Barcelona, Spain • October 29-31, 2013 © 2014Parker, Van Alstyne & Choudary Webinar: Alternative business models around Distributed Energy Resources Geoffrey Parker Director, Tulane Energy Institute Fellow, MIT Center for Digital Business [email protected], [email protected] @g2parker The Rise of Networks and Platforms

Webinar: Alternative Business Models for Distributed Energy Resources

Aug 08, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Barcelona, Spain • October 29-31, 2013

© 2014Parker, Van Alstyne & Choudary

Webinar: Alternative business models around Distributed Energy Resources

Geoffrey ParkerDirector, Tulane Energy InstituteFellow, MIT Center for Digital [email protected], [email protected]@g2parker

The Rise of Networks and Platforms

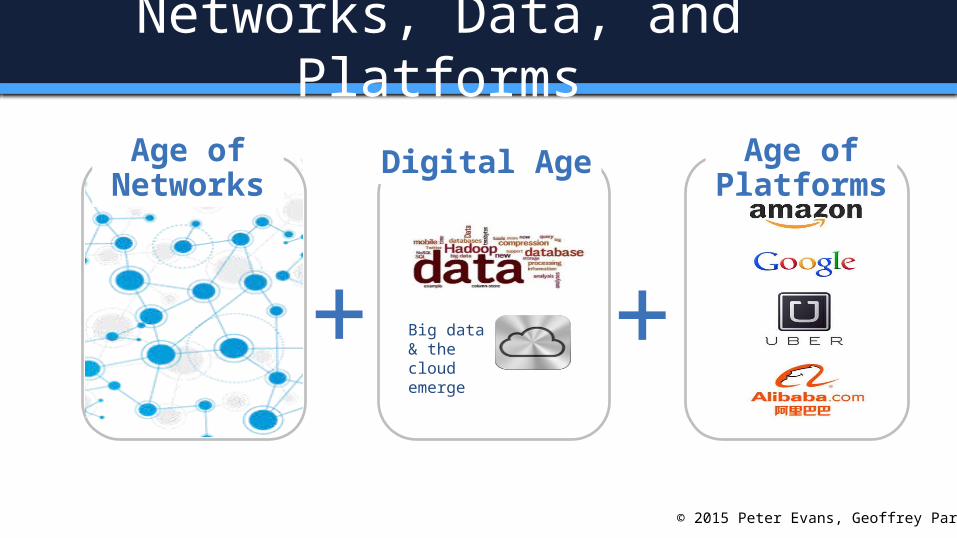

+ Big data & the cloud emerge

Digital Age Age of Platforms

+

Age of Networks

Networks, Data, and Platforms

© 2015 Peter Evans, Geoffrey Parker

Age of Networks

Source: GE, Global Strategy and Planning, 2013

Land-based pipelines networks

Expanding global gas pipeline network

547 bcm of LNG traded42 buyers, 25 sellers

Source: P. Evans and Mike Farina, Age of Gas and the Power of Networks, GE, 2013

LNG trade… a view to 2020

