A PROJECT REPORT ON “VICTORY PORTFOLIO LIMITED” {Investor Behavior on Stock Market} A Project Report Submitted in the partial fulfillment of the requirement for the award of the Degree of Bachelor of Business Administration Submitted By: Under the Guidance Rahul garg Rupali mam ___________________ BBA-5th Semester BHARATI VIDYAPEETH UNIVERSITY 1

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

8/8/2019 Victory Portfolio Ltd 3

http://slidepdf.com/reader/full/victory-portfolio-ltd-3 1/85

A

PROJECT REPORT

ON

“VICTORY PORTFOLIO LIMITED”{Investor Behavior on Stock Market}

A Project Report

Submitted in the partial fulfillment of the requirement for the award of the

Degree of Bachelor of Business Administration

Submitted By: Under the Guidance

Rahul garg Rupali mam

___________________

BBA-5th Semester

BHARATI VIDYAPEETH UNIVERSITY

1

8/8/2019 Victory Portfolio Ltd 3

http://slidepdf.com/reader/full/victory-portfolio-ltd-3 2/85

8/8/2019 Victory Portfolio Ltd 3

http://slidepdf.com/reader/full/victory-portfolio-ltd-3 3/85

PREFACE

A brief cursory look of any economy will definitely and easily point out the significantrole played by the financial system. As a matter of fact, the financial works as it were or

something sort of nucleus. It is a trust that pools the savings, which are then invested in

capital market instruments such as share, debentures and other securities. It works in a

distinctively different matter as compared to other saving organization such as banks,

national savings, post offices, non-banking financial companies etc.

Market is full of uncertainty and on the top of that new event is adding up to the fuel.

Take the output trend in infrastructure and industry.

The stock market have bid farewell to badla system and have introduced sophisticated

finance products and other options of investments that are giving right to the holder to

buy or sell units at a predetermined rates.

I have made an attempt to evaluate the performance of mutual funds among various

categories of investors in different plans and schemes, which are distributed by

VICTORIA PORTFOLIO LIMITED AMC.

3

8/8/2019 Victory Portfolio Ltd 3

http://slidepdf.com/reader/full/victory-portfolio-ltd-3 4/85

ACKNOWLEDGEMENT

I would like to take this opportunity to thank ______________, my project guide,Director Dr. S.S.Verenekar, for their continuous guidance and support and

for making me comfortable without which this project would not have

materialized.

I would also like to thank Mr. Nitin Goel, Asst. sales manager, VICTORIA PORTFOLIO

LIMITED Mutual Fund for extending valuable support and providing me vital

information on investment market.

Finally, I would express my gratitude to distributor Mr, A.K.Jain for helping me

throughout my project.

__________________

4

8/8/2019 Victory Portfolio Ltd 3

http://slidepdf.com/reader/full/victory-portfolio-ltd-3 5/85

CONTENTS

PREFACE

ACKNOWLEDGEMENT

CHAPTER -1 1.0 INTRODUCTION

1.1 Overview of Indian Mutual Fund Industry

1.2 Profile of victory portfolio limited1.3 Problems of the Organization

1.4 Competitor’s Information

1.5 SWOT Analysis

CHAPTER –2 2.0 CONCEPTUAL DISCUSSION

2.1 Theoretical backdrop and Literature Review

2.2 Investors behaviour

CHAPTER –3 3.0 OBJECTIVES AND METHODOLOGY

3.1 Significance of the Study

3.2 Managerial Usefulness of the Study

3.3 Objectives

3.4 Scope of the Study

3.5 Methodology

CHAPTER –4 4.0 DATA ANALYSIS AND INTERPRETATIONS

5

8/8/2019 Victory Portfolio Ltd 3

http://slidepdf.com/reader/full/victory-portfolio-ltd-3 6/85

CHAPTER –5 5.0 FINDINGS AND RECOMMENDATIONS

ANNEXURES

Chapter-1

Introduction of report

6

8/8/2019 Victory Portfolio Ltd 3

http://slidepdf.com/reader/full/victory-portfolio-ltd-3 7/85

1.1 Overview

HISTORY OF THE INDIAN MUTUAL FUND INDUSTRY

The mutual fund industry in India started in 1963 with the formation of Unit Trust of

India, at the initiative of the Government of India and Reserve Bank the. The history of

mutual funds in India can be broadly divided into four distinct phases:-

First Phase (1964-87) -Unit Trust of India (UTI) was established on 1963 by an Act of

Parliament. It was set up by the Reserve Bank of India and functioned under the

Regulatory and administrative control of the Reserve Bank of India. In 1978 UTI was de-

linked from the RBI and the Industrial Development Bank of India (IDBI) took over the

regulatory and administrative control in place of RBI. The first scheme launched by UTI

was Unit Scheme 1964. At the end of 1988 UTI had Rs.6,700 crores of assets under

management.

Second Phase (1987-1993)- (Entry of Public Sector Funds) 1987 marked the entry of

non- UTI, public sector mutual funds set up by public sector banks and Life Insurance

Corporation of India (LIC) and General Insurance Corporation of India (GIC). SBI

Mutual Fund was the first non- UTI Mutual Fund established in June 1987 followed by

Canbank Mutual Fund (Dec 87), Punjab National Bank Mutual Fund (Aug 89), Indian

Bank Mutual Fund (Nov 89), Bank of India (Jun 90), Bank of Baroda Mutual Fund (Oct

92). LIC established its mutual fund in June 1989 while GIC had set up its mutual fund in

7

8/8/2019 Victory Portfolio Ltd 3

http://slidepdf.com/reader/full/victory-portfolio-ltd-3 8/85

December 1990. At the end of 1993, the mutual fund industry had assets under

management of Rs.47,004 crores.

Third Phase (1993-2003)- (Entry of Private Sector Funds ) With the entry of private

sector funds in 1993, a new era started in the Indian mutual fund industry, giving the

Indian investors a wider choice of fund families. Also, 1993 was the year in which the

first Mutual Fund Regulations came into being, under which all mutual funds, except UTI

were to be registered and governed. The erstwhile Kothari Pioneer (now merged with

Franklin Templeton) was the first private sector mutual fund registered in July 1993. The

1993 SEBI (Mutual Fund) Regulations were substituted by a more comprehensive and

revised Mutual Fund Regulations in 1996. The industry now functions under the SEBI(Mutual Fund) Regulations 1996. The number of mutual fund houses went on increasing,

with many foreign mutual funds setting up funds in India and also the industry has

witnessed several mergers and acquisitions. As at the end of January 2003, there were 33

mutual funds with total assets of Rs. 1,21,805 crores. The Unit Trust of India with

Rs.44,541 crores of assets under management was way ahead of other mutual funds.

Fourth Phase (since February 2003)- In February 2003, following the repeal of theUnit Trust of India Act 1963 UTI was bifurcated into two separate entities. One is the

Specified Undertaking of the Unit Trust of India with assets under management of

Rs.29,835 crores as at the end of January 2003, representing broadly, the assets of US 64

scheme, assured return and certain other schemes. The Specified Undertaking of Unit

Trust of India, functioning under an administrator and under the rules framed by

Government of India and does not come under the purview of the Mutual Fund

Regulations. The second is the UTI Mutual Fund Ltd, sponsored by SBI, PNB, BOB and

LIC. It is registered with SEBI and functions under the Mutual Fund Regulations. With

the bifurcation of the erstwhile UTI which had in March 2000 more than Rs.76,000

crores of assets under management and with the setting up of a UTI Mutual Fund,

conforming to the SEBI Mutual Fund Regulations, and with recent mergers taking place

among different private sector funds, the mutual fund industry has entered its current

8

8/8/2019 Victory Portfolio Ltd 3

http://slidepdf.com/reader/full/victory-portfolio-ltd-3 9/85

phase of consolidation and growth. As at the end of September, 2004, there were 29

funds, which manage assets of Rs.153108 crores under 421 schemes.

1.2 PROFILE

INDUSTRY PROFILE

Structure of the Indian mutual fund industry

The Indian mutual fund industry is dominated by the Unit Trust of India which has a total

corpus of Rs700bn collected from more than 20 million investors. The UTI has many

funds/schemes in all categories ie equity, balanced, income etc with some being open-

ended and some being closed-ended. The Unit Scheme 1964 commonly referred to as US

64, which is a balanced fund, is the biggest scheme with a corpus of about Rs200bn. UTI

was floated by financial institutions and is governed by a special act of Parliament. Most

of its investors believe that the UTI is government owned and controlled, which, while

legally incorrect, is true for all practical purposes.

