ELSEVIER Journal of Development Economics Vol. 52 (1997) 279-294 JOURNAL OF Development ECONOMICS Welfare effects of liberalization reforms with distortions in financial and labor markets Ann Marie Battle * Economics Department, Virginia Commonwealth Universi~. , PO Box 4000, Richmond, VA 23284-4000, USA Received 27 May 1994; revised 29 August 1995 Abstract Liberalization can have ambiguous effects on welfare and produce unexpected macroe- conomic changes because of conflicting effects stemming from distortions in other markets both within the same period and across time. This approach presents a two-period intertemporal model of a small open economy to examine the welfare effects of removing one distortion (financial repression, tariffs) while others (wage and price rigidity) remain in place. The equilibrium conditions from this model are used to derive welfare effects of various liberalization policies and to determine optimal levels of the policy variables. © 1997 Elsevier Science B.V. JEL classification: O10; O12 Keywords: Trade; Liberalization; Welfare 1. Liberalization issues The Southern Cone countries of Latin America, namely Argentina, Chile, and Uruguay, implemented liberalization policies during the 1970s. The liberalization in each country involved varying degrees of decontrol over external trade, domestic financial markets, and international capital flows, The experience of the Southern Cone countries, as well as others, gives rise to some important questions * Tel.: (804) 828-7148; fax: (804) 828-1719; e-mail: [email protected]. (1304-3878/97/$17.00 © 1997 Elsevier Science B.V. All rights reserved. PII S0304-3878(96)0045 1-8

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

ELSEVIER Journal of Development Economics

Vol. 52 (1997) 279-294

JOURNAL OF D e v e l o p m e n t E C O N O M I C S

Welfare effects of liberalization reforms with distortions in financial and labor markets

Ann Marie Battle *

Economics Department, Virginia Commonwealth Universi~. , PO Box 4000, Richmond, VA 23284-4000, USA

Received 27 May 1994; revised 29 August 1995

Abstract

Liberalization can have ambiguous effects on welfare and produce unexpected macroe- conomic changes because of conflicting effects stemming from distortions in other markets both within the same period and across time. This approach presents a two-period intertemporal model of a small open economy to examine the welfare effects of removing one distortion (financial repression, tariffs) while others (wage and price rigidity) remain in place. The equilibrium conditions from this model are used to derive welfare effects of various liberalization policies and to determine optimal levels of the policy variables. © 1997 Elsevier Science B.V.

JEL classification: O10; O12

Keywords: Trade; Liberalization; Welfare

1. Liberalization issues

The Southern Cone countries of Latin America, namely Argentina, Chile, and

Uruguay, implemented liberalization policies during the 1970s. The liberalization in each country involved varying degrees of decontrol over external trade, domestic financial markets, and international capital flows, The experience of the Southern Cone countries, as well as others, gives rise to some important questions

* Tel.: (804) 828-7148; fax: (804) 828-1719; e-mail: [email protected].

(1304-3878/97/$17.00 © 1997 Elsevier Science B.V. All rights reserved. PII S0304-3878(96)0045 1-8

280 A.M. Battle/Journal of Development Economics 52 (1997) 279-294

regarding liberalization policies. Specifically, if both the current and capital accounts are controlled, in which order should they be opened? Should the policy reforms be carried out gradually or all at once (one-stage)? The focus of this paper will be to explore these questions with two additional distortions added to the analysis: financial repression and real wage rigidity.

Liberalization can have ambiguous effects on welfare because of conflicting effects which were summarized by Edwards (1989). Direct effects occur in the market in which the reform has taken place and within the same time period. These correspond to the efficiency gains from liberalization. Intratemporal indi- rect effects occur within the period in which the reform occurs because of the interaction between two or more distortions in different markets. Finally, intertem- poral indirect effects stem from the dynamic nature of the model and show that a reform in one period alters the equilibrium in distorted markets in the next period (or vice versa).

Welfare implications of liberalization have been discussed by Frenkel (1982), Krueger (1986), McKinnon (1982) and others, but Edwards and van Wijnbergen (1986) formalized the discussion using an intertemporal optimization model of a small open economy. Extensions of the Edwards and van Wijnbergen model were developed by Rodrik (1987) who added a wage-price rigidity and KShkiSnen (1987) who added financial repression to the analysis. The authors generally agree that the current account should be opened first because the negative indirect welfare effect of opening the capital account in the presence of trade distortions will be greater than the indirect effects resulting from the opposite ordering. 1

As Rodrik (1987) stressed, the issue of sequencing of the current and capital account liberalization is trivial unless there are other distortions which cannot be eliminated immediately. In my model the "additional distortions" are financial repression and wage-price rigidity. I build on the work of Edwards and van Wijnbergen (1986), Rodrik (1987), and KS_hk~Snen (1987) to develop a more general model in which the combination of Keynesian disequilibrium and financial repression can be examined in a single framework to analyze the welfare effects of liberalization. Specifically, the addition of financial repression and wage-price rigidity produce intertemporal and intratemporal effects which harm welfare.