Expanding global gas pipeline network

Strategically located liquefaction plant

investment of $15 to $20 billion could

displace up to 30% of transport diesel

Fueling infrastructure a key to linking networks

Micro-LNG plantNatural gas

liquefaction plant producing up to

250,000 gallons per day

Sources: EIA, Office of Oil & Gas and CSX, 2013

Rail + natural gas + trucking

Expanding network synergies

© 2015 Peter Evans, Geoffrey Parker

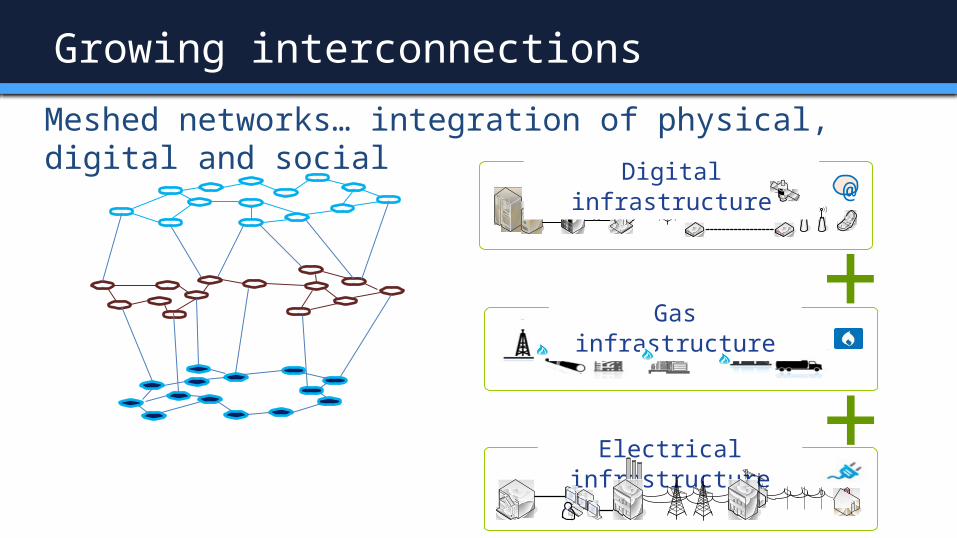

Meshed networks… integration of physical, digital and social

Electrical infrastructure

+Gas infrastructure +

Digital infrastructure@

Growing interconnections

Digital Age

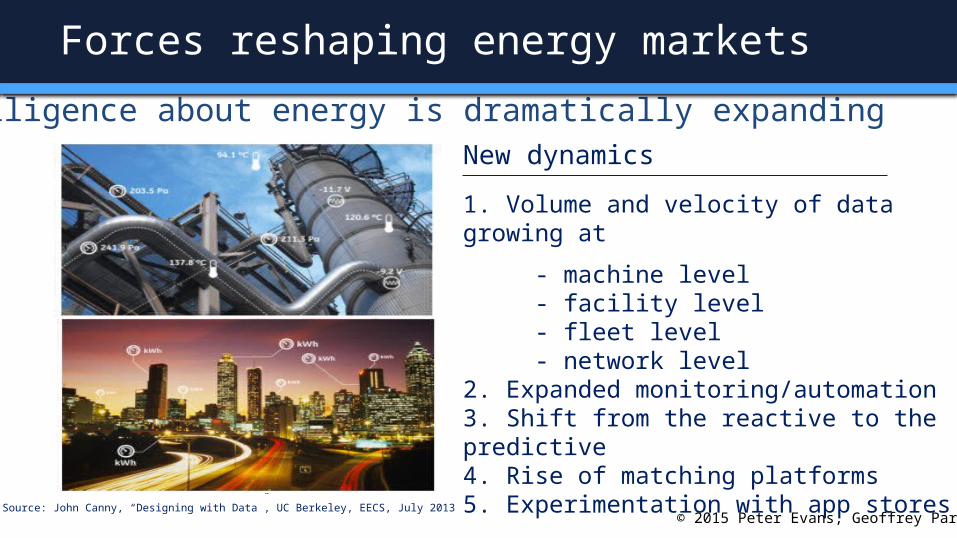

Intelligence about energy is dramatically expanding

Source: John Canny, “Designing with Data”, UC Berkeley, EECS, July 2013

New dynamics

1. Volume and velocity of data growing at

- machine level - facility level - fleet level - network level 2. Expanded monitoring/automation3. Shift from the reactive to the predictive 4. Rise of matching platforms5. Experimentation with app stores

Forces reshaping energy markets

© 2015 Peter Evans, Geoffrey Parker

10

Applications of the industrial internet

© 2015 Peter Evans, Geoffrey Parker

FUEL (group)

