Confidential. © 2017 IHS Markit TM . All Rights Reserved. VMA MARKET OUTLOOK WORKSHOP / August 2017 Confidential. © 2017 IHS Markit TM . All Rights Reserved. Global Petrochemical Market Outlook: Will Expansion Activity in North America Continue? Mark Eramo, Vice President Oil / Midstream / Downstream / Chemicals IHS Market ‐ Houston, TX [email protected] Presented to: VMA MARKET OUTLOOK WORKSHOP OMNI Parker House, Boston, MA

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

VMA MARKET OUTLOOK WORKSHOP / August 2017

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

Global Petrochemical Market Outlook:Will Expansion Activity in North America Continue?

Mark Eramo, Vice President Oil / Midstream / Downstream / Chemicals IHS Market ‐ Houston, TX [email protected]

Presented to:

VMA MARKET OUTLOOK WORKSHOPOMNI Parker House, Boston, MA

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

VMA MARKET OUTLOOK WORKSHOP / August 2017

Addressing strategic challenges with interconnected capabilities

2

Resources

Financial

Consolidated Markets & Solutions

Transportation

© 2017 IHS Markit. All Rights Reserved.

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

VMA MARKET OUTLOOK WORKSHOP / August 2017 3

Best-in-Class Brand Names

Brought together to form the most comprehensive single source for global data & information, key industry events, market insights, analysis & forecasts, technology & analytical platforms, and consulting services

3

Oil Markets / Midstream / Downstream / Chemicals

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

VMA MARKET OUTLOOK WORKSHOP / August 2017

Core Segments within Energy & Natural Resources

4

• Country E&P Terms and Above-Ground Risk

• Plays and Basins• Costs and Technology• Companies and

Transactions

UPSTREAM

• Global Gas• Coal• Power and Renewables• Regional Gas, Power

and Coal Markets

POWER, GAS, COAL& RENEWABLES

• Long-Term Planning & Scenarios • Climate Strategy

• Curated Content• Integrated Energy Events & CERAWeek

ENERGY-WIDE PERSPECTIVES

• Crude Oil Markets• Midstream Oil and

Natural Gas Liquids• Refining and Marketing• Company Strategies and

Performance

OIL MARKETS, MIDSTREAM, DOWNSTREAM & CHEMICAL

• Chemical Week and Market Daily Service

• Base Chemicals & Plastics

• Specialty Chemicals• Costs & Technology• Company Benchmarking

& Analytics

Our core capabilities serve our energy and chemical customers across the value chain through focused data and insight subscriptions as well as consulting.