The paper is organized in the following manner. Section 2 presents the foundation of the two-period intertemporal model used to analyze sequencing and timing issues of liberalization reform. The welfare effects of each liberalization policy are analyzed in Section 3, while the final section consists of some general conclusions regarding liberalization in an economy with financial repression and a Keynesian wage-price rigidity.

] K~hktinen actually finds an independence of the effects of opening the current and capital accounts, but a strong relationship between trade liberalization and domestic financial deregulation.

A.M. Battle / Journal of Development Economics 52 (1997) 279-294 28 l

2. The model: financial repression and wage-price rigidity

The model developed in this section follows KahkBnen (1987) in incorporating domestic financial liberalization. The model under consideration is a two-period intertemporal model of a small open economy which produces two goods in each period: an exportable (not consumed domestically) and a nontradeable. Con- sumers, on the other hand, consume an importable (not produced domestically) and a nontradeable. The domestic prices for these goods are: 1, pi, and qi, where the world price of the traded goods are normalized to unity and superscripts denote the time periods (i = 1, 2). There are two factors of production, labor and capital, with labor freely mobile across sectors in both periods and capital sector-specific in the first period and mobile in the second.

2.1. Consumpt ion

Consumers ' behavior may be captured by use of the expenditure function, defined as the minimum expenditure needed to achieve a level of welfare u, at given prices. 2 Assuming that the utility function is weakly separable in its arguments in the two periods, the expenditure function is written as:

E = E[Tr ' ( p l , q l ) , r D T r 2 ( pZ ,qZ) ,L1 ,LZ ,u]

where 7r I and 7r 2 are the exact price indices for each period and u is a f ixed level of welfare. Following Rodrik (1987), the labor supplied in each period also is an argument of the constrained expenditure function since consumers are rationed in their supply of labor due to the assumption that wages are fixed above the market-cleat ing level. 3

2.2. Product ion

Due to the assumed excess supply of nontraded goods, producers are con- strained to produce the demand-determined amount of the nontraded good, N i. Producers maximize revenue from production of the exportable and nontradeable goods given prices and factor supplies. 4

2 The derivation is as follows: ,-1 i , q i c i ]U( . )> E['] = min{ ~,~ D [ p % + _u}

3 Subscripts denote a partial derivative with respect to the appropriate argument in the expenditure function. For example, E 3 is the derivative of the expenditure function with respect to labor in the first period. See Rodrik (1987), p. 116. Some noteworthy properties of the expenditure function include the fact that it is increasing in all of its arguments and it is concave as well as homogeneous of degree one in prices (K~hk~Snen, 1987, p.535). Also see Dixit and Norman (1980) for more on duality and the properties of the expenditure function.

4 The general form of the revenue function is: R i( l, q i L i, K i) = max{ Qi, + q iQil( Qi x ,Qi l J, K ) feasible}

where Qi denotes output of the exportable and Q~ denotes output of the nontradeable.

282 A.M. Battle/Journal of Development Economics 52 (1997) 279-294

Producer behavior is represented by a constrained revenue function, given the quantity demanded of the nontraded good, N~:

e i ( l , q i , L i , g i , N i ) ~- max{Q / + qiNi l ( Qi,Ni,Li ,K )feasible}

The constrained revenue function can be rewritten using the homogeneity and derivative properties (see Dixit and Norman, 1980, p. 33):

e i ( . ) = RI(I,77i,Li,K) + qiRi2(l,~i,Li,K )

--i i --i i =Ri(1,~i,Li ,K) + qiR~(1,pi,~li,Li,K ) + (qi q )R2(1, q , L , K )

= Ri(1,~i,Li,K) + (qi ~i)Ni

The R(-) functions without overbars represent unconstrained revenue functions. 5 The "virtual price" of the nontraded good is given by ~i, which is the price at which producers would willingly supply the demand-determined amount N~:

Ni= Ri2(1,~i,IJ,K)

Similarly, the supply function of the exportable is given by the partial deriva- tives of R 1 and R 2 with respect to the price in each period.

Since investment becomes productive in the second period, the revenue func- tion for period two will include investment: 6

R2(1,gI2,L2,K + I )

thus the capital stock in the second period is equal to the first-period capital stock plus investment (K z = K 1 + I). 7

The demand for labor is determined by producers setting the value marginal product of labor equal to the fixed wage rate:

W i = R~(1 -i i ,q ,L ,K)

2.3. Financial sector

The banking sector reflects financial repression in the economy (see K~kSnen, 1987) in a simple fashion by focusing on interest rate controls and ignoring the additional financial repression caused by high reserve requirements. The govern- ment has a monopoly in the banking sector and, thereby, controls the domestic

5 See Neary and Roberts (1980) for a discussion of unconstrained and constrained functions. 6 Following K~ihkiSnen, I assume that only the exportable good is used in investment. This

assumption also has been made by Edwards and van Wijnbergen (1986). In addition, this model is set up so that producers are the only economic agents who invest.

7 The investment function can be derived from the profit maximizing condition: 6LR](I,q2,L2,K + 1) = 1, yielding 1 = I(SL), I' > O.