The second largest category of mutual funds are the ones floated by nationalized banks.

Canbank Asset Management floated by Canara Bank and SBI Funds Management floated

by the State Bank of India are the largest of these. GIC AMC floated by General

Insurance Corporation and Jeevan Bima Sahayog AMC floated by the LIC are some of

the other prominent ones. The aggregate corpus of funds managed by this category of

AMCs is about Rs150bn.

The third largest category of mutual funds are the ones floated by the private sector and

by foreign asset management companies. The largest of these are Prudential ICICI AMC

and Birla Sun Life AMC. The aggregate corpus of assets managed by this category of

AMCs is in excess of Rs250bn.

9

8/8/2019 Victory Portfolio Ltd 3

http://slidepdf.com/reader/full/victory-portfolio-ltd-3 10/85

VICTORY PORTFOLIO LIMITED GROUP PROFILE

Victory portfolio limited is one of India’s leading Mutual Funds agency with Average AssetsUnder Management (AAUM) of Rs. 10,451 thousand and an investor count of over 720.

Victory portfolio is one of the fastest growing mutual funds in the country. Victory portfoliooffers investors a well-rounded portfolio of products to meet varying investor requirements.Victory portfolio limited constantly endeavors to launch innovative products and customer service initiatives to increase value to investors.Victory portfolio limited is owned by Promod goel who is the director of the company. it is listedin NSE in 1980. Its SEBI REGISTRATION NO.= INB230781930

Vision of the group is that to makemoney for all the clients and to reduce

risk.Mission is to make victory port foliothe largest mutual fund in the world

10

8/8/2019 Victory Portfolio Ltd 3

http://slidepdf.com/reader/full/victory-portfolio-ltd-3 11/85

1.3 Problems of the organization

1. Less Number of employees in the organization to cater market needs.2. Low promotional activities.

3. Highly dependent on distributors and brokers for business.

4. Increasing competition.

5. Communication gap between the distributor/broker and organization.

11

8/8/2019 Victory Portfolio Ltd 3

http://slidepdf.com/reader/full/victory-portfolio-ltd-3 12/85

1.4 Competitor’s Information

Some of the AMCs operating currently are:

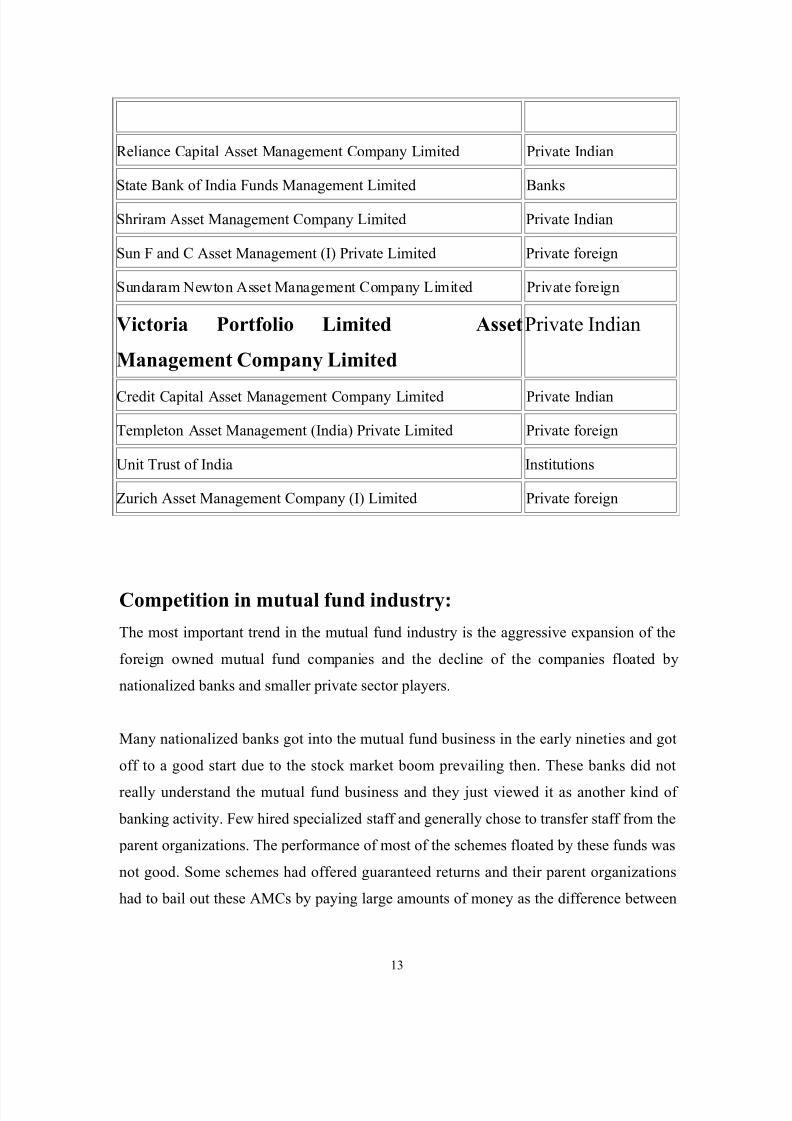

Name of the AMC Nature of ownership

Alliance Capital Asset Management (I) Private Limited Private foreign

Birla Sun Life Asset Management Company Limited Private Indian

Bank of Baroda Asset Management Company Limited Banks

Bank of India Asset Management Company Limited Banks

Canbank Investment Management Services Limited Banks

Cholamandalam Cazenove Asset Management Company Limited Private foreign

Dundee Asset Management Company Limited Private foreign

DSP Merrill Lynch Asset Management Company Limited Private foreign

Escorts Asset Management Limited Private Indian

First India Asset Management Limited Private Indian

GIC Asset Management Company Limited Institutions

IDBI Investment Management Company Limited Institutions

Indfund Management Limited Banks

ING Investment Asset Management Company Private Limited Private foreign

J M Capital Management Limited Private Indian

Jardine Fleming (I) Asset Management Limited Private foreign

Kotak Mahindra Asset Management Company Limited Private Indian

Kothari Pioneer Asset Management Company Limited Private Indian

Jeevan Bima Sahayog Asset Management Company Limited Institutions

Morgan Stanley Asset Management Company Private Limited Private foreign

Punjab National Bank Asset Management Company Limited Banks

12

8/8/2019 Victory Portfolio Ltd 3

http://slidepdf.com/reader/full/victory-portfolio-ltd-3 13/85

Reliance Capital Asset Management Company Limited Private Indian

State Bank of India Funds Management Limited Banks

Shriram Asset Management Company Limited Private Indian

Sun F and C Asset Management (I) Private Limited Private foreign

Sundaram Newton Asset Management Company Limited Private foreign

Victoria Portfolio Limited Asset

Management Company Limited

Private Indian

Credit Capital Asset Management Company Limited Private Indian

Templeton Asset Management (India) Private Limited Private foreign

Unit Trust of India Institutions

Zurich Asset Management Company (I) Limited Private foreign

Competition in mutual fund industry:

The most important trend in the mutual fund industry is the aggressive expansion of the

foreign owned mutual fund companies and the decline of the companies floated by

nationalized banks and smaller private sector players.

Many nationalized banks got into the mutual fund business in the early nineties and got

off to a good start due to the stock market boom prevailing then. These banks did not

really understand the mutual fund business and they just viewed it as another kind of

banking activity. Few hired specialized staff and generally chose to transfer staff from the

parent organizations. The performance of most of the schemes floated by these funds was

not good. Some schemes had offered guaranteed returns and their parent organizations

had to bail out these AMCs by paying large amounts of money as the difference between

13

8/8/2019 Victory Portfolio Ltd 3

http://slidepdf.com/reader/full/victory-portfolio-ltd-3 14/85

the guaranteed and actual returns. The service levels were also very bad. Most of these

AMCs have not been able to retain staff, float new schemes etc. and it is doubtful

whether, barring a few exceptions, they have serious plans of continuing the activity in a

major way.

The experience of some of the AMCs floated by private sector Indian companies was also

very similar. They quickly realized that the AMC business is a business, which makes

money in the long term and requires deep-pocketed support in the intermediate years.

