UNDERSTANDING THE PVIL SHAREHOLDER TRUST 1 August 11, 2015

UNDERSTANDING THE PVIL SHAREHOLDER TRUST 1 August 11, 2015.

Dec 28, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

UNDERSTANDING THE PVIL SHAREHOLDER TRUST

1

August 11, 2015

KEY TERMS

Trust Agreement: The Contract between PVIL and the Trustees of the Trust that establishes the Trust and the rules under which the Trust will operate

Trustees: PVIL’s DirectorsBeneficiaries: PVIL’s shareholders

2

KEY TERMS

Contributions: What is placed in the TrustIncome: What the Trust earns Principal or Corpus: Contributions plus any

income reinvested in the TrustTrust Review: The process by which a

decision is made whether certain major modifications should be made to the Trust after the Trust is established

3

Advantages To The Trust

Tax Savings Superior Tax Reporting

Creditor ProtectionPermanence

Dedication of Assets to Specific Purpose

4

Special ANCSA Rules For The Trust

The Trust Cannot Operate A Business – Passive Investment Only

PVIL must control Trustee AppointmentOnly Individuals Can Be Trustees

Trust Must Be Registered In AlaskaNo reconveyance of ANCSA lands by Trust

5

Information About Other Existing ANCSA Settlement Trusts

• There are presently about 30 ANCSA settlement trusts, holding about $330 million in assets•Most common type is a Pro Rata Income

Distribution Trust • Next common is an Elders Trust• There are a small number of other types of

Trusts 6

CURRENT TAX TREATMENT OF PVIL & ITS SHAREHOLDERS

• PVIL is currently fully taxable• PVIL will pay a combined state and federal

tax rate of about 40% on ALL income • Shareholders pay tax on PVIL’s dividends at

rates of 0% to approximately 20%• “Average” PVIL Shareholder tax rate: 15%

7

SPECIAL TAX RULES APPLY TO THE TRUST AND ITS BENEFICIARIES• Contributions to Trust Are Tax Free To the

Trust• No corporate deduction for contributions• Distributions Of Trust Income To

Beneficiaries are Tax Free• NO 1099s sent to Beneficiaries• Beneficiaries do NOT include tax free Trust

distributions on their tax returns 8

SPECIAL TAX RULES APPLY TO THE TRUST AND ITS BENEFICIARIES• Trust pays a 10% Tax Rate On the Trust’s

Ordinary Income• Examples: Interest, Rent• Contrasted with 40% PVIL tax rate• Trust has a 0% Tax Rate On the Trust’s

Dividend/Capital Gain Income• Contrasted with 40% PVIL tax rate

9

Contrast of Tax Treatment of PVIL & Trust on $500,000 of Income

PVIL Trust

(With 646 Election)

Assumed Income ($10 million investment fund earning 5% annual interest)

$500,000 $500,000

Tax To Either PVIL or Trust (200,000) (50,000)

Available for Distribution $ 300,000 $ 450,000

Tax to Shareholders (assumed overall 15%)or Beneficiaries (0%)

(45,000) (0)

Kept By Shareholders or Beneficiaries $ 255,000 (51%)

$450,000 (90%)

10

10

Contrast of Tax Treatment of PVIL & Trust on $500,000 of Income

• The Trust is highly tax efficient• This means more net after tax income is

available to produce a given level of distributions for PVIL’s shareholders • It also means PVIL’s shareholders (as the

Trust’s Beneficiaries) will keep more of what the Trust distributes versus what PVIL distributes 11

SPECIFIC PROVISIONS OF THE PVIL SHAREHOLDER TRUST

12

Title, Parties, Whereas Clauses

• Provides Introduction, Background• Trust Intent: Long Term Distributions to

PVIL’s Shareholders•Trustees: PVIL BOD•Trust Name: THE PVIL SHAREHOLDER

TRUST

13

Sections 1 and 2

•Beneficiaries•PVIL’s Shareholders are the only

Beneficiaries•Trust Units•One PVIL Share = One Trust Unit•Regardless of Class

14

Section 3 Covers Certain ANCSA What Ifs? • If PVIL shares become transferable (3.1):

Separate votes on shares and trust units

• If PVIL issues additional stock (3.2, 3.4):Decoupling of trust units and PVIL

shares• If PVIL is dissolved (3.3): Decoupling• If PVIL is merged (3.5): Decoupling 15

Sections 4 and 5 • Contributions (4.1. 4.2)• Directors Not Trustees Decide

Contributions• $1000 has been contributed to start Trust • Trust is Irrevocable (5)

