Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

COMMITTED TOSUSTAINABLE GROWTHTOGETHER Nature has spirit and is the main seat of excellence. If we look deep

into nature, we get a variety of lessons from its different components

and forms. The gushing river heading towards the sea for awaited

unison teaches us to face odds with courage and fortitude. The

wonderful blooming flowers from the green teach us to smile. The lush

green grass signaling safety teaches us to be patient and generous. A

mountain with its huge strength teaches us determination. Beyond the

clouds, the sky is always blue and the sun is always shining. They want

us to be persistent and ready for the upcoming days. A small plant’s

gradual turning into a giant tree teaches us to pursue growth

trajectory with hope and tenacity. The change in nature with the

advent of each season displays that actions explain a lot more than

words do. Nature, as a whole, also teaches us integrity and stability.

Nature has many forms and patterns, and teaches us the benefit of

togetherness. It provides us sustenance and stimulates us to excel in

performance. It is our bounden duty to protect and nurture nature.

In the cover picture, the plant is growing into a better and more

advanced state by a process of evolution. So is our Bank. It is gradually

evolving into a higher stage and stature by execution of the strategies

of sustainable growth strongly supported by all stakeholders especially

the loyal customers. We submit ourselves to the nature’s intelligence to

rise up high. Our pursuit of sustainable growth path with the

togetherness of customers is a quest for superior performance for

continuous improvement. Ours is a safe depository for our all

stakeholders. Our pledge is to make it a customers’ coveted destination

and their preferred Bank to shape up their desired future. Together we

shall grow, excel and our actions shall determine our destination. We

firmly believe together we shall reach the goal we sincerely long for.

COMMITTED TOSUSTAINABLE GROWTH

TOGETHER

A N N U A L R E P O R T 2 0 1 6

Table ofContents

SEBL AT A GLANCE

Letter of Transmittal 4

Notice of the 22nd Annual General Meeting 5

Vision and Mission 7

Strategic Objectives, Planning and Priorities 9

Core Values, Code of Conduct and Ethical Principles 12

Corporate Profile 17

Corporate Philosophy and Business Model 18

22 Years of Glorious Journey 20

Awards and Recognitions 22

Corporate Organogram 25

Group Corporate Structure 26

Last 10 Years Financial Indicators 27

Forward Looking Ideology 28

PROFILE OF BOARD OF DIRECTORS AND REVIEW OF THE GROUP CHAIRMAN

Composition of Board of Directors and its Committees 29

Directors’ Profiles and their representation on Board of other Companies 36

Directors’ Responsibility Statement 48

Review from the office of the Group Chairman 50

Managing Director’s Review and Corporate Management 64

DIRECTORS’ REPORT 69

CORPORATE GOVERNANCE

Corporate Governance Report 85

Managing Director’s and CFO’s Declaration on Integrity ofFinancial Statements to the Board 99

Management Review, Responsibility and Evaluation 100

Credit Rating 143

Audit Committee (Composition, Role, Meetings,

Attendance etc.) and Internal Control 144

Report of the Risk Management Committee 149

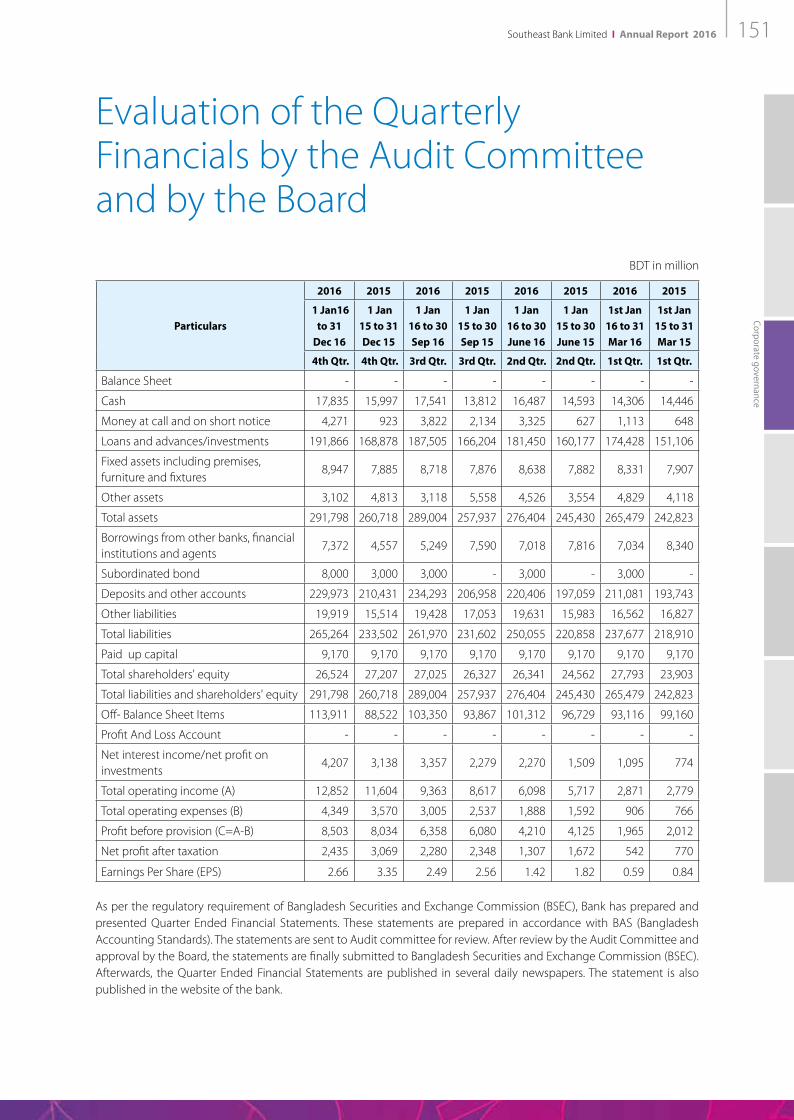

Evaluation of the Quarterly Financials by the

Audit Committee and by the Board 151

Report of the Bank’s Shariah Supervisory Committee 152

Capital Plan 154

FINANCIAL STATEMENTS Independent Auditor’s Report to the Shareholders 260

Consolidated Balance Sheet 262

Consolidated Profit and Loss Account 264

Consolidated Cash Flow Statement 265

Consolidated Statement of Changes in Equity 266

Notes to the Financial Statements 272

FINANCIAL STATEMENTS OF ISLAMIC BANKING BRANCHES 344FINANCIAL STATEMENTS OF OFFSHORE BANKING 354FINANCIAL STATEMENTS OF SEBL SUBSIDIARIES 364

STANDARD DISCLOSURES CHECKLIST 419SAFA Corporate Governance Disclosure Checklist 420

Integrated Reporting Checklist 422

SAFA Standard Disclosure Checklist 427

Important Financial Indicators with Quantitative and Qualitative Factors 430

Proxy Form and Attendance Slip 441

RISK MANAGEMENT AND CONTROL FRAMEWORK

Report on Risk Management Framework,

Mitigation Methodology and Risk Reporting by CRO 159

Disclosure on Risk Based Capital Adequacy (Basel III) 166

Capital Market Exposure 177

SEBL OUTLOOK

Products and Services 218

Caring for the Employees (Health and Safety) 224

Career Development Program 225

Contribution to National Exchequer 226

Empowering Women 226

Financial Inclusion: Mobile Banking Services – Telecash 230

Service Excellence in Action 231

Bank’s Network: List of Branches and ATMs 232

Memories of 21st AGM 242

SUSTAINABILITY APPRAISAL AND INTEGRATED REPORTING

Sustainability Report - At A Glimpse 180

Report on Corporate Social Responsibility 182

Environment Related Initiatives 186

Green Banking Initiatives – Environmental and Social Obligation 188

Integrated Reporting 189

Communication to Shareholders and Stakeholders 197

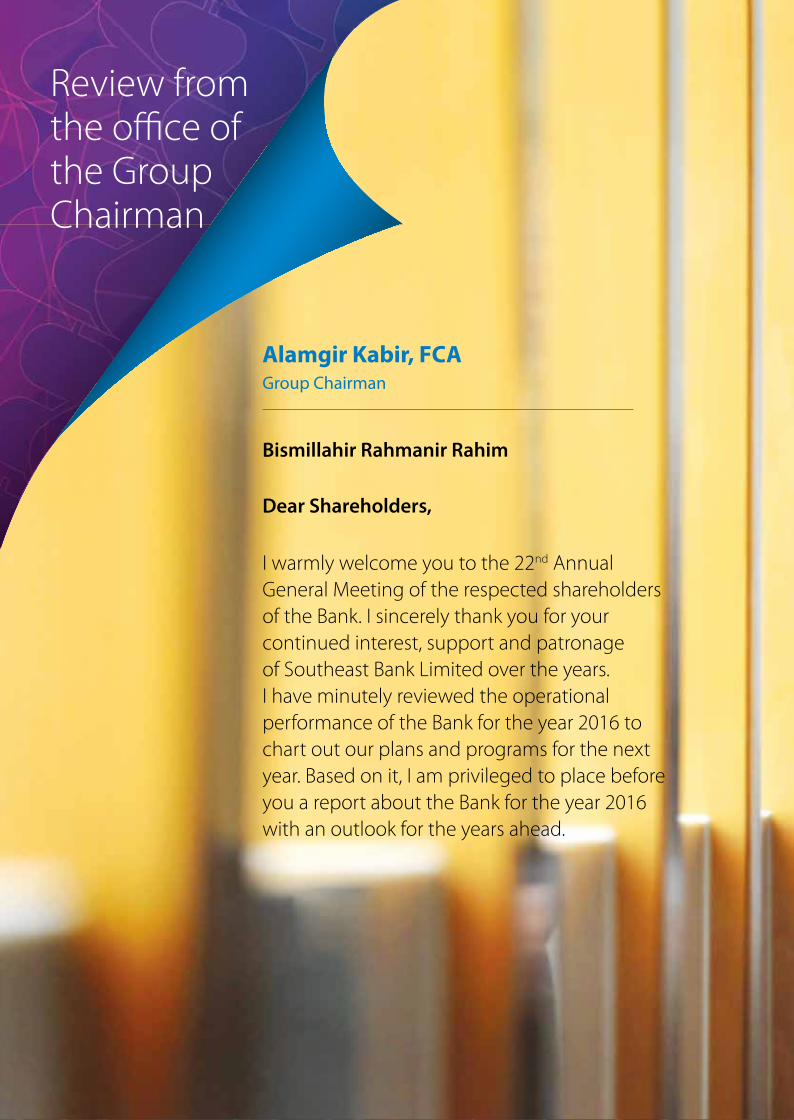

Southeast Bank Limited I Annual Report 20164

All Shareholders of Southeast Bank Limited, Bangladesh Bank, Bangladesh Securities and Exchange Commission, Registrar of Joint Stock Companies & Firms, Dhaka Stock Exchange Limited and Chittagong Stock Exchange Limited

Annual Report of Southeast Bank Limited for the Year -2016

Dear Sir,

Thank you for supporting us in the preceding years.

