August 18, 2021 2 Valuation (Standalone) Rs cr Particulars FY20 FY21 FY22E FY23E Net sales 544 764 952 1,163 Growth (%) (11.6) 40.6 24.5 22.2 EBIDTA 17 105 121 151 OPM (%) 3.2 13.8 12.7 13.0 Adj PAT 18 104 115 140 Growth (%) (60.9) 479.2 10.2 22.1 FD EPS 20.8 120.7 133.0 162.3 P/E (x) 126.6 21.9 19.8 16.2 P/BV (x) 3.9 3.4 3.1 2.9 EV/EBITDA (x) 129.9 21.4 18.7 14.9 RoE (%) 3.1 16.8 16.5 18.4 RoCE (%) 3.2 16.9 16.7 18.6 Source: Company; Sharekhan estimates Automobiles Sharekhan code: VSTTILLERS New Idea + Positive = Neutral - Negative 3R MATRIX + = - Right Sector (RS) ü Right Quality (RQ) ü Right Valuation (RV) ü Powered by the Sharekhan 3R Research Philosophy VST Tillers and Tractors Ltd Cultivating a strong growth foundation VST Tillers and Tractors Limited (VST Tillers) is one of the leading power tillers and compact tractor manufacturers in India, with a dominant ~54% market share in power tillers, which is used primarily for farm mechanisation, a direct beneficiary of rural farming. We believe VST Tillers is well-positioned to benefit from a strong rural economy that is showing signs of recovering after a sudden spike in COVID-19 cases in the second wave. We expect the rural economy to recover strongly, led by the government’s initiatives for the farm sector, a strong kharif crop in the previous year, higher reservoir levels and the positive forecast of normal monsoon this year. Rural cash flows have further been supported by the government’s increased outlay for MSP procurement (targeting farmers) and MGNREGS (targeting migrant labourers). Large tractor OEMs have given a healthy guidance for the industry, though they expect the growth rate to moderate to mid-single digits due to a high base. VST Tillers is expected to increase its market share in power tillers and tractors segments, led by stronger rural sentiments, new product launches and a strong brand recall among small & marginal farmers. The company is looking to widen its addressable markets through technological partnerships and a focus on niche segments. In addition, the power tiller market, which has been traditionally a subsidy driven market, is now pegging growth on farmers without waiting for subsidies. The change has been largely on the back of a positive impact of increasing farm mechanisation. This trend marks a structural shift and would support healthy growth in the long term. Further, imports of power tiller have been restricted since June, which is helping domestic players such as VST Tillers. We expect power tillers to remain a long-term driver for the company, led by its dominant market share, strong rural penetration and brand recall. The company also focused on increasing market share in compact tractors through new launches and rural reach. The company aspires to be a Rs. 3,000 crore global brand in the diversified farm mechanisation products and solutions sector by FY2025. VST Tillers is virtually debt-free and has a strong balance sheet. Earnings are expected to grow strongly at 16% CAGR over FY21-23E on a large base, led by a 23.3% revenue CAGR, partially offset by drop in EBITDA margin. Going forward, VST will be largely focused on increasing market share through product development in niche area, increasing distribution network, and brand-building exercises. We remain positive on the rural economy and expect VST Tillers to be a key beneficiary. Thus, we initiate viewpoint coverage on VST Tillers with a positive view and expect an upside of 21-23%. Our Call Valuation - Initiate Viewpoint Coverage with Positive view and expect an upside of 21- 23%: VST Tillers is well-positioned to maintain its dominant market share in the power tiller market. Market share gains driven by new product launches across brands would increase the company’s addressable market. In addition, the company is strengthening its distribution network across the country. The company has technological tie-ups with Pubert (France) and Zetor (Czech Republic) for product development. VST Tillers has invested in California, US- based Zimeno Inc, a manufacturer of driver optional born electric tractors under the Monarch brand. The stock is trading below its historical average at P/E multiple of 16.2x and EV/EBITDA of 14.9x on its FY23E estimates. In addition, the company has a land parcel of ~20 acres at a premium location (Whitefield) in Bangalore, which it intends to monetise at a later stage that we have not factored in our estimates. We believe that current valuations offer investors a good entry point, given a strong brand recall, extensive network, strong balance sheet and superior return ratio profile. We initiate viewpoint coverage on the stock with positive view and expect an upside of 21-23%. Key Risks Demand for agricultural machinery is highly dependent on the monsoons and can be affected by erratic rains. Also, prolonged COVID-19 infections in India would impact economic growth and consequently impact the rural economy. Summary We initiate viewpoint coverage on VST Tillers and Tractors Limited (VST Tillers) with a positive view and expect a 21-23% upside. Company is well-placed to benefit from a strong rural economy and increase in farm mechanisation. Robust earnings growth, balance sheet and return ratios; long-term growth through technological tie-ups, new launches, increasing penetration and market share gains would drive value for VST Tillers. Stock trades below historical average at P/E multiple of 16.2x and EV/EBITDA of 14.9x on FY23E earnings; provides a good entry point. Viewpoint Company details Market cap: Rs. 2,278 cr 52-week high/low: Rs. 2,664 / 1,504 NSE volume: (No of shares) 22,253 BSE code: 531266 NSE code: VSTTILLERS Free float: (No of shares) 0.4 cr Shareholding (%) Promoters 54.8 FII 5.3 DII 13.6 Others 26.4 Price performance (%) 1m 3m 6m 12m Absolute 11.1 18.9 17.7 33.9 Relative to Sensex 6.1 7.8 7.7 -11.7 Sharekhan Research, Bloomberg Reco/View View: Positive CMP: Rs. 2,637 Upside potential: 21-23% Price chart 1000 1200 1400 1600 1800 2000 2200 2400 Aug-20 Dec-20 Apr-21 Aug-21

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

August 18, 2021 2

Valuation (Standalone) Rs cr

Particulars FY20 FY21 FY22E FY23E

Net sales 544 764 952 1,163

Growth (%) (11.6) 40.6 24.5 22.2

EBIDTA 17 105 121 151

OPM (%) 3.2 13.8 12.7 13.0

Adj PAT 18 104 115 140

Growth (%) (60.9) 479.2 10.2 22.1

FD EPS 20.8 120.7 133.0 162.3

P/E (x) 126.6 21.9 19.8 16.2

P/BV (x) 3.9 3.4 3.1 2.9

EV/EBITDA (x) 129.9 21.4 18.7 14.9

RoE (%) 3.1 16.8 16.5 18.4

RoCE (%) 3.2 16.9 16.7 18.6

Source: Company; Sharekhan estimates

Automobiles Sharekhan code: VSTTILLERS New Idea

+ Positive = Neutral - Negative

3R MATRIX + = -

Right Sector (RS) ü

Right Quality (RQ) ü

Right Valuation (RV) ü

Powered by the Sharekhan 3R Research Philosophy

VST Tillers and Tractors LtdCultivating a strong growth foundation

VST Tillers and Tractors Limited (VST Tillers) is one of the leading power tillers and compact tractor manufacturers in India, with a dominant ~54% market share in power tillers, which is used primarily for farm mechanisation, a direct beneficiary of rural farming. We believe VST Tillers is well-positioned to benefit from a strong rural economy that is showing signs of recovering after a sudden spike in COVID-19 cases in the second wave. We expect the rural economy to recover strongly, led by the government’s initiatives for the farm sector, a strong kharif crop in the previous year, higher reservoir levels and the positive forecast of normal monsoon this year. Rural cash flows have further been supported by the government’s increased outlay for MSP procurement (targeting farmers) and MGNREGS (targeting migrant labourers). Large tractor OEMs have given a healthy guidance for the industry, though they expect the growth rate to moderate to mid-single digits due to a high base. VST Tillers is expected to increase its market share in power tillers and tractors segments, led by stronger rural sentiments, new product launches and a strong brand recall among small & marginal farmers. The company is looking to widen its addressable markets through technological partnerships and a focus on niche segments. In addition, the power tiller market, which has been traditionally a subsidy driven market, is now pegging growth on farmers without waiting for subsidies. The change has been largely on the back of a positive impact of increasing farm mechanisation. This trend marks a structural shift and would support healthy growth in the long term. Further, imports of power tiller have been restricted since June, which is helping domestic players such as VST Tillers. We expect power tillers to remain a long-term driver for the company, led by its dominant market share, strong rural penetration and brand recall. The company also focused on increasing market share in compact tractors through new launches and rural reach. The company aspires to be a Rs. 3,000 crore global brand in the diversified farm mechanisation products and solutions sector by FY2025. VST Tillers is virtually debt-free and has a strong balance sheet. Earnings are expected to grow strongly at 16% CAGR over FY21-23E on a large base, led by a 23.3% revenue CAGR, partially offset by drop in EBITDA margin. Going forward, VST will be largely focused on increasing market share through product development in niche area, increasing distribution network, and brand-building exercises. We remain positive on the rural economy and expect VST Tillers to be a key beneficiary. Thus, we initiate viewpoint coverage on VST Tillers with a positive view and expect an upside of 21-23%.

