Unit # 5 – Revenue & Expense Accounts

Unit # 5 – Revenue & Expense Accounts. To date we have learned about various types of Asset and Liability accounts, but only one Owner’s Equity Account.

Dec 30, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Unit # 5 – Revenue & Expense Accounts

Unit # 5 – Revenue & Expense Accounts

To date we have learned about various types of Asset and Liability accounts, but only one Owner’s Equity Account (Capital).

We will be introduced to 3 new accounts Revenue Expenses Drawings

Unit # 5 – Revenue & Expense Accounts

Before we start, we must know how these accounts operate.

First off, they are all new accounts under Owner’s Equity (giving us a total of 4 accounts) Capital Revenue Drawings Expenses

Unit # 5 – Revenue & Expense Accounts

To review Revenue is money received from sale

of goods or services. Expenses are the cost to sell goods

(and earn Revenue) and operate the business.

Unit # 5 – Revenue & Expense Accounts

So what is the “Drawings” Account? The Drawings Account is the account

that keeps track of any (or all) the money an Owner “withdrawals” from the business.

It is listed under the Owner’s Equity section because it effects “Net Worth” of the company.

Unit # 5 – Revenue & Expense Accounts

The Balance Sheet A = L + OE

Assets Liabilities Owner’s Equity (including Capital & Drawings)

The Income Statement NI = R - E

Revenue Expenses

Unit # 5 – Revenue & Expense Accounts

Debits & Credits with respect to Revenue, Expenses, and Drawings Accounts

Ok, so we already know there is an increase in Capital we Credit (use the RHS) of the T-Account.

A decrease we Debit (use the LHS).

Unit # 5 – Revenue & Expense Accounts

Revenue acts the exact same as Capital. Increase = Credit (RHS), Decrease =

(Debit) LHS of T-Account This is because Revenue has a

positive effect on Capital. Think about it, the money more you

make by selling goods or services, the greater the company Net Worth.

Unit # 5 – Revenue & Expense Accounts

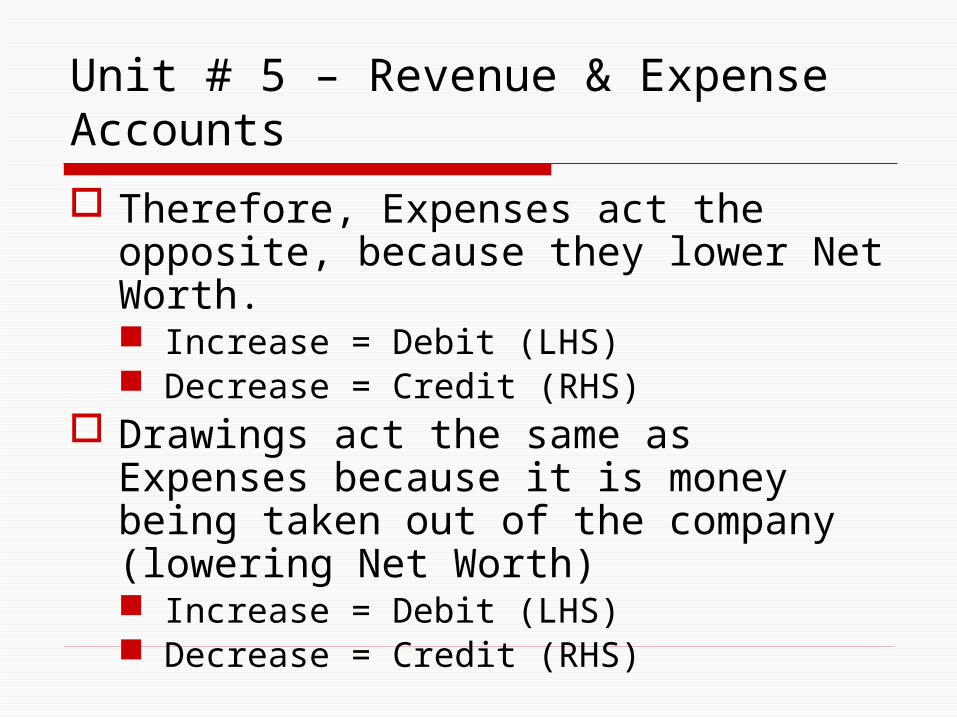

Therefore, Expenses act the opposite, because they lower Net Worth. Increase = Debit (LHS) Decrease = Credit (RHS)

