Vol. XII December, 2014

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Vol. XIIDecember, 2014

i

ISSN 0975-1211

REVELATION

The Research Journal

of

K.P.B. Hinduja College

Volume XII

December 2014

K.P.B. Hinduja College of Commerce

315, New Charni Road, Mumbai 400 004.

ii

ISSN 0975-1211

Editorial Board

Chief Editor: Dr. T.A.Shiware

Managing Editor: Dr. (Ms.) Minu Madlani

Executive Editor: Dr. (Ms.) Rajeshwary G.

Advisors:

1. Dr. J.F.Patil

2. Dr. S.K.G. Sundaram

3. Dr. L. M. Dani

4. Dr. G.M.Talhar

5. Dr. R.R.Khan

6. Dr. Madhu Nair

7. Dr S. Kaptan

Place of Publication: K.P.B. Hinduja College of Commerce

315, New Charni Road,

Mumbai 400004.

Views expressed in the articles are those of the authors and do not necessarily represent

those of the Editor of the Journal. All rights are reserved. No part of this publication may be

reproduced or copied in any form by any means without prior written permission.

iii

ISSN 0975-1211

Vol. No. 12 December 2014

Contents

Sr. No. Subjects Page No.

1 Foreword from the Chief Editor v

2. From the Executive Editor’s Desk vi

3. Perception Mapping On Purchase Behaviour of Smart Phone among

Working Women in the Corporate of Coimbatore City

Dr. Angamuthu

Balasubramaniam

1

4 Micro Finance- A Way to Alleviate Poverty

Shweta Sawhney

21

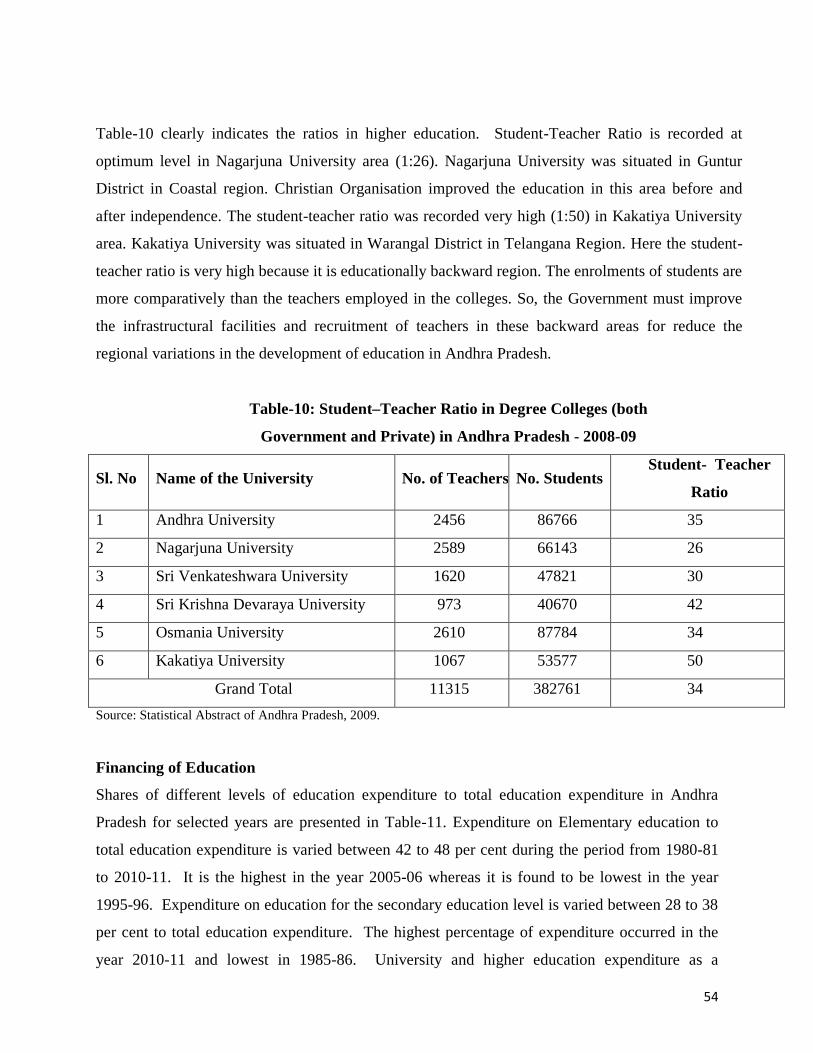

5 Trends In The Growth Of Higher Education In Andhra Pradesh

Dr. D. Pulla Rao

37

6 The Retail Revolution in Mumbai

Dr. L. R. Bahadur

58

7 A Study of Pre and Post Impact of Online trading in Indian Stock

Market

Dr. Gayatri Agarwal

68

8 Enhancing Airline Warehousing Productivity through State-Of-The-

Art Information Technology Implementation

Dr. Siddhartha Ghosh

74

iv

From the Editor’s Desk

The Research Journal Revelation is being brought out by K.P.B. Hinduja College of

Commerce with a view to assist academicians, professionals and researchers to share

information on topics related to Growth and Development of Business in India. The aim of

this Journal is to encourage researchers to contribute research articles based on

Industry Studies or on the Findings of Research Projects that have been executed. Issues

relevant to the growth and development of Indian Economy, in the streams of Arts, Science,

Social Sciences, Economics, Commerce and Management are also welcome.

Original research articles based on an up to date review of literature and supportive

primary/secondary data are invited.

Frequency of Publication: Biannual

Contact Address:

K.P.B. Hinduja College of Commerce, 315, New Charni Road, Mumbai.400 004.

Phone 022 4098 9000 Fax : 2385 93 97.

Email : [email protected]

Executive Editor’s E mail address: [email protected]

v

Foreword from the Chief Editor

India will have to radically transform its manufacturing sector by focusing on a large scale

labor-intensive factors by producing exportable goods and by reducing the share of

employment in agriculture from the present 58% to 25% by 2030, with industry doubling its

labor demand. To usher in a manufacturing revolution in India, the country’s exports have to

play a critical role and this must accelerate at a much faster pace to achieve a growth rate of

20-25% in real terms.

Small and medium enterprises (SMEs) play a significant role in generating millions of jobs.

India needs to enhance their scale of operations, to ensure better adoption of technology, to

provide innovative financing and a mechanism for upgrading the skills of workers. Labor-

intensive sectors like food processing, apparels and textile, leather and footwear contribute to

over 60 per cent of SMEs employment. Hence a greater focus on the growth of labor

intensive sectors will enable the absorption of a growing surplus of unskilled labor. As

energy costs have a major bearing on the manufacturing sector, India needs to make available

a continuous supply of power by removing constraints on coal and gas. It is a known fact that

freight and logistics costs are enormously high and that 70 per cent of container

transportation is through roads, a model shift from road to rail is therefore necessary. In

addition, port infrastructure needs a radical overhaul as the average turnaround time in India

is a 3.5 days as against a mere 10 hours in Hongkong. For large-scale manufacturing to take

off, India must be transformed into an attractive investment hub with businesses clearances

becoming less time –consuming, expensive and cumbersome.

India needs to focus on the development of industrial clusters where it can create an

ecosystem of supply-chain responsiveness, lower logistics costs, availability of labor and

vi

technology up gradation. These clusters will converge the advantages of higher innovation

and employment generation for small firms with scale and costs advantages of larger

organizations.

Finally, India needs to vigorously pursue FDP in manufacturing in defence, telecom,

transportation and power. Over the next two decades, there will be a huge shift of

manufacturing capacity from the developed to the emerging economies. India needs to

capture a disproportionate share of this shift to create jobs for its very young population.

Dr. T. A. Shiware

Chief Editor

vi

From the Executive Editor’s Desk…

The Indian Economy is firmly set on a high growth plan for the next few years. The

proportion of working age persons in the total population is on the rise. If the working age

population can be productively employed, the ratio of earners to dependents will keep rising

for the next few years yielding a large ‘demographic dividend’ of higher growth rates,

rapidly rising per capita income and rising consumption. Another trend that is visible is that

the Indian workforce has slowly moved from low productivity agriculture to higher

productivity sectors like industry and services. This change in trend points to a potential rise

in productivity, saving and investment. If the growth rate rises to 6.7 % or more in the next

two decades, it will enable the productive employment of an additional 8,00,000 to one

million youth who will enter the workforce. However, realization of the long cycle of high

growth will depend upon some critical pre-conditions being fulfilled. One pre-condition is

the accumulation of physical capital not just in plants and equipment’s, but also in

infrastructure such as roads, railways, ports, airports, communication and power. There has

been a remarkable improvement in this field during the past decade. In the power sector,

which is the main bottleneck today, new capacity has been created, but the sector is hobbled

by a shortage of coal supply. Fortunately the PMO is now focused on this challenge and one

can hope to see some forward movement in the near future.

An important pre-condition and a much bigger challenge is education. Education is the key to

equipping the workforce with the necessary knowledge and skills required to migrate from

low to high productivity jobs. The quality of education is poor and the learning levels are

declining. Hence it is an added responsibility of the government to provide not only quality

vii

education by providing education to all, but also to make an attempt to control the drop-out

level in schools and colleges.

Another problem the country faces is the challenge of hunger. There is a high incidence of

malnutrition. About 38% of Indians are malnourished; hence there is an urgent need to make

provision for quick distribution of food at reasonable rates to the poor. Bold imaginative

reforms in the distribution of food, as well as in the delivery of education services and

infrastructure are the key pre-conditions that India must fulfill in order to realize its potential

long cycle of high inclusive growth.

Dr. (Ms.) Rajeshwary

Executive Editor

1

Perception Mapping On Purchase Behaviour of Smart Phone among

Working Women in the Corporate of Coimbatore City∗Dr. Angamuthu Balasubramaniam

Abstract

This exploratory study aims to study the brand possession of smart phone and factors

that determine brand positioning of smart phone among working women. Self-designed

questionnaire has been used to collect the primary data and the data were collected from

200 working women in various corporate offices like Cognizant Technology Solutions,

First Source Solutions Ltd, Ugam, Ford Business Services Centre, Vanenburg Software

(India) Private Limited, VWR, Nous Infosystems, C Bay systems etc. Purposive

sampling method is most suitable for sample selection of current research work. This

study reported that majority of the working women have Samsung (28%) brand of smart

phone, followed by Micromax (23.5%) and Sony (20%). Chi-square analysis reveals

that there is a significant relationship of brand possession of Smart phone among

various age groups of working women. Factoring of various parameters are done using

SPSS and it is found that the factors like value added features, pricing and quality,

brand image of smart phone determine brand possession of smart phone. Finally, this

study explains that the purchase behavior of smart phone through the different

perceptual maps.

