1 © OLIVER WYMAN | CHI-HLC06101-046 HEALTH & LIFE SCIENCES HEALTH CARE 2020 ROADMAP – THE VOLUME TO VALUE REVOLUTION AOA Meeting San Antonio June 7, 2014 Jim Bonnette, MD Partner, Chief Medical Officer 1 © OLIVER WYMAN | CHI-HLC06101-046 1 Volume to Value Pre-Test • In a population pyramid what is the savings potential of patient centered care? – A. 5% – B. 10% – C. 15% • South Central Foundation has been providing population based care for how many years? – A. 10 – B. 20 – C. 30 • The top 1% of Medicare patients cost on average how much per year? – A. $75,000 – B. $125,000 – C. $200,000 • Efficient population health managers can reduce Medicare admissions – A. 25% – B. 35% – C. 50% 2 © OLIVER WYMAN | CHI-HLC06101-046 2 VOLUME TO VALUE REVOLUTION

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

© OLIVER WYMAN | CHI-HLC06101-046

HEALTH & LIFE SCIENCES

HEALTH CARE 2020 ROADMAP –THE VOLUME TO VALUE REVOLUTION

AOA Meeting San Antonio

June 7, 2014

Jim Bonnette, MDPartner, Chief Medical Officer

1© OLIVER WYMAN | CHI-HLC06101-046 1

Volume to Value Pre-Test• In a population pyramid what is the savings potential of patient centered care?

– A. 5%

– B. 10%

– C. 15%

• South Central Foundation has been providing population based care for how many years?

– A. 10

– B. 20

– C. 30

• The top 1% of Medicare patients cost on average how much per year?

– A. $75,000

– B. $125,000

– C. $200,000

• Efficient population health managers can reduce Medicare admissions

– A. 25%

– B. 35%

– C. 50%

2© OLIVER WYMAN | CHI-HLC06101-046 2

VOLUME TO VALUE REVOLUTION

2

3© OLIVER WYMAN | CHI-HLC06101-046 3

Momentum is building

Medicare

Employers Medicaid

Consumers

Across populations

Across geographies

Across health conditions

Easy

Personal

Integrated

Error free

Personalized

Mobile/social

Always available

Less invasive

Predictive/preventative

Accessible

Much better value

Population Health and Lifestyle Managers rotating over $1 TN

towards higher value

4CASECODE-FILENAME (YYYYMMDD Descriptor).ppt© Oliver Wyman � www.oliverwyman.com

Concepts driving change

�No matter what the regulatory or payment system, physicians and caregivers around the globe fundamentally deliver care the same way focusing on symptomatic treatment and acute care, not longitudinal care or prevention

�The age wave, extended longevity and new medical technologies are exacerbating the cost issue – and this will get significantly worse without change

�Current care systems are neither safe nor efficient, most care provided by physicians could be provided by those of a lesser skill level as part of a team

�Automating the current symptomatic treatment system through EHR’s is insufficient to drive the quality, cost and efficiency gains required to create an affordable and sustainable system

�Payment mechanism reforms alone are insufficient to put the healthcare system on a sustainable cost and quality track – and the economic weight of the current system could cripple the economic vitality of any country (and FFS is a problem)

�Providing more of the right services to the sickest of the sick actually reduces total cost

�Only when we change in a very fundamental fashion how we engage and manage patients will we significantly impact the safety, quality and cost