Our CallValuation - Initiate Viewpoint Coverage with Positive view and expect an upside of 21-23%: VST Tillers is well-positioned to maintain its dominant market share in the power tiller market. Market share gains driven by new product launches across brands would increase the company’s addressable market. In addition, the company is strengthening its distribution network across the country. The company has technological tie-ups with Pubert (France) and Zetor (Czech Republic) for product development. VST Tillers has invested in California, US-based Zimeno Inc, a manufacturer of driver optional born electric tractors under the Monarch brand. The stock is trading below its historical average at P/E multiple of 16.2x and EV/EBITDA of 14.9x on its FY23E estimates. In addition, the company has a land parcel of ~20 acres at a premium location (Whitefield) in Bangalore, which it intends to monetise at a later stage that we have not factored in our estimates. We believe that current valuations offer investors a good entry point, given a strong brand recall, extensive network, strong balance sheet and superior return ratio profile. We initiate viewpoint coverage on the stock with positive view and expect an upside of 21-23%.

Key RisksDemand for agricultural machinery is highly dependent on the monsoons and can be affected by erratic rains. Also, prolonged COVID-19 infections in India would impact economic growth and consequently impact the rural economy.

Summary

� We initiate viewpoint coverage on VST Tillers and Tractors Limited (VST Tillers) with a positive view and expect a 21-23% upside.

� Company is well-placed to benefit from a strong rural economy and increase in farm mechanisation.

� Robust earnings growth, balance sheet and return ratios; long-term growth through technological tie-ups, new launches, increasing penetration and market share gains would drive value for VST Tillers.

� Stock trades below historical average at P/E multiple of 16.2x and EV/EBITDA of 14.9x on FY23E earnings; provides a good entry point.

Vie

wp

oin

t

Company details

Market cap: Rs. 2,278 cr

52-week high/low: Rs. 2,664 / 1,504

NSE volume: (No of shares)

22,253

BSE code: 531266

NSE code: VSTTILLERS

Free float: (No of shares)

0.4 cr

Shareholding (%)

Promoters 54.8

FII 5.3

DII 13.6

Others 26.4

Price performance

(%) 1m 3m 6m 12m

Absolute 11.1 18.9 17.7 33.9

Relative to Sensex

6.1 7.8 7.7 -11.7

Sharekhan Research, Bloomberg

Reco/View

View: Positive

CMP: Rs. 2,637

Upside potential: 21-23%

Price chart

10001200140016001800200022002400

Aug-

20

Dec-

20

Apr-2

1

Aug-

21

August 18, 2021 3

Vie

wp

oin

t

Powered by the Sharekhan3R Research Philosophy

Investment Rationale

Strong rural revival to fuel growth

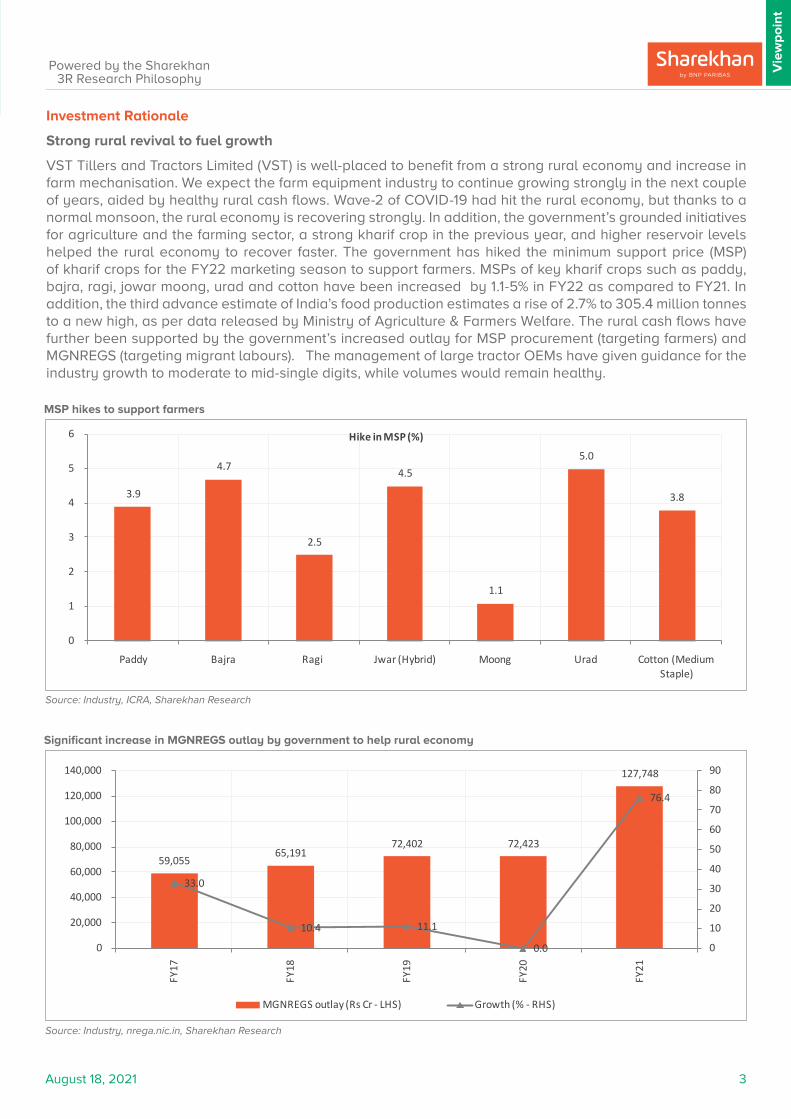

VST Tillers and Tractors Limited (VST) is well-placed to benefit from a strong rural economy and increase in farm mechanisation. We expect the farm equipment industry to continue growing strongly in the next couple of years, aided by healthy rural cash flows. Wave-2 of COVID-19 had hit the rural economy, but thanks to a normal monsoon, the rural economy is recovering strongly. In addition, the government’s grounded initiatives for agriculture and the farming sector, a strong kharif crop in the previous year, and higher reservoir levels helped the rural economy to recover faster. The government has hiked the minimum support price (MSP) of kharif crops for the FY22 marketing season to support farmers. MSPs of key kharif crops such as paddy, bajra, ragi, jowar moong, urad and cotton have been increased by 1.1-5% in FY22 as compared to FY21. In addition, the third advance estimate of India’s food production estimates a rise of 2.7% to 305.4 million tonnes to a new high, as per data released by Ministry of Agriculture & Farmers Welfare. The rural cash flows have further been supported by the government’s increased outlay for MSP procurement (targeting farmers) and MGNREGS (targeting migrant labours). The management of large tractor OEMs have given guidance for the industry growth to moderate to mid-single digits, while volumes would remain healthy.