Keywords: Mobile phone, Smart phone, Purchase behavior, Perception

1 Introduction

With rapid technological developments, mobile phone has evolved from a mere

communication device to smart phone with an ability to tap a plethora of information &

services. A smart phone, or smart phone, is a mobile phone with more advanced

computing capability and connectivity than basic feature phones. The first smart phones, the

IBM Simon and Nokia Communicator 9000 were released way back in 1994 and 1996 respectively, and

integrated the features of a mobile phone and a personal digital assistant (PDA) for managing calendars

and contacts. Both were much larger than regular phones. It wasn’t until 2000 that the first real smart

∗ Assistant Professor of Commerce, Kovai Kalaimagal College of Arts and Science, Coimbatore.

2

phone, the Ericsson R380, was released. It wasn’t any larger than a regular phone, and in the early 2000s

many others followed suit, with phones like the Palm and Blackberry achieving big success. In 2007,

Apple released the iPhone, which eschewed hardware buttons for full touch screen control and has been

the template for smart phones ever since. In the 21st Century most of the mobile makers are released

variety of smart phones. The Worldwide mobile phones sales, which includes both smart

phone and feature phone sales, increased to 1.81 billion in the year of 2013from 1.75

billion over the year of 2012. Among the mobile makers, Samsung continued to be the

biggest mobile phone company internationally by selling 444.44 million devices in

2013. This is followed by Nokia, Apple, LG etc. (Refer Table -1)

Table – 1: Worldwide Mobile Phone Sales to End Users by Vendors

Company 2013 (Units in 000’s) 2012 (Units in 000’s)

Samsung 444,444.2 384,631.2

Nokia 250,793.1 333,938.0

Apple 150,785.9 130,133.2

LG 69,024.5 58,015.9

ZTE 59,898.8 67,344.4

Huawei 53,295.1 47,288.3

TCL Communication 49,531.3 37,176.6

Lenovo 45,284.7 28,151.4

Sony 37,595.7 31,394.2

Yulong 32,601.4 18,557.5

Others 613,710.0 609,544.9

Source: Gartner

Value Added Services of Smart phone Technology

The services provided over a mobile phone today role of voice communications to a

range of value added services. The value added service (VAS) is provided either

directly by the telecom operators themselves or by a third party Value Added Service

Provider (VASP). VASP connects to the core equipment of telecom operators through

inter-working units using protocols like short message peer-to-peer protocol (SMPP),

connecting either directly to the short message service centre (SMSC) or to a messaging

gateway that allows the telecom operators to have control of the content. In view of the

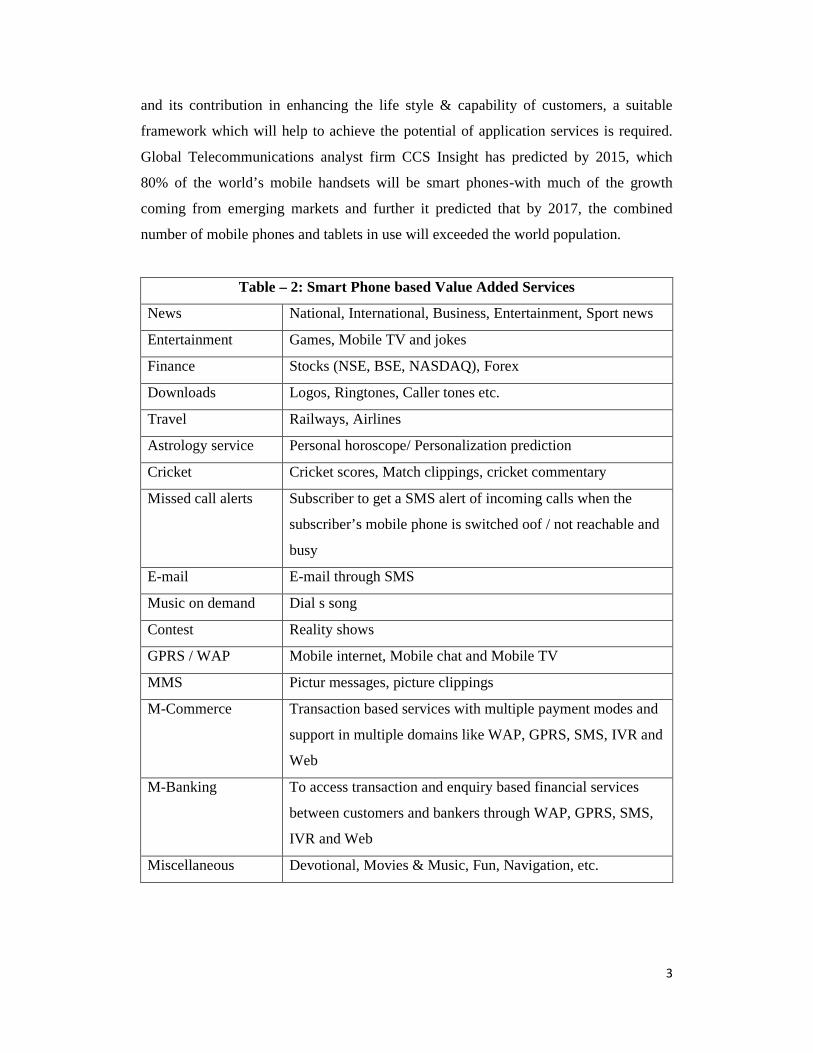

growing and likely unprecedented expansion of value added services (Refer Table – 2)

3

and its contribution in enhancing the life style & capability of customers, a suitable

framework which will help to achieve the potential of application services is required.

Global Telecommunications analyst firm CCS Insight has predicted by 2015, which

80% of the world’s mobile handsets will be smart phones-with much of the growth

coming from emerging markets and further it predicted that by 2017, the combined

number of mobile phones and tablets in use will exceeded the world population.

Table – 2: Smart Phone based Value Added Services

News National, International, Business, Entertainment, Sport news

Entertainment Games, Mobile TV and jokes

Finance Stocks (NSE, BSE, NASDAQ), Forex

Downloads Logos, Ringtones, Caller tones etc.

Travel Railways, Airlines

Astrology service Personal horoscope/ Personalization prediction

Cricket Cricket scores, Match clippings, cricket commentary

Missed call alerts Subscriber to get a SMS alert of incoming calls when the

subscriber’s mobile phone is switched oof / not reachable and

busy

E-mail E-mail through SMS

Music on demand Dial s song

Contest Reality shows

GPRS / WAP Mobile internet, Mobile chat and Mobile TV

MMS Pictur messages, picture clippings

M-Commerce Transaction based services with multiple payment modes and

support in multiple domains like WAP, GPRS, SMS, IVR and

Web

M-Banking To access transaction and enquiry based financial services

between customers and bankers through WAP, GPRS, SMS,

IVR and Web

Miscellaneous Devotional, Movies & Music, Fun, Navigation, etc.

4

Growth of Mobile Phone Services of India in the 21st Century

Here, the growth of mobile phone services measured through mobile subscription base.

The Year-on-Year trend growth rate of the subscriber base depicted a positive trend

over the periods from 2001-2002 to 2011-2012. The maximum growth of subscriber

base was 158.31 percent during the year 2002-2003 (Refer Table - 3). The above

discussion clearly indicates that the potential development and growth of mobile phone

service in India. The comparison of actual growth of mobile subscriber base declining

trend compared with expected growth from 2004-2005 to 2009-2010 (Refer Figure – 1).

The data predicts that the growth of mobile phone service in terms of subscriber base in

2014-2015 has crossed to 1000 million with the growth rate of 13.11 percent compared

to 2011-2012.

Table – 3:Trends in Mobile Services from 2001-2002 to 2011-2012

Year Subscribe (in Millions) Growth (%)

2001-2002 13 -

2002-2003 33.58 158.31

2003-2004 50 48.90

2004-2005 76 52.00

2005-2006 98.77 29.96

2006-2007 165.11 67.17

2007-2008 261.07 58.12

2008-2009 391.76 50.06

2009-2010 584.32 49.15

2010-2011 811.59 38.89

2011-2012 919.17 13.26

2014-2015* 1039.65 13.11

Source: Computed from secondary data

*forecast

5

Source: Secondary data

Growth of Mobile Phone Service in the Urban India

The urban mobile phone subscriber base since March 2007 is indicated in Figure 2. As

on 31st March 2012, the mobile services according to subscriber base in urban areas has

reached the 595.06 million mark as against 538.05 million as on 31st March 2011. The

urban subscriber base is steadily increasing with CAGR of 35.15 percent for six years

period from 2006-2007 to 2011-2012. Further, the data predict that mobile phone

subscriber in urban areas has reached to around 900 million at the end of 31st March

2015.

Source: Secondary data

6

2 Statement of the Problem

Smart phone became integral part of our life. The usage of smart phone depends on the

many vital points that make its necessity like applications, GPS functionality, organizer,

alarm & calendar, media playing, capturing precious moments of personal life on the

go, texting/messaging, the internet/web surfing, e-mail, operating system, life style,

social status and so on. The present era most of the peoples are using smart phone than

basic features phone and also the mobile makers are releasing variety of smart phones at

different prices in the competitive market. So, this study focuses on purchasing behavior

of smart phone among corporate workers because of those are having capable to buy

smart phone and live according to modern trend.

3. Objectives of the Study

1. To study the brand possession of Smart phone among working women and also study

the relationship of brand possession of smart phone among various age groups,

education, monthly income and marital status of the working women

2. To find out the factors that determine for brand positioning of smart phone among

working women

3. To draw out the perceptual map towards responsible factors on brand positioning

strategies of smart phone among working women

4. Hypotheses of the Study

1. Ho1: There is no significant relationship between age group, education, monthly

income, marital status of the working women and their brand possession of smart

phone.

2. Ho2: f1, f2, f3,………f4 determines that brand positioning of samrtphone among

working women.

5. Review of Literature

Babita et al. (2013) in their research attempt to analyze the purchase behavior of men

and women towards different branded apparels and to study the effect of promotional

activities on their purchasing. This study considers brand awareness includes

both brand recognition as well as brand recall. Brand recognition is the ability of

consumer to recognize prior knowledge of brand when they are asked questions about

7

that brand or when they are shown that specific brand. Chaitanya (2013) investigates

customers' choice for the mobile phones with a right blend of features and price. A

survey conducted among 214 Indian undergraduate student mobile phone users reveal

their criteria for selecting mobile phone with maximum features and an affordable price.

