I. CASE STATEMENT In light of the changes within the Philippine pharmaceutical industry, how do Unilab's research & development and innovation processes contribute to the company's market leadership? Accordingly, what improvements in research & development and innovation activities can the company implement to sustain its competitive edge? II. THE PHARMACEUTICAL INDUSTRY Overview of the Global Scenario The pharmaceutical industry is involved in developing, producing, and marketing drugs licensed for use as medications. Pharmaceutical companies are allowed to deal in generic and/or brand medications as well as medical devices. This industry is highly regulated, capital intensive, and is driven by large research and development expenditures. Most companies are primarily privately owned and are technologically sophisticated. With today’s dynamic and highly-regulated market, differentiation is becoming more important. Consumers are generally concerned about two criteria: (1) health outcomes and (2) affordability. Global industry data show that the pace of innovation remains slow: the long-term average is merely one new remedy drug a year per company. In relation to this, a significant factor that will fundamentally impact individual pharmaceutical companies in the near future is patent cliff 1 . The revenues of drugs having patents that will expire from 2010 to 2014 are about $89.5 billion USD 2 . Revenues hammered by patent cliffs can only be partially compensated by newly launched products. Price cuts and regulatory pressures also continue to limit growth. Governments around the world drive for solutions addressing treatments for nonlethal indications with large patient numbers, decreasing the profit margins of drug companies. Pharmaceutical companies are also being watched on their marketing practices, forcing them to adapt their promotional models. Moreover, protection and enforcement of IP rights remains a difficult issue in many emerging markets, with counterfeit and first-copy products prevalent. Consequently, the companies have adapted their strategies in that many have altered their drug portfolios from primary care driven blockbusters towards specialties such as oncology, immunology and inflammation, where the medical need is so high that prices are more easily accepted by the regulators. 1 Patent cliff describes what happens to the sales of an original drug when its protection (patent, regulatory, etc.) ceases: A dramatic drop in sales because of declining unit numbers, and a price erosion of up to 70 % within months. 2 In 2011, Lipitor, the world’s biggest selling drug, will go off-protection. Other drugs that lose protection in 2011 are Plavix (used to inhibit blood clots), Actos (diabetes), and Seroquel and Zyprexa (schizophrenia and bipolar disorder).

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

I. CASE STATEMENT

In light of the changes within the Philippine pharmaceutical industry, how do Unilab's research & development and innovation processes contribute to the company's market leadership?

Accordingly, what improvements in research & development and innovation activities can the company implement to sustain its competitive edge?

II. THE PHARMACEUTICAL INDUSTRY

Overview of the Global Scenario

The pharmaceutical industry is involved in developing, producing, and marketing drugs

licensed for use as medications. Pharmaceutical companies are allowed to deal in generic

and/or brand medications as well as medical devices. This industry is highly regulated,

capital intensive, and is driven by large research and development expenditures. Most

companies are primarily privately owned and are technologically sophisticated.

With today’s dynamic and highly-regulated market, differentiation is becoming more

important. Consumers are generally concerned about two criteria: (1) health outcomes and

(2) affordability. Global industry data show that the pace of innovation remains slow: the

long-term average is merely one new remedy drug a year per company. In relation to this, a

significant factor that will fundamentally impact individual pharmaceutical companies in the

near future is patent cliff1. The revenues of drugs having patents that will expire from 2010 to

2014 are about $89.5 billion USD2. Revenues hammered by patent cliffs can only be partially

compensated by newly launched products.

Price cuts and regulatory pressures also continue to limit growth. Governments around the

world drive for solutions addressing treatments for nonlethal indications with large patient

numbers, decreasing the profit margins of drug companies. Pharmaceutical companies are

also being watched on their marketing practices, forcing them to adapt their promotional

models. Moreover, protection and enforcement of IP rights remains a difficult issue in many

emerging markets, with counterfeit and first-copy products prevalent. Consequently, the

companies have adapted their strategies in that many have altered their drug portfolios from

primary care driven blockbusters towards specialties such as oncology, immunology and

inflammation, where the medical need is so high that prices are more easily accepted by the

regulators.

1 Patent cliff describes what happens to the sales of an original drug when its protection (patent, regulatory, etc.) ceases: A dramatic drop in sales because of declining unit numbers, and a price erosion of up to 70 % within months. 2 In 2011, Lipitor, the world’s biggest selling drug, will go off-protection. Other drugs that lose protection in 2011 are Plavix (used to inhibit blood clots), Actos (diabetes), and Seroquel and Zyprexa (schizophrenia and bipolar disorder).

01 SEP 2011

2 | P a g e

Philippine Pharmaceutical Industry

The Philippines is projected to be the 10th largest economy (and 9th largest pharmaceutical

market) in the Asia Pacific region by 2016. It also has one of the highest drug prices in the

world. The balance of pharmaceutical trade remains significantly negative. The Philippines is

heavily reliant on imports of finished medicaments and has little in the way of exports; thus,

the deficit will only widen in the forecast period.

The Philippine pharmaceutical industry is a monopolistically competitive market. It is

characterized by many sellers composed of both local and multinational companies, each

with a loyal set of customers and patient base depending on its product offerings. GSK, for

instance, dominates in the anti-asthma segment with patented drugs and innovative delivery

systems used in Ventolin and Seretide inhalers. Unilab, on the other hand, is at the forefront

of quality and affordable branded generics. The intensity of price competition in the local

pharmaceutical industry depends heavily on product differentiation. Products with existing

molecule or process patents can be priced at a premium since there are no substitutes for

these products. Research & development is often very costly to most multinational firms but

the patent protection provides the security of niche pricing and the guarantee of yielding

more profits in the long-run. Conversely, for off-patent molecules such as Paracetamol

(analgesic) or Carbocisteine (mucolytic), price competition is fierce. Since these products

have become highly commoditized due to the introduction of a multitude of branded

generics, their selling prices tend to drop to effectively compete with all the existing generic

counterparts in the market.

The controversial Cheaper Medicine Act has impacted the Philippines pharmaceutical

market whereby 200 drugs have seen price reductions by up to 50% since August 2009. On

June 6, 2008, former President Arroyo signed Republic Act No. 95023, known as the

Universally Accessible Cheaper and Quality Medicines Act of 2008. The law took effect on

August 15, 2009, and was intended to enhance access to generic drugs that will provide

cheaper but quality medicines to Filipinos. The law basically:

• allows the parallel importation of patented medicines from other countries where they are

more affordable

• bars the grant of new patents based only on newly-discovered uses of an ingredient of

an existing drug

• allows generics firms to test, produce, and register their versions of patented drugs

• allows the government use of patented drugs when the public interest is at stake

More importantly, the law cut in half the prices of essential medicines. The medicines

covered by price regulations are:

01 SEP 2011

3 | P a g e

• drugs or medicines indicated for treatment of chronic illnesses and life threatening conditions like diabetes, endocrine disorder, gastrointestinal disorders, peptic ulcer, cardiovascular diseases, hypertension, among others

• drugs or medicines indicated for prevention of diseases like vaccines, immunoglobulin and anti-serums

• drugs or medicines indicated for prevention of pregnancy such as oral contraceptives

• anesthetic agents

• intravenous fluids

Products Sold within the Industry

The total Philippine pharmaceutical market includes all products classified as:

Drugs. According to Philippine Republic Act 3720, drugs refer to medication or medicine or

other substance (either ethical or OTC) intended for use in the diagnosis, cure, mitigation,

treatment or prevention of disease in man and/or intended to affect the structure or any

function of the human body, but which does not include devices or their components, parts

and accessories. The common and widely used classification system is the Anatomical

Therapeutic Chemical Classification System or ATC system.

• Ethical or prescription drugs refer to drug products which are prescribed by a medical

practitioner and are only exclusively promoted ethically by drug companies via

deployment of professional medical representatives. Consumers are not able to

purchase medicines from the drugstore or hospital pharmacy without a supporting

prescription from a licensed doctor (by Philippine law).

• OTC or over-the-counter (also Proprietary ) drugs refer to drug products which can be

bought by the consumer in a drugstore, pharmacy, pharmacy-licensed supermarket or

grocery even without a doctor’s prescription. In contrast to ethical drugs, OTC products

may be advertised via print, radio and TV media.

Both ethical and OTC products are marketed either branded or unbranded3.

Non-drug. Non-drug items refer to nutritional and infant milk preparations, baby care,

cosmetics, diagnostic and other medical devices.

Market Players

The market is composed of a host of multinational companies (MNCs) & local emerging

firms, making the competitive landscape more intense than before. There are three kinds of

pharmaceutical companies:

� Innovators refer to the R&D-based multinational companies e.g. Pfizer, Glaxo

SmithKlline, AstraZeneca

3 Branded drugs refer to any drug manufactured and sold under the protection of a patent, brand name or trademark. Unbranded drugs basically refer to the generic equivalents of their original counterparts.