It is our immense pleasure to lay before you the Bank’s Annual Report-2016 along with the Audited Financial Statements (consolidated and separate) as at and for the year ended 31st December, 2016. Annual Report-2016 of the Bank comprises Balance Sheet, Profit and Loss Accounts, Statement of Changes in Equity, Cash Flow Statement along with Notes to the Accounts.

Information given in our Annual Report-2016 is complete, full and in line with Bangladesh Accounting Standard and International Accounting Standard. We hope that the report will be of use to you today and tomorrow.

Best regards,

Yours sincerely,

Muhammad Shahjahan Additional Managing Director & Company Secretary

Letter of Transmittal

Southeast Bank Limited I Annual Report 2016 5

Notice of the 22nd AnnualGeneral MeetingNotice is hereby given to all members of Southeast Bank Limited that the 22nd Annual General Meeting of the Shareholders of the Company will be held on Monday, May 22, 2017 at 11.00 a.m. at Officers’ Club Dhaka, 26 Baily Road, Dhaka to transact the following business and adopt necessary resolutions:

AGENDA

1. To receive, consider and adopt the Profit and Loss Accounts of the Company for the year ended on 31st December, 2016 and the Balance Sheet as at that date together with the Reports of the Board and the Auditors thereon.

2. To declare dividend for the financial year ended 31st December, 2016.

3. To elect / re-elect Directors.

4. To appoint Auditors for the term until the next Annual General Meeting and fix their remuneration.

5. Miscellaneous, if any, with the permission of the chair.

All Members are requested to attend the meeting on the date, time and place mentioned above. By order of the Board

Dated: May 07, 2017 Muhammad Shahjahan Additional Managing Director and Company SecretaryNOTES

a) The Record Date for the purpose was on April 27, 2017.

b) Any member of the Company entitled to attend and vote at the general meeting may appoint a proxy to attend and vote on his/her behalf. Such proxy except for a Corporation must also be a member of the Company. An Attorney of a member need not himself/herself be a member.

c) The instrument appointing a Proxy or the Power of Attorney duly signed by the Member and stamped with requisite stamp duty must be submitted at the Registered Office of the Company at least 48 hours before the meeting, i.e. latest by 11.00 a.m. of May 20, 2017.

d) Attendance of the Shareholder/Attorney/Proxy shall be recorded up to 11.30 a.m. at the entrance of the venue. Attendance slip has to be submitted at the Registration Counter duly signed. The signature must agree with the recorded signature.

e) Annual Report containing, among other papers, this Notice of the 22nd Annual General Meeting, Attendance Slip and Proxy Form are being sent to every member by post. The members may also collect “Proxy Form” from the Share Office of the Company.

f ) All members are requested to update: (i) The particulars of their Bank Account (ii) Change of Address and (iii) 12 Digits Tax Payer’s Identification Number (e-TIN) in their BOID through Depository Participants (DP) on or before May 15, 2017, with intimation to us.

g) Brokerage Houses and DPs are requested to notify us in details showing Shareholder’s name, BOID Number, e-TIN, client-wise shareholding position, Bank Account Number, Routing Number etc. of their Margin Loan holders who hold shares of Southeast Bank Ltd. on the Record Date on or before May 15, 2017.

h) If any individual shareholder fails to provide us his/her e-TIN within May 15, 2017, his/her Income Tax at source will be deducted from payable Dividend @15% (fifteen percent) instead to 10% (ten percent) as per amended Income Tax Ordinance 1984 (Section 54)

PS: As per Bangladesh Securities and Exchange Commission’s Circular No.SEC/CMRRCD/2009-193/154 dated October 24, 2013, “no benefit in cash or kind, other than in the form of cash dividend or stock dividend, shall be paid to the holders of equity securities” for attending the 22nd Annual General Meeting of the Bank.

SEBL at a glance

Southeast Bank Limited I Annual Report 20166

Vision &MissionOur vision, mission and value statements are the keys to the philosophy on which we base ourselves on, what we do and what we want to be

Southeast Bank Limited I Annual Report 2016 7

Vision &MissionOur vision, mission and value statements are the keys to the philosophy on which we base ourselves on, what we do and what we want to be

Vision

Mission

To be a premier banking institution in Bangladesh and contribute

signi�cantly to the national economy.

High quality �nancial services with state of the art technology.

Fast customer service.

Sustainable growth strategy.

High Ethical standards in business.

Steady return on shareholders’ equity.

Innovative banking at a competitive price.

Attraction and retention of quality human resource.

Commitment to Corporate Social Responsibility.

Southeast Bank Limited I Annual Report 20168

Vision

Mission

To be a premier banking institution in Bangladesh and contribute

signi�cantly to the national economy.

High quality �nancial services with state of the art technology.

Fast customer service.

Sustainable growth strategy.

High Ethical standards in business.

Steady return on shareholders’ equity.

Innovative banking at a competitive price.

Attraction and retention of quality human resource.

Commitment to Corporate Social Responsibility.

Southeast Bank Limited I Annual Report 2016 9

Strategic Objectivesa) Maintaining a high quality assets portfolio to achieve

strong and sustainable returns and to continuously build shareholders’ value.

b) Maintaining adequate capital in line with risk appetite of the Bank.

c) Strengthening trust and partnerships with customers by focusing on the Bank’s core values of quality customer service, professionalism, teamwork and integrity.

d) Hiring professionals with strong background and knowledge.

e) Strengthening technologies that reduce operational risks and promote the implementation of best practices in the industry.

f ) Developing innovative products and services that attract our targeted customers and market segments.

g) Exploring new avenues for growth and profitability.

h) Practicing efficient risk management principles in

i) Excellence in banking operations through maintaining strong fundamentals of Capital Adequacy, Business Diversification and Exploring Non-funded Business

ii) Prudent Asset Management

iii) Prudent Liability Management

iv) Excellence in Delivering Customer Service

v) Effective Risk Management

vi) Effective IT Framework and System

line with all six core risks in banking operation and green banking and environmental risk management.

i) Practicing efficient corporate governance and compliance processes through meeting all regulatory requirements and disclosures in line with national and international best practices by ensuring best internal control monitoring practices.

j) Upholding Bank’s brand image as a customer friendly bank through efficient and prompt customer service, product diversification with a view to establishing a long term profitable relationship with our customers.

k) Serving the society as part of our Corporate Social Responsibility (CSR) by giving stipends to poor students, distributing warm clothes to winter-hit people and contributing to the different relief fund. We also contribute to the society by paying taxes to the national exchequer timely.

l) Extending banking services to the un-banked people for financial inclusion meeting socio-economic requirements.

vii) Efficient Internal Control and Regulatory Compliance System

viii) Strong Human Resource Base

ix) Going green in the future of banking

Priorities followed in 2016The Bank had the following plans and road-map for business success in 2016.

Vision

Mission

To be a premier banking institution in Bangladesh and contribute

signi�cantly to the national economy.

High quality �nancial services with state of the art technology.

Fast customer service.

Sustainable growth strategy.

High Ethical standards in business.

Steady return on shareholders’ equity.

Innovative banking at a competitive price.

Attraction and retention of quality human resource.

Commitment to Corporate Social Responsibility.

SEBL at a glance

Southeast Bank Limited I Annual Report 201610

Strategic PrioritiesWe have strong conviction that SEBL will keep on flourishing as a leading financial institution of Bangladesh, despite existence of external challenges: first, because we have a visionary Board, dynamic management and an enthusiastic & skilled group of employee base that is committed to working together to provide our customers with excellent service; second, because we are building on a solid foundation of key strengths, including a strong capital base, and excellent risk and cost management skills; third, because we are strategically diversifying our business lines, products and locations; and finally, because we have a clear focus on our strategy and where we need to direct our efforts. Our strategic focus is built around a few key priorities that will guide our actions as we move forward over the next several years. They will serve as a roadmap to help us navigate through the new landscape in which we are now operating. Sustainable revenue growth, capital management, leadership, prudent risk & appetite management, efficiency & expense management – will be the pillars of our strategy in upcoming years. They will play a critical role in our success and, given the ongoing market uncertainty, they deserve a prominent place in our strategic framework.

Strategic priorities for sustainable revenue growth:

Sustainable revenue growth comes from our ability to build relationships with our customers and creating niche markets. We do this by providing our customers with exceptional service, such us:

Ensuring quality customer service at primary distribution channel such as Branch and development of alternative delivery channels to improve customer experience

Developing and upgrading customized asset, liability and transaction products for Retail, SME and Corporate clients

Mobilizing low cost sustainable deposit from retail and institutional client base

Increasing client base for financial inclusion and wider market penetration

Diversification and increasing loan clients and maintaining quality assets

Export expansion and diversification

Promoting Islamic banking through conventional branches

Emphasizing Small and Medium Enterprises financing

Agricultural & Rural Credit through Micro Financial Institutions

Sustainable financing for Energy efficiency and renewable energy projects

Arranging funds from overseas sources for Off-shore banking service and long term foreign currency loans for corporate clients

Integrated marketing development initiative by creation of customer oriented culture

Mobilizing remittance as a source of foreign currency

Strategic priorities for Capital management & maintaining strong capital base:

SEBL is committed to consolidate its solid capital base to support the risks associated with our diversified businesses, while still providing investors with superior returns. We actively manage our capital to support the execution of our business strategies. Our goal is to achieve the lowest cost of capital by managing its mix and by building our base through earnings and selective capital issues.

Expediting borrowers’ rating

Concentrating on lending portfolio having lower capital charge

Strengthening internal Capital adequacy assessment process (ICAP)

Preemptive preparation for Basel –III compliance

Revising the capital allocation to business in line with revised capital adequacy target ratios

Strategic priorities for Leadership/HR capacity development

SEBL’s success depends on having the right leaders to execute our strategy. For this reason, leadership remains one of our strategic priorities. Our leadership strategy continues to build competitive advantage through comprehensive development programs and tools.

Hiring the best talents in different arenas of Banking

Southeast Bank Limited I Annual Report 2016 11

Fostering a culture of creativity, innovation and diversity with a view to achieving sustainable business growth

Developing a Human resource base by rendering training and motivation so that they remain capable to lead new initiatives

Creating alignment between the leadership development strategy and the business strategy

Evaluating employees based on Key Performance Indicators (KPIs)

Developing Human resource management system to transform the organization

Strategic priorities for prudent risk & apatite management

At SEBL, we are known for our risk management culture, characterized by a conservative approach and rigorous processes. We try to know our customer fully. But at the heart of our strength is experience and good judgment.

For Credit Risk, our focus is developing a strategic business plan for apatite management and structured policy guideline and framework in order to manage default risk

Ensuring effective risk management system especially prudent management of Asset Liability risk, Foreign Exchange risk and Operational risk

Ensuring meticulous compliance of disbursement procedures and monitoring and follow-up of each loan by the Branch manager to ensure in time recovery

Strengthening recovery drive to bring down NPL at a minimum level

Ensuring efficient internal control and regulatory compliance in all levels of banking operations

Efficiency and expense management

Expense management is a traditional strength at SEBL – and today, it’s more important than ever. While revenue growth is ultimately decided by our customers & external factors, expenses are something we can control. At SEBL, we are carefully monitoring our spending and looking for ways to improve productivity by being innovative and doing more with less. Our priorities are:

Clear cost saving strategies

Business process reengineering (BPR) in different business and operational areas to improve efficiency

Optimizing efficiency by budgetary control

Paperless banking

Implementing green office guide

SEBL at a glance

Southeast Bank Limited I Annual Report 201612

Core Values

Our ValuesServe as a compass for our action

and describe our direction.