Feature-wise comparison is also made between mobile phones of most preferred

companies. Dhevika et al. (2013) studied brand switching among cellular network

service users and this study found that users’ satisfaction is the main influencing factors

for brand switching. Dapeno et al. (2012) their study explores the perceived importance

of various aspects of service quality and customer switching behavior in China's mobile

phone service sector. The study identifies the following seven critical factors, listed in

descending order of influence, that cause customers to switch mobile phone service

providers: core service failure, high price, ethical problems, competition, inconvenience,

service encounter failure, and influence from family/friends/group. Duhan et al. (2012)

in their study investigate to trace about the brand awareness and also know the effects

of brand name on purchase decision regarding the durables like television, refrigerator

and washing machine in the rural areas of Haryana. The results show

that brand awareness is increasing day-by-day among rural population due to effect of

information technology. Further, the survey has found that there were many issues faced

by rural people when they decide about brand of a particular product to use. Syed and

Ravi (2012) examines the consumer perception and their impact on purchase intentions

towards branded men` garments. The result of this research is socio-cultural and

personality related factors induce the purchase intention among the consumers. Arpita et

al. (2011) their research paper focuses on identifying factors responsible for brand-

awareness in the high- and low-involvement category products. The findings suggest

that brand functions play a significant role in consumers' purchase behaviour in high-

involvement products and advertising plays a significant role in low-involvement

product purchase decision. Krishna Kumar (2011) reported that occupational status has

no significant association over the time taken to decide on purchase, mode of purchase

and item possed. On the other hand, occupational status has significant influence over

the media creating awareness towards electronic goods. Matti (2011) investigate the

mobile phone feature preferences among male respondents in Finland. The results

indicate that battery/talk time is the most important feature for the respondents. The

respondents perceive there to be six logical factors among the feature preferences as

8

follows: business functionality, support functions, aesthetics + design, parts + processes,

solidity, and tones + games. Bong Gyou et al. (2010) analyze the influential factors on

continuous use intention for 3G mobile video phone services. The results showed that

attitude, subjective norm, and video phone function exert a significant influence on

continuous use intention for video phone services and video phone function and video

phone call quality exert influence on user attitude. Lalit and Manish (2009) reported that

the major factors influencing the choice of service provider were network coverage,

price, value-for-money and billing integrity, recommendations from family and friends,

customer service and company image. Further, network problem was observed to be the

most important reason for switching over to other mobile phone service provider.

Mody-Kamdar Rutu and Srivastava Mala (2009) in their study attempts to understand

how consistency of brand image across consumers is affected by the consumers’

involvement with the product category and familiarity with the brand. Vijayakumar

(2006) reported that the satisfaction derived by the subscribers of Airtel Network has

been influenced by the clarity of signals, availability of plan options, low call charges

and activation formalities. Revathy et al. (2005) found that the factors like lower service

charges offered by Department of Telecommunications (DOT) than other private

players, convenience of contact, accessibility, improvement of own business/profession,

prestige and status symbol as the influencing factors for the possession of cell phone

connections.

6. Research Methodology

The study is an exploratory in nature and based on survey method. The self-designed

questionnaire has been used to collect primary data. The data were collected from 200

women respondents who are working in various corporate offices of Coimbatore City,

Tamil Nadu State. The sample respondents are selected in various corporate offices that

are functioning in KGISL Campus & KCT Techpark (Saravanmpatty), Rathinam

Techzone (Eachanari) and TIDEL Park (Aerodrome). The secondary data has been used

to discuss the theoretical part of this study and the secondary data have been collected

from official reports of Telecom Regulatory Authority of India (TRAI), books, Journals

and various websites. Purposive sampling method has been adopted. The primary data

collected from respondents during the months of February, March and April’ 2014. The

statistical tools such as % analysis, Chi-square test(χ2), Kaiser-Meyer-Olkin (KMO) test,

9

Bartlett’s test of Sphercity and factor analysis were applied which are considered

appropriate to the current research.

7. Analysis and Interpretations

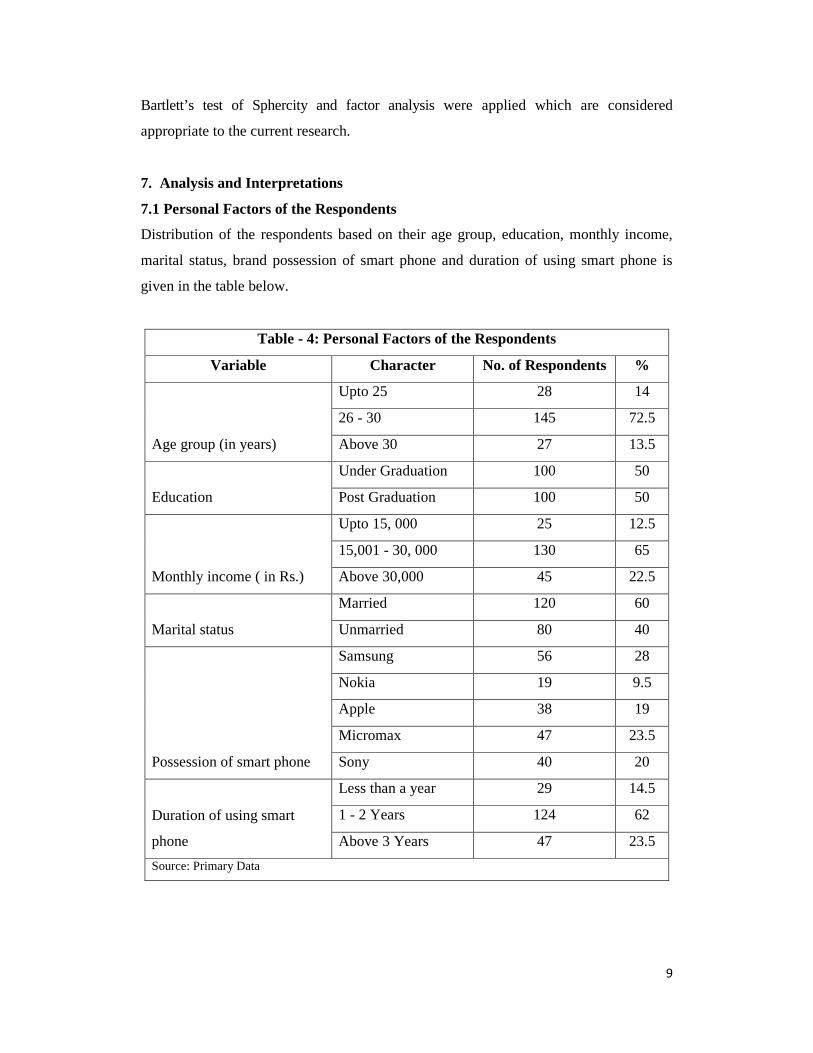

7.1 Personal Factors of the Respondents

Distribution of the respondents based on their age group, education, monthly income,

marital status, brand possession of smart phone and duration of using smart phone is

given in the table below.

Table - 4: Personal Factors of the Respondents

Variable Character No. of Respondents %

Age group (in years)

Upto 25 28 14

26 - 30 145 72.5

Above 30 27 13.5

Education

Under Graduation 100 50

Post Graduation 100 50

Monthly income ( in Rs.)

Upto 15, 000 25 12.5

15,001 - 30, 000 130 65

Above 30,000 45 22.5

Marital status

Married 120 60

Unmarried 80 40

Possession of smart phone

Samsung 56 28

Nokia 19 9.5

Apple 38 19

Micromax 47 23.5

Sony 40 20

Duration of using smart

phone

Less than a year 29 14.5

1 - 2 Years 124 62

Above 3 Years 47 23.5

Source: Primary Data

10

It could be collected from the table – 4 that the majority (72.5%) of the respondents

belongs to the age group of 26-30 years, 14% of the respondents belong to the age

group of upto 25 years and the remaining 13.5% of the respondents belongs to the age

group of Above 30 years. The sample includes half of the respondents have their

educational qualification is Post Graduation and the remaining half of them is Under

Graduation. This is followed by 65% of the respondents belongs to their monthly

income of Rs. 15, 001 – Rs.30,000 category compared upto Rs. 15, 000 (12.5%) and

High income (Above Rs.30,000) category. Nearly 6/10th of the respondents are married

amd the remaining 4/10th of them unmarried. Majority (28%) of the respondents have

Samsung brand of smart phone, followed by Micromax (23.5%), Sony (20%), Apple

(19%) and Nokia (9.5%). Little more than 6/10th of the respondents have using preferred

brand of smart phone for 1 to 2 years.

7.2 Relationship of personal profile of the Respondents and Brand Possession of

Samrt Phone

Here, χ2 analysis were used to test the relationship between independent and dependent

variable. The χ2 statistic is to carry out through the difference between the observed and

the expected frequencies in the cells of the contingency table using proper formula. The

framed hypotheses are:

Ho: There is no significant relationship between age group, education, monthly income,

marital status of the respondents and their brand possession of smart phone.

Ho1: There is no significant relationship between age group, education, monthly

income, marital status of the respondents and their brand possession of smart phone.

Table - 5: Relationship between Personal Factors and Brand Possession of

Smart phone

Variables

d

f Result TV

Age group & Brand possession

of smart phone

16.6

54* 8

Reject Ho &

Accept Ho1

15.51 @ 5% level &

20.09 @ 1% level

Education & Brand possession

of smart phone

4.18

8 4

Accept Ho &

Reject Ho1

9.49 @ 5% level &

13.23 @ 1% level

Monthly income & Brand 6.72 8 Accept Ho & 15.51 @ 5% level &

11

possession of smart phone 5 Reject Ho1 20.09 @ 1% level

Marital status & Brand

possession of smart phone 6.9 4

Accept Ho &

Reject Ho1

9.49 @ 5% level &

13.23 @ 1% level

Source: Primary data ** Sig. @ 1% and * Sig. @ 5% level

Age Group and Brand Possession of Smart Phone: It is obvious from the table - 5

that calculated χ2 value (χ2 = ∑ (Oi-Ej)2 / Ej) is greater than tabulated value of 15.51 and

lesser than tabulated value of 20.09 @ 5% and 1% level respectively. Hence, Accept

Ho1 & Reject Ho @ 5% level but Accept Ho & Reject Ho1 @ 1% level.

Education & Brand possession of Smart Phone: It could be collected from the table –

5 that the calculated χ2 value (χ2 = ∑ (Oi-Ej)2 / Ej) between education and brand

possession of smart phone is lesser than tabulated value of 9.49 and 13.3 @ 5% and 1%

level respectively. Hence, Accept Ho & Reject Ho1. For that reason, it says that there is

no significant relationship between education of the respondents and their brand

possession of smart phone.

Monthly Income & Brand possession of Smart Phone: It is obvious from the table –

5 that the calculated χ2 value (χ2 = ∑ (Oi-Ej)2 / Ej) between monthly income of the

respondents and their brand possession is lesser than tabulated value of 15.51 and 20.09

@ 5% and 1% level of significant respectively. So, Accept Ho & Reject Ho1. Finally, it

is reported that there is no significant relationship between monthly income of the

respondents and their brand possession of smart phone.

Marital Status & Brand possession of Smart Phone: It could be collected from the

table – 5 that the calculated χ2 value (χ2 = ∑ (Oi-Ej)2 / Ej) between marital status of the

respondents and their brand possession of smart phone is lesser than tabulated value of

9.49 and 13.23 @ 5% and 1% level respectively. Hence, Accept Ho & Reject Ho1. For

that reason, it says that there is no significant relationship between marital status of the

respondents and their brand possession of smart phone.