Drawings act the same as Expenses because it is money being taken out of the company (lowering Net Worth) Increase = Debit (LHS) Decrease = Credit (RHS)

Unit # 5 – Revenue & Expense Accounts

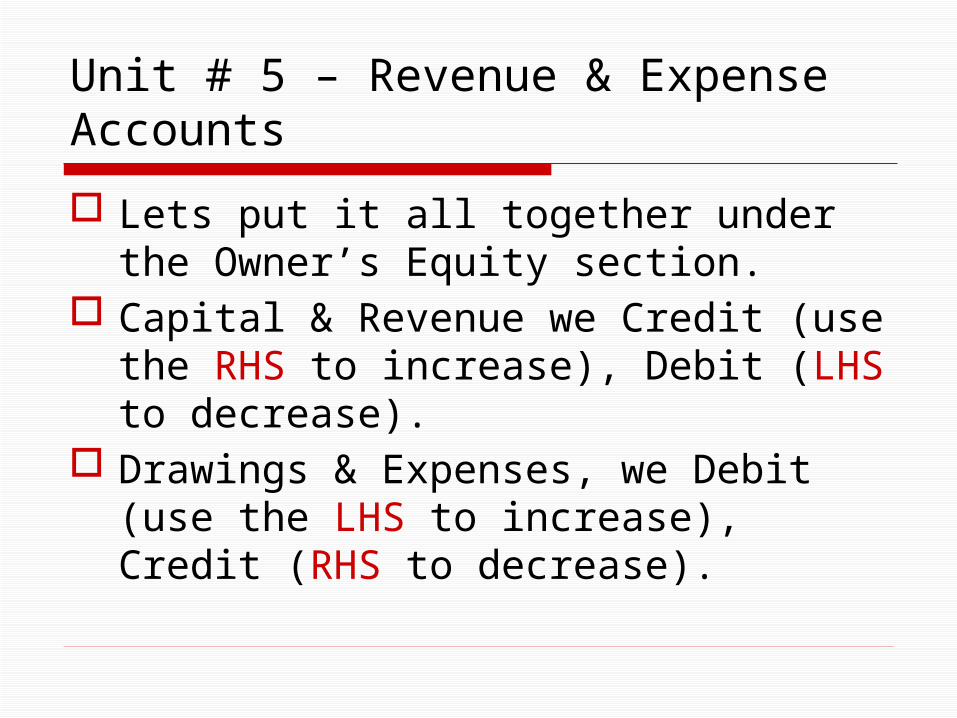

Lets put it all together under the Owner’s Equity section.

Capital & Revenue we Credit (use the RHS to increase), Debit (LHS to decrease).

Drawings & Expenses, we Debit (use the LHS to increase), Credit (RHS to decrease).