Natural Gas

Coal

Nuclear

Hydro

Wind

Oil

Biomass

Solar

Geothermal

Other

US power plant fleet

Data source: Platts, 2013

6,670* Natural gas plants

• less down time• better fuel economy• Improved system

coordination

Digital benefits

* Out of a total of 23,290 power plants

Improved asset productivity

© 2015 Peter Evans, Geoffrey Parker

Digital technologies will augment field service engineers

Source: P. Evans, “Big Data Innovation Summit,” Boston, MA, September 2013

Transformation of work & the Crew Change

© 2015 Peter Evans, Geoffrey Parker

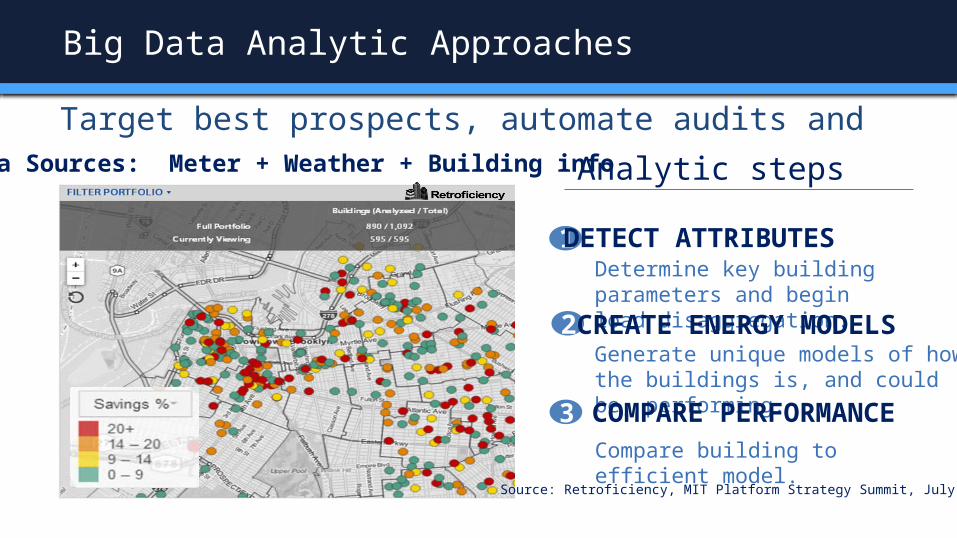

1Determine key building parameters and begin load disaggregation.

DETECT ATTRIBUTES

Generate unique models of how the buildings is, and could be, performing.

2 CREATE ENERGY MODELS

Compare building to efficient model.

3 COMPARE PERFORMANCE

Target best prospects, automate audits and track efficiency savingsData Sources: Meter + Weather + Building info

Source: Retroficiency, MIT Platform Strategy Summit, July 2014

Analytic steps

Big Data Analytic Approaches

Age of Platforms

Platform companies are found in a growing number of industries

Source: CGE Platform Database, 2014

Companies Sectors

Platforms… new business models

© 2015 Peter Evans, Geoffrey Parker

Platform providerComponents Rules Architecture

UsersDemand side

UsersSupply side

Match service providers to customers

Source: Eisenmann, Parker, Van Alstyne 2009

Leverage networks

Mobile Device Platform Ecosystem

Source: Rahul Basole, 2009

Digital enables platforms

© 2015 Peter Evans, Geoffrey Parker

17

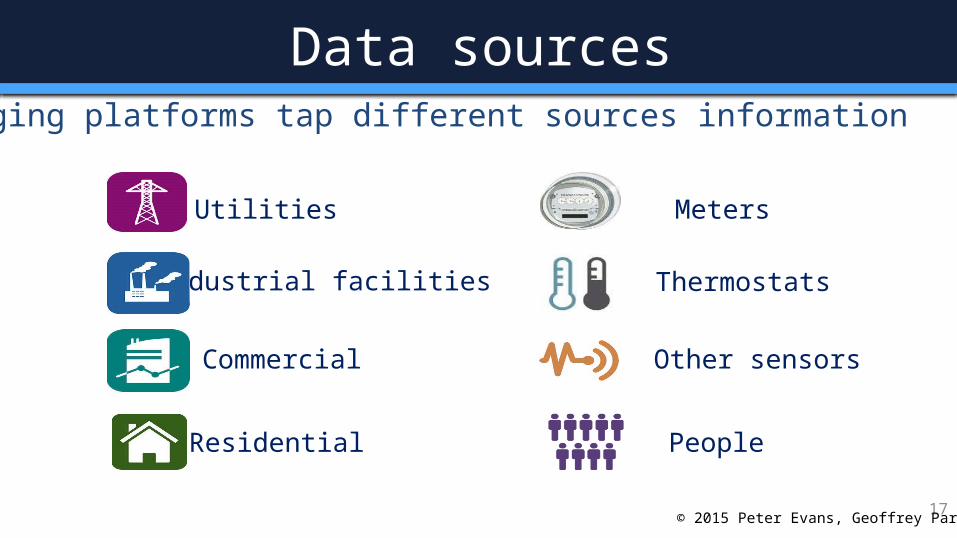

Utilities

Industrial facilities

Commercial

Residential

Emerging platforms tap different sources information

Meters

Other sensors

Thermostats

People

Data sources

© 2015 Peter Evans, Geoffrey Parker

Variability of Wind, Solar, GeoThermal

CAISO data August 2008

Traditional Response

Platform providerComponents Rules Architecture

Consumer Users

Supply sideUsers

User Flexibility Meets Distributed Energy Resource Variability

Supply Side participates:• Storage• Load shift• Micro generation

Platform coordinates through• DLMPs• Contracts• Financial flows• Technical Standards

