1 For VPJ Classes – CA Vinod Parakh Jain, Ph/whatsapp:75036305943, website:www.vpjclasses.com VPJ CLASSES By: CA VINOD PARAKH JAIN CA FINAL AUDIT AMENDMENTS MODULE Applicable for Nov. 2016 Exams

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1 For VPJ Classes – CA Vinod Parakh Jain, Ph/whatsapp:75036305943, website:www.vpjclasses.com

VPJ CLASSES

By: CA VINOD PARAKH JAIN

CA FINAL AUDIT AMENDMENTS

MODULE

Applicable for Nov. 2016 Exams

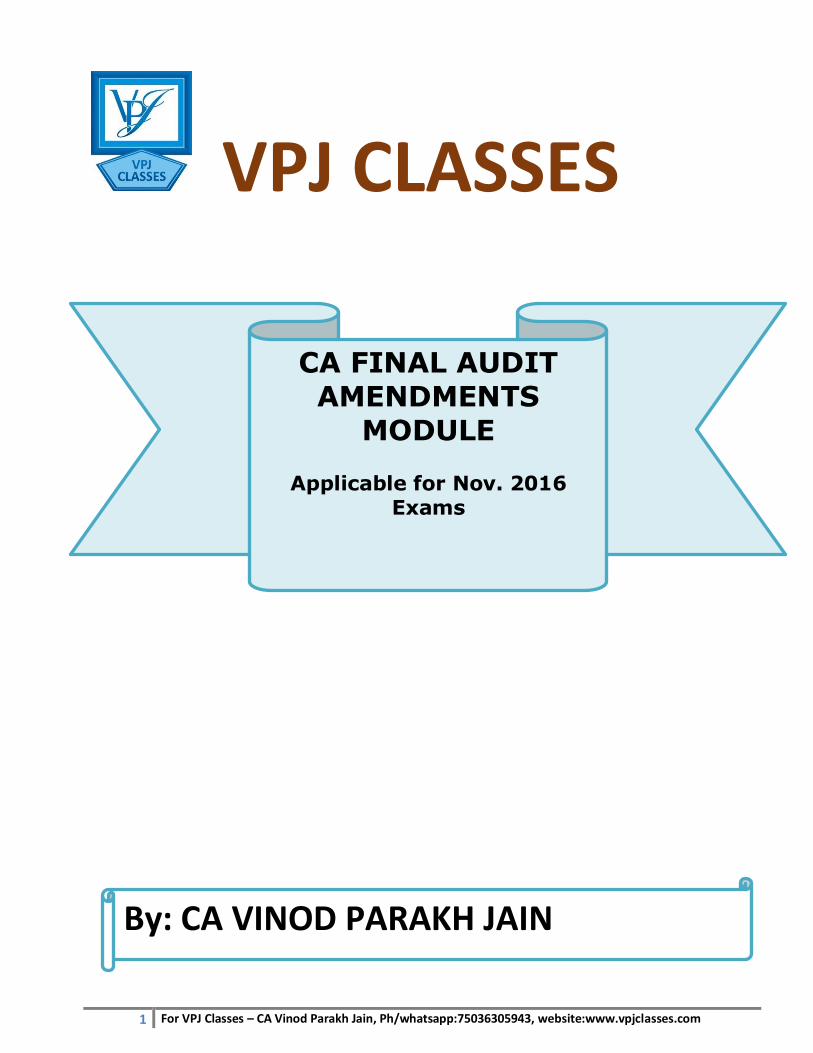

2 For VPJ Classes – CA Vinod Parakh Jain, Ph/whatsapp:75036305943, website:www.vpjclasses.com

INDEX

S.No. PARTICULARS Page No.

1. Professional Ethics 7-14

2. Audit of PSUs 15-24

3. Bank Audit 25-37

4. Audit of General Insurance Companies 38-40

5. Cost Audit 41-46

6. Special Audit Assignments 47-48

7. Audit of NBFCs 49-52

8. Investigation and Due Diligence 53-54

9. Audit under Fiscal Laws 55-58

10. Audit Report 59-62

3 For VPJ Classes – CA Vinod Parakh Jain, Ph/whatsapp:75036305943, website:www.vpjclasses.com

CA VINOD PARAKH JAIN

Ruchika

81 marks Rajesh

74 marks Manish

74 marks Mukesh 73 marks

Himanshu 73 marks

Surbhi 71 marks

Anubhav 71 marks

Nidhi 71 marks

Nitika 70 marks

Vishal 70 marks

Poonam 68 marks

Subrat 68 marks

Ambika

68 marks Priya

67 marks Aman

67 marks Puneet

67 marks Ruchika

67 marks Harsh

66 marks

SPECTACULAR PERFORMANCE IN SUCH A SHORT SPAN OF TIME

EFFECTIVE OUTPUT ORIENTED CLASSES

(Just 48 Classes for IDT & 22 Classes for Audit)

100% COVERAGE OF STUDY MATERIAL PM, SA & RTP Questions ALSO COVERED IN CLASS

4 For VPJ Classes – CA Vinod Parakh Jain, Ph/whatsapp:75036305943, website:www.vpjclasses.com

Kapil

65 marks Sweety

65 marks Aditya

65 marks Arjun

65 marks Amit

65marks Madhav 65 marks

Lalit Dutt 64 marks

Badal 64 marks

Topendra 64 marks

Yash 64 marks

Rahul 64 marks

Kuldeep 64 marks

DHANWAL 64 MARKS

AMIT 63 MARKS

AAMIR 63 MARKS

AANCHAL 63 MARKS

SHREYANS 63 MARKS

MANISH 63 MARKS

Utsaha

62 marks Karan

62 marks Jyoti

62 marks Manish

62 marks Shubhi

62 marks Rohit

62 marks

Chirag

62 marks Aditya

61 marks Rachit

61 marks Sridhar

61 marks Avinav

61 marks Yogesh

61 marks

5 For VPJ Classes – CA Vinod Parakh Jain, Ph/whatsapp:75036305943, website:www.vpjclasses.com

Classes at ITO/Laxmi Nagar; For Details Cnct/Whatsapp:7503630594 Facebook Page- vpjclasses; [email protected]; www.vpj classes.com

Kamal

61 marks Anchal

61 marks Swati

61 marks Anu

61 marks Deepali

60 marks Naresh – 60 marks

Kushna

60 marks Urvi

60 marks Rahul

60 marks Akriti Jain 60 marks

Vikas 60 marks

Abhishek 60 marks

AND MANY MORE………………………………

Mohit 60 marks

Monica 60 marks

Bhawna 60 marks

Akash –3rdrank in uttrakhand

May 2016 Attempt

Ambika Rathi -68 Marks

VPJ Sir PRESENTING LAPTOP TO MUKESH

FOR SCORING

ALL INDIA HIGHEST 73 MARKS

CA VINOD PARAKH JAIN PRESENTING LAPTOPTO HIS STUDENT MUKESH SETHIA FOR SECURING

ALL INDIA HIGHEST 73 MARKS IN AUDIT

6 For VPJ Classes – CA Vinod Parakh Jain, Ph/whatsapp:75036305943, website:www.vpjclasses.com

FOR NOV 2016 / MAY 2017

Daily Morning Batch – Full Coverage Start Date End Date Days Timing Fees 1st Sep. 2016 3rd week of Oct. 2016* Daily 6:45- 10:30 AM 14,000

1st week of Dec.16 End of Jan 2017 Daily 6:45- 10:30 AM 14,000 *For Nov 2016 Attempt Extra Classes will be held to Complete the course by 10th Oct. 20016

DAILY EVENING BATCH-FULL COVERAGE Start Date Completion Date Days Timing Fees

27th Aug. 2016 18th Sep. 2016 Daily 5:30PM– 9:00PM 7,000

CA Final-Audit @ 22 Classes

COMPLETE YOUR CA Final-IDT in Just 1.5 Months- 48 Daily Classes

Comprehensive Coverage of 1100 Pages of Study Material and 350+Questions of PM, SA and RTP covered in Class.

Cover Your Entire Audit in JUST 80 Hours with our EXPERT GUIDANCE and save AT LEAST 240+ Hours of Self Study with One’s Own Limitations

For details : Log on to vpjclasses.com

Ph/Whatsapp: 7503630594

Email:[email protected]

By CA Vinod Parakh Jain

{FCA, DISA, CVO, B.COM (H)} 9 Years Practical Experience across leading

MNC’s

110 Case Studies issued by ICAI for May/Nov 2016 Exams will be

Covered in Class and WE ARE THE ONLY ONE TO DO SO

100% COVERAGE-NOT A FAST TRACK COURSE

With 650+ Questions of PM,RTP, SA are covered in Class

7 For VPJ Classes – CA Vinod Parakh Jain, Ph/whatsapp:75036305943, website:www.vpjclasses.com

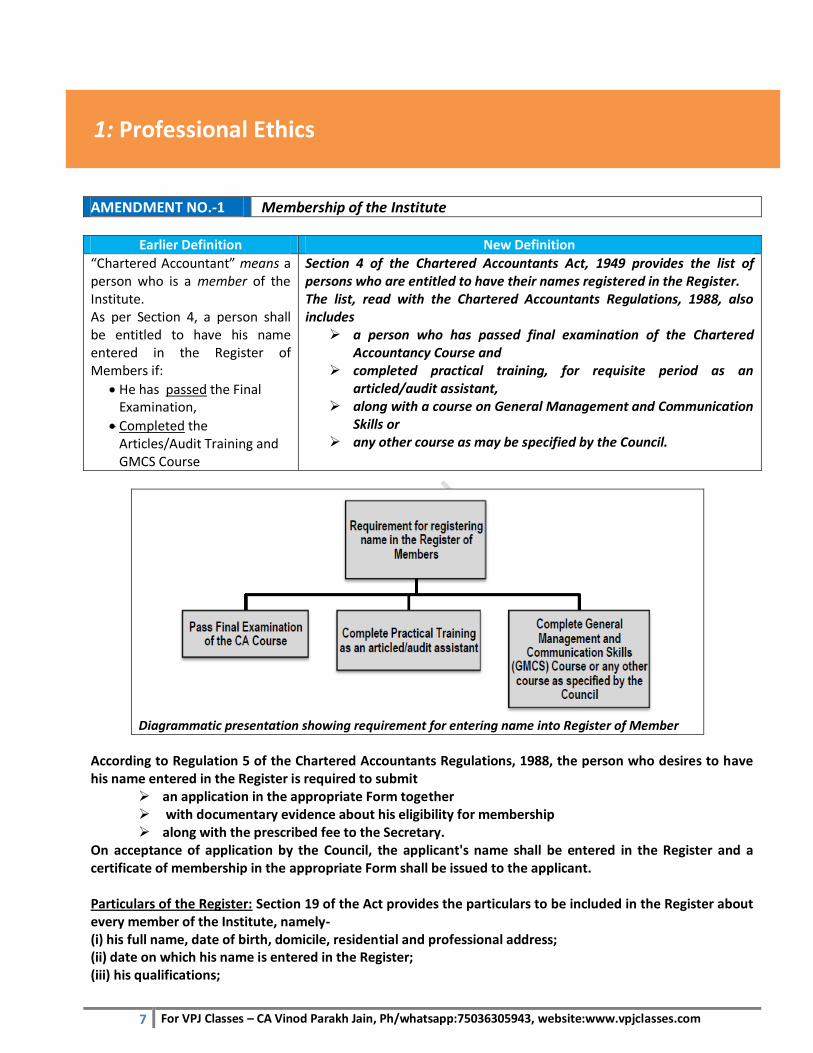

AMENDMENT NO.-1 Membership of the Institute

Earlier Definition New Definition

“Chartered Accountant” means a person who is a member of the Institute. As per Section 4, a person shall be entitled to have his name entered in the Register of Members if:

He has passed the Final Examination,

Completed the Articles/Audit Training and GMCS Course

Section 4 of the Chartered Accountants Act, 1949 provides the list of persons who are entitled to have their names registered in the Register. The list, read with the Chartered Accountants Regulations, 1988, also includes

a person who has passed final examination of the Chartered Accountancy Course and

completed practical training, for requisite period as an articled/audit assistant,

along with a course on General Management and Communication Skills or

any other course as may be specified by the Council.

Diagrammatic presentation showing requirement for entering name into Register of Member

According to Regulation 5 of the Chartered Accountants Regulations, 1988, the person who desires to have his name entered in the Register is required to submit

an application in the appropriate Form together with documentary evidence about his eligibility for membership along with the prescribed fee to the Secretary.

On acceptance of application by the Council, the applicant's name shall be entered in the Register and a certificate of membership in the appropriate Form shall be issued to the applicant. Particulars of the Register: Section 19 of the Act provides the particulars to be included in the Register about every member of the Institute, namely- (i) his full name, date of birth, domicile, residential and professional address; (ii) date on which his name is entered in the Register; (iii) his qualifications;

1: Professional Ethics

8 For VPJ Classes – CA Vinod Parakh Jain, Ph/whatsapp:75036305943, website:www.vpjclasses.com

(iv) whether he holds a certificate of practice (COP); and (v) any other particulars which may be prescribed.