55© OLIVER WYMAN | CHI-HLC06101-046

Unleashing free market competition – What is possible

20% total cost reduction

5.5% trend reduction

25% consumer value improvement

$7 TN of cost reduction over ten years

$1 TN of value rotation

100X the diffusion rate

3

66© OLIVER WYMAN | CHI-HLC06101-046

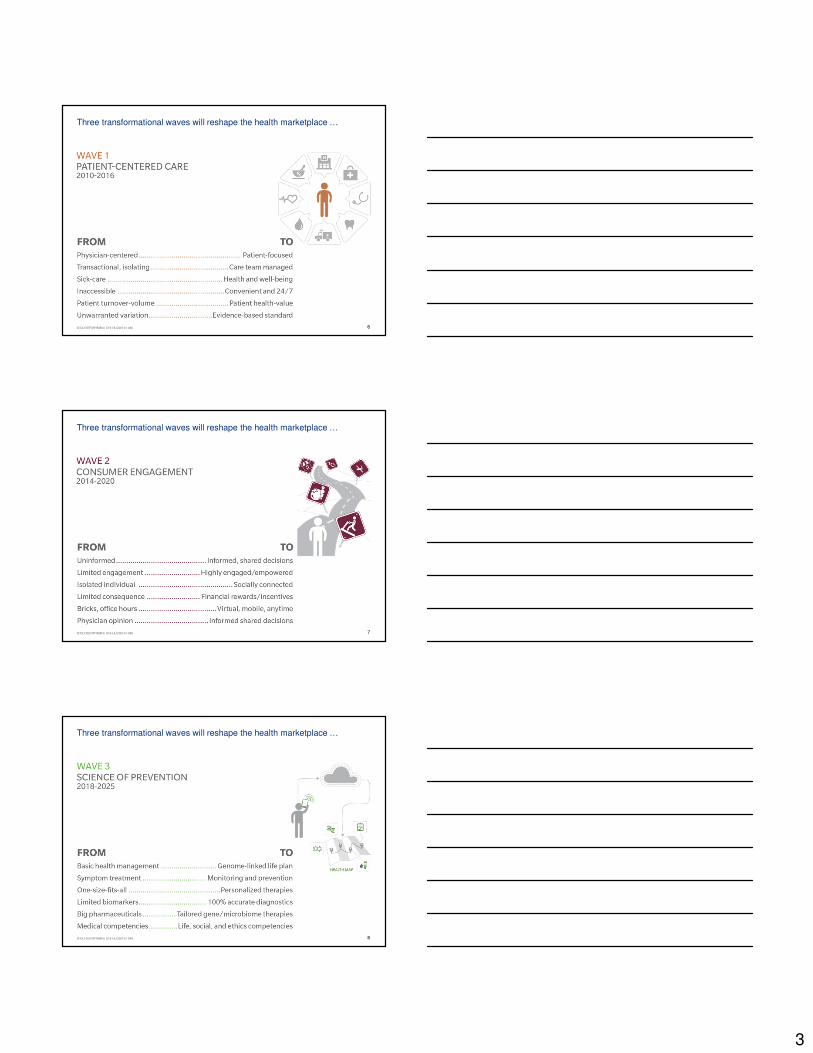

Three transformational waves will reshape the health marketplace …

77© OLIVER WYMAN | CHI-HLC06101-046

Three transformational waves will reshape the health marketplace …

88© OLIVER WYMAN | CHI-HLC06101-046

Three transformational waves will reshape the health marketplace …

4

99© OLIVER WYMAN | CHI-HLC06101-046

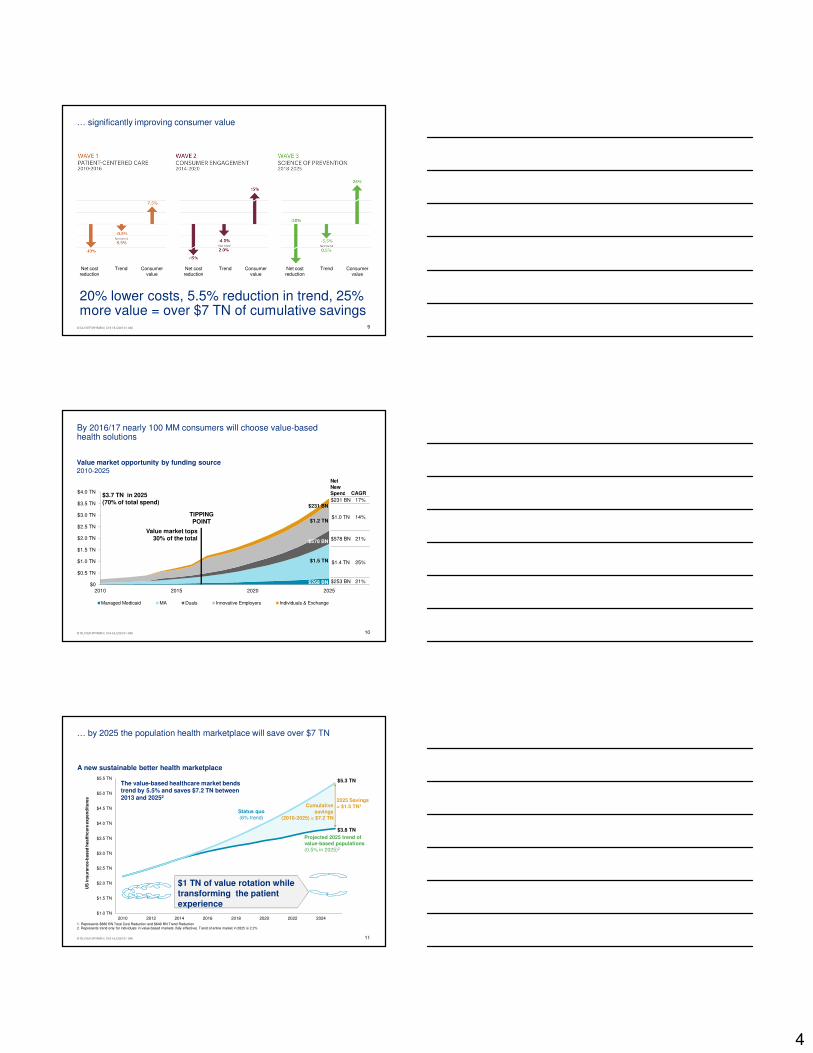

… significantly improving consumer value

20% lower costs, 5.5% reduction in trend, 25% more value = over $7 TN of cumulative savings

