CBIZ & MHM Executive Education Series™ Not-For-Profit Update: Internal Controls, Accounting Standards & Federal Grant Reform Presented by: Tracey McDonald Morgan Padgett & Michelle Spriggs April 29, 2015

Webinar Slides: Not-for-Profit Update - Internal Controls, Accounting Standards & Federal Grant Reform

Jul 15, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

CBIZ & MHM Executive Education Series™ Not-For-Profit Update: Internal Controls,

Accounting Standards & Federal Grant Reform Presented by: Tracey McDonald

Morgan Padgett & Michelle Spriggs

April 29, 2015

2 #CBIZMHMwebinar

To view this webinar in full screen mode, click on view options in the upper right hand corner.

Click the Support tab for technical assistance.

If you have a question during the presentation, please use the Q&A feature at the bottom of your screen.

Before We Get Started…

3 #CBIZMHMwebinar

This webinar is eligible for CPE credit. To receive credit, you will need to answer periodic participation markers throughout the webinar.

External participants will receive their CPE certificate via email immediately following the webinar.

CPE Credit

4 #CBIZMHMwebinar

The information in this Executive Education Series course is a brief summary and may not include all

the details relevant to your situation.

Please contact your service provider to further discuss the impact on your business.

Disclaimer

5 #CBIZMHMwebinar

Today’s Presenters

Tracey McDonald, CPA Shareholder, MHM 813.316.4051 | [email protected] Tracey has extensive audit experience with clients in a number of industries including not-for-profit organizations, manufacturing, distribution, employee leasing, food service, professional employee organizations and healthcare. In addition, she has substantial knowledge of the reporting requirements for employee benefit plans, OMB A-133 and HUD audits.

Morgan Padgett, CPA Shareholder, MHM 785.272.3176 | [email protected] Morgan has several years of experience working with a variety of clients including not-for-profit organizations, governmental entities and construction contractors. She has extensive experience in providing accounting services to not-for-profit clients and in managing financial statement audits of not-for-profit organizations.

6 #CBIZMHMwebinar

Today’s Presenters

Michelle Spriggs, CPA Shareholder, MHM 774.206.8336 | [email protected] Michelle is a Shareholder in the Firm’s Not-For-Profit and Higher Education Audit Practice. Michelle is the not-for-profit subject matter expert in the Firm’s National Professional Standards Group. She has over 20 years of audit experience and is solely dedicated to serving not-for-profit organizations. Her experience includes managing financial statement and OMB Circular A-133 audits; assisting in bond offerings; providing recommendations on internal controls; and training other accounting and auditing professionals to provide support to not-for-profit clients.

7 #CBIZMHMwebinar

Today’s Agenda

1

2

Changes to Accounting Standards – What to Expect This Year

New Uniform Grant Guidance for Federal Awards

The New COSO Internal Control Model 3

4

Changes to Accounting Standards – What to Expect Going Forward 5

6

The New NFP Reporting Model

Questions & Answers

CHANGES TO ACCOUNTING STANDARDS – WHAT TO EXPECT

THIS YEAR

9 #CBIZMHMwebinar #CBIZMHMwebinar

Services Received from Personnel of an Affiliate - FASB ASU No. 2013-06

Clarifies the guidance that not-for-profit entities apply for recognizing and measuring services received from personnel of an affiliate Services provided by personnel of an affiliate under direct

supervision of the recipient not-for-profit Shared services of an affiliate group

that the recipient would have to purchase if they were not provided

Affiliated Services

10 #CBIZMHMwebinar #CBIZMHMwebinar

How services from affiliates should be measured: At the cost recognized by the affiliate for the personnel

providing the services If recognizing at cost will significantly overstate the value of

the services received, then recipient NFP may elect to recognize at either: Cost recognized by affiliate for the

personnel providing the service, or Fair value of the service

Affiliated Services

11 #CBIZMHMwebinar #CBIZMHMwebinar

Financial statement presentation If Health Care Entity, report the services as an equity

transfer from the affiliate and increase in net assets. All others:

Increase in contribution revenue Corresponding decrease in net assets (expense or asset)

Effective for fiscal years beginning after June 15, 2014 (i.e. June 30, 2015 and after)

Affiliated Services

NEW UNIFORM GRANT GUIDANCE FOR FEDERAL AWARDS

13 #CBIZMHMwebinar #CBIZMHMwebinar

OMB Grant Reform – Chronology

Presidential Direction

(Executive Order; Memorandum to

Agencies)

2/28/12 –

Advance Notice of Proposed Guidance

2/1/13 –

Notice of Proposed Guidance

(Rulemaking)

12/26/13 –

Issue of Final

Guidance (2 CFR Part

200)

6/26/14 –

Federal Agency Draft

Regulations to OMB

12/26/14 –

Uniform Adoption by All Federal Agencies

Fiscal years

beginning after

12/26/14 –

Single Audit Requirement (Subpart F)

Applies

14 #CBIZMHMwebinar #CBIZMHMwebinar

OMB Grant Reform – Intent

Consolidate

Simplicity

Streamline

Consistency

15 #CBIZMHMwebinar #CBIZMHMwebinar

• Must implement policies and procedures by promulgating regulations

• Effective December 26, 2014

Federal Agencies

• Will need to implement the new Administrative Requirements and Cost Principles

• All NEW Federal awards and ADDITIONAL funding to existing awards made after December 26, 2014

Non-Federal Entities

• Effective for fiscal years beginning on or after December 26, 2014

• 12/31/15, 6/30/16

Audit Requirements

Key Effective Dates

Early implementation is NOT permitted!