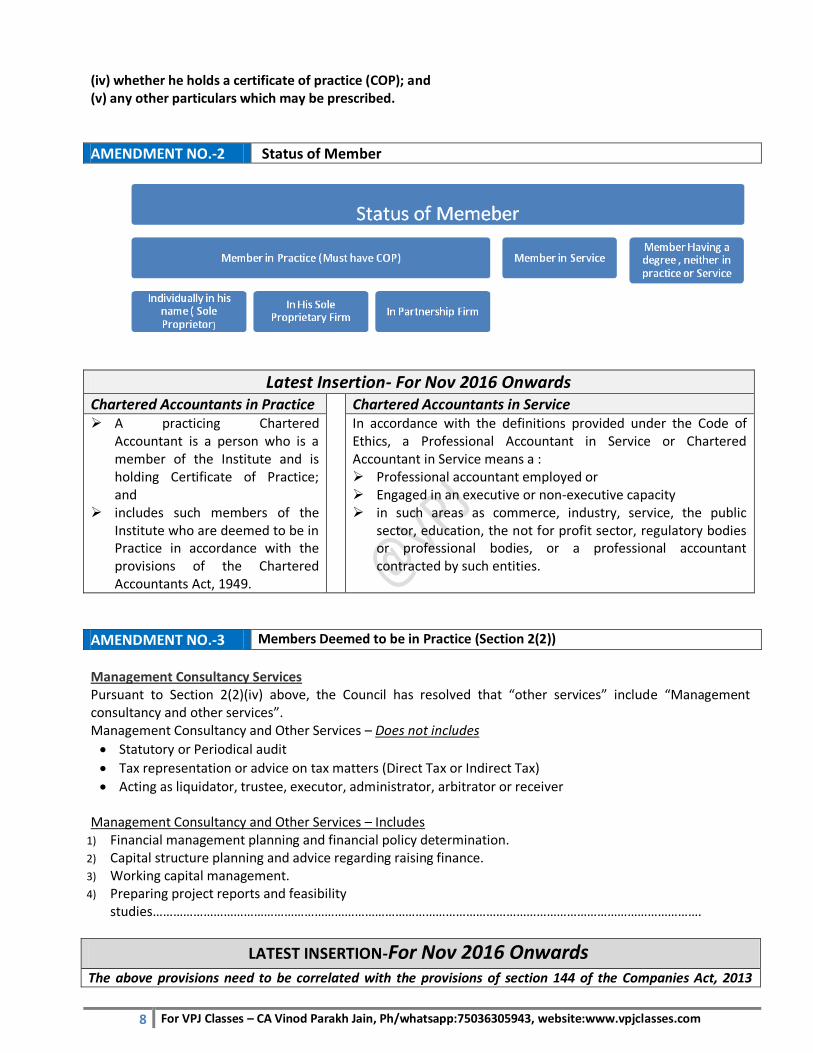

AMENDMENT NO.-2 Status of Member

Latest Insertion- For Nov 2016 Onwards Chartered Accountants in Practice Chartered Accountants in Service A practicing Chartered

Accountant is a person who is a member of the Institute and is holding Certificate of Practice; and

includes such members of the Institute who are deemed to be in Practice in accordance with the provisions of the Chartered Accountants Act, 1949.

In accordance with the definitions provided under the Code of Ethics, a Professional Accountant in Service or Chartered Accountant in Service means a : Professional accountant employed or Engaged in an executive or non-executive capacity in such areas as commerce, industry, service, the public

sector, education, the not for profit sector, regulatory bodies or professional bodies, or a professional accountant contracted by such entities.

AMENDMENT NO.-3 Members Deemed to be in Practice (Section 2(2))

Management Consultancy Services Pursuant to Section 2(2)(iv) above, the Council has resolved that “other services” include “Management consultancy and other services”. Management Consultancy and Other Services – Does not includes

Statutory or Periodical audit

Tax representation or advice on tax matters (Direct Tax or Indirect Tax)

Acting as liquidator, trustee, executor, administrator, arbitrator or receiver Management Consultancy and Other Services – Includes

1) Financial management planning and financial policy determination. 2) Capital structure planning and advice regarding raising finance. 3) Working capital management. 4) Preparing project reports and feasibility

studies……………………………………………………………………………………………………………………………………………….

LATEST INSERTION-For Nov 2016 Onwards

The above provisions need to be correlated with the provisions of section 144 of the Companies Act, 2013

9 For VPJ Classes – CA Vinod Parakh Jain, Ph/whatsapp:75036305943, website:www.vpjclasses.com

which prohibits an auditor of the company from rendering certain services directly or indirectly to the company or its holding company or its subsidiary company.

AMENDMENT NO.-4 Cancellation and Restoration of Certificate of Practice

Cancellation [Regulation 10]

Certificate of Practice (COP) shall be liable for cancellation, if: (i) the name of the holder of the certificate is removed from the Register; or (ii) the Council is satisfied, after giving an opportunity of being heard to the person concerned, that such certificate was issued on the basis of incorrect, misleading or false information, or by mistake or inadvertence; or (iii) a member has ceased to practise; or (iv) a member has not paid annual fee for certificate of practice till 30th day of September of the relevant year. Where a COP is cancelled, the holder shall surrender the same to the Secretary.

Restoration of COP [Regulation 11]

On an application made in the approved Form and on payment of such fee, the Council may restore the COP with effect from the date on which it was cancelled, to a member whose certificate has been cancelled due to non-payment of the annual fee for the COP and whose application, complete in all respects, together with the fee, is received by the Secretary before the expiry of the relevant year.

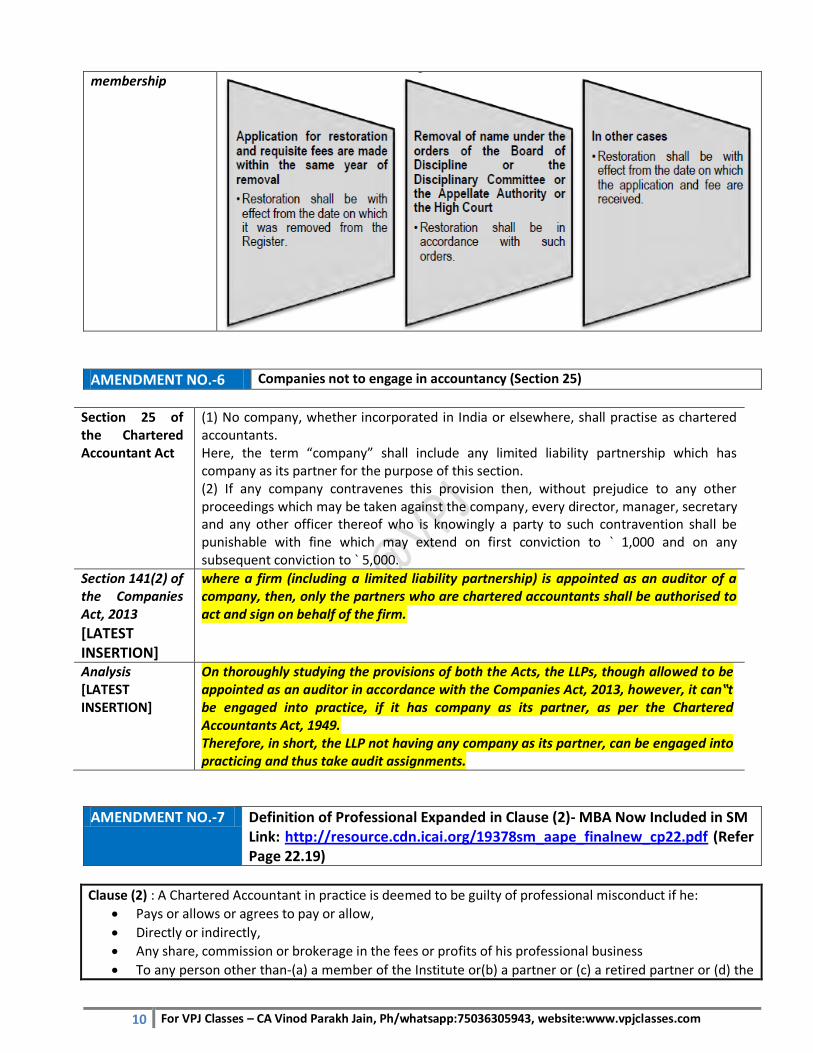

AMENDMENT NO.-5 Removal of Name from the Register & Restoration of Membership

Removal of Name from the Register

As per section 20 of the Act, the Council may remove, from the Register, the name of any member of the Institute in the following cases- (i) who is dead; or (ii) from whom a request has been received to that effect; or (iii) who has not paid any prescribed fee required to be paid by him; or (iv) who is found to have been subject at the time when his name was entered in the Register, or who at any time thereafter has become subject, to any of the disabilities mentioned in Section 8, or who for any other reason has ceased to be entitled to have his name borne on the Register. The Council shall remove the name of any member from the Register in respect of whom an order has been passed under this Act removing him from membership of the Institute. If the name of any member has been removed from the Register for non-payment of prescribed fee as required to be paid by him, then, on receipt of an application, his name may be entered again in the Register on payment of the arrears of annual fee and entrance fee along with such additional fee, as may be determined by the Council.

Restoration of Membership

In addition to the provisions of the section 20 of the Chartered Accountants Act, 1949 (as discussed in above Para), Regulation 19 of the Chartered Accountants Regulations, 1988, as well states that the name of the member may be restored by the Council in the Register on an application, in the appropriate Form, received in this behalf whose name has been removed from the Register for non-payment of prescribed fee as required to be paid by him, if he is otherwise eligible to such membership, on his paying the arrears of annual membership fee, entrance fee and additional fee determined by the Council under the Act.

Effective date in case of restoration of cancelled

However, the effective date in case of restoration of cancelled membership, in different situations, shall be in the following manner:

10 For VPJ Classes – CA Vinod Parakh Jain, Ph/whatsapp:75036305943, website:www.vpjclasses.com

membership

AMENDMENT NO.-6 Companies not to engage in accountancy (Section 25)

Section 25 of the Chartered Accountant Act

(1) No company, whether incorporated in India or elsewhere, shall practise as chartered accountants. Here, the term “company” shall include any limited liability partnership which has company as its partner for the purpose of this section. (2) If any company contravenes this provision then, without prejudice to any other proceedings which may be taken against the company, every director, manager, secretary and any other officer thereof who is knowingly a party to such contravention shall be punishable with fine which may extend on first conviction to ` 1,000 and on any subsequent conviction to ` 5,000.

Section 141(2) of the Companies Act, 2013

[LATEST INSERTION]

where a firm (including a limited liability partnership) is appointed as an auditor of a company, then, only the partners who are chartered accountants shall be authorised to act and sign on behalf of the firm.

Analysis [LATEST INSERTION]

On thoroughly studying the provisions of both the Acts, the LLPs, though allowed to be appointed as an auditor in accordance with the Companies Act, 2013, however, it can‟t be engaged into practice, if it has company as its partner, as per the Chartered Accountants Act, 1949. Therefore, in short, the LLP not having any company as its partner, can be engaged into practicing and thus take audit assignments.

AMENDMENT NO.-7 Definition of Professional Expanded in Clause (2)- MBA Now Included in SM Link: http://resource.cdn.icai.org/19378sm_aape_finalnew_cp22.pdf (Refer Page 22.19)

Clause (2) : A Chartered Accountant in practice is deemed to be guilty of professional misconduct if he:

Pays or allows or agrees to pay or allow,

Directly or indirectly,

Any share, commission or brokerage in the fees or profits of his professional business

To any person other than-(a) a member of the Institute or(b) a partner or (c) a retired partner or (d) the

11 For VPJ Classes – CA Vinod Parakh Jain, Ph/whatsapp:75036305943, website:www.vpjclasses.com

legal representative of a deceased partner, or (e) a member of any other professional body or (f) with such other persons having such qualification as may be prescribed, for the purpose of rendering such professional services from to time in or outside India Explanation - In this item, “partner” includes a person residing outside India with whom a CAIP has entered into partnership which is not in contravention of item (4) of this Part

Notified Professional Bodies Professionals Qualified in India

The Council has prescribed [Regulation 53A(1) of the Chartered Accountants Regulations, 1988] the professional bodies, which are as under:- (a) The Institute of Company Secretaries of India established under the Company Secretaries Act, 1980. (b) The Institute of Cost & Works Accountants of India established under the Cost & Works Accountants Act, 1959. (c) Bar Council of India established under the Advocates Act, 1961. (d) The Indian Institute of Architects established under the Architects Act, 1972.

(e) The Institute of Actuaries of India established under the Actuaries Act, 2006.

