United States, Brazil, China Variations in Purchasing Patterns

United States, Brazil, China Variations in Purchasing Patterns.

Dec 16, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

United States, Brazil, China

Variations in Purchasing Patterns

2

Copyright © 2012 The Nielsen Company. Confidential and proprietary.

Overview

• Trends in Consumer Choice Environment • Focus on United States : modern trade, largely stagnant• Focus on Brazil and China: modern and traditional growth• Advertising • Social media data• Bringing it all together: an example

2

3

Copyright © 2012 The Nielsen Company. Confidential and proprietary.

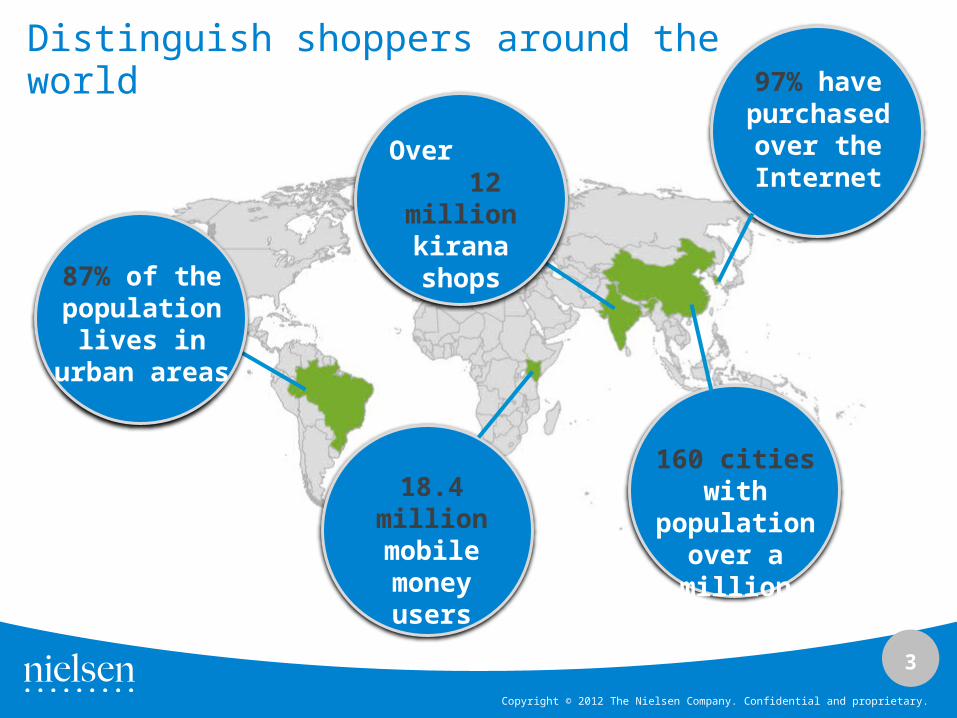

Distinguish shoppers around the world

87% of the population

lives in urban areas

Over 12 million

kirana shops

160 cities with population

over a million18.4 million

mobile money users

97% have purchased

over the Internet

4

Copyright © 2012 The Nielsen Company. Confidential and proprietary.

