SUZANNE LINDAMOOD, SHERMAN D. HANNA, AND LAN BI Using the Survey of Consumer Finances: Some Methodological Considerations and Issues We identify and present original analyses of four methodological issues related to using Survey of Consumer Finances data sets and illustrate these issues with recent articles published in this journal. The issues are recognizing that the respondent is not necessarily the household head, reporting race and ethnicity in conformity with Survey of Consumer Finances and federal standards, using the repeated-imputation infer- ence method to combine the five implicates in each survey year’s data set, and discussing the use of weighted or unweighted data in multivar- iate analysis. We found a considerable variation in how authors dealt with these issues, which could hinder replication or comparison of research results. Authors and reviewers should consider methodologi- cal issues related to the Survey of Consumer Finances more carefully. Editor’s note: After this refereed paper was accepted for publication, Jeanne M. Hogarth was asked to solicit comments and assume the role of moderator for the discussion essays. As editor as these commentaries, her observations immediately follow the article plus those of Darryl E. Getter and Sandra J. Huston. The Survey of Consumer Finances (SCF), sponsored by the Federal Reserve Board, is a rich and convenient source of information about house- hold finances. It has been conducted every three years since 1983, employ- ing a complex sampling system that provides a sizable number of households and allows estimations of the U.S. population as a whole (Aizcorbe, Kennickell, and Moore 2003). The public data set is free, and the substantial online assistance includes working papers and well-documented codebooks. A user-developed Web site with tips for researchers is also available (Hanna 2006). However, despite the apparent ease of use, care is needed in using and reporting the data because of the sampling proce- dures, the method of imputing missing values, and the nature of some demographic variables. As with any research, those who use SCF data Suzanne Lindamood is a research attorney with the Ohio Legislative Service Commission, Columbus, OH ([email protected]). Sherman D. Hanna is a professor in the Consumer Sciences Depart- ment, The Ohio State University, Columbus, OH ([email protected]). Lan Bi is a risk management consultant in Wells Fargo Financial, Des Moines, IA ([email protected]). This publication was made possible by a generous grant from the FINRA Investor Education Foun- dation, formerly known as the NASD Investor Education Foundation. The authors thank Jessie Fan for helpful suggestions. The Journal of Consumer Affairs, Vol. 41, No. 2, 2007 ISSN 0022-0078 Copyright 2007 by The American Council on Consumer Interests WINTER 2007 VOLUME 41, NUMBER 2 195

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

SUZANNE LINDAMOOD, SHERMAN D. HANNA, AND LAN BI

Using the Survey of Consumer Finances: SomeMethodological Considerations and Issues

We identify and present original analyses of four methodological issuesrelated to using Survey of Consumer Finances data sets and illustratethese issues with recent articles published in this journal. The issues arerecognizing that the respondent is not necessarily the household head,reporting race and ethnicity in conformity with Survey of ConsumerFinances and federal standards, using the repeated-imputation infer-ence method to combine the five implicates in each survey year’s dataset, and discussing the use of weighted or unweighted data in multivar-iate analysis. We found a considerable variation in how authors dealtwith these issues, which could hinder replication or comparison ofresearch results. Authors and reviewers should consider methodologi-cal issues related to the Survey of Consumer Finances more carefully.Editor’s note: After this refereed paper was accepted for publication,Jeanne M. Hogarth was asked to solicit comments and assume the roleof moderator for the discussion essays. As editor as these commentaries,her observations immediately follow the article plus those of DarrylE. Getter and Sandra J. Huston.

The Survey of Consumer Finances (SCF), sponsored by the Federal

Reserve Board, is a rich and convenient source of information about house-

hold finances. It has been conducted every three years since 1983, employ-

ing a complex sampling system that provides a sizable number of

households and allows estimations of the U.S. population as a whole

(Aizcorbe, Kennickell, and Moore 2003). The public data set is free, and the

substantial online assistance includes working papers and well-documented

codebooks. A user-developed Web site with tips for researchers is also

available (Hanna 2006). However, despite the apparent ease of use, care

is needed in using and reporting the data because of the sampling proce-

dures, the method of imputing missing values, and the nature of some

demographic variables. As with any research, those who use SCF data

Suzanne Lindamood is a research attorney with the Ohio Legislative Service Commission, Columbus,

OH ([email protected]). Sherman D. Hanna is a professor in the Consumer Sciences Depart-

ment, The Ohio State University, Columbus, OH ([email protected]). Lan Bi is a risk management

consultant in Wells Fargo Financial, Des Moines, IA ([email protected]).

This publication was made possible by a generous grant from the FINRA Investor Education Foun-

dation, formerly known as the NASD Investor Education Foundation. The authors thank Jessie Fan for

helpful suggestions.

The Journal of Consumer Affairs, Vol. 41, No. 2, 2007

ISSN 0022-0078

Copyright 2007 by The American Council on Consumer Interests

WINTER 2007 VOLUME 41, NUMBER 2 195

need to make appropriate decisions, justify procedures, precisely define

variables, and provide sufficient detail so readers can understand the find-

ings and other researchers can replicate the study.

It might seem that precise reporting is not necessary when a researcher

works with a widely used national data set that provides detailed online doc-

umentation. A reader might assume that SCF researchers employ standard

variables and commonly agreed uponmethods for analysis, making it possible

to compare research across studies. However, our initial overview of 28

articles that used the SCF, published in the Journal of Consumer Affairs,Financial Counseling and Planning, Financial Services Review, and the Jour-nal of Family and Economic Issues, revealed a number of problems and incon-

sistencies in the use of variables and description of methods. Six of the articles

we reviewed appeared in the Journal of Consumer Affairs during the years

2001–2004. In this article, we focus on those articles, analyzing their treatment

of the following four issues that we identified as particularly problematic.

d Recognizing that the respondent is not necessarily the household

head.

d Reporting race and ethnicity in conformity with SCF categories and

federal standards.

d Using the data of all five implicates and the repeated-imputation infer-

ence (RII) method to combine the implicates.

d Discussing the use of weighted or unweighted data in multivariate

analysis.

Table 1 lists the articles we used in our analysis and summarizes how

each dealt with the four issues. We do not propose that any lack of pre-

cision related to these issues affected the authors’ conclusions. The gen-

eral problems we discuss, using these articles as examples, are not limited

to these articles nor to this journal but occur in many articles using the

SCF, including some we have authored. We analyzed these issues because

precision and ability to replicate and compare results are fundamental to

research, and paying attention to these issues can improve future research

using the SCF.

ANALYSIS

The Household Head vs. the Survey Respondent

In the SCF, the respondent and the household head are not neces-

sarily the same person, and either partner in a couple household could

196 THE JOURNAL OF CONSUMER AFFAIRS

TABLE1

ArticlesUsing

theSC

Fin

theJournal

ofConsumer

Affairs,20

01–2

004

Article

Respondentvs.Head

Race/Ethnicity

ImplicatesandRII

WeightingMultivariate

Analysis

Hogarth,Anguelov,

andLee

(2004)

Notdiscussed;education,race,

andageare‘‘ofhousehold’’

Threecategories:whiteandother

(combined),black,andHispanic

Discussed

implicatesand

whydid

notuse

RII

Notstated

Getter(2003)

Notdiscussed;referred

toincome,

educationofrespondent,and

race

ofhead

Twocategories:black

orHispanic

(combined)andnotnam

ed

(appears

toincludewhite

andother)

Nodiscussion

Did

notweightmultivariate

analysis

Lyons(2003)

Notdiscussed

Twocategories:black,andwhite

(appears

toincludewhite,

Hispanic,andother)

Nodiscussion

Weightedmultivariate

analysis(implied

by

footnote

totable

1)

Lee

andKwon(2002)

Did

notdiscuss

distinction;referred

toageofrespondent;ethnicity

andeducationnotspecified

Fourcategories:black,white,

Hispanic,andother

non-w

hite

minorities

UsedRIIformeanstests.

