OPTIONS UNSCRAMBLING THE BINARY CODE Binary options, unlike standard options, tend to have discontinuous pay-offs. Mark Rubinste in and Eric Reiner value a variety ofthese instruments T he pay-offs of binary options tend to be switched completely one way or the other depending on whether the underlying asset price satisfies some condition. 1 This articl e considers a wide variety of binaries, first thos e with path- independent pay-off s and then the more complex barrier binaries with path- dependent pay-offs. Our objective is to value a variety of these options in a Black-Scholes environ- ment, that is: (1) where the underlying asset return can be assumed to follow a lognormal random walk, and (2) wh e re arbitrage arguments allow us to use a risk-neutral valuation approach - discount the expected pay-off of the option at expiration by the riskless interest rate, where the underl ying asset price is expected to appreciate at the same riskless rat e less pay-outs. Under these conditions, the (Black- Scho les) formula for a standard option is C=<j>Sd - 1 N(<j>x)-<j>Kr - 1 N(<j>x-<j>oVt) where x=[log(Sd- 1 /Kr- 1 )-,-oVt]+½oVt S is th e present value of the underlying asset, K is the strik e price , r is one plus the rate of interest, d is one plus the pay- out rate of the underlying asse t, t is the time-to-expiration of the option, o is the volatility of the underlying asset, N(·) is the standard normal distribution function, and the binary variable <j> is set equa l to 1 for a call and -1 for a put. 2 Path-independent binary options Caslr-or-11otlri11g calls a11dputs The simp- lest binar y call (put) pays off nothing if the und erlying asset price (S") finishes 1 Fora brief taxonomy of someof thesecontracts(referred to there as digitaloptions). see Mike Hudson. Thevalue ingoing out, RISK March 1991, page 31. ' Since the values of standard European optionsdependonly on the price of the underlying assetat expiration. it 1s possible to letr, d and o beknown functions oftime. However, since the options discussed in this article dependin complexways on the pathstaken by the underlying assetthroughtime. to keepmatters simple, we a~sume herethat thesevariables are constant. RISK below (above) th e strike price (K), or pays out a predetermined constant amount (X) if the underlying asset finishes above (be- low) the _s trike price: call: 0 if S':SK, or X if S'>K put: 0 if S 0 2:K, or X if S"<K In a Black-Scholes environment, such an option is easy to value . Recall that the Black-Scholes formula can be decomposed into the difference between two terms: the unprotected present value of the underlying asset price conditional upon exercising the option, Sd- tN(<j>x) , and the The pay-off ofbinary options tend to beswitched completely one way orthe other depending on whether the underlying asset price satisfies some condition present value of the strike price, Kr- 1 , times th e risk-neutral probability of exercising the option, N(<j>x-<j>oVt). If the predeter- mined pay-off of the cash-or-nothing call (X) were equal to the strike price (K), then a cash-or-nothing call would be like a stan dard written call except that, although the writer receives the strike price, he is under no obligation to deliver the under- lying asset. Such a "par tial call" would then be worth Kr- 1 N(x-oVt) to the writer. More ge nerally, allowi ng X'FK, the value of a cas h-or-nothin g call would be xr- 1 N (<j>x-<j>oVt)with <j>=l. Similarly, th e value of a cash-or-nothing put is th e same, but with <j>=-1. Assct-or-11otlri11g calls a11d puts' Somewha t more compl ex binary options, these have the following pay-offs : call: 0 if S':SK, or s· if S">K put: 0 if s ·2:K, ors· if S'<K 3 These optionsare discussed inJohnCoxand MarkRubinstein. Options Markets. page 460, Prentice-Hall, 1985. These options are simi lar to cash-or- nothing options, except that when they pay off th e amount is not predetermined but rather is equal to the underlying asset price at expiration. To value these, we look instead to the first term of the Black- Scho les formula. This gives us exactly what we need : the unprotected present va lu e of the underlying asset price con- ditional upon exercising the option. So the value of an asset-or-nothing call is simply Sd- 1 N(<j>x) with <j>=l, and the value of an asset-or-nothing pu t is the same, but with <j>= -1. Gap options Our next options are sligh tly more complex than stan dard options: call: 0 if S':SK, or s· -X if S">K put: 0 if S'2:K, or S' -X if S'<K These options highlight th e dual role played by th e strike price in a standard op tion: K not only determines whether the option finishes in the money or out of the money but also the size of the resulting pay-off (X). Th ere is no logical necessity for these tw o functions to be vested in a sing le number. The "gap" is defined as X-K. Positive gap calls will clearly sell for less than standard calls, while positive gap puts will be worth more than their sta ndard counterparts . The value of a gap option may be derived by subtractin g a cash-or-nothing option from an asset-or-nothing option: C=<j>Sd - 1 N(<j> x)-<j>Xr- 1 N(<j>x -<j>oVt) where This is almost identical to the Black- Scholes formula for a standard option. Supershares In an article publish ed in 1976, Nils Hakansson proposed a financial intermediary that would hold an under- lying portfolio and issue claims called "s upershar es" against thi s portfolio to investors . 4 A supershare is a security that 4 SeeNilsHakansson, The purchasing power fund:a newkind of financial intermediary, Financial Analysts Journal, November- December 1976 . VOL 4/N0 9/OCTOBER 1991 75

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

OPTIONS

UNSCRAMBLING THE BINARY CODE

Binary options, unlike standard options, tend to have discontinuous pay-offs. Mark Rubinstein and Eric Reiner value a variety of these instruments

The pay-offs of binary options tend to be switched completely one way or

the other depending on whether the underlying asset price satisfies some condition. 1 This articl e considers a wide variety of binaries, first thos e with pathindependent pay-off s and then the more complex barrier binaries with pathdependent pay-offs.