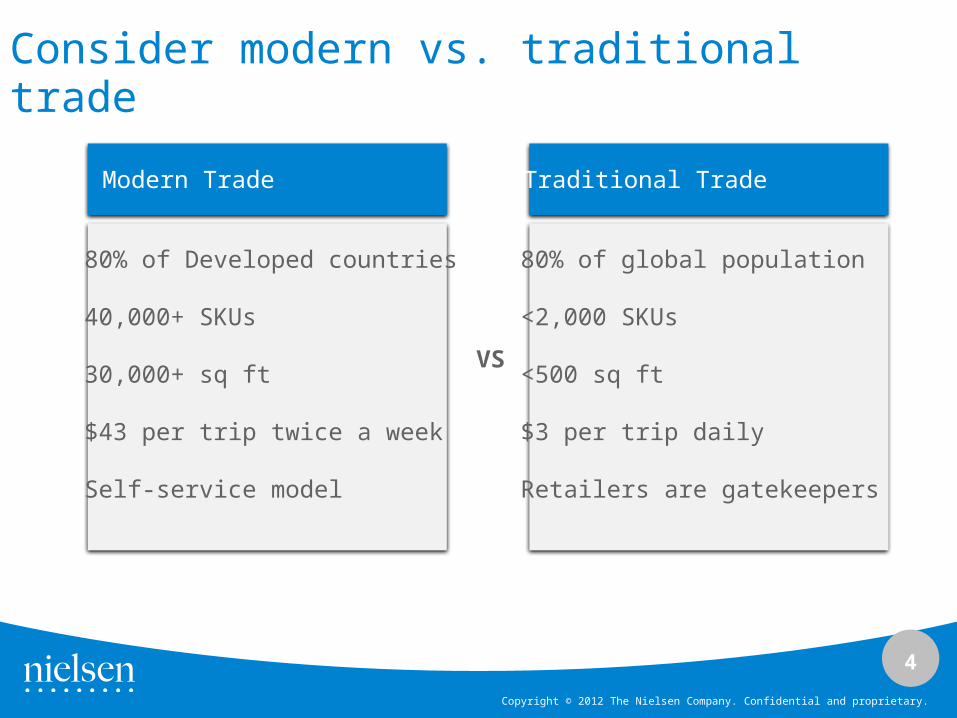

Consider modern vs. traditional trade

Modern Trade Traditional Trade

80% of Developed countries

40,000+ SKUs

30,000+ sq ft

$43 per trip twice a week

Self-service model

80% of global population

<2,000 SKUs

<500 sq ft

$3 per trip daily

Retailers are gatekeepers

VS

5

Copyright © 2012 The Nielsen Company. Confidential and proprietary.

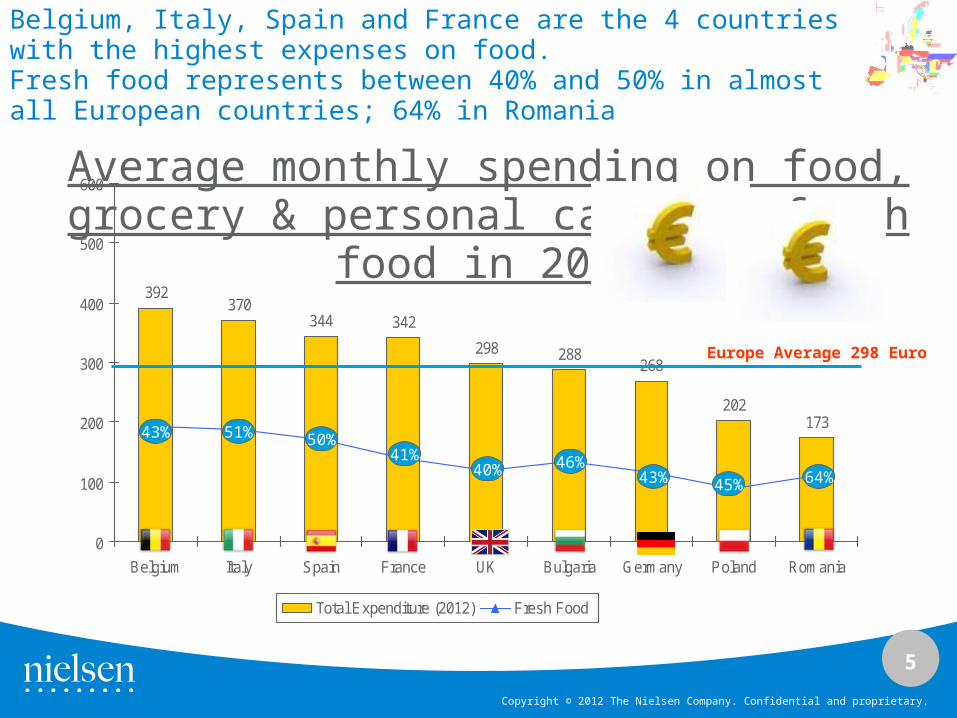

344 342

298 288268

202173

392370

0

100

200

300

400

500

600

Belgium Italy Spain France UK Bulgaria Germany Poland Romania

Total Expenditure (2012) Fresh Food

Average monthly spending on food, grocery & personal care vs. fresh food in 2012

Europe Average 298 Euro

51%

41%40% 46%

43%

45% 64%

50%

43%

Belgium, Italy, Spain and France are the 4 countries with the highest expenses on food.Fresh food represents between 40% and 50% in almost all European countries; 64% in Romania

6

Copyright © 2012 The Nielsen Company. Confidential and proprietary.

