November 18, 2011 Weekly REIT Insights NAREIT Convention Roundup This week we focus on the top themes at NAREIT. Chasing growth through portfolio reinvention. It was hard not to be struck during our 46 NAREIT Convention meetings by the prevalence of strategic initiatives to upgrade asset portfolios, recycling capital from weak to strong markets, submarkets, asset niches, and even countries. We view the trends as a reflection of (1) a fundamental realization that growth is likely to remain biased towards highly-educated industries and the locations where they are concentrated (e.g., tech in San Francisco, biotech in Boston, etc.) and (2) the fact that core internal growth outweighs the potential impact of external investment as REITs mature – meaning it is not worth sacrificing long-term rent growth for short-term FFO-accretive deals in scattered markets. Another way that scale matters – marketing. Outside the mall, industrial, and possibly healthcare REIT sectors, we have long been skeptical of the merits of scale in commercial real estate. There are too many examples of underperforming, overextended operators set against outperforming, focused players to convince us that scale beyond a minimum threshold (~$1B equity cap) adds enough value to be an end unto itself. Recently, however, the apartment & self-storage REITs have demonstrated that scale offers the ability to absorb technology investments in operations & marketing that lend sustainable competitive advantages in customer acquisition and retention, as well as pricing. Apart from PSA, we are not convinced these merits are reflected in current valuations. DC concerns mount. While concerns about BRAC realignment, potential federal cuts, challenging Y/Y comps, and 2012-13 supply growth have become well-known for Washington, DC, we were nevertheless struck by the caution now being expressed by the largest REIT players in the market, as opposed to stemming from those throwing stones from afar. Recent Reports Title Date American Assets Trust: Index Addition a Positive, Reiterate OW Nov 16, 2011 Paul Morgan / Chris Caton Weekly REIT Insights: NAREIT Convention Preview: A Lone Star Hoedown Nov 11, 2011 REIT Valuation Analyst: Yield spreads still attractive Nov 11, 2011 Hudson Pacific Properties: Delivering Its Growth Strategy Nov 9, 2011 Paul Morgan / Chris Caton American Assets Trust: Operating Stats Belie ’12 Growth Opportunity Nov 8, 2011 Paul Morgan / Chris Caton Health Care Reit Incorporated: Guidance raise following acquisitions Nov 4, 2011 Paul Morgan / Jorel Guilloty Weekly REIT Insights: Helpful highlights to navigate the earnings deluge Nov 4, 2011 Paul Morgan / Chris Caton / Swaroop Yalla, PhD / Jorel Guilloty / Stephen Bakke REITs: Mall Sales Monitor: Below expectations for October Nov 3, 2011 Paul Morgan / Stephen Bakke Equity One Inc.: Entering the late innings of portfolio transformation Nov 3, 2011 Paul Morgan / Stephen Bakke Kimco Realty Corp.: International drives ss-NOI; offers new 2012 guidance Nov 2, 2011 Paul Morgan / Stephen Bakke Essex Property Trust: Guidance raised for 2011, ss-NOI accelerates 200bps Nov 2, 2011 Paul Morgan / Swaroop Yalla, PhD HCP, Inc.: Core Upside in Q3, With All Quiet on the Transaction Front Nov 2, 2011 Paul Morgan / Jorel Guilloty BRE Properties, Inc.: Steady acceleration across BRE markets Nov 2, 2011 Paul Morgan / Swaroop Yalla, PhD Kilroy Realty Corp.: Strong Execution Amid Improving Markets Nov 2, 2011 Paul Morgan / Chris Caton Morgan Stanley does and seeks to do business with companies covered in Morgan Stanley Research. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of Morgan Stanley Research. Investors should consider Morgan Stanley Research as only a single factor in making their investment decision. For analyst certification and other important disclosures, refer to the Disclosure Section, located at the end of this report. Morgan Stanley & Co. LLC Paul Morgan [email protected] +1 415 576 2627 Chris Caton [email protected] +1 415 576 2637 Swaroop Yalla, PhD [email protected] +1 415 576 2361 Jorel Guilloty [email protected] +1 415 576 2631 MORGAN STANLEY RESEARCH NORTH AMERICA Industry View Attractive

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

November 18, 2011

Weekly REIT Insights NAREIT Convention Roundup

This week we focus on the top themes at NAREIT.

Chasing growth through portfolio reinvention. It was hard not to be struck during our 46 NAREIT Convention meetings by the prevalence of strategic initiatives to upgrade asset portfolios, recycling capital from weak to strong markets, submarkets, asset niches, and even countries. We view the trends as a reflection of (1) a fundamental realization that growth is likely to remain biased towards highly-educated industries and the locations where they are concentrated (e.g., tech in San Francisco, biotech in Boston, etc.) and (2) the fact that core internal growth outweighs the potential impact of external investment as REITs mature – meaning it is not worth sacrificing long-term rent growth for short-term FFO-accretive deals in scattered markets.

Another way that scale matters – marketing. Outside the mall, industrial, and possibly healthcare REIT sectors, we have long been skeptical of the merits of scale in commercial real estate. There are too many examples of underperforming, overextended operators set against outperforming, focused players to convince us that scale beyond a minimum threshold (~$1B equity cap) adds enough value to be an end unto itself. Recently, however, the apartment & self-storage REITs have demonstrated that scale offers the ability to absorb technology investments in operations & marketing that lend sustainable competitive advantages in customer acquisition and retention, as well as pricing. Apart from PSA, we are not convinced these merits are reflected in current valuations.

DC concerns mount. While concerns about BRAC realignment, potential federal cuts, challenging Y/Y comps, and 2012-13 supply growth have become well-known for Washington, DC, we were nevertheless struck by the caution now being expressed by the largest REIT players in the market, as opposed to stemming from those throwing stones from afar.

Recent Reports

Title Date

American Assets Trust: Index Addition a Positive, Reiterate OW

Nov 16, 2011

Paul Morgan / Chris Caton Weekly REIT Insights: NAREIT Convention Preview: A Lone Star Hoedown

Nov 11, 2011

REIT Valuation Analyst: Yield spreads still attractive

Nov 11, 2011

Hudson Pacific Properties: Delivering Its Growth Strategy

Nov 9, 2011

Paul Morgan / Chris Caton American Assets Trust: Operating Stats Belie ’12 Growth Opportunity

Nov 8, 2011

Paul Morgan / Chris Caton Health Care Reit Incorporated: Guidance raise following acquisitions

Nov 4, 2011

Paul Morgan / Jorel Guilloty Weekly REIT Insights: Helpful highlights to navigate the earnings deluge

Nov 4, 2011

Paul Morgan / Chris Caton / Swaroop Yalla, PhD / Jorel Guilloty / Stephen Bakke

REITs: Mall Sales Monitor: Below expectations for October

Nov 3, 2011

Paul Morgan / Stephen Bakke Equity One Inc.: Entering the late innings of portfolio transformation

Nov 3, 2011

Paul Morgan / Stephen Bakke Kimco Realty Corp.: International drives ss-NOI; offers new 2012 guidance

Nov 2, 2011

Paul Morgan / Stephen Bakke Essex Property Trust: Guidance raised for 2011, ss-NOI accelerates 200bps

Nov 2, 2011

Paul Morgan / Swaroop Yalla, PhD HCP, Inc.: Core Upside in Q3, With All Quiet on the Transaction Front

Nov 2, 2011

Paul Morgan / Jorel Guilloty BRE Properties, Inc.: Steady acceleration across BRE markets

Nov 2, 2011

Paul Morgan / Swaroop Yalla, PhD Kilroy Realty Corp.: Strong Execution Amid Improving Markets

Nov 2, 2011

Paul Morgan / Chris Caton

Morgan Stanley does and seeks to do business with companies covered in Morgan Stanley Research. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of Morgan Stanley Research. Investors should consider Morgan Stanley Research as only a single factor in making their investment decision. For analyst certification and other important disclosures, refer to the Disclosure Section, located at the end of this report.

Morgan Stanley & Co. LLC Paul Morgan

[email protected] +1 415 576 2627

Chris Caton [email protected] +1 415 576 2637

Swaroop Yalla, PhD [email protected] +1 415 576 2361

Jorel Guilloty [email protected] +1 415 576 2631

M O R G A N S T A N L E Y R E S E A R C H N O R T H A M E R I C A

Industry View Attractive

2

M O R G A N S T A N L E Y R E S E A R C H

November 18, 2011 Weekly REIT Insights

Retail REIT Roundup How will the holiday season matter? With Black Friday fast approaching and retailers reporting Q3 results, the topic of tenant health and the outlook for the holiday shopping season was the lead in our meetings with regional mall REITs. Strong year-to-date sales growth has boosted the prospects for rent growth in 2012, as occupancy costs have returned to levels that offer landlords greater pricing power. While the bulk of the tenant base appears to have a gradually improving mindset, exceptions exist in the form of chains that survived the Great Recession intact, but without their prior vibrancy – as reflected, for example, by stock prices in the $3-and-under range for PacSun, Talbot’s, New York & Co, Coldwater Creek, Christopher & Banks and BonTon. These concepts operate over 3,300 stores and are among the chains whose ongoing or potential store closings could partly offset the upside to ss-NOI growth in 2012-13, especially if the broader holiday season disappoints. Nevertheless, managing these combinations of vibrant, growth-oriented tenants and their more challenged peers is part of playbook for mall operators and we expect the shifts to translate into greater market share for REIT-owned assets and among these, the most productive, trade-area dominant malls.

Can small shops recover in 2012? The lack of a recovery in small shop leasing has plagued strip center REITs this year, despite a strong rebound in demand from public retailers with stronger balance sheets and better access to growth capital. Signs of modest improvements exist, for example, in the form of Regency’s strong leasing velocity and a sharp decline in “midnight moveouts” by mom’n’pop shops. Several factors contribute to the ongoing weakness – one new candidate being delayed permitting approvals by under-staffed municipalities – though in our view the biggest challenge remains simply an oversupply of newly-built small-shop retail in housing bust submarkets across the country. These lessons should translate into more conservative development projects for the next cycle, with less reliance on building excess non-anchor space in order to pad development yields to offset the impact of falling cap rates.

LatAm and Asia still enticing the bigger players. Taubman continues to expect an announcement of project plans for China by 1H12 as originally outlined, while management highlighted the potential for TCO to exploit opportunities stemming from liquidity challenges facing local residential

developers (who also build much of the new retail space in China). We are constructive on the Taubman Asia potential, however, given past failures, we do not expect the upside potential to be built into TCO’s valuation until investors have had an opportunity to assess the details behind future project announcements. Meanwhile, LatAm continues to entice both companies with existing ventures in the market (incl. DDR, KIM & GGP), as well as potential new entrants (e.g., SPG). Kimco is also enthusiastic about potential growth in less crowded investment markets Peru & Chile.

Outlet competition harkens back to the old days. With both public and private developers in pursuit of avenues to kickstart their value-creation platforms, the outlet center has burst into activity and reminds us of the pre-1990s regional mall industry and the 2003-08 lifestyle center wave. Both generations of development led to a mix of highly successful projects, failures, and many projects that never achieved liftoff at all. Simon and Tanger are appropriately highlighting that a marketing pamphlet doesn’t mean a project will happen, so it is premature to talk of oversupply, and both competitors are certain to make efforts to defend their profitable territory, with one battleground appearing in St. Louis where TCO & SPG have announced competing projects a few miles apart.

AAT MSCI REIT Index addition: This week, MSCI announced that AAT will be added to the MSCI REIT Index (RMZ) on December 1, along with four other REITs (EXL, RLJ, INN, and MNR). We analyzed the last 10 RMZ index additions during the past five years and on average, stocks saw a ~+550bp outperformance driven by index buyers. AAT outperformed the index by ~400bp on Wednesday and Thursday, leaving some potential upside from here. Also, ave. daily trading volume doubled upon index addition

Exhibit 1 AAT: RMZ index inclusion a near-term catalyst

DEI

DCT

DFT

GOV

PEB

CHSP

PDM

HPPCORCCG

Avg (xGOV)

-20

-15

-10

-5

0

5

10

15

-15 -10 -5 0 5 10 15 20 25 30 35 40 45

Performance Relative to RMZ, %, Indexed to MSCI REIT Index Set vs. Date of Announcement of Addition to the MSCI REIT Index (RMZ)

Source: FactSet, MSCI, Morgan Stanley Research

NAREIT Roundup

3

M O R G A N S T A N L E Y R E S E A R C H

November 18, 2011 Weekly REIT Insights

Apartment REIT Roundup Demand intact but 2012 more dependent on job growth. Our management meetings with various apartment REITs (CPT, HME, MAA, AIV) confirmed our thesis of a bifurcation in certain submarkets/price points. AIMCO management, for example, acknowledged seeing higher pressure at its lower price point assets and plans continued dispositions to improve the portfolio exposure to more robust markets. Meanwhile, operators with assets in higher-growth markets continue to show momentum: Camden reported sending renewal notices in the 7-8% in Oct/Nov and ss-revenue growth for Q4 is trending towards low to mid 6s, in line with guidance. Camden and MAA also reported seeing their rent to income ratio drop sequentially, as residents leaving due to rent increases are replaced by higher-income tenants. An eye on same-store expenses in 2012. Management teams voiced some concerns for 2012 after two years of little to no expense growth, helped by tax appeals and various technology initiatives that conserved marketing spend. Camden is anticipating 3-4% increases in taxes, while AIV also anticipates similar rates of increase. MAA, with its exposure to Florida and Texas markets, has seen earlier tax adjustments than peers (which may set them up for better comps next year). Expense guidance in February (post-budgeting and tax appeal discussions) should provide better color on the sustainability of peak NOI growth into 2012 and beyond. Development risks not as high as last cycle. With macro factors posing some risk to core revenue growth, apartment REITs are dialing up development pipelines. With little competition from merchant builders, the risk of development – at least at this phase of the cycle – is not as high as last cycle for well-capitalized REITs. Camden has $500M in current development and is planning $250-400M in new starts for 2012 (maintaining CIP/EV of ~10%). Land costs continue to rise in response to this demand – Camden mentioned that land costs in California have doubled in six months, which bodes well for the pipeline value for BRE and ESS. Development yields continue to pencil at a 150bps spread to comparable acquisitions – e.g., CPT is developing a 310-unit deal in the Buckhead submarket of Atlanta, where they are looking at a +6.5% yield on un-trended rents (vs. 5% cap rate for a core acquisition).