Reported

only

one

implicate

formultivariate

Notstated

ChienandDeV

aney

(2001)

Did

notdiscuss

distinction;age

andrace

ofhead;education

notspecified

Twocategories:Caucasian

and

non-Caucasian

(compositionof

categories

notdiscussed)

Usedonly

oneim

plicate

Notstated

Xiaoet

al.(2001)

Discussed

distinction;listed

dem

ographic

dataforhead

Twocategories:Caucasian

and

non-Caucasian

(compositionof

thesecategories

notdiscussed)

Nodiscussion

Weightedmultivariate

analyses

WINTER 2007 VOLUME 41, NUMBER 2 197

be the respondent. Because of the detailed nature of the financial data

the SCF gathers, interviewers are trained to establish who is the most

financially knowledgeable person in the household and to interview that

person (Lindamood and Hanna 2005, 2006). Therefore, the respondent

is the most financially knowledgeable person. The household head,

however, is an arbitrary designation. In the SCF, the male always

is designated as the head for mixed-sex couple households and the

older partner always is designated as the head for same-sex couple

households.

Correctly identifying whose demographic data is being used—the

respondent’s or the head’s—is particularly important when analyzing

variables such as race and the various attitude variables because

the SCF collects race and attitude variables only for the respondent. It

would be inappropriate, for example, to study the relationship of age

and attitude using the head’s age because attitudes are those of the

respondent. The mistake might not be limited to a small number of house-

holds. In our weighted analysis of the 2001 SCF, about 60% of the house-

holds included couples, and about 87% of those were husband-wife

couples. The wife was the respondent in 46% of the husband-wife couple

households.

None of the six articles that appeared in the Journal of ConsumerAffairs discussed the distinction between the respondent and the head

(Table 1). Four articles referred to the race of the head or the race of

the household, both of which are inaccurate under the SCF because

the race of the head is known only if the head is the respondent. If

researchers assume that a spouse/partner is of the same race as the

respondent, that assumption should be specified and only then should

the race of the respondent be used as a proxy for other members of

the household.

The article by Hogarth, Anguelov, and Lee (2004) generally was the

most careful in describing methods, but the tables and the discussion of

the variables described ‘‘household age’’ and ‘‘education of the house-

hold’’ without identifying whether the ‘‘household’’ data represented

the respondent, the head, or a composite the researchers created. The arti-

cle also referred to the race of the household, which the SCF does not

measure.

Getter (2003) did not discuss any methodological details but listed the

variables of the model he tested. The listing represented education and

employment as that of the respondent. However, the discussion and find-

ings were presented in terms of the household head. He did not discuss

198 THE JOURNAL OF CONSUMER AFFAIRS

whose race was measured, but his article replicated a study by Canner,

Gabriel, and Woolley (1991), which incorrectly listed race as that of

the head. Getter stated, ‘‘Demographic variables such as age, race, and

whether or not the respondent has a college degree are also included

in the analysis,’’ making it possible that the demographic variables

reflected the respondent.

Lyons (2003) did not discuss how demographic variables were mea-

sured or the difference between the respondent and the head. In her pre-

sentation of multivariate models, she referred to income of the head but

did not mention whose age, gender, and ethnicity was included. The dis-

cussion of the results referred to the age of the head, and two of the tables

listed age, education, and income variables as related to the head, but

other tables did not specify whether the variables were of the head or

respondent.

Lee and Kwon (2002) reported using the age of the respondent in their

table describing independent variables but did not identify whose education

or ethnicity was used. Ethnicity, by definition, had to be of the respondent.

However, given the mean value reported for age, it is likely that they used

the age of the head. Using the head’s demographic data to study the atti-

tudes expressed by the respondent is inappropriate without justification. If

both partners in couple households are of similar age, this error may not be

important. However, our analysis of the 1998 SCF (which Lee and Kwon

used) shows that 10% of married couples had an age difference of 11 years

or more, a difference that could have a biasing effect on analyses of age and

attitude.

Chien and DeVaney (2001) correctly stated that attitudes were provided

by the respondent but did not discuss the distinction between the head and

the respondent. They listed age as being of the head but did not identify

whose education was used in the analysis. They reported ethnicity as that of

the head, which is not possible because race/ethnicity data are available

only for the respondent.

Xiao et al. (2001) included only a couple of households in their analysis

of family business owners, but characterized the sample as including only

family heads. They reported that unlike previous research on business

owners, they did not use gender as an independent variable because

99% of their sample was male, correctly noting that the SCF coded

the male as the head in mixed-sex couple households and the older person

as the head in same-sex couple households. However, they did not report

that the head was not necessarily the respondent or the business owner

and did not report the proportion of respondents who were female. Their

WINTER 2007 VOLUME 41, NUMBER 2 199

discussion referred to the characteristics of the ‘‘family business owner’’;

yet, the analysis apparently was based on the age, race, and education of

the head. Using the head’s characteristics is problematic because those

characteristics were used to analyze the SCF risk tolerance variable, a vari-

able available only for the respondent. Although that variable is supposed

to reflect a couple’s risk tolerance, it is likely that it reflects the risk

tolerance of the respondent in married couple households (Hanna and

Lindamood 2005).

Race/Ethnicity of the Respondent

Race is a controversial topic (American Anthropological Association

1997), and even the title chosen to describe a group has importance.

The 2001 and 1998 SCFs did not directly use the term race or ethnicity

on the card that listed the respondent’s choices of race/ethnicity categories.

Instead, the researcher asked the respondent ‘‘which of these categories do

you feel best describe you?’’ when showing a card that directed: ‘‘Please list

your strongest identification first.’’ Even though seven identity categories

were offered to respondents, the SCF reports only four in the public data

set: white, black/African American, Hispanic/Latino, and Other. The

‘‘Other’’ category in the public dataset includes Asian, American Indian,

Alaska Native, and Native Hawaiian/Other Pacific Islander, as well as the

response ‘‘Other.’’ Earlier surveys (1989–1995) provided respondents with

a similar list of categories but asked them to identify their ‘‘race.’’ The 1983

race variable was determined only by interviewer observation. There were

some minor changes in terminology from 1983 to 2001 (Yao, Gutter, and

Hanna 2005).

The 1998–2001 surveys allowed respondents to indicate more than one

identity choice, but the public data sets include only two variables for race:

(1) the category of the respondent’s strongest identification and (2) whether

the respondent indicated additional categories of race/ethnic identification.

The categories of those additional choices are not reported in the public data

sets. Therefore, even though Federal Reserve Board publications list ‘‘non-

Hispanic white,’’ researchers using the public data sets before 2004 should not

use that description because they do not have the information to determine

whether all persons responding ‘‘white’’ were also non-Hispanic. The SCF

changed its method of asking race/ethnic questions for the 2004 survey, ask-

ing a separate Hispanic question in addition to the categories offered in the

1989 through 2001 surveys. Therefore, researchers using the 2004 SCF could

use the term non-Hispanic white by combining the results of the two variables,

200 THE JOURNAL OF CONSUMER AFFAIRS

although procedures should be carefully described because of the alternate

ways of presenting the race/ethnic data.1

Guidance in using race/ethnic variables and normative standards for

reporting race are available from several sources. The Office of Manage-

ment and Budget’s directive, The Statistical Policy Directive No. 15,Race and Ethnic Standards for Federal Statistics and AdministrativeReporting (commonly called OMB 15), provides useful guidelines andstandards that federal agencies and agencies receiving federal funds

(including universities) are to use in gathering and reporting data on race

and ethnicity (Office of Management and Budget 1997). Originally

adopted in 1977, the directive was updated in October 1997. Although

researchers who publish in this journal are not necessarily required

to follow the directive, the publication reflects decisions made after

hearings and comments from many individuals and organizations

and provides guidelines that reflect current thought on race and ethnic

classifications.

OMB 15 requires the use of specific categories when reporting race and

ethnicity data acquired with a single question format, such as the SCF race/

ethnic question for the 1989 through 2001 surveys. The SCF single ques-

tion format used during those years has categories identical to those

OMB 15 requires, except that the SCF also offered respondents the categoryOther. The SCF race/ethnicity information was collected and made avail-

able in a format that enables researchers to comply with the federal directive

just by using the SCF categories and names.

Some of the OMB 15 reporting conventions of which researchers shouldbe aware are the names that are appropriate for combined categories and the

names that are ‘‘prohibited.’’ The directive states that when categories of

race are combined, the terms ‘‘other races’’ and ‘‘all other races’’ are appro-

priate to describe the collapsed categories. The collapsed categories in the

SCF public data set are appropriately named Other. Certain names for

reporting data are not appropriate under OMB 15, however. Of note is

1. Researchers working with the 2004 SCF data set have a choice of using the variable based on the

single race/ethnic question or using that question in combination with the new separate question about

Hispanic status. The results will differ slightly depending upon the researcher’s choice. Our weighted

analysis of the 2004 SCF public data set shows that in the single question format that offered a choices

including ‘‘white’’ and ‘‘Hispanic,’’ 9.2% of the respondents chose Hispanic, but 11.2% of the respond-

ents chose Hispanic in the new separate question: Do you consider yourself to be Hispanic or Latino in

culture or origin? If that question is used with the traditional SCF race/ethnic question to create a cat-

egory ‘‘non-Hispanic white,’’ the results will differ slightly for the other categories. For instance, 73.6%

of respondents chose white in response to the traditional question, but excluding those who also

answered Hispanic produces the result that 71.8% of the respondents are non-Hispanic white.

