DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT CONTAINS IMPORTANT DISCLOSURES, ANALYST CERTIFICATIONS, AND THE STATUS OF NON-US ANALYSTS. US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. CREDIT SUISSE SECURITIES RESEARCH & ANALYTICS BEYOND INFORMATION ® Client-Driven Solutions, Insights, and Access 08 September 2014 Americas/United States Equity Research Airlines United Continental Holdings, Inc. (UAL) INITIATION Top Pick - What's Right with United ■ Initiating Coverage of UAL with an Outperform Rating, $68 Target Price. ■ The Sector's Turnaround Story: While UAL shares still embed substantial execution risk, we see a string of catalysts and tailwinds in 2015 that should drive earnings & valuation upside. We believe 2015 earnings improvement is underappreciated for the following reasons: (1) maturing revenue initiatives should lead to 2015 PRASM outperformance by as much as 100 bps; (2) accelerating cost reductions and easing wage inflation will likely permit flat to down ex-fuel unit cost growth, despite only modest capacity additions; (3) we expect UAL to exceed buyback expectations. Our more optimistic assumptions yield a 2015 EBIT forecast 23% ahead of the consensus and 230 bps of margin improvement Y/Y. The earlier-than-expected buyback underpins management's confidence in the earnings trajectory, and we expect a strong Q3 will build on Q2's reassuring performance that United's extended period of postmerger underperformance is coming to a close. ■ Mind the Gap, We Think It's Closing: We look at UAL's margin progress in the four years following the merger versus Delta's and highlight that it isn’t all that different. The consensus has Delta's year-six postmerger EBIT margins +570 bps above year four, whereas the consensus only embeds 200 bps of improvement over the same period for United. We think that this is overly conservative and see no structural impediments to UAL achieving a low-double-digit EBIT margin by year six (2016 +500 bps versus 2014E). ■ Catalysts: (1) investor update 10/7, (2) Q3 2014 earnings 10/23, (3) fall conferences, (4) investor day in 2015 (tbd); (5) buyback pace, (6) the potential for a dividend or a margin target, (7) >10% ROIC target. ■ Valuation: We blend a 12.5x midcycle P/E multiple and a 6.5x EV/EBITDAR multiple on our 2015 (fully taxed) estimates to yield our $68 target price. Note, while 2015 is untaxed, we fully tax our 2016 earnings estimate. Share price performance 29 34 39 44 49 Sep-13 Dec-13 Mar-14 Jun-14 Daily Sep 09, 2013 - Sep 03, 2014, 9/09/13 = US$31.03 Price Indexed S&P 500 INDEX On 09/03/14 the S&P 500 INDEX closed at 2007.71 Quarterly EPS Q1 Q2 Q3 Q4 2013A -1.08 1.35 1.49 0.76 2014E -1.33 2.34 2.54 1.12 2015E -0.13 2.83 3.20 1.65 Financial and valuation metrics Year 12/13A 12/14E 12/15E 12/16E EPS (CS adj.) (US$) 3.01 4.68 7.55 7.45 Prev. EPS (US$) — — — — P/E (x) 16.8 10.9 6.7 6.8 P/E rel. (%) 94.0 65.7 45.4 51.2 Revenue (US$ m) 38,279.0 38,866.4 40,436.1 42,020.6 EBITDA (US$ m) 3,458.0 4,166.1 5,243.9 6,579.1 OCFPS (US$) 3.82 8.18 10.96 11.08 P/OCF (x) 9.9 6.2 4.6 4.6 EV/EBITDA (current) 8.1 6.7 5.3 4.2 Net debt (US$ m) 9,189 10,077 6,280 2,997 Number of shares (m) 373.57 IC (current, US$ m) 12,173.00 BV/share (Next Qtr., US$) 10.6 EV/IC (x) 2.2 Net debt (Next Qtr., US$ m) 8,091.5 Dividend (current, US$) — Net debt/tot eq (Next Qtr., %) 196.3 Dividend yield (%) — Source: Company data, Credit Suisse estimates. Rating OUTPERFORM* Price (05 Sep 14, US$) 50.73 Target price (US$) 68.00¹ 52-week price range 50.73 - 29.65 Market cap. (US$ m) 18,951.44 Enterprise value (US$ m) 29,027.95 *Stock ratings are relative to the coverage universe in each analyst's or each team's respective sector. ¹Target price is for 12 months. Research Analysts Julie Yates 212 325 3706 [email protected] Krishna Vege 212 325 6949 [email protected]

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT CONTAINS IMPORTANT DISCLOSURES, ANALYST CERTIFICATIONS, AND THE STATUS OF NON-US ANALYSTS. US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

CREDIT SUISSE SECURITIES RESEARCH & ANALYTICS BEYOND INFORMATION®

Client-Driven Solutions, Insights, and Access

08 September 2014

Americas/United States

Equity Research

Airlines

United Continental Holdings, Inc. (UAL)

INITIATION

Top Pick - What's Right with United

■ Initiating Coverage of UAL with an Outperform Rating, $68 Target Price.

■ The Sector's Turnaround Story: While UAL shares still embed substantial execution risk, we see a string of catalysts and tailwinds in 2015 that should drive earnings & valuation upside. We believe 2015 earnings improvement is underappreciated for the following reasons: (1) maturing revenue initiatives should lead to 2015 PRASM outperformance by as much as 100 bps; (2) accelerating cost reductions and easing wage inflation will likely permit flat to down ex-fuel unit cost growth, despite only modest capacity additions; (3) we expect UAL to exceed buyback expectations. Our more optimistic assumptions yield a 2015 EBIT forecast 23% ahead of the consensus and 230 bps of margin improvement Y/Y. The earlier-than-expected buyback underpins management's confidence in the earnings trajectory, and we expect a strong Q3 will build on Q2's reassuring performance that United's extended period of postmerger underperformance is coming to a close.

■ Mind the Gap, We Think It's Closing: We look at UAL's margin progress in the four years following the merger versus Delta's and highlight that it isn’t all that different. The consensus has Delta's year-six postmerger EBIT margins +570 bps above year four, whereas the consensus only embeds 200 bps of improvement over the same period for United. We think that this is overly conservative and see no structural impediments to UAL achieving a low-double-digit EBIT margin by year six (2016 +500 bps versus 2014E).

■ Catalysts: (1) investor update 10/7, (2) Q3 2014 earnings 10/23, (3) fall conferences, (4) investor day in 2015 (tbd); (5) buyback pace, (6) the potential for a dividend or a margin target, (7) >10% ROIC target.

■ Valuation: We blend a 12.5x midcycle P/E multiple and a 6.5x EV/EBITDAR

multiple on our 2015 (fully taxed) estimates to yield our $68 target price. Note, while 2015 is untaxed, we fully tax our 2016 earnings estimate.

Share price performance

29

34

39

44

49

Sep-13 Dec-13 Mar-14 Jun-14

Daily Sep 09, 2013 - Sep 03, 2014, 9/09/13 = US$31.03

Price Indexed S&P 500 INDEX

On 09/03/14 the S&P 500 INDEX closed at 2007.71

Quarterly EPS Q1 Q2 Q3 Q4 2013A -1.08 1.35 1.49 0.76 2014E -1.33 2.34 2.54 1.12 2015E -0.13 2.83 3.20 1.65

Financial and valuation metrics

Year 12/13A 12/14E 12/15E 12/16E EPS (CS adj.) (US$) 3.01 4.68 7.55 7.45 Prev. EPS (US$) — — — — P/E (x) 16.8 10.9 6.7 6.8 P/E rel. (%) 94.0 65.7 45.4 51.2 Revenue (US$ m) 38,279.0 38,866.4 40,436.1 42,020.6 EBITDA (US$ m) 3,458.0 4,166.1 5,243.9 6,579.1 OCFPS (US$) 3.82 8.18 10.96 11.08 P/OCF (x) 9.9 6.2 4.6 4.6 EV/EBITDA (current) 8.1 6.7 5.3 4.2 Net debt (US$ m) 9,189 10,077 6,280 2,997

Number of shares (m) 373.57 IC (current, US$ m) 12,173.00 BV/share (Next Qtr., US$) 10.6 EV/IC (x) 2.2 Net debt (Next Qtr., US$ m) 8,091.5 Dividend (current, US$) — Net debt/tot eq (Next Qtr., %) 196.3 Dividend yield (%) —

Source: Company data, Credit Suisse estimates.

Rating OUTPERFORM* Price (05 Sep 14, US$) 50.73 Target price (US$) 68.00¹ 52-week price range 50.73 - 29.65 Market cap. (US$ m) 18,951.44 Enterprise value (US$ m) 29,027.95

*Stock ratings are relative to the coverage universe in each

analyst's or each team's respective sector.

¹Target price is for 12 months.

Research Analysts

Julie Yates

212 325 3706

Krishna Vege

212 325 6949

08 September 2014

United Continental Holdings, Inc. (UAL) 2

Investment Overview We initiate coverage of United Continental Holdings (UAL) as our top pick with an

Outperform rating and a $68 target price. We launch coverage of the U.S. Airline sector at

Overweight, with a favorable bias to the network carriers structural industry changes, a

strong demand environment, and ongoing margin enhancing initiatives. See our

accompanying report, titled, "U.S. Airline Industry Coverage Initiation: Network

Carriers Flying on Course for Continued Outperformance" for our industry views.

What's Right with United? The question, "What's wrong with United?", has been a

dominant theme for airline investors over the last 12 months. We think that United's

operational and financial underperformance has come to a close as the carrier recalibrates

and optimizes its network and cost structure following an extended period of integration

challenges. Management's tone has improved over the last six months as it aggressively

implements cost and revenue initiatives. Confidence in improving earnings was supported

by the earlier-than-expected buyback announcement in July 2014, and we see a string of

catalysts and tailwinds in 2015 that should drive earnings and valuation upside. Our

estimates are ahead of the Street on a combination of higher unit revenues and lower unit

costs.

