COMPANY REGISTRATION NUMBER 07876075 Aon plc Annual Report and Accounts For the year ended December 31, 2018

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

COMPANY REGISTRATION NUMBER 07876075

Aon plc

Annual Report and Accounts

For the year ended December 31, 2018

2

CONTENTS PAGES

Strategic Report

Report of the Directors

Directors’ Remuneration Report

Statement of Directors’ Responsibilities

Independent Auditor’s Report to the Members

Consolidated Financial Statements:

Consolidated Statements of Income

Consolidated Statements of Comprehensive Income

Consolidated Statements of Financial Position

Consolidated Statements of Shareholders’ Equity

Consolidated Statements of Cash Flows

Notes to Consolidated Financial Statements

Parent Company Financial Statements:

Parent Company Statements of Financial Position

Parent Company Statements of Shareholders’ Equity

Parent Company Statements of Cash Flows

Notes to Parent Company Financial Statements

3

34

40

54

55

63

64

65

66

67

68

137

138

139

140

3

STRATEGIC REPORT

STRATEGY AND BUSINESS MODEL

Aon plc and its controlled subsidiaries (which may be referred to as “Aon,” the “Company,” “Group,” “we,” “us,” or “our”) is a leading global professional services firm that provides advice and solutions to clients focused on risk, retirement, and health, delivering distinctive client value via innovative and effective risk management and workforce productivity solutions that are under-pinned by industry-leading data and analytics. Our strategy is to be the preeminent professional services firm in the world, focused on risk and people.

Our clients are globally diversified and include all market segments (individuals through personal lines, mid-market companies, and large global companies) and almost every industry in over 120 countries and sovereignties. This diversification of our customer base helps provide us stability in different economic scenarios that could affect specific industries, customer segments, or geographies. The Company’s registered office is located at the Aon Centre, 122 Leadenhall Street, London, England.

We have continued to focus our portfolio on higher-margin, capital-light professional services businesses that have high recurring revenue streams and strong cash flow generation. We endeavor to make capital allocation decisions based upon return on invested capital (“ROIC”).

BUSINESS SEGMENT

Beginning in 2017 and following the sale of our benefits administration and business process outsourcing business (the “Divested Business”) on May 1, 2017, the Company led a set of initiatives designed to strengthen Aon and unite the firm with one portfolio of capability enabled by proprietary data and analytics and one operating model to deliver additional insight, connectivity, and efficiency. These initiatives reinforce Aon’s ROIC decision making process and emphasis on operating cash flow. The Company is now operating as one segment that includes all of Aon’s continuing operations, which, as a global professional services firm, provides advice and solutions to clients focused on risk, retirement, and health through five principal products and services: Commercial Risk Solutions, Reinsurance Solutions, Retirement Solutions, Health Solutions, and Data & Analytic Services. Collectively, these products and service revenue lines make up our one segment: Aon United.

In 2018, our consolidated total revenue was $10,770 million. This includes $4,652 million in Commercial Risk Solutions, $1,563 million in Reinsurance Solutions, $1,865 million in Retirement Solutions, $1,596 million in Health Solutions, and $1,105 million in Data & Analytic Services, before intercompany eliminations.

Principal Products and Services

Commercial Risk Solutions includes retail brokerage, cyber solutions, global risk consulting, and captives. In retail brokerage, our team of expert risk advisors applies a client-focused approach to commercial risk products and services that leverage Aon’s global network of resources, industry-leading data and analytics, and specialized expertise. Cyber solutions is one of the industry’s premier resources in cyber risk management. Our strategic focus extends to identify and protect critical digital assets supported by best-in-class transactional capabilities, enhanced coverage expertise, deep carrier relationships, and incident response expertise. Global risk consulting is a world-leading provider of risk consulting services supporting clients to better understand and manage their risk profile through identifying and quantifying the risks they face. We assist clients with the selection and implementation of the appropriate risk transfer, risk retention, and risk mitigation solutions, and ensure the continuity of their operations through claims consulting. Captives is a leading global captive insurance solutions provider that manages over 1,100 insurance entities worldwide including captives, protected segregated and incorporated cell facilities, as well as entities that support insurance-linked securities and specialist insurance and reinsurance companies.