12

7.3 Responsible Factors that determine for brand positioning of Smart Phone

Initially, the KMO measures of sampling adequacy were used and it is an index that

compares the sizes of the observed correlation coefficients to the sizes of the partial

correlation Coefficients. It is derived as follows

=(∑∑r2ij)/( ∑∑r2ij)+( ∑∑a2

ij)

Further, Bartlett’s test of Sphericity tests studied whether the correlation matrix is an

identity matrix, which would indicate that the factor model is inappropriate or

appropriate. Here, chi-square also considered and it is calculated as follows

= [(n-1)-1/6(2p+1+2/p)] [In|S|+pIn(1/p) ∑Ij]

p=number of variables

k=number of components

Ij =jth eigen value of Sdf=(p-a) (p-2)/2

The responses against all the 14 variables are used to test the above tests. The

calculated value of KMO Measure of Sampling Adequacy comes out >0.6 and Bartlett’s

Test of Sphericity (Approx. χ2 2032.619** with df 91) significant @ 1% level. Further,

suggestion given by them this study has been used to further interpretation. Factor

analysis is a generic name given to a class of multivariate statistical methods whose

primary purpose is data reduction and summarization. Factor analysis identifies

common dimensions of factors from the observed variables that link together the

seemingly unrelated variables and provides insight in the underlying structure of the

data. The common intention of factor analytic technique is to find way of condensing

(summarizing) the information contained in a number of original variables into a smaller

group of new composite factors with a minimum loss of information. In this current

study, the Principal Component Analysis (PCA) was used. The PCA has been described

as a mathematical procedure that uses an orthogonal transformation to convert a set of

observations of possibly correlated variables into a set of uncorrelated variables called

principal components. PCA is usually done when we have a number of observed

variables that are believed to influence a given dependent variable, but then these

variables are so many that they are correlated. In this situation we want a smaller

number of important variables that will account for most of the variance in the observed

variables. Further, varimax rotations have been used in order to simplify the factor

structure by maximizing the variance of a column of pattern matrix because it is one of

13

the most popular methods used in several social sciences research papers. In addition

Eigen value is also used; it helps to find out the amount of variance in overall data. Finally,

determination of the factors based on the factor score are estimated for each factor with a

new name given about grouped variables. Below is the general form for the formula to

compute scores on the first component extracted (created) in a PCA

Fi = Wi1X1 + Wi2 X2 + ……………….. Wik Xk

Where,

Fi = Estimate of the ith factor

W1 = Factor (weight) score co-efficient

k = Number of variables

Factor analysis is performed in order to group the variables on priority basis based on

the strength of inter-correlation between these opinions, called ‘Factors’ and clustering

these variables in to the factors extracted and the results are presented in the following

tables. Table – 6 gives the rotated factor loadings, communalities, eigen values and the

percentage of variance explained by the factors. There were three factors each having

eigen value exceeding two for factors that determine brand positioning of s smart phone.

The Eigen values for three factors were 3.944, 2.894 and 2.538 respectively. Further,

factors have been extracted and these factors put together explain the total variance of

these factors to the extent of 66.96%. In order to reduce the number of factors and

enhance the interpretability, the factors are rotated. The rotation increases the quality of

interpretation of the factors. There are several methods of the initial factor matrix to

attain simple structure of the data. The varimax rotation is one such method to obtain

better result for interpretation is employed and the results are given in Table – 7.

Table – 6: Responsible Factors on Brand Positioning of Smart phone

Variables I II III Communalities

V1 -0.086 0.642 0.617 0.800

V2 0.314 0.754 -0.067 0.671

V3 0.042 0.907 0.182 0.857

V4 0.139 0.604 0.570 0.709

V5 0.676 0.301 0.287 0.630

V6 0.691 0.232 0.171 0.560

14

V7 0.778 0.111 0.148 0.639

V8 0.429 0.151 0.565 0.525

V9 0.727 0.300 0.160 0.644

V10 0.166 0.121 0.679 0.503

V11 0.615 -0.037 0.523 0.653

V12 0.350 -0.009 0.727 0.652

V13 0.523 0.663 0.046 0.715

V14 0.874 -0.042 0.230 0.819

Eigen Value 3.944 2.894 2.538 9.375

% of variance 28.171 20.669 18.126 66.966

Cum. % of Variance 28.171 48.840 66.966

Extraction Method: Principal Component Analysis.

Rotation Method: Varimax with Kaiser Normalization.

Source: Primary data

15

Table - 7: Clustering of Parameters into Factors that Determine Brand

Positioning of Smart phone

Factor Variables

Rotated Factor

Loadings

I - 28.171

Availability of value added services (V14) 0.874

E-mail accessibility (V7) 0.778

Wi-Fi connectivity (V9) 0.727

Large Random Access Memory (RAM) (V6) 0.691

High-end camera and high-quality audio, display

and digital media (V5) 0.676

Fit between smart phone and brand name (V11) 0.615

II - 20.669

Quality of the phone (V3) 0.907

Warranty & durability (V2) 0.754

Sales channel (V13) 0.663

Pricing (V1) 0.642

After sales service (V4) 0.604

III - 18.126

Advertising & Effective promotion (V12) 0.727

Global positioning system (V10) 0.679

Brand image & values (V8) 0.565

Source: Primary data

Table-7 explains that the 6 variables V14, V7, V9, V6, V5 and V11 were grouped

together as factor I and accounts for 28.171% of the total variance. The 5 variables V3,

V2, V13, V1 and V4 constituted the factor II and accounts for 20.669% of the total

variance. The 3 variables V12, V10 and V8 constituted the factor III and accounts for

18.126% of the total variance. Finally, factor analysis given factors like value added

features of smart phone, quality and pricing of smart phone, brand image that determine

brand positioning of smart phone.

7.4 Perceptual map towards Responsible Factors on Brand Positioning Strategies

of Smart Phone

The average factor scores for all the variables regarding responsible factors on brand

positioning strategies of smart phone which is used for building perceptual maps. Figure

16

– 3 gives the perceptual map for value added features of smart phone (Factor –I) and

pricing, quality of smart phone (Factor – II). The coordinates of all the points that are

displayed on the perceptual map for the variables represents that factor scores with

respect to the two major axes of factor I & II. From the figure – 3 it is observed that

three clusters are existing, cluster one comprises four variables which are included in

the factor of quality, pricing of smart phone. The second cluster has three variables and

each variables of which belongs to value added features of smart phone, pricing and

quality, brand image. The third cluster comprises seven variables five of which are

value added services of smart phone and two variables belongs to the factor of brand

image of smart phone.

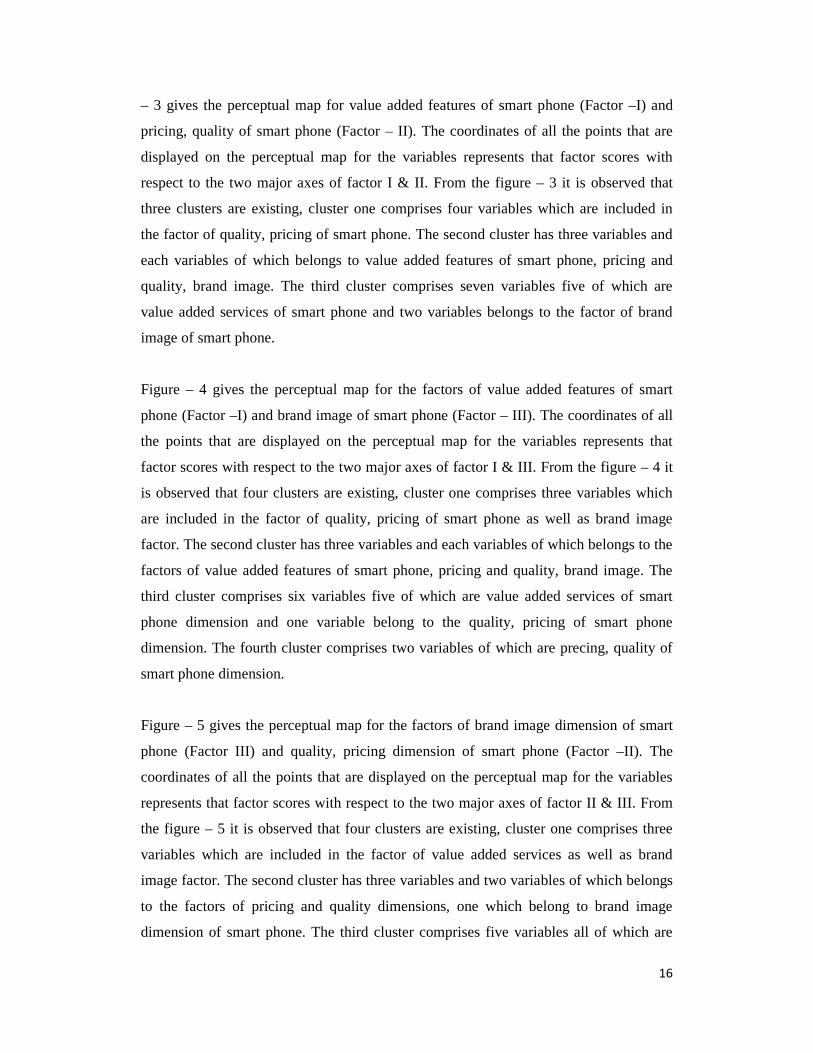

Figure – 4 gives the perceptual map for the factors of value added features of smart

phone (Factor –I) and brand image of smart phone (Factor – III). The coordinates of all

the points that are displayed on the perceptual map for the variables represents that

factor scores with respect to the two major axes of factor I & III. From the figure – 4 it

is observed that four clusters are existing, cluster one comprises three variables which

are included in the factor of quality, pricing of smart phone as well as brand image

factor. The second cluster has three variables and each variables of which belongs to the

factors of value added features of smart phone, pricing and quality, brand image. The

third cluster comprises six variables five of which are value added services of smart

phone dimension and one variable belong to the quality, pricing of smart phone

dimension. The fourth cluster comprises two variables of which are precing, quality of

smart phone dimension.

Figure – 5 gives the perceptual map for the factors of brand image dimension of smart

phone (Factor III) and quality, pricing dimension of smart phone (Factor –II). The

coordinates of all the points that are displayed on the perceptual map for the variables

represents that factor scores with respect to the two major axes of factor II & III. From

the figure – 5 it is observed that four clusters are existing, cluster one comprises three

variables which are included in the factor of value added services as well as brand

image factor. The second cluster has three variables and two variables of which belongs

to the factors of pricing and quality dimensions, one which belong to brand image

dimension of smart phone. The third cluster comprises five variables all of which are

17

the dimensions related to value added services of smart phone. The fourth cluster

comprises three variables and all of which are dimensions of pricing, quality of smart

phone.

18

19

8. Conclusion

Yesterday‘s luxuries are today‘s necessities. Now-a-days, all classes of people are using

cell phones but rich categories, youngsters, new technology adopters are using smart

phones. The completed research shows that most of the corporate womens are having

Samsung, Micromax and Sony brand of smart phones. Brand possession of smart phone

among women workers is not associated with their education, monthly income and

marital status whereas age group of the women workers associated with their brand

possession. There are three different factors namely value added features of smart phone,

quality and pricing of smart phone, brand image determine that brand positioning

strategies of smart phone among corporate women.