United States: Quantity Shift Analysis: Non-Alcoholic Beverages

2010 Growth

2011 Growth

Source: Nielsen ScanTrack; Note: 2009 refers to year ending May 2010, 2011 refers to year ending May 2012;

7

Copyright © 2012 The Nielsen Company. Confidential and proprietary.

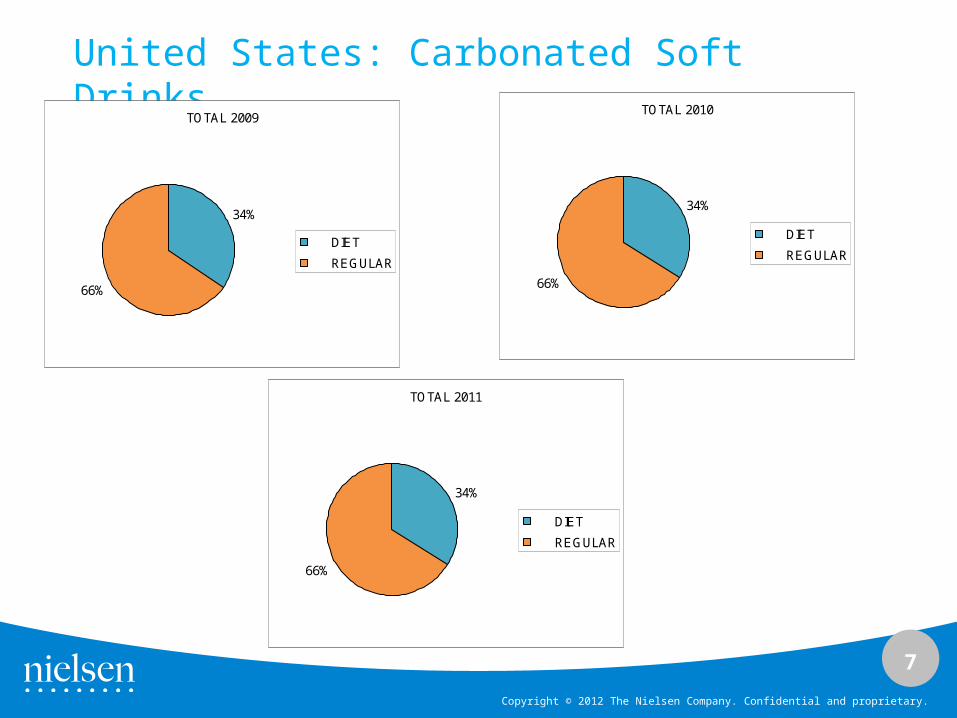

United States: Carbonated Soft Drinks

TOTAL 2009

34%

66%

DIET

REGULAR

TOTAL 2011

34%

66%

DIET

REGULAR

TOTAL 2010

34%

66%

DIET

REGULAR

8

Copyright © 2012 The Nielsen Company. Confidential and proprietary.