16 #CBIZMHMwebinar #CBIZMHMwebinar

OMB Grant Reform – Changes

Hello • Uniform Administrative Requirements, Cost Principles,

and Audit Requirements for Federal Awards • UARCPARFA • Super Circular • Omni Circular • Uniform Grant Guidance (OMB preference)

Goodbye • Administrative requirements: • A-102 State & Local Government • A-110 Colleges, Universities and Not-for-profits • A-89 Catalog of Federal Domestic Assistance

• Cost circulars: • A-21 Colleges & Universities • A-87 State & Local Government • A-122 Not-for-profits

• A-133

17 #CBIZMHMwebinar #CBIZMHMwebinar

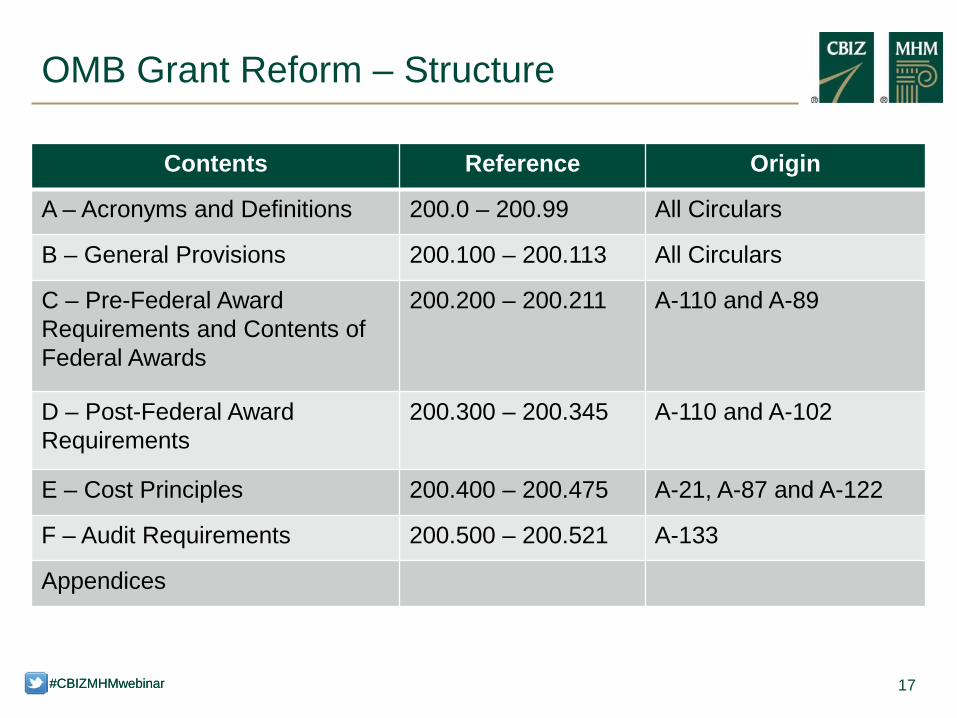

OMB Grant Reform – Structure

Contents Reference Origin

A – Acronyms and Definitions 200.0 – 200.99 All Circulars

B – General Provisions 200.100 – 200.113 All Circulars

C – Pre-Federal Award Requirements and Contents of Federal Awards

200.200 – 200.211 A-110 and A-89

D – Post-Federal Award Requirements

200.300 – 200.345 A-110 and A-102

E – Cost Principles 200.400 – 200.475 A-21, A-87 and A-122

F – Audit Requirements 200.500 – 200.521 A-133

Appendices

18 #CBIZMHMwebinar

OMB Grant Reform – Changes to Subpart F

Final Changes to A-133 Audits – Effective for December 31, 2015 Year-Ends Impact

Single audit threshold to increase from $500,000 to $750,000

Allows for relief for entities doing modest business from federally derived funds.

Type A/B program minimum threshold increase from $300,000 to $750,000

May reduce the number of programs considered major in an audit and therefore fewer programs audited.

Major program determination focus on areas with internal control deficiencies that have been identified as material weaknesses

Entities with strong internal controls and few audit findings could have fewer high-risk Type A programs and fewer programs audited.

19 #CBIZMHMwebinar

Final Changes to A-133 Audits – Effective for December 31, 2015 Year-Ends Impact

Percentage of audit coverage decrease from 25% to 20% for low-risk auditee and 50% to 40% for high-risk auditee

Could reduce the number of programs considered major in an audit.

Threshold for reporting questioned costs to increase from $10,000 to $25,000

Could reduce the number of reported findings but more detail would be required for reported findings.

Further changes to the compliance requirements required for audit are being considered by OMB

We will keep you updated on developments; expecting guidance in summer/fall of 2015.

OMB Grant Reform – Changes to Subpart F

20 #CBIZMHMwebinar

2 CFR 200 – Subpart E

2 CFR 200.400 – 475 Applicable to States, Local Governments, Tribal

Governments, Colleges and Universities and Nonprofit Organizations

Not applicable to Commercial Organizations and Hospitals Maybe later

The New Cost Principles “Package”

21 #CBIZMHMwebinar

421 Advertising and public relations

423 Alcoholic beverages 424 Alumni(ae) activities 425 Audit services 426 Bad debts 429 Commencement and

convocation costs 445 Goods and services for

personal use

Cost Principles with Little or No Change

450 Lobbying 455 Organization costs 457 Plant and homeland

security costs 458 Pre-award costs 459 Professional service

costs 467 Selling and marketing

costs 469 Student activity costs

22 #CBIZMHMwebinar

427 Bonding costs 430 Compensation –

personal services 431 Compensation – fringe

benefits 433 Contingency provisions 434 Contributions and

donations 436 Depreciation 437 Employee morale,

health and welfare costs

Cost Principles with Changes

439 Equipment and other capital expenditures

441 Fines, penalties, damages and other settlements

447 Insurance and indemnification

449 Interest 453 Materials and supplies

costs, including costs of computing devices

454 Memberships, subscriptions, and professional activity costs

23 #CBIZMHMwebinar

460 Proposal costs 461 Publication and printing

costs 462 Rearrangement and

reconversion costs 463 Recruiting costs 464 Relocation of

employees 465 Rental costs of real

property and equipment

Cost Principles with Changes

468 Specialized service facilities

470 Taxes (including Value Added Taxes)

471 Termination costs 472 Training and education 474 Travel

24 #CBIZMHMwebinar #CBIZMHMwebinar

Purpose was to reduce the administrative burden of documenting time and effort

More principles-based (e.g., removed A-21 examples) Less prescriptive on documentation and places more

emphasis on internal controls over personnel-related costs

Compensation – Personal Services (200.430)

