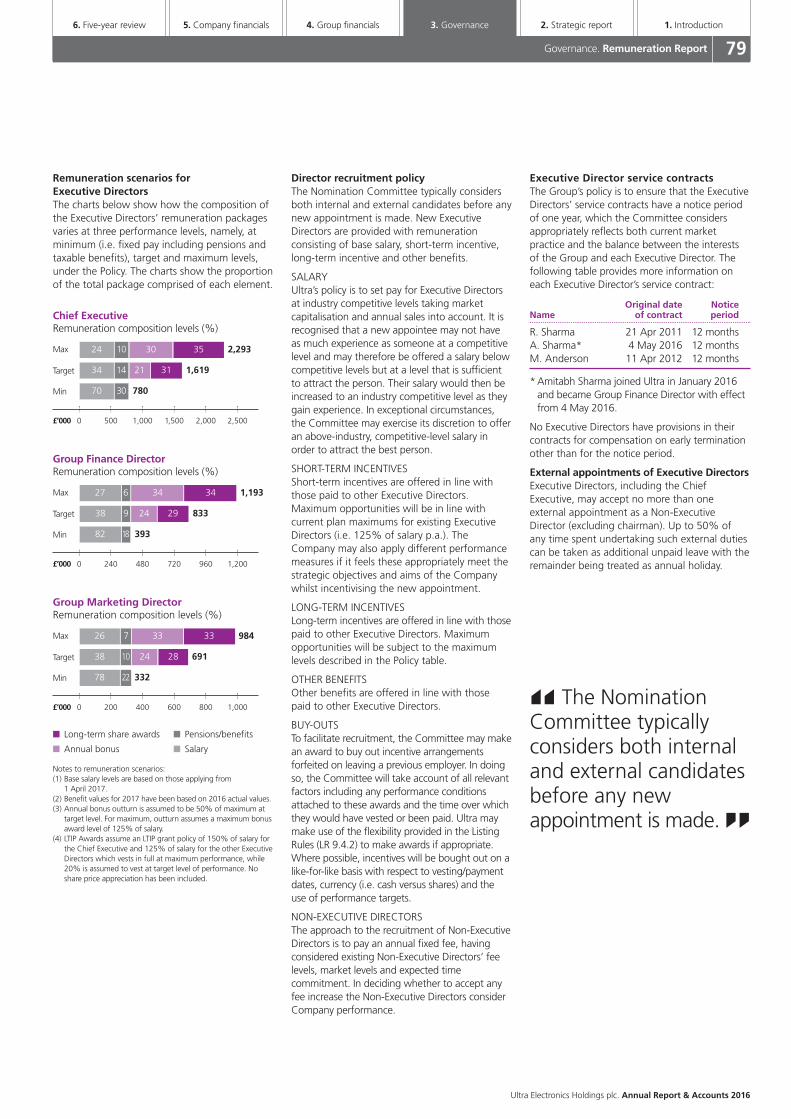

Ultra Electronics Holdings plc Annual Report and Accounts 2016 Why Ultra? We enjoy solving tough problems, beating our competitors and making a difference for our customers , shareholders and employees.

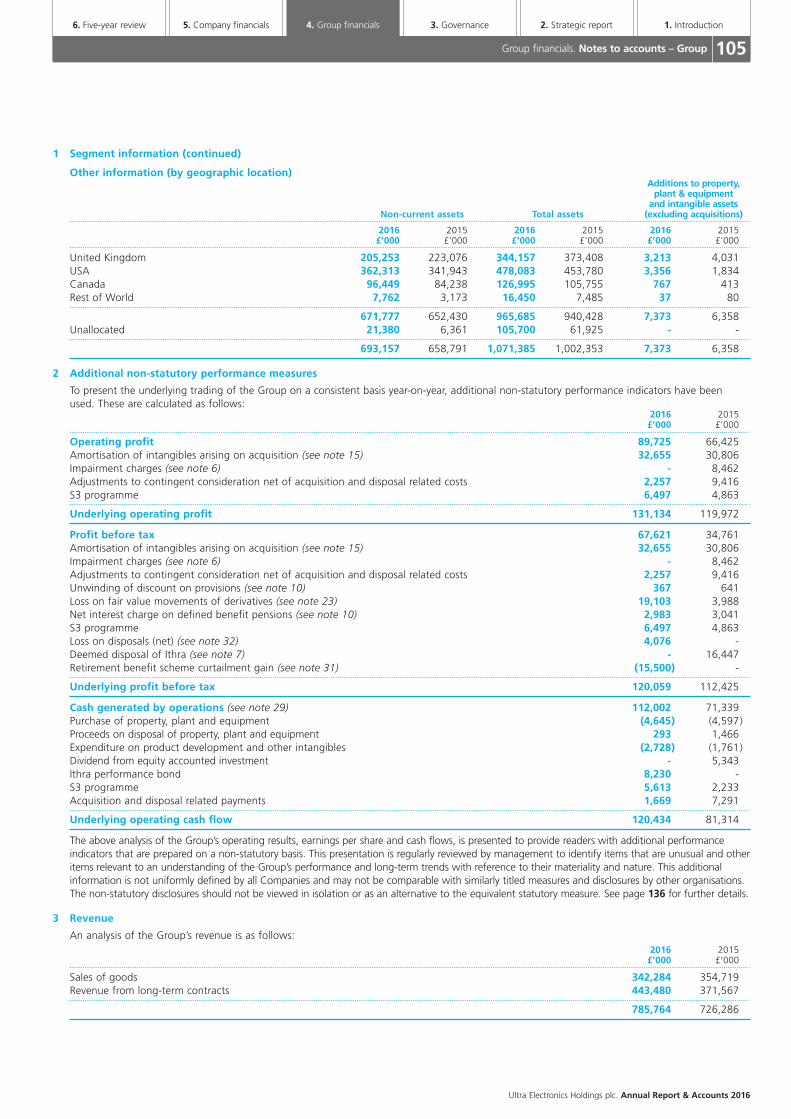

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

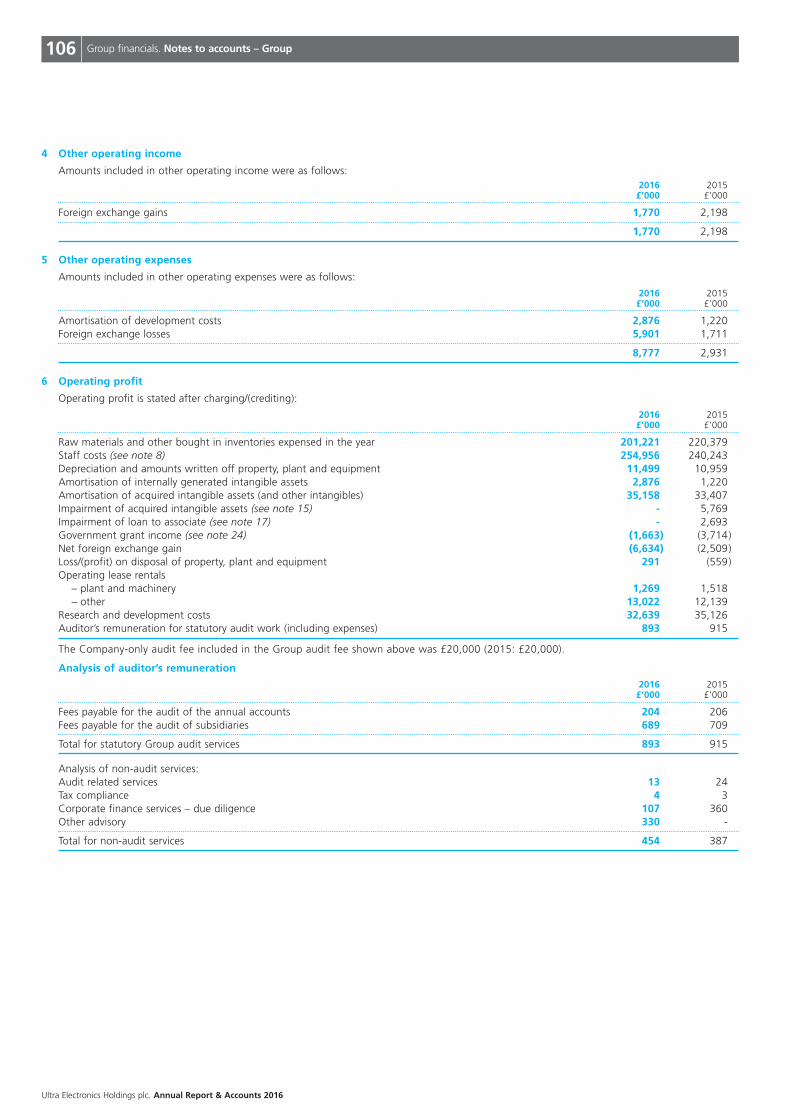

Ultra Electronics Holdings plcAnnual Report and Accounts 2016

Why Ultra?We enjoy solving tough problems, beating our competitors and making a difference for our customers, shareholders and employees.