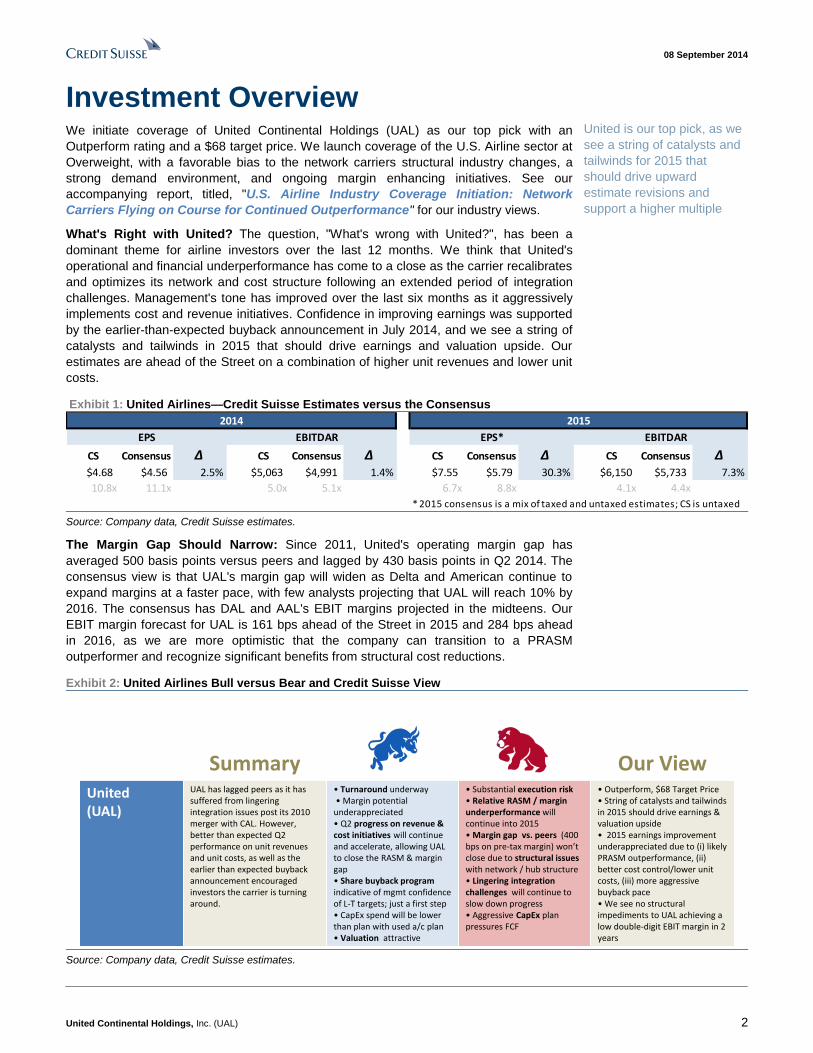

Exhibit 1: United Airlines—Credit Suisse Estimates versus the Consensus

2014 2015

EPS EBITDAR EPS* EBITDAR

CS Consensus ∆ CS Consensus ∆ CS Consensus ∆ CS Consensus ∆$4.68 $4.56 2.5% $5,063 $4,991 1.4% $7.55 $5.79 30.3% $6,150 $5,733 7.3%

10.8x 11.1x 5.0x 5.1x 6.7x 8.8x 4.1x 4.4x

* 2015 consensus is a mix of taxed and untaxed estimates; CS is untaxed Source: Company data, Credit Suisse estimates.

The Margin Gap Should Narrow: Since 2011, United's operating margin gap has

averaged 500 basis points versus peers and lagged by 430 basis points in Q2 2014. The

consensus view is that UAL's margin gap will widen as Delta and American continue to

expand margins at a faster pace, with few analysts projecting that UAL will reach 10% by

2016. The consensus has DAL and AAL's EBIT margins projected in the midteens. Our

EBIT margin forecast for UAL is 161 bps ahead of the Street in 2015 and 284 bps ahead

in 2016, as we are more optimistic that the company can transition to a PRASM

outperformer and recognize significant benefits from structural cost reductions.

Exhibit 2: United Airlines Bull versus Bear and Credit Suisse View

Summary Our ViewUnited(UAL)

UAL has lagged peers as it has suffered from lingering integration issues post its 2010 merger with CAL. However, better than expected Q2 performance on unit revenues and unit costs, as well as the earlier than expected buyback announcement encouraged investors the carrier is turning around.

• Turnaround underway• Margin potential

underappreciated• Q2 progress on revenue & cost initiatives will continue and accelerate, allowing UAL to close the RASM & margin gap• Share buyback program indicative of mgmt confidence of L-T targets; just a first step• CapEx spend will be lower than plan with used a/c plan• Valuation attractive

• Substantial execution risk• Relative RASM / marginunderperformance will continue into 2015 • Margin gap vs. peers (400 bps on pre-tax margin) won’t close due to structural issues with network / hub structure • Lingering integration challenges will continue to slow down progress• Aggressive CapEx plan pressures FCF

• Outperform, $68 Target Price• String of catalysts and tailwinds in 2015 should drive earnings & valuation upside• 2015 earnings improvement underappreciated due to (i) likely PRASM outperformance, (ii) better cost control/lower unit costs, (iii) more aggressive buyback pace• We see no structural impediments to UAL achieving a low double-digit EBIT margin in 2 years

Source: Company data, Credit Suisse estimates.

United is our top pick, as we

see a string of catalysts and

tailwinds for 2015 that

should drive upward

estimate revisions and

support a higher multiple

08 September 2014

United Continental Holdings, Inc. (UAL) 3

Key Investment Points ■ Performance Has Lagged Peers, and Investor Expectations Are Mixed: United

has lagged network peers in operational and financial performance as it has continued

to struggle with postmerger integration challenges and execution. However,

management has identified self-help opportunities to improve PRASM performance

and reduce its industry-high cost structure, which should drive margin expansion. (We

detail these initiatives in Exhibit 28 and Exhibit 35.) Expectations continued to

deteriorate up until Q2 2014 as investors have become accustomed to United's

relative underperformance and a 400-500 basis point margin gap. Q2 drove renewed

optimism, as PRASM (3.7% versus 1.0-3.0% guidance) and CASM (-0.2% versus

+1.25-2.25% guidance) displayed surprising strength, and the Q3 PRASM guidance of

2-4% improvement Y/Y was in-line with peers.

■ Q2 Performance Is Starting to Restore Confidence; Strong Q3 Performance Is

Crucial to the Bull Case: Management's tone improved markedly with the Q2

earnings report versus Q1, and the $1B buyback announcement came earlier than

expected, underpinning management's confidence in ongoing earnings improvement.

In our view, if Q3 continues to show progress on cost control and if PRASM comes in

at midend to high end or ahead of the 2-4% guidance, confidence should continue to

rebuild. We see a string of catalysts and tailwinds in 2015 that should drive earnings

and valuation upside in 2015, and we believe that 2015 earnings improvement is

underappreciated for the following reasons:

o Maturing Revenue Initiatives Should Drive as Much as 100 Bps of

PRASM Outperformance in 2015: After Q3 2013 unit revenue growth

came in lower than management's expectations and those of peers

(2.7% versus guidance for 3-5% Y/Y versus the network peer average of

4.2%), management has taken action to drive better revenue growth.

Since Q3's disappointment, every quarter since then management has

outlined new initiatives to improve revenue performance. These initiatives

are ramping and should reach a full run rate in 2015 to drive what we

think will be peer-leading PRASM performance as UAL receives assists

from initiatives and easier comps in H2 2014 and 2015 relative to DAL

and AAL. In addition, ancillary initiatives are continuing to drive high-

margin revenue, and high-yielding corporate revenue is growing.

Exhibit 3: These Should Help PRASM in H2 2014 & 2015 Exhibit 4: 2015 Comps Are Easier for United Too

Maturing revenue initiatives

Could drive +100 bps

PRASM outperformance

relative to peers, and 2x

2014's growth

• Q3'14 - shifting booking curve for close-in

bookings (1 pt of PRASM in Q3, shld help Q4 and

Q1 Y/Y too)

• Q1'14 - De-hubbing CLE, rebanking at DEN,

IAH, and ORD (start in Q4'14)

• Q2'14 - more seasonal shaping, optimization

of RJ operations, scaling down operators (start in

H2'14)

3.6%

2.1%

3.3%

2.8%

1.6%

3.4%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

2014E 2015E

PR

ASM

Y/Y

Gro

wth

DAL AAL UAL

Source: Company data, Credit Suisse estimates. Source: Company data, Credit Suisse estimates.

o Ex-Fuel Unit Cost Growth in 2015 Should Be Flat to Down on

Accelerating Cost Reductions and Easing Wage Inflation Despite

Only Modest Capacity Additions: United will give guidance for 2015

non-fuel unit cost growth in January 2015, and we expect it to be below

08 September 2014

United Continental Holdings, Inc. (UAL) 4

inflation, in-line with United's longer-term goals with Project Quality.

While United has relatively easy unit cost comps in 2014, given the poor

2013 performance, it faced a significant headwind from the pilot increase

(8.5%) and airport employee increase (5-10%) from the new agreements

signed in 2012. In 2015, the normalizing wage increases, benefits from

dehubbing CLE, regional flying optimization, and 50-seater replacement

should all provide a tailwind on top of the stated Project Quality targets.

We see greater potential for cost reductions beyond what management

outlined in Project Quality in maintenance, productivity, and sourcing.

Exhibit 5: Subinflation Unit Cost Growth Exhibit 6: 2013 Was High-Water Mark for UAL Cost

Growth – Expecting Flatting Unit Costs in 2015

Cost reductions

Unit cost (ex-fuel)

growth flat to slightly

down Y/Y in 2015

• Project Quality rolled out Nov'13; progress

made in Q2'14 should accelerate

• Potential PQ upside in productivity, sourcing

and maintenance

• Wage increases normalize in 2015 Y/Y

• CLE de-hubbing benefits H1

• Reducing regional flying and replacing 130 50-

seaters

3.1%

6.2%

2.0%

-0.2%

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

2012 2013 2014E 2015E

no

n-f

ue

l u

nit c

ost

gro

wth

Y/Y

UAL DAL AAL

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

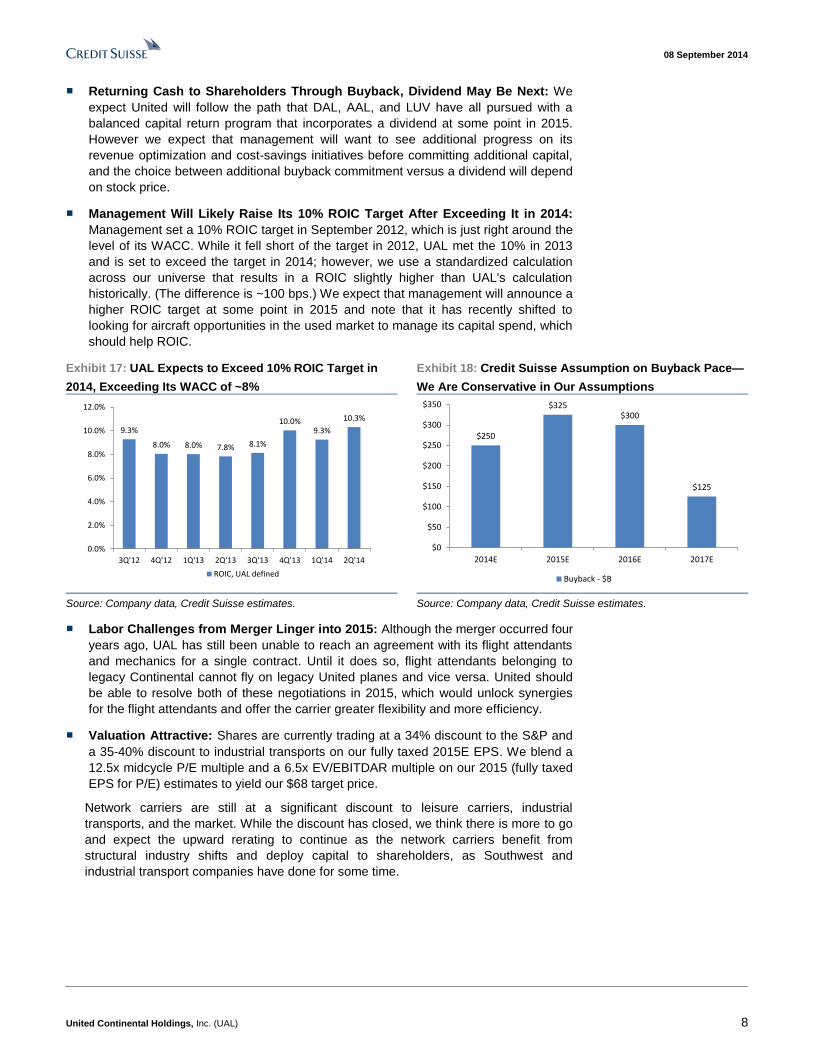

o We Expect UAL to Exceed Buyback Expectations: Management

announced a $1B buyback with Q2 results in July 2014, six months

earlier than investor expectations. United approved a $200M ASR for Q3

as well, and we wouldn’t be surprised if management continues to

aggressively buyback shares in H2 2014 and early 2015. While UAL set

a three-year time horizon, we think this was conservative and model

completion by year end 2016.

