Using Financial Information and Accounting Chapter 14

Using Financial Information and Accounting Chapter 14.

Dec 13, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Using FinancialInformation and Accounting

Using FinancialInformation and Accounting

Chapter 14

Chapter 14 Learning Goals

• Why are financial reports and accounting information important, and who uses them?

• What are the differences between public and private accountants?

• What are the six steps in the accounting cycle?• In what terms does the balance sheet describe the

financial condition of an organization?

Chapter 14 Learning Goals (cont’d.)

• How does the income statement report a firm’s profitability?

• Why is the statement of cash flows an important source of information?

• How can ratio analysis be used to identify a firm’s financial strengths and weaknesses?

• What major trends are affecting the accounting industry today?

Learning Goal 1• Why are financial reports and accounting

information important, and who uses them?– Financial reports give information about a company’s past,

present and future performance to:• Managers

– Can use reports to make decisions about firm’s operations

• Employees• Investors and customers• Suppliers, creditors, and government agencies

AccountingAccounting::

The process of collecting, recording, classifying, summarizing, reporting, and analyzing financial activities; results in reports that describe the financial condition of an organization

Learning Goal 2• What are the differences between public and private

accountants?– Public accountants

• Work for independent firms that provide accounting services to other organizations on a fee basis

– Financial report preparation and auditing

– Tax return preparation

– Management consulting

– Private accountants• Employed to serve one particular organization

– Prepare financial statements

– Tax returns

– Management reports

Public accountantPublic accountant::

Independent accountant who serves organizations & individuals on a fee basis; offers a wide range of services including preparation of financial statements & tax returns, independent auditing, & management consulting

Private accountantPrivate accountant::

Accountant who is employed by one particular organization and works only for it

Learning Goal 3

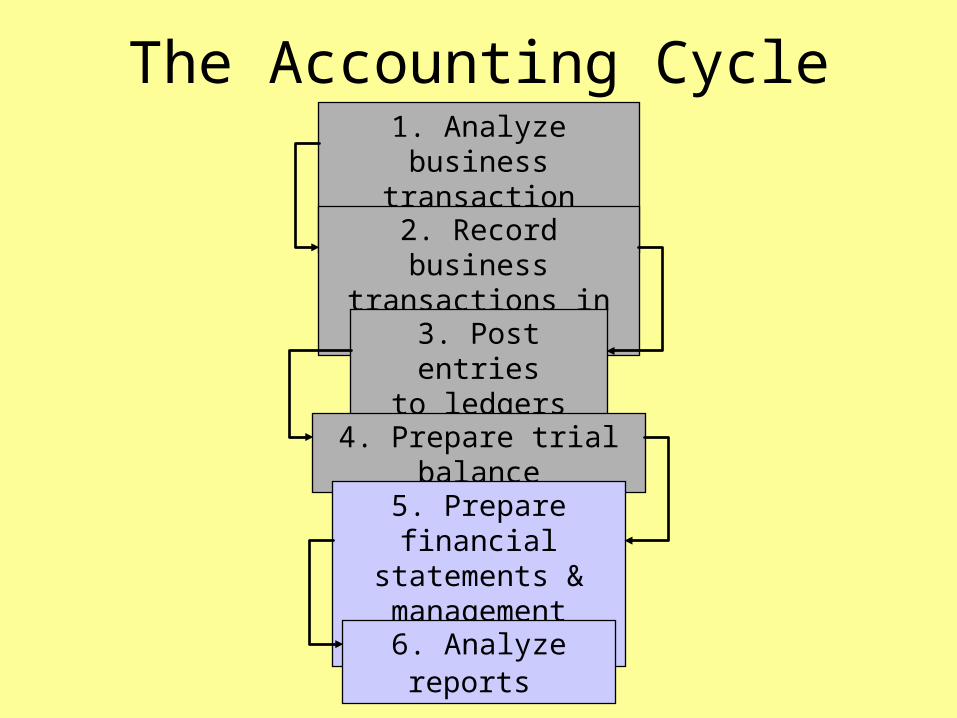

• What are the six steps in the accounting cycle?– Accounting cycle:Accounting cycle: the process of generating financial

