Wealth Management An Unbiased Approach to Managing Your Investments Designed for the Affluent Investor

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Wealth ManagementAn Unbiased Approach to Managing Your Investments Designed for the Affluent Investor

Basics of InvestingFundamental Principle of Investing

RISK

EXPE

CTED

RET

URN

LOW HIGH

CASH

BONDS

STOCKS

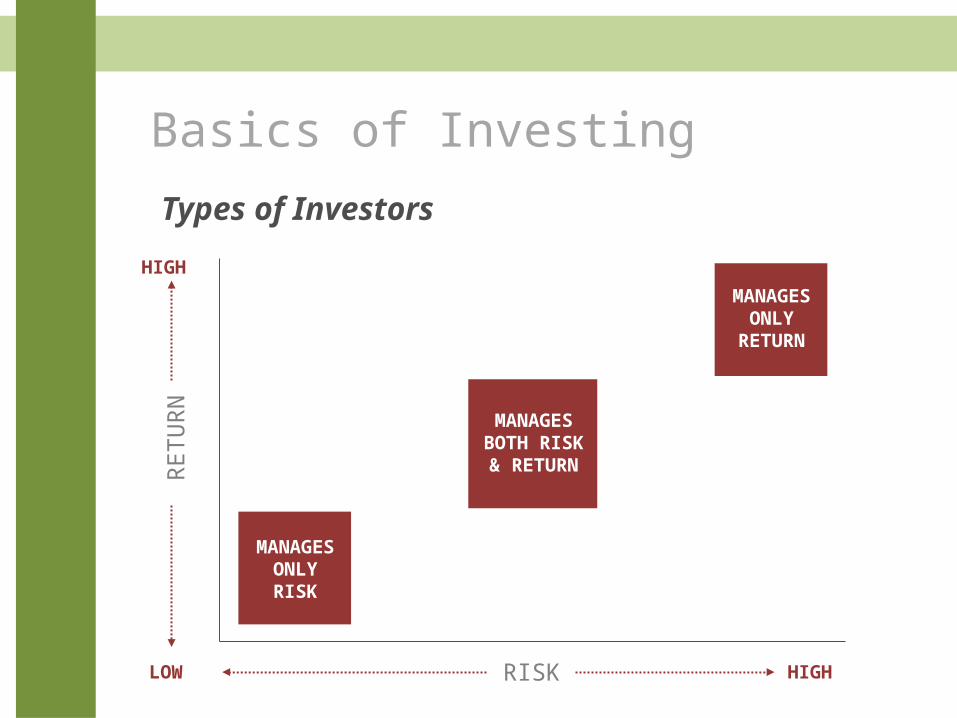

Basics of Investing

Types of Investors

RISK

RETU

RN

LOW HIGH

HIGH

MANAGESONLYRISK

MANAGESBOTH RISK& RETURN

MANAGESONLY

RETURN

Something to Consider:

“Stocks have outperformed fixed income securities over time.

Why not always invest in stocks for future funding?”

Answer: Time Horizon and Risk Tolerance evolve with age

The impact

of risk on retirement

income

© American Funds Distributors, Inc.

The impact of risk on retirement income

The primary concern for most investors is the possibility of permanently losing their money. Such a loss can prevent them from reaching their financial goals..

Whether investing to meet a long-term objective or taking retirement income from their investments, it’s critical that investors recognize the risks they face and try to manage them with the help of their financial adviser.

During retirement, if market volatility becomes magnified and time to recover losses becomes compressed, the margin for error narrows. That’s why it’s important for investors at this stage to seek retirement-income strategies that can be resilient when markets decline and can generate consistent streams of income.

© American Funds Distributors, Inc.

Some Assumptions Do Not Apply

Before RetirementCash flow not an issue

Known time horizon

Risk = standard deviation

Cash flow is critical

Unknown time horizon

Risk = loss of capital

During Retirement

Why Do We Invest? To satisfy a current goal

To satisfy a future goal

Goals Drive Investments,

Investments DO NOT Drive Goals

Basics of Investing

Asset Allocation OverviewWhat type of investor are you?Influencing Factors:

Age, Retirement Goals and Horizon, Investment Experience, Personality

Source: Investopedia.com

Fixed Income

Equities

Cash Equivalents

Fixed IncomeEquities

Cash EquivalentsFixed

Income

Equities

Cash EquivalentsFixed Income

Equities

Cash Equivalents

Less Risk More Risk

Conservative Moderate Aggressive Very Aggressive

The Common Approach:

Aggressive

I don’t want to lose any money, but if I can still

make a little money, that’s great!

I want to make money and I don’t mind taking a few risks to make it happen. I want to make the most

money possible! I am willing to take whatever risks

needed to make it happen!

Conservative

Moderate

Determining Your Risk Tolerance

Determining Your Risk ToleranceThe Expanded Approach:

Risk Questionnaires

Your Age and Time Horizon

Your Assets and Savings Potential

Your Level of Comfort

Your Spending Level

Risk is approached from two different directions

1. How much risk do I need to take?

2. How much risk do I want to take?

I need to consider several factors to determine my true

risk tolerance…

Objective – Buy a New Home

DougAccumulation period: One yearDistribution period: One-time distribution

Sample Portfolio – Accumulation Phase

This sample portfolio is for illustrative purposes only. Please consider individual objectives, risk tolerance and time horizon.

