Presented by : Mr. Jeremy Lau E-series course 1 Understanding M&A: from acquisition to reverse takeover

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Presented by : Mr. Jeremy Lau E-series course

1

Understanding M&A: from acquisition to reverse takeover

2

About the SpeakerMr. Jeremy Lau

o Jeremy has over 15 years of experience in corporate finance, auditingand advisory. He has served as responsible officers in a couple ofsponsor firms. Jeremy is currently a Managing Director of Grande CapitalLimited and a sponsor principal approved by SFC. He is also a fellowmember of HKICPA.

o Jeremy has extensive experience in IPOs, corporate finance, complianceof listed companies, auditing and financial reporting. Over time, He hasparticipated in numerous IPOs and spin-offs projects, involving variousindustries, such as consumables, technology products, media, securities,property management and constructions.

2

3

Course Outline

- Regulatory framework- Size test and classification of notifiable

transaction- Requirements for different notifiable transactions- Settling the consideration- Reverse takeover and extreme transaction- Case study

3

4

Regulatory Framework

4

5

Framework of M&A transactions• Companies listed in HK conducting M&A transactions are subject to

Chapter 14 of the Main Board Listing Rules – Notifiable Transactions (or Chapter 19 of the GEM Listing Rules)

• M&A transactions are generally “notifiable transactions” under Chapter 14 of the Listing Rules, and the regulatory requirements depend on the size of the M&A targets relative to the listco, as determined by the “5 size test”

5

6

Framework of M&A transactions• If the counterparty is connected to the listco, the M&A transactions are also

subject to Chapter 14A of the Main Board Listing Rules – Connected Transactions (or Chapter 20 of the GEM Listing Rules)

• The transactions may be further subject to Takeovers Code if the seller is allotted shares of the listco exceeding certain limits.

6

7

Definition of “transaction” under Chapter 14• The following are “transactions” governed under Listing Rules Chapter 14 :

a) Acquisition or disposal of assets

b) An option to subscribe for shares or buy or sell assets

c) Entering into or terminating a finance lease

d) Entering into or terminating operating leases with significant impact on the company’s operation

e) Providing financial assistance

f) Formation of JV

• Exclude some transactions of a revenue nature in the ordinary and usual course of business