24

25 #CBIZMHMwebinar #CBIZMHMwebinar

Four standards for documentation of personnel expenses Charges for salaries must be based on records that

accurately reflect the work performed Must be supported by a system of internal controls which

provides reasonable assurance the amounts charged are accurate, allowable and properly allocated

Be incorporated into official records Reasonably reflect total activity for which employee is

compensated

Compensation – Personal Services (200.430)

25

26 #CBIZMHMwebinar

Use allowance no longer allowed

No depreciation on assets that are fully depreciated

New: depreciation over life of the asset

Depreciation (200.436)

27 #CBIZMHMwebinar

Computing devices do not meet the threshold requirement so are considered supplies Tablets

Laptops

Smartphones

Lesser of $5,000 or entity capitalization threshold Revisit policy if below this amount

Equipment and Other Capital Expenditures (200.439)

28 #CBIZMHMwebinar

Allowable as an indirect cost Preparing proposals for both Federal and non-Federal Successful and not successful bids Allocated to all activities of the organization

This was in college and university and government cost circulars, but not NFP.

Thank you OMB!

Proposal Costs (200.460)

29 #CBIZMHMwebinar

Salaries of administrative and clerical staff are normally treated as indirect unless all of the following are met (200.413(c)):

1. Such services are integral to the activity 2. Individuals can be specifically identified with the activity 3. Such costs are explicitly included in the budget or have prior

written approval 4. Costs not also recovered as indirect

Key Changes to Indirect Costs – Subpart E

30 #CBIZMHMwebinar

More changes in Section 200.414:

Mandating (or encouraging) indirect charging of certain allowable costs Administrative support

Proposal costs

Audit services

Required recognition by federal agencies of federally negotiated rates Enforcement of long standing policy

No more side deals

Key Changes to Indirect Costs – Subpart E

31 #CBIZMHMwebinar

More changes in Section 200.414 – Continued:

Introduction of de minimis 10% rate in lieu of negotiation Good if don’t want to deal with rate negotiation

Authorization to continue use of a negotiated rate for up to four years Don’t have to go through rate finalization every year

Key Changes to Indirect Costs – Subpart E

32 #CBIZMHMwebinar

More changes in Section 200.414 – Continued:

Procedures for recognition of subrecipient indirect costs Recognize Federally negotiated rates

Permit use of 10% de minimis rate

Small organizations without negotiated indirect cost rates now have mechanism to get indirect costs reimbursed

Must be addressed in subgrant agreement

Key Changes to Indirect Costs – Subpart E

33 #CBIZMHMwebinar

Similar in A-87 but not A-21 or A-122 Certification on annual and final fiscal reports or

vouchers requesting payment Assurance that expenditures are proper and in accordance with the

terms and conditions of the federal award and approved budget

Required on EVERY voucher requesting payment? Does this apply to drawdowns also?

Required Certifications – Subpart E (200.415)

34 #CBIZMHMwebinar

Signed by an official who is authorized to legally bind the entity Who will be designated at the organization?

CFO? CEO?

Organizations should start thinking about this

Subject to criminal, civil or administrative penalties for fraud, false statements or false claims

Required Certifications – Subpart E (200.415

35 #CBIZMHMwebinar

Mandatory disclosures An entity must disclose in writing in a timely manner to a

federal agency or pass-through: All violations of federal criminal law involving fraud, bribery

or gratuity violations potentially affecting the Federal award What constitutes in writing? What is timely manner? What if organization doesn’t have gratuity policy? No mention of materiality

Changes to Subpart B General Provisions (200.113)

36 #CBIZMHMwebinar #CBIZMHMwebinar

The Entity MUST establish and maintain effective internal control over Federal awards.

The internal controls SHOULD be in compliance with guidance in:

“Standards for Internal Control in the Federal Government” issued by the Comptroller General of the US - Green Book

“Internal Control Integrated Framework” issued by the Committee of Sponsoring Organizations of the Treadway Commission - COSO

Internal Controls – Subpart D Post-Award Requirements (200.303)

37 #CBIZMHMwebinar

Now five procurement methods 1. Micro-purchases Acquisition of supplies or services value not to exceed

$3,000 Awarded without soliciting competitive quotations if price

is considered reasonable 2. Small purchase procedures Subject to simplified acquisition threshold ($150,000) Price or rate quotations must be obtained from an

adequate number of qualified sources Adequate number not defined

Procurement – Subpart D Post-Award Requirements (200.320)

38 #CBIZMHMwebinar

Now five procurement methods - continued 3. Procurement by sealed bids Publicly solicited Fixed price contract awarded to lowest bidder Preferred for procuring construction

Procurement – Subpart D (200.320)

39 #CBIZMHMwebinar

Now five procurement methods - continued 4. Competitive proposals Must follow these requirements: RFP must be publicized Proposals solicited from adequate number of

qualified sources Organization must have written method for

conducting evaluation of proposals received Contract awarded to the firm with proposal most

advantageous to the program – price and other factors considered

Doesn’t need to be lowest price

Procurement – Subpart D (200.320)

40 #CBIZMHMwebinar

Now five procurement methods - continued 5. Noncompetitive proposals ONLY appropriate when: Goods or services only available from a single

source There is public emergency After soliciting number of sources competition is

deemed inadequate NEW: Awarding agency expressly authorized

noncompetitive proposals in response to written request from organization

Just naming a vendor in a grant or budget isn’t enough

Procurement – Subpart D (200.320)