Source: Industry, ICRA, Sharekhan Research

Source: Industry, nrega.nic.in, Sharekhan Research

MSP hikes to support farmers

Significant increase in MGNREGS outlay by government to help rural economy

3.9

4.7

2.5

4.5

1.1

5.0

3.8

0

1

2

3

4

5

6

Paddy Bajra Ragi Jwar (Hybrid) Moong Urad Cotton (Medium Staple)

Hike in MSP (%)

59,055 65,191

72,402 72,423

127,748

33.0

10.4 11.1

0.0

76.4

0

10

20

30

40

50

60

70

80

90

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

FY17

FY18

FY19

FY20

FY21

MGNREGS outlay (Rs Cr - LHS) Growth (% - RHS)

August 18, 2021 4

Vie

wp

oin

t

Powered by the Sharekhan3R Research Philosophy

Source: Industry, TMA, Sharekhan Research

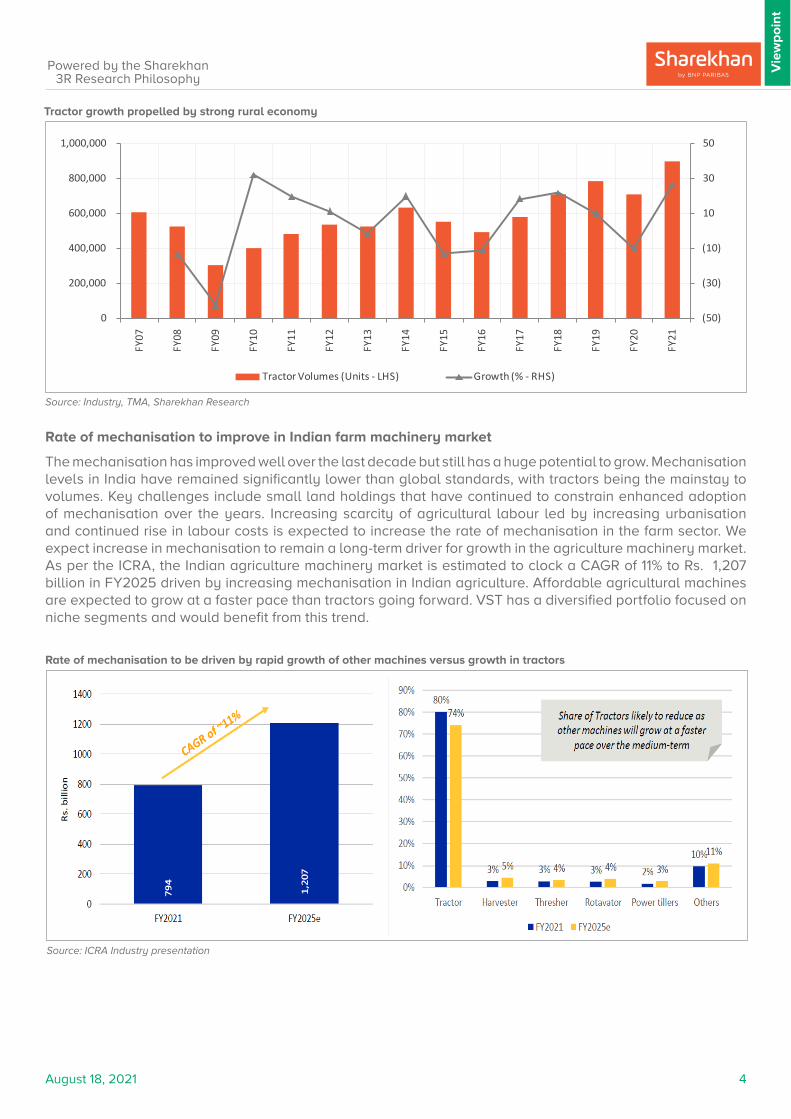

Tractor growth propelled by strong rural economy

Rate of mechanisation to improve in Indian farm machinery market

The mechanisation has improved well over the last decade but still has a huge potential to grow. Mechanisation levels in India have remained significantly lower than global standards, with tractors being the mainstay to volumes. Key challenges include small land holdings that have continued to constrain enhanced adoption of mechanisation over the years. Increasing scarcity of agricultural labour led by increasing urbanisation and continued rise in labour costs is expected to increase the rate of mechanisation in the farm sector. We expect increase in mechanisation to remain a long-term driver for growth in the agriculture machinery market. As per the ICRA, the Indian agriculture machinery market is estimated to clock a CAGR of 11% to Rs. 1,207 billion in FY2025 driven by increasing mechanisation in Indian agriculture. Affordable agricultural machines are expected to grow at a faster pace than tractors going forward. VST has a diversified portfolio focused on niche segments and would benefit from this trend.

Source: ICRA Industry presentation

Rate of mechanisation to be driven by rapid growth of other machines versus growth in tractors

(50)

(30)

(10)

10

30

50

0

200,000

400,000

600,000

800,000

1,000,000 FY

07

FY08

FY09

FY10

FY11

FY12

FY13

FY14

FY15

FY16

FY17

FY18

FY19

FY20

FY21

Tractor Volumes (Units - LHS) Growth (% - RHS)

August 18, 2021 5

Vie

wp

oin

t

Powered by the Sharekhan3R Research Philosophy

Robust brand image among small & marginal farmers with strong market share in niche products

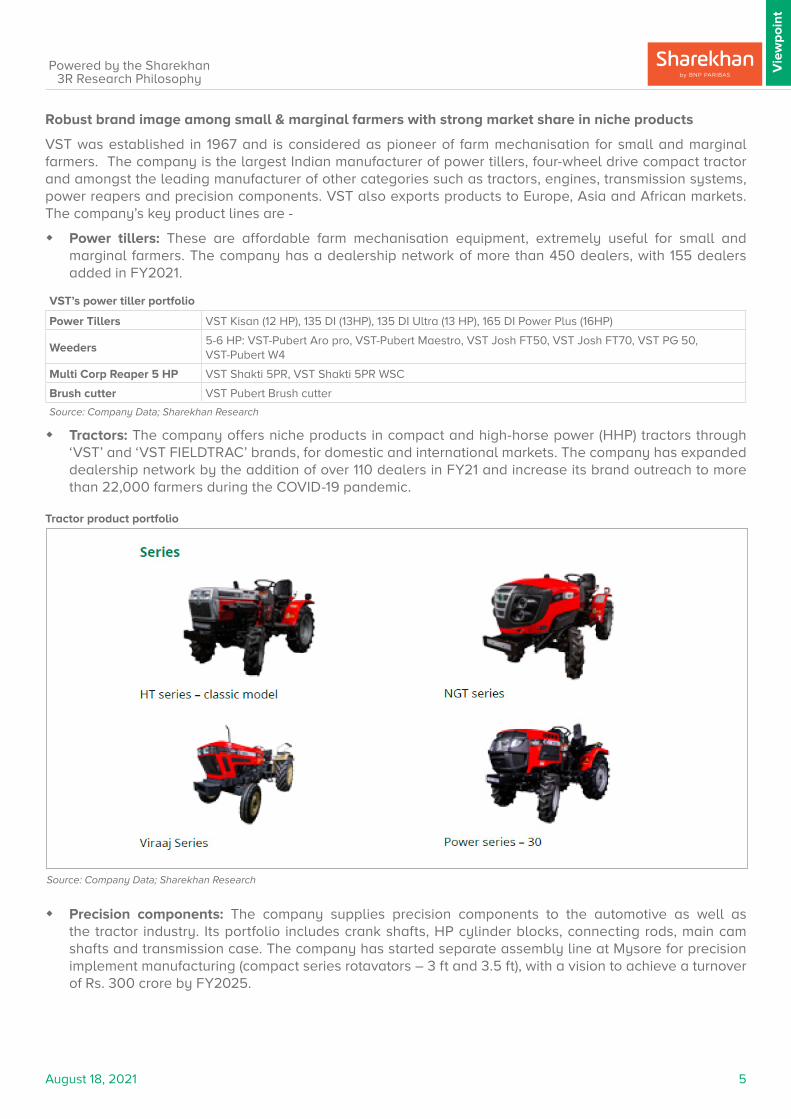

VST was established in 1967 and is considered as pioneer of farm mechanisation for small and marginal farmers. The company is the largest Indian manufacturer of power tillers, four-wheel drive compact tractor and amongst the leading manufacturer of other categories such as tractors, engines, transmission systems, power reapers and precision components. VST also exports products to Europe, Asia and African markets. The company’s key product lines are -

� Power tillers: These are affordable farm mechanisation equipment, extremely useful for small and marginal farmers. The company has a dealership network of more than 450 dealers, with 155 dealers added in FY2021.

