Investor Presentation VRTV Veritiv Corporation

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Investor Presentation VRTV

Veritiv Corporation

| 2

This document contains forward-looking statements that involve risks, uncertainties and changes in circumstances. Forward-looking statements generally can be identified by the use of forward-looking terminology such as “may,” “will,” “expect,” “intend,” “estimate,” “anticipate,” “believe,”

“project,” “continue” or other similar words. The forward-looking statements are not historical facts, but rather are based on Veritiv Corporation’s (the Company’s) current expectations, estimates,

assumptions and projections about our industry, business and future financial results. The Company’s actual results could differ materially from the results contemplated by these forward-looking statements due to a number of factors, including those discussed in the sections entitled

“Risk Factors” and “Note Regarding Forward-Looking Statements and Information” in the prospectus forming part of the Company’s Registration Statement on Form S-1 originally filed with the Securities and Exchange Commission on February 14, 2014, as the same has been amended

to date. For the foregoing reasons, you are cautioned against relying on any forward-looking statements contained in this presentation. The Company does not undertake any obligation to update or revise these forward-looking statements, except as required by law. This presentation

also contains certain non-GAAP financial measures including adjusted EBITDA. Adjusted EBITDA is not considered a measure of financial performance under generally accepted accounting

principles and the items excluded in the calculation are significant components in understanding and assessing our financial performance. Non-GAAP measures should not be considered in

isolation or as an alternative to GAAP measures and such measures may not be comparable to other similarly titled measures of other companies. The reconciliation of these non-GAAP items can

be found in the appendix to this presentation.

Forward-Looking Statement

| 3

Agenda

Topic

Transaction Overview

Veritiv: Background and Investment Highlights

Financials and Leadership

| 4

Executive Summary

Ø Two industry leaders

Ø Complimentary businesses

Ø Significant synergies

Ø Invest in high-margin growth

| 5

Structure and consideration

Ownership

Closing

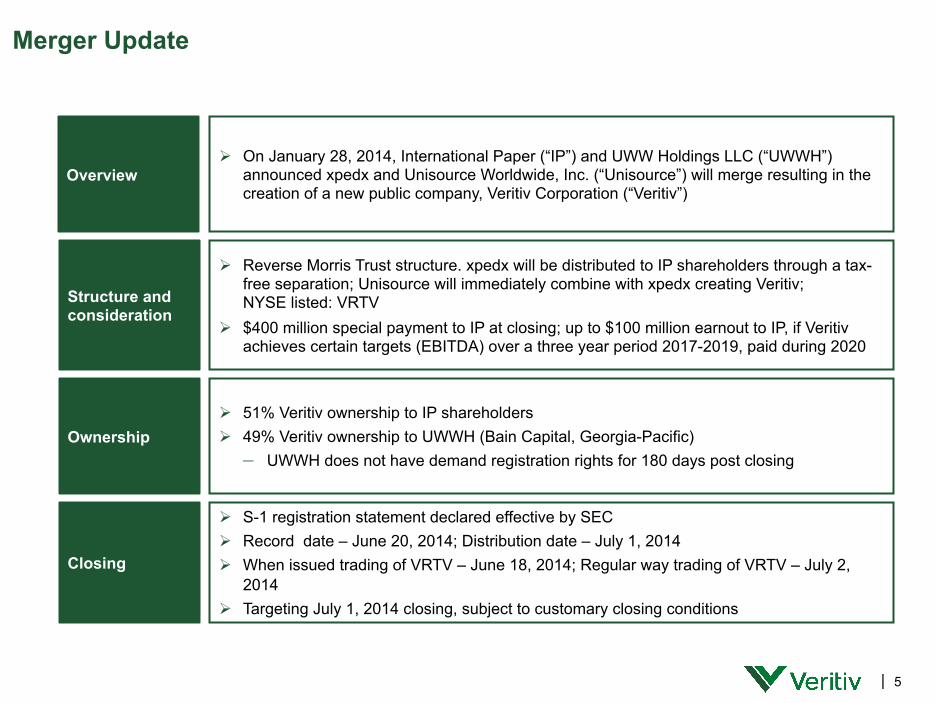

Ø Reverse Morris Trust structure. xpedx will be distributed to IP shareholders through a tax-free separation; Unisource will immediately combine with xpedx creating Veritiv; NYSE listed: VRTV