© 2017 IHS Markit

VMA MARKET OUTLOOK WORKSHOP / August 2017

© 2017 IHS Markit

VMA MARKET OUTLOOK WORKSHOP / August 2017

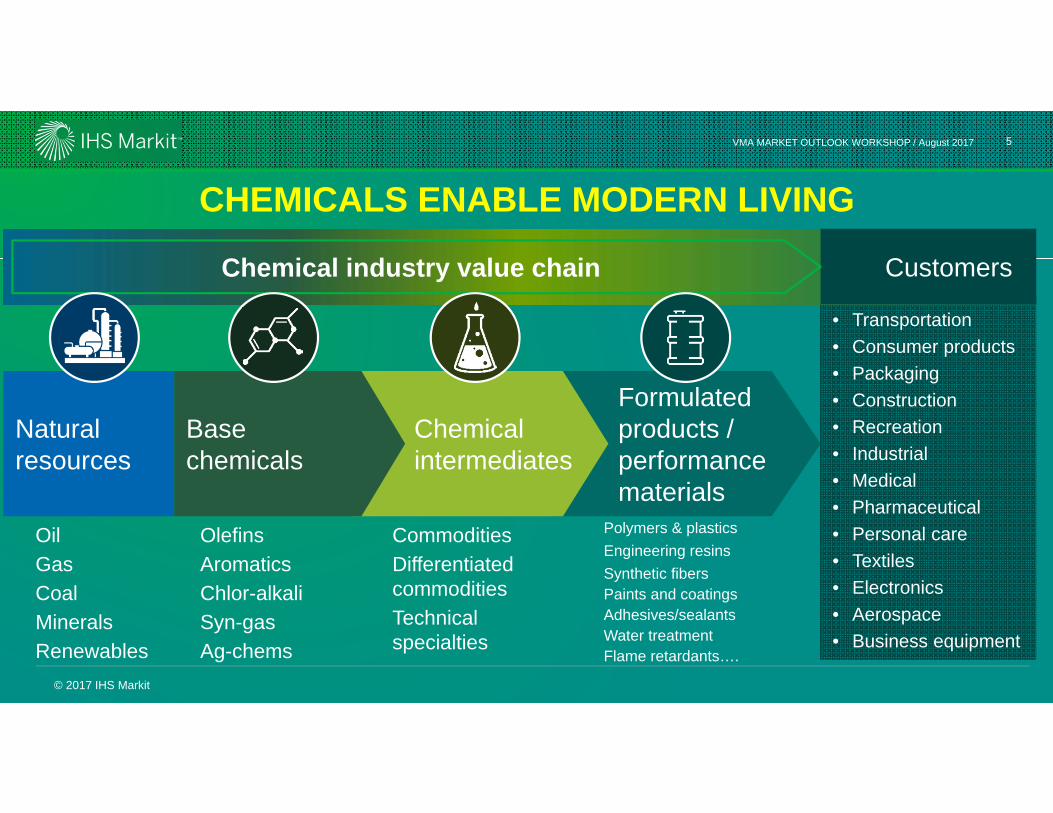

• Transportation• Consumer products• Packaging• Construction• Recreation• Industrial• Medical• Pharmaceutical• Personal care• Textiles• Electronics• Aerospace• Business equipment

OilGasCoalMineralsRenewables

Customers

Olefins AromaticsChlor-alkaliSyn-gasAg-chems

CommoditiesDifferentiated commoditiesTechnical specialties

Chemical industry value chain

Formulated products / performance materials

Natural resources

Chemicalintermediates

Base chemicals

CHEMICALS ENABLE MODERN LIVING

Polymers & plasticsEngineering resinsSynthetic fibersPaints and coatingsAdhesives/sealantsWater treatment Flame retardants….

5

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

VMA MARKET OUTLOOK WORKSHOP / August 2017

• Energy markets will see natural gas in North America significantly advantaged versus crude oil

• Global economy will grow at 2.5-3.0 % leading to annual demand growth of:

Ethylene ~ 5.5 to 6 million tons

Propylene ~ 4 to 4.5 million tons

Methanol ~ 3.5 to 4 million tons

• North America will remain an attractive region for base chemical and derivatives capital investments

• Investments continue in China and Middle East at a more moderate pace

Petrochemical Market OutlookAs global demand grows, North America will continue to attract new investments

Ethylene

PropyleneMethanol

6

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

VMA MARKET OUTLOOK WORKSHOP / August 2017

Energy fundamentals impact chemical industry investment decisions, short term demand growth

• Energy trends impact regional competitiveness, industry profitability, and ultimately drive investment decisions in the global petrochemical industry

• Advantaged investments in North America, Middle East and China see lower margins in low crude oil market

• IHS Markit Vice Chairman Daniel Yergin observes that there are two major forces currently operating on the global oil market, rebalancing and recalibration.

• The North American natural gas market is becoming more integrated, complex, and globally connected, subject to demand uncertainties in a currently oversupplied world market.

• Crude oil (energy) “at the extremes” impacts demand for chemicals and plastics. At the extremes, energy trends will both destroy and stimulate demand

7

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

VMA MARKET OUTLOOK WORKSHOP / August 2017

Combination of high crude prices and stable gas is attractive for North America chemical investments, based on natural gas and natural gas liquids

0

3

7

10

13

17

20

0

20

40

60

80

100

120

00 02 04 06 08 10 12 14 16 18 20 22 24

USGC Natural Gas

Brent Crude

Global crude oil vs. USGC natural gas

Source: History: Argus (crude), Intelligence Press (gas); Forecast by IHS Markit Energy

$/B

arre

l, C

rude

$/ M

MB

tu, N

atur

al G

as

Source: IHS Markit

Lower longer case

8

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

VMA MARKET OUTLOOK WORKSHOP / August 2017

Demand growth for chemicals & plastics directly linked to global economic growth

• Basic chemicals and plastics represent the key building blocks for durable and non-durable consumer goods

• Multiple years of positive economic growth results in acceleration of base chemical demand growth

• Aligning capacity additions with demand growth is the balance producers are seeking

• Economic contractions/stimulus causing supply-chains to respond rapidly (inventor de-stock / re-stock).