■ Are There Structural Issues Impeding Earnings? We Don't Believe There Are…

Industry observers and investors have speculated that structural issues with United's

network and endemic cultural issues following the merger are insurmountable. We

think that this concern has been overstated and that United's inability to reap greater

benefits from its now four-year-old CAL acquisition have been magnified by

American's quick resurgence and impressive performance out of the gate following the

December merger with US Airways. United does face unique challenges such as

outsized Asia exposure (where competitive capacity is pressuring yields) and hubs

geography (more expensive enplanement fees and winter weather prone in Northeast

(EWR) and Midwest (ORD) United States. That said, United and Star alliance have the

best, most comprehensive, business-centric network globally and management is

executing on a $2B structural cost reduction program announced in November 2013.

We expect that, as United is now past most of its painful merger woes, it can begin to

implement many of the revenue and cost initiatives that Delta already has, as well as

rebuild corporate customer confidence in operations.

■ UAL's Merger Was More Challenging, and It Is Still Two Years Behind Delta in

Integration; on a Timeline, the Trajectories Aren't that Different: We think it is

important to point out that United is a full two years behind Delta in its merger, and

negotiations weren’t as amicable as those of DAL-NWA. That said, when we look at

where United is four years after its merger and where Delta was in 2012 four years

after its merger, the numbers aren't all that different. Granted, United has a better

08 September 2014

United Continental Holdings, Inc. (UAL) 5

macro environment and should be earning more in today's demand/pricing picture

than DAL was able to in 2012, we think that UAL can narrow the gap to Delta over the

next two to three years.

United did announce its share repurchase program one year earlier than Delta did (in

year four, versus Delta in year five), and United's was 6% of market cap, whereas

Delta's was 3%, although complemented by a dividend (1% yield at the time). Delta

subsequently completed its buyback two years early and announced a $2B

authorization in year six (May 2014) and a 50% increase to its dividend just one year

after the initial program.

Exhibit 7: Delta Wasn’t that Far Ahead of Where United Is

in 2014 During Its Fourth Year Following the Merger

Exhibit 8: Consensus Is Forecasting United's Margin

Improvement from Year Four to Six Will Be Less than

One-Half of Delta's

7.1%

4.2%

11.5%

6.4%

4.7%

11.0%

Op Margin Pre-tax margin ROIC

Year 4 after merger close

Delta - 2012 United - 2014E CS est

12.5%

10.9%11.4%

9.7%

8.6%8.1%

Op Margin Pre-tax margin

Year 6 after merger close

Delta - 2014 consensus United - 2016 CS est United - 2016 consensus

Source: Company data, Credit Suisse estimates. Source: Company data, Credit Suisse estimates.

Costs Highest Among Peers, but There Is a Plan in Place, and Q2 Showed

Progress: In Exhibit 9 and Exhibit 10, we highlight the relative operating margin gap

for United versus the peer average (including pro forma American-US Airways for

2013) and the stage-length-adjusted unit costs excluding fuel for the trailing 12 months

as of Q1 2014, demonstrating United's unit costs are 22% higher than the average of

DAL and AAL. Since 2011, United's operating margin gap has averaged 500 basis

points versus peers and was still 430 basis points in Q2; the consensus forecasts the

gap actually widens in 2015. We think this is overly bearish, and believe that 2014 is

the most exaggerated the margin differential will be. United is improving, but Delta and

American should maintain their cost structures, which is why we still anticipate UAL will

be at a gap in 2016.

Primary contributors to United's margin gap include: higher labor costs, less domestic

exposure and a greater reliance on Asia (where competitive pressures are high),

higher cost geography hubs that are less efficient and prone to winter weather,

lingering integration issues (including revenue management challenges, cultural

divides that have contributed to poor customer service), and lower fleet efficiency due

to a higher proportion of capacity from 50-seat jets (United has more than double the

number of 50-seat jets as Delta today). Management is addressing these challenges

by optimizing its domestic network (de-hubbing CLE, rebanking, seasonal shaping,

reducing regional flying), restructuring its Pacific network (transitioning more flights to

codeshare partner, ANA and rightsizing aircraft), accelerated replacement of 50-seat

aircraft and 20-year old 757s.

08 September 2014

United Continental Holdings, Inc. (UAL) 6

Exhibit 9: UAL Margin Gap to Network Carrier Avg

**Uses CS estimates for unreported periods

Exhibit 10: TTM LTM CASM ex-Fuel as of Q1 2014

Stage-length adjusted *Virgin America as of TTM 12/2013

-305bp

-410bp

-544bp-513bp

-321bp

-560bp-600bp

-530bp

-700bp

-600bp

-500bp

-400bp

-300bp

-200bp

-100bp

0bp

2012 2013 2014E 2015E 2016E

Credit Suisse Est. Consensus

5.32¢ 5.57¢

6.81¢7.19¢ 7.23¢ 7.30¢ 7.56¢

8.57¢9.10¢

10.76¢

0.00¢

2.00¢

4.00¢

6.00¢

8.00¢

10.00¢

12.00¢

Source: Company data, Credit Suisse estimates, Bloomberg. Source: Company Reports, Alaska Air.

■ Lower Hub Market Share Might Be an Issue, but There Should Be Revenue

Offsets from O&D Traffic and Corporate Relevance: While United has an excellent

network with hubs in major business centers, its hub profitability lags peers. United

lacks dominant market share at major hubs, unlike Delta in Atlanta (70%+ share) and

America in Dallas/Ft. Worth (70% share). United averages 35% market share in its top

five markets, while Delta and American average closer to 50%.

Exhibit 11: Carrier Market Share in Major Hubs

Delta Mkt Share United Mkt Share American Mkt Share

Atlanta (ATL) 69% Houston 41% Dal las/Ft Worth (DFW) 70%

Minneapol is (MSP) 49% Chicago (ORD) 20% Charlotte 59%

Detroit (DTW) 46% San Francisco (SFO) 39% Phoenix 38%

New York (LGA & JFK) 22% Denver 24% Miami 71%

Salt Lake City (SLC) 46% Newark 49% Chicago 17%

Average 46% Average 34% Average 51% Source: BTS Web site, Credit Suisse estimates.

As previously mentioned, United and Star Alliance have the best positioning in top

domestic and international markets for corporate travel, which should provide

somewhat of an offset and a naturally higher percentage of high-yielding traffic.

Exhibit 12: Top Domestic Markets for Corporate Travel

with Passenger Share by Network Carrier

Exhibit 13: Top International Markets for Corporate Travel

with ASM Share to Destination by Alliance

RankMarket

(incl secondary airports)American United Delta

1) New York 22% 24% 26%

2) Las Vegas 12% 10% 12%

3) Chicago 29% 27% 8%

4) San Francisco 12% 28% 10%

5) Houston 11% 43% 7%

6) Orlando 15% 10% 17%

7) Atlanta 9% 3% 63%

8) San Diego 15% 13% 12%

9) Charlotte 67% 9% 18%

10) Dal las 55% 5% 8%

**Share calculated from % of passengers from O&D reports for YE 2013

Top Domestic Corporate Travel Markets

Rank Market oneworld Star Alliance Sky Team

1) London 53% 20% 6%

2) Shanghai , China 10% 27% 40%

3) Singapore 11% 53% 7%

4) Bei jing, China 5% 52% 24%

5) Tokyo, Japan 29% 43% 16%

6) Toronto, Canada 7% 58% 6%

7) Hong Kong 59% 18% 7%

8) Paris , France 10% 12% 63%

9) Mexico City, Mexico 14% 14% 46%

10) Montreal , Canada 9% 48% 13%

**Share calculated from schedule data for TTM July 2014, ASMs into market

Top International Corporate Travel Markets

Source: Concur, Diio Mi, CS research and estimates. Source: Concur, Diio Mi, CS research and estimates.

We also note United has dominant share on half of the Top 25 U.S. city pairs, and that

three or fewer airlines control 60% of these routes.

08 September 2014

United Continental Holdings, Inc. (UAL) 7

Exhibit 14: Percentage of Top 25 U.S. Routes where

Carrier is Dominant (>45% market share)

Exhibit 15: Number of Competitors on Top 25 Domestic

Routes Shows Oligopolistic Market Structure

United53%

American35%

Delta12%

Duopoly

24%

3

competitors

36%

4

competitors

24%

5

competitors

16%

Source: Diio Mi. Source: Diio Mi.

■ Consistent Capacity Discipline Central to Strategy: United has demonstrated that

capacity discipline is central to its strategy by keeping capacity growth below GDP

since 2008. Since 2008, United's system-wide capacity has fallen ~2% annually, more

than double the industry average. For 2014, United expects to keep system-wide

capacity growth to 0-1% Y/Y (a full point below initial plans), and over the next three

years it is targeting annual capacity growth below GDP, or 1-2%. United expects the

consolidated fleet count to remain flat, between 1,250 and 1,300 aircraft and has

recently announced that it will pursue opportunities in the used aircraft market, making

more return-driven decisions that would result in capital expenditures below its

previous plan of $2.8-3.0B from 2014 to 2017, 65% of which is for aircraft

replacement.

Exhibit 16: UAL Consolidated Capacity versus GDP

-2.3%

-6.4%

1.1%

-0.2%

-1.5% -1.4%

0.5%

1.8%

-0.3%

-2.8%

2.5%1.8%

2.8%1.9%

1.5%

3%

-8.0%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

2008 2009 2010 2011 2012 2013 2014E 2015E

United consolidated capacity GDP

Source: Company data, Credit Suisse estimates.

Capacity additions from UAL are efficient, mostly consisting of upgauging and

installation of slimline seats. The carrier is installing slimline seats that are 10-15%

lighter and provide one to two more rows of seats per plane on the regional (CRJ 700)

and mainline fleets (A320 and 737s). New routes in the Pacific and upgauging the

regional fleet are the other capacity contributors this year. United began reducing

flying from its Cleveland hub in April 2014, targeting a 60% reduction in average daily

departures, primarily through regional departures. Reductions were fully implemented

in June 2014.

United has that

demonstrated capacity

discipline is central to its

strategy by keeping capacity

growth below GDP since

2008

08 September 2014

United Continental Holdings, Inc. (UAL) 8

■ Returning Cash to Shareholders Through Buyback, Dividend May Be Next: We

expect United will follow the path that DAL, AAL, and LUV have all pursued with a

balanced capital return program that incorporates a dividend at some point in 2015.

However we expect that management will want to see additional progress on its

revenue optimization and cost-savings initiatives before committing additional capital,

and the choice between additional buyback commitment versus a dividend will depend

on stock price.