1. IntroductionGroup at a glance 02

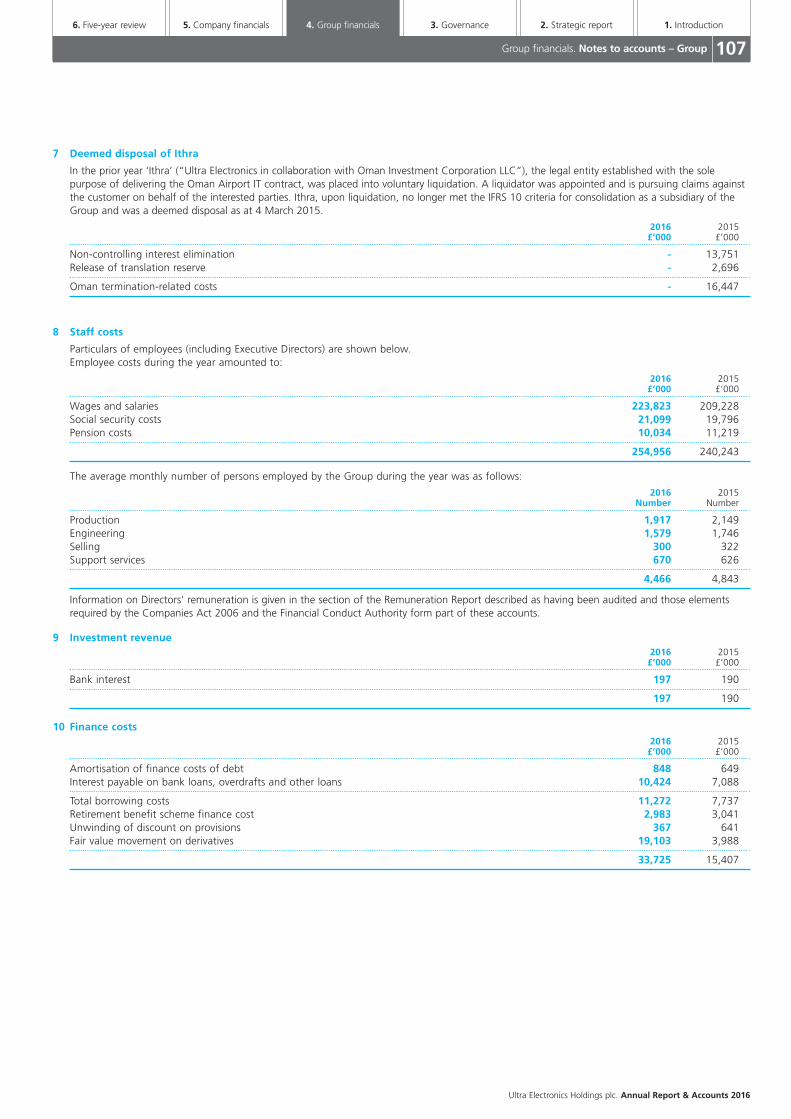

2. Strategic reportChief Executive’s review Rakesh Sharma, Chief Executive 04

Business model 08

Strategies for growth 10

Standardisation & Shared Services 12

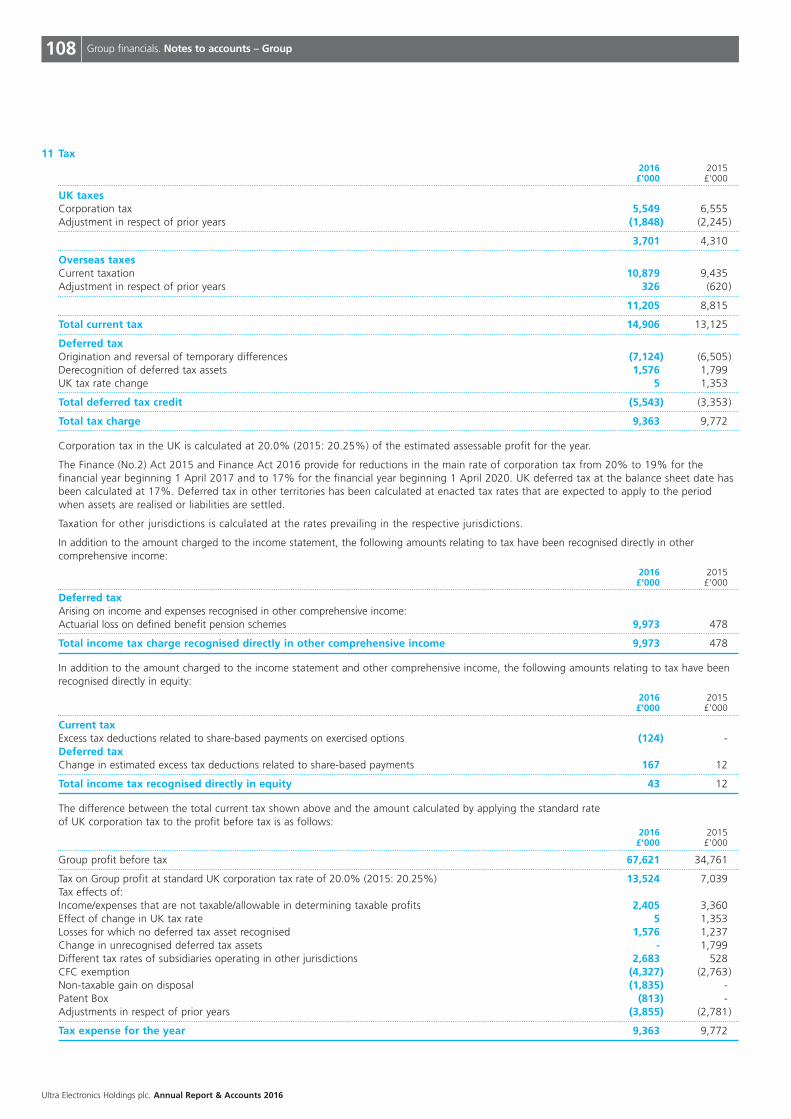

Market-facing segments 14

Financial review Amitabh Sharma, Group Finance Director 22

Key Performance Indicators 28

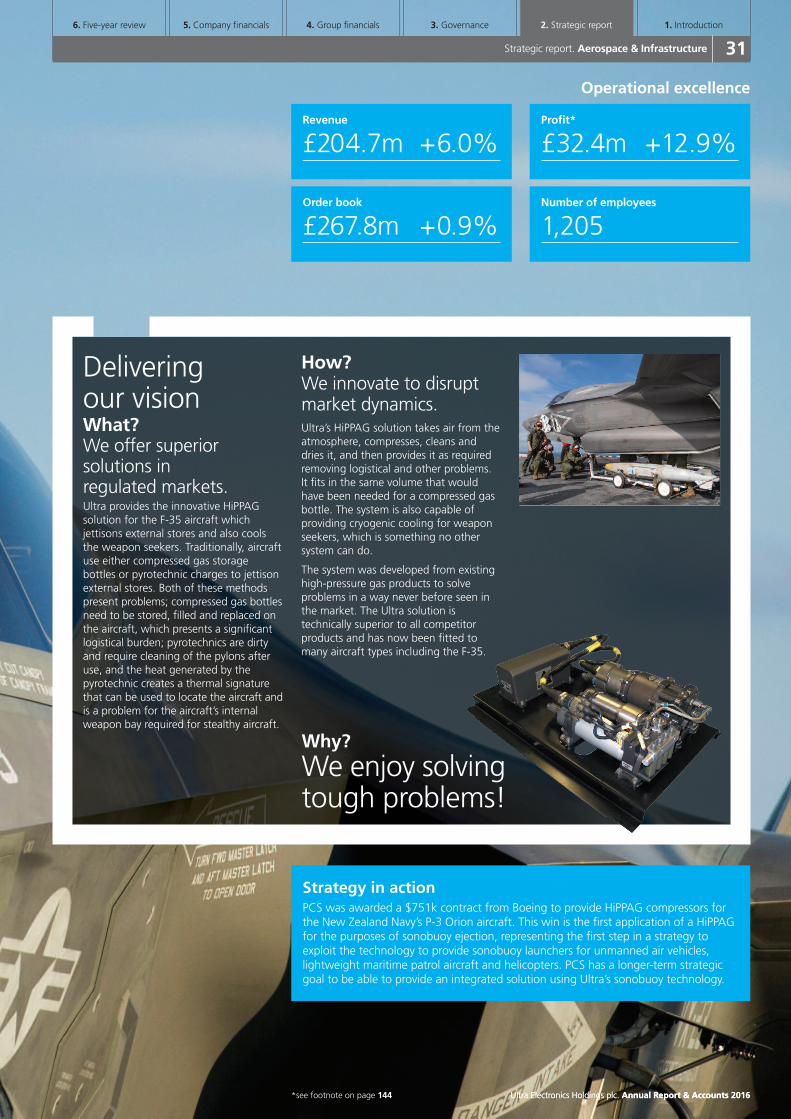

Aerospace & Infrastructure 30

Communications & Security 32

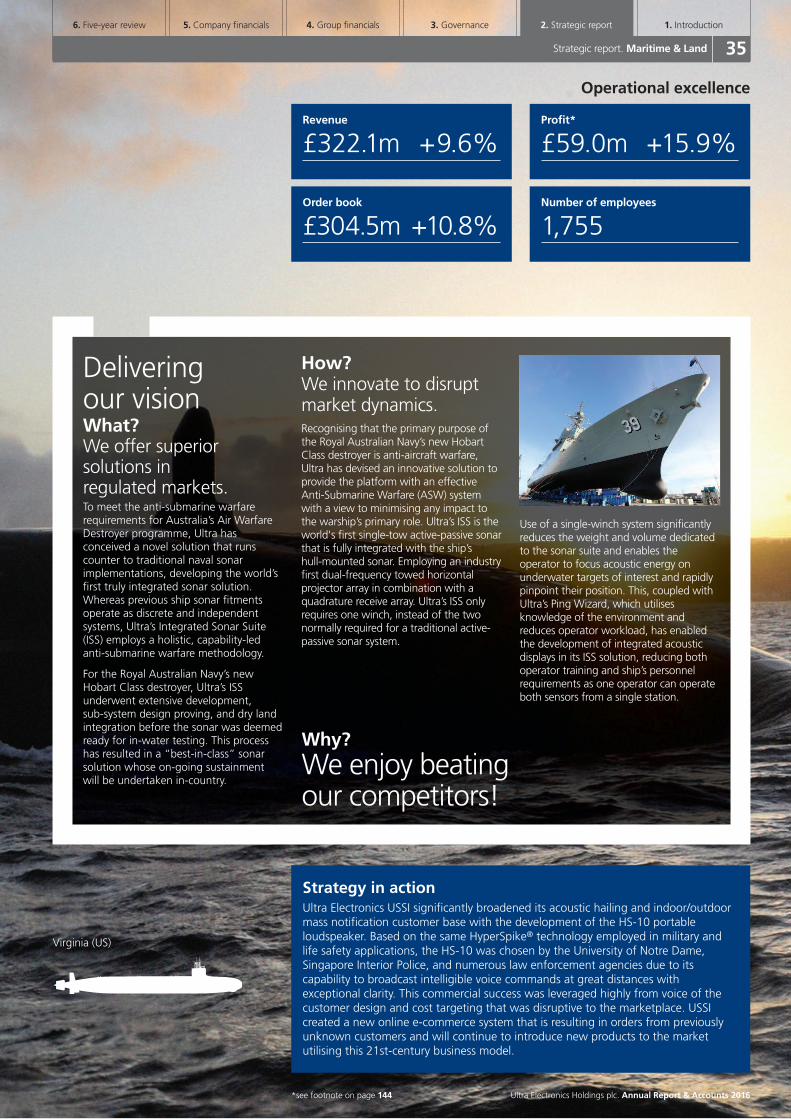

Maritime & Land 34

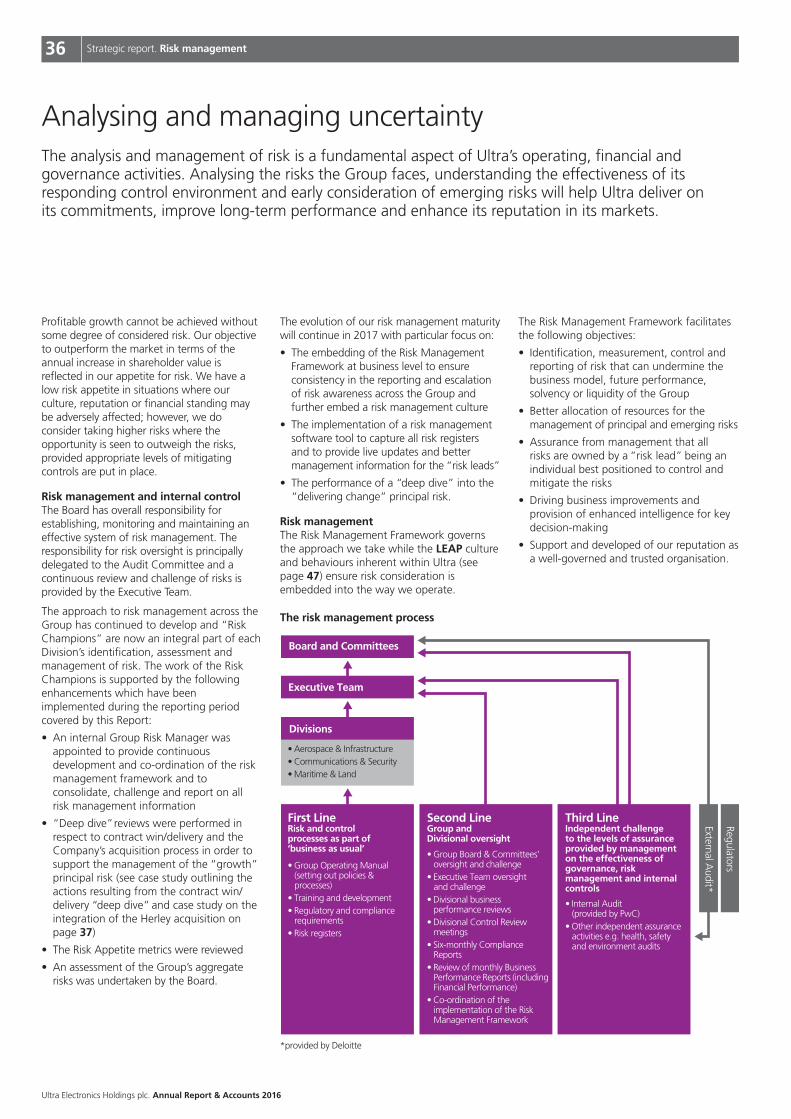

Risk management 36

Making a difference 44

Developing Ultra’s people 46

Corporate and social responsibility 51

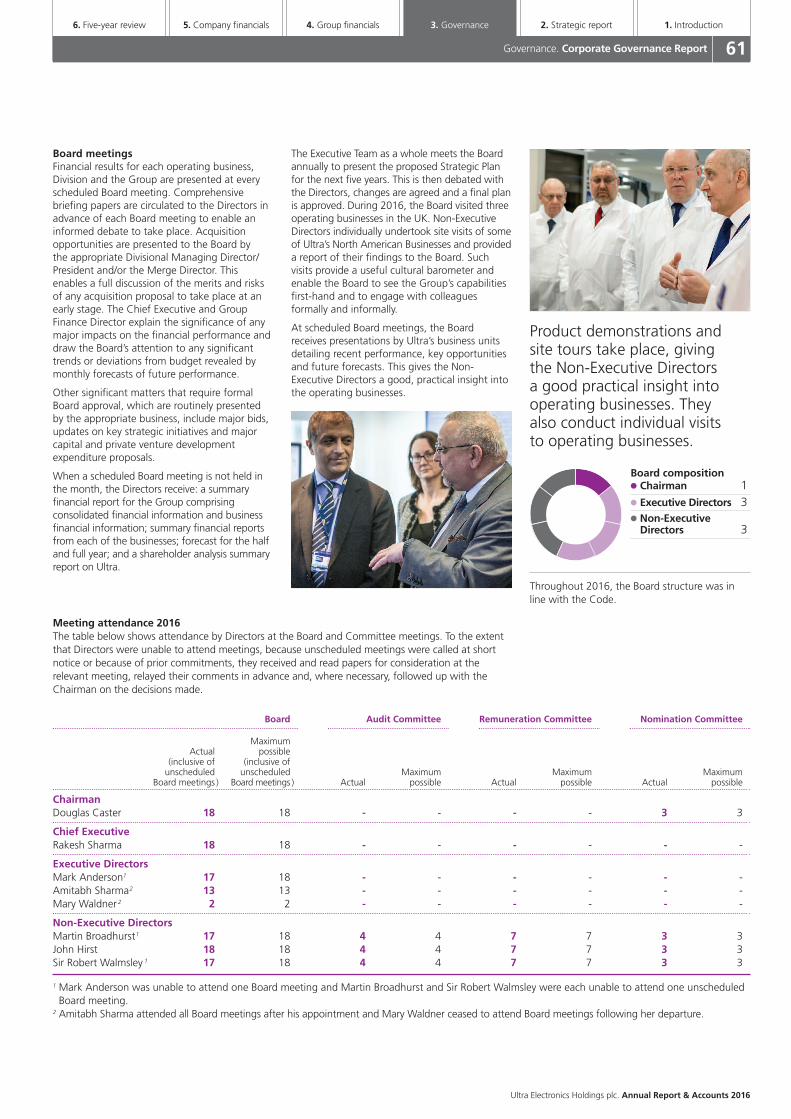

3. GovernanceBoard of Directors 54

Chairman’s governance statement Douglas Caster, Chairman 56

Corporate Governance Report 57

Nomination Committee Report 67

Audit Committee Report 69

Remuneration Report 74

Directors’ Report 89

Executives and advisors 91

4. Group financialsIndependent auditor’s report 92

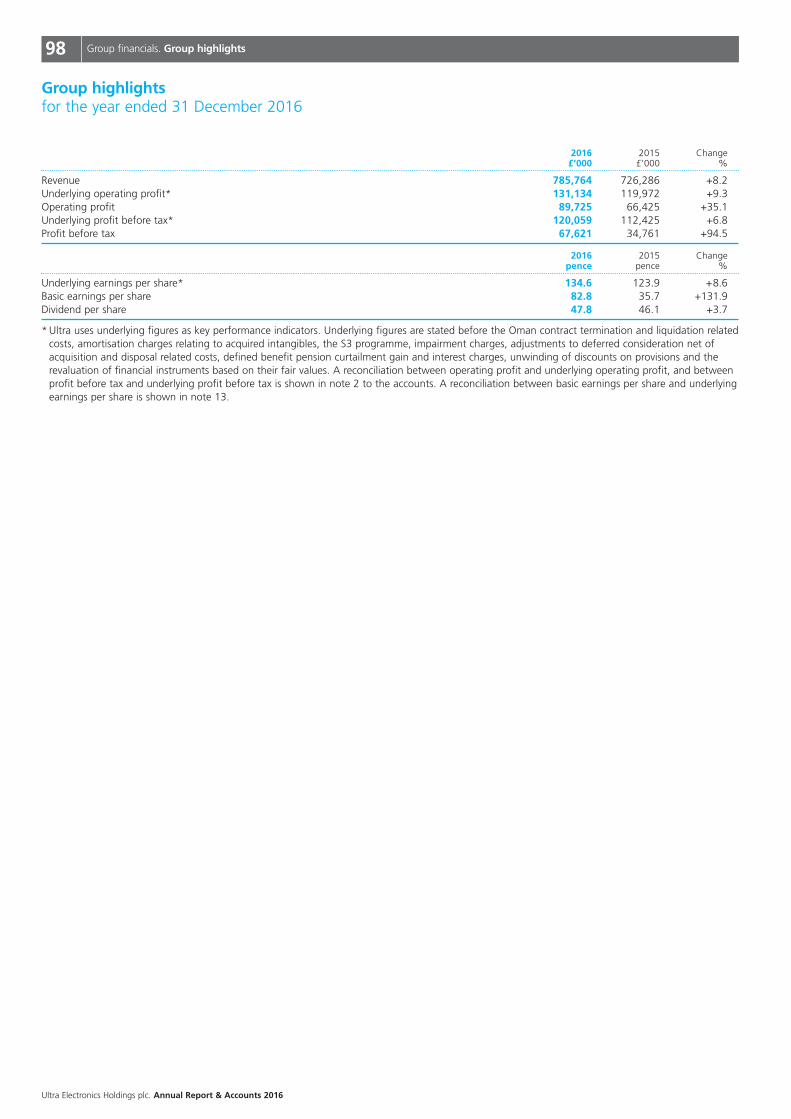

Group highlights 98

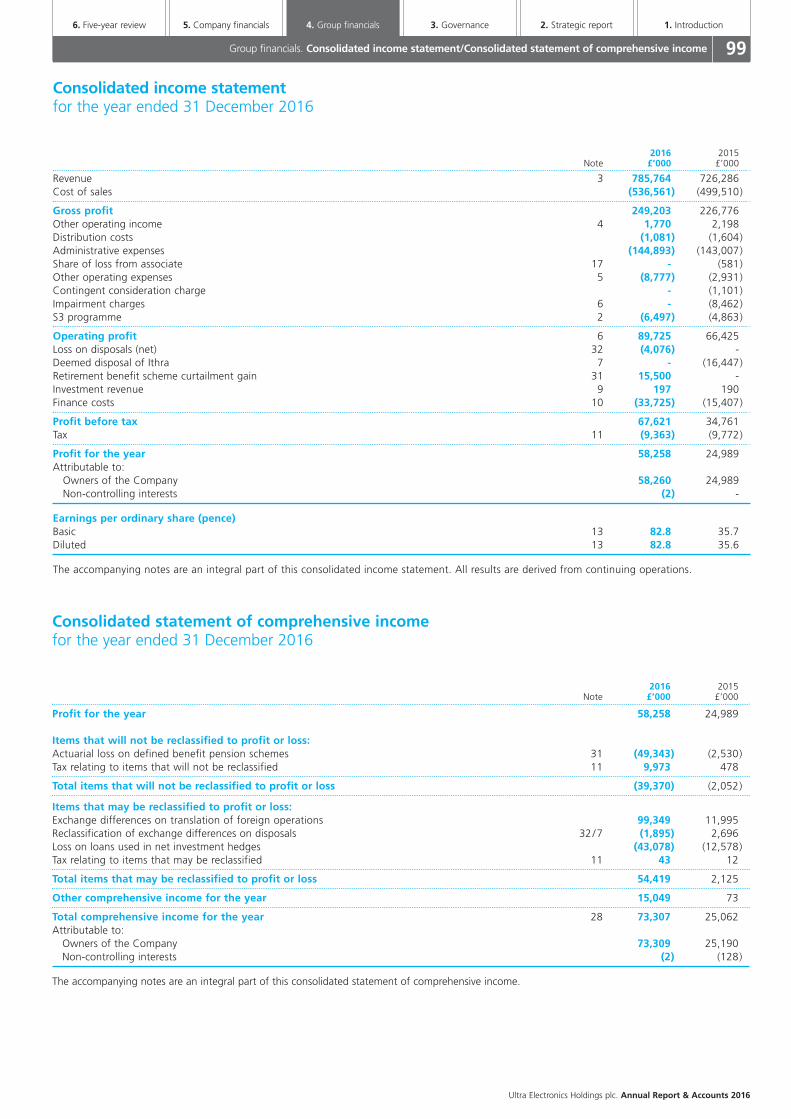

Consolidated income statement 99

Consolidated statement of comprehensive income 99

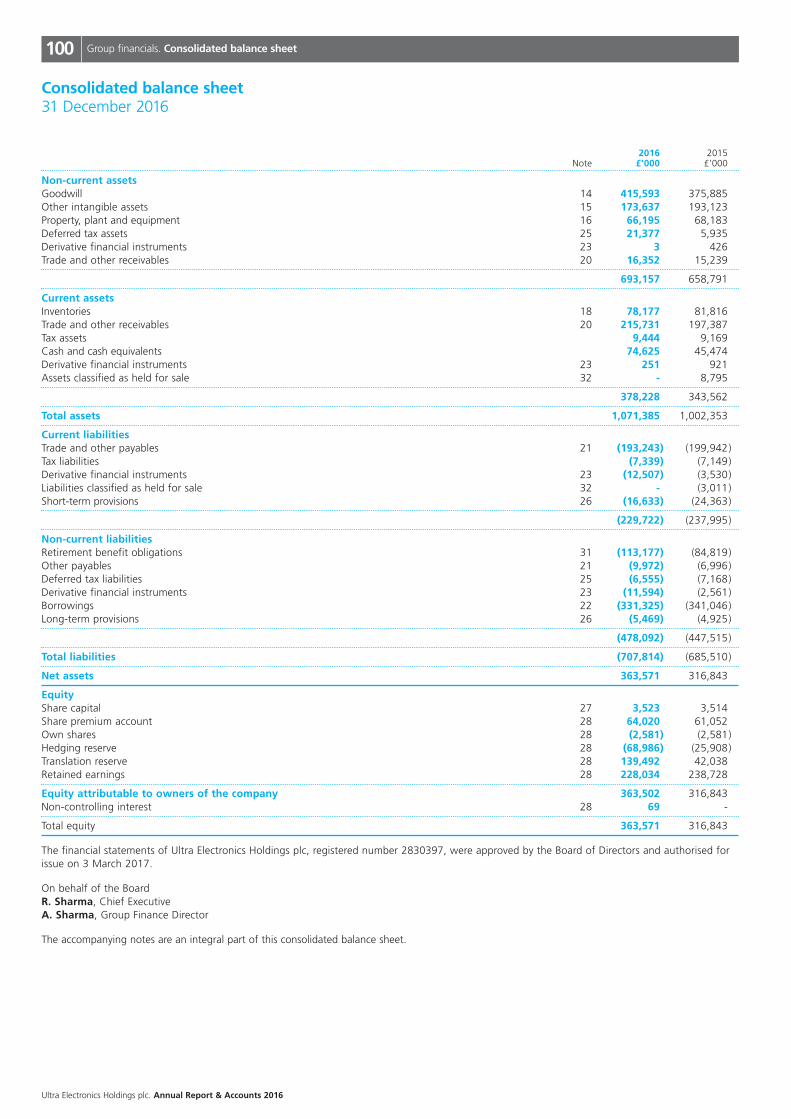

Consolidated balance sheet 100

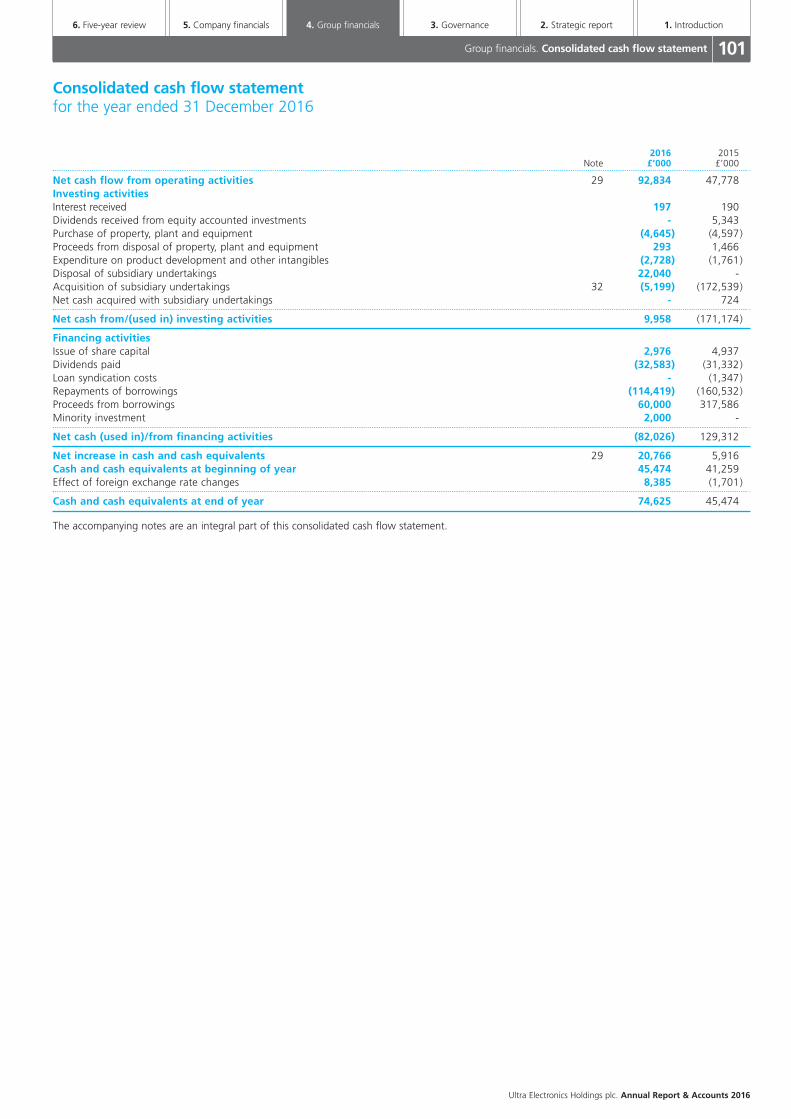

Consolidated cash flow statement 101

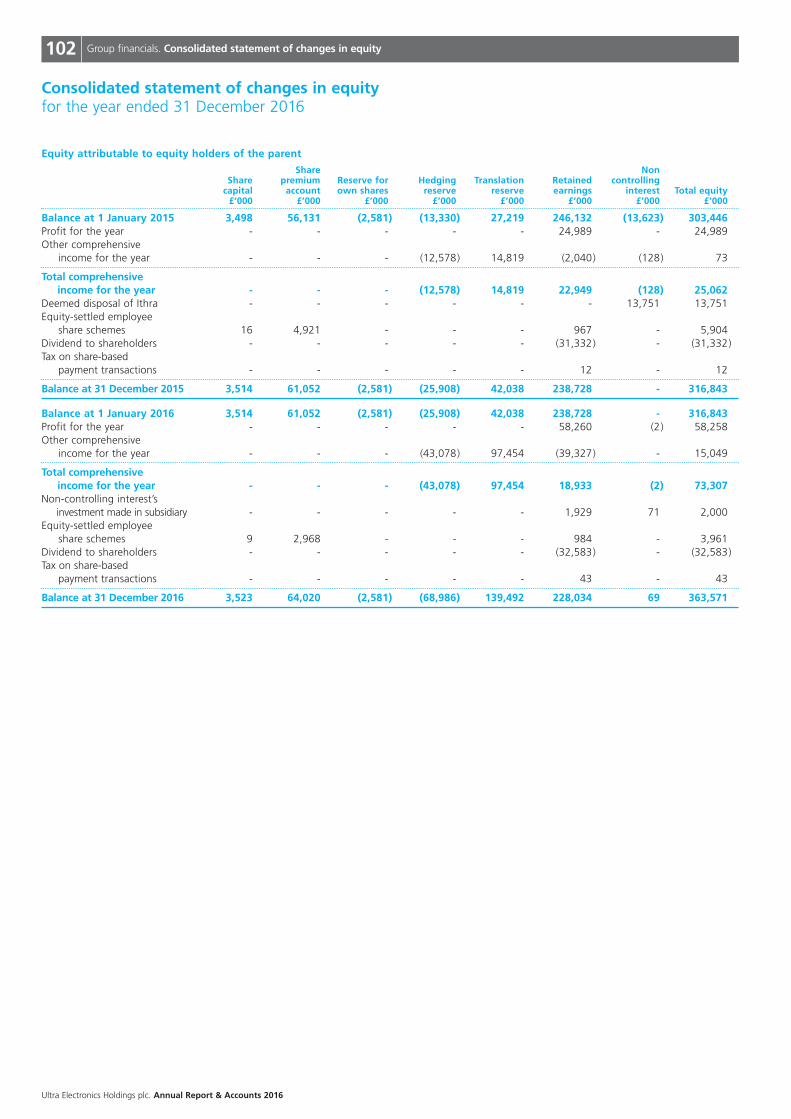

Consolidated statement of changes in equity 102

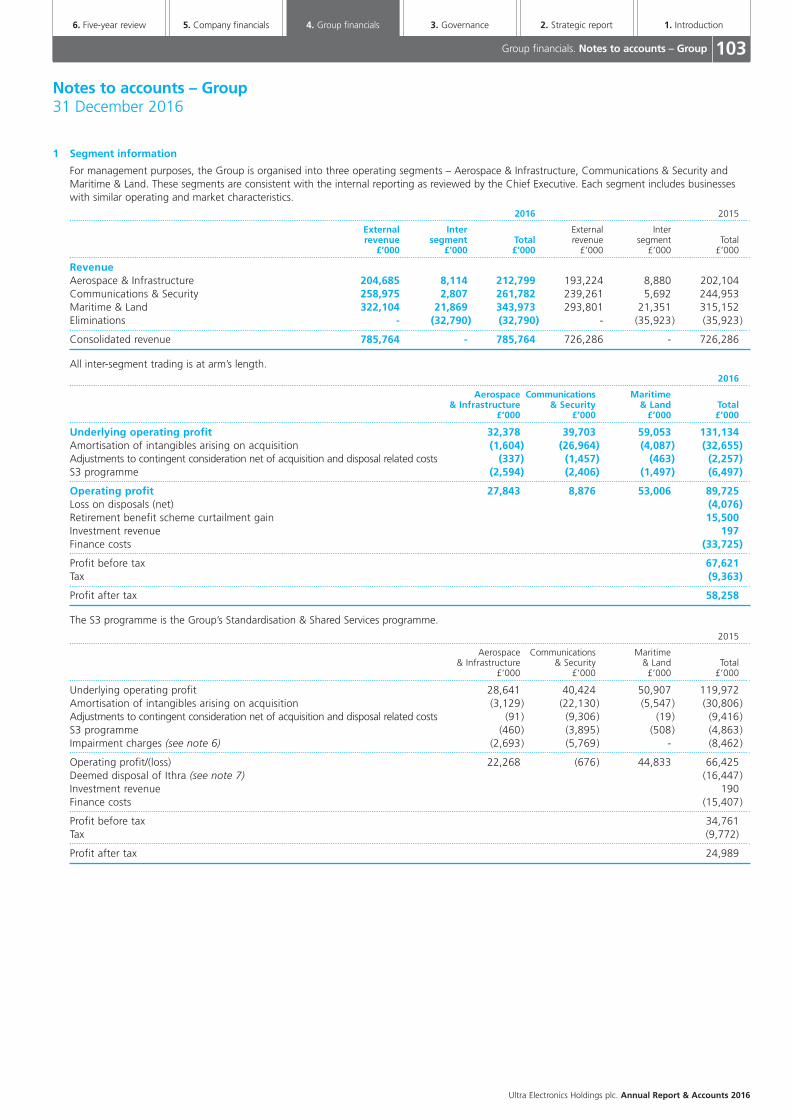

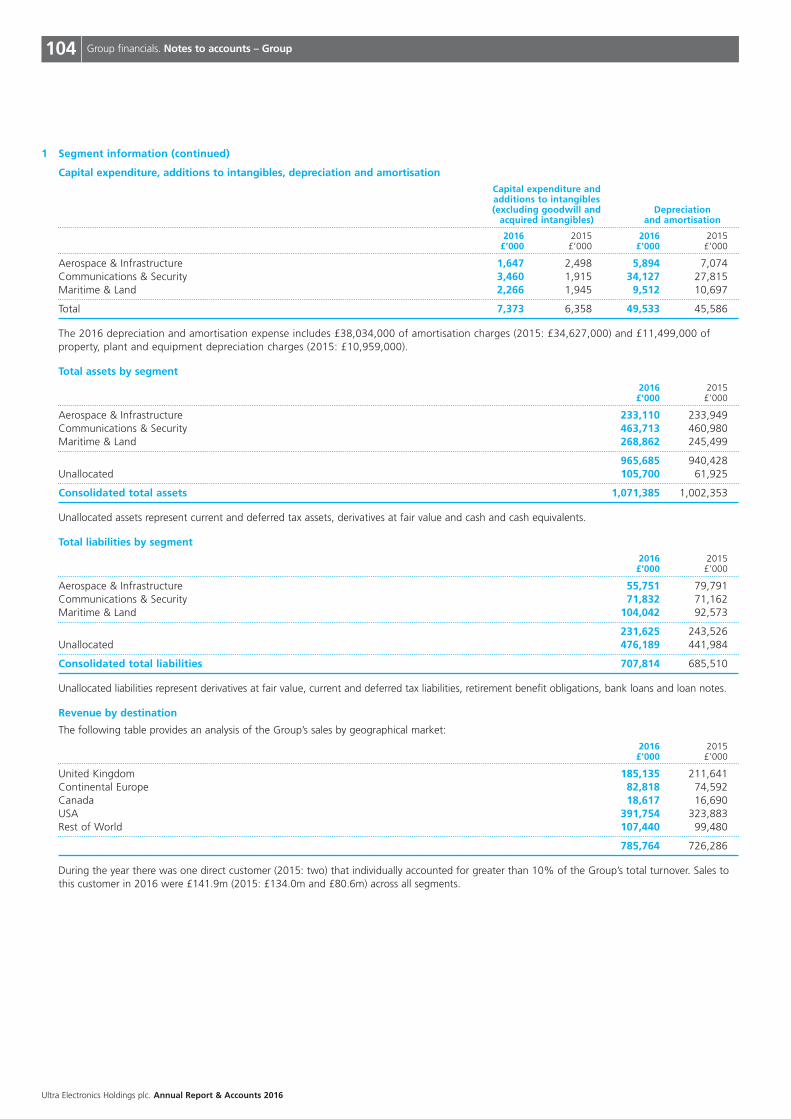

Notes to accounts 103

Statement of accounting policies in respect of the Group’s consolidated financial statements 131

5. Company financialsCompany balance sheet 138

Company statement of changes in equity 138

Notes to accounts 139

Statement of accounting policies for the Company accounts 142

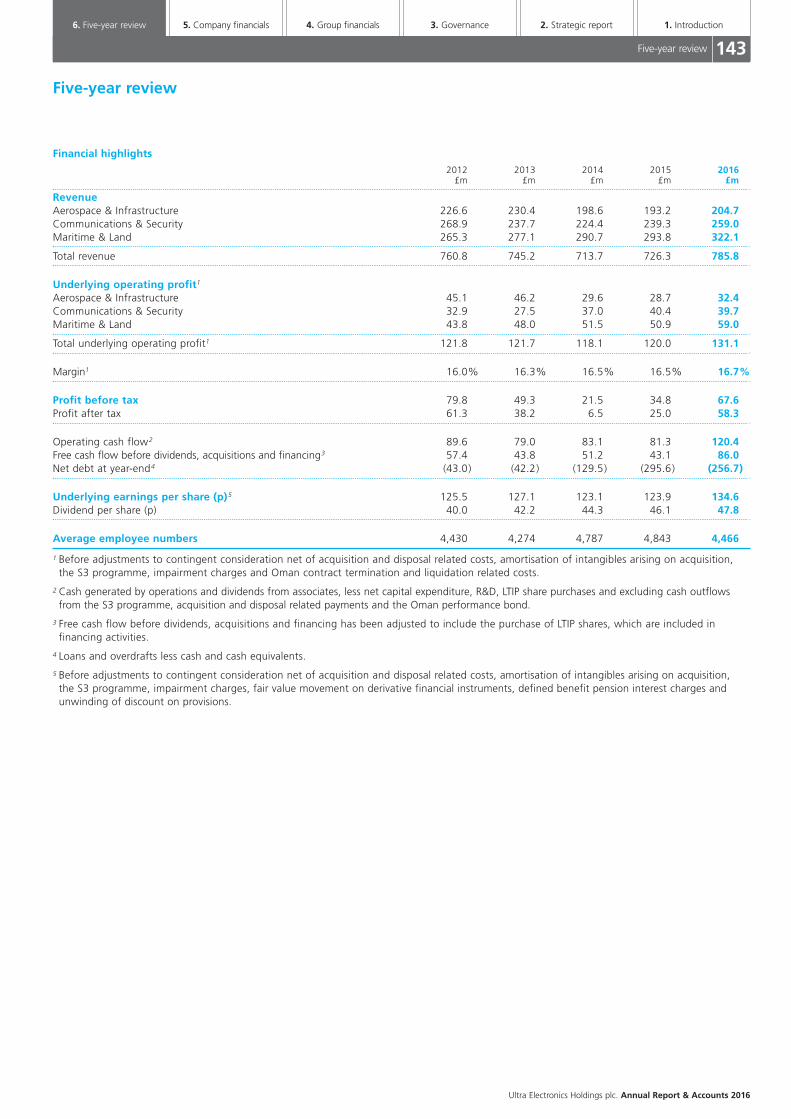

6. Five-year reviewFive-year review 143