� Integrity

� Respect

� Fairness

� Harmony

� Team Spirit

� Courtesy

� Commitment

� Service Excellence

� Insight and Spirit

� Enthusiasm for work

� Business Ethics

CORESTRENGTHS

CORECOMPETENCIES

� Professionally Strong Board of Directors

� Strong Capital Base

� Transparent and Quick Decision Making

� E�cient Team of Performers

� Satis�ed Customers

� E�ective Internal Control

� Skilled Risk Management

� Knowledge

� Experience and Expertise

� Customer Orientation and Focus

� Transparency

� Determination

� Zeal for Improvement

� Pursuit of Disciplined Growth Strategies

� Reliability

� Focus on Diversi�cation

� Quality Customer Service

� Unique Corporate Culture

� Sharp bifurcation Between Board and Management Functions

� Strong Asset Base

Southeast Bank Limited I Annual Report 2016 13

Core Values

Our ValuesServe as a compass for our action

and describe our direction.

� Integrity

� Respect

� Fairness

� Harmony

� Team Spirit

� Courtesy

� Commitment

� Service Excellence

� Insight and Spirit

� Enthusiasm for work

� Business Ethics

CORESTRENGTHS

CORECOMPETENCIES

� Professionally Strong Board of Directors

� Strong Capital Base

� Transparent and Quick Decision Making

� E�cient Team of Performers

� Satis�ed Customers

� E�ective Internal Control

� Skilled Risk Management

� Knowledge

� Experience and Expertise

� Customer Orientation and Focus

� Transparency

� Determination

� Zeal for Improvement

� Pursuit of Disciplined Growth Strategies

� Reliability

� Focus on Diversi�cation

� Quality Customer Service

� Unique Corporate Culture

� Sharp bifurcation Between Board and Management Functions

� Strong Asset Base

Southeast Bank Limited I Annual Report 201614

Code of Conduct and Ethical Principles

A. WE ADHERE TO THE FOLLOWING PRINCIPLES IN DEALING WITH CUSTOMERS

1. Follow strict ethical banking practices.

2. Provide fair treatment to all customers, depositors and borrowers without any discrimination.

3. Provide speedy customer service at a very competitive cost.

4. Deal with customers in a transparent manner and without any hidden cost.

5. Maintain strict secrecy of customer account.

6. Provide free financial advice to clients.

7. Deal quickly with complaints received from the customers. We endeavour continuously to build relationship of trust and understanding with our customers.

8. Give very competitive return to the depositors on their investment.

9. Listen to our customers and work for improvement of customer service as per their suggestion.

10. Keep relations with customers in weal and woe.

11. Keep promises that we make.

12. Take competitive service charges and rates.

13. Discourage any sort of privilege/donation from customer

B. WE BELIEVE IN THE FOLLOWING PRINCIPLES IN DEALING WITH SHAREHOLDERS

1. Adequate disclosure of corporate information and operational results to help them take suitable investment decisions / options.

2. Stable Dividend Policy

3. Dialogue with them and implement their suggestions for improvement

4. Equal treatment to all shareholders irrespective of their individual size of shareholding.

5. Effective Risk Management

6. Maintenance of fairness and accuracy of financial reporting and records.

7. Restrictions on insider trading.

C. WE ABIDE BY THE FOLLOWING PRINCIPLES IN DEALING WITH OUR REGULATORS

1. We are transparent in operations and governance.

2. We have a culture of timely compliance of regulatory requirements.

3. We take their suggestions with utmost importance and implement those for improvement of our corporate governance standard.

4. We safeguard information and do not misuse it.

Southeast Bank believes that its efforts to become a leading bank in the private sector can only be achieved and sustained by creating effective corporate governance, inculcating professionalism among its staff and strictly adhering to rules and regulations. We believe that our aims and objectives can only be realized fully and sustained over time by adherence to ethics that cannot always be built into sets of rules and regulations. This belief in ethics motivates the Bank in its dealings with those with whom it interacts.

Southeast Bank Limited I Annual Report 2016 15

D. WE CONFORM TO THE FOLLOWING PRINCIPLES IN RESPECT OF OUR EMPLOYEES

1. We do not discriminate on grounds of religion, sex or race at any stage. We recruit the best on the basis of merit under a rigorous recruitment policy without any biasness or favoritism to anybody.

2. We pay competitive compensation package for the really deserving employees.

3. We care for our employees and create an environment to work together with dignity.

4. We have clearly defined duties and responsibilities for each employee. No one is responsible for unassigned jobs.

5. We have a zero tolerance to any act of dishonesty.

6. We provide a congenial work environment.

7. We encourage freedom to our employees to give opinion for both qualitative and quantitative improvement of the Bank.

8. We take care of their health and safety.

9. Our employees avoid conflict of interest.

10. Our employees obey code of conduct.

11. Professionalism, honesty, integrity and high moral and ethical standards are the creed of our employees.

E. WE UPHOLD THE UNDER NOTED PRINCIPLES IN RESPECT OF SOCIETY

1. We believe that the Bank gets business sustenance from the community in which it operates and, therefore, it must remain responsive to the community and the society in reciprocity.

2. We discourage financing projects that are not environment-friendly.

3. We provide material support for protection of environment.

4. We give aid to the poor, helpless and natural calamity-hit people.

5. We support charitable ventures.

6. We give sponsorships to sports, culture, education, health-care and community development ventures.

7. We support the women as a community and contribute to women empowerment.

8. We are keen to move fast for green banking to protect environment.

F. WE DEVOTE TO THE FOLLOWING PRINCIPLES IN RESPECT OF NATIONAL INTEREST

1. We protect national interests.

2. We refrain from prohibited business.

3. We promote causes for national upliftment.

4. We support nation building efforts from our position.

Commitments to Clients

Ours is a customer focused modern banking institution in Bangladesh. We deliver unparalleled financial services to Retail, Small and Medium Scale Enterprises (SMEs), Corporates, Institutions, Government, and individual clients through branches across the country. Our business initiatives center around the emerging demands of the market. Our commitments to the clients are as follows:

a) Provide service with high degree of professionalism and use of modern technology.

b) Create long-term relationship based on mutual trust.

c) Respond to customer needs with speed and accuracy.

d) Share their values and beliefs.

e) Grow as our customers grow.

f ) Provide products and services at competitive price.

g) Ensure safety and security of customers’ valuables in trust with us

SEBL at a glance

Southeast Bank Limited I Annual Report 201616

Our Banking Heritage

Southeast Bank Limited is a second-generation bank that was established in 1995 with a dream and a vision to become a pioneer banking institution of the country and contribute significantly to the growth of the national economy. The Bank’s journey began when it was incorporated as a Public Limited Company on March 12, 1995. The Registrar of Joint Stock Companies and Firms issued the Certificate of Commencement of Business of the Bank on the same date. The Southeast Bank received its Banking License from the Bangladesh Bank on March 23,1995. The Bank’s 1st branch was opened by Late M. Saifur Rahman, the then Honourable Finance Minister of the Government of the People’s Republic of Bangladesh as the Chief Guest at the commercial hub of the country at 1, Dilkusha Commercial Area, Dhaka on May 25, 1995.

In its arduous journey since, Southeast Bank has succeeded in realizing the dreams of those who established it. Today it is one of the country’s leading banks in the private sector contributing significantly to the national economy. The Authorized Capital of the Bank today is BDT 15,000 million. Its Paid-Up-Capital and Reserve reached BDT 34,056.28 million as on December 31, 2016. The Bank had 2,616 Staff of whom 229 were Executives, 1,860 were Officers and 527 were other Staff as on December 31, 2016.

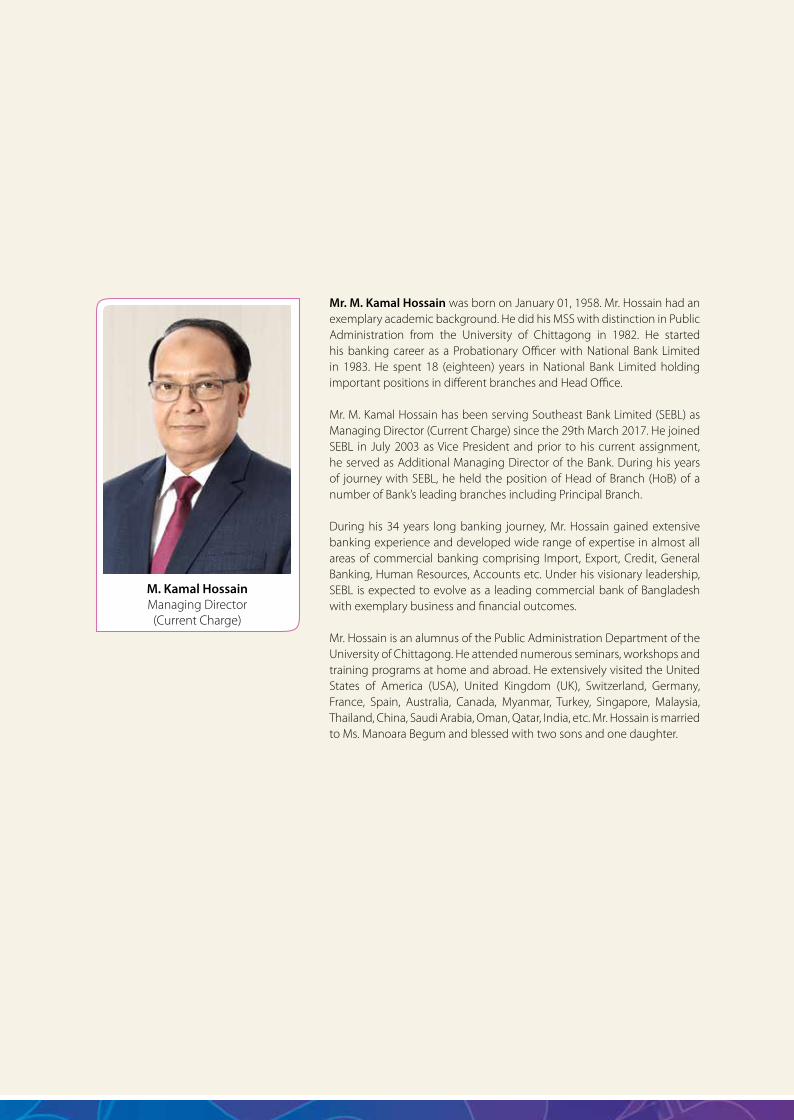

The Southeast Bank was established by leading business personalities and eminent industrialists of the country with stakes in various segments of the national economy. They established the Bank with a vision to bring efficient and professional banking service to the people and the business community of Bangladesh to help the national economy grow. The incumbent Chairman of the Bank is Mr. Alamgir Kabir, FCA, a professional Chartered Accountant. The Bank’s Managing Director (Current Charge) is Mr. M. Kamal Hossain, a creative, experienced and eminent banker of the country with 34 years of experience in banking to his credit.