Our objective is to value a variety of these options in a Black-Scholes environment, that is:

(1) where the underlying asset return can be assumed to follow a lognormal random walk, and (2) wh ere arbitrage arguments allow us to use a risk-neutral valuation approach - discount the expected pay-off of the option at expiration by the riskless interest rate, where the underl ying asset price is expected to appreciate at the same riskless rate less pay-outs.

Under these conditions, the (BlackScho les) formula for a standard option is

C=<j>Sd- 1N(<j>x)-<j>Kr- 1N(<j>x-<j>oVt) where

x=[log(Sd- 1/Kr- 1)-,-oVt]+½oVt

S is the present value of the underlying asset, K is the strik e price , r is one plus the rate of interest, d is one plus the payout rate of the underlying asse t, t is the time-to-expiration of the option, o is the volatility of the underlying asset, N(·) is the standard normal distribution function, and the binary variable <j> is set equa l to 1 for a call and -1 for a put. 2

Path-independent binary options

Caslr-or-11otlri11g calls a11d puts The simplest binar y call (put) pays off nothing if the und erlying asset price (S") finishes

1 For a brief taxonomy of some of these contracts (referred to there as digital options). see Mike Hudson. The value in going out, RISK March 1991, page 31.

' Since the values of standard European options depend only on the price of the underlying asset at expiration. it 1s possible to let r, d and o be known functions of time. However, since the options discussed in this article depend in complex ways on the paths taken by the underlying asset through time. to keep matters simple, we a~sume here that these variables are constant.

RISK

below (above) th e strike price (K), or pays out a predetermined constant amount (X) if the underlying asset finishes above (below) the _strike price:

call: 0 if S':SK, or X if S'>K put: 0 if S0 2:K, or X if S"<K

In a Black-Scholes environment, such an option is easy to value . Recall that the Black-Scholes formula can be decomposed into the difference between two terms: the unprotected present value of the underlying asset price conditional upon exercising the option, Sd- tN(<j>x), and the

The pay-off of binary options tend to be switched completely one way or the other depending on whether the underlying asset price satisfies some condition

present value of the strike price, Kr- 1, times th e risk-neutral probability of exercising the option, N(<j>x-<j>oVt). If the predetermined pay-off of the cash-or-nothing call (X) were equal to the strike price (K), then a cash-or-nothing call would be like a stan dard written call except that, although the writer receives the strike price, he is under no obligation to deliver the underlying asset. Such a "par tial call" would then be worth Kr- 1N(x-oVt) to the writer. More ge nerally, allowi ng X'FK, the value of a cash-or-nothin g call would be xr- 1N (<j>x-<j>oVt)with <j>=l. Similarly, th e value of a cash-or-nothing put is th e same, but with <j>=-1.

Assct-or-11otlri11g calls a11d puts' Somewha t more compl ex binary options, these have the following pay-offs :

call: 0 if S':SK, or s· if S">K put: 0 if s ·2:K, ors· if S'<K

3 These options are discussed in John Cox and Mark Rubinstein. Options Markets. page 460, Prentice-Hall, 1985.

These options are simi lar to cash-ornothing options, except that when they pay off th e amount is not predetermined but rather is equal to the underlying asset price at expiration. To value these, we look instead to the first term of the BlackScho les formula. This gives us exactly what we need : the unprotected present value of the underlying asset price conditional upon exercising the option. So the value of an asset-or-nothing call is simply Sd- 1N(<j>x) with <j>=l, and the value of an asset-or-nothing pu t is the same, but with <j>= -1.

Gap options Our next options are sligh tly more complex than stan dard options:

call: 0 if S':SK, or s· -X if S">K put: 0 if S'2:K, or S' -X if S'<K

These options highlight th e dual role played by th e strike price in a standard op tion: K not only determines whether the option finishes in the money or out of the money but also the size of the resulting pay-off (X). Th ere is no logical necessity for these tw o functions to be vested in a sing le number. The "gap" is defined as X-K. Positive gap calls will clearly sell for less than standard calls, while positive gap puts will be worth more than their sta ndard counterparts . The value of a gap option may be derived by subtractin g a cash-or-nothing option from an asset-or-nothing option:

C=<j>Sd- 1N(<j>x)-<j>Xr-1N(<j>x-<j>oVt) where

This is almost identical to the BlackScholes formula for a standard option.