■ Management Will Likely Raise Its 10% ROIC Target After Exceeding It in 2014:

Management set a 10% ROIC target in September 2012, which is just right around the

level of its WACC. While it fell short of the target in 2012, UAL met the 10% in 2013

and is set to exceed the target in 2014; however, we use a standardized calculation

across our universe that results in a ROIC slightly higher than UAL's calculation

historically. (The difference is ~100 bps.) We expect that management will announce a

higher ROIC target at some point in 2015 and note that it has recently shifted to

looking for aircraft opportunities in the used market to manage its capital spend, which

should help ROIC.

Exhibit 17: UAL Expects to Exceed 10% ROIC Target in

2014, Exceeding Its WACC of ~8%

Exhibit 18: Credit Suisse Assumption on Buyback Pace—

We Are Conservative in Our Assumptions

9.3%

8.0% 8.0% 7.8% 8.1%

10.0%9.3%

10.3%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

3Q'12 4Q'12 1Q'13 2Q'13 3Q'13 4Q'13 1Q'14 2Q'14

ROIC, UAL defined

$250

$325$300

$125

$0

$50

$100

$150

$200

$250

$300

$350

2014E 2015E 2016E 2017E

Buyback - $B

Source: Company data, Credit Suisse estimates. Source: Company data, Credit Suisse estimates.

■ Labor Challenges from Merger Linger into 2015: Although the merger occurred four

years ago, UAL has still been unable to reach an agreement with its flight attendants

and mechanics for a single contract. Until it does so, flight attendants belonging to

legacy Continental cannot fly on legacy United planes and vice versa. United should

be able to resolve both of these negotiations in 2015, which would unlock synergies

for the flight attendants and offer the carrier greater flexibility and more efficiency.

■ Valuation Attractive: Shares are currently trading at a 34% discount to the S&P and

a 35-40% discount to industrial transports on our fully taxed 2015E EPS. We blend a

12.5x midcycle P/E multiple and a 6.5x EV/EBITDAR multiple on our 2015 (fully taxed

EPS for P/E) estimates to yield our $68 target price.

Network carriers are still at a significant discount to leisure carriers, industrial

transports, and the market. While the discount has closed, we think there is more to go

and expect the upward rerating to continue as the network carriers benefit from

structural industry shifts and deploy capital to shareholders, as Southwest and

industrial transport companies have done for some time.

08 September 2014

United Continental Holdings, Inc. (UAL) 9

Exhibit 19: U.S. Airlines 2015 Price-to-Earnings—UAL Still

Trades at a Significant Discount to Leisure Carriers &

S&P

Exhibit 20: UAL's Valuation Gap to the S&P Has Started to

Close in 2013, but Is Still ~34% on Fully Taxed EPS

(8/25/2011 – 8/25/2015 –FY2 Bloomberg Estimates)

10.1x

7.9x

10.4x

15.8x

13.6x

15.7x

DAL AAL UAL LUV JBLU S&P 500

-80%

-70%

-60%

-50%

-40%

-30%

-20%

-10%

0%

0.0x

2.0x

4.0x

6.0x

8.0x

10.0x

12.0x

(Dis

cou

nt)

/ P

rem

ium

to

S&

P 5

00

FY2

P/E

UAL FY2 P/E (discount) to S&P 500 UAL FY2 P/E

Source: Bloomberg. Source: Bloomberg.

On EV/EBITDAR, UAL currently trades at a 12% discount to DAL, given its execution

issues, less consistent results, and higher leverage. That said, we think the group

should be trading closer to 6-7x EV/EBITDAR, reflecting the strong midcycle demand

fundamentals. On EV/IC, United trades at a ratio of 1.8x, reflecting a lower ROIC

versus DAL.

Exhibit 21: U.S. Airlines 2015 EV/EBITDAR Exhibit 22: U.S. Airlines Enterprise Value/Invested Capital

5.0x

4.1x4.4x

5.6x

4.6x

DAL AAL UAL LUV JBLU

2.1x

1.7x1.8x 1.8x

1.0x

DAL AAL UAL LUV JBLU

Source: Bloomberg, Credit Suisse estimates. Source: Bloomberg, Credit Suisse estimates.

■ Risks: Primary risks for investing in the airline sector include: it is a highly cyclical

industry sensitive to fuel prices and the health of the economy; any terrorist attack or

threat, epidemic, or natural disaster (real or perceived) would significantly reduce

demand for air travel; airlines are capital-intensive, high-fixed-cost businesses, with

fuel and labor constituting 60% of operating expenses; and airlines are highly

competitive, and if other major carriers lose capacity discipline, yields may come under

pressure. For our full risks section, see pages 29-30.

08 September 2014

United Continental Holdings, Inc. (UAL) 10

Postmerger Margin Progress Analysis In Exhibit 20, we put all three mega mergers among network carriers on a similar timeline

to analyze progress following the merger close date. The macro environment varies to

some extent, but we found it useful to look at where UAL is today in year four following the

merger versus where Delta was in year four (2012).

We think the consensus for 8.6% operating margin in 2016 is conservative and expect

UAL's margin expansion will accelerate in 2015 and 2016 with margins in our model

reaching 11.4% in 2016 (500 bps of expansion 2014 – 2016, versus consensus of 240

bps). While 11.4% is still 120 bps below Delta's projected EBIT in 2014, we attribute the

difference to UAL's higher cost hub structure. A significant driver behind United's

improvement is cost control where the company is targeting subinflation non-fuel unit cost

growth.

Exhibit 23: Financial Progress Timeline Following the Merger

# Years Since Close 1 2 3 4 5 6

# Months Since Close 12 mths 18 mths 24 mths 36 mths 48 mths 60 mths 72 mths

Calendar Close: Oct-2008 2011 2012 2013 2014E

Delta –

Northwest

SOC received Dec-2009IT Integrated Feb-2010

Non fuel unit costs grew

3% YY

High water mark for non-fuel unit costs

grew 4.5% YY

$500M buyback

(3% mkt cap)

Dividend

$2B buyback

(6% mkt cap)

Dividend +50%

Op margin: 6.4% 7.1% Op margin 9.3% 12.6%

PT margin: 3.4% 4.2% PT margin 7.1% 10.3%

Net income: $770M $1B $2.5B $4.2B

ROIC: 10.7% 11.5% 11.9% 18%

# Months Since Close 12 mths 18 mths 24 mths 36 mths 48 mths 60 mths 72 mths

Calendar Close: Oct-2010 2013 2014E 2015E 2016E

United-

Continental

SOC received Nov-2011

IT integratedMar-2012

High water mark for non-fuel unit

cost growth +6.2% YY

Non-fuel unit costs growth of 1-2% Y/Y

Sub inflation non-fuel unit cost growth

$1B buyback

(6% mkt cap)

Op margin: 4.6% 6.1% Op margin 7.1% 8.6%

PT margin: 2.8% 4.5% PT margin 6.0% 8.1%

Net income: $1.1B $1.6B $2.2B $3.0B

ROIC: 8% 10% 11-12%

# Months Since Close 12 mths 18 mths 24 mths 36 mths 48 mths 60 mths 72 mths

Calendar Close: Dec-2013 2014 2015E 2016E

American-

US Airways

$1B buyback

(3% mkt cap)

Dividend

Op margin: 11.3% SOC targeted mid'15 12.0% 14.3%

PT margin: 9.3% IT integration Q3'15 11.1% 12.5%

The UAL-DAL pretax profit margin gap is only 30 bps four years from merger close

Looking at United’s Margin Progress Post-Merger versus Delta’s…

Consensus onlyforecasting 240 bpsof margin expansion, we forecast 500 bps

Note: Unreported years are Bloomberg consensus

Four years after merger close,Delta’s PTP margin and ROIC

were not that much higher than United’s in 2014

Source: Company data, Credit Suisse estimates, Bloomberg.

08 September 2014

United Continental Holdings, Inc. (UAL) 11

Targeting Structural Cost Reductions to Improve Margins United appears to have a structural cost disadvantage relative to peers, given its cost

structure (inclusive or exclusive of fuel) is ~22-24% higher than network peers. As

previously mentioned, we think this is due to a number of issues, including a larger

proportion of 50-seaters, higher labor costs, lingering integration issues, and network

challenges (high-cost geography hubs, lower hub market share, outsized Asian exposure).

Since 2011, United's operating margin gap has averaged 500 basis points versus peers

and was still 430 basis points in Q2; the consensus currently forecasts the margin gap will

widen as Delta and American continue to expand margins at a faster pace.

Management is taking corrective action by restructuring parts of its network, revamping its

fleet structure, and instituting a major cost-savings program.

Exhibit 24: 2013 Cost Structure vs. Profitability Exhibit 25: Average Peer EBIT Margin vs. UAL

6.8%

3.6%

11.4%12.1%

8.2% 8.7%

6.5%

14.7% 15.1%

10.8%11.9%

13.9%14.6%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

United EBIT margin, adj Network Carrier Adj. EBIT Margin (avg ex-UAL)

Source: Company data, Credit Suisse estimates. Source: Company data, Credit Suisse estimate.

Non-Fuel Unit Cost Growth Targeted Below Inflation 2015-17: While these changes

will take time to fully implement in such a large system, unit cost performance year to date

has been better than originally expected despite lower capacity. Management expects the

strong cost performance to continue in H2 2014, and its guidance for 1-2% unit cost

growth is in-line with the average of Delta's (0-2%) and American's (1-3%). Looking

beyond 2014, UAL expects to keep non-fuel unit cost growth below inflation from 2015 to

2017.

UAL's cost structure, both

including and excluding fuel,

is ~24% higher than network

peers when adjusted for

stage length, and its

operating margins have

lagged by ~400-500 bps

08 September 2014

United Continental Holdings, Inc. (UAL) 12

Exhibit 26: UAL Unit Cost Growth Has Exceeded Peers Up

Until Q2'14 as Cost Initiatives Showed Progress

Exhibit 27: UAL Unit Labor Costs Higher than Peers

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

2012 2013 Q1'14 Q2'14

United CASM, ex Y/Y

Network Carrier CASM, ex

Y/Y Average

0.00¢

1.00¢

2.00¢

3.00¢

4.00¢

5.00¢

6.00¢

LCC AA DAL UAL

Stage Length Adj. Labor CASM

UAL's Labor CASM is 34% higher than the peer average

Source: Company data, Credit Suisse estimates. Source: Company data, Credit Suisse estimates.

Project Quality Was Announced Last Fall, but Management Continues to Look for

Structural Cost Reductions: Project Quality (PQ) was announced last fall at UAL's 2013

investor day and is intended to reduce ~$2B in expenses by 2017, with one-half of the

savings coming from fuel and the other half from a variety of operational improvements in

maintenance, productivity, sourcing, and distribution. The program is expected to eliminate

$500M of expenses this year alone, of which $200M will come from fuel savings. Benefits

from Project Quality should help to keep non-fuel unit cost growth below inflation from

2015 to 2017 on annual capacity growth that is below GDP.

We see upside to several of the PQ initiatives including maintenance, productivity, and

sourcing. Management is continuing to take cost-corrective actions beyond PQ such as

the decision to substantially reduce flying in Cleveland, dehubbing the airport, given its

high costs and lack of profitability. Management most recently announced substantial

changes to its regional flying, including reducing the number of partners (from eight to four

in Washington-Dulles [IAD] and from seven to four in Chicago O'Hare [ORD]).