7

8

Size test andclassificationof notifiable transaction

8

9

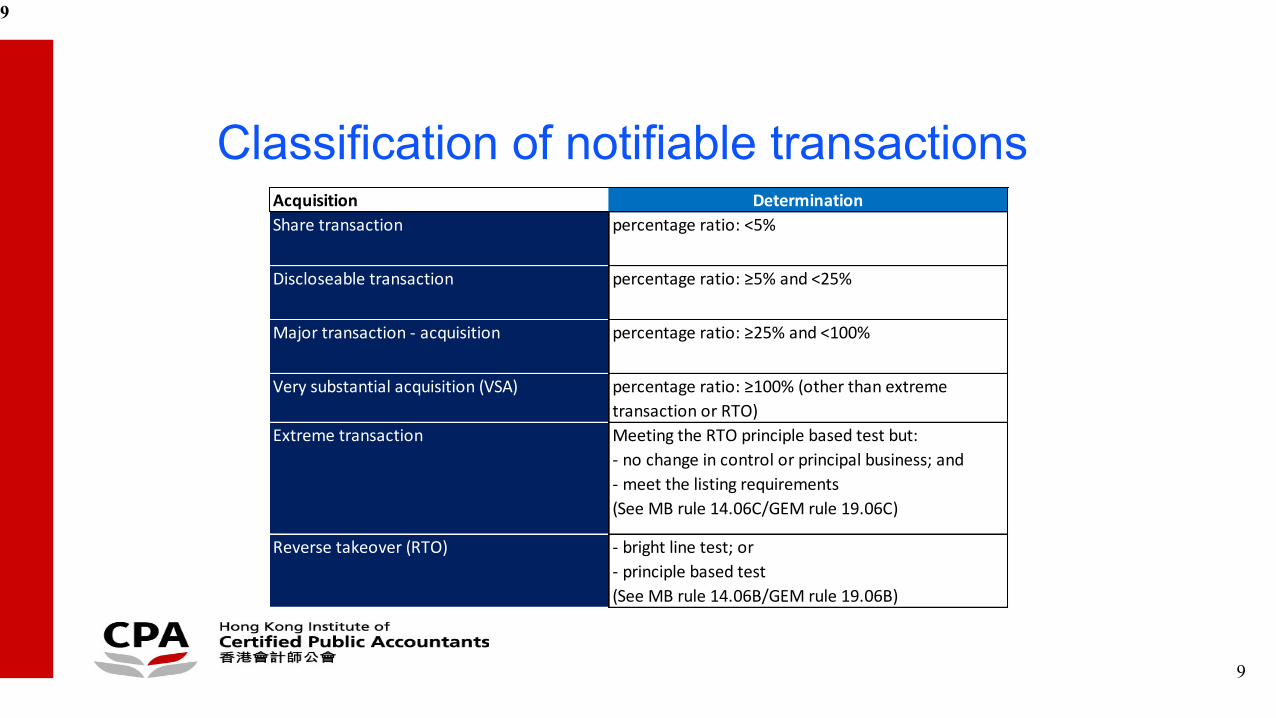

Classification of notifiable transactions

9

Acquisition DeterminationShare transaction percentage ratio: <5%

Discloseable transaction percentage ratio: ≥5% and <25%

Major transaction - acquisition percentage ratio: ≥25% and <100%

Very substantial acquisition (VSA) percentage ratio: ≥100% (other than extreme transaction or RTO)

Extreme transaction Meeting the RTO principle based test but:- no change in control or principal business; and- meet the listing requirements(See MB rule 14.06C/GEM rule 19.06C)

Reverse takeover (RTO) - bright line test; or- principle based test(See MB rule 14.06B/GEM rule 19.06B)

10

Classification of notifiable transactions

10

Disposal Determination

Discloseable transaction percentage ratio: ≥5% and <25%

Major transaction - disposal percentage ratio: ≥25% and <75%

Very substantial disposal (VSD) percentage ratio: ≥75%

11

5 size tests

11

* Equity capital ratio relates only to an acquisition (and not a disposal) by a listed issuer issuing new equity capital

12

5 size testsGeneral principles:1. The source of issuer’s figures is its published information.2. The source of target’s figures is its audited accounts or other acceptable

accounts.3. Acquisition/ disposal of equity capital

Ø resulting in consolidation/ de-consolidation?− Yes - 100% − No - % bought or sold

4. Transaction via non wholly owned subsidiaryØ Same size test computation as for transactions via wholly owned

subsidiary

12

13

Special circumstancesWhen the consideration cannot be determined

13

Under the acquisition agreement, Listcohas to pay:

• cash consideration: HK$5 million; plus

• an amount as adjusted by the valuation of the Target at the time of completion, which cannot be determined now

Listco

Acquisition target

How to determine the consideration ratio?

14

Special circumstancesUnder R14.15(4), when calculating the consideration ratio, if the listed issuer may pay consideration in the future, the consideration is the maximum total consideration payable under the agreement.

For the proposed acquisition of the target company, the numerator of the consideration ratio should include the fixed amount of cash as well as the maximum value of the further consideration that may be paid by the listed issuer in the future. If the total consideration is not subject to a maximum or such maximum value cannot be determined, the proposed acquisition will normally be classified as a very substantial acquisition, notwithstanding the transaction class into which it otherwise falls.

Reference: FAQ Series 7, FAQ No. 8

14

15

Size test case study

15

Case 1: if % of shareholding after acquisition >50%

Case 2: if % of shareholding after acquisition ≤50%

1 Listco A is to acquire 25% shares of Target B Listco A is to acquire 25% shares of Target B

2 At the beginning, Listco A owned 0% shares of Target B

At the beginning, Listco A owned 40% shares of Target B

3 Listco A's interest in Target B will increase from 0% to 25%

Listco A's interest in Target B will increase from 40% to 65%

4 After the acquisition, Target B will not become a subsidiary of Listco A

After the acquisition, Target B will become a subsidiary of Listco A

5 For calculating percentage ratio, assuming Listco A's base is 100, Target B's is 60

For calculating percentage ratio, assuming Listco A's base is 100, Target B's is 60

16

Size test case study

16

Case 1: if % of shareholding after acquisition >50%

Case 2: if % of shareholding after acquisition ≤50%

6 So the percentage ratio of this spinoff is: So the asset, revenue and profits ratio of this spinoff is:

7 Since the percentage ratio is more than 5% but less than 25%, it is a disclosable transaction

Since the percentage ratio is more than 25% but less than 100%, it is a major transaction

8 The acquisition is subject to (i) notification to Exchange and (ii) announcement only

The acquisition is subject to (i) notification to Exchange, (ii) announcement, (iii) circular and (iv) shareholders' approval

17

Requirements for differentnotifiable transactions

17

18

Requirements for different notifiable transactions

18

Notify Exchange Announcement

Shareholders' approval / circular to shareholders

Accountants' report

Appoint sponsor/ financial adviser for due diligence

Treated as new listing, listing approval required

Share transaction Yes Yes

No (if consideration shares are issued under general mandate)

No No No

Discloseable transaction Yes Yes No No No No

Major transaction - acquisition

Yes Yes Yes Yes No No

Very substantial acquisition (VSA)