© American Funds Distributors, Inc.AI-30038

Bonds

Growth-and-Income

Equity-Income/ Balanced

Objective: Save for Child’s College Education

JanetAccumulation period: 15 yearsDistribution period: 4 years

Equity-income/balanced

Bonds

Growth-and-income

Growth

This sample portfolio is for illustrative purposes only. Please consider individual objectives, risk tolerance and time horizon.

© American Funds Distributors, Inc.AI-30038

Sample Portfolio – Accumulation Phase

Objective: Invest for Retirement

RicardoAccumulation period: 20 yearsDistribution period: 20+ years

Growth-and-income Growth

Equity-income/balanced

This sample portfolio is for illustrative purposes only. Please consider individual objectives, risk tolerance and time horizon.

© American Funds Distributors, Inc.AI-30038

Sample Portfolio – Accumulation Phase

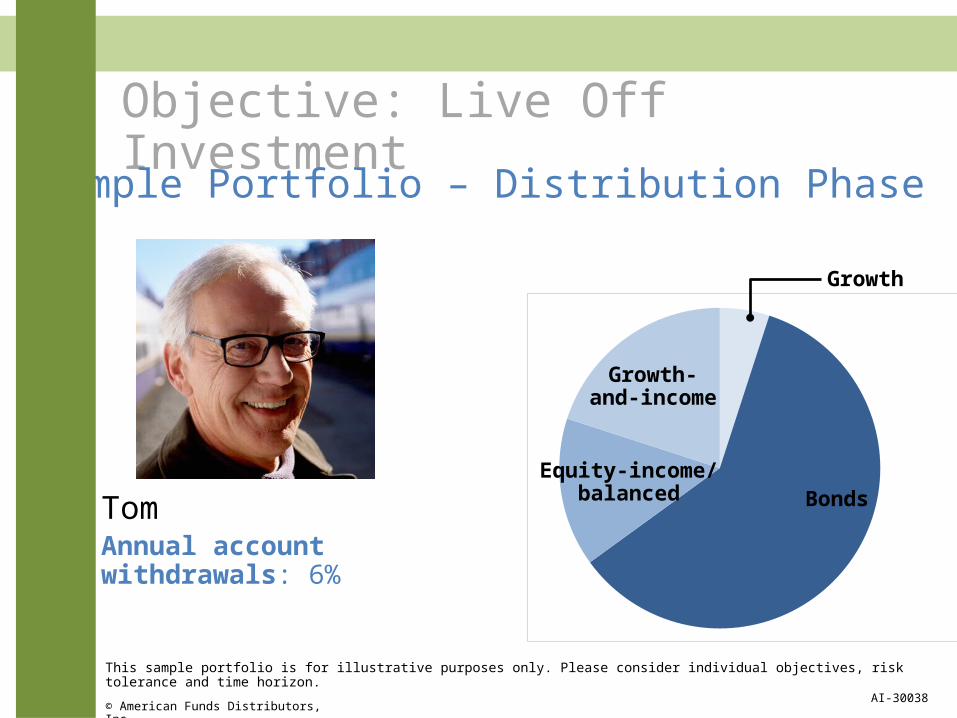

Objective: Live Off Investment

TomAnnual account withdrawals: 6%

Equity-income/balanced Bonds

Growth-and-income

Growth

Sample Portfolio – Distribution Phase

This sample portfolio is for illustrative purposes only. Please consider individual objectives, risk tolerance and time horizon.

© American Funds Distributors, Inc.AI-30038

Objective: Supplement Existing Income

LoriAnnual account withdrawal: 3%

Bonds

Growth-and-income

Equity-income/balanced

Growth

This sample portfolio is for illustrative purposes only. Please consider individual objectives, risk tolerance and time horizon.

© American Funds Distributors, Inc.AI-30038

Sample Portfolio – Distribution Phase

Basics of InvestingEffect of Variability

PORTFOLIO A PORTFOLIO B

First Year Return Gain 30% Gain 10%Value After First Year $1,300,000 $1,100,000Second Year Return Loss 10% Gain 10%Value After Second Year $1,170,000 $1,210,000

Average return for each portfolio was 10% per year. Portfolio B with a stable return had a real dollar return which was $40,000 greater than Portfolio A

RULE: Given 2 portfolios with the same arithmetic return the portfolio with the lowest volatility will always have the highest real dollar return.

For illustrative purposes only. This chart does not reflect the performance of any specific investment.

Original Value $1,000,000 $1,000,000

Not in Hard Copies: Variance Drain• Here’s an example:

– Using coin-flipping– 50% chance of coming up heads or tails– In the experiment, heads doubles your money and tails loses half your money

Head 100%Tails -50%Heads 100%Heads 100%Tails -50%Heads 100%Tails -50%Tails -50%Heads 100%Tails -50%

Average 25%

Seems highly profitable right?

Variance drain: Average Return• Let’s put some money to the numbers and see

– For the experiment, we will start with $2000

Head 100% $4000Tails -50% $2000Heads 100% $4000Heads 100% $8000Tails -50% $4000Heads 100% $8000Tails -50% $4000Tails -50% $2000Heads 100% $4000Tails -50% $2000

Return 0%

You started with $1000 and ended with $1000• How is that possible?• Your average return was 25%,

but your compounded return is 0

Variance drain: Compounded Return– Volatility is reduced by lowering the risk you take– In this experiment, you will only commit half of your

capital, thereby halving your risk

Investment: $1000

Half BalanceReturn

Head 50% $1500Tails -25% $1125Heads 50% $1688Heads 50% $2531Tails -25% $1898Heads 50% $2848Tails -25% $2136Tails -25% $1602Heads 50% $2403Tails -25% $1802

Total Return 80%

After 10 flips, you had a total return of 80%, or 6.1% compounded per flip• You netted a profit of

$800 on this investment so far

The Impact of Volatility

Impact on a Hypothetical $100,000 PortfolioYear 1

ReturnYear 2

ReturnAverage

ReturnCompound

ReturnValue at End

of Year 2

Portfolio #1 50% -50% 0% -13.4% $75,000

Portfolio #2 10% -10% 0% -0.5% $99,000

For illustrative purposes only.