WINTER 2007 VOLUME 41, NUMBER 2 201

the term ‘‘non-white.’’ The policy directive states, ‘‘The term �nonwhite’ isnot acceptable for use in the presentation of Federal Government data. It

shall not be used in any publication or in the text of any report’’ (Office of

Management and Budget 1997).

Some of the articles we reviewed renamed the race/ethnic categories

without clarifying or justifying the new names and used inappropriate

names. The most extreme deviation was use of the term ‘‘Caucasian.’’

Two articles published in 2001 (Table 1) used the term. The SCF does

not gather data using the term,2 and for that reason alone, its use is

not appropriate for analyses based on SCF data sets after 1986. The

American Heritage� Dictionary of the English Language (2000) under

its definition of Caucasian notes, ‘‘No longer in scientific use.’’ A report

by the American Anthropological Association (1997), commenting on the

proposed 1997 revision of OMB 15, discussed the controversies relating

to the definition of race and ethnicity and mentioned the racist origin of

the term Caucasian.

The different treatment of race/ethnic categories by authors underscores

the need for justification of groupings and names. In the six articles we

reviewed, the different race/ethnic category combinations resulted in

groupings with similar names but included different groups, so that accu-

rate comparisons cannot be made across studies (Table 1). Because of the

similar category names, readers could incorrectly assume comparability

and come to inaccurate conclusions about results.

Hogarth, Anguelov, and Lee (2004) reported only race/ethnic categories:

‘‘black,’’ ‘‘Hispanic,’’ and ‘‘white and other.’’ They formed the latter cat-

egory by combining the SCFwhite and Other categories, with the result that

Asian, American Indian, Alaska Native, Native Hawaiian, other Pacific

Islanders, and other groups were included with white. They did not offer

justification for grouping white and Other, but they did clearly report their

procedures.

Lee and Kwon (2002) reported race/ethnic category on the basis of the

four categories the SCF provided in the public data set. However, they

renamed the other category as ‘‘other non-white minorities.’’ The research-

ers introduced an element of confusion when they also used non-white to

describe a different grouping of respondents, stating ‘‘a greater percentage

of non-whites including black and Hispanic.’’ The renamed category, other

non-white minorities, is inconsistent with the OMB 15 directive to use the

2. The SCF instructs coders that if a respondent says ‘‘Caucasian,’’ the response should be coded as

‘‘white.’’ However, the respondent is not offered Caucasian as a choice.

202 THE JOURNAL OF CONSUMER AFFAIRS

term other races or all other races when grouping categories and the pro-

hibition of using the term non-white.

Getter (2003) did not describe how he measured race/ethnic variables. In

each of the two results tables, only one race/ethnic category was listed,

‘‘black or Hispanic,’’ indicating that these were combined and presumably

were compared with all others. No justification was given for combining

the two groups.

Lyons (2003) did not describe or justify how the race/ethnic variables in

her article were created. She presented a list of variables in one table of

results, which included only the category black, making it appear that black

was compared with all other categories combined. Another table, however,

compared ‘‘blacks’’ with whites, with no clarification of whether any other

categories were included with either blacks or whites. Lyons stated that the

table showed a trend for ‘‘all households,’’ so that a reader might assume

that all respondents were categorized as either black or white, making it

appear that white included ‘‘Hispanic’’ and Other.

Comparability and interpretation of research would be improved if

researchers reporting race/ethnicity data would use the categories that

are reported in the SCF data sets. A researcher who renames the categories

should justify doing so, and a researcher who collapses categories should

clearly report the components of the collapsed category along with a ratio-

nale for the action.

Multiple Implicates

Survey research inevitably results in missing data because of refusal to

answer or mistakes on the part of field staff. Researchers have a choice

between deleting cases with missing information and making a reasonable

estimate of that data by some method of imputation. Different methods of

imputingmissing data include usingmultiple regression to estimate the data

based on known characteristics of the respondent, using the mean of the

values obtained for those who responded, or randomly choosing a valid

response category to replace the missing data. The researcher’s goal should

be to make as close an estimate of the true value as possible and to keep bias

to a minimum.

Starting with the 1989 survey, the SCF has imputed missing values using

a ‘‘multiple imputation’’ method with a goal of providing data that are the

best possible estimate of the missing data. Instead of providing just one

estimate for a piece of missing data, multiple responses are provided for

each case to represent the likely range of responses for the particular

WINTER 2007 VOLUME 41, NUMBER 2 203

respondent. The multiple imputation method the SCF employs results in

each respondent having five different sets of data, which results in a total

data set with five times the actual number of households. The SCF refers to

each of the five data sets as an ‘‘implicate.’’ While it is possible to do an

analysis with just one implicate, the benefits of the multiple imputations

would be lost and the results may be biased. Researchers ideally should

use all five implicates with the ‘‘repeated-imputation inference’’ (RII)

method (Rubin 1987). The use of RII results in estimated variances that

more closely represent the true variances than would be obtained by using

just one implicate. Montalto and Sung (1996) demonstrated that signifi-

cance tests might have different results based on RII versus running anal-

yses on only one implicate.

The implicate system also serves to protect the privacy of the survey

households. As the codebook states, ‘‘Data were also blurred by other

means intentionally not specified’’ (Kennickell 2003). Our analysis of

the 2001 SCF, for example, shows that the number of white respondents

differs among the implicates, ranging from 3,579 in Implicates 1 and 5 to

3,583 in Implicate 4. Only 3,576 respondents are coded white in all five

implicates. We have no way of knowing whether race was missing for

these respondents or intentionally blurred to protect privacy. However,

the different values and different group sizes among the implicates sug-

gest that it is not appropriate to use only one implicate when analyzing

SCF data.

The RII technique may not be practical for some types of multivariate

analyses, but researchers always should note whether it is used and justify

the decision. None of the articles in this journal report using the RII method

in multivariate analyses (Table 1). Although, Hogarth, Anguelov and

Lee (2004) did not use RII, they justified not doing so and explained their

procedure:

. Stata does not provide the necessary output covariance matrices to use this tech-

nique with a multinomial logit analysis. Therefore, we must content ourselves with

analyzing the 5 implicate data sets separately. However, to make up for the inability

to use an RII technique, we apply a criterion that the parameter estimates must be

significant at the 0.05 level in at least 4 of the 5 implicate data sets in order for us to

count a variable as significant.

Lee and Kwon (2002) reported using RII for their means comparisons. In

their multivariate analysis, they only reported the results obtained for Impli-

cate 1 but stated that the results for the other four implicates were consistent

and available from the first author.

204 THE JOURNAL OF CONSUMER AFFAIRS

Getter (2003), Lyons (2003), and Xiao et al. (2001) did not discuss RII or

the implicates, so a reader cannot discern which implicates they used, what

procedure they used, or why they used that procedure. Chien and DeVaney

(2001) stated that they used only Implicate 1 without justifying why or

discussing possible problems of not using RII.