Yes Yes Yes Yes No No

Extreme transaction Yes Yes Yes Yes Yes No

Reverse takeover (RTO) Yes Yes Yes Yes Yes Yes

19

Aggregation of transactionsPrevent circumvention of Listing Rules by splitting a transaction

Two types of aggregation:- Applicable to share transaction, discloseable transaction, major transaction and VSA

(R14.22-R14.23)- Applicable to extreme transaction and RTO (R14.06B)

19

20

Aggregation of transactionsApplicable to share transaction, discloseable transaction, major transaction and VSA:

R14.22 the Exchange may require listed issuers to aggregate a series of transactions and treat them as if they were one transaction if they are all completed within a 12 month period or are otherwise related. In such cases, the listed issuer must comply with the requirements for the relevant classification of the transaction when aggregated and the figures to be used for determining the percentage ratios are those as shown in its accounts or latest published interim report (whichever is more recent), subject to any adjustments or modifications......

20

21

Aggregation of transactionsApplicable to share transaction, discloseable transaction, major transaction and VSA:

R14.23 Non-exhaustive factors the Exchange will consider:

(1) are entered into by the listed issuer with the same party or with parties connectedor otherwise associated with one another;

(2) involve the acquisition or disposal of securities or an interest in one particular company or group of companies;

(3) involve the acquisition or disposal of parts of one asset; or(4) together lead to substantial involvement by the listed issuer in a business activity

which did not previously form part of the listed issuer’s principal business activities (i.e. new business).

21

22

Aggregation of transactions

All factors are considered. Aggregation is not automatic only because one factor is triggered.The Exchange will also consider the effect of aggregation: à whether aggregation would result in a higher transaction classification.

New classification only applies to the current transaction.

22

First Transaction

Second Transaction

If aggregated Will aggregation result in a higher classification?

Second Transaction

Major Discloseable Major No Discloseable

Major Discloseable VSA Yes VSA

23

Aggregation of transactionsApplicable to extreme transaction and RTO:

R14.06B Note 1(f) – applicable to principle based testThe Exchange may regard acquisitions and other transactions or arrangements as a series if they take place in a reasonable proximity to each other (which normally refers to a period of 36 months or less) or are otherwise related.

R14.06B Note 2(b) – applicable to bright line testacquisition(s) of assets from a person or a group of persons or any of his/their associates pursuant to an agreement, arrangement or understanding entered into by the listed issuer within 36 months of such person or group of persons gaining control

23

24

Settling the consideration

24

25

Settling the considerationConsiderations for acquisition are normally settled by:- cash;- promissory note or bond;- convertible bond;- shares of the listco; and/or- shares of the subsidiary of the listco

25

Amount to deemed disposal of the interest of the subsidiary

Involve issuing shares of the listco, subject to listing approval

26

Settling the considerationIssuing listco’s shares or convertible debts is subject to the following restrictions:

- General mandate: not more than 20% of the number of issued shares of the listco as at the date of the resolution granting the general mandate by shareholders

- Specific mandate: requires shareholder approval

…cont’d

26

27

Settling the considerationIssuing listco’s shares or convertible debts is subject to the following restrictions:

- Takeovers code: a general offer may be required under Takeovers Code if the purchaser’s interests exceed a certain limit.

When the issue of new securities as consideration for an acquisition, would otherwise result in an obligation to make a mandatory offer, the Executive of the SFC will normally grant a whitewash waiver if the whitewash waiver and the underlying transaction(s) are separately approved by at least 75% and more than 50% respectively of the independent vote that are cast either in person or by proxy at a shareholders’ meeting.

27

28

Reverse takeover and extremetransaction

28

29

Changes on rules for backdoor listing, RTO and extreme transaction

Jun 2018 – The Stock Exchange published a consultation paper on theListing Rules amendments in relation to backdoor listing

Jul 2019 – The Stock Exchange published the conclusion on the consultation paper

Oct 2019 – Listing Rules were revised in relation to backdoor listings,reverse takeover and extreme transaction

29

30

Changes on rules for backdoor listing, RTO and extreme transactionRTO – Bright line tests:

Modify the bright line tests to:

(i) apply to very substantial acquisitions from an issuer’s controlling shareholder within36 months from a change in control of the issuer; and

(ii) restrict disposals (or distributions in specie) of all or a material part of the issuer’sbusiness proposed at the time of or within 36 months after a change in control ofthe issuer. The Exchange may also apply the restriction to disposals (ordistributions in specie) at the time of or within 36 months after a change in de factocontrol (as set out in the principle based test) of the issuer

30

31

Changes on rules for backdoor listing, RTO and extreme transactionRTO – Principle based test: Codify the six assessment factors under the principle based test in Guidance Letter GL78-14:- transaction size- target quality- nature and scale of issuer’s business- fundamental change in principal business- change in control/de facto control- series of transactions and/or arrangements (this includes acquisitions,

disposals and/or change in control or de facto control that take place inreasonable proximity (normally within 36 months) or are otherwise related)