Image Source: http://www.saturdayeveningpost.com/2010/07/26/in-the-magazine/finance/investing-america.html

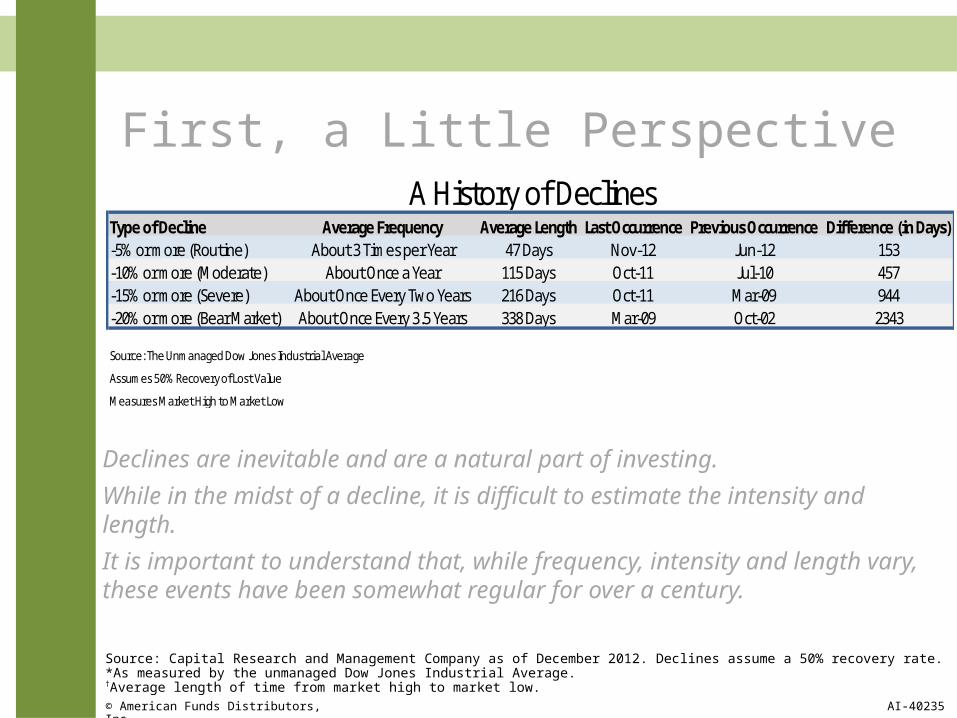

First, a Little Perspective

Source: Capital Research and Management Company as of December 2012. Declines assume a 50% recovery rate.*As measured by the unmanaged Dow Jones Industrial Average. †Average length of time from market high to market low.© American Funds Distributors, Inc. AI-40235

Type of Decline Average Frequency Average Length Last Occurrence Previous Occurrence Difference (in Days)-5% or more (Routine) About 3 Times per Year 47 Days Nov-12 Jun-12 153-10% or more (Moderate) About Once a Year 115 Days Oct-11 Jul-10 457-15% or more (Severe) About Once Every Two Years 216 Days Oct-11 Mar-09 944-20% or more (Bear Market) About Once Every 3.5 Years 338 Days Mar-09 Oct-02 2343

Source: The Unmanaged Dow Jones Industrial Average

Assumes 50% Recovery of Lost Value

Measures Market High to Market Low

A History of Declines

Declines are inevitable and are a natural part of investing.

While in the midst of a decline, it is difficult to estimate the intensity and length.

It is important to understand that, while frequency, intensity and length vary, these events have been somewhat regular for over a century.

Market Declines are Inevitable

From October 2007 to March 2009, the S&P 500 fell over 56%. As of February 2010, it has since rallied back 40%.

MSCI Index Affiliation

Developed Markets Frontier Markets

Emerging Markets

SCALE Ten BillionOne Trillion

StocksHistorical Return from 1926 to 2011:

0%

2%

6%

8%

% R

ETU

RN

12%

4%

10%

ASSET CLASSES

CASH (T-Bill)

FIXED INCOME/BONDS

(LT Gov Bonds)

STOCKS

(LC Stocks)

14%

Ibbotson Associates U.S. Return & Risk Data: 1926-2009

Source: Stocks, Bonds, Bills and Inflation 2009 Yearbook. 2009 Ibbotson Associates, Inc. Based on copyrighted works by Ibbotson and Sinquefield. All right reserved. Used with permission.

Past performance does not guarantee future results.

5.72%

3.59%

9.77%

Risk

Different Asset Classes can be Measured

Cash

Fixed Income/Bonds

Stocks

HOW DO WE MEASURE THE RISK FOR EACH ASSET CLASS?

Measuring Risk

Consider the weather in San Francisco and Kansas City

Measuring Risk

Defines risk in terms of variability or volatility of return

Measures total volatility -- both downside and upside dispersion of a portfolio’s return -- to the average return

It shows how much variation there is from the average. 95% of ALL observations fall with +/- 2 standard deviations

MEAN RETURN-1 SD-2 SD +1 SD +2 SD

Standard Deviation

= 95%

Measuring Risk

US T-Bills have a historical mean return of 2.96% and a standard deviation of 0.57% We would expect 95% of all returns to fall within a range of 1.85% to 4.1%.