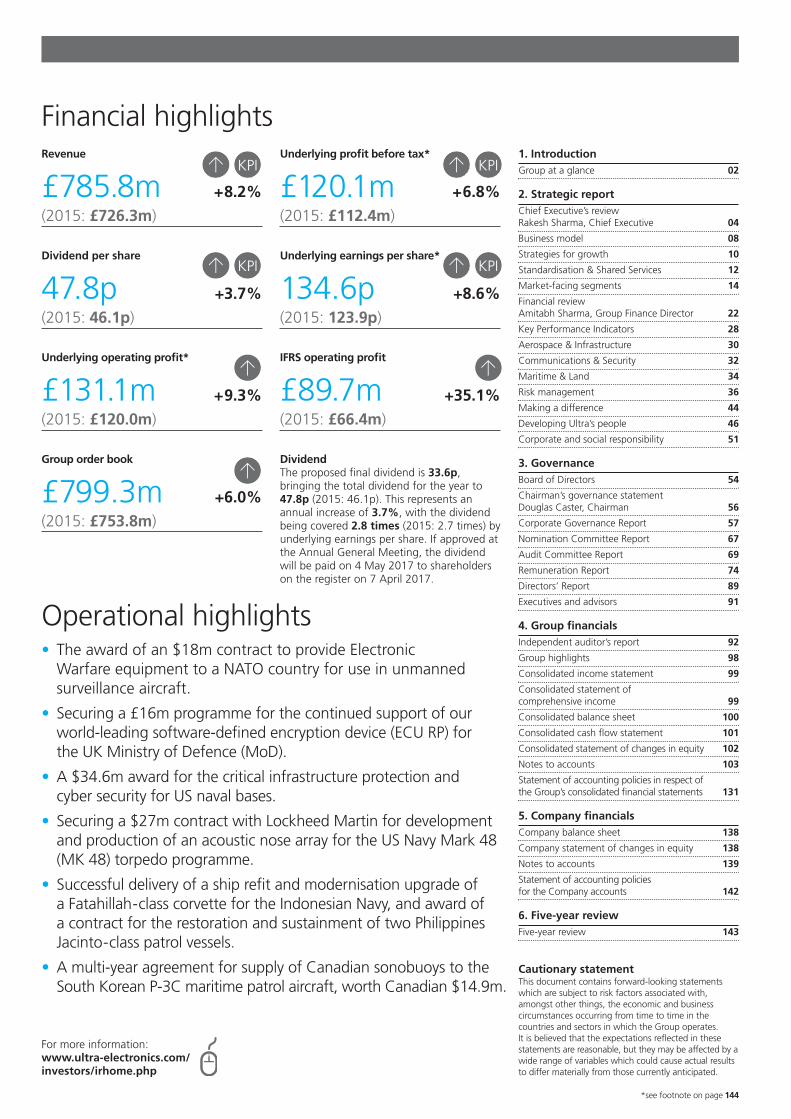

Financial highlights

Operational highlights• The award of an $18m contract to provide Electronic Warfare equipment to a NATO country for use in unmannedsurveillance aircraft.

• Securing a £16m programme for the continued support of ourworld-leading software-defined encryption device (ECU RP) for the UK Ministry of Defence (MoD).

• A $34.6m award for the critical infrastructure protection and cyber security for US naval bases.

• Securing a $27m contract with Lockheed Martin for developmentand production of an acoustic nose array for the US Navy Mark 48(MK 48) torpedo programme.

• Successful delivery of a ship refit and modernisation upgrade of a Fatahillah-class corvette for the Indonesian Navy, and award of a contract for the restoration and sustainment of two PhilippinesJacinto-class patrol vessels.

• A multi-year agreement for supply of Canadian sonobuoys to theSouth Korean P-3C maritime patrol aircraft, worth Canadian $14.9m.

Revenue

£785.8m +8.2%(2015: £726.3m)

Underlying profit before tax*

£120.1m +6.8%(2015: £112.4m)

Dividend per share

47.8p +3.7%(2015: 46.1p)

Underlying earnings per share*

134.6p +8.6%(2015: 123.9p)

Underlying operating profit*

£131.1m +9.3%(2015: £120.0m)

IFRS operating profit

£89.7m +35.1%(2015: £66.4m)

Group order book

£799.3m +6.0%(2015: £753.8m)

> KPI

> KPI

>

> KPI

> KPI

>>

For more information:www.ultra-electronics.com/investors/irhome.php

Cautionary statementThis document contains forward-looking statementswhich are subject to risk factors associated with,amongst other things, the economic and businesscircumstances occurring from time to time in thecountries and sectors in which the Group operates. It is believed that the expectations reflected in thesestatements are reasonable, but they may be affected by awide range of variables which could cause actual resultsto differ materially from those currently anticipated.