Reinsurance Solutions includes treaty and facultative reinsurance and capital markets. Treaty reinsurance addresses underwriting and capital objectives on a portfolio level, allowing our clients to more effectively manage the combination of premium growth, return on capital, and rating agency interests. This includes the development of more competitive, innovative, and efficient risk transfer options. Facultative reinsurance empowers clients to better understand, manage, and transfer risk through innovative facultative solutions and provides the most efficient access to the global facultative reinsurance markets. Capital markets is a global investment bank with expertise in mergers and acquisitions, capital raising, strategic advice, restructuring, recapitalization services, and insurance-linked securities. We partner with insurers, reinsurers, investment firms, banks, and corporations in the management of complex commercial issues through the provision of corporate finance advisory services, capital markets solutions, and innovative risk management products.

Retirement Solutions includes core retirement, investment consulting, and talent, rewards, and performance. Retirement consulting specializes in providing organizations across the globe with strategic design consulting on their retirement programs, actuarial services, and risk management, including pension de-risking, governance, integrated pension administration, and legal and compliance consulting. Investment consulting provides public and private companies and other institutions with advice on

4

developing and maintaining investment programs across a broad range of plan types, including defined benefit plans, defined contribution plans, endowments, and foundations. Our delegated investment solutions offer ongoing management of investment programs and fiduciary responsibilities either in a partial or full discretionary model for multiple asset owners. It partners with clients to deliver our scale and experience to help them effectively manage their investments, risk, and governance and potentially lower costs. Talent, rewards, and performance delivers advice and solutions that help clients accelerate business outcomes by improving the performance of their people. It supports the full employee lifecycle, including assessment and selection of the right talent, optimized deployment and engagement, and the design, alignment, and benchmarking of compensation to business strategy and performance outcomes.

Health Solutions includes heath and benefits brokerage and health care exchanges. Health and benefits brokerage partners with employers to develop innovative, customized benefits strategies that help manage risk, drive engagement, and promote accountability. Our private health exchange solutions help employers transform how they sponsor, structure, and deliver health benefits by building and operating a cost effective alternative to traditional employee and retiree health care. We seek outcomes of reduced employer costs, risk, and volatility, alongside greater coverage and plan choices for individual participants.

Data & Analytic Services includes Affinity, Aon InPoint, and ReView. Affinity specializes in developing, marketing and administering customized insurance programs and specialty market solutions for Affinity organizations and their members or affiliates. Aon InPoint draws on the Global Risk Insight Platform, one of Aon’s proprietary databases, and is dedicated to making insurers more competitive by providing data, analytics, engagement, and consulting services. ReView draws on another Aon proprietary database and broker market knowledge to provide advisory services, analysis, and benchmarking to help reinsurers more effectively meet the needs of cedents through the development of more competitive, innovative, and efficient risk transfer options.

Revenue and Compensation

Our business generates revenues primarily through commissions, compensation from insurance and reinsurance companies for services we provide to them, and fees from customers. Commissions and fees for brokerage services vary depending upon several factors, which may include the amount of premium, the type of insurance or reinsurance coverage provided, the particular services provided to a client, insurer, or reinsurer, and the capacity in which we act. Compensation from insurance and reinsurance companies includes: (1) fees for consulting and analytics services, and (2) fees and commissions for administrative and other services provided to or on behalf of insurers. Fees from clients for advice and consulting services are dependent on the extent and value of the services we provide. Payment terms are consistent with current industry practices.

Fiduciary Funds

We typically hold funds on behalf of clients, including premiums received from clients and claims due to clients that are in transit to and from insurers. Certain funds held on behalf of clients are invested in interest-bearing premium trust accounts and can fluctuate significantly depending on when we collect and remit cash. The principal is segregated and not available for general operating purposes, though we earn interest on these accounts.

Competition

Our business operates in a highly competitive and fragmented environment. We compete with other global insurance brokers and consulting companies, including Marsh & McLennan Companies, Inc., Willis Towers Watson Public Limited Company, Arthur J Gallagher & Company, and Jardine Lloyd Thompson Group plc, as well as numerous specialist, regional, and local firms in almost every area of our business. We also compete with insurance and reinsurance companies that market and service their insurance products without the assistance of brokers or agents, and with other businesses that do not fall into the categories above, including large financial institutions and independent consulting firms and consulting organizations affiliated with accounting, information systems, technology, and financial services firms.