One integrated framework for different resource types

Age of Networks

Digital Age

Age of Platforms

New business models that leverage networks

and intelligence

Mesh networks linking physical, digital and social

Surge in information about energy for

insight and improved decision-making

Energy system

Rise of energy intelligence

© 2015 Peter Evans, Geoffrey Parker

Financing DER – Lessons from Home Solar

Webinar: Alternative Business Models for Distributed Energy Resources

April 30, 2015

Sierra PetersonDirector, Business Development

24

What We’ll Cover

1) Context on Clean Power Finance

2) U.S. Residential Solar Market Trends

3) Finance Products for Residential Solar

4) Does Solar’s Success Translate to Storage?

5) Mass Market Demand Drivers: Win on $/kWh

6) Transactive Energy Markets

Proprietary

25

CPF Connects Supply and Demand

Right Financing for the Right Customer

Financial Servicesand Software

for the Residential Solar Industry

Solar IndustrySells, Installs and

Maintains Systems

InvestorsProvide Capital, Own

Assets

PPAs

Proprietary

Leases Loans PACE GEMS

26

Residential Solar Cost and Financing Trends

● Before 2008, most solar was consumer-owned

● Bipartisan approval of ITC in 2008 spurred private capital flows

● Reduced cost of capital and hardware costs

● Galvanized competition, further reducing costs and scaling deployment

Source: GTM Research

27

Home Solar Finance Products: Leases and PPAsLease and Power Purchase Agreement (PPA)

“Third-Party Owned” or TPO Solar

Solar Lease* Solar PPA*

20-year contract 20-year contract

Payments fixed over life of contract Customer pays for electricity the solar system produces

Production guarantee – if consumer doesn’t get power promised, company

pays the difference

No production guarantee – customer only pays for electricity

O&M, insurance and monitoring O&M, insurance and monitoring

*Based on standard contracts from SAPC

28

Home Solar Finance Products: Loans, PACE

Solar Loan Solar PACE Product

20-year contract 20-year contract

Customer makes loan payments over life of contract

Customer pays for cost of system through property taxes

In general, no production guarantee – customer only pays for electricity

No production guarantee

Optional O&M, insurance and monitoring

Optional O&M, insurance and monitoring

Alternatives to TPO Solar Products

Many TPO Companies Sell Loans and PACE

29

Lessons from Solar Financing: Win on $/kWh

● Solar’s $/kWh savings proposition applicable to millions of homeowners

● Early adopters buy energy independence and novel technology

● Mass market buys $/kWh savings

30

Barriers to Mass Market Financing for Storage

Technology- Murky value prop: calculation

of $/kWh value remains complicated

Markets- Static pricing- NEM

- NEM provides pricing signal for value of solar

- Real-time pricing would accurately value solar, storage, other DER

Graphic: Green Living Ideas

Net Energy Metering 101

31

Storage Finance Today: PACE, Purchase & Tesla LeasePACE Tesla Pilot Lease

5+ year contract 10-year contract;battery then returned to SolarCity

Payments fixed over life of contract; repaid on property taxPurchase prices: $10K+

$1500 upfront; $15/month for 10 yearsPurchase price: $13K

Manufacturer-specific warranty 10-year warranty

Optional O&M, insurance and monitoring

O&M, insurance and monitoring

32

Regulatory Framework Trailing Market Trends

20TH CENTURY GRID 21ST CENTURY GRID

Reliable, safe, & least-cost Clean, resilient, & customer choice

Centralized hierarchy & monopoly Decentralized networks & P2P

Cost-plus pricing Value-based pricing

Ratepayers Customers & prosumers

“Waterfall” development & price design set by utilities & regulators

“Agile” development & dynamic pricing determined by markets

33

Solution: Transactive Energy Markets

Power prices should provide:

Transactive energy markets enable new financing mechanisms and properly value costs and benefits of DER and the grid

