Understanding Retail Financial Products - 1 - Bank Products

Nov 27, 2015

Series on Retail Financial Products

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Insurance

Insurance

Insurance

Insurance

Products

Products

Products

Products

Investment

Investment

Investment

Investment

Products

Products

Products

Products

Credit

Credit

Credit

Credit

Products

Products

Products

Products

Session 1

Session 1

Session 1

Risk Risk -+

Savings Bank Deposits

Short Term

Debt Funds

Liquid Funds

Long Term

Debt Funds

Gold

Secured Debentures

Bank Fixed Deposits

Fixed Maturity Plans

Unsecured Debentures

Sectoral Equity Funds

Direct Equity

Hybrid Funds

Diversified Equity Funds

Risk Risk -+

Savings Bank Deposits

Bank Fixed Deposits

Let’s begin with the

sim

plest of the

Retail Financial Products -

At the very base

of the risk scale.

Risk Risk -+

Savings Bank Deposits

Savings Bank Deposits

Bank Fixed Deposits

Bank Fixed Deposits

Repayment of principal and payment of interest

on bank deposits is a contractual oblig

ation of the

bank. Therefore, bank deposits carry the least of risk.

Since the savings deposits are essentially of a

shorter term

as compared to the fixed deposits, they

carry a relatively lower

risk. As time passes the

chances of deterioration of financial health of the bank

increase; therefore the risk tends to increase w

ith the

term

of the deposits.

Two types of risk

Two types of risk

Two types of risk

-Default risk

-Market risk

--Default risk

Default risk

--Market risk

Market risk

Default

risk

is

the

possibility of the principal

not being repaid or interest

not being paid.

Market risk arises in case of investm

ent

products that are traded in a m

arket; it is the

risk of the price of the products falling. If the

price falls the investor loses.

Bank deposits are not traded; so

they do not have “m

arket risk”; they

have only “default risk”.

Risk bears an unique relationship

with return –

risk and return vary in the

same

direction.

That

is,

as

risk

increases, return also increases; and

vice versa.

Return

Return

Return

Return

Return

Return

Return

Return

To understand the risk –

return

relationship, we need to look into the

composition of return.

Rew

ard

fo

r

wait

ing

Rew

ard

fo

r R

ew

ard

fo

r

wait

ing

wait

ing

Co

mp

en

sa

tio

n f

or

infl

ati

on

Co

mp

en

sa

tio

n f

or

Co

mp

en

sa

tio

n f

or

infl

ati

on

infl

ati

on

Rew

ard

fo

r

risk b

eari

ng

Rew

ard

fo

r R

ew

ard

fo

r

risk b

eari

ng

risk b

eari

ng

Rew

ard

fo

r w

ait

ing

Rew

ard

fo

r w

ait

ing

Every investm

ent requires us to m

ake

a choice :

To use the purchasing power in our

hands to buy goods and services for

consumption.

OR

To save and invest it.

If w

e use the purchasing power to buy

goods and services for consumption, we get

satisfaction from it.

If we decide to save and invest the

purchasing power, w

e need to postpone this

satisfaction.

Investm

ent, therefore, involves w

aiting,

sacrificing.

And w

hy should w

e w

ait, unless w

e are

sufficiently rewarded for the wait ?

That is the “reward for waiting”that the

return on investm

ent needs to give us. This

is the first

component

of

the return on

investm

ent.

And w

hy should w

e w

ait, unless w

e are

sufficiently rewarded for the wait ?

That is the “reward for waiting”that the

return on investm

ent needs to give us. This

is the first

component

of

the return on

investm

ent.

But we do not usually reason this out

But we do not usually reason this out

continuously; this

continuously; this

tim

e

pre

fere

nce

tim

e

pre

fere

nce

is built

is built

into our psyche.

into our psyche.

As a result we prefer liquidity

As a result we prefer liquidity ––

we

we

prefer to hold our purchasing power in a

prefer to hold our purchasing power in a

liquid form

( in a form

that lets us deploy it

liquid form

( in a form

that lets us deploy it

easily for purchase of goods and services),

easily for purchase of goods and services),

unless we have a reason not to.

unless we have a reason not to.