01 SEP 2011

4 | P a g e

� Branded generics include all local companies that market off-patent products using

their own brand names e.g. Unilab, Pascual

� Pure generics are companies that use a mother brand for all generics e.g. Ritemed,

Pharex

Figure 1 Top Pharmaceutical Companies in the Philippines

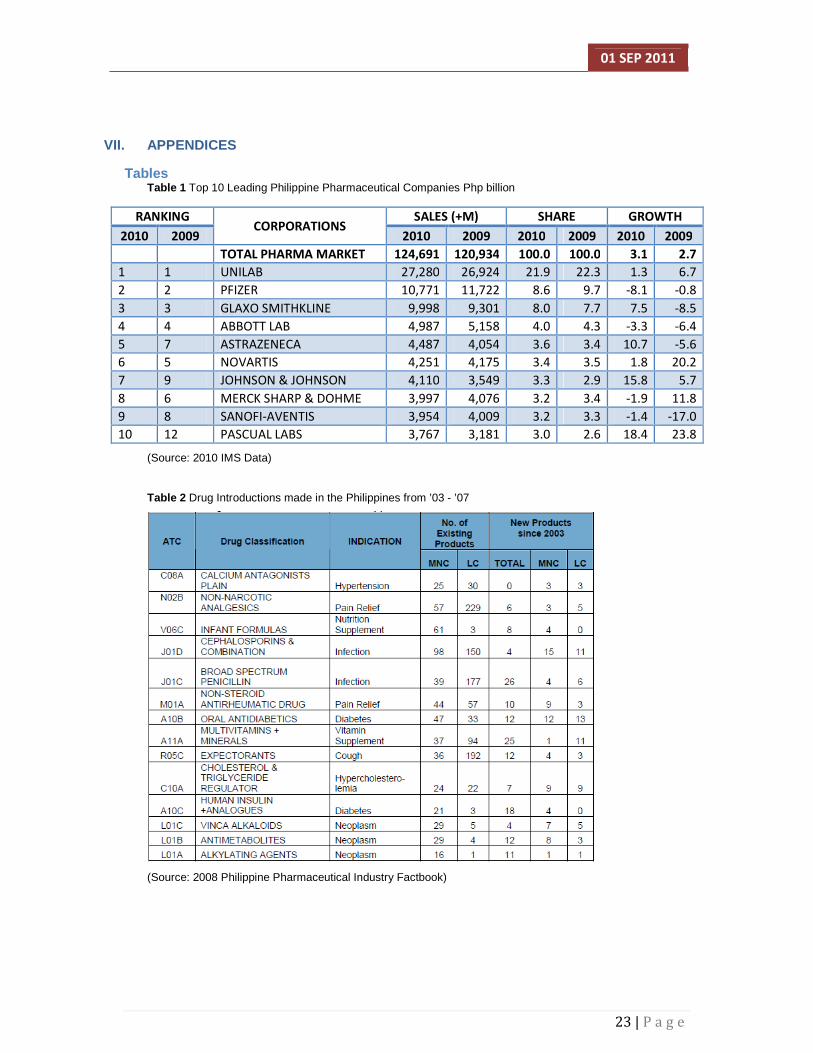

Figure 1 shows that the local industry has been consistently dominated by Unilab with a

commanding 22% market share. Unilab has ranked #1 in sales since 1998, and last year

attained PhP 27.3 B with a +1.7% growth. Following Unilab is Pfizer with 8.6% market share.

Pfizer, a US-based company with an extensive array of pharmaceutical products, lead the

cardiovascular, central nervous system, anti-infective, pain, urological, oncology and

ophthalmology markets but has been declining by -8.1% due to MDRP. Glaxo SmithKline

(GSK) comes in at 3rd with 8.0% market share driven by its megabrands Ventolin, Pritor and

Zantac. It has the largest MNC manufacturing facility in the country. Rounding up the list of

the leading pharmaceutical companies in the Philippines are Abbott, AstraZeneca, Novartis,

Johnson & Johnson, Sanofi-Aventis, Pascual Labs, and Boehringer Ingelheim. See Table 1

(Appendix) for further information.

Market Growth Drivers

• New Prod/SKU: Growth is driven by new product launches i.e. new brands, new line

extensions.

• Quantity: Growth is driven by increase in units or quantity sold.

• Price : Growth is driven by the increase in selling prices of products; conversely if

negative, there is a decrease in price.

• Combined Effect: Growth is driven by all three factors.

01 SEP 2011

5 | P a g e

Significant Market Movements

Figure 2 Philippine Pharmaceutical Market (Source: IMS 2010)

As seen in Figure 2, the market drastically slowed down to 2.6% growth in 2009, the first

time in the last decade. This is attributed to the full implementation of the Maximum Drug

Retail Price (MDRP) regulation, which reduced the selling price of most blockbuster drugs by

half and severely affected the sales performance of several multinational companies. Both

over-the-counter (OTC) and ethical businesses registered upbeat growths at 3.7% and 1.8%

respectively. The market has significant growths in pure and branded generics in terms of

sales. Even the multinationals are now encroaching into this market.

Figure 3 Innovators, Branded Generics and Pure Generics Growth Drivers (Source: IMS 2010)

Figure 3 shows that the OTC sector emerged as the growth driver (8.4%), despite price

increases, with new product introductions. The Ethical business declined, the first time for it

to have a negative growth in price. It had a significant drop in terms of peso sales and

growth (0.3%).

01 SEP 2011

6 | P a g e

Figure 4 Total Pharma Market: Innovators, Branded Generics and Pure Generics (Source: IMS 2010)

Figure 4 shows that branded generics and pure generics are growing, while innovators are

declining. The innovators seem to have suffered the blow of MDRP as their peso sales

declined due to price reduction which was not compensated by the increase in units. The top

MNCs such as Pfizer, GSK, Abbott, Astra Zeneca and Sanofi-Aventis are the market

decelerators due to the decline in sales of their leading brands such as Norvasc, Ventolin,

Klaricid, Plendil ER and Plavix, which are mostly MDRP-affected products.

Forecasts

The market will recover by 2011 with 7.7%, onwards to 7.8% until 2014. The market has

significant growths in pure and branded generics in terms of sales. Even the multinationals

are now encroaching into this market. Major MNCs will enter the branded generics market to

penetrate the lower middle class market. Much greater competition is anticipated in the

generics market, but still dominated by branded generics.

Industry Analysis: Porter’s Five Forces

Element Assessment

Competitive Rivalry

High Competition is considered aggressive with over 80 companies operating in the Philippines vying for the much-coveted share of prescriptions. The top 50 local pharmaceutical companies comprise 92.4% of the entire industry while the remaining balance is divided among several regional players and grassroots companies. For research-based multinational firms, however, there are gains generated by the first mover advantage by maximizing the use of patents. All in all, this makes the ever-changing business landscape competitive yet lucrative at the same time.

01 SEP 2011

7 | P a g e

Threat of Potential Entrants

Low for patented pharmaceuticals High for generics For patented drugs, barriers to entry restrict small players to participate in the cutthroat business environment. Barriers to entry include high R&D costs, patent limitations, and restrictive costs of innovating and testing new drugs through numerous clinical trials. For generics, it has become easier to penetrate the pharmaceutical industry via marketing of off-patent drugs as branded generics similar to the existing business models of Unilab and Pascual Labs. Also, the emergence of toll manufacturers eradicated the need for an in-house manufacturing facility. These toll manufacturers are able to produce large batches of medicines at cheaper costs.

Buyers' Bargaining Power

Low for patented pharmaceuticals High for generics Buyers have limited power when purchasing patented drugs since there are minimal substitutes compared to off-patent generics that proliferate in the market. Consumers of generics are very empowered and well-informed on the different illnesses and medications. Some would even self-medicate and purchase OTC medicines without consulting a physician. Moreover, there is a shift of power from producers to retailers. Trade outlets like Mercury Drug, Watsons, The Generics Pharmacy and Generika have the power to influence the buying habits of the public. These pharmacies can suggest to buyers which ones are better or cheaper.

Threat of Substitutes

Low within the patent period High after patent expiration For products under a patent, the producers are protected against threat of copycat substitutes within the patent period. However, once patent expires, it is expected that branded generic companies will reproduce those off-patent drugs. Moreover, there is a drastic increase in medicinal substitutes in forms of herbals, natural supplements, and wellness products that aim to encroach into the pharmaceutical market. These substitutes are a lot more affordable than chemically-made medicines and are aggressively promoted through tri-media efforts.

Suppliers' Bargaining Power

Low Pharmaceutical actives are becoming cheaper through the years with a slew of low-cost suppliers operating in large-scale manufacturing facilities in India and China. Also, with globalization, importing finished goods from a network of suppliers worldwide has become easier and more cost effective.

III. THE COMPANY

History

United Laboratories, Inc. (Unilab) was founded in 1945 by Jose Yao Campos as a small

drugstore in a street corner in the war-torn downtown Manila. The company offered quality

medicines at affordable prices. A few years later, the drugstore had quickly developed into a

pharmaceutical company, with a simple manufacturing setup and a modest marketing force

to promote and sell high quality and affordable medicines. By the end of 1950s, Unilab had

become the top pharmaceutical company in the Philippines. At about the same time, its

presence in Southeast Asia had begun to take shape, with the creation of marketing and

manufacturing tie-ups in the major countries in the region. Through the years, Unilab has

been able to solidify its position of leadership not only in the Philippines but in Southeast

Asia as well.

01 SEP 2011

8 | P a g e

Business

Unilab’s core business is to develop, manufacture, and market a wide range of prescription

and consumer health products covering all major therapeutic categories. Many of these

products are now leading brands in the Philippines. The company has a strong leading

presence in the region as a major provider of healthcare goods and services in several

countries – Indonesia, Thailand, Malaysia, Singapore, Hong Kong and Vietnam, among

others. Unilab operates in strategically located manufacturing facilities throughout Southeast

Asia, linked to extensive and expanding market coverage and technical support. The major

Unilab manufacturing complex is in Metro Manila, (the Philippines is the region's largest and

most significant pharmaceutical market) and has been cited by international health

organizations, as one of the finest is Asia.