Industrial REIT Roundup Filling vacancy. Management teams remain constructive on filling vacancy into 2012 and beyond, although with some pressure from recent macroeconomic uncertainty. While market wide rent momentum is expected to be modest next year, replacing expiring rent levels are making for easier comps as 2012 renewals will include shorter-term leases signed at low 2008 and 2009 rents.

Development starts expanding. Management highlighted the dwindling availability of large spaces as a catalyst for rent growth across a range of markets (e.g., Los Angeles / Inland Empire, Houston, Lehigh Valley, New Jersey). Lack of availability is spurring new development, much of it led by REITs over private market competitors, likely due to differences in balance sheets.

Prologis (PLD-OW): Along with leasing, we look for progress on the deleveraging front at Prologis. Private capital markets remain robust and are not a limiting factor at this point: for example, we expect Prologis to form two funds in Japan in 2012, an open-ended core fund and a development fund. Development starts are likely to remain dominated by build to suits, with a healthy near-term pipeline supporting a moderate level of activity until a broader pickup in the market resumes.

EastGroup Properties (EGP-EW): We expect external growth sources to increasingly supplement growth as portfolio occupancy has reverted to the low- to mid-90s. Management seemed incrementally more positive on sourcing investments as more assets become available for sale (e.g., Prologis’ non-core dispositions in the Sunbelt). We look for the company to reach stabilized $100m of annual development starts, led initially by Houston and Orlando, although reaching this full potential will require recovery in other of their core markets.

Office REIT Roundup

Limited visibility on core growth: Increased macro uncertainty has led users to delay leasing decisions where they can, which has reduced the REITs’ leasing pipelines and added some uncertainty on filling vacancy in 2012. The upward momentum of rents in NYC has been checked, while tech-oriented submarkets (e.g., Cambridge, SoMa, Silicon Valley) continue to lead the way.

Intense competition for core assets: Acquisition markets remain strong, standing in contrast to the latest slowing in leasing activity. Competition remains intense as institutional

4

M O R G A N S T A N L E Y R E S E A R C H

November 18, 2011 Weekly REIT Insights

buyers continue to seek the safe inflation-protected yields. Activity has consolidated in the top markets (e.g., 24 hour cities), which could slow the portfolio repositioning of REITs looking to sell weaker properties in secondary cities. In contrast, those management teams willing to take leasing risk in their acquisition programs continue to believe they can find better-priced opportunities.

Highlights from covered companies:

Kilroy Realty (KRC-EW): Portfolio repositioning continues to be successful, with disposition activities on track. The recent 370 Third St acquisition (largest block of availability in San Francisco’s SoMa submarket) has a handful of prospects which should give clarity on a stabilized yield in the low- to mid-7s at the property. The recovery in San Diego has continued and has not seen a setback amidst weaker macroeconomic data – rents are rising in the best submarkets.

Piedmont Office (PDM-UW): 2012 & 2013 will be years of transitioning tenants and will likely pressure operating metrics. As a result, we expect a dividend cut to $0.80 as new tenants require capital, which will pressure AFFO. Crain’s has reported that PDM renewed Aon for 400ksf (currently a sublease tenant from BP), the largest lease deal in Chicago this year. With this lease, PDM would have successfully pre-leased the BP expiration (along with new leases to Integrys and others), although the replacement rents are as much as $7/ft NNN above market (would result in upwards of ~$5m reduced NOI in 2014+).

Highwoods Properties (HIW-EW): We came away incrementally more constructive on the new PPG Place acquisition as HIW appears to have increased their forward looking budget on better expense management and opportunities to drive better revenues through the retail. We look for the stabilized NOI yield to rise into the 9s as HIW adds occupancy over time. With regard to development, management may be working on a handful of small build-to-suits, although activity is otherwise likely to remain quite. We think HIW will be patient on finding permanent financing for 3Q acquisitions and their 4Q debt retirement; a new fixed rate financing seems likely in the near term, although new cash will introduced at a more measured pace (~$100M/yr of asset dispositions and occasional equity issuance via the ATM, in our view).

First Potomac (FPO-EW): Management has executed amidst a slower DC leasing environment. The company has over 500ksf of leases to commence by the end of 2012 (predominantly mid-2012). The First Street and 1200 17th St.

redevelopments are both likely to move forward in 2012 (although a deeper market setback could delay 1200) and could show some preleasing by mid- to late-2012.

Hudson Pacific (HPP-EW): Management is focused on creating value across a handful of their leasing opportunities. On the margin, we look for progress across all of their leasing challenges (i.e., 1455, Rincon retail, Arizona, 275 Brannan, City Plaza), although results are more likely to hit in early- to mid-2012. On the margin, HPP seemed to have a reduced focus on exposure to studio/media assets.

Gov’t Properties (GOV-EW): We look for portfolio occupancy to settle in the mid-90s over time from the current 97% level. Management is exploring term loans as well as watching the unsecured bond markets as a permanent financing solution for the current elevated line of credit balance.

Healthcare REIT Roundup The RIDEA vs. NNN lease structure debate continues. Encouraged by 4%+ ss-NOI growth potential, healthcare REITs announced over ~$6B in senior housing RIDEA transactions since HCN first announced its Merrill Gardens JV in August 2010. The structure’s direct cash flow upside (& downside) entices, but also requires the REIT to bear direct capex responsibility, unlike the more conservative triple-net structure where the exposure is indirect. For mature, stabilized assets, the balance could favor steady growth NNN deals, while for non-stabilized assets with significant lease-up or margin expansion potential, RIDEA helps transfer the upside to the REIT. HCP expressed the need for a 150bp+ return premium to compensate for RIDEA cash flow risk, while HCN appears content with a modestly lower risk premium. HCN and SNH expressed confidence that their RIDEA portfolios could achieve the pro-forma NOIs over the long term given the quality of the assets and operators, the potential occupancy growth (from mid 80s to mid 90s) and increasing margins. Exhibit 2 Healthcare REITs’ portfolio NOI composition

Ticker Hospital SNF

Senior Housing - Triple Net

Senior Housing - Operating

Medical Office

Life Sciences/

OtherHCP 6% 27% 33% 4% 14% 16%HCN 7% 31% 30% 14% 16% 2%SNH 2% 4% 49% 12% 29% 4%

Gov't Reimbursed Private-Pay Healthcare Office

Source: Company data, Morgan Stanley Research

5

M O R G A N S T A N L E Y R E S E A R C H

November 18, 2011 Weekly REIT Insights

Much ado about reimbursement. Healthcare REIT management teams almost unanimously indicated that the most asked topic during NAREIT had been government reimbursement, specifically how operators will mitigate current and future government cuts and the ultimate impact on lease coverage. Teams reiterated that their operators were well under way mitigating 1/3 to 2/3 of the 11% Medicare cuts, mostly through labor costs, which allows for rent coverage for HCN (1.3 x to 1.4x) and HCP's (1.5x) major SNF portfolios. HCN believes that Genesis could offset this impact by increasing the portfolio’s quality mix (SNF revenue stemming from Medicare + private pay sources) from the current 53% to the 60% to 65% range (with every 1% increase in quality mix equating to a 6bps increase in rent coverage). HCP reiterated its belief that deal activity within the SNF space could pick up in 1Q12 assuming some budget clarity emerges from the Supercommittee negotiations – even if the news is somewhat worse than expected. Management teams were not as worried about potential additional Medicare cuts given current overall coverage ratios and potential offsets arising from regular market basket updates.

Self-storage REIT Roundup Market rents rising, with discounting mixed. EXR and PSA reported seeing increasing market rents (approximately 4-5%); however, interestingly, EXR reported that discounting is down 9% y/y while PSA reported seeing a flat to modest increase in discounting. Given that they are both operating near their “optimal” occupancy levels given frictional turnover rates, revenue growth in 2012 will likely be driven by rental rate growth. While early signs of market rent growth are promising, the divergence across discounting strategies reduces clarity regarding true underlying pricing power. Consolidation still a theme in self-storage. SDSS data (which includes a survey of 5,000 properties including 1,500 REIT properties) showed a +10bps y/y increase for overall self-storage market occupancies, at a time when storage companies are reporting almost +150bps increase in occupancies. We believe this is driven partly by the significant economies of scale being exercised by the large public operators, particularly in an increasingly sophisticated Internet marketing landscape. As this gulf continues to widen and the top operators gain share from locals, we believe the industry pressure to consolidate will continue, potentially contributing to the acquisitions pipelines of the REITs.

6

M O R G A N S T A N L E Y R E S E A R C H

November 18, 2011 Weekly REIT Insights

Weekly News Flow

Industry

CRE Pricing Recovery Continues With September Rebound – Third-Quarter CoStar Sales data reflects less distress, firmer retail pricing and broadening strength across the spectrum of CRE properties. (CoStar, Nov 16) Global Office Rents, Values Continue To Rise In 3Q, Says CBRE Index – The CBRE Global Office Rent Index posted a YoY increase of 5.1%, and a QoQ increase of 0.9%, a sixth straight quarterly rise for the world's prime office markets. (World Property Channel, Nov 14)

Apartments Campus Apartments To Break Ground On $200M Project – On the first phase of a $200m student housing project at Shippensburg University in Philadelphia this week. (Business Journals, Nov 16) $159M Sale of Chicago Apartments Completed – Crescent Heights sold its Regents Part Apartment Complex in Chicago to an affiliate of Antheus Capital for $159 M. (Commercial Real Estate Direct, Nov 16)

Commercial Cleveland Announces $1b Waterfront Plan – The city announced a new development plan that could transform the lakefront area, with the potential for 1.5m SF of commercial projects. (GlobeSt, Nov 15) Crescent Closes Regents Park Sale For $159m – RP Holdings LLC, purchased the two towers with 1,031 units in Chicago from Crescent Heights. (GlobeSt, Nov 15) Genessee Executive Plaza Sells For $47m – DivcoWest and Stockbridge Capital Group have jointly purchased the 159,425 SF office complex in San Diego's University Town Center submarket, for $46.8m. (GlobeSt, Nov 11)

Rosslyn Office Trades For $57m – Has acquired 1400 Wilson Blvd., a 108,296 SF office building in Virginia for $57m. (GlobeSt, Nov 11)

7

M O R G A N S T A N L E Y R E S E A R C H

November 18, 2011 Weekly REIT Insights

The Week Ahead: Economic Indicator Preview

Existing Home Sales (M)