That is why, the reward for waiting is

That is why, the reward for waiting is

also called the

also called the ““liquidity premium

liquidity premium”” ..

Co

mp

en

sati

on

fo

r in

flati

on

Co

mp

en

sati

on

fo

r in

flati

on

Investm

ent

means parting with our

Investm

ent

means parting with our

purchasing power NOW and getting it back

purchasing power NOW and getting it back

LATER.

LATER.

But the purchasing power we get back

But the purchasing power we get back

later may not be equal to the purchasing

later may not be equal to the purchasing

power

we had parted with,

if in the

power

we had parted with,

if in the

intervening period inflation has eroded the

intervening period inflation has eroded the

value of money.

value of money.

Therefore investm

ent can result in loss

of purchasing power.

Therefore the return on investm

ent

needs to compensate us for this loss, so that

the purchasing power we get back is equal to

the purchasing power we had parted with.

That

is

the

“compensation for

inflation”that the return on investm

ent needs

to give us. This is the second component of

the return on investm

ent.

Therefore investm

ent can result in loss

of purchasing power.

Therefore the return on investm

ent

needs to compensate us for this loss, so that

the purchasing power we get back is equal to

the purchasing power we had parted with.

That

is

the

“compensation for

inflation”that the return on investm

ent needs

to give us. This is the second component of

the return on investm

ent.

But investm

ent also involves risk –

of

principal not being repaid a

nd / o

r interest

not being paid. When w

e invest, w

e have to

necessarily bear this risk.

So, we w

ill invest if, and only if, w

e are

rewarded for bearing this risk.

That is the “reward for risk bearing”

that the return on investm

ent needs to give

us. This is the third component of the return

on investm

ent.

But investm

ent also involves risk –

of

principal not being repaid a

nd / o

r interest

not being paid. When w

e invest, w

e have to

necessarily bear this risk.

So, we w

ill invest if, and only if, w

e are

rewarded for bearing this risk.

That is the “reward for risk bearing

reward for risk bearing”

that the return on investm

ent needs to give

us. This is the third component of the return

on investm

ent.

The return from those investm

ents

which do not carry any risk, will therefore

have only two components : reward for

waiting and compensation for inflation.

Such investm

ents are called risk free

investm

ents and the rate of return from such

investm

ents is called the “risk free rate of

return”. Short term

investm

ents guaranteed by

the government, pay a risk free rate of

return.The return from those investm

ents

which do not carry any risk, will therefore

have only two components : reward for

waiting and compensation for inflation.

Such investm

ents are called risk free

investm

ents and the rate of return from such

investm

ents is called the “ risk free rate of

risk free rate of

return

return”. Short term

investm

ents guaranteed by

the government, pay a risk free rate of

return.

All other investm

ents pay a rate higher

All other investm

ents pay a rate higher

than the risk free rate, depending upon the

than the risk free rate, depending upon the

risk that they carry.

risk that they carry.

Bank deposits pay a rate very close to

Bank deposits pay a rate very close to

the risk free rate of return. Weaker the bank,

the risk free rate of return. Weaker the bank,

higher will be the rate of interest that it pays.

higher will be the rate of interest that it pays.

Compensation

for

inflation

Reward for

waiting

Risk

premium

Compensation

for

inflation

Reward for

waiting

Risk

premium

Compensation

for

inflation

Reward for

waiting

Risk

premium

Risk free rate of return

Higher the risk,

higher the risk premium,

higher the return.

Total return

The rate of

return also bears a

The rate of

return also bears a

relationship to the liquidity of investm

ent.

relationship to the liquidity of investm

ent.

Liquidity refers to the ease and cost of

Liquidity refers to the ease and cost of

converting

any

invetsment

into

cash;

converting

any

invetsment

into

cash;

greater the ease and lower the cost, higher

greater the ease and lower the cost, higher

is the liquidity.

is the liquidity.

Other

things remaining the same,

Other

things remaining the same,

higher

the liquidity, lower

is the rate of

higher

the liquidity, lower

is the rate of

return, and vice versa.

return, and vice versa.