Seasonality

Due to buying patterns and delivery of certain products in the markets we serve, revenues recognized tend to be higher in the first three months and last three months of each fiscal year.

Licensing and Regulation

Our business activities are subject to licensing requirements and extensive regulation under the laws of countries in which we operate, including United States (“U.S.”) federal and state laws. See the “Principal Risks and Uncertainties” section of this report for information regarding how actions by regulatory authorities or changes in legislation and regulation in the jurisdictions in which we operate may have an adverse effect on our business.

5

Regulatory authorities in the countries and states in the U.S. in which our operating subsidiaries conduct business may require individual or company licenses to act as producers, brokers, agents, third-party administrators, managing general agents, reinsurance intermediaries, or adjusters. Under the laws of most countries and states, regulatory authorities have relatively broad discretion with respect to granting, renewing, and revoking producers’, brokers’, and agents’ licenses to transact business in the country or state. The operating terms may vary according to the licensing requirements of the particular country or state, which may require, among other things, that a firm operates in the country or state through a local corporation. In a few countries and states, licenses may be issued only to individual residents or locally owned business entities. In such cases, our subsidiaries either have such licenses or have arrangements with residents or business entities licensed to act in the country or state.

Our subsidiaries must comply with laws and regulations of the jurisdictions in which they do business. These laws and regulations are enforced by the Financial Conduct Authority (“FCA”) in the United Kingdom (“U.K.”), by federal and state agencies in the U.S., and by various regulatory agencies and other supervisory authorities in other countries through the granting and revoking of licenses to do business, the licensing of agents, the monitoring of trade practices, policy form approval, limits on commission rates, and mandatory remuneration disclosure requirements.

Insurance authorities in the U.K., U.S., and certain other jurisdictions in which our subsidiaries operate have enacted laws and regulations governing the investment of funds, such as premiums and claims proceeds, held in a fiduciary capacity for others. These laws and regulations generally require the segregation of these fiduciary funds and limit the types of investments that may be made with them.

Investment, securities, and futures licensing authorities also govern certain of our business activities. For example, in the U.S., we use Aon Securities, LLC, a U.S.-registered broker-dealer and investment advisor, member of the Financial Industry Regulatory Authority (“FINRA”) and Securities Investor Protection Corporation, and an indirect, wholly owned subsidiary of Aon, for capital management transaction and advisory services and other broker-dealer activities. Similar operations exist in other jurisdictions outside of the U.S.

Further, pension and financial laws and regulations, including oversight and supervision by the FCA in the U.K., the Securities and Exchange Commission (“SEC”) in the U.S., and regulators in other countries govern certain of the retirement-related consulting services provided by Aon and its subsidiaries and affiliates. This includes Aon subsidiaries that provide investment advisory services regulated by various U.S. federal authorities including the SEC and FINRA, as well as authorities on the state level. In addition, other services provided by Aon and its subsidiaries and affiliates, such as trustee services and retirement and employee benefit program administrative services, are subject in various jurisdictions to pension, investment, securities, and insurance laws and regulations, and supervision.

Clientele

Our clients operate in many businesses and industries throughout the world. No one client accounted for more than 1% of our consolidated total revenues in 2018. Additionally, we place insurance with many insurance carriers, none of which individually accounted for more than 10% of the total premiums we placed on behalf of our clients in 2018.

Employees

At December 31, 2018, we employed approximately 50,000 employees and conducted our operations through various subsidiaries in more than 120 countries and sovereignties.

Information Concerning Forward-Looking Statements

This report and in reports we subsequently file or furnish and have previously filed or furnished with Companies House contains certain statements related to future results, or states our intentions, beliefs, and expectations or predictions for the future which are forward-looking statements as that term is defined in the Private Securities Litigation Reform Act of 1995. Forward-looking statements represent management’s expectations or forecasts of future events. Forward-looking statements are typically identified by words such as “anticipate,” “believe,” “estimate,” “expect,” “forecast,” “project,” “intend,” “plan,” “probably,” “potential,” “looking forward,” “continue,” and other similar terms, and future or conditional tense verbs like “could,” “may,” “might,” “should,” “will,” and “would.” You can also identify forward-looking statements by the fact that they do not relate strictly to historical or current facts. For example, we may use forward-looking statements when addressing topics such as: market and industry conditions, including competitive and pricing trends; changes in our business strategies and methods of generating revenue; the development and performance of our services and products; changes in the composition or level of our revenues; our cost structure and the outcome of cost-saving or restructuring initiatives; the outcome of contingencies; dividend policy; the expected impact of acquisitions and dispositions; pension obligations; cash flow and liquidity; expected effective tax rate; future actions by regulators; and the impact of changes in accounting rules. These forward-looking statements are subject to certain risks and uncertainties that could cause actual results to differ materially from either historical or anticipated results depending on a variety