9

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

VMA MARKET OUTLOOK WORKSHOP / August 2017

Economic growth in advanced countries and emerging markets are key drivers to petrochemical demand

2014 2015 2016 2017 2018 2019

World 2.8 2.8 2.5 3.0 3.2 3.1USA 2.4 2.6 1.6 2.3 2.7 2.3

Canada 2.6 0.9 1.4 2.7 2.3 2.3

Eurozone 1.2 1.9 1.7 2.0 1.8 1.7

UK 3.1 2.2 1.8 1.4 1.0 1.2

China 7.3 6.9 6.7 6.6 6.3 6.1

Japan 0.2 1.2 1.0 1.3 1.0 0.7

India 6.9 7.7 7.0 7.3 7.4 7.6

Brazil 0.5 -3.8 -3.6 0.2 1.7 3.5

Russia 0.8 -2.8 -0.2 1.5 2.1 1.8

-4

-2

0

2

4

6

8

10

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

World Advanced countries Emerging markets

Real GDP, Annual % Change

Source: IHS Markit © 2017 IHS Markit

Annual % Change in GDP

10

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

VMA MARKET OUTLOOK WORKSHOP / August 2017

Chemical demand growth (vs GDP) has been decelerating over time; forecast to continue

0.0

0.5

1.0

1.5

2.0

2.5

3.0

1990-1999 2000-2007 2011-2016 2017-2025

Ethylene Propylene Methanol ParaxyleneBenzene Chlorine Weighted Average

Average global GDP elasticity, by market & time period

Source: IHS Markit

11

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

VMA MARKET OUTLOOK WORKSHOP / August 2017

Ethylene and propylene continue pattern of accelerating demand growth / strong capacity growth is needed

0.0

2.0

4.0

6.0

8.0

Ethylene Propylene Methanol2016 Dmd GrowthAvg. Dmd Growth (2011-2015)Avg. Dmd Growth (2017-2021)

Demand growth: past / present / forecast (million metric tons)

Source: IHS Markit

0.0

2.0

4.0

6.0

8.0

Ethylene Propylene Methanol2016 Cap. GrowthAvg. Cap. Growth (2011-2015)Avg. Cap. Growth (2017-2021)

Nameplate capacity growth: past / present / forecast (million metric tons)