Ø $400 million special payment to IP at closing; up to $100 million earnout to IP, if Veritiv achieves certain targets (EBITDA) over a three year period 2017-2019, paid during 2020

Ø 51% Veritiv ownership to IP shareholders Ø 49% Veritiv ownership to UWWH (Bain Capital, Georgia-Pacific)

– UWWH does not have demand registration rights for 180 days post closing

Ø S-1 registration statement declared effective by SEC Ø Record date – June 20, 2014; Distribution date – July 1, 2014 Ø When issued trading of VRTV – June 18, 2014; Regular way trading of VRTV – July 2,

2014 Ø Targeting July 1, 2014 closing, subject to customary closing conditions

Overview Ø On January 28, 2014, International Paper (“IP”) and UWW Holdings LLC (“UWWH”)

announced xpedx and Unisource Worldwide, Inc. (“Unisource”) will merge resulting in the creation of a new public company, Veritiv Corporation (“Veritiv”)

Merger Update

| 6

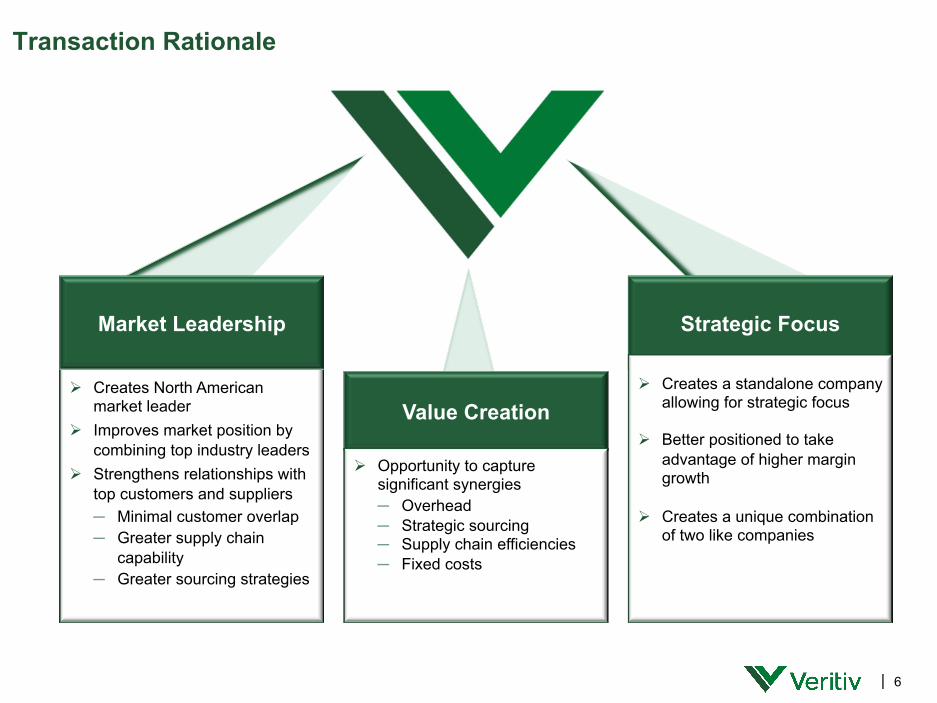

Transaction Rationale

Market Leadership

Ø Creates North American market leader

Ø Improves market position by combining top industry leaders

Ø Strengthens relationships with top customers and suppliers ─ Minimal customer overlap ─ Greater supply chain

capability ─ Greater sourcing strategies

Value Creation

Ø Opportunity to capture significant synergies ─ Overhead ─ Strategic sourcing ─ Supply chain efficiencies ─ Fixed costs

Strategic Focus

Ø Creates a standalone company allowing for strategic focus

Ø Better positioned to take advantage of higher margin growth

Ø Creates a unique combination of two like companies

| 7

Agenda

Topic

Transaction Overview

Veritiv: Background and Investment Highlights

Financials and Leadership

| 8

xpedx Business Overview

($ Millions) YE 12/31/13

Net Sales $5,652

Adj. EBITDA $75

EBITDA Margin 1.3%

Employees 5,200

DCs 73

Mini-DCs 13

2013 Revenue by Primary Segment

North American Footprint Primary Segment Descriptions Provides end-to-end print solutions, including the sale & distribution of print substrates, graphics supplies and wide format, corporate end-user paper solutions

Provides packaging expertise through design, sourcing, sale and distribution of custom & standard packaging supplies and equipment

Facility Solutions provider through the sale and distribution of products necessary to maintain large facilities

xpedx DCs

Leading business-to-business distributor of print, packaging and facility solutions in the United States and Mexico.