6

of factors. Potential factors, which may be revised or supplemented in subsequent reports filed or furnished with Companies House, that could impact results include:

• general economic and political conditions in the countries in which we do business around the world, including the U.K.’s expected withdrawal from the European Union;

• changes in the competitive environment or damage to our reputation;

• fluctuations in exchange and interest rates that could influence revenues and expenses;

• changes in global equity and fixed income markets that could affect the return on invested assets;

• changes in the funding status of our various defined benefit pension plans and the impact of any increased pension funding resulting from those changes;

• the level of our debt limiting financial flexibility or increasing borrowing costs;

• rating agency actions that could affect our ability to borrow funds;

• volatility in our tax rate due to a variety of different factors including U.S. federal income tax reform;

• changes in estimates or assumptions on our financial statements;

• limits on our subsidiaries to make dividend and other payments to us;

• the impact of lawsuits and other contingent liabilities and loss contingencies arising from errors and omissions (“E&O”) and other claims against us;

• the impact of, and potential challenges in complying with, legislation and regulation in the jurisdictions in which we operate, particularly given the global scope of our businesses and the possibility of conflicting regulatory requirements across jurisdictions in which we do business;

• the impact of any investigations brought by regulatory authorities in the U.S., U.K., and other countries;

• the impact of any inquiries relating to compliance with the U.S. Foreign Corrupt Practices Act and non-U.S. anti-corruption laws and with U.S. and non-U.S. trade sanctions regimes;

• failure to protect intellectual property rights or allegations that we infringe on the intellectual property rights of others;

• the effects of English law on our operating flexibility and the enforcement of judgments against us;

• the failure to retain and attract qualified personnel;

• international risks associated with our global operations;

• the effect of natural or man-made disasters;

• the potential of a system or network breach or disruption resulting in operational interruption or improper disclosure of personal data;

• our ability to develop and implement new technology;

• damage to our reputation among clients, markets or third parties;

• the actions taken by third parties that perform aspects of our business operations and client services;

• the extent to which we manage certain risks created in connection with the various services, including fiduciary and investment consulting and other advisory services, among others, that we currently provide, or will provide in the future, to clients;

• our ability to continue, and the costs and risks associated with, growing, developing and integrating companies that we acquire or new lines of business;

• changes in commercial property and casualty markets, commercial premium rates or methods of compensation;

• changes in the health care system or our relationships with insurance carriers;

• our ability to implement initiatives intended to yield cost savings and the ability to achieve those cost savings;

7

• our risks and uncertainties in connection with the sale of the Divested Business; and

• our ability to realize the expected benefits from our restructuring plan.

Any or all of our forward-looking statements may turn out to be inaccurate, and there are no guarantees about our performance. The factors identified above are not exhaustive. Aon and its subsidiaries operate in a dynamic business environment in which new risks may emerge frequently. Accordingly, readers should not place undue reliance on forward-looking statements, which speak only as of the dates on which they are made. We are under no obligation (and expressly disclaim any obligation) to update or alter any forward-looking statement that we may make from time to time, whether as a result of new information, future events or otherwise. Further information about factors that could materially affect Aon, including our results of operations and financial condition, is contained in the “Principal Risks and Uncertainties” section of this report.

PRINCIPAL RISKS AND UNCERTAINTIES

The principal risks and uncertainties set forth below reflect material risks associated with existing and potential business and contain “forward-looking statements” as discussed in the “Business Segment” section of this report. Readers should consider them in addition to the other information contained in this report as our business, financial condition, or results of operations could be adversely affected if any of these risks were to actually occur.

The following are material risks related to our business specifically and the industries in which we operate generally that could adversely affect our business, financial condition, and results of operations and cause our actual results to differ materially from those stated in the forward-looking statements in this document and elsewhere.