Exhibit 28: Taking Steps to Cut Costs and Keep CASM (ex-fuel) Growth Below Inflation

Driver Savings Source

Fuel Consumption $1BTargeting 7% improvement in fuel efficiency in 2017 vs . 2013 through a ircraft

replacement, winglets and operational ini tiatives

Maintenance $100-$150MTargeting 10-15% improvement in maintenance CASM from new a ircraft, improved

qual i ty through lean, preventative maintenance

Productivi ty $500MTargeting 15-20% improvement in productivi ty by 2017 through a l igning s taff, best

sourcing, increas ing qual i ty, reducing defects , investing in IT

Sourcing $100-$150M Bring engine contracts in-l ine with market rates ; restructure a i rport rental agreements

Distribution $100-$150M Shift traffic mix to internal webs ite (optimal dis tribution channel )

and there

are more

Other changes outs ide

Project Qual i ty?? Dehubbing CLE (ann. Feb'14), Accelerated optimization of Regional flying (ann. July'14)

Cost Reduction InitiativesProject Quality = $2B annually by 2017

2014-2017 ex-fuel unit cost growth < inflation

We see

upside to

these PQ

savings

initiatives

Source: Company data, Credit Suisse estimates.

Project Quality is a

cost-savings initiative that is

intended to reduce ~$2B in

expenses by 2017

08 September 2014

United Continental Holdings, Inc. (UAL) 13

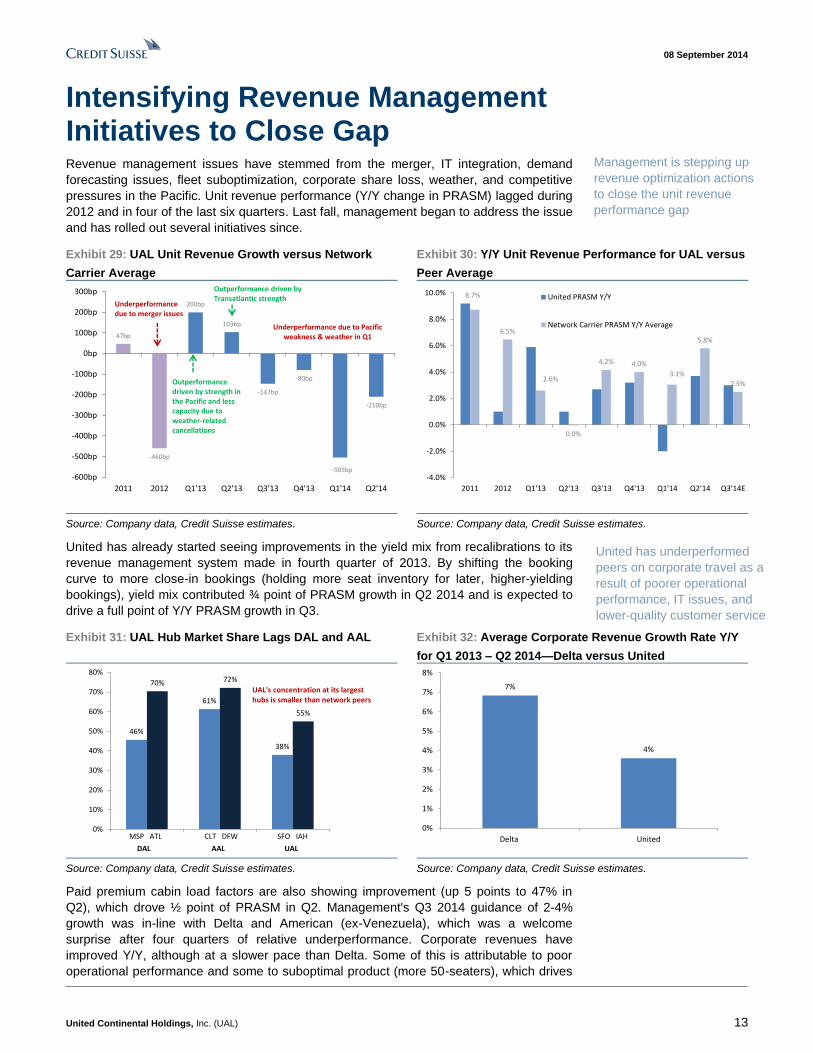

Intensifying Revenue Management Initiatives to Close Gap Revenue management issues have stemmed from the merger, IT integration, demand

forecasting issues, fleet suboptimization, corporate share loss, weather, and competitive

pressures in the Pacific. Unit revenue performance (Y/Y change in PRASM) lagged during

2012 and in four of the last six quarters. Last fall, management began to address the issue

and has rolled out several initiatives since.

Exhibit 29: UAL Unit Revenue Growth versus Network

Carrier Average

Exhibit 30: Y/Y Unit Revenue Performance for UAL versus

Peer Average

47bp

-460bp

200bp

103bp

-147bp

-80bp

-505bp

-210bp

-600bp

-500bp

-400bp

-300bp

-200bp

-100bp

0bp

100bp

200bp

300bp

2011 2012 Q1'13 Q2'13 Q3'13 Q4'13 Q1'14 Q2'14

Outperformancedriven by strength in the Pacific and less capacity due to weather-related cancellations

Outperformance driven by Transatlantic strength

Underperformancedue to merger issues

Underperformance due to Pacific weakness & weather in Q1

8.7%

6.5%

2.6%

0.0%

4.2% 4.0%

3.1%

5.8%

2.5%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

2011 2012 Q1'13 Q2'13 Q3'13 Q4'13 Q1'14 Q2'14 Q3'14E

United PRASM Y/Y

Network Carrier PRASM Y/Y Average

Source: Company data, Credit Suisse estimates. Source: Company data, Credit Suisse estimates.

United has already started seeing improvements in the yield mix from recalibrations to its

revenue management system made in fourth quarter of 2013. By shifting the booking

curve to more close-in bookings (holding more seat inventory for later, higher-yielding

bookings), yield mix contributed ¾ point of PRASM growth in Q2 2014 and is expected to

drive a full point of Y/Y PRASM growth in Q3.

Exhibit 31: UAL Hub Market Share Lags DAL and AAL Exhibit 32: Average Corporate Revenue Growth Rate Y/Y

for Q1 2013 – Q2 2014—Delta versus United

46%

61%

38%

70% 72%

55%

0%

10%

20%

30%

40%

50%

60%

70%

80%

UAL's concentration at its largest hubs is smaller than network peers

DAL AAL UAL

MSP ATL CLT DFW SFO IAH

7%

4%

0%

1%

2%

3%

4%

5%

6%

7%

8%

Delta United

Source: Company data, Credit Suisse estimates. Source: Company data, Credit Suisse estimates.

Paid premium cabin load factors are also showing improvement (up 5 points to 47% in

Q2), which drove ½ point of PRASM in Q2. Management's Q3 2014 guidance of 2-4%

growth was in-line with Delta and American (ex-Venezuela), which was a welcome

surprise after four quarters of relative underperformance. Corporate revenues have

improved Y/Y, although at a slower pace than Delta. Some of this is attributable to poor

operational performance and some to suboptimal product (more 50-seaters), which drives

Management is stepping up

revenue optimization actions

to close the unit revenue

performance gap

United has underperformed

peers on corporate travel as a

result of poorer operational

performance, IT issues, and

lower-quality customer service

08 September 2014

United Continental Holdings, Inc. (UAL) 14

customers to book away from United. We expect with American now a much stronger

competitor, the competitive environment for high-yielding corporate contracts will only

intensify, but United does have arguably the strongest network suited for corporate travel.

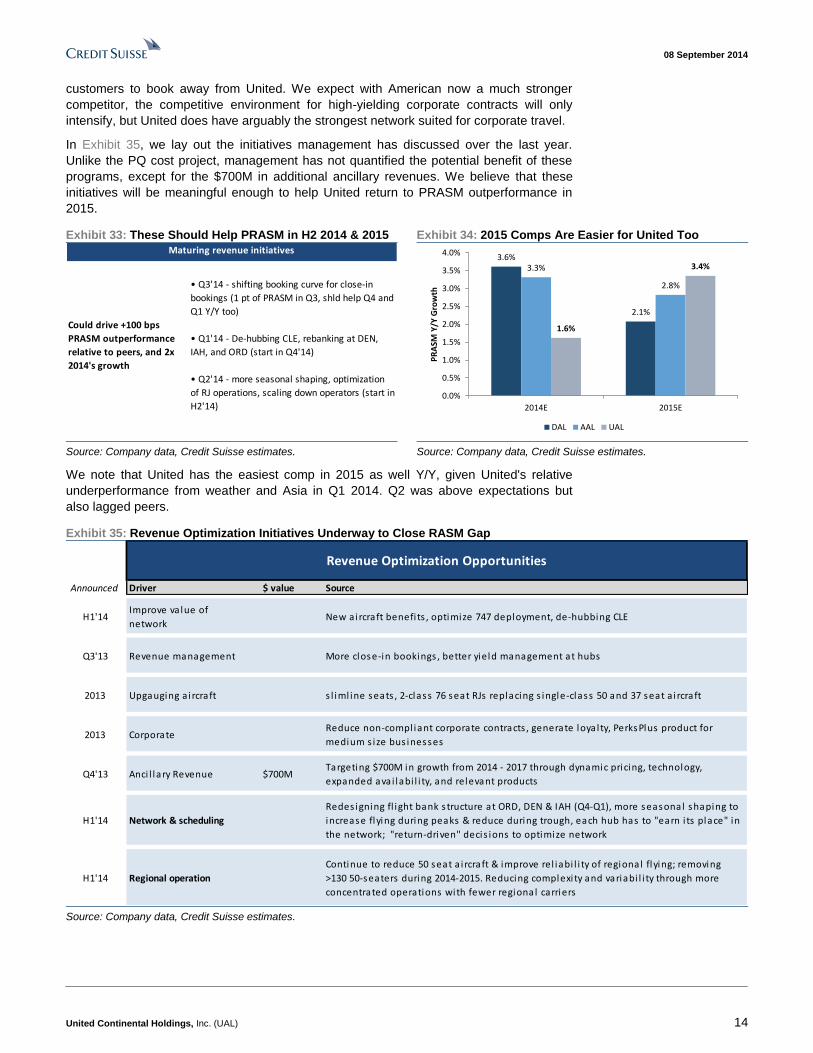

In Exhibit 35, we lay out the initiatives management has discussed over the last year.

Unlike the PQ cost project, management has not quantified the potential benefit of these

programs, except for the $700M in additional ancillary revenues. We believe that these

initiatives will be meaningful enough to help United return to PRASM outperformance in

2015.

Exhibit 33: These Should Help PRASM in H2 2014 & 2015 Exhibit 34: 2015 Comps Are Easier for United Too

Maturing revenue initiatives

Could drive +100 bps

PRASM outperformance

relative to peers, and 2x

2014's growth

• Q3'14 - shifting booking curve for close-in

bookings (1 pt of PRASM in Q3, shld help Q4 and

Q1 Y/Y too)

• Q1'14 - De-hubbing CLE, rebanking at DEN,

IAH, and ORD (start in Q4'14)

• Q2'14 - more seasonal shaping, optimization

of RJ operations, scaling down operators (start in

H2'14)

3.6%

2.1%

3.3%

2.8%

1.6%

3.4%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

2014E 2015E

PR

ASM

Y/Y

Gro

wth

DAL AAL UAL

Source: Company data, Credit Suisse estimates. Source: Company data, Credit Suisse estimates.