Print 57%

Packaging 28%

Facility Solutions

15%

Packaging

Facility Solutions

| 9

Unisource Business Overview

Leading business-to-business distributor of print, packaging and facility solutions in the United States and Canada.

($ Millions) YE 12/31/13

Net Sales $4,089

Adj. EBITDA $87

EBITDA Margin 2.1%

Employees 4,200

DCs 93

Provides end-to-end print solutions: print management, the sale & distribution of print substrates, graphics supplies and wide format

Provides custom, end-to-end packaging solutions, from material innovation to design, sourcing and selling of packing materials and equipment

Facility solutions provider through the sale and distribution of products necessary to maintain large facilities

Inbound and outbound logistics solutions, comprehensive supply chain analytics and value-added offerings

Unisource DCs

2013 Revenue by Primary Segment

Print 54% Packaging

28%

Facility Solutions

16%

Logistics Solutions 2%

Packaging

Facility Solutions

Logistics Solutions

North American Footprint Primary Segment Descriptions

| 10

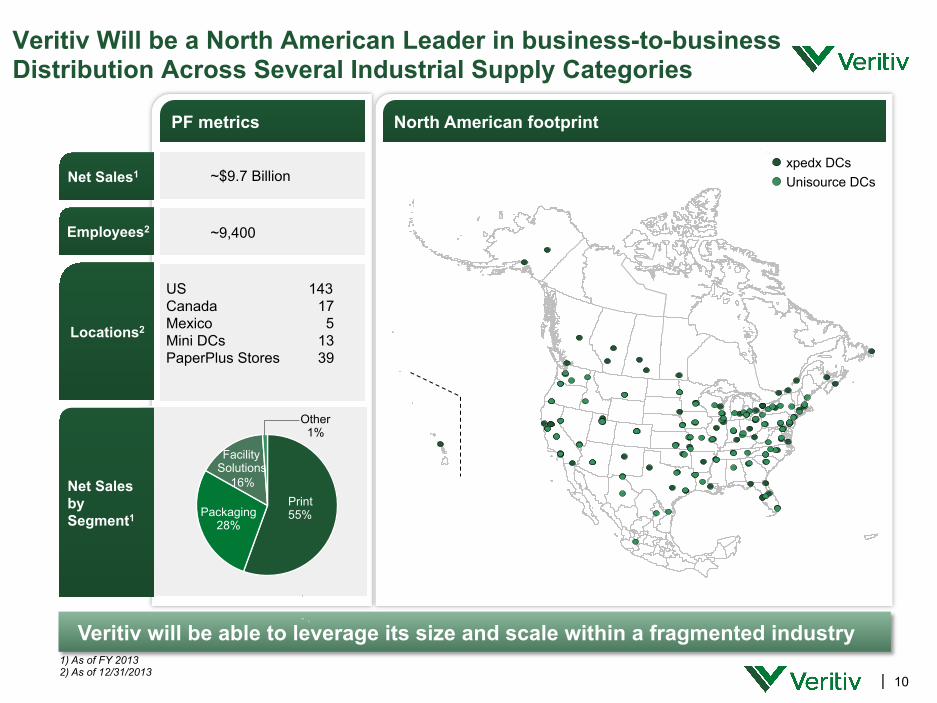

Net Sales1 ~$9.7 Billion

Net Sales by Segment1

1) As of FY 2013 2) As of 12/31/2013

PF metrics North American footprint

Locations2

US Canada Mexico Mini DCs PaperPlus Stores

143 17 5

13 39

Employees2 ~9,400

Veritiv will be able to leverage its size and scale within a fragmented industry

xpedx DCs Unisource DCs

Veritiv Will be a North American Leader in business-to-business Distribution Across Several Industrial Supply Categories