Some have sold out to foreign owned companies, some have merged with others and

there is general restructuring going on.

The foreign owned companies have deep pockets and have come in here with the

expectation of a long haul. They can be credited with introducing many new practices

such as new product innovation, sharp improvement in service standards and disclosure,

usage of technology, broker education and support etc. In fact, they have forced the

industry to upgrade itself and service levels of organizations like UTI have improved

dramatically in the last few years in response to the competition provided by these.

1.5 SWOT ANALYSIS

Strengths

Premiere market image

Largest distributor of Mutual Fund

Largest corpus of Mutual Fund

Wide range if investment products

Committed staff

Satisfied customer

Wide range of portfolio in investment

14

8/8/2019 Victory Portfolio Ltd 3

http://slidepdf.com/reader/full/victory-portfolio-ltd-3 15/85

Weakness

Declining customer service

Low awareness and usage levels of a few schemes can disappoint the investors

Limited investment centers

Slow processing

Lack of skilled consellor of investment products

Due to wide range of products, lack of focus towards any particular product

Threats

Increasing number in new Mutual Fund floaters

Highly competitive market in distribution

Stagnant urban demand

Highly volatile market

Unawareness of investors can spoil the image of AMC

Low commission to investors like agents as well as individuals can loose their

customer base.

Opportunity

By providing all investment products at one stop can keep them on top on

distribution

By giving more commission to investors, customer base can be increased at other

distributors

Educate the investors about the portfolio management se as to increase their database of investors

Victoria Portfolio Limited can open new investment centers in small cities or

new upcoming economic zones.

15

8/8/2019 Victory Portfolio Ltd 3

http://slidepdf.com/reader/full/victory-portfolio-ltd-3 16/85

Chapter 2

Conceptual

discussion16

8/8/2019 Victory Portfolio Ltd 3

http://slidepdf.com/reader/full/victory-portfolio-ltd-3 17/85

CHAPTER 2: conceptual discussion

INTRODUCTION

A Mutual Fund is a trust that pools the savings of a number of investors who share a

common financial goal. The money thus collected is invested by the fund manager in

different types of securities depending upon the objective of the scheme. These could

range from shares to debentures to money market instruments. The income earned

through these investments and the capital appreciation realized by the scheme is shared

by its unit holders in proportion to the number of units owned by them (pro rata). Thus a

Mutual Fund is the most suitable investment for the common man as it offers an

opportunity to invest in a diversified, professionally managed portfolio at a relatively low

17

8/8/2019 Victory Portfolio Ltd 3

http://slidepdf.com/reader/full/victory-portfolio-ltd-3 18/85

cost. Anybody with an investible surplus of as little as a few thousand rupees can invest

in Mutual Funds. Each Mutual Fund scheme has a defined investment objective and

strategy.

A mutual fund is the ideal investment vehicle for today’s complex and modern financial

scenario. Markets for equity shares, bonds and other fixed income instruments, real

estate, derivatives and other assets have become mature and information driven. Price

changes in these assets are driven by global events occurring in faraway places. A typical

individual is unlikely to have the knowledge, skills, inclination and time to keep track of

events, understand their implications and act speedily. An individual also finds it difficult

to keep track of ownership of his assets, investments, brokerage dues and bank

transactions etc.

A mutual fund is the answer to all these situations. It appoints professionally qualified

and experienced staff that manages each of these functions on a full time basis. The large

pool of money collected in the fund allows it to hire such staff at a very low cost to each

investor. In effect, the mutual fund vehicle exploits economies of scale in all three areas -

research, investments and transaction processing. While the concept of individuals

coming together to invest money collectively is not new, the mutual fund in its present

form is a 20th

century phenomenon. In fact, mutual funds gained popularity only after theSecond World War. Globally, there are thousands of firms offering tens of thousands of

mutual funds with different investment objectives. Today, mutual funds collectively

manage almost as much as or more money as compared to banks.

A draft offer document is to be prepared at the time of launching the fund. Typically, it

pre specifies the investment objectives of the fund, the risk associated, the costs involved

in the process and the broad rules for entry into and exit from the fund and other areas of

operation. In India, as in most countries, these sponsors need approval from a regulator,SEBI (Securities exchange Board of India) in our case. SEBI looks at track records of the

sponsor and its financial strength in granting approval to the fund for commencing

operations.

18

8/8/2019 Victory Portfolio Ltd 3

http://slidepdf.com/reader/full/victory-portfolio-ltd-3 19/85

A sponsor then hires an asset management company to invest the funds according to the

investment objective. It also hires another entity to be the custodian of the assets of the

fund and perhaps a third one to handle registry work for the unit holders (subscribers) of

the fund.

In the Indian context, the sponsors promote the Asset Management Company also, in

which it holds a majority stake. E.g. VICTORIA PORTFOLIO LIMITED Sons Ltd. and

VICTORIA PORTFOLIO LIMITED Investment Corporation Ltd. are the sponsors of

the VICTORIA PORTFOLIO LIMITED Asset Management Company Ltd. which has

floated different mutual funds schemes and also acts as an asset manager for the funds

collected under the schemes.

Recent trends in mutual fund industry

The most important trend in the mutual fund industry is the aggressive expansion of the

foreign owned mutual fund companies and the decline of the companies floated by

nationalized banks and smaller private sector players.

Many nationalized banks got into the mutual fund business in the early nineties and got

off to a good start due to the stock market boom prevailing then. These banks did not

really understand the mutual fund business and they just viewed it as another kind of banking activity. Few hired specialized staff and generally chose to transfer staff from the

parent organizations. The performance of most of the schemes floated by these funds was

not good. Some schemes had offered guaranteed returns and their parent organizations

had to bail out these AMCs by paying large amounts of money as the difference between

the guaranteed and actual returns. The service levels were also very bad. Most of these

AMCs have not been able to retain staff, float new schemes etc. and it is doubtful

whether, barring a few exceptions, they have serious plans of continuing the activity in a

major way.

The experience of some of the AMCs floated by private sector Indian companies was also

very similar. They quickly realized that the AMC business is a business, which makes

money in the long term and requires deep-pocketed support in the intermediate years.

19

8/8/2019 Victory Portfolio Ltd 3

http://slidepdf.com/reader/full/victory-portfolio-ltd-3 20/85

Some have sold out to foreign owned companies, some have merged with others and

there is general restructuring going on.

The foreign owned companies have deep pockets and have come in here with the

expectation of a long haul. They can be credited with introducing many new practices

such as new product innovation, sharp improvement in service standards and disclosure,

usage of technology, broker education and support etc. In fact, they have forced the

industry to upgrade itself and service levels of organizations like UTI have improved

dramatically in the last few years in response to the competition provided by these.

HOW IS A MUTUAL FUND SET UP?

⇒ Is set up in the form of a trust, which has sponsor, trustees, asset Management

Company (AMC) and custodian.⇒ The trust is established by a sponsor or more than one sponsor who is like a promoter

of a company.

⇒ The trustees of the mutual fund hold its property for the benefit of the unit holders.

⇒ Asset Management Company (AMC) approved by SEBI manages the funds by making

investments in various types of securities.

⇒ Custodian, who is registered with SEBI, holds the securities of various schemes of the

fund in its custody.

SPONSOR

What a promoter to a company, a sponsor is to a mutual fund. The sponsor initiates the

idea to set up a mutual fund .It could be a financial services company, a bank or a

financial institution. It could be Indian or foreign. It could do it alone or through a joint

venture. In order to run a mutual fund in India, the sponsor has to obtain a license from

SEBI. For this, it has to satisfy certain conditions, such as on capital and profits, track

record(at least five years in financial services),default-free dealings and a general

reputation for fairness.

Like the company promoter, the sponsor takes big-picture decisions related to the mutual

fund, leaving money management and other such nitty-gritty to the other constituents,

whom it appoints. The sponsor should inspire confidence in you as a money manager

20

8/8/2019 Victory Portfolio Ltd 3

http://slidepdf.com/reader/full/victory-portfolio-ltd-3 21/85

and, preferably, be profitable. Financial muscle, so long as it is complemented by good

fund management, helps, as money is then not an impediment for the mutual fund-it can

hire the best talent, invest in technology, and continuously offer high service standards to

investors.

In the days of assured return schemes, sponsors also had to fulfill return promises made

to unit holders. This sometimes meant meeting shortfalls from their own pockets, as the

government did for UTI. Now that assured return schemes are passé, such bailouts wont

be required. All things considered, choose sponsors who are good money managers, who

have a reputation for fair business practices, and who have deep pockets.