Supershares In an article publish ed in 1976, Nils Hakansson proposed a financial intermediary that would hold an underlying portfolio and issue claims called "supershar es" against thi s portfolio to investors . 4 A supershare is a security that

4 See Nils Hakansson, The purchasing power fund: a new kind of financial intermediary, Financial Analysts Journal, NovemberDecember 1976.

VOL 4/N0 9/OCTOBER 1991

75

OPTIONS 5 Cox and Rubinstein, Options Markets, p.371-375. describes a rule for using a portfolio of standard call options. and possibly cash and the underlying asset itself, to construct generalised piecewise linear pay-off patterns. However, since these ~basis" securities all have continuous pay-otts, all portfolios constructed from them must also have continuous pay-off patterns. Using cash-or-nothing and asset-or-nothing calls permits discontinuous pay-otts as well (as illustrated In the example). For a given set of breakpoints, this approach also permits greater control over the slope of the pay-off pattern between breakpoints than can be provided with supershares.

entitles its owner, on its ex piration date , to a given dollar value proportion of the assets of the underlying portfolio, provided the value of those assets on that date lies between a lower value K1 and an upper value Kh. Otherwise, the sup ers har e expires worthless, Th a t is , the pay-off is:

0 if S'<K 1 S'/K1 if K1:oS<Kh

0 if Kh:::S

It is easy to see that such an option has the same pa y -off as (l / K1) bullish vertical spreads of asset-or-nothing calls, where the purchased asset-or-nothing call ha s a strike price K1 and the written asset-ornothing call ha s a strike pric e Kh, That is,

C=(Sd - 1/ K1)[N(x1)-N(x h)l x1=[1og(Sd- 1/K1r- 1)-:-0Vt]+½0Vt, xh=[log(Sd- 1/Khr- 1)-:-oVt]+ ½oVt

These securities can be shown to be building blocks for constructing other mor e common securities such as purchased standard calls and puts,