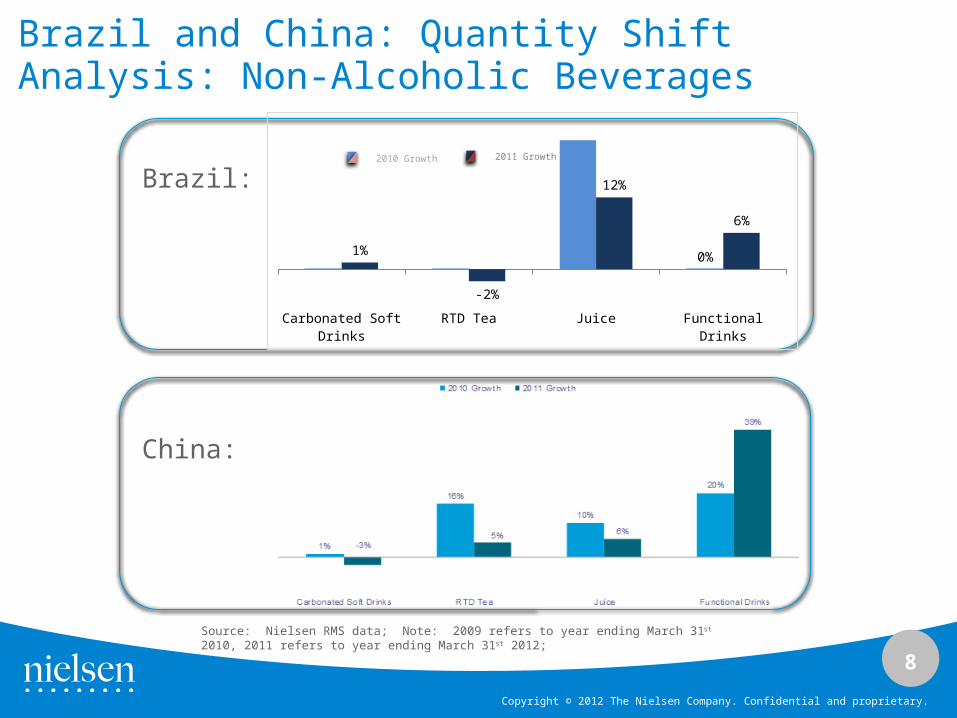

Brazil and China: Quantity Shift Analysis: Non-Alcoholic Beverages

2010 Growth 2011 Growth

Brazil:

China:

Source: Nielsen RMS data; Note: 2009 refers to year ending March 31st 2010, 2011 refers to year ending March 31st 2012;

Carbonated Soft Drinks

RTD Tea Juice Functional Drinks

1%

-2%

12%

6%

0%

9

Copyright © 2012 The Nielsen Company. Confidential and proprietary.

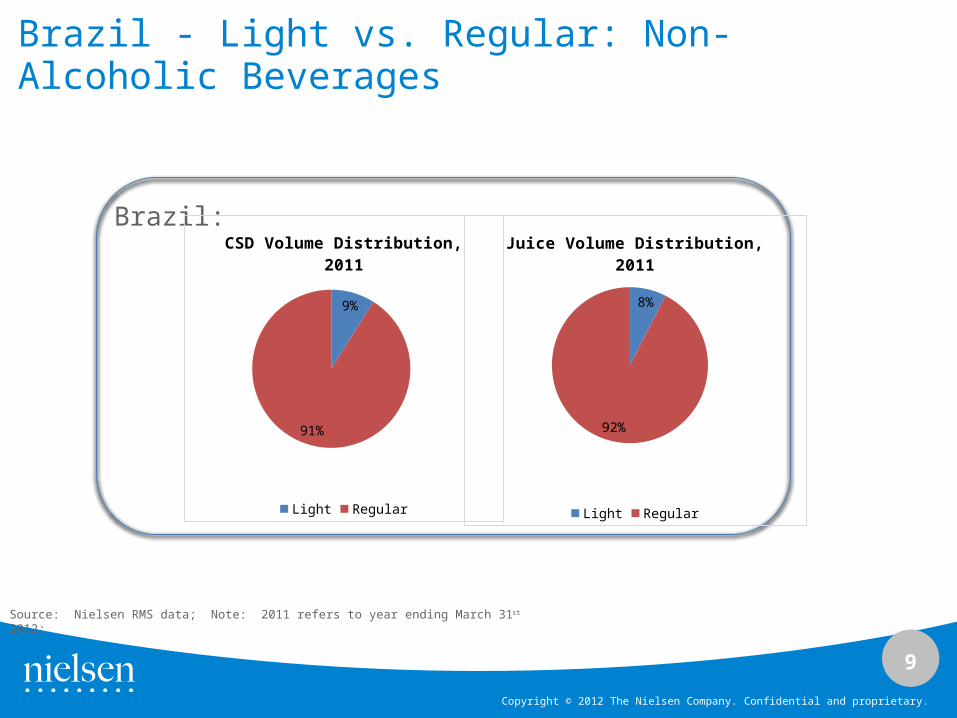

Brazil - Light vs. Regular: Non-Alcoholic Beverages

Brazil:

9%

91%

CSD Volume Distribution, 2011

Light Regular

8%

92%

Juice Volume Distribution, 2011

Light Regular

Source: Nielsen RMS data; Note: 2011 refers to year ending March 31st 2012;

10

Copyright © 2012 The Nielsen Company. Confidential and proprietary.