VST’s power tiller portfolio

Power Tillers VST Kisan (12 HP), 135 DI (13HP), 135 DI Ultra (13 HP), 165 DI Power Plus (16HP)

Weeders5-6 HP: VST-Pubert Aro pro, VST-Pubert Maestro, VST Josh FT50, VST Josh FT70, VST PG 50, VST-Pubert W4

Multi Corp Reaper 5 HP VST Shakti 5PR, VST Shakti 5PR WSC

Brush cutter VST Pubert Brush cutter

Source: Company Data; Sharekhan Research

� Tractors: The company offers niche products in compact and high-horse power (HHP) tractors through ‘VST’ and ‘VST FIELDTRAC’ brands, for domestic and international markets. The company has expanded dealership network by the addition of over 110 dealers in FY21 and increase its brand outreach to more than 22,000 farmers during the COVID-19 pandemic.

Source: Company Data; Sharekhan Research

Tractor product portfolio

� Precision components: The company supplies precision components to the automotive as well as the tractor industry. Its portfolio includes crank shafts, HP cylinder blocks, connecting rods, main cam shafts and transmission case. The company has started separate assembly line at Mysore for precision implement manufacturing (compact series rotavators – 3 ft and 3.5 ft), with a vision to achieve a turnover of Rs. 300 crore by FY2025.

August 18, 2021 6

Vie

wp

oin

t

Powered by the Sharekhan3R Research Philosophy

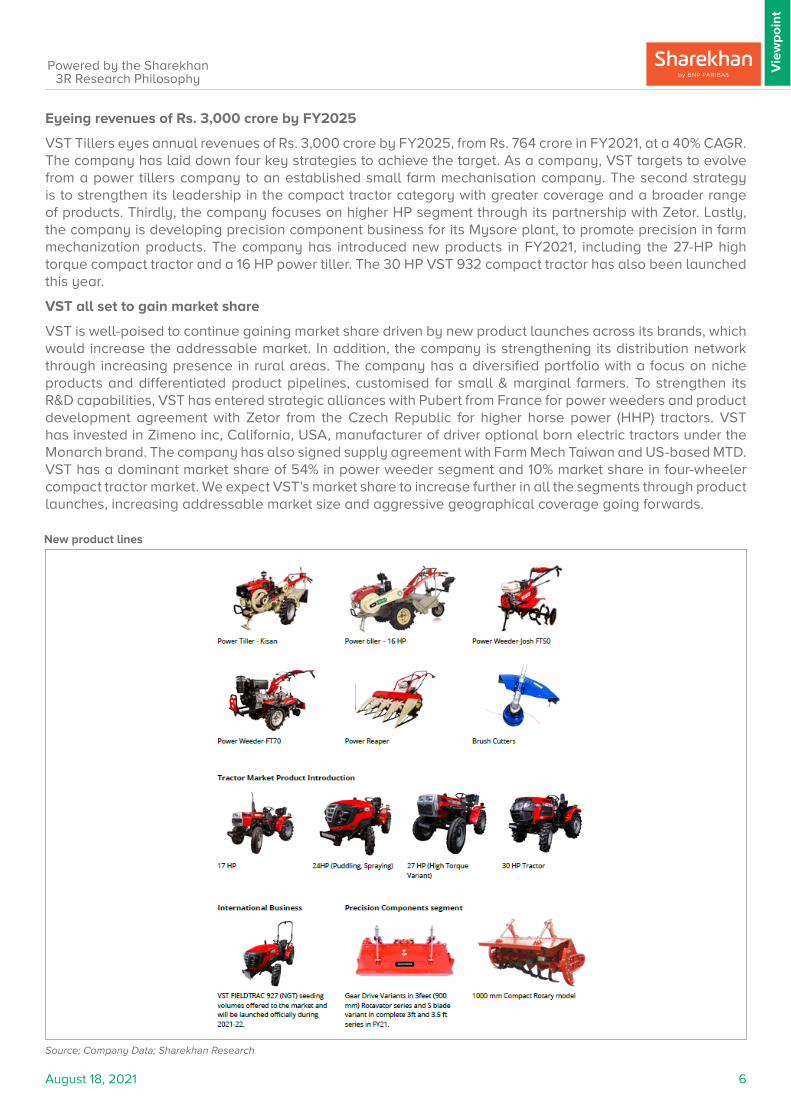

Eyeing revenues of Rs. 3,000 crore by FY2025

VST Tillers eyes annual revenues of Rs. 3,000 crore by FY2025, from Rs. 764 crore in FY2021, at a 40% CAGR. The company has laid down four key strategies to achieve the target. As a company, VST targets to evolve from a power tillers company to an established small farm mechanisation company. The second strategy is to strengthen its leadership in the compact tractor category with greater coverage and a broader range of products. Thirdly, the company focuses on higher HP segment through its partnership with Zetor. Lastly, the company is developing precision component business for its Mysore plant, to promote precision in farm mechanization products. The company has introduced new products in FY2021, including the 27-HP high torque compact tractor and a 16 HP power tiller. The 30 HP VST 932 compact tractor has also been launched this year.

VST all set to gain market share

VST is well-poised to continue gaining market share driven by new product launches across its brands, which would increase the addressable market. In addition, the company is strengthening its distribution network through increasing presence in rural areas. The company has a diversified portfolio with a focus on niche products and differentiated product pipelines, customised for small & marginal farmers. To strengthen its R&D capabilities, VST has entered strategic alliances with Pubert from France for power weeders and product development agreement with Zetor from the Czech Republic for higher horse power (HHP) tractors. VST has invested in Zimeno inc, California, USA, manufacturer of driver optional born electric tractors under the Monarch brand. The company has also signed supply agreement with Farm Mech Taiwan and US-based MTD. VST has a dominant market share of 54% in power weeder segment and 10% market share in four-wheeler compact tractor market. We expect VST’s market share to increase further in all the segments through product launches, increasing addressable market size and aggressive geographical coverage going forwards.

Source: Company Data; Sharekhan Research

New product lines

August 18, 2021 7

Vie

wp

oin

t

Powered by the Sharekhan3R Research Philosophy

Exports remain a key focus area

In the overseas market, the company has offering of its complete range of VST Tractors and VST FIELDTRAC. VST’s focus has been on Europe, Africa & Asia. The company has established significant presence in Europe with distribution in France, Germany, Netherland, Spain, Portugal, Poland, Romania, Bulgaria etc. The company has over 10% market share in France in greater than 30 HP segment. In the export market, the company has collaborated with eminent global partners such as Monarch, Pubert France and Zetor. The company has strengthened its distributor network across various countries including Germany, Hungary, Nepal, Bangladesh, Sri Lanka, Guinea, Tunisia, Liberia and Congo. In FY2021, VST added 42 new dealers in Europe and 10 new dealers in Asia & Africa. The company plans to build the VST brand in international markets in FY22 through online and offline marketing activities. Social media campaigns were also undertaken for strengthening its FILEDTRAC brand in Europe to increase reach in existing and new markets.