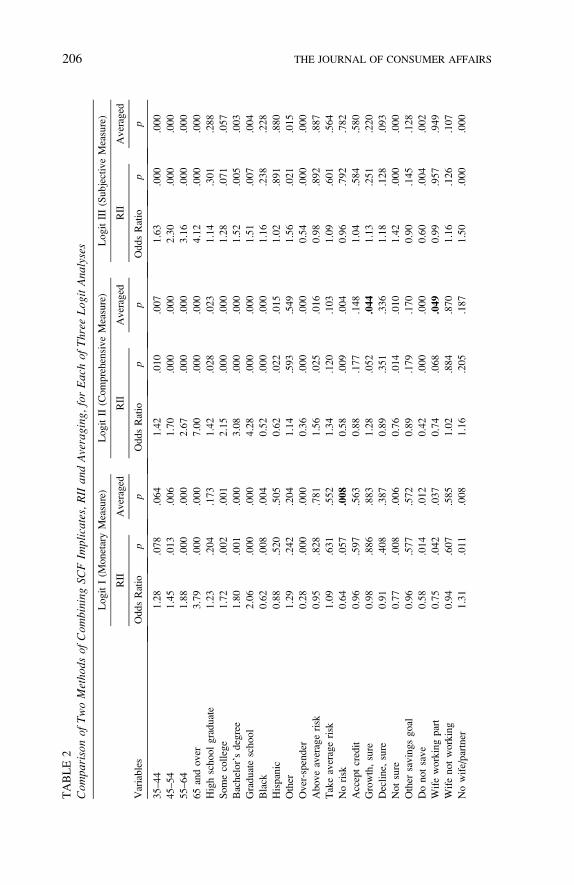

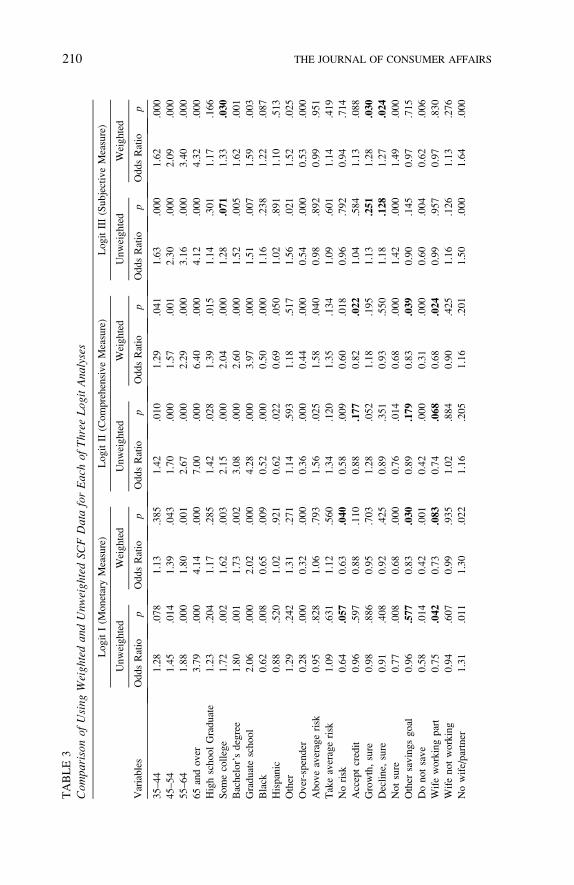

Controlled Comparisons between RII and Averaging Implicates

Is using RII important, and if it makes a difference, is that difference

great enough to justify the extra effort? To determine the possible impact

of not using RII, we performed original analyses to compare using a sim-

ple averaging technique with using RII. In our simple averaging tech-

nique, we combined all five implicates, then applied a constant weight

equal to 0.2 (the equivalent of dividing by five). To provide a controlled

comparison, we replicated the models Bi and Montalto (2004) used in

their logit analyses, in which they used the RII procedure. We took care

to assure that the only difference in our logit analyses and the Bi andMon-

talto logit analyses was whether RII or the averaging method was used to

combine the five implicates of the data set. The two methods produced

estimates of logistic regression coefficients that were equal, which we

expected based on the definition of the RII method for multivariate anal-

ysis. For the three logits we tested, with a total of 99 variables, three coef-

ficients not significant (p , .05) when using RII were statistically

significant when using the averaging method (Table 2).3 In general,

RII produced higher p values and therefore less significant results.

The differences, with some variables classified as not significant (p ,

.05) using RII but significant using the averaging method, occurred in

Logit I (Monetary) and Logit II (Comprehensive), in which the dependent

variables were based on financial data that presumably had many imputed

values. For instance, the variable ‘‘No Risk’’ in Logit I had a significance

level of .057 with RII, but with the averaging method, it had a significance

level of .008. In Logit III (Subjective), there were no differences in any

conventional significance levels (p, .05) between RII and the averaging

method for the 33 coefficients.

3. In order to have Tables 2 and 3 be more compact, we omitted the listings from Bi and Montalto

(2004) for the reference categories for sets of dummy variables. For instance, they listed ‘‘white, non-

Hispanic’’ as the reference category for the race/ethnic variables in the logits. The category for ‘‘black’’

was listed as ‘‘black, non-Hispanic.’’ Both ‘‘non-Hispanic’’ descriptions are inappropriate and should

have been white and black.

WINTER 2007 VOLUME 41, NUMBER 2 205

TABLE2

Com

parisonof

TwoMetho

dsof

Com

bining

SCFIm

plicates,RIIan

dAveraging

,forEachof

Three

Log

itAna

lyses

Variables

LogitI(M

onetaryMeasure)

LogitII(ComprehensiveMeasure)

LogitIII(SubjectiveMeasure)

RII

Averaged

RII

Averaged

RII

Averaged

OddsRatio

pp

OddsRatio

pp

OddsRatio

pp

35–44

1.28

.078

.064

1.42

.010

.007

1.63

.000

.000

45–54

1.45

.013

.006

1.70

.000

.000

2.30

.000

.000

55–64

1.88

.000

.000

2.67

.000

.000

3.16

.000

.000

65andover

3.79

.000

.000

7.00

.000

.000

4.12

.000

.000

Highschoolgraduate

1.23

.204

.173

1.42

.028

.023

1.14

.301

.288

Somecollege

1.72

.002

.001

2.15

.000

.000

1.28

.071

.057

Bachelor’sdegree

1.80

.001

.000

3.08

.000

.000

1.52

.005

.003

Graduateschool

2.06

.000

.000

4.28

.000

.000

1.51

.007

.004

Black

0.62

.008

.004

0.52

.000

.000

1.16

.238

.228

Hispanic

0.88

.520

.505

0.62

.022

.015

1.02

.891

.880

Other

1.29

.242

.204

1.14

.593

.549

1.56

.021

.015

Over-spender

0.28

.000

.000

0.36

.000

.000

0.54

.000

.000

Aboveaveragerisk

0.95

.828

.781

1.56

.025

.016

0.98

.892

.887

Takeaveragerisk

1.09

.631

.552

1.34

.120

.103

1.09

.601

.564

Norisk

0.64

.057

.008

0.58

.009

.004

0.96

.792

.782

Acceptcredit

0.96

.597

.563

0.88

.177

.148

1.04

.584

.580

Growth,sure

0.98

.886

.883

1.28

.052

.044

1.13

.251

.220

Decline,

sure

0.91

.408

.387

0.89

.351

.336

1.18

.128

.093

Notsure

0.77

.008

.006

0.76

.014

.010

1.42

.000

.000

Other

savingsgoal

0.96

.577

.572

0.89

.179

.170

0.90

.145

.128

Donotsave

0.58

.014

.012

0.42

.000

.000

0.60

.004

.002

Wifeworkingpart

0.75

.042

.037

0.74

.068

.049

0.99

.957

.949

Wifenotworking

0.94

.607

.585

1.02

.884

.870

1.16

.126

.107

Nowife/partner

1.31

.011

.008

1.16

.205

.187

1.50

.000

.000

206 THE JOURNAL OF CONSUMER AFFAIRS

Can

borrow

from

retirementaccount

0.98

.876

.867

1.14

.242

.201

0.72

.001

.000

Homeequity,$18,000

1.17

.301

.262

1.35

.040

.027

0.99

.921

.919

$18,001–$45,000

1.70

.000

.000

1.70

.000

.000

1.25

.103

.061

$45,001–$85,000

2.58

.000

.000

3.21

.000

.000

1.55

.001

.000

.$85,000

2.33

.000

.000

4.00

.000

.000

1.66

.000

.000

Creditcard

limit,$3,000

1.26

.163

.126

1.49

.006

.004

0.97

.837

.822

$3,001–$8,000

2.06

.000

.000

2.25

.000

.000

1.36

.013

.009

$8,001–$17,000

2.88

.000

.000

3.39

.000

.000

1.44

.005

.002

.$17,000

2.81

.000

.000

4.26

.000

.000

1.50

.001

.001

Note:Eachofthreelogisticmodelswas

analyzedusingboth

RIIandaveragingmethodofcombiningtheim

plicates.Themodelsusedin

thecomparisonswerethe

likelihoodofmeetingem

ergency

fundguidelines

(BiandMontalto2004)based

ondependentvariables:(I)Monetary,(II)Comprehensive,and(III)SubjectiveMeasures

ofAdequacy.W

eusedtheversionofthe1998SCFdatasetthatBiandMontaltoused,asresultsareslightlydifferentinthemostrecentversionofthe1998SCFdataset

posted

in2006.Allresultsarebased

onunweighteddata.TheRIIresultsarefromBiandMontalto(2004).Theaveragingmethodresultswerecalculatedbytheauthors

usingthesamemodelandvariablesas

BiandMontaltobutcombiningtheim

plicatesbyusingweight¼0.2withpooleddatafromthefiveim

plicates.Apvalueinbold

indicates

that

theaveragingmethodresultwas

significantat

the.05level,buttheRIItechniquewas

notsignificantat

the.05level.