A.M. Battle/Journal of Development Economics 52 (1997) 279-294 283

deposit rate so as to keep it below the world interest rate. The potential excess demand for loanable funds at the controlled deposit rate r o is eliminated by a tax on international capital movements which basically drives a wedge between loan and deposit rates and keeps the domestic loan rate above the world interest rate. Households and finns are prohibited from carrying out transactions in the interna- tional capital markets. The equilibrium interest rate (on deposits and loans) that would prevail in a liberalized domestic financial market with free international movements would tend toward the world interest rate. 8

2.4. Equilibrium

In equilibrium, expenditure will equal income and this condition can be summarized by an intertemporal version of the income-expenditure identity:

E [ T r ' ( p ' , q i ) , 6 o T r 2 ( p2,qz),LI,L2,u] = y' + 6by 2

With some manipulation, households' discounted lifetime income can be written: 9

y =yl + 6oy2

= 8o( 2 + , % , )

- - ( 8 D / 8 " -- 1)((1 + t ' )E , , + q'E12 )

The prices of the traded goods are exogenous in a small economy and normalized to unity, for simplicity, so we substitute p~ = 1 + t I and p2 = 1 + t z, to obtain the final equilibrium condition of the model, equating intertemporal income and expenditure:

E [Tr ' ( (1 +t ' ) ,q l ) ,8oTr2((1 +t2),qZ),L' ,LZ,u]

= re , t) + + , % , )

- ( ( 8 o / 6 " ) - 1)((1 + t ' )El , + q'E,2 )

3. Welfare effects of liberalization

Given the equilibrium condition which concisely summarizes the behavior of the economy, I will derive the welfare effects of various liberalization policies. I

The equilibrium domestic interest rate will not necessarily equal the world interest rate due to such factors as differing degrees of risk for domestic assets as compared to foreign assets and the expected depreciation of the domestic currency vis-h-vis the foreign currency.

9 The derivation of household discounted lifetime income is provided in Appendix A.

284 A.M. Battle/Journal of Development Economics 52 (1997) 279-294

examine the welfare effect of each liberalization policy assuming the other distortions remain in place. This method is particularly important in analyzing domestic financial deregulation, since most of the authors (with the exception of K~ihk~inen, 1987) assume that the domestic financial system has been deregulated and is functioning efficiently. In Appendix A the above equations are used to solve the system, deriving the reduced form equation which expresses welfare as a function solely of the policy variables. The resulting equation is of the form:

A d u = B d t ~ + C d t 2 + D d q J + E d q 2 + F d 8 o + G d 6 L + H d w 1 + I d w 2

3.1. F i r s t - p e r i o d t rade l ibera l i za t ion

Trade liberalization involves reducing the tariff partially in period one and completely in period two (gradual liberalization) or lowering the tariff completely in both periods (abrupt liberalization). The effect of a first-period tariff can be seen by the terms:

du B ~0

dt ~ A

For trade liberalization to increase welfare unambiguously we would like to show that d u / d t ~ < 0. A positive sign for term A is necessary for the stability of the system, therefore term B must be negative for the desired effect on welfare. However, trade liberalization will have an ambiguous effect on welfare in an intertemporal model because of several conflicting factors which are reflected in the different components of term B. These components can be categorized in terms of the three possible types of effects discussed in the introduction: direct, intratemporal indirect and intertemporal indirect.

The reduction of the tariff will cause a static welfare gain due to the correction for underconsumption of the previously protected good. This direct effect is negative and proportional to the first-period tariff. There are several intratemporal indirect effects stemming from the distortions in the nontradeables, labor, and financial markets. Beginning with the financial market, tariff reduction in the first period will shift consumption to the first period, thus reducing saving. In an economy with financial repression (low deposit rates) and a small tariff in period one, this effect will worsen already suboptimal saving (K~ihkiSnen, 1987, p. 542) causing a deterioration of welfare.

Ambiguity also arises due to additional factors stemming from the wage and price rigidities. Aggregate employment will fall during a first-period trade liberal- ization, increasing the excess supply of labor which already existed due to the fixed wage, thus having a negative effect on welfare. In the market for the nontraded good, a lower tariff will cause a shift in consumption from the nontradeable to the importable, aggravating the excess supply due to the distortion

A.M. Banle / Journal of Development Economics 52 (1997) 279-294 285

in that market. This negative effect on welfare is proportional to the price wedge, (ql _~1) .

The intertemporal indirect effects for each market are of the opposite sign from the direct and intratemporal indirect effects. The effect of first-period trade liberalization on second-period consumption of the importable good is positive because as the tariff in period one falls, second-period consumption falls as expenditure shifts to the first period. The extent of the fall in second-period consumption of the importable is proportional to the second-period tariff. This intertemporal expenditure-switching effect has a negative impact on welfare and is magnified by the domestic financial market distortion.

