Get the facts What every homeowner who is at least 62 years of age should know about reverse mortgage loans Chris Beard, NMLS# 353274 Reverse Mortgage Specialist 9822 Montague Street ● Tampa, FL 33626 Cell: 813-857-1254 ● Toll Free: 866-684-7868 [email protected] www.GoLocalReverseMortgage.com

What is a Reverse Mortgage

Nov 03, 2014

Tampa FL as a reverse mortgage consultant. Chris Beard works exclusively with senior homeowners seeking a reverse mortgage, a home financing program that allows mature homeowners to utilize the equity in their homes to supplement retirement income.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Get the facts What every homeowner who is at least 62 years of age should know about reverse mortgage loans

Chris Beard, NMLS# 353274

Reverse Mortgage Specialist

9822 Montague Street ● Tampa, FL 33626

Cell: 813-857-1254 ● Toll Free: 866-684-7868

www.GoLocalReverseMortgage.com

2

1. Consult a tax advisor

What is a reverse mortgage loan? It’s a home loan that enables you to convert a portion

of your home equity into potentially tax-free funds1

Unlike a traditional mortgage, you do not need to repay the loan

as long as you or one of the borrowers continues to live in the home, keep the taxes and insurance on the property current, maintain the property to FHA standards and all other program requirements are met

1. Consult a tax advisor

3

Why get a reverse mortgage loan?

A reverse mortgage loan can give you access to your home equity without the burden of monthly mortgage payments as a traditional mortgage

Again, unlike a traditional mortgage, you do not need to repay the loan as long as you or one of the borrowers continues to live in the home, keep the taxes and insurance on the property current, maintain the property to FHA standards and all other program requirements are met

Why get a reverse mortgage loan? Reverse mortgage loan proceeds may be used for any purpose,

including: Meeting daily or monthly expenses

Covering healthcare costs

Remodeling or home repairs

Consolidating credit card debt

Refinance your existing mortgage to a reverse

mortgage loan, without making the monthly

mortgage payments of a traditional mortgage2

With the reverse mortgage loan for purchase feature, the loan proceeds may be used to help you buy a new primary residence better suited to your needs

4

2. Borrower is required to refinance the existing mortgage balance with the reverse mortgage loan proceeds or own the home free and clear.

5

How are the reverse mortgage loan proceeds disbursed?Distribution options to receive your reverse mortgage proceeds:

Lump sum — a specific amount is made immediately available (required with a fixed-rate reverse mortgage loan)

Term — funds are released in fixed monthly amounts for a set period requested by the customer with a variable-rate reverse mortgage line of credit

Tenure — funds are distributed in equal monthly advances for as long as at least one borrower continues to occupy the home as a principal residence with a variable-rate reverse mortgage line of credit

Line of credit — funds remain available for the borrower to draw on as needed or in automatic monthly disbursements

Combination — with a variable-rate reverse mortgage, choose any combination of lump sum, monthly advances or line of credit disbursements; even receive an initial lump sum and leave the rest in a line of credit. Change the way proceeds are received as often as you wish provided sufficient loan proceeds are available.

6

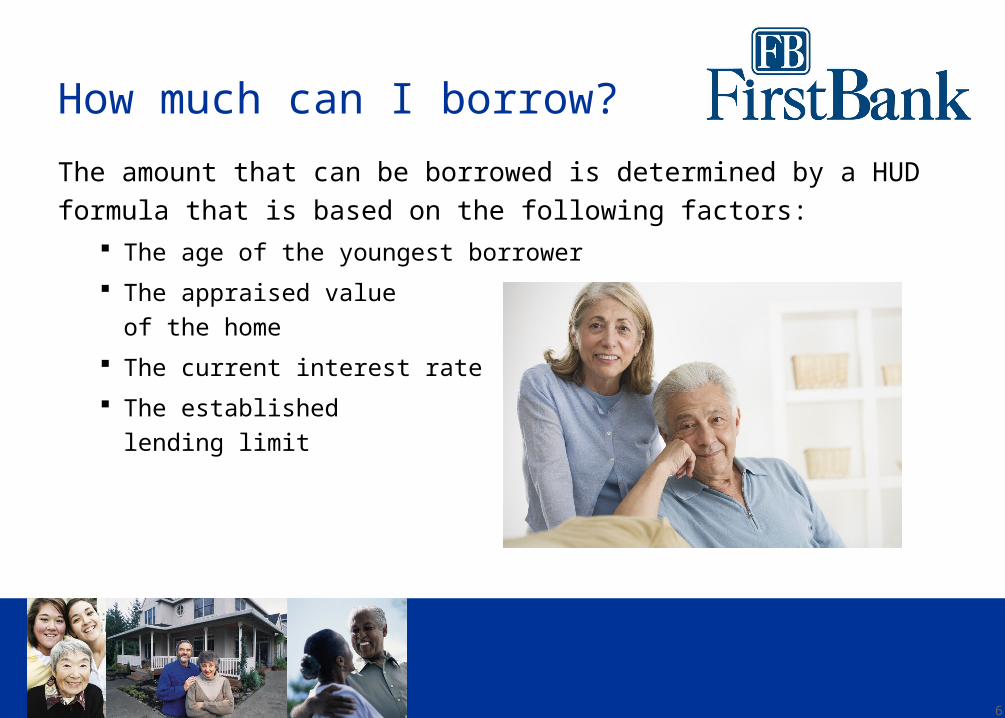

How much can I borrow?

