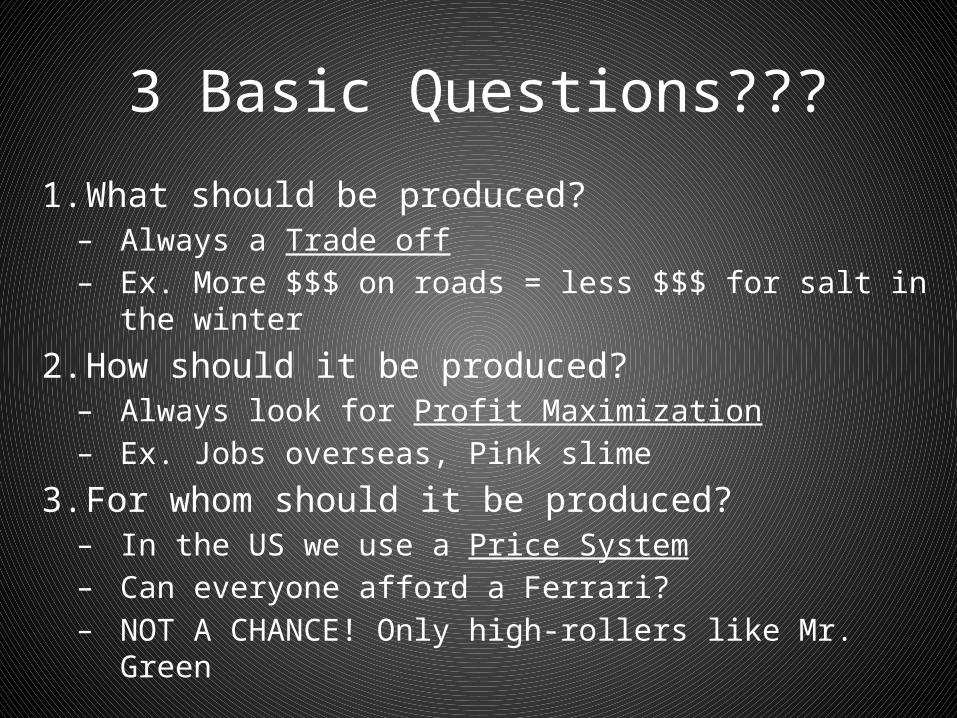

3 Basic Questions???

1. What should be produced?– Always a Trade off– Ex. More $$$ on roads = less $$$ for salt in the winter

2. How should it be produced?– Always look for Profit Maximization– Ex. Jobs overseas, Pink slime

3. For whom should it be produced?– In the US we use a Price System– Can everyone afford a Ferrari?– NOT A CHANCE! Only high-rollers like Mr. Green

Supply & Demand

• Is what determines this price system• Demand: represents a consumer’s willingness

and ability to pay; how we define this is with...• Law of Demand: As price goes up, quantity

demanded goes down; as price goes down, quantity demanded goes up

Supply & Demand

• Factor effecting quantity demanded of a product:– Real Income: people are limited by income as to what

they can buy; only a few that can afford a Ferrari– Substitution Effect: people can replace one product

with another if it satisfies the same need– Diminishing Marginal Utility: how one’s additional

satisfaction for a product lessens with each additional use/purchase of it

Supply & Demand

• Supply: willingness and ability of producers to provide goods and services

• Law of Supply: As prices increase, the quantity supplied increases, as prices decrease, the quantity supplied decreases

Supply & Demand

• Factors Determining Supply: • Price of Inputs: how much it costs to produce

the product• Number of firms in the industry: competition;

more = more supply; less = less supply• Taxes: increase = reduction of supply (not

making as much money off product)• Technology: increase can reduce cost of

production and increase supply

Putting Supply & Demand Together

• Equilibrium Price: point at which quantity demanded & quantity supplied meet

• Shortage: causes prices to rise, while a Surplus causes prices to drop…Why???

• Price Ceiling: prevents prices from going above a specified amount; Ex. Rent in NYC

• Price Floor: prevents prices from dropping too low; Ex. Minimum wage

Related Documents