The Bank’s operations are built upon unequivocal emphasis on effective corporate governance. The objective is to create, promote and build long-term company value. The Bank’s first and the highest priority is to provide effective services and maximum satisfaction to the customers. The ethos of harmony and co-operation is widely practiced in the Bank. We take pride in the fact that the public and private face of the Bank is one and identical. We believe that transparency in decision-making, monitoring mechanism and full disclosure to shareholders and regulatory authorities are essential aspects of bank’s corporate governance and that they create an intense pressure to rationalize bank’s services and search for new competitive advantages. We work ceaselessly within these parameters.

A team of efficient professionals manages the Bank. They create and generate an environment of trust and discipline that encourages everybody in the Bank to work together for achieving the objectices of the Bank. The culture of maintaining congenial work-environment in the Bank has further enabled the staff to benchmark themselves better against management expectations. A commitment to quality and excellence in service is the hallmark of their identity.

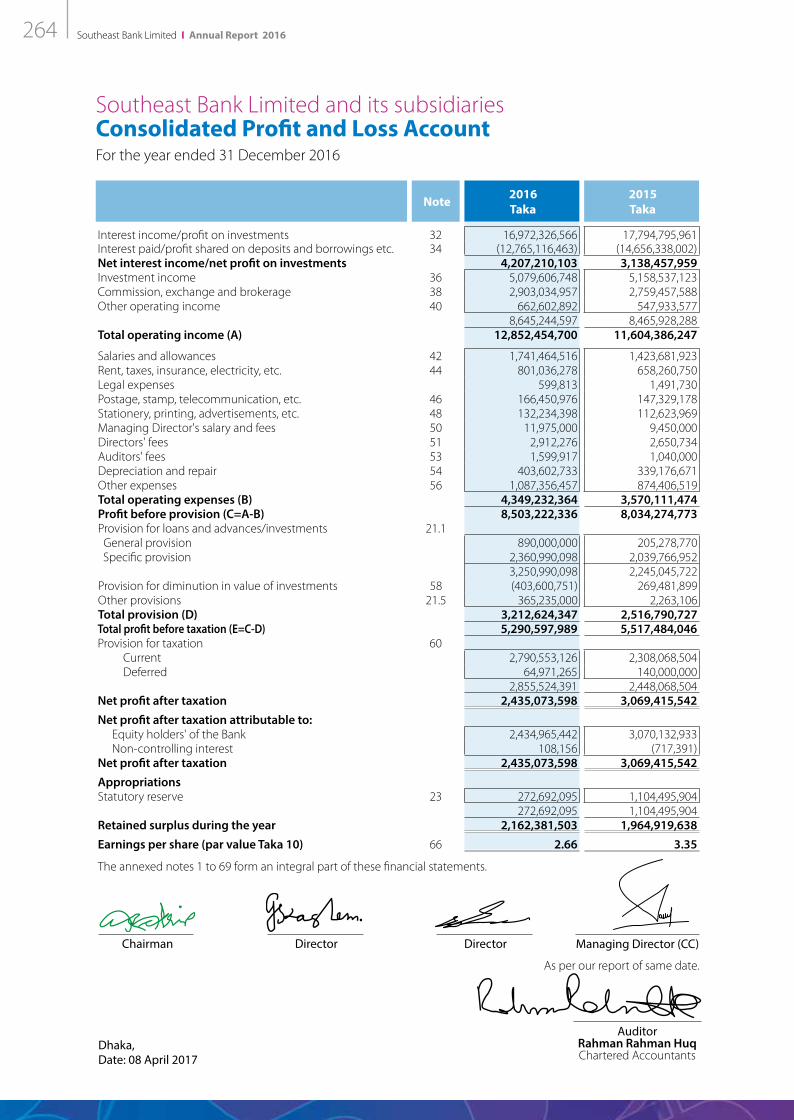

Southeast Bank has become a synonym of quality banking services and products. It has a diverse array of products and services tailored carefully to cater to the needs of all segments of customers. Our operational strategies are structured to address the special and often complex needs of the customers. In the growth graph, the Bank has generated profit of BDT 2,435.07 million after provision and income tax in the year 2016. The curve keeps soaring upward everyday making it one of the leading and most successful banking institutions in Bangladesh with a total asset base of BDT 291,798.01 million as on December 31, 2016.

Southeast Bank Limited I Annual Report 2016 17

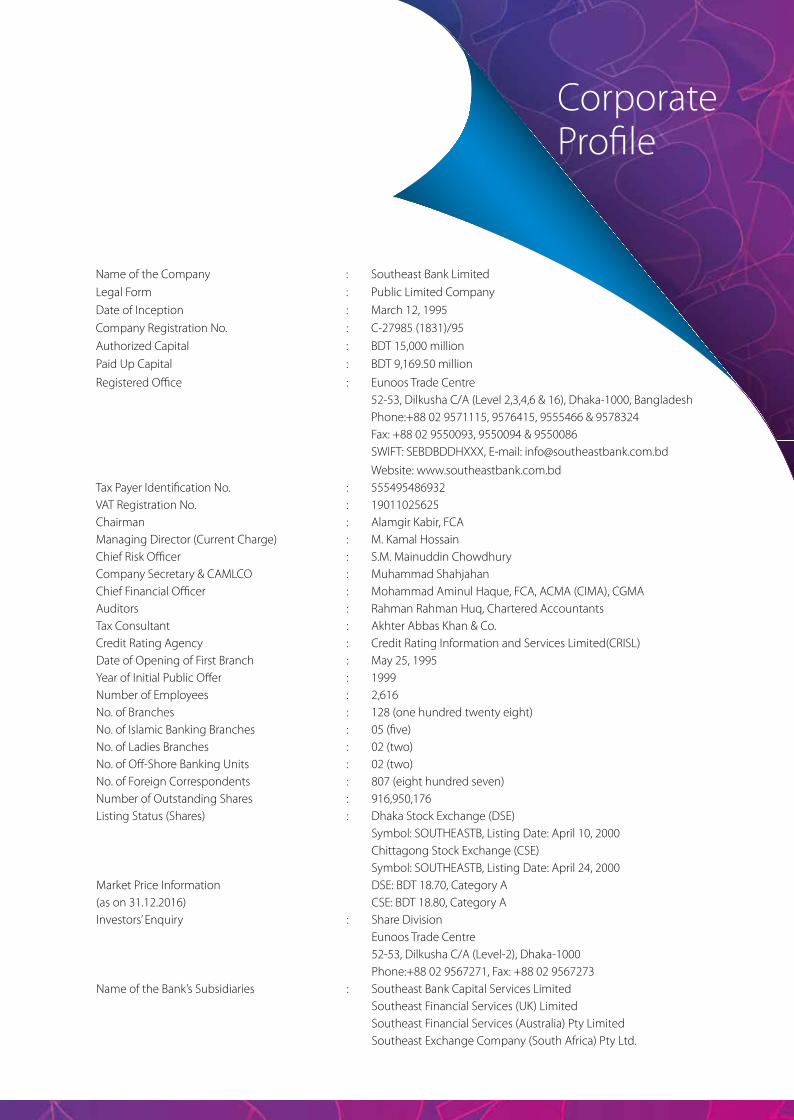

CorporateProfile

Name of the Company : Southeast Bank LimitedLegal Form : Public Limited CompanyDate of Inception : March 12, 1995Company Registration No. : C-27985 (1831)/95Authorized Capital : BDT 15,000 millionPaid Up Capital : BDT 9,169.50 millionRegistered Office : Eunoos Trade Centre 52-53, Dilkusha C/A (Level 2,3,4,6 & 16), Dhaka-1000, Bangladesh Phone:+88 02 9571115, 9576415, 9555466 & 9578324 Fax: +88 02 9550093, 9550094 & 9550086 SWIFT: SEBDBDDHXXX, E-mail: [email protected] Website: www.southeastbank.com.bdTax Payer Identification No. : 555495486932VAT Registration No. : 19011025625Chairman : Alamgir Kabir, FCAManaging Director (Current Charge) : M. Kamal HossainChief Risk Officer : S.M. Mainuddin ChowdhuryCompany Secretary & CAMLCO : Muhammad ShahjahanChief Financial Officer : Mohammad Aminul Haque, FCA, ACMA (CIMA), CGMAAuditors : Rahman Rahman Huq, Chartered Accountants Tax Consultant : Akhter Abbas Khan & Co.Credit Rating Agency : Credit Rating Information and Services Limited(CRISL)Date of Opening of First Branch : May 25, 1995Year of Initial Public Offer : 1999Number of Employees : 2,616No. of Branches : 128 (one hundred twenty eight)No. of Islamic Banking Branches : 05 (five)No. of Ladies Branches : 02 (two)No. of Off-Shore Banking Units : 02 (two)No. of Foreign Correspondents : 807 (eight hundred seven)Number of Outstanding Shares : 916,950,176Listing Status (Shares) : Dhaka Stock Exchange (DSE) Symbol: SOUTHEASTB, Listing Date: April 10, 2000 Chittagong Stock Exchange (CSE) Symbol: SOUTHEASTB, Listing Date: April 24, 2000Market Price Information DSE: BDT 18.70, Category A(as on 31.12.2016) CSE: BDT 18.80, Category A Investors’ Enquiry : Share Division Eunoos Trade Centre 52-53, Dilkusha C/A (Level-2), Dhaka-1000 Phone:+88 02 9567271, Fax: +88 02 9567273Name of the Bank’s Subsidiaries : Southeast Bank Capital Services Limited Southeast Financial Services (UK) Limited Southeast Financial Services (Australia) Pty Limited Southeast Exchange Company (South Africa) Pty Ltd.

Southeast Bank Limited I Annual Report 201618

Corporate Philosophy and Business Model

Our corporate philosophy centers around our corporate missions, business domain and management goals. We devote our talent and technology to the creation of value for our stakeholders. Everyday our people bring this philosophy to life and to their work. Our philosophy cannot be bound by a few words or issues. Yet we narrate the following: Customers

Our company philosophy is simple. It is customer-friendly and fully responsive to customer needs and expectations. We carry out required research, analysis and survey to find out what the customers expect. We leverage technology and expertise to provide best services and convenience to the customers. We spend money on things that matter to them and add value to the Bank in terms of image and profit. That is why our customer-base has been steadily expanding over the years.

Human Resource

Our people are smart, professional, well-qualified, energetic and sincere. They are passionate about what they do. Since they enjoy their work, it becomes easy for them to work hard. They do not follow any set model, rather they create models. They completely own what they plan and do.

Communication

Our philosophy is to reduce lines and layers of communication. We believe in free flow of ideas within the Management Team. The Senior Management Team is also open to ideas suggested by the lower level executives and officers. At the same time, our decision making process is short but quick.

Control Mechanism

Our control mechanism is practiced at all levels. We strive to control the behavior of the employees. Our control mechanism is closely linked to efficiency, quality, innovation and responsiveness to customers.

Quality and Productivity

Our philosophy is geared towards boosting productivity and maintaining a reliable high quality service standard. In the process of delivery of service, co-ordination is the essence of our business. Our philosophy is to achieve our goals through a combination of budgetary control, pay for performance, incentive system, unique corporate culture that continuously stresses key values.