Print 55% Packaging

28%

Facility Solutions

16%

Other 1%

| 11

Veritiv’s Business Model

Ø Full product line to reduce inbound complexity

Ø National network to service large customers

Ø Service and solutions to customers where they lack expertise or capabilities

Ø Veritiv conducts business with more than half of the Fortune 500

Partner with world class suppliers…

…then add value through multiple capabilities…

…to a wide range of customer segments

Ø Customer Reach

Ø Effective Supply Chain

Select

Solve

Source Service

Sell

Veritiv

| 12

Veritiv Business Strategy

Veritiv’s business strategy will be underpinned by two foundational objectives – growth in more profitable segments and operational excellence.

Profitable Revenue Mix – Segment Specific Market Leadership

Operational Excellence

Ø Standardized processes and procedures with local execution

Ø Extensive supply chain capabilities (systems, tools, resources)

Ø Monitoring and measuring tools

Ø Size and scale advantages

Ø Investment in tools and capabilities; continuously improving

Ø Expertise in paper & access to best in class product breadth value Print

Ø Expertise in paper & access to best in class product breadth value

Publishing and Print Mgmt.

Ø Full service design, sourcing and delivery of substrate agnostic specialty packaging solutions, as well as standard packaging

Packaging

Ø Aggregate sourcing, tiered offerings, supply chain reach and assured buying compliance

Facility Supplies

| 13

Veritiv’s Print Segment

Providing more than just products – creating solutions.

1) Combined xpedx and Unisource 2013 sales 2) Based on industry data and company estimates (2013 – 2018)

High-Quality Commercial Paper

n Printing, writing, copy, digital, and specialty

n National and private brands

Graphics

n Graphics supplies

n Equipment sales and service

Wide Format Solutions

n Wide format solutions ̶ Equipment ̶ Substrates

Small Order Service

n Support growth of digital print small runs

n Small order delivery

E-Commerce & E-Procurement

n Automated e-procurement platforms, allowing customers to define specification, review estimates, and place orders

Forecasted Market Growth Rate: (3%)2

Sustainable Solutions

n Sustainable green printing

n Chain of Custody certifications

Veritiv Net Sales¹ $4.0 billion

| 14

Veritiv’s Publishing & Print Management Segment

Veritiv Net Sales¹ $1.5 billion

Paper Sourcing & Delivery n Extensive sourcing options

n Expert service and delivery

Print Consulting n End user consulting for the most

effective, cost competitive solutions

Global Market Solutions n Paper procurement needs of

multinational customers with offshore affiliates or locations

Workflow Management n Customer workflow managed to

optimize print jobs

Print Management n End user end-to-end solutions in

printing, substrate sourcing, and delivery

Forecasted Market Growth Rate: (4%)2

Providing solutions to the world’s largest publishers and consumer retail companies.

1) Combined xpedx and Unisource 2013 sales 2) Based on industry data and company estimates (2013 – 2018)

| 15

Veritiv’s Packaging Segment

Positioned for growth as the single-point resource for all packaging needs, from design, to sourcing to delivery.

Custom Packaging n End-to-end design, engineering,

sourcing and delivery

n Nation-wide network of design centers

Material Innovation & Sustainable Sourcing

n Design and/or sourcing of leading-edge alternative materials

n Green packaging

Standard Packaging n Broad portfolio, tiered

offerings ̶ Branded ̶ Private Label

Value Added Services

n Logistic and supply chain services

Equipment Solutions & Support

n Production packaging equipment solutions

n Sales and service

International Capabilities n Sourcing and delivery outside

the U.S. for U.S. based customers manufacturing in Asia, Europe and Brazil

Specification Management n Master data management of all

packaging material specifications

Forecasted Market Growth Rate: 2%2

1) Combined xpedx and Unisource 2013 sales 2) Based on industry data and company estimates (2013 – 2018)

Veritiv Net Sales¹ $2.7 billion

| 16

Veritiv’s Facility Solutions Segment

Standard Products n Broad portfolio of branded and

private label products n Supply chain efficiency

Green Product Offerings n Branded and private label

products n Chain of custody certifications

Healthy Building Consulting n Quality control audits and

action plans n Certified specialists

Reporting & Analytics n Inventory management

analytics n Green reporting n Spend reporting to support

customer budgets

Customer Inventory Optimization

n System to optimize customer inventory

n Automatic replenishment

Forecasted Market Growth Rate: 2%2

1) Combined xpedx and Unisource 2013 sales 2) Based on industry data and company estimates (2013 – 2018)

Providing products, services and solutions nationally across multiple channels.