3.0

3.5

4.0

4.5

5.0

5.5

6.0

6.5

7.0

7.5

Dec

-99

Dec

-00

Dec

-01

Dec

-02

Dec

-03

Dec

-04

Dec

-05

Dec

-06

Dec

-07

Dec

-08

Dec

-09

Dec

-10

Recession Period

Source: FactSet, Morgan Stanley Research

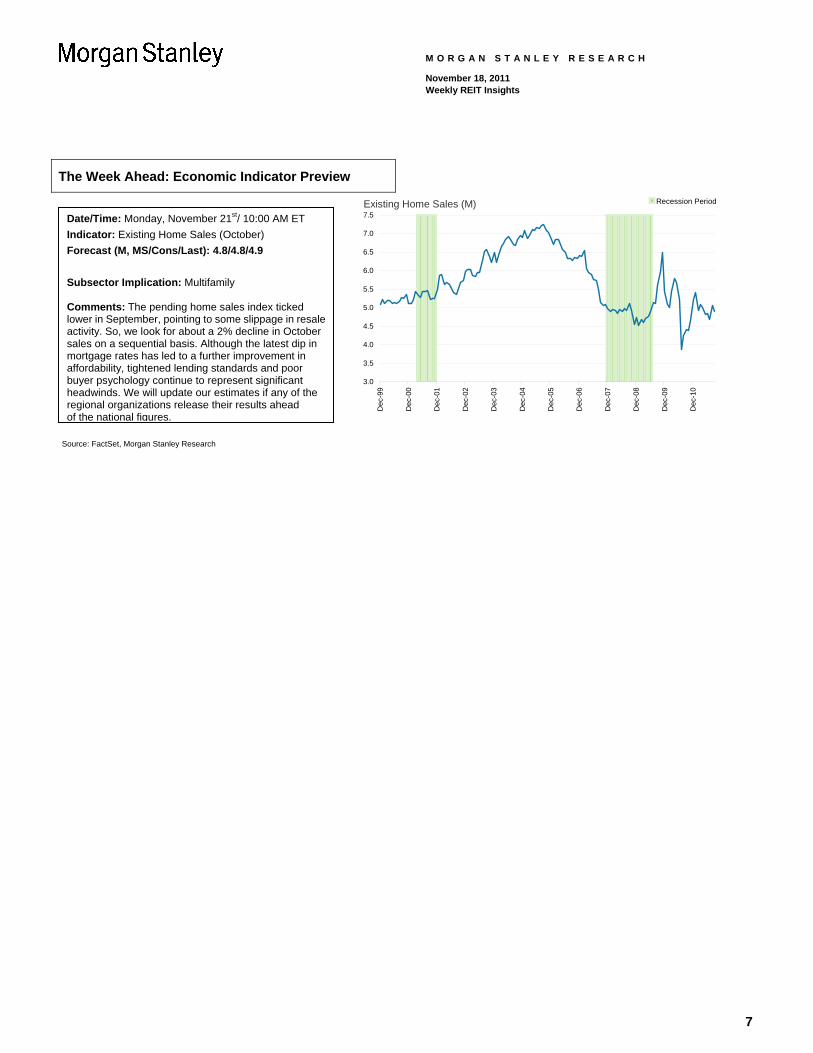

Date/Time: Monday, November 21st/ 10:00 AM ET Indicator: Existing Home Sales (October) Forecast (M, MS/Cons/Last): 4.8/4.8/4.9 Subsector Implication: Multifamily Comments: The pending home sales index ticked lower in September, pointing to some slippage in resale activity. So, we look for about a 2% decline in October sales on a sequential basis. Although the latest dip in mortgage rates has led to a further improvement in affordability, tightened lending standards and poor buyer psychology continue to represent significant headwinds. We will update our estimates if any of the regional organizations release their results ahead of the national figures.

8

M O R G A N S T A N L E Y R E S E A R C H

November 18, 2011 Weekly REIT Insights

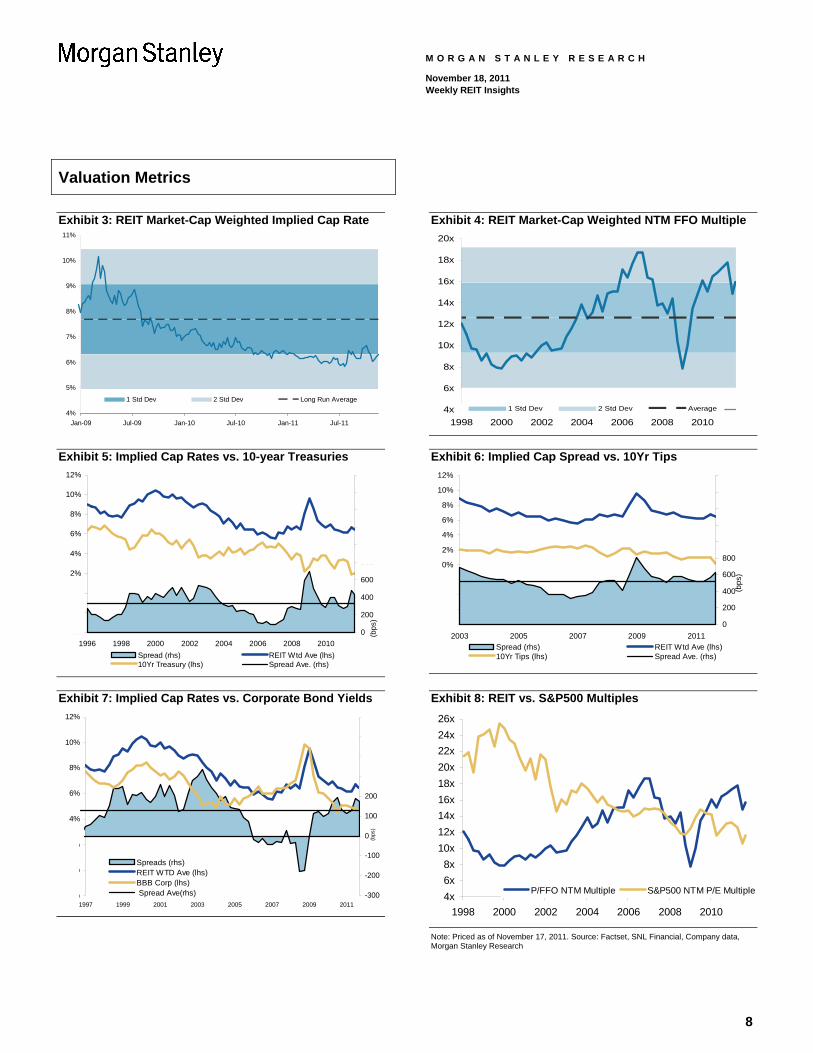

Valuation Metrics

Exhibit 3: REIT Market-Cap Weighted Implied Cap Rate

4%

5%

6%

7%

8%

9%

10%

11%

Jan-09 Jul-09 Jan-10 Jul-10 Jan-11 Jul-11

1 Std Dev 2 Std Dev Long Run Average

Exhibit 4: REIT Market-Cap Weighted NTM FFO Multiple

4x

6x

8x

10x

12x

14x

16x

18x

20x

1998 2000 2002 2004 2006 2008 20101 Std Dev 2 Std Dev Average

Exhibit 5: Implied Cap Rates vs. 10-year Treasuries

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

1996 1998 2000 2002 2004 2006 2008 20100

200

400

600

800

1000

1200

1400

1600

1800

(bps

)

Spread (rhs) REIT Wtd Ave (lhs)10Yr Treasury (lhs) Spread Ave. (rhs)

Exhibit 6: Implied Cap Spread vs. 10Yr Tips

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

2003 2005 2007 2009 20110

200

400

600

800

1000

1200

1400

1600

1800

(bps

)

Spread (rhs) REIT Wtd Ave (lhs)10Yr Tips (lhs) Spread Ave. (rhs)

Exhibit 7: Implied Cap Rates vs. Corporate Bond Yields

-2%

0%

2%

4%

6%

8%

10%

12%

1997 1999 2001 2003 2005 2007 2009 2011-300

-200

-100

0

100

200

300

400

500

600

(bps

)

Spreads (rhs)REIT WTD Ave (lhs)BBB Corp (lhs) Spread Ave(rhs)

Exhibit 8: REIT vs. S&P500 Multiples

4x6x8x

10x12x14x16x18x20x22x24x26x

1998 2000 2002 2004 2006 2008 2010

P/FFO NTM Multiple S&P500 NTM P/E Multiple

Note: Priced as of November 17, 2011. Source: Factset, SNL Financial, Company data, Morgan Stanley Research

9

M O R G A N S T A N L E Y R E S E A R C H

November 18, 2011 Weekly REIT Insights

REIT Weekly Price Performance Heat Maps Exhibit 9: Trailing 5D Relative to RMZ Heat Map (Sorted by Implied Cap Rate; Color Intensity Represents Return Quartile)

Subsectors Malls Strips Office Mixed OI Industrial Apartments Healthcare Hotels StorageStorage TCO FRT BXP MSW EGP AVB UHT PEB PSA

Apts SPG SKT MPG DLR PLD ESS HCP FCH EXRMalls MAC AKR SLG WRE TRNO ACC VTR HST SSSOffice GGP AAT DEI DFT DCT EQR NHI CHSP CUBEHcare GRT ROIC VNO PSB FR BRE HR LHOStrips CBL BFS BPO DRE UDR HCN DRH

Mixed O/I PEI EQY BMR LRY PPS LTC CLDTIndustrial KIM KRC COR EDR CSA HT

REG ARE FPO CPT SNH SHOWRI PDM MAA MPW HPTIRC OFC HME OHI AHT

1 +207< DDR BDN AIV SBRA BEE2 +25 < x <+207 KRG HIW3 -123 < x <+25 CDR GOV4 -123> RPT CLI

EXL PKYHPPCUZCWH

Rel. Performance in bpsQuar.

Exhibit 10: Trailing 5D Absolute Price Performance Heat Map Sorted by Subsector Lease Duration (Color Intensity Represents Quartile)

HO

T.ST

O.

APA

RTM

ENTS

STR

IPS

IND

MIX

OFF

ICE

MA

LLS

H.C

AR

E

VTR-2.4

HCP-0.9

HCN-1.5 M

PW

HST+1.3

HPT-4.4

LHO-2.5

DRH+1.4

PSA-0.5

SNH+0.6

ESS-2.7

EXR+2.7

OHI-0.5 H

R

MAA-2.8

OFC

EQR-5.1

AVB-2.3

SSS+1.1

CUBE+0.4

CLPACC

+3.4 PPS

CBL-3.2

HIW

NH

I

AIV-4.0

BRE-2.9

HME-2.9

DCT+0.4

EGP-1.7

FR-1.4

UDR-3.4

CPT-2.2

DFT+2.1

PSB-1.1 FP

O

MSW

PLD+0.8

DLR+2.3

LRY-1.4

DRE-2.0

WRE-0.5

KRC

CW

HBD

N

DEIARE

-1.1

AAT

AKR

IRC

VNO-3.4

BXP-1.7

BPO-3.5

SLG-3.3

PDM-1.0

CLI-2.3

BFS

BMR

KIM-2.9

FRT-0.4

REG-2.0

DDR-3.6

WRI+0.2

SKT+1.1

EQY-2.0

SHO-1.1

HT-1.4

AHT-4.1

BEE-4.0 FC

HPE

B

SPG-3.0

MAC-1.0

GGP-3.3

TCO+0.4

Note: REIT box size indicates relative equity market capitalization. Row height represents relative subsector market cap and column width with rows represents stock market cap relative to subsector. Both exhibits as of November 17, 2011. Source: FactSet, Morgan Stanley Research

10

M O R G A N S T A N L E Y R E S E A R C H

November 18, 2011 Weekly REIT Insights

REIT YTD Price Performance Heat Maps Exhibit 11: YTD Relative to RMZ Heat Map (Sorted by Implied Cap Rate; Color Intensity Represents Return Quartile)

Subsectors Malls Strips Office Mixed OI Industrial Apartments Healthcare Hotels StorageStorage TCO FRT BXP MSW EGP AVB UHT PEB PSA

Apts SPG SKT MPG DLR PLD ESS HCP FCH EXRMalls MAC AKR SLG WRE TRNO ACC VTR HST SSSOffice GGP AAT DEI DFT DCT EQR NHI CHSP CUBEHcare GRT ROIC VNO PSB FR BRE HR LHOStrips CBL BFS BPO DRE UDR HCN DRH

Mixed O/I PEI EQY BMR LRY PPS LTC CLDTIndustrial KIM KRC COR EDR CSA HT

REG ARE FPO CPT SNH SHOWRI PDM MAA MPW HPTIRC OFC HME OHI AHT

1 +428< DDR BDN AIV SBRA BEE2 -795 < x <+428 KRG HIW3 -1991 < x <-795 CDR GOV4 -1991> RPT CLI

EXL PKYHPPCUZCWH

Quar.Rel. Performance

in bps

Exhibit 12: YTD Absolute Price Performance Heat Map Sorted by Subsector Lease Duration (Color Intensity Represents Quartile)

HO

T.ST

O.

APA

RTM

ENTS

STR

IPS

IND

MIX

OFF

ICE

MA

LLS

H.C

AR

E

VTR-1.9

HCP+1.6

HCN+2.4 M

PW

HST-24.2

HPT-8.6

LHO-14.3

DRH-28.0

PSA+21.7

SNH-2.3

ESS+14.4

EXR+31.4

OHI-23.7 H

R

MAA-8.2

OFC

EQR+4.6

AVB+8.7

SSS+11.7

CUBE+0.1

CLP

ACC+22.