Further, the Council has also prescribed [Regulation 53A(3) of the Chartered Accountants Regulations, 1988] the persons qualified in India, which are as under: (i) Company Secretary within the meaning of the Company Secretaries Act, 1980; (ii) Cost Accountant within the meaning of the Cost and Works Accountants Act, 1959; (iii) Actuary within the meaning of the Actuaries Act, 2006; (iv) Bachelor in Engineering from a University established by law or an Institution recognised by law; (v) Bachelor in Technology from a University established by law or an institution recognised by law; (vi) Bachelor in Architecture from a University established by law or an institution recognised by law; (vii) Bachelor in Law from a University established by law or an institution recognised by law; (viii) Master in Business Administration from Universities established by law or technical institutions recognised by All India Council for Technical Education.

AMENDMENT NO.-8 Definition of Professional Bodies Expanded in Clause (4)- MBA Now Included in SM Link: http://resource.cdn.icai.org/19378sm_aape_finalnew_cp22.pdf (Refer Page 22.21)

Clause (4) -A Chartered Accountant in practice is deemed to be guilty of professional misconduct if he enters into partnership, in or outside India, with any person other than:

(a) a CAIP or (b) Member of any other professional body having prescribed qualifications (c) A person resident outside India who but for his residence abroad would be entitled to be registered as

a member u/s 4(1)(v) or (d) Whose qualifications are recognized by the CG/ Council for the purpose of permitting such

partnerships:

12 For VPJ Classes – CA Vinod Parakh Jain, Ph/whatsapp:75036305943, website:www.vpjclasses.com

Professionals notified for entering into partnership

Clause 4 of the Part 1 of the first schedule

The Council has prescribed Regulation 53A(3) (as discussed under clause (2) of this part) and Regulation 53B of the Chartered Accountants Regulations, 1988 for the persons qualified and the professional bodies. The Regulation 53B prescribes the membership of following professional bodies for entering into partnership: (a) Company Secretary, member, The Institute of Company Secretaries of India, established under the Company Secretaries Act, 1980; (b) Cost Accountant, member, The Institute of Cost and Works Accountants of India established under the Cost and Works Accountants Act, 1959; (c) Advocate, member, Bar Council of India established under the Advocates Act, 1961; (d) Engineer, member, The Institution of Engineers, or Engineering from a University established by law or an institution recognized by law. (e) Architect, member, The Indian Institute of Architects established under the Architects Act, 1972; (f) Actuary, member, The Institute of Actuaries of India, established under the Actuaries Act, 2006.

AMENDMENT NO.-9 Definition of Relative to be considered as Per AS-18 and not as Per Companies Act

Council General Guidelines

Opinion on FS when there is substantial interest

A member of shall not express his opinion on FS of any business or enterprise in which one or more persons who are his “relatives” within the meaning Section 6 of the Companies Act, 1956 (now Section 2(77) of the Companies Act, 2013) Accounting Standard (AS-18) (Insertion) have, either by themselves or in conjunction with such member, a substantial interest in the said business or enterprise Explanation: “substantial interest” shall have the same meaning as is assigned thereto under Appendix (9) to the Chartered Accountants Regulations, 1988

AMENDMENT NO.-10 Clarification on Limits for Tax Audit

Tax Audit assignments under Section 44 AB of the Income-tax Act, 1961

A member of the Institute in practice shall not accept, in a financial year, more than the 45 tax audit assignments in a Financial Year. Further additional points in this regards are:

Situations Limits

For Individuals CA’s or Proprietary firms 60 Tax Audits

For Partnership Firm 60 Tax Audits per partner of the Firm

When a CA is a partner in a number of a firms

60 Tax Audit on his account in all the firms taken together in which he is a partner or proprietor.

Where the partner of a Firm also holds office in his individual capacity

60 Tax Audits in his individual capacity and all Firms taken together.

*According to a clarification on Tax Audit Assignments by Committee on Ethical Standards (CES) of the Institute, if there are 10 partners in a firm of Chartered Accountants in practice, then all the partners of the firm can collectively sign 600 tax audit reports. This maximum limit of 600 tax audit assignments may be distributed between the partners in any manner whatsoever. For instance, 1 partner can individually sign 600 tax audit reports in case remaining 9 partners are not signing any tax audit report.(Insertion) Note: Audits conducted under Section 44AD, 44AE and 44AF of the Income Tax Act, 1961

13 For VPJ Classes – CA Vinod Parakh Jain, Ph/whatsapp:75036305943, website:www.vpjclasses.com

shall not be taken into account for computing the specified limits of tax audit assignments

Tax Audit assignments in a FY includes tax audit assignments of both corporate & non corporate assesse

Each year’s audit would be taken as a separate assignment. Audit of the head office and branch offices of a concern shall be regarded as one tax

audit assignment. A CA in part time practice practicing as a partner of a firm shall not be taken into

account for computing the aforesaid limit. CAIP shall maintain a record of the tax audit assignments accepted by him for each FY.

AMENDMENT NO.-10 Specified no. of Audit Assignment

Specified number of audit assignments

A member of the Institute in practice shall not hold at any time appointment of more than the 30 audit assignments of Private and other “specified number of audit assignments ”Companies u/s 224 and/or Section 228 of the Companies Act, 1956 (now Section 139 and/or Section 143(8) read with Section 141(3)(g) of the Companies Act, 2013).

Situations Limits

For Individuals CA’s or Proprietary firms

30 Audits

For Partnership Firm 30 Audits per partner of the Firm

When a CA is a partner in a number of a firms

30 Audit on his account in all the firms taken together in which he is a partner or proprietor.

Where the partner of a Firm also holds office in his individual capacity

30 Audits in his individual capacity and all Firms taken together.

Provided that in the case of a firm of Chartered Accountants in practice, the “specified number of audit assignments” shall be construed as the specific number of audit assignments for every partner of the firm. Provided further that where any partner of the firm of Chartered Accountants in practice is also a partner of any other firm or firms of Chartered Accountants in practice, the number of audit assignments which may be taken for all the firms together in relation to such partner shall not exceed the “specified number of audit assignments” in the aggregate. Provided further where any partner of a firm or firms of Chartered Accountants in practice accepts one or more audit of Companies in his individual capacity, or in the name of his proprietary firm, the total number of such assignments which may be accepted by all firms in relation to such Chartered Accountant and by him shall not exceed the “specified number of audit assignments” in the aggregate.

Students may note that the limit for holding maximum number of assignments has been changed under the Companies Act, 2013. According to Section 141(3)(g) of the said Act, a person or a partner of a firm holding appointment as its auditor, shall not be eligible for appointment as an Auditor of a Company, if such person or partner is at the date of such appointment or reappointment holding appointment as auditor of more than 20 Companies other than one person companies, dormant companies, small

companies and private companies having paid-up share capital less than Rs.100 crore.

14 For VPJ Classes – CA Vinod Parakh Jain, Ph/whatsapp:75036305943, website:www.vpjclasses.com

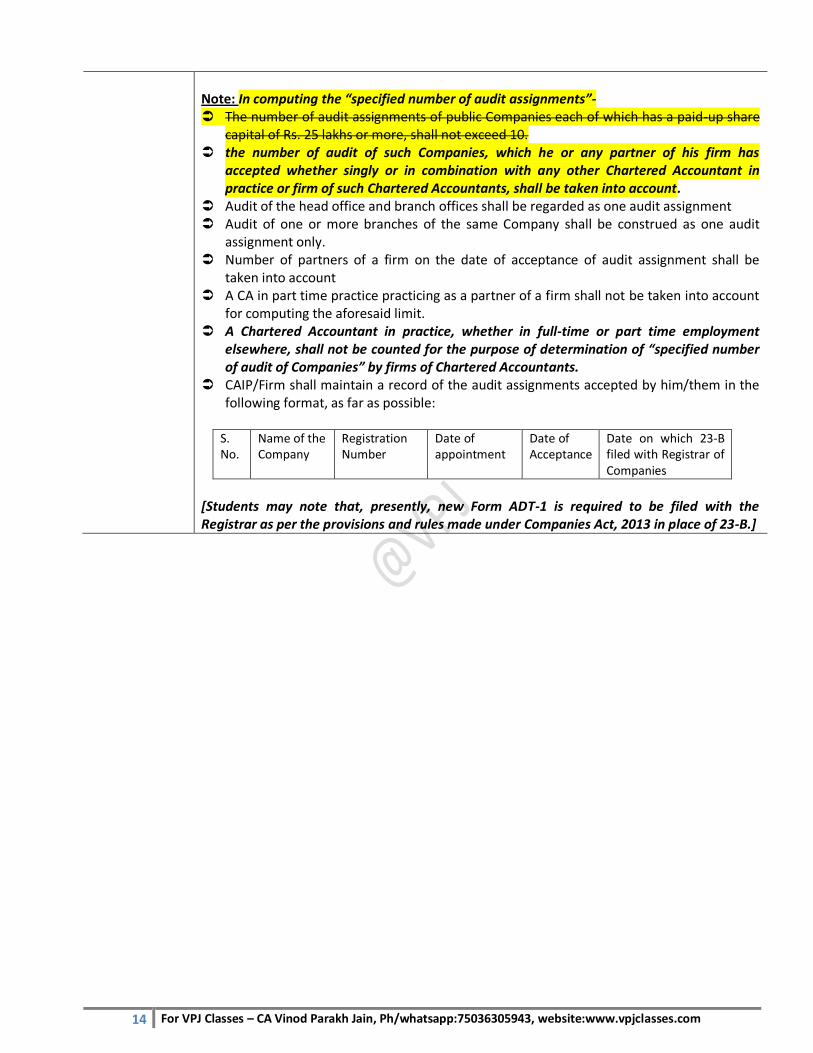

Note: In computing the “specified number of audit assignments”- The number of audit assignments of public Companies each of which has a paid-up share

capital of Rs. 25 lakhs or more, shall not exceed 10. the number of audit of such Companies, which he or any partner of his firm has

accepted whether singly or in combination with any other Chartered Accountant in practice or firm of such Chartered Accountants, shall be taken into account.

Audit of the head office and branch offices shall be regarded as one audit assignment Audit of one or more branches of the same Company shall be construed as one audit

assignment only. Number of partners of a firm on the date of acceptance of audit assignment shall be

taken into account A CA in part time practice practicing as a partner of a firm shall not be taken into account

for computing the aforesaid limit. A Chartered Accountant in practice, whether in full-time or part time employment

elsewhere, shall not be counted for the purpose of determination of “specified number of audit of Companies” by firms of Chartered Accountants.

CAIP/Firm shall maintain a record of the audit assignments accepted by him/them in the following format, as far as possible:

S. No.

Name of the Company

Registration Number

Date of appointment

Date of Acceptance

Date on which 23-B filed with Registrar of Companies

[Students may note that, presently, new Form ADT-1 is required to be filed with the Registrar as per the provisions and rules made under Companies Act, 2013 in place of 23-B.]

15 For VPJ Classes – CA Vinod Parakh Jain, Ph/whatsapp:75036305943, website:www.vpjclasses.com

No. of New Topics has been added in the study Material in this Chapter. Some of the Topics Presentation has been Changed by us. Topics whose Presentation has been Changed or has

been amended or New Topics has been Introduced has been Specified Below

5.1. Introduction

5.2. Framework For Government Audit- Presentation Changed and one New Topic Introduced

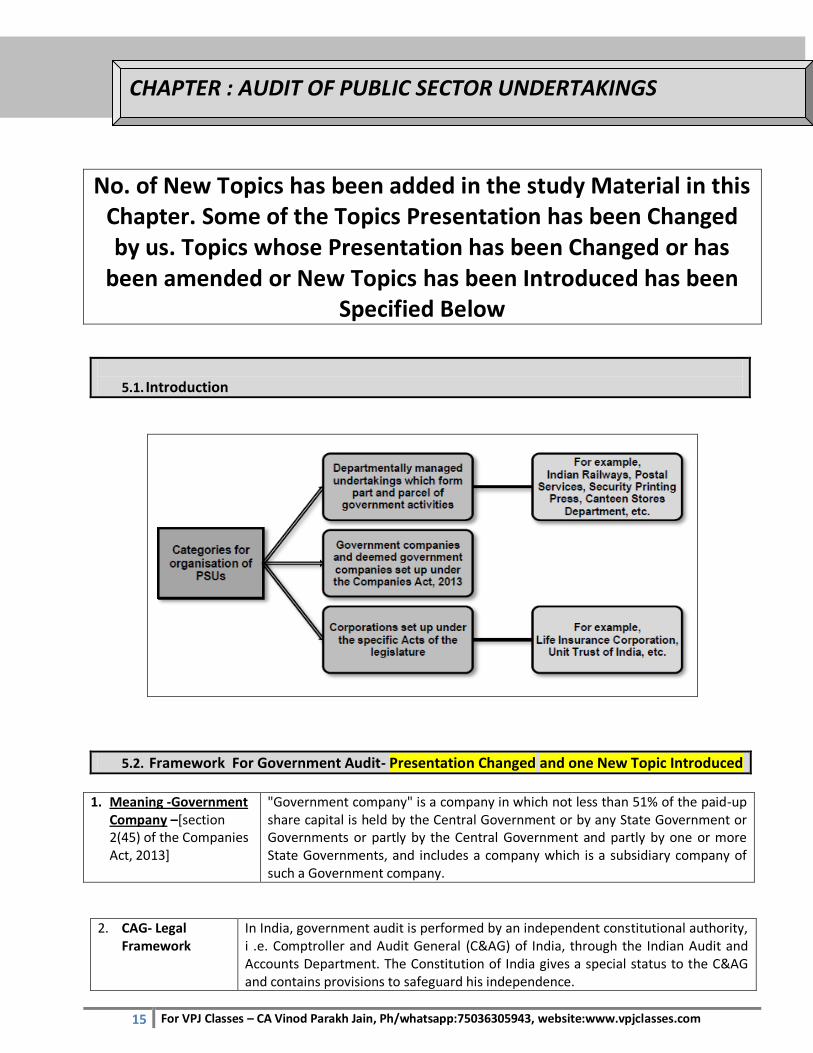

1. Meaning -Government Company –[section 2(45) of the Companies Act, 2013]

"Government company" is a company in which not less than 51% of the paid-up share capital is held by the Central Government or by any State Government or Governments or partly by the Central Government and partly by one or more State Governments, and includes a company which is a subsidiary company of such a Government company.