Unit # 5 – Revenue & Expense Accounts

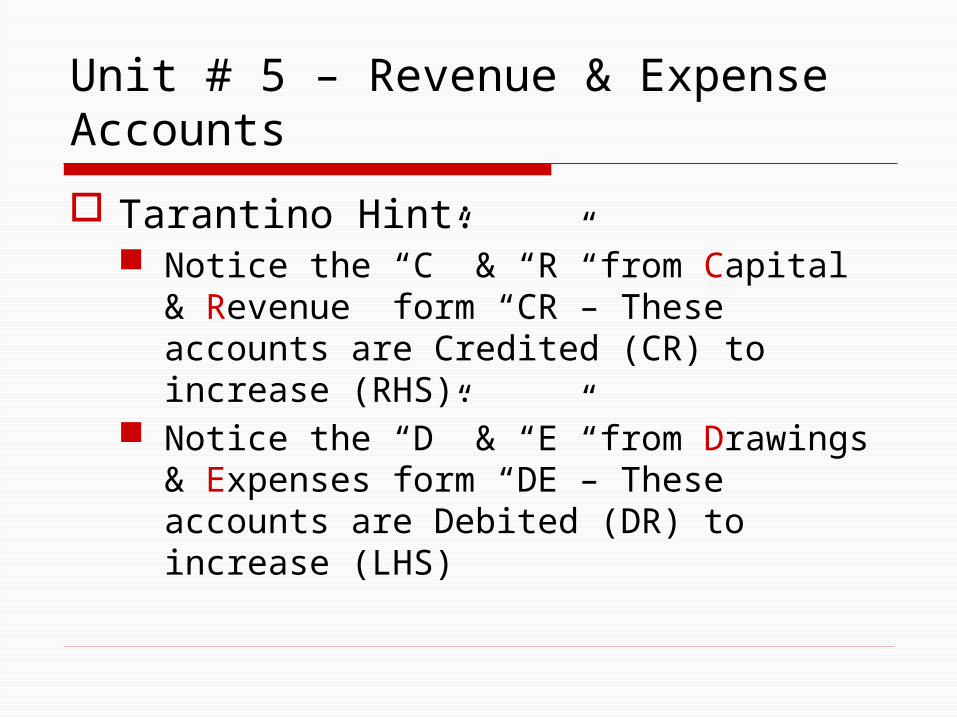

Tarantino Hint: Notice the “C” & “R” from Capital &

Revenue form “CR”– These accounts are Credited (CR) to increase (RHS).

Notice the “D” & “E” from Drawings & Expenses form “DE”– These accounts are Debited (DR) to increase (LHS)

Unit # 5 – Revenue & Expense Accounts

One more thing about the Drawings Account It is known as a “Contra Account” (This is

your first, we will have more) because they act contrary to the account they are married with.

Drawings is “married” to Capital. Because owner uses the Capital Account to

invest money into the business – The owner uses the Drawings Account to take money out of the business for personal use.

Unit # 5 – Revenue & Expense Accounts

Example # 1: Jul. 1 - Received $175 cash from a client for drawing up a new will.

Unit # 5 – Revenue & Expense Accounts

Example # 2: Jul. 2 - Billed client $1200 for legal services to close purchase of home.

Unit # 5 – Revenue & Expense Accounts

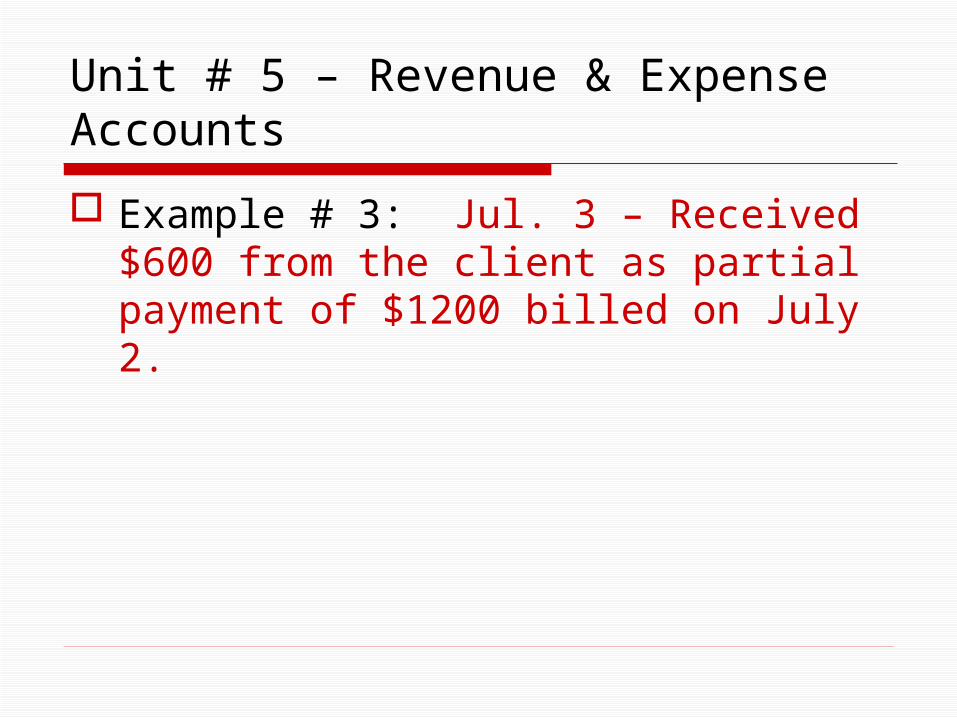

Example # 3: Jul. 3 – Received $600 from the client as partial payment of $1200 billed on July 2.