statements• AAnalyzing business transactions

• RRecording transactions in journals

• PPosting transactions to ledgers

• SSummarizing ledger totals in a trial balance

• PPreparing financial statements and reports

• AAnalyzing reports and making decisions

The Accounting Cycle1. Analyze business

transaction documents

2. Record business transactions in journal

3. Post entriesto ledgers

4. Prepare trial balance

5. Prepare financial statements &

management reports

6. Analyze reports

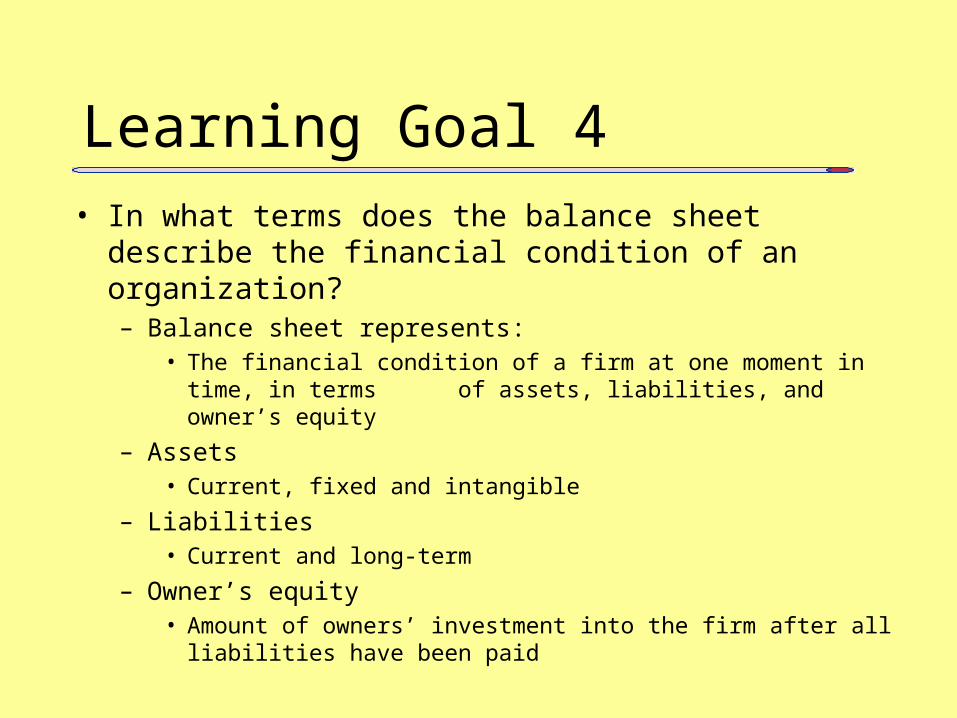

Learning Goal 4• In what terms does the balance sheet describe the financial

condition of an organization?– Balance sheet represents:

• The financial condition of a firm at one moment in time, in terms of assets, liabilities, and owner’s equity

– Assets• Current, fixed and intangible

– Liabilities• Current and long-term

– Owner’s equity• Amount of owners’ investment into the firm after all liabilities have been