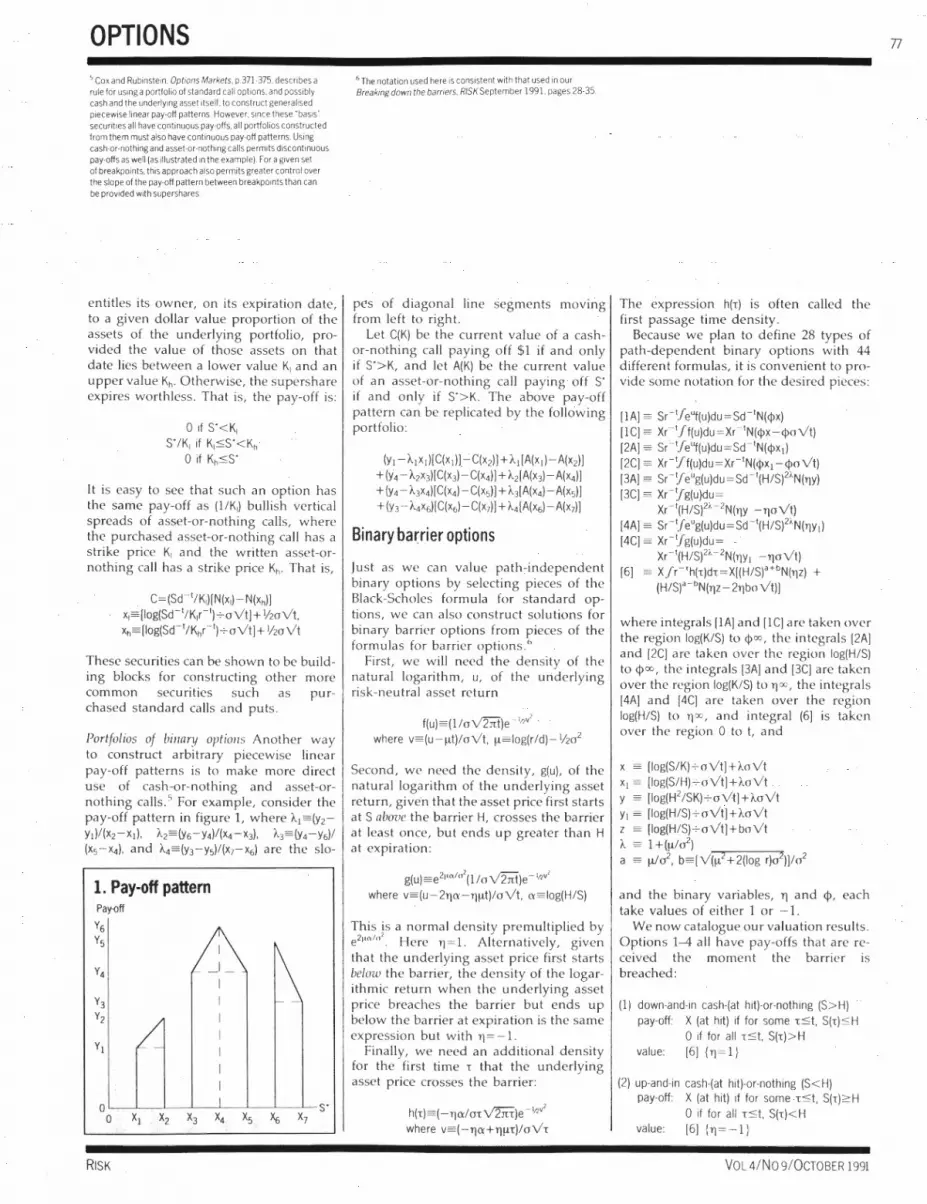

Portfolios of binary options Another wa y to construct arbitrary piecewis e linear pay-off patterns is to mak e more direct use of cash-or-nothing and asset-ornothing calls, 5 For example, consider the pay-off pattern in figure 1, where )..1 = (y2-Y1)/ (x2-x i), A2=(y6-y4)/(xcx3), ),3= (YcY6)/ (x5-X4), and A4=(y3-y 5)/(x7-x 6) are the slo-

1. Pay-off pattern Pay-off

y6

Y5

Oc_--' _ _j_ _ _J_ _ .....L _ _,.__--'--_.,___ S. 0

RISK

6 The notation used here is consistent with that used in our Breaking down the barriers, RISK September 1991, pages 28-35.

pe s of diagonal line segments moving from left to right

Let C(K) be the current value of a cashor-nothing call paying off $1 if and only if S'>K, and let A(K) be th e current value of an asse t-or -nothin g call pa ying off s· if a nd on ly if S'> K. The above pay-off pattern can be re plicat e d by th e following p or tfoli o:

(Y1 -A1X1)[C(xi)]-C(x2)]+ ),i(A(xi)- A(x2)] +(y4 - A2X3)[C(x3)-C(x4)] + A2[A(x3)-A(x4)] + (y4 - A3X4)[C(x4)-C(x5)] + A3(A(x4)-A(x5)] + (y3- A4X6)[C(x6)-C(x1)l + ),4[A(x6)-A(x7)]

Binary barrier options

just as w e can value path-ind ependent binary options by selecting pi eces of th e Black -Sc hole s formula for standard option s, we can also construct so lutions for binary barrier options from pieces of the formulas for barrier options."

First, we will n ee d th e d e nsity of the natural logarithm , u, of the und e rlying risk-neutr a l asse t re turn

f(u)= (lloV2Jct)e- 'av' where v=(u-µt)/oYt, ft=log(r/d) - ½o 2

Second, we n ee d the d e nsity , g(u), of the natural logarithm of the underl y ing asset return, given that the asset pric e first starts at S above the barri e r H, crosses th e barrier at least onc e, but ends up greater than H at ex piration :

g(u)=e21'n/o7( 1 /oY2rrt)e - l,:,v2

where v=(u - 2T]U'-1iµt)/0Yt, U'=log(H/S)

This js a normal density pr e multipli ed by e2" 0 1". Herc Tj=l. Alternatively, given that th e underlyin g asset pric e first s ta rts below the barrier, the density of th e logarithmic return wh e n th e und e rlying asset price breaches the barrier but ends up below the ba rrier at expiration is the same ex pres sion but with T]=- 1.

Finally, we need an additional density for the first tim e t that the und e rlying asset price crosses th e barrier:

h(t)=(- T]U'lo tV2in)e - 'av' where v=(-TJU'+T]µt)/oYt

The expression h(t) is often called the first passage time density.