Flexibility- Signals real-time market conditions - Accurately values DER- Encourages optimization

Use Buy Store

Predictability - Guides investment - Enables planning

Transactive energy markets enable:

- Time-of-Use Rate Arbitrage- Solar & DER Optimization- Grid Services

34

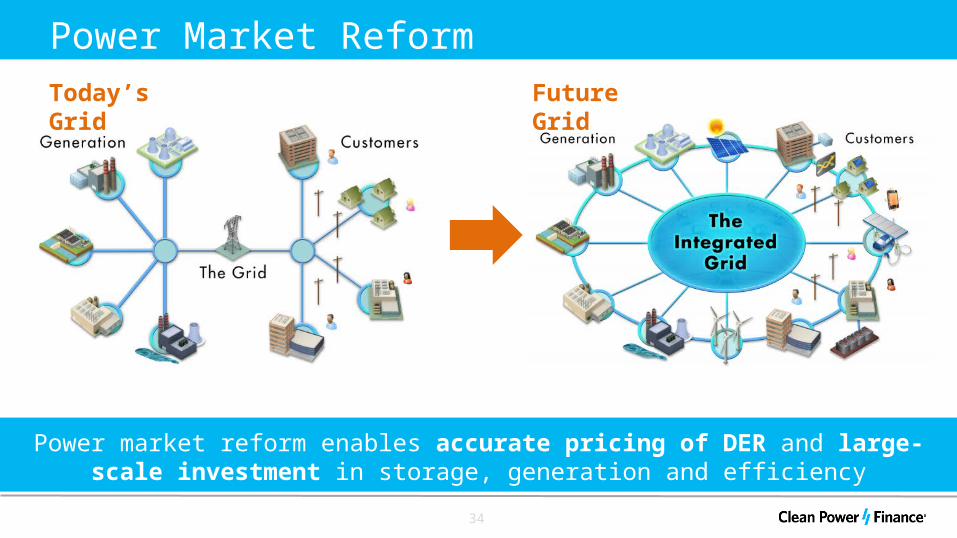

Power Market ReformToday’s Grid Future Grid

Power market reform enables accurate pricing of DER and large-scale investment in storage, generation and efficiency

36

The utility industry is changing

New competition

Rate pressureFlat demand AMI data

Distributedresources Regulation

RISE OF THE

CUSTOMER

The key: transform the utility-customer relationship

37

Right message, right channel, right customer, right moment.