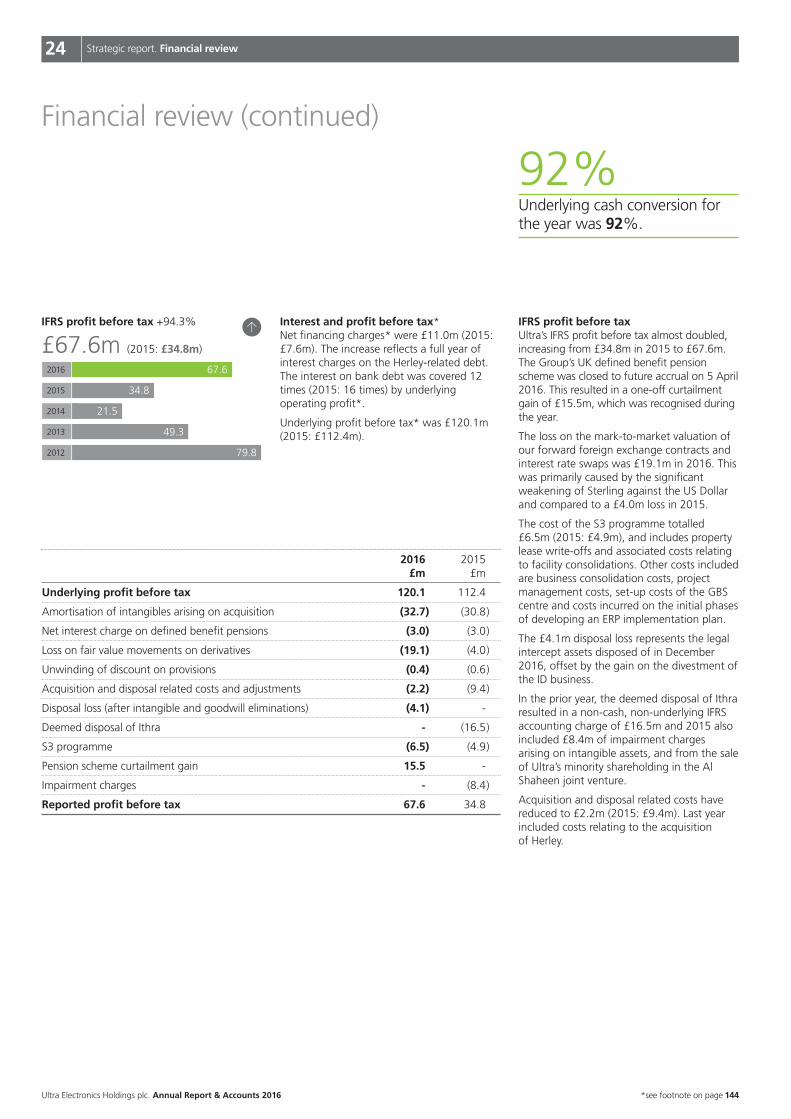

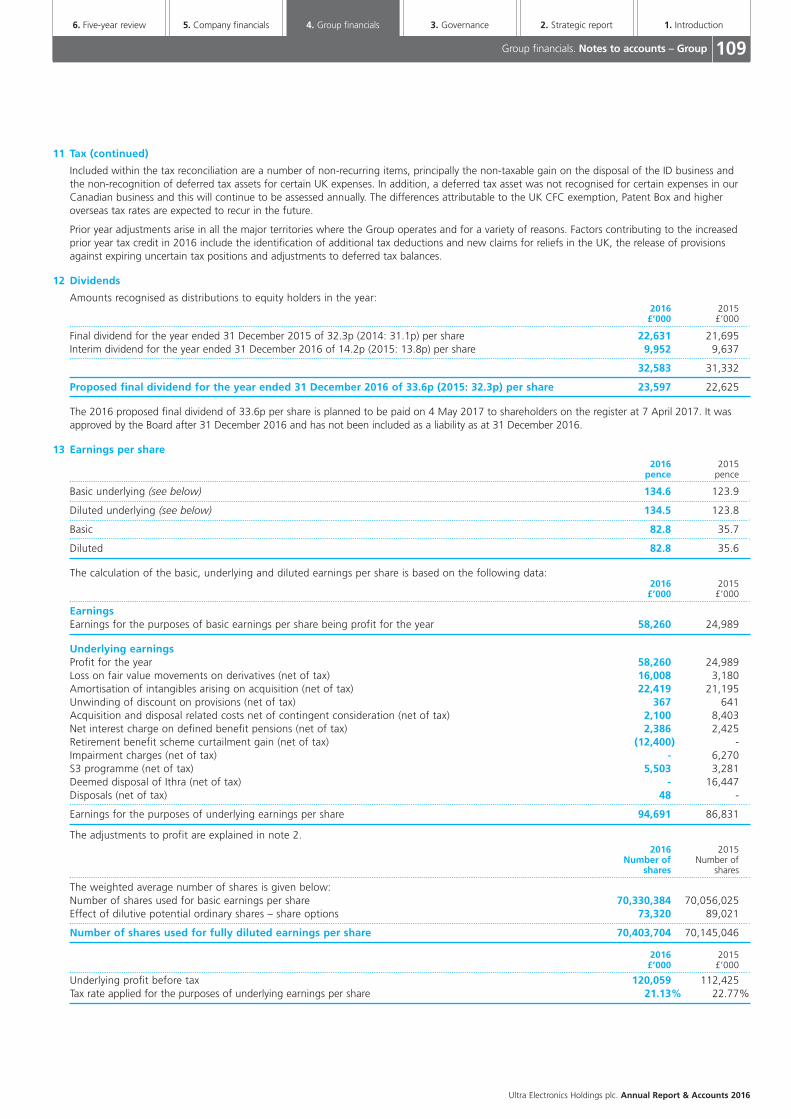

DividendThe proposed final dividend is 33.6p,bringing the total dividend for the year to47.8p (2015: 46.1p). This represents anannual increase of 3.7%, with the dividendbeing covered 2.8 times (2015: 2.7 times) byunderlying earnings per share. If approved atthe Annual General Meeting, the dividendwill be paid on 4 May 2017 to shareholderson the register on 7 April 2017.

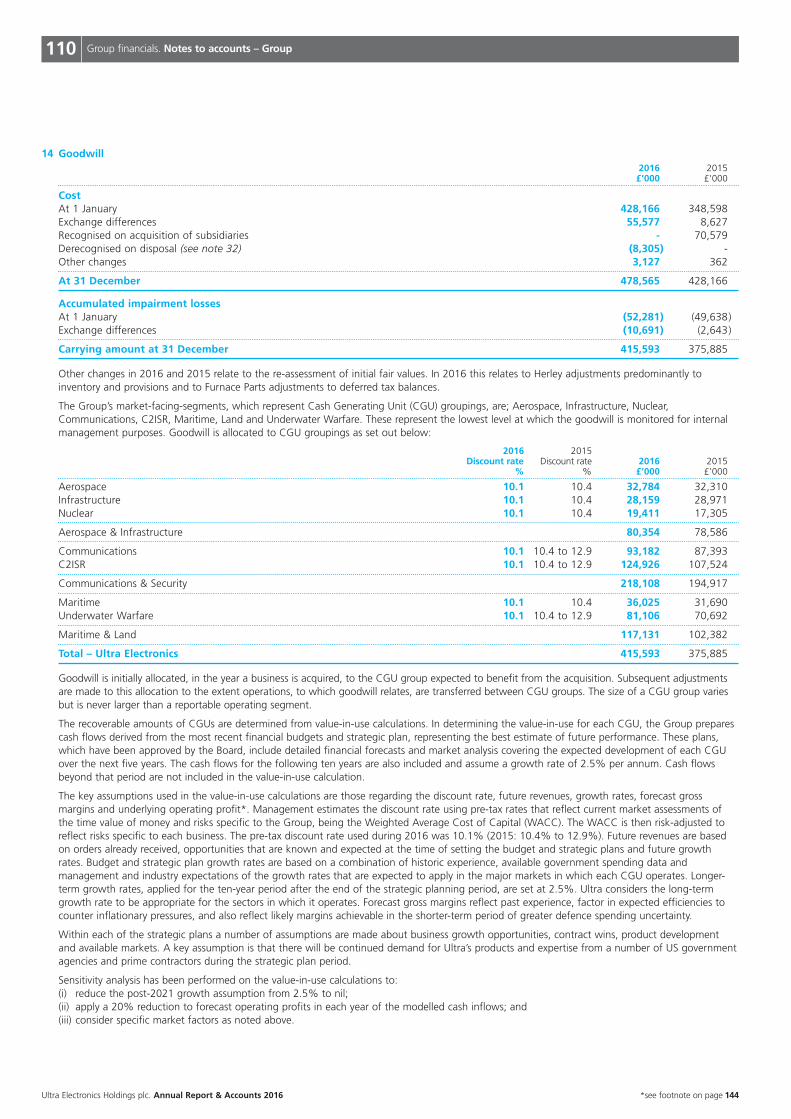

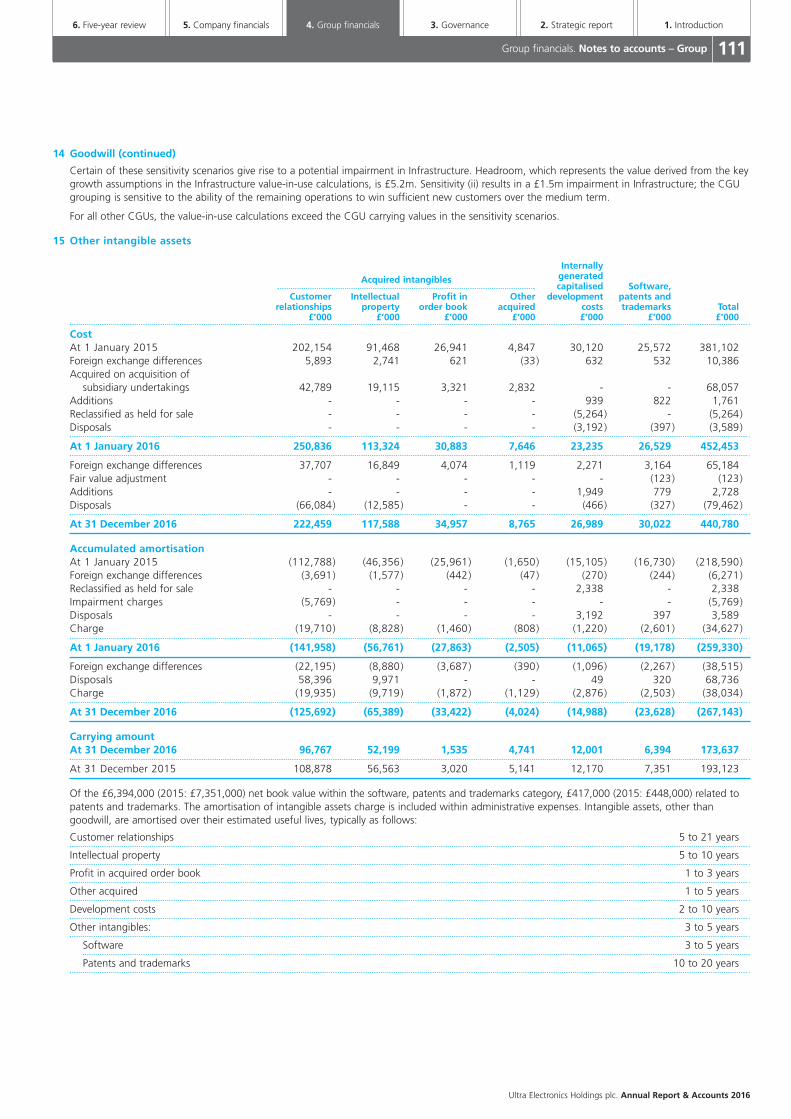

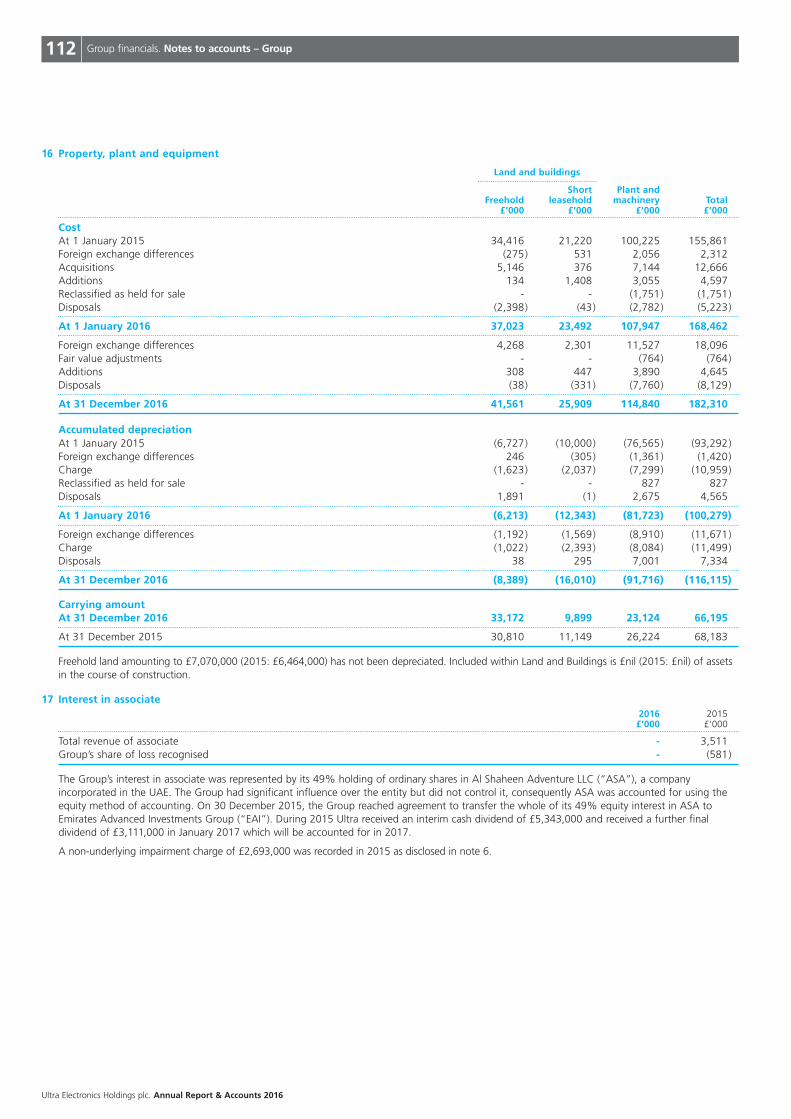

*see footnote on page 144

Portfoliostrength

Operationalexcellence

Focus oncustomer need

See pages 4-21 See pages 4-21

See pages 22-35

Outperform themarket in terms ofannual increases inshareholder return

Objective

Risk m

anagement See pages 36-43

Sust

aina

bilit

y

See p

ages 4

4-53

Good governan

ce Se

e pa

ges

54-9

1People and culture See pages 44-53

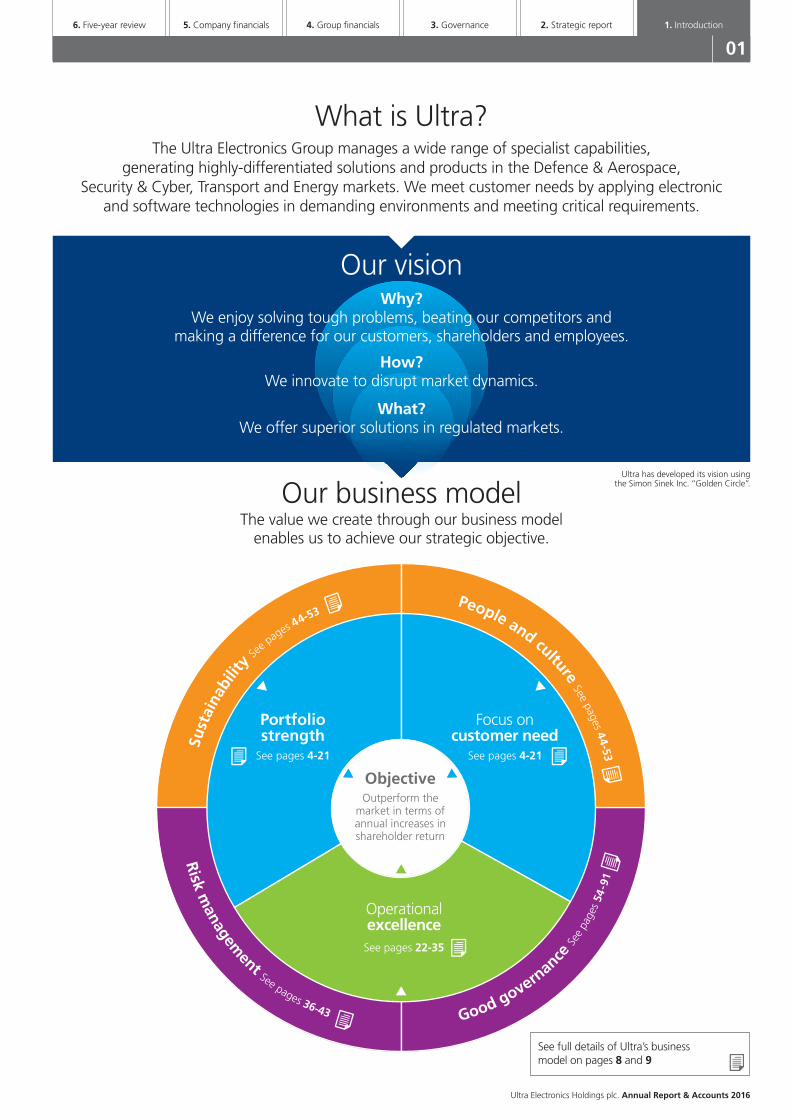

What is Ultra?The Ultra Electronics Group manages a wide range of specialist capabilities,

generating highly-differentiated solutions and products in the Defence & Aerospace, Security & Cyber, Transport and Energy markets. We meet customer needs by applying electronic

and software technologies in demanding environments and meeting critical requirements.

Our visionWhy?

We enjoy solving tough problems, beating our competitors and making a difference for our customers, shareholders and employees.

How?We innovate to disrupt market dynamics.

What?We offer superior solutions in regulated markets.

Our business modelThe value we create through our business model enables us to achieve our strategic objective.

1. Introduction2. Strategic report3. Governance4. Group financials5. Company financials6. Five-year review

01

Ultra Electronics Holdings plc. Annual Report & Accounts 2016

See full details of Ultra’s business model on pages 8 and 9

Ultra has developed its vision using the Simon Sinek Inc. “Golden Circle”.

Ultra Electronics Holdings plc. Annual Report & Accounts 2016

Ultra continues to focus on its main markets of Defence & Aerospace, Security & Cyber,Transport and Energy. To explain its wideportfolio of capabilities more effectively, theGroup uses market segmentation. Each of the eight segments generate highly-differentiated, cost-effective and proventechnologies at the system, sub-system andcomponent level. These technologies are oftenfundamental to the performance, safety ormission success of the platforms in which theyare incorporated, making Ultra a critical supplier on many complex platforms, enjoying long-term positions.

