Views on the U.S. Housing Market Prepared: May 15, 2012 Overview The deflating of the U.S. housing bubble was a primary driver of the 2008-2009 financial crises. As of January 2012, the decline in housing prices has been 34% since the 2006 peak, according to S&P/Case-Shiller 20 City Composite. In the meantime, U.S. economic growth remains below potential expectations and this condition is likely to persist until the housing market finds some solid footing. While much has been made this spring about a full recovery in the housing market, we are much more sanguine in our view. We see the strong positives of affordability and improving builder sentiment counterbalanced by still high delinquencies and vacancy rates. We believe time will be part of the solution as it affords lenders the ability to get through the foreclosure backlog, and perhaps implement novel solutions such as “rent to foreclose.” Time may also allow for greater recovery in employment and for foreclosed properties to provide supply to the growing rental market. Over the next two years, we believe the pace of decline in housing prices should stabilize and housing inventories should normalize. We are likely to see improving homebuilder activity, especially targeted at the rental market. At this point, we feel housing will likely become a positive contributor to economic growth in the near future. Housing prices have fallen significantly below long-term trends and many homes may be quite undervalued. Real Housing Prices Important disclosures provided on page 3. Situation Analysis 400 350 300 250 200 150 100 50 0 1980 Quarterly U.S. House Price Index 1975 1985 1990 1995 2000 2005 Dec 2011 2010 Trendline Source: Federal Housing Finance Agency (FHFA); data through December 2011

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Views on the U.S. Housing MarketPrepared: May 15, 2012

OverviewThe deflating of the U.S. housing bubble was a primary driver of the 2008-2009 financial crises. As of January 2012, the decline in housing prices has been 34% since the 2006 peak, according to S&P/Case-Shiller 20 City Composite. In the meantime, U.S. economic growth remains below potential expectations and this condition is likely to persist until the housing market finds some solid footing. While much has been made this spring about a full recovery in the housing market, we are much more sanguine in our view. We see the strong positives of affordability and improving builder sentiment counterbalanced by still high delinquencies and vacancy rates. We believe time will be part of the solution as it affords lenders the ability to get through the foreclosure backlog, and perhaps implement novel solutions such as “rent to foreclose.” Time may also allow for greater recovery in employment and for foreclosed properties to provide supply to the growing rental market. Over the next two years, we believe the pace of decline in housing prices should stabilize and housing inventories should normalize. We are likely to see improving homebuilder activity, especially targeted at the rental market. At this point, we feel housing will likely become a positive contributor to economic growth in the near future.

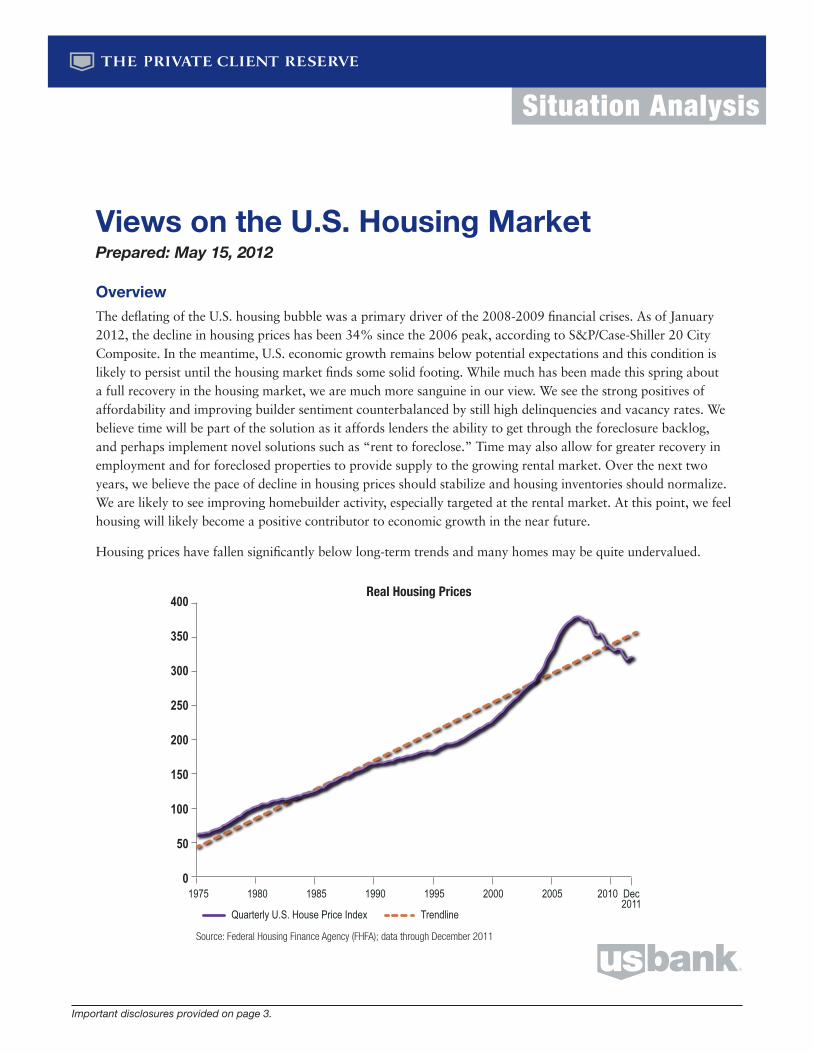

Housing prices have fallen significantly below long-term trends and many homes may be quite undervalued.