16

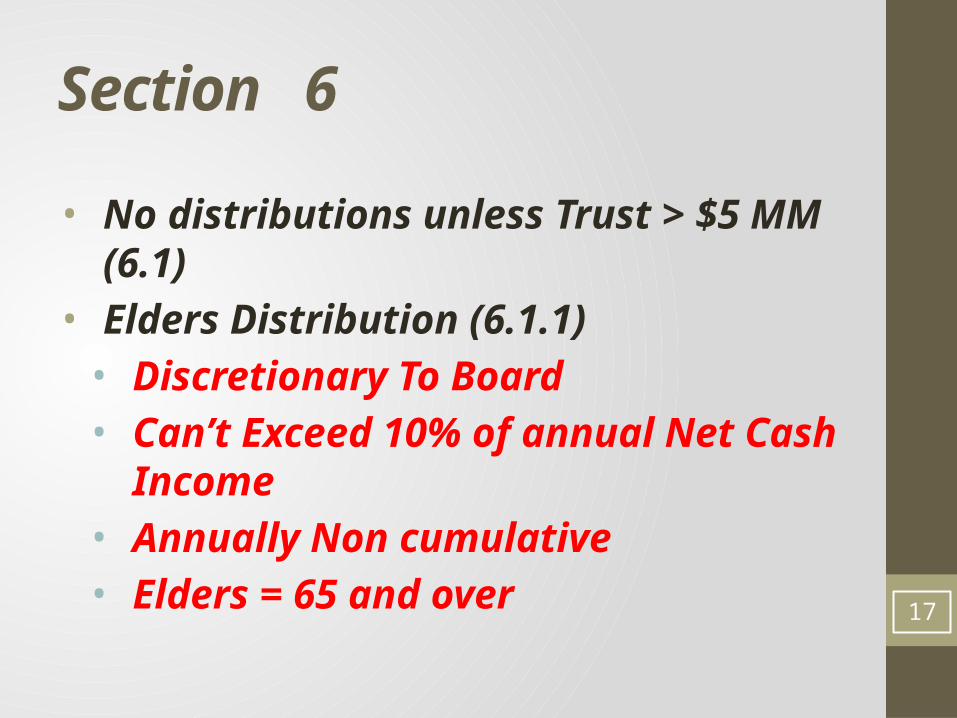

Section 6

• No distributions unless Trust > $5 MM (6.1)• Elders Distribution (6.1.1)• Discretionary To Board• Can’t Exceed 10% of annual Net Cash

Income• Annually Non cumulative• Elders = 65 and over

17

Section 6

• Educational Distributions (6.1.2)• Discretionary To Trustees• Can’t Exceed 10% of annual Net Cash

Income• Annually Non cumulative

18

Section 6

• Pro Rata Distribution (6.1.3)• Discretionary• Separate from Elders distribution• Separate from Educational distribution• Annually Cumulative

• No principal distributions (6.2)• Adjustment if overdistribution > $100K

(6.3) 19

Section 7 • 1st Review (7.1)• 10 yr Anniversary (i.e., 2025)• Modify Distribution/Termination Rules• Majority of Trustees & 2/3rds of Unitholders

must approve• No reversions to PVIL• Trust continues unless terminated

(“evergreen”)• 2nd & later reviews (7.3)• Every 10 years on Anniversary• Otherwise same as 1st review

20

Section 8

• Termination for Material Adverse Change (8.1.1, 27.7, 10.4.3)• At any time• Event External to Trust• 2/3rds of Trustees & Court Must

Approve• Trust distributed to shareholders

21

Sections 9 and 10• Investments made under investment policy

(9)• PVIL Directors = Trustees unless decoupling

(10.1)• Annual Trustees meeting To Be Held (10.2)• PVIL Officers = Trust officers unless

decoupling (10.3)• No Trustee Fees (10.6) or Bonding (10.7)

22

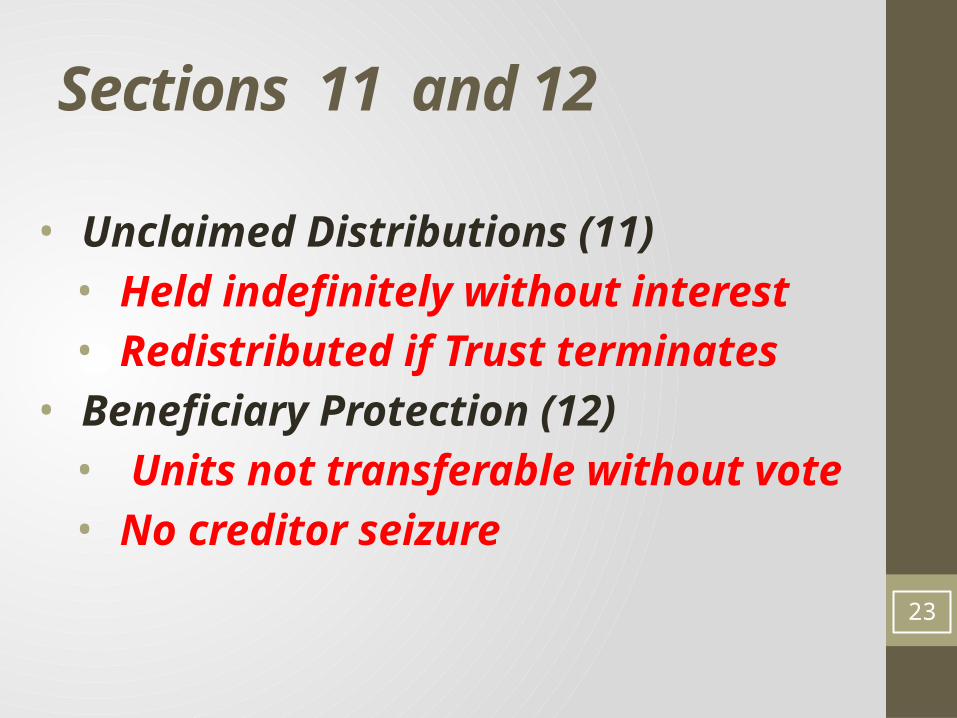

Sections 11 and 12

• Unclaimed Distributions (11)• Held indefinitely without interest• Redistributed if Trust terminates