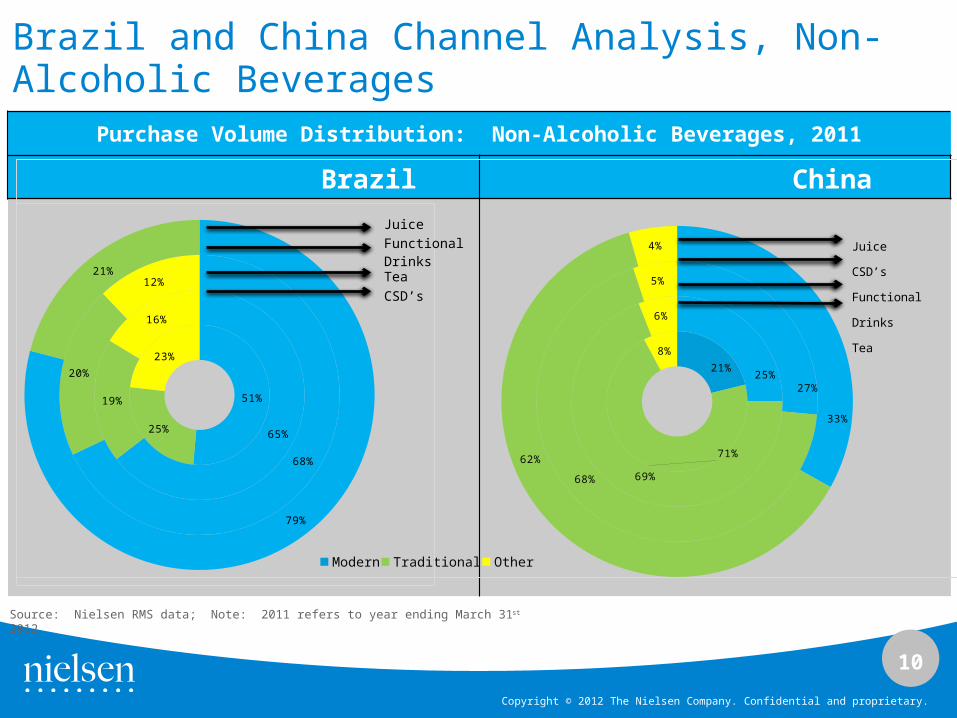

Purchase Volume Distribution: Non-Alcoholic Beverages, 2011

Brazil China

21%

71%

8%

25%

69%

6%

27%

68%

5%

33%

62%

4%

Modern Traditional Other

Juice

CSD’s

Functional Drinks

Tea

Brazil and China Channel Analysis, Non-Alcoholic Beverages

51%

25%

23%

65%

19%

16%

68%

20%

12%

79%

21%

JuiceFunctional DrinksTeaCSD’s

Source: Nielsen RMS data; Note: 2011 refers to year ending March 31st 2012

11

Copyright © 2012 The Nielsen Company. Confidential and proprietary.