In addition to the negative intertemporal effect in the importables sector, there are some positive intertemporal effects stemming from the distortions in other markets. The reduction of the first-period tariff not only affects consumption of the importable in period two, but also increases consumption of the nontradeable in the second period. This will have a positive effect on welfare since it will alleviate some of the excess supply due to the fixed price. Additionally, since the demand for the nontradeable increases so will aggregate employment in period two, providing an additional positive effect from the trade reform.

In conclusion, first-period trade liberalization will be welfare-improving if the initial tariff (t 1) is high and if the second-period tariff, t 2, and first-period price wedges, (ql _~/1) and (w 1 - E 3) are small. The presence of the Keynesian disequilibria strengthens the argument for gradualism because the complete re- moval of the tariff in period one may not improve welfare. The high initial tariff is important to promote sufficient savings due to the financial repression. Addition- ally, the smaller the degree of financial repression or the closer 6 0 is to 6 *, the more likely trade liberalization will improve welfare. In the case just described, the static welfare gain which traditionally stems from trade liberalization will outweigh the negative indirect effects and d u / d t 1 will be negative, showing a favorable effect of trade liberalization.

3.2. Second-period trade liberalization

In this section I examine the effect of an anticipated second-period trade liberalization, keeping in mind that this is a model with perfect foresight. 10 The effect on welfare is seen by the derivative of welfare with respect to the tariff in period two:

du C ~0

dt 2 A

The effect of a second-period trade reform is analogous to the first-period trade

l0 I am also assuming that the government policy is credible enough that the public believes the second-period trade liberalization will in fact take place.

286 A.M. Battle/Journal of Development Economics 52 (1997) 279-294

liberalization, and hinges on the sign of term C above. Again, the components of term C consist of direct, intratemporal indirect, and intertemporal indirect effects. Of course, the reduction of the tariff in period two causes a static welfare gain which is the direct effect on welfare. The indirect effects are exactly analogous to those obtained in the first-period trade liberalization though they are opposite in sign. The only exception is the intertemporal effect on first-period savings due to the reduction of the tariff in period two. Consumption shifts from the present to the future as a result, and thus saving increases in period one, showing a favorable effect on welfare. In general, more of the intertemporal and intratemporal effects of trade liberalization are positive in the case of a second-period tariff reduction as compared to trade liberalization in the first period. This result, coupled with the possibility that the government may obtain the instruments with which to remove the wage and price rigidities in the longer run, or that markets may adjust automatically, provides additional support for the argument that trade liberalization should be carried out gradually rather than abruptly.

3.3. Domes t ic f inanc ia l liberalization

The domestic financial liberalization of this section consists of raising the deposit rate of interest, or lowering 6 0 , in the first period. In order for financial liberalization to improve welfare, the derivative, d u / d 6 o, must be negative. This derivative is:

du F

d6 o A

Domestic financial liberalization has an ambiguous effect on welfare, as seen by the conflicting signs of the components of term (F). The direct effect of an increase in the deposit rate is welfare-improving because, with a low initial tariff in period one, savings increase from a level that was previously suboptimal. On the other hand, the presence of a high tariff in period one may cause oversaving which is only worsened by the rise in the deposit rate. 1~

The intratemporal effects of financial deregulation occur in the nontradeable and labor markets. Since a higher deposit rate causes a transfer of income from expenditure to savings, the demand for the nontraded good in period one will decrease. The excess supply due to the price rigidity will worsen, thus the effect on welfare is negative. Additionally, since consumption falls in period one, aggregate employment will fall, causing a welfare deterioration.

The intertemporal effects of financial deregulation all tend to improve welfare. The intuition behind this is the fact that the higher deposit rate in period one shifts consumption from the present to the future. Since the markets for the importable,

11 These first two results are all that KEhkiSnen obtains in his more simple model.

A.M. Battle / Journal of Development Economics 52 (1997) 279-294 287

nontradeable, and labor are all distorted in period two, with excess supply in each market, the welfare effect will be positive. In the importable and nontradeable goods markets the increased expenditure in period two corrects the underconsump- tion due to the tariff and the fixed price of the nontraded good. Finally, increased consumption in period two promotes an increase in aggregate employment in the second period which is also welfare-improving.

The conclusion to be drawn from this exercise is that domestic financial deregulation will have beneficial effects on welfare only if the distortions in the nontradeable, importable, and labor markets are relatively small in period one. The positive welfare effect will hold true regardless of the tax on foreign borrowing. Therefore, I conclude that domestic financial deregulation should proceed gradu- ally only to the extent that the first-period tariff and wage and price rigidities exceed those in the second period. If, on the other hand, the first-period distortions are low relative to the second period, then an abrupt financial deregulation is more appropriate.