We note that United has the easiest comp in 2015 as well Y/Y, given United's relative

underperformance from weather and Asia in Q1 2014. Q2 was above expectations but

also lagged peers.

Exhibit 35: Revenue Optimization Initiatives Underway to Close RASM Gap

Announced Driver $ value Source

H1'14Improve va lue of

networkNew aircraft benefi ts , optimize 747 deployment, de-hubbing CLE

Q3'13 Revenue management More close-in bookings , better yield management at hubs

2013 Upgauging a i rcraft s l iml ine seats , 2-class 76 seat RJs replacing s ingle-class 50 and 37 seat a i rcraft

2013 CorporateReduce non-compl iant corporate contracts , generate loyalty, PerksPlus product for

medium s ize bus inesses

Q4'13 Anci l lary Revenue $700MTargeting $700M in growth from 2014 - 2017 through dynamic pricing, technology,

expanded avai labi l i ty, and relevant products

H1'14 Network & scheduling

Redes igning fl ight bank s tructure at ORD, DEN & IAH (Q4-Q1), more seasonal shaping to

increase flying during peaks & reduce during trough, each hub has to "earn i ts place" in

the network; "return-driven" decis ions to optimize network

H1'14 Regional operation

Continue to reduce 50 seat a i rcraft & improve rel iabi l i ty of regional flying; removing

>130 50-seaters during 2014-2015. Reducing complexi ty and variabi l i ty through more

concentrated operations with fewer regional carriers

Revenue Optimization Opportunities

Source: Company data, Credit Suisse estimates.

08 September 2014

United Continental Holdings, Inc. (UAL) 15

Scaling Down Unprofitable Hubs

The company reduced its average daily departures from Cleveland (CLE) by ~60%,

starting in phases in April of this year. The reductions were completed in June 2014, and

UAL took its CLE capacity down by ~36% from 200 daily departures to 72 departures with

destinations served falling to 72 from 200. The reduction will largely come from regional

departures, with mainline operations remaining largely unchanged. The decision was

driven in part by the hub's lack of profitability, as well as by new industry regulations on

pilot hours that have caused mainline carriers to increase hiring of regional pilots,

drastically reducing the supply of regional pilots. Poor profitability resulted from the lack of

higher-yielding connecting traffic, as many passengers opted instead to travel through

Detroit or Chicago.

Given the decisions by other carriers to scale down Cincinnati, Milwaukee, Memphis,

Pittsburgh, and St. Louis since consolidation, this wasn’t so surprising. CLE was a

Continental hub and served a vital purpose in the network for connecting passengers in

the Midwest. However, its O&D traffic was small and it's close enough to Chicago that

United didn’t need both.

There could be more scaledowns to come as management continues to evaluate its

network.

Restructuring Pacific Network & Routes

United has shifted its Asia strategy by (1) restructuring Narita flying by working with JV

partner ANA (eliminating unprofitable flying beyond Tokyo), (2) optimizing 747 deployment

(improving reliability and down gauging where appropriate to 777s), (3) transitioning flights

to Tier 2 cities with less competition (offering flights from San Francisco to Chengdu and

Taipei), and (4) rightsizing with 787 flying (to better match capacity with demand and

increase fuel efficiency). The Pacific performed better than expected in Q2 2014,

exhibiting progress on the initiatives and a benefit from the seasonal peak. However,

competitive capacity will pressure yields after the seasonal peak.

Ancillary Products and Services Offer High Margin Growth

United has grown ancillary revenues to $3B (~8% of sales) in 2014 and is planning to

grow that to $3.5B dollars by 2017, a 7% CAGR from 2010's $2.2B level. Ancillary

products are extremely high margin, as they extract additional revenue from an existing

customer with little to no incremental expense with no associated working capital. United

trails Delta, for which non-ticket revenues are closer to 20% of sales at >$5B.

United is targeting growth through unbundling (charging for bags, meals), new in-flight

products (streaming entertainment, onboard Wi-Fi), and optimization of the customer

experience (premier access, United Club, flexibility through FareLock, and premium cabin

upsell). United is also improving dynamic pricing and expanding availability through digital

channels, as well as stimulating growth via smart bundling of products. Wi-Fi is currently

offered on 170 aircraft, and the airline plans to expand that offering to its entire mainline

fleet.

The company has also launched a dynamic pricing system that offers multiple price points

for Economy Plus seats on a plane based on the demand for the seat (i.e., people will pay

more for an aisle versus the middle), as well as for demand for the flight. The enhanced

pricing of these seats will also be available to a wider consumer base. UAL is expanding

the distribution of this product by offering Economy Plus on TravelPort as well as two other

distribution systems.

Management commented in

July that each hub has to

"earn its place in the

network" and it is making

"return-driven" decisions to

optimize the network,

suggesting that there could

be more hub scaledowns to

come

United is targeting $3B

dollars in ancillary revenues

this year and is planning to

grow that to $3.5B dollars by

2017

08 September 2014

United Continental Holdings, Inc. (UAL) 16

Exhibit 36: UAL Ancillary Revenues

$2.2B$2.4B $2.5B

$2.8B$3.0B

$3.5B+

$0.0B

$0.5B

$1.0B

$1.5B

$2.0B

$2.5B

$3.0B

$3.5B

$4.0B

2010 2011 2012 2013 2014 2017E

+7% CAGR

Source: Company data, Credit Suisse estimates.

Corporate Market Share Has Suffered from Merger Integration but Is Positioned Well

The company has significant share at several hubs in prime business markets, such as

San Francisco, Chicago, and New York via Newark, that also attract higher-yielding

corporate and international travel. UAL is able to leverage its globally expansive network

and membership in Star Alliance, which the strongest market share in the top ten

international markets for corporate travel, particularly in Asia and Canada (see Exhibit 38)

as a result of its joint venture partners.

Exhibit 37: Top Domestic Markets for Corporate Travel

with Passenger Share by Network Carrier

Exhibit 38: Top International Markets for Corporate Travel

with ASM Share to Destination by Alliance

RankMarket

(incl secondary airports)American United Delta

1) New York 22% 24% 26%

2) Las Vegas 12% 10% 12%

3) Chicago 29% 27% 8%

4) San Francisco 12% 28% 10%

5) Houston 11% 43% 7%

6) Orlando 15% 10% 17%

7) Atlanta 9% 3% 63%

8) San Diego 15% 13% 12%

9) Charlotte 67% 9% 18%

10) Dal las 55% 5% 8%

**Share calculated from % of passengers from O&D reports for YE 2013

Top Domestic Corporate Travel Markets

Rank Market oneworld Star Alliance Sky Team

1) London 53% 20% 6%

2) Shanghai , China 10% 27% 40%

3) Singapore 11% 53% 7%

4) Bei jing, China 5% 52% 24%

5) Tokyo, Japan 29% 43% 16%

6) Toronto, Canada 7% 58% 6%

7) Hong Kong 59% 18% 7%

8) Paris , France 10% 12% 63%

9) Mexico City, Mexico 14% 14% 46%

10) Montreal , Canada 9% 48% 13%

**Share calculated from schedule data for TTM July 2014, ASMs into market

Top International Corporate Travel Markets

Source: Concur, Diio Mi, Credit Suisse research and estimates. Source: Concur, Diio Mi, Credit Suisse research and estimates.

Despite its strong route network, United has underperformed peers recently on corporate

travel, which seems to be a direct result of poorer operational performance, IT issues, and

lower-quality customer service. United ranked last in BTN's 2012 Airline Survey, in which

corporate travel buyers rank airlines on ten categories. United managed to improve three

spots in 2013 but is still well behind the Delta Airlines, which has led since 2011. Delta has

capitalized on United's struggles through the merger and managed to take share from

United as a result of significant investments, better operational performance, and leading

customer service. Now, with a much stronger American Airlines, we think regaining lost

share will be challenging for United and that it take some time to regain customers

satisfied with their new carrier.

United saw corporate revenue steadily increase in 2013 in the midsingle-digit range, but

this slowed in Q1 2014 when revenues increased only 2% versus peers posting

high-single-digit Y/Y growth. In Q2 2014, revenue for large corporate accounts grew 3%

Y/Y but was pressured by a decline in April from the Easter shift. Including its PerksPlus

program for smaller businesses, overall corporate grew 6% in Q2.

United has a joint ventures

with Lufthansa and Air

Canada covering the

transatlantic and another

with ANA for transpacific

routes

08 September 2014

United Continental Holdings, Inc. (UAL) 17

Balance Sheet and Capital Allocation Improving its Balance Sheet: To meet its long-term capital structure goals, United is

reducing higher-coupon, non-aircraft-related debt and managing total debt including

capitalized aircraft rent (aircraft rent x7) to ~$15B by 2017 from ~$18.7B as of June 30,

2014. Net debt (lease-adjusted) was $5.8B at June 30, 2014. Since 2009 (pro forma), total

debt has declined over $5B, and United has over $4B in additional debt payments

scheduled before the end of 2017. In addition, United announced in July that it will redeem

its $800M 6.75% secured notes in September when the notes become prepayable at par.

The airlines using highly efficient sources of aircraft funding, accessing the EETC market

for all of its 2014 deliveries (except seven ERJ175 aircraft). Stated interest rates on recent

EETCs have averaged ~4%. UAL's 2014 interest expense is 30% lower than four years

ago.

Exhibit 39: UAL—Total Debt Outstanding ($B)

*pro forma Note: includes aircraft rent capitalized at 7x

Exhibit 40: Debt Payments—Actual & Scheduled

*incl. capital lease payments; scheduled payments include all commitments for which co. has secured financing

$25.9

$23.8

$20.1$19.0 $18.7

$15.0

$0.0

$5.0

$10.0

$15.0

$20.0

$25.0

$30.0

2006* 2009* 2012A 2013A 6/30/2014A 2017E

Total Debt Outstanding $B (inc. aircraft rent x7)

$2.5$2.6

$1.5

$2.3

$1.5

$2.0

$1.2

$0.7

$0.0

$0.5

$1.0

$1.5

$2.0

$2.5

$3.0

2010A 2011A 2012A 2013A 2014E 2015E 2016E 2017E

Debt payments

$1.35B average'14 - '17

Source: Company data, Credit Suisse estimates. Source: Company data, Credit Suisse estimates.

Liquidity 18% of LTM Sales: United ended Q2 2014 with $5.8B in cash and short-term

investments and a fully undrawn $1B revolving credit line (which UAL plans to increase to

$1.35B in September 2014). Total liquidity as a percentage of LTM revenue increased 187

basis points to 17.6% sequentially. The net lease debt to LTM EBITDAR ratio was 2.9x by

our calculation, an improvement of 0.3x over Q1 2014. We forecast this ratio to continue to

decline as debt comes down and EBITDAR improves. Moody's rates UAL Stable, with a

B2 long-term rating.