UNILAB develops and markets a wide range of ethical and consumer products in the

following therapeutic segments:

Segments Anti-infective Endocrine Metabolic

Somatics Anti-Tuberculosis

Cough-Cold Dermatological

Cardiovascular Vitamins/Minerals

Gastrointestinal (GIT) Dietetics

Anti-Asthma Women's Health

Unilab’s famous brands include Alaxan, Biogesic, Ceelin, and Solmux, among others. For a

complete list, see: http://www.unilab.com.ph/about/brands.asp. See Appendix for a complete

list of Unilab’s divisions and subsidiaries and their corresponding products.

Product Acquisition

There are four ways that Unilab acquires its products. First, everything is done internally

such as development and manufacturing. Examples of these products are Biogesic and

Alaxan. Second, the company imports products as completely finished goods from other

countries and just markets them in the Philippines. These products are mostly antibiotics

and injectables. Third, Unilab imports products but packages them in the Philippines.

Examples for these are antibiotics and asthma inhalers. Fourth, the company imports raw

materials and then manufactures them locally through the toll manufacturers. Toll

manufacturing is an arrangement in which a company (which has specialized equipment,

e.g., Interphil in Canlubang) processes raw materials or semi-finished goods for Unilab. The

company’s toll-manufactured products include some of its Myra products and personal care

products. Unilab’s existing resources and facilities as well as a project’s overall

manufacturing costs are the important factors in determining its sourcing strategy.

01 SEP 2011

9 | P a g e

Performance

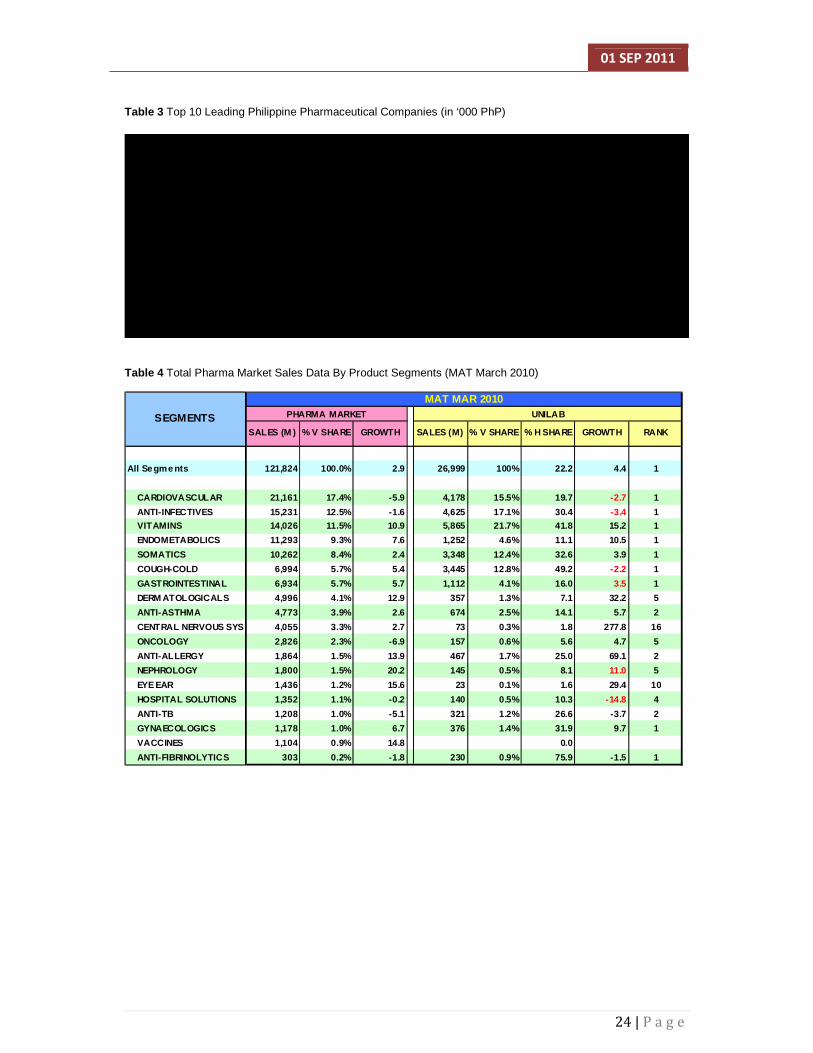

Unilab has been able to sustain its market leadership for the 2010. It has 22.2% market

share and has maintained leadership in both Ethical (16%) and Proprietary (36.2%) markets.

Its high performing brands include Myra E, Alaxan, Bioflu, and Diatabs. The company’s

growth drivers include New Products, Combined Effect, and Price. The company is #1 in the

following product categories: cardiovascular, anti-infectives, vitamins, endometabolics,

somatics, cough-colds, and gastrointestinal. It is second in anti-asthma and anti-allergies.

Some market analysts say that price is no longer a point of differentiation for Unilab with the

implementation of MDRP and the MNCs’ generic participation. The proliferation of many

generic companies poses stiff competition to Unilab.

Competitive Advantage

The company’s competitive advantage lies in its positioning: affordable quality products. Its

core strategy is to produce copycat or “me-too” products. When an innovator product is

nearing the patent expiration, this is when Unilab comes up with its own version of the said

product. Upon expiration, the company is ready to register its “me-too” product.

The company’s mantra is “We offer affordable, trusted, quality healthcare”: Affordable

because its product prices are 30% to 50% lower than that of the MNCs or innovator

companies; Trusted because the company’s established brands have been patronized by

consumers for more than 60 years already; and Quality because all of its products pass

through strict quality and manufacturing guidelines and procedures.

IV. UNILAB’S INNOVATION PROCESS

How the Company Views Innovation

According to Unilab CEO Clinton Campos-Hess, “Innovation is the cornerstone of our

strategy. We aspire to be the best provider of healthcare in Asia not merely to survive as a

business organization, but continue delivering value to our customers far better than

competition. To do this, we have to innovate and innovate well.”

The company defines innovation as “simply creating new businesses or new ways of doing

business that generate value for the customers and for the company. Moreover, aside from

simply introducing something new, it has to be accepted by the target users before it can be

considered an innovation.”

The company also views innovation as an integral component of its organization. This is

because “value is what drives business. The purpose of innovation is to constantly improve

the value provided to customers. In turn, it is the customers that will help convert

opportunities into sustainable business growth.”

01 SEP 2011

10 | P a g e

Innovative Activities

The following are examples of Unilab’s innovative activities:

• The company is one of the first Filipino companies to go overseas and tap new markets.

With innovative thinking and a lot of communication, Unilab has found ways to promote

its products overseas. Also, they are one of the first Southeast Asian companies to have

a world-class manufacturing facility. At first, the rationale was to serve migrant Filipino

workers who are accustomed to taking Unilab medicines. Later, it became another

revenue stream for the company and they were able to also maximize economies of

scale with the local manufacturing plant serving both domestic and international markets.

• Back in the day when doctors were still compounding, Unilab came out with fixed-dose

combinations which are bestselling products today such as Decolgen, Neozep, Alaxan.

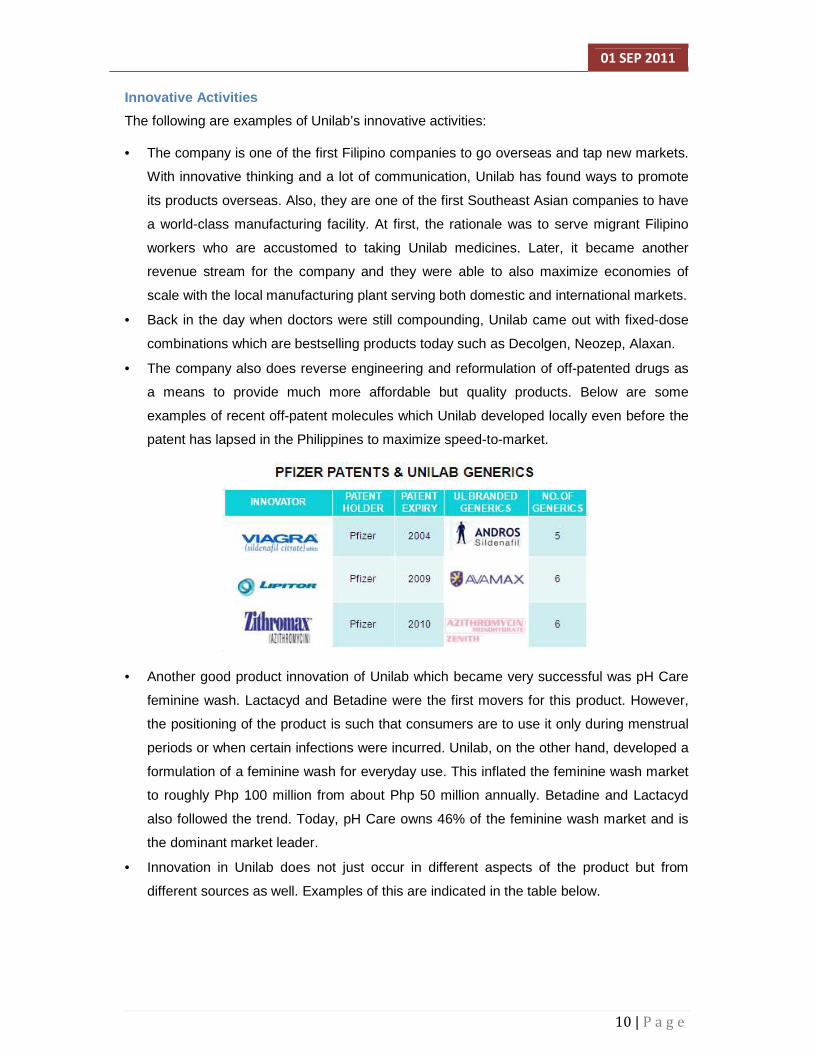

• The company also does reverse engineering and reformulation of off-patented drugs as

a means to provide much more affordable but quality products. Below are some

examples of recent off-patent molecules which Unilab developed locally even before the

patent has lapsed in the Philippines to maximize speed-to-market.