Net cost reduction

Trend Consumer value

Net cost reduction

Trend Consumer value

Net cost reduction

Trend Consumer value

10© OLIVER WYMAN | CHI-HLC06101-046 10

By 2016/17 nearly 100 MM consumers will choose value-based health solutions

$0

$0.5 TN

$1.0 TN

$1.5 TN

$2.0 TN

$2.5 TN

$3.0 TN

$3.5 TN

$4.0 TN

2010 2015 2020 2025

Managed Medicaid MA Duals Innovative Employers Individuals & Exchange

$268 BN

$1.5 TN

$578 BN

$1.2 TN

$231 BN

Value market opportunity by funding source2010-2025

NetNew Spend CAGR

$231 BN 17%

$1.0 TN 14%

$578 BN 21%

$1.4 TN 25%

$253 BN 21%

$3.7 TN in 2025(70% of total spend)

Value market tops 30% of the total

TIPPING POINT

11© OLIVER WYMAN | CHI-HLC06101-046 11

… by 2025 the population health marketplace will save over $7 TN

$1.0 TN

$1.5 TN

$2.0 TN

$2.5 TN

$3.0 TN

$3.5 TN

$4.0 TN

$4.5 TN

$5.0 TN

$5.5 TN

2010 2012 2014 2016 2018 2020 2022 2024

US

in

su

ran

ce-b

ased

healt

hcare

exp

en

dit

ure

s

Status quo(6% trend)

Projected 2025 trend of value-based populations(0.5% in 2025)2

2025 Savings = $1.5 TN1

The value-based healthcare market bends trend by 5.5% and saves $7.2 TN between 2013 and 20252

$5.3 TN

$3.8 TN

1. Represents $880 BN Total Cost Reduction and $640 BN Trend Reduction2. Represents trend only for individuals in value-based markets (fully effective). Trend of entire market in 2025 is 2.2%

Cumulative savings

(2010-2025) = $7.2 TN

$1 TN of value rotation while transforming the patient experience

A new sustainable better health marketplace

5

12© OLIVER WYMAN | CHI-HLC06101-046 12

The race to value will drive consolidation and convergence

Near-term population

risk arbitrage

Procedure

volume

PCPs

Payers

Hospitals

Diagnostics/Labs

Specialists

Ambulatory Facilities

Physical/Occupational Therapy

Long-term Care

Home Care

Behavioral Health

PBMs

Brokers/Distribution

Ethical Drugs

Devices/Equipments

Sales volume

(prescription)

Fitness/Nutrition

OTC

HIT

TPAs

CROs

Web-based consumer information

Commissions

Advertising

Sales volume

(consumer)

On-going revenue

streams for B2B service

Value Model Value Models

Long-term clinical risk arbitrage

Efficient episode management

On-demand al-a-carte services

Shared savings

Consumer subscriptions

B2B enablement

Product and service add-ons

App/gadget/software sales

Traditional siloed business designs Converged wellness health ecosystems

1313© OLIVER WYMAN | CHI-HLC06101-046

Next generation leaders / innovators will leverage the work of the pioneers

• 18% lower than average member costs

• 24% lower than average hospitalization rate

• 38% shorter than average hospital stays

• $2 MM savings for every 1,000 members

• Medicare readmission rates up to 30% lower than national average

• Leader in CA in patient satisfaction (top 10%)

• 50% drop in urgent care and ER utilization

• 40% drop in hospital admissions

• Patient and staff satisfaction over 90%

Founded: 1992

Whole-Pyramid Focus

Founded: 1997

Complex/Polychronic Focus

Founded: 1982

Whole-Pyramid Focus

Imp

act

Sources: WellPoint; http://www.gogreendps.com/HealthCarePartnersCommReport.htm; Southcentral Foundation - Nuka System of Care 09-05-12 V2; http://content.healthaffairs.org/content/30/3/416.extract

… only better – open, social / mobile, scalable, portable, assimilative, personalized and always available

14© OLIVER WYMAN | CHI-HLC06101-046 14

From physician to patient (or will it be consumer) centered

6

15© OLIVER WYMAN | CHI-HLC06101-046 15

Today: Fee-for-Service (2013)

My doctor controls my referrals, and I don’t know who provides the best care

Doctor’s hours don’t match real life hours

I feel rushed during doctor visits

I only seek care when I have no other alternative

I am the only person coordinating my care –doctors don’t talk to each other and don’t think about me once I leave their office

I avoid my healthcare because it’s too confusing and inconvenient

I have no idea how my insurance works – it’s so confusing

I feel lost and overwhelmed

1616© Oliver Wyman | CHI-SRH01811-007

This is what we currently call “patient-centered” care

Payer Affiliated physicians Care/access programs FQHCs County/community services Collaboration Flow of funds Claims reimbursement Informal linkages

Additional resources include: psychiatrists for inpatient, social workers, palliative care, hospitalists, advanced practice providers, RNs/MAs, etc.

h

County programs

Lancaster General Health

Clinic A

Hospital A

Specialty Group

Superutilizers program

MH/MR/EI

Office of aging

Coalition to end homelessness

Drug & alcohol commission

Other county programs include: Children & Youth Agency, County Prison, Adult Probation & Parole Services, Veteran’s Affairs

Poverty assistance

FQHC

Medicaid

MedicaidFFS

Mobile psychiatric nursing

Mental Health MCO

FQHC BH Integration Project

Assertive Community Treatment (ACT)

Rehab/detox services

State

Treatment for serious mental illness

Food stamps, welfare, etc.

Safety net services for the frail elderly

Housing support and transitional assistance

Healthy beginnings+

Nurse family partnership

Geriatric house call

Heart failure/high risk clinic

MCO B

MCO A

MCO E

MCO D

MCO C

County A

County C

County B

County E

County D

Medical & dental center FQHC

Medical Group A

IPA A

HIV clinic

PCMH NCQA level 3 accreditation

PACE/program participation

Transportation programs

Inpatient psych

Emergency department

Urgent care

Rx assistance programs

Employment assistance

Home care providers

Support groups for drug &

alcohol

Inpatient rehabilitation

facilities

Crisis interventions

Case management

Support helplines

Food banks/stamps/

distribution

Child welfareProtective services

Pharmacies

Social rehabilitation

Low-income energy

assistance

Drug & alcohol outpatient centers

Domestic abuse support

services

Housing, shelters, missions

Unaffiliated healthcare providers

Outpatient center/clinic

Health express

Community resources

Other MH/BH networks

Emergency/transitional

housing

Support for the disabled

Counseling and legal services

IDN ACounty

project access

Member

Mental health collaborative

1717© OLIVER WYMAN | CHI-HLC06101-046

Wave 1: Patient-centered care

My care team truly cares about my holistic health –I am not alone

I work with my care team to improve my health and live better – we have a shared plan that is personalized to me

I believe that my healthiest days are ahead of me

My care team takes care of all my health needs

The system isworking for me

My substance abuse and depression are managed

My care team proactively motivates me to stick to my care plan

I monitor my health with tools to identify issues early

Care extends beyond my doctor’s office to my home and to local retailers

7

1818© OLIVER WYMAN | CHI-HLC06101-046

Wave 1 – Patient-centered population managers come of age

Patient-centered care“Team-based, guided, and coordinated”

1919© OLIVER WYMAN | CHI-HLC06101-046

Wave 1: … and provide more benefits for each dollar across the population pyramid

Population health management requires specific strategies and health management approaches for each layer of the pyramid

Pyramid value redistribution

2020© OLIVER WYMAN | CHI-HLC06101-046

Wave 1: Population health managers master the pyramid

Expenditure Population PMPY

$258 BN 12.9 MM $19,929

Expenditure Population PMPY

$136 BN 15.4 MM $8,864

Expenditure Population PMPY

$150 BN 51.3 MM $2,929

Expenditure Population PMPY

$255 BN N/A N/A

Expenditure Population PMPY

$158 BN 4.7 MM $33,259

Expenditure Population PMPY

$125 BN 7.7 MM $16,433

Expenditure Population PMPY

$334 BN 29.0 MM $11,506

Expenditure Population PMPY

$80 BN 18.1 MM $4,418

Expenditure Population PMPY

$185 BN 121.7 MM $1,520

C

D

F

HAcute episodic care

I

Severe mental/neurological illness

B

Chronic with extensive social needs

E

Early stage behavioral and risk factors

G

End of life/long-term careA

Frail elder

Poly-chronic/complex

Early stage chronic

General healthy

8

2121© OLIVER WYMAN | CHI-HLC06101-046

Wave 1: Population health managers grow at the expense today’s FFS profit centers

Inpatient

Outpatient

Emergency Department

Retail

Primary care hubs

Direct primary care

Virtual web based health models

Convenient care clinics

Diagnostics

Specialty care offices

Ambulatory center

LTC facilities

Behavioral health

Home health care

Outlook for traditional players in a value-based population management ecosystem

22CASECODE-FILENAME (YYYYMMDD Descriptor).ppt© Oliver Wyman � www.oliverwyman.com

The shift in patient care will drive practice revenue to PCPs and select specialties that play coordinating roles at the primary expense of surgical specialists

40%

27%

6%

7%

26%

23%

12%

13%

13%

12%

4%

3%

0%

20%

40%

60%

80%

100%

Current expenditures Future expenditures

with care models

Impact of care models on medical expenditures1

Hospitals

Rx

Med equip & non-durable med prod.

Legend

Nursing home / home health

Medical specialists

PCP

% change

(5%)

(10%)

10%

(10%)

20%

(32%)

(15%)

$2.0 T

$1.7 T

19% 23%

6%7%

14%15%

17%17%

3%2%11%

10%

10%8%

21% 14%

0%

20%

40%

60%

80%

100%

Current expenditures Future expenditures

with care models

Impact of care models on physician specialties

5% decrease

10% decrease

20% decrease

30% decrease

Legend

5% increase

10% increase

20% increase

Types of physicians

$597 B$574 B

1 Excludes other non-IHM spend (e.g., private insurance, dental, gov’t) which represent $0.3T in spend and are not impacted by care models

No change

�Internal medicine�Pediatrics

�Oncology�Pulmonology

�Cardiologist�Endocrinologist

�Neurology�ENT

�ER medicine

�Gastroent.�OB/GYN

�Cardio int. �Orthopedic surg

�Gen surg.�Radiology�CV surgery

Specialists 10% decline

PCP20% increase

Med

ical exp

en

dit

ure

s

23© OLIVER WYMAN | CHI-HLC06101-046 23

Wave 1: Population health managers redefine patient value

Wave 1: Patient-centered care

Wave 1 predictions 10% less cost, 0.5% trend reduction, 7.5% more value

Wave 3: The science

of prevention

Wave 2: Consumer engagement

Most patients love their population health manager and value thepatient experience

Multi-skilled health and wellness teams (social workers, nutritionist, coaches) are the norm

70% of provider visits are conducted virtually, or outside of normaloffice hours

75% of patients have a personal health record and a health management plan

75% of poly-chronic patients have their care coordinated across settings by a navigator

35 national and regional population health managers will control 70% of the market and compete on value

Patient-centered population health organizations will replace PPO networks

Population health managers will control 70% of clinical risk

9

24© OLIVER WYMAN | CHI-HLC06101-046 24

From patient to consumer centered

2525© OLIVER WYMAN | CHI-HLC06101-046

Wave 2: Consumer engagement

I know how to livewell and be healthy –I have great resources (apps) at my disposal to inform me

I feel engagedin my health and am empowered to make informed decisions

I know what I need and how to buy it – shopping and health tools have made it easy and boosted my confidence

I use crowdsourced reviews of goods and service providers (like Yelp) to decide where I can get the best value

Competing against friends in online health challenges motivates me to live healthier – I earn great rewards that I value

I connect through social media to other “patients like me”

Consumer-driven competition is great – all the population health managers have extended office hours and most offervirtual web visits

I can surf and navigate the health system with ease and the patient-centered care models are so convenient and easy to work with

I have web-based/mobile tools so I can manage my healthcare

2626© OLIVER WYMAN | CHI-HLC06101-046

• Disease status

• Benefit status

• Episodic/point-in-Time View

Wave 2: Redefine the consumer experience by shifting the lens

• Disease status

• Benefit status

• Motivational profile

• Lifestyle factors

• Socioeconomics & life stage

• Health needs & behavioral profile

• Preferences, interests, goals

• Family situation

• Longitudinal lifetime view

Heart

patient

Whole

patient

Whole

consumer

Today’s transactional system

Wave 1 Patient-centered care

Wave 2 Consumer engagement

Consumer mindshare

Consumer loyalty

Consumer timeshare

Consumer wallet share

Consumer biodata share

10

27© OLIVER WYMAN | CHI-HLC06401-026 27

How many times a year does an average consumer visit a grocery

store?

How many consumers visit a Walmart every month in the US?

28© OLIVER WYMAN | CHI-HLC06401-026 28

Retailers have chosen to focus their investments to-date on one or more of seven potential business designs

Retailer Healthcare Business Designs

Value-based healthcare Healthcare enablement

Representative offering and early movers

Retail integrated delivery network

5

• Care delivery• Care

networks• Health

insurance / population risk

Health product marketplace

1

• Pharmacy• Optometry• Audiology• Insurance• Health &

beauty• OTC• Fresh

Population health management

4

• Care coordination

• Chronic condition management

• Frail elder programs

Wellness and lifestyle support

2

• Nutrition programs

• Health education

• Fitness games / P2P

Shopper health data and analytics

7

• Shopper purchase data sets / dashboards

• Consumer behavior analytics

Financial products & decision support

6

• Health insurance exchange

• Plan selection guidance

• HSAs• Financial

planning

Primary care delivery

3

• In-store or standalone primary care clinics

• Health kiosks• EMRs

Transactional healthcare

(emerging)

2929© Oliver Wyman

My thoughts on healthcare• Nearly everything I do affects my health• My health status directly impacts my health costs!• I need to select benefits (insurance) that fit me• There are many things I can control (nutrition, fitness)• There are some things I can’t control (genetics)• There are intrinsic and extrinsic reasons to be as

healthy as I can• I need a plan for my health, and partners to help me• I need to spend smart – and find the best value!• “Ah – Insurance means Insurance…not ‘Free’”• Out-of-pocket spending sucks!

Consumers are demanding a solution for their healthcare issues, driving them from unengaged to behaviorally and economically motivated

Things I plan for• Housing• Food • Clothing• Transportation• Fun and entertainment• Healthcare• Higher education• Retirement

Things I plan for• Housing• Food • Clothing• Transportation• Fun and

entertainment• Healthcare• Higher education• Retirement

My thoughts on healthcare• How do I get Insurance?

It’s confusing!• What’s a Healthcare exchange?• Why doesn’t it cover everything? • Should I choose a private Medicaid plan?• Where should I go for care, and how often?• Out-of-pocket spending sucks!

Healthcare today“Disconnected, unengaged,

entitled”

Healthcare tomorrow“Economically and behaviorally

aware and accountable”

11

3030© OLIVER WYMAN | CHI-HLC06101-046

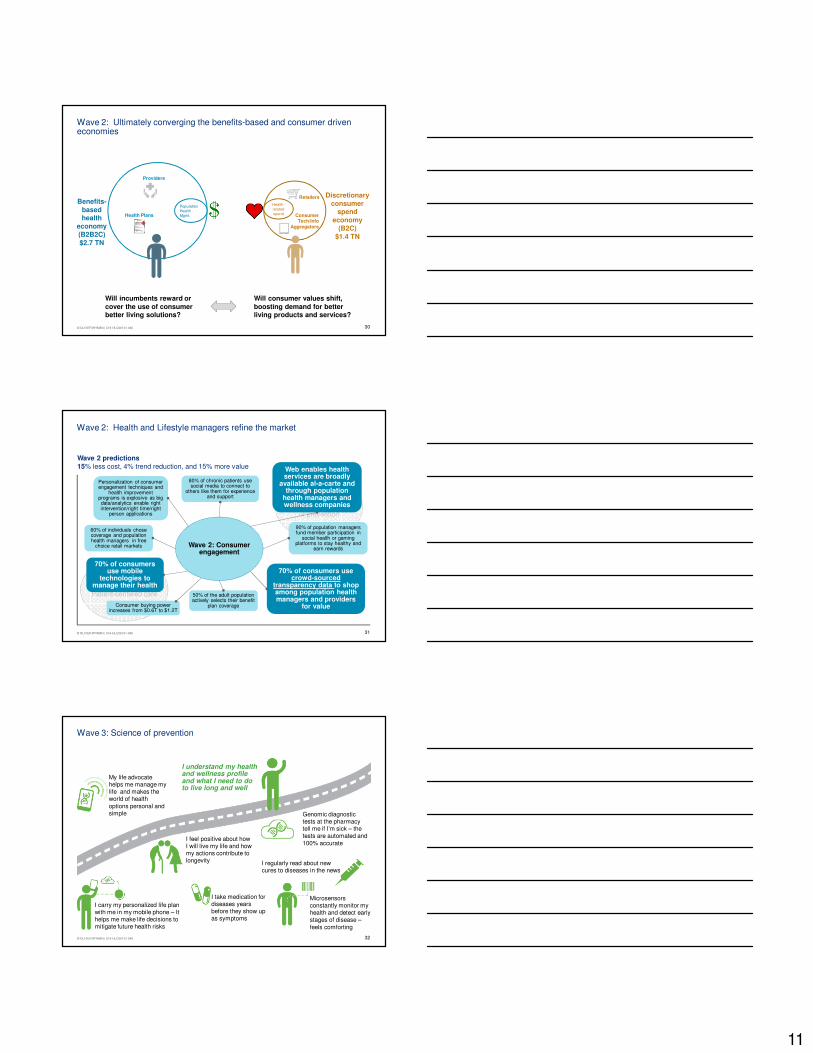

Wave 2: Ultimately converging the benefits-based and consumer driven economies

Population Health Mgmt.

Health-related spend

Benefits-basedhealth

economy(B2B2C)$2.7 TN

Discretionary consumer

spend economy

(B2C)$1.4 TN

Retailers

Consumer Tech/Info

Aggregators+

Providers

Health Plans

Will incumbents reward or cover the use of consumer better living solutions?

Will consumer values shift, boosting demand for better living products and services?

3131© OLIVER WYMAN | CHI-HLC06101-046

Wave 2: Health and Lifestyle managers refine the market

Wave 2: Consumer engagement

Wave 2 predictions15% less cost, 4% trend reduction, and 15% more value

Wave 1Patient-centered care

Wave 3The science of prevention

Personalization of consumer engagement techniques and

health improvement programs is explosive as big data/analytics enable right intervention/right time/right

person applications

60% of individuals chose coverage and population health managers in free

choice retail markets

Web enables health services are broadly

available al-a-carte and through population

health managers and wellness companies

Consumer buying power increases from $0.6T to $1.2T

70% of consumers use crowd-sourced

transparency data to shop among population health managers and providers

for value

80% of chronic patients use social media to connect to

others like them for experience and support

70% of consumers use mobile

technologies to manage their health

50% of the adult population actively selects their benefit

plan coverage

90% of population managers fund member participation in

social health or gaming platforms to stay healthy and

earn rewards

3232© OLIVER WYMAN | CHI-HLC06101-046

Wave 3: Science of prevention

I understand my health and wellness profile and what I need to do to live long and well

My life advocate helps me manage my life and makes the world of health options personal and simple

I carry my personalized life plan with me in my mobile phone – It helps me make life decisions to mitigate future health risks

I feel positive about how I will live my life and how my actions contribute to longevity

Genomic diagnostic tests at the pharmacy tell me if I’m sick – the tests are automated and 100% accurate

I take medication for diseases years before they show up as symptoms

I regularly read about new cures to diseases in the news

Microsensors constantly monitor my health and detect early stages of disease –feels comforting

12

3333© OLIVER WYMAN | CHI-HLC06101-046

Pri

ce

Genomic sequencing cost curve

Time

Imp

act

Biomarker and pathway inventory

New treatment development

+ Low cost high power computing+ Big data+ Advanced analytics+ Super high speed networks+ Nano pore technology

Low cost sequencing

Advanced computing

Real economic and clinical impact

Tech platform change – PCR to sequencing

2013 20252020

$100

$1,000

$10,000

High

Low

+ =

Wave 3: Low-cost sequencing and advanced computing redefine what is possible

• $100 at home sequencing• 100% accurate diagnosis• 100% best treatment EBM• 100% personalized

3434© OLIVER WYMAN | CHI-HLC06101-046

Wave 3: Better Living organizations redefine prevention and early intervention while virtually eliminating diagnostic errors and personalizing treatments

Wave 2Consumer

engagement

Wave 1Patient-centered care

Life expectancy is 20% longer than today, with a higher

quality of life up until death

The discovery of 10,000 new biomarkers/pathways lead to more than 1,000 new predictive diagnostics and a 100 super-early stage treatments

75% of diagnosis are completed in real time through a single

sample, at home or in a convenient retail location with

100% accuracy

60% of therapeutics are focused on “prevention” and “very early stage treatment” vs. responsive

symptomatic sick care

75% of population has a life plan linked to personal genome

sequence and genomicrisk profile

Two major diseases are cured or eradicated

Wave 3The science of prevention

Wave 2 predictions15% less cost, 4% trend reduction, and 15% more value

35© OLIVER WYMAN | CHI-HLC06101-046 35

SIX BIG QUESTIONS every leader should be considering

13

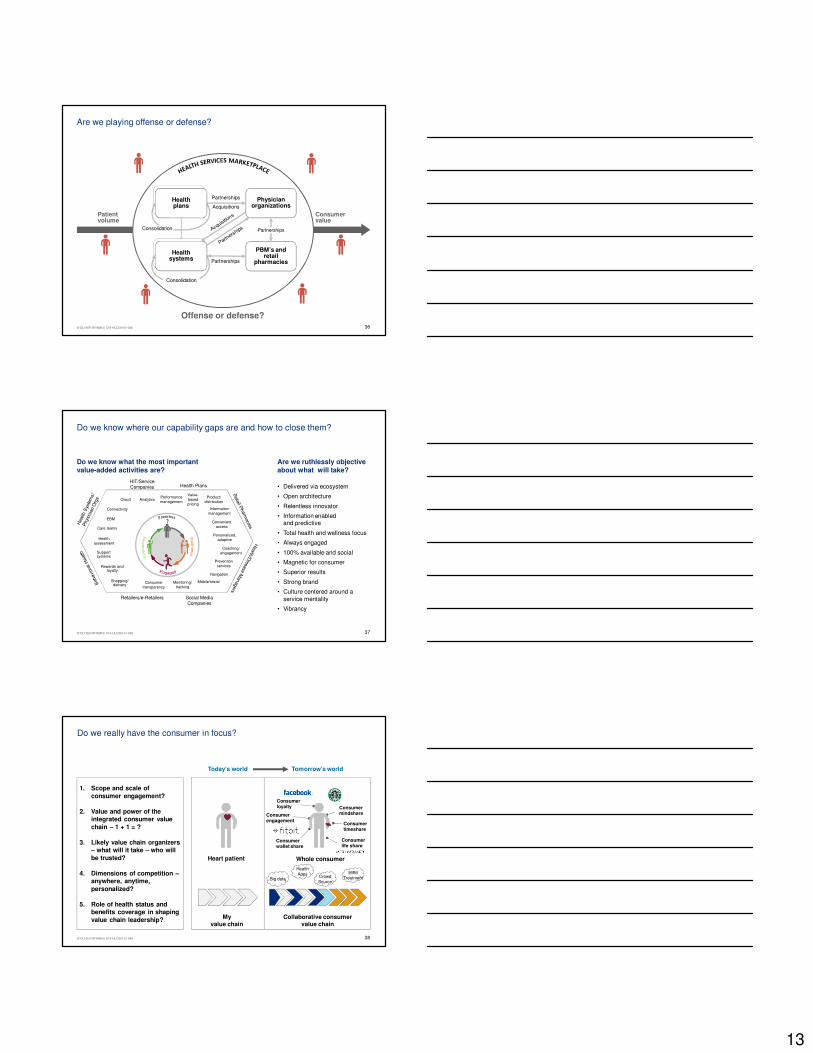

3636© OLIVER WYMAN | CHI-HLC06101-046

Patient volume

Consumer value

PBM’s and retail

pharmacies

Partnerships

Acquisitions

Partnerships

Partnerships

Healthplans

Consolidation

Healthplans

Consolidation

Healthplans

Physicianorganizations

Healthsystems

Offense or defense?

Are we playing offense or defense?

3737© OLIVER WYMAN | CHI-HLC06101-046

• Delivered via ecosystem

• Open architecture

• Relentless innovator

• Information enabled and predictive

• Total health and wellness focus

• Always engaged

• 100% available and social

• Magnetic for consumer

• Superior results

• Strong brand

• Culture centered around a service mentality

• Vibrancy

Retailers/e-Retailers Social Media Companies

HIT/Service Companies Health Plans

Healthassessment

Personalized,adaptive

Navigation

Convenientaccess

Analytics

Preventionservices

Mobile/social

Connectivity

Cloud

EBM

Monitoring/tracking

Performancemanagement

Product/distribution

Value-basedpricing

Care teams

Coaching/engagement

Shopping/delivery

Rewards andloyalty

Consumertransparency

Supportsystems

Informationmanagement

Do we know where our capability gaps are and how to close them?

Do we know what the most important value-added activities are?

Are we ruthlessly objective about what will take?

38© OLIVER WYMAN | CHI-HLC06101-046 38

Do we really have the consumer in focus?

My value chain

Collaborative consumer value chain

Heart patient

Consumer mindshare

Consumer loyalty

Consumer timeshare

Consumer engagement

Consumer wallet share

Consumer life share

Whole consumer

Today’s world Tomorrow’s world

1. Scope and scale of consumer engagement?

2. Value and power of the integrated consumer value chain – 1 + 1 = ?

3. Likely value chain organizers – what will it take – who will be trusted?

4. Dimensions of competition –anywhere, anytime, personalized?

5. Role of health status and benefits coverage in shaping value chain leadership?

Big data

Health Apps

Crowd Source

EBM Treatment

14

39© OLIVER WYMAN | CHI-HLC06101-046 39

Are we prepared to play in a multi-chain world?

From To

Solo-sport orientation Ecosystem-based

Wholesale Retail

Sickness Total health & wellness

Reactive Predictive/preventative

Body part or diagnostic code Whole person

Physical Virtual/anywhere/real-time

Transactional Relational

One-size-fits-all Personalized

Opaque Transparent

Individual/expert Crowd

My value chain Collaborative consumer value chain

Big data

Health Apps

Crowd Source

EBM Treatment

40© OLIVER WYMAN | CHI-HLC06101-046 40

Health retailers and e-retailers

Tech, consumer goods and services

Providers

Health plans

Have we really considered the compete or converge question?

Extra-industry players

Race to capitalize on higher value consumer relationships

Traditional healthcare players

Consumer mindshare

Consumer loyalty

Consumer timeshare

Consumer wallet share

Consumer biodata share

4141© OLIVER WYMAN | CHI-HLC06101-046

• Is the cost of inaction on the rise?

• Is there an inflection point where we can’t catch up to the leaders of the pack?

• If one of these models entered our markets, could we respond?

Are we moving fast enough?

The leader advantage is expanding, fueled by new technology, capital markets, and hare earned lessons

Today-player questions

Today’s Volume Players

Org

an

iza

tio

na

l s

op

his

tic

ati

on

Value creation

2nd Generation Leaders

1st Generation Leaders

15

42© OLIVER WYMAN | CHI-HLC06101-046 42

Volume to Value Post-Test• When is the estimated tipping point to value based insurance coverage?

– A. 2020

– B. 2017

– C. 2025

• What is the potential reduction in hospital admissions with value-based care?

– A. 10%

– B. 20%

– C. 30%

• What % of patients drive 45% of the cost?

– A. 10%

– B. 15%

– C. 5%

• What is the potential range of savings for these patients?

– A. 15%

– B. 25%

– C 35%

Related Documents