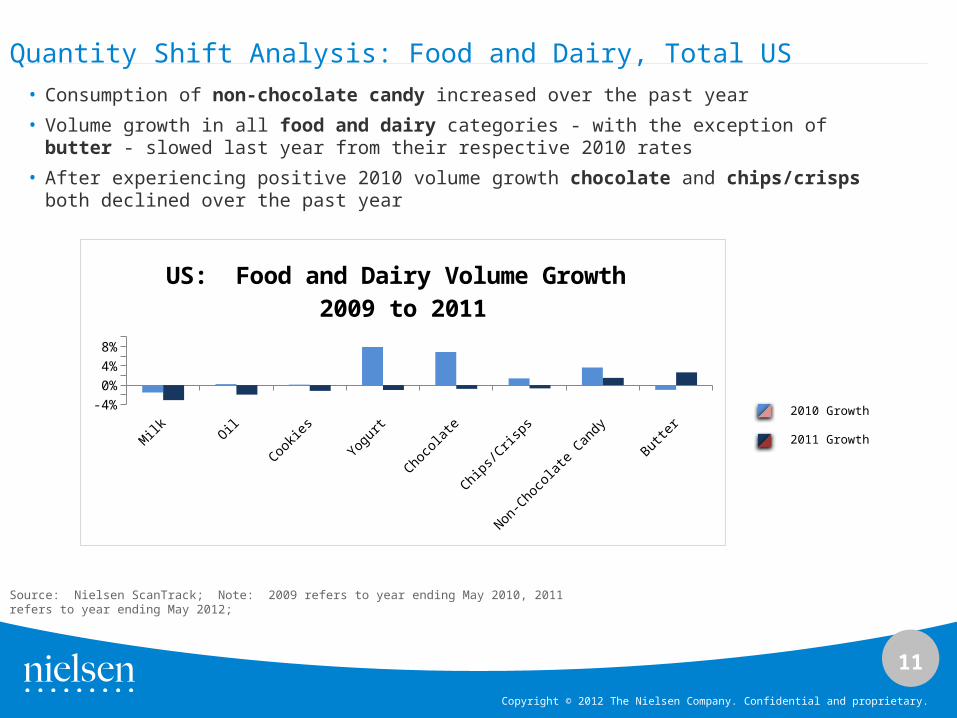

Quantity Shift Analysis: Food and Dairy, Total US

2010 Growth

2011 Growth

Milk Oil

Cookies

Yogu

rt

Chocolat

e

Chips/Cris

ps

Non-Chocolat

e Can

dyButter

-4%-2%0%2%4%6%8%

10%

US: Food and Dairy Volume Growth 2009 to 2011

• Consumption of non-chocolate candy increased over the past year

• Volume growth in all food and dairy categories - with the exception of butter - slowed last year from their respective 2010 rates

• After experiencing positive 2010 volume growth chocolate and chips/crisps both declined over the past year

Source: Nielsen ScanTrack; Note: 2009 refers to year ending May 2010, 2011 refers to year ending May 2012;

12

Copyright © 2012 The Nielsen Company. Confidential and proprietary.

Quantity Shift Analysis: Food and Dairy, Total Brazil and China

• Chocolate and chips/crisps experienced notable growth each of the past two years in both Brazil and China

• While sales of non-chocolate candy continued to grow last year in China, sales slowed in Brazil

Source: Nielsen RMS data; Note: 2009 refers to year ending March 31st 2010, 2011 refers to year ending March 31st 2012;

2010 Growth

2011 Growth

Milk Oil Cookies Yogurt Chocolate Chips/Crisps Non-chocolate candy

Margarine-8%-6%-4%-2%0%2%4%6%8%

10%12%

Brazil: Food and Dairy Volume Growth 2009 to 2011

Milk Oil Yoghurt Chocolate Chips/crisps Non-chocolate candy

0%

5%

10%

15%

20%

25%

30%China: Food and Dairy Volume Growth 2009 to 2011

13

Copyright © 2012 The Nielsen Company. Confidential and proprietary.