Veritiv Net Sales¹ $1.5 billion

Re-distribution n Small distributors n One-stop shopping n Leverage supply chain

| 17

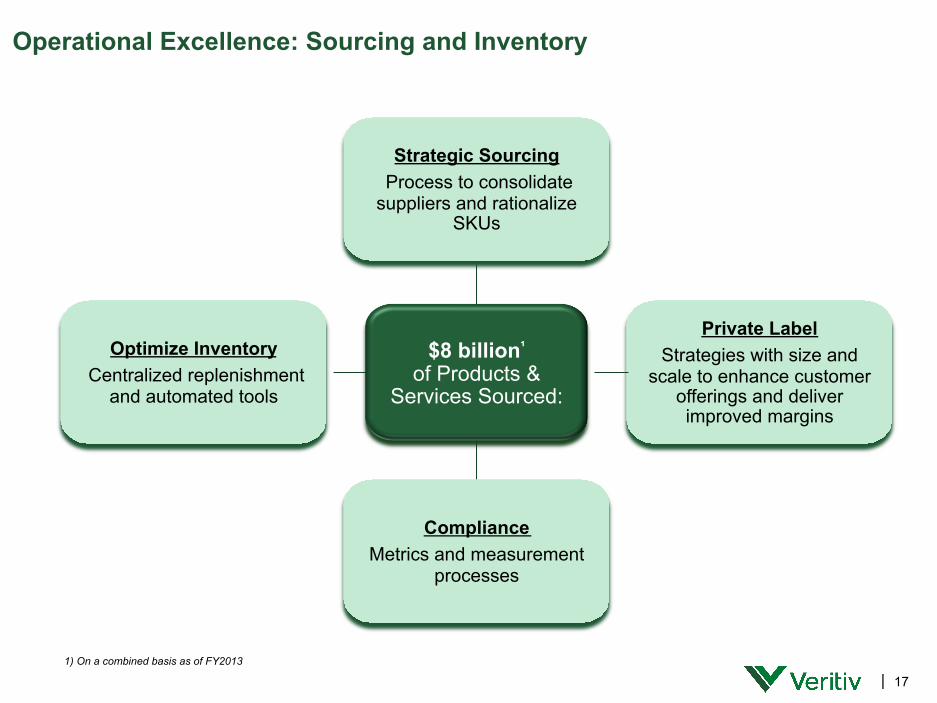

$8 billion¹ of Products &

Services Sourced:

Private Label Strategies with size and

scale to enhance customer offerings and deliver improved margins

Optimize Inventory Centralized replenishment

and automated tools

1) On a combined basis as of FY2013

Strategic Sourcing Process to consolidate suppliers and rationalize

SKUs

Compliance Metrics and measurement

processes

Operational Excellence: Sourcing and Inventory

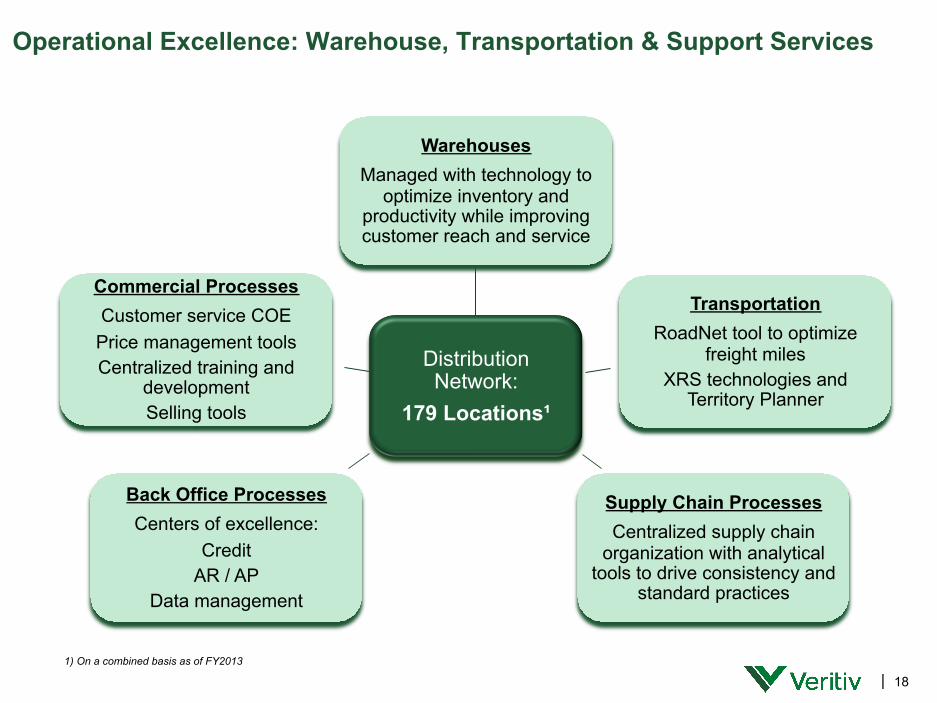

| 18

Distribution Network:

179 Locations¹

Warehouses Managed with technology to

optimize inventory and productivity while improving customer reach and service

Transportation RoadNet tool to optimize

freight miles XRS technologies and

Territory Planner

Supply Chain Processes Centralized supply chain

organization with analytical tools to drive consistency and

standard practices

Back Office Processes Centers of excellence:

Credit AR / AP

Data management

Commercial Processes Customer service COE

Price management tools Centralized training and

development Selling tools

Operational Excellence: Warehouse, Transportation & Support Services

1) On a combined basis as of FY2013

| 19

Consolidating Operational Excellence Programs to capture and sustain synergies

Centralized Supply Chain will assist Field and SBUs to increase profit without sacrificing profitable growth

Deliver operational excellence: Enhance cross-functional processes while allowing for appropriate local flexibility

Capture synergy

Deliver operational excellence

Capture synergies: Rigorous programs to systematically attack the opportunity across business units

a) Profitable service – Provide field with information on opportunities to adjust handling/delivery, customer service, and inventory costs

b) Logistics excellence – Optimize routing, transfers, freight rates, warehouse productivity and space

c) Sourcing – Partner with SBUs to drive down unit costs and rationalize SKUs

1

2

Ope

ratio

nal E

xcel

lenc

e Pr

ogra

m

| 20

Agenda

Topic

Transaction Overview

Veritiv: Background and Investment Highlights

Financials and Leadership

| 21

Revenues

Synergies

2014 Adjusted EBITDA expected to be $135 million - $145 million

Ø Investing in growth segments Ø Organized around

– Large nation/regional accounts – scale matters – Local accounts – manage cost to serve

Ø Strategic account management - optimize customer mix and SKUs Ø Initial downward pressure

Ø Better positioned to take advantage of higher margin growth segments Ø Management intends to improve Adjusted EBITDA by an incremental $100

million over next few years Ø Transaction and transition expenses meaningful….but, one-time in nature

– Strategic sourcing – Supply chain efficiencies

– Fixed costs (e.g. warehouse) – Overhead (e.g. back office)

Ø Opportunity to capture significant synergies Ø Significant driver to business model in next several years

Financial Summary

| 22

Synergies and one-time integration costs

Veritiv expects significant net synergies of $150M - $225M

Ø Key areas that synergies will be derived from include: – Supply chain efficiencies – Selling, General and Administrative

0%

20%

40%

60%

80%

100%

YE 2014 YE 2015 YE 2016 YE 2017

0%

15% - 25%

50% - 60%

80% - 90% Net synergies expected to be realized

Costs to achieve1

($225M): 30-35% 60-70% 80- 90% 90-100%

1) Includes ~ $55 million of one-time integration capital expenditures

| 23

Liquidity and Capital Discussion

Cap Structure Capital Allocation

– Fund costs of synergies and reinvest in the business ̶ Maintain fleet and facilities to

preserve premium customer service levels compared to lesser capitalized, smaller, competitors