• Another good product innovation of Unilab which became very successful was pH Care

feminine wash. Lactacyd and Betadine were the first movers for this product. However,

the positioning of the product is such that consumers are to use it only during menstrual

periods or when certain infections were incurred. Unilab, on the other hand, developed a

formulation of a feminine wash for everyday use. This inflated the feminine wash market

to roughly Php 100 million from about Php 50 million annually. Betadine and Lactacyd

also followed the trend. Today, pH Care owns 46% of the feminine wash market and is

the dominant market leader.

• Innovation in Unilab does not just occur in different aspects of the product but from

different sources as well. Examples of this are indicated in the table below.

01 SEP 2011

11 | P a g e

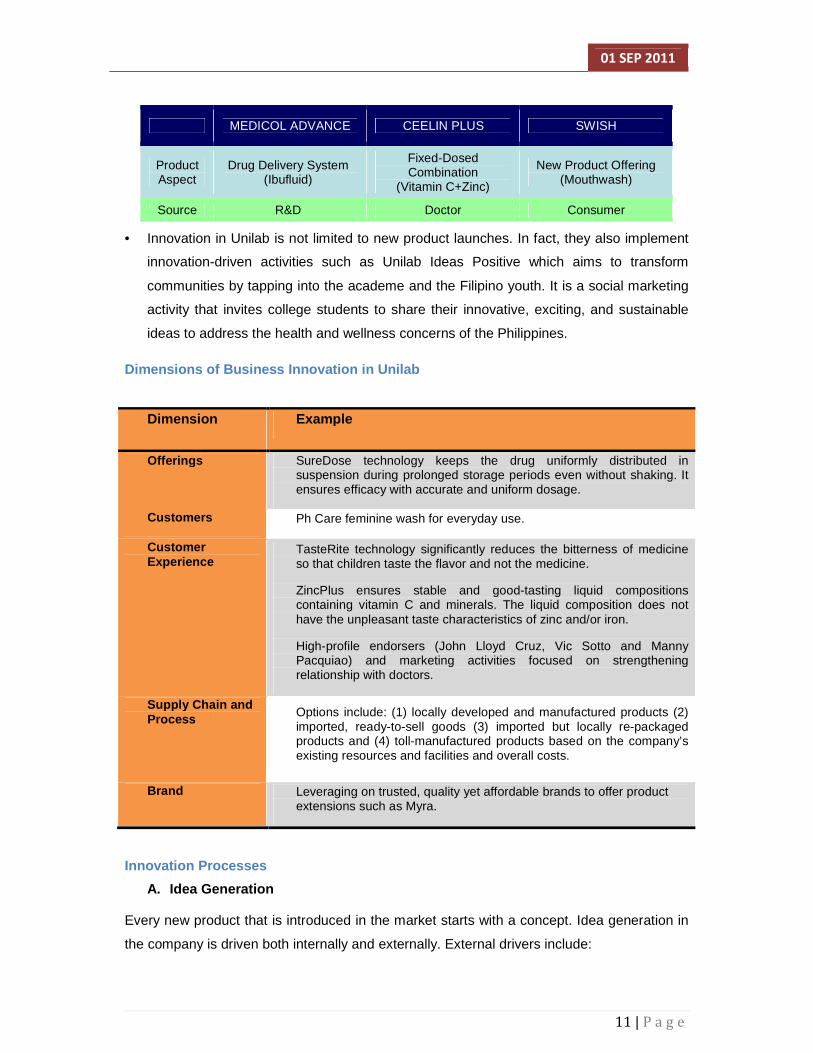

MEDICOL ADVANCE CEELIN PLUS SWISH

Product Aspect

Drug Delivery System (Ibufluid)

Fixed-Dosed Combination

(Vitamin C+Zinc)

New Product Offering (Mouthwash)

Source R&D Doctor Consumer

• Innovation in Unilab is not limited to new product launches. In fact, they also implement

innovation-driven activities such as Unilab Ideas Positive which aims to transform

communities by tapping into the academe and the Filipino youth. It is a social marketing

activity that invites college students to share their innovative, exciting, and sustainable

ideas to address the health and wellness concerns of the Philippines.

Dimensions of Business Innovation in Unilab

Dimension Example

Offerings SureDose technology keeps the drug uniformly distributed in suspension during prolonged storage periods even without shaking. It ensures efficacy with accurate and uniform dosage.

Customers Ph Care feminine wash for everyday use.

Customer Experience

TasteRite technology significantly reduces the bitterness of medicine so that children taste the flavor and not the medicine.

ZincPlus ensures stable and good-tasting liquid compositions containing vitamin C and minerals. The liquid composition does not have the unpleasant taste characteristics of zinc and/or iron.

High-profile endorsers (John Lloyd Cruz, Vic Sotto and Manny Pacquiao) and marketing activities focused on strengthening relationship with doctors.

Supply Chain and Process Options include: (1) locally developed and manufactured products (2)

imported, ready-to-sell goods (3) imported but locally re-packaged products and (4) toll-manufactured products based on the company’s existing resources and facilities and overall costs.

Brand Leveraging on trusted, quality yet affordable brands to offer product extensions such as Myra.

Innovation Processes

A. Idea Generation

Every new product that is introduced in the market starts with a concept. Idea generation in

the company is driven both internally and externally. External drivers include:

01 SEP 2011

12 | P a g e

• Fieldwork and interviews with doctors (i.e. Ceelin Plus was formulated as per the requests and inputs from pediatricians.)

• Focused group discussions with consumers (Conzace is a nutritional supplement that contains vitamins A, C, and E, and zinc. These nutrients act as antioxidants. A lot of consumers wanted the benefits of all these nutrients in just a single tablet.)

• Competitor benchmarking (Unilab released Growee, which is a growth stimulant, to compete with Cherifer.)

• FDA and other government regulations (Disudrin was reformulated by changing an active ingredient. This was done to conform to an FDA regulation.)

Internal drivers include:

• Top management during long-range planning.

• Marketing group which performs brainstorming sessions, business reviews, and sales trend analyses.

• Analytics and Business Intelligence Group which performs formal market research es and market gap analyses.

• R&D Group which is responsible for the product pipeline.

B. Product Concept Approval

Upon recognition of ideas and new business opportunities, the Corporate Product Board

(CPB) is responsible for the approval of new product candidates or ideas for product

improvements. The board will approve ideas that would help Unilab achieve its medium and

long-term sales, market share, and growth objectives.

C. Business Plan Development

A feasibility study will then be conducted by both Marketing and Analytics groups which

involves a thorough evaluation of the ff:

• Market potential & pricing strategy - an in-depth analysis of the IMS sales, prescription data, and the market survey results is conducted to fully assess the market potential of the new product. Pricing strategy, 5-year product sales forecast, and market share objectives are also agreed upon.

• Medical usefulness - Medical Affairs prepares the Medical Position Paper (MPP) to rate if the product is of “high interest”, “interest”, “conditional interest”, or of “no interest”. The required technical documents are: acute and chronic toxicity studies, reproductive and teratogenicity studies, carcinogenicity studies, bioequivalence and bioavailability, and efficacy and safety data.

• Patent situation - R&D and Legal conduct a patent check report of the new product. A “clear” patent status ensures no infringement cases with any of the existing pharmaceutical products available in the local market. In cases where there is a process patent, R&D will consider developing or using other procedures or both, so as not to infringe on the existing process patent.

• Initial technical and manufacturing feasibility - a clearance report is conducted from R&D, Quality Assurance & Chemistry (QA&C), and Manufacturing regarding Unilab’s capability in developing, handling, and producing the new product.

01 SEP 2011

13 | P a g e

• Distribution inputs and product packaging - based on inputs from R&D, Business Development Group (BDG), and Distribution, information regarding handling, storage facilities, and the new product packaging system is consolidated.

• Regulatory evaluation – inputs is solicited from the Office of Regulatory Affairs (ORA) regarding pertinent regulatory matters/issues concerning the new product.

• Initial product costing & financial evaluation - Based on all information, Finance computes for initial product cost and the 5-year financial evaluation. Also, the initial financial feasibility report is conducted.

D. Business Plan Approval

The Corporate Product Board (CPB) together with Mancom is responsible for approval of the

business plan. Once approved, a cross-functional team will be convened to set up initial

timelines and firm up critical project milestones.

Based on the generated inputs from the various support areas, CPB is responsible for

approval of the business plan. The CPB-approved business plan includes product

development milestones with timelines. These are used as standard of performance for the

project team’s Key Result Areas (KRAs). The same milestones and timelines also serve as

partial basis for the individual team member’s Performance Management System (PMS).

Upon approval of the business plan, a cross-functional project team is organized. Its first

agenda is to firm up plans for the new product. The project team then meets regularly to

pursue the critical activities for the product’s timely development and eventual market

launch.

E. Product Development

It is best to develop and manufacture new products locally. However, in cases where there is

a patent constraint, or Unilab lacks the necessary facilities or technology to manufacture, or

when it is not economically feasible for Unilab to manufacture locally, then importation of

non-infringing products may be considered.

R&D is responsible for locally manufactured products. On the other hand, BDG is

responsible for importing products as completely finished goods.