ASSET MANAGEMENT COMPANY (AMC)

An AMC is the legal entity formed by the sponsor to run a mutual fund. It’s the AMC

that employs fund managers and analysts, and other personnel. It’s the AMC that handles

all operational matters of a mutual fund-from launching schemes to managing them to

interacting with investors.

The people in the AMC who should matter the most to you are those who take investment

decisions. There is the head of the fund house, generally referred to as the chief executive

officer (CEO). Under him comes the chief investment officer (CIO),who shapes the

fund’s investment philosophy, and fund managers, who manages its schemes. They areassisted by a team of analysts, who track markets, sectors and companies.

Although, these people are employed by the AMC, its you, the unit holder, who pays

their salaries, partly or wholly. Each scheme pays the AMC an annual ‘fund management

fee’, which is linked to the scheme size and results in a corresponding drop in your

return. If a scheme’s corpus is up to Rs.100 crore it pays 1.25% of its corpus a year; on

over Rs.100 crore, the fee is 1% of corpus. So, if a fund house has two schemes, with a

corpus of Rs.100 crore and Rs.200 crore respectively, the AMC will earn Rs.3.25

crore(1.25+2) as fund management fee that year.

If an AMC’s expenses for the year exceed what it earns as fund management fee from its

schemes, the balance has to be met by the sponsor. Again, financial strength comes into

play: a cash-rich sponsor can easily pump in money to meet short falls, while a sponsor

21

8/8/2019 Victory Portfolio Ltd 3

http://slidepdf.com/reader/full/victory-portfolio-ltd-3 22/85

8/8/2019 Victory Portfolio Ltd 3

http://slidepdf.com/reader/full/victory-portfolio-ltd-3 23/85

Registrars, also known as transfer agents, handle all investor-related services.This

includes issuing and redeeming units, sending fact sheets and annual reports. Some fund

houses handle such functions in-house. Others outsource it to registrars;Karvy and

CAMS are the more popular ones.It doesn’t really matter which model your mutual fund

opt for, as long as it is prompt and efficient in servicing you. Most mutual funds, in

addition to registrars, also have investor service centers of their own in some cities.

Types of Mutual Funds

Mutual fund schemes may be classified on the basis of its structure and its investment

objective.

By Structure:

Open-ended Funds

An open-end fund is one that is available for subscription all through the year. These do

not have a fixed maturity. Investors can conveniently buy and sell units at Net Asset

Value ("NAV") related prices. The key feature of open-end schemes is liquidity.

Closed-ended Funds

A closed-end fund has a stipulated maturity period which generally ranging from 3 to 15

years. The fund is open for subscription only during a specified period. Investors can

invest in the scheme at the time of the initial public issue and thereafter they can buy or

sell the units of the scheme on the stock exchanges where they are listed. In order to

provide an exit route to the investors, some close-ended funds give an option of selling

back the units to the Mutual Fund through periodic repurchase at NAV related prices.

23

8/8/2019 Victory Portfolio Ltd 3

http://slidepdf.com/reader/full/victory-portfolio-ltd-3 24/85

SEBI Regulations stipulate that at least one of the two exit routes is provided to the

investor.

Interval Funds

Interval funds combine the features of open-ended and close-ended schemes. They are

open for sale or redemption during pre-determined intervals at NAV related prices.

By Investment Objective:

Schemes can be classified by way of their stated investment objective such as Growth

Fund, Income Fund, Balanced Fund etc.

Growth Funds

The aim of growth funds is to provide capital appreciation over the medium to long-

term. Such schemes normally invest a majority of their corpus in equities. It has been

proven that returns from stocks, have outperformed most other kind of investments held

over the long term. Growth schemes are ideal for investors having a long-term outlook

seeking growth over a period of time.

Income Funds

The aim of income funds is to provide regular and steady income to investors. Such

schemes generally invest in fixed income securities such as bonds, corporate debentures

and Government securities. Income Funds are ideal for capital stability and regular

income.

Balanced Funds

The aim of balanced funds is to provide both growth and regular income. Such schemes

periodically distribute a part of their earning and invest both in equities and fixed income

securities in the proportion indicated in their offer documents. In a rising stock market,

the NAV of these schemes may not normally keep pace, or fall equally when the market

falls. These are ideal for investors looking for a combination of income and moderate

growth.

24

8/8/2019 Victory Portfolio Ltd 3

http://slidepdf.com/reader/full/victory-portfolio-ltd-3 25/85

Money Market Funds

The aim of money market funds is to provide easy liquidity, preservation of capital and

moderate income. These schemes generally invest in safer short-term instruments such as

treasury bills, certificates of deposit, commercial paper and inter-bank call money.

Returns on these schemes may fluctuate depending upon the interest rates prevailing in

the market. These are ideal for Corporate and individual investors as a means to park

their surplus funds for short periods.

Load Funds

A Load Fund is one that charges a commission for entry or exit. That is, each time you

buy or sell units in the fund, a commission will be payable. Typically entry and exit loadsrange from 1% to 2%. It could be worth paying the load, if the fund has a good

performance history.

No-Load Funds

A No-Load Fund is one that does not charge a commission for entry or exit. That is, no

commission is payable on purchase or sale of units in the fund. The advantage of a no

load fund is that the entire corpus is put to work.

Other Schemes:

Tax Saving Schemes

These schemes offer tax rebates to the investors under specific provisions of the Indian

Income Tax laws as the Government offers tax incentives for investment in specified

avenues. Investments made in Equity Linked Savings Schemes (ELSS) and Pension

Schemes are allowed as deduction u/s 88 of the Income Tax Act, 1961. The Act also

25

8/8/2019 Victory Portfolio Ltd 3

http://slidepdf.com/reader/full/victory-portfolio-ltd-3 26/85

provides opportunities to investors to save capital gains u/s 54EA and 54EB by investing

in Mutual Funds, provided the capital asset has been sold prior to April 1, 2000 and the

amount is invested before September 30, 2000.

Special Schemes

• Industry Specific Schemes

Industry Specific Schemes invest only in the industries specified in the offer document.

The investment of these funds is limited to specific industries like InfoTech, FMCG, and

Pharmaceuticals etc.

• Index Schemes

Index Funds attempt to replicate the performance of a particular index such as the BSE

Sensex or the NSE 50.NAV’s of such schemes rise or fall in accordance with the rise or

fall in the index,though not exactly by the same percentage due to some factors known as

“tracking error” in technical terms.

• Sectoral Schemes

These schemes restrict their investing to one or more pre-defined sectors, e.g. technology

sector. Depending upon the performance of select sectors only, these schemes are

inherently more risky than general-purpose schemes.They are suited for informed

investors who wish to take a viewand risk on the concerned sector.

Benefits of Mutual Fund investment

Professional Management

Mutual Funds provide the services of experienced and skilled professionals, backed by a

dedicated investment research team that analyses the performance and prospects of

companies and selects suitable investments to achieve the objectives of the scheme.

26

8/8/2019 Victory Portfolio Ltd 3

http://slidepdf.com/reader/full/victory-portfolio-ltd-3 27/85

8/8/2019 Victory Portfolio Ltd 3

http://slidepdf.com/reader/full/victory-portfolio-ltd-3 28/85

Flexibility

Through features such as regular investment plans, regular withdrawal plans and dividend

reinvestment plans, you can systematically invest or withdraw funds according to your

needs and convenience.

Affordability

Investors individually may lack sufficient funds to invest in high-grade stocks. A mutual

fund because of its large corpus allows even a small investor to take the benefit of its

investment strategy.

Choice of Schemes

Mutual Funds offer a family of schemes to suit your varying needs over a lifetime.

Well Regulated

All Mutual Funds are registered with SEBI and they function within the provisions of

strict regulations designed to protect the interests of investors. The operations of Mutual

Funds are regularly monitored by SEBI.

Net Asset Value (NAV)The net asset value of the fund is the cumulative market value of the assets fund net of its

liabilities. In other words, if the fund is dissolved or liquidated, by selling off all the

assets in the fund, this is the amount that the shareholders would collectively own. This

gives rise to the concept of net asset value per unit, which is the value, represented by the

ownership of one unit in the fund. It is calculated simply by dividing the net asset value

of the fund by the number of units. However, most people refer loosely to the NAV per

unit as NAV, ignoring the "per unit". We also abide by the same convention.