Pay down debt ̶ Improve balance sheet

Position company to return value to shareholders over time

▪ New $1.4bn ABL facility in place, matures 2019 ̶ Initial draw down of ~ $750 million at

closing ̶ Available liquidity at closing of

~ $450 million

▪ Initial ABL drawings used to repay Unisource debt and to fund IP cash dividend of $400 million

▪ Over the next few years, Veritiv

expects revolver availability plus cash flow from operations will be sufficient to fund costs of achieving synergies and other working capital needs

| 24

Veritiv’s Leadership & Governance

q Lead Director William E. Mitchell, retired chairman and chief executive officer, Arrow Electronics, Inc. and founder of Sequel Capital Management, LLC

q Allan Dragone, current Unisource CEO, will serve as a director of the new company and will advise on integration activities.

q Daniel T. Henry, retired executive vice president and chief financial officer, American Express

q Tracy Leinbach, retired executive vice president and CFO, Ryder System, Inc.

q Seth Meisel, managing director, Bain Capital

q Michael Muldowney, former CFO and interim CEO of Houghton Mifflin Harcourt Publishing Co., and founder and CEO of Foxford Capital, LLC

q Charles G. Ward, partner, Perella Weinberg Partners, and former president, Lazard Ltd.

q John Zillmer, retired chairman, president and chief executive officer, Univar, Inc.

Mary Laschinger Chairman and Chief Executive Officer Current President, xpedx and SVP, International Paper

Management Team Board of Directors SVP, Packaging Darin Tang

SVP, Print Dan Watkoske

SVP, Supply Chain Tim Kutz

SVP, Field Sales & Operations Tom Lazzaro

SVP, General Counsel Mark Hianik

SVP, CFO Steve Smith

SVP, Corporate Affairs Neil Russell

SVP, Integration & Change Mgmt Bruce Henry

SVP, Chief Human Resources Officer Beth Patrick

SVP, Publishing & Print Management Barry Nelson

SVP, Facility Solutions/Strategy & Commercial Excellence Joe Myers

Significant leadership incentives will be linked to earnings performance

| 25

Why Invest in Veritiv (VRTV)…

Ø Industry leader with significant size and scale Ø Business model creates value for both customers and

suppliers Ø Growth segments in packaging, facility solutions and logistics

with differentiating value propositions Ø Positioned to win in the print segment Ø Strong and stable platform to invest for future growth Ø Experienced team

| 26

Non-GAAP Reconciliations

| 27

Adjusted EBITDA is defined as earnings before interest, income taxes, depreciation and amortization, cash and non-cash restructuring (gains) expenses, merger expenses, gain from sale of equity investments, asset impairments, non-restructuring stock-based compensation expense, LIFO (income) expense, non-restructuring severance charges, non-restructuring pension settlement charges, (loss) income from discontinued operations, net of income taxes, and certain other costs. Adjusted EBITDA Margin is calculated based on Adjusted EBITDA divided by net sales. Veritiv supplements its financial information prepared in accordance with GAAP with Adjusted EBITDA because we believe investors commonly use Adjusted EBITDA as a main component of valuing companies such as Veritiv. In addition, the credit agreement governing Veritiv’s ABL Facility will permit Veritiv to exclude these and other charges and expenses in calculating “Consolidated EBITDA” pursuant to such credit agreement. A reconciliation of Adjusted EBITDA to net income determined in accordance with GAAP is provided for the periods presented.

Non-GAAP Adjusted EBITDA Reconciliation Disclaimer

| 28

Veritiv Historical Non-GAAP Adjusted EBITDA Reconciliation

Veritiv Historical Non-GAAP Adjusted EBITDA Reconciliation ($mm) FY '11A FY '12A FY '13A LTM 1Q '14A 1Q '13A 1Q '14A

Net income (loss) $(5) $10 $243 $251 $(6) $2 Interest expense, net 67 28 27 27 7 6

Income tax provision (benefit) ¹ 16 24 (228) (225) (0) 3

Depreciation and amortization 40 39 42 42 11 11

EBITDA $117 $102 $84 $96 $11 $23 Restructuring expenses (gains) 58 42 35 27 8 -

Merger expenses - - 14 22 0 8

Gain from sale of equity investment² - - - (7) - (7)