MEAN RETURN-1 SD-2 SD +1 SD +2 SD

Range of 2.25%

1.85% 2.42% 3.53% 4.10%

2.96%

1989-2012Std Dev = 0.57%

Data Source: Morningstar, Barclays US Treasury Bill TR

US T-Bills

Measuring RiskS&P 500 Large Cap Stocks

The S&P 500 has a historical mean return of 9.62% and a standard deviation of 18.11% We would expect 95% of all returns to fall within a range of -26.6% to 45.8%.

MEAN RETURN-1 SD-2 SD +1 SD +2 SD

Range of 72.44%

-26.60% -8.49% 27.73% 45.84%

9.62%

Std Dev = 18.11%Data Source: www.russell.com 1973-2011

Measuring Risk

Small Cap Stocks have a historical mean return of 11.47% with a standard deviation of 22.23%. We would expect 95% of all returns to fall within a range of -32.9% to 55.9%

MEAN RETURN-1 SD-2 SD +1 SD +2 SD

Range of 88.92%

-32.99% -10.76% 33.7% 55.93%

11.47%

Std Dev of 22.23%

Small Cap Stocks

Data Source: www.russell.com, Ibbotson & Associates, 1973-1978, Russell 2000, 1979-2011

Measuring Risk

International Stocks have a historical mean return of 8.97% with a standard deviation of 22.58%. We would expect 95% of all returns to fall within a range of -36.1% to 54.1%

MEAN RETURN-1 SD-2 SD +1 SD +2 SD

Range of 90.32%

-36.19% -13.61% 31.55% 54.13%

8.97%

Std Dev of 22.58%

International Stocks

Data Source: www.russell.com, MSCI EAFE

Measuring Risk

Real Estate has a historical mean return of 10.35% with a standard deviation of 14.79%. We would expect 95% of all returns to fall within a range of -19.23% to 39.93%

MEAN RETURN-1 SD-2 SD +1 SD +2 SD

Range of 56.16%

-19.23% -4.44% 25.14% 39.93%

10.35%

Std Dev of 14.79%

Real Estate

Data Source: www.russell.com, NAREIT Equity REIT Index

Summary As of 12/31/2012

3 Yr Historical

IWB Large Cap

IWN Small Cap

DODFX Intl. Fund

VWO Emrg.

Markets

FGOVX Intermd

Govt

DODIX Corp/ Mrtg

VUSTXLT Gov

GSHIX High Yield

Ave. Return 5.06% 6.49% 0.65% 0.23% 4.83% 6.85% 8.34% 9.62%

Std. Dev. 19.20% 24.62% 26.72% 29.60% 3.67% 4.76% 13.65% 13.06%

Equity Funds Bond/ Fixed Income Funds

Increasing Standard Deviation & Returns

Fund Names are not investment recommendations. Data Source: Asset Allocation, Roger Gibson, 2008

Measuring Risk

Standard Deviation of Asset Classes

-30% -10% 30% 50%

3%

CASH

9%

BONDS

10%

LARGE STOCKS

11.5%

SMALL STOCKS

1972-2008 Data Source: Asset Allocation, Roger Gibson, 2008

Measuring Risk

2006

Histogram of Stocks’ Performance Based on the S&P 500 (given in percent)

2004 20092000 2007 1998 2003 19971990 2005 1986 1999 19951981 1994 1979 1998 1991

1977 1993 1972 1996 19891969 1992 1971 1983 19851962 1987 1968 1982 19801953 1984 1965 1976 19751946 1978 1964 1967 1955

2001 1940 1970 1959 1963 1950 1973 1939 1960 1952 1961 1945

2002 19661934 1956 1949 1951 1938 1958 1974 19571932 1948 1944 1943 1936 1935 1954

1931 1937 19301941 1929 1947 1926 1942 1927 1928 1933

LARGE COMPANY

STOCKS

-40 -30 -20 -10 0 10 20 30 40 50 60

Source: Stocks, Bonds, Bills and Inflation 2009 Yearbook. 2009 Ibbotson Associates, Inc. Based on copyrighted works by Ibbotson and Sinquefield. All right reserved. Used with permission.

Past performance does not guarantee future results.

2008

2010 20122011

Mixing Assets Together

Equity Assets

Fixed Assets

Real estate

Hedge funds

Annuities

Insurance

Private Equity

Venture Capital

Assets choices

How do I mix them together?

Modern Portfolio Theory (MPT)Diversification

Every investment decision should have as its objective the enhancement of the portfolio’s return, the reduction of risk, or both.

The purpose of diversification is not merely to increase returns, but rather to achieve a desired level of return with a minimum level of risk.

To protect a portfolio from being vulnerable to just one asset class, it is important to develop policies that will lead to diversified portfolios.

Modern Portfolio Theory (MPT)Perfect Positive Correlation of Returns

TIME

$

Modern Portfolio Theory (MPT)Perfect Negative Correlation of Returns

TIME

$

Modern Portfolio Theory (MPT)No Correlation of Returns

TIME

$

Modern Portfolio Theory (MPT)Real World Example

TIME

Past performance is not indicative of future results.