Calculation of NAV

The most important part of the calculation is the valuation of the assets owned by the

fund. Once it is calculated, the NAV is simply the net value of assets divided by the

28

8/8/2019 Victory Portfolio Ltd 3

http://slidepdf.com/reader/full/victory-portfolio-ltd-3 29/85

number of units outstanding. The detailed methodology for the calculation of the asset

value is given below.

Asset value is equal to

Sum of market value of shares/debentures

+ Liquid assets/cash held, if any

+ Dividends/interest accrued

Amount due on unpaid assets

Expenses accrued but not paid

Details on the above items

For liquid shares/debentures, valuation is done on the basis of the last or closing market

price on the principal exchange where the security is traded

For illiquid and unlisted and/or thinly traded shares/debentures, the value has to be

estimated. For shares, this could be the book value per share or an estimated market priceif suitable benchmarks are available. For debentures and bonds, value is estimated on the

basis of yields of comparable liquid securities after adjusting for illiquidity. The value of

fixed interest bearing securities moves in a direction opposite to interest rate changes

Valuation of debentures and bonds is a big problem since most of them are unlisted and

thinly traded. This gives considerable leeway to the AMCs on valuation and some of the

AMCs are believed to take advantage of this and adopt flexible valuation policies

depending on the situation.

Interest is payable on debentures/bonds on a periodic basis say every 6 months. But, with

every passing day, interest is said to be accrued, at the daily interest rate, which is

calculated by dividing the periodic interest payment with the number of days in each

period. Thus, accrued interest on a particular day is equal to the daily interest rate

multiplied by the number of days since the last interest payment date.

29

8/8/2019 Victory Portfolio Ltd 3

http://slidepdf.com/reader/full/victory-portfolio-ltd-3 30/85

Usually, dividends are proposed at the time of the Annual General meeting and become

due on the record date. There is a gap between the dates on which it becomes due and the

actual payment date. In the intermediate period, it is deemed to be "accrued".

Expenses including management fees, custody charges etc. are calculated on a daily

basis.

Mutual Funds in India (1964-2000)

The end of millennium marks 36 years of existence of mutual funds in this country. The

ride through these 36 years is not been smooth. Investor opinion is still divided. While

some are for mutual funds others are against it.

UTI commenced its operations from July 1964 .The impetus for establishing a formal

institution came from the desire to increase the propensity of the middle and lower groups

to save and to invest. UTI came into existence during a period marked by great political

and economic uncertainty in India. With war on the borders and economic turmoil that

depressed the financial market, entrepreneurs were hesitant to enter capital market.

The already existing companies found it difficult to raise fresh capital, as investors did

not respond adequately to new issues. Earnest efforts were required to canalize savings of

the community into productive uses in order to speed up the process of industrial growth.The then Finance Minister, T.T. Krishnamachari set up the idea of a unit trust that would

be "open to any person or institution to purchase the units offered by the trust. However,

this institution as we see it, is intended to cater to the needs of individual investors, and

even among them as far as possible, to those whose means are small."

His ideas took the form of the Unit Trust of India, an intermediary that would help fulfill

the twin objectives of mobilizing retail savings and investing those savings in the capital

market and passing on the benefits so accrued to the small investors.

UTI commenced its operations from July 1964 "with a view to encouraging savings and

investment and participation in the income, profits and gains accruing to the

Corporation from the acquisition, holding, management and disposal of securities."

Different provisions of the UTI Act laid down the structure of management, scope of

30

8/8/2019 Victory Portfolio Ltd 3

http://slidepdf.com/reader/full/victory-portfolio-ltd-3 31/85

business, powers and functions of the Trust as well as accounting, disclosures and

regulatory requirements for the Trust.

One thing is certain – the fund industry is here to stay. The industry was one-entity show

till 1986 when the UTI monopoly was broken when SBI and Canbank mutual fund

entered the arena. This was followed by the entry of others like BOI, LIC, GIC, etc.

sponsored by public sector banks. Starting with an asset base of Rs0.25bn in 1964 the

industry has grown at a compounded average growth rate of 26.34% to its current size of

Rs1130bn.

The period 1986-1993 can be termed as the period of public sector mutual funds (PMFs).

From one player in 1985 the number increased to 8 in 1993. The party did not last long.

When the private sector made its debut in 1993-94, the stock market was booming.

The opening up of the asset management business to private sector in 1993 saw

international players like Morgan Stanley, Jardine Fleming, JP Morgan, George Soros

and Capital International along with the host of domestic players join the party. But for

the equity funds, the period of 1994-96 was one of the worst in the history of Indian

Mutual Funds.

1999-2000 Year of the funds

Mutual funds have been around for a long period of time to be precise for 36 yrs but the

year 1999 saw immense future potential and developments in this sector. This year

signaled the year of resurgence of mutual funds and the regaining of investor confidence

in these MF’s. This time around all the participants are involved in the revival of the

funds from the AMC’s, the unit holders, the other related parties. However the sole factor

that gave lifr to the revival of the funds was the Union Budget. The budget brought about

a large number of changes in one stroke. An insight of the Union Budget on mutual fundstaxation benefits is provided later.

It provided centrestage to the mutual funds, made them more attractive and provides

acceptability among the investors. The Union Budget exempted mutual fund dividend

given out by equity-oriented schemes from tax, both at the hands of the investor as well

31

8/8/2019 Victory Portfolio Ltd 3

http://slidepdf.com/reader/full/victory-portfolio-ltd-3 32/85

as the mutual fund. No longer were the mutual funds interested in selling the concept of

mutual funds they wanted to talk business which would mean to increase asset base, and

to get asset base and investor base they had to be fully armed with a whole lot of schemes

for every investor .So new schemes for new IPO’s were inevitable. The quest to attract

investors extended beyond just new schemes. The funds started to regulate themselves

and were all out on winning the trust and confidence of the investors under the aegis of

the Association of Mutual Funds of India (AMFI)

One cam say that the industry is moving from infancy to adolescence, the industry is

maturing and the investors and funds are frankly and openly discussing difficulties

opportunities and compulsions.

Future Scenario

The asset base will continue to grow at an annual rate of about 30 to 35 % over the next

few years as investor’s shift their assets from banks and other traditional avenues. Some

of the older public and private sector players will either close shop or be taken over.

Out of ten public sector players five will sell out, close down or merge with stronger

players in three to four years. In the private sector this trend has already started with two

mergers and one takeover. Here too some of them will down their shutters in the near

future to come.

But this does not mean there is no room for other players. The market will witness a

flurry of new players entering the arena. There will be a large number of offers from

various asset management companies in the time to come. Some big names like Fidelity,

Principal, Old Mutual etc. are looking at Indian market seriously. One important reason

for it is that most major players already have presence here and hence these big names

would hardly like to get left behind.

The mutual fund industry is awaiting the introduction of derivatives in India as this would

enable it to hedge its risk and this in turn would be reflected in it’s Net Asset Value

(NAV).

32

8/8/2019 Victory Portfolio Ltd 3

http://slidepdf.com/reader/full/victory-portfolio-ltd-3 33/85

SEBI is working out the norms for enabling the existing mutual fund schemes to trade in

derivatives. Importantly, many market players have called on the Regulator to initiate the

process immediately, so that the mutual funds can implement the changes that are

required to trade in Derivatives.

Banks Vs Mutual Funds

Mutual funds are now also competing with commercial banks in the race for retail

investor’s savings and corporate float money. The power shift towards mutual funds has

become obvious. The coming few years will show that the traditional saving avenues are

losing out in the current scenario. Many investors are realizing that investments insavings accounts are as good as locking up their deposits in a closet. The fund

mobilization trend by mutual funds indicates that money is going to mutual funds in a big

way.

India is at the first stage of a revolution that has already peaked in the U.S. The U.S.

boasts of an Asset base that is much higher than its bank deposits. In India, mutual fund

assets are not even 10% of the bank deposits, but this trend is beginning to change.

This is forcing a large number of banks to adopt the concept of narrow banking wherein

the deposits are kept in Gilts and some other assets which improves liquidity and reduces

risk. The basic fact lies that banks cannot be ignored and they will not close down

completely. Their role as intermediaries cannot be ignored. It is just that Mutual Funds

are going to change the way banks do business in the future.