Asset impairments³ 1 5 0 0 0 -

Non-restructuring stock-based compensation 11 14 14 11 4 1

LIFO (income) expense 1 1 7 5 (3) (4)

Non-restructuring severance charges 1 1 3 4 0 2

Non-restructuring pension settlement charges - 1 1 1 - - (Loss) income from discontinued operations, net of income taxes

(14) (10) 0 (0) 0 (0)

Employee strike related costs - 2 - - - -

Bain athisory fees 4 4 4 4 1 1

Adjusted EBITDA $208 $181 $162 $163 $22 $24

1) FY '12 includes a $17 million charge related to a deferred tax asset valuation allowance for Unisource Canada FY '13 and LTM 1Q '14 includes a $230 million of tax benefit related to the reversal of the Unisource U.S. tax valuation allowance

2) LTM 1Q '14 includes gains of $5 million and $2 million from the sale of two of Unisource's joint ventures 3) FY '11 includes write-off of trade names by Unisource Canada of $1 million FY '12 primarily includes a $3 million impairment of cold storage equipment by Unisource Canada, a $1 million of impairment of packaging equipment Unisource Sweden and a $1 million impairment of goodwill by Unisource Canada

| 29

xpedx Historical Non-GAAP Adjusted EBITDA Reconciliation

xpedx Historical Non-GAAP Adjusted EBITDA Reconciliation ($mm) FY '11A FY '12A FY '13A LTM 1Q '14A 1Q '13A 1Q '14A

Net income (loss) $22 $4 $0 $6 $(1) $6

Interest expense, net - - - - - -

Income tax provision (benefit) 21 9 0 5 (1) 4

Depreciation and amortization 16 14 17 17 4 5

EBITDA $59 $28 $18 $28 $3 $14

Restructuring expenses (gains) 44 35 38 31 7 (0)

Non-restructuring stock-based compensation 10 13 14 10 4 1

LIFO (income) expense (1) 1 3 2 (2) (4)

Non-restructuring severance charges 0 1 2 4 0 2

(Loss) income from discontinued operations, net of income taxes

(14) (10) 0 (0) 0 (0)

Employee strike related costs - 2 - - - -

Adjusted EBITDA $126 $90 $75 $75 $13 $13

| 30

Unisource Historical Non-GAAP Adjusted EBITDA Reconciliation

Unisource Historical Non-GAAP Adjusted EBITDA Reconciliation ($mm) FY '11A FY '12A FY '13A LTM 1Q '14A 1Q '13A 1Q '14A

Net income (loss) $(27) $5 $242 $245 $(6) $(3)

Interest expense, net 67 28 27 27 7 6

Income tax provision (benefit)¹ (6) 15 (229) (229) 0 (0)

Depreciation and amortization 25 25 25 25 6 6

EBITDA $59 $74 $66 $67 $8 $9

Restructuring expenses (gains) 15 7 (3) (4) 1 0

Merger expenses - - 14 22 0 8

Gain from sale of equity investment² - - - (7) - (7)

Asset impairments³ 1 5 0 0 0 -

Non-restructuring stock-based compensation 1 1 0 0 0 -

LIFO (income) expense 2 (0) 3 4 (1) (0)

Non-restructuring severance charges 1 1 1 1 - 0

Non-restructuring pension settlement charges - 1 1 1 - -

Bain advisory fees 4 4 4 4 1 1

Adjusted EBITDA $83 $92 $87 $89 $10 $11

1) FY '12 includes a $17 million charge related to a deferred tax asset valuation allowance in Canada FY '13 and LTM 1Q '14 includes a $230 million of tax benefit related to the reversal of the Unisource U.S. tax valuation allowance

2) LTM 1Q '14 includes gains of $5 million and $2 million from the sale of two of Unisource's joint ventures 3) FY '11 includes impairment of trade names in Canada FY '12 primarily includes a $3 million impairment of cold storage equipment in Canada, a $1 million of impairment of packaging equipment in Sweden and a $1 million impairment of goodwill in Canada

Related Documents