$

In US dollars. Indices are not available for direct investment. Their performance does not reflect the expenses associated with the management of an actual portfolio. Past performance is not a guarantee of future results. US value and growth index data (ex utilities) provided by Fama/French. The S&P data are provided by Standard & Poor’s Index Services Group. CRSP data provided by the Center for Research in Security Prices, University of Chicago. International Value data provided by Fama/French from Bloomberg and MSCI securities data. International Small data compiled by Dimensional from Bloomberg, StyleResearch, London Business School, and Nomura Securities data. MSCI EAFE Index is net of foreign withholding taxes on dividends; copyright MSCI 2010, all rights reserved. Emerging markets index data simulated by Fama/French from countries in the IFC Investable Universe; simulations are free-float weighted both within each country and across all countries.

The Risk Dimensions Delivered

Periods based on rolling annualized returns. 121 total 25-year periods. 181 total 20-year periods. 241 total 15-year periods. 301 total 10-year periods. 361 total 5-year periods.International Value and Growth data provided by Fama/French from Bloomberg and MSCI securities data. International Small data compiled by Dimensional from Bloomberg, StyleResearch, London Business School, and Nomura Securities data. International Large is MSCI EAFE Index net of foreign withholding taxes on dividends; copyright MSCI 2010, all rights reserved. Foreign securities prices may decline or fluctuate because of: (a) economic or political actions of foreign governments, and/or (b) less regulated or liquid securities markets. Investors holding these securities are also exposed to foreign currency risk (the possibility that foreign currency will fluctuate in value against the US dollar). Securities of small companies are often less liquid than those of large companies. As a result, small company stocks may fluctuate relatively more in price. Mutual funds distributed by DFA Securities LLC.

Value beat growth 100% of the time.

Value beat growth 100% of the time.

Value beat growth 100% of the time.

Value beat growth 100% of the time.

Value beat growth 98% of the time.

Small beat large 100% of the time.

Small beat large 100% of the time.

Small beat large 84% of the time.

Small beat large 76% of the time.

Small beat large 75% of the time.

International Value vs. International Growth International Small vs. International Large

January 1975 – December 2011

In 5-Year Periods

In 10-Year Periods

In 15-Year Periods

In 20-Year Periods

In 25-Year Periods Value beat growth 100% of the time.

Value beat growth 100% of the time.

Value beat growth 100% of the time.

Value beat growth 100% of the time.

Value beat growth 98% of the time.

The Risk Dimensions Delivered

Periods based on rolling annualized returns. 703 total 25-year periods. 763 total 20-year periods. 823 total 15-year periods. 883 total 10-year periods. 943 total 5-year periods.Performance based on Fama/French Research Factors. Securities of small companies are often less liquid than those of large companies. As a result, small company stocks may fluctuate relatively more in price. Mutual funds distributed by DFA Securities LLC.

Value beat growth 100% of the time.

Value beat growth 100% of the time.

Value beat growth 99% of the time.

Value beat growth 96% of the time.

Value beat growth 86% of the time.

Small beat large 96% of the time.

Small beat large 83% of the time.

Small beat large 78% of the time.

Small beat large 68% of the time.

Small beat large 60% of the time.

US Value vs. US Growth US Small vs. US Large

July 1926 – December 2011

Asset AllocationWhat is Asset Allocation?

CASH STOCKS

BONDS

Asset AllocationIs Asset Allocation Important?

ASSET ALLOCATION POLICY: 91.5%

MARKET TIMING: 1.8%

SECURITY SELECTION: 4.6%

OTHER FACTORS: 2.1%

Source: Asset Allocation by Roger Gibson

Asset Allocation cannot eliminate the risk of fluctuating prices or uncertain returns.

In other words it cannot eliminate Market Risk

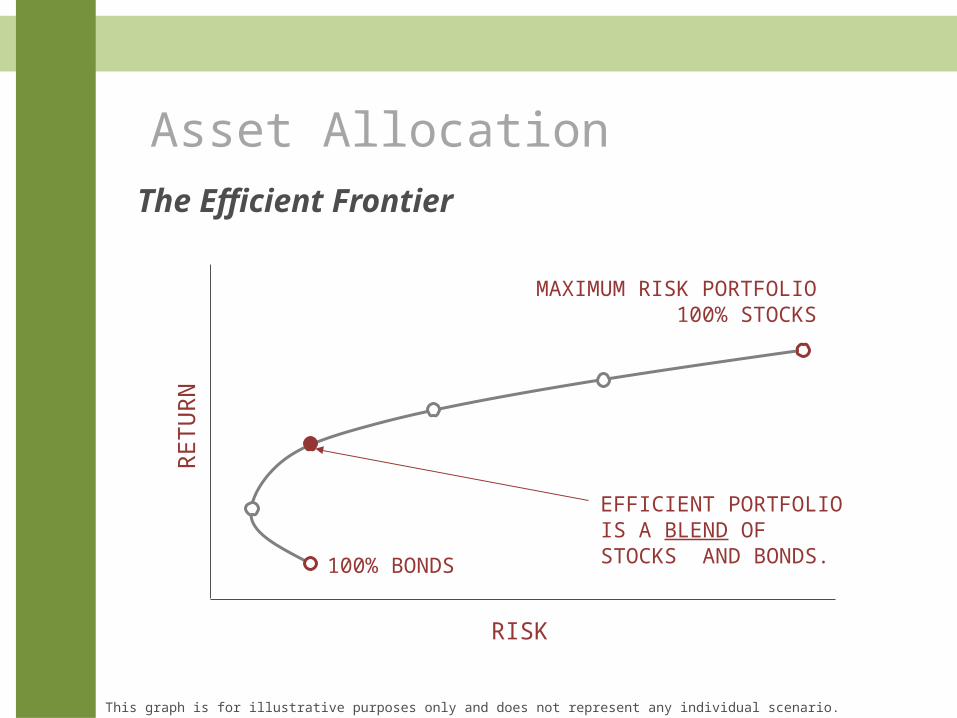

Asset AllocationThe Efficient Frontier

RETU

RN

RISK

100% BONDS

MAXIMUM RISK PORTFOLIO100% STOCKS

This graph is for illustrative purposes only and does not represent any individual scenario.