Building Future

Our philosophy is to make decisions today to improve performance tomorrow. We know a company which is successful has to continue to be successful. We do not fear our future, we shape it by our corporate conduct.

Southeast Bank Limited I Annual Report 2016 19

Business Model Canvas ofSoutheast Bank Limited

Key Partners

Customers Shareholders Employees Regulators Strategic Partners

Value Proposition

Complete Solution of Business Needs One Stop Service for Personal Banking Innovative Tailor-made Products Timely, Cost-e�ective and Superior Services Geographically Well-spread Availability

Key Activities

Deposit Lending International Trade Remittance Treasury Solutions Islamic Banking O�-shore Banking

Key Resources

Highly Professional and Experienced Board Nationwide Network Worldwide Correspondent Network Highly Skilled Sta� Dedicated Service Attitude Wide Range of Products Strong IT platform Strong Capital Base

Cost Structure

Interest Expense Operating Expense Capital Expenditure

Customer Segments

Corporate Clients Small and Medium Enterprises Non-Banking Financial Institutions Banks Individuals/ Retail Clients Institutional Clients Govt. and Non-Govt. Organizations

Customer Care

KYC – Know Your Customer Personal Visit Phone Call/ Email/ SMS Automated Services Special Campaign In-depth Analysis Individual Solution Continuous Review Research and Development Receiving Feedback

Revenue Streams

Interest Income Investment Income Fees, Commission, etc. Other Operating Income

Delivery Channels

Branches ATMs Internet Banking Mobile Banking Call Center Subsidiary Companies

SEBL at a glance

Southeast Bank Limited I Annual Report 201620

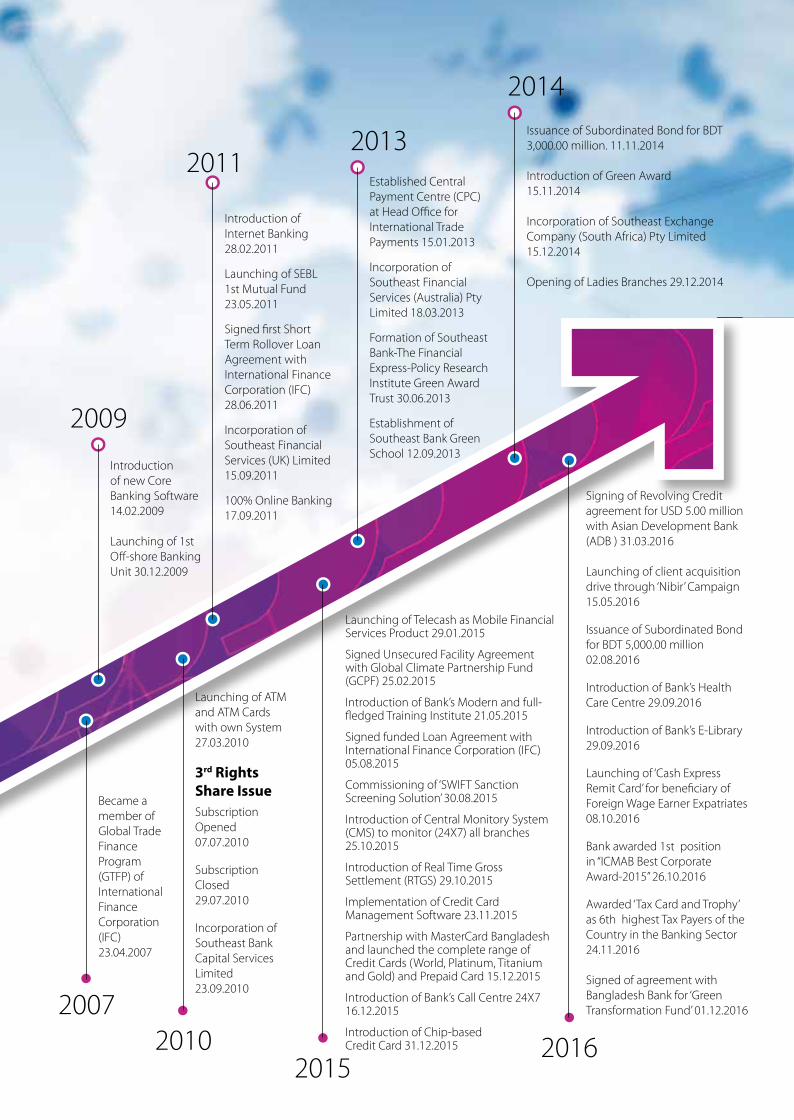

22 Years ofGlorious Journey

Incorporation of SEBL 12.03.1995

Certificate of Commencement of Business 12.03.1995

License Issued by Bangladesh Bank 23.03.1995

Formal Inauguration 25.05.1995

Inauguration of 1st Branch 25.05.1995

Formation of SEBL Foundation 12.03.2002

Listing with Dhaka Stock Exchange Limited 12.04.2000

Listing with Chittagong Stock Exchange Limited 24.04.2000

Registered as Depository Participant of CDBL 17.02.2004

1st to Demat Shares in CDS of CDBL in Banking Sector 16.05.2004

Became a member of Trade Finance Program (TFP) of Asian Development Bank (ADB) 20.10.2004

1995

2000

20022004

Initial Public Offer (IPO)

Subscription Opened25.11.1999

Subscription Closed05.12.1999

1999

2001

2003

1st Rights Share Issue

Subscription Opened15.02.2003 Subscription Closed 15.03.2003

Commencement of Islamic Banking business from Chhagalnaiya Islamic Banking Branch, Feni 28.07.2003

License Issued from Bangladesh Bank as a Primary Dealer 28.10.2003

Launching of ATM 01.09.2001

Launching of Credit Card 01.01.2005

2nd Rights Share Issue

Subscription Opened 15.10.2006

Subscription Closed 31.10.2006

2005

2006

Southeast Bank Limited I Annual Report 2016 21

Introduction of new Core Banking Software 14.02.2009

Launching of 1st Off-shore Banking Unit 30.12.2009

Established Central Payment Centre (CPC) at Head Office for International Trade Payments 15.01.2013

Incorporation of Southeast Financial Services (Australia) Pty Limited 18.03.2013

Formation of Southeast Bank-The Financial Express-Policy Research Institute Green Award Trust 30.06.2013

Establishment of Southeast Bank Green School 12.09.2013

Issuance of Subordinated Bond for BDT 3,000.00 million. 11.11.2014

Introduction of Green Award 15.11.2014

Incorporation of Southeast Exchange Company (South Africa) Pty Limited 15.12.2014

Opening of Ladies Branches 29.12.2014

Introduction of Internet Banking 28.02.2011

Launching of SEBL 1st Mutual Fund 23.05.2011

Signed first Short Term Rollover Loan Agreement with International Finance Corporation (IFC) 28.06.2011

Incorporation of Southeast Financial Services (UK) Limited 15.09.2011

100% Online Banking 17.09.2011

Became a member of Global Trade Finance Program (GTFP) of International Finance Corporation (IFC) 23.04.2007

Signing of Revolving Credit agreement for USD 5.00 million with Asian Development Bank (ADB ) 31.03.2016

Launching of client acquisition drive through ‘Nibir’ Campaign 15.05.2016

Issuance of Subordinated Bond for BDT 5,000.00 million 02.08.2016

Introduction of Bank’s Health Care Centre 29.09.2016

Introduction of Bank’s E-Library 29.09.2016

Launching of ‘Cash Express Remit Card’ for beneficiary of Foreign Wage Earner Expatriates 08.10.2016

Bank awarded 1st position in “ICMAB Best Corporate Award-2015” 26.10.2016

Awarded ‘Tax Card and Trophy’ as 6th highest Tax Payers of the Country in the Banking Sector 24.11.2016

Signed of agreement with Bangladesh Bank for ‘Green Transformation Fund’ 01.12.2016

Launching of Telecash as Mobile Financial Services Product 29.01.2015

Signed Unsecured Facility Agreement with Global Climate Partnership Fund (GCPF) 25.02.2015

Introduction of Bank’s Modern and full-fledged Training Institute 21.05.2015

Signed funded Loan Agreement with International Finance Corporation (IFC) 05.08.2015

Commissioning of ‘SWIFT Sanction Screening Solution’ 30.08.2015

Introduction of Central Monitory System (CMS) to monitor (24X7) all branches 25.10.2015

Introduction of Real Time Gross Settlement (RTGS) 29.10.2015

Implementation of Credit Card Management Software 23.11.2015

Partnership with MasterCard Bangladesh and launched the complete range of Credit Cards (World, Platinum, Titanium and Gold) and Prepaid Card 15.12.2015

Introduction of Bank’s Call Centre 24X716.12.2015

Introduction of Chip-basedCredit Card 31.12.2015

Launching of ATM and ATM Cards with own System 27.03.2010

3rd Rights Share Issue Subscription Opened 07.07.2010

Subscription Closed 29.07.2010

Incorporation of Southeast Bank Capital Services Limited 23.09.2010

2007

2009

20112013

2014

2010 20162015

Southeast Bank Limited I Annual Report 201622

Southeast Bank Limited has been awarded the First Position as the best Corporate in the Banking Sector (Private Bank-Traditional Operation) by “ICMAB Best Corporate Award-2015”. The Institute of Cost and Management Accountants of Bangladesh (ICMAB) exhaustively analyzed the Bank’s Annual Report -2015 and bestowed the prestigious award of the “First Position” for Bank’s outstanding performance, encouraging financial results

and indicators, sufficient disclosures for all stockholders and its commitment to quality Corporate Governance, and compliance with legal and regulatory requirements. Former Managing Director of Southeast Bank Limited received The Award from Abul Maal Abdul Muhith M. P., Hon’ble Minister, Ministry of Finance, Government of the People’s Republic of Bangladesh in a ceremony held on October 26, 2016.

Muhammad Shahjahan, Additional Managing Director and Company Secretary, Southeast Bank Limited received Tax Card and Crest from Md. Nojibur Rahman, Senior Secretary, Internal Resources Division (IRD) and Chairman National Board of Revenue (NBR), Ministry of Finance,

Government of the People’s Republic of Bangladesh. Southeast Bank has been given the country’s 6th highest Tax Payers Award in the Banking Institutions Category for the assessment year 2015-2016.

Awards and Recognitions

Southeast Bank Limited I Annual Report 2016 23

Awards and Recognitions

Southeast Bank Limited I Annual Report 201624

Awards and Recognitions

Southeast Bank Limited I Annual Report 2016 25

Board of Directors

Managing Director

Risk Management Committee

Additional Managing Director (Retail Banking and Technology Administration)

Additional Managing Director (Corporate Banking)

Additional Managing Director (Company Affairs

and Islamic Banking)

ExecutiveCommittee

Board Audit Committee

P. S to MD

Board Audit Cell

P.S. to Chairman

Corporate Banking Division

Information Technology

Division

BoardDivision

Internal Control and Compliance

Division

MD’sSecretariat

International Division Retail Banking

Division

ShareDivision Human Resources

Division

SME and Agri. Credit Division Card

Division

Islamic Banking Division Training

Institute

Legal Affairs and Recovery Division

Treasury Back Office Unit Alternative

Delivery Channel Unit

Corporate Marketing Division

Financial Control and Accounts

Division Management Information System Unit

Research and Development Unit

Branches and General Banking

Division

Remittance Division

TreasuryDivision

Central Compliance Unit

Credit Risk Management

Division

EstateDepartment

Logistic and General Services

Division Risk Management Division

Corporate Organogram

Deputy ManagingDirector

Southeast Bank Limited I Annual Report 201626

Group Corporate Structure

Sout

heas

t Ban

k Ltd

., a

2nd

gene

ratio

n ba

nk

was

inco

rpor

ated

as a

Publ

ic Lim

ited

Com

pany

on

Mar

ch 1

2, 19

95.