Source: IHS Markit

12

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

VMA MARKET OUTLOOK WORKSHOP / August 2017

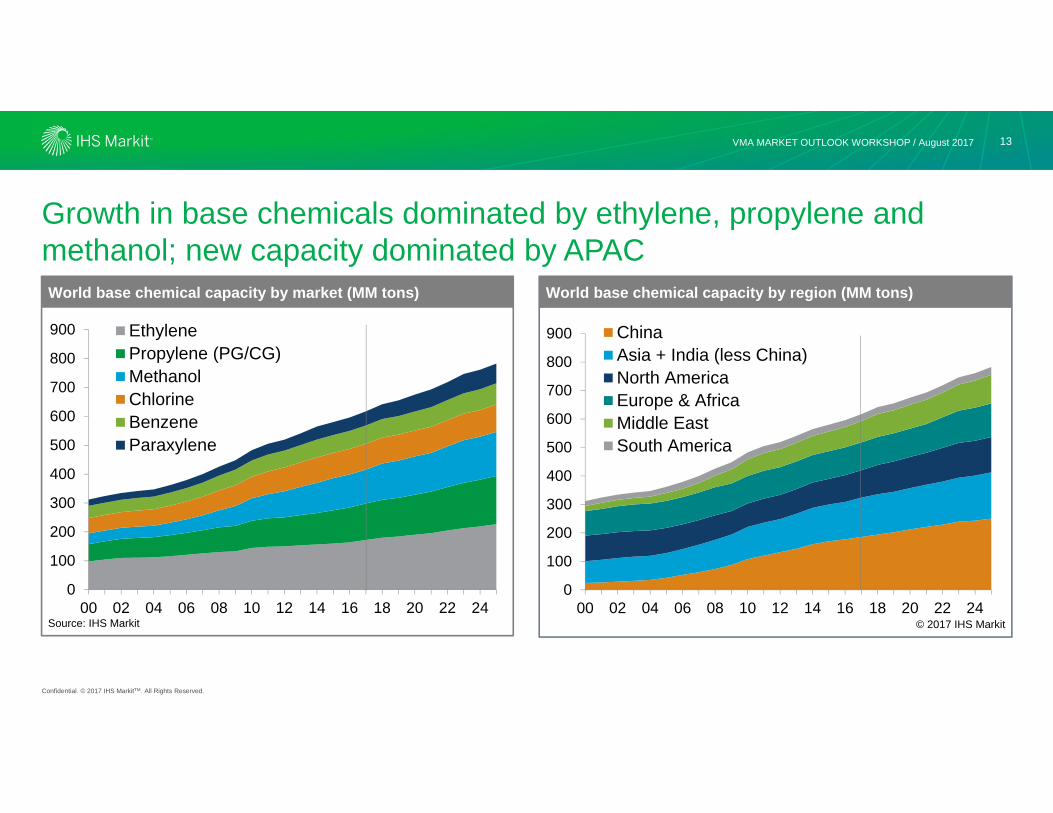

Growth in base chemicals dominated by ethylene, propylene and methanol; new capacity dominated by APAC

0

100

200

300

400

500

600

700

800

900

00 02 04 06 08 10 12 14 16 18 20 22 24

EthylenePropylene (PG/CG)MethanolChlorineBenzeneParaxylene

World base chemical capacity by market (MM tons)

Source: IHS Markit

0

100

200

300

400

500

600

700

800

900

00 02 04 06 08 10 12 14 16 18 20 22 24

ChinaAsia + India (less China)North AmericaEurope & AfricaMiddle EastSouth America

World base chemical capacity by region (MM tons)

© 2017 IHS Markit

13

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

VMA MARKET OUTLOOK WORKSHOP / August 2017

Other unknowns impact strategic investment decisions

• Energy risk in an OPEC / shale regime • Demand risk given China’s economic and

industrial pivot • Unpredictable capital and project EPC

performance• Climate policy post Paris Accords• Disruptive technologies (e.g. Siluria)• Country risk with geo-political unrest• Market access risk under protectionist

backlash

14

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

VMA MARKET OUTLOOK WORKSHOP / August 2017

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

Capital investments in chemicals are seeking a sustainable competitive advantage

Chemical Investment “Drivers”• Secure an energy & feedstock

advantage.• Leverage current technology and

build world-scale.• Invest with proximity to local

markets and/or access to trade routes.

• Build to leverage an upstream and/or downstream integrated position.

Braskem-Idesa Ethylene/PE PlantNanchital, Veracruz, MexicoStart-Up: June 2016

Photo courtesy of Braskem IDESA

15

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

VMA MARKET OUTLOOK WORKSHOP / August 2017 16

Beyond energy and economic growth, there are many other factors to consider:

Additional Investment Considerations:• Crude oil/energy price trends

• Global economic growth

• Geo-political considerations

• Govt. fiscal policy / currency strength

• Global energy markets

• State of industry profit cycle

• China structural changes

• Non-conventional technology

• Sustainability

• Levels of integration

• Regional CAPEX differentials

• Logistics investments

• Evolving Consumer Products

Braskem-Idesa Ethylene/PE PlantNanchital, Veracruz, MexicoStart-Up: June 2016

16

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

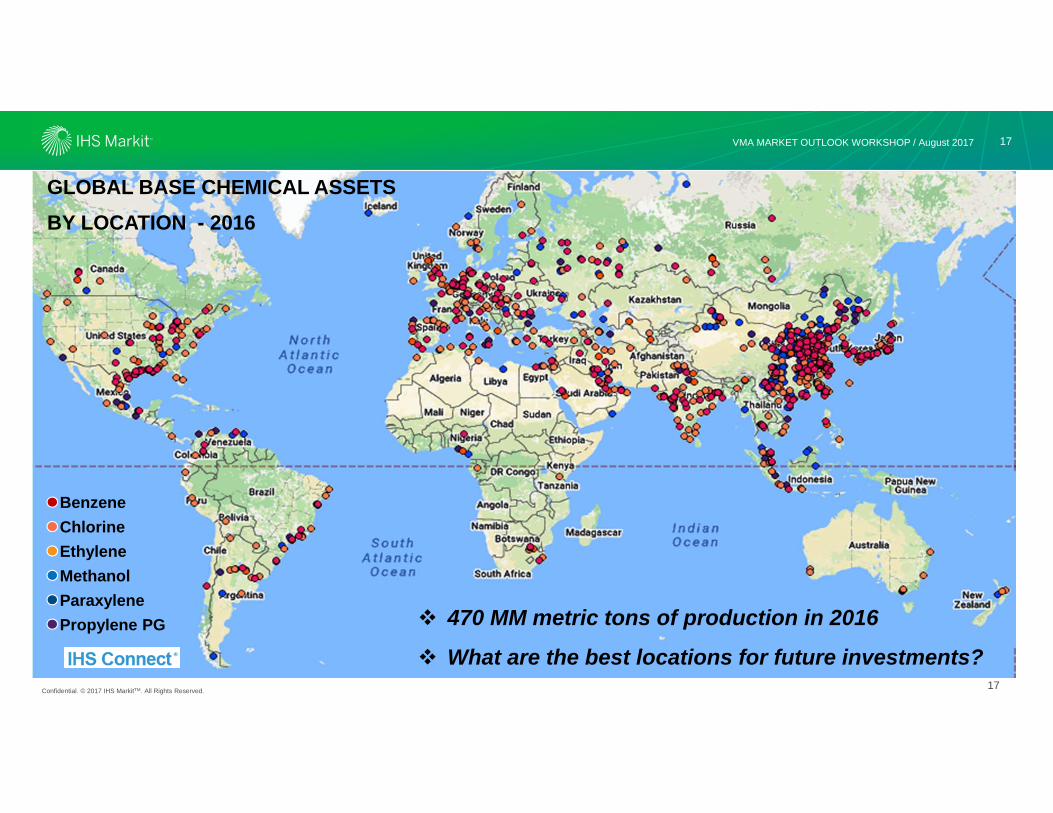

VMA MARKET OUTLOOK WORKSHOP / August 2017 17

17

BenzeneChlorineEthyleneMethanolParaxylenePropylene PG 470 MM metric tons of production in 2016

What are the best locations for future investments?

GLOBAL BASE CHEMICAL ASSETS BY LOCATION - 2016

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

VMA MARKET OUTLOOK WORKSHOP / August 2017

Market uncertainty results in slowdown in new capacity additions; 2019 forecast to decline to 2012 levels

-5.0

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

91 93 95 97 99 01 03 05 07 09 11 13 15 17 19 21

Mill

ion

Met

ric T

ons

Ethylene Propylene Methanol Chlorine Benzene Paraxylene

Annual Base Chemical Capacity Change By Market

© 2017 IHS MarkitSource: IHS Markit

18

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

VMA MARKET OUTLOOK WORKSHOP / August 2017

Driven by a number of major initiatives, China investment in base chemicals has accelerated since 2000 and will continue into the 2020’s

• Secure an energy & feedstock advantage

• Leverage current technology and build world-scale

• Invest with proximity to local markets and/or access to trade routes

• Build to leverage an upstream and/or downstream integrated position

0

50

100

150

200

250

300

90 92 94 96 98 00 02 04 06 08 10 12 14 16 18 20 22 24 26

United States Canada

Mexico Saudi Arabia

Iran South Korea

Singapore China

India

Total base chemical capacity for select countries

Mill

ion

Met

ric T

ons

Source: IHS Markit Base Chemical Capacity = ethylene, propylene, methanol, benzene, paraxylene, chlorine