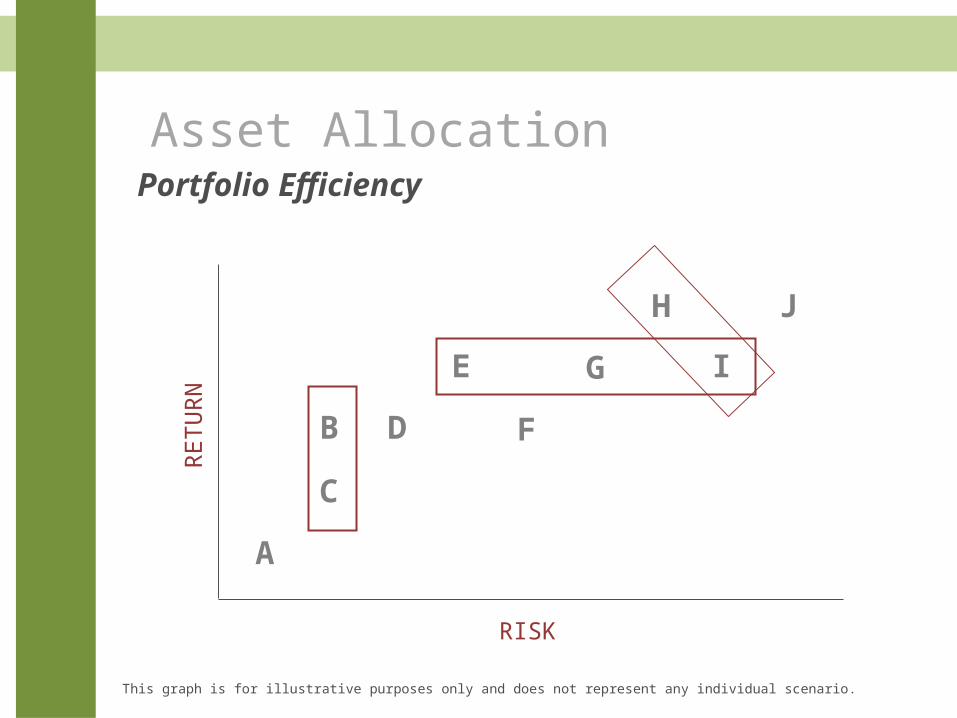

Asset AllocationPortfolio Efficiency

RETU

RN

A

B

C

D

E

F

G

H

I

J

RISK

This graph is for illustrative purposes only and does not represent any individual scenario.

Asset AllocationThe Efficient Frontier

RETU

RN

RISK

100% BONDS

MAXIMUM RISK PORTFOLIO100% STOCKS

This graph is for illustrative purposes only and does not represent any individual scenario.

EFFICIENT PORTFOLIOIS A BLEND OF STOCKS AND BONDS.

The Basic Institutional Portfolio

Barclays Capital data, formerly Lehman Brothers, provided by Barclays Bank PLC. The S&P data are provided by Standard & Poor’s Index Services Group. Indexes are not available for direct investment. Their performance does not reflect the expenses associated with the management of an actual portfolio.Past performance is not a guarantee of future results. Not to be construed as investment advice. Returns of model portfolios are based on back-tested model allocation mixes designed with the benefit of hindsight and do not represent actual investment performance. See cover page for additional information.

S&P 500 Index

Barclays US Government/Credit Bond IndexAnnualizedCompound

Return

Annualized Standard

Deviation

Model Portfolio 1 9.41% 11.18%

Barclays US Govt./Credit

Bond Index S&P 500 Index

Model Portfolio 1 40% 60%

Substituting Short-Term for Long-Term Fixed Income

Annualized Compound

Return

Annualized Standard

Deviation

Model Portfolio 1 9.41% 11.18%

Model Portfolio 2 8.82% 10.18%

Barclays US Govt./Credit

Bond IndexS&P 500

Index

Merrill Lynch One-Year US

Treasury Note Index

Model Portfolio 1 40% 60%

Model Portfolio 2 60% 40%

S&P 500 Index

One-Year US Treasury Note Index

Barclays Capital data, formerly Lehman Brothers, provided by Barclays Bank PLC. The S&P data are provided by Standard & Poor’s Index Services Group. The Merrill Lynch Indices are used with permission; copyright 2010 Merrill Lynch, Pierce, Fenner & Smith Incorporated; all rights reserved. Indexes are not available for direct investment. Their performance does not reflect the expenses associated with the management of an actual portfolio.Past performance is not a guarantee of future results. Not to be construed as investment advice. Returns of model portfolios are based on back-tested model allocation mixes designed with the benefit of hindsight and so not represent actual investment performance. See cover page for additional information.