Corporate Culture Towards Innovation

A. Imperatives of Innovation

To further concretize the company’s plans to employ innovation as a strategy, management

inculcates to the entire organization what they call “The Seven Imperatives of Innovation”

01 SEP 2011

14 | P a g e

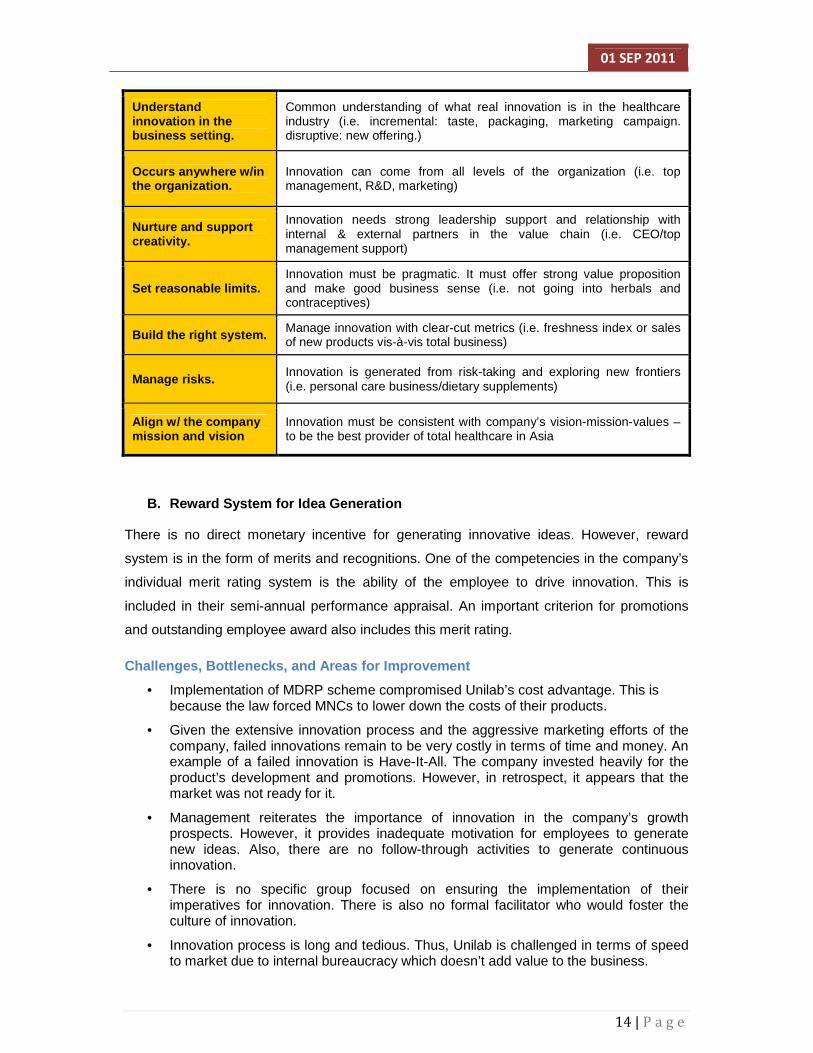

Understand innovation in the business setting.

Common understanding of what real innovation is in the healthcare industry (i.e. incremental: taste, packaging, marketing campaign. disruptive: new offering.)

Occurs anywhere w/in the organization.

Innovation can come from all levels of the organization (i.e. top management, R&D, marketing)

Nurture and support creativity.

Innovation needs strong leadership support and relationship with internal & external partners in the value chain (i.e. CEO/top management support)

Set reasonable limits. Innovation must be pragmatic. It must offer strong value proposition and make good business sense (i.e. not going into herbals and contraceptives)

Build the right system. Manage innovation with clear-cut metrics (i.e. freshness index or sales of new products vis-à-vis total business)

Manage risks. Innovation is generated from risk-taking and exploring new frontiers (i.e. personal care business/dietary supplements)

Align w/ the company mission and vision

Innovation must be consistent with company’s vision-mission-values – to be the best provider of total healthcare in Asia

B. Reward System for Idea Generation

There is no direct monetary incentive for generating innovative ideas. However, reward

system is in the form of merits and recognitions. One of the competencies in the company’s

individual merit rating system is the ability of the employee to drive innovation. This is

included in their semi-annual performance appraisal. An important criterion for promotions

and outstanding employee award also includes this merit rating.

Challenges, Bottlenecks, and Areas for Improvement

• Implementation of MDRP scheme compromised Unilab’s cost advantage. This is because the law forced MNCs to lower down the costs of their products.

• Given the extensive innovation process and the aggressive marketing efforts of the company, failed innovations remain to be very costly in terms of time and money. An example of a failed innovation is Have-It-All. The company invested heavily for the product’s development and promotions. However, in retrospect, it appears that the market was not ready for it.

• Management reiterates the importance of innovation in the company’s growth prospects. However, it provides inadequate motivation for employees to generate new ideas. Also, there are no follow-through activities to generate continuous innovation.

• There is no specific group focused on ensuring the implementation of their imperatives for innovation. There is also no formal facilitator who would foster the culture of innovation.

• Innovation process is long and tedious. Thus, Unilab is challenged in terms of speed to market due to internal bureaucracy which doesn’t add value to the business.

01 SEP 2011

15 | P a g e

• Another bottleneck pertains to hierarchy of approvers. Too many approvals are required prior to implementation of a certain project. According to the resource person, Unilab has this culture wherein the processes are slow even with regular day-to-day operations. For example, if one requests to purchase a particular product, it will usually take 3 weeks just to be approved. As per approval of budgets, projects above Php 1M has to be approved by several managers, VP for finance, as well as the company’s president. This is a tedious process because there are a lot of Php 1M projects. Also, there is redundancy because the budget for a certain division is already approved at the beginning of the calendar year.

• Roles of cross-functional teams are not well-defined. This results in either neglect or redundancy of responsibilities.

• Corporate moral conviction also somehow hinders innovation. For example, contraceptive industry is a growing market. However, Unilab will definitely not tap this market because it is against the moral principles of the CEO. The marketing people already did an extensive proposal for contraceptives, but management still disapproved.

V. UNILAB’S RESEARCH AND DEVELOPMENT MANAGEMENT

Research and Development Purpose

As mentioned earlier, Unilab maintains strategically located manufacturing facilities all over

Southeast Asia. As disclosed, each regional Unilab unit with a manufacturing facility has its

own R&D group; otherwise, they only have a marketing department to handle business in

the country where they operate in. Among the countries with manufacturing and R&D units

include the Philippines, Vietnam and Indonesia.

The main purpose of having an R&D group for each regional Unilab unit is to allow each unit

to have flexibility and the autonomy in deciding what products to launch based on the market

needs, or what is applicable to the country.

In this way, specific local market needs are properly identified and henceforth, addressed;

thus, giving support and further expanding Unilab’s business.

Research and Development Activities

Unlike other larger pharmaceutical companies such as Pfizer, Unilab’s R&D is more focused

on improving product formulation, delivery, and format of off-patent drugs, rather than new

drug discovery.

Common and main function therefore of all regional R&D units is to facilitate the formulation,

and its improvement thereof, of off patent drugs, and ensure compliance to standards of

stability, efficacy and safety. Some of the specific tasks of the R&D Group include raw

material sourcing, development of product candidate, stability testing, and process validation

development.

01 SEP 2011

16 | P a g e

Most R&D’s projects are initiated by marketing (from generic products/basis is what is

available in the market) although it can research and develop on their own based on new

ingredient available in the scientific communities: natural products backed by clinical

evidence.

Meanwhile, activities involving development of new and innovative products are undertaken

in Shanghai, China where Unilab and an affiliate company – Shanghai United Cell

Biotechnology Co. Ltd., jointly operate a biotechnology plant.

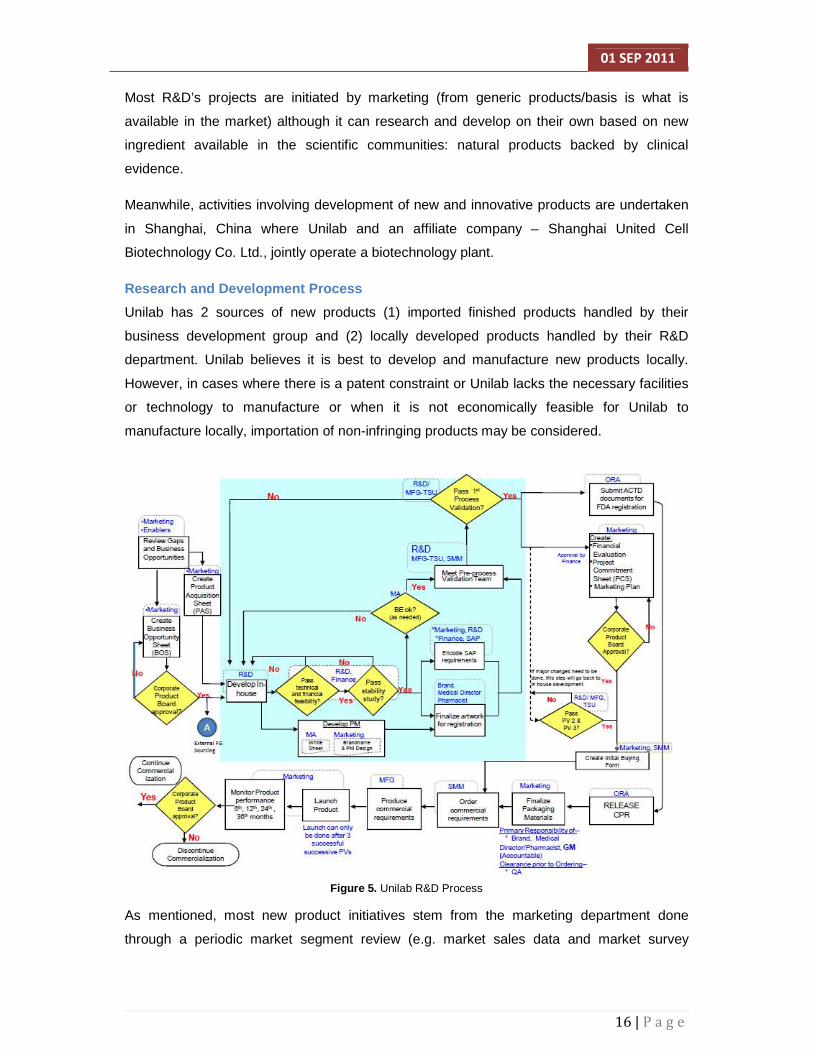

Research and Development Process

Unilab has 2 sources of new products (1) imported finished products handled by their

business development group and (2) locally developed products handled by their R&D

department. Unilab believes it is best to develop and manufacture new products locally.