This is w

hy, given a bank, the rate of

This is w

hy, given a bank, the rate of

interest on savings deposits is lower than

interest on savings deposits is lower than

the rate of interest on fixed deposits.

the rate of interest on fixed deposits.

Let

us

now

move further

on the

risk

scale

in

the

investm

ent

products

spectrum, to products

that

carry

higher

levels of risk.

Risk Risk-+

Liquid Funds

Liquid Funds

Fixed Maturity Plans

Fixed Maturity Plans

Liquid Funds

Liquid Funds

Fixed Maturity Plans

Fixed Maturity Plans

Both these products are Mutual Fund

schemes.

A mutual fund is a company that pools

A mutual fund is a company that pools

investm

ent from m

any investors and invests it

investm

ent from m

any investors and invests it

in stocks,

bonds,

short

in stocks,

bonds,

short-- term

money

term

money-- m

arket

market

instruments,

other

securities or

assets,

or

instruments,

other

securities or

assets,

or

some combination of these securities.

some combination of these securities.

The combined holdings of securities held by

The combined holdings of securities held by

the M

F are known as its portfolio.

the M

F are known as its portfolio.

The total investm

ents collected by a MF

The total investm

ents collected by a MF

from the investors is known as its corpus or AUM

from the investors is known as its corpus or AUM

( Assets U

nder Management).

( Assets U

nder Management).

The total corpus of a MF is divided into

The total corpus of a MF is divided into

units.

Each

unit

represents

an

investor's

units.

Each

unit

represents

an

investor's

proportionate ownership of the portfolio

held by

proportionate ownership of the portfolio

held by

the M

F. The unit holder has a right to the income

the M

F. The unit holder has a right to the income

those holdings generate; the unit holder

also

those holdings generate; the unit holder

also

bears the erosion in the value of holdings, if any.

bears the erosion in the value of holdings, if any.

Investo

rIn

vesto

r

Investo

rIn

vesto

r

Investo

rIn

vesto

r

Investo

rIn

vesto

r

Investo

rIn

vesto

r

Investo

rIn

vesto

rIn

vesto

rIn

vesto

r

Investo

rIn

vesto

r

Investo

rIn

vesto

r

Investo

rIn

vesto

r

Investo

rIn

vesto

rIn

vesto

rIn

vesto

r

Mutual

Mutual

Fund

Fund

SECURITIES AND EXCHANGE BOARD OF INDIA

MUTUAL FUNDS REGULATIONS,

1996

SECURITIES AND EXCHANGE BOARD OF INDIA

MUTUAL FUNDS REGULATIONS,

1996

7.

For the purpose of grant of a certificate of

registration, the applicant has to fulfill the

following conditions, namely :

(a) the sponsor should have a sound track record

and general reputation of fairness and integrity in

all his business transactions;

(e) appointm

ent of trustees to act as trustees for

the mutual fund in accordance with the provisions

of the regulations;

(f) appointm

ent of asset management company to

manage the mutual fund and operate the schemes

of such funds in accordance with the provisions of

these regulations;

(g) appointm

ent of a custodian in order to keep

custody of the securities or gold and gold related

instruments and carry out the custodian activities

as may be authorised by the trustees.

Sponsor

Sponsor

Trustees

Trustees

A M C

A M C

Custodian

Custodian

Appoints

Appoints

Provides custodial

services

Mu

tual

Mu

tual

Fu

nd

Fu

nd

Supervise the fund on

behalf of the unitholders.

Manages the portfolio of

the fund.

Provides the initial

capital to start the fund.

14.

A mutual fund shall be constituted in the form

of a

trust and the instrument of trust shall be in the

form

of a deed, duly registered under the provisions

of the Indian Registration Act, 1908 (16 of 1908),

executed by the sponsor in favour of the trustees

named in such an instrument.

20.

The sponsor or, if so authorised by the trust deed,

the trustee, shall appoint an asset management

company, which has been approved by the Board.

26.

The mutual fund shall appoint a Custodian to

carry out the custodial services for the schemes of

the fund.