3.4. Relaxation of capital account restrictions

The liberalization of the capital account consists of raising the firms' discount factor, /5 L, or lowering the loan rate. The effect of this liberalization on welfare is seen by:

du G - > 0

dt~ L A

where G = 6o[(1 /~ L) - ( 1 / 6 " ) ] I ' > 0. Assuming that only the exportable is used in investment, the lower loan rate

unambiguously increases welfare since firms can now borrow more to finance investment. There are no indirect effects on welfare because the loan rate is relevant only for firms for the purposes of investment. Therefore, when only the exportable is used in investment, there are no interactions with distortions in other markets. 12

It is important to note that the positive welfare effect of capital account liberalization follows directly from the fact that foreign borrowing can only be done by firms for the purposes of investment. ~3 If consumption decisions were also dependent on 8 L (not 6 o) the reduction of the tax on foreign borrowing would have mixed indirect effects since it would alter the intertemporal allocation of consumption, not just production. The intuition behind this is that consumers

12 Welfare still improves when the importable is used in investment rather than the exportable. 13 It is also important to point out that there is no capital flight in this model, nor is there any risk in

borrowing abroad.

288 A.M. Battle~Journal of Development Economics 52 (1997) 279-294

will borrow to increase expenditures in the present. This results in larger expendi- tures on the importable and nontradeable, and greater employment in period one, all of which improve welfare. However, since consumption is reduced in period two, the second-period effects will be negative. In this case the welfare effect of a relaxation of capital controls will be ambiguous and will depend on the relative size of the effects in each period.

4. Conclusion

The benefit of using a two-period general equilibrium model is the ability to capture the intertemporal effects of liberalization policies. The inclusion of distortions in other markets besides just the importable and foreign borrowing provides additional intertemporal effects which are key in determining the effect of liberalization policies on welfare.

From the previous exercises, some general conclusions emerge with regard to the sequencing of liberalization reforms. First, because of the way the model is set up, capital account liberalization is independent of distortions in other markets. Therefore, the argument put forth by some authors that trade liberalization should precede capital account liberalization is not supported using this framework. However, this framework does support some other very important observations regarding the order of liberalization reform.

The most important result is the relationship between domestic financial deregulation and trade liberalization. Since both of these reforms will only improve welfare if the other liberalization has already taken place, the appropriate policy would be a simultaneous gradual liberalization of both the domestic financial system and trade. Of course, the presence of wage and price rigidities strengthens the argument for gradualism on both fronts and points out the possibility that liberalization in the second period may still be suboptimal if the distortions remain large.

Appendix A. Derivation of welfare effects

The equations of the model include:

N i = Ei,rr ~ = El2

N i = R i 2 ( 1 , ~ i , L i , K )

W i = R ~ ( 1 , F T i , L i , K )

(A.I)

(A.2)

(A.3)

Using the information regarding the financial system and income in the two

A.M. Battle/Journal of Development Economics 52 (1997) 279-294 289

periods, we can write the intertemporal version of the income-expenditure iden- tity:

E[Tr ' (p l ,q~) ,60~2(p2,q2) ,L ' ,L2 ,u ]

= ( 6 D / 6 * ) ( R ' - I + t ' E , , ) + 6D(R 2 + tZEzl)

--((6o/6" ) - -1) ( (1 + t ' )El, + qlE12 ). (a.4)

Total differentiation of (A.4), with some substitution from (A.1) and (A.3), yields:

Eu{I -[- [( 6D/6" )(1 - - ( t l / (1 -~-tl))- 1)]MPC~

+ (( 60 /6* ) - 1)MPC 1,

_ 6 o ( t 2 / ( 1 + t2))MPCZ_(6D/6*)[MPCl(q, _ ~ l ) / q , ]

_ 6 o [ M P C 2 ( q 2 772)/q2]}du

= [ ( ( 6 0 / 6 " ) w ~ - e~) + ( 6 0 / 6 " ) ~ e 1 , , 3 + 6 j ~ e ~ . 3

- ( ( 6 0 / 6 " ) - 1)((1 + P)EI1.3 +¢E,: .3)]dL'

~- [(60 W2 -- E4) + ( 6D/6*) t 'E , , .4 + 6Dt2E21,4

--((6D/6" ) -- 1)((1 + t ')E,, .4 + q'E,2.4)]dL 2

+ ( 6 o / 6 " ) ( q ' - 01 )aN' + 60(q 2 - 772)dN 2

+ [ ( 6 ~ , / 6 * ) t ' e , , . l ~ + 6.t~e~,.~, - ( 6 0 / 6 * - 1)((1 + t ' ) e , , . , ,

+qlEl:. l l)]dtl

+ [6t)t2E2,.21 + (6D/6*)tIE,,.21 -- (60 /6" -- 1)((1 + t ')E,,.2 ,

+qlE12.21)]dt2

+ [ ( 6 0 / 6 * ) t ' e , , . , : + 6 o r : e : , . , : - ( 6 0 / 6 * - l ) ( (1 + t ' )e , , . ._

+qlEl2,12)]dql + [( 6 o / 6 " ) 6DtlE,,.22 + (6o) 2 t2E2,.22 - ( 60 /6* - 1)((1 + t ') E, 1.2~ -

+ ql E,:z.22 )]dq 2

+ ~ - ~ [ ( 6 0 / 6 *)t 'e l l .~ + 6.t~E~,.~ - ( 6 D / 6 " - 1)((1 + t ' )e , , .2