References

1. Arpita, K., & Sapna, R., (2011). “Antecedents to purchase decision of high and low

involvement products amongst Indian Youth”, International Journal of Business

Competition and Growth, Vol. 1, No.3 pp. 262 – 275.

2. Babita., Gaur Arti., Arora Nancy., and Bhardwaj Deepak., (2013). “Brand awareness

of readymade garments: A comparative study of males and females”, International

Journal of Managment, IT and Engineering, Vol.3, No.2, pp. 141-154.

3. Bong Gyou, L., Younghee, L., and Sang, C., (2010). “The continuous use behaviour

of 3G mobile video phone services”, International Journal of Mobile Communications,

Vol. 8, No.4 pp. 371 – 391.

4. Chaitanya, V., (2013). “What do Indian customers want in a cell phone? Strategies for

network providers and handset manufacturers”, International Journal of Indian Culture

and Business Management, Vol. 7, No.3 pp. 384 – 398.

5. Dapeno, L., Zhenzhong, M., and Liyun, Q., (2013). “Service quality and customer

switching behavior in China's mobile phone service sector”, Journal of Business

Research, Vol. 66, No. 8, pp. 1161-1167.

6. Dhevika, V.P.T., Latasri, O.T.V., & Maruthamuthu, S., (2013): “A study

on brand switching among cellular network service users in Tiruchirappalli”,

International Journals of Marketing and Technology, Vol.3, No.4, pp. 160-176.

20

7. Duhan, A., Pannu, R.S., Goyal, R., & Jain, P., (2012). “A study of brand awareness

regarding consumer durables in rural Haryana”, Indian Journal of Economics and

Development, Vol.8, No.4, pp.83-89.

8. Krishna Kumar, R., (2011). “Consumer Behaviour Towards Electronic Goods With

Reference To Occupational Factors - A Study In Cuddalore Town”, International

Referred Research Journal, Vol-2, No. 24, pp. 60-63.

9. Lalit, M., K., and Manish, J., (2009). “Factors Influencing the Selection of a Mobile

Phone Service Provider: An Empirical Study among Rural Consumers”, Asia-Pacific

Journal of Management Research and Innovation, Vol. 5, No. 4, pp. 128-136.

10. Matti, H., (2011). “Mobile phone feature preferences, customer satisfaction and

repurchase intent among male users”, Australasian Marketing Journal, Vol.19, No. 4, pp.

238-246.

11. Mody-Kamdar Rutu., and Srivastava Mala., (2009). “Brand Image Formation as a

function of involvement and familiarity”, The Journal of Indian Management & Strategy

8M, Vol.14, No.4, pp. 4-10.

12. Syed, A.S., & Ravi, A., (2012). “A study on consumer perception towards branded

men’s garments in hosur, Krishnagiri district, Tamilnadu”, South Asian Journal of

Marketing & Management Research, Vol.2, No.9, pp. 198-205.

13. Shalini Singh (2013) “Mobile Subscriptions approaches total global population in

2013”, The Hindu, 8-7-2013, P.No. 11.

14. Vijay Kumar, R., and Ruthra Priya, P., (2006): “Satisfaction derived by the Airtel

subscribers in Coimbatore”, Indian Journal of Marketing, Vol. XXXVI, No.1, P.No. 3.

15. Revathi, S., and Padmavathy, S., (2005): P”reference in cellular service providers in

the post liberalization era”, Indian Journal of marketing, Vol. XXXV, No.2, pp. 6-10, 20

.

http://www.phonearena.com/

http://listcrux.com/

http://www.techulator.com/

https://www.telstra.com.

http://www.ibtimes.com/

http://www.medianama.com/ and other websites

21

Micro Finance- A Way to Alleviate Poverty

∗Shweta Sawhney

Abstract

The article traces the fruition of the Microfinance insurrection in India as a potent tool for

poverty mitigation and women empowerment. Where institutional finance failed

Microfinance delivered. In a country like India, where almost 70 per cent of the

population is in the rural areas, with little or no access to main stream financing options,

microfinance has a huge role to play and a huge population to uplift. The paper discusses

the present scenario of microfinance Institutions (MFIs) in India. In spite of the

impressive figures, the supply side of microfinance in India is still presently abhorrently

inadequate to fill the fissure between demand and supply but it holds the promise to act as

a great opportunity for the financial sector and the economy as a whole.

Key Words: Financial services, savings, micro enterprises, integrated services

Introduction

There is growing interest in microfinance as one of the avenues to enable low income

population to access financial services. Micro finance is the provision of thrift, credit and

other financial services and products of very small amounts to the poor for enabling them

to raise their income levels and improve their living standards. It has been recognized that

micro finance helps the poor people meet their needs for small credit and other financial

services. The informal and flexible services offered to low-income borrowers for meeting

their modest consumption and livelihood needs have not only made micro finance

movement grow at a rapid pace across the world, but in turn has also impacted the lives

of millions of poor positively. Micro finance is the provision of financial services to low

∗ Assistant Professor, Mangalmay Institute of Management & Technology, Plot No. 8&9, Knowledge Park-

2, Greater Noida.

22

income clients including consumers and self employed who traditionally lack access to

banking and related services.

Microfinance is gathering momentum to become a significant force in India. The self

help group (SHG) model with bank lending to groups of (often) poor women without

collateral has become an accepted part of rural finance. “Microfinance” is often defined

as financial services for poor and low-income clients. In practice, the term is often used

more narrowly to refer to loans and other services from providers that identify themselves

as “microfinance institutions” (MFIs). ‘Microfinance refers to small scale financial

services for both credits and deposits- that are provided to people who farm or fish or

herd; operate small or micro enterprise where goods are produced, recycled, repaired, or

traded; provide services; work for wages or commissions; gain income from renting out

small amounts of land, vehicles, draft animals, or machinery and tools; and to other

individuals and local groups in developing countries in both rural and urban areas’-

Marguerite S. Robinson. Microfinance refers to a movement that envisages a world in

which low-income households have permanent access to a range of high quality financial

services to finance their income-producing activities, build assets, stabilize consumption,

and protect against risks. These services are not limited to credit, but include savings,

insurance, and money transfers.

Microfinance in India

In the case of India, the banking sector witnessed large scale branch extension after the

nationalization of banks in 1969, which facilitated a shift in focus of banking from class

banking to mass banking. It was, however, realized that, despite the wide spread of

formal financial institutions, these institutions were not able to gratify completely to the

small and frequent credit needs of most of the poor. This led to a search for alternative

policies and reforms for reaching out to the poor to satisfy their credit needs.

The non-availability of credit and banking facilities to the poor and deprived segments of

the society has always been a major concern in India. Accordingly, both the Government

and the Reserve Bank realized that direct efforts were required to address the credit needs

of poor. In response to this requirement, the micro finance movement started in India

23

with the introduction of SHG-bank linkage programme (SBLP) in the early 1990s. At

present, there are two models of micro finance delivery in India: the SBLP model and the

MFI model. The SBLP model has emerged as the dominant model in terms of number of

borrowers and loans outstanding.

Microfinance Clients

Microfinance clients are poor and low-income people that do not have access to other

formal financial institutions. Microfinance clients are usually self-employed, household-

based entrepreneurs. Their assorted “micro enterprises” include small retail shops, street

vending, artesian manufacture, and service provision. In rural areas, micro entrepreneurs

often have small income-generating activities such as food processing and trade; some

but far from all are farmers.

Data on the poverty status of clients is limited, but leans to suggest that most of the

microfinance clients fall near the poverty line, both above and below. Households in the

poorest 10% of the population, including the impoverished, are not traditional micro

credit clients because they lack stable cash flows to repay loans. Most clients below the

poverty line are in the upper half of the poor. Women often comprise the majority of

clients.

Over the past decade, a few MFIs have started developing a range of products to meet the

needs of other clients, including pensioners and salaried workers. Although little is

known about the universe of potential clients, the number of households without effective

access to financial services is gargantuan.

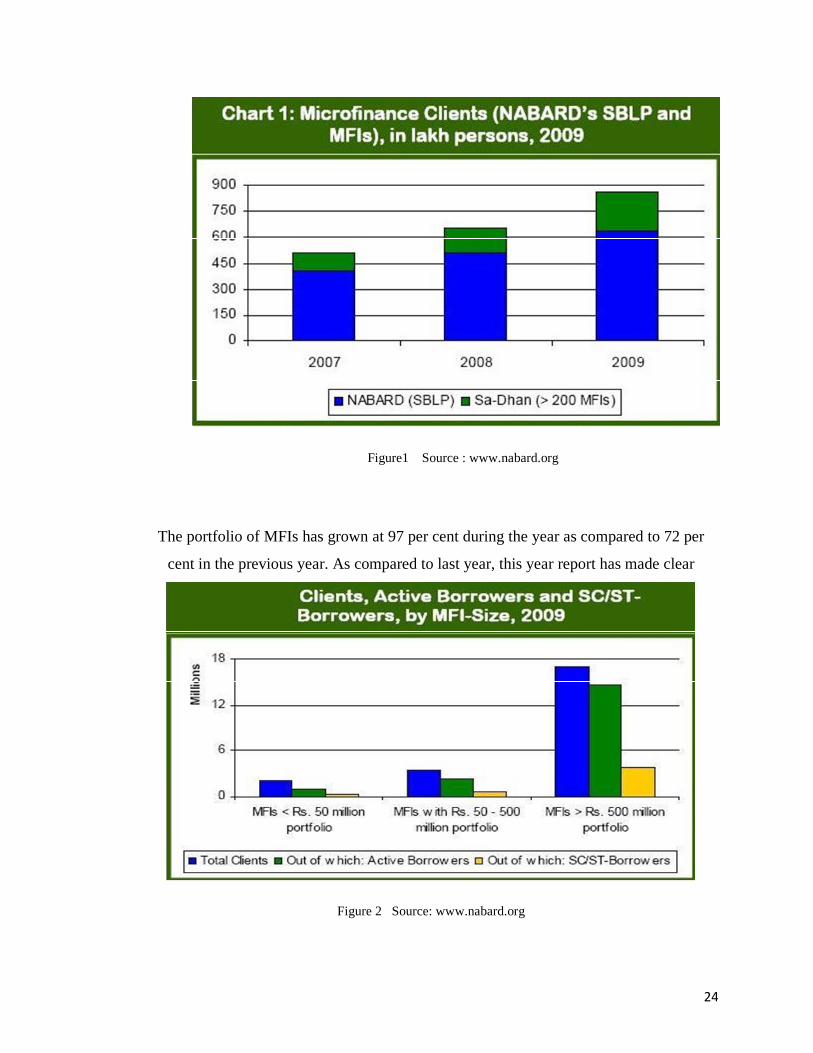

• Clients and Portfolio

This data reveals that Indian microfinance has reached at 86.2 million clients and the

portfolio outstanding of Rs. 351 billion including MFI channel actual data and SBLP

estimated data for March 2009

24

Figure1 Source : www.nabard.org

The portfolio of MFIs has grown at 97 per cent during the year as compared to 72 per

cent in the previous year. As compared to last year, this year report has made clear

Figure 2 Source: www.nabard.org

25

distinction between client outreach and active borrowers. Out of 22.6 million clients of

MFIs, 17.9 million (79 percent) are active borrowers. This year’s Quick Data is

contributed by 233 MFIs as against 223 MFIs in Quick Data 2008.