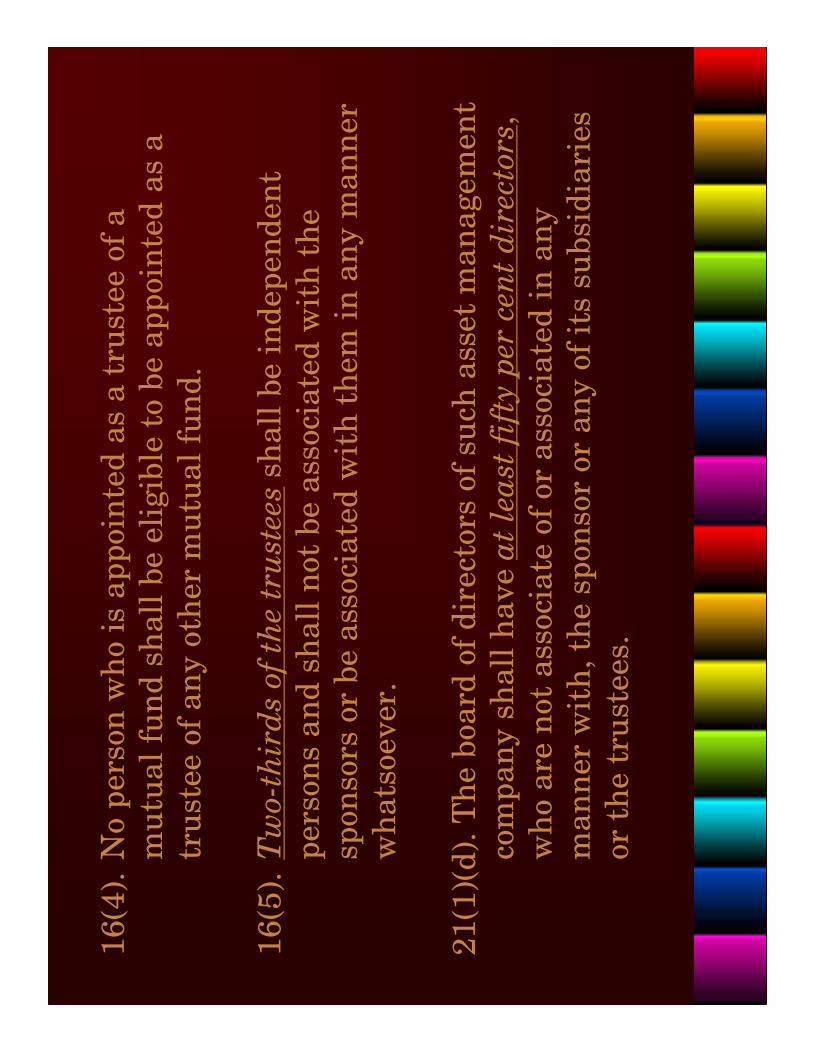

16(4). No person who is appointed as a trustee of a

mutual fund shall be eligible to be appointed as a

trustee of any other mutual fund.

16(5).

Tw

o-t

hir

ds

of

the

tru

stee

sshall be independent

persons and shall not be associated with the

sponsors or be associated with them in any manner

whatsoever.

21(1)(d). The board of directors of such asset management

company shall have a

t le

ast

fif

ty p

er c

ent

dir

ecto

rs,

who are not associate of or associated in any

manner with, the sponsor or any of its subsidiaries

or the trustees.

Sponsor

Sponsor

Trustees

Trustees

A M C

A M C

Custodian

Custodian

The purpose of these regulations

is to keep an “arms length”distance

between the different entities in the

mutual fund structure;

so that they do not collude to harm

the investor’s interest.

Risk Risk -+

Savings Bank Deposits

Short Term

Debt Funds

Liquid Funds

Long Term

Debt Funds

Gold

Secured Debentures

Bank Fixed Deposits

Fixed Maturity Plans

Unsecured Debentures

Sectoral Equity Funds

Direct Equity

Balanced Funds

Diversified Equity Funds

At

the e

nd

of

sessio

n 1

,

we h

ave r

each

ed

here

on

th

e

sp

ectr

um

of

Investm

en

t P

rod

ucts

.

We still need to look deeper

into Liquid funds and FMPs.

Related Documents