Afte

r rec

eivin

g Ba

nkin

g Lic

ense

, its 1

st br

anch

w

as o

pene

d on

May

25

, 199

5. Pr

esen

tly th

e Ba

nk h

as 1

28

Bran

ches

&

117

ATM

s acr

oss t

he

coun

try.

A nu

mbe

r of a

ttrac

tive

Depo

sits a

nd Lo

an

prod

ucts

are

avail

able

in

its p

rodu

ct b

aske

t. SE

BL h

as la

unch

ed R

etail

Ba

nkin

g, D

ebit

Card

s, Cr

edit

Card

s, M

obile

Ba

nkin

g (T

eleca

sh),

Ladi

es B

ranc

hes a

nd

24/7

Call

Cen

tre to

ca

ter t

o th

e ne

eds o

f all

segm

ents

of cu

stom

ers.

Asse

t Size

:BD

T 26

5,01

1.95

milli

onD

epos

its:

BDT

213,

771.

32 m

illion

Loan

s & A

dvan

ces:

BDT

173,

746.

47 m

illion

Ope

ratin

g Pr

ofit:

BDT

7,65

4.18

milli

on

Asse

t Size

:BD

T 20

,606

.07

milli

onD

epos

its:

BDT

16,7

40.5

7 m

illion

Inve

stm

ent:

BDT

9,29

1.20

milli

onO

pera

ting

Profi

t:BD

T 73

5.84

milli

onAs

set S

ize:

BDT

6,37

4.98

milli

onLo

ans &

Adv

ance

s: BD

T 6,

327.

28 m

illion

Ope

ratin

g Pr

ofit:

BDT

107.

79 m

illion

Dat

e of

Inco

rpor

atio

n:Se

ptem

ber 2

3,20

10Pa

id u

p Ca

pita

l: BD

T.5,5

00 m

illion

Ow

ners

hip

Inte

rest

in

Capi

tal:

BDT

5,48

9.93

milli

onIn

Per

cent

age:

99.

82%

Asse

t Size

: BD

T 5,

801.

61 m

illion

Dat

e of

Inco

rpor

atio

n:Fe

brua

ry 2

2, 2

011

Paid

up

Capi

tal:

GBP

300

,000

Ow

ners

hip

Inte

rest

in

Capi

tal:

BDT

38.4

9 m

illion

In P

erce

ntag

e: 1

00%

Asse

t Size

: G

BP 3

71,3

25

Dat

e of

In

corp

orat

ion:

Mar

ch 1

8,20

13Pa

id u

p Ca

pita

l:AU

D 3

12,0

82.9

0O

wne

rshi

p In

tere

st

in C

apita

l:BD

T 25

.06

milli

onIn

Per

cent

age:

100

%As

set S

ize:

AUD

52,

303.

19

Dat

e of

Inco

rpor

atio

n:D

ecem

ber 1

5,20

14Pa

id u

p Ca

pita

l:RA

ND

6,6

32,1

79O

wne

rshi

p In

tere

st in

Ca

pita

l:BD

T 50

.10

milli

onIn

Per

cent

age:

100

%As

set S

ize:

RAN

D 1

3,02

0,60

5

Tota

l CSR

rela

ted

Expe

nditu

re u

nder

SE

B Fo

unda

tion

in

2016

: BD

T 13

5.85

milli

on

Besid

es c

onve

ntio

nal

Bank

ing,

SEB

L ha

s 05

(five

) Isla

mic

ban

king

Br

anch

es b

ased

on

Isla

mic

Sha

riah

whe

re S

epar

ate

Acco

untin

g sy

stem

is

bein

g m

aint

aine

d.As

a p

art o

f str

ateg

ic

busin

ess p

lan,

Isla

mic

Ba

nkin

g Se

rvic

e D

esk

(IBSD

) has

alre

ady

been

exp

ande

d to

ev

ery

conv

entio

nal

Bran

ch.

To c

ater

to th

e de

man

d fo

r off-

shor

e ba

nkin

g se

rvic

es,

Sout

heas

t Ban

k es

tabl

ished

two

(02)

O

ff-sh

ore

Bank

ing

Uni

ts (O

BUs)

, one

in

DEP

Z an

d th

e ot

her

is CE

PZ. S

EBL

OBU

s pr

ovid

e a

cont

inuu

m

of fi

nanc

ial s

ervi

ces

such

as F

C Ac

coun

t fo

r Non

-resid

ents

, U

sanc

e Pa

yabl

e At

Sig

ht (U

PAS)

D

ocum

enta

ry C

redi

t, Ti

me/

Term

Loa

n in

Fo

reig

n Cu

rrenc

y, Fu

ll fle

dged

exp

ort-

impo

rt se

rvic

es e

tc.

from

200

9.

To c

arry

on

Mer

chan

t Ba

nkin

g O

pera

tions

in

a st

ruct

ured

way

, th

e Ba

nk e

stab

lishe

d ‘S

outh

east

Ban

k Ca

pita

l Ser

vice

s Li

mite

d’ a

s a

subs

idia

ry c

ompa

ny

in 2

010.

To c

olle

ct re

mitt

ance

fro

m B

angl

ades

hi

expa

triat

es in

Uni

ted

King

dom

for t

heir

bene

ficia

ries i

n Ba

ngla

desh

thro

ugh

prop

er B

anki

ng

Chan

nel, t

he B

ank

esta

blish

ed ‘S

outh

east

Fi

nanc

ial S

ervi

ces

(UK)

Lim

ited’

as a

su

bsid

iary

com

pany

in

201

1.

To c

olle

ct re

mitt

ance

fro

m B

angl

ades

hi

expa

triat

es in

Aus

tralia

fo

r the

ir be

nefic

iarie

s in

Ban

glad

esh

thro

ugh

prop

er

Bank

ing

Chan

nel,

the

Bank

est

ablis

hed

‘Sou

thea

st F

inan

cial

Se

rvic

es (A

ustra

lia)

Pty

Lim

ited’

as a

su

bsid

iary

com

pany

in

201

3.

To c

olle

ct re

mitt

ance

fro

m B

angl

ades

hi

expa

triat

es o

f So

uth

Afri

ca fo

r th

eir b

enefi

ciar

ies

in B

angl

ades

h th

roug

h pr

oper

Ba

nkin

g Ch

anne

l th

e Ba

nk e

stab

lishe

d ‘S

outh

east

Exc

hang

e Co

mpa

ny (S

outh

Af

rica)

Pty

Lim

ited’

as

a su

bsid

iary

com

pany

in

201

4.

To c

arry

out

Co

rpor

ate

Soci

al

Resp

onsib

ility

(CSR

) re

late

d a

ctiv

ities

in

an o

rgan

ized

and

sust

aina

ble

man

ner,

‘Sou

thea

st B

ank

Foun

datio

n’ w

as

esta

blish

ed b

y th

e Ba

nk in

-200

2.It

also

runs

an

Engl

ish

Med

ium

scho

ol

nam

ed S

outh

east

Ba

nk G

reen

Sch

ool a

t D

haka

.

Sout

heas

t Ban

k Li

mite

d

Conv

entio

nal

Bank

ing

Isla

mic

Ba

nkin

g

Mai

n O

pera

tions

Subs

idia

ries

CSR

Win

g

Off

-Sho

re

Bank

ing

Uni

ts

Sout

heas

t Ban

k Ca

pita

l Ser

vice

s Lt

d.

Sout

heas

t Fi

nanc

ial S

ervi

ces

(UK)

Ltd

.

Sout

heas

t Fi

nanc

ial S

ervi

ces

(Aus

tral

ia) P

ty L

td.

Sout

heas

t Ex

chan

ge

Com

pany

(Sou

th

Afric

a) P

ty L

td.

Sout

heas

t Ban

kFo

unda

tion

Southeast Bank Limited I Annual Report 2016 27

Last 10 Years’ Financial IndicatorsBD

T in

mill

ion

PART

ICU

LARS

2016

2015

2014

2013

2012

2011

2010

2009

2008

2007

Auth

oriz

ed C

apita

l15

,000

.00

15,

000.

00

15,

000.

00

10,

000.

00

10,0

00.0

0 10

,000

.00

10,0

00.0

0 10

,000

.00

3,50

0.00

3,

500.

00

Paid

up

Capi

tal

9,16

9.50

9,16

9.50

9,16

9.50

8,73

2.86

8

,732

.86

8,31

7.01

6,

930.

84

3,42

2.64

2,

852.

20

2,28

1.76

Rese

rve

Fund

/ Oth

ers

24,8

86.7

8 1

9,34

0.03

1

8,29

2.59

1

3,07

4.71

10

,864

.68

10,6

83.0

5 10

,265

.96

6,50

4.52

4,

804.

81

4,18

6.60

Tota

l Cap

ital (

Tier

-I+Ti

er-II

)34

,056

.28

28,5

09.5

3 27

,462

.09

21,8

07.5

7 19

,597

.54

19,0

00.0

6 17

,196

.80

9,92

7.16

7,

657.

01

6,46

8.36

Dep

osit

229,

973.

43

210,

431.

09

189,

472.

54

1

77,5

19.4

6 15

2,90

1.24

12

7,17

8.22

10

7,25

3.19

96

,669

.05

68,7

14.6

7 55

,474

.05

Adva

nce

191,

865.

59

168,

878.

46

147,

070.

81

134,

863.

82

126,

968.

97

107,

288.

56

93,9

81.2

0 77

,497

.57

60,2

81.2

6 48

,164

.60

Inve

stm

ent

61,7

31.6

3 58

,829

.27

56,3

78.5

9 57

,589

.06

39,0

11.2

8 29

,846

.60

18,8

69.0

7 21

,350

.23

12,2

99.6

1 8,

462.

86

Impo

rt B

usin

ess

171,

531.

73

151,

812.

58

155,

691.

00

131,

644.

82

111,

537.

50

99,5

09.0

1 10

3,72

6.70

69

,582

.92

58,0

19.7

7 38

,470

.34

Expo

rt B

usin

ess

146,

606.

09

1

26,4

23.8

9 11

2,13

7.60

95

,220

.40

84,4

64.2

0 75

,982

.06

58,1

58.0

6 46

,724

.47

42,1

78.6

0 28

,771

.36

Fore

ign

Rem

ittan

ce64

,665

.84

60,7

08.5

0 48

,740

.50

39,2

99.1

0 41

,455

.40

49,5

44.1

0 28

,082

.25

23,7

79.2

0 15

,221

.87

11,0

40.1

7

Gua

rant

ee B

usin

ess i

nclu

ding

ILC

16,3

69.3

6 15

,245

.19

13,6

03.3

0 17

,226

.41

21,5

06.6

5 25

,673

.90

22,7

81.1

9 11

,916

.74

15,0

78.9

9 9,

008.