• Beneficiary Protection (12)• Units not transferable without vote• No creditor seizure

23

Sections 13 and 14

• Broad Trustee Powers (13)• Tax Code section 646 election

mandatory (13.11)• Trust Certificates Optional (13.13)• Trustees indemnified by Trust and PVIL

(14.2 and 14.3)24

Sections 15, 16 and 17

• Trustees Must estimate net cash income in good faith (15.4)

• No duty to equate distributions (15.6)• Third parties can rely (17)• Annual audited financial statements required

(17)• Calendar year basis• Sent to beneficiaries at same time as PVIL’s

financial statements25

Sections 18 and 19• Distributions to Minors (18):• Any Native parent• Any sole custodial parent• If joint custody, then Native custodial

parent• Trustees’ allocation power (19)• Includes “rainy day” accumulation power• Income taxes allocated to income if 646

governs26

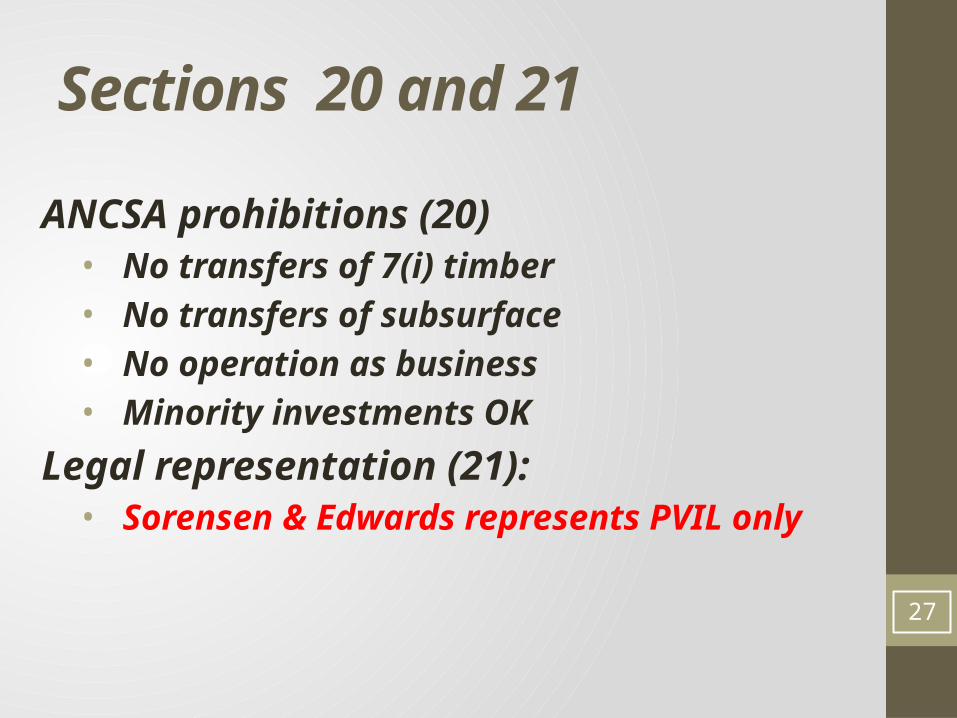

Sections 20 and 21

ANCSA prohibitions (20)• No transfers of 7(i) timber• No transfers of subsurface• No operation as business• Minority investments OK

Legal representation (21):• Sorensen & Edwards represents PVIL only

27

Sections 22, 23, and 24

• Savings (22):• Any invalid provisions do not invalidate trust

• Headings (23):• Do not control interpretation of Trust

• Applicable law (24):• Alaska law controls• Trust must be registered in Alaska

28

Sections 25 and 26• Grammatical references (25):• Intended to be neutral

• Minor, technical changes permissible (26.1):• Distribution timing/voting procedures/annual

meeting dates/section numbering/bonding• Trust must be registered in Alaska

• Trust modifications in lieu of termination (26.2, 26.4):• Material Adverse Effect situations

29

Section 27• Definition of Material Adverse Effect (27.4):• Adverse changes in tax law• Successful litigation challenges• Adverse changes to ANCSA• Elimination of investment alternatives

• Definition of Trust Fund and Principal (27.10, 27.13):• Implements “Rainy day” fund concept

30

Section 28, Signatures, Ex. A

• Shareholders Vote on 10/17/15 • Approval Standard: Majority of a

Quorum• Trustees• All current Directors have accepted

trusteeship• Successor Directors become Trustees

upon election as PVIL Directors 31

ANY QUESTIONS?

THANK YOU.

32

Related Documents