The segment structure allows Ultra to harnessthe capabilities of its 19 businesses together,providing technical expertise and domainknowledge to deliver the adaptable,comprehensive and cost-effective solutionscustomers demand. Where required, the Groupwill seek partners with best-of-breed suppliersto offer a more complete solution and willseamlessly “lead or follow” as a non-threatening mid-tier company in order to satisfycustomer needs. Equally, individual businessescontinue to develop and supply the specifichigh-end technologies for which they are wellknown, providing the agility and responsivenessof a smaller, autonomous business unit. Tomaintain its position, the Group harnesses bothinternal and customer-funded research anddevelopment, tailoring its solutions to changingcustomer needs and budgets. This sustains theGroup’s reputation as an innovative supplier ofenabling technology.

Ultra’s core markets remain North Americaand the United Kingdom. In mainlandEurope the Group generally suppliestechnologies that are unavailable fromindigenous suppliers, for example,sonobuoys. Given this relatively low exposureto mainland Europe, the UK decision to exitthe EU (BREXIT) has not had a significantspecific impact on the Group, globalmacroeconomic impacts aside. Elsewhere inthe world, the Group has developed strategicpositions in its target regions of Australia,the Middle East, India, and (for non-defenceproducts) China, while continuing to pursueindividual opportunities and businessrelationships in many other nations. Lookingahead, Japan is considered a promisingmarket for Ultra. These core markets andtarget regions allow Ultra to access thelargest addressable defence and securitybudgets in the world, positioning for long-term growth through well-consideredpartnerships and government relationships.

This market position, together with Ultra’sindependence, allows the Group to workclosely with the world’s prime contractors inour chosen markets. The chart above showsUltra’s major customers, including the USDepartment of Defense (DoD), the UKMinistry of Defence (MoD) and LockheedMartin. The Group supplies to a wide rangeof project offices, integrated project teamsand platform teams, having a larger numberof different partners and customers than thechart might at first suggest, and executingagainst tens of thousands of contracts andproduction orders on an annual basis.

How and where Ultra operates

1 United Kingdom 24

2 North America 52

3 Mainland Europe 10

4 Rest of the world 14

% of Group revenue by market

1 Defence & Aerospace 64

2 Security & Cyber 18

3 Transport & Energy 18

% of Group revenue by region

2

3

41

2

3

1

5 10 15 20 25% 30

US DoD

UK MoD

Lockheed Martin

BAE Systems

Boeing

Australian DoD

Northrop Grumman

US Alcohol, Tobacco & Firearms

Raytheon

EDF Energy

Thales

Rolls Royce

Level 3 for US Navy

Airbus

UTC

See Ultra’s business model on pages 8 and 9

Ultra’s place in the market

Where Ultraoperates

Ultra’s customers

2016 saw the embedding of Ultra’s three new Divisions; Aerospace & Infrastructure,Communications & Security and Maritime & Land, through which it delivers and reportsits performance. Ultra’s Divisions deliver specialist capabilities to our key end markets ofDefence & Aerospace, Security & Cyber, Transport and Energy. The Group addressesthese end markets through eight distinct market segments, discussed on pages 14 to 21.

02 Group at a glance. How and where Ultra operates

Ultra Electronics Holdings plc. Annual Report & Accounts 2016

For more information on Ultra’s Divisions see pages 30-35

*see footnote on page 144

Market segments

1. Aerospace

2. Infrastructure

3. Nuclear

Revenue

£204.7m +6.0%2015: £193.2m

Underlying operating profit*

£32.4m +12.9%2015: £28.7m

Order book

£267.8m +0.9%2015: £265.4m

Market segments

4. Communications

5. C2ISR+

Revenue

£259.0m +8.2%2015: £239.3m

Underlying operating profit*

£39.7m -1.7%2015: £40.4m

Order book

£227.0m +6.2%2015: £213.7m

Market segments

6. Underwater warfare

7. Maritime

8. Land

Revenue

£322.1m +9.6%2015: £293.8m

Underlying operating profit*

£59.0m +15.9%2015: £50.9m

Order book

£304.5m +10.8%2015: £274.7m

% of Group revenue % of Group profit*

26% 25%

% of Group revenue % of Group profit* % of Group revenue % of Group profit*

33% 30% 41% 45%

Aerospace & Infrastructure

Communications& Security

Maritime & Land

+ Command & Control, Intelligence, Surveillance and Reconnaissance Ultra’s Cyber capabilities sit primarily in C2ISR andCommunications, but run across all eight segments

1. Introduction2. Strategic report3. Governance4. Group financials5. Company financials6. Five-year review

03Group at a glance. How and where Ultra operates

2

4

6

7 8

5

3

1

Chief Executive’s review

A year of surprises and opportunities2016 will be remembered as a year of shocksand surprises. The UK electorate’s surprisedecision to exit the European Union (BREXIT)was a result that continues to cause UKbusinesses uncertainty. Despite having a lessimmediate impact on the national economy,concerns remain regarding long-term UKinflation and currency instability as the detailsof withdrawal emerge. Ultra is largelyinsulated from the direct impacts of BREXIT,with exports from the UK to mainland Europecontributing just 7% of Group revenue, andminimal dependency on the free movementof skilled staff. Indeed, our much greaterexposure to the US should providereassurance to our investors during a periodof such uncertainty.

The US election provided the second majorshock of the year with the full implicationsyet to be realised. However, there is now astrong expectation in the market of a returnto growth of about 3% in the defence sector,fuelled by increased US defence spending.This will need to be enabled by the expectedearly repeal of the Budget Control Act andaction to achieve an agreed defence budgetfor FY17. President Trump is also insistentthat those allies living under a US defenceumbrella “pay their way”, implying increaseddefence expenditure in those nations. Initialsigns of the new Administration’scommitment to closer working with the UK,on both trade and defence, are also positiveindicators for Ultra given that they representUltra’s two largest markets.

Rakesh Sharma Chief Executive

We are wellprepared to exploitthe challenges andopportunities in ourmarket and returnUltra to growth.

“

”

Ultra Electronics Holdings plc. Annual Report & Accounts 2016

04 Strategic report. Chief Executive’s review

Portfolio strength focused on customer need

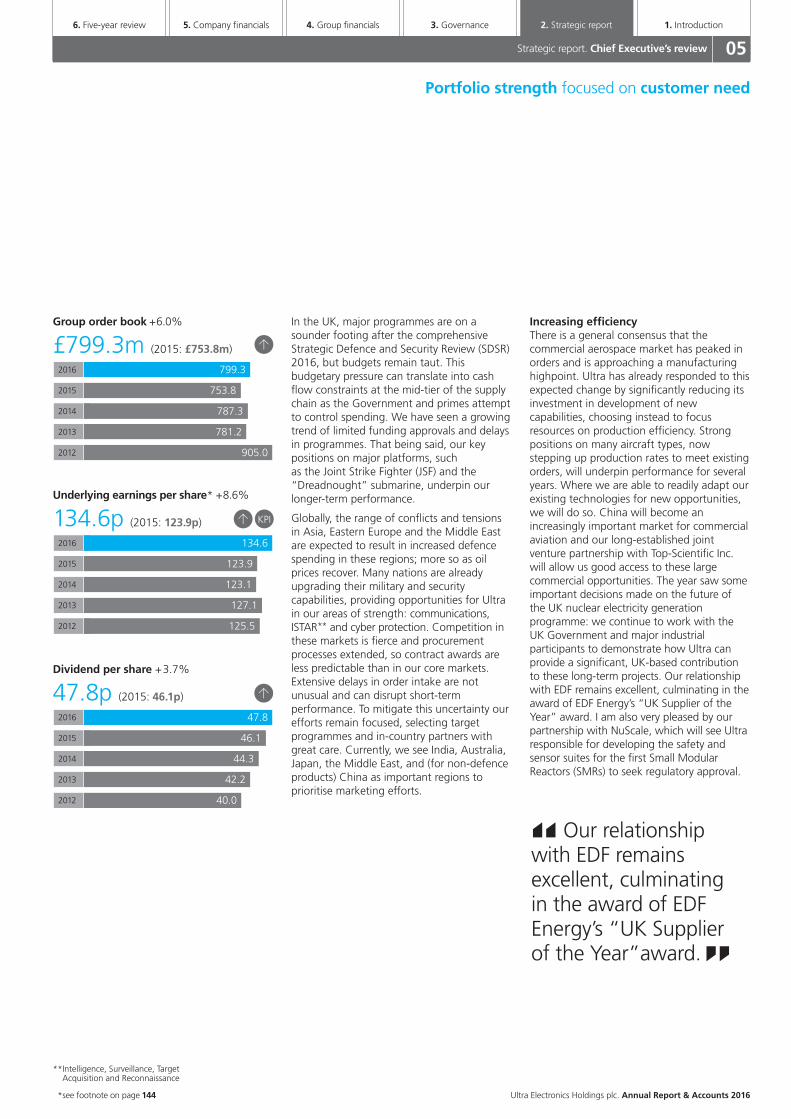

In the UK, major programmes are on asounder footing after the comprehensiveStrategic Defence and Security Review (SDSR)2016, but budgets remain taut. Thisbudgetary pressure can translate into cashflow constraints at the mid-tier of the supplychain as the Government and primes attemptto control spending. We have seen a growingtrend of limited funding approvals and delaysin programmes. That being said, our keypositions on major platforms, such as the Joint Strike Fighter (JSF) and the“Dreadnought” submarine, underpin ourlonger-term performance.

Globally, the range of conflicts and tensionsin Asia, Eastern Europe and the Middle Eastare expected to result in increased defencespending in these regions; more so as oilprices recover. Many nations are alreadyupgrading their military and securitycapabilities, providing opportunities for Ultrain our areas of strength: communications,ISTAR** and cyber protection. Competition inthese markets is fierce and procurementprocesses extended, so contract awards areless predictable than in our core markets.Extensive delays in order intake are notunusual and can disrupt short-termperformance. To mitigate this uncertainty ourefforts remain focused, selecting targetprogrammes and in-country partners withgreat care. Currently, we see India, Australia,Japan, the Middle East, and (for non-defenceproducts) China as important regions toprioritise marketing efforts.

Increasing efficiencyThere is a general consensus that thecommercial aerospace market has peaked inorders and is approaching a manufacturinghighpoint. Ultra has already responded to thisexpected change by significantly reducing itsinvestment in development of newcapabilities, choosing instead to focusresources on production efficiency. Strongpositions on many aircraft types, nowstepping up production rates to meet existingorders, will underpin performance for severalyears. Where we are able to readily adapt ourexisting technologies for new opportunities,we will do so. China will become anincreasingly important market for commercialaviation and our long-established jointventure partnership with Top-Scientific Inc.will allow us good access to these largecommercial opportunities. The year saw someimportant decisions made on the future ofthe UK nuclear electricity generationprogramme: we continue to work with theUK Government and major industrialparticipants to demonstrate how Ultra canprovide a significant, UK-based contributionto these long-term projects. Our relationshipwith EDF remains excellent, culminating in theaward of EDF Energy’s “UK Supplier of theYear” award. I am also very pleased by ourpartnership with NuScale, which will see Ultraresponsible for developing the safety andsensor suites for the first Small ModularReactors (SMRs) to seek regulatory approval.

**Intelligence, Surveillance, Target **Acquisition and Reconnaissance

Underlying earnings per share* +8.6%

134.6p (2015: 123.9p)

2016 134.6

2015 123.9

2014

2013

2012 125.5

127.1

123.1

> KPI

Dividend per share +3.7%

47.8p (2015: 46.1p)

2016 47.8

2015 46.1

2014

2013

2012 40.0

42.2

44.3

Ultra Electronics Holdings plc. Annual Report & Accounts 2016**see footnote on page 144

1. Introduction2. Strategic report3. Governance4. Group financials5. Company financials6. Five-year review

05Strategic report. Chief Executive’s review

Group order book +6.0%

£799.3m (2015: £753.8m)

2016 799.3

2015 753.8

2014

2013

2012 905.0

781.2

787.3

>

Our relationshipwith EDF remainsexcellent, culminatingin the award of EDFEnergy’s “UK Supplierof the Year”award.

“

”

>

Delivering excellenceDuring our annual Business LeadersConference, I sought my senior team's viewon the core question of why we do what do,as more important than who we are andwhat we do. The “Why”we developed fromour own discussions is set out on the frontcover of this report and neatly capturesUltra’s fundamental culture (see also page 1).We are disruptors in the marketplace. Simplyput, this means that Ultra is always lookingfor a new approach or a new method thatutilises our technology to displace theincumbent supplier, through innovative andadaptive solutions.

Achieving this still depends upon theinnovation and agility of our businesses, whichstems from their autonomy. Ultra businessesretain great freedom to make decisions andreact quickly to market opportunities, whilemeeting their budget goals. Over the past twoyears, we have enhanced this responsivenessby restructuring into three Divisions (pages 30-35) which reflect the eight market segmentswe face. This structure has increased the levelof collaboration across the Group, improvingshared understanding of Ultra’s capabilitiesand the market as a whole, resulting in greateropportunities to provide well-matchedsolutions to customer needs. This approachhas led to some further consolidation, from 24 businesses in 2015 to the current 19,where businesses face a similar customer set and have complementary capabilities. An additional benefit to these selectiveconsolidations is the generation of a smallnumber of larger businesses that are capableof taking on larger opportunities at a Tier 2level (defined on page 8), with the greaterdepth, experience and skill set that a larger-scale business allows us to attract into our management teams. We willcontinue to retain a core of capability at Tiers 3 and 4, with most Ultra businessesreflecting this focus.

In 2016 we made our first significantdisposal, with the sale of the ID Cardbusiness for £22m. This important exercise of discipline demonstrates the greaterattention we are paying to the developmentof our capability portfolio across the Group,as we reposition to achieve long-termgrowth. Acceleration of the integration ofHerley and an excellent cash conversion ratehas quickly reduced the Group’s leverage to a point where we can actively consider ournext significant acquisition.

Our Standardisation & Shared Services (S3)workstreams continue to make good progress(see pages 12-13). Importantly, thisprogramme does not reduce businessautonomy but instead brings together non-differentiating activities (including HR, financeand IT) into a single hub and service provider.Individual businesses retain expert roles inorder to support managerial decisions and tobe “demanding customers” for S3 services.

In 2016 I was delighted to welcome the returnof Amitabh Sharma to the Head Office, wherehe succeeded Mary Waldner as Group FinanceDirector. When he was with Ultra previously,Amitabh was formative in the development ofmany of Ultra’s financial control systems, so histransition into the lead financial role has beenvery swift. He brings an important insight,rigour and discipline to our financial processesand is leading the S3 programme.

We will continue to retain a core ofcapability at Tiers 3and 4, with most Ultrabusinesses reflecting this focus.

“

”

In 2016 we made our first significant disposal.“ ”Ultra Electronics Holdings plc. Annual Report & Accounts 2016

Chief Executive’s review (continued)

06 Strategic report. Chief Executive’s review

0

50

100

150

200

250

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

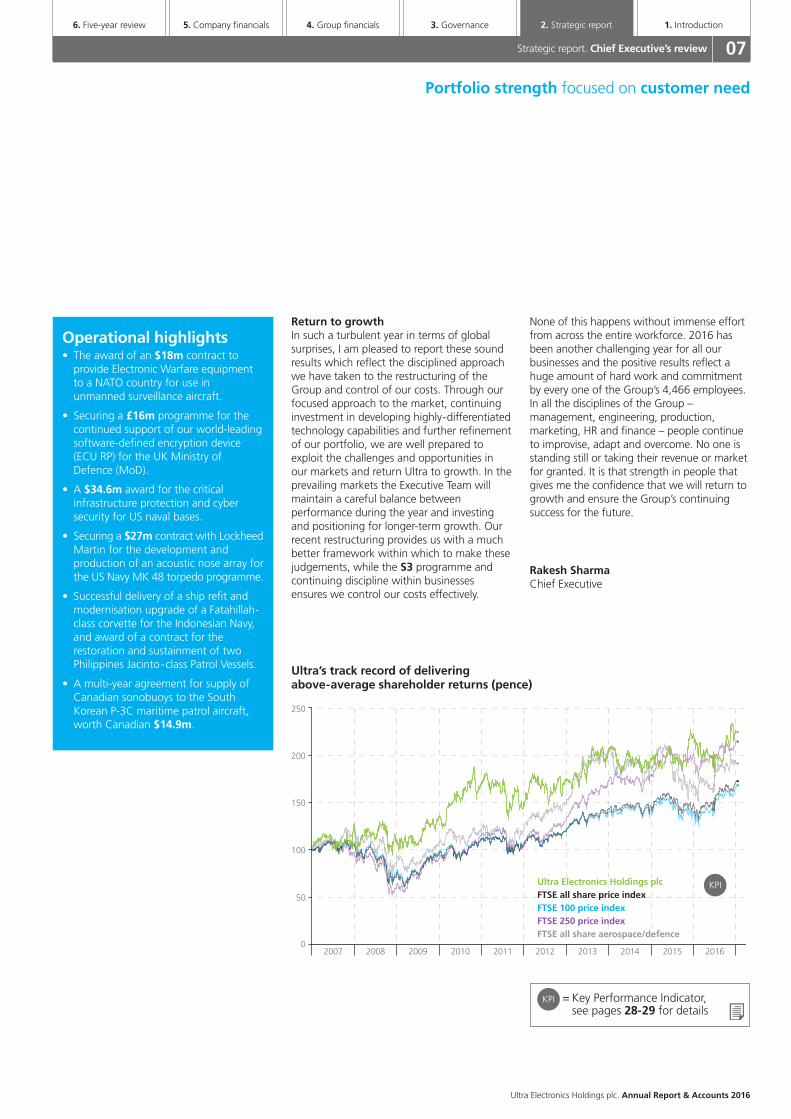

Return to growthIn such a turbulent year in terms of globalsurprises, I am pleased to report these soundresults which reflect the disciplined approachwe have taken to the restructuring of theGroup and control of our costs. Through ourfocused approach to the market, continuinginvestment in developing highly-differentiatedtechnology capabilities and further refinementof our portfolio, we are well prepared toexploit the challenges and opportunities inour markets and return Ultra to growth. In theprevailing markets the Executive Team willmaintain a careful balance betweenperformance during the year and investingand positioning for longer-term growth. Ourrecent restructuring provides us with a muchbetter framework within which to make thesejudgements, while the S3 programme andcontinuing discipline within businessesensures we control our costs effectively.

None of this happens without immense effortfrom across the entire workforce. 2016 hasbeen another challenging year for all ourbusinesses and the positive results reflect ahuge amount of hard work and commitmentby every one of the Group’s 4,466 employees.In all the disciplines of the Group –management, engineering, production,marketing, HR and finance – people continueto improvise, adapt and overcome. No one isstanding still or taking their revenue or marketfor granted. It is that strength in people thatgives me the confidence that we will return togrowth and ensure the Group’s continuingsuccess for the future.