Real Housing Prices

Important disclosures provided on page 3.

Situation Analysis

400

350

300

250

200

150

100

50

01980

Quarterly U.S. House Price Index

1975 1985 1990 1995 2000 2005 Dec2011

2010

Trendline

Source: Federal Housing Finance Agency (FHFA); data through December 2011

Important disclosures provided on page 3.

Page 2Views on the U.S. Housing Market

Situation Analysis

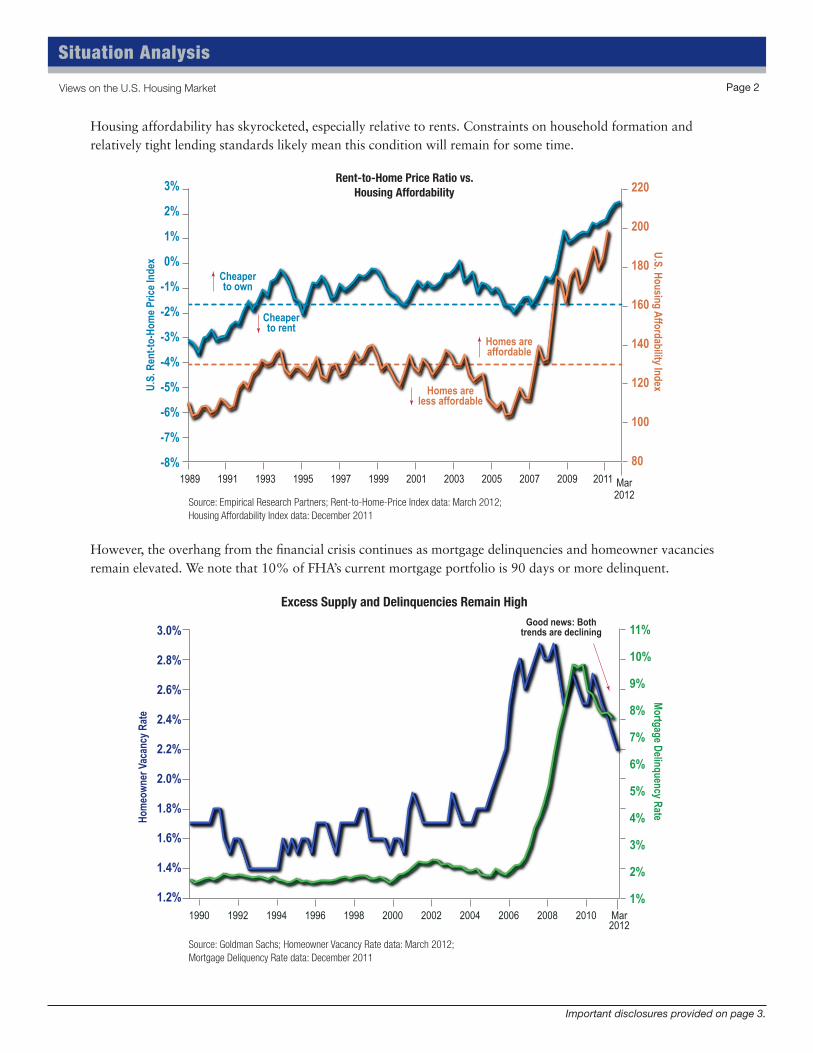

Housing affordability has skyrocketed, especially relative to rents. Constraints on household formation and relatively tight lending standards likely mean this condition will remain for some time.

Rent-to-Home Price Ratio vs.Housing Affordability

However, the overhang from the financial crisis continues as mortgage delinquencies and homeowner vacancies remain elevated. We note that 10% of FHA’s current mortgage portfolio is 90 days or more delinquent.

Excess Supply and Delinquencies Remain High

3%

2%

1%

0%

-1%

-2%

-3%

-4%

-5%

-6%

-7%

-8%

220

200

180

160

140

120

100

801989 1991

U.S

. Ren

t-to-

Hom

e Pr

ice

Inde

xU

.S. Housing A

ffordability Index

1993 1995 19991997 2003 20052001 2007 2011 Mar2012

2009

Cheaperto own

Cheaperto rent

Homes areaffordable

Homes areless affordable

3.0%

2.8%

2.6%

2.4%

2.2%

2.0%

1.8%

1.6%

1.4%

1.2%

11%

10%

9%

8%

7%

6%

5%

4%

3%

2%

1%1990 1992

Hom

eow

ner V

acan

cy R

ate

Mortgage D

elinquency Rate

1994 1996 20001998 2004 20062002 2008 Mar2012

2010

Good news: Bothtrends are declining

Source: Empirical Research Partners; Rent-to-Home-Price Index data: March 2012; Housing Affordability Index data: December 2011