41 #CBIZMHMwebinar

Subrecipient Relationship An assistance relationship Determines eligibility Performance measured against

federal program objectives Responsible for programmatic

decision-making Adheres to applicable federal

program requirements Uses federal funds to carry out a

program for a public purpose specified in statute, as opposed to providing goods or services for the benefit of the pass-through entities

Contractor (Vendor) Relationship A procurement relationship Provides goods and services within

normal business operations Provides similar goods and services

to many purchasers Normally operates in a competitive

environment Provides goods or services that are

ancillary to the federal program Not subject to compliance

requirements of the federal program

Subrecipient Monitoring – Subpart D Post-Award Requirements (200.330-332)

Distinguishing Between Subrecipient and Contractor

42 #CBIZMHMwebinar

Requirements of pre-award assessment of subrecipients: Subrecipients prior award experience Subrecipients prior audit experience Subrecipients staffing and systems Extent of any federal (or pass-through) entity monitoring

Subrecipient Monitoring – Subpart D (200.330-332)

43 #CBIZMHMwebinar

Post-award subrecipient monitoring mandatory steps: Review financial and performance reports Verify single-audit compliance (presumably using data gathered during

the pre-award stage) Ensure corrective action on any deficiencies, regardless of how they

are disclosed Issue management decisions on relevant subrecipient audit findings Consider whether audit results or other factors necessitate adjustment

to pass-through entity records Consider whether enforcement actions are necessary

Subrecipient Monitoring – Subpart D (200.330-332)

44 #CBIZMHMwebinar

All these documents can be found at http://www.whitehouse.gov/omb/grants_docs

Uniform Administrative Requirements, Cost Principles and Audit Requirements for Federal Awards - 2 CFR 200 http://www.ecfr.gov/cgi-bin/text-idx?SID=d6d9a62155484b2fb6176d7d01a640cc&node=2:1.1.2.2.1&rgn=div5

Links to Helpful Documents

45 #CBIZMHMwebinar

Uniform Guidance Cost Principles Text Comparisons http://www.whitehouse.gov/sites/default/files/omb/fedreg/2013/uniform-guidance-cost-principles-requirements-text-comparison.pdf

Uniform Guidance Audit Requirements Text Comparisons http://www.whitehouse.gov/sites/default/files/omb/fedreg/2013/uniform-guidance-audit-requirements-text-comparison.pdf

Links to Helpful Documents

46 #CBIZMHMwebinar

Uniform Guidance Administrative Requirements Text Comparisons http://www.whitehouse.gov/sites/default/files/omb/fedreg/2013/uniform_guidance_administrative_requirements_text_comparison.pdf

COFAR’s FAQ for New Uniform Guidance on 2 CFR 200 https://cfo.gov/wp-content/uploads/2013/01/2-C.F.R.-200-FAQs-2-12-2014.pdf

E-mail COFAR at [email protected]

Links to Helpful Documents

47 #CBIZMHMwebinar

There is no substitute for a “deep dive”

Review 2 CFR 200 and COSO Monitor OMB and federal agency actions

Stay tuned for OMB’s plans for changes to the Compliance Supplement

Subscribe to our monthly e-newsletter

What To Do Now

48 #CBIZMHMwebinar #CBIZMHMwebinar

Create a team across all applicable divisions of the organization Inventory of current policies and procedures Review current Uniform Grant Guidance and COSO Assessment of changes to significant processes and internal

controls, or affirm no changes needed Make changes to policies, as necessary Implement procedures and controls Train personnel Get early buy-in from auditors Monitor compliance

What To Do Now

48

THE NEW COSO INTERNAL CONTROL MODEL

50 #CBIZMHMwebinar

The Committee of Sponsoring Organizations of the Treadway Commission (COSO) is a joint initiative of five sponsoring organizations formed in 1985

Provides thought leadership through the development of frameworks and guidance on: Internal control Enterprise risk management Fraud

Designed to improve organization performance and governance and to reduce the extent of fraud in organizations

Release original Internal Control-Integrated Framework in 1992 which has become one of the most widely used control frameworks

Revised in 2013 – consists of 17 principles and 81 points of focus

What is COSO 2013?

51 #CBIZMHMwebinar

Update expected to increase ease of use and broaden application

Updated COSO Framework

What is not changing... What is changing...

• Core definition of internal control

• Three categories of objectives and five components of internal control

• Each of the five components of internal control are required for effective internal control

• Important role of judgment in designing, implementing and conducting internal control, and in assessing its effectiveness

• Changes in business and operating

environments considered

• Operations and reporting objectives expanded

• Fundamental concepts underlying five components articulated as principles

• Additional approaches and examples relevant to operations, compliance, and non-financial reporting objectives added