However, in cases where there is a patent constraint or Unilab lacks the necessary facilities

or technology to manufacture or when it is not economically feasible for Unilab to

manufacture locally, importation of non-infringing products may be considered.

Figure 5. Unilab R&D Process

As mentioned, most new product initiatives stem from the marketing department done

through a periodic market segment review (e.g. market sales data and market survey

01 SEP 2011

17 | P a g e

results) from which Unilab form strategies (business plan) for existing business and create a

line-up of new product candidates that will fill up identified market opportunities.

The business plan includes profit and loss plan (with 5-year sales forecast, pricing strategy,

cost of goods (COG), promotional strategies, product positioning and expenses), brand-

name candidates and final divisional assignee. The plan also includes product development

milestones with timelines, which are used as standard of performance for the project team’s

key result area. The same milestones and timelines also serve as partial basis for the

individual team member’s performance appraisal. Once business plan is approved R&D

activities start.

R&D forms part of a cross-functional project team whose first agenda is to firm-up plans for

the new product. The team involves not only the research group but also includes finance,

marketing, manufacturing and product sourcing. The project team then meets regularly to

pursue the critical activities for the product’s timely development and eventual market

launch. Pre-marketing activities are also initiated concurrently with product development

(brand name approval, market research study and packaging prototype development). R&D

activities end once new products passed the process validations.

Research and Development Metrics

The Research & Development team of Unilab is evaluated based on the corporate balanced scorecard approach focusing on four key result areas:

Figure 6 Unilab Balanced Scorecard

• Financials (20%) Delivering total business (sales performance of new products) and managing cost judiciously to improve bottom line (manage R&D spending)

• Customer (30%) Completing the development of planned products in the pipeline on time (product's efficacy, safety, stability etc should pass internal standards)

01 SEP 2011

18 | P a g e

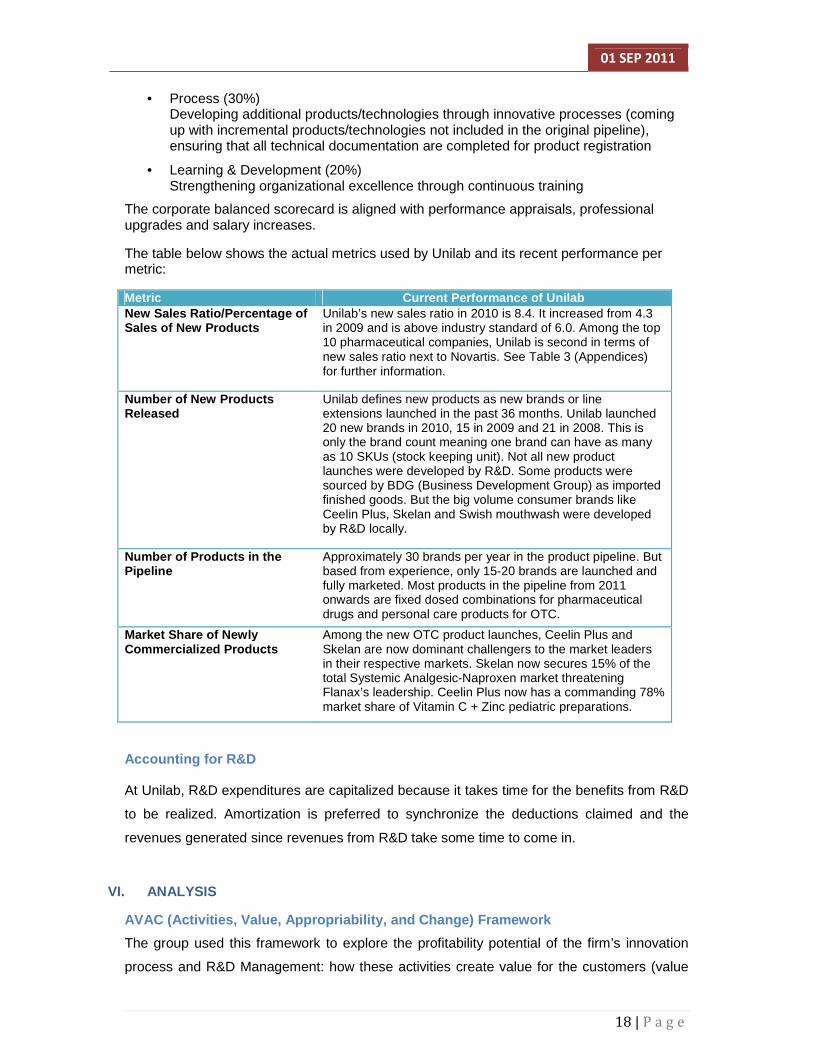

• Process (30%) Developing additional products/technologies through innovative processes (coming up with incremental products/technologies not included in the original pipeline), ensuring that all technical documentation are completed for product registration

• Learning & Development (20%) Strengthening organizational excellence through continuous training

The corporate balanced scorecard is aligned with performance appraisals, professional upgrades and salary increases.

The table below shows the actual metrics used by Unilab and its recent performance per metric:

Metric Current Performa nce of Unilab New Sales Ratio/Percentage of Sales of New Products

Unilab’s new sales ratio in 2010 is 8.4. It increased from 4.3 in 2009 and is above industry standard of 6.0. Among the top 10 pharmaceutical companies, Unilab is second in terms of new sales ratio next to Novartis. See Table 3 (Appendices) for further information.

Number of New Products Released

Unilab defines new products as new brands or line extensions launched in the past 36 months. Unilab launched 20 new brands in 2010, 15 in 2009 and 21 in 2008. This is only the brand count meaning one brand can have as many as 10 SKUs (stock keeping unit). Not all new product launches were developed by R&D. Some products were sourced by BDG (Business Development Group) as imported finished goods. But the big volume consumer brands like Ceelin Plus, Skelan and Swish mouthwash were developed by R&D locally.

Number of Products in the Pipeline

Approximately 30 brands per year in the product pipeline. But based from experience, only 15-20 brands are launched and fully marketed. Most products in the pipeline from 2011 onwards are fixed dosed combinations for pharmaceutical drugs and personal care products for OTC.

Market Share of Newly Commercialized Products

Among the new OTC product launches, Ceelin Plus and Skelan are now dominant challengers to the market leaders in their respective markets. Skelan now secures 15% of the total Systemic Analgesic-Naproxen market threatening Flanax’s leadership. Ceelin Plus now has a commanding 78% market share of Vitamin C + Zinc pediatric preparations.

Accounting for R&D

At Unilab, R&D expenditures are capitalized because it takes time for the benefits from R&D

to be realized. Amortization is preferred to synchronize the deductions claimed and the

revenues generated since revenues from R&D take some time to come in.

VI. ANALYSIS

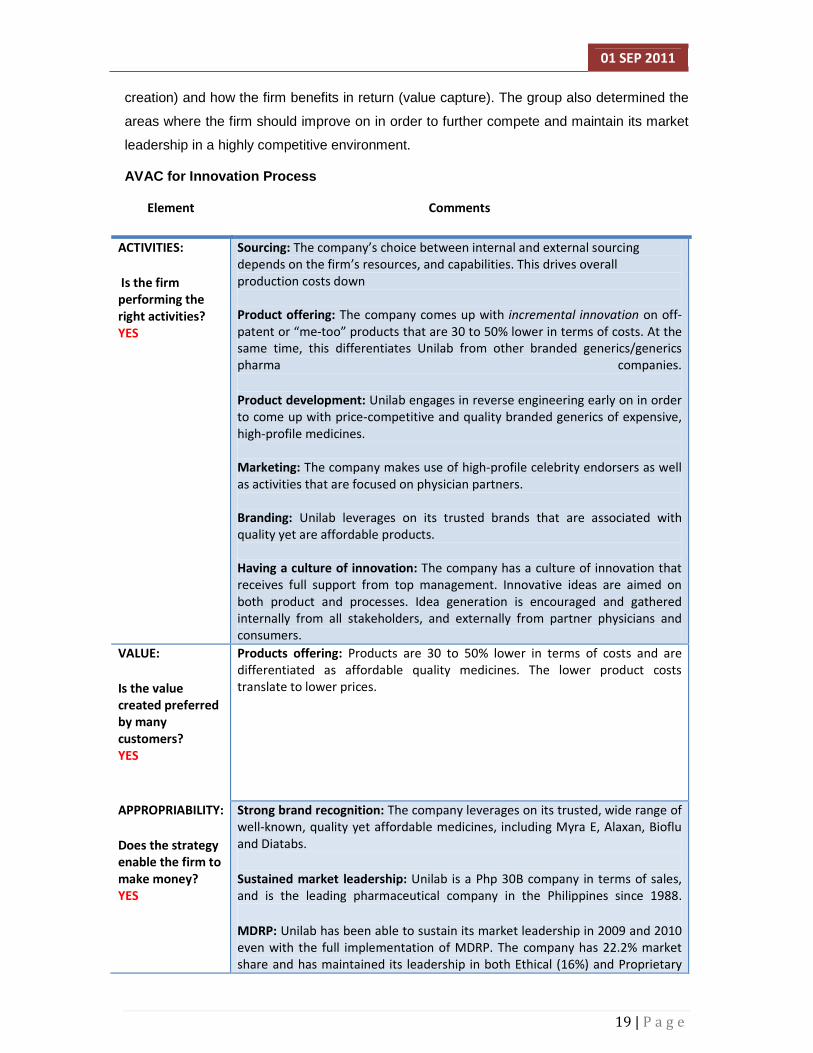

AVAC (Activities, Value, Appropriability, and Chang e) Framework

The group used this framework to explore the profitability potential of the firm’s innovation

process and R&D Management: how these activities create value for the customers (value

01 SEP 2011

19 | P a g e

creation) and how the firm benefits in return (value capture). The group also determined the

areas where the firm should improve on in order to further compete and maintain its market

leadership in a highly competitive environment.