Source: Goldman Sachs; Homeowner Vacancy Rate data: March 2012; Mortgage Deliquency Rate data: December 2011

Page 3Views on the U.S. Housing Market

Situation Analysis

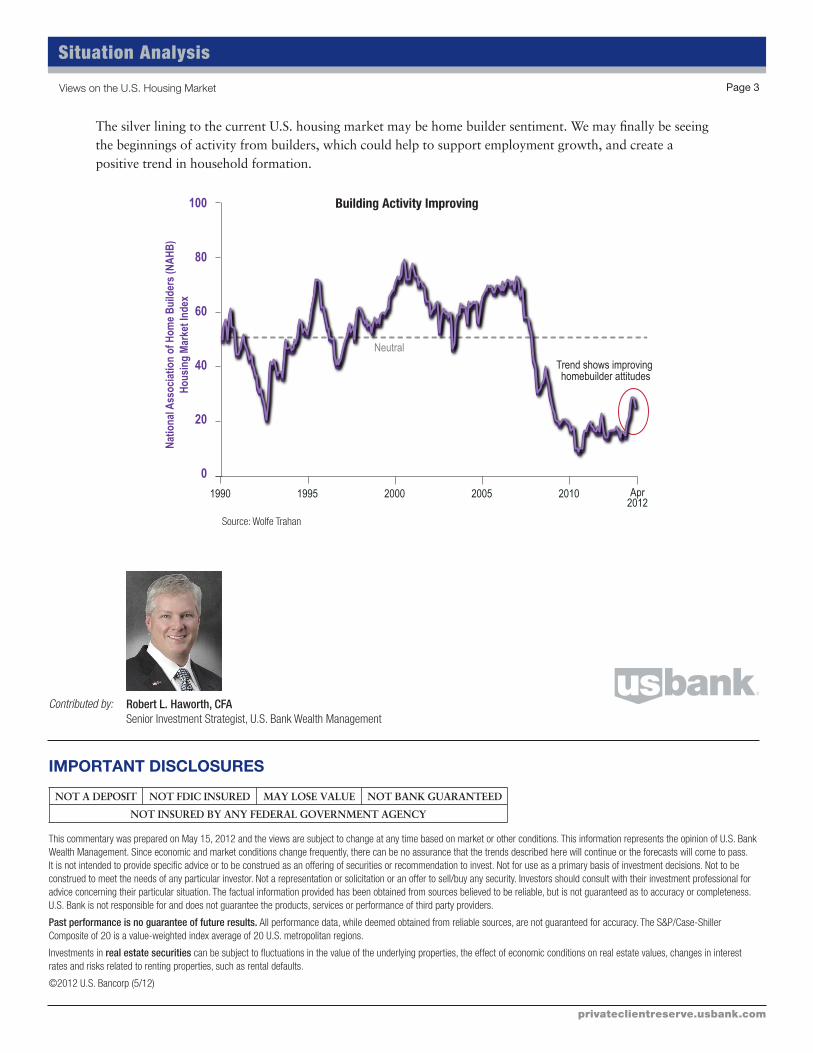

The silver lining to the current U.S. housing market may be home builder sentiment. We may finally be seeing the beginnings of activity from builders, which could help to support employment growth, and create a positive trend in household formation.

Building Activity Improving

IMPORTANT DISCLOSURES

This commentary was prepared on May 15, 2012 and the views are subject to change at any time based on market or other conditions. This information represents the opinion of U.S. Bank Wealth Management. Since economic and market conditions change frequently, there can be no assurance that the trends described here will continue or the forecasts will come to pass. It is not intended to provide specific advice or to be construed as an offering of securities or recommendation to invest. Not for use as a primary basis of investment decisions. Not to be construed to meet the needs of any particular investor. Not a representation or solicitation or an offer to sell/buy any security. Investors should consult with their investment professional for advice concerning their particular situation. The factual information provided has been obtained from sources believed to be reliable, but is not guaranteed as to accuracy or completeness. U.S. Bank is not responsible for and does not guarantee the products, services or performance of third party providers.

Past performance is no guarantee of future results. All performance data, while deemed obtained from reliable sources, are not guaranteed for accuracy. The S&P/Case-Shiller Composite of 20 is a value-weighted index average of 20 U.S. metropolitan regions.

Investments in real estate securities can be subject to fluctuations in the value of the underlying properties, the effect of economic conditions on real estate values, changes in interest rates and risks related to renting properties, such as rental defaults.

©2012 U.S. Bancorp (5/12)

privateclientreserve.usbank.com

Contributed by: Robert L. Haworth, CFASenior Investment Strategist, U.S. Bank Wealth Management

100

80

60

40

20

0

1990 1995 2000 2005 2010

Neutral

Trend shows improving homebuilder attitudes

Apr2012

Nat

iona

l Ass

ocia

tion

of H

ome

Bui

lder

s (N

AH

B)

Hou

sing

Mar

ket I

ndex

Source: Wolfe Trahan

Related Documents