BANKS MUTUAL FUNDS

Returns Low Better

33

8/8/2019 Victory Portfolio Ltd 3

http://slidepdf.com/reader/full/victory-portfolio-ltd-3 34/85

8/8/2019 Victory Portfolio Ltd 3

http://slidepdf.com/reader/full/victory-portfolio-ltd-3 35/85

about when they compare products. The effective post tax return from many of these

schemes will now be lower. For example, the post tax return on the post office MIP will

be 5.6% with 2.4% payable as tax(which can get higher including surcharge and

cess).The reduction in the competitive rate of return for a number of debt products is a

big opportunity for debt funds.

Gold ETFs is a new opportunity for mutual funds. We can now offer units, whose value

is linked to the gold prices, thus enabling a liquid and market linked manner of investing

in gold. The dividends of the gold fund will be tax exempt, as it comes from mutual fund,

though the government is likely to impose a dividend distribution tax on the product.

According to the World Gold Council, India has the largest hoard of private gold in the

world,90% of it as jewellery, estimated at over 15,000 tons, and the retail buyer in India

represents 25% of annual gold demand in India is from the rural segment. World Gold

Council acknowledges that Indian gold demand is rooted in viewing jewellery as an

investment, and even poor Indians aspire to buy gold with their savings. About Rs.7000

crore is invested in gold by the Indian household every year.

The budget proposes a uniform stamp duty for CPs, except that it mentions uniform

across “issuers” whereas the differential stamp duties also apply for “investors”. While

banks pay a stamp duty ranging from 0.012% to 0.4% (depending on maturity),non-banks

pay 0.06% to 0.5%.If this difference is also removed, mutual funds will be able to buy

CPs directly from issuers, rather than the present practice of banks buying them out and

then re-selling to mutual funds. The lower costs due to lower stamp duties, and the ability

of mutual funds to directly negotiate rates with the issuer, should be positive for short-

term funds that buy CPs.

Asset backed securities market has grown quite significantly in the last few years, and

automobile loan receivables, home loans and such credits have been securitised by banks.

The budget now makes it possible to list and perhaps trade on these assets backed

securities, now that ABS is being included in the list of securities under the SCRA. That

in itself may not create liquidity in the instrument, but is a positive for the ABS markets

that should see higher volumes. Larger investible universe for debt funds, if that happens.

35

8/8/2019 Victory Portfolio Ltd 3

http://slidepdf.com/reader/full/victory-portfolio-ltd-3 36/85

Other minor developments:

⇒ The inclusion of funds under the STT has not happened.

⇒ NRI deposits continue to be tax exempt. The large shift to MFs not expected to

materialize.

⇒ TDS for NRIs on STCG from equity funds, remains unchanged at 33.6%

⇒ Corporates now subject to 10% SC, which increases DDT on debt funds to 22.4%.

Core point:

The budget has ingeniously moved investors away from administered rate products and

debt products, to a wider range of products, most importantly portfolio products like

mutual funds, annuities and pension products. This is sensible because there is no one-

size-fits-all in financial product choice. To have extended this to all tax payers, makes it

possible for many new investors to consider these products, market expansion for players

like us. The relative attractiveness of investment choices has changed and higher

allocation to long-term tax advantaged investment is finally here.

Regulatory Aspects

Schemes of a Mutual Fund

• The asset management company shall launch no scheme unless the trustees

approve such scheme and a copy of the offer document has been filed with the

Board.

• Every mutual fund shall along with the offer document of each scheme pay filing

fees.

• The offer document shall contain disclosures which are adequate in order to

enable the investors to make informed investment decision including the

disclosure on maximum investments proposed to be made by the scheme in the

listed securities of the group companies of the sponsor A close-ended scheme

36

8/8/2019 Victory Portfolio Ltd 3

http://slidepdf.com/reader/full/victory-portfolio-ltd-3 37/85

shall be fully redeemed at the end of the maturity period. "Unless a majority of

the unit holders otherwise decide for its rollover by passing a resolution".

• The mutual fund and asset management company shall be liable to refund the

application money to the applicants,-

(i) If the mutual fund fails to receive the minimum subscription amount

referred to in clause (a) of sub-regulation (1);

(ii) If the moneys received from the applicants for units are in excess of

subscription as referred to in clause (b) of sub-regulation (1).

• The asset management company shall issue to the applicant whose application has

been accepted, unit certificates or a statement of accounts specifying the number

of units allotted to the applicant as soon as possible but not later than six weeks

from the date of closure of the initial subscription list and or from the date of

receipt of the request from the unit holders in any open ended scheme.

Rules Regarding Advertisement:

• The offer document and advertisement materials shall not be misleading or

contain any statement or opinion, which are incorrect or false.

Investment Objectives And Valuation Policies:

• The price at which the units may be subscribed or sold and the price at which such

units may at any time be repurchased by the mutual fund shall be made available

to the investors.

General Obligations:

• Every asset management company for each scheme shall keep and maintain proper books of accounts, records and documents, for each scheme so as to

explain its transactions and to disclose at any point of time the financial position

of each scheme and in particular give a true and fair view of the state of affairs of

the fund and intimate to the Board the place where such books of accounts,

records and documents are maintained.

37

8/8/2019 Victory Portfolio Ltd 3

http://slidepdf.com/reader/full/victory-portfolio-ltd-3 38/85

• The financial year for all the schemes shall end as of March 31 of each year.

Every mutual fund or the asset management company shall prepare in respect of

each financial year an annual report and annual statement of accounts of the

schemes and the fund as specified in Eleventh Schedule.

• Every mutual fund shall have the annual statement of accounts audited by an

auditor who is not in any way associated with the auditor of the asset management

company.

Procedure For Action In Case Of Default:

• On and from the date of the suspension of the certificate or the approval, as the

case may be, the mutual fund, trustees or asset management company, shall cease

to carry on any activity as a mutual fund, trustee or asset management company,

during the period of suspension, and shall be subject to the directions of the Board

with regard to any records, documents, or securities that may be in its custody or

control, relating to its activities as mutual fund, trustees or asset management

company.

Restrictions On Investments:

• A mutual fund scheme shall not invest more than 15% of its NAV in debt

instruments issued by a single issuer, which are rated not below investment grade

by a credit rating agency authorized to carry out such activity under the Act. Such

investment limit may be extended to 20% of the NAV of the scheme with the

prior approval of the Board of Trustees and the Board of asset Management

Company .

• A mutual fund scheme shall not invest more than 10% of its NAV in un-rated

debt instruments issued by a single issuer and the total investment in such

instruments shall not exceed 25% of the NAV of the scheme. All such

investments shall be made with the prior approval of the Board of Trustees and

the Board of asset Management Company.

38

8/8/2019 Victory Portfolio Ltd 3

http://slidepdf.com/reader/full/victory-portfolio-ltd-3 39/85

• No mutual fund under all its schemes should own more than ten per cent of any

company's paid up capital carrying voting rights.

• Such transfers are done at the prevailing market price for quoted instruments on

spot basis.

The securities so transferred shall be in conformity with the investment objective of the

scheme to which such transfer has been made.

• A scheme may invest in another scheme under the same asset management

company or any other mutual fund without charging any fees, provided that

aggregate inter scheme investment made by all schemes under the samemanagement or in schemes under the management of any other asset management

company shall not exceed 5% of the net asset value of the mutual fund.

• The initial issue expenses in respect of any scheme may not exceed six per cent of

the funds raised under that scheme.

• Every mutual fund shall buy and sell securities on the basis of deliveries and shall

in all cases of purchases, take delivery of relative securities and in all cases of

sale, deliver the securities and shall in no case put itself in a position whereby it

has to make short sale or carry forward transaction or engage in badla finance.

• Every mutual fund shall, get the securities purchased or transferred in the name of

the mutual fund on account of the concerned scheme, wherever investments are

intended to be of long-term nature.

• Pending deployment of funds of a scheme in securities in terms of investment

objectives of the scheme a mutual fund can invest the funds of the scheme in shortterm deposits of scheduled commercial banks.

• No mutual fund scheme shall make any investment in;

i. Any unlisted security of an associate or group company of the

sponsor; or

39

8/8/2019 Victory Portfolio Ltd 3

http://slidepdf.com/reader/full/victory-portfolio-ltd-3 40/85

8/8/2019 Victory Portfolio Ltd 3

http://slidepdf.com/reader/full/victory-portfolio-ltd-3 41/85

Real Estate Moderate Moderate High Moderate Low

Mutual

Funds

Moderate High Moderate High High

Investors behavior

Investors behavior means the behavior of investor when he invest in any

kind of stock, commodity and property for an appropriate return is called as

investors behavior.