AVAC for Innovation Process

Element Comments

ACTIVITIES:

Is the firm

performing the

right activities?

YES

Sourcing: The company’s choice between internal and external sourcing

depends on the firm’s resources, and capabilities. This drives overall

production costs down

Product offering: The company comes up with incremental innovation on off-

patent or “me-too” products that are 30 to 50% lower in terms of costs. At the

same time, this differentiates Unilab from other branded generics/generics

pharma companies.

Product development: Unilab engages in reverse engineering early on in order

to come up with price-competitive and quality branded generics of expensive,

high-profile medicines.

Marketing: The company makes use of high-profile celebrity endorsers as well

as activities that are focused on physician partners.

Branding: Unilab leverages on its trusted brands that are associated with

quality yet are affordable products.

Having a culture of innovation: The company has a culture of innovation that

receives full support from top management. Innovative ideas are aimed on

both product and processes. Idea generation is encouraged and gathered

internally from all stakeholders, and externally from partner physicians and

consumers.

VALUE:

Is the value

created preferred

by many

customers? YES

Products offering: Products are 30 to 50% lower in terms of costs and are

differentiated as affordable quality medicines. The lower product costs

translate to lower prices.

APPROPRIABILITY:

Does the strategy

enable the firm to

make money? YES

Strong brand recognition: The company leverages on its trusted, wide range of

well-known, quality yet affordable medicines, including Myra E, Alaxan, Bioflu

and Diatabs.

Sustained market leadership: Unilab is a Php 30B company in terms of sales,

and is the leading pharmaceutical company in the Philippines since 1988.

MDRP: Unilab has been able to sustain its market leadership in 2009 and 2010

even with the full implementation of MDRP. The company has 22.2% market

share and has maintained its leadership in both Ethical (16%) and Proprietary

01 SEP 2011

20 | P a g e

(36.2%) markets.

CHANGES:

Does the strategy

take advantage of

change (present

or future)? YES

Industry changes include the full implementation of MDRP and the entry of

MNCs in the generics market.

Product and process innovations play a big factor in maintaining the

company’s positioning as “affordable, quality me-too drugs.” It also helped the

company sustain sales and market leadership despite the implementation of

MDRP and the entry of MNCs in the generics market.

Rigorous marketing campaign through high-profile celebrity endorsers and

partner physicians were the company’s primary weapons against emerging

competitors in the branded generics market.

Company leverages on its trusted brand to get ahead of competitors.

Though expiration of high-profile patented drugs would be a welcome addition

to the company’s arsenal, the company’s growing consumer product segment

is insurance once the pipeline dries out.

AVAC for R&D Management

Element Comments

ACTIVITIES:

Is the firm

performing the

right activities?

YES

Low cost & better pricing: With the help of R&D, COG ranges from 30% to

50% of Net Price, effectively enabling to price its products lower by 5% to 50%

versus competitor brands.

Differentiation: Unilab is active in improving the formulation of existing drugs,

as well as their formats. It is also able to reformulate and combine medicines

i.e. “Alaxan” (Ibuprofen + Paracetamol). It also does research and develops

new formulation for its own based on new ingredient available in scientific

communities.

Reaching more customers: Unilab’s R&D has developed and currently employs

various technologies used to cater to the unique needs of different types of

customers.

On improving position vis-a-vis coopetitor: At present, Unilab’s R&D does not

form partnerships with its competitors, although, it collaborates with other

pharmaceutical or research companies from abroad.

VALUE:

Is the value

created preferred

by many

Many customers prefer the value created by Unilab over competition: Unilab is able to sustain its market leadership from 2009-2010.

Customers of Unilab are valuable: Number one in most therapeutic categories i.e. cardio, antibiotics, vitamins.

01 SEP 2011

21 | P a g e

customers? YES

See Table 4 (Appendices) for further information. Its banner brands are the most prescribed products in their segments next to

generics. See Table 5 (Appendices) for further information.

Unilab is currently filling out some nearby white spaces: For growth and economies of scope, Unilab is actively pursuing one of its long-

term strategies: related diversification. Unilab is pursuing other forms of

businesses that might not be of the pharmaceutical kind, but should be related

to the core business of healthcare and wellness. In line with this, Unilab is

developing ways to cater the unserved market for Personal Care and Dietary

Supplements.

APPROPRIABILITY:

Does the strategy

enable the firm to

make money? YES

Superior position vis-à-vis its competitors: Unilab has been able to sustain its

market leadership. It has also maintained its leadership in both Ethical (16%)

and Proprietary (36.2%) markets.

Exploits its position vis-à-vis its competitors and customer benefits: Unilab is

the most trusted branded generic drugs. Its products are affordable, of quality

and trusted by consumers. With this, Unilab ensure to capture new and

untouched niche and market by offering new products and heightened R&D

efforts.

Have the right resources/capabilities, including complementary assets: Some

patented imported finished/bulk products are also marketed by Unilab

through a license agreement with the patent owner. These products are called

Alliance Products and usually have higher prices and cost but strategically

enhance the acceptability of the other products of Unilab. Foreign partners,

choose Unilab because it is the leader in the market and trusted by consumers.

Not difficult to imitate, in terms of R&D activities: Many players in the

Philippine pharmaceutical industries can easily imitate Unilab's strategies of

cost leadership and differentiation.

CHANGES:

Does the strategy

take advantage of

change (present

or future)? YES

Takes advantage of new ways to ensure value creation and value capture:

Unilab develops new processes to be able to offer drugs at a cheaper price

with the same level of quality.

Maximizes distinctive capabilities: Through its extensive experience and large

network, Unilab is able to look for products which are in demand in the

market, then offer these products at a lower cost while still maintaining the

level of quality that is warranted by the market.

Acts on competitors’ reactions: Unilab is always on a look for new drugs that

could be offered through reverse engineering and reformulating them at a

lower costing advantage.

Utterback - Abernathy (UA) Model

This model shows that product innovation, process innovation, competitive environment, and

organizational structure are all interacting and closely linked.

The group has determined that the company operates within the Specific Phase. In this

phase, competition shifted differentiation to product performance and costs after the

01 SEP 2011

22 | P a g e

appearance of a dominant design. The company has a clear picture of market segments and

has concentrated on serving specific customers. Manufacturing uses highly specialized

equipment. Commoditization has taken place such that the bargaining powers of both

suppliers and customers have increased.

Variable Unilab, as it relates to Local Industry

Comments

Type of Innovation

Specific Unilab is NOT an innovator; it focuses on incremental product and process innovations to offer affordable, quality me-too drugs.

Nature of Products

Specific Branded generics: Unilab offers off-patent products but it leverages on its reputation as a trusted brand.

Production Processes

Specific Efficient, capital intensive but rigid. The company’s existing resources and facilities as well as overall costs are the important factors in determining whether to source internally or externally.

R&D Specific Focuses on incremental product and process innovations to maintain quality. This complements types of innovations being pursued.

Plant Specific Large-scale, highly specific to particular products. Unilab’s existing resources and facilities as well as overall costs are the main factors in determining which products to grow internally or source externally.

Competitors Transition / Specific

There are a lot of competitors, but Unilab is the market leader since 1988.

Basis of Competition

Specific Wide range of affordable, quality products is Unilab's main competitive advantage. Upon implementation of MDRP, price has become the basis of competition. Also, MNCs are starting to enter the generics market. Price has become a market decelerator in 2010 due to the reduction in prices of most big volume brands;

Vulnerability of Market Leaders

Specific Unilab is the market leader. Threats include entry of MNC that can offer higher quality and cheap branded generic products or substitutes. Also, with the declining number of new patented disruptive products, product pipeline may eventually dry out. Hence, the company has to look for new market segments to serve.