The amount that can be borrowed is determined by a HUD formula that is based on the following factors:

The age of the youngest borrower

The appraised value of the home

The current interest rate

The established lending limit

7

What are the interest rate options? Both fixed-rate and variable-rate reverse mortgage loans.

With a fixed-rate reverse mortgage loan, your interest rate will remain the same throughout the life of the loan You would receive a lump sum distribution

With a variable-rate reverse mortgage loan, the interest rate may adjust monthly The frequency at which your interest rate adjusts — will not affect the

number of loan advances you receive, but will affect how fast or slow your loan balance grows

You can change your distribution options as often as you like

8

How does a reverse mortgage loan differ from a traditional mortgage?With a traditional mortgage or home equity loan:

Borrowers qualify based on their income, employment and credit score. These loans require the borrower to repay the amount borrowed by making monthly mortgage payments over a specified term to the loan servicer.

With a reverse mortgage loan: There are no income, employment or credit score qualifying

restrictions.3

3. Reverse mortgage borrowers are required to obtain an eligibility certificate by receiving counseling sessions with a HUD-approved agency. Family members are also strongly encouraged to participate in these informative sessions.

9

Age and eligibility requirements

You and any co-borrowers must be at least 62 years of age

Your home must be your primary residence

You must own your home free and clear, or the

existing mortgage is required to be refinanced

with the reverse mortgage proceeds

Educational counseling with a HUD-approved

counselor is required

10

Reverse mortgage costs

A deposit for the appraisal is an out-of-pocket cost

There are additional closing costs which may be financed as part of the loan such as:

Title insurance

Mortgage insurance premiums

Attorney fees

11

Reverse mortgage repayment

You do not need to repay the loan as long as all program requirements are met, including: You or one of the borrowers continue to live in the house You keep the taxes and insurance on the property current You maintain the property to FHA standards

The balance due can come from home sale proceeds, or from other resources such as, personal savings, life insurance or possibly applying for a new mortgage. There is no requirement the home be sold, only that the loan be repaid.

Reverse mortgage repayment

There is no requirement that the home be sold,

only that the loan be repaid.

If you die and your heirs choose to retain ownership

of the home, the full outstanding loan balance must

be paid. And, there is a possibility that the balance owed may be greater than the value of your home.

Because the home is the only collateral attached to the loan, any remaining home equity, along with your other possessions, belongs to you or your heirs.

12

13

Three essential facts

Making an educated decision begins with understanding your responsibilities when applying for a reverse mortgage loan.

Three points you need to be aware of are:

1. You must live in the home as your primary residence.

2. You must stay current on property tax and homeowners insurance payments and maintain the home to FHA standards.

3. If you or your heirs choose to retain ownership of the home, the full outstanding loan balance must be paid. Depending on how long the loan has been in place and market conditions, there is a possibility the loan balance may be higher than the value of the home.

14

The reverse mortgage loan process1. Discuss your home financing goals with a reverse mortgage

consultant. 2. Receive consumer counseling from a HUD-approved

counselor.3. Meet with a FirstBank Mortgage reverse mortgage consultant

to apply for your loan. Fill out an application Select a payment plan Present required documentation

4. Underwriting and loan decisions take place.

15

The reverse mortgage loan process5. Upon approval, a closing is scheduled with all of the required

parties, which may include your lender, your attorney and the title company representative

6. Depending on your state’s laws, you can choose where you would like the closing to take place, the closing can take place in the title office, or your home.

7. After the 3 day right of rescission, and any existing debt on your home is paid in full with proceeds from your new reverse mortgage loan, your remaining loan proceeds are disbursed.

Who owns the home?

Can the bank take my home?

16

What have we learned?

17

What have we learned?

Are there restrictions on how I can use my reverse mortgage proceeds?

18

What have we learned?

Will receiving my reverse mortgage proceeds in monthly payments affect my Social Security or Medicare benefits?

If you opt to receive monthly payments, they will not affect your Social Security or Medicare benefits.

However, your eligibility for need-based programs such as Medicaid or state assistance programs may be impacted. We recommend that you consult a tax or legal advisor and your local Area Agency on Aging for more information.

19

Count on our capabilities

FirstBank is Tennessee’s largest independently owned and operated bank, with more than $2 billion in total assets.

FirstBank has mortgage bankers in 19 locations across the entire Southeast.

Reverse mortgage loans are insured by the Federal Housing Administration (FHA), part of the U.S. Dept of Housing and Urban Development.

20

FirstBank Mortgage provides a variety of loan products with different rates, payments and fees. Please discuss financing alternatives with your mortgage consultant so that you can select the financing you determine is the most advantageous for you. The information in this presentation is accurate as of the date of printing and is subject to change without notice.

Reverse mortgage loans

I’m ready to listen to your needs and help you understand your reverse mortgage loan options, so you can make an informed decision.

Chris Beard, NMLS# 353274

Reverse Mortgage Specialist

9822 Montague Street

Tampa, FL 33626

Cell: 813-857-1254

Toll Free: 866-684-7868

www.GoLocalReverseMortgage.com

Related Documents