Rakesh SharmaChief Executive

Ultra’s track record of delivering above-average shareholder returns (pence)

KPIUltra Electronics Holdings plcFTSE all share price indexFTSE 100 price indexFTSE 250 price indexFTSE all share aerospace/defence

Ultra Electronics Holdings plc. Annual Report & Accounts 2016

1. Introduction2. Strategic report3. Governance4. Group financials5. Company financials6. Five-year review

07Strategic report. Chief Executive’s review

= Key Performance Indicator, see pages 28-29 for details

KPI

Operational highlights • The award of an $18m contract toprovide Electronic Warfare equipmentto a NATO country for use inunmanned surveillance aircraft.

• Securing a £16m programme for thecontinued support of our world-leadingsoftware-defined encryption device(ECU RP) for the UK Ministry ofDefence (MoD).

• A $34.6m award for the criticalinfrastructure protection and cybersecurity for US naval bases.

• Securing a $27m contract with LockheedMartin for the development andproduction of an acoustic nose array forthe US Navy MK 48 torpedo programme.

• Successful delivery of a ship refit andmodernisation upgrade of a Fatahillah-class corvette for the Indonesian Navy,and award of a contract for therestoration and sustainment of twoPhilippines Jacinto-class Patrol Vessels.

• A multi-year agreement for supply ofCanadian sonobuoys to the SouthKorean P-3C maritime patrol aircraft,worth Canadian $14.9m.

Portfolio strength focused on customer need

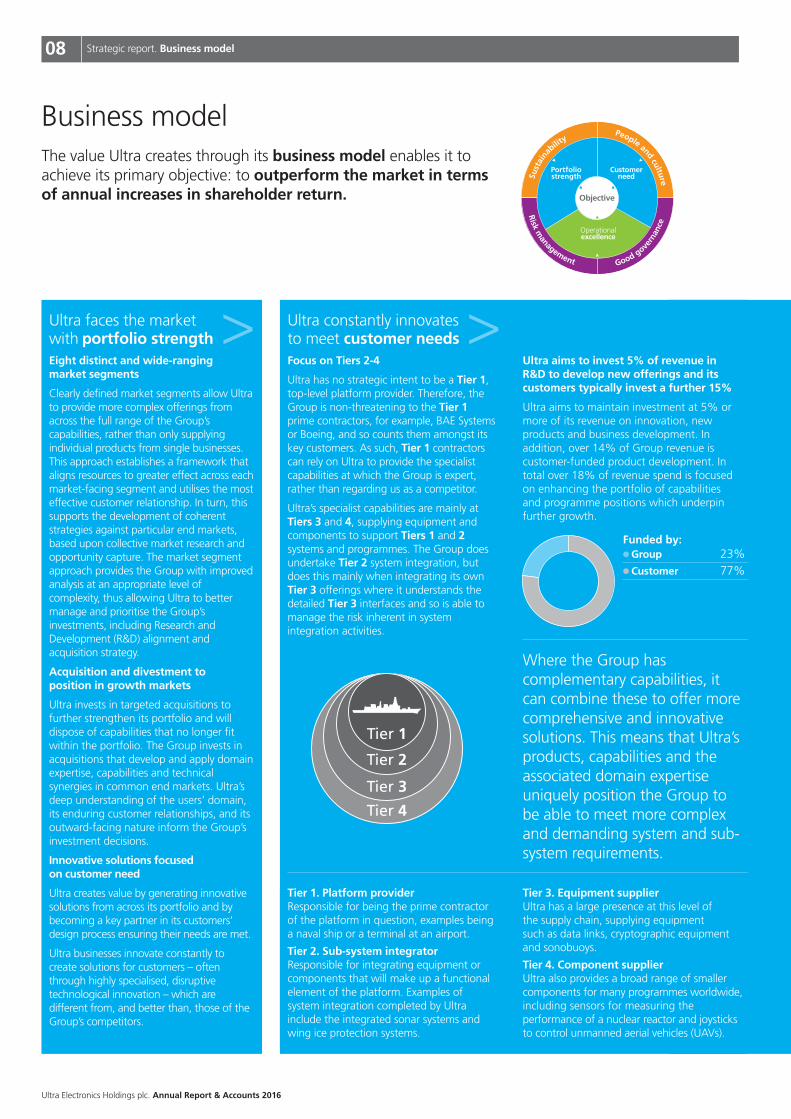

The value Ultra creates through its business model enables it toachieve its primary objective: to outperform the market in termsof annual increases in shareholder return.

Ultra constantly innovates to meet customer needsFocus on Tiers 2-4

Ultra has no strategic intent to be a Tier 1,top-level platform provider. Therefore, theGroup is non-threatening to the Tier 1prime contractors, for example, BAE Systemsor Boeing, and so counts them amongst itskey customers. As such, Tier 1 contractorscan rely on Ultra to provide the specialistcapabilities at which the Group is expert,rather than regarding us as a competitor.

Ultra’s specialist capabilities are mainly atTiers 3 and 4, supplying equipment andcomponents to support Tiers 1 and 2systems and programmes. The Group doesundertake Tier 2 system integration, butdoes this mainly when integrating its ownTier 3 offerings where it understands thedetailed Tier 3 interfaces and so is able tomanage the risk inherent in systemintegration activities.

Ultra aims to invest 5% of revenue inR&D to develop new offerings and itscustomers typically invest a further 15%

Ultra aims to maintain investment at 5% ormore of its revenue on innovation, newproducts and business development. Inaddition, over 14% of Group revenue iscustomer-funded product development. Intotal over 18% of revenue spend is focusedon enhancing the portfolio of capabilitiesand programme positions which underpinfurther growth.

Where the Group hascomplementary capabilities, itcan combine these to offer morecomprehensive and innovativesolutions. This means that Ultra’sproducts, capabilities and theassociated domain expertiseuniquely position the Group tobe able to meet more complexand demanding system and sub-system requirements.

Tier 1. Platform providerResponsible for being the prime contractorof the platform in question, examples beinga naval ship or a terminal at an airport.

Tier 2. Sub-system integratorResponsible for integrating equipment orcomponents that will make up a functionalelement of the platform. Examples ofsystem integration completed by Ultrainclude the integrated sonar systems andwing ice protection systems.

Tier 3. Equipment supplierUltra has a large presence at this level of the supply chain, supplying equipment such as data links, cryptographic equipmentand sonobuoys.

Tier 4. Component supplierUltra also provides a broad range of smallercomponents for many programmes worldwide,including sensors for measuring theperformance of a nuclear reactor and joysticksto control unmanned aerial vehicles (UAVs).

Ultra faces the market with portfolio strengthEight distinct and wide-ranging market segments

Clearly defined market segments allow Ultrato provide more complex offerings fromacross the full range of the Group’scapabilities, rather than only supplyingindividual products from single businesses.This approach establishes a framework thataligns resources to greater effect across eachmarket-facing segment and utilises the mosteffective customer relationship. In turn, thissupports the development of coherentstrategies against particular end markets,based upon collective market research andopportunity capture. The market segmentapproach provides the Group with improvedanalysis at an appropriate level ofcomplexity, thus allowing Ultra to bettermanage and prioritise the Group’sinvestments, including Research andDevelopment (R&D) alignment andacquisition strategy.

Acquisition and divestment to position in growth markets

Ultra invests in targeted acquisitions tofurther strengthen its portfolio and willdispose of capabilities that no longer fitwithin the portfolio. The Group invests inacquisitions that develop and apply domainexpertise, capabilities and technicalsynergies in common end markets. Ultra’sdeep understanding of the users’ domain,its enduring customer relationships, and itsoutward-facing nature inform the Group’sinvestment decisions.

Innovative solutions focused on customer need

Ultra creates value by generating innovativesolutions from across its portfolio and bybecoming a key partner in its customers’design process ensuring their needs are met.

Ultra businesses innovate constantly tocreate solutions for customers – oftenthrough highly specialised, disruptivetechnological innovation – which aredifferent from, and better than, those of theGroup’s competitors.

�Group 23%� Customer 77%

Funded by:

Tier 1

Tier 2

Tier 3

Tier 4

> >

Ultra Electronics Holdings plc. Annual Report & Accounts 2016

Business model

08 Strategic report. Business model

Portfoliostrength

Operationalexcellence

Customerneed

Objective

Good govern

ance

Risk m

anagement

Sust

aina

bility People and culture

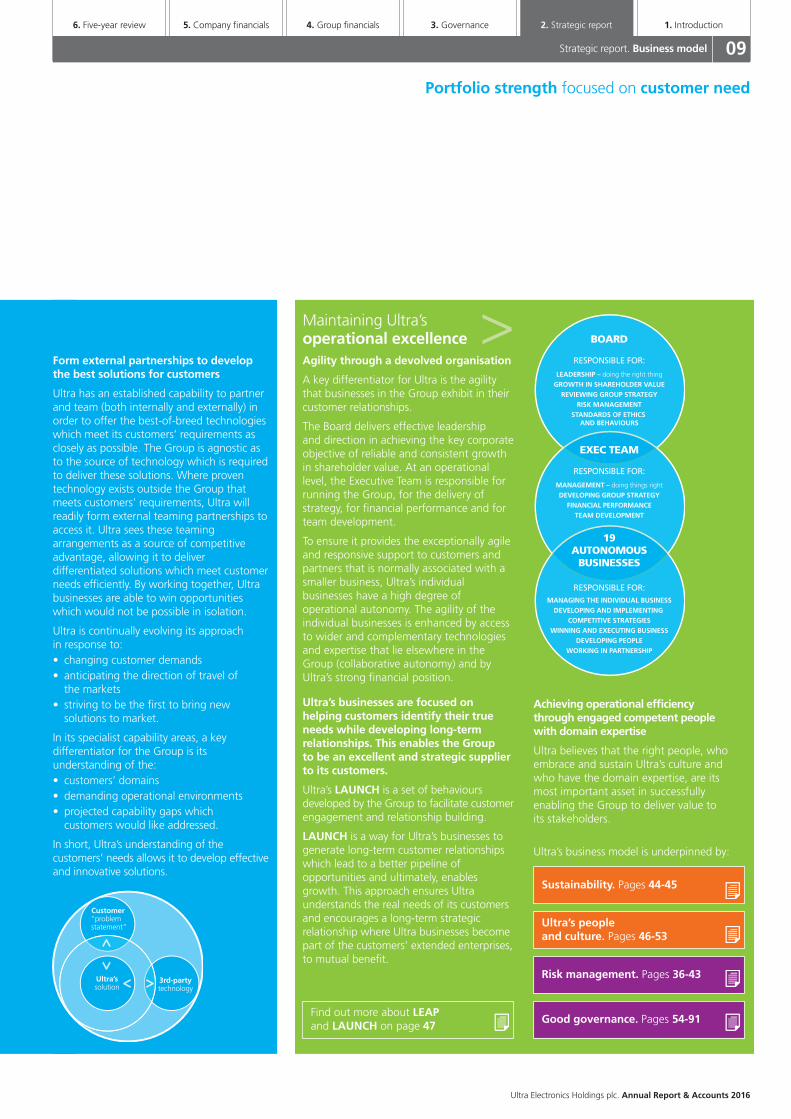

Maintaining Ultra’soperational excellenceAgility through a devolved organisation

A key differentiator for Ultra is the agilitythat businesses in the Group exhibit in theircustomer relationships.

The Board delivers effective leadership and direction in achieving the key corporateobjective of reliable and consistent growthin shareholder value. At an operationallevel, the Executive Team is responsible forrunning the Group, for the delivery ofstrategy, for financial performance and forteam development.

To ensure it provides the exceptionally agileand responsive support to customers andpartners that is normally associated with asmaller business, Ultra’s individualbusinesses have a high degree ofoperational autonomy. The agility of theindividual businesses is enhanced by accessto wider and complementary technologiesand expertise that lie elsewhere in theGroup (collaborative autonomy) and byUltra’s strong financial position.

Ultra’s businesses are focused onhelping customers identify their trueneeds while developing long-termrelationships. This enables the Group to be an excellent and strategic supplierto its customers.

Ultra’s LAUNCH is a set of behavioursdeveloped by the Group to facilitate customerengagement and relationship building.

LAUNCH is a way for Ultra’s businesses togenerate long-term customer relationshipswhich lead to a better pipeline ofopportunities and ultimately, enablesgrowth. This approach ensures Ultraunderstands the real needs of its customersand encourages a long-term strategicrelationship where Ultra businesses becomepart of the customers’ extended enterprises,to mutual benefit.

Achieving operational efficiency through engaged competent people with domain expertise

Ultra believes that the right people, whoembrace and sustain Ultra’s culture andwho have the domain expertise, are itsmost important asset in successfullyenabling the Group to deliver value to its stakeholders.

Ultra’s business model is underpinned by:

Form external partnerships to developthe best solutions for customers

Ultra has an established capability to partnerand team (both internally and externally) inorder to offer the best-of-breed technologieswhich meet its customers’ requirements asclosely as possible. The Group is agnostic asto the source of technology which is requiredto deliver these solutions. Where proventechnology exists outside the Group thatmeets customers’ requirements, Ultra willreadily form external teaming partnerships toaccess it. Ultra sees these teamingarrangements as a source of competitiveadvantage, allowing it to deliverdifferentiated solutions which meet customerneeds efficiently. By working together, Ultrabusinesses are able to win opportunitieswhich would not be possible in isolation.

Ultra is continually evolving its approach in response to:• changing customer demands• anticipating the direction of travel of the markets

• striving to be the first to bring newsolutions to market.

In its specialist capability areas, a keydifferentiator for the Group is itsunderstanding of the:• customers’ domains• demanding operational environments• projected capability gaps whichcustomers would like addressed.

In short, Ultra’s understanding of thecustomers’ needs allows it to develop effectiveand innovative solutions.

BOARD

RESPONSIBLE FOR:

LEADERSHIP – doing the right thing

GROWTH IN SHAREHOLDER VALUE

REVIEWING GROUP STRATEGY

RISK MANAGEMENT

STANDARDS OF ETHICS AND BEHAVIOURS

EXEC TEAM

RESPONSIBLE FOR:

MANAGEMENT – doing things right

DEVELOPING GROUP STRATEGY

FINANCIAL PERFORMANCE

TEAM DEVELOPMENT

19AUTONOMOUS

BUSINESSES

RESPONSIBLE FOR:MANAGING THE INDIVIDUAL BUSINESS

DEVELOPING AND IMPLEMENTING

COMPETITIVE STRATEGIES

WINNING AND EXECUTING BUSINESS

DEVELOPING PEOPLE

WORKING IN PARTNERSHIP

>

Ultra Electronics Holdings plc. Annual Report & Accounts 2016

1. Introduction2. Strategic report3. Governance4. Group financials5. Company financials6. Five-year review

09Strategic report. Business model

Sustainability. Pages 44-45

Ultra’s people and culture. Pages 46-53

Risk management. Pages 36-43

Good governance. Pages 54-91Find out more about LEAPand LAUNCH on page 47

Portfolio strength focused on customer need

3rd-partytechnology

Customer“problem statement”

Ultra’ssolution

Ultra’s objective is to add long-term shareholder value, as measuredby market capitalisation and the Group’s ranking in the FTSE index,more rapidly than other companies in order to outperform themarket. This will be facilitated by an above-average rate of revenuegrowth. Ultra constantly strives to increase its share of the high-growth sectors of the markets in which it has positioned itself.

Ultra’s four strategies for growth

10 Strategic report. Strategies for growth

• Concentrate on providing customerswith capabilities and systems

• Offer electronic and software solutions in niche markets

• Focus on developing specialistcapabilities with demanding and criticalrequirements

• Provide specialist solutions, often fordemanding environments

• Identify new platforms andprogrammes to apply Ultra capabilities

• Platform lives are typically 30 to 50 years which provides a long-term“flywheel” effect

• Enables resilient financial performancedespite market fluctuation

• Independence allows portfolio to be sold to a broad range ofcustomers globally

• Supply to different project offices,teams and platform teams withinwider customer relationships

• Build on largest customers, including: US DoD, UK MoD,Lockheed Martin, BAE Systems,Boeing and Australian DoD

• Increased access to two of the largest addressable defence budgets in the world

• The US still spends more on defence each year than other nations combined

• Undertaken the majority ofacquisitions in North America toachieve transatlantic capability

• Focus now is to gain competitiveadvantage through measuredexpansion into Australia, the MiddleEast, India and Asia-Pacific

Increase the Group’s portfolio of specialist capability areas

Increase the number of long-termplatforms and programmes on which Ultra’s specialist capabilities are specified

Broaden customer base Widen geographic footprint

1 2

3 4

Ultra Electronics Holdings plc. Annual Report & Accounts 2016

Examples of how the Group is performing in each strategy can be found below:

1. Introduction2. Strategic report3. Governance4. Group financials5. Company financials6. Five-year review

11Strategic report. Strategies for growth

• Precision Control Systems (PCS) received an order from the US DoD forCombatConnect, a new electronic soldierarchitecture Ultra had developed for theUK Army. This breakthrough order couldlead to a significant opportunity utilisingcutting-edge technology.

• Ultra Electronics signed a strategicmemorandum of agreement with NorthropGrumman (NG) Corporation to deliver newMaritime Domain Awareness (MDA) andAnti-Submarine Warfare (ASW) capabilitiesfor NG’s family of autonomous vehicles andsystems. This expands Ultra’s specialistcapability areas to include unmannedautonomous platforms to supplement ourexisting position on manned ASW platforms.

• 3eTI was contracted by the US Departmentof the Navy to continue providing cyber-secure critical infrastructure solutions. Thecontract will see 3eTI work with the Navy todesign, develop, integrate and install avariety of cyber-secure systems for criticalinfrastructure control and monitoring.

• PCS has secured a position on the SaabGripen NG aircraft for the supply of theHiPPAG stores management solution. This isthe first time a dual-purpose HiPPAGsystem has been fielded, capable ofproviding stores ejection and seeker headcooling from the same unit. The Gripenaircraft is enjoying strong sales and has along service future ahead of it. Production isexpected to start ramping up in 2019 andcontinue for at least a decade.

• The US WIN-T Increment 1 SignalModernization – Terrestrial TransmissionProgram was established as a DoD Programof Record enabling funding to be appliedto the long-term procurement of TCS’Orion radios.