38

DER will result in changing load profiles

New competition

Rate pressureFlat demand AMI data

RISE OF THE

CUSTOMER

Distributedresources Regulation

39

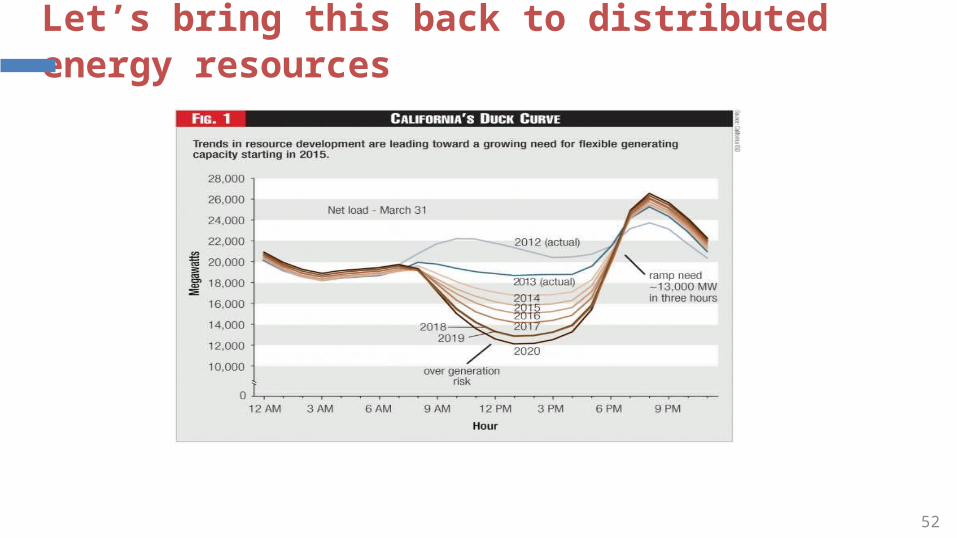

If it looks like a duck, quacks like a duck…

40

To meet this challenge, we first need AMI data

New competition

Rate pressureFlat demand AMI data

RISE OF THE

CUSTOMER

Distributedresources Regulation

41

With big infrastructure investment comes a bit of hype

1990’s: INTERNET IPOs GONE WILD

42

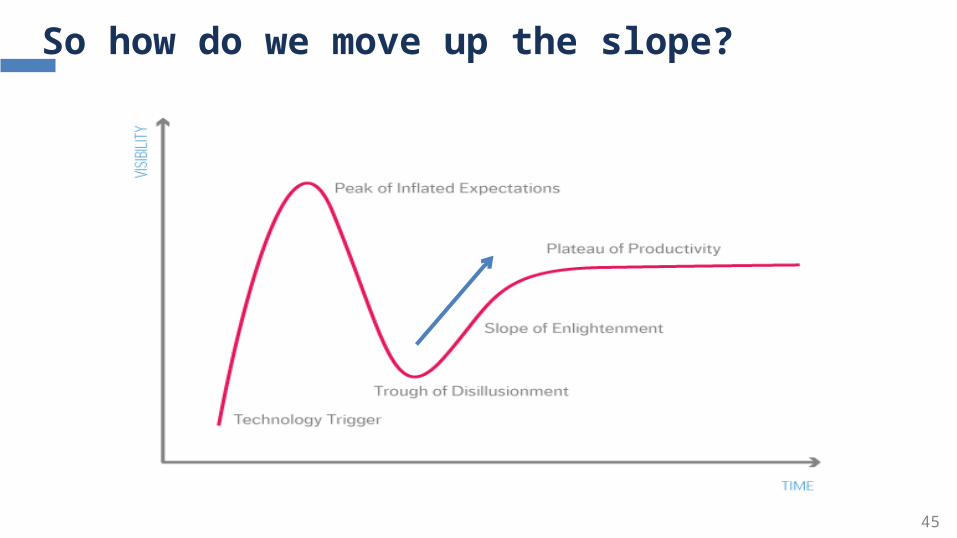

Commonly referred to as the hype cycle

43

This hype cycle has held true for AMI in the US

What does the trough look like?

44

$37M spent to enroll the first 22k customers

77%

of UtilityCo customers would benefit from a CPP rate

1.5%of UtiltyCo’s customers enrolled in CPP Rate

45

So how do we move up the slope?