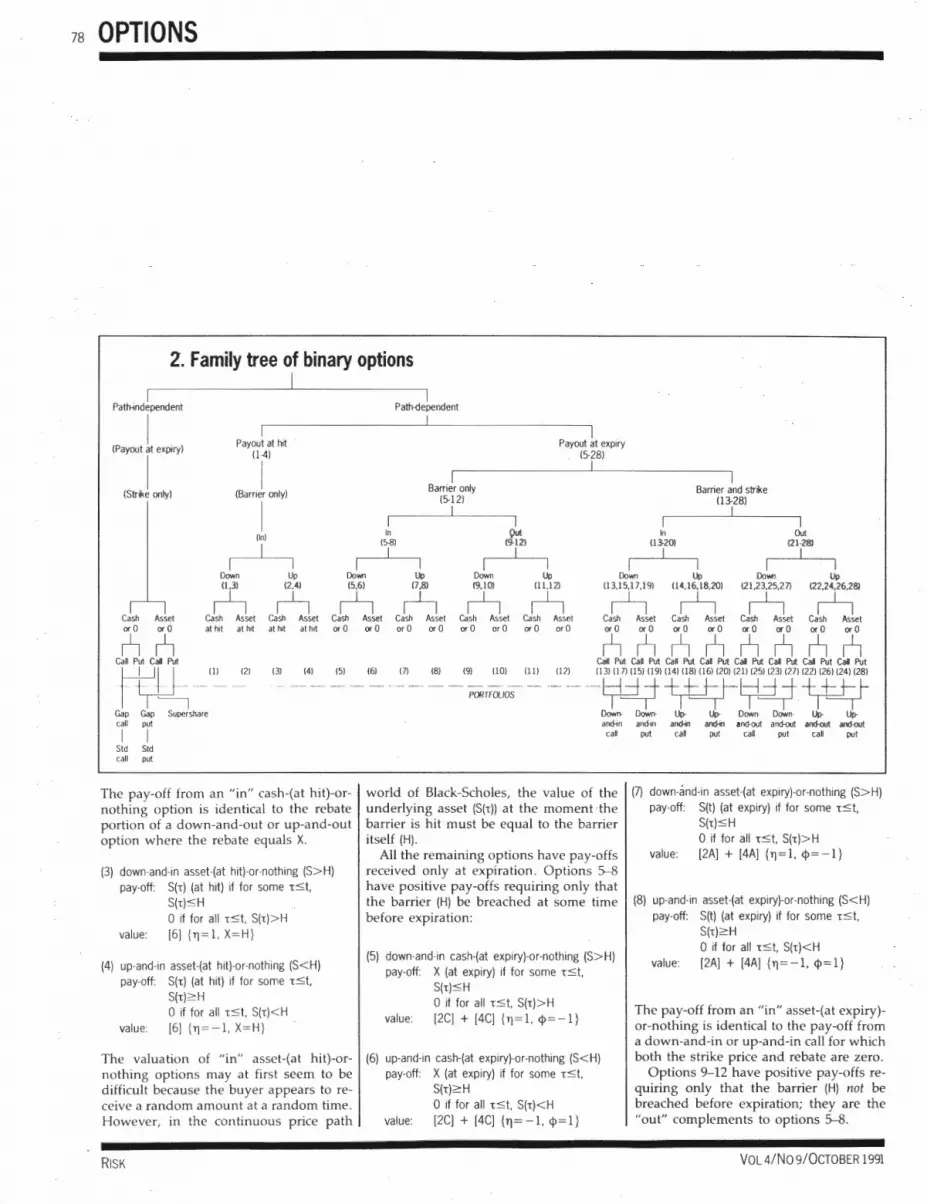

Because we plan to define 28 typ es of path-dependent binary options with 44 different formulas , it is convenient to provide some notation for th e desired pi eces:

[lA] = sr- 1/e"f(u)du=Sd - 'N(<jlx) [lC] = xr- 1./f(u)du=Xr - 1N(<jlx-<jloY t) [2A] = sr - '/e"f(u)du=Sd- 1N(<jixi) [2C] = xr- 1/f(u)du=Xr- 1N(<jlx1 -<jloYt) [3A] = Sr- './e"g(u)du=Sd - 1(H/S)2;·N(TJY) [3C] = Xr- '.f g(u)du=

Xr- 1(H/S)2;·- 2N(TJY -110Vt) [4A] = Sr- 1.f e"g(u)du=Sd- 1(H/S)2;,N(11yi) [4C] = Xr- 1.f g(u)du=

Xr- 1(H/S)2)·- 2N(11Y1 - TJoYt) [6] = Xf r- 'h(i:)di:=X[(H/S)a+bN(TJZ) +

(H/S)°-bN(T]Z- 211bo Vt)]

where integrals [lA] and [lC] are taken over the region log(K/S) to qioo, the integrals [2A] and [2C] arc tak e n over the region log(H/S) to qioo, the integrals [3A] and [3C] are taken over the reg ion log(K/S) to T]oo, the integrals [4A] and [4C] are tak e n over the region log(H/S ) to T]00 , and integral (6] is taken over the region 0 to t, and

x = [log(S/ K)-:-oV t]+) ,oY t x1 = [log(S/H)-:-oVt] +),oY t y = [log(H2/SK)-:-oVt]+AoYt y1 = [log(H/S)-:-oVt]HoVt z = [log(H/S)-:-oVt]+bo V t ),_ = 1 +(µ/o 2) a = µ/ o2, b=[Y(µ 2+2(1og r)o2)]/o2

and the binary variables, T] and qi, each take values of either 1 or - 1.

We now catalogue our valuation res ults. Options 1-4 all have pa y-o ffs th a t arc received th e moment the barrier is breached:

(1) down-and-in cash·(at hit)-or-nothing (S>H) pay-off: X (at hit) if for some ,:S t, S(1)S H

0 if for all ,:S t, S(i:)>H value: [6] {T]=l}

(2) up-and-in cash-(at hit)-or-nothing (S< H) pay-off: X (at hit) if for some ,:SI, S(1)::,.H

0 if for all i:S t, S(i:)<H value: [6] {ri=-1}

VOL4/N09/0CTOBER 1991

77

1s OPTIONS

2. Family tree of binary options

Path-indipendent

(Payout r expiry)

(Strike only)

I

Payout at hit (1-4)

I (Barril only)

Un}

I Down 0 ,3}

Up 12,4}

I 0o""1 15,6}

Path-<lependent

In 15-8}

I I

Up 17,8}

Barrier only (5-12)

I Down 19,10}

Qut (9-12}

I

Payout at expiry (5-28)

In (13-20}

Barrier and strike (13-28)

I I I

Out 121-28}

Up (11,12}

Down Up Down Up 03,15,17,19} (14,16, 18,20} (21,23,25,27) 122,24,26,28} n n n n n n nnnn

Cash Asset Cash Asset Cash Asset Cash Asset Cash Asset Cash Asset Cash Asset Cash Asset Cash Asset Cash Asset Cash Asset orO orO at hit at hrt atM athit orO orO or O or 0 or O or 0 or O orO orO orO orO orO orO orO orO orO nn

Call Put Call Put r~ Gap Gap Supershare

(I} 12} 13} (4} 15}

call put

I I Std Std call put

The pay-off from an "in" cash-(at hit)-ornothing option is identical to the rebate portion of a down-and-out or up-and-out option where the rebate equals X.