Diversifying a Portfolio Into US Small Cap StocksAnnualizedCompound

Return

Annualized Standard

Deviation

Model Portfolio 1 9.41% 11.18%

Model Portfolio 2 8.82% 10.18%

Model Portfolio 3 9.63% 11.86%

Barclays US Govt./Credit

Bond IndexS&P 500

Index

Merrill Lynch One-Year US

Treasury Note Index

US Small Cap

Index

Model Portfolio 1 40% 60%

Model Portfolio 2 60% 40%

Model Portfolio 3 30% 40% 30%

One-Year US Treasury Note IndexS&P 500 IndexUS Small Cap Index

Barclays Capital data, formerly Lehman Brothers, provided by Barclays Bank PLC. The S&P data are provided by Standard & Poor’s Index Services Group. The Merrill Lynch Indices are used with permission; copyright 2010 Merrill Lynch, Pierce, Fenner & Smith Incorporated; all rights reserved. Dimensional Index data compiled by Dimensional. Indexes are not available for direct investment. Their performance does not reflect the expenses associated with the management of an actual portfolio. Past performance is not a guarantee of future results. Not to be construed as investment advice. Returns of model portfolios are based on back-tested model allocation mixes designed with the benefit of hindsight and do not represent actual investment performance. See cover page for additional information.

Diversifying a Portfolio Into US Value Stocks

Barclays Capital data, formerly Lehman Brothers, provided by Barclays Bank PLC. The S&P data are provided by Standard & Poor’s Index Services Group. The Merrill Lynch Indices are used with permission; copyright 2010 Merrill Lynch, Pierce, Fenner & Smith Incorporated; all rights reserved. Dimensional Index data compiled by Dimensional. Indexes are not available for direct investment. Their performance does not reflect the expenses associated with the management of an actual portfolio.Past performance is not a guarantee of future results. Not to be construed as investment advice. Returns of model portfolios are based on back-tested model allocation mixes designed with the benefit of hindsight and do not represent actual investment performance. See cover page for additional information.

AnnualizedCompound

Return

Annualized Standard

Deviation

Model Portfolio 1 9.41% 11.18%

Model Portfolio 2 8.82% 10.18%

Model Portfolio 3 9.63% 11.86%

Model Portfolio 4 10.60% 11.78%

Barclays US Govt./Credit

Bond Index

S&P 500 Index

Merrill Lynch One-Year US

Treasury Note Index

US Small Cap

Index

US Large Value Index

Targeted Value Index

Model Portfolio 1 40% 60%

Model Portfolio 2 60% 40%

Model Portfolio 3 30% 40% 30%

Model Portfolio 4 15% 40% 15% 15% 15%

One-Year US Treasury Note Index

S&P 500 Index

US Small Cap Index

US Large Value Index

Targeted Value Index

A Fully Diversified Portfolio

Rebalanced annually. Barclays Capital data, formerly Lehman Brothers, provided by Barclays Bank PLC. The S&P data are provided by Standard & Poor’s Index Services Group. The Merrill Lynch Indices are used with permission; copyright 2010 Merrill Lynch, Pierce, Fenner & Smith Incorporated; all rights reserved. Dimensional Index data compiled by Dimensional. Emerging Markets Blended Index consists of 50% Fama/French Emerging Markets Index, 25% Fama/French Emerging Markets Small Cap Index, and 25% Fama/French Emerging Markets Value Index. Fama/French Emerging Markets, Fama/French Emerging Markets Value and Fama/French Emerging Markets Small Cap Index weightings allocated evenly between Dimensional International Small Cap Index and Fama/French International Value Index prior to January 1989 data inception. Dimensional International Small Cap Value Index weighting allocated to International Small Cap Index prior to July 1981 data inception. International Value weighting allocated evenly between International Small Cap and MSCI World ex USA Index prior to January 1975 data inception. Indexes are not available for direct investment. Their performance does not reflect the expenses associated with the management of an actual portfolio. Past performance is not a guarantee of future results. Not to be construed as investment advice. Returns of model portfolios are based on back-tested model allocation mixes designed with the benefit of hindsight and do not represent actual investment performance. See cover page for additional information.

AnnualizedCompound

Return

Annualized Standard

Deviation

Model Portfolio 1 9.41% 11.18%

Model Portfolio 2 8.82% 10.18%

Model Portfolio 3 9.63% 11.86%

Model Portfolio 4 10.60% 11.78%

Model Portfolio 5 11.64% 11.24%

Barclays US

Govt./CreditBond

Index

S&P 500

Index

Merrill Lynch One-Year US

Treasury Note Index

US Small

Cap Index

US Large Value Index

Targeted Value Index

Intl. LargeIndex

Intl.SmallIndex

Intl. Large ValueIndex

Intl.Small ValueIndex

Emerging Markets Blended

Index

Model Portfolio 1 40% 60%

Model Portfolio 2 60% 40%

Model Portfolio 3 30% 40% 30%

Model Portfolio 4 15% 40% 15% 15% 15%

Model Portfolio 5 7.5% 40% 7.5% 7.5% 7.5% 6% 6% 6% 6% 6%

One-Year US Treasury Note Index

S&P 500 Index

US Small Cap Index

US Large Value Index

Targeted Value Index

International Large Index

International Small Index

International Large Value Index

International Small Value Index

Emerging Markets Blended Index

Quarterly: 1973-2013

The Importance of Long-Term Discipline

The S&P data are provided by Standard & Poor’s Index Services Group. One-Month US Treasury Bills data © Stocks, Bonds, Bills, and Inflation Yearbook™, Ibbotson Associates, Chicago (annually updated work by Roger G. Ibbotson and Rex A. Sinquefield).For illustrative purposes only. Indexes are not available for direct investment. Their performance does not reflect the expenses associated with the management of an actual portfolio. Past performance is not a guarantee of future results. Values change frequently and past performance may not be repeated. There is always the risk that an investor may lose money.