6 PPS

CBL-21.1

HIW

NH

I

AIV-15.2

BRE+7.5

HME-0.9

DCT-11.7

EGP-1.7

FR+5.0

UDR-0.6

CPT+7.2

DFT+5.5

PSB-6.9 FP

O

MSW

PLD-13.4

DLR+24.7

LRY-3.6

DRE-10.2

WRE-10.8

KRC

CW

HBD

N

DEIARE

-9.9

AAT

AKR

IRC

VNO-9.6

BXP+8.9

BPO-12.9

SLG-3.5

PDM-17.6

CLI-22.7

BFS

BMR

KIM-13.4

FRT+10.3

REG-13.1

DDR-20.0

WRI-12.3

SKT+8.7

EQY-10.7

SHO-28.9

HT-35.3

AHT-24.7

BEE-5.7 FC

HPE

B

SPG+22.7

MAC+1.8

GGP-11.6

TCO+20.5

Note: REIT box size indicates relative equity market capitalization. Row height represents relative subsector market cap and column width with rows represents stock market cap relative to subsector. Both exhibits as of November 17, 2011. Source: FactSet, Morgan Stanley Research

11

M O R G A N S T A N L E Y R E S E A R C H

November 18, 2011 Weekly REIT Insights

REIT Price Performance Charts Exhibit 13: REIT Subsector Relative Performance

-40

-30

-20

-10

0

10

20

Dec-10 Feb-11 Apr-11 Jun-11 Aug-11 Oct-11

Apartments Regional MallsShopping Centers OfficeIndustrial Health Care Self Storage Lodging/Resorts

Exhibit 14: REIT Subsector Price Performance - YTD -30% -20% -10% 0% 10% 20% 30%

Self Storage

Regional Malls

Apartments

Health Care

RMZ

Office

Shopping Centers

Industrial

Lodging

Exhibit 15: REIT Subsector Price Performance-Trailing 5D -1% -1% 0% 1% 1% 2% 2% 3% 3%

Self Storage

Lodging

Industrial

Health Care

Apartments

RMZ

Shopping Centers

Regional Malls

Office

Exhibit 16: REIT Subsector Dividend Yields 0% 1% 2% 3% 4% 5% 6%

Health Care

Shopping Centers

Industrial

REITs

Office

Regional Malls

Self Storage

Apartments

Lodging

Exhibit 17: REIT Subsector Price Performance - MTD -7% -6% -5% -4% -3% -2% -1% 0%

Self Storage

Lodging

Regional Malls

RMZ

Apartments

Office

Health Care

Industrial

Shopping Centers

Exhibit 18: Top 10 REIT Dividend Yields 0% 2% 4% 6% 8% 10% 12% 14%

SBRA

CWH

CDR

STIR

CSA

OHI

HPT

MPW

IRC

GOV

Note: Price performance charts as of November 16, 2011. Dividend yield charts as of November 17, 2011. Source: FactSet, Morgan Stanley Research

12

M O R G A N S T A N L E Y R E S E A R C H

November 18, 2011 Weekly REIT Insights

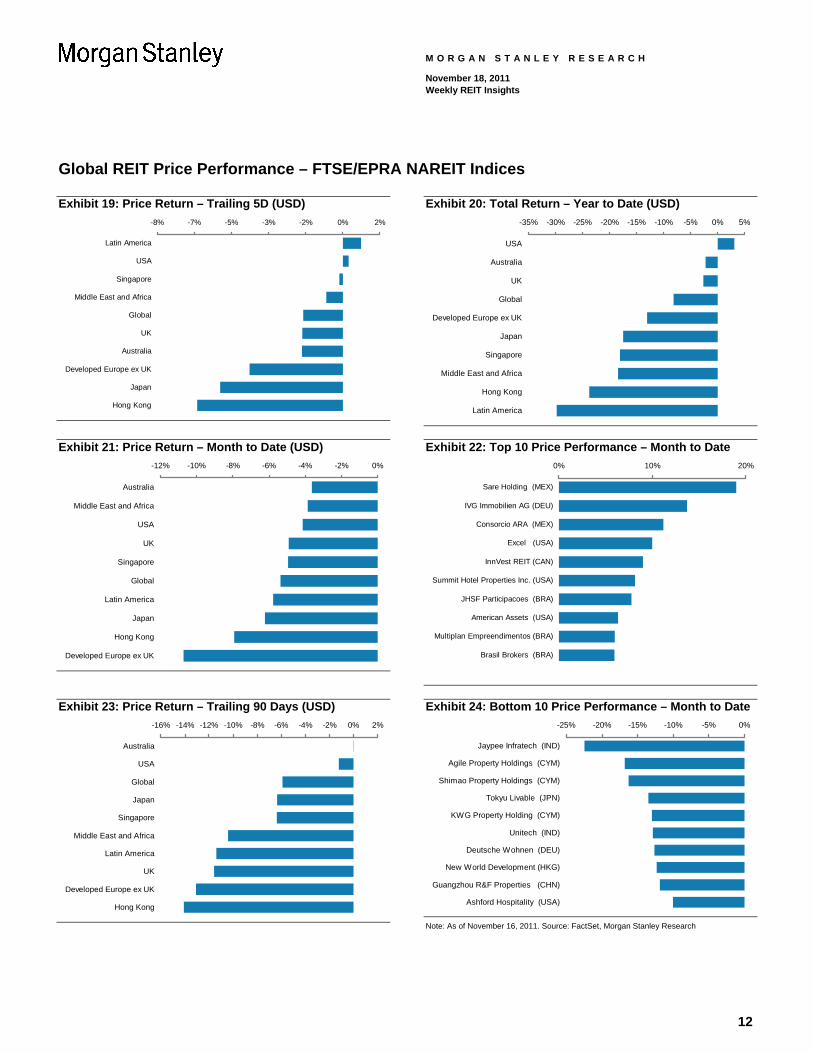

Global REIT Price Performance – FTSE/EPRA NAREIT Indices Exhibit 19: Price Return – Trailing 5D (USD)

-8% -7% -5% -3% -2% 0% 2%

Latin America

USA

Singapore

Middle East and Africa

Global

UK

Australia

Developed Europe ex UK

Japan

Hong Kong

Exhibit 20: Total Return – Year to Date (USD) -35% -30% -25% -20% -15% -10% -5% 0% 5%

USA

Australia

UK

Global

Developed Europe ex UK

Japan

Singapore

Middle East and Africa

Hong Kong

Latin America

Exhibit 21: Price Return – Month to Date (USD) -12% -10% -8% -6% -4% -2% 0%

Australia

Middle East and Africa

USA

UK

Singapore

Global

Latin America

Japan

Hong Kong

Developed Europe ex UK

Exhibit 22: Top 10 Price Performance – Month to Date 0% 10% 20%

Sare Holding (MEX)

IVG Immobilien AG (DEU)

Consorcio ARA (MEX)

Excel (USA)

InnVest REIT (CAN)

Summit Hotel Properties Inc. (USA)

JHSF Participacoes (BRA)

American Assets (USA)

Multiplan Empreendimentos (BRA)

Brasil Brokers (BRA)

Exhibit 23: Price Return – Trailing 90 Days (USD) -16% -14% -12% -10% -8% -6% -4% -2% 0% 2%

Australia

USA

Global

Japan

Singapore

Middle East and Africa

Latin America

UK

Developed Europe ex UK

Hong Kong

Exhibit 24: Bottom 10 Price Performance – Month to Date -25% -20% -15% -10% -5% 0%

Jaypee Infratech (IND)

Agile Property Holdings (CYM)

Shimao Property Holdings (CYM)

Tokyu Livable (JPN)

KWG Property Holding (CYM)

Unitech (IND)

Deutsche Wohnen (DEU)

New World Development (HKG)

Guangzhou R&F Properties (CHN)

Ashford Hospitality (USA)

Note: As of November 16, 2011. Source: FactSet, Morgan Stanley Research

13

M O R G A N S T A N L E Y R E S E A R C H

November 18, 2011 Weekly REIT Insights

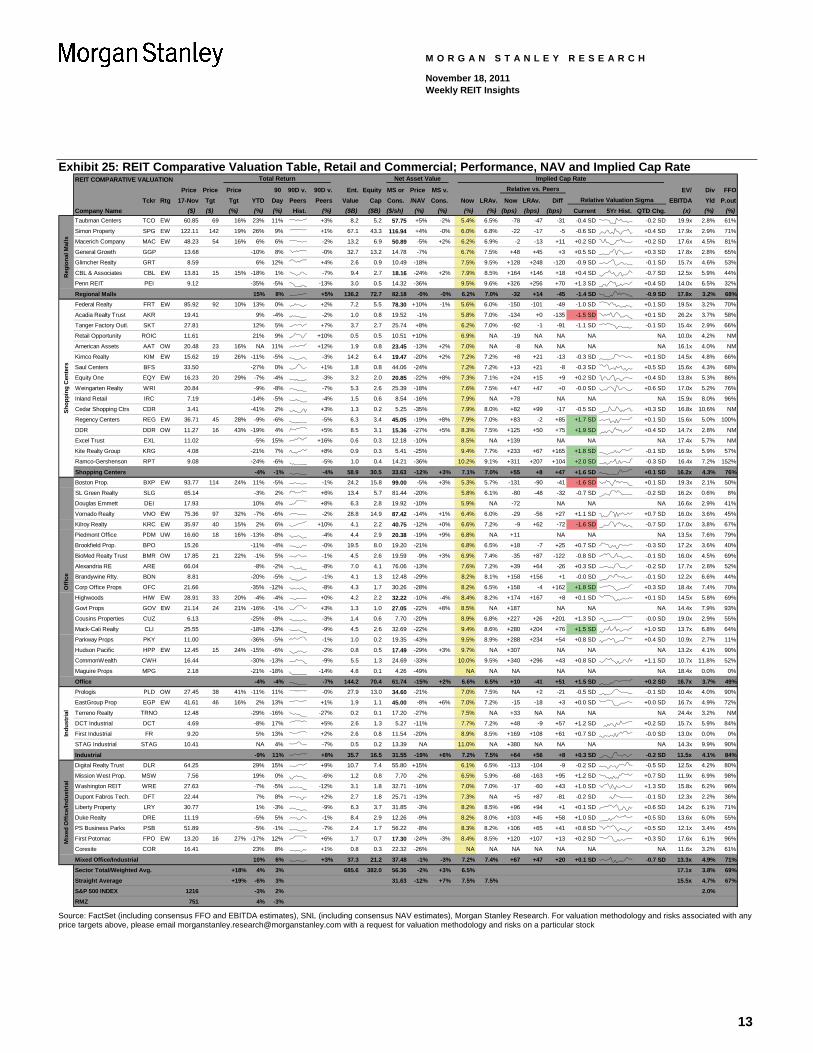

Exhibit 25: REIT Comparative Valuation Table, Retail and Commercial; Performance, NAV and Implied Cap Rate REIT COMPARATIVE VALUATION Total Return Net Asset Value Implied Cap Rate

Price Price Price 90 90D v. 90D v. Ent. Equity MS or Price MS v. Relative vs. Peers EV/ Div FFOTckr Rtg 17-Nov Tgt Tgt YTD Day Peers Peers Value Cap Cons. /NAV Cons. Now LRAv. Now LRAv. Diff Relative Valuation Sigma EBITDA Yld P.out

Company Name ($) ($) (%) (%) (%) Hist. (%) ($B) ($B) ($/sh) (%) (%) (%) (%) (bps) (bps) (bps) Current 5Yr Hist. QTD Chg. (x) (%) (%)Taubman Centers TCO EW 60.85 69 16% 23% 11% +3% 8.2 5.2 57.75 +5% -2% 5.4% 6.5% -78 -47 -31 -0.4 SD -0.2 SD 19.9x 2.8% 61% Simon Property SPG EW 122.11 142 19% 26% 9% +1% 67.1 43.3 116.94 +4% -0% 6.0% 6.8% -22 -17 -5 -0.6 SD +0.4 SD 17.9x 2.9% 71%

Macerich Company MAC EW 48.23 54 16% 6% 6% -2% 13.2 6.9 50.89 -5% +2% 6.2% 6.9% -2 -13 +11 +0.2 SD +0.2 SD 17.6x 4.5% 81%

General Growth GGP 13.68 -10% 8% -0% 32.7 13.2 14.78 -7% 6.7% 7.5% +48 +45 +3 +0.5 SD +0.3 SD 17.8x 2.8% 65%

Glimcher Realty GRT 8.59 6% 12% +4% 2.6 0.9 10.49 -18% 7.5% 9.5% +128 +248 -120 -0.9 SD -0.1 SD 15.7x 4.6% 53%

CBL & Associates CBL EW 13.81 15 15% -18% 1% -7% 9.4 2.7 18.16 -24% +2% 7.9% 8.5% +164 +146 +18 +0.4 SD -0.7 SD 12.5x 5.9% 44%

Penn REIT PEI 9.12 -35% -5% -13% 3.0 0.5 14.32 -36% 9.5% 9.6% +326 +256 +70 +1.3 SD +0.4 SD 14.0x 6.5% 32%

Regional Malls 15% 8% +5% 136.2 72.7 82.18 -0% -0% 6.2% 7.0% -32 +14 -45 -1.4 SD -0.9 SD 17.8x 3.2% 68%Federal Realty FRT EW 85.92 92 10% 13% 0% +2% 7.2 5.5 78.30 +10% -1% 5.6% 6.0% -150 -101 -49 -1.0 SD +0.1 SD 19.5x 3.2% 70%

Acadia Realty Trust AKR 19.41 9% -4% -2% 1.0 0.8 19.52 -1% 5.8% 7.0% -134 +0 -135 -1.5 SD +0.1 SD 26.2x 3.7% 58%

Tanger Factory Outl. SKT 27.81 12% 5% +7% 3.7 2.7 25.74 +8% 6.2% 7.0% -92 -1 -91 -1.1 SD -0.1 SD 15.4x 2.9% 66%

Retail Opportunity ROIC 11.61 21% 9% +10% 0.5 0.5 10.51 +10% 6.9% NA -19 NA NA NA NA 10.0x 4.2% NM

American Assets AAT OW 20.48 23 16% NA 11% +12% 1.9 0.8 23.45 -13% +2% 7.0% NA -8 NA NA NA NA 16.1x 4.0% NM