(3) down-and-in asset-(at hit)-or-nothing (S>H) pay-off: S{t) (at hit) if for some ,st,

S(t)SH 0 if for all ,:St, S(,:)>H

value: [6] {TJ=l, X=H}

(4) up-and-in asset-(at hit)-or-nothing (S<H) pay-off: S(t) (at hit) if for some ,st,

S{t)~H 0 if for all ,:St, S(,:)<H

value: [6] {TJ=-1, X=H}

nnnnnnnn (6} 18} 19} (10} (II} (12}

Call Put Call Put Call Put Call Put Call Put Can Put Call Put Call Put (13} (17} (15} (19} (14} 118} 116} 120} 121} 125} (23} 127} 122} 126} 124} 128}

PORTFOLIOS --·-M ·M -·M ·-M Down- Down- Up- Up- Down- Down- Up- Up-and-in and-in and-in and-in and-out and-Out and-Out and-OU! call put can put caU put call put

world of Black-Scholes, the value of the underlying asset (S(t)) at the moment the barrier is hit must be equal to the barrier itself (H).

All the remaining options have pay-offs received only at expiration . Options 5--8 have positive pay-offs requiring only that the barrier (H) be breached at some time before expiration:

(5) down-and-in cash-(at expiry)-or-nothing (S>H) pay-off: X (at expiry) if for some ,st,

S(t)SH 0 if for all ,:St, S(t)>H

value: [2C] + [4C] {TJ=l, <jJ=-1}

(7) down-and-in asset-(at expiry)-or-nothing (S>H) pay-off: S(t) (at expiry) if for some ,st,

S{t)SH 0 if for all ,:St, S(i:)>H

value: [2A] + [4A] {TJ=l, <jJ=-1}

(8) up-and-in asset-(at expiry)-or-nothing (S<H) pay-off: S(t) (at expiry) if for some ,:St,

S(t)~H 0 if for all ,:St, S(t)<H

value: [2A] + [4A] {TJ=-1, <jJ=l}

The valuation of "in" asset-(at hit)-or- (6) nothing options may at first seem to be difficult because the buyer appears to receive a random amount at a random time . However, in the continuous price path

up-and-in cash-(at expiry)-or-nothing (S<H) pay-off: X (at expiry) if for some ,st,

S(t)~H 0 if for all ,st, S(i:)<H

value: [2C] + [4C] {TJ= -1, qi= 1}

The pay-off from an "in" asset-(at expiry)or-nothing is identical to the pay-off from a down-and-in or up-and-in call for which both the strike price and rebate are zero.

Options 9-12 have positive pay-offs requiring only that the barrier (H) not be breached before expiration; they are the "out" complements to options 5--8.

RISK VOL 4/N0 9/OCTOBER 1991

OPTIONS

(9) down-and-out cash-or-nothing (S> H) pay-off: X (at expiry) if for all , s t, S(1)> H

0 if for some 1st, S(1)SH value: [2C] - [4C] {l]=l, cj>=l}

(10) up-and-out cash-or-nothing (S<H) pay-off: X (at expiry) if for all , s t, S(1)< H

0 if for some 1st, S(1)2 H value: [2C] - [4C] {l]= - 1, cj>=-1}

(11) down-and-out asset-or-nothing (S>H) pay-off: S(t) (at expiry) if for all 1st, S(1)>H

0 if for some 1s t, S(1)SH value: [2A] - [4A] {l]=l, cj>=l}

(12) up-and-out asset-or-nothing (S< H) pay-off: S(t) (at expiry) if for all 1s t, S(,)< H

0 if for some 1st, S(1)2H value: [2A] - [4A] {l]=-1, cj>=-1}

The pay -off of a down -a nd -o ut cash-ornothing option is equal to - X/H times the cash portion of th e p ay -off of a down and-ou t call with strike price H, and the pay-off of an up-and-out cash -o r-nothing is equal to X/ H times the cash portion of an up -and-out put with strike price H. Similarly, the pay -o ff from an "o ut " assetor -nothing is identi ca l to the pay -off from a down-and-out or up -and -out ca ll with both th e strike price a nd rebate equal to zero.

These results may be obtained from formulas 5-8 by noting that a portfolio consisting of an "out" option and its complementary " in" will always pay off at expiry, re gar dle ss of whether or not the barrier is crossed. Co n seq u e ntly, we ca n derive parity rela tion s eq u a tin g th e sum of the present values of th e two option s to the present valu e of deliv e ry at expiration of cash or the und e rlyin g asset. For example, th e value of a down -a nd -o ut cash -or-nothing (9) is merely th e differ e nce be tw ee n th e present va lu e of X deli vered un co ndition a lly a t exp iry (Xr- 1) and o ur re sult for op tion 5.