2. CAG- Legal Framework

In India, government audit is performed by an independent constitutional authority, i .e. Comptroller and Audit General (C&AG) of India, through the Indian Audit and Accounts Department. The Constitution of India gives a special status to the C&AG and contains provisions to safeguard his independence.

CHAPTER : AUDIT OF PUBLIC SECTOR UNDERTAKINGS

16 For VPJ Classes – CA Vinod Parakh Jain, Ph/whatsapp:75036305943, website:www.vpjclasses.com

Current CAG of India

Shashi Kant Sharma

Article 148

Appointment of C&AG by the President. • Special procedure for removal of C&AG, only on the ground of proven misbehaviors or incapacity. • Salary and other conditions of service to be determined by the Parliament.

Article 149

Perform such duties and exercise such powers in relation to the accounts of the Union and States and of any other authority or body as may be prescribed by or under any law made by the Parliament.

• The C&AG’s (Duties, Powers and Conditions of Service) Act, 1971 defines these functions and powers in detail.

Article 150

On the advice of the C&AG, President to prescribe such form in which accounts of the Union and States shall be kept.

Article 151

Audit reports of the C&AG relating to the accounts of the Central/ State Government should be submitted to the President/Governor of the State who shall cause them to be laid before Parliament/State Legislative.

The Comptroller and Audit General‟s (Duties, Power and Conditions of Services) Act, 1971, prescribes that the C&AG shall hold office for a term of six years or upto the age of 65 years, whichever is earlier. He can resign at any time through a resignation letter addressed to the President.

Powers & Duties

The C&AG shall perform such duties and exercise such powers in relation to the accounts of the union and of the state and of any other authority or body as may be prescribed Under C&AG (Duties, Power and Conditions of Services) Act, 1971.

Accounts Maintenance

The accounts of the union and of the states shall be kept in such form as the President may, on the advice of the C&AG, prescribe.

Submission of Accounts

The reports of C&AG relating to the accounts of the Union/State shall be submitted to the President/Governor who shall cause them to be laid before the house of the parliament/state legislature.

Organisations subject to the audit of C&AG

All the Union and State Government departments and offices including the Indian Railways and Posts and Telecommunications.

About 1200 public commercial enterprises controlled by the Union and State governments, i.e. government companies and corporations.

Around 400 non-commercial autonomous bodies and authorities owned or controlled by the Union or the States.

Over 4400 authorities and bodies substantially financed from Union or State revenues.

Action on Audit Reports – The scrutiny of the Annual Accounts and the Audit Reports thereon by the Parliament as a whole would be an arduous task, so Parliament and the State Legislatures have, for this purpose, constituted specialized Committees like the Public Accounts Committee (PAC) and the Committee on Public Undertakings (COPU), to which these audit Reports and Annual Accounts automatically stand referred.

Public Accounts Committee

The Public Accounts Committee satisfies itself that: a) Moneys (shown in accounts) were disbursed legally on the service or purpose to

which they were applied. b) Expenditure was authorised. c) Re-appropriation has been made in accordance with the provisions made (i.e.

distribution of funds).

17 For VPJ Classes – CA Vinod Parakh Jain, Ph/whatsapp:75036305943, website:www.vpjclasses.com

It is also the duty of the PAC to examine the statement of accounts of autonomous and semiautonomous bodies, the audit of which is conducted by the Comptroller & Auditor General either under the directions of the President or by a Statute of Parliament.

Estimates Committee [New Topic Inserted for Nov 2016 onwards]

The Committee examines the estimates with a view to: (i) report that economies, improvements in organization, efficiency, consistent with the policy underlying the estimates may be effected; (ii) suggest alternative policies; (iii) examine whether the money is well laid out within the limit; and (iv) suggest the form in which the estimates shall be presented to Parliament. The Committee does not comment upon a policy approved by Parliament, but where there is evidence that a particular policy is not leading to the desired results, or is leading to waste, it is the duty of the Committee to bring it to the notice of the House.

Committee on Public Undertakings

The Committee on Public Undertakings exercises the financial control on the public sector undertakings. The functions of the Committee are To examine the reports and accounts of public undertakings. To examine the reports of the Comptroller & Auditor General on public

undertakings. To examine the efficiency of public undertakings and to see whether they are being

managed in accordance with sound business principles and prudent commercial practices.

to exercise such other functions vested in the PAC and the Committee on Estimates as are not covered above and as may be allotted by the Speaker from time to time.

5.3. Objective and Scope of Public Enterprises Audit-[New Topic Inserted for Nov 2016 onwards]

The C&AG‟s (Duties, Power and Conditions of Services) Act, 1971 specifies the entities that come under audit purview of C&AG at the Union and State level, however, the scope and extent of audit is determined by the C&AG itself.

1. Audit of PSUs not constrained to Financial & Compliance Audit:

It also extends also to performance (efficiency, economy and effectiveness) with which these operate and fulfill their objectives and goals.

2. Propriety Audit This audit is directed towards an examination of management decisions in sales, purchases, contracts, etc. to see whether these have been taken in the best interests of the undertaking and conform to accepted principles of financial propriety.

3. Comprehensive Audit

He conducts an appraisal or an efficiency-cum-performance audit. He sees whether the undertakings have fulfilled the objectives for which they have been established, whether value-for-money spent has been obtained, whether the targets have been achieved, etc. He locates the areas of weakness including review of the decisions taken by the management and a comprehensive appraisal of the performance of the

18 For VPJ Classes – CA Vinod Parakh Jain, Ph/whatsapp:75036305943, website:www.vpjclasses.com

undertaking

4. Organisation’s Decision to be taken by Competent Authority

In examining the decisions of a management, the auditor examines that these were taken by the competent authority after examination of all aspects (economic, technological, public interest) on the basis of all the relevant information available at that time and taking into consideration the different alternatives available to management and that the decisions were consistent with the aims and objectives of the enterprise.

5. Helping Government:

Auditing besides being an instrument of accountability. help the Government and the enterprise Managements by bringing out financial and operational deficiencies, inadequacies or ineffectiveness of systems, shortfalls in performance, etc. and by analysing the causes of shortfall from acceptable standards of performance.

6. Highlighting Issues of Efficient and Economic Operations

7. Fiscal and Managerial Accountability

In the broader context, Government audit encompasses two main elements, viz., (a) Fiscal Accountability: It includes audit of provisions of funds, sanctions, compliances and propriety; and (b) Managerial Accountability: It includes audit of efficiency, economy and effectiveness (This is often referred to as efficiency –cum performance audit).

5.4. Audit of Government Companies (Commercial Audit)- SAME AS EARLIER. Refer to VPJ Module

5.4. Financial Audit [New Topic Inserted for Nov 2016 onwards]

Financial audit is primarily conducted to express an audit opinion on a set of financial statements. It includes: (i) examination and evaluation of financial records and expression of opinion on Financial Statements; (ii) audit of financial systems and transactions including an evaluation of compliance with applicable statutes and regulations which affect the accuracy and completeness of accounting records; and (iii) audit of internal control and internal audit functions that assist in safeguarding assets and resources and assure the accuracy and completeness of accounting records.

5.5. Compliance Audit [New Topic Inserted for Nov 2016 onwards]

Compliance audit is an independent verification process of evaluating audit evidence to determine whether specified compliance requirements are met. It examines the transactions relating to expenditure, receipts, assets and liabilities of Government for compliance with: (i) the provisions of the Constitution of India and the applicable laws; and (ii) the rules, regulations, orders and instructions issued by the competent authority either in pursuance of the provisions of the Constitution of India and the laws or by virtue of the powers formally delegated to it by a superior authority. Compliance audit also includes an examination of the rules, regulations, orders and instructions for their legality, adequacy, transparency, propriety, prudence and effectiveness, that is, whether these are: (i) intra vires of the provisions of the Constitution of India and the laws (Legality); (ii) sufficiently comprehensive and ensure effective control over Government receipts, expenditure, assets and liabilities with sufficient safeguards against loss due to wastage, misuse, mismanagement, errors, frauds and other irregularities (Adequacy);

19 For VPJ Classes – CA Vinod Parakh Jain, Ph/whatsapp:75036305943, website:www.vpjclasses.com

(iii) clear and free from ambiguity and promote observance of probity in decision making (Transparency); (iv) effective and achieve the intended objectives and aims (Effectiveness).

5.5. Comprehensive Audit of Public Enterprises- SAME AS EARLIER

5.6. Propriety Audit

Relevant provisions in the Companies Act, 2013

Section 148 relating to Cost Records and Audit

Cost records and the provisions of cost audit are designed to inculcate cost consciousness in the management and to know whether productivity is of acceptable order and whether undue wastage or loss etc. has occurred. It would be useful to go into some of the specific requirement of cost audit report in this context.

Section 143(1) requiring enquiry into certain specified matters

This Involve Enquiry into 6 Matters. These have been Covered under the Chapter- Company Audit

Section 143(6) and 143(7) requiring a supplementary audit and test audit respectively in respect of the Government companies on matters specified.

Additional information in Part II of Schedule III.

Some of the matters in the additional information sought through the Statement of Profit and Loss (i.e., Part II of Schedule III) provide a basis for making more searching enquiries into such vital matters as consumption of raw materials under broad heads, goods purchased under broad heads, work in progress under broad heads, any item of income or expenditure which exceeds one percent of the

revenue from operations or ` 1,00,000, whichever is higher, etc.

Propriety elements under CARO, 2015

(a) If the company has granted loans, secured or unsecured, to companies, firms or other parties covered in the register maintained under section 189 of the Companies Act, whether the receipt of the principal amount and interest are regular (b) If the overdue amount of the loan given to companies, firms or other parties covered in the register maintained under section 189 of the Companies Act is

more than ` 1 lakh, what reasonable steps have been taken by the company for recovery of the principal and interest. (c) Is the company regular in depositing undisputed statutory dues including Provident Fund, Investor Education and Protection Fund, Employees’ State Insurance, Income-Tax, Sales Tax, Wealth Tax, Service Tax, Custom Duty, Excise Duty, Value Added Tax, Cess and any other statutory dues with the appropriate authorities and if not, the extent of the arrears of outstanding statutory dues as at the last day of the financial year concerned for a period of more than six months from the date they became payable, shall be indicated by the auditor. (d) If the company has defaulted in repayment of dues to a financial institution or bank or debenture holders, the period and amount of default to be reported by the auditor. (e) Whether the term loans were applied for the purpose for which the loans were

20 For VPJ Classes – CA Vinod Parakh Jain, Ph/whatsapp:75036305943, website:www.vpjclasses.com

obtained. (f) If any fraud on or by the company has been noticed or reported during the year , the nature and the amount involved is to be indicated in the report.