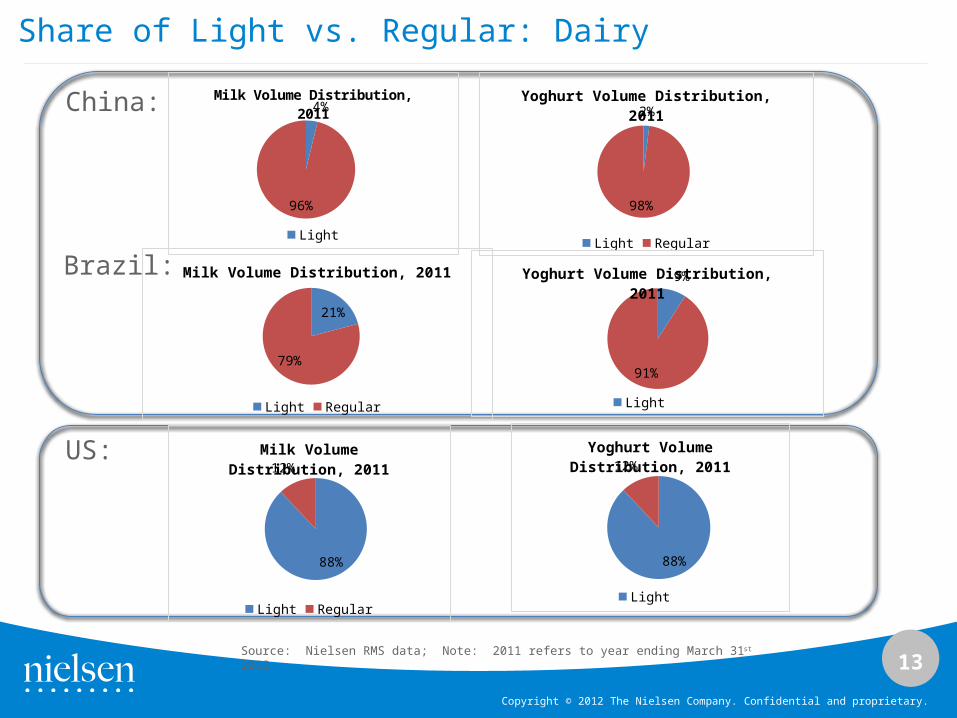

Share of Light vs. Regular: Dairy

China: 4%

96%

Milk Volume Distribution, 2011

Light Regular

2%

98%

Yoghurt Volume Distribution, 2011

Light Regular

Brazil:

21%

79%

Milk Volume Distribution, 2011

Light Regular

9%

91%

Yoghurt Volume Distribution, 2011

Light Regular

88%

12%

Yoghurt Volume Distribution, 2011

Light Regular

88%

12%

Milk Volume Distribution, 2011

Light Regular

US:

Source: Nielsen RMS data; Note: 2011 refers to year ending March 31st 2012

14

Copyright © 2012 The Nielsen Company. Confidential and proprietary.

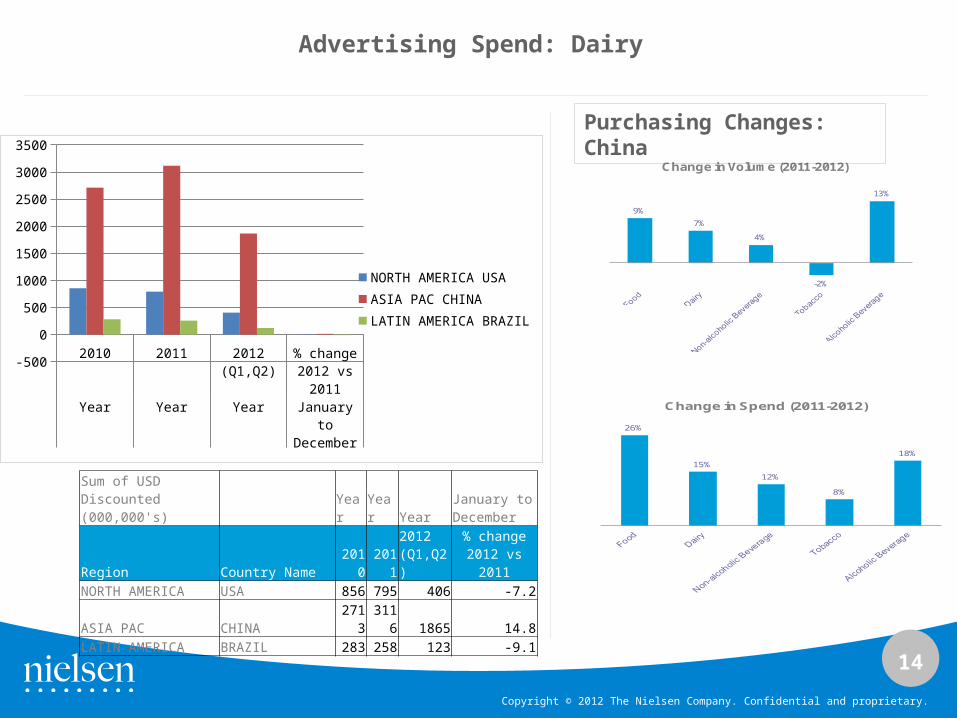

Sum of USD Discounted (000,000's) Year Year Year

January to December

Region Country Name 2010 20112012 (Q1,Q2)

% change 2012 vs 2011

NORTH AMERICA USA 856 795 406 -7.2ASIA PAC CHINA 2713 3116 1865 14.8LATIN AMERICA BRAZIL 283 258 123 -9.1

2010 2011 2012 (Q1,Q2)

% change 2012 vs

2011Year Year Year January to

December

-500

0

500

1000

1500

2000

2500

3000

3500

NORTH AMERICA USA

ASIA PAC CHINA

LATIN AMERICA BRAZIL

Advertising Spend: Dairy

9%

7%

4%

-2%

13%

Change in Volume (2011-2012)

Purchasing Changes: China

26%

15%

12%

8%

18%

Change in Spend (2011-2012)

15

Copyright © 2012 The Nielsen Company. Confidential and proprietary.