Kimco Realty KIM EW 15.62 19 26% -11% -5% -3% 14.2 6.4 19.47 -20% +2% 7.2% 7.2% +8 +21 -13 -0.3 SD +0.1 SD 14.5x 4.8% 66%

Saul Centers BFS 33.50 -27% 0% +1% 1.8 0.8 44.06 -24% 7.2% 7.2% +13 +21 -8 -0.3 SD +0.5 SD 15.6x 4.3% 68%

Equity One EQY EW 16.23 20 29% -7% -4% -3% 3.2 2.0 20.85 -22% +8% 7.3% 7.1% +24 +15 +9 +0.2 SD +0.4 SD 13.8x 5.3% 86%

Weingarten Realty WRI 20.84 -9% -8% -7% 5.3 2.6 25.39 -18% 7.6% 7.5% +47 +47 +0 -0.0 SD +0.6 SD 17.0x 5.2% 76%

Inland Retail IRC 7.19 -14% -5% -4% 1.5 0.6 8.54 -16% 7.9% NA +78 NA NA NA 15.9x 8.0% 96%

Cedar Shopping Ctrs CDR 3.41 -41% 2% +3% 1.3 0.2 5.25 -35% 7.9% 8.0% +82 +99 -17 -0.5 SD +0.3 SD 16.8x 10.6% NM

Regency Centers REG EW 36.71 45 28% -9% -6% -5% 6.3 3.4 45.05 -19% +8% 7.9% 7.0% +83 -2 +85 +1.7 SD +0.1 SD 15.6x 5.0% 100%

DDR DDR OW 11.27 16 43% -19% 4% +5% 8.5 3.1 15.36 -27% +5% 8.3% 7.5% +125 +50 +75 +1.9 SD +0.4 SD 14.7x 2.8% NM

Excel Trust EXL 11.02 -5% 15% +16% 0.6 0.3 12.18 -10% 8.5% NA +139 NA NA NA 17.4x 5.7% NM

Kite Realty Group KRG 4.08 -21% 7% +8% 0.9 0.3 5.41 -25% 9.4% 7.7% +233 +67 +165 +1.8 SD -0.1 SD 16.9x 5.9% 57%

Ramco-Gershenson RPT 9.08 -24% -6% -5% 1.0 0.4 14.21 -36% 10.2% 9.1% +311 +207 +104 +2.0 SD -0.3 SD 16.4x 7.2% 152%

Shopping Centers -4% -1% -4% 58.9 30.5 33.63 -12% +3% 7.1% 7.0% +55 +8 +47 +1.6 SD +0.1 SD 16.2x 4.3% 76%Boston Prop. BXP EW 93.77 114 24% 11% -5% -1% 24.2 15.8 99.00 -5% +3% 5.3% 5.7% -131 -90 -41 -1.6 SD +0.1 SD 19.3x 2.1% 50%

SL Green Realty SLG 65.14 -3% 2% +6% 13.4 5.7 81.44 -20% 5.8% 6.1% -80 -48 -32 -0.7 SD -0.2 SD 16.2x 0.6% 8%

Douglas Emmett DEI 17.93 10% 4% +8% 6.3 2.8 19.92 -10% 5.9% NA -72 NA NA NA 16.6x 2.9% 41%

Vornado Realty VNO EW 75.36 97 32% -7% -6% -2% 28.8 14.9 87.42 -14% +1% 6.4% 6.0% -29 -56 +27 +1.1 SD +0.7 SD 16.0x 3.6% 45%

Kilroy Realty KRC EW 35.97 40 15% 2% 6% +10% 4.1 2.2 40.75 -12% +0% 6.6% 7.2% -9 +62 -72 -1.6 SD -0.7 SD 17.0x 3.8% 67%

Piedmont Office PDM UW 16.60 18 16% -13% -8% -4% 4.4 2.9 20.38 -19% +9% 6.8% NA +11 NA NA NA 13.5x 7.6% 79%

Brookfield Prop. BPO 15.26 -11% -4% -0% 19.5 8.0 19.20 -21% 6.8% 6.5% +18 -7 +25 +0.7 SD -0.3 SD 17.2x 3.6% 40%

BioMed Realty Trust BMR OW 17.85 21 22% -1% 5% -1% 4.5 2.6 19.59 -9% +3% 6.9% 7.4% -35 +87 -122 -0.8 SD -0.1 SD 16.0x 4.5% 69%

Alexandria RE ARE 66.04 -8% -2% -8% 7.0 4.1 76.06 -13% 7.6% 7.2% +39 +64 -26 +0.3 SD -0.2 SD 17.7x 2.8% 52%

Brandywine Rlty. BDN 8.81 -20% -5% -1% 4.1 1.3 12.48 -29% 8.2% 8.1% +158 +156 +1 -0.0 SD -0.1 SD 12.2x 6.6% 44%

Corp Office Props OFC 21.66 -35% -12% -8% 4.3 1.7 30.26 -28% 8.2% 6.5% +158 -4 +162 +1.8 SD +0.3 SD 18.4x 7.4% 70%

Highwoods HIW EW 28.91 33 20% -4% -4% +0% 4.2 2.2 32.22 -10% -4% 8.4% 8.2% +174 +167 +8 +0.1 SD +0.1 SD 14.5x 5.8% 69%

Govt Props GOV EW 21.14 24 21% -16% -1% +3% 1.3 1.0 27.05 -22% +8% 8.5% NA +187 NA NA NA 14.4x 7.9% 93%

Cousins Properties CUZ 6.13 -25% -8% -3% 1.4 0.6 7.70 -20% 8.9% 6.8% +227 +26 +201 +1.3 SD -0.0 SD 19.0x 2.9% 55%

Mack-Cali Realty CLI 25.55 -18% -13% -9% 4.5 2.6 32.69 -22% 9.4% 8.6% +280 +204 +76 +1.5 SD +1.0 SD 13.7x 6.8% 64%

Parkway Props PKY 11.00 -36% -5% -1% 1.0 0.2 19.35 -43% 9.5% 8.9% +288 +234 +54 +0.8 SD +0.4 SD 10.9x 2.7% 11%

Hudson Pacific HPP EW 12.45 15 24% -15% -6% -2% 0.8 0.5 17.49 -29% +3% 9.7% NA +307 NA NA NA 13.2x 4.1% 90%

CommonWealth CWH 16.44 -30% -13% -9% 5.5 1.3 24.69 -33% 10.0% 9.5% +340 +296 +43 +0.8 SD +1.1 SD 10.7x 11.8% 52%

Maguire Props MPG 2.18 -21% -18% -14% 4.8 0.1 4.26 -49% NA NA NA NA NA NA 18.4x 0.0% 0%

Office -4% -4% -7% 144.2 70.4 61.74 -15% +2% 6.6% 6.5% +10 -41 +51 +1.5 SD +0.2 SD 16.7x 3.7% 49%Prologis PLD OW 27.45 38 41% -11% 11% -0% 27.9 13.0 34.60 -21% 7.0% 7.5% NA +2 -21 -0.5 SD -0.1 SD 10.4x 4.0% 90%

EastGroup Prop EGP EW 41.61 46 16% 2% 13% +1% 1.9 1.1 45.00 -8% +6% 7.0% 7.2% -15 -18 +3 +0.0 SD +0.0 SD 16.7x 4.9% 72%

Terreno Realty TRNO 12.48 -29% -16% -27% 0.2 0.1 17.20 -27% 7.5% NA +33 NA NA NA NA 24.4x 3.2% NM

DCT Industrial DCT 4.69 -8% 17% +5% 2.6 1.3 5.27 -11% 7.7% 7.2% +48 -9 +57 +1.2 SD +0.2 SD 15.7x 5.9% 84%

First Industrial FR 9.20 5% 13% +2% 2.6 0.8 11.54 -20% 8.9% 8.5% +169 +108 +61 +0.7 SD -0.0 SD 13.0x 0.0% 0%

STAG Industrial STAG 10.41 NA 4% -7% 0.5 0.2 13.39 NA 11.0% NA +380 NA NA NA NA 14.3x 9.9% 90%

Industrial -9% 11% +8% 35.7 16.5 31.55 -19% +6% 7.2% 7.5% +64 +56 +8 +0.3 SD -0.2 SD 11.5x 4.1% 84%Digital Realty Trust DLR 64.25 29% 15% +9% 10.7 7.4 55.80 +15% 6.1% 6.5% -113 -104 -9 -0.2 SD -0.5 SD 12.5x 4.2% 80%

Mission West Prop. MSW 7.56 19% 0% -6% 1.2 0.8 7.70 -2% 6.5% 5.9% -68 -163 +95 +1.2 SD +0.7 SD 11.9x 6.9% 98%

Washington REIT WRE 27.63 -7% -5% -12% 3.1 1.8 32.71 -16% 7.0% 7.0% -17 -60 +43 +1.0 SD +1.3 SD 15.8x 6.2% 96%

Dupont Fabros Tech. DFT 22.44 7% 8% +2% 2.7 1.8 25.71 -13% 7.3% NA +5 +87 -81 -0.2 SD -0.1 SD 12.3x 2.2% 36%

Liberty Property LRY 30.77 1% -3% -9% 6.3 3.7 31.85 -3% 8.2% 8.5% +96 +94 +1 +0.1 SD +0.6 SD 14.2x 6.1% 71%

Duke Realty DRE 11.19 -5% 5% -1% 8.4 2.9 12.26 -9% 8.2% 8.0% +103 +45 +58 +1.0 SD +0.5 SD 13.6x 6.0% 55%

PS Business Parks PSB 51.89 -5% -1% -7% 2.4 1.7 56.22 -8% 8.3% 8.2% +106 +65 +41 +0.8 SD +0.5 SD 12.1x 3.4% 45%

First Potomac FPO EW 13.20 16 27% -17% 12% +6% 1.7 0.7 17.30 -24% -3% 8.4% 8.5% +120 +107 +13 +0.2 SD +0.3 SD 17.6x 6.1% 96%

Coresite COR 16.41 23% 8% +1% 0.8 0.3 22.32 -26% NA NA NA NA NA NA NA 11.6x 3.2% 61%

Mixed Office/Industrial 10% 6% +3% 37.3 21.2 37.48 -1% -3% 7.2% 7.4% +67 +47 +20 +0.1 SD -0.7 SD 13.3x 4.9% 71%

Sector Total/Weighted Avg. +18% 4% 3% 685.6 382.0 56.36 -2% +3% 6.5% 17.1x 3.8% 69%

Straight Average +19% -6% 3% 31.63 -12% +7% 7.5% 7.5% 15.5x 4.7% 67%

S&P 500 INDEX 1216 -3% 2% 2.0%

RMZ 751 4% -3%

Indu

stria

lM

ixed

Offi

ce/In

dust

rial

Shop

ping

Cen

ters

Offi

ceR

egio

nal M

alls

Source: FactSet (including consensus FFO and EBITDA estimates), SNL (including consensus NAV estimates), Morgan Stanley Research. For valuation methodology and risks associated with any price targets above, please email [email protected] with a request for valuation methodology and risks on a particular stock

14

M O R G A N S T A N L E Y R E S E A R C H

November 18, 2011 Weekly REIT Insights

Exhibit 26: REIT Comparative Valuation Table, Retail and Commercial; FFO and Leverage Parameters REIT COMPARATIVE VALUATION Funds from Operations (FFO) Leverage Parameters Short Int.