FOR REST OF THE TOPIC REFER TO VPJ MODULE

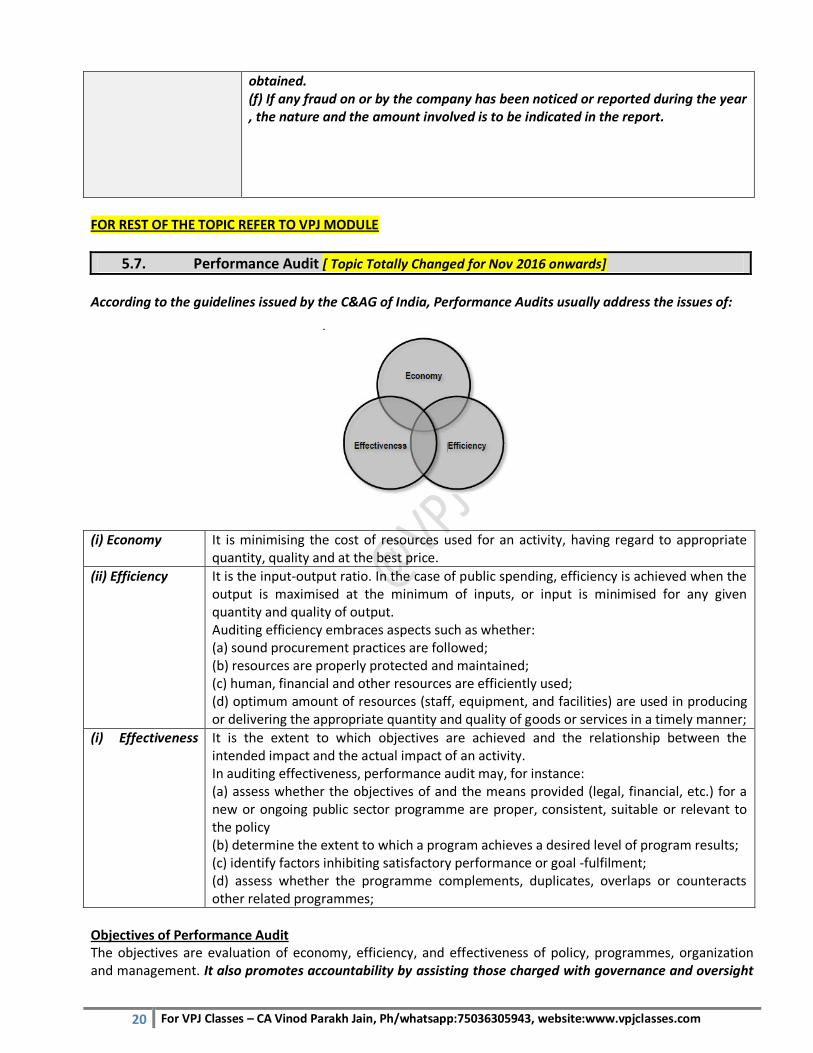

5.7. Performance Audit [ Topic Totally Changed for Nov 2016 onwards]

According to the guidelines issued by the C&AG of India, Performance Audits usually address the issues of:

(i) Economy It is minimising the cost of resources used for an activity, having regard to appropriate quantity, quality and at the best price.

(ii) Efficiency It is the input-output ratio. In the case of public spending, efficiency is achieved when the output is maximised at the minimum of inputs, or input is minimised for any given quantity and quality of output. Auditing efficiency embraces aspects such as whether: (a) sound procurement practices are followed; (b) resources are properly protected and maintained; (c) human, financial and other resources are efficiently used; (d) optimum amount of resources (staff, equipment, and facilities) are used in producing or delivering the appropriate quantity and quality of goods or services in a timely manner;

(i) Effectiveness It is the extent to which objectives are achieved and the relationship between the intended impact and the actual impact of an activity. In auditing effectiveness, performance audit may, for instance: (a) assess whether the objectives of and the means provided (legal, financial, etc.) for a new or ongoing public sector programme are proper, consistent, suitable or relevant to the policy (b) determine the extent to which a program achieves a desired level of program results; (c) identify factors inhibiting satisfactory performance or goal -fulfilment; (d) assess whether the programme complements, duplicates, overlaps or counteracts other related programmes;

Objectives of Performance Audit The objectives are evaluation of economy, efficiency, and effectiveness of policy, programmes, organization and management. It also promotes accountability by assisting those charged with governance and oversight

21 For VPJ Classes – CA Vinod Parakh Jain, Ph/whatsapp:75036305943, website:www.vpjclasses.com

responsibilities to improve performance; and transparency by affording taxpayers, those targeted by government policies and other stakeholders an insight into the management and outcomes of different government activities.

Planning for Performance Audit

(A) Understanding the entity/programme

The auditor may use the following sources for understanding the entity: (i)Documents of the entity Like annual reports, budget documents, accounts, minutes of meetings, information on the website, internal audit reports, (ii) Legislative documents Like parliamentary questions and debates, reports of PAC/ Committee on Public Undertakings (iii) Policy documents: Documents of Planning Commission, Ministry of Finance etc. (iv) Academic or special research (v) Past audits (vi) Media coverage (vii) Special focus groups like reports of World Bank, Reserve Bank of India, reports by special interest groups, NGOs, etc.

(B) Defining the objectives and the scope of audit Needs

Setting audit objectives ensures good quality performance audits. Defining the scope constrict the audit to significant issues that relate to the audit objectives. It mainly focuses the extent, timing and nature of the audit.

(C) Determining audit criteria -

Audit criteria are the standards used to determine whether a program meets or exceeds expectations.

(D) Deciding audit approach

There is no uniform audit approach prescribed that can be applicable to all types of subjects of performance audits. Selection of approach also determine methods and means used for conducting the audit. Some of the methods which could be used in conducting performance audits include: (i) Analysis of procedures (ii) Case studies (iii) Use of existing data (iv) Surveys v) Analysis of results (vi) Quantitative analysis

(E) Developing audit questions

the audit team is required to prepare a list of questions to which they would seek answers.

(F) Assessing audit team skills and whether outside expertise required

It is essential that the performance auditors possess special aptitude and knowledge. The audit team needs to decide at the planning stage on which aspect expertise is required. Though, the Accountant General may use the work of an expert, he retains full responsibility for the expression of opinion in the auditor’s report.

(G) Preparing Audit Design Matrix (ADM) -

Audit team should prepare an Audit Design Matrix. It is a structured and highly focused approach to designing a performance audit study. It highlights the data collection and analysis method as well as the type and sources of evidence required to support audit opinion/findings. The specimen of ADM is given as under:

Audit Objective

Audit Questions

Audit Criteria

Evidence

Data Collection And Analysis

22 For VPJ Classes – CA Vinod Parakh Jain, Ph/whatsapp:75036305943, website:www.vpjclasses.com

(1) (2) (3)

(4)

Method (5)

(H) Establishing time table and resources -

(I) Intimation of Audit programme to audit entities -

[Relevant for May 2016 Attempt only. Now Changed]

Meaning A performance audit is an objective and systematic examination of evidence for the purpose of providing

an independent assessment of the performance of a government organization, program, activity, or function.

It provide information to improve public accountability and facilitate decision-making by parties with responsibility to oversee or initiate corrective action

Type of Performance Audit

Economy and efficiency audits Program audits

Auditor shall determine: a) Whether the entity is acquiring, protecting, and

using its resources (such as personnel, property, and space) economically and efficiently,

b) What are the causes of inefficiencies or uneconomical practices, and

c) Whether the entity has complied with laws and regulations on matters of economy and efficiency.

Auditor shall determine: a) The extent to which the desired results or

benefits established by the legislature or other authorizing body are being achieved,

b) The effectiveness of organizations, programs, activities, or functions,

c) Whether the entity has complied with significant laws and regulations applicable to the program.

The Mandate and Objectives of Performance Audit Section 143(6) and Section 143(7) of the Companies Act, empowers Comptroller and Auditor General of India to conduct supplementary audit or test audit of Government companies. The CAG shall have right to conduct supplementary or test audit of the Government company’s accounts by such person or persons as he may authorize in his behalf; and for the purposes of such audit to require information or additional information to such person or persons and in such form as the Comptroller and/ Auditor General may, by general or special order, direct. Section 143(5) of Companies Act requires the statutory auditor (chartered accountant appointed by CAG under section 139(5) or 139(7) of the Act) to submit a copy of his audit report on the accounts of the Government company to C&AG as discussed before. Thus while section 143(6) and 143(7) of the Companies Act empowers C&AG to conduct supplementary audit and test audit respectively of annual accounts of a Government company. In so far as Statutory corporations are concerned the respective statutes provide for audit by CAG. The Scope includes conducting performance Audit of these corporations also though specially not stated so The objectives are evaluation of economy, efficiency, and effectiveness of policy, programmes, organization and management. a) Policy: an effort to achieve certain aims with certain resources and perhaps within a certain time.

23 For VPJ Classes – CA Vinod Parakh Jain, Ph/whatsapp:75036305943, website:www.vpjclasses.com

b) Programme: a set of interrelated means-legal, financial, etc. to implement a given policy. c) Organisation: It is aggregate of people, structures and processes that have the aim of achieving particular

objectives. d) Management: It refers to a person or group person(s), like Board of Directors in a company, vested with

powers to take all decisions, actions and framing rules for the steering, accounting and development of human, financial and material resources.

Planning for Performance Audit

Work is to be adequately planned

Define the audit's objectives and the scope and methodology to achieve those objectives. While planning, auditor should:

a) Consider significance and the needs of potential users of the audit report. b) Obtain an understanding of the program to be audited. c) Consider legal and regulatory requirements. d) Consider management controls. e) Identify criteria needed to evaluate matters subject to audit. f) Identify significant findings and recommendations from previous audits g) Identify potential sources of data that could be used as audit evidence h) Provide sufficient staff and other resources to do the audit. i) Consider whether the work of other auditors and experts may be used j) Prepare a written audit plan.

Significance and User Needs

The significance of a matter is its relative importance to the audit objectives and potential users of the audit report. Qualitative, as well as quantitative, factors are important in determining significance.

An awareness of these potential users' interests and influence can help auditors understand why the program operates the way it does. This awareness can also help auditors judge whether possible findings could be significant to these other users.

Understanding the Program

a) Auditors should obtain an understanding of the program to be audited to help assess, among other matters, the significance of possible audit objectives and the feasibility of achieving them.

b) The auditors' understanding may come from i. knowledge they already have about the program; and

ii. knowledge they gain from inquiries and observations they make in planning the audit.

c) Following Aspect of the program should be covered:

Laws and regulations – L&R for Govt. Programs are more specific than private sector

Purpose & Goals – Use purpose & goal as criteria for assessing program performance.

24 For VPJ Classes – CA Vinod Parakh Jain, Ph/whatsapp:75036305943, website:www.vpjclasses.com

Efforts - Efforts are the amount of resources (in terms of money, material, personnel, and so forth) that are put into a program.

Program operations - Program operations are the strategies, processes, and activities the auditee uses to convert efforts into outputs.

Outputs - Outputs are the quantity of goods and services provided.

Outcome - Outcomes are accomplishments or results that occur (at least partially) because of services provided.

Criteria a) Criteria are the standards used to determine whether a program meets or exceeds expectations. They provide a context for understanding the results of the audit.

b) The audit plan, where possible, should state the Government Auditing Standards criteria to be used.

c) In selecting criteria, auditors have a responsibility to use criteria that are reasonable, attainable, and relevant to the matters being audited.

Audit Follow-Up

a) Auditors should follow up on significant findings and recommendations from previous audits that could affect the audit objectives.

b) They should do this to determine whether timely and appropriate corrective actions have been taken by auditee officials.

c) The audit report should disclose the status of uncorrected significant findings and recommendations from prior audits that affect the audit objectives.

Considering Others' Work

If other auditor has done Performance audit or Financial audit, they may be useful source of information for planning and performing the Performance Audit – a) areas that warrant further study b) selection of methodology, as the auditors may be able to rely on that work to limit the

extent of their own testing

25 For VPJ Classes – CA Vinod Parakh Jain, Ph/whatsapp:75036305943, website:www.vpjclasses.com

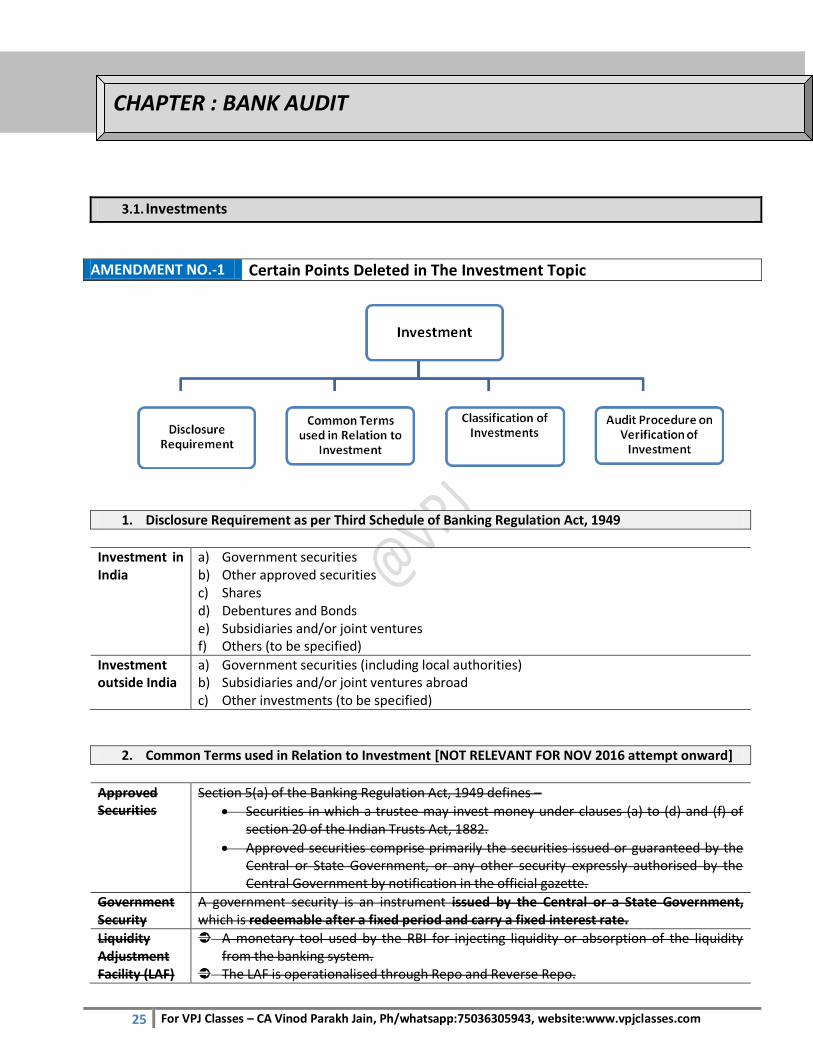

3.1. Investments

AMENDMENT NO.-1 Certain Points Deleted in The Investment Topic

1. Disclosure Requirement as per Third Schedule of Banking Regulation Act, 1949

Investment in India

a) Government securities b) Other approved securities c) Shares d) Debentures and Bonds e) Subsidiaries and/or joint ventures f) Others (to be specified)

Investment outside India

a) Government securities (including local authorities) b) Subsidiaries and/or joint ventures abroad c) Other investments (to be specified)

2. Common Terms used in Relation to Investment [NOT RELEVANT FOR NOV 2016 attempt onward]

Approved Securities

Section 5(a) of the Banking Regulation Act, 1949 defines –

Securities in which a trustee may invest money under clauses (a) to (d) and (f) of section 20 of the Indian Trusts Act, 1882.