WINTER 2007 VOLUME 41, NUMBER 2 207

Recommendations for Use of RII

Based on our analysis, it appears that for exploratory analyses for

conference presentations or for statistical methods where the RII coding

has not been defined, it would be reasonable to use either the averaging

method we tested or the four out of five implicate threshold approach

Hogarth, Anguelov and Lee (2004) discussed. Otherwise, researchers

should use RII for both descriptive and multivariate analyses, as suggested

in the SCF codebook (Kennickell 2003).

Weighting of Analyses

The SCF uses a dual sampling technique that includes a probability sam-

ple collected in specified geographic regions and a sample from the tax list

provided by the Internal Revenue Service for those same regions (Kennickell

2003). The resulting sample overrepresents higher wealth groups and there-

fore is not representative of the U.S. population as a whole. The SCF pro-

vides weights that researchers may use to obtain estimates of the U.S.

population. Referring to the need to weight data, the 2001 SCF codebook

(Kennickell 2003) stated:

Because the SCF sample is not an equal-probability design, weights play a critical

role in interpreting the survey data. The main data set contains the final nonresponse-

adjusted sampling weights. These weights are intended to compensate for unequal

probabilities of selection in the original design and for unit nonresponse (failure to

obtain an interview).

Therefore, it is necessary to weight descriptive analyses to make the results

representative of U.S. households. As an example of the skewed results

obtained from unweighted data, our calculations show that the mean net

worth of households in the 2001 SCF, based on the population weight,

was $395,837, but the unweighted mean net worth was $6,882,747. Even

the median net worth was far higher without weighting, $189,580, com-

pared with $86,100 when calculated with weighting. The issue of weight-

ing in multivariate analyses, such as regression analysis, is controversial

(Kennickell 2003). Weighting regression analyses when the weights are

endogenous is suspect for hypothesis testing (Deaton 1997, 66–73; and

noted by Yao, Hanna, and Lindamood 2004).

None of the articles we reviewed in this or other journals discussed

the issue of weighting multivariate analyses. Xiao et al. (2001) noted that

the population weight was used in all analyses so that the results could be

208 THE JOURNAL OF CONSUMER AFFAIRS

generalized to all families owning a business in the United States. Lyons

(2003) stated in her footnote to Table 1 that in ‘‘. all remaining tables,

observations are weighted .,’’ which implies that her multivariate anal-

yses in tables 3–5 were weighted. Hogarth, Anguelov, and Lee (2004)

had an excellent discussion of the need for weighting but did not explicitly

state whether they weighted their multivariate analysis. Getter (2003) noted

that the Canner, Gabriel, andWoolley (1991) analysis had used weights but

stated that the weights created for the different survey years he used could

not be used with combined data, making it appear that he did not weight the

data. Lee and Kwon discussed weighting of their means comparisons but

did not discuss whether they weighted their multivariate analysis.

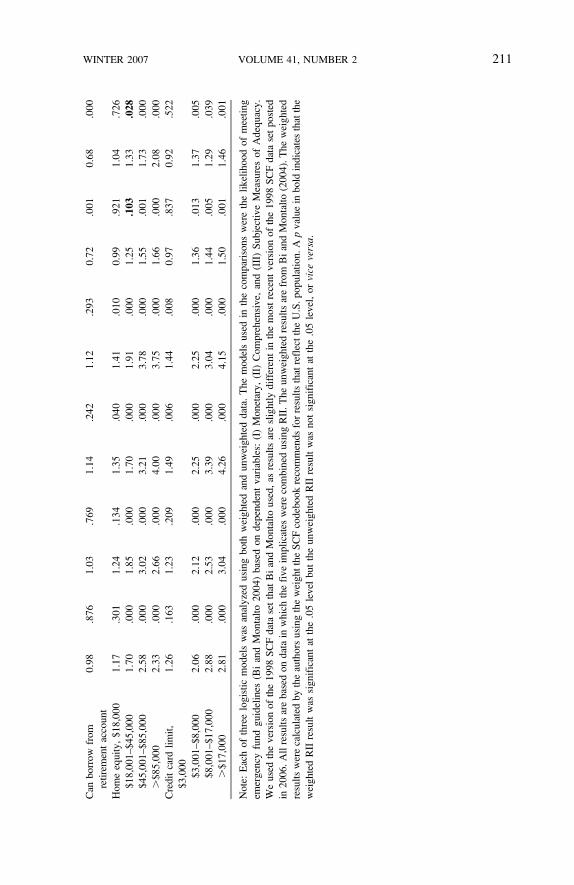

Controlled Comparisons between Weighted and Unweighted

Multivariate Analyses

To compare the effects of using weighted versus unweighted data in

multivariate analyses, we performed a controlled comparison by using

weighted data to analyze the same three logit regression models that Bi

and Montalto (2004) had analyzed with unweighted data. For our weighted

analysis, we applied the SCF population weight scaled so that the total

apparent sample size for each implicate equaled the actual sample size.

Both our weighted analyses and the Bi and Montalto unweighted analyses

used the RII method of combining the five implicates. The results of using

weighted compared with unweighted data generally were similar (Table 3),

with most of the magnitudes of effects (as shown by the odds ratios) being

similar between unweighted and weighted analyses. However, out of 99

coefficients in the three logits, nine were significant at the .05 level in

the weighted analyses but not significant in the unweighted analyses, and

one was significant at the .05 level in the unweighted analysis but not in

the weighted analysis. Given that the preferred approach is to use unweighted

data, it is notable that in Logit I (Monetary), the variable ‘‘Wife Working

Part-Time’’ is significant at the .042 level in the unweighted analysis, while

in the weighted analysis, it is significant at the .083 level.

Recommendations for Weighting Multivariate Analyses

In determining whether weighted or unweighted data should be used in

multivariate analyses, we should not presume that the unweighted estimates

are valid and the weighted estimates are invalid. In particular, if the multi-

variate analysis does not adequately control for variables that are skewed due

to the sampling rate variations, the effects of some variables of interest might

WINTER 2007 VOLUME 41, NUMBER 2 209

TABLE3

Com

parisonof

Using

Weigh

tedan

dUnw

eigh

tedSC

FDataforEachof

Three

Log

itAna

lyses

Variables

LogitI(M

onetaryMeasure)

LogitII(ComprehensiveMeasure)

LogitIII(SubjectiveMeasure)