31

32

Changes on rules for backdoor listing, RTO and extreme transactionExtreme transactions:

(i) codify the “extreme VSAs” requirements in Guidance Letter GL78-14 and renamethis category of transactions as “extreme transactions”; and

(ii) impose additional eligibility criteria on the issuer that may use this transactioncategory: (a) the issuer must operate a principal business of substantial size; or (b) the issuer must have been under the control or de facto control of the same

person(s) for a long period (normally not less than 36 months) and thetransaction will not result in a change in control or de facto control of the issuer

32

33

Changes on rules for backdoor listing, RTO and extreme transactionRequirements for RTOs and extreme transactions:

Modify the Listing Rules to require the acquisition targets in a RTO or extreme transaction to meet the requirements of Rule 8.04 (i.e. suitable for listing) and Rule 8.05, 8.05A or 8.05B (i.e. profit test or other eligibility test), and the enlarged group to meet all the new listing requirements in Chapter 8 of the Listing Rules (i.e. qualification for listing). Where the RTO is proposed by an issuer that does not meet Rule 13.24 (i.e. sufficient level of operation), the acquisition targets must also meet the requirement of Rule 8.07 (i.e. sufficient public interest)

33

34

Reverse takeoverR14.06B Note 2 – Bright line test:(a) an acquisition or a series of acquisitions (aggregated under Rules 14.22 and

14.23) of assets constituting a very substantial acquisition wherethere is or which will result in a change in control (as defined in the TakeoversCode) of the listed issuer (other than at the level of its subsidiaries); or

(b) acquisition(s) of assets from a person or a group of persons or any of his/theirassociates pursuant to an agreement, arrangement or understanding entered intoby the listed issuer within 36 months of such person or group of persons gainingcontrol (as defined in the Takeovers Code) of the listed issuer (other than at thelevel of its subsidiaries), where such gaining of control had not been regarded as areverse takeover, which individually or together constitute(s) a very substantialacquisition.

34

35

Reverse takeoverR14.06B Note 1 – Principle based test:Rule 14.06B is aimed at preventing acquisitions that represent an attempt to circumvent the new listing requirements. In applying this principle based test, the Exchange will normally take into account the following factors:(a) the size of the acquisition or series of acquisitions relative to the size of the issuer;(b) a fundamental change in the issuer's principal business;(c) the nature and scale of the issuer’s business before the acquisition or series of

acquisitions;(d) the quality of the acquisition targets;(e) a change in control (as defined in the Takeovers Code) or de facto control of the listed

issuer (other than at the level of its subsidiaries); and

….cont’d

35

36

Reverse takeoverR14.06B Note 1 – Principle based test:

(f) other transactions or arrangements which, together with the acquisition or series ofacquisitions, form a series of transactions or arrangements to list the acquisition targets.

These transactions or arrangements may include changes in control/de facto control, acquisitions and/or disposals. The Exchange may regard acquisitions and other transactions or arrangements as a series if they take place in a reasonable proximity to each other (which normally refers to a period of 36 months or less) or are otherwise related.

The Exchange will consider whether, taking the factors together, an issuer’s acquisition or series of acquisitions constitute an attempt to list the acquisition targets and circumvent the new listing requirements.