Exhibit 41: Net Lease Adj. Debt /LTM EBITDAR Exhibit 42: Unfunded Pension Liability

3.5x

3.1x2.9x

1.3x

0.0x

0.5x

1.0x

1.5x

2.0x

2.5x

3.0x

3.5x

4.0x

2012A 2013A 6/30/2014A 2016E

Net Lease Adj. Debt / LTM EBITDAR

$1.50

$1.80

$2.40

$1.65 $1.59

$0.0

$0.5

$1.0

$1.5

$2.0

$2.5

$3.0

2010 2011 2012 2013 Q2'14

Unfunded pension liability ($B)

Source: Company data, Credit Suisse estimates. Source: Company data, Credit Suisse estimates.

08 September 2014

United Continental Holdings, Inc. (UAL) 18

Managing Down Pension Risk: United is contributing $290M to its pension in 2014,

double its minimum funding requirements. It expects it will continue fund the pension

above the minimum to reduce risk over the long term. UAL has stated it will fund

~$125-150M above required contributions going forward. The unfunded pension obligation

has declined to <$1.6B as of June 30, 2014, a greater than 30% decline since 2012.

Capital Expenditures—Making Return-Oriented Decisions: United has guided to

average capital expenditures of $2.8-3.0B from 2014 to 2017, of which aircraft

replacement accounts for 65%. This is under 7% of sales on average. We forecast that

United will come in slightly below the low end as it manages down capital expenditure

spend by deferring new aircraft deliveries in favor of used in the near-term, as discussed

on the July earnings call. United's fleet strategy takes into account three financial

objectives: (1) consistent, manageable levels of capital investment, (2) earnings/cash flow

generation, and ( 3) ROIC over asset life.

Inconsistent aircraft investment during historical peaks and troughs of profitability has

resulted in large, cyclical aircraft orders. United is accelerating and deferring certain

aircraft replacement to smooth capital investment, in some instances making modest

investments to defer capex (i.e., A319/A320 fleet exit planning decision and interior

upgrades), and is now looking to the used aircraft market opportunistically and deferring

new deliveries. United has 258 firm commitments for deliveries as of Q2, which is 20% of

its current fleet (mainline and regional). United expects to keep the consolidated fleet

count roughly flat between 1,250 and 1,350 aircraft.

Exhibit 43: United Capital Expenditures 2012A – 2017E Exhibit 44: Credit Suisse Forecast for Pace on UAL's $1B

Buyback – We Forecast Completion by 2016 YE

$2.5 $2.4

$3.1$2.7 $2.7 $2.8

6.8%6.3%

8.0%

6.7% 6.6%6.6%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

$0.0

$0.5

$1.0

$1.5

$2.0

$2.5

$3.0

$3.5

2012A 2013A 2014E 2015E 2016E 2017E

CapEx - $B CapEx as a % Sales

$275

$400

$325

$0

$50

$100

$150

$200

$250

$300

$350

$400

$450

2014E 2015E 2016E

Buyback - $B

Source: Company data, Credit Suisse estimates. Source: Company data, Credit Suisse estimates.

Share Repurchase Authorization Signifies Confidence: United authorized a $1B share

repurchase over three years, implying completion mid-2017 (6% of its market cap), and

initiated a $200M ASR to be completed in Q3 2014. We think that most expected this

announcement would come closer to YE 2014, or even early 2015.

United had previously stated that returning cash to shareholders was something it wanted

to do by sometime in 2015, with the caveat it wasn’t precluded from doing something in

2014. The company saw two gating items to shareholder returns including (1) addressing

the $800M 6.75% secured notes, which it plans to redeem in September when the notes

become prepayable at par; and (2) generating a level of earnings and cash that supported

capital distribution. United management is now confident more in its financial outlook and

believes that UAL shares are currently trading at a discount to intrinsic value. United will

evaluate if and when it will complement its repurchase plan with a dividend as it increases

earnings and pays down debt.

We forecast that United will

come in slightly below the

low end as it manages down

capital expenditure spend

by deferring new aircraft

deliveries in favor of used in

the near-term, as discussed

on the July earnings call

United characterized its

buyback announcement as

a "first step" and a

"watershed moment" in the

airline industry, as the four

largest carriers are returning

cash to shareholders

08 September 2014

United Continental Holdings, Inc. (UAL) 19

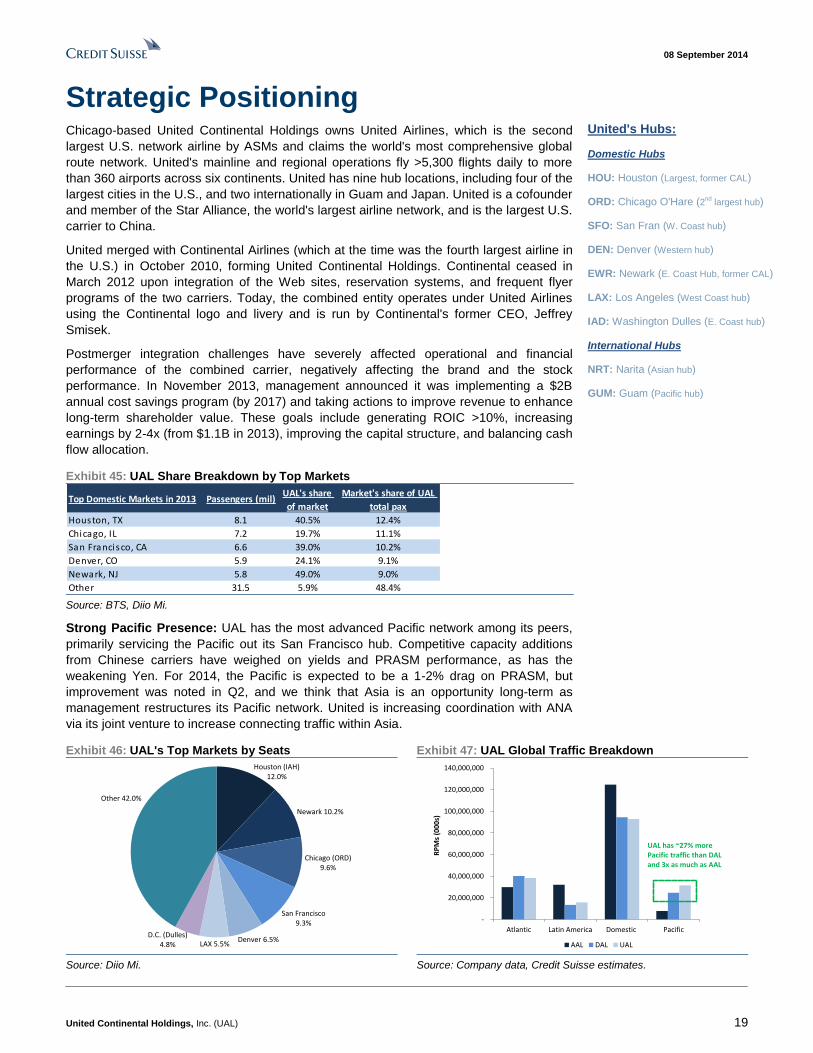

Strategic Positioning Chicago-based United Continental Holdings owns United Airlines, which is the second

largest U.S. network airline by ASMs and claims the world's most comprehensive global

route network. United's mainline and regional operations fly >5,300 flights daily to more

than 360 airports across six continents. United has nine hub locations, including four of the

largest cities in the U.S., and two internationally in Guam and Japan. United is a cofounder

and member of the Star Alliance, the world's largest airline network, and is the largest U.S.

carrier to China.

United merged with Continental Airlines (which at the time was the fourth largest airline in

the U.S.) in October 2010, forming United Continental Holdings. Continental ceased in

March 2012 upon integration of the Web sites, reservation systems, and frequent flyer

programs of the two carriers. Today, the combined entity operates under United Airlines

using the Continental logo and livery and is run by Continental's former CEO, Jeffrey

Smisek.

Postmerger integration challenges have severely affected operational and financial

performance of the combined carrier, negatively affecting the brand and the stock

performance. In November 2013, management announced it was implementing a $2B

annual cost savings program (by 2017) and taking actions to improve revenue to enhance

long-term shareholder value. These goals include generating ROIC >10%, increasing

earnings by 2-4x (from $1.1B in 2013), improving the capital structure, and balancing cash

flow allocation.

Exhibit 45: UAL Share Breakdown by Top Markets

Top Domestic Markets in 2013 Passengers (mil)UAL's share

of market

Market's share of UAL

total pax

Houston, TX 8.1 40.5% 12.4%

Chicago, IL 7.2 19.7% 11.1%

San Francisco, CA 6.6 39.0% 10.2%

Denver, CO 5.9 24.1% 9.1%

Newark, NJ 5.8 49.0% 9.0%

Other 31.5 5.9% 48.4% Source: BTS, Diio Mi.

Strong Pacific Presence: UAL has the most advanced Pacific network among its peers,

primarily servicing the Pacific out its San Francisco hub. Competitive capacity additions

from Chinese carriers have weighed on yields and PRASM performance, as has the

weakening Yen. For 2014, the Pacific is expected to be a 1-2% drag on PRASM, but

improvement was noted in Q2, and we think that Asia is an opportunity long-term as

management restructures its Pacific network. United is increasing coordination with ANA

via its joint venture to increase connecting traffic within Asia.

Exhibit 46: UAL's Top Markets by Seats Exhibit 47: UAL Global Traffic Breakdown

Houston (IAH) 12.0%

Newark 10.2%

Chicago (ORD) 9.6%

San Francisco 9.3%

Denver 6.5%LAX 5.5%

D.C. (Dulles) 4.8%

Other 42.0%

-

20,000,000

40,000,000

60,000,000

80,000,000

100,000,000

120,000,000

140,000,000

Atlantic Latin America Domestic Pacific

RP

Ms

(00

0s)

AAL DAL UAL

UAL has ~27% more Pacific traffic than DAL and 3x as much as AAL

Source: Diio Mi. Source: Company data, Credit Suisse estimates.

United's Hubs:

Domestic Hubs

HOU: Houston (Largest, former CAL)

ORD: Chicago O'Hare (2nd largest hub)

SFO: San Fran (W. Coast hub)

DEN: Denver (Western hub)

EWR: Newark (E. Coast Hub, former CAL)

LAX: Los Angeles (West Coast hub)

IAD: Washington Dulles (E. Coast hub)

International Hubs

NRT: Narita (Asian hub)

GUM: Guam (Pacific hub)

08 September 2014

United Continental Holdings, Inc. (UAL) 20

Fuel—19% Hedged for 2015: In 2013, fuel represented UAL's single-largest operating

cost at 33% of total operating expenses. For the full-year 2014, fuel price per gallon

(including hedging impacts) is expected to be $3.06-3.11 based on the July 17, 2014,

forward fuel curve (Brent crude spot $107.89), down ~1.2% from $3.13 in 2013. UAL

typically hedges a portion of its forecast fuel consumption. As of Q2, the company had

hedged 21% of 2014 projected fuel requirements and 19% of its projected 2015

consumption.

Regional Partner Flying

United relies on regional contract carriers as an efficient means to feed its route network

and operate commuter flights. Network carriers outsource to regional airlines as many of

the smaller airports served by regional contract carriers would be unprofitable to service

with a mainline aircraft. United partners with a number of regional carriers including

Republic Airlines, CommutAir Airline, ExpressJet Airlines, GoJet Airlines, Mesa Airlines,

Shuttle America, SkyWest Airlines, and Trans States Airlines to provide regional service

under the United Express brand as an extension of the mainline network.