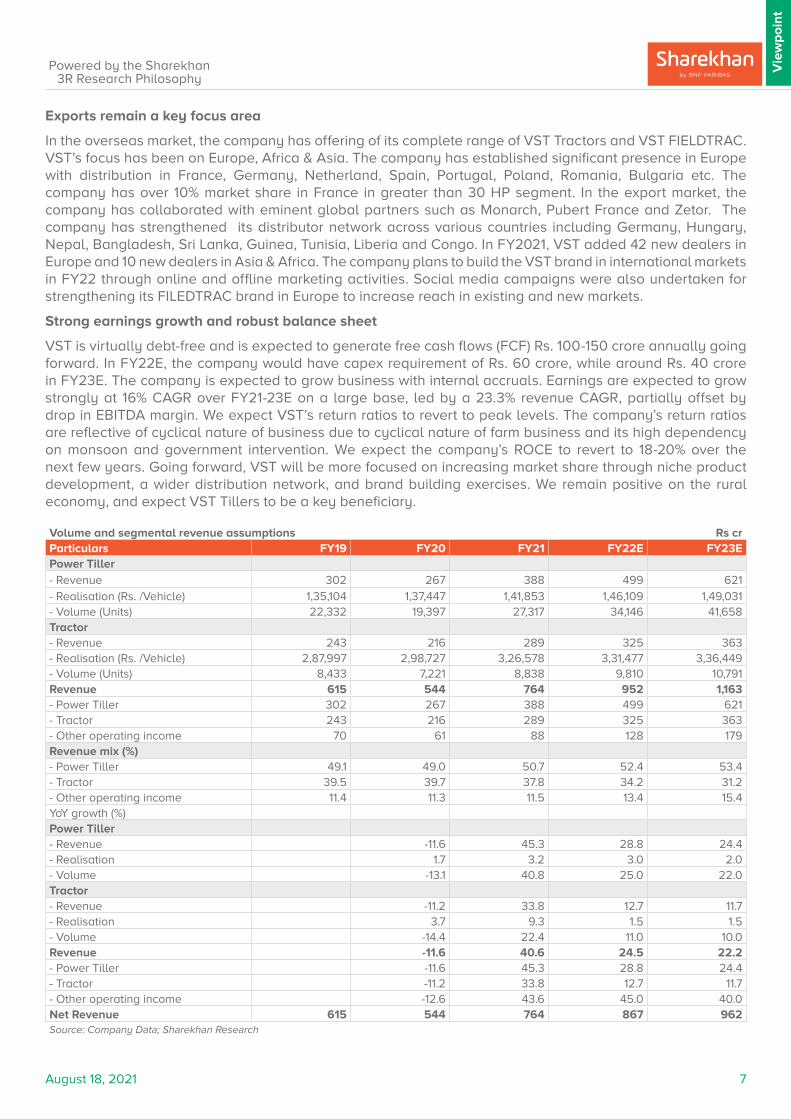

Strong earnings growth and robust balance sheet

VST is virtually debt-free and is expected to generate free cash flows (FCF) Rs. 100-150 crore annually going forward. In FY22E, the company would have capex requirement of Rs. 60 crore, while around Rs. 40 crore in FY23E. The company is expected to grow business with internal accruals. Earnings are expected to grow strongly at 16% CAGR over FY21-23E on a large base, led by a 23.3% revenue CAGR, partially offset by drop in EBITDA margin. We expect VST’s return ratios to revert to peak levels. The company’s return ratios are reflective of cyclical nature of business due to cyclical nature of farm business and its high dependency on monsoon and government intervention. We expect the company’s ROCE to revert to 18-20% over the next few years. Going forward, VST will be more focused on increasing market share through niche product development, a wider distribution network, and brand building exercises. We remain positive on the rural economy, and expect VST Tillers to be a key beneficiary.

Volume and segmental revenue assumptions Rs crParticulars FY19 FY20 FY21 FY22E FY23EPower Tiller - Revenue 302 267 388 499 621 - Realisation (Rs. /Vehicle) 1,35,104 1,37,447 1,41,853 1,46,109 1,49,031 - Volume (Units) 22,332 19,397 27,317 34,146 41,658 Tractor - Revenue 243 216 289 325 363 - Realisation (Rs. /Vehicle) 2,87,997 2,98,727 3,26,578 3,31,477 3,36,449 - Volume (Units) 8,433 7,221 8,838 9,810 10,791 Revenue 615 544 764 952 1,163 - Power Tiller 302 267 388 499 621 - Tractor 243 216 289 325 363 - Other operating income 70 61 88 128 179 Revenue mix (%) - Power Tiller 49.1 49.0 50.7 52.4 53.4 - Tractor 39.5 39.7 37.8 34.2 31.2 - Other operating income 11.4 11.3 11.5 13.4 15.4 YoY growth (%) Power Tiller - Revenue -11.6 45.3 28.8 24.4- Realisation 1.7 3.2 3.0 2.0- Volume -13.1 40.8 25.0 22.0Tractor - Revenue -11.2 33.8 12.7 11.7- Realisation 3.7 9.3 1.5 1.5- Volume -14.4 22.4 11.0 10.0Revenue -11.6 40.6 24.5 22.2- Power Tiller -11.6 45.3 28.8 24.4- Tractor -11.2 33.8 12.7 11.7- Other operating income -12.6 43.6 45.0 40.0Net Revenue 615 544 764 867 962 Source: Company Data; Sharekhan Research

August 18, 2021 8

Vie

wp

oin

t

Powered by the Sharekhan3R Research Philosophy

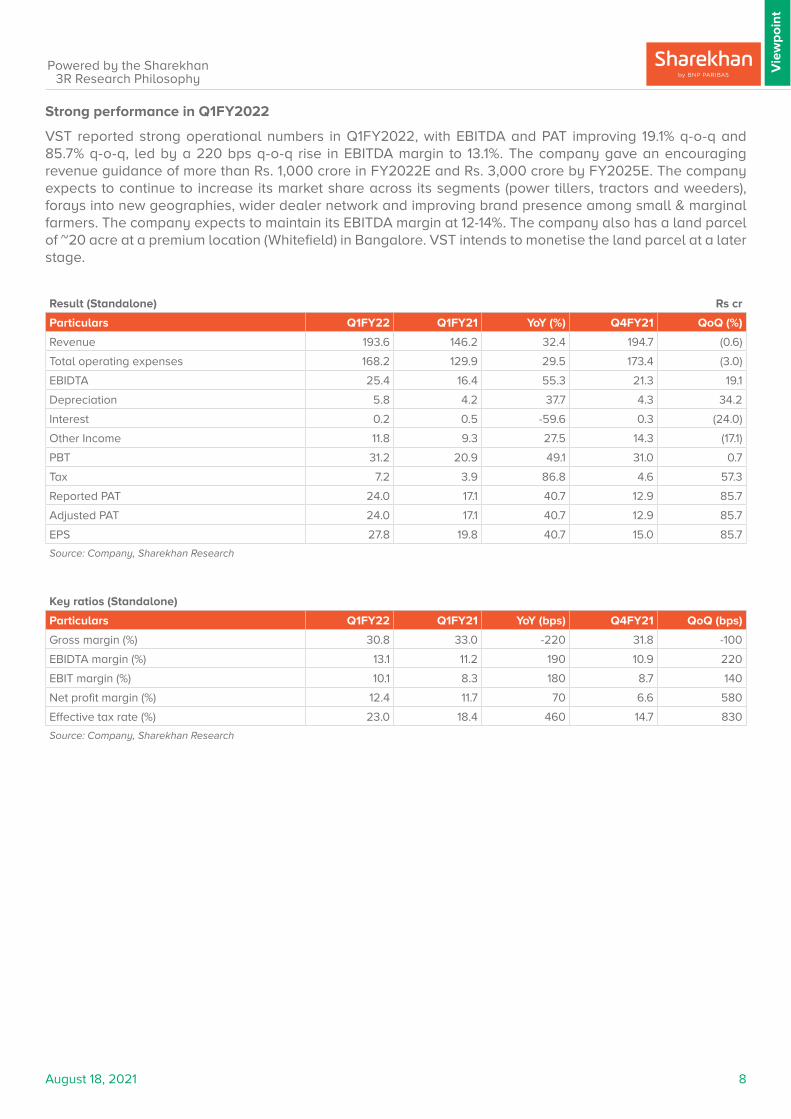

Strong performance in Q1FY2022

VST reported strong operational numbers in Q1FY2022, with EBITDA and PAT improving 19.1% q-o-q and 85.7% q-o-q, led by a 220 bps q-o-q rise in EBITDA margin to 13.1%. The company gave an encouraging revenue guidance of more than Rs. 1,000 crore in FY2022E and Rs. 3,000 crore by FY2025E. The company expects to continue to increase its market share across its segments (power tillers, tractors and weeders), forays into new geographies, wider dealer network and improving brand presence among small & marginal farmers. The company expects to maintain its EBITDA margin at 12-14%. The company also has a land parcel of ~20 acre at a premium location (Whitefield) in Bangalore. VST intends to monetise the land parcel at a later stage.