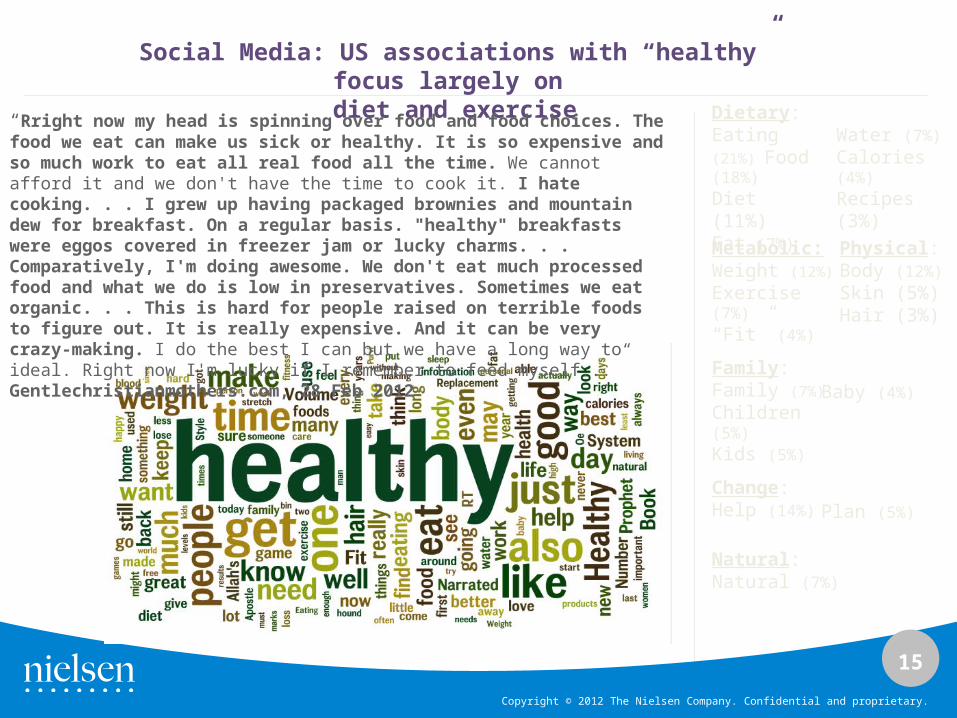

Dietary: Eating (21%)

Food (18%)

Diet (11%)Fat (7%)

Water (7%)

Calories (4%)

Recipes (3%)

Metabolic:Weight (12%)

Exercise (7%)

“Fit” (4%)

Physical: Body (12%)

Skin (5%)Hair (3%)

Family: Family (7%)

Children (5%)

Kids (5%)

Baby (4%)

Change: Help (14%) Plan (5%)

Natural: Natural (7%)

Social Media: US associations with “healthy” focus largely on diet and exercise

“Rright now my head is spinning over food and food choices. The food we eat can make us sick or healthy. It is so expensive and so much work to eat all real food all the time. We cannot afford it and we don't have the time to cook it. I hate cooking. . . I grew up having packaged brownies and mountain dew for breakfast. On a regular basis. "healthy" breakfasts were eggos covered in freezer jam or lucky charms. . . Comparatively, I'm doing awesome. We don't eat much processed food and what we do is low in preservatives. Sometimes we eat organic. . . This is hard for people raised on terrible foods to figure out. It is really expensive. And it can be very crazy-making. I do the best I can but we have a long way to ideal. Right now I'm lucky if I remember to feed myself...” Gentlechristianmothers.com, 28 Feb 2012

16

Copyright © 2012 The Nielsen Company. Confidential and proprietary.

Interaction Between Cigarette Sales and Advertising

Related Documents