Approved securities comprise primarily the securities issued or guaranteed by the Central or State Government, or any other security expressly authorised by the Central Government by notification in the official gazette.

Government Security

A government security is an instrument issued by the Central or a State Government, which is redeemable after a fixed period and carry a fixed interest rate.

Liquidity Adjustment Facility (LAF)

A monetary tool used by the RBI for injecting liquidity or absorption of the liquidity from the banking system.

The LAF is operationalised through Repo and Reverse Repo.

CHAPTER : BANK AUDIT

26 For VPJ Classes – CA Vinod Parakh Jain, Ph/whatsapp:75036305943, website:www.vpjclasses.com

Portfolio Management Scheme (PMS)

In a portfolio management scheme, the bank administering the scheme makes investments on behalf of clients for a ‘management fee’. This is a fiduciary activity in which the profit or loss from the transactions belongs to the client.

A bank can perform the services of PMS only after approval of RBI and getting registered with SEBI.

Ready-forward Transactions or Repo

a) Ready-forward or Repo transactions are arrangements for current sale of securities and their simultaneous re-purchase at a future date at a price fixed at the time of sale.

b) Difference between two prices constitutes -

Financing cost of the bank that sells and agrees to repurchase the securities subsequently from the other party to the transaction.

Yield on the transaction from the view point of the other party.

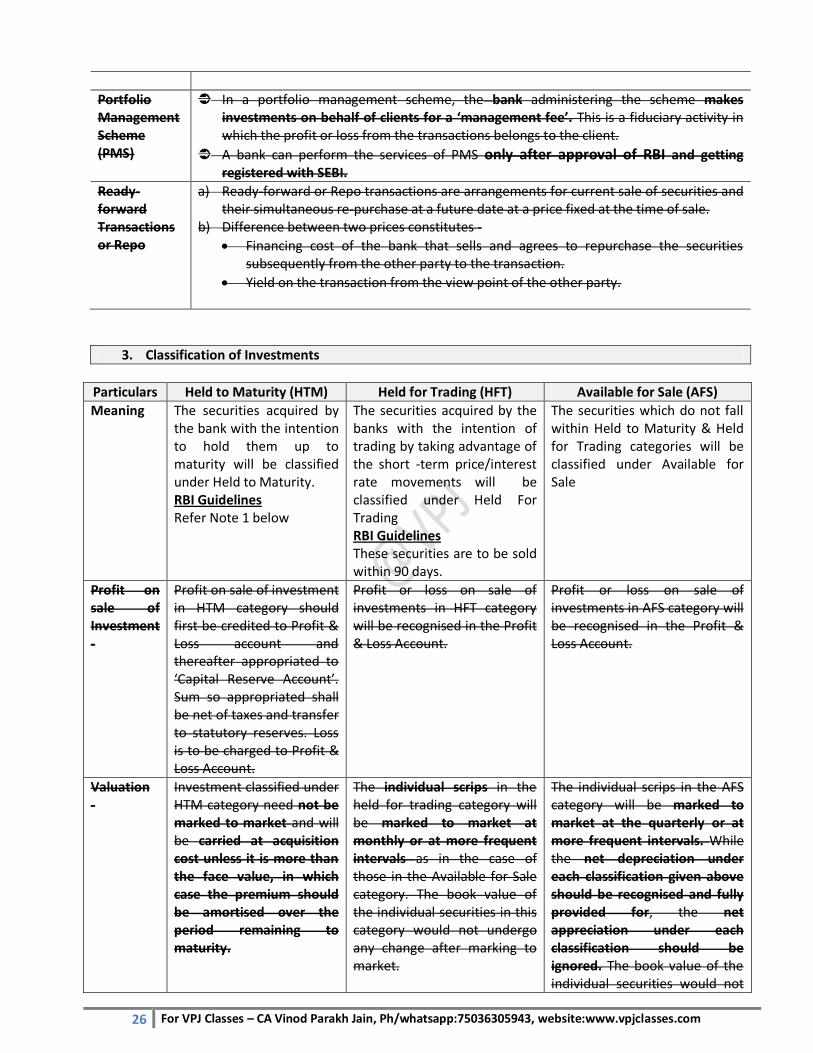

3. Classification of Investments

Particulars Held to Maturity (HTM) Held for Trading (HFT) Available for Sale (AFS)

Meaning The securities acquired by the bank with the intention to hold them up to maturity will be classified under Held to Maturity. RBI Guidelines Refer Note 1 below

The securities acquired by the banks with the intention of trading by taking advantage of the short -term price/interest rate movements will be classified under Held For Trading RBI Guidelines These securities are to be sold within 90 days.

The securities which do not fall within Held to Maturity & Held for Trading categories will be classified under Available for Sale

Profit on sale of Investment -

Profit on sale of investment in HTM category should first be credited to Profit & Loss account and thereafter appropriated to ‘Capital Reserve Account’. Sum so appropriated shall be net of taxes and transfer to statutory reserves. Loss is to be charged to Profit & Loss Account.

Profit or loss on sale of investments in HFT category will be recognised in the Profit & Loss Account.

Profit or loss on sale of investments in AFS category will be recognised in the Profit & Loss Account.

Valuation -

Investment classified under HTM category need not be marked to market and will be carried at acquisition cost unless it is more than the face value, in which case the premium should be amortised over the period remaining to maturity.

The individual scrips in the held for trading category will be marked to market at monthly or at more frequent intervals as in the case of those in the Available for Sale category. The book value of the individual securities in this category would not undergo any change after marking to market.

The individual scrips in the AFS category will be marked to market at the quarterly or at more frequent intervals. While the net depreciation under each classification given above should be recognised and fully provided for, the net appreciation under each classification should be ignored. The book value of the individual securities would not

27 For VPJ Classes – CA Vinod Parakh Jain, Ph/whatsapp:75036305943, website:www.vpjclasses.com

undergo any change after revaluation.

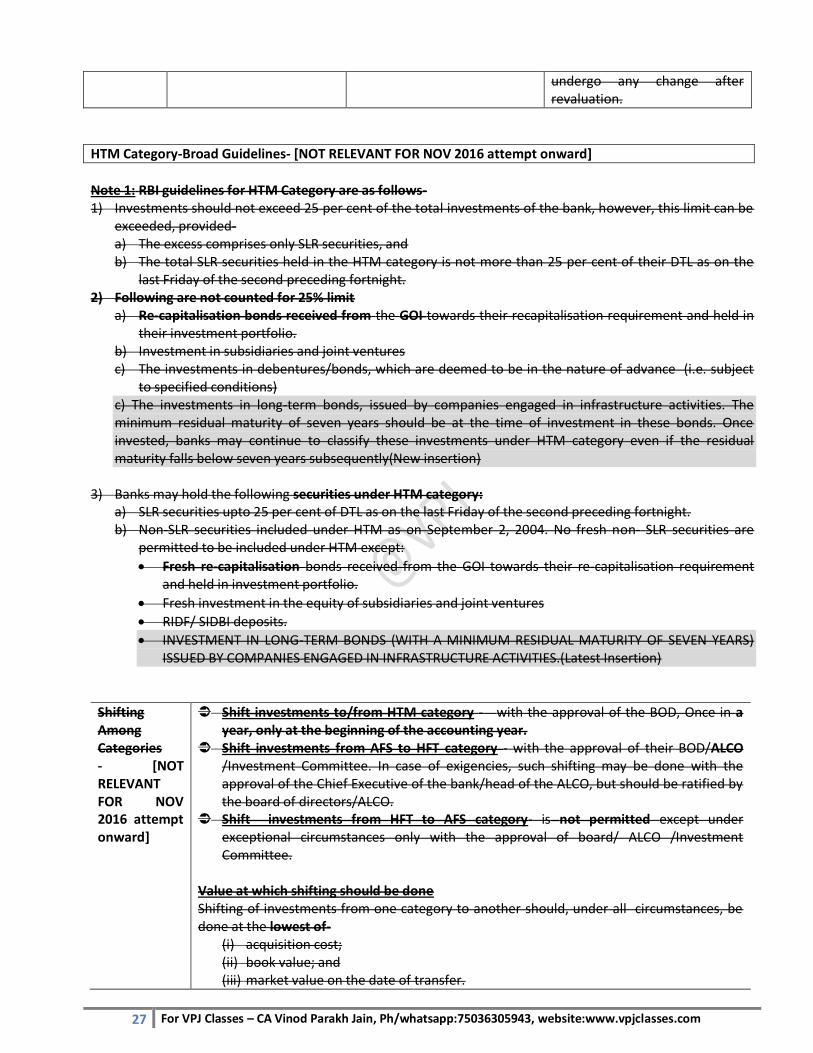

HTM Category-Broad Guidelines- [NOT RELEVANT FOR NOV 2016 attempt onward]

Note 1: RBI guidelines for HTM Category are as follows- 1) Investments should not exceed 25 per cent of the total investments of the bank, however, this limit can be

exceeded, provided- a) The excess comprises only SLR securities, and b) The total SLR securities held in the HTM category is not more than 25 per cent of their DTL as on the

last Friday of the second preceding fortnight. 2) Following are not counted for 25% limit

a) Re-capitalisation bonds received from the GOI towards their recapitalisation requirement and held in their investment portfolio.

b) Investment in subsidiaries and joint ventures c) The investments in debentures/bonds, which are deemed to be in the nature of advance (i.e. subject

to specified conditions) c) The investments in long-term bonds, issued by companies engaged in infrastructure activities. The minimum residual maturity of seven years should be at the time of investment in these bonds. Once invested, banks may continue to classify these investments under HTM category even if the residual maturity falls below seven years subsequently(New insertion)

3) Banks may hold the following securities under HTM category: a) SLR securities upto 25 per cent of DTL as on the last Friday of the second preceding fortnight. b) Non-SLR securities included under HTM as on September 2, 2004. No fresh non- SLR securities are

permitted to be included under HTM except:

Fresh re-capitalisation bonds received from the GOI towards their re-capitalisation requirement and held in investment portfolio.

Fresh investment in the equity of subsidiaries and joint ventures

RIDF/ SIDBI deposits.

INVESTMENT IN LONG-TERM BONDS (WITH A MINIMUM RESIDUAL MATURITY OF SEVEN YEARS) ISSUED BY COMPANIES ENGAGED IN INFRASTRUCTURE ACTIVITIES.(Latest Insertion)

Shifting Among Categories - [NOT RELEVANT FOR NOV 2016 attempt onward]

Shift investments to/from HTM category - with the approval of the BOD, Once in a year, only at the beginning of the accounting year.

Shift investments from AFS to HFT category - with the approval of their BOD/ALCO /Investment Committee. In case of exigencies, such shifting may be done with the approval of the Chief Executive of the bank/head of the ALCO, but should be ratified by the board of directors/ALCO.

Shift investments from HFT to AFS category- is not permitted except under exceptional circumstances only with the approval of board/ ALCO /Investment Committee.

Value at which shifting should be done Shifting of investments from one category to another should, under all circumstances, be done at the lowest of-

(i) acquisition cost; (ii) book value; and (iii) market value on the date of transfer.