19

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

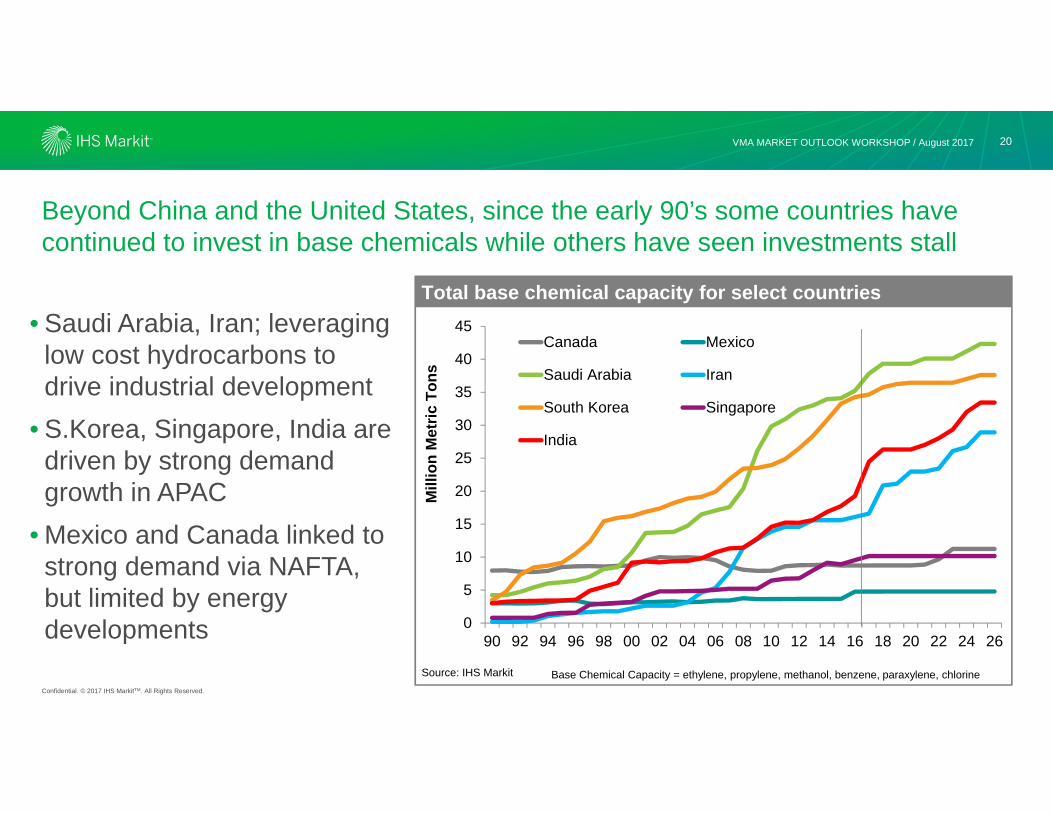

VMA MARKET OUTLOOK WORKSHOP / August 2017

Beyond China and the United States, since the early 90’s some countries have continued to invest in base chemicals while others have seen investments stall

• Saudi Arabia, Iran; leveraging low cost hydrocarbons to drive industrial development

• S.Korea, Singapore, India are driven by strong demand growth in APAC

• Mexico and Canada linked to strong demand via NAFTA, but limited by energy developments 0

5

10

15

20

25

30

35

40

45

90 92 94 96 98 00 02 04 06 08 10 12 14 16 18 20 22 24 26

Canada Mexico

Saudi Arabia Iran

South Korea Singapore

India

Total base chemical capacity for select countries

Mill

ion

Met

ric T

ons

Source: IHS Markit Base Chemical Capacity = ethylene, propylene, methanol, benzene, paraxylene, chlorine