Unweighted

Weighted

Unweighted

Weighted

Unweighted

Weighted

OddsRatio

pOddsRatio

pOddsRatio

pOddsRatio

pOddsRatio

pOddsRatio

p

35–44

1.28

.078

1.13

.385

1.42

.010

1.29

.041

1.63

.000

1.62

.000

45–54

1.45

.014

1.39

.043

1.70

.000

1.57

.001

2.30

.000

2.09

.000

55–64

1.88

.000

1.80

.001

2.67

.000

2.29

.000

3.16

.000

3.40

.000

65andover

3.79

.000

4.14

.000

7.00

.000

6.40

.000

4.12

.000

4.32

.000

HighschoolGraduate

1.23

.204

1.17

.285

1.42

.028

1.39

.015

1.14

.301

1.17

.166

Somecollege

1.72

.002

1.62

.003

2.15

.000

2.04

.000

1.28

.071

1.33

.030

Bachelor’sdegree

1.80

.001

1.73

.002

3.08

.000

2.60

.000

1.52

.005

1.62

.001

Graduateschool

2.06

.000

2.02

.000

4.28

.000

3.97

.000

1.51

.007

1.59

.003

Black

0.62

.008

0.65

.009

0.52

.000

0.50

.000

1.16

.238

1.22

.087

Hispanic

0.88

.520

1.02

.921

0.62

.022

0.69

.050

1.02

.891

1.10

.513

Other

1.29

.242

1.31

.271

1.14

.593

1.18

.517

1.56

.021

1.52

.025

Over-spender

0.28

.000

0.32

.000

0.36

.000

0.44

.000

0.54

.000

0.53

.000

Aboveaveragerisk

0.95

.828

1.06

.793

1.56

.025

1.58

.040

0.98

.892

0.99

.951

Takeaveragerisk

1.09

.631

1.12

.560

1.34

.120

1.35

.134

1.09

.601

1.14

.419

Norisk

0.64

.057

0.63

.040

0.58

.009

0.60

.018

0.96

.792

0.94

.714

Acceptcredit

0.96

.597

0.88

.110

0.88

.177

0.82

.022

1.04

.584

1.13

.088

Growth,sure

0.98

.886

0.95

.703

1.28

.052

1.18

.195

1.13

.251

1.28

.030

Decline,

sure

0.91

.408

0.92

.425

0.89

.351

0.93

.550

1.18

.128

1.27

.024

Notsure

0.77

.008

0.68

.000

0.76

.014

0.68

.000

1.42

.000

1.49

.000

Other

savingsgoal

0.96

.577

0.83

.030

0.89

.179

0.83

.039

0.90

.145

0.97

.715

Donotsave

0.58

.014

0.42

.001

0.42

.000

0.31

.000

0.60

.004

0.62

.006

Wifeworkingpart

0.75

.042

0.73

.083

0.74

.068

0.68

.024

0.99

.957

0.97

.830

Wifenotworking

0.94

.607

0.99

.935

1.02

.884

0.90

.425

1.16

.126

1.13

.276

Nowife/partner

1.31

.011

1.30

.022

1.16

.205

1.16

.201

1.50

.000

1.64

.000

210 THE JOURNAL OF CONSUMER AFFAIRS

Can

borrow

from

retirementaccount

0.98

.876

1.03

.769

1.14

.242

1.12

.293

0.72

.001

0.68

.000

Homeequity,$18,000

1.17

.301

1.24

.134

1.35

.040

1.41

.010

0.99

.921

1.04

.726

$18,001–$45,000

1.70

.000

1.85

.000

1.70

.000

1.91

.000

1.25

.103

1.33

.028

$45,001–$85,000

2.58

.000

3.02

.000

3.21

.000

3.78

.000

1.55

.001

1.73

.000

.$85,000

2.33

.000

2.66

.000

4.00

.000

3.75

.000

1.66

.000

2.08

.000

Creditcard

limit,

$3,000

1.26

.163

1.23

.209

1.49

.006

1.44

.008

0.97

.837

0.92

.522

$3,001–$8,000

2.06

.000

2.12

.000

2.25

.000

2.25

.000

1.36

.013

1.37

.005

$8,001–$17,000

2.88

.000

2.53

.000

3.39

.000

3.04

.000

1.44

.005

1.29

.039

.$17,000

2.81

.000

3.04

.000

4.26

.000

4.15

.000

1.50

.001

1.46

.001

Note:Eachofthreelogisticmodelswas

analyzedusingboth

weightedandunweighteddata.

Themodelsusedin

thecomparisonswerethelikelihoodofmeeting

emergency

fundguidelines

(BiandMontalto2004)based

ondependentvariables:

(I)Monetary,(II)Comprehensive,

and(III)SubjectiveMeasuresofAdequacy.

Weusedtheversionofthe1998SCFdatasetthat

BiandMontaltoused,as

resultsareslightlydifferentin

themostrecentversionofthe1998SCFdatasetposted

in2006.Allresultsarebased

ondatain

whichthefiveim

plicateswerecombined

usingRII.Theunweightedresultsarefrom

BiandMontalto(2004).Theweighted

resultswerecalculatedbytheauthorsusingtheweighttheSCFcodebookrecommendsforresultsthatreflecttheU.S.population.Apvaluein

bold

indicates

thatthe

weightedRIIresultwas

significantat

the.05level

buttheunweightedRIIresultwas

notsignificantat

the.05level,orvice

versa.

WINTER 2007 VOLUME 41, NUMBER 2 211

be distorted. Deaton (1997, 72) suggested that it would be wise to examine

both weighted and unweighted results frommultivariate analyses. If an effect

is significant in both analyses, presumably we can be more confident about

the result. As noted above, our comparisons found 10 coefficients out of 99

differed in significance levels between unweighted logits and weighted log-

its. Nine of those differences were for variables that met the .05 level of

significance in the weighted logits but not in the unweighted logits and

one was for the reverse, meeting the .05 level in the unweighted logit but

not in the weighted logit. Using the more conservative .01 significance level

would have no differences in terms of the significance threshold.

Presenting the p values, rather than indicators of significance thresholds,seems a reasonable approach in reporting results, as then the reader can

consider the relative importance of Type I or Type II errors in evaluating

the conclusions. The practice of presenting only notes of significance cat-

egories is questionable, as effects that are close to the conventional level of

.05 may switch due to weighting or lack of weighting as well as model

specification issues.

Unlike the comparison between the RII and averaging method of com-

bining implicates, the case for using weighted or unweighted data is not one

of the complete superiority of one approach over the other. In a majority of

the estimates, the significance level estimated is more conservative for

unweighted data than for weighted data, so presenting the unweighted results

in publications seems reasonable. It also seems reasonable, however, for

researchers to follow the advice of Deaton (1997) and try both unweighted

and weighted analyses. If the most important variable in an analysis is sig-

nificant using the unweighted analysis but not significant using the weighted

analysis, the researcher should reconsider the model specification.

CONCLUSIONS

Authors of research reports should accurately describe and justify

their methods with sufficient detail to enable readers to evaluate the

findings and researchers to replicate the research. Many of the articles

we reviewed using the SCF data sets, including recent articles in this

journal, did not provide a sufficient level of detail or justify important

choices made in analyses. Readers and reviewers of research using the

SCF data sets should be aware of these issues. The problems identified

are common in research using the SCF data sets in many other journals, and

there may well be similar problems with research using other data sets. Some

of the problems we identified are simply a matter of inadequate discussions

of methods. It is unlikely that the problems we identified would affect the

212 THE JOURNAL OF CONSUMER AFFAIRS

main conclusions in any of the articles. It would be desirable, however, for

authors to more carefully describe and justify their methods so that readers

have a better understanding of the results and future researchers can more

efficiently build upon published research.

REFERENCES

Aizcorbe, Ana M., Arthur B. Kennickell, and Kevin B. Moore. 2003. Recent Changes in U.S. Family

Finances: Results from the 1998 and 2001 Survey of Consumer Finances. Federal Reserve Bulletin,

89 (January): 1–32.

American Anthropological Association. 1997. Response to OMB Directive 15: Race and Ethnic Stand-

ards for Federal Statistics and Administrative Reporting. http://www.aaanet.org/gvt/ombdraft.htm.

American Heritage� Dictionary of the English Language. 2000. Boston: Houghton Mifflin. http://

www.bartleby.com/61/.

Bi, Lan and Catherine P. Montalto. 2004. Emergency Funds and Alternative Forms of Saving.

Financial Services Review, 13 (2): 93–109. http://www.rmi.gsu.edu/FSR/abstracts/Vol13/zux00204000093.

PDF.

Canner, Glenn B., Stuart A. Gabriel, and J. Michael Woolley. 1991. Race, Default Risk and Mortgage

Lending: A Study of the FHA and Conventional LoanMarkets. Southern Economic Journal, 58 (1):249–262.

Chien, Yi-Wen and Sharon A. DeVaney. 2001. The Effects of Credit Attitude and Socioeconomic Fac-

tors on Credit Card and Installment Debt. The Journal of Consumer Affairs, 35 (1): 162–179.

Deaton, Angus. 1997. The Analysis of Household Surveys: A Microeconometric Approach to Devel-

opment Policy. Baltimore, MD: Johns Hopkins University Press.

Getter, Darryl E. 2003. Contributing to the Delinquency of Borrowers. Journal of Consumer Affairs,

37 (1): 86–100.

Hanna, Sherman D. 2006. SCF Users Web Page. http://hec.osu.edu/scf/.

Hanna, Sherman D. and Suzanne Lindamood. 2005. Risk Tolerance of Married Couples. Proceedings

of the Academy of Financial Services, http://www.academyfinancial.org/.

Hogarth, JeanneM., Chris E. Anguelov, and Jinkook Lee. 2004.Why Don’t Households Have a Check-

ing Account? Journal of Consumer Affairs, 38 (1): 1–34.