32

Tota

l Inc

ome

25,6

17.5

7 26

,260

.72

27,6

67.1

0 26

,918

.30

23,1

34.1

8 19

,931

.91

16,1

00.8

1 13

,415

.21

10,2

50.1

3 8,

670.

47

Tota

l Exp

endi

ture

17,1

14.3

5 18

,226

.45

19,3

77.3

4 20

,218

.11

17,6

38.9

9 13

,846

.24

9,33

1.55

8,

800.

55

7,23

7.55

5,

754.

27

Ope

ratin

g Pr

ofit

8,50

3.22

8,

034.

27

8,28

9.76

6,

700.

20

5,49

5.19

6,

085.

67

6,76

9.26

4,

614.

66

3,01

2.58

2,

916.

20

Net

Pro

fit a

fter T

ax a

nd P

rovi

sion

2,43

5.07

3,

069.

42

3,83

6.94

3,

378.

82

1,64

8.72

1,

912.

19

2,76

3.93

1,

870.

19

887.

24

1,22

2.97

Fixe

d As

sets

8,94

7.16

7,

885.

23

7,91

3.00

7,

795.

65

7,67

7.51

7,

373.

11

4,46

3.64

4,

323.

59

2,68

5.56

1,

708.

11

Tota

l Ass

ets

291,

798.

01

260,

718.

03

236

,608

.40

220,

930.

85

191

,276

.30

158,

078.

59

131,

784.

27

112,

676.

98

81,1

81.5

3 64

,370

.69

Earn

ing

per S

hare

(BD

T)2.

66

3.35

4

.18

3

.68

1.

89

2.19

3.

77

3.24

3.

11

4.28

Div

iden

d C

ash

(%)

20%

15%

15%

16%

15%

15%

10%

- 15

%15

%

Bonu

s Sha

res

-

- 5%

(20:

1)

-

5% (2

0:1)

20%

(5:1

)35

% (2

0:7)

20%

(5:1

)25

% (4

:1)

Retu

rn o

n Eq

uity

(RO

E)9.

06%

11.8

6%16

.51%

16.2

0%8.

42%

10.4

7%19

.41%

16.5

1%12

.06%

19.9

0%

Retu

rn o

n As

set (

ROA)

0.88

%1.

23%

1.67

%1.

64%

0.95

%1.

32%

2.26

%1.

66%

1.09

%1.

90%

Non

-Per

form

anin

g Lo

an4.

89%

4.25

%3.

64%

3.94

%4.

47%

3.51

%4.

26%

3.73

%4.

12%

3.77

%

Capi

tal A

dequ

acy

Ratio

12.1

5%11

.52%

12.4

1%10

.90%

10.8

7%11

.46%

11.2

5%11

.72%

11.1

2%13

.00%

Num

ber o

f Cor

resp

onde

nt B

anks

248

220

211

211

183

161

152

146

145

140

Num

ber o

f For

eign

Cor

resp

onde

nts

807

811

791

778

691

654

645

589

587

598

Num

ber o

f Sha

reho

lder

s39

,009

46

,285

58

,169

65

,413

64,

060

68,0

39

66,8

98

22,1

52

12,5

36

9,63

6

Num

ber o

f Em

ploy

ees -

Ban

king

2,08

9 18

8917

8017

0416

5515

2613

7312

5410

8096

4

-

Non

Ban

king

527

487

441

414

355

322

240

148

151

152

Num

ber o

f Bra

nche

s12

8 12

211

310

394

8476

5646

38

SEBL at a glance

Southeast Bank Limited I Annual Report 201628

Forward Looking Ideology

This Annual Report-2016 of Southeast Bank Limited also contains forward-looking statements. Since there are uncertainties about the occurrence of the future events, those should be treated from that viewpoint in decision-making by the users of the Annual Report.

A forward-looking statement is a statement that contains predictions, projections and possibilities. It relates to future events. It often predicts expected future business and financial performance. It contains words such as ‘expect’, ‘anticipate’, ‘believe’, ‘seek’, ‘will’, ‘may’, ‘would’, ‘presume’, ‘assure’, ‘hope’, so on and so forth. A forward-looking statement naturally addresses matters that are, to certain degrees, uncertain and may not happen. In most cases, a forward-looking statement is made in respect of company’s expected income, earning, business growth, horizontal expansion, cost structure, capital structure, dividends etc. Such a statement is made based on some assumptions about future events which may happen or may not happen.

Southeast Bank Limited I Annual Report 2016 29

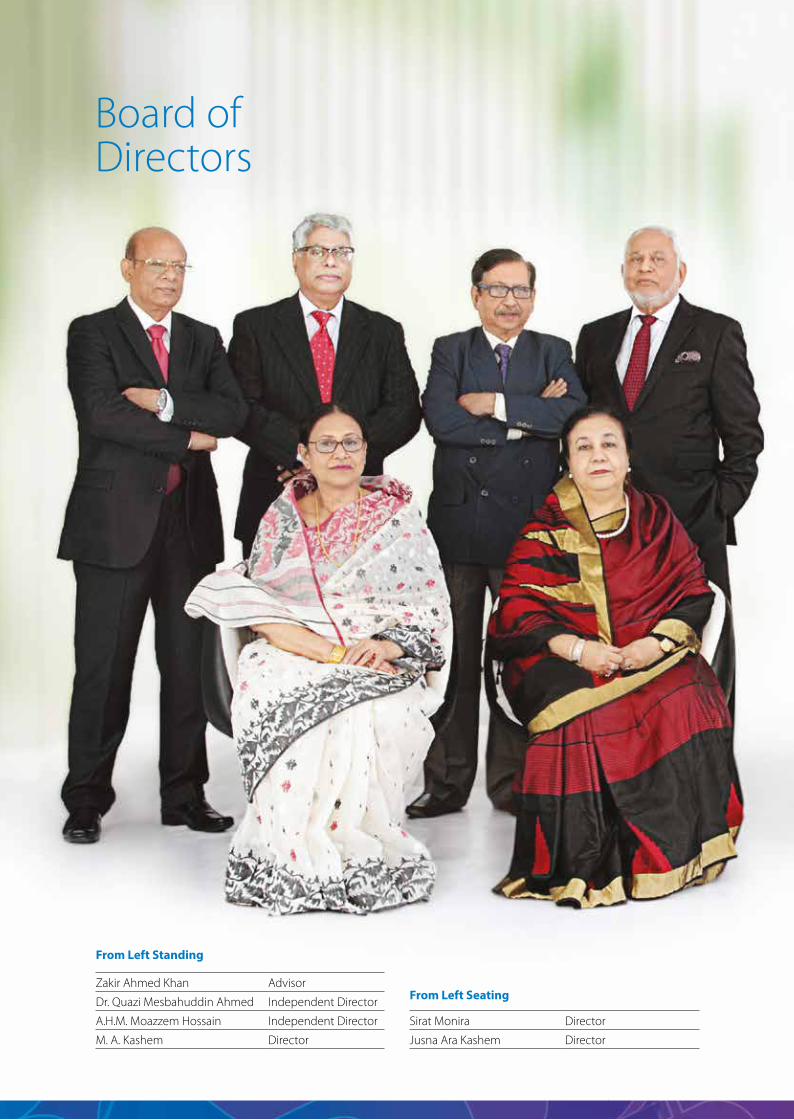

Board of Directors

ChairmanAlamgir Kabir, FCA

Directors M. A. Kashem

Azim Uddin AhmedDuluma Ahmed

Jusna Ara KashemMd. Akikur Rahman

Rehana RahmanSirat Monira

IndependentDirectors

A.H.M. Moazzem HossainDr. Quazi Mesbahuddin Ahmed

AdvisorZakir Ahmed Khan

Managing Director (CC)M. Kamal Hossain

SEBL at a glance

Board ofDirectors

Zakir Ahmed Khan Advisor

Dr. Quazi Mesbahuddin Ahmed Independent Director

A.H.M. Moazzem Hossain Independent Director

M. A. Kashem Director

From Left Standing

Sirat Monira Director

Jusna Ara Kashem Director

From Left Seating

Alamgir Kabir, FCA Chairman

Azim Uddin Ahmed Director

Md. Akikur Rahman Director

M. Kamal Hossain Managing Director (CC)

From Left Standing

Duluma Ahmed Director

Rehana Rahman Director

From Left Seating

Southeast Bank Limited I Annual Report 201632

ChairmanAlamgir Kabir, FCA

Members

M. A. Kashem

Azim Uddin Ahmed

M. Kamal Hossain

Executive Committee

Committees of the Board of Directors

Southeast Bank Limited I Annual Report 2016 33

Audit Committee

ChairmanA.H.M. Moazzem Hossain

Members

Duluma Ahmed

Jusna Ara Kashem

Rehana Rahman

Dr. Quazi Mesbahuddin Ahmed

Southeast Bank Limited I Annual Report 201634

hjhjhjh

Risk Management Committee

ChairmanAlamgir Kabir, FCA

Members

M. A. Kashem

Azim Uddin Ahmed

A.H.M. Moazzem Hossain

Southeast Bank Limited I Annual Report 2016 35

Shariah Supervisory Committee

ChairmanProfessor Moulana Mohammad Salah-Uddin (not in the picture)

Members

M. Kamaluddin Chowdhury

Moulana Mohammad Kafiluddin Sarker

Alamgir Kabir, FCA

M. A. Kashem

Azim Uddin Ahmed

M. Kamal Hossain

Mr. Alamgir Kabir, FCA was born on December 28, 1947. He did B.Com (Hons.) from the University of Dhaka and M.Com from Punjab University. He is a professional Chartered Accountant. He has wide experience and profound knowledge in Auditing, Accounting, Banking, Insurance and Financial Institutions both at home and abroad.

Mr. Kabir has been Chairman of the Board of Directors of the Bank since September 29, 2004. He is also the Chairman of the Executive Committee of the Board of Directors and the Risk Management Committee of the Board of Directors. He is the Chairman of its all subsidiary companies. He is also the Director of Asia Insurance Limited and Independent Director of National Life Insurance Co. Limited.

Mr. Kabir started his career in the year 1969 with Rahman Rahman Huq and Co., Chartered Accountants, Member Firm of KPMG, and continued with EWP Associates, Management Consultants, a sister concern of Rahman Rahman Huq and Co. and stayed there until 1979. In 1972, he wasin-charge of Audit Team for the first statutory Audit of Accounts of Bangladesh Bank. He moved to Riyadh, Saudi Arabia in 1979 with assignment in Saudi Accounting Bureau, Chartered Accountants, member firms of Coopers & Lybrand, Moores Rowland International and Inbucon International Ltd., as Management Consultant from 1979 to 1993. He returned to Bangladesh in 1993 with assignment in Bangladesh Securities and Exchange Commission as Member from 1993 to 1996 and also acted as the acting Chairman for a period. During his stay with BSEC, he substantially contributed to the development of the Capital Market of Bangladesh. From 1996 onward, he has been involved in different capacities in formation and development of Bank, Non-Banking Financial Institution, Insurance and Capital Market related Institutions and others.