28 For VPJ Classes – CA Vinod Parakh Jain, Ph/whatsapp:75036305943, website:www.vpjclasses.com

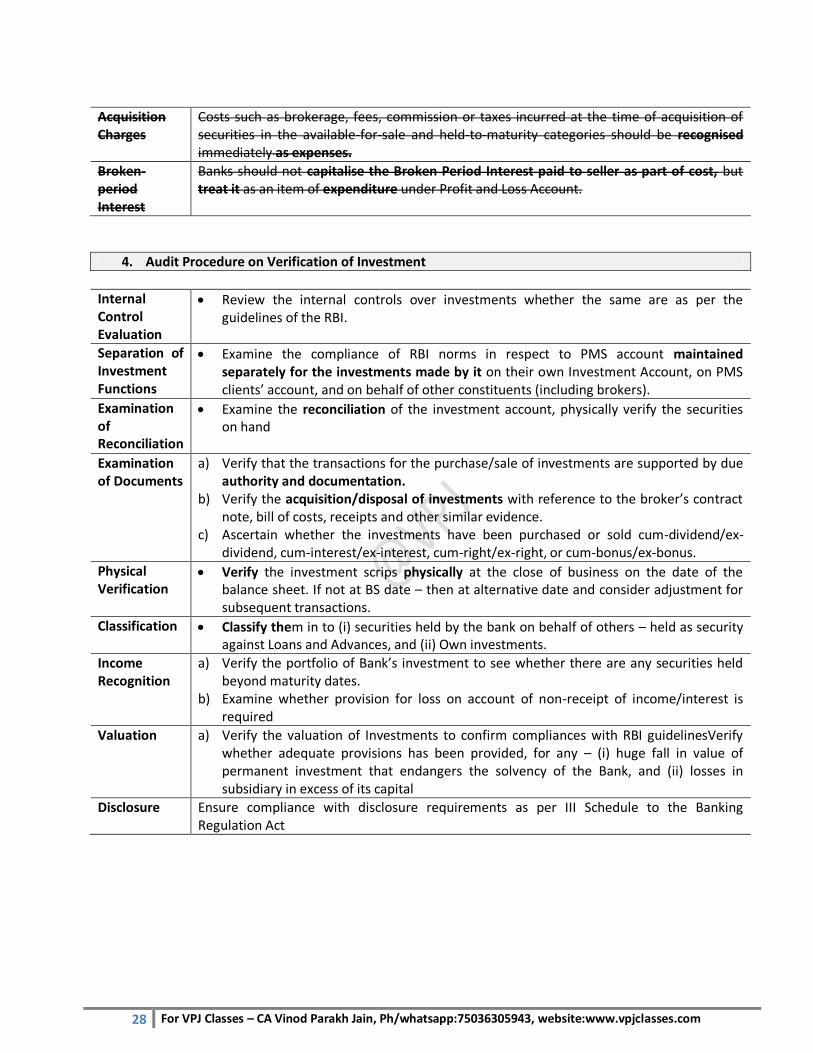

Acquisition Charges

Costs such as brokerage, fees, commission or taxes incurred at the time of acquisition of securities in the available-for-sale and held-to-maturity categories should be recognised immediately as expenses.

Broken-period Interest

Banks should not capitalise the Broken Period Interest paid to seller as part of cost, but treat it as an item of expenditure under Profit and Loss Account.

4. Audit Procedure on Verification of Investment

Internal Control Evaluation

Review the internal controls over investments whether the same are as per the guidelines of the RBI.

Separation of Investment Functions

Examine the compliance of RBI norms in respect to PMS account maintained separately for the investments made by it on their own Investment Account, on PMS clients’ account, and on behalf of other constituents (including brokers).

Examination of Reconciliation

Examine the reconciliation of the investment account, physically verify the securities on hand

Examination of Documents

a) Verify that the transactions for the purchase/sale of investments are supported by due authority and documentation.

b) Verify the acquisition/disposal of investments with reference to the broker’s contract note, bill of costs, receipts and other similar evidence.

c) Ascertain whether the investments have been purchased or sold cum-dividend/ex-dividend, cum-interest/ex-interest, cum-right/ex-right, or cum-bonus/ex-bonus.

Physical Verification

Verify the investment scrips physically at the close of business on the date of the balance sheet. If not at BS date – then at alternative date and consider adjustment for subsequent transactions.

Classification Classify them in to (i) securities held by the bank on behalf of others – held as security against Loans and Advances, and (ii) Own investments.

Income Recognition

a) Verify the portfolio of Bank’s investment to see whether there are any securities held beyond maturity dates.

b) Examine whether provision for loss on account of non-receipt of income/interest is required

Valuation a) Verify the valuation of Investments to confirm compliances with RBI guidelinesVerify whether adequate provisions has been provided, for any – (i) huge fall in value of permanent investment that endangers the solvency of the Bank, and (ii) losses in subsidiary in excess of its capital

Disclosure Ensure compliance with disclosure requirements as per III Schedule to the Banking Regulation Act

29 For VPJ Classes – CA Vinod Parakh Jain, Ph/whatsapp:75036305943, website:www.vpjclasses.com

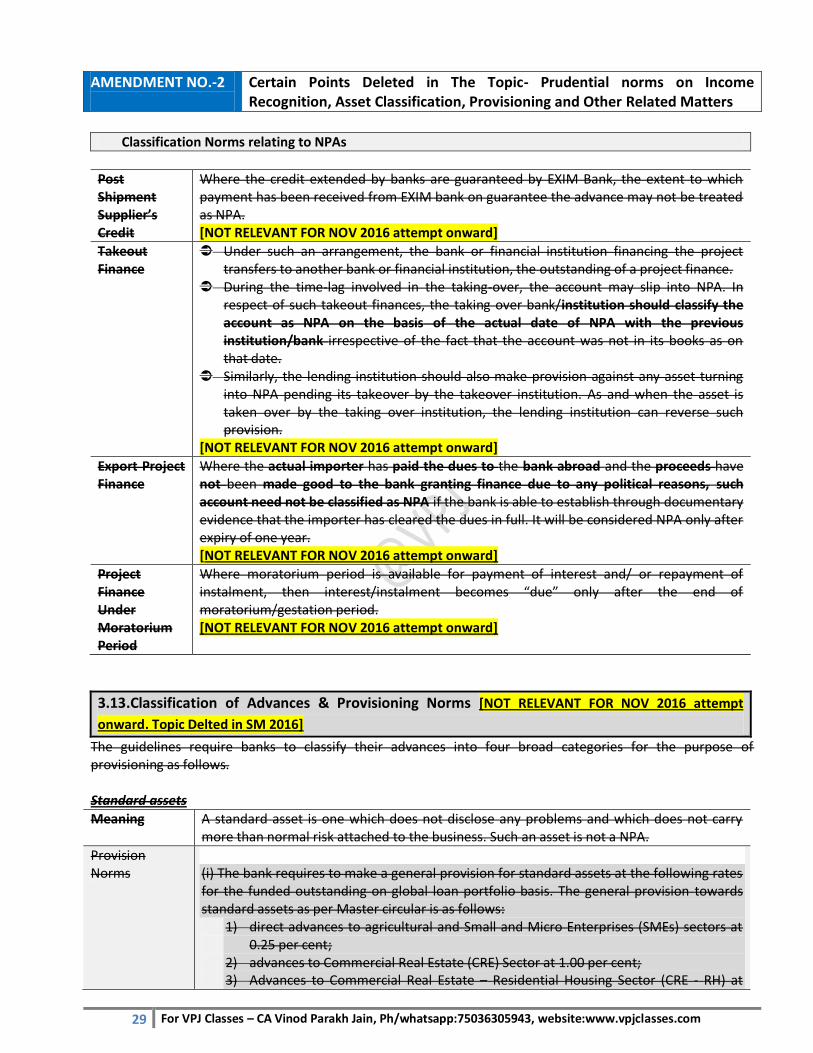

AMENDMENT NO.-2

Certain Points Deleted in The Topic- Prudential norms on Income Recognition, Asset Classification, Provisioning and Other Related Matters

Classification Norms relating to NPAs

Post Shipment Supplier’s Credit

Where the credit extended by banks are guaranteed by EXIM Bank, the extent to which payment has been received from EXIM bank on guarantee the advance may not be treated as NPA. [NOT RELEVANT FOR NOV 2016 attempt onward]

Takeout Finance

Under such an arrangement, the bank or financial institution financing the project transfers to another bank or financial institution, the outstanding of a project finance.

During the time-lag involved in the taking-over, the account may slip into NPA. In respect of such takeout finances, the taking over bank/institution should classify the account as NPA on the basis of the actual date of NPA with the previous institution/bank irrespective of the fact that the account was not in its books as on that date.

Similarly, the lending institution should also make provision against any asset turning into NPA pending its takeover by the takeover institution. As and when the asset is taken over by the taking over institution, the lending institution can reverse such provision.

[NOT RELEVANT FOR NOV 2016 attempt onward]

Export Project Finance

Where the actual importer has paid the dues to the bank abroad and the proceeds have not been made good to the bank granting finance due to any political reasons, such account need not be classified as NPA if the bank is able to establish through documentary evidence that the importer has cleared the dues in full. It will be considered NPA only after expiry of one year. [NOT RELEVANT FOR NOV 2016 attempt onward]

Project Finance Under Moratorium Period

Where moratorium period is available for payment of interest and/ or repayment of instalment, then interest/instalment becomes “due” only after the end of moratorium/gestation period. [NOT RELEVANT FOR NOV 2016 attempt onward]

3.13.Classification of Advances & Provisioning Norms [NOT RELEVANT FOR NOV 2016 attempt

onward. Topic Delted in SM 2016]

The guidelines require banks to classify their advances into four broad categories for the purpose of provisioning as follows. Standard assets

Meaning A standard asset is one which does not disclose any problems and which does not carry more than normal risk attached to the business. Such an asset is not a NPA.

Provision Norms

(i) The bank requires to make a general provision for standard assets at the following rates for the funded outstanding on global loan portfolio basis. The general provision towards standard assets as per Master circular is as follows:

1) direct advances to agricultural and Small and Micro Enterprises (SMEs) sectors at 0.25 per cent;

2) advances to Commercial Real Estate (CRE) Sector at 1.00 per cent; 3) Advances to Commercial Real Estate – Residential Housing Sector (CRE - RH) at

30 For VPJ Classes – CA Vinod Parakh Jain, Ph/whatsapp:75036305943, website:www.vpjclasses.com

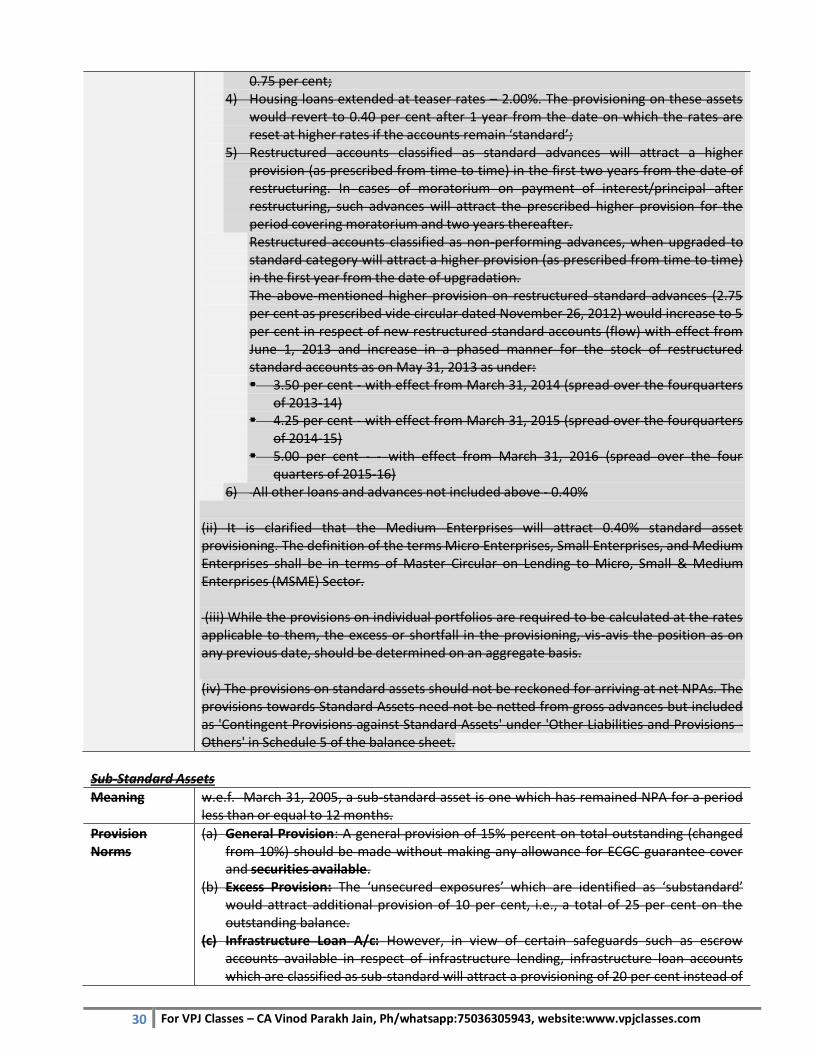

0.75 per cent; 4) Housing loans extended at teaser rates – 2.00%. The provisioning on these assets

would revert to 0.40 per cent after 1 year from the date on which the rates are reset at higher rates if the accounts remain ‘standard’;

5) Restructured accounts classified as standard advances will attract a higher provision (as prescribed from time to time) in the first two years from the date of restructuring. In cases of moratorium on payment of interest/principal after restructuring, such advances will attract the prescribed higher provision for the period covering moratorium and two years thereafter. Restructured accounts classified as non-performing advances, when upgraded to standard category will attract a higher provision (as prescribed from time to time) in the first year from the date of upgradation. The above-mentioned higher provision on restructured standard advances (2.75 per cent as prescribed vide circular dated November 26, 2012) would increase to 5 per cent in respect of new restructured standard accounts (flow) with effect from June 1, 2013 and increase in a phased manner for the stock of restructured standard accounts as on May 31, 2013 as under: 3.50 per cent - with effect from March 31, 2014 (spread over the fourquarters

of 2013-14) 4.25 per cent - with effect from March 31, 2015 (spread over the fourquarters

of 2014-15) 5.00 per cent - - with effect from March 31, 2016 (spread over the four

quarters of 2015-16) 6) All other loans and advances not included above - 0.40%

(ii) It is clarified that the Medium Enterprises will attract 0.40% standard asset provisioning. The definition of the terms Micro Enterprises, Small Enterprises, and Medium Enterprises shall be in terms of Master Circular on Lending to Micro, Small & Medium Enterprises (MSME) Sector. (iii) While the provisions on individual portfolios are required to be calculated at the rates applicable to them, the excess or shortfall in the provisioning, vis-avis the position as on any previous date, should be determined on an aggregate basis. (iv) The provisions on standard assets should not be reckoned for arriving at net NPAs. The provisions towards Standard Assets need not be netted from gross advances but included as 'Contingent Provisions against Standard Assets' under 'Other Liabilities and Provisions - Others' in Schedule 5 of the balance sheet.