Price 11E MS/ MS v 12E MS/ MS v Growth Multiple Relative vs. Peers Debt / Debt/ S.Debt/ Fxd % of 2wkTckr 17-Nov Cons. Cons. Cons. Cons. 11E 12E 11E 12E LRAvg Now LRAvg Diff Relative Valuation Sigma EBITDA GAV Assets Chg S/O Chg

Company Name ($) ($/sh) ($/sh) ($/sh) ($/sh) (%) (%) (x) (x) (x) (%) (%) (%) Current 5Yr Hist. QTD Chg. (x) (%) (%) (x) (%) (bps)Taubman Centers TCO 60.85 2.70 (0.01) 2.94 (0.11) -2% 9% 22.5x 20.7x 15.7x +32% +18% +14% +1.0 SD +0.5 SD 7.3x 38% 67% 2.4x 5% -41

Simon Property SPG 122.11 6.86 0.00 7.35 0.10 37% 7% 17.8x 16.6x 14.1x +4% +6% -2% +0.3 SD -0.2 SD 6.5x 37% 19% 3.1x 4% -66

Macerich Company MAC 48.23 2.87 0.27 3.16 0.01 5% 11% 16.8x 15.3x 13.2x -2% -7% +5% +0.1 SD +0.0 SD 8.8x 47% 35% 2.5x 6% -23

General Growth GGP 13.68 0.92 0.97 53% 5% 14.9x 14.1x 10.5x -13% -1% -12% NA NA 11.1x 58% 55% 1.3x 2% -4

Glimcher Realty GRT 8.59 0.46 0.74 -38% 61% 18.7x 11.6x 7.5x +9% -48% +58% +1.0 SD +0.3 SD 11.3x 59% 52% 1.6x 6% +2

CBL & Associates CBL 13.81 1.89 (0.03) 2.00 (0.04) 13% -9% 7.3x 6.9x 6.9x -57% -51% -6% -0.4 SD +0.3 SD 9.0x 66% 52% 2.2x 12% +69

Penn REIT PEI 9.12 0.86 1.74 -54% 102% 10.6x 5.2x 6.7x -38% -53% +15% -0.9 SD +0.1 SD 11.8x 75% 55% 1.8x 7% +103

Regional Malls 31% 8% 17.1x 15.8x 13.1x +0% -11% +14% +1.6 SD +0.5 SD 7.8x 44% 32% 2.6x 4% -42Federal Realty FRT 85.92 4.04 0.01 4.16 (0.03) 3% 3% 21.3x 20.7x 19.4x +36% +35% +2% +0.6 SD -0.0 SD 4.7x 26% 11% 3.7x 6% -36

Acadia Realty Trust AKR 19.41 0.96 1.06 -22% 10% 20.2x 18.3x 17.7x +30% +23% +6% +0.5 SD -0.4 SD 4.7x 28% 47% 2.3x 8% -7

Tanger Factory Outl. SKT 27.81 1.44 1.60 19% 11% 19.3x 17.4x 15.7x +24% +10% +14% +0.4 SD -0.2 SD 5.3x 28% 5% 4.1x 8% +92

Retail Opportunity ROIC 11.61 0.12 0.22 -12% 83% NM NM NA NA NA NA NA NA 0.7x 6% 10% 3.7x 6% -31

American Assets AAT 20.48 1.09 (0.03) 1.25 (0.04) NM 15% 18.8x 16.4x NA +21% NA NA NA NA 7.2x 39% 48% 2.1x 3% -13

Kimco Realty KIM 15.62 1.20 0.01 1.25 (0.00) 3% 3% 13.0x 12.5x 13.4x -17% -9% -8% -0.4 SD +0.2 SD 8.1x 50% 10% 2.5x 5% +4

Saul Centers BFS 33.50 2.06 2.37 -3% 15% 16.3x 14.1x +4% NA NA NA 9.0x 49% 55% 1.7x 2% +9

Equity One EQY 16.23 1.03 (0.33) 1.11 0.03 26% -17% 15.8x 14.6x 15.7x +1% +10% -9% -0.7 SD +0.5 SD 5.1x 31% 17% 2.6x 5% -77

Weingarten Realty WRI 20.84 1.63 1.85 15% 13% 12.8x 11.3x 11.6x -18% -21% +3% -0.4 SD -0.4 SD 7.6x 47% 18% 1.9x 8% -82

Inland Retail IRC 7.19 0.81 0.86 35% 6% 8.9x 8.4x 10.1x -43% -30% -13% -2.4 SD -0.7 SD 9.8x 57% 29% 2.4x 4% -7

Cedar Shopping Ctrs CDR 3.41 -0.09 0.43 NM NM NM 7.9x NA NA NA NA 12.1x 74% 49% 1.6x 5% -1

Regency Centers REG 36.71 2.42 0.04 2.50 (0.03) 32% 6% 15.2x 14.7x 15.3x -3% +6% -8% -0.9 SD -0.0 SD 7.5x 42% 9% 2.3x 9% +46

DDR DDR 11.27 1.00 0.03 1.03 (0.01) NM 44% 11.3x 10.9x 10.4x -28% -33% +5% +0.4 SD +0.0 SD 9.4x 56% 20% 1.8x 6% +50

Excel Trust EXL 11.02 0.92 1.09 NM 18% 12.0x 10.1x -23% NA NA NA 8.2x 41% 39% 1.9x 7% -25

Kite Realty Group KRG 4.08 0.43 0.47 2% 9% 9.5x 8.7x 10.2x -39% -32% -7% -0.7 SD +0.1 SD 10.5x 63% 40% 2.0x 3% -8

Ramco-Gershenson RPT 9.08 0.95 0.96 121% 1% 9.6x 9.5x 9.3x -39% -38% -0% +0.3 SD +0.5 SD 10.1x 52% 26% 2.0x 8% +27

Shopping Centers 13% 10% 15.6x 14.4x 14.0x -8% -2% -4% -0.9 SD -0.8 SD 7.0x 41% 17% 2.7x 6% -0Boston Prop. BXP 93.77 4.81 (0.02) 5.03 0.22 26% 0% 19.5x 18.6x 18.4x +37% +25% +12% +1.8 SD +0.6 SD 7.6x 36% 19% 2.9x 7% +1

SL Green Realty SLG 65.14 4.81 4.33 -1% -10% 13.5x 15.0x 15.1x -5% -3% -2% +0.4 SD +0.2 SD 11.7x 53% 29% 1.9x 7% -12

Douglas Emmett DEI 17.93 1.37 1.39 10% 1% 13.1x 12.9x 14.7x -8% -1% -7% -0.3 SD -0.3 SD 10.7x 55% 50% 2.4x 11% +88

Vornado Realty VNO 75.36 6.08 0.02 5.38 (0.10) 0% -12% 12.4x 14.0x 15.1x -13% +4% -17% -0.9 SD -0.3 SD 8.2x 46% 37% 2.2x 4% -44

Kilroy Realty KRC 35.97 2.22 (0.01) 2.47 0.00 8% 11% 16.2x 14.6x 15.2x +14% +3% +11% -0.3 SD +0.5 SD 7.8x 43% 12% 2.2x 7% +17

Piedmont Office PDM 16.60 1.55 0.00 1.40 (0.07) -1% -10% 10.7x 11.9x -25% NA NA NA 4.8x 30% 25% 4.9x 6% -40

Brookfield Prop. BPO 15.26 1.12 1.13 -18% 1% 13.6x 13.5x 12.4x -4% -18% +14% +1.4 SD +0.5 SD 9.8x 54% 33% NA 1% -13

BioMed Realty Trust BMR 17.85 1.20 0.01 1.30 0.01 3% 9% 14.9x 13.7x 12.6x +5% -14% +19% +1.0 SD -0.0 SD 6.9x 40% 14% 2.4x 9% +134

Alexandria RE ARE 66.04 4.40 4.59 25% 4% 15.0x 14.4x 14.6x +6% +0% +5% -0.0 SD -0.0 SD 8.3x 39% 11% 4.2x 2% +17

Brandywine Rlty. BDN 8.81 1.38 1.38 3% 0% 6.4x 6.4x 8.0x -55% -47% -8% -0.7 SD +0.2 SD 8.4x 60% 9% 2.2x 8% +35

Corp Office Props OFC 21.66 1.21 2.14 -47% 77% 17.9x 10.1x 15.2x +26% +7% +19% -1.6 SD +0.1 SD 10.3x 53% 25% 2.3x 5% -5

Highwoods HIW 28.91 2.48 (0.04) 2.65 (0.03) 2% 7% 11.6x 10.9x 12.6x -18% -11% -7% -1.1 SD -0.3 SD 7.1x 46% 23% 2.6x 10% -19

Govt Props GOV 21.14 2.01 (0.00) 1.98 (0.02) 2% -1% 10.5x 10.7x -26% NA NA NA 3.6x 20% 3% 7.9x 4% -26

Cousins Properties CUZ 6.13 0.43 0.49 34% 14% 14.3x 12.5x 18.2x +0% +24% -23% -1.2 SD -0.0 SD 9.7x 50% 22% 2.2x 4% +6

Mack-Cali Realty CLI 25.55 2.77 2.68 2% -3% 9.2x 9.5x 10.8x -35% -25% -10% -1.0 SD -0.6 SD 4.9x 37% 13% 3.2x 4% +85

Parkway Props PKY 11.00 1.49 2.19 -44% 47% 7.4x 5.0x 8.0x -48% -46% -2% -1.7 SD +0.0 SD 6.2x 66% 49% 1.9x 9% -10

Hudson Pacific HPP 12.45 1.03 (0.06) 1.12 (0.19) 61% 7% 12.1x 11.1x -15% NA NA NA 6.4x 37% 29% NA 4% -28

CommonWealth CWH 16.44 3.45 3.38 -8% -2% 4.8x 4.9x 6.9x -67% -53% -13% -2.5 SD -1.2 SD 9.0x 68% 8% 1.9x 2% -36

Maguire Props MPG 2.18 1.92 -0.56 NM NM 1.1x NM -92% NA NA NA 24.3x 95% 103% 0.8x 10% -75

Office 6% -1% 14.2x 14.2x 13.9x -16% -2% -6% -0.5 SD +0.0 SD 8.3x 45% 26% 2.8x 5% -2Prologis PLD 27.45 1.00 (0.36) 1.67 0.01 109% 32% 27.6x 16.4x 17.0x +14% +12% +2% -0.8 SD +0.1 SD 9.0x 48% 11% 2.7x 3% -33

EastGroup Prop EGP 41.61 3.11 0.15 3.28 0.17 3% 6% 13.4x 12.7x 13.5x -45% -7% -37% -0.3 SD -0.1 SD 6.8x 39% 38% 3.3x 7% -32

Terreno Realty TRNO 12.48 -0.52 -0.08 NM NM NM NM NA NA NA NA NA NA NA NA 26% 2.4x 4% -10

DCT Industrial DCT 4.69 0.37 0.38 12% 3% 12.7x 12.3x 12.7x -48% -14% -33% -0.4 SD -0.3 SD 8.4x 49% 9% 2.4x 7% -84

First Industrial FR 9.20 0.86 0.85 NM -1% 10.7x 10.8x 7.7x -56% -50% -6% +1.3 SD +0.2 SD 9.1x 63% 21% 1.5x 5% -20

STAG Industrial STAG 10.41 1.04 1.10 -9% 6% 10.0x 9.5x NA -59% NA NA NA NA NA NA 56% 2.3x 6% -1

Industrial 92% 26% 24.2x 15.4x 15.9x +42% +3% -2% -0.3 SD +0.2 SD 8.8x 48% 14% 2.6x 4% -36Digital Realty Trust DLR 64.25 4.04 4.41 19% 9% 15.9x 14.6x 15.7x +17% +22% -5% -0.9 SD +0.2 SD 5.3x 34% 15% 3.7x 14% +53

Mission West Prop. MSW 7.56 0.54 0.55 2% 2% 14.0x 13.7x 16.0x +3% +25% -22% -0.8 SD -0.9 SD 4.6x 30% 30% 3.5x 3% -1

Washington REIT WRE 27.63 1.92 1.99 7% 4% 14.4x 13.9x 14.4x +6% +12% -6% -0.6 SD -1.0 SD 6.6x 37% 16% 2.6x 9% +127

Dupont Fabros Tech. DFT 22.44 1.60 1.81 20% 13% 14.0x 12.4x +3% NA NA NA 4.8x 30% 5% 4.7x 18% -217

Liberty Property LRY 30.77 2.57 2.61 -3% 2% 12.0x 11.8x 11.5x -12% -12% -0% +0.9 SD -0.2 SD 6.1x 41% 5% 3.4x 3% -3

Duke Realty DRE 11.19 1.13 1.09 -8% -4% 9.9x 10.3x 10.2x -27% -23% -4% +0.3 SD +0.3 SD 9.2x 63% 13% 1.8x 5% +80

PS Business Parks PSB 51.89 4.72 4.50 22% -5% 11.0x 11.5x 12.7x -19% -1% -18% -1.8 SD -1.2 SD 4.1x 31% 2% 4.1x 3% -22

First Potomac FPO 13.20 0.88 (0.17) 1.12 (0.01) 5% 27% 14.9x 11.7x 11.1x +10% -27% +37% +0.1 SD -0.4 SD 10.6x 52% 25% 1.9x 5% -10

Coresite COR 16.41 1.21 1.35 42% 12% 13.6x 12.2x NA -0% NA NA NA NA NA NA 14% 18.8x 4% -13

Mixed Office/Industrial 10% 5% 13.6x 12.8x 12.3x -20% -12% -4% -0.9 SD +0.2 SD 6.1x 39% 12% 3.6x 9% +19

Sector Total/Weighted Avg. 20% 10% 17.0x 15.3x 14.2x 7.2x 40% 21% 3.1x 6% -11

Straight Average 13% 17% 14.7x 13.2x 13.4x 7.8x 45% 26% 3.2x 6% -2

S&P 500 INDEX SPX

Indu

stria

lO

ffice

Reg

iona

l Mal

lsM

ixed

Offi

ce/In

dust

rial

Shop

ping

Cen

ters

Source: FactSet (including consensus FFO and EBITDA estimates), SNL (including consensus NAV estimates), Morgan Stanley Research. For valuation methodology and risks associated with any price targets above, please email [email protected] with a request for valuation methodology and risks on a particular stock

15

M O R G A N S T A N L E Y R E S E A R C H

November 18, 2011 Weekly REIT Insights

Exhibit 27: REIT Comparative Valuation Table, Residential and Other; Performance, NAV and Implied Cap Rate REIT COMPARATIVE VALUATION Total Return Net Asset Value Implied Cap Rate

Price Price Price 90 90D v. 90D v. Ent. Equity MS or Price MS v. Relative vs. Peers EV/ Div FFORtg 17-Nov Tgt Tgt YTD Day Peers Peers Value Cap Cons. /NAV Cons. Now LRAv. Now LRAv. Diff Relative Valuation Sigma EBITDA Yld P.out