paid

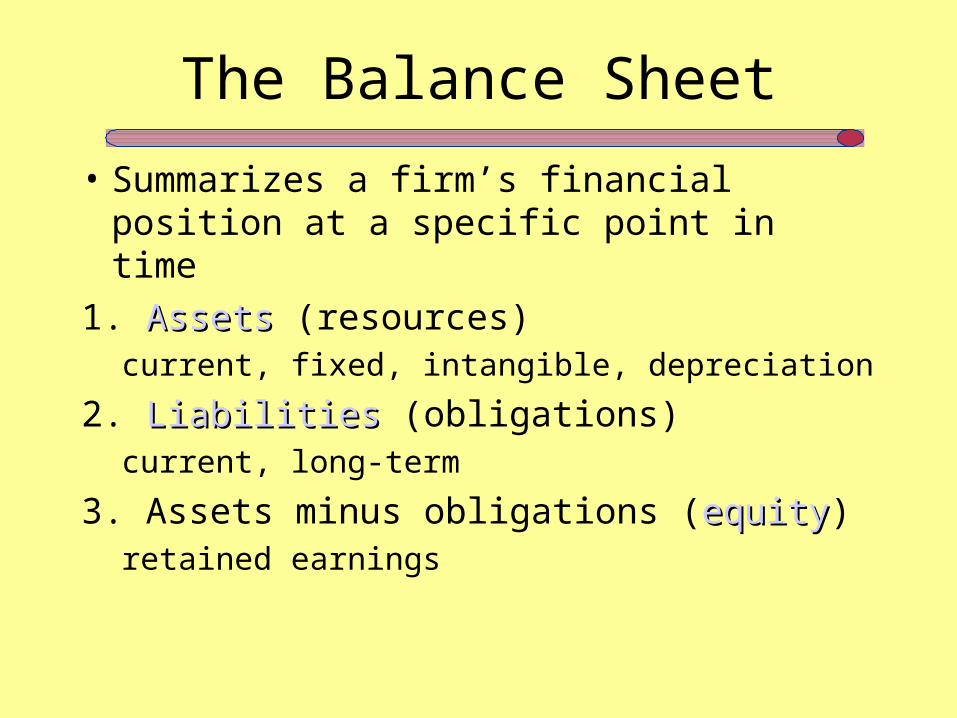

The Balance Sheet

• Summarizes a firm’s financial position at a specific point in time

1. AssetsAssets (resources)current, fixed, intangible, depreciation

2. LiabilitiesLiabilities (obligations)current, long-term

3. Assets minus obligations (equityequity)retained earnings

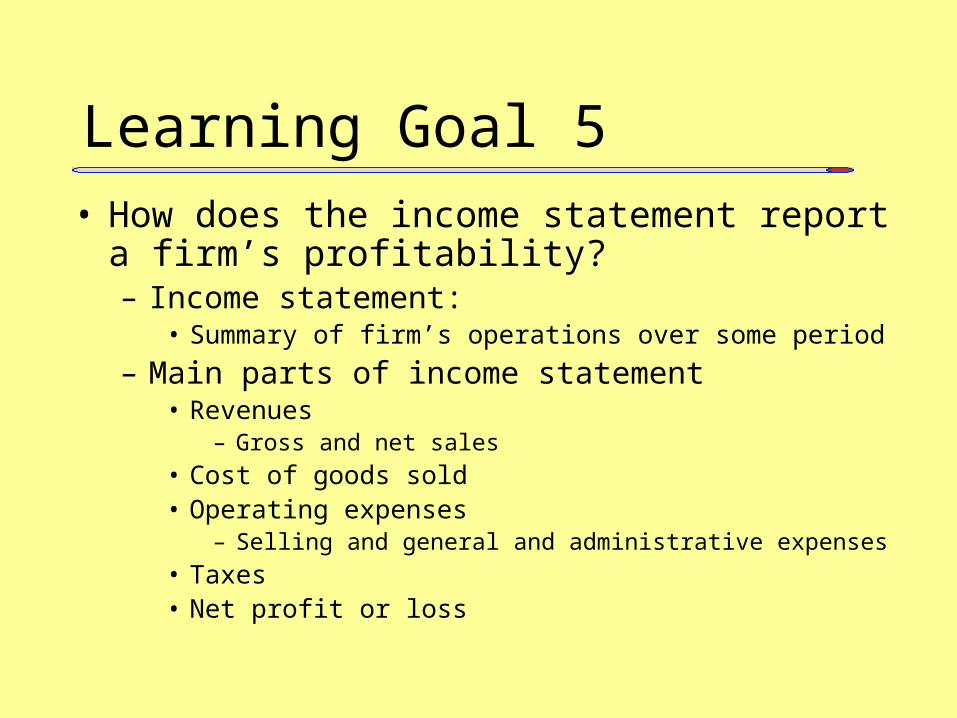

Learning Goal 5• How does the income statement report a firm’s

profitability?– Income statement:

• Summary of firm’s operations over some period

– Main parts of income statement• Revenues

– Gross and net sales

• Cost of goods sold• Operating expenses

– Selling and general and administrative expenses

• Taxes• Net profit or loss

The Income Statement

• Summarizes the firm’s revenues & expenses and shows total profit or loss over a period of time

1. RevenuesRevenuesgross sales, net sales

2. ExpensesExpensescost of goods sold, operating expenses

3. Net profitNet profit or lossloss

The Income Statement: Revenues

• Increased revenues don’t always lead to increased stock value:– US Office ProductsUS Office Products had very high revenue

growth in 1998, but it’s stock price decreaseddecreased 88%

Source: Fortune, Sept. 28, 1998, p. 232.

Learning Goal 6

• Why is the statement of cash flows an important source of information?– Statement of cash flows

• Summarizes the firm’s sources and uses of cash during financial reporting period

• Shows net change in firm’s cash and marketable securities

– Breaks firm’s cash flows into those from:• Operating activities

• Investment activities

• Financing activities

The Statement of Cash Flows

• Summarizes the money flowing into and out of a firm for a period of time

• Sources of cash flow:– operating activities– investment activities– financing activities