Result (Standalone) Rs cr

Particulars Q1FY22 Q1FY21 YoY (%) Q4FY21 QoQ (%)

Revenue 193.6 146.2 32.4 194.7 (0.6)

Total operating expenses 168.2 129.9 29.5 173.4 (3.0)

EBIDTA 25.4 16.4 55.3 21.3 19.1

Depreciation 5.8 4.2 37.7 4.3 34.2

Interest 0.2 0.5 -59.6 0.3 (24.0)

Other Income 11.8 9.3 27.5 14.3 (17.1)

PBT 31.2 20.9 49.1 31.0 0.7

Tax 7.2 3.9 86.8 4.6 57.3

Reported PAT 24.0 17.1 40.7 12.9 85.7

Adjusted PAT 24.0 17.1 40.7 12.9 85.7

EPS 27.8 19.8 40.7 15.0 85.7

Source: Company, Sharekhan Research

Key ratios (Standalone)

Particulars Q1FY22 Q1FY21 YoY (bps) Q4FY21 QoQ (bps)

Gross margin (%) 30.8 33.0 -220 31.8 -100

EBIDTA margin (%) 13.1 11.2 190 10.9 220

EBIT margin (%) 10.1 8.3 180 8.7 140

Net profit margin (%) 12.4 11.7 70 6.6 580

Effective tax rate (%) 23.0 18.4 460 14.7 830

Source: Company, Sharekhan Research

August 18, 2021 9

Vie

wp

oin

t

Powered by the Sharekhan3R Research Philosophy

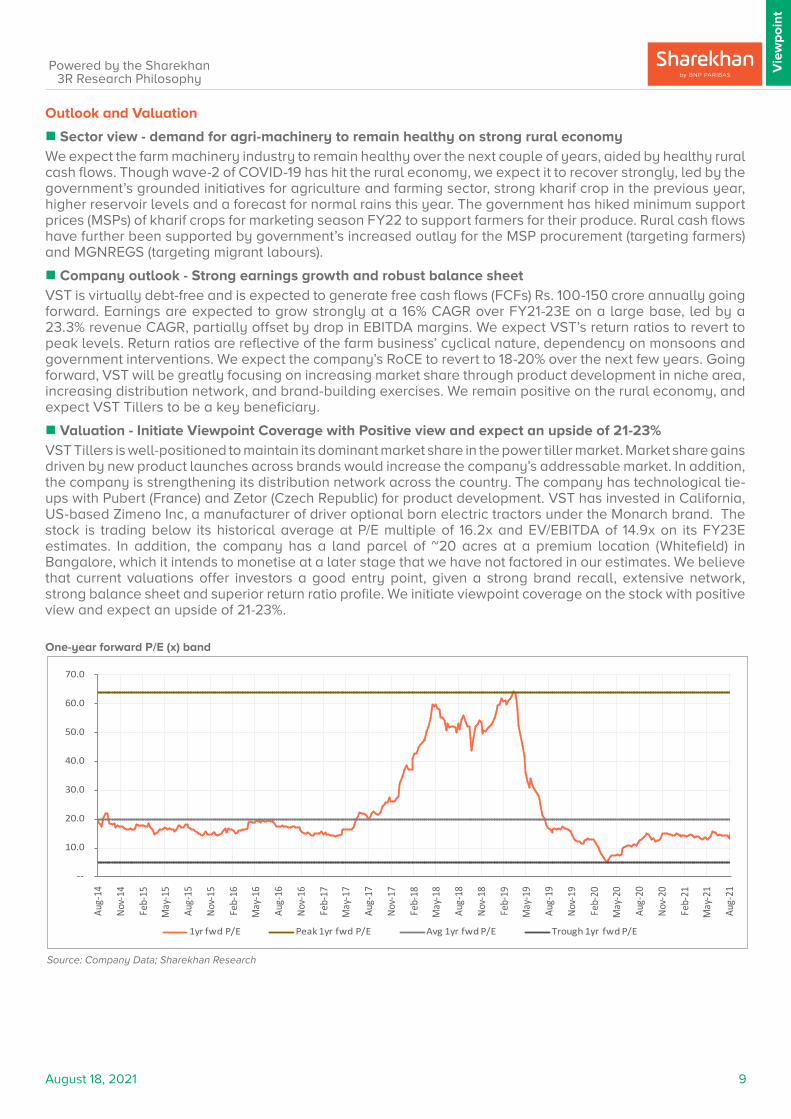

Outlook and Valuation

n Sector view - demand for agri-machinery to remain healthy on strong rural economy We expect the farm machinery industry to remain healthy over the next couple of years, aided by healthy rural cash flows. Though wave-2 of COVID-19 has hit the rural economy, we expect it to recover strongly, led by the government’s grounded initiatives for agriculture and farming sector, strong kharif crop in the previous year, higher reservoir levels and a forecast for normal rains this year. The government has hiked minimum support prices (MSPs) of kharif crops for marketing season FY22 to support farmers for their produce. Rural cash flows have further been supported by government’s increased outlay for the MSP procurement (targeting farmers) and MGNREGS (targeting migrant labours).

n Company outlook - Strong earnings growth and robust balance sheetVST is virtually debt-free and is expected to generate free cash flows (FCFs) Rs. 100-150 crore annually going forward. Earnings are expected to grow strongly at a 16% CAGR over FY21-23E on a large base, led by a 23.3% revenue CAGR, partially offset by drop in EBITDA margins. We expect VST’s return ratios to revert to peak levels. Return ratios are reflective of the farm business’ cyclical nature, dependency on monsoons and government interventions. We expect the company’s RoCE to revert to 18-20% over the next few years. Going forward, VST will be greatly focusing on increasing market share through product development in niche area, increasing distribution network, and brand-building exercises. We remain positive on the rural economy, and expect VST Tillers to be a key beneficiary.

n Valuation - Initiate Viewpoint Coverage with Positive view and expect an upside of 21-23% VST Tillers is well-positioned to maintain its dominant market share in the power tiller market. Market share gains driven by new product launches across brands would increase the company’s addressable market. In addition, the company is strengthening its distribution network across the country. The company has technological tie-ups with Pubert (France) and Zetor (Czech Republic) for product development. VST has invested in California, US-based Zimeno Inc, a manufacturer of driver optional born electric tractors under the Monarch brand. The stock is trading below its historical average at P/E multiple of 16.2x and EV/EBITDA of 14.9x on its FY23E estimates. In addition, the company has a land parcel of ~20 acres at a premium location (Whitefield) in Bangalore, which it intends to monetise at a later stage that we have not factored in our estimates. We believe that current valuations offer investors a good entry point, given a strong brand recall, extensive network, strong balance sheet and superior return ratio profile. We initiate viewpoint coverage on the stock with positive view and expect an upside of 21-23%.