+ qlE12,2)] d 6D

+6 D[(1/6L) - (1 /6")1 l'd6L (A.5)

290 A.M. Battle~Journal of Development Economics 52 (1997) 279-294

where

gl l , l 1 = E l l ' 7T~, EI, , I 2 = E l l . "B "l, Ell,2 ' = E l l " 77 -2

and so on, for notational simplicity. This equation shows the income equivalent of welfare changes of the first order

around an initial equilibrium. This formulation compares with a similar form used by Rodrik to show the presence of the Keynesian disequilibria. The coefficients on employment and output of the nontraded good involve the corresponding wedge between the (fixed) demand and supply prices. An increase in employment will unambiguously increase welfare in both periods, while an increase in the nontrade- able will also do so under plausible conditions. The remaining variables on the right-hand side of (A.5) show the effects of varying each of the policy variables: t l, t a, ql, q2, 6D ' and 6 L.

Using (A. 1) through (A.4), the model is solved for the endogenous responses of output and employment to the policy parameters. These equations are then substituted in (A.5) to get the reduced form equation which expresses welfare as a function solely of the policy variables. The resulting equation is of the form:

A d u = B d t 1 + C d t 2 + D d q 1 + E d q 2 + F d 6 D + G d 6 r + H d w I + I d w 2

where,

a = Eu{1 + [( 6 o / 6 " ) ( 1 - ( t l / ( 1 + t l ) ) - 1)]MPC 1

+ (( 8 0 / 8 *) -- 1)MPC' n

_6D ( t 2 / ( 1 + t 2))MPC2m _ ( ~ o / 6 , ) [ M P C l ( q l _ ~ , ) / q l ]

- - 6 D [ M P C Z , ( q 2 - - ~ 2 ) / q 2 ] }

+ O l ( O, E12.u -- a~O2E22, , ) + 0 2 ( 0 2 E 2 2 , , - a20~E,2 .u )

B = ( 6 D / 6 * ) t'Ell,ll -- ( 6 D / 8 * -- 1)((1 + t l ) E l , , , , + qlE12, , , )

+ 6Dt2E21,1j

+ ( 8 o / 8 " ) ( q ' - ql)E12,11 --I- 6 o ( q 2 - ~2)Ezz , , ,

-I- [ ( ( ~D//6 * )W 1 -- E3) -{- ( ~D//6 * ) t lEll ,3 q- 6ot2E2,.3

- ( ( 8 0 / 8 * ) - 1)((1 + tl) E11,3 + ¢E1:,3) + ( 6 0 / 6 " ) ( q I - 7/1)E,2,3

+ 60(q2 - ~2)Ezz,s ]

-I-[( ~O W2 --E4) -I- ( ~ D / 6 * ) t lE l l , 4 -t- 6Dt2E21.4

A.M. Battle/Journal of Development Economics 52 (1997) 279-294

- - ( ( 6 0 1 6 * ) -- 1)((1 + t l )E , l . 4 + q'E,z.4) + ( 30 /6* ) ( q ' - ( / ' ) E,2.4

q- 8o(q2--~]2)E22,4]

[ 6 2 ( ~ 2 o , e , 2 1 , - o~e22,1,)1 C = ( 6 0 / 6 * ) t l E I 1 . 2 , -- ( 6 0 / 6 " -- 1)((1 + t l )E , , . e l + q'Elz.21)

+ 8t)t2E21.zl

+ ( 8 0 / 8 * ) ( q ' - Y/') E,2.21 + 8 0 ( q 2 - ~2) E22.2 ,

+ [(( 8 0 / 8 * ) w I - e3) + ( 8 o / 8 " ) t i e 1 , 3 + 80t2e2, 3

- ( ( 8 D / 8 * ) -- 1)((1 + tl)E11,3 -k- qlE,2.3 ) + ( 8 0 / 8 * ) ( q I -- q l )E,2 .3

+ 8 0 ( q 2 - ~2)E2~d

[ 61( - o , E1221 + ~1 o3 E22,2,)]

if" [( 8D W2 -- E4) -]- ( 8D// 6 . ) tl g, l,4 "1- 60t2 E21,4

-(( 8 0 / 6 *) - 1)((1 + t ' ) El1.4 -k- qlE12.4 ) -1- ( 8 0 / 6 * ) ( q I -- ql)E,2.4

+ 6D(q 2 - q2)E22.4 ] [ a ~ ( -2o1 e122, - o3 e~2,2,)]

O = ( 6 0 / 8 * ) t ' E l , . 1 2 + 8Dt2E2,.,2 + ( 6 0 / 8 * ) ( q ' -- ~l)E12.,2

+ 8,9(q2 _ c~:) E22,12

+ [(( 6 0 / 6 * ) w' - e3) + ( 6 0 / 6 * )t~el,,3 + 8ot2e:,,3

- ( ( 6 1 ) / 8 " ) - 1 ) ( ( 1 + t ' ) f , , . 3 + q ' f , ~ . 3 ) + ( 8 , , / 6 * ) ( q ' _ 01) E1~.3