Options 13- 16 have positive pay -offs requiring not only that th e barrier (H) be breach ed, but also that the underlying asset finish above a g iven leve l (K).

RISK

(13) down-and-in cash-or-nothing call (S>H) pay-off: X (at expiry) if S(t)> K and for

some 1st, S(1)SH 0 if S(t)< K or for all 1st, S(1)>H

value (K> H): [3C] { 1'l = 1) value (K<H) [lC] - [2C] + (4C] {ri=l,

cj>=l}

(14) up-and-in cash-or-nothing call (S< H) pay-off: X (at expiry) if S(t)> K and for

some 1st, S(1)2H 0 if S(t)< K or for all 1st, S(1)< H

value (K> H): [lC] {cj>= l) value (K< H):[2C] - [3C] + [4C] {ri=- 1,

cj>= l}

Suppose X were equal to the strike pric e of a down-and-in or up-and in call. Then the strike price portion of the pay -o ff of th ese ca lls ha s the same value as an other wi se id entical "in" cash-or-nothing ca ll.

(15) down-and-in asset-or-nothing call (S> H) pay-off: S(t) (at expiry) if S(t)> K and for

some 1s t, S(1)SH 0 if S(t)<K or for all 1s t, S(i:)> H

value (K> H): [3A] {l]= 1} value (K< H): [lA] - [2A] -l- [4A] {ri= l ,

cj>= l)

(16) up-and-in asset-or-nothing call (S< H) pay-off: S(t) (at expiry) if S(t)> K and for

some 1s t, S(1)2 H 0 if S(t)< K or for all 1s t, S(1)< H

value (K> H): [lA] { cj>= 1) value (K< H): [2A] - [3A] + [4A] {l]=-1,

cj>= l}

An "in" asset-or-nothing call has th e same value as the asset portion of the pay -off of an otherwise id e nti ca l down -and -in or up -and -in ca ll .

Options 17- 20 h ave positive pay -offs requiring not only that the barrier (H) be breached but also that the und e rlying as se t finish below a given leve l (K).

(17) down-and-in cash-or-nothing put (S> H) pay-off: X (at expiry) if S(t)< K and for

some 1st, S(1)sH 0 if S(t)<K or for all 1st, S(1)>H

value (K> H)[2C] - [3C] + [4C] {l]=-1 , cj>=- 1)

value (K<H): [lC] { cj>= - 1)

(18) up-and-in cash-or-nothing put (S<H) pay-off: X (at expiry) if S(t)< K and for

some 1st, S(1)2 H 0 if S(t)<K or for all , s t, S(1)<H

value (K> H):[lC] - [2C] + [4C] {ri=- 1, cj>=- 1)

value (K< H):[3C] {l]=- 1}

Suppos e X were e qual to the strike pric e of a down-and-in or up-and-in put. Then the strike pric e portion of th e pay-off of thes e puts h as th e same value as an otherwis e identical "in" cas h-or-nothing put.

(19) down-and-in asset-or-nothing put (S> H) pay-off: S(t) (at expiry) if S(t)< K and for

some 1st, S(1)S H 0 if S(t)< K or for all 1s t, S(1)> H

value (K> H):[2A] - [3A] + (4A] [ri= l , cj>=- 1}

value (K< H): [lA] {cj>=- 1}

(20) up-and-in asset -or-nothing put (S< H) pay-off: S(t) (at expiry) if S(t)< K and for

some 1s t, S(1)2 H 0 if S(t)< K or for all 1s t, S(1)< H

value (K> H)[lA] - [2A] + [3A] (l]=- 1, cj>=-1}

value (K< H):[3A] {l]= - 1)

An " in " asset -or -nothin g put ha s th e sa m e value as th e asset portion of th e pay off of an otherwise ide nti ca l down -a nd in or u p -an d -in ca ll .

Options 17- 20 hav e positive p ay -off s requirin g not only that the barri er (H) be breach ed but also that the under lying asset fini sh below a given lev e l (K).

VOL 4/NO 9/ 0CTOBER 1991

81

OPTIONS

(21) down-and-out cash-or-nothing call (S> H) pay-off: X (at expiry) if S(t)> K and for

all r s t, S(i:)>H 0 if S(t)<K or for some ,::St, S(i:):SH

value (K> H):[lC] - [3C] {ri=l, cp=l} value (K< H) [2C] - [4C] {ri= l, cp=l}

(22) up-and-out cash-or-nothing call (S< H) pay-off: X (at expiry) if S(t)> K and for

all , :St, S(i:)<H 0 if S(t)<K or for some t:St, S(t)2:H

value (K> H): 0 value (K< H) [IC] - [2C] + [3C] - [4C]

{ri=- 1, cp= l}

Suppose X were equal to th e strike price of a down-and-out or up-and-out call. Then the strike price portion of th e payoff of th ese calls has the same value as an otherwise identical "out" cash-or-nothing call. It may seem surprising that an up a nd -out cas h-or-nothing call should be worth nothin g wh en th e st rik e price is g rea te r than th e barrier. But it is easy to see why . Since S< H< K, in order for the und erlyin g asset to end up above K, it must first breach the barri er H, but in this event , th e ca ll is exting ui shed .