One-year forward P/E (x) band

Source: Company Data; Sharekhan Research

--

10.0

20.0

30.0

40.0

50.0

60.0

70.0

Aug-

14

Nov-

14

Feb-

15

May

-15

Aug-

15

Nov-

15

Feb-

16

May

-16

Aug-

16

Nov-

16

Feb-

17

May

-17

Aug-

17

Nov-

17

Feb-

18

May

-18

Aug-

18

Nov-

18

Feb-

19

May

-19

Aug-

19

Nov-

19

Feb-

20

May

-20

Aug-

20

Nov-

20

Feb-

21

May

-21

Aug-

21

1yr fwd P/E Peak 1yr fwd P/E Avg 1yr fwd P/E Trough 1yr fwd P/E

August 18, 2021 10

Vie

wp

oin

t

Powered by the Sharekhan3R Research Philosophy

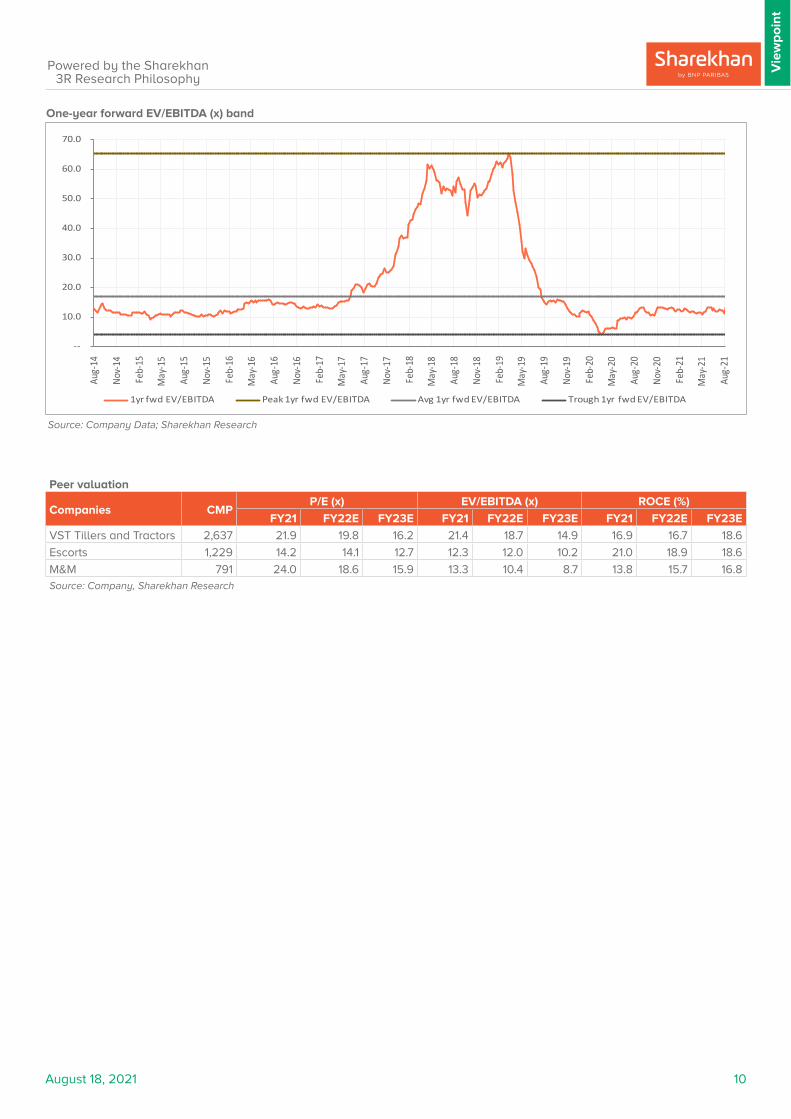

One-year forward EV/EBITDA (x) band

Source: Company Data; Sharekhan Research

Peer valuation

Companies CMPP/E (x) EV/EBITDA (x) ROCE (%)

FY21 FY22E FY23E FY21 FY22E FY23E FY21 FY22E FY23E

VST Tillers and Tractors 2,637 21.9 19.8 16.2 21.4 18.7 14.9 16.9 16.7 18.6

Escorts 1,229 14.2 14.1 12.7 12.3 12.0 10.2 21.0 18.9 18.6

M&M 791 24.0 18.6 15.9 13.3 10.4 8.7 13.8 15.7 16.8 Source: Company, Sharekhan Research

--

10.0

20.0

30.0

40.0

50.0

60.0

70.0

Aug-

14

Nov-

14

Feb-

15

May

-15

Aug-

15

Nov-

15

Feb-

16

May

-16

Aug-

16

Nov-

16

Feb-

17

May

-17

Aug-

17

Nov-

17

Feb-

18

May

-18

Aug-

18

Nov-

18

Feb-

19

May

-19

Aug-

19

Nov-

19

Feb-

20

May

-20

Aug-

20

Nov-

20

Feb-

21

May

-21

Aug-

21

1yr fwd EV/EBITDA Peak 1yr fwd EV/EBITDA Avg 1yr fwd EV/EBITDA Trough 1yr fwd EV/EBITDA

August 18, 2021 11

Vie

wp

oin

t

Powered by the Sharekhan3R Research Philosophy

Source: Company, Sharekhan Research

Revenue and Volume Trend

Source: Company, Sharekhan Research

Revenue Mix (%)

EBITDA and OPM Trend

Source: Company, Sharekhan Research

Financials in charts

Volumes and Realisation Trend

Source: Company, Sharekhan Research

PAT and Growth Trend

Source: Company, Sharekhan Research

Return Ratios Trend

Source: Company, Sharekhan Research

(30)

(15)

0

15

30

45

0

10,000

20,000

30,000

40,000

50,000

60,000

FY19

FY20

FY21

FY22

E

FY23

E

Volumes - Tractor & Power tillers (Units - LHS)

Growth (% - RHS)

Power Tiller, 50.7%

Tractor, 37.8%

Others, 11.5%

(30)(20)(10)0 10 20 30 40 50

0

200

400

600

800

1,000

1,200

1,400

FY19

FY20

FY21

FY22

E

FY23

E

Revenues (Rs Cr - LHS) Growth (% - RHS)

0 2 4 6 8 10 12 14 16

0 20 40 60 80

100 120 140 160

FY19

FY20

FY21

FY22

E

FY23

E

EBITDA (Rs Cr - LHS) OPM (% - RHS)

(100)

0

100

200

300

400

500

600

0 20 40 60 80

100 120 140 160

FY19

FY20

FY21

FY22

E

FY23

E

PAT (Rs Cr - LHS) Growth (% - RHS)

0.0

5.0

10.0

15.0

20.0

FY19 FY20 FY21 FY22E FY23E

ROCE (%) ROE (%)

August 18, 2021 12

Vie

wp

oin

t

Powered by the Sharekhan3R Research Philosophy

About company

VST Tillers and Tractors Limited was established in the year 1967 by the VST Group of companies. The company is the largest Indian manufacturer of power tillers, four-wheel drive compact tractor and amongst the leading manufacturer of the other category such as tractors, engines, transmission, power reaper and precision components. VST also exports products to European, Asian, and African markets.

Investment theme

VST would gain from the revival of rural economy. Higher rabi sowing and water reservoir levels and expectations of a normal monsoon is likely to result in strong growth in agriculture machinery industry. The company is expected to increase its market share in power tillers and tractors segments, led by stronger rural sentiments, new launches and strong brand recall among small and marginal farmers. The company is targeting to increase in addressable markets through technological partnership and focus on niche segments. VST aims to achieve revenue of Rs. 3,000 crore by FY2025 from revenue of Rs. 764 crore in FY21. VST is well positioned to gain from its strategy of product development, brand building exercise and increase in distribution network. Key Risks

� Erratic monsoons can have adverse impact on the growth in the tractor segment.

� Prolonged COVID infection in India would impact economic growth and consequently impact the rural economy.

Additional Data

Key management personnel

V K Surendra Chairman

V P Mahendra Vice Chairman

V T Ravindra Managing Director

Antony Cherukara Chief Executive Officer

Pankaj Khemka Chief Financial OfficerSource: Company

Top 10 shareholders

Sr. No. Holder Name Holding (%)

1 V K Surendra 21.6

2 V P Mahendra 7.3

3 Kotak Small Cap Fund 5.0

4 VST Motors Private Limited 4.1

5 Nippon Life India Trustee 4.0

6 First Sentier Investments Icvc 3.9

7 L&T Mutual Fund Trustee 3.3

8 Mitsubishi Heavy Industries Engine 2.9

9 V V Pravindra 2.6

10 V S Arun 2.5 Source: Bloomberg

Sharekhan Limited, its analyst or dependant(s) of the analyst might be holding or having a position in the companies mentioned in the article.