Things that judge the behavior of investor are:

• Facts

• Theory’s

• Mental status

• Profit and Loss

• Over confidence

41

8/8/2019 Victory Portfolio Ltd 3

http://slidepdf.com/reader/full/victory-portfolio-ltd-3 42/85

1) Facts – A piece of information which has already occurred in the past. It

tells the investor that what will happen in the future by foreseeing the

past events.

2) Theories – A well substantial explanation of some aspect of natural

world.

Example – Recession which occurs after a period of time which gives

opptunity to some and gives threat to others.

3) Mental status – A mental status which guide a person to take risk and

earn profit in the stock market.

4) Profit and loss – it is the main aspect which bring a person to stock

market for taking chances and earn profit but if luck don’t help investor

lands making loss.

5) Over confidence – it is the major enemy of an investor which leads him

ending into trouble and leads to losses.

Conclusion - Behavioral finance certainly reflects some of the attitudesembedded in the investment system. Behaviorists will argue that investorsoften behave irrationally, producing inefficient markets and mispricedsecurities - not to mention opportunities to make money. That may be truefor an instant, but consistently uncovering these inefficiencies is a challenge.Questions remain over whether these behavioral finance theories can be usedto manage your money effectively and economically. (To continue readingon behavioral finance, see taking A Chance On Behavioral Finance .)

That said, investors can be their own worst enemies. Trying to out-guess themarket doesn't pay off over the long term. In fact, it often results in quirky,irrational behavior, not to mention a dent in your wealth. Implementing astrategy that is well thought out and sticking to it may help you avoid manyof these common investing mistakes .

42

8/8/2019 Victory Portfolio Ltd 3

http://slidepdf.com/reader/full/victory-portfolio-ltd-3 43/85

Chapter 3

ResearchMethodology

43

8/8/2019 Victory Portfolio Ltd 3

http://slidepdf.com/reader/full/victory-portfolio-ltd-3 44/85

CHAPTER 3: OBJECTIVES AND METHODOLOGY

3.1 Significance

Significance of the project is to find out prospect investors of Victoria Portfolio

Limited Mutual Funds investment centers in Delhi and also to provide key

information about the investors perception and preferences by Mutual Fund industry.

The study helps the Victoria Portfolio Limited in getting information about their

performance at other distributors as well as at their own investment center or why

people go for Victoria Portfolio Limited Mutual Fund for investments. Study alsohelps in finding out the problems related to distribution.

3.2 Managerial Usefulness of study

44

8/8/2019 Victory Portfolio Ltd 3

http://slidepdf.com/reader/full/victory-portfolio-ltd-3 45/85

1) From the study, VICTORIA PORTFOLIO LIMITED Mutual Fund will come to

know about its prospective, individual as well as corporate clients in different

areas.

2) The study provides the complete information about all close competitors inMutual Fund investment so as to remain no. 1 investment service provider.

3) It provides the AMC a feedback from customers regarding their problems and

perception about investing in Mutual Funds so that they can improve their

services.

4) The study also provides the problems related to distribution of Mutual Fund so

that they can improve the service rendered by them as a distributor.

5) The study also gives information about prospective investors both individual as

well as institutional clients in areas of surrey where they can get lead.

3.3 Objectives

1) To study the performance of VICTORIA PORTFOLIO LIMITED Mutual Fund

at other distributor’s end.

2) To compare the total sales in Mutual Fund’s of various companies in different

schemes at VICTORIA PORTFOLIO LIMITED Mutual Fund.

3) To compare the most popular and widely invested Mutual Fund schemes offered

at VICTORIA PORTFOLIO LIMITED Mutual Fund distribution outlet.

4) To find out prospective investors or leads in Mutual Funds for VICTORIA

PORTFOLIO LIMITED .

5) To analyze the major problems faced by the investors while accessing theVICTORIA PORTFOLIO LIMITED services and devise methods to improve the

VICTORIA PORTFOLIO LIMITED services towards this service of distribution

of different Mutual Funds.

45

8/8/2019 Victory Portfolio Ltd 3

http://slidepdf.com/reader/full/victory-portfolio-ltd-3 46/85

6) To analyze the perception of investors by investing in different schemes of

various Mutual Funds.

7) To analyze that what ails the Indian Mutual Fund Industry.

3. 4 Scope of the study

1 In current scenario, the bank rates have been cut down rapidly due to severe

competition, so people are not going for contemporary deposits because that

cannot provide them. The better returns or the desired interest rates. So, they can

look for some other investment options like Mutual Funds, which can provide

them higher returns in short term and can easily meet their financial goals.

2 To look out for new prospective customers who are willing to invest in Mutual

Funds.

3 Due to changing economic scenario the small new economic zones are emerging

rapidly, so VICTORIA PORTFOLIO LIMITED can look out for those small

zones and can make available their all investment products by opening new

investment centers.

Limitations1 To get the information about the performance of VICTORIA PORTFOLIO

LIMITED Mutual Fund at various distributors was very difficult, so very few of

them revealed their sales record as well as total investments in all Mutual Funds

hiding all other trade secrets as it was against their rule and regulations. Only

close competitors are taken for comparison.

2 The survey was conducted in selective areas because of constraints of time and

resource. Therefore the generalisability of the findings cannot be claimed untilfurther research has been carried out.

3 The sample size is 120, which may not reflect a true picture of the investors

objective. Because of these constraints, the analysis may not be accurate and may

vary when tested among different category of investors in different plans among

46

8/8/2019 Victory Portfolio Ltd 3

http://slidepdf.com/reader/full/victory-portfolio-ltd-3 47/85

existing and new investors from different places like industrial as well as

residential sectors.

4 Details on the precise nature of investors objective was limited. For example the

measures used only captured certain information on standards that individuals hadin mind as acceptable outcomes of their goal directed objective.

5 Also the research does not alicit subtle goals such as mood repair motives. So the

possibility of personal biases of the respondents may not be precluded.

6 The situation in which a investor is questioned about routine actions is an

artificial one at best. Due to the influence of questioning process, respondents

may furnish quite different information from facts.

7 Thus, though the study is not conclusive in nature, it tends to explore the investors

perception and ideas about the investment services of the VICTORIA

PORTFOLIO LIMITED Mutual Fund as a distributor of Mutual Fund.

3.5 Methodology

The project is divided into four stages. The included gathering information about the

VICTORIA PORTFOLIO LIMITED Mutual Fund profile, the various investment

schemes available and other which launched by the AMC and getting acquainted

with the system of distribution work of the VICTORIA PORTFOLIO LIMITED .

The second stage involved determining the objective of the study, knowing the

target investors and drafting a questionnaire. The questionnaire was designed

keeping in mind the target investors and their objectives of the investment in any

plan. It was non-disguised in nature and included a few open-ended questions.Visits to residential areas of Delhi were made. Around 50% of the respondents

surveyed were from patpargang area…etc.

The 3 rd stage covers the conceptual study of the topic and 4 th stage covers the data

analysis, which leads to some findings and recommendations.

47

8/8/2019 Victory Portfolio Ltd 3

http://slidepdf.com/reader/full/victory-portfolio-ltd-3 48/85

8/8/2019 Victory Portfolio Ltd 3

http://slidepdf.com/reader/full/victory-portfolio-ltd-3 49/85

respondents belonged to the main types of aggressive investors conservative and

moderate type in different age group.

The research was carried out in the following areas in Delhi:-

Patparganj

Lakshminagar etc etc..

49

8/8/2019 Victory Portfolio Ltd 3

http://slidepdf.com/reader/full/victory-portfolio-ltd-3 50/85

Chapter 4

Data

analysis

50

8/8/2019 Victory Portfolio Ltd 3

http://slidepdf.com/reader/full/victory-portfolio-ltd-3 51/85

8/8/2019 Victory Portfolio Ltd 3

http://slidepdf.com/reader/full/victory-portfolio-ltd-3 52/85

Investor’s Perspective

Funds V/S other investment products

Investment

objective

Risk tolerance Investment horizon

Equity Capital appreciation High Long term

Fi Bonds Income Low Medium

Corporate debenture Income High-medium-low Medium

Compa ny FD Income High-medium-low MediumBank FD Income Generally low All terms

PDF Income Low Long term

Life insurance Risk cover Low Long term

Gold Inflation hedge Low Long term

Real estate Inflation hedge Low Long term

Mutual Funds Capital, growth,

income

High-medium-low All terms

52

8/8/2019 Victory Portfolio Ltd 3

http://slidepdf.com/reader/full/victory-portfolio-ltd-3 53/85

Perception of investors about Mutual Fund.