From 1999 to 2003, Mr. Kabir was the founder Advisor of Export Import Bank of Bangladesh Limited of which his brother Late Shahjahan Kabir was the Founder Chairman. Both the brothers were involved in the formation of EXIM Bank and contributed to its rapid growth.

Mr. Kabir belongs to a family whose members are involved with Banks, Insurances and Financial Institutions. He is member of a number of associations and also associated with many social organizations where he is working very silently for the welfare of the people. Mr. Kabir is a widely traveled person across the globe.

Alamgir Kabir, FCAChairman

Directors’ Profiles and their representationon Board of otherCompanies

Southeast Bank Limited I Annual Report 2016 37

Mr. M.A. Kashem was the Founder Chairman of Southeast Bank Limited. Currently, he is a Sponsor Director of the Bank. He is also a member of the Executive Committee and the Risk Management Committee of the Board of Directors of the Bank. He is a member of North South University Trustee Board.

Mr. Kashem is the former President of the Federation of Bangladesh Chamber of Commerce and Industry (FBCCI), the apex body of all the business communities of Bangladesh. He was the Chairman of Arbitration Tribunal of FBCCI. He is the past Chairman of the Association of Private Universities of Bangladesh (APUB) which represented all Private Universities of the country. Mr. Kashem was a member of Board of Trustees of Hamdard Laboratories (WAQF) Bangladesh, the leading producer of herbal medicines in the sub-continent for over 17 (Seventeen) years. He is the President of SAHIC Trust (Society for Assistance to Hearing Impaired Children), the only voluntary organization rendering health care assistance of the ear, nose and throat services to destitute and poor patients.

Mr. Kashem is an eminent industrialist, renowned patron of education, distinguished philanthropist and an active social worker. He is the winner of “President Export Trophy Award” for the year 1982-83 & 1983-84 for excellent export performance. Mr. Kashem also got “C.R. Das Gold” Medal for excellent contribution in the Industrial sector in the year 1995. He was awarded the “Highest Tax Prayer-2011” by National Board of Revenue (NBR) for Dhaka City Corporation.

Mr. Kashem was the leader of 20-member FBCCI Trade delegation to Far Eastern Countries in the year 1986. He was also the leader of 5 member Govt. delegations to U.K., U.S.A. and Canada sponsored by UNDP in 1987 and leader of 12 member EPB Govt. of Bangladesh delegations to EEC countries in 1985. As an industrialist, he travelled almost all major cities of the world many times on his own business and also led trade delegations.

As a philanthropist, Mr. Kashem set up a number of Schools, Madrashas, Moshjid, Club etc. and erected free dwelling houses for the poor and destitute people of his locality. He has established a Trust named M. Kashem Trust to foster education to the primary and mid-level students of schools in his locality. The Trust awarded stipends and Scholarships to the meritorious students during the last couple of years. Moreover, a General Hospital (Non-Profit) of 50 Beds in the name of “Tareque Memorial Hospital” is at present in operation at his home district. Mr. Kashem is a member of the Rotary Club of Dhaka West, Kurmitola Golf Club, Gulshan Club Limited, Bangladesh Diabetic Association, Dhaka, Bangladesh Red Crescent Society, National Shooting Club and Shishu Hospital, Chittagong.

M. A. KashemDirector

SEBL at a glance

Southeast Bank Limited I Annual Report 201638

Mr. Azim Uddin Ahmed was born on June 30, 1940. He is a graduate from the University of Dhaka. As a former Chairman of Southeast Bank Limited, he pushed the Bank forward. Currently, he is a Sponsor Director of the Bank. He is also a member of the Executive Committee and the Risk Management Committee of the Board of Directors of the Bank.

Mr. Azim Uddin Ahmed is a well-known business personality of the country. He is the Chairman of Mutual Food Products Limited, Mutual Milk Products Limited and Mutual Trading Co. Ltd. He is also the partner of Mutual Agro-complex, Mutual Departmental Store and Mutual Distribution and Silonia Agencies. Mr. Azim is the current chairman of the Board of Trustees of North South University and founder life member of North South University Foundation.

Mr. Azim is associated with a number of trade bodies and associations devoted to social work. He is the past President of Rotary Club of Dhaka North and Area Governor of Rotary District. He was the past President of Gulshan Club Ltd. He is the President of Baridhara Society. He served in different capacities in Dhaka Chamber of Commerce and Industry (DCCI), Federation of Bangladesh Chamber of Commerce and Industry (FBCCI) and Bangladesh Indenting Association. He is the current President of Bangladesh Consumer Products Manufacturers and Marketers Association. He represented Bangladesh as a member of Trade Delegation to Europe and many other Govt. and private trade delegations to European, American and Asian countries.

Mr. Azim is also engaged in philanthropic activities. He is the Founder of Azimia Islamia Senior Madrasha, Duluma Azim High School, Fatema Farzana Kindergarten and Purba Silonia Forkania Madrasha. He is a widely traveled person across the globe.

Azim Uddin AhmedDirector

Southeast Bank Limited I Annual Report 2016 39

Mrs. Duluma Ahmed was born on July 7, 1947. She hails from a very respectable Muslim family. She is a Sponsor Director of the Bank and a member of the Audit Committee of the Board of Directors of the Bank. She is associated with business activities. She is the Director of Mutual Food Products Limited, Mutual Milk Products Ltd., Mutual Trading Co. Ltd. She is the partner of Mutual Distribution and Silonia Agencies.

Mrs. Duluma Ahmed is also associated with philanthropic activities. She is the Founder of Duluma Azim High School. She is the patron of Azimia Islamia Senior Madrasha and Fatema Farzana Kindergarten School in Chhagalnaiya. She is a member of Gulshan Ladies Community Club and Inner Wheel Club of Dhaka North. As a social worker, she is lavishly contributing to the poor and the needy section of the society. She traveled many countries of the world.

Duluma AhmedDirector

SEBL at a glance

Southeast Bank Limited I Annual Report 201640

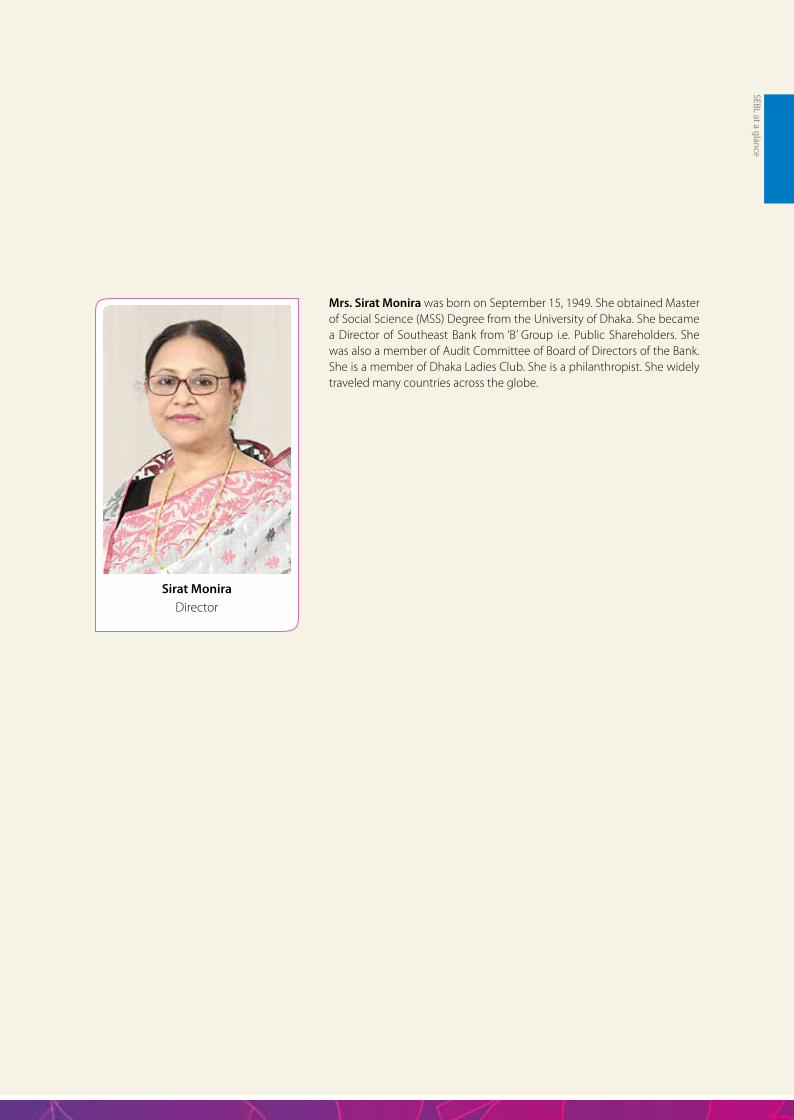

Mrs. Jusna Ara Kashem was born on December 7, 1951. She is a leading industrialist and business leader of the country. She is a Director of Rose Corner (Pvt.) Limited. She hails from a very respectable Muslim family of Rajshahi. She is a Sponsor Director of the Bank and a member of the Audit Committee of the Board of Directors of the Bank.

Mrs. Jusna Ara Kashem is associated with many humanitarian and philanthropic organizations and is the Vice Chairman of M. Kashem Foundation. This Foundation set up a 50 bed Hospital namely “Tareque Memorial Hospital” at Chhagalnaiya, Feni. Mrs. Jusna Ara Kashem is very amiable in nature and a good social worker.

Jusna Ara KashemDirector

Southeast Bank Limited I Annual Report 2016 41

Mr. Md. Akikur Rahman was born on February 15, 1945. He is a Sponsor Director of the Bank. He is a successful businessman. He is the Chairman of RAR Investment Limited of Murad Vill, Nower Road, Dorking Surrey, RH43Y, United Kingdom. He is also the Chairman of Dorking Muslim Community Association of 11/15, Hart Road, Doring, Surrey, RH4 1JS, United Kingdom. He is the Managing Director of RAR Holding Limited, 12-25, Prioy Prangan Tower, 19 Kemal Ataturk Avenue, Banani, Dhaka. He is also the Vice Chairman of International Medical College and Hospital, Gusholia, Tongi, Gazipur, Bangladesh. Mr. Akikur Rahman is associated with Southeast Bank Limited since its inception in 1995 as a Sponsor.

Md. Akikur RahmanDirector

SEBL at a glance

Southeast Bank Limited I Annual Report 201642

Mrs. Rehana Rahman was born on June 06, 1948 in a respectable Muslim family of Khulna. She is a graduate. She is a leading industrialist and a business leader. She is the Managing Director of Bengal Trade Ways Limited and a Director of Drift Packaging Limited. She is a member of the Board of Trustees of North South University Foundation. Formerly, she was the Chairman of North South University Foundation. She was appointed a Sponsor Director of the Bank by the Board of Directors in its 443rd meeting held on August 11, 2014. Her appointment as Director was approved by Bangladesh Bank by Letter dated August 31, 2014. She is a Member of the Audit Committee of the Board of Directors of the Bank. Mrs. Rehana Rahman is a widely traveled person and a social worker.

Rehana RahmanDirector

Southeast Bank Limited I Annual Report 2016 43