Company Name ($) ($) (%) (%) (%) Hist. (%) ($B) ($B) ($/sh) (%) (%) (%) (%) (bps) (bps) (bps) Current 5Yr Hist. QTD Chg. (x) (%) (%)AvalonBay AVB 122.29 11% -4% +1% 14.3 11.6 122.93 -1% 4.9% 5.8% -70 -42 -28 -0.6 SD -0.2 SD 22.3x 2.8% 87%

Essex Property ESS OW 130.65 163 28% 17% -3% +2% 7.0 4.7 139.45 -6% +10% 5.0% 5.5% -63 -69 +6 +0.2 SD -0.1 SD 23.4x 3.1% 75%

BRE Properties BRE OW 46.76 56 23% 10% -1% +5% 5.3 3.5 51.15 -9% +7% 5.2% 6.1% -43 -13 -30 -0.6 SD -0.4 SD 22.4x 3.1% 93%

Equity Residential EQR 54.36 7% -6% -0% 25.9 16.8 55.57 -2% 5.3% 5.8% -36 -40 +5 +0.6 SD +0.4 SD 20.0x 2.4% 63%

UDR UDR 23.39 3% -6% -1% 9.7 5.3 24.66 -5% 5.4% 6.1% -29 -10 -19 -0.3 SD +0.1 SD 24.2x 3.3% 71%

MAA MAA EW 58.30 72 28% -4% -12% -6% 3.9 2.3 65.71 -11% +4% 6.2% 6.6% +51 +43 +8 +0.2 SD +0.5 SD 18.0x 4.2% 69%

Post Properties PPS 39.32 10% 0% +5% 3.1 2.0 44.39 -11% 6.2% 6.9% +56 +75 -19 -0.3 SD -0.7 SD 18.7x 2.2% 71%

Camden Property CPT 57.86 10% -8% -2% 7.2 4.4 62.83 -8% 6.4% 6.9% +78 +67 +11 +0.6 SD +0.1 SD 17.6x 3.3% 70%

Home Properties HME EW 55.01 66 24% 3% -12% -6% 5.5 3.2 65.29 -16% +2% 6.5% 6.7% +90 +49 +41 +0.7 SD +0.6 SD 17.3x 4.4% 78%

AIMCO AIV EW 21.90 28 30% -14% -10% -5% 7.7 2.8 31.53 -31% +12% 7.2% 7.3% +160 +112 +48 +1.5 SD +0.7 SD 14.5x 2.1% 34%

Associated Estates AEC 16.30 11% -1% +4% 1.3 0.7 20.70 -21% 7.4% 8.7% +179 +252 -73 -1.1 SD +0.0 SD 13.2x 4.1% 78%

Colonial Properties CLP 19.03 9% -3% +2% 3.6 1.8 22.26 -15% 8.8% 8.5% +315 +229 +85 +1.2 SD -0.0 SD 16.3x 3.1% 57%

Apartments 7% -5% -8% 94.5 59.3 70.83 -7% +7% 5.6% 6.2% -91 -71 -20 -0.4 SD +0.2 SD 20.3x 2.9% 71%

American Campus ACC 38.93 27% 6% +11% 4.0 2.8 33.98 +15% 4.5% 5.3% -118 -18 -100 -1.1 SD -0.2 SD 16.4x 3.4% 82%

Education Realty EDR 9.19 22% 11% +17% 0.9 0.7 9.18 +0% 5.9% 6.4% +29 +89 -60 +0.4 SD -0.2 SD 19.2x 3.0% NM

Student Housing 26% 7% +4% 4.9 3.5 29.21 +12% 4.7% 5.5% -180 -141 -40 -0.6 SD +0.4 SD 17.0x 3.4% 82%Equity Lifestyle ELS 61.89 13% -3% -2% 4.4 2.4 63.69 -3% 6.9% NA -20 NA NA NA 13.3x 2.4% 43%

Sun Communities SUI 36.11 16% 4% +5% 2.2 0.8 32.42 +11% 7.8% NA +62 NA NA NA 13.1x 6.9% 85%

Manu. Homes 14% -1% -4% 6.6 3.2 56.06 +1% 7.1% NA +59 NA NA NA NA 12.2x 3.5% 53%

Universal Health UHT 35.95 3% 3% -1% 0.6 0.5 34.50 +4% 5.7% NA -109 NA NA NA NA 25.4x 6.6% 90%

HCP HCP EW 37.38 40 12% 7% 8% +4% 23.4 15.2 29.16 +28% -0% 6.3% 6.4% -56 -70 +14 +0.4 SD -0.1 SD 17.0x 5.0% 93%

Ventas Inc. VTR 51.46 1% 3% -1% 22.2 14.8 39.91 +29% 6.4% 7.0% -44 -13 -31 -1.5 SD +0.4 SD 21.7x 4.4% 84%

National Health Inv. NHI 42.43 -2% -1% -5% 1.2 1.2 33.91 +25% 6.8% 8.1% -5 +103 -108 -0.9 SD +0.2 SD 14.2x 5.8% 87%

Healthcare Realty HR 17.05 -14% 6% +2% 2.8 1.3 17.82 -4% 6.8% 6.3% -3 -79 +76 +1.4 SD +1.1 SD 16.1x 7.0% 104%

Health Care REIT HCN EW 48.80 53 14% 9% 3% -1% 13.9 8.7 42.99 +14% +5% 7.1% 7.1% +28 -6 +35 +0.9 SD +0.3 SD 14.2x 5.7% 91%

LTC Properties LTC 28.24 6% 15% +11% 1.0 0.9 25.41 +11% 7.9% 8.4% +104 +129 -25 -0.7 SD -1.3 SD 12.1x 5.9% 90%

Senior Housing Prop. SNH EW 21.44 24 19% 4% -2% -6% 4.9 3.3 23.73 -10% +8% 8.3% 8.6% +142 +148 -6 -0.1 SD +0.6 SD 13.6x 7.0% 88%

Cogdell Spencer CSA 3.96 -28% 3% -2% 0.8 0.2 5.59 -29% 8.7% 8.1% +188 +99 +89 +0.6 SD +0.5 SD 15.3x 9.8% NM

Medical Props Trust MPW 9.59 -6% -2% -6% 1.7 1.1 8.30 +16% 8.9% 8.3% +210 +119 +91 +1.0 SD +0.6 SD 11.3x 8.2% NM

Omega Healthcare OHI 17.12 -18% 2% -2% 3.1 1.8 14.33 +19% 9.6% 8.3% +281 +120 +161 +2.0 SD -0.2 SD 12.3x 9.2% 111%

Sabra Health Care SBRA 10.23 -40% -4% -9% 0.7 0.4 17.02 -40% NA NA NA NA NA NA NA NA 12.5% NM

Healthcare 3% 4% +1% 76.3 49.3 33.07 +20% +2% 6.8% 7.0% +29 +14 +15 +0.3 SD +0.0 SD 17.3x 5.5% 90%

Public Storage PSA UW 123.45 115 -4% 25% 6% -0% 24.2 21.1 92.56 +33% -2% 5.1% 6.9% -38 -15 -22 -1.4 SD +0.3 SD 22.1x 3.1% 80%

Extra Space Storage EXR EW 22.87 23 3% 34% 13% +7% 3.5 2.3 20.83 +10% +7% 6.8% 7.6% +137 +58 +79 +0.8 SD -0.5 SD 21.4x 2.4% 60%

Sovran Self Storage SSS 41.12 17% 8% +2% 1.9 1.2 41.60 -1% 6.9% 7.8% +150 +82 +68 +1.1 SD +0.2 SD 14.2x 4.3% 73%

CubeSmart CUBE 9.54 3% -5% -11% 1.6 1.0 10.20 -6% 8.6% NA +318 NA NA NA NA 14.0x 2.9% 54%

Storage 24% 6% +3% 31.2 25.5 80.68 +28% -1% 5.4% 7.0% -111 +5 -116 -1.7 SD -0.4 SD 21.4x 3.1% 77%

Realty Income Corp O 33.36 2% 1% -4% 6.6 4.4 27.57 +21% 6.3% NA -66 NA NA NA 14.5x 5.2% 95%

National Retail Props NNN 26.26 5% 5% -1% 3.9 2.5 24.26 +8% 6.6% NA -35 NA NA NA 15.6x 5.8% 117%

Entertainment Props EPR 44.23 0% 15% +10% 3.6 2.1 42.36 +4% 8.2% NA +127 NA NA NA 14.6x 6.3% 93%

CapLease LSE 3.92 -30% 11% +5% 1.5 0.3 5.90 -34% 11.4% NA +440 NA NA NA NA 6.6% 49%

Triple Net 1% 6% +3% 15.6 9.3 29.36 +12% 7.0% NA +42 NA NA NA NA 14.9x 5.7% 99%Host Hotels HST OW 13.54 14 4% -24% 28% +5% 16.0 9.6 21.00 -36% +24% 8.0% 8.1% -84 -79 NA NA NA 16.1x 1.1% 23%

LaSalle Hotel Props LHO EW 22.62 20 -10% -13% 45% +22% 3.3 1.9 30.00 -25% +15% 8.1% 8.7% -79 -14 NA NA NA 14.6x 1.9% 53%

Diamondrock Hosp. DRH EW 8.64 8 -4% -26% 20% -3% 2.4 1.4 12.00 -28% +18% 8.3% 8.3% -52 -60 NA NA NA 14.3x 3.6% 57%

Strategic Hotels BEE OW 4.99 7 30% -6% 17% -6% 2.7 0.9 8.00 -38% +31% 8.5% 8.8% -37 -6 NA NA NA 14.4x 0.0% 0%

Hersha Hospitality HT EW 4.27 5 11% -33% 14% -9% 1.8 0.7 6.00 -29% +12% 9.2% 9.3% +28 +45 NA NA NA 13.2x 5.5% 65%

Ashford Hospitality AHT OW 7.27 10 43% -22% 1% -22% 4.3 0.5 14.00 -48% +33% 9.3% 9.3% +42 +42 NA NA NA 11.1x 5.5% 27%

Sunstone Hotel Inv SHO EW 7.34 6 -16% -29% 40% +17% 2.9 0.9 12.00 -39% +16% 9.5% 8.1% +67 -80 NA NA NA 10.2x 0.0% 0%

Hospitality Prop. HPT EW 21.05 24 23% -2% -3% -26% 5.3 2.6 28.00 -25% +6% 12.6% 11.7% +370 +284 NA NA NA 9.5x 8.3% 54%

FelCor Lodging FCH 2.99 -58% 16% -7% 2.4 0.4 3.81 -22% NA NA NA NA NA NA NA 11.6x 0.0% 0%

Pebblebrook Trust PEB 18.44 -7% 26% +3% 1.6 0.9 18.27 +1% NA NA NA NA NA NA NA 7.2x 2.6% NM

Chesapeake Lodging CHSP 14.71 -19% 20% -3% 0.7 0.5 18.00 -18% NA NA NA NA NA NA NA 6.8x 5.4% NM

Chatham Lodging CLDT 10.71 -35% 9% -14% 0.3 0.1 11.02 -3% NA NA NA NA NA NA NA 6.5x 6.5% 131%

Summit INN 8.25 NA 17% -6% 0.5 0.2 8.41 -2% NA NA NA NA NA NA NA NA 5.4% 108%

Lodging -20% 23% +20% 44.2 20.7 19.71 -30% +20% 8.9% 8.8% +232 +187 NA NA NA 13.6x 2.7% 34%

Sector Total/Weighted Avg. 18% 4% 3% 685.6 382.0 56.36 -2% +3% 6.5% 17.1x 3.8% 69%

Straight Average +19% -6% 3% 31.63 -12% +7% 7.5% 7.5% 15.5x 4.7% 67%

S&P 500 INDEX 1216 -3% 2% 2.0%

RMZ 751 4% -3%

Hea

lthca

reM

anu.

HA

part

men

tsSt

uden

t H.

Lodg

ing

Stor

age

Trip

le N

et

Source: FactSet (including consensus FFO and EBITDA estimates), SNL (including consensus NAV estimates), Morgan Stanley Research. For valuation methodology and risks associated with any price targets above, please email [email protected] with a request for valuation methodology and risks on a particular stock

16

M O R G A N S T A N L E Y R E S E A R C H

November 18, 2011 Weekly REIT Insights

Exhibit 28: REIT Comparative Valuation Table, Residential and Other; FFO and Leverage Parameters REIT COMPARATIVE VALUATION Funds from Operations (FFO) Leverage Parameters Short Int.