Unit # 5 – Revenue & Expense Accounts

Example # 4: Jul. 4 – Paid $95 to Telus for telephone bill received today.

Unit # 5 – Revenue & Expense Accounts

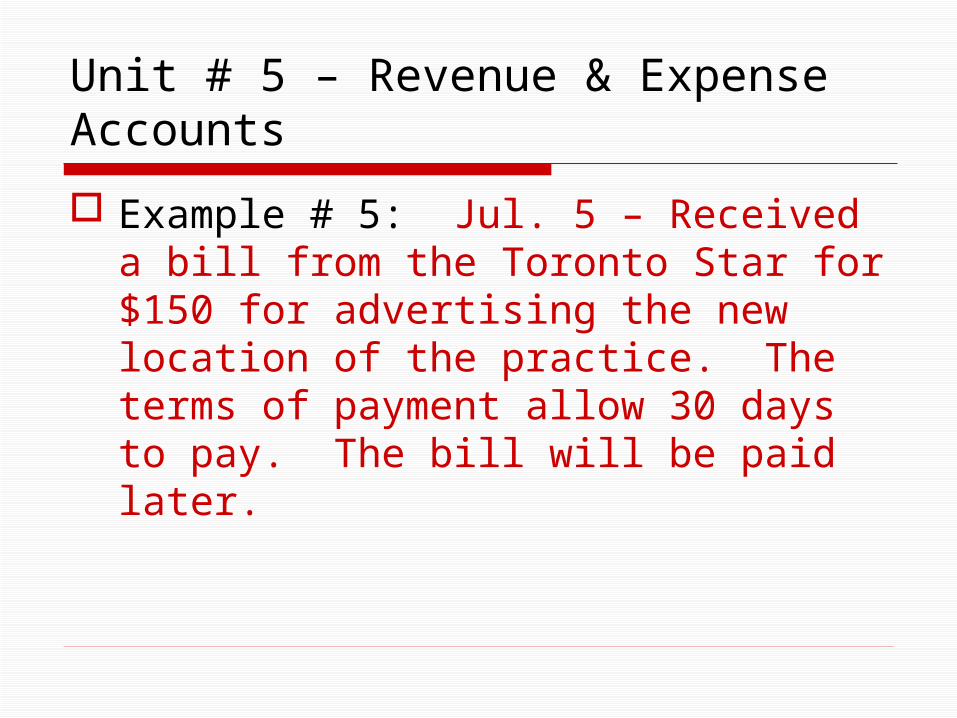

Example # 5: Jul. 5 – Received a bill from the Toronto Star for $150 for advertising the new location of the practice. The terms of payment allow 30 days to pay. The bill will be paid later.

Unit # 5 – Revenue & Expense Accounts

Example # 6: Jul. 6 – Paid $100 to the Toronto Star as partial payment of their bill for the $150 received on July 5.

Unit # 5 – Revenue & Expense Accounts

Practice Makes Perfect! Turn to Page 90 of your textbook and

complete Questions 13-16 and Exercises 8-12.