52 #CBIZMHMwebinar

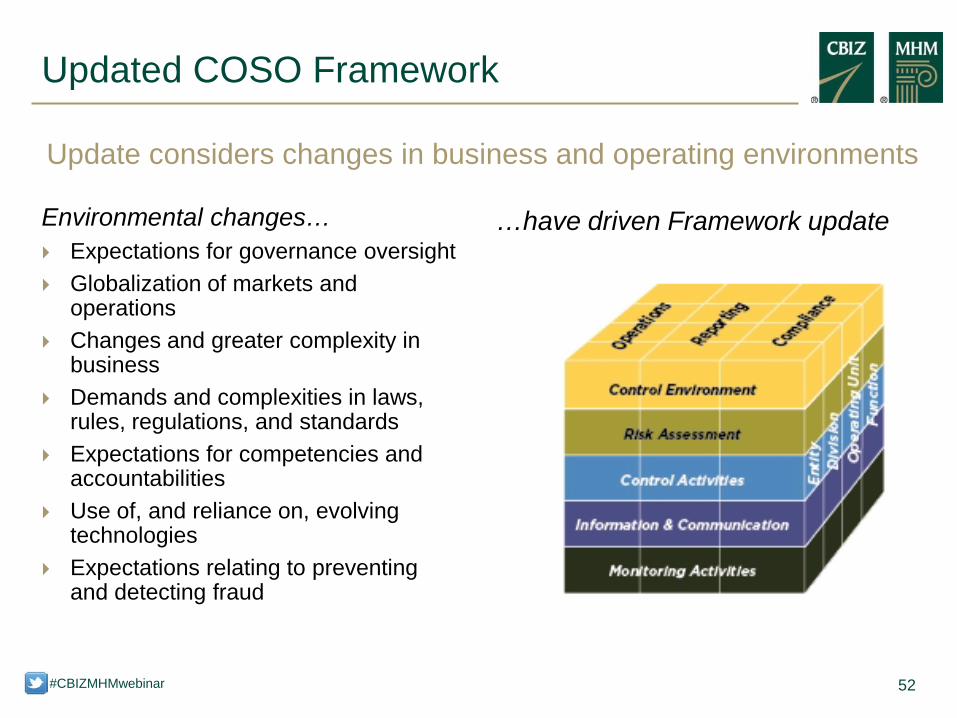

Update considers changes in business and operating environments

Environmental changes… Expectations for governance oversight Globalization of markets and

operations Changes and greater complexity in

business Demands and complexities in laws,

rules, regulations, and standards Expectations for competencies and

accountabilities Use of, and reliance on, evolving

technologies Expectations relating to preventing

and detecting fraud

…have driven Framework update

Updated COSO Framework

53 #CBIZMHMwebinar

Control Environment 1. Demonstrates commitment to integrity an ethical values 2. Exercises oversight responsibility 3. Establishes structure, authority and responsibility 4. Demonstrates commitment to competence 5. Enforces accountability

Risk Assessment 6. Specified suitable objectives 7. Identifies and analyzes risk 8. Assesses fraud risk 9. Identifies and analyzes significant change

Control Activities 10. Selects and develops control activities 11. Selects and develops general controls over technology 12. Deploys through policies and procedures

Information & Communication

13. Uses relevant information 14. Communicates internally 15. Communicates externally’

Monitoring Activities 16. Conducts ongoing and/or separate evaluations 17. Evaluates and communicates deficiencies.

Updated COSO Framework – 17 Principles

54 #CBIZMHMwebinar

Update describes important characteristics or principles, e.g.,

Control Environment 1. Organization demonstrates a commitment to integrity and ethical values Points of focus: • Sets the Tone at the Top • Establishes Standards of Conduct • Evaluates Adherence to Standards of Conduct • Addresses Deviations in a Timely Manner

Updated COSO Framework

• Points of focus may not be suitable or relevant, and others may be identified • Points of focus may facilitate designing, implementing and conducting internal

control • There is no requirement to separately assess whether points of focus are in

place

55 #CBIZMHMwebinar

Updated COSO Framework

Transition & Impact Users are encouraged to

transition applications and related documentation to the updated Framework as soon as feasible

Updated Framework will supersede original Framework at the end of the transition period (i.e., December 15, 2014)

56 #CBIZMHMwebinar

Use and reliance on evolving technologies was a main driver in the framework update

“COSO In the Cyber Age” – thought leadership piece published January 2015

2013 COSO framework provides an effective and efficient approach to evaluating and managing risks related by cyber security

COSO and Cyber Security

57 #CBIZMHMwebinar

Result – information asset inventory, gap analysis and prioritized controls to be implemented

COSO and Cyber Security

• Identify information categories based on business and Organization objectives using the following as a guide: ― Corporate Policies ― Industry Standards (e.g.,

ISO) ― Regulatory Requirements ― Business Objectives ― Intellectual Property ― Financials ― Customer or Employee

Data

• Identify how information is collected, used, transferred stored and archived

• Identify business, system and application owners for information assets

• Create data flows to understand how information moves within business process, systems and applications

• Analyze asset inventories and data flows to identify control risks

• Assess the likely perpetrators of cyber attacks and their likely attack methods

• Identify controls to address identified risks bases on risk profile of the process, system or application

Identify Critical information

Systems

Identify Risks Associated with

Information Systems

Understand Risks Associated with

Information Systems

58 #CBIZMHMwebinar

Don’t forget about third parties or other outsourced service providers! Service auditor reports, or Take steps to understand controls in place by third parties

COSO and Cyber Security

59 #CBIZMHMwebinar

Each principle is suitable for all entities; all principles are assumed relevant Would be rare that a principle is not relevant

Framework does not prescribe controls to be selected, developed and deployed for effective internal control Selection of controls for each principle is based on

management’s judgment based on the entity A deficiency in a component or principle can not be

overcome solely by controls covering other principles or components, however… Selecting, developing and deploying controls to effect

multiple principles may reduce the number of layered-on controls

Implementation of COSO Framework

60 #CBIZMHMwebinar

What you need to do… • Read, understand and train others • Match current controls to

principles • Fill in any gaps and ensure

controls are in writing • Identify key controls for each

principle • Discuss with audit firm

throughout the process

Implementation of COSO Framework

61 #CBIZMHMwebinar

Key questions to ask 1. Are we focused on the right things? 2. Are we proactive or reactive? 3. Are we adapting to change? 4. Do we have the right talent? 5. Are we incentivizing openness and collaboration? 6. Can executive management articulate its risks and

explain its approach and response to such risks?

