Welcome! Four Federal Ways to Enter the Wine Business Or We Have the Grapes- Now What ?

Welcome! Four Federal Ways to Enter the Wine Business Or We Have the Grapes- Now What ?

Dec 17, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Welcome!

Four Federal Ways to Enter the Wine BusinessOr

We Have the Grapes- Now What ?

Speaker

Martha J. Tebbenkamp, TTB Investigator

503 946 8346

Morning Agenda

4 Ways In

Advantages

Disadvantages

Key Concepts Production-turning materials into wine

Bond-legal agreement protecting excise tax liability.

Bonded Premises-winery/wine cellar covered by a bond.

Key Concepts

In Bond-untaxpaid wine at a BW/BWC

Transfer in bond-moving wine from one bonded facility to another

Removal from bond-identifying wine and creating a removal record

Taxpaid-wine removed from bond

Key Concepts

Wine is always either taxpaid or in bond.

Whoever removes the wine from bond pays the taxes

Whoever bottles the wine gets the COLA-always before bottling

Four Options Bonded Winery

Bonded Wine Cellar

Alternating Proprietor

Custom Crush Client

“Stand Alone” Bonded Winery Produce/blend/bottle wine

Do so ONLY on own premises

CANNOT loan/rent/share premises, except with specifically authorized alternator

Is responsible for all wine there

Stand Alone: ADV:

Complete autonomy

Small producer tax credit

DISADV:

Complete responsibility

Larger capital outlay

Bonded Wine Cellar Receive, store, blend wine in bond MAY receive bulk, bottled, labeled or

unlabeled wine MUST pay taxes on all removals Is NOT an extension of any other winery

premises

Bonded Wine Cellar

ADV:

Less capital outlay

Simple system

DISAD:

Limited label claims

No producer credit

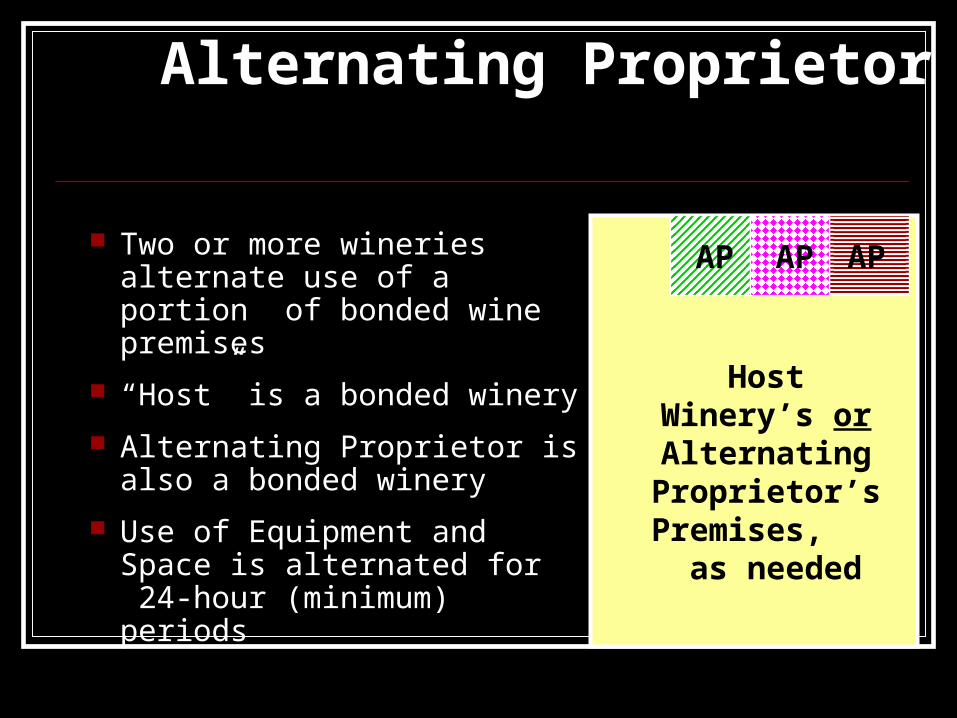

Alternating Proprietor

Two or more wineries alternate use of a portion of bonded wine premises

“Host” is a bonded winery

Alternating Proprietor is also a bonded winery

Use of Equipment and Space is alternated for 24-hour (minimum) periods

Host Winery’s or Alternating Proprietor’s Premises, as needed

AP AP AP

Alternating Proprietor-Host

Must fully qualify as a winery

Host winery proprietor files documents with TTB to curtail its bonded premises

Responsible for own production, recordkeeping, reporting, labeling and taxes,

$$$ Investment- in major winemaking equipment or winery premisesAP

AP

AP

AP-Host

ADV:

Fuller use of expensive equipment

Improved cash flow

DISAD:

Much more complicated record system

Must coordinate with tenant

May lose certain label claims

Alternating Proprietor-Tenant

Must fully qualify as a winery

Responsible for own production, recordkeeping, reporting, labeling and taxes, independent of host winery

Less investment in major winemaking equipment or winery premises

AP

AP

AP

Alternating Prop-Tenant

ADV:

Less capital outlay

Quick entry to the wine business

DISAD:

Much more complicated records

Must coordinate with host

May lose certain label claims

Other Factors for Alternators Economies of scale-bulk glass, etc Crush pad chaos

No “Divorce Court” No “virtual wineries”

Custom Crush Operations

Client contracts with a Bonded Winery to have wine produced

Winery produces the wine to client’s specifications

Client receives finished, taxpaid wine

Bonded Winery

WLD

Taxpaid Wine

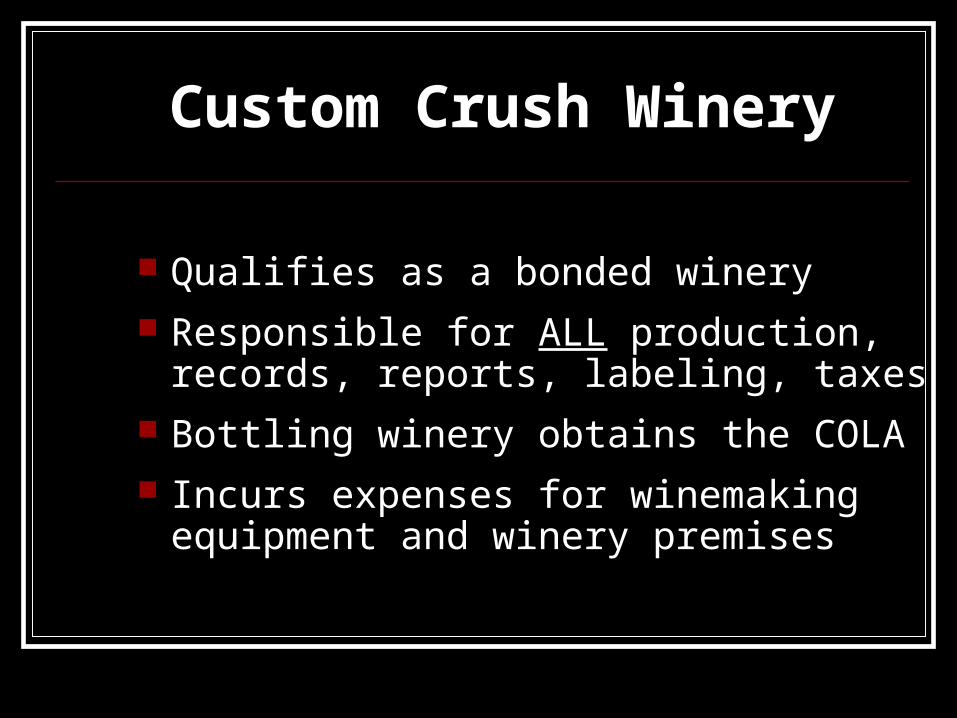

Custom Crush Winery

Qualifies as a bonded winery Responsible for ALL production, records,

reports, labeling, taxes Bottling winery obtains the COLA Incurs expenses for winemaking

equipment and winery premises

Custom Crush Winery

ADV:

Cash flow from extra capacity

DISAD:

Must count all production as theirs

Full recordkeeping, reporting responsibility

Must deal with client

Custom Crush Client

Qualifies with TTB as a Wholesaler

Minimal recordkeeping requirements as a Wholesaler; no report to file

No responsibility for production, recordkeeping, reporting, labeling or tax

No investment in winemaking equipment or premises

Custom Crush Client

ADV

Quickest, cheapest way in to the industry

DISAD

Limited label claims

May be “lowest priority” for crusher

Must deal with crusher

Other Factors for Crusher/Client Client may receive wine in bond as “starter

inventory” after issuance Client has to allow name to be used Some states restrict ownership of brands BOTTLER MUST GET COLA REMOVER MUST PAY TAXES

RECAP In Bond Tax Paid Bonded Premises 4 Options:

1) Stand Alone BW

2) BWC

3) Alternator

4) Custom Crush

THANK YOU!

QUESTIONS?

Related Documents