36

37

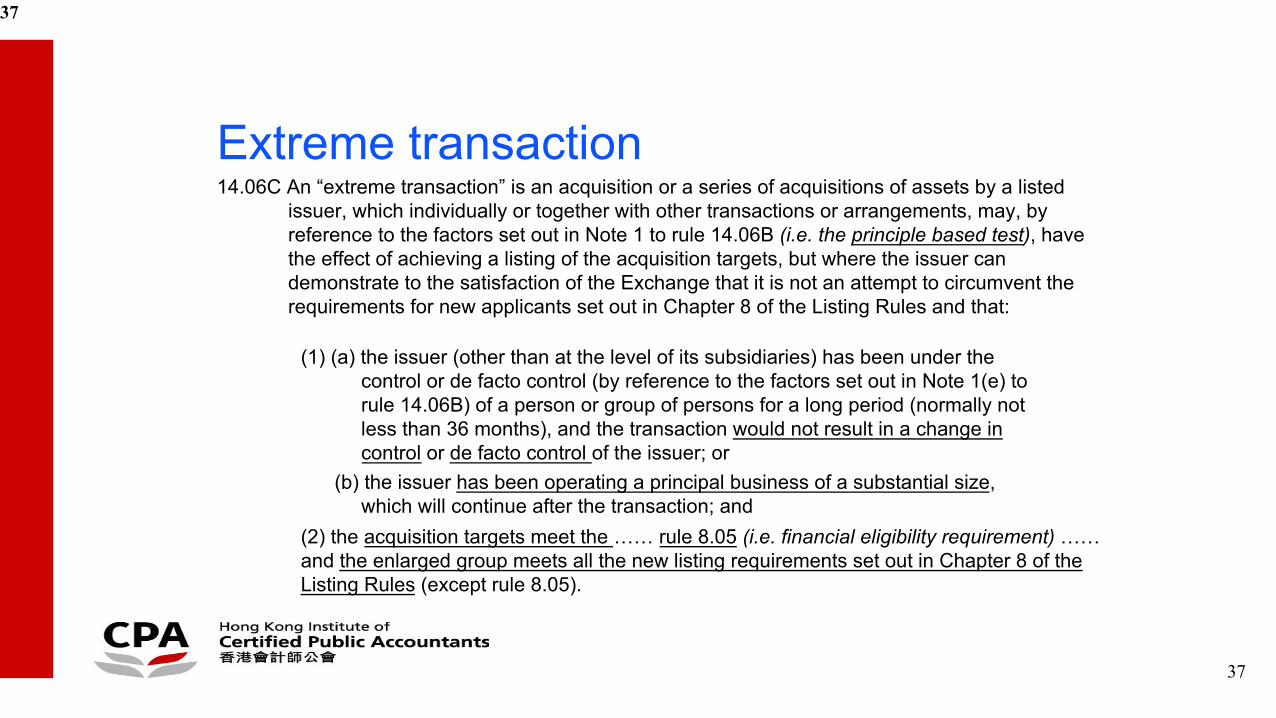

Extreme transaction14.06C An “extreme transaction” is an acquisition or a series of acquisitions of assets by a listed

issuer, which individually or together with other transactions or arrangements, may, byreference to the factors set out in Note 1 to rule 14.06B (i.e. the principle based test), havethe effect of achieving a listing of the acquisition targets, but where the issuer can demonstrate to the satisfaction of the Exchange that it is not an attempt to circumvent therequirements for new applicants set out in Chapter 8 of the Listing Rules and that:

(1) (a) the issuer (other than at the level of its subsidiaries) has been under thecontrol or de facto control (by reference to the factors set out in Note 1(e) torule 14.06B) of a person or group of persons for a long period (normally notless than 36 months), and the transaction would not result in a change incontrol or de facto control of the issuer; or

(b) the issuer has been operating a principal business of a substantial size,which will continue after the transaction; and

(2) the acquisition targets meet the …… rule 8.05 (i.e. financial eligibility requirement) …… and the enlarged group meets all the new listing requirements set out in Chapter 8 of the Listing Rules (except rule 8.05).

37

38

Timeline of reverse takeover/ extreme transaction

38

Bright line testR14.06B Note 2(a) change in control & VSA

R14.06B Note 2(b) change in control VSA

Principle based testR14.06B Note 1(e)&(f)

Day 0

Year 1 Year 2 Year 3

acquisitions and/or disposals

39

Timeline of reverse takeover/ extreme transaction

39

change in control major acquisition 1 major acquisition 2

Day 0

Year 1 Year 2 Year 3

Question 1: Will it be treated as reverse takeover?

Answer: We have to consider whether the two major acquisitions from a person or a group of persons or any of his/their associates will be classified as VSA when aggregated, this will amount to a VSA within 36 months after change in control, and resulting in a reserve takeover according to the bright line test under R14.06B Note 2(b).