Sub-Standard Assets

Meaning w.e.f. March 31, 2005, a sub-standard asset is one which has remained NPA for a period less than or equal to 12 months.

Provision Norms

(a) General Provision: A general provision of 15% percent on total outstanding (changed from 10%) should be made without making any allowance for ECGC guarantee cover and securities available.

(b) Excess Provision: The ‘unsecured exposures’ which are identified as ‘substandard’ would attract additional provision of 10 per cent, i.e., a total of 25 per cent on the outstanding balance.

(c) Infrastructure Loan A/c: However, in view of certain safeguards such as escrow accounts available in respect of infrastructure lending, infrastructure loan accounts which are classified as sub-standard will attract a provisioning of 20 per cent instead of

31 For VPJ Classes – CA Vinod Parakh Jain, Ph/whatsapp:75036305943, website:www.vpjclasses.com

the aforesaid prescription of 25 per cent. To avail of this benefit of lower provisioning, the banks should have in place an appropriate mechanism to escrow the cash flows and also have a clear and legal first claim on these cash flows.

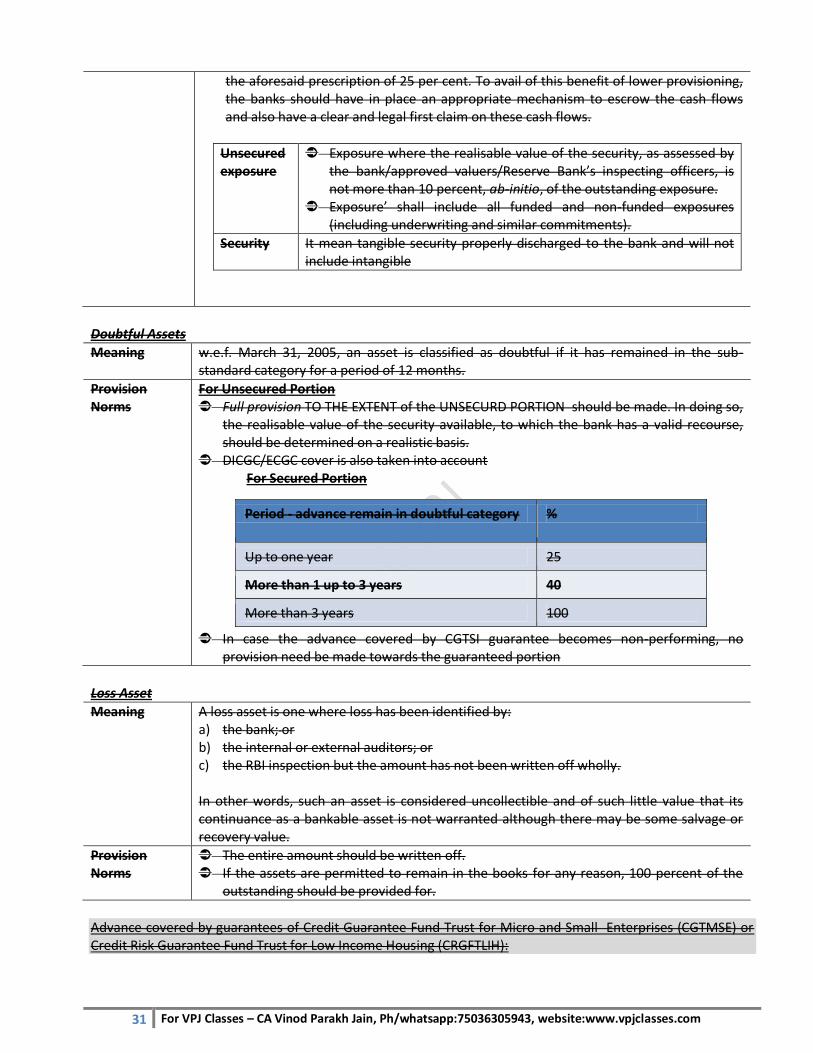

Unsecured exposure

Exposure where the realisable value of the security, as assessed by the bank/approved valuers/Reserve Bank’s inspecting officers, is not more than 10 percent, ab-initio, of the outstanding exposure.

Exposure’ shall include all funded and non-funded exposures (including underwriting and similar commitments).

Security It mean tangible security properly discharged to the bank and will not include intangible

Doubtful Assets

Meaning w.e.f. March 31, 2005, an asset is classified as doubtful if it has remained in the sub-standard category for a period of 12 months.

Provision Norms

For Unsecured Portion Full provision TO THE EXTENT of the UNSECURD PORTION should be made. In doing so,

the realisable value of the security available, to which the bank has a valid recourse, should be determined on a realistic basis.

DICGC/ECGC cover is also taken into account For Secured Portion

In case the advance covered by CGTSI guarantee becomes non-performing, no provision need be made towards the guaranteed portion

Period - advance remain in doubtful category %

Up to one year 25

More than 1 up to 3 years 40

More than 3 years 100

Loss Asset

Meaning A loss asset is one where loss has been identified by: a) the bank; or b) the internal or external auditors; or c) the RBI inspection but the amount has not been written off wholly. In other words, such an asset is considered uncollectible and of such little value that its continuance as a bankable asset is not warranted although there may be some salvage or recovery value.

Provision Norms

The entire amount should be written off. If the assets are permitted to remain in the books for any reason, 100 percent of the

outstanding should be provided for.

Advance covered by guarantees of Credit Guarantee Fund Trust for Micro and Small Enterprises (CGTMSE) or Credit Risk Guarantee Fund Trust for Low Income Housing (CRGFTLIH):

32 For VPJ Classes – CA Vinod Parakh Jain, Ph/whatsapp:75036305943, website:www.vpjclasses.com

In case the advance covered by CGTMSE or CRGFTLIH guarantee becomes non-performing, no provision need be made towards the guaranteed portion. The amount outstanding in excess of the guaranteed portion should be provided for as per the extant guidelines on provisioning for non- performing advances. After statutory audit, RBI conducts annual financial inspection of banks .Auditors may go through the divergence reported by RBI, if any, in terms of classification as well as provisioning and whether the same divergence has been appropriately addressed /clarified, by Banks. Accordingly auditor would be well advised to consider these aspects while take final view on classification /provisioning of such accounts.

Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act (SRFAESI), 2002 Securitisation of Standard Assets: [NOT RELEVANT FOR NOV 2016 attempt onward] After the enactment of the Securitization and Reconstruction of Financial Asset and Enforcement of Security Interest Act, 2002, banks have got significant power to possess the securities of defaulting borrower. Banks can now take possession of the assets from borrower and convert the same in Security Receipts.

Process In the process of securitisation, assets are sold to a bankruptcy remote special purpose vehicle (SPV) in return for an immediate cash payment. The cash flow from the underlying pool of assets is used to service the securities issued by the SPV.

Stages Securitisation follows a twostage process. In the first stage, there is sale of single asset or pooling and sale of pool of assets to a 'bankruptcy remote' special purpose vehicle (SPV) in return for an immediate cash payment and in the second stage repackaging and selling the security interests representing claims on incoming cash flows from the asset or pool of assets to third party investors by issuance of tradable debt securities. Thus, the non-performing asset of the banker is taken out of the balance sheet of the bank and converted into Security Receipts.

Accounting Securitised asset should be derecognised in the books of the bank, if the bank loses control of the contractual rights that comprise the securitised asset. The bank loses such control if it surrenders the rights to benefits specified in the contract. For enabling the transferred assets to be removed from the balance sheet of the originator in a securitisation structure, the isolation of assets or ‘true sale’ from the originator to the SPV is an essential prerequisite. In case the assets are transferred to the SPV by the originator in full compliance with all the conditions of true sale, the transfer would be treated as a 'true sale' and originator will not be required to maintain any capital against the value of assets so transferred from the date of such transfer. The effective date of such transfer should be expressly indicated in the subsisting agreement. In the event of the transferred assets not meeting the "true-sale" criteria the assets would be deemed to be on the balance sheet of the originator and accordingly the originator would be required to maintain capital for those assets. Profit & Loss on Such Sale When a bank sells the non-performing assets to securitising company, if the sale value of assets is less than the Net book Value, i.e., books value of advances less provisions, the shortfall needs to be debited to Profit & Loss Account. However, in case the sale value being higher, excess provision cannot be reversed and is kept to meet the shortfall/ loss on account of other non-performing assets

Acounting Treatment in the Book of subscribing

These Security Receipts are treated as non-SLR security (Investment) in the books of subscribing bank as per RBI guidelines. In the absence of ready market for the Security Receipts, the subscribing bank needs to value Security Receipts on the basis of Net Asset Value to be declared by Securitising Company on a quarterly basis.

33 For VPJ Classes – CA Vinod Parakh Jain, Ph/whatsapp:75036305943, website:www.vpjclasses.com

Bank

AMENDMENT NO.-3

Restructuring / Re-scheduling of Loans NOT RELEVANT FOR NOV 2016 ATTEMPT. Content of the Topic has been Changed

Eligibility Criteria

Banks may restructure the accounts classified under 'standard', 'sub-standard' and

'doubtful' categories.

Banks cannot reschedule / restructure / renegotiate borrowable accounts with

retrospective effect.

While a restructuring proposal is under consideration, the usual asset classification

norms would continue to apply.

Financial Viability

a) Account restructuring can be taken up by the banks when – (ii) the financial viability is established; and (iii) there is a reasonable certainty of repayment from the borrower, as per the terms

of restructuring package. b) The viability should be determined by the banks based on the acceptable viability

benchmarks determined by them, which may be applied on a case-by-case basis, depending on merits of each case. The parameters may include:

Return on Capital Employed

Debt Service Coverage Ratio

Assessing the viability of the project

Cash flow of the borrower c) BIFR cases are not eligible for restructuring without the express approval of the BIFR.

Asset Classification Norms

1) STAGES OF RESTRUCTURING The stages at which the restructuring/rescheduling/ renegotiation of the terms of loan agreement could take place are as under:

a) before commencement of commercial production/operation; b) after commencement of commercial production/operation but before the asset

has been classified as sub standard; and c) after commencement of commercial production/operation and after the asset has

been classified as sub standard or doubtful 2) Treatment of Restructured Standard/Sub-Standard Accounts:

a) The accounts classified as 'standard assets' should be immediately re-classified as 'substandard assets' upon restructuring

b) The non-performing assets, upon restructuring, would continue to have the same asset classification as prior to restructuring and slip into further lower asset classification categories as per extant asset classification norms with reference to the pre-restructuring repayment schedule

c) Any additional finance may be treated as ‘standard asset’, up to a period of one year after the first interest/principal payment, whichever is earlier, falls due under the approved restructuring package.

d) If the restructured asset does not qualify for up-gradation at the end of the above specified one year period, the additional finance shall be placed in the same asset classification category as the restructured debt.

Upgradation of Accounts

All restructured accounts which have been classified as NPA upon restructuring, would be eligible for up-gradation to the ‘standard’ category after observation of ‘satisfactory performance’ during the ‘specified period’.

Specified Period means a period of one year from the date when the first payment of

34 For VPJ Classes – CA Vinod Parakh Jain, Ph/whatsapp:75036305943, website:www.vpjclasses.com

interest or instalment of principal falls due under the terms of restructuring package. If satisfactory is not evidenced, the asset classification of the restructured account

would be governed as per the applicable prudential norms with reference to the pre-restructuring payment schedule.

Income Recognition Norms

Interest income in respect of restructured accounts classified as 'standard assets' is to be recognised on accrual basis and that in respect of the accounts classified as 'non-performing assets' is to be recognised on cash basis.

Provisioning Norms

Normal Provisions Additional Provisions (Note 1)

As per the existing provisioning norms on all restructured advance