(23) down-and-out asset-or-nothing call (S> H) pay-off: S(t) (at expiry) if S(t)> K and for

all t :St, S{t )> H 0 if S(t)< K or for some t :St, S{t):SH

value (K> H):[lA] - [3A] {ri=l, cj>= l} value (K< H):[2A]- [4A] {ri= I , cp= l}

(24) up-and-out asset-or-nothing call (S< H) pay-off: S(t) (at expiry) if S(t)> K and for

all 1:St, S(t)< H 0 if S(t)< K or for some t :St, S(1)2:H

value (K> H):0 value (K< H): [IA] - [2A] + [3A] - [4A]

{ri=- 1, cp= l}

An "ou t" asse t-or -nothin g call h as th e sa me valu e as th e asse t portion of th e pay off of an o th erwi se identical down -and out or up-and-out call.

Options 25--28 have positive p ay -offs requirin g not on ly th at th e barrier (H) 110/

RISK

be breached but also that th e underlying asset finish below a given lev el (K).

(25) down-and-out cash-or-nothing put (S>H) pay-off: X (at expiry) if S(t)<K and for all

t :St, S{t)> H 0 if S(t)< K or for some t :St, S(t):SH

value (K> H): [IC] - [2C] + [3C] - [4C] {ri= l, cp=- 1}

value (K< H): 0

(26) up-and-out cash-or-nothing put (S< H) pay-off: X (at expiry) if S(t)< K and for all

t :St, S(t)< H 0HSW < Korforwmei: :St, S(t)2:H

value (K> H):[2C] - [4C] {ri=- 1, cp=- 1} value (K< H):[lC] - [3C] {ri=-1 , cp=-1}

Suppose X were equal to th e strike price of a down-and-out or up-and- out put. Then the stri ke price portion of the pay off of thes e puts ha s th e same value as an oth erwise identica l "out " cas h -or nothin g put.

(27) down-and-out asset-or-nothing put (S> H) pay-off: S(t) (at expiry) if S(t)< K and for

all t :St, S(t)> H 0 if S(t)< K or for some t :St, S(i:):SH

value (K> H): [IA] - [2A] + [3A] - [4A] {ri= l, <1>=- l}

value (K< H): 0

(28) up-and-out asset -or-nothing put (S< H) pay-off: S(t) (at expiry) if S(t)< K and for

all t :St, S(t)< H 0 if S(t)< K or for some i::St, S(t)2:H

value (K> H):[2A] - [4A] {ri=- 1, cp=- 1} value (K< H):[lA] - [3A] {ri=- 1, cp=- 1)

An "out " asset-o r-nothin g put has th e same value as the asset portion of th e payoff of an othe rwi se identical down-andout or up -an d-out ca ll.

Ju st as th ere are "parity" relations betw ee n our res ult s 5--8 and 9- 12, so, too , can we find equ alities that link sum s of th e values of option s 12- 28 with th e values of less complex securities . For exa mple , a portfolio con sistin g of an "in " option from

the list 13-20 and its "out" complement from 21- 28 is equivalent to one of th e path-independent binaries we discussed earlier. Alternatively, an "in " call from 13-16 togeth er with the corresponding put from 17-20 comprise a position identical to one of the barri er-onl y " in" options from 5--8. Similar res ult s link position s constructed from the "o ut " calls and put s 21- 24 an d 25--28 with barrier-only "ou t" options from 9-12.

We ma y also combine options 13-28 in ways that yield more familiar securities . Each of the barrier options examined in our previou s article ma y be built from an asset-or-nothing option from this list and a corres pondin g cas h -or- nothin g with X se t equal to K. For exa mpl e, a do wn and-in call ma y be synthesised from a long asset-or-nothing down-and-in call and a short cash-or-nothing down-and in call with th e same strike price and with X=K.

Finall y , we can construct barri er de pendent and strike -dep end ent gap op tions and sup ers h ares ana logo us to th ose presented in the first part of this articl e for path-dependent conditions. Howeve r, perhaps .. -•

Mark Rubinstein is a professor of finance at the University of California, Berkeley, and he and Eric Reiner are, respectively, a principal and vice-president of Leland O'Brien Rubinstein Associates

VOL 4/ N0 9/ OCT0BER 1991

83

CORRECTION A production error led to the repetition of a paragraph in Mark Rubinstein and Eric Reiner's article Unscrambling the binary code in the October 1991 issue of RISK. The final paragraph of the third column of page 81 should read:

Options 21-24 have positive payoffs requiring not only that the barrier (H) not be breached but also that the underlying asset finish above a given level (K).

VOL 5/NO I/DECEMBER 1991-JANUARY 1992

Related Documents