40

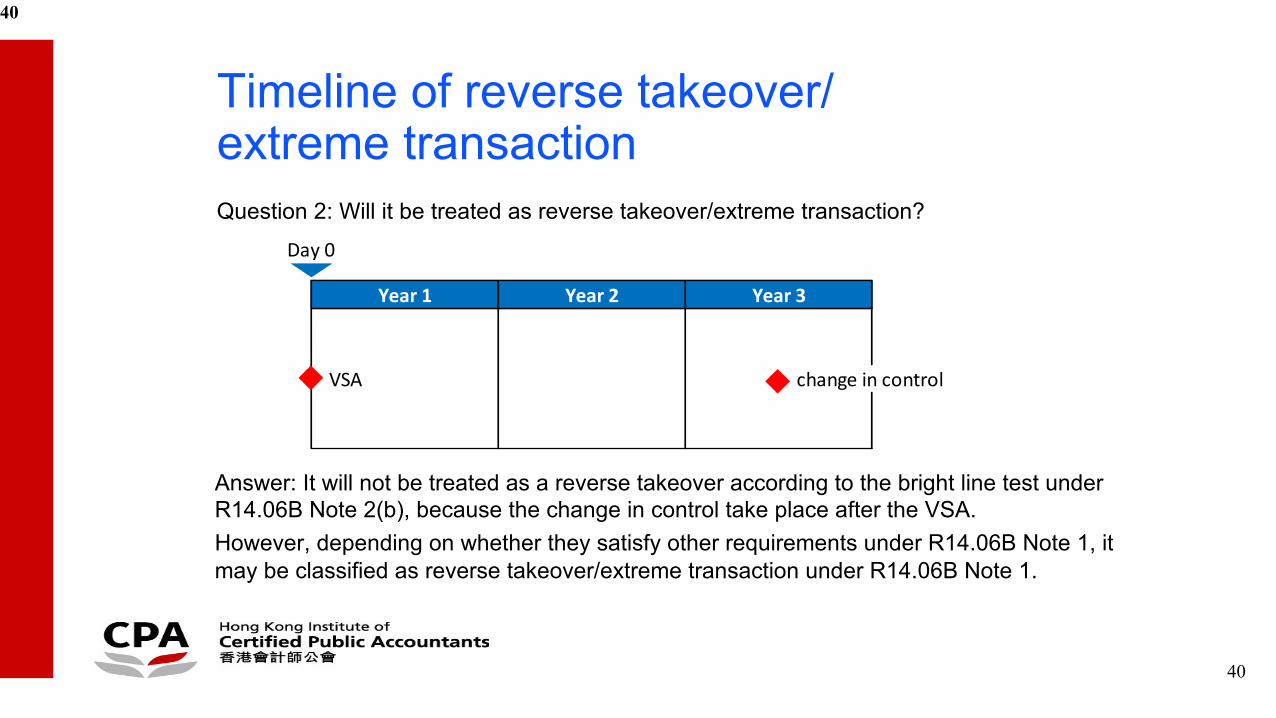

Timeline of reverse takeover/ extreme transaction

40

Question 2: Will it be treated as reverse takeover/extreme transaction?

Answer: It will not be treated as a reverse takeover according to the bright line test under R14.06B Note 2(b), because the change in control take place after the VSA. However, depending on whether they satisfy other requirements under R14.06B Note 1, it may be classified as reverse takeover/extreme transaction under R14.06B Note 1.

VSA change in control

Day 0

Year 1 Year 2 Year 3

41

Requirements for reverse takeover14.54 The Exchange will treat a listed issuer proposing a reverse takeover as if it were

a new listing applicant.(1) The acquisition targets must meet the …… rule 8.05 (i.e. financial eligibility

test) (or rule 8.05A or 8.05B). In addition, the enlarged group must meet allthe new listing requirements set out in Chapter 8 of the Listing Rules(except rule 8.05).

(2) Where the reverse takeover is proposed by a listed issuer that has failed tocomply with rule 13.24 (i.e. sufficient operation), the acquisition targets mustalso meet the requirement of rule 8.07 (i.e. sufficient public interest)(in addition to the requirements for the acquisition targets and the enlargedgroup set out in rule 14.54(1)).

(3) The listed issuer must comply with the requirements for all transactions setout in rules 14.34 to 14.37 (i.e. requirements for all notifiable transactions).

41

42

Requirements for reverse takeover14.57 A listed issuer proposing a reverse takeover must comply with the procedures

and requirements for new listing applications as set out in Chapter 9 of theListing Rules. The listed issuer will be required, among other things,to issue a listing document and pay the non-refundable initial listing fee. Alisting document relating to a reverse takeover must contain the informationrequired under rules 14.63 and 14.69. The listing document must bedespatched to the shareholders of the listed issuer at the same time as orbefore the listed issuer gives notice of the general meeting to approve thetransaction. The listed issuer must state in the announcement on the reversetakeover when it expects the listing document to be issued.

42

43

Requirements for extreme transaction14.53A In the case of an extreme transaction, the listed issuer must:

(1) comply with the requirements for very substantial acquisitions set out inrules 14.48 to 14.53. The circular must contain the information requiredunder rules 14.63 and 14.69; andNote: See also rule 14.57A if the extreme transaction involves a series oftransactions and/or arrangements.

(2) appoint a financial adviser to perform due diligence on the acquisitiontargets to put itself in a position to be able to make a declaration in theprescribed form set out in Appendix 29. The financial adviser must submitto the Exchange the declaration before the bulk-printing of the circular forthe transaction.

43

44

Case study

44

45

Case study – LD75-2(published in Oct 2009)Company A proposed to acquire controlling interests in the Target by issuing shares to the Vendor (the Acquisition). Company A and the Target had the same line of business.

Based on the percentage ratio calculation, the Acquisition was a very substantial acquisition.

The Acquisition would result in a change in its shareholding structure: - The Company A's holding company’s shareholding would be diluted from above 50% to about 20% of the enlarged issued share capital. - The Vendor would hold more than 50% of Company A’s enlarged issued share capital.