• Ocean Systems was contracted by LockheedMartin to provide fully integrated ArrayNose Assemblies to increase the US Navy’sinventory of MK 48 torpedoes. This contractwill provide Ultra with access to additionalplatforms because the MK 48 is used by allclasses of US Navy submarines as well as bymany western navies as their primary ASWand anti-surface warfare (ASuW) weapon.In addition, Ocean Systems plans to expandits acoustic sensor capability to include theMK 54 acoustic nose assemblies. The MK 54is the primary ASW weapon for theairborne and seagoing ASW assets of manywestern navies.

• Following on from its success upgradingthe first Indonesian Navy’s Fatahillah Classcorvette, Ultra continues to expand itsgeographic footprint as its Command &Sonar Systems business was awarded acontract from the Philippine Governmentfor the restoration of their Jacinto ClassPatrol Vessels. This two-year contract willinclude replacement of the electro-optic firecontrol system and navigation sensors andoverhaul of the 25mm and 76mm guns ontwo ships of the Jacinto Class.

• Ultra’s CIS business expanded its footprintin the Middle East region with the award ofa major contract to provide an integratedsecurity system to protect naval ports fromunderwater threats.

• In 2016, Flightline Electronics wassuccessful in working with Airbus to securedevelopment and production funding toimplement Ultra’s aircraft Health and UsageMonitoring System (HUMS) into the USArmy’s fleet of UH-72 Lakota light utility helicopters. Ultra’s HUMS product is gainingglobal attention as the Aviation Industry

Corporation of China (AVIC) has requesteda demonstration prior to negotiating asupply agreement with Ultra, and the USState Department is interested in using thistechnology to upgrade its UH-1, CH-46 andUH-60 rotorcraft platforms.

• PCS is entering into a partnership withNanjing Engineering Institute of Aircraft Systems (NEIAS) to supply theNose Wheel Steering System for theMA700. This is Ultra’s first partnershipwith a Chinese company for the provisionof aerospace systems.

• NCS’s acquisition Lab Impex is now fullyintegrated into the business and hasfacilitated engagement with new customersacross markets that were previously notaccessible, offering access to a much widercustomer base and enabling totally newbusiness to be won in 2016 at the Sequoiareactor in the US and EDF Heysham IIreactor in UK.

• Herley was awarded a contract by a majorUS prime contractor to supply next-generation RF assemblies for the SurfaceElectronic Warfare Improvement Program(SEWIP), a substantial and long-termprogramme focused on electronic supportcapability improvements on US navy ships.

• Following a successful Integrated BallisticIdentification System (IBIS) trial installationin Beijing, Ultra’s Forensic Technologybusiness anticipates its first IBIS order fromChina in early 2017.

• Ultra successfully delivered the first of threeAir Warfare Destroyer Integrated SonarSuites to the Royal Australian Navy.

Ultra Electronics Holdings plc. Annual Report & Accounts 2016

Portfolio strength focused on customer need

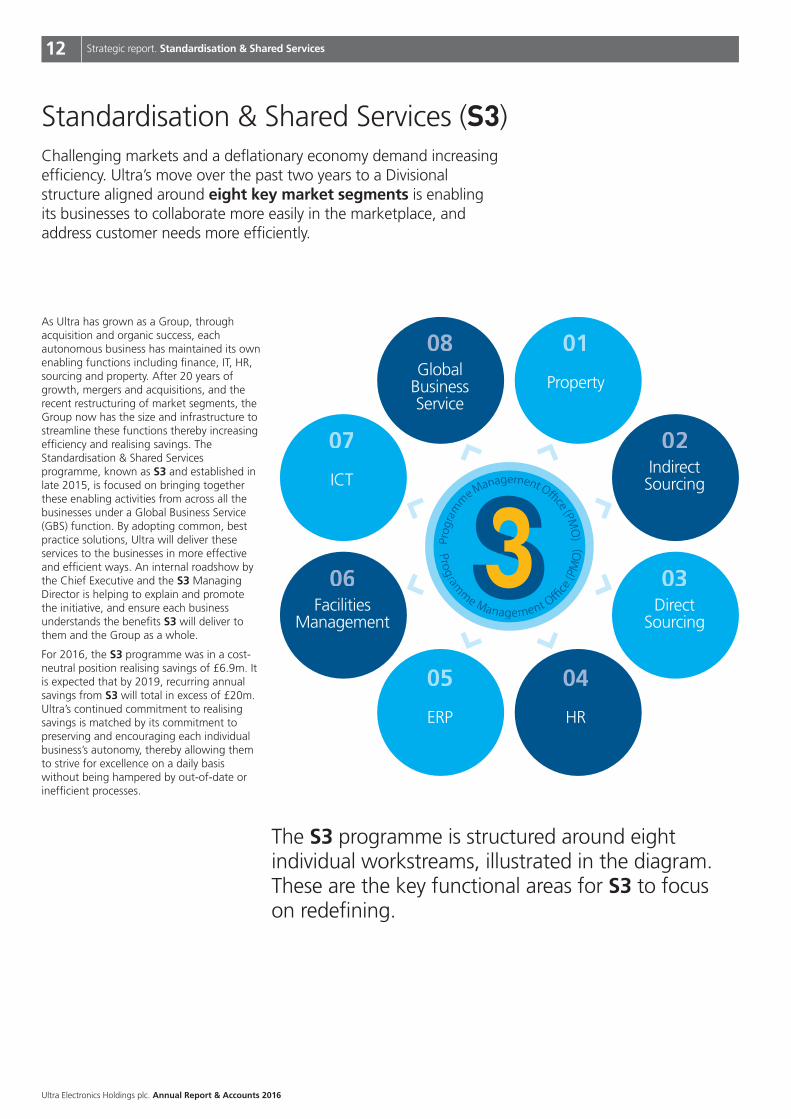

Challenging markets and a deflationary economy demand increasingefficiency. Ultra’s move over the past two years to a Divisionalstructure aligned around eight key market segments is enablingits businesses to collaborate more easily in the marketplace, andaddress customer needs more efficiently.

Ultra Electronics Holdings plc. Annual Report & Accounts 2016

As Ultra has grown as a Group, throughacquisition and organic success, eachautonomous business has maintained its ownenabling functions including finance, IT, HR,sourcing and property. After 20 years ofgrowth, mergers and acquisitions, and therecent restructuring of market segments, theGroup now has the size and infrastructure tostreamline these functions thereby increasingefficiency and realising savings. TheStandardisation & Shared Servicesprogramme, known as S3 and established inlate 2015, is focused on bringing togetherthese enabling activities from across all thebusinesses under a Global Business Service(GBS) function. By adopting common, bestpractice solutions, Ultra will deliver theseservices to the businesses in more effectiveand efficient ways. An internal roadshow bythe Chief Executive and the S3 ManagingDirector is helping to explain and promotethe initiative, and ensure each businessunderstands the benefits S3 will deliver tothem and the Group as a whole.

For 2016, the S3 programme was in a cost-neutral position realising savings of £6.9m. Itis expected that by 2019, recurring annualsavings from S3 will total in excess of £20m.Ultra’s continued commitment to realisingsavings is matched by its commitment topreserving and encouraging each individualbusiness’s autonomy, thereby allowing themto strive for excellence on a daily basiswithout being hampered by out-of-date orinefficient processes.

Standardisation & Shared Services (S3)

12

01

04

08

07

0306

05

Property

HR

GlobalBusinessService

ICT

DirectSourcing

FacilitiesManagement

ERP

02Indirect

Sourcing

Programme

ManagementO ce(PM

O)

Program

me ManagementO O

ce(PMO))

The S3 programme is structured around eightindividual workstreams, illustrated in the diagram.These are the key functional areas for S3 to focuson redefining.

Strategic report. Standardisation & Shared Services

Ultra Electronics Holdings plc. Annual Report & Accounts 2016

Some S3 Highlights to date: Global Business Services (GBS) The first stage of the S3 programme centredaround understanding the requirements of the individual businesses and ensuring that any changes did not detract from abusiness’s autonomy or restrict their ability to outperform the market. Having identifiedpotential areas to increase efficiency, theprogramme has now reached its secondphase and is actively managing theimplementation of the appropriate changesnecessary to bring the service functionstogether. A key requirement for theprogramme is the setting up of two sharedservice centres, one in the UK and one in the US.

UK GBS, based in Dorset, opened on 1 June2016 with the direct and indirect sourcingteams being the first functions on site.Following the successful pilot tests of GBSsystems and processes, services will, business bybusiness, be migrated into GBS. This includespayroll management, facilities management,and expenses processing and payment.

Continuous improvement techniques will beput in place within GBS to develop theseservices going forward. In most cases, thiswill involve the implementation and adoptionof new systems and best practice processes.In turn, this will lead to Ultra businessesenjoying the benefits of an integral servicepartner and the efficiencies gained fromconsistent service and product contractsnegotiated at a Group level as opposed to anindividual business level.

An announcement made in February 2017confirmed that the second GBS, supportingthe US businesses, will be located inRochester, New York and will mirror the sameapproach and services as the UK GBS centre.

PropertyGreater attention is being paid to Ultra’sproperty portfolio. By the end of 2016, theproperty footprint had reduced by 6%, atotal of 218,967ft2. A further 587,017ft2 hasbeen identified for 2017, to be achievedthrough a combination of exiting, subleasingand general consolidation of the estate. This represents a further 15% reduction.Following the development of a centraldatabase, managed by GBS, work is alreadyunderway to rigorously assess the futureproperty requirements across the Ultra Grouptargeting a total reduction of 21% by theend of 2017.

SourcingWith a forecast to achieve £7.6m of totalsavings from indirect and direct sourcing,work on increasing efficiencies has alreadyhelped to realise £0.5m of savings by the endof 2016 through changes to indirectsourcing, procurement and payment. Theimplementation of the Coupa system as thesingle Group-wide online system for sourcing,procurement and expenses is underway, withall UK businesses due to adopt the system inthe first half of 2017. Similarly, changes indirect sourcing have delivered savings on anumber of items by increased collaborationacross the Group and new supplier sourcingas indicated in the following examples:

• By combining the requirements of threeUltra businesses, negotiations with a wiresupplier resulted in an average combinedprice reduction of 7.1%

• Expanding an existing relationship with afreight supplier to cover more Ultrabusinesses for their truck freight service isforecast to realise full year savings of $230k

• Sourcing from lower-cost regions will see areduction of 60% against costs on theindustrial Thermowell line at NSPI.

Elsewhere in the Group, workshops have beenheld in collaboration with distributors. As aresult new supply chain solutions are beingestablished with the aim of tailoring the supplychain to better meet Ultra’s needs. In one case,a forecast-driven “Reduced Lead Time”programme to decrease costs is now beingpiloted for a major project. It is expected thatthis pilot will also reduce working capital costsand supply chain risk, and improve overalloperational excellence.

ERPAdditionally, some key S3 enablers are beingprogressed, including a new ERP strategywhich will deliver significant operationalefficiencies over the next three years andtransform businesses’ ability to report andextract data in ways they have not been ableto before. This will lead to efficiencies widerreaching than finance, providing transparencyand agility in manufacturing and projects too,through automation and elimination ofduplicate processes.

ITThe appointment of a Chief InformationOfficer in February 2017 is helping tostreamline and encourage IT efficiency andcompatibility across the Group. By buildingan internal capability through a specialisedteam, continuous improvement will beenabled across the Group, reducing ITsupport costs, and greatly improving long-term system robustness and alignment withbest practice models.

Global Property Footprint (ft2)

0 0.5M 1.0M 1.5M 2.0M 2.5M 3.0M 3.5M

End of 2015. 100%

End of 2016. 94%

End of 2017. 79%

6%

21%

£6.9mThe S3 programme generatedsavings of £6.9m in 2016.

7.1%Price reduction throughconsolidation of wire suppliers.

1. Introduction2. Strategic report3. Governance4. Group financials5. Company financials6. Five-year review

13Strategic report. Standardisation & Shared Services

Portfolio strength focused on customer need

It is expected that by2019, recurring annualsavings from S3 will totalin excess of £20m.

“”

14 Strategic report. Market-facing segments

Market overviewCommercial aerospace remains a vibrantsector with predictions of worldwidepassenger growth doubling over the next 15 years. Large aircraft manufacturers arebuoyed by record order backlogs that exceed13,000 aircraft, although new orders haveprobably reached a peak. This growth inplatform numbers is driven by the demand fornew aircraft in developing regions, while themore established markets need new aircraftto replace ageing fleets as well as to capturethe greater efficiencies in fuel, emissions andsystem reliability. The military aerospacemarket continues to see growth drivenpredominantly by the production ramp-up ofthe existing major military aircraftprogrammes. There are few new militaryaircraft programmes, with the market focusedon technology insertion and capabilityupgrades of existing airframes.

Market outlookIn the civil aerospace sector the twin-aislemarket continues to grow, and will remaindominated by Airbus and Boeing for theforeseeable future. Ultra provides uniqueelectrical wing ice protection systems andposition sensing electronics to the Boeing 787as well as providing specialist harnessing,landing gear service panels and a newelectrical ground door opening system to thenew Airbus A350. The single-aisle market isalso in growth and, while currently dominatedby Boeing and Airbus, is seeing new entrantsfrom China and Canada. The regional aircraftmarket is highly competitive. Nonetheless,Ultra has secured content on the JapaneseMitsubishi Regional Jet and the new ChineseMA700 regional turboprop. Growth in thebusiness jet market is focused on largeraircraft, where Ultra has secured business onthe new Gulfstream G650, G600 and G500as well as the Cessna Citation Longitude. Inthe rotary wing market the large reduction inenergy prices is reducing orders from the oiland gas rig servicing businesses and keyrequirements in this market are minimisingaircraft through-life costs. Ultra’s new Healthand Usage Monitoring System (HUMS)specifically targets these requirements. In themilitary aerospace sector, the fixed wingcombat aircraft market will be dominated forthe next 20 years by the increasing build rateand entry-into-service of the F-35 Joint StrikeFighter and its F-135 engine. Ultra providessignificant content to this aircraft/enginecombination including precision pneumatics(HiPPAG) for weapons ejection and the engineinlet ice protection system controller. The airtransport market is seeing a number ofcompetitors looking to fill the niches left byC-17 and C-130. In this sector Ultra hassecured positions on the Embraer KC-390 andon the Airbus A400M. The UAV marketremains an attractive but crowded sector.

Ultra’s portfolio strengthUltra’s CORE capabilities include:

• Ice protection and detection

• Position sensing and control

• Active noise and vibration control

• Health and Usage Monitoring (HUMS)

• Fuel system solutions

• Ground handling equipment

• Pilot controls

• Data and power transfer

• Stores and gas management

Strategy in actionIn 2016, Ultra’s Flightline business inVictor, NY collaborated with Curtiss-Wright to provide a new compact andlightweight Cockpit Voice and Flight DataRecorder with integral HUMS capabilitydesigned for use on rotorcraft platforms.

Revenue by segment

Aerospace

17%

Across the civil and military aerospace sectors, demand for innovativetechnologies to reduce cost, improve efficiency and increase safetyplay well to Ultra’s established strengths in controls systems andniche aviation technologies. This has allowed the Group to establishpositions on a number of long-term aerospace programmes nowramping up production.

Aerospace

Ultra Electronics Holdings plc. Annual Report & Accounts 2016

1. Introduction2. Strategic report3. Governance4. Group financials5. Company financials6. Five-year review

15Strategic report. Market-facing segments

Market overviewTransportation, including airport and railsystems, remains an area of stronginvestment worldwide. The increase in globalair traffic and national prestige projects isdriving investment in airport infrastructure,although competition in this sector isincreasing. Globally, rail infrastructure is alsogrowing rapidly as a key commercial andnational enabler in both established andemerging economies. In establishedeconomies infrastructure investment isfocused on upgrading existing capabilitiesand driving economic recovery. In emergingeconomies, such investment is being used tosecure growth and build national capacity.Increasing global demand for energy has ledto increased investment in power generation,power distribution, secure powermanagement and the renewables markets.Energy dominates the global trend in smartinfrastructure, with Smart Grid and secureenergy management lying at the heart ofSmart Cities and Critical NationalInfrastructure. Whilst global infrastructuredemand is largely being driven by China,India and the Middle East and North Africaregions, at least 50% of the global marketfor smart solutions lies in Europe and the US.

Market outlookIn the airport sector, the market for AirportMaster Systems Integration continues toexperience growth, especially in the demandfor Tier 2 airport capabilities. This is particularlyso in South America, the Middle East and Asia,where there are a number of key capitalprojects. The airport and airline informationmanagement market is also forecast to seeinvestment grow, although many of theoperational systems are becoming increasinglycommoditised. There is growing polarisationbetween global offerings and those with morelocalised niche expertise, so Ultra hascontinued to focus upon market intimacy,customer relationships and comprehensivesolutions over individual products. The railtransit power conversion and control market isalso anticipated to see significant growth.However, with the exception of the rail controlsector and the drive towards smart digitalsolutions, the market is becoming increasinglyprice-sensitive. In the power management andrenewables sector, the growing need forcompact, power-dense solutions plays toUltra’s capabilities with power resilience,energy storage and fast switching all beingkey drivers for growth. The secure energymanagement sector is forecast to seesubstantial investment, particularly in areasrelated to secure monitoring, analysis andcontrol. The emergent Smart Grid marketrelies on the ability to securely identify eachconnected device. In 2015, Ultra launched acyber-hardened critical infrastructuremanagement system to improve sitemanagement and performance without theneed to replace legacy equipment. This is nowbeing fielded. Opportunities in the Smart Gridmarket are likely to remain fragmented untilthe appropriate regulatory frameworks areestablished. However, Ultra’s broader securecommunication and data portfolio places it ina strong position with the Group able to offerthe highest level of assurance that can begained for the storage of unique digital keysand identifiers of devices.

Ultra’s portfolio strengthUltra’s CORE capabilities include:

• Broad suite of integrated infrastructure offerings spanningairports, rail and energy

• Secure localised networkcommunications for measurement and control

• Protection of critical energy andtransport information systems

• Power management and control

• Compact power solutions

• Flexible delivery models; outstandingservice reputation

• Integration and domain expertise atboth technological and programme level

Revenue by segment

Infrastructure

4%

Ultra is a trusted international provider and integrator of criticalsystems and software needed to operate and secure today’s andtomorrow’s transport and energy infrastructure.

Strategy in action In response to the growing need forcompact, power-dense solutions, Ultrasupplied the London Underground JubileeLine Upgrade project with compacttransformer rectifier equipment.