Kennickell, Arthur B. 2003.Codebook for 2001 Survey of Consumer Finances. Washington, DC: Board

of Governors of the Federal Reserve System. http://www.federalreserve.gov/pubs/oss/oss2/2001/

codebk2001.txt.

Lee, Jinkook and Kyoung-Nan Kwon. 2002. Consumers’ Use of Credit Cards: Store Credit Card Usage

as an Alternative Payment and Financing Medium. The Journal of Consumer Affairs, 36 (2):

239–262.

Lindamood, Suzanne and Sherman D. Hanna. 2005. Determinants of the Wife Being the Financially

Knowledgeable Spouse. Proceedings of the Academy of Financial Services, http://www.academy-

financial.org/.

———. 2006. The More Financially Knowledgeable Person in Older Couple Households. ConsumerInterests Annual, 52: 327–342.

Lyons, Angela C. 2003. How Credit Access Has Changed Over Time for U.S. Households. Journal of

Consumer Affairs, 37 (2), 231–255.

Montalto, Catherine P. and Jaimie Sung. 1996. Multiple Imputation in the 1992 Survey of Consumer

Finances. Financial Counseling and Planning, 7: 133–146.

Office of Management and Budget. 1997. Revisions to the Standards for the Classification of Federal

Data on Race and Ethnicity. www.whitehouse.gov/omb/fedreg/print/ombdir15.html.

Rubin, Donald B. 1987. Multiple Imputation for Nonresponse in Surveys. New York: John

Wiley & Sons.

WINTER 2007 VOLUME 41, NUMBER 2 213

Xiao, Jing J., M. J. Alhabeeb, Gong-Soog Hong, and George W. Haynes. 2001. Attitude Toward

Risk and Risk-Taking Behavior of Business-Owning Families. Journal of Consumer Affairs,

35 (2): 307–325.

Yao, Rui, Michael S. Gutter, and Sherman D. Hanna. 2005. The Financial Risk Tolerance of Blacks,

Hispanics and Whites. Financial Counseling and Planning, 16 (1): 51–62.

Yao, Rui, Sherman D. Hanna, and Suzanne Lindamood. 2004. Changes in Financial Risk Tolerance,

1983-2001. Financial Services Review, 13 (4), 249–266.

Sins, Sinners, Data, and Details, Commentary by Jeanne M. Hogarth,Consumer Education & Research, Consumer & Community Affairs, Federal Reserve Board,

Washington, DC ([email protected])

Having failed at some of the issues Lindamood, Hanna, and Bi identify,

let me first confess—mea culpa. I have done those things that I ought not to

have done (such as use only one implicate of the Survey of Consumer

Finances, SCF) and I have not done those things that I ought to have done

(such as not explaining variables and methods clearly). I will try to not let

these things happen again.

Lindamood, Hanna, and Bi have written an article that invites us all to

reflect on the standards and reputation of the field of consumer research.

As I read the article, I believe they raised two main issues—how careful

we are in our data analysis (what might be in Huston’s commentary called

a sin of commission) and how careful we are in reporting our results (in

Huston’s terms, the sin of omission of relevant details). Their comments

apply not only specifically to the SCF but also more generally to all data

sets and research reporting—for anyone to skip reading this article just

because they do not use the SCF would be a serious sin of omission,

to say the least.

As researchers, our results are only as good as the data we use to build

our models. We want data that are clean and robust—data that are truly

representative of the groups we are studying—so that we can trust the

outcome of our analysis. We rely on data providers—be it government

data, academic research center data, or private survey data—to provide

us with accurate data from a representative sample and good docu-

mentation. In turn, it is our responsibility as researchers to respect the

data we use—to learn its limits and handle it appropriately, whether our

The analysis and conclusions set forth in this article represent the work of the author and do not

indicate concurrence of the Federal Reserve Board, the Federal Reserve Banks, or their staff. Mention

or display of a trademark, proprietary product, or firm in the presentation by the author does not con-

stitute an endorsement or criticism by the Federal Reserve System and does not imply approval to the

exclusion of other suitable products or firms.

214 THE JOURNAL OF CONSUMER AFFAIRS

data are from a small, local program evaluation or a large, nationally repre-

sentative survey.

There is no doubt that the SCF is a wonderfully detailed—and nuan-

ced—data set. Any first-time user needs to spend a lot of time reviewing the

codebook materials or, even better, collaborating with a more experienced

user. The breadth, depth, and detail of the data can be almost overwhelm-

ing. For researchers, this means that wemust carefully identify the variables

wewant to work with and note their definition—whowas the respondent and

on whose behalf did the respondent answer. For example, Klawitter and

Fletschner (2006) provide an interesting analysis of the individual and joint

saving and checking account holdings of married and unmarried different-

sex couples. This particular article represents a tour de force in the intricacies

of the SCF—we have respondents, spouses, and partners and we have indi-

vidually owned assets as well as jointly owned assets. Keeping all the asso-

ciations straight can be a challenge for both the researcher and the reader.

Issues of differentiating the respondent versus the primary economic unit

head and handling the five implicate data sets may be only the tip of the

SCF iceberg. Depending on the research question under study, researchers

need to know when to maintain distinctions of respondent, head, and other

family members and when aggregation is both acceptable and preferable.

Similarly, it is important to aggregate in a way that makes sense for the

research design but at the same time is true to the data. Lindamood, Hanna,

and Bi make a special plea for care in aggregating across racial categories.

The same could be said for a number of other variables in the SCF as well as

other large data sets, such as the Consumer Expenditure Survey, the Survey

of Income and Program Participation, and the Health and Retirement Study,

among others.

Selecting the right variables for our analyses, using the appropriate

analysis tools, and making use of all the available data are perhaps the

more ‘‘technological’’ aspects of our research. And technical accuracy

is a necessary component of any rigorous research. Communicating

our results, on the other hand, is the more artful aspect of our work,

and it is here that we may be falling short. Much of the critique that Lin-

damood, Hanna and Bi make really has to do with the care and clarity of

our writing.

Few would deny that ‘‘household’’ is a more reader-friendly term than

‘‘primary economic unit’’ (and perhaps a more human and humane one as

well). But we should be explicit about terms we use interchangeably—or

better yet, select one term and stick with it throughout the article to avoid

confusion. The challenge for all of us is to find the right balance between

accurately describing what we did and how we did it and not overwhelming

WINTER 2007 VOLUME 41, NUMBER 2 215

the reader with technical details that get in the way of the results (and

annoying reviewers and editors). Huston’s commentary highlights the

American Economic Review’s data availability policy as an alternative

for lengthy data and variable descriptions—yet such a policy would not

have addressed the concerns raised by Lindamood, Hanna, and Bi regard-

ing clear definitions of variables and research protocols.

There are some problems raised by Lindamood, Hanna, and Bi that are

endogenous to the type of models we build—our unit of analysis may be the

household (e.g., a household’s net worth or level of indebtedness), but

many of the control measures we want to use (age, race, and education)

are specific to an individual within the household. The solution to this

is, as pointed out by Lindamood, Hanna, and Bi, is to clearly define our

measures and use the appropriate terms in our writing.

For me, the main message of the Lindamood, Hanna, and Bi article is

that it is all about respect—respecting the data and respecting the reader. If

we as researchers keep this in mind, everything else will fall into place.

REFERENCES

Klawitter, Marieka and Diana Fletschner. 2006. Banked or Unbanked? Individual and Family Access

to Savings and Checking Accounts. Paper prepared for Closing the Wealth Gap Research Forum

sponsored by CFED, September 19, 2006. http://www.frbsf.org/community/research/assets/

BankedorUnbanked.pdf.

Commentary by Darryl E. Getter, Specialist in Financial Economics, Congressional

Research Service, Library of Congress, Washington, DC ([email protected])

In their article, Lindamood, Hanna, and Bi discuss methodological errors

they believe other researchers have made while using the Surveys of Con-

sumer Finances (SCF). Because the article ineluctably could be read as an

attack on some quality work previously published from the database, my

discussion will provide context for reviewing these works. This note would

therefore explain past SCF-based studies and give additional directions for

future analysis.