01 SEP 2011

23 | P a g e

VII. APPENDICES

Tables Table 1 Top 10 Leading Philippine Pharmaceutical Companies Php billion

RANKING CORPORATIONS

SALES (+M) SHARE GROWTH

2010 2009 2010 2009 2010 2009 2010 2009

TOTAL PHARMA MARKET 124,691 120,934 100.0 100.0 3.1 2.7

1 1 UNILAB 27,280 26,924 21.9 22.3 1.3 6.7

2 2 PFIZER 10,771 11,722 8.6 9.7 -8.1 -0.8

3 3 GLAXO SMITHKLINE 9,998 9,301 8.0 7.7 7.5 -8.5

4 4 ABBOTT LAB 4,987 5,158 4.0 4.3 -3.3 -6.4

5 7 ASTRAZENECA 4,487 4,054 3.6 3.4 10.7 -5.6

6 5 NOVARTIS 4,251 4,175 3.4 3.5 1.8 20.2

7 9 JOHNSON & JOHNSON 4,110 3,549 3.3 2.9 15.8 5.7

8 6 MERCK SHARP & DOHME 3,997 4,076 3.2 3.4 -1.9 11.8

9 8 SANOFI-AVENTIS 3,954 4,009 3.2 3.3 -1.4 -17.0

10 12 PASCUAL LABS 3,767 3,181 3.0 2.6 18.4 23.8

(Source: 2010 IMS Data)

Table 2 Drug Introductions made in the Philippines from ’03 - ’07

(Source: 2008 Philippine Pharmaceutical Industry Factbook)

01 SEP 2011

24 | P a g e

Table 3 Top 10 Leading Philippine Pharmaceutical Companies (in ‘000 PhP)

RANK

MAT DEC 2010 MAT DEC 2009 MAT DEC 2010 MAT DEC 2009 DEC 2010 DEC 2009

Total Pharma Market 124,690,636 120,934,444 7,474,457 3 ,591,916 6.0 3.0

1 UNITED LAB 27,279,722 26,923,693 2,288,899 1,163,900 8.4 4.32 PFIZER INC 10,770,852 11,721,786 330,723 65,978 3.1 0.63 GLAXO SMITHKLINE 9,998,447 9,300,694 136,530 93,055 1.4 1.04 ABBOTT LAB 4,986,997 5,157,830 72,768 43,410 1.5 0.85 ASTRAZENECA 4,486,611 4,053,961 49,280 5,318 1.1 0.16 NOVARTIS 4,251,368 4,174,727 767,954 330,350 18.1 7.97 JOHNSON 4,110,058 3,548,562 115,390 104,791 2.8 3.08 MERCK SHARP&DOHME 3,997,381 4,075,744 286,011 165,705 7.2 4.19 SANOFI-AVENTIS 3,953,615 4,008,542 246,678 252,633 6.2 6.310 PASCUAL LABS 3,767,433 3,180,867 229,685 97,795 6.1 3.1

MAT DEC 2010

PESOS (+000)

NEW PRODUCTS

NEW BRAND INDEX

MAT CORPORATIONS TOTAL PHARMA MARKET

Table 4 Total Pharma Market Sales Data By Product Segments (MAT March 2010)

SALES (M ) % V SHARE GROWTH SALES (M) % V SHARE % H SHARE GROWTH RANK

All Segme nts 121,824 100.0% 2.9 26,999 100% 22.2 4.4 1

CARDIOVASCULAR 21,161 17.4% -5.9 4,178 15.5% 19.7 -2.7 1

ANTI-INFECTIVES 15,231 12.5% -1.6 4,625 17.1% 30.4 -3.4 1

VITAMINS 14,026 11.5% 10.9 5,865 21.7% 41.8 15.2 1

ENDOMETABOLICS 11,293 9.3% 7.6 1,252 4.6% 11.1 10.5 1

SOMATICS 10,262 8.4% 2.4 3,348 12.4% 32.6 3.9 1

COUGH-COLD 6,994 5.7% 5.4 3,445 12.8% 49.2 -2.2 1

GASTROINTESTINAL 6,934 5.7% 5.7 1,112 4.1% 16.0 3.5 1

DERM ATOLOGICALS 4,996 4.1% 12.9 357 1.3% 7.1 32.2 5

ANTI-ASTHMA 4,773 3.9% 2.6 674 2.5% 14.1 5.7 2

CENTRAL NERVOUS SYS 4,055 3.3% 2.7 73 0.3% 1.8 277.8 16

ONCOLOGY 2,826 2.3% -6.9 157 0.6% 5.6 4.7 5

ANTI-ALLERGY 1,864 1.5% 13.9 467 1.7% 25.0 69.1 2

NEPHROLOGY 1,800 1.5% 20.2 145 0.5% 8.1 11.0 5

EYE EAR 1,436 1.2% 15.6 23 0.1% 1.6 29.4 10

HOSPITAL SOLUTIONS 1,352 1.1% -0.2 140 0.5% 10.3 -14.8 4

ANTI-TB 1,208 1.0% -5.1 321 1.2% 26.6 -3.7 2

GYNAECOLOGICS 1,178 1.0% 6.7 376 1.4% 31.9 9.7 1

VACCINES 1,104 0.9% 14.8 0.0

ANTI-FIBRINOLYTICS 303 0.2% -1.8 230 0.9% 75.9 -1.5 1

SEGMENTS

MAT MAR 2010PHARMA MARKET UNILAB

01 SEP 2011

25 | P a g e

Table 5 Prescription Share by Corporation.

NO. OF Rx % SHTOTAL PHARMA 179,383,421 100.00 GENERIC 30,767,619 17.15 UNITED LAB 29,587,234 16.49 GLAXO SMITHKLINE 15,315,071 8.54 PFIZER INC 11,150,744 6.22 MERCK SHARP&DOHME 5,130,037 2.86 ABBOTT LAB 4,875,147 2.72 BOE. INGELHEIM 4,806,428 2.68 NOVARTIS 3,760,788 2.10 SANOFI-AVENTIS 3,727,099 2.08 NATRAPHARM 3,433,720 1.91 * Others * 66,829,534 37.25

2010TOP CORPORATIONS

01 SEP 2011

26 | P a g e

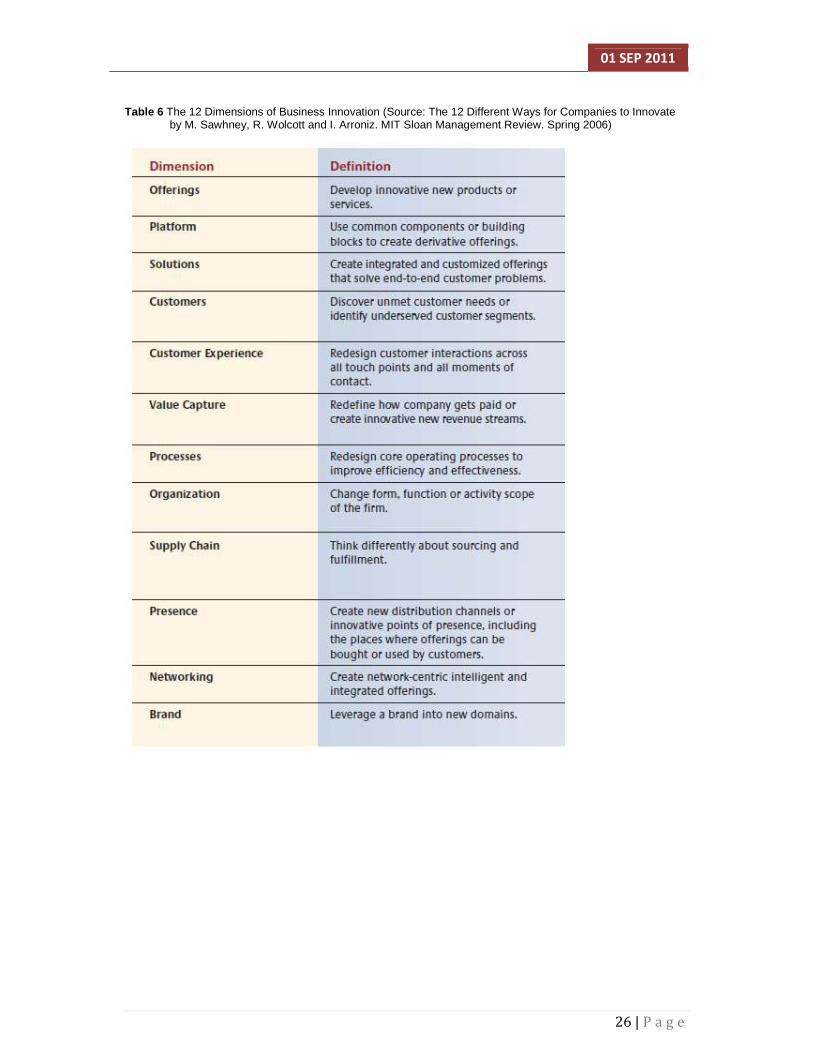

Table 6 The 12 Dimensions of Business Innovation (Source: The 12 Different Ways for Companies to Innovate

by M. Sawhney, R. Wolcott and I. Arroniz. MIT Sloan Management Review. Spring 2006)

01 SEP 2011

27 | P a g e

AVAC Framework

VIII. REFERENCES

1. Unilab company website. http://www.unilab.com.ph/

2. Unilab internal materials

3. Philippine Pharmaceutical Industry Factbook 7th Edition July 2008

4. IMAP Pharmaceuticals & Biotech Industry 2011 Global Report

5. http://www.mb.com.ph/node/73659

6. http://www.manilastandardtoday.com/insideBusiness.htm?f=2009/october/24/business1.isx&d=/2009/october/24

7. http://newsinfo.inquirer.net/inquirerheadlines/nation/view/20090820-221122/Cheap-medicines-law-registers-90-compliance

8. NEDA Development Advocacy Fact Sheet. Vol. XII, no. 12 , June 30, 2008

9. Allan Afuah. 2009. Strategic Innovation: New Game Strategies for Competitive Advantage. New York: Routledge.

Related Documents