Annualized Compound Returns (%) 1926-2011 1965-1981 1982-2011

S&P 500 Index 9.81 6.33 11.17

One-Month US Treasury Bills 3.66 6.66 4.98

Asset Allocation

Importance of a Rebalancing Strategy

TIME

100%

75%

50%

25%TARG

ET A

LLO

CATI

ON

REBALANCING REQUIRED

REBALANCING REQUIRED

REBALANCING REQUIRED

TARGET RANGE

Source: Sungard® Expert Solutions

Scenario Average Annual Return Standard Deviation End Value

Scenario One: Buy & Hold 11.53% 13.57% $8,874,742

Scenario Two: Periodic Rebalancing – Rebalance at the end of each quarter

11.85% 10.87% $9,391,171

Scenario Three: Threshold Rebalancing – Rebalance when the allocation deviates beyond +/- 20% of target

11.98% 12.14% $9,606,430

Source: Financial Planning Magazine, Dec 2005

Assume a hypothetical $1,000,000 Portfolio over 20 years,Allocated as shown

Russell 1000 Growth

25%

Russell 1000 Value25%

Russell 200010%

MSCI EAFE10%

Barclays Municipal30%

Why Rebalance?

Monte Carlo Simulation

A large number of random trials are run.

Patterns in the trial’s outcomes show the most likely range and concentration of results.

Please Note:

The following examples are for illustrative purposes only. The results shown do not represent the returns of any particular investment.

Monte Carlo Simulation

1973

1992

1993

1961

1998

1967

1978

1975

1983

19961991

1960

1961

1997

1974

195819951969

19941972

1955

1979

1990

19561970

1965

1954

19781997

1969

Monte Carlo Simulation

1998 1965 1953 1957 1991 1971

1955 1979 1978 1993 1969 1992

1974 1961 1990 1996 1962 1956

1983 1951 1958 1967 1973 1997

1950 1956 1976 1994 1995 1948

Monte Carlo Simulation

Example:If you could choose from any of the following three investments, which would you select?

#1 11.6 $299

#2 11.6 $299

#3 11.6 $299

INVESTMENT CHOICE

TEN YEARRETURN

GROWTHOF $100

Monte Carlo SimulationYou would think that they would all be the same…but…

0 1 2 3 4 5 6 7 8 9 10

$400

$350

$300

$250

$200

$150

$100

$50

YEAR

GROWTH OF $100

#1#2#3

BULL

MARKET

BEAR MARKET

BULL

MARKET

BEAR MARKET

You may want to understand the path you took to achieve the ending goal

Monte Carlo Simulation

Instead of a single $100 investment, test the same choices for different investors…

What if I were saving $10,000 a year?

Would they produce the same results?

Monte Carlo SimulationOne choice may produce over TWICE the amount of money

0 1 2 3 4 5 6 7 8 9 10

$300,000

$250,000

$200,000

$150,000

$100,000

$50,000

$0

GROWTH OF $10,000 INVESTED EACH YEAR

#1#2#3

BULL

MARKET

BEAR

MARKET

BULL

M

ARKE

T

BEAR MARKET

Same returns…BIG difference in ending results… #2 Wins!

YEAR

Monte Carlo Simulation

What about a different investor?

If I had $100,000 and I needed $15,000 per year, would it last 10 years?

Monte Carlo SimulationYou would run out of money with #2!

0 1 2 3 4 5 6 7 8 9 10

$250,000

$200,000

$150,000

$100,000

$50,000

$0

-$50,000

-$100,000

VALUE OF $100,000 WITHDRAWING $15,000 ANNUALLY

#1#2#3

BULL

MARKETBEAR MARKET

BULL MARKET

BEAR MARKET

Same returns… big difference in ending results… #1 Wins!

YEAR

Monte Carlo SimulationThe ending results of our three choices depend on YOUR plan…

They all produced an average of 11.6 % over the 10 year period!

INVESTMENT 1INVESTOR INVESTMENT 2 INVESTMENT 3

Invest $100

Save $10K/year

Invest $100K Withdraw $15K/year

$299 $299 $299

$119,117 $256,038 $171,909

$120,285 -$55,722 $41,097

Declines Can Erode Retirement Income

© American Funds Distributors, Inc. AI-33386

2000 2001 2002

100,000

80,000

60,000

40,000

20,000

0

S&P 500 Index, $100,000 initial investment, monthly withdrawals totaling 5% annually, increasing 4% each year, 3/24/00 – 10/9/02

Results reflect reinvestment of all distributions.

9

6

3

0

15%

12

12.3%withdrawal rate

5%withdrawal rate

$43,961

Monte Carlo Simulation

WHEN you receive a return can be far more important than your average return

Monte Carlo Simulation

Most plans assume you will achieve the average return each year and ignore bull and bear markets.

Understand your Odds

With probability analysis, you project many results; including both bull and bear markets

Future Markets

— Warren BuffettBerkshire Hathaway shareholder letter, 1988

© American Funds Distributors, Inc. AI-90863

“We do not have, never have had, and never will have an opinion about where the stock market, interest rates, or business activity will be a year from now.”

Investing in an Uncertain MarketSet realistic expectations

Stick to sound investment strategies

Customize your portfolio to suit your investment objective

Invest for the long term and stay the course

© American Funds Distributors, Inc. AI-30043

Related Documents