20

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

VMA MARKET OUTLOOK WORKSHOP / August 2017

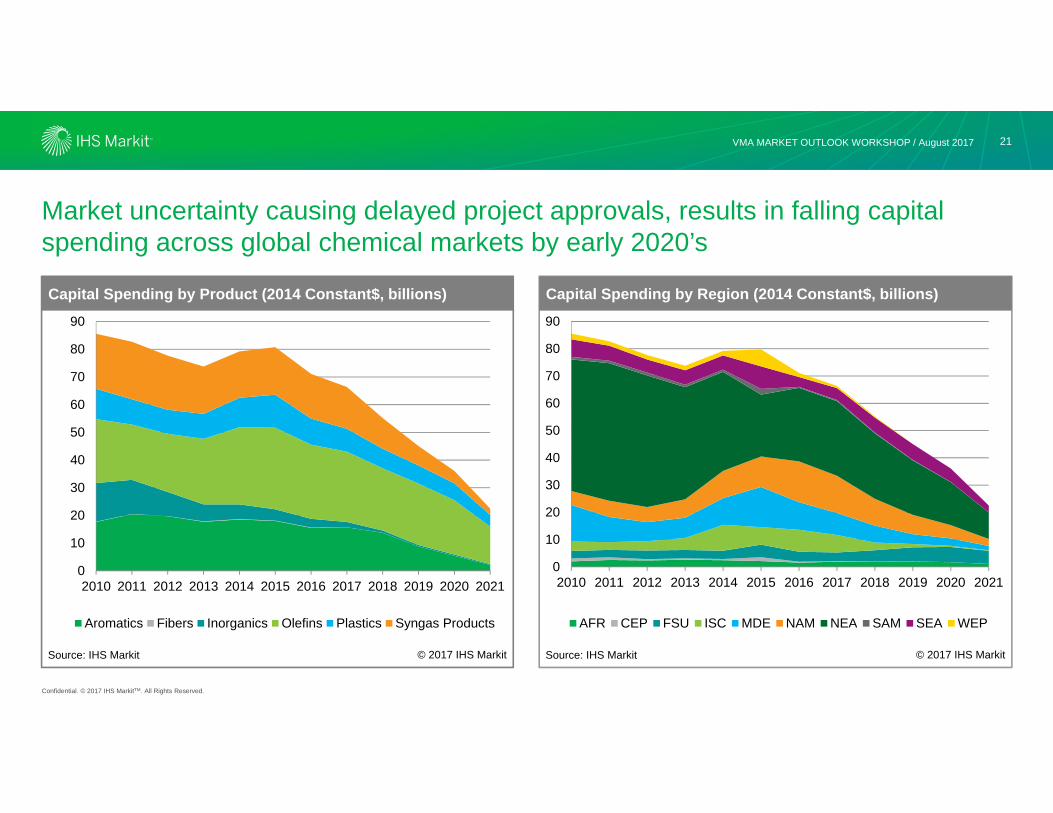

Market uncertainty causing delayed project approvals, results in falling capital spending across global chemical markets by early 2020’s

21

0

10

20

30

40

50

60

70

80

90

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Aromatics Fibers Inorganics Olefins Plastics Syngas Products

Capital Spending by Product (2014 Constant$, billions)

Source: IHS Markit © 2017 IHS Markit

0

10

20

30

40

50

60

70

80

90

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

AFR CEP FSU ISC MDE NAM NEA SAM SEA WEP

Capital Spending by Region (2014 Constant$, billions)

Source: IHS Markit © 2017 IHS Markit

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

VMA MARKET OUTLOOK WORKSHOP / August 2017

Ammonia, along with ethylene, propylene (and related derivatives) make up the vast majority of new capital spending in the next wave of investments

0.0 10.0 20.0 30.0 40.0 50.0 60.0 70.0 80.0 90.0

PROPYLENE OXIDEBUTADIENE

BENZENEETHYLENE OXIDE

CHLORINELLD POLYETHYLENE

LD POLYETHYLENEHD POLYETHYLENE

PARAXYLENEMONOETHYLENE GLYCOL

POLYPROPYLENETEREPHTHALIC ACID

METHANOLMIXED XYLENES

PROPYLENE (PG/CG)AMMONIA

ETHYLENE

Capital Spending (US$ billions) Capacity Additions (million tons)

Capacity additions (MM tons) and Capital spending (US$ billions) by chemical market: 2016 to 2025

Source: IHS Markit © 2017 IHS Markit

22

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

VMA MARKET OUTLOOK WORKSHOP / August 2017

North America Low Cost Brings Back Base Chemical & Associated Derivative Investments

-10

10

30

50

70

90

110

130

150

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25

Ethylene Propylene (PG/CG) Methanol Chlorine Benzene Paraxylene

North America - Base Chemical Total Capacity

Source: IHS Markit

Mill

ion

Met

ric T

ons

© 2017 IHS Markit

23

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

VMA MARKET OUTLOOK WORKSHOP / August 2017

North America ethylene capacity growth including firm and announced projects

24

Company Location Timing Total Growth-000- metric tons

Dow Plaquemine, LA 1H-17 250

Equistar Corpus Christi, TX 1H-17 401

Oxy/Mexichem Ingleside, TX 1H-17 550

ChevronPhillips Cedar Bayou, TX 2H-17 1,500

Dow Freeport, TX 2H-17 1,500

ExxonMobil Baytown, TX 1H-18 1,500

Indorama Lake Charles,LA 2H-18 420

Formosa Point Comfort, TX 2H-18 1,150

Shin-Etsu Plaquemine, LA 1H-19 500

Sasol Lake Charles, LA 1H-19 1,550

LACC Lake Charles, LA 1H-20 1,000

Shell Monaca, PA 1H-22 1,500

Total additions 11,821

Company Location Total Growth-000- metric tons

Ascent / Braskem West Virginia 1,000

Badlands NGL 1 North Dakota 1,500

Badlands NGL 2 “Shangri-La” 1,000

ChevronPhillips 2 Cedar Bayou, TX 1,500

Formosa St James Parish, LA 1,000

Formosa LA 1,000

Hanwha TBA 1,000

Indorama LA or TX 1,500

PTTCG/Marubeni Shadyside, OH 1,000

Total additions 10,500

Firm Projects: 2017 - 2022 Announced Projects: 2022+

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

VMA MARKET OUTLOOK WORKSHOP / August 2017

Chemical industry earnings forecasts to decline with new waves of capacity in the near term; Chlor-alkali market showing good recovery by 2020