Price 11E MS/ MS v 12E MS/ MS v Growth Multiple Relative vs. Peers Debt / Debt/ S.Debt/ Fxd % of 2wkTckr 17-Nov Cons. Cons. Cons. Cons. 11E 12E 11E 12E LRAvg Now LRAvg Diff Relative Valuation Sigma EBITDA GAV Assets Chg S/O Chg

Company Name ($) ($/sh) ($/sh) ($/sh) ($/sh) (%) (%) (x) (x) (x) (%) (%) (%) Current 5Yr Hist. QTD Chg. (x) (%) (%) (x) (%) (bps)AvalonBay AVB 122.29 4.61 5.44 15% 18% 26.5x 22.5x 21.4x +24% +22% +2% -0.6 SD +0.2 SD 5.8x 23% 21% 3.4x 10% -19

Essex Property ESS 130.65 5.71 0.01 6.49 0.02 7% 14% 22.9x 20.1x 19.2x +7% +10% -3% -0.5 SD +0.1 SD 8.2x 33% 40% 2.9x 8% 13

BRE Properties BRE 46.76 2.16 0.02 2.39 0.01 35% 10% 21.6x 19.6x 18.2x +1% +3% -2% +0.2 SD +0.6 SD 7.4x 31% 20% 3.1x 5% 56

Equity Residential EQR 54.36 2.43 2.78 17% 14% 22.4x 19.6x 17.9x +4% +2% +2% +1.7 SD +0.2 SD 7.3x 34% 21% 2.6x 5% 18

UDR UDR 23.39 1.27 1.42 17% 12% 18.4x 16.5x 15.1x -14% -14% -0% +0.2 SD -0.0 SD 10.9x 44% 24% 2.6x 3% -12

MAA MAA 58.30 3.97 (0.02) 4.39 0.03 11% 10% 14.7x 13.3x 13.8x -31% -20% -12% -1.3 SD -0.7 SD 7.6x 39% 43% 3.4x 5% -48

Post Properties PPS 39.32 1.89 2.02 56% 7% 20.8x 19.5x 19.6x -3% +12% -15% -1.0 SD +0.2 SD 7.2x 32% 22% 2.5x 7% -28

Camden Property CPT 57.86 2.71 3.41 0% 26% 21.4x 17.0x 15.4x -0% -12% +12% +0.3 SD -0.5 SD 8.0x 37% 17% 3.1x 5% 35

Home Properties HME 55.01 3.49 0.00 3.79 0.00 12% 9% 15.8x 14.5x 15.1x -26% -12% -14% -1.2 SD -0.7 SD 7.1x 37% 48% 2.4x 8% 138

AIMCO AIV 21.90 1.49 0.05 1.83 0.05 3% 23% 14.7x 12.0x 12.4x -31% -32% +0% -0.1 SD -0.2 SD 9.7x 56% 53% 1.7x 8% -37

Associated Estates AEC 16.30 1.04 1.23 22% 18% 15.7x 13.3x 11.5x -27% -36% +9% +0.8 SD +0.0 SD 8.4x 42% 35% 2.4x 6% 98

Colonial Properties CLP 19.03 1.16 1.26 14% 9% 16.4x 15.1x 12.1x -23% -33% +10% +0.9 SD -0.1 SD 9.2x 46% 18% 2.0x 6% -19

Apartments 16% 15% 21.4x 18.6x 17.5x +26% +18% +4% +1.0 SD -0.2 SD 7.6x 35% 26% 2.8x 6% 11

American Campus ACC 38.93 1.79 1.95 9% 9% 21.7x 20.0x 18.1x -1% +5% -6% -1.6 SD -0.4 SD 6.4x 33% 33% 2.7x 8% 7

Education Realty EDR 9.19 0.40 0.47 NM 18% 23.0x 19.6x 14.0x +5% -21% +25% +1.2 SD +0.3 SD 5.9x 27% 34% 1.1x 7% -23

Student Housing 7% 11% 22.0x 19.9x 0.0x +29% +18% +16% +0.9 SD -1.0 SD 6.8x 35% 36% 2.6x 9% 1

Equity Lifestyle ELS 61.89 3.44 4.46 -1% 30% 18.0x 13.9x +10% NA NA NA 8.2x 47% 47% 1.9x 4% -46

Sun Communities SUI 36.11 3.15 3.39 8% 8% 11.5x 10.7x -30% NA NA NA 9.8x 67% 68% 2.1x 6% -13

Manu. Homes 1% 24% 16.4x 13.1x 13.8x -4% +10% -23% NA NA 8.6x 52% 52% 1.9x 5% -38

Universal Health UHT 35.95 2.52 2.55 -5% 1% 14.3x 14.1x NA -3% NA NA NA NA 5.3x 20% 5% 8.2x 4% 6

HCP HCP 37.38 2.54 0.02 2.79 (0.01) 22% 10% 14.7x 13.4x 14.3x +0% +1% -1% -0.1 SD +0.3 SD 6.0x 41% 10% 3.5x 8% -47

Ventas Inc. VTR 51.46 3.24 3.61 21% 11% 15.9x 14.3x 15.3x +8% +8% -0% +0.2 SD -0.7 SD 7.4x 39% 15% 4.3x 6% -37

National Health Inv. NHI 42.43 2.92 3.08 4% 5% 14.5x 13.8x -1% NA NA NA 0.8x 7% 0% 33.8x 3% -26

Healthcare Realty HR 17.05 1.14 1.31 0% 15% 15.0x 13.0x 15.9x +2% +13% -11% -1.7 SD -0.1 SD 9.0x 51% 7% 2.3x 6% -14

Health Care REIT HCN 48.80 3.39 0.04 3.81 0.03 10% 12% 14.4x 12.8x 13.5x -2% -3% +2% +0.4 SD -0.1 SD 8.2x 51% 13% 2.4x 8% 31

LTC Properties LTC 28.24 2.14 2.29 17% 7% 13.2x 12.3x 12.6x -10% -10% -0% +0.4 SD +0.8 SD 2.4x 19% 0% 7.4x 4% -46

Senior Housing Prop. SNH 21.44 1.75 (0.01) 1.84 (0.05) 4% 5% 12.3x 11.7x 12.3x -17% -13% -4% -0.8 SD -1.5 SD 4.6x 32% 16% 3.6x 2% 1

Cogdell Spencer CSA 3.96 0.30 0.41 NM 37% 13.2x 9.7x -10% NA NA NA 12.3x 63% 54% 2.0x 5% 4

Medical Props Trust MPW 9.59 0.74 0.90 100% 22% 13.0x 10.7x 10.5x -12% -26% +15% +0.5 SD -0.2 SD 6.1x 44% 1% 1.4x 5% -20

Omega Healthcare OHI 17.12 1.78 1.93 25% 8% 9.6x 8.9x 11.5x -34% -17% -17% -1.9 SD +0.1 SD 4.9x 47% 7% 3.3x 9% 89

Sabra Health Care SBRA 10.23 0.39 0.43 NM 10% 26.2x 23.8x NA +79% NA NA NA NA NA NA 18% 2.2x 4% -36

Healthcare 19% 11% 14.7x 13.3x 11.7x -14% -3% -12% -1.1 SD -0.2 SD 6.6x 41% 12% 4.3x 6% -19

Public Storage PSA 123.45 5.84 0.01 6.15 (0.07) 24% 5% 21.1x 20.1x 17.4x +2% +3% -1% +0.4 SD -0.2 SD 3.0x 17% 2% 4.6x 3% 2

Extra Space Storage EXR 22.87 1.11 (0.04) 1.27 (0.02) 22% 14% 20.6x 18.1x 14.6x -0% -15% +14% +0.4 SD +0.4 SD 7.9x 38% NA 2.9x 7% 3

Sovran Self Storage SSS 41.12 2.43 2.93 -1% 21% 16.9x 14.0x 13.3x -18% -21% +3% -0.8 SD -0.4 SD 6.6x 38% 5% 3.0x 4% 30

CubeSmart YSI 9.54 0.62 0.69 22% 11% 15.4x 13.8x NA -26% NA NA NA NA 5.7x 38% 19% 2.9x NA NA

Storage 22% 7% 20.7x 19.4x 14.2x +21% +16% +8% +0.6 SD +0.0 SD 3.7x 21% 3% 4.3x 3% 3

Realty Income Corp O 33.36 1.98 2.10 8% 6% 16.8x 15.9x 14.5x -1% -2% +1% NA NA 6.1x 39% 1% 2.8x 6% 3

National Retail Props NNN 26.26 1.55 1.63 18% 5% 16.9x 16.1x 13.4x -0% -13% +12% NA NA 6.7x 39% 1% 2.6x 14% -84

Entertainment Props EPR 44.23 2.40 3.54 -20% 48% 18.4x 12.5x 11.0x +8% -26% +34% NA NA 6.1x 44% 22% 2.6x 9% 16

CapLease LSE 3.92 0.47 0.64 -11% 36% 8.3x 6.1x 6.9x -51% -29% -22% NA NA NA 77% 59% 1.7x 4% 2

Triple Net 4% 16% 17.0x 14.9x 9.2x -0% -30% +26% NA NA 6.2x 41% 8% 2.7x 9% -18

Host Hotels HST 13.54 0.88 (0.00) 1.13 0.04 27% 28% 15.4x 12.0x 13.8x +33% +16% +17% -0.5 SD +0.4 SD 6.3x 29% 5% 2.4x 5% -35

LaSalle Hotel Props LHO 22.62 1.55 (0.01) 1.97 (0.04) 12% 27% 14.6x 11.5x 12.7x +26% +8% +18% -0.6 SD -0.8 SD 7.1x 36% 21% NA 7% -25

Diamondrock Hosp. DRH 8.64 0.65 0.01 0.69 (0.07) 4% 7% 13.4x 12.5x 11.5x +16% -1% +16% -0.0 SD -0.5 SD 6.9x 36% 29% 3.0x 6% -41

Strategic Hotels BEE 4.99 0.14 0.01 0.26 (0.01) NM 88% NM 19.0x NA NA NA NA 12.1x 55% 38% 1.5x 5% -30

Hersha Hospitality HT 4.27 0.38 0.01 0.43 0.01 -3% 14% 11.4x 10.0x 9.1x -2% -22% +21% NA NA 8.7x 49% 41% 2.1x 4% 21

Ashford Hospitality AHT 7.27 1.97 (0.00) 2.28 0.30 31% 16% 3.7x 3.2x 5.3x -68% -54% -14% NA NA 12.9x 76% 57% 1.1x 6% 32

Sunstone Hotel Inv SHO 7.34 0.81 (0.02) 1.03 0.06 44% 26% 9.0x 7.1x 10.2x -22% -19% -3% -0.6 SD +0.4 SD 10.7x 61% 42% 1.7x 6% 34

Hospitality Prop. HPT 21.05 3.32 0.01 3.41 0.15 2% 3% 6.3x 6.2x 6.9x -45% -36% -9% NA NA 4.8x 44% 0% 3.4x 4% -21

FelCor Lodging FCH 2.99 0.18 0.32 NM 78% 16.6x 9.3x +44% NA NA NA 10.8x 83% 46% 1.0x 6% -5

Pebblebrook Trust PEB 18.44 0.12 0.47 NM NM NM NM NA NA NA NA 7.3x 36% 17% 2.8x 8% 43

Chesapeake Lodging CHSP 14.71 0.32 0.87 -11% 172% NM 16.9x NA NA NA NA 8.8x 40% 41% 3.8x 5% 14

Chatham Lodging CLDT 10.71 0.94 1.46 77% 55% 11.4x 7.3x -2% NA NA NA 8.7x 57% 44% 1.8x 4% -19

Summit INN 8.25 0.71 0.91 73% 28% 11.6x 9.1x NA +0% NA NA NA NA 6.8x 54% NA 3.6x 4% -48

Lodging 20% 30% 11.6x 10.5x 9.4x -32% -22% -2% -0.1 SD +0.3 SD 7.1x 39% 16% 2.5x 5% -21

Sector Total/Weighted Avg. 20% 10% 17.0x 15.3x 14.2x 7.2x 40% 21% 3.1x 6% -11

Straight Average 13% 17% 14.7x 13.2x 13.4x 7.8x 45% 26% 3.2x 6% -2

S&P 500 INDEX SPX

Apa

rtm

ents

Stud

ent H

.M

anu.

HLo

dgin

gH

ealth

care

Stor

age

Trip

le N

et

Source: FactSet (including consensus FFO and EBITDA estimates), SNL (including consensus NAV estimates), Morgan Stanley Research. For valuation methodology and risks associated with any price targets above, please email [email protected] with a request for valuation methodology and risks on a particular stock

17

M O R G A N S T A N L E Y R E S E A R C H

November 18, 2011 Weekly REIT Insights

Glossary for Comparative Valuation Tables

For estimates (including NAV & Funds from Operations) bold denotes MS covered company estimate.

• Total Return: 90 D v. Peers = Past 90 days total return performance relative to subsector weighted average. The peer for the subsector averages themselves is the overall industry average.

• Equity Cap ($B) = Equity market cap taking into account OP units and other potentially dilutive securities.

• LRAv. = Long-run average: the 5yr quarterly valuation metric average.

• Relative vs. Peers Sections (Implied Cap Rate; Funds From Operations)

o Now (bps) = Current valuation metric premium relative to subsector peer average.

o Diff. (bps) = Difference between current valuation metric premium and 5 yr average

• Relative Valuation Sigma (from Implied Cap Rate and Funds from Operations)

o Current: The Z-score of the valuation metric premium relative to peer group average, which is expressed in standard deviations from the same metric’s long run (5yr) average. For implied cap rates, if a stock is trading at or above +1.5 SD we highlight it as cheap (green) by this metric alone; when trading below -1.5 SD we highlight as expensive (red); for FFO multiples, the sign is reversed.

o QTD Chg.: The difference between reported relative valuation sigma at the end of the previous quarter (based on earnings reporting periods, not calendar dates) and the current sigma.

18

M O R G A N S T A N L E Y R E S E A R C H

November 18, 2011 Weekly REIT Insights