Microfinance data can be used by both private sector and public sector. We can collect

data related to microfinance through provider surveys ( surveys of financial institutions

and their regulators) and through household surveys.

Under the microfinance, loans are extended to the ‘Self Help Groups (SHG)’ who pools a

part of their income into a common fund from which they can borrow. The members of

the group decide on the minimum amount of deposit which ranges from Rs 20 to Rs 100

per month depending upon the size of the group. The group funds are deposited with a

Micro Finance Institution (MFI) against which they usually lend (The deposits are

usually placed with a bank by the MFI) at a credit deposit ratio of 4:1 but the ratio

improves with account performance record i.e. prompt repayment of loans.

Microfinance Delivery Vehicles

Most MFIs started as not-for-profit organizations like NGOs (non-governmental

organizations), credit unions and other financial cooperatives, and state-owned

development and postal savings banks. An increasing number of MFIs are now organized

as for-profit entities, often because it is a requirement to obtaining a license from banking

authorities to offer savings services. For-profit MFIs may be organized as non-bank

financial institutions (NBFIs), commercial banks that specialize in microfinance, or

microfinance departments of full-service banks.

Most MFIs are societies and trusts. Among the large MFIs, most are NBFCs, but not-for-

profit organizations are also counted in this category.

26

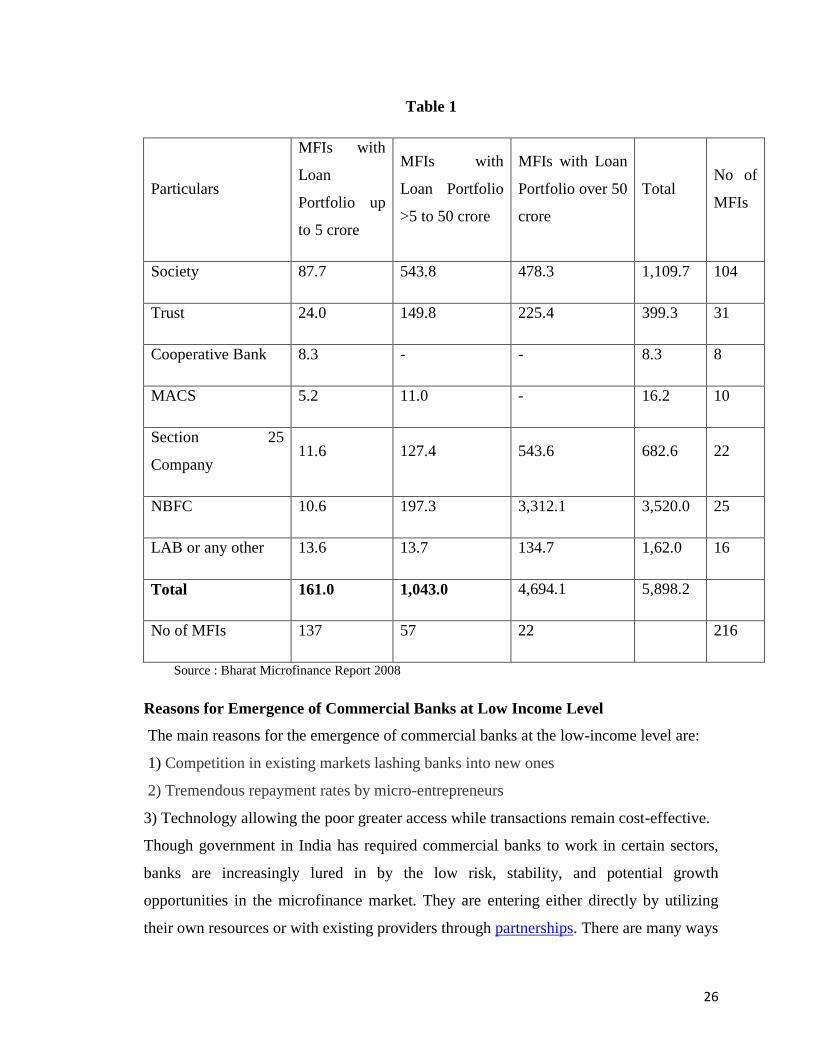

Table 1

Particulars

MFIs with

Loan

Portfolio up

to 5 crore

MFIs with

Loan Portfolio

>5 to 50 crore

MFIs with Loan

Portfolio over 50

crore

TotalNo of

MFIs

Society 87.7 543.8 478.3 1,109.7 104

Trust 24.0 149.8 225.4 399.3 31

Cooperative Bank 8.3 - - 8.3 8

MACS 5.2 11.0 - 16.2 10

Section 25

Company11.6 127.4 543.6 682.6 22

NBFC 10.6 197.3 3,312.1 3,520.0 25

LAB or any other 13.6 13.7 134.7 1,62.0 16

Total 161.0 1,043.0 4,694.1 5,898.2

No of MFIs 137 57 22 216

Source : Bharat Microfinance Report 2008

Reasons for Emergence of Commercial Banks at Low Income Level

The main reasons for the emergence of commercial banks at the low-income level are:

1) Competition in existing markets lashing banks into new ones

2) Tremendous repayment rates by micro-entrepreneurs

3) Technology allowing the poor greater access while transactions remain cost-effective.

Though government in India has required commercial banks to work in certain sectors,

banks are increasingly lured in by the low risk, stability, and potential growth

opportunities in the microfinance market. They are entering either directly by utilizing

their own resources or with existing providers through partnerships. There are many ways

27

how women are empowered through microfinance such as it provides ability to save and

access loans, provides opportunity to undertake an economic activity, provides awareness

on local issues, banking transactions, MFL procedures, etc., provides skills for income

generation, helps in performing role in community development activities, etc.

The Impacts of Microfinance

Microfinance loans are used for starting new business as well as for existing businesses

or for non producing purposes such as for purchasing household items like refrigerator;

or for marriage of children etc. As per data available 30% of loans are used for starting a

new business; 22% were supposed to be used to buy stock for existing business, 30% to

repay an existing loan, 15% to buy a durable for household use, and 15% to smooth

household consumption. (Respondents could list more than one purpose). In other words,

while some households plan to use their loans to start a business and others use a loan to

expand a business they already have, many others use the loan for a non-business

purpose, such as repaying another loan, buying a television or meeting day-to-day

household expenses.

A feature of starting a business is that there are some costs that must be paid before any

revenue is earned. While a small business like those operated by households in our

sample may not require a lot of sturdy assets (machinery, property, etc.), they normally

need working capital, such as stock for business, fabric to make dresses, etc. And as there

is always a .fixed minimum time commitment in any of these businesses, it makes no

sense to operate them below a certain scale and hence it is hard to imagine operating even

these businesses without a minimum assurance of working capital. Many businesses also

have some assets, such as a sewing machine, stove, etc. The need to purchase assets and

working capital constitutes a .fixed cost of starting a business, and one impact of

microfinance may be that it enables households who would not or could not pay this

fixed cost without borrowing, to become entrepreneurs.

Current Trends in Microfinance

MFIs and commercial banks have enabled each to leverage their competitive advantages.

While MFIs are more knowledgeable at the community level for instance, banks have the

28

advantage in greater access to capital and existing infrastructure. MFIs have scaled up to

“access higher levels of credit, augment their portfolios, and strengthen management and

efficiency levels,” while commercial banks have purposely scaled down to profit from

this emerging industry. Both types of institutions “scale-up and scale-down” by

redesigning their financial products to suite the clientele they are targeting.

Integration between these sectors leads to another current trend in microfinance—the

increase in deposits as a source of funding. Conventionally nationalized banks in India

have a wider reach through their branch network to provide microfinance to rural folks.

But the new generation banks are at a disadvantage. Hence new banks relied profoundly

on microfinance institutions by way of providing indirect finance.

Microfinance remains forte of nationalized banks. Banks with lead bank responsibilities

have excelled in microfinance in the respective lead districts. Due to certain irregularities

observed by Reserve Bank of India, the banks may be finding it difficult to lend directly

to MFIs. Therefore better route for MFIs is to form NBFCs whereby they will be able to

raise finance and provide micro finance. Due to limited knowledge and a lack of trust

beyond the community, the local poor may therefore be more inclined to make deposits

into local savings accounts. One of the main links between these trends is technological

advancement. Efficient technology has allowed smaller and simpler banking transactions

to become more cost effective, motivating commercial banks to scale down and reach a

greater number of people Local currency deposits have the potential to increase further

from an expansion of service machines and phone banking systems. Such progress in

physical banking and financial services infrastructure poises microfinance to emerge as

an asset class. As commercial banks have realized that poor people’s finance can be

profitable, an increasing number have gone down market to tap lower income clientele.

The World Bank’s microfinance unit, the Consultative Group to Assist the Poor,

estimates that there are currently around 225 commercial banks “engaged in

microfinance”— a figure that is increasing.

29

Government Initiatives

In 1993, the Ministry of Human Resource Development, Government of India set up the

Rashtriya Mahila Kosh (RMK) with initial funding of Rs.310 million to act as a provider

of wholesale funds for the sector and to develop the sector through capacity building and

advocacy. In 1999, the SIDBI Foundation for micro credit was launched to provide both

financial and non financial support to MFIs. In 2001, the microfinance development fund

of Rs.1 billion was set up under NABARD to fund various development activities

relating to microfinance. It was later in 2005-06, re-designated as Regulating India’s

Microfinance Sector: A Suggested Framework of the Microfinance Development and

Equity Fund with an increased corpus of Rs.2 billion. In 2005, NBFCs engaged in

microfinance were permitted to obtain foreign equity investment subject to the

permission of the Foreign Investment Promotion Board. The minimum amounts were

$0.5 million when investment was less than 51% of the total equity, $5 million when it

was less between 51% and 75% of total equity and $7.5 million when investment was

greater than 75% of total equity. Government can contribute most effectively by:

• Setting sound macroeconomic policy that provides stability and low inflation

• Avoiding interest rate ceilings - when governments set interest rate limits, political

factors usually result in limits that are too low to permit sustainable delivery of credit that

involves high administrative costs—such as tiny loans for poor people. Such ceilings

often have the announced intention of protecting the poor, but are more likely to strangle

off the supply of credit

• Adjusting bank regulation to facilitate deposit taking by solid MFIs, once the country

has experience with sustainable microfinance delivery,

Creating government wholesale funds to support retail MFIs if funds can be lagged from

politics, and they can hire and protect strong technical management and avoid

disbursement pressure that force fund to support unpromising MFIs.