-200-100

0100200300400500600700800900

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Dol

lars

Per

Met

ric T

on

Global

Aromatics Chlor Alkali Olefins Plastics Syn Gas

Global Cash Earnings Trends by Chemical Value-Chain

Source: IHS Markit © 2017 IHS Markit

25

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

VMA MARKET OUTLOOK WORKSHOP / August 2017

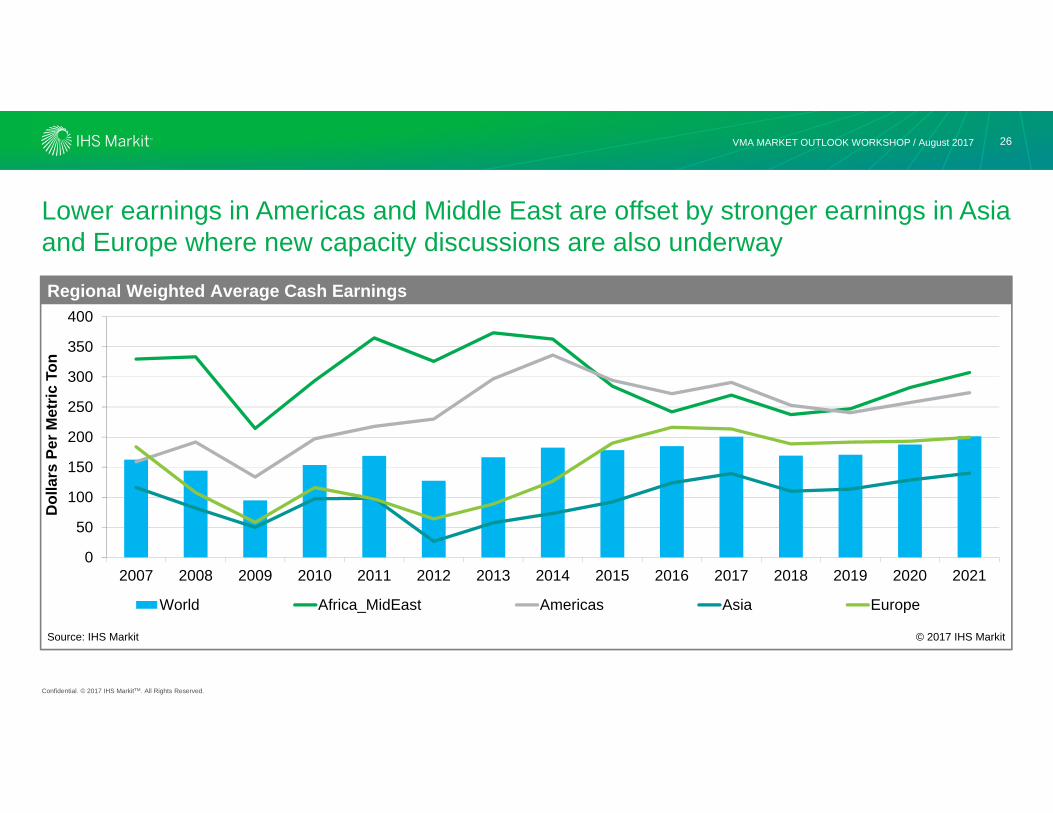

Lower earnings in Americas and Middle East are offset by stronger earnings in Asia and Europe where new capacity discussions are also underway

0

50

100

150

200

250

300

350

400

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Dol

lars

Per

Met

ric T

on

World Africa_MidEast Americas Asia Europe

Regional Weighted Average Cash Earnings

Source: IHS Markit © 2017 IHS Markit

26

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

VMA MARKET OUTLOOK WORKSHOP / August 2017

• Energy markets will see natural gas in North America advantaged versus crude oil (BTU basis)

• Two major forces in the global oil market, rebalancing and (cost) recalibration will play out in the near term

• Global economic fundamentals remain solid; uncertainty indicators have declined; US is strong; Europe is brighter; China remains resilient.

• Capital spending slowdown will create tight market conditions in olefins and chlor-alkali by end of the decade

• North America will remain an attractive region for petrochemical and related investments; investors to include both domestic and foreign companies

27

Final Thoughts As You Plan Your Next Move In The Chemical Sector

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

VMA MARKET OUTLOOK WORKSHOP / August 2017

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

Global Petrochemical Market Outlook:Will Expansion Activity in North America Continue?

Mark Eramo, Vice President Oil / Midstream / Downstream / Chemicals IHS Market ‐ Houston, TX [email protected]

Presented to:

VMA MARKET OUTLOOK WORKSHOPOMNI Parker House, Boston, MA

Thank You!

Related Documents