46

Behavioral Demand Response: 1M HHs, 4 utilities

47

Two flavors: Delivered with or without a price signal

2Peak Reduction

withDynamic Pricing

1Peak Reduction

48

Record temperatures put BDR in the hot seat

49

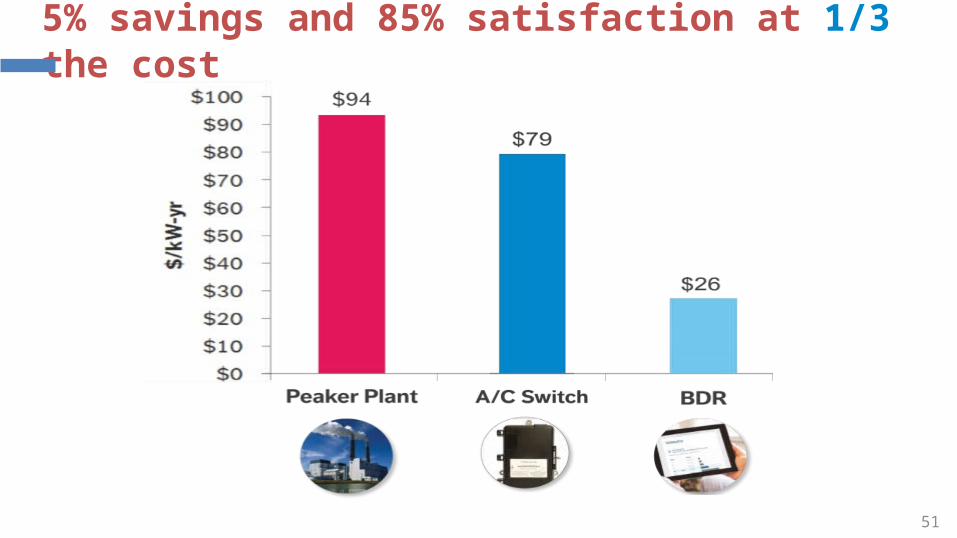

During this heat wave, 5% savings on the peak

50

And 85% of customers were satisfied

Ice Cream The Beach BDR

64%

75%

85%

provides trustworthy EE

information

wants to help me save money

provides useful suggestions to save energy, lower bills

64%49%

58%71%

59% 66%

Control Group Recipient Group

+7% +10% +8%

My Utility….I’m satisfied with…

51

5% savings and 85% satisfaction at 1/3 the cost

52

Let’s bring this back to distributed energy resources

53

Lesson 1: AMI is necessary but insufficient

54

Lesson 2: Utilities are critical to scale in residential

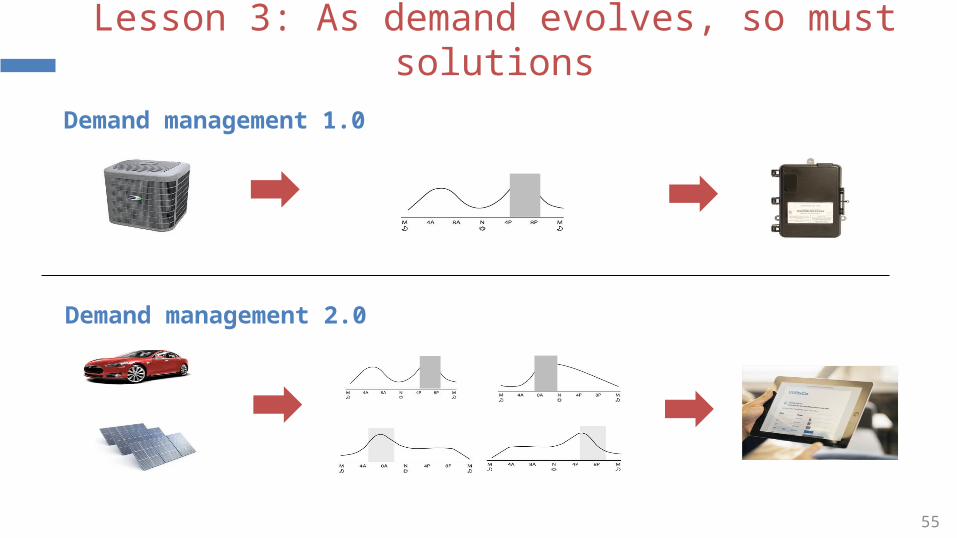

Lesson 3: As demand evolves, so must solutions

55

Demand management 1.0

Demand management 2.0

DNV GL © SAFER, SMARTER, GREENERDNV GL ©

Alternative Business Models for Distributed Energy Resources

56

Business Opportunities & Scenarios

DNV GL ©

Changing the electricity supply value chain

57

Delivery End UseProduction

Delivery

End UseProduction

(Independent Grid)

DNV GL ©

Framing the pieces

58

Utility Distribution

End UseProduction

• Energy Management• Customer-Cited Generation

• Energy Efficiency• Demand Response• Customer Engagement

• DER Distribution TBD Shared services Production aggregation

• DER Wholesale In Progress

DNV GL ©

Framing the pieces

59

Utility Distribution

End UseProduction

• Energy Management• Customer-Cited Generation

• Energy Efficiency• Demand Response• Customer Engagement

• DER Distribution TBD Shared services Production aggregation

• DER Wholesale In ProgressIndependent

Grid

• Microgrid

DNV GL ©

Drivers shaping DER business

• Utility. DER-based planning, procurement approaches & programs take form.• Markets. Wholesale markets clarify rules and payment approaches. Distribution

markets evolve. • Customer. Customer value increase / DER cost decreases & ease of financing

facilitates customer procurement. 60

DER Growth & Mix

Commercial & Physical Access to the Grid

Mechanisms for Realizing Value

• Physical. Interconnection rule updating. Regulators prompting increased efficiency in negotiating access. IT systems facilitating DER integration deploying / maturing. T&D microgrid costs dropping & reliability demand growing.

• Commercial. (Virtual) Net metering and standby rules/rates being clarified & made consistent across U.S. as with measurement and verification approaches.

• Energy $. Technology cost reductions. Performance improvements. Grid $s up.• Reliability. Severe weather, grid degradation or physical attacks prompt action.• Emissions. Concern for air quality and climate change grows. • Productivity. Automated control, monitoring & detection with matching services.