Business Risks

An overall decline in economic activity could have a material adverse effect on the financial condition and results of operations of our business.

The results of our operations are generally affected by the level of business activity of our clients, which in turn is affected by the level of economic activity in the industries and markets these clients serve. Economic downturns, volatility, or uncertainty in some markets may cause reductions in technology and discretionary spending by our clients, which may result in reductions in the growth of new business or reductions in existing business. If our clients become financially less stable, enter bankruptcy, liquidate their operations or consolidate, our revenues and collectability of receivables could be adversely affected.

The demand for property and casualty insurance generally rises as the overall level of economic activity increases and generally falls as such activity decreases, affecting both the commissions and fees generated by our Commercial Risk Solutions, Reinsurance Solutions, and Data and Analytic Services revenue lines. The economic activity that impacts property and casualty insurance is most closely correlated with employment levels, corporate revenue, and asset values. Downward fluctuations in the year-over-year insurance premiums charged by insurers to protect against the same risk, referred to in the industry as softening of the insurance market, could adversely affect these businesses as a significant portion of the earnings are determined as a percentage of premium charged to our clients. Insolvencies and consolidations associated with an economic downturn, especially insolvencies in the insurance industry, could adversely affect our brokerage business through the loss of clients by hampering our ability to place insurance and reinsurance business. Also, error and omission claims against us, which we refer to as E&O claims, may increase in economic downturns, also adversely affecting our business.

We face significant competitive pressures.

As a global professional services firm, we compete with global, national, regional and local insurance companies that market and service their own products, other financial services providers, brokers, and investment managers, independent firms, and consulting organizations affiliated with accounting, information systems, technology, and financial services firms. We compete with respect to service, product features, price, commission structure, financial strength, ability to access certain insurance markets, and name recognition.

Our competitors may have greater financial, technical and marketing resources, larger customer bases, greater name recognition, more comprehensive products, stronger presence in certain geographies, or more established relationships with their customers and suppliers than we have. In addition, new competitors, alliances among competitors, or mergers of competitors could emerge and gain significant market share, and some of our competitors may have or may develop a lower cost structure, adopt more aggressive pricing policies, or provide services that gain greater market acceptance than the services that we offer or develop. Competitors may be able to respond to the need for technological changes and innovate faster, or price their services more aggressively. They may also compete for skilled professionals, finance acquisitions, fund internal growth, and compete for market share more effectively than we do. This competition is intensified by an industry trend where clients engage multiple brokers to

8

service different portions of their accounts. If we fail to respond successfully to the competition we face, our financial condition or results of operations might be adversely affected.

If our clients or third parties are not satisfied with our services, we may face additional cost, loss of profit opportunities, damage to our reputation, or legal liability.

We depend, to a large extent, on our relationships with our clients and our reputation for high-quality advice and solutions focused on risk, retirement, and health. If a client is not satisfied with our services, it could cause us to incur additional costs and impair profitability. Many of our clients are businesses that band together in industry groups or trade associations and actively share information among themselves about the quality of service they receive from their vendors. Accordingly, poor service to one client may negatively impact our relationships with multiple other clients. Moreover, if we fail to meet our contractual obligations, we could be subject to legal liability or loss of client relationships.

The nature of much of our work involves assumptions and estimates concerning future events, the actual outcome of which we cannot know with certainty in advance. In our investment consulting business, we may be measured based on our track record regarding judgments and advice on investments that are susceptible to influences unknown at the time the advice was given. In addition, we could make computational, software programming, or data entry or management errors. A client may claim it suffered losses due to reliance on our consulting advice, which poses risks of liability exposure and costs of defense and increased insurance premiums. In addition, claims arising from our professional services may produce publicity that could hurt our reputation and business and adversely affect our ability to retain business or secure new business.

Damage to our reputation could have a material adverse effect on our business.

Our reputation is a key asset of the Company. We advise our clients on and provide services related to a wide range of subjects and our ability to attract and retain clients is highly dependent upon the external perceptions of our level of service, trustworthiness, business practices, financial condition, and other subjective qualities. Negative perceptions or publicity regarding these matters or others could erode trust and confidence and damage our reputation among existing and potential clients, which could make it difficult for us to attract new clients and retain existing ones. Negative public opinion could also result from actual or alleged conduct by us or those