Of United's regional flights, 95% are operated under capacity purchase agreements

(CPAs), which include a fixed fee plus variable reimbursement (incentive payment based

on operational performance). Fuel, landing fees, and facilities rent are passed through by

the regional carrier at cost. United determines the schedules, pricing, and revenue

management. In 2013, regional capacity purchase represented 6.5% of total operating

expenses for the carrier.

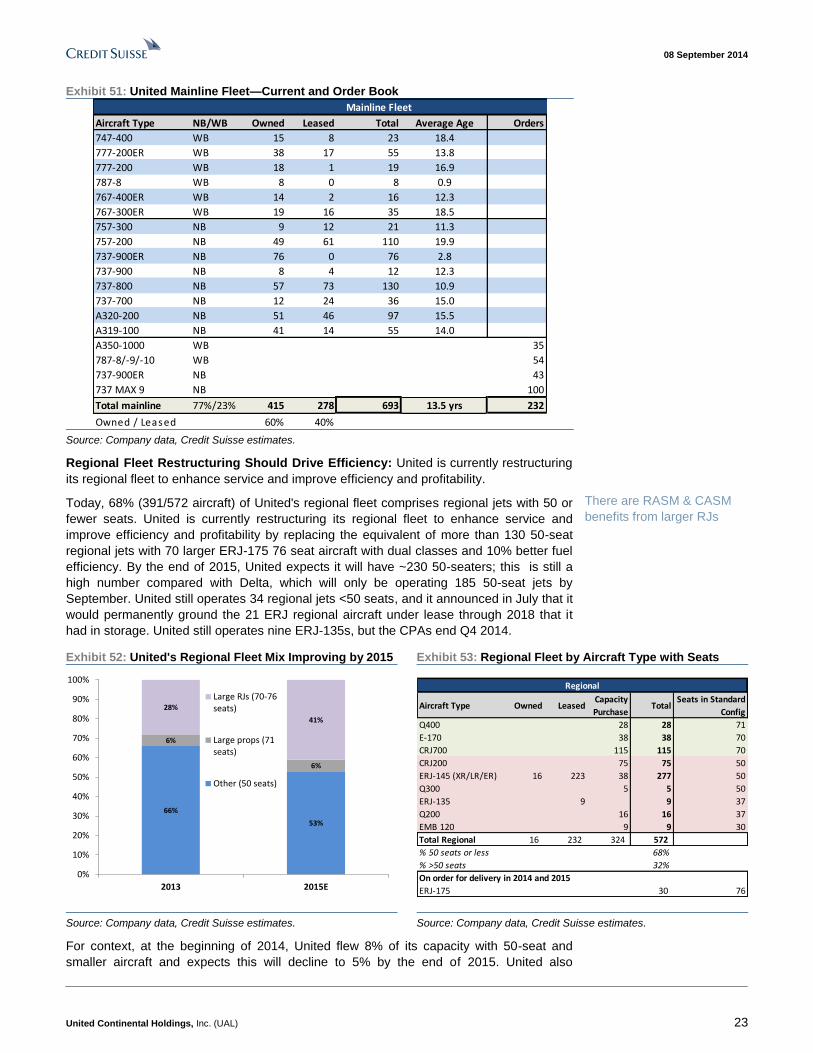

Restructuring Regional Flying to Improve Profitability and Reliability: Today, 68%

(391/572 aircraft) of United's regional fleet comprises regional jets with 50 or fewer seats.

United is currently restructuring its regional fleet to enhance service and improve efficiency

and profitability by replacing the equivalent of more than 130 50-seat regional jets with 70

larger ERJ-175 76 seat aircraft with dual classes and 10% better fuel efficiency. By the

end of 2015, United expects it will have ~230 50-seaters. For context, at the beginning of

2014, United flew 8% of its capacity with 50-seat and smaller aircraft and expects this will

decline to 5% by the end of 2015.

United also announced in July that it is taking action to improve the reliability of its regional

operations, including reducing complexity and variability through more concentrated

operations and fewer regional carriers. This means a reduction in the number of partners

out of a given hub (i.e., going from eight to four out of Washington-Dulles and seven to

four in Chicago O'Hare), which should improve profitability by providing both revenue and

cost benefits. (See Exhibit 52 and Exhibit 53 in the Fleet Strategy section for more detail.)

UAL has 24% of its 2014

fuel consumption hedged

08 September 2014

United Continental Holdings, Inc. (UAL) 21

Merger Integration Since the 2010 merger, United has underperformed peers operationally and financially,

and while UAL shares have risen 108% (since the merger close date in October 2010),

DAL shares are up 300% over the same period. Labor and IT issues have been the

primary culprits, and the flight attendants and mechanic unions are still negotiating for a

single contract four years after the merger was announced, creating inefficiencies and

cultural challenges. United flight attendants and cabin crews are still unable to fly on

Continental flights and vice versa, and the airline has had the highest rate of complaints

filed with the DoT among major airlines in the past three years.

The merger was expected to generate net annual synergies of approximately $1.0-1.2B

dollars a year, and the combined entity has faced many difficulties in the integration

process. The transition to a single-passenger services system in 2012 created numerous

challenges both internally with revenue management and efficiency, as well as from a

customer perspective, with ticketing glitches and poorly perceived customer service

responses.

More problems arose earlier this year when United suffered an outsized impact from the

severe winter weather. On its Q1 call, UAL acknowledged it is still operating a number of

parallel systems and processes that resulted from the merger and are driving inefficiencies

and costs. United has also admitted that its customer service has been subpar following

the merger, and it is spending time and money and leveraging third parties to train its

employees. The lack of operational reliability, combined with IT issues and poor customer

service, has weighed on United's brand image and ratings and resulted in corporate

market share loss as previously outlined.

Exhibit 48: UAL-CAL Integration Timeline

Stock swapmerger announced

ShareholdersApprove MergerNew ticker ann. UAL

CAL leadership is appointed to run combined entity

Government Approves Merger

Merger closesOctober 1, 2010

May-2010 Aug-2010 Sep-2010 Oct-2010

CAL CEO Jeff Smisek takes CEO role at combined carrier

Single Operating Certificate Issued

Nov-2011

Reservation Systems & Frequent Flier Programscombined

Union Negotiations for single contracts

Flight attendants and mechanics still negotiating -Legacy United flight attendants cannot fly on Continental Planes and vice versa

Single Livery & Uniform

Mar-2012 Apr-2012 Aug-2012 - Present

Decision to migrate to smaller, legacy Continental system results in numerous operation challenges

UAL Pilots ratify new 4-yr laboragreement

Dec-2012

Under terms of agreement pilots receive an 8.5% raise in Jan 14 and 3 annual raises of 3%

Decision enables Continental pilots to fly >50 seat aircraft

Source: ACI, WSJ, Credit Suisse Research, Company data.

History of Merger: Continental left the Sky Team Alliance following the DAL-NWA merger

and subsequently joined Star Alliance. United and Continental contemplated merging in

late 2006 and again in 2008; however, in April 2008, negotiations ceased. United then

began talks (again) with US Airways (with which it also considered merging in 2000), but

eventually United and Continental signed an alliance that ultimately paved the way for the

merger, which was approved in May of 2010. This came not even a month after United

formally announced it would not merge with US Airways.

The transition to a

single-passenger services

system in 2012 created

numerous challenges both

internally with revenue

management and efficiency,

as well as from a customer

perspective, with ticketing

glitches and poorly perceived

customer service responses

On its Q1 call, UAL

acknowledged it is still

operating a number of parallel

systems and processes;

these are lingering from the

merger and are driving

inefficiencies and costs

08 September 2014

United Continental Holdings, Inc. (UAL) 22

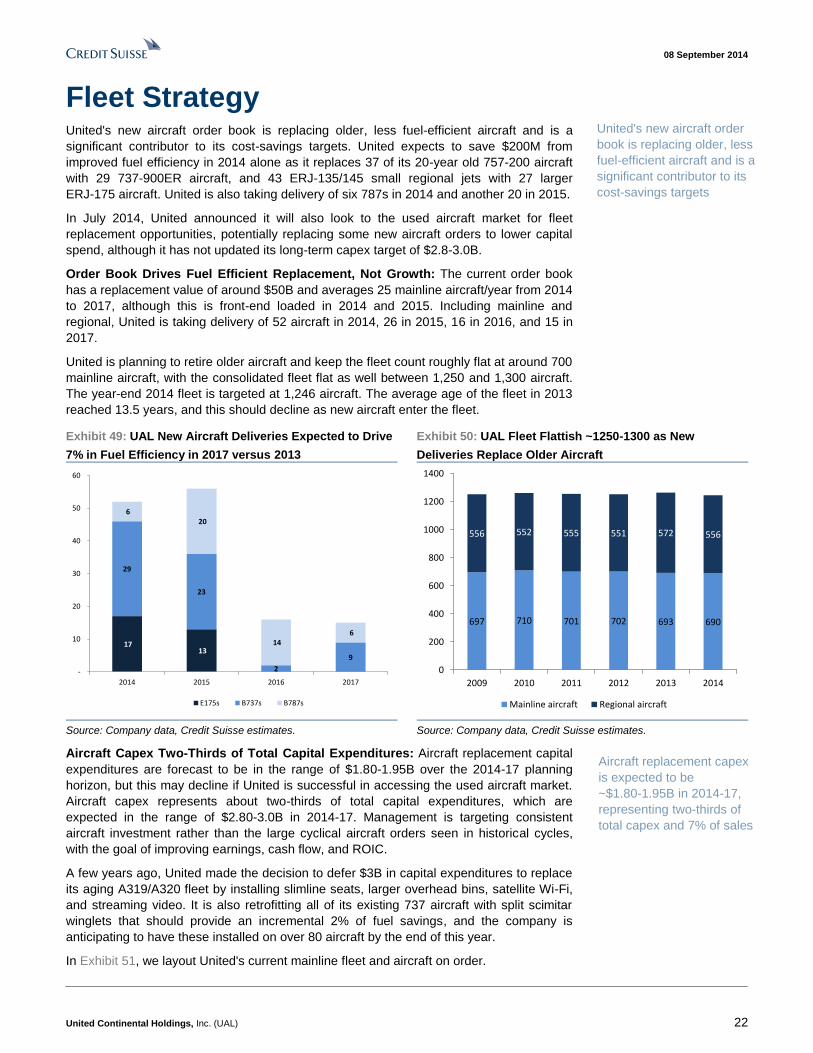

Fleet Strategy United's new aircraft order book is replacing older, less fuel-efficient aircraft and is a

significant contributor to its cost-savings targets. United expects to save $200M from

improved fuel efficiency in 2014 alone as it replaces 37 of its 20-year old 757-200 aircraft

with 29 737-900ER aircraft, and 43 ERJ-135/145 small regional jets with 27 larger

ERJ-175 aircraft. United is also taking delivery of six 787s in 2014 and another 20 in 2015.

In July 2014, United announced it will also look to the used aircraft market for fleet

replacement opportunities, potentially replacing some new aircraft orders to lower capital

spend, although it has not updated its long-term capex target of $2.8-3.0B.

Order Book Drives Fuel Efficient Replacement, Not Growth: The current order book

has a replacement value of around $50B and averages 25 mainline aircraft/year from 2014

to 2017, although this is front-end loaded in 2014 and 2015. Including mainline and