Infrastructure

Ultra Electronics Holdings plc. Annual Report & Accounts 2016

Portfolio strength focused on customer need

16 Strategic report. Market-facing segments

Ultra Electronics Holdings plc. Annual Report & Accounts 2016

Market overviewThere are over 430 commercial nuclear powerreactors operating in 31 countries worldwide.They provide over 11% of the world’selectricity as continuous, reliable, base-loadpower and remain an important part of thelow carbon energy mix. In addition, 56countries operate around 240 civil researchreactors, with many of these in developingcountries. Globally there are over 70 newreactors under construction. Many of the newbuilds are being developed within emergingeconomies and in those countries where thereis substantial state backing. However, theemphasis in established Western markets haslargely shifted to a shorter-term focus onsafety system upgrades, life extensions,emergency management and plantsustainment programmes. In addition to this,the UK is proceeding with a new commercialmodel it has pioneered in support of newnuclear build ambitions. The nuclear market isgenerally very conservative and supportedthrough large multinational organisations;however, there remain several complex nichesserved by smaller specialist companies. It is ahighly regulated market, with high barriers toentry, and as such is dominated by a numberof well-established global players. Thequalification of sensors and products acrossmultiple standards and platforms is extremelyexpensive and offers further barriers to entryonce established.

Market outlookAlthough the nuclear market is a long-cycleone, with plants taking several years to cometo completion, the outlook is positive. Muchof the current global fleet of plants will needlife extensions and upgrades. These plantsare largely older analogue Instrumentationand Control (I&C) designs, with the biggestmarket by far being the US. The new build,digital I&C market, which is currentlydominated by China, India and Russia, is of a similar magnitude. Ultra has investedsignificantly in new facilities for the testing,development and manufacture of sensors.This has shown its value through furthercontract wins with EDF for the provision ofspecialist sensors and, with the StrategicPartnership announcement with NuScale, to develop a suite of reactor and plant I&Csystems for their Small Modular Reactor(SMR). The Group currently providesequipment to over 190 reactors across 16countries, plus another 32 reactors currentlyunder construction. Furthermore, Ultra isuniquely qualified on eight new types (as wellas many legacy plants), meaning that it iswell positioned for the future.

Growth in the nuclear emergencymanagement market continues, prompted by the Fukushima accident which caused aglobal reassessment of post-accidentresponse and support needs. Plant safety isnow increasingly reliant on secure data and,as such, cyber security is a key part ofmeeting the formal safety requirements.Security concerns around the proliferation ofnuclear and the threat of terrorism are alsodriving the growth in new deployable securityand surveillance systems for nuclear plantsand enhanced border security. Ultra’s domainknowledge, through its SQEP, coupled withits extensive security and surveillancecapabilities (as described on page 18),position Ultra well in this sector.

Through its established relationships with Original EquipmentManufacturers (OEMs), the domain knowledge of its SuitablyQualified and Experienced Personnel (SQEP), and its broad range of qualified safety systems and sensors, Ultra is well positioned tosupport the growing market in the licensing, delivery and safeoperation of reactors and associated systems via a full “defence in depth” approach.

Ultra’s portfolio strengthUltra’s CORE capabilities include:• Extensive pool of Suitably QualifiedExperienced Personnel (SQEP)

• Nuclear safety system expertise

• Qualified reactor instrumentation and control

• Radiation detection sensors

• Nuclear energy management systems

• Nuclear operational support

• Nuclear rod control for submarines

Revenue by segment

Nuclear

8%

Strategy in actionEDF’s ageing fleet of AGR reactors areundergoing life extension reviews toensure their continued operationalavailability to end of station life. In 2016,NCS was awarded a £7.3m contractspanning 10 years to maintain designintegrity and equipment reliability acrossthe fleet via a structured managementand risk-mitigation approach.

Nuclear

1. Introduction2. Strategic report3. Governance4. Group financials5. Company financials6. Five-year review

17Strategic report. Market-facing segments

Ultra Electronics Holdings plc. Annual Report & Accounts 2016

Market overviewThe communications market includesshipborne, ground-based, underwater, air-to-ground and airborne communications, andencompasses a wide and diverse range ofcapabilities. Within the military and securitysector, there is continued demand for greaterbandwidth and broader connectivity, coupledwith a growing need for interoperability. Theemphasis today on secure networkedcommunications is spreading to all nationsseeking to modernise their systems. Theability to deliver real-time voice and data withad hoc mesh capabilities was becomingessential. This is driving investment in amarket where proven designs, which can beintegrated with existing equipment and areinteroperable with allies, are preferred.Additionally, this is where commercial “off theshelf” technology is increasingly being appliedto reduce costs and improve performance. Inparticular, there is a shift towards software-defined solutions that enable fast-cycleupgrades of capability and the use of openand commercial standards. Outside themilitary and security market, there is agrowing reliance on Machine-to-Machine(M2M) communications and, with the risingprevalence of connected devices, increasingemphasis on the “Internet of Things” (IoT).

Market outlookThe trend towards greater connectivity andnetworking will persist, driving significantfurther investment in militarycommunications. The emphasis will be onresilient networked communicationcapabilities enabling people to be connectedanywhere, anytime, all the time. On thebattlefield, this will drive the requirement forhigh-performance tactical communicationsystems such as the Ultra Orion multi-missionsoftware-defined radio, one of the mostversatile and advanced radios available today.It will also see military satellite systemsmoving towards higher frequency Ka bandsolutions and smaller, more portable earthstations that deliver higher bandwidth;developments that Ultra, in collaboration witha number of partners, is positioned to exploit.Similarly, in the data link market, in whichUltra remains well placed with its wide rangeof advanced data link and airborne gatewaysolutions, the demand for secure tactical andfull-motion video links will continue to grow.

In the encryption market, the move to smallerform factor products and from link to InternetProtocol (IP)-based cryptographic solutions willcontinue. Additionally, there is a shift frompaper-based key to electronic key distributionand management systems. Ultra has provennext-generation end-to-end cryptographicproducts and a strong position in both UKand US cryptographic programmes. This,allied to the Group's electronic keydistribution and management solutions,ensures Ultra remains well positioned in thissector to pursue a variety of opportunities.Finally, with the increasing awareness of thevulnerabilities of M2M communications, anda growing recognition of the need forsolutions to secure such systems, the secureM2M market will continue to grow. Ultra’sproven certified security solutions, which aretailored to meet critical national infrastructureand industrial needs, position the Group wellin this arena and have led to partnerships withOEMs in the building automation,energy/utilities, and oil and gas markets.

Ultra’s portfolio strengthUltra’s CORE capabilities include:

• Encryption and key managementsolutions

• Data link systems

• High-performance, high-reliability radio and wireless systems

• Secure voice, video and datacommunication platforms

• Secure wireless mesh networking

• Fixed, mobile and transportable satellite earth stations

• Identification and autonomousguidance products

• Airborne communication exchange

• Personal protective gearcommunications

• Acoustic hailing devices

• “Through the earth” communications

Revenue by segment

Communications

15%

Ultra is well positioned as one of the most trusted and respectedproviders of secure communication capabilities in the world offeringadvanced, interoperable solutions that are scalable and low-risk.

Strategy in actionIn November, Ultra’s TCS business wasawarded a substantial contract to supplyUltra Orion radios, through a strategiccollaboration with a major systemsintegrator for a large militarycommunications programme in theMiddle East.

CommunicationsPortfolio strength focused on customer need

18 Strategic report. Market-facing segments

Ultra Electronics Holdings plc. Annual Report & Accounts 2016

Market overviewC2ISR remains a priority capability withinglobal defence budgets due, primarily, to theincreased importance of these systems inmodern warfare. C2ISR applications are usedacross a variety of platforms with air power,as the principal mechanism for early orurgent delivery of military effect, driving thedemand for intelligence, surveillance, targetacquisition and reconnaissance (ISTAR). Here,the growth in platforms, particularlyunmanned platforms, fulfilling these rolescontinues unabated. The challenge, as ever,being the timely and secure dissemination ofthe associated data, typically video, aroundthe battlespace. In the face of terrorism,organised crime, drug trafficking and illegalimmigration, C2ISR capabilities are alsogrowing in importance in the wider bordersecurity and Critical National Infrastructure(CNI) protection markets. Overall, therecontinues to be an increasing demand forinteroperable and mobile networks thatdeliver a single integrated picture for timelysituational awareness. With a growingnumber of devices capable of collectingsensor data operating across multiplecommunication networks, the complexityand scale of integrated surveillance systemsalso continues to increase. Solutions need to be tailored to customers’ needs,comprehensive and able to draw on “best-of-breed”, established and clearlydifferentiated technologies.

Market outlookGlobal spending on C2ISR systems isexpected to remain robust. In the militaryarena, there will be a continued emphasis onintelligence and surveillance assets, as well asthe ability to fuse or correlate these datastreams into a single real-time integratedpicture that can be disseminated down to thelowest level. This will drive growth in real-time ISTAR (for both manned and unmannedplatforms) and the connectivity betweenassets in the battlespace. Ultra’s leading datafusion, situational awareness andvisualisation systems play well to this growingneed. Electronic Warfare (EW) is also gainingin prominence. The global EW market isforecast to grow significantly over the nextfew years driven by the increasing emphasisplaced on information superiority andsituational awareness. Ultra bolstered itscapability in this area with the acquisition ofHerley in 2015 and continues to grow itsshare of the EW market.

The border security and CNI protectionmarkets are also projected to grow. Theillegal movement of arms, narcotics andpeople will continue to drive growth, whilethe shift from labour-intensive security tohigh-tech networked solutions will continue.Ultra has all the necessary elements to delivermultiple applications into these markets andis focused on those opportunities wherethere is a growing need, the political impetusand the necessary funding. Growth in theCNI physical protection market will continueto be underpinned by the increasingadoption of video surveillance and wirelesstechnologies for perimeter security. The risingawareness of cyber threats and governmentmandates will drive similar growth in theprotection of industrial control systems.Drawing on its advanced securecommunications and surveillance capabilities,Ultra remains well-positioned to providecomplete cyber-physical security solutions tothis growing market.

Revenue by segment

C2ISR

21%

Ultra’s portfolio strengthUltra’s CORE capabilities include:

• Surveillance solutions for critical national infrastructure, coastal andborder security needs

• Covert surveillance solutions

• Command and control systems

• Airborne surveillance and targeting

• Electronic Warfare solutions, Electronic Warfare simulators and radar test systems

• Document examination systems

• Ballistics and crime scene analysis

Strategy in actionIn 2016, 3eTI was awarded a $34.6mcontract by the US Navy to continueproviding critical infrastructure protectionsolutions. Initial tasks of $13.9m are dueto be completed by September 2017.

As a trusted supplier of innovative surveillance and securitysolutions to government and commercial customers, Ultra is wellpositioned to exploit this growing market.

C2ISR*

*Command & Control, Intelligence, Surveillance and Reconnaissance

1. Introduction2. Strategic report3. Governance4. Group financials5. Company financials6. Five-year review

19Strategic report. Market-facing segments

Ultra Electronics Holdings plc. Annual Report & Accounts 2016

Market overviewSubmarines are strategic assets, able to fulfil avariety of missions from covert surveillancethrough to anti-surface warfare, stand-off landattack and ultimately, strategic deterrence.This multi-mission capability, combined withtheir innate characteristics of stealth andendurance, has made submarines highlyattractive to nations wishing to exercise cost-effective power projection. Submarines posemore than just a military threat. Theseplatforms can easily and effectively disrupt thesea lines of trade that sustain the globaleconomy. As a consequence, there has been a substantial investment in submarinetechnology by Russia, China, North Korea, andIran. Moreover, many smaller nations in Asia-Pacific are rapidly procuring submarines in aneffort to protect their national interests. Thisgrowth in submarine capability is no longeroffset by traditional western underwatertechnological superiority, which has erodedthrough years of neglect. Therefore,investment in ASW has become a top priorityfor nations.

Global financial pressures, coupled withincreased capital platform costs, mean thatnations can typically no longer affordplatforms dedicated to a specific role. Instead,they are generally moving to the use ofincreased, smaller multi-role platforms, offrigate or offshore patrol vessel size. As aresult, ASW solutions now need to be modularwith reduced footprints to fit on these smallervessels. Another key factor in this growingASW market is the desire for increasingly shortdevelopment times, requiring investment inadvance of contract awards. Ultra haspositioned itself well in both of these areas,with continued investment in ASWtechnologies including multistatic activesystems and sonobuoys for use withUnmanned Aerial Vehicles (UAV). A key exportmarket driver is the increasing requirement forindigenous technology transfer to overseascustomers, another area where Ultra has astrong pedigree with recent export contracts.

Market outlookThe US continues its strategic rebalancing ofmilitary assets and capability between theAtlantic and Pacific theatres. As a result,despite the wider US government fundingpressures, ASW and submarines remain areasof preferential spend with increased budgetallocation. Specifically, the US continues tobuild two Virginia Class SSNs per year, andhas delivered more than 30 P-8A maritimepatrol aircraft to the US Navy, as well asawarding contracts to upgrade both light andheavyweight torpedoes. Future funding isearmarked to further bolster the US Navy’sASW capability through the award of nextgeneration torpedo countermeasures andtorpedo defence systems. Elsewhere, severalof the major Commonwealth countries haveembarked on a major recapitalisation of theirASW frigates; the steel on the Royal Navy’sfirst T-26 Global Combat Ship is due to be cutduring the summer of 2017. Activity is wellunderway on Canada’s Common SurfaceCombatant fleet with the initial contracts dueto be released in 2018. Similarly, Australia’sSEA5000 programme has started thecompetitive evaluation process and should goto contract in 2020. In all, more than 30vessels will be constructed with a missionemphasis on ASW. More broadly in theaddressable Asia-Pacific market, spendrelated to ASW systems, including towedtorpedo defence solutions, is projected to riseto almost £0.5bn. Specifically, India intendsto award three major ASW relatedprogrammes totalling in excess of £100mover the next five years. Ultra is well placedto address these needs based on itscontinued investment in integrated sonarsystems and surface ship torpedo defencesystem technologies.

Ultra’s world-leading domain knowledge, acoustic technical expertiseand ability to provide leading technology in Anti-Submarine Warfare(ASW) performance through rapidly delivered, modular, affordableand reliable solutions means that it is well positioned to exploit thislarge and growing market.

Ultra’s portfolio strengthUltra’s CORE capabilities include:

• Expert knowledge of acousticperformance in the maritime domain

• Design and manufacture of air-deployable sonobuoys

• Sonar transducer and towed arraydesign and manufacture

• Acoustic countermeasure techniques for torpedo defence

• Sonar processing, display, and decision aids

• Recognised integrator of complex sonarsystems both towed and hull-mounted

Revenue by segment

Underwater warfare

25%

Strategy in action The Royal Netherlands Navy received itssecond Multistatic Active Passive Sonar(MAPS) system from Ultra in 2016. It wasinstalled and underwent successfulharbour acceptance tests in October whilstthe first system completed its operationalevaluation trial with the Dutch Navy inNovember. The trials were so successfulthat the commander of the Dutch Navytweeted “the MAPS system was aquantum leap in ASW capability”. LastlyUltra, through its joint venture ERAPSCO,commenced production of the nextgeneration of High Altitude Anti-Submarine Warfare (HAASW) sonobuoys.These sensors have been designed to bedeployed from P-8A Poseidon aircraft andwill provide extended detection ranges onenemy submarines due to their coherentmultistatic active capability.

Underwater warfarePortfolio strength focused on customer need

20 Strategic report. Market-facing segments

Ultra Electronics Holdings plc. Annual Report & Accounts 2016

Market overviewPost the Afghanistan and Iraq land-basedconflicts, many nations are now looking torebalance their force structure and have arenewed focus on the procurement ofmaritime and air domain equipment. As aresult, national military shipbuilding strategiesare being developed by several Westernnations with the objective to stimulate long-term, sustained new ship construction. In theUS and the UK, the construction of newstrategic deterrent submarine fleets has beenapproved and is now underway. In otherparts of the world the requirement forincreased maritime capability is clear, butfiscal constraints are driving life extensions ofexisting platforms through cost-effectivecapability upgrades. Consequently, thedemand for system/sensor upgrades andtechnology insertion programmes on existinghulls is growing, particularly for navies inemerging nations. For the export market ingeneral, maritime platform programmes areoften dominated by the industrial politics ofthe nation concerned, especially if they haveindigenous capabilities. As a result,technology transfer is an increasinglyimportant factor enabling business in theexport market.

Market outlookThe power products segment in the USmarket remains stable. The Virginia ClassSubmarine (VCS) production is well protectedwith manufacturing steady at two hulls peryear for the foreseeable future. Longer-termgrowth opportunities for Ultra specialistpower products will come with the newColumbia Class SSBN, projected to provide12 new hulls beginning in 2021. The use ofcommon sub-systems with VCS will helplower the cost-growth risk that currentlyexists on the Ohio Replacement Programme.The US Navy is investing in a technical refreshof Arleigh Burke Class guided missiledestroyers (DDG-51), landing platform docks(LX-R) and replenishment naval vessels (T-AOX)which will provide further opportunities forgrowth of the Group’s advanced power andsignature management products.

The incumbent position on the UKDreadnought SSBN development andqualification programme will ensure a highprobability of production follow on for mainstatic converters, electric cruise propulsion andsignature management. Clean Powerrequirements of the US DoD and aerospacespecifications will continue to drive the needfor Ultra’s speciality components such aspower filters and multi-phase transformers.The Group’s specialist signature managementcapabilities will see growth opportunities inthe next five years through the US Navy’sColumbia Class SSBN Programme,replacement auxiliary vessels, ongoing LittoralCombat Ship production and DDG-51upgrades. There is also increased focus onelectric field signature management due to thegrowing awareness of Influence mine threat.

With the protection of maritime resourcesrising in importance in areas such as the SouthChina Sea, there are increasing requirementsfor submarines with extended patrol times.The advent of air-independent propulsioncapability is expected to increase demand forpower conversion and degaussing products.

More broadly, the continuing demand forsurface platform system and sensor upgradesplays well to Ultra’s strengths in naval combatsystems and electro-optics and the Group’spedigree in partnering with local industry.

Combining its expertise in power electronics and open architecturedesign, Ultra provides innovative, scalable and affordable solutionsto meet customer needs in signature management, power-densemotors and command and control systems for maritime platforms.

Ultra’s portfolio strengthUltra’s CORE capabilities include:

• Magnetic and electric signaturemanagement for ships and submarines

• Specialist motor drives and powerconverters

• Power conversion and controlmanagement

• Nuclear rod control for submarines

• Stable positioning for precise electro-optic (EO) tracking on moving platforms

• Customised command, control andnavigation systems for small ships

Revenue by segment

Maritime

7%