The authors disagree with how some of the researchers have defined

variables used in their analysis. For example, they recommend that all

researchers using the SCF race variables should define them according

to guidelines set by the Office of Management and Budget. Generally

speaking, researchers should have the freedom to define variables the

216 THE JOURNAL OF CONSUMER AFFAIRS

way they see fit in order to answer their particular research questions. Read-

ers may feel that more suitable variable definitions could be used to answer

a particular research question but that does not necessarily mean that a

methodological error was made. If a reader believes that a respecification

of a variable definition will alter previously published empirical results, then

the burden falls upon that reader to perform another analysis and present new

findings that incorporate the improved variable definitions. With regard to

the specific criticism of how previous authors used the race variable, those

criticisms seem rather unfair. Researchers are limited to the questions avail-

able. If the SCF did not explicitly break race into ethnicity groups or simply

did not collect race information in accordance with the federal guidelines

prior to 2004, then researchers should not be criticized for doing the best

they can with the variables available to them at the time.

Lindamood, Hanna, and Bi also criticize authors who do not distinguish

between the ‘‘respondent’’ and the ‘‘household head.’’ Again, there is no

reason to suspect that a methodological error has occurred when these terms

are used interchangeably in articles. The SCF codes the answers of the

household head separately from those of the spouse. Looking at the online

SCF codebook, the responses of the household head clearly appear above

those of the spouse or second household member. Even if the second

respondent answers questions on behalf of the household head, the SCF

staff goes through the responses and assigns them to the appropriate indi-

vidual. Assuming a competent researcher uses the correct SCF variable

codes consistent with the household head’s responses, there really is no

reason to suspect any confusion. Moreover, such a distinction between

the respondent and the household head may only matter for certain types

of research questions or if the respondent were of a race different from that

of the household head, for example, suppose a non-white respondent who

was not the head reports belonging to a minority household even though the

household head is white. That response may not be entirely inaccurate since

the household does consist of a person who belongs to an official minority

group. Nevertheless, the care with which the SCF staff codes variables sug-

gests that it is unnecessary for a researcher to go out of his or her way to talk

about this distinction. All the researcher must do is to pay close attention

and choose the correct variable code from the codebook.

The suggestion that SCF researchers should always discuss whether or

not all five implicates are being used is simply unnecessary. Most research-

ers would presume all five implicates are being used, and the only reason

to bring up this issue would be if a researcher had a good reason for notusing all five implicates. Generally, the SCF staff recommends using all

WINTER 2007 VOLUME 41, NUMBER 2 217

implicates at all times. Of course, to avoid incorrectly reporting a sample

size inflated by a factor of five, authors may prefer to divide the total num-

ber of observations by five and report a sample size closer to the truth.

Furthermore, it is not necessary for researchers to rehash the discussion

about the SCF implicates in their academic articles when they can simply

reference the Federal Reserve Bulletin articles written on this topic. In fact,it makes far more sense for readers to go directly to publications by the

Federal Reserve staff who construct the SCF to find out the specific details

about the implicates, how to use the weights, etc.

While it is true many researchers using the SCF data have varying levels

of familiarity and expertise pertaining to the correct way to use them, this

problem is universal for all data sets. Many published articles, even after

having been presented several times and surviving the intense scrutiny of

the journal review process, may still have what appears to be errors—

especially when various details have been omitted. Perhaps such details were

left out because authors considered them to be excessive and detracted from

the readability or flow of their papers. Some journal editors or referees will

ask authors to be more concise or limit their use of footnotes, which forces

them to omit certain details. As a result, it may be incorrect to assume that

highly scrutinized papers contain errors without first contacting researchers

directly to ask clarification questions. Finally, I certainly believe that

researchers should be open-minded to criticisms since one is never too

old to learn frommistakes. On the other hand, it would be extremely helpful

if critics, in addition to pointing out the shortcomings of published works,

would take advantage of the opportunity to contribute to academic discus-

sions by publishing new and improved findings.

Commentary by Sandra J. Huston, Research Associate at the Center for Financial

Responsibility, Texas Tech University, Lubbock, TX ([email protected])

Not since Montalto and Sung (1996) has such a useful tool been made

available to researchers who use the Survey of Consumer Finances (SCF)

data. Montalto and Sung (1996) provide a SAS macro that allows

researchers to combine the five data implicates using the repeated impu-

tation inference technique.1 Lindamood, Hanna, and Bi reiterate the

importance of using all available data (i.e., incorporating all five

1. A SAS program for repeated imputation inference procedures, fromMontalto and Sung (1996), is

available online at hec.osu.edu/people/shanna/imput.htm. The SAS macro is also referenced on the

Federal Reserve Board’s SCF data Web site at www.federalreserve.gov/pubs/oss/oss2/scfindex.html.

218 THE JOURNAL OF CONSUMER AFFAIRS

implicates of data) and identify three additional concerns regarding the

use of SCF data: head versus respondent, race and ethnicity specification,

and weighting. The authors highlight the improper use of the SCF data

that involve errors of both commission and omission. Do researchers fail

to incorporate proper data techniques into their research? Do researchers

fail to adequately report the data manipulation and method(s) used? Or do

researchers fail on both accounts?

An error of commission (e.g., using only one implicate of data rather

than all five implicates) should be discouraged. When there is an error

of omission (failing to report if all data were used), the reader is left to

wonder if all implicates were included and, if so, what technique was used

to combine the implicates.

As social scientists and responsible authors and reviewers, we should

insist on reducing both errors. What is the most efficient way to ensure

correct use of SCF data? Lindamood, Hanna, and Bi certainly make the

case that the four issues raised are important to researchers using the

SCF, but unfortunately they do not explicitly provide remedies within their

article. However, information, including specific SAS code for three of the

four issues raised, is available at the SCF Users Group Web site within the

Dataset Section (www.hec.ohio-state.edu/scf/). While it may be true that

many of the findings from the highlighted studies would not be drastically

altered, we should all be interested in making sure ‘‘it is done right’’ for

the sake of replication, scientific advancement, and training of future

researchers.

The importance of this article will ultimately be determined by authors

and reviewers who will themselves decide the value of doing it right or

simply doing it well enough. Following the important contribution of

Montalto and Sung (1996), Lindamood, Hanna, and Bi reaffirm that

‘‘Researchers ideally should use all five implicates with the �repeated-imputation inference’ (RII) method’’ (Rubin, 1987). More than a decade

later, it seems unreasonable to accept for publication research that does

not use all five implicates. There are studies available that provide

evidence of biased results when all available data are not used (see Lin-

damood, Hanna, and Bi for references). The Federal Reserve Board pro-

vides excellent resources to guide researchers on how to combine the data

for both descriptive and multivariate analyses (www.federalreserve.gov/

pubs/oss/oss2/faq.html). Given evidence from previous research and

the ease with which authors can use the available data correctly, it is

fair to say that this error of commission is not acceptable. And, as

highlighted in Lindamood, Hanna, and Bi, when using all five implicates,

the repeated imputation inference technique is clearly better than averaging.

WINTER 2007 VOLUME 41, NUMBER 2 219

Distinguishing between the primary economic unit head (or household

head) and the designated respondent is important when analyzing couple

households. All respondent-level variables (e.g., X14, X5901) are assigned

to the male (in mixed-sex couples) or the older person (in same-sex cou-

ples) regardless of whether that person actually provided the data. In the

SCF data, variable X8000 can be used to check if the primary economic unit

head (male or oldest person) is in fact the survey respondent.2 To properly

attribute employment, pension, and demographic characteristics to the

actual respondent, a SAS code example for education and marital status

is available at hec.osu.edu/scf/RespondentversusheadinSurveyConsumer-

Finances.htm. This code could be used and modified for all separately col-

lected respondent/spouse or partner variables included in research using the

SCF data. SAS code to assist in creating race variables using both questions

in the 2004 SCF data (X6809 and X7004) is available at hec.osu.edu/scf/

Race_ethnic%20status%20in%20the%202004%20SCF.htm.

To weight or not to weight is one of the most contentious and unresolved

questions posed by SCF researchers. The answer is a resounding yes for

descriptive statistics but, as Lindamood, Hanna, and Bi point out, not so

clear for multivariate analyses. Using unweighted data for multivariate

analyses is a conservative default position. But if researchers want to follow

the recommendation of Deaton (1997), and now Lindamood, Hanna, and

Bi, to compare results between weighted and unweighted regressions, how

does one get a weighted sample? Lindamood, Hanna, and Bi, state, ‘‘For

our weighted analysis, we applied the SCF population weight scaled so that

the total apparent sample size for each implicate equaled the actual sample

size.’’ Unfortunately, at this time there is no SAS code available at the SCF

Users Group Web site to guide researchers in this process. Perhaps the