45

46

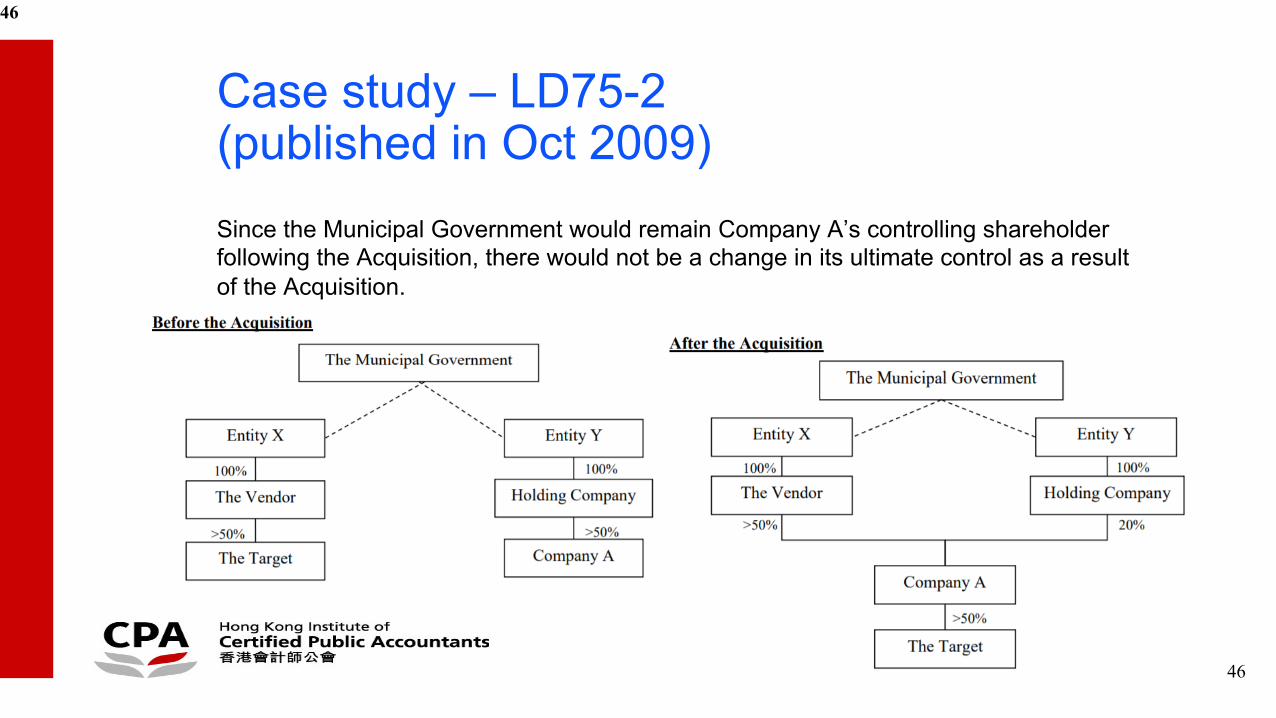

Case study – LD75-2(published in Oct 2009)Since the Municipal Government would remain Company A’s controlling shareholder following the Acquisition, there would not be a change in its ultimate control as a result of the Acquisition.

46

47

Case study – LD75-2(published in Oct 2009)The Exchange also took into account the assessment of “control” under the Takeovers Code. In this case, the Takeovers Executive had granted a waiver to the Vendor from its obligation to make a general offer under Note 6(a) to Rule 26.1 of the Takeovers Code. This was different from the situation where the control of an issuer changed and a whitewash waiver was granted subject to independent shareholders’ approval under the Takeovers Code.

The Acquisition was not regarded as a reverse takeover of Company A.

The Listing Rule amendments in Oct 2019 would not change the analysis and conclusion in this case.

47

48

Case study – LD109-2017 (published in June 2017)Company A was principally engaged in the manufacturing and sale of certain food products for many years.

On Day 0, Mr. X ceased to be the controlling shareholder of Company A but remained as a director of Company A.

A few months later, Company A announced a major transaction to acquire a company engaging in video gaming business (“First Target”) from independent third parties for cash consideration (“First Acquisition”).

In the Year 2, Mr. Y acquired about 20% interest in Company A.

48

49

Case study – LD109-2017 (published in June 2017)Around the end of Year 2, Company A proposed the following transactions:

(1) Acquisition of another company engaging in video gaming business from independent third parties for cash consideration (“Proposed Acquisition”). Based on its size tests, the Proposed Acquisition would, on its own, constitute a major transaction; and

(2) Disposal of its food business (“Proposed Disposal”) to Mr. X. The ProposedDisposal would constitute a very substantial disposal.

49

50

Case study – LD109-2017 (published in June 2017)The acquisition targets could meet the profit requirement under Rule 8.05 and there was no material concern about circumvention of new listing requirements. The Exchange decided to require aggregation of the Acquisitions and treat them as an extreme VSA (i.e. now known as extreme transaction).