Implementation of COSO Framework

62 #CBIZMHMwebinar

COSO Publications that might be helpful Internal Control-Integrated Framework (2013 Edition) Executive summary, tools for assessing effectiveness of a

system of internal control

Internal Control over External Financial Reporting: A Compendium of Approaches and Examples Approaches and examples of how principles are applied,

examples from a variety of entities – including not-for-profit organizations

COSO in the Cyber Age

Implementation of COSO Framework

http://www.cpa2biz.com/AST/Main/CPA2BIZ_Primary/InternalControls/COSO/PRDOVR~PC-990026/PC-990026.jsp

THE NEW NFP REPORTING MODEL

64 #CBIZMHMwebinar

Not-for-Profit Advisory Committee

Sep 2011

NAC Recommendations

Nov 2011

Project Added to

FASB Agenda

2012

Project Planning/

Board Education/

Initial Outreach

2013/2014

Deliberations continue

Q2 2015

Exposure

Draft Expected

April 22-August 20, 2015

Comment

Period

TBD

Final ASU

65 #CBIZMHMwebinar

Primary Topics – NFP Reporting Model

Net Asset Classifications

Financial Performance

Reporting of Expenses

Cash Flow Statement Liquidity NFP

Disclosures

66 #CBIZMHMwebinar

Current GAAP

Proposed GAAP

Disclosures

+

* New disclosure requirement

Unrestricted Temp. Restricted Perm. Restricted

Without Donor Restrictions

Amount, purpose, and type of board

designations*

With Donor Restrictions

Nature and amount of donor restrictions

Net Assets

67 #CBIZMHMwebinar

Mission: Based on whether resources are from or directed at carrying out a NFP’s purpose for existence (excludes general investing and financing)

Availability: Based on whether resources are available for current period activities and reflect limits imposed by: - external donors - internal actions of a NFP’s governing board

Defined a required intermediate operating measure for all NFPs – based on two dimensions:

Financial Performance

68 #CBIZMHMwebinar

Operating Measures

Present on the face of the statement of activities two subtotals of operating activities associated with changes in net assets without donor restrictions:

Operating excess (deficiency) before

transfers

Amount, purpose, and type of board

designations* Operating excess (deficiency) after

transfers

Operating revenues, support, expenses, gains and losses (all without donor-imposed restrictions) plus releases

Operating excess (deficiency) before transfers plus designations, appropriations, and similar transfers

69 #CBIZMHMwebinar

Temp. Restricted Perm. Restricted

Operating excess before transfers

Amount, purpose, and type of board

designations*

With Donor Restrictions

Nature and amount of donor restrictions

Presentation of Transfers

Governing Board designations, appropriations and similar transfers, if used by the NFP, shall be reported in accordance with the following requirements: All transfers shall be reported in a discrete section on the statement of

activities The discrete section will be presented after operating excess (deficiency)

before transfers and immediately before operating excess (deficiency) after transfers. At a minimum, present aggregated line items for transfers out of operating

activities and transfers into operating activities Note disclosure of the amounts and types of transfers that are

presented in the aggregate is required unless all transfers are presented as discrete line items on the face of the statement

Qualitative disclosures required: Major purposes, amounts and types of board transfers One-time decisions vs. recurring or standing board policies

70 #CBIZMHMwebinar

Other Performance Measure Issues

Release of restriction for long-lived assets Current U.S. GAAP alternatives: When asset placed in service or Over time to match depreciation

Exposure draft: Only permits release of restriction when asset is placed

in service (significant impact for some NFPs).

71 #CBIZMHMwebinar

Financial Performance: Statement Approach

Ability to present total revenue and contributions

Effect of transfers easier to identify

Too much information in one statement

Labeling of totals difficult

Greater emphasis on the operating measure

Facilitates multi-year comparison

Some may ignore the second statement

Incorrectly equate the operating measure to net income

1 Statement

2 Statements Retain

Flexibility

72 #CBIZMHMwebinar

Sample Statement of Activities

Without Donor

RestrictionsWith Donor Restrictions Total

Support and revenues:Contributions and bequests 8,640$ 8,390 17,030 Fees 5,200 5,200 Gains 350 350

Total support and revenue 14,190 22,580

Net assets released from restrictions:Satisfaction of program restrictions 23,240 (23,240) - Satisfaction of equipment acquisition restriction 1,500 (1,500) - Appropriation from donor endowment 7,500 (7,500) -

Total net assets released from restrictions 32,240 Total revenues, gains and other support 46,430

Expenses and losses:Program expenses 27,400 27,400 Supporting services 4,188 4,188

Total expenses 31,588 31,588 Loss from fire damages 80 80

Total expenses and losses 31,668 31,668

Operating excess before transfers 14,762

73 #CBIZMHMwebinar

Sample Statement of Activities – Cont’d Without Donor

RestrictionsWith Donor Restrictions Total

Operating excess before transfers 14,762

Board designations, appropriations and other:Investment returns appropriated from quasi-endowment 2,000 2,000 Transfer of gifted equipment (140) (140) Transfer of equipment acquired with donor-restricted funds and placed in service (1,500) (1,500)

Operating excess after transfers 15,122

Nonoperating Changes:Investment return 4,678 20,272 24,950 Interest expense (382) (382) Actuarial loss on annuity obligations (30) (30)

Board designations, appropriations and other:Investment returns designated for current operations (2,000) (2,000) Transfer of gifted equiupment 140 140 Transfer of equipment acquired with donor-restricted funds and placed in service 1,500 1,500

Increase (decrease) in net assets 19,058 (3,608) 15,450

Net assets at beginning of year 73,619 197,021 270,640 Net assets at end of year 92,677$ 193,413 286,090

74 #CBIZMHMwebinar

Reporting of Expenses

NFP must report information about all expenses in one location (SOA, separate statement, or notes).

Operating expenses shall be presented by their function and by their natural classification.