+ 80(q2 - ~2)E22.3]

[61( ~, o~ e22,12 - o , e12,,2)]

-]- [( 80 W2 -- E4) -]- ( 80 /6 *)t 'El 1.4 -[" 80t2E21.4

- ( ( 80 /6* ) - 1)((1 + t ' )E,, .4 + qlE12,4 ) + ( 6 0 / 6 " ) ( q ' - ~/1)E12.4 + 80( qz - YlZ)E22.4]

[ a 2 ( ,~o1E1~,1~ - o2 E22,,~)]

E = (SD/8*) t16DE11.22 + (SD)2t2E21.2z + ( 8 D / 6 * ) ( q l _ ~1)E,2,2 z

+ 8o(q 2 - ~2)E2~,2 ~

q- [(( 6D/6* ) W1 -- E3) q- ( 80 /8* )/1Ell,3 q- 8Dt2621,3

291

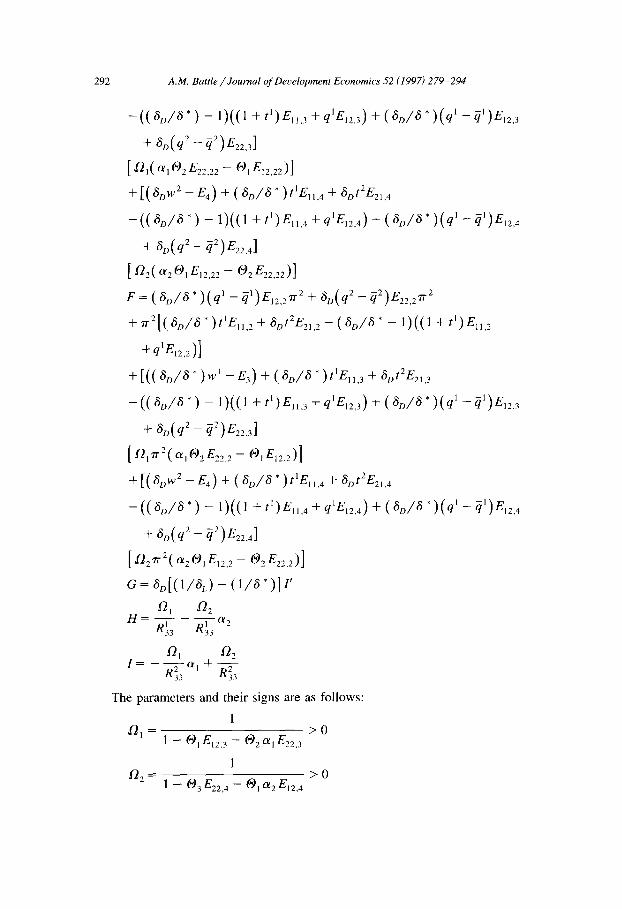

292 A.M. Battle/Journal of Development Economics 52 (1997) 279-294

- - ( ( 6 D / 6 * ) -- 1)((1 + t ' )E , 1.3 + q'E,2.3 ) + ( 6 D / 6 * ) ( q' -~ ' )E ,2 .3

[ a l ( O~10 2 E22,22 -- O 1 E12,22)]

-t- [(6D W2 -- E4) -~ ( 6D/6" ) tlEll,4 + 6Dg2E21,4

- ( ( 6 0 / 6 *) - 1)((1 + P )E l l . 4 + q 'e l~,4) + ( 6 0 / 6 " ) ( q ' - ~ ' )e ,2 ,4

-1- 6D(q2--Q2)E22.4]

[ g2z ( a2 O1 E,2,22 - 02 E22,22 )]

F = ( 6D/6 * ) (q ' - ~')E,e.27r 2 + 6D(q 2 -- 02)E22.27r 2

+ 7r2[ (6D/6*) t 'E , , , 2 + 60t2E21,2 -- ( 6 D / 6 " -- 1)((1 + t l )Ell ,2

+q'E12,2)]

+ [(( 6 0 / 6 * ) W 1 --E3) -k- ( 6 0 / 6 * ) tiE1, ,3 -[- 6Dt2E21,3

-((60/6*) - 1)((1 + tl)f~11,3 + q~E~2,3) + ( 6 o / 6 " ) ( q ~ - ~)E~2.3

+ 60 (q2 _ c-/2)E22,3]

+ [(6D w2 -- E4) + ( 6 D / 6 *)tlEll ,4 -I- 6Dt2E21A

- ( ( 6 D / 6 " ) -- 1)((1 + tl)E1,,4 + q1E,2,4 ) + ( 6 D / 6 " ) ( q l @1)E12,4 --2 + 6D(qe - -q )E22,4]

[ a2, 2( 20,e,2,2- O2E2 ..2 ] G = 6D[ ( l / 6 L ) -- ( 1 / 6 " ) ] I'