Unit # 5 – Revenue & Expense Accounts

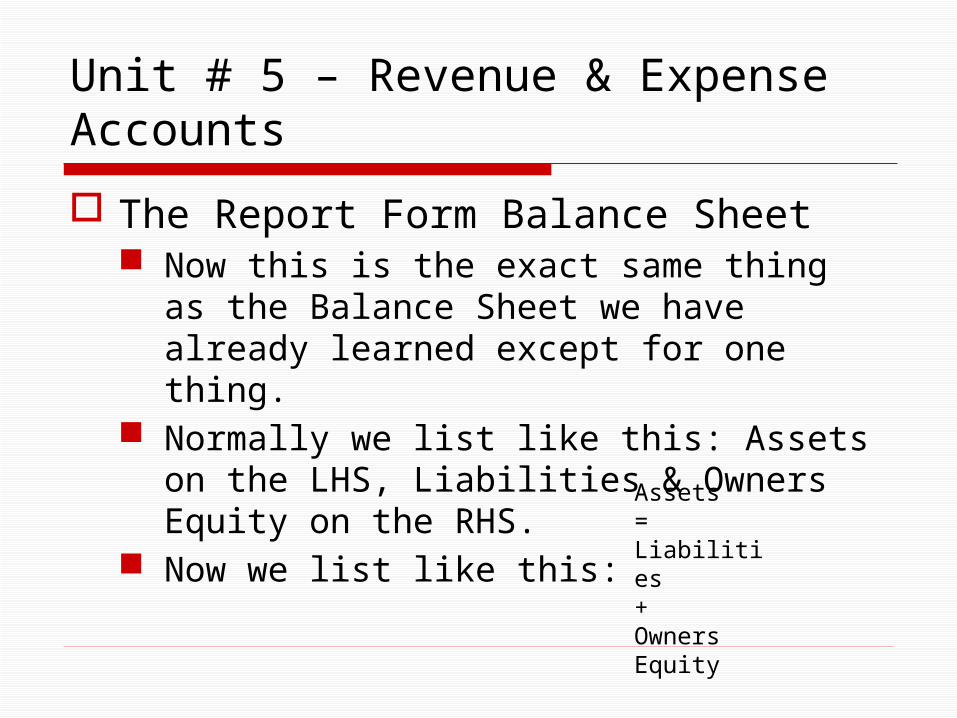

The Report Form Balance Sheet Now this is the exact same thing as the

Balance Sheet we have already learned except for one thing.

Normally we list like this: Assets on the LHS, Liabilities & Owners Equity on the RHS.

Now we list like this:Assets=Liabilities+Owners Equity

Unit # 5 – Revenue & Expense Accounts

The Owner’s Equity Account on the Balance Sheet!

RULE!!! ALWAYS Prepare the Income Statement before the Balance Sheet! This is because as Revenue increases (or

decreases) their will be a change in the Owner’s Equity section of the Balance Sheet (Net Worth of the Business)

Unit # 5 – Revenue & Expense Accounts

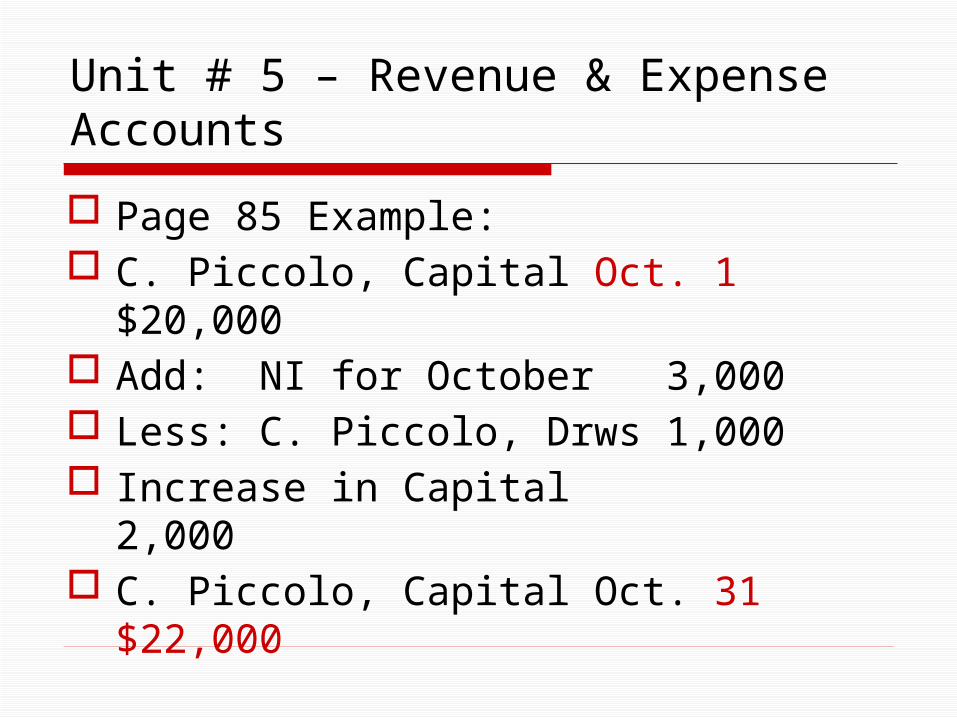

Page 85 Example: C. Piccolo, Capital Oct. 1 $20,000 Add: NI for October 3,000 Less: C. Piccolo, Drws 1,000 Increase in Capital 2,000 C. Piccolo, Capital Oct. 31 $22,000

Related Documents