Non-operating expenses are neither required nor precluded from being reported by function. External and direct internal investment expenses that have

been netted against investment return need not be included in functional expense analysis (disclose the amount of internal salaries and benefits)

75 #CBIZMHMwebinar

Reporting of Expenses

Nonfunctional

Function*Total

Program Services Supporting Services Operating Nonoperating TotalExpenses Program A Program B M&G Fundraising Expenses Expenses Expenses

Salaries and benefitsGrants to othersProfessional feesOccupancy costsEquipment rentalSuppliesTravelPrintingInterestOtherDepreciation

* Either (or both) on face of Statement of Activities

Nature*

Expense by nature and function – one place in the F/S

76 #CBIZMHMwebinar

Changes to Statement of Cash Flows

Direct method for operating cash flows is required Indirect method may be added as supplemental disclosure

Re-categorize certain items to better align with operating activities presented in statement of activities: Purchases of and proceeds on sale of PPE (operating) Cash contributions restricted for PPE (operating) Cash received from interest and dividends (investing) Cash paid for interest on debt (financing)

77 #CBIZMHMwebinar

Cash received from donors Cash received from service recipients

Cash paid to employees

Purchase of property and equipment Cash paid to vendors

Proceeds on sale of property and equipment Contributions restricted for property and equipment

Net cash from operating activities

Cash received from interest and dividends

Proceeds from sale of investments Net cash from investing activities

Net cash from financing activities

Payments of principal on long-term debt Interest paid on long-term debt Contributions restricted for endowment

Net increase in cash Cash at the beginning of year

Cash Flows from Operating Activities

Cash Flows from Investing Activities

Cash Flows from Financing Activities

Cash at end of year

Statement of Cash Flows Sample

Purchase of investment assets

78 #CBIZMHMwebinar

Asset type / debt

maturity

Donor / other external

restrictions and internal limits

Board decisions: Sequencing of items or use of a classified balance sheet Quantitative and qualitative information Additional disclosures (e.g. assets whose use is limited)

Liquidity & Availability

79 #CBIZMHMwebinar

Liquidity Disclosures

Quantitative information about: The total amount of financial assets Amounts that are not available to meet cash needs within the time

horizon because of (1) external limits and (2) internal actions of a governing board

The total amount of financial liabilities that are due within that time horizon.

Qualitative information about how the entity manages its liquidity. For example, an entity might disclose: Its strategy for addressing entity-wide risks that may affect liquidity,

including its use of lines of credit Its policy for establishing liquidity reserves Its basis for determining the time horizon used for managing liquidity.

80 #CBIZMHMwebinar

Revised net asset classification

Enhanced disclosures

To be reflected in net assets with donor restrictions rather than in net assets without donor restrictions

In addition to aggregate amounts by which funds are underwater (current GAAP), also disclose aggregate of original gift amounts (or level required by donor or law) for such funds, fair value, and any governing board policy or decision to reduce or not spend from such funds.

Underwater Endowments

81 #CBIZMHMwebinar

e.g., endowment/ investment/fair

value

e.g., accounting policies

e.g., cost allocation

approaches

Other Disclosure Enhancements

82 #CBIZMHMwebinar

Required to include a description of the method used to allocate costs among program and support functions

Disclose total program expenses and information about why total program expenses disclosed in the notes do not articulate with the statement of activities, if applicable.

Cost Allocation Disclosures

83 #CBIZMHMwebinar

How to present?

What to disclose?

Net presentation of investment expenses against investment return on the face of the statement of activities

Netting limited to external and direct internal expenses

Disclosure of investment expenses no longer required, except for the disclosure of the amount of internal salaries and benefits that have been netted (if any) against investment return

Reporting of Investment Expenses

CHANGES TO ACCOUNTING STANDARDS – WHAT TO EXPECT

GOING FORWARD

85 #CBIZMHMwebinar

FASB Accounting Standard Update (ASU) 2014-09 – Revenue from Contracts with Customers (Topic 606)

Fundamental principle: An entity must recognize revenue in a manner that

represents the entity’s transfer of goods or services to customers, measured at the amount that reflects the consideration the entity expects to receive from the exchange.

Revenue Recognition

86 #CBIZMHMwebinar

Five-step model: 1. Identify contract(s) with customer 2. Identify separate performance obligations in the contract(s) 3. Determine the transaction price 4. Allocate the transaction price 5. Recognize revenue when the

performance obligation is satisfied

Revenue Recognition

87 #CBIZMHMwebinar

Definitions Customer: a party that has contracted with a company

(organization) to obtain a good or service that is an output of the company's ordinary activities in exchange for consideration

Revenue Recognition

88 #CBIZMHMwebinar

Potential Impact on Not-for-Profits Only applies to exchange transactions (not investment

income, etc.) Many transactions of NFPs do not involve a vendor-customer

relationship and are not within scope of the ASU – no transfer of good or service to a customer

Contributions are scoped out of ASU by definition – voluntary and nonreciprocal

Grants and collaborative arrangements – Assess on a case by case basis

Nature of the agreement Are goods and services part of the not-for-profit entities ordinary

activities

Revenue Recognition

89 #CBIZMHMwebinar

Potential Impact on Not-for-Profits Grants – typically arrangements under which funds are

provided to the organization to fulfill mutually agreeable goals that are in keeping with the organization’s mission Performance of research vs. creation of an output with commercial

value Collaborative arrangement – both parties share in the risks

and rewards associated with the commercial success of a venture Is there a contract to obtain the output of the entity's ordinary

activities? Sponsored arrangements – implementation is unclear

Not meet definition of contribution, grant or collaborative arrangement.

Revenue Recognition

90 #CBIZMHMwebinar

Potential Impact on Not-for-Profits Revenue streams that could be considered revenue from

contracts with customers: Minimal impact for those contracts entered into that have a short-term

Revenue Recognition

Memberships Conferences and seminars Subscriptions Tuition

Products and services Advertising Royalty agreements Licensing

Sponsorships Federal and state grants and contracts

91 #CBIZMHMwebinar

Potential Impact on Not-for-Profits Likely enhanced disclosures

Allow users to understand the nature, amount, timing and uncertainty of revenue and cash flows from contracts with customers

Practical expedients have been provided for some disclosure requirements (e.g. exclusion of certain disclosures of contracts with durations of one year or less)

Revenue Recognition

92 #CBIZMHMwebinar

Steps for implementation: 1) Inventory all current revenue streams and evaluate if

there are differences in recognition methods 2) Evaluate differences in current and new standards

regarding how contract modifications are addressed 3) Determine if changes are needed to systems,

processes and controls 4) Consider other areas of organization that could be

impacted (e.g. employee incentive based compensation, calculation of debt covenants)

Revenue Recognition

93 #CBIZMHMwebinar

Revenue Recognition

Effective dates (US GAAP) Public entities – first interim

period within annual period beginning on or after December 15, 2016 (2017 calendar year-ends or 2018 fiscal year-ends.