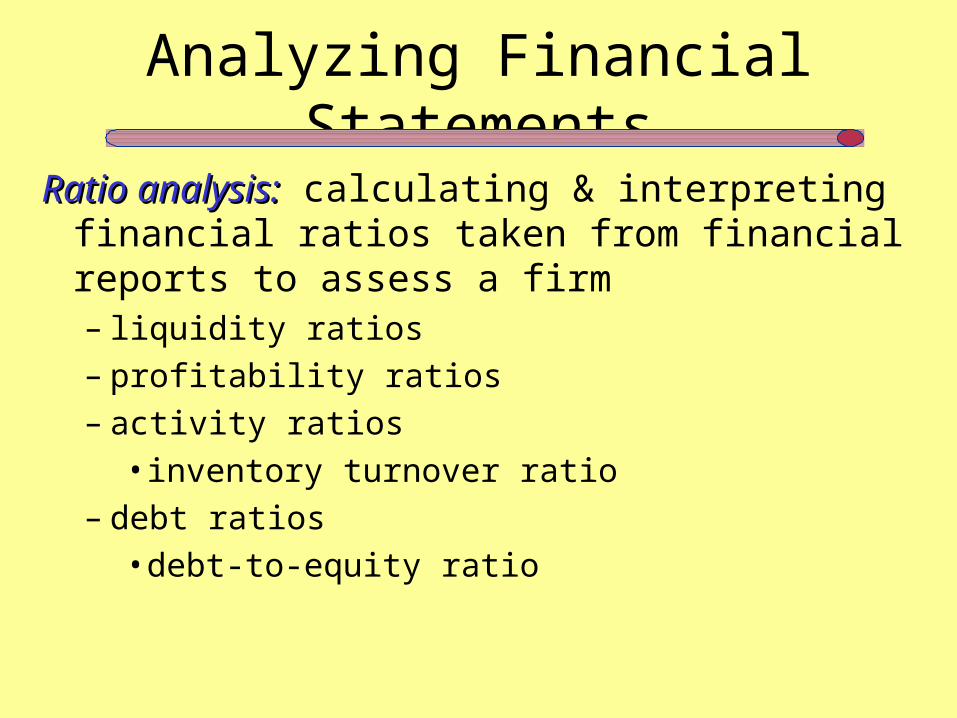

Learning Goal 7• How can ratio analysis be used to identify a firm’s financial

strengths and weaknesses?– Ratio analysis

• Using financial statements to gain insight into a firm’s– Operations– Profitability– Overall financial condition

• Comparing ratio’s can indicate trends and highlight financial strengths and weaknesses

– Four main types of ratios• Liquidity ratios• Profitability ratios• Activity ratios• Debt ratios

Analyzing Financial Statements

Ratio analysis:Ratio analysis: calculating & interpreting financial ratios taken from financial reports to assess a firm– liquidity ratios– profitability ratios– activity ratios

• inventory turnover ratio– debt ratios

• debt-to-equity ratio

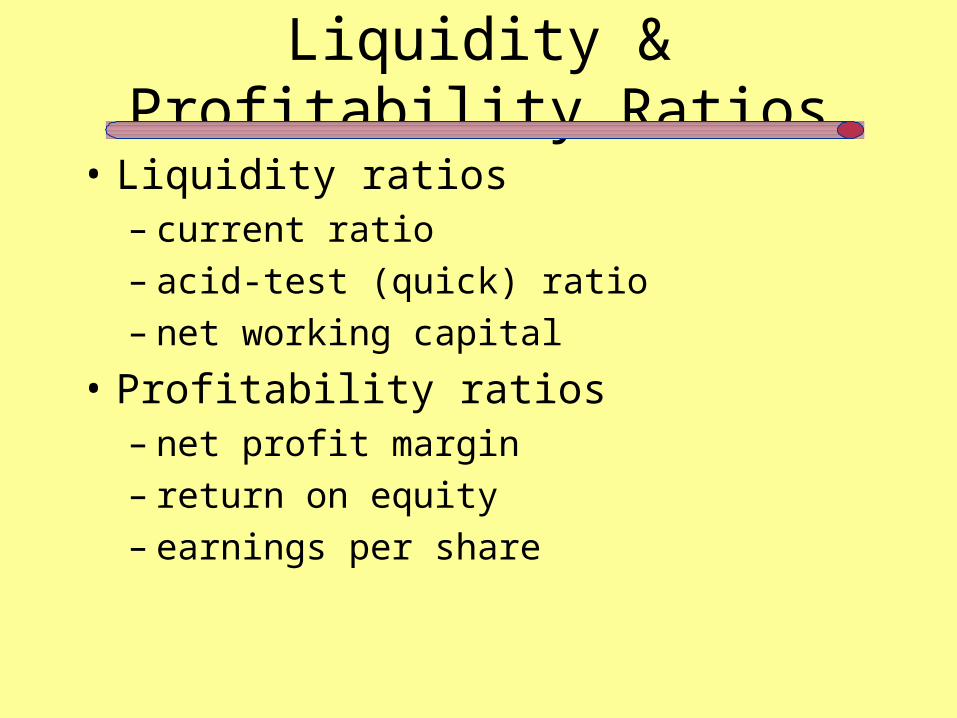

Liquidity & Profitability Ratios

• Liquidity ratios– current ratio– acid-test (quick) ratio– net working capital

• Profitability ratios– net profit margin– return on equity– earnings per share

Learning Goal 8

• What major trends are affecting the accounting industry today?– Role of accountants has expanded

• Includes management consulting in areas such as:– Computer systems

– Human resources

– Electronic commerce

– Major issue: How to treat key intangible assets• FASB and SEC are raising concerns about quality of reported

earnings

Trends in Accounting

• Accountants expand their role more involvement in operations

• Valuing knowledge assets– R&D, brands, trademarks, employee talent

• Tightening the GAAP reducing loopholes

Related Documents