~21 ~22 H -

R~33 R~30~2

~'Q1 ~Q2 I R~ 3 c~j + R--Y-33

The parameters and their signs are as follows:

l O~ = > 0

1 - (91 E12,3 - O 2 a 1 E22,3

l

1 -- O3E22,4- Ol 0/2El2,4

A.M. Battle/Journal of Development Economics 52 (1997) 279-294 293

~)1 1 1 I = R s 2 / R 3 3 R 2 2 < 0

0 2 2 2 1 = R32/R33R22 < 0

0 3 = R~2/R~3R~2 < 0

1

O'l = 0)1EI2 '4 (1 - {~3E22,4) > 0

1

OL2 = ~ 2 E 2 2 ' 3 (1 - 0)1E12.3 ) < 0

Term A has been simplified by defining the marginal propensities to spend lifetime income on the two goods in each period. Edwards and van Wijnbergen and K~ihkonen both use this method in writing their results. The marginal propensities to consume out of lifetime income in the first period are defined as:

MPC~ = (1 + t l ) ( d ( d ~ ) / d y ) , M P C ' . = q ' ( d ( d ' . ) / d y )

where dlm['rrl,aorrZ,y] and i 1 2 dn[1r ,6,~,y] are the Marshallian (uncompensated) demand functions. If we let V[rr l, 6Drr 2, y] be the indirect utility function obtained by substituting the Marshallian demand functions into the utility function, then the following identities will hold:

E,,[vr ' .6Drr2.V] = dIm[Trl,6Dvr2.y] (a)

E,2[rr' ,6Drr2.V] =dl~[rrl,607r2,y] (b)

= y (c)

Differentiating (a) through (c) with respect to y yields:

d ( d ' , . ) / d y = U,,. . • V,,, d ( d l . ) / d y = U,2.. " V,, and e u • V,, = 1

Since V~ - 1 /E . , the marginal propensities can be rewritten:

MPCI, , = (1 + t ' ) E ~ I . . / E . and MPCI. = q 'E ,2 . . /U .

In term A. the substitutions consist of:

E,I. . = (MPCIm/(1 + t ' ) ) . E , and El2.. = (MPCln/q I ) . E u

The marginal propensities to spend lifetime income in period two are derived in the same manner as above.

Discounted lifetime income,

y = y l + 8Dy2 = ( S D / 8 *) (~1 - - I + t lE l l ) q- 8D(R 2 -}-t2E21)

- ( 8 0 / 8 * - 1)((1 + , l ) e l , + q'e,2 ),

was obtained by defining income in each period, yl and y2. Income in period one

294 A.M. Battle~Journal of Development Economics 52 (1997) 279-294

simply consists of revenue from production plus revenue from the tariff imposed in that period:

yl = ~1 + tiE11

First-period saving can therefore be written:

s = y l I 1 I I R 1 - p c m - q c n = + t l E l l - p i E 1 1 -q lE12

where cj = consumption of good j in period i, with i = 1,2, j = m,n. Income in the second period consists of revenue from production and the

second period tariff, plus the proceeds the government collects from taxation of banks ' profits and restrictions on international capital movements.

y2 = ~2 _ I / ~ L + t2E2, + (l/cSL_ 1 / 6 o ) s + (1/6 L- 1/~3")(I- s)

= ~ 2 + t2e21 - I / ~ * - ( 1 / ~ D - 1/~*)s Combining income from period one with the discounted income from period

two, with some simplification, yields:

y = y l + 6by2 = ( 60//~ * ) ( ~ 1 - - I + tiE11) + ~D(R 2 + t2E21)

-(6o/6" - 1 ) ( ( 1 + tl)E~l + qlE12 )

References

Dixit, A.K. and V. Norman, 1980, Theory of international trade, Ch. 2: Supply and demand using duality (Cambridge University Press, Cambridge, UK).

Edwards, S., 1989, On the sequencing of structural reforms, Working paper no. 3138 (NBER, Cambridge, MA).

Edwards, S. and S. van Wijnbergen, 1986, The welfare effects of trade and capital market liberaliza- tion, International Economic Review 27(1), 141-148.

Frenkel, J.A., 1982, The order of economic liberalization: Lessons from Chile and Argentina, a comment, in: K. Brunner and A.H. Meltzer, eds., Economic policy in a world of change (Carnegie-Rochester Conference Series on Public Policy, vol. 17).

K~ihkiSnen, J., 1987, Liberalization policies and welfare in a financially repressed economy, IMF Staff Papers, 34(3), 531-547.

Krueger, A.O., 1986, Problems of liberalization, in: A.M. Choksi and D. Papageorgiou, eds., Economic liberalization in developing countries (Basil Blackwell, Oxford).

McKinnon, R.I., 1982, The order of economic liberalization: Lessons from Chile and Argentina, in: K. Brunner and A.H. Meltzer, eds., Economic policy in a world of change (Carnegie-Rochester Conference Series on Public Policy, vol. 17).

Neary, J.P. and K.W.S. Roberts, 1980, The theory of household behavior under rationing, European Economic Review 13, 25-42.

Rodrik, D., 1987, Trade and capital-account liberalization in a Keynesian economy, Journal of International Economics 23, 113-129.

Related Documents