One-year deferral for non-public entities

April 1, 2015 FASB proposed one-year delay on effective date

94 #CBIZMHMwebinar

Stay tuned for additional implementation guidance to be issued FASB Not-for-Profit Advisory Committee and AICPA Not-for-

Profit Entities Revenue Recognition Task Force Accounting Guide on Revenue Recognition is being

developed by AICPA Implementation issues identified:

Tuition discounts Impact on contribution revenue (if any) Grants with deliverables Self-pay patient revenue Sponsored arrangements And others

Revenue Recognition

95 #CBIZMHMwebinar #CBIZMHMwebinar

Lease accounting continues to be a topic for discussion, with continued Exposure Drafts and deliberation

Current status: Exposure draft issued May 2013 and modifications and

clarifications have been made since then Final standard is being drafted to be issued in second half of

2015 Effective date unknown

Will be announced before final standard is issued

Leases

96 #CBIZMHMwebinar #CBIZMHMwebinar

Type A and Type B lease classification Virtually all leases – lessee would recognize a right-of-

use asset and a liability on its balance sheet. Type A (most leases other than real estate):

Asset and liability initially recognized at the present value of lease payments

Recognize and report the interest expense on the lease liability separately from the amortization of the right of use asset

Type B (most real estate leases): Asset and liability initially recognized at the present value of lease

payments Recognize a single lease cost – that combines the interest on the

lease liability with the amortization of the right of use asset – on a straight-line basis

Leases

97 #CBIZMHMwebinar

Implementation No leases will be grandfathered – all operating leases will

need to be considered Even if the lease has less than 12 months remaining at the initial

application date, unless it is a short-term lease No requirement to adjust carrying amounts of assets and liabilities

associated with existing finance or capital leases

Modified retrospective transition approach for leases existing at, or entered into after, the date of initial application Would not apply to leases expired before the date of initial

application

Leases

98 #CBIZMHMwebinar #CBIZMHMwebinar

Effect on Not-for-Profit Organizations Financial statement impact

Increase in total assets and total liabilities Lease payment expense replaced by amortization of right-to-use

asset and interest expense Overall change in net assets Cash flow – financing vs. operating cash out flows

Could have an impact on financial ratios

Slight changes to accounting for lessors as well

Leases

99 #CBIZMHMwebinar #CBIZMHMwebinar

Accounting Standards Update No 2015-01, Simplifying Income Statement Presentation by Eliminating the Concept of Extraordinary Items

No longer requires extraordinary events or transactions to be separately classified, presented and disclosed

FASB retained guidance on items that are unusual or infrequently occurring Presented as separate components of continuing operations, or Disclosed

Effective for 2016 calendar year-end and 2017 fiscal year-ends Can early adopt and apply presentation retroactively

Presentation of Extraordinary Items

100 #CBIZMHMwebinar #CBIZMHMwebinar

FASB proposed ASU Exposure Draft (Issued October 30, 2014 – Comment period ended January 15, 2015)

Removes the requirement to categorize within the fair value hierarchy investments for which fair values are measured at net asset value (NAV) using the practical expedient. Proposed ASU was issued to address diversity in practice in

categorizing investments redeemable at a future date. Criteria used to determine category within the fair value

hierarchy differ from the criteria used to categorize other fair value measurements.

Disclosures for Investment in Certain Entities That Calculate Net Asset Value per Share

101 #CBIZMHMwebinar

The reporting entity that uses NAV per share as a practical expedient shall disclose information that helps users of its financial statements to understand the nature and risks of the investments and whether the investments are probable of being sold at amounts different from NAV per share including: Fair value measurement of the investments in the class

including a description of the investment strategies For nonredeemable investments, the anticipated liquidation

period of the underlying assets of the investee

Disclosure Requirements

102 #CBIZMHMwebinar

The amount of unfunded commitments related to investments in the class

A general description of the terms and conditions upon which an investor may redeem investments in the class

A description of circumstances when investments may or may not be redeemable (when restrictions will lapse)

Plans to sell and any remaining actions needed to complete the sale

Any other significant restrictions

Disclosure Requirements

103 #CBIZMHMwebinar

Customer’s Accounting for Fees Paid in a Cloud Computing Arrangement

Current GAAP doesn’t include explicit guidance about a customer’s accounting for fees paid in a cloud computing arrangement such as: Software as a service Platform as a service Infrastructure as a service Other hosting arrangements

ASU 2015-05 Intangibles – Goodwill and Other – Internal Use Software

104 #CBIZMHMwebinar

Determine whether arrangement includes a software license: Account for the software license element consistent with the

acquisition of software licenses Account for the remainder of the arrangement as a service

contract Effective for annual periods beginning after December 15,

2015 (early adoption is permitted). May elect to adopt the amendments either prospectively or

retrospectively (required disclosures about the effect of the accounting change).

Fees Paid in a Cloud Computing Arrangement

105 #CBIZMHMwebinar

Questions?

106 #CBIZMHMwebinar

Join us for these upcoming courses: 6/9 & 6/18: Perspectives from the CFO of Charity Navigator 6/10 & 7/8: How DOL Enforcement and Recent Litigation is

Impacting Your Employee Benefit Plan 6/30 & 7/7: Second Quarter Accounting Update

Subscribe to our Newsletter: Not-for-Profit Viewpoint

If You Enjoyed This Webinar…

107 #CBIZMHMwebinar

Connect with Us

linkedin.com/company/ mayer-hoffman-mccann-p.c.

@mhm_pc

youtube.com/ mayerhoffmanmccann

slideshare.net/mhmpc

linkedin.com/company/ cbiz-mhm-llc

@cbizmhm

youtube.com/user/BizTipsVideos

slideshare.net/CBIZInc

MHM CBIZ

Related Documents