Under the new rule, an issuer proposing to use the extreme transaction category must satisfy one of the additional eligibility criteria set out in Rule 14.06C(1). As there was a change in de facto control of Company A within the last 36 months and Company A would cease to operate its existing food business after the transactions. Should the amended Rules apply, Company A would not meet the additional eligibility criteria under Rule 14.06C(1). Accordingly, the Acquisitions would be classified as a reverse takeover (and not an extreme transaction).

50

51

Case study – Chong Kin Group Holdings Ltd. (1609.HK)Oct 2016 - Chong Kin is principally engaged in concrete placing services and other ancillary

services in Hong Kong and became listed in Oct 2016. Its is owned as to 75% byPioneer Investment at the time of listing, which is co-owned by Mr. Cheung and Mr. Chan (collectively, the "Original Controlling Shareholders")

The Original Controlling Shareholders undertook not to sell their interest below 30%within one year after listing

51

Nov 2017 - Mr. Zhang acquired the entire interests of the Original Controlling Shareholders in Chong Kin

Oct 2018 - Chong Kin acquired Zhong Jun Kai Xuan Automotive Leasing Company Limited* (中軍凱旋汽車租賃有限公司) from an I3P and entered into new energy vehicles andlogistics related services industry in the PRC. The acquisition is a discloseabletransaction

52

Case study – Chong Kin Group Holdings Ltd. (1609.HK)Dec 2018 - Chong Kin announced it would acquire 1,347 new energy vehicles

52

Apr 2019 - Chong Kin acquired finance leasing business in PRC from an I3P. The acquisition isa major transaction

Jun 2021 - Stock Exchange considers Chong Kin’s principal business has been changed to thenew energy vehicle and logistics and finance leasing business and Chong Kin is nolonger suitable for listing given the Disposal has already been completed

Jan 2021 - Chong Kin entered into a sale and purchase agreement to sell Chong Kin Group Ltd,the business of provision of concrete placing and other ancillary services in Hong Kong to the Original Controlling Shareholders (the "Disposal"). The Disposal is a discloseable transaction

53

Case study – Chong Kin Group Holdings Ltd. (1609.HK)

53

54

Case study – Chong Kin Group Holdings Ltd. (1609.HK)

Stock Exchange considers Chong Kin’s principal business has been changedto the new energy vehicle and logistics and finance leasing business after the disposal of Chong Kin Group Limited to the Original Controlling Shareholders in January 2021, and all of which took place within 27 months. The Disposal, the acquisitions of the new energy vehicle and logistics and finance leasing business by Chong Kin in October 2018 and April 2019 and the related acquisition of a total of 1,847 new energy vehicles in December 2018 should be treated as if they were one transaction and constitute a reverse takeover under Rule 14.06B.

54

55

Case study – Chong Kin Group Holdings Ltd. (1609.HK)Under Rule 14.54, Chong Kin would have been treated as if it were a new listing applicant and hence required to meet all the new listing requirements under Chapter 8 of the Listing Rules in order for it to be considered suitable for continued listing. Further, the new energy vehicle and logistics and finance leasing business did not meet the new listing requirements under Rule 8.05. Without going through the new listing procedures and complying with the relevant requirements, the Stock Exchange considers that Chong Kin is no longer suitable for listing given the Disposal has already been completed. Trading in Chong Kin’s shares will be suspended under Rule 6.01(4). Under Rule 6.01A(1), the Stock Exchange may cancel the listing of Chong Kin’s shares if trading remains suspended for a continuous period of 18 months.

55

Quiz(1) Question: What is the percentage ratio for a transaction to be treated as a VSA?a. ≥75%b. ≥100%c. ≥125%d. Satisfy the bright line test or principle based test under MB rule 14.06B

(2) Question: Which of the following is not a regulatory requirement for a major transaction?a. Notify Stock Exchangeb. Announce the transactionc. Seek shareholders' approvald. Appoint a financial adviser for due diligence

56

Quiz(3) Question: What is the period when transactions will normally be aggregated under the principle based test according to R14.06B Note 1?a. 12 monthsb. 36 daysc. 36 monthsd. transactions will not be aggregated under the principle based test

(4) Question: Which of the following transaction followed by a change in control of the listed issue will amount to an RTO under the bright line test?a. Major transactionb. Very substantial acquisition (VSA)c. Very substantial disposal (VSD)d. Extreme transaction

57

Answers

1) B2) D3) C4) B

58

For more details and enrolling, please visit the link below:-

https://www.hkicpa.org.hk/-/media/Document/MS/CPD/Flyer/2020/e-Series/FlyereSeries-Dec-2019.pdf

You may also be interested in other e-Series courses

End of Learning

Thank you very much

By : Mr. Jeremy Lau

60

Tel: (852) 6752-2521Email: [email protected]

Related Documents