Challenges Ahead

A World Bank study assessing access to financial institutions found that amongst rural

households in Andhra Pradesh and Uttar Pradesh, 59% lack access to deposit account and

78% lack access to credit. Considering that the majority of the 360 million poor

30

households (urban and rural) lack access to formal financial services, the numbers of

customers to be reached, and the variety and quantum of services to be provided are

really large.

A tiny segment of this US$30 billion potential market has been reached so far and this is

unlikely to be addressed by MFIs and NGOs alone. Reaching this market requires serious

technology and human resources. However, 80% of the financial sector is still controlled

by public sector institutions. Competition, consolidation an capital, the convergence are

all being discussed to improve efficiency and outreach but significant opposition remains;

Microfinance on its own is unlikely to be able to address formidable challenges of

underdevelopment, poor infrastructure and governance.

There is still lot of policy focus on what activities are and are not allowed and not enough

operational freedom as yet for banks and financial institutions to design and deliver

programmes, and be responsible for their actions. Prescriptions and detailed circulars

often limit organizational innovation and market segmentation. If the right indicators are

monitored and operational freedom and incentives are clear, both public and private

banks have the capacity to rapidly address the remaining challenges. Regulation of the

microfinance sector poses unique challenges. They are worth enumerating as there

appears to be inadequate appreciation of these challenges in India.

The CGAP (Consultative Group to Assist the Poor), an international consortium of public

and private development agencies evolved a set of “Microfinance regulation consensus

guidelines” which have been adopted by its donor agencies. These guidelines are general

in nature and each country is expected to evolve its own regulatory framework based on

considerations of likely effectiveness and cost of supervision.

The regulation of microfinance poses certain unique challenges, different from bank

regulation.

• MFIs may not pose systemic challenges in the sense that it is unlikely that even the

largest MFIs are “too big to fail”. MFIs however deal with low income groups least likely

31

to bear downside risks, in a democratic country, politically the MFIs may be “too

sensitive to fail”.

• In the case of MFIs, most loans are collateral free and hence no such measures are

possible. On-time repayments on microfinance loans however tend to be high, though

experience shows that once a loan is overdue, the ultimate collection of the loan is less

likely, than in the case of loans that are backed by collateral (Rosenberg, 2008). As a

result, provisioning already delinquent loans needs to be more aggressive for micro credit

loans as compared to other loans.

• While bank failures may be contagious in the sense that the failure of one bank is

likely to impact solvency of others due to the interdependent nature of the payments

system, the interdependencies between group members in microfinance can lead at times

to a different kind of contagion effect. Widespread defaults can occur either if some

members start consistently defaulting or if there are rumors of MFI failures. An important

incentive for repayment of collateral free MFI loans is the ability to obtain larger loans in

the future. Any event which Regulating India’s Microfinance Sector: A Suggested

Framework 11 makes the possibility of future loans reduce considerably, has the potential

to trigger widespread defaults. A regulator of MFIs has therefore to be highly sensitive to

these realities.

• MFI customers are often first time users of financial services and usually have low

education. The responsibility on the MFI to offer the right products which suit their

members’ needs as well as provide adequate financial education and training to them is

considerable. Regulation needs to necessarily oversee this important element of MFI

operations.

• Merely formulating regulation regarding codes of conduct for MFIs and providing

channels for dispute resolution regarding MFI practices is not sufficient. MFI customers

need to be made aware of them by using appropriate communication. Moreover the

channels need to be easily accessible.

• The cost that MFIs would incur in complying with regulation needs to be considered,

as it may have an impact on their lending rates.

32

Criticism

High interest rates charged to borrowers is very much criticized. The real average

portfolio yield cited by the a sample of 704 microfinance institutions that voluntarily

submitted reports to the Micro Banking Bulletin in 2006 was 22.3% annually. However,

annual rates charged to clients are higher, as they also include local inflation and the bad

debt expenses of the microfinance institution. Muhammad Yunus has recently made

much of this point, and in his latest book argues that microfinance institutions that charge

more than 15% above their long-term operating costs should face penalties.

The role of donors has also been questioned. The Consultative Group to Assist the Poor

(CGAP) recently commented that "a large proportion of the money they spend is not

effective, either because it gets hung up in unsuccessful and often complicated funding

mechanisms or it goes to partners that are not held accountable for performance. In some

cases, poorly conceived programs have retarded the development of inclusive financial

systems by distorting markets and displacing domestic commercial initiatives with cheap

or free money.”

There has also been criticism of micro lenders for not taking more responsibility for the

working conditions of poor households, particularly when borrowers become quasi-wage

laborers, selling crafts or agricultural produce through an organization controlled by the

MFI. Critics maintain that there are few if any rules or standards in these cases governing

working hours, holidays, working conditions, safety or child labor, and few inspection

regimes to correct abuses.

Financial services, particularly credit, are not appropriate for all people at all times. For

loans that will be used for business purposes, micro credit best serves those who have

identified an economic opportunity and can capitalize on it if they have access to a small

amount of ready cash. Regardless of how loans are used, MFIs can provide long-term,

stable credit access only when clients have both the willingness and ability to meet

scheduled loan repayments.

33

Microfinance is particularly inappropriate for the penniless, who may need grants or

other public resources to improve their economic situation. Grants are a more efficient

way to transfer resources to the destitute than are loans that many will not be unable to

repay. Too much risk is placed on the MFI and client, when the only way a client can

repay a loan is by starting a successful business. Basic requirements like food, shelter,

and employment are often more urgently needed than financial services and should be

appropriately funded by government and donor subsidies.

Governments and development agencies often use microfinance as a tool to address

socio-economic problems such as relocation of refugees from civil dissension, generating

employment among demilitarized soldiers, or assistance following a natural disaster.

Microfinance may or may not be able to respond to these situations effectively, and

certainly not as a stand-alone intervention. Implementing a successful microfinance

program to address these types of situations depends upon a number of factors, the most

important of which is a client base capable of making regular repayments.

Conclusions

Providing microfinance to poor for starting business or improving existing business or

providing finance for household needs is a great step by government and the financial

institutions such as Grameen Bank, BARC, etc.

Micro-Finance can be a powerful instrument initiating a cyclical process of growth

and development.

Using microfinance as a platform to offer integrated services increases economies

of scope for all the organizations involved in trying to service the same base of

clienteles. With leveraged resources – assets, infrastructure, knowledge, distribution

channels, etc. – we can increase the capacity of the service offerings to reach more

clients and to reach them more effectively.

Micro-Finance activity improved access of rural poor to financial services, both

savings and credit.

Increased access signifies overcoming isolation of rural women in terms of their

access to financial services and denial of credit due to absence of collateral.

34

The pool of savings generated out of very small but regular contributions improved

access of the poor women to bank loans.

It could also help in strengthening poor families’ resistance to external shocks and

reducing dependence on moneylenders.

The observed support for consumption smoothening would not have been possible,

but for the SHGs internal support.

The predominance of borrowing for crop cultivation reflects support for meeting

working capital needs.

Possibilities could be of explored for using SHGs as a strong conduit for purveying crop

cultivation loans to very small and marginal farmers to step up crop loan finance.

MFIs that took steps of forge in offering integrated services to their clients and to partner

wherever it makes sense must be appreciated. The fight to assuage poverty is

too great a task for anyone or any one discipline to combat it alone. As an ingrained and

recognized leader in this mission, microfinance can serve as a bridge beyond banking and

development. It can be the link that brings together the services and products available

today to the people who need them most. Only through a collective effort will we have

the best chance of succeeding.

Bibliography

1. Almario,J., E. Jimenez and B.R. Pia (2006) : The development and implementation of

a uniform set of performance standards for all types of microfinance institutions in the

Philippines

(http://www.microfinanceregulationcenter.org/files/34558_file_Philippines_PESO.pdf)

2. Asian Banker (2007) : Upwardly Mobile Asian Banker August 13 Basu, P (2006):

Improving access to finance for India’s rural poor, Washington DC: World Bank CGAP

(2002) : Microfinance Consensus Guidelines

(http://www2.cgap.org/gm/document-1.9.2787/Guideline_RegSup.pdf)

3. CGAP (2008) : Note on Regulation of Branchless Banking in India

(http://www.cgap.org/gm/document-1.9.2322/India-Notes-On-Regulation-Branchless-

Banking-2008.pdf)

35

4. Economist (2009) : The power of mobile money Economist September 26th –

October 2nd

5. Ghate, P (2006) : Microfinance in India A State of the Sector Report, 2006, New

Delhi:

6. Microfinance India Ghate, P (2007) : Financial inclusion via exclusion? Economic

Times

7. Ghate, P, S Gunaranjan, V Mahajan, P Regy, F Sinha, and S Sinha (2007) :

Microfinance in India A State of the Sector Report, 2007, New Delhi: Microfinance India

8. Intellecap (2007) : Inverting the pyramid: The Changing face of Microfinance

(www.microfinancegateway.org)

9. Maegher, P (2002) : Microfinance Regulation in Developing Countries: A

Comparative Review of Current Practice IRIS Centre

(http://www.microfinancegateway.com)

10. Mahajan, V (2007) : Charting the History of Microfinance in India ISB Insight March

11. Micro credit Ratings International Ltd. (2005) A Study of the Regulatory

Environment and its implications for legal form by Microfinance Institutions in India

Final Report (http://www.microfinancegateway.com)

12. NABARD website. (http://www.nabard.org/)

13. Regulating India’s Microfinance Sector: A Suggested Framework 23 NCAER (2008)

Impact and sustainability of SHG Bank Linkage Programme

http://www.apmas.org/pdf%5CGTZ_NCAER.pdf.

14. Porteous, D (2006) : Competition and Microcredit Interest Rates

(http://www.cgap.org/)

15. Rajan, R (2008) : A Hundred Small Steps Draft Report of the Committee on Financial

Sector Reforms

(http://planningcommission.nic.in/reports/genrep/report_fr.htm)

16. Rangarajan, C (2008) : Report of the Committee on Financial inclusion

(http://www.nabard.org/pdf/report_financial/Full%20Report.pdf)

36

17. Reddy, Y V (2005) : Microfinance: Reserve Bank’s Approach, Address at the

Microfinance Conference organised by the Indian School of Business, August 6 Reserve

Bank of India (http://www.rbi.org.in/)

18. Reserve Bank of India (2009) : Handbook of Statistics on Indian Economy

(http://www.rbi.org.in/)

19. Rosenberg, R (2008) : How should governments regulate microfinance? In: S.

Sundaresan, ed.

20. Microfinance Emerging Trends and Challenges, (Cornwall: MPG Books pp) 85-107

21. Rutherford,S (2001): The Poor and their Money

(http://www.microfinancegateway.com)

22. Sa-dhan (2009) Bharat Microfinance Report

(http://www.indiamicrofinance.com/microfinance/microfinance-india/the-bharat-

microfinancereport-quick-data-2009.html)

23. Shankar, S (2007) Transaction Costs in Group Microcredit in India Management

Decision 45(8):1331-1342

24. Shylendra, H S (2006) : Microfinance Institutions in Andhra Pradesh Crisis and

Diagnosis

25. Economic and Political Weekly May 20 1959-1963

26. Srinivasan, N (2009) : Microfinance India State of the Sector Report, 2008 New

Delhi: Sage Publications

27. Tankha, A., (2006) : Challenges and potential for Indian banks to implement Business

Facilitator and Business Correspondent models A status report GTZ Rural Finance

Program India Paper October.