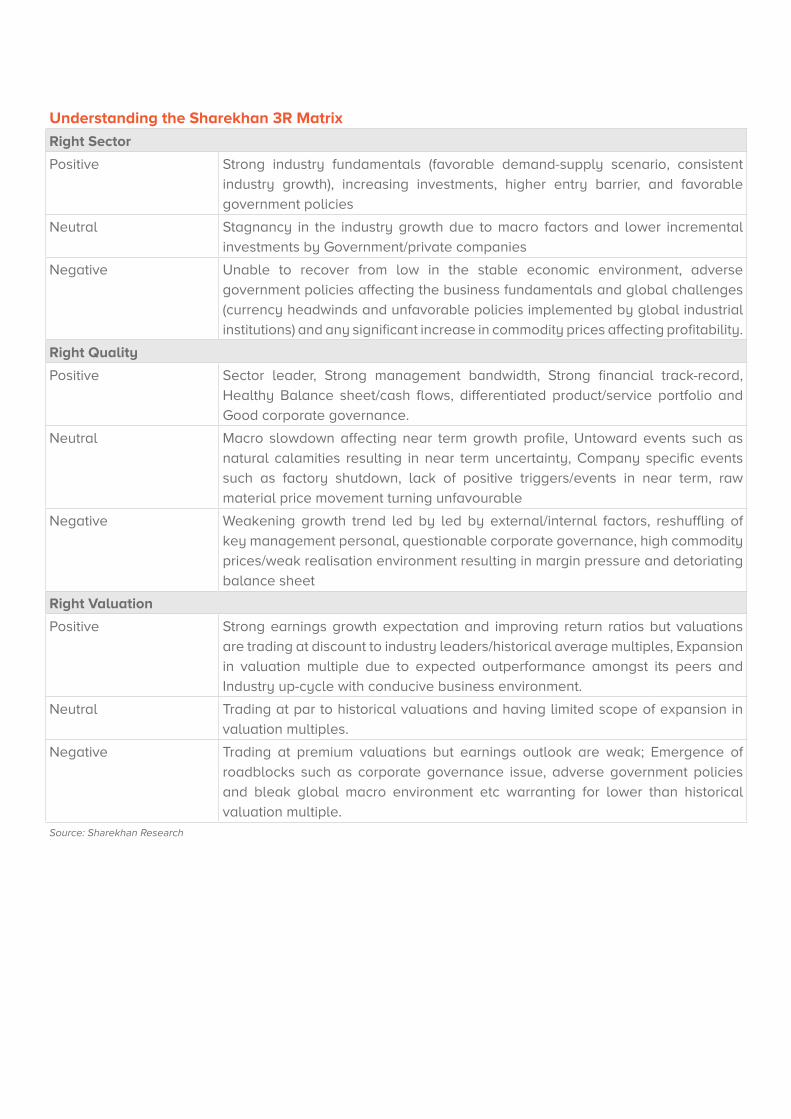

Understanding the Sharekhan 3R Matrix

Right Sector

Positive Strong industry fundamentals (favorable demand-supply scenario, consistent

industry growth), increasing investments, higher entry barrier, and favorable

government policies

Neutral Stagnancy in the industry growth due to macro factors and lower incremental

investments by Government/private companies

Negative Unable to recover from low in the stable economic environment, adverse

government policies affecting the business fundamentals and global challenges

(currency headwinds and unfavorable policies implemented by global industrial

institutions) and any significant increase in commodity prices affecting profitability.

Right Quality

Positive Sector leader, Strong management bandwidth, Strong financial track-record,

Healthy Balance sheet/cash flows, differentiated product/service portfolio and

Good corporate governance.

Neutral Macro slowdown affecting near term growth profile, Untoward events such as

natural calamities resulting in near term uncertainty, Company specific events

such as factory shutdown, lack of positive triggers/events in near term, raw

material price movement turning unfavourable

Negative Weakening growth trend led by led by external/internal factors, reshuffling of

key management personal, questionable corporate governance, high commodity

prices/weak realisation environment resulting in margin pressure and detoriating

balance sheet

Right Valuation

Positive Strong earnings growth expectation and improving return ratios but valuations

are trading at discount to industry leaders/historical average multiples, Expansion

in valuation multiple due to expected outperformance amongst its peers and

Industry up-cycle with conducive business environment.

Neutral Trading at par to historical valuations and having limited scope of expansion in

valuation multiples.

Negative Trading at premium valuations but earnings outlook are weak; Emergence of

roadblocks such as corporate governance issue, adverse government policies

and bleak global macro environment etc warranting for lower than historical

valuation multiple.Source: Sharekhan Research

Disclaimer: This document has been prepared by Sharekhan Ltd. (SHAREKHAN) and is intended for use only by the person or entity to which it is addressed to. This Document may contain confidential and/or privileged material and is not for any type of circulation and any review, retransmission, or any other use is strictly prohibited. This Document is subject to changes without prior notice. This document does not constitute an offer to sell or solicitation for the purchase or sale of any financial instrument or as an official confirmation of any transaction. Though disseminated to all customers who are due to receive the same, not all customers may receive this report at the same time. SHAREKHAN will not treat recipients as customers by virtue of their receiving this report.

The information contained herein is obtained from publicly available data or other sources believed to be reliable and SHAREKHAN has not independently verified the accuracy and completeness of the said data and hence it should not be relied upon as such. While we would endeavour to update the information herein on reasonable basis, SHAREKHAN, its subsidiaries and associated companies, their directors and employees (“SHAREKHAN and affiliates”) are under no obligation to update or keep the information current. Also, there may be regulatory, compliance, or other reasons that may prevent SHAREKHAN and affiliates from doing so. This document is prepared for assistance only and is not intended to be and must not alone be taken as the basis for an investment decision. Recipients of this report should also be aware that past performance is not necessarily a guide to future performance and value of investments can go down as well. The user assumes the entire risk of any use made of this information. Each recipient of this document should make such investigations as it deems necessary to arrive at an independent evaluation of an investment in the securities of companies referred to in this document (including the merits and risks involved), and should consult its own advisors to determine the merits and risks of such an investment. The investment discussed or views expressed may not be suitable for all investors. We do not undertake to advise you as to any change of our views. Affiliates of Sharekhan may have issued other reports that are inconsistent with and reach different conclusions from the information presented in this report.

This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution, publication, availability or use would be contrary to law, regulation or which would subject SHAREKHAN and affiliates to any registration or licensing requirement within such jurisdiction. The securities described herein may or may not be eligible for sale in all jurisdictions or to certain category of investors. Persons in whose possession this document may come are required to inform themselves of and to observe such restriction.

The analyst certifies that the analyst has not dealt or traded directly or indirectly in securities of the company and that all of the views expressed in this document accurately reflect his or her personal views about the subject company or companies and its or their securities and do not necessarily reflect those of SHAREKHAN. The analyst and SHAREKHAN further certifies that neither he or his relatives or Sharekhan associates has any direct or indirect financial interest nor have actual or beneficial ownership of 1% or more in the securities of the company at the end of the month immediately preceding the date of publication of the research report nor have any material conflict of interest nor has served as officer, director or employee or engaged in market making activity of the company. Further, the analyst has also not been a part of the team which has managed or co-managed the public offerings of the company and no part of the analyst’s compensation was, is or will be, directly or indirectly related to specific recommendations or views expressed in this document. Sharekhan Limited or its associates or analysts have not received any compensation for investment banking, merchant banking, brokerage services or any compensation or other benefits from the subject company or from third party in the past twelve months in connection with the research report.

Either, SHAREKHAN or its affiliates or its directors or employees / representatives / clients or their relatives may have position(s), make market, act as principal or engage in transactions of purchase or sell of securities, from time to time or may be materially interested in any of the securities or related securities referred to in this report and they may have used the information set forth herein before publication. SHAREKHAN may from time to time solicit from, or perform investment banking, or other services for, any company mentioned herein. Without limiting any of the foregoing, in no event shall SHAREKHAN, any of its affiliates or any third party involved in, or related to, computing or compiling the information have any liability for any damages of any kind.

Compliance Officer: Mr. Joby John Meledan; Tel: 022-61150000; email id: [email protected];

For any queries or grievances kindly email [email protected] or contact: [email protected]

Registered Office: Sharekhan Limited, 10th Floor, Beta Building, Lodha iThink Techno Campus, Off. JVLR, Opp. Kanjurmarg Railway Station, Kanjurmarg (East), Mumbai – 400042, Maharashtra. Tel: 022 - 61150000. Sharekhan Ltd.: SEBI Regn. Nos.: BSE / NSE / MSEI (CASH / F&O / CD) / MCX - Commodity: INZ000171337; DP: NSDL/CDSL-IN-DP-365-2018; PMS: INP000005786; Mutual Fund: ARN 20669; Research Analyst: INH000006183;

Disclaimer: Client should read the Risk Disclosure Document issued by SEBI & relevant exchanges and the T&C on www.sharekhan.com; Investment in securities market are subject to market risks, read all the related documents carefully before investing.

Know more about our products and services

For Private Circulation only

Related Documents