0

20

40

60

80

100

Best Good Bad W ors t

Remark

F r e q u e n c y

Interpretation

There is very strong approach towards the investment in Mutual Fund as the market is

growing up rapidly in equity plans so around 70% praised Mutual Fund investment; 21%

says good to get safe return from balanced of gilt funds, around 5% said that they had a

bad experience with Mutual Fund investments, very few says that they have worst

experience with Mutual Funds.

Remarks FrequencyBest 85Good 25Bad 7Worst 3

53

8/8/2019 Victory Portfolio Ltd 3

http://slidepdf.com/reader/full/victory-portfolio-ltd-3 54/85

Type of investors

Interpretation:

Among various categories of investors, 66% are Aggressive which are ready to take the

high risk. 17% of the investors are found to be slightly conservative in respect of MutualFund investments they don’t want to take any sort of risk they generally prefer to invest

in gilt funds, 13% are moderate investors i.e. they want good return but without much

risk so they prefer this kind of investments. Rest of them usually shifts to others

frequently.

Types of investors Percentages

Aggressive 66%Conservative 17%Moderate 13%Others 4%

Types of investors

66%17%

13% 4% AggressiveConservative

Moderate

Others

54

8/8/2019 Victory Portfolio Ltd 3

http://slidepdf.com/reader/full/victory-portfolio-ltd-3 55/85

Shifting nature of the investors for better returns

Investors perspecti

020406080

Yes No Can't Say

Respons

N u m b e r o f

p e r s o n s

Interpretation:

In survey, it was found that many investors can shift to other Mutual Fund form

VICTORIA PORTFOLIO LIMITED Mutual Fund in need of better returns but large

number of them said that they’ll not shift because VICTORIA PORTFOLIO LIMITED

Mutual Fund has a better track record for the past period (however past record is not the

bare of selecting any Mutual Fund) it has the largest corpus among all Mutual Fund

Company, few of the investors told that they cannot say, it depends on the better schemes

provided by any Mutual Fund Company.

ResponseNumber of persons

Yes 72

No 30Can't Say 18

55

8/8/2019 Victory Portfolio Ltd 3

http://slidepdf.com/reader/full/victory-portfolio-ltd-3 56/85

Drives behind the performance of the fund

3055

20105

Services renderedby floaters

PortfolioDiversification

Corpus of the fund

Past performance

Agents network

Interpretation:

After analyzing this question, we come to conclusion that main factor which is behind

any investment is portfolio of any Mutual Fund, well there are other factors also behindany investment like corpus of that fund, service rendered by distributor and past

performance of that fund through past performance is not the criteria for selecting any

fund. So about 46% of investors look for the portfolio diversification and rest are least

important accordingly.

Drivers ScoreServices rendered

by floaters 20PortfolioDiversification 55Corpus of the fund 30Past performance 5Agents network 10

56

8/8/2019 Victory Portfolio Ltd 3

http://slidepdf.com/reader/full/victory-portfolio-ltd-3 57/85

AWARENESS OF VICTORIA PORTFOLIO LIMITED

MUTUAL FUND AMONG INVESTORS

Interpretation:

After survey in different category of investors, we found that 15% of the investors are

aware of VICTORIA PORTFOLIO LIMITED Mutual Fund. It is surprisingly that there

is no such regarding unawareness of VICTORIA PORTFOLIO LIMITED Mutual Fund.

Awareness Level ScoreHighly Aware 95%Aware 3%Less Aware 2%

Score

95%

2%

3%Less Aware

Aware

Not aware

57

8/8/2019 Victory Portfolio Ltd 3

http://slidepdf.com/reader/full/victory-portfolio-ltd-3 58/85

VICTORIA PORTFOLIO LIMITED Mutual Fund performance on

various parameters

020406080

100

S e r v i

c e

R e t u r

n s

N e t w

o r k i n g

G o o d

w i l l

Parameters

S c o r e Good

Satisfactory

Unsatisfactory

Interpretation:

During survey, it was found that there dimensions of performance varies at each level and

also depends on investors objective and his expectation level from funds. Returns aspect

is on top level where as goodwill also matters a lot, very few client are unsatisfied by the

service at distributor level while networking was satisfactory among good number of

investors.

Parameters Good Satisfactory UnsatisfactoryService 65 40 15

Returns 85 25 10Networking 40 60 20Goodwill 95 15 10

58

8/8/2019 Victory Portfolio Ltd 3

http://slidepdf.com/reader/full/victory-portfolio-ltd-3 59/85

Questions asked during the survey

Q-Is it true that globally mutual funds under perform benchmark indices? Why are

smart money managers unable to do as well as the market? Or is it that they are not

smart at all? What are the limitations of mutual funds?

It is 100% true that globally, most mutual fund managers under perform the asset class

that they are investing in, over the very long-term. It is not true that the fund managers

are dumb; this under performance is largely the result of limitations inherent in the

concept of mutual funds. These limitations are as follows:

Entry and exit costs: Mutual funds are a victim of their own success. When a large body

like a fund invests in shares, the concentrated buying or selling often results in adverse

price movements i.e. at the time of buying, the fund ends up paying a higher price and

while selling it realizes a lower price. This problem is especially severe in emerging

markets like India, where, excluding a few stocks, even the stocks in the Sensex are not

liquid, let alone stocks in the NSE 50 or the CRISIL 500. So, there is simply no way that

a fund can beat the Sensex or any other index, if it blindly invests in the same stocks as

those in the Sensex and in the same proportion. For obvious reasons, this problem is evenmore severe for funds investing in small capitalization stocks. However, given the large

size of the debt market, excluding UTI, most debt funds do not face this problem

Wait time before investment : It takes time for a mutual fund to invest money.

Unfortunately, most mutual funds receive money when markets are in a boom phase and

investors are willing to try out mutual funds. Since it is difficult to invest all funds in one

day, there is some money waiting to be invested. Further, there may be a time lag before

investment opportunities are identified. This ensures that the fund under performs theindex. For open-ended funds, there is the added problem of perpetually keeping some

money in liquid assets to meet redemptions. The problem of impracticability of quick

investments is likely to be reduced to some extent with the introduction of index futures.

59

8/8/2019 Victory Portfolio Ltd 3

http://slidepdf.com/reader/full/victory-portfolio-ltd-3 60/85

Fund management costs: The costs of the fund management process are deducted from

the fund. This includes marketing and initial costs deducted at the time of entry itself,

called "load". Then there is the annual asset management fee and expenses, together

called the expense ratio. Usually, the former is not counted while measuring

performance, while the latter is. A standard 2% expense ratio means that, everything else

being equal, the fund manager under performs the benchmark index by an equal amount.

Cost of churn: The portfolio of a fund does not remain constant. The extent to which the

portfolio changes is a function of the style of the individual fund manager i.e. whether he

is a buy and hold type of manager or one who aggressively churns the fund. It is also

dependent on the volatility of the fund size i.e. whether the fund constantly receives fresh

subscriptions and redemptions. Such portfolio changes have associated costs of brokerage, custody fees, registration fees etc. that lowers the portfolio return

commensurately.

Change of index composition: World over, the indices keep changing to reflect

changing market conditions. There is an inherent survivorship bias in this process, with

the bad stocks weeded out and replaced by emerging blue chips. This is a severe problem

in India with the Sensex having been changed twice in the last 5 years, with each change

being quite substantial. Another reason for change index composition is Mergers &Acquisitions. The weight age of the shares of a particular company in the index changes

if it acquires a large company not a part of the index .

Tendency to take conformist decisions: From the above points, it is quite clear that the

only way a fund can beat the index is through investment of some part of its portfolio in

some shares where it gets excellent returns, much more than the index. This will pull up

the overall average return. In order to obtain such exceptional returns, the fund manager

has to take a strong view and invest in some uncommon or unfancied investment options.Most people are unwilling to do that. They follow the principle "No fund manager ever