DNV GL ©

Historical value realization mechanisms

Incentives drive customer adoption

Likely to continue though form may change

societal value = emissions; energy securitycustomer value = cost of energy, corporate targets

Tariff adjustments drive customer adoption

Residential tariff proposals are afootsocietal value = grid capacity

customer value = energy bill management

Wholesale market access for provision of grid services

Rules are changingsocietal value = lower cost resources; higher

efficiencycustomer: direct or indirect payments

Distribution grid services

Increased regulator emphasis on DER & planning– Targeted DSM (e.g., ConEd) societal value = lower cost resources; higher efficiency

customer: direct or indirect payments; bill mgmt.

– Market mechanism (TBD, e.g., NY-REV)

61

DNV GL ©

How is value changing? Driving up demand & driving down costs

Energy.– PV and storage installed prices are forecasted to decline– State initiatives support distributed renewable and energy efficiency– Dynamic pricing programs are being considered for expansion

Reliability. – Expected increase in outages due to weather aging infrastructure– State initiatives exist to incentivize customer reliability investments (e.g.,

NYSERDA CHP N+1 incentive)

T&D.

– Microgrids are increasing their capability

– (Parallel trends on the utility distribution system (DERMs, VVO, DA, etc.))

Productivity (comfort / operations). Smart appliances, advanced controls

Emissions. – Corporations are setting and working towards clean energy goals– By 2025, Millenials will make up 75 % of the workforce. The majority place a

priority on alternative energy over fossil fuels and support federal funding of renewables. Two-thirds see climate change as a real problem.

62

DNV GL ©

How access is changing?

Rule 21 (CA) & IEEE 1547

Interconnection study (FERC)

Individual net metering

Virtual metering rules

Default utility provider right to own

DER integrated into planning

– CA DER rulemakings

– MA Grid Modernization

– NY-REV

– MN (E21)

– etc.

63

DNV GL ©

Finding value: having access and exchanging services

64

MarketAdministrative

Open

Restricted

Utility DR Programs

NY-REV Initiative

Utility DG Programs

Acc

ess

Value Transaction Approach

TOU Tariffs

Microgrid Community Microgrid

ISO/RTO DR Programs

DNV GL ©

Implications & Examples

DER ESCO-type services are relevant across all scenarios.– Value must come from:

• utility procurement (e.g., DR programs), • tariff ‘pain’ (e.g., storage; energy management or • customer clean energy target (e.g., PV ownership or PPAs)where wholesale access (e.g., Viridity) does not exist

– There is an opportunity to bundle with additional services to leverage infrastructure and add value.• Market examples include: o Vivint; ADT Energy Management & Honeywell Security Systemso Nest Labs, Whirlpool, LG, Philipso NEST & SolarCity, etc.

Utility programs are expanding to incorporate DER.– Planning, DR Programs, etc.

Distribution management services offer potential through utility programs or a DSO. – Energy and non-energy services? (Ancillaries, financial, etc.) via DR, smart

inverters, etc. Microgrids & NY REV might conceptualize new services?

– Localized transactions, mini-ISO/RTO, forecasting, financial hedging, etc.

65

DNV GL ©

Implications & Examples

Production and end-use services have already evolved, and are in some ways “piggy-backing” on traditional utility T&D services. IT developments are increasing efficiencies for customers, allowing improved wholesale market participation, and enabling virtual power plants.

Policies will shape how this progresses, including: – how open the distribution system is, – how costly/efficient it is to connect, and – how service costs are allocated. Currently limited substitutes exist for

distribution delivery.

Virtual power plants and microgrids provide a potential alternative and the possibility of full unbundling.

A number of services in addition to energy management services are viable under market models and utility-administered programs. – These include financing, data analytics, customer hedging, building-related

services.

Several roles for utilities are feasible. (There is the potential that utilities will become the market operator or the customer).

66

DNV GL ©

SAFER, SMARTER, GREENER

www.dnvgl.com

Thank you

Access the on-demand webinar here.

67

Jessica [email protected]

Related Documents

![[Srijan Wednesday Webinar] Finding success with a distributed workforce](https://static.cupdf.com/doc/110x72/587564471a28abd80a8b4b77/srijan-wednesday-webinar-finding-success-with-a-distributed-workforce.jpg)