37

Trends in the Growth of Higher Education in Andhra Pradesh

Dr. D. Pulla Rao

Abstract

Higher education promotes social and economic development by building human and

technical capabilities of a society. The development of higher education is highly correlated

with the level of overall development. Andhra Pradesh is one of the few states, which had the

advantage of a sound educational system and structure. After formation of the state of

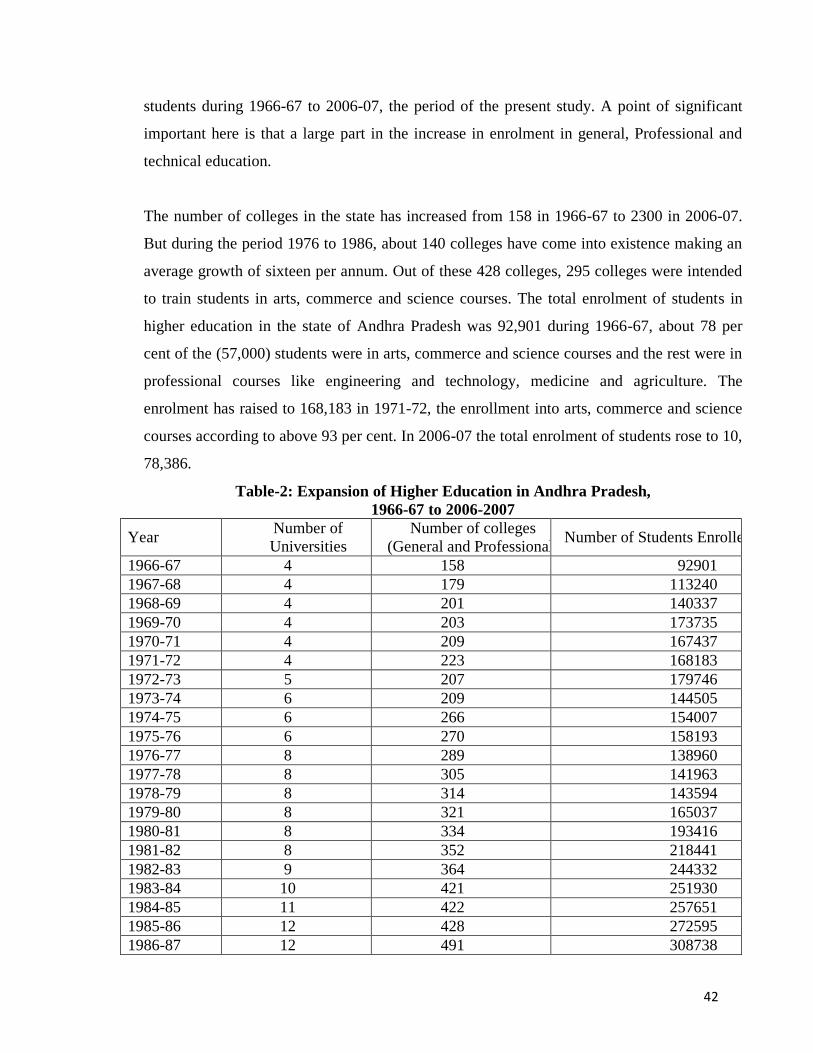

Andhra Pradesh in 1956, there has taken place a tremendous expansion in the growth of

higher education. The number of degree colleges increased from 158 in 1966-67 to 2,300 in

2006-07 and enrollment of students increased from 92,901 in 1966-67 to 10,78,386 in 2006-

07. The number of teachers increased from 4,563 in 1966-67 to 29,036 in 2006-07. The

highest number of Government colleges (17) situated in Mahaboonagar District and the

lowest number (4) in Vizianagaram District. The student-teacher ratio is recorded at optimum

level in Acharya Nagarjuna University area and the lowest in Kakatiya University area. So,

the Government must improve the infrastructural facilities and recruitment of teachers in the

backward areas. The Government gradually reducing the expenditure on education in the

total budget. It is not positive sign for the development of education. So, the Government

should increase the allocation of expenditure on education in general and on higher education

in particular.

Key Words: Higher education, enrolment, elementary education

Introduction

Andhra Pradesh has been recognized as the fifth largest state in the Indian Union with an

area of 2, 75,068 sq.kms. and the population of 8.46 crores as per the 2011Census. Andhra

Pradesh is the first state in India that has been formed on purely linguistic basis, out of a

several political units with different histories. Educationally, Andhra Pradesh is one of the

Professor of Economics, Andhra University, Visakhapatnam-3, A.P.

38

nine backward states in India, and it lowest among the Southern States. This state however,

has developed a sound educational system and structure and it was the first state to

implement the educational structure of 10+2+3 in 1969 as per the recommendations of

Kothari Commission.

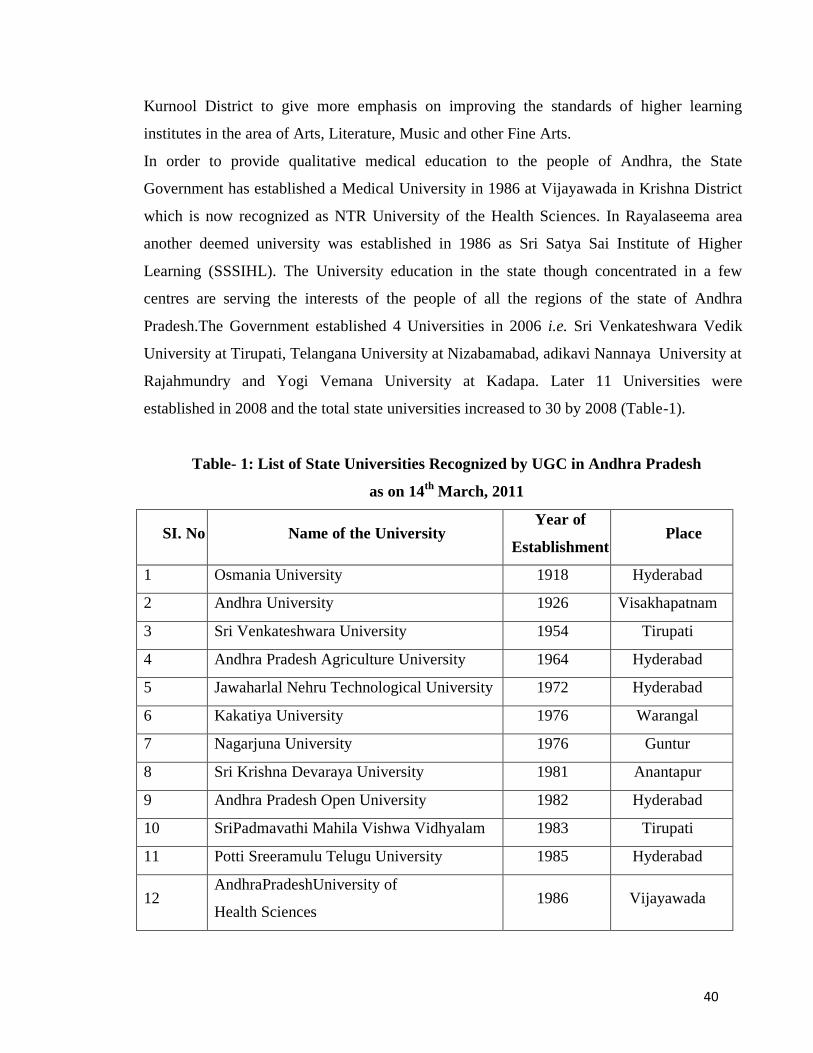

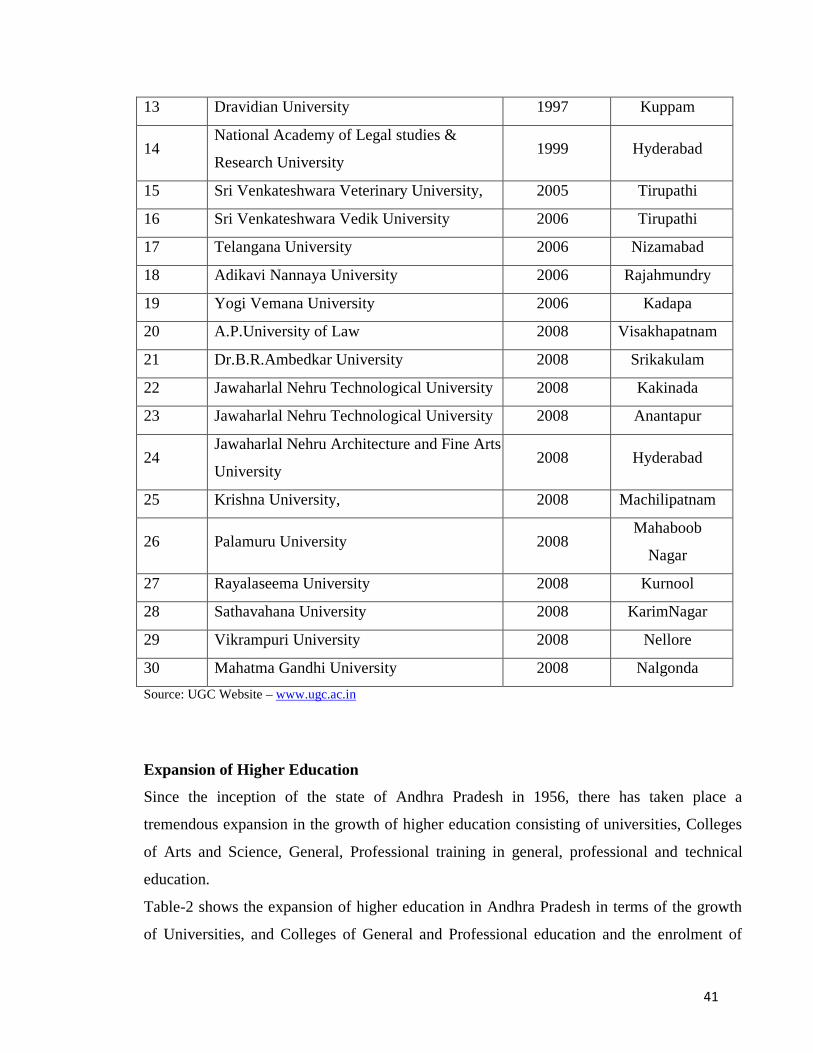

University System of Education in Andhra Pradesh

Since independence, significant progress is seen in University system of education in Andhra

Pradesh. The ladder of general education is now within the purview of an ordinary man to get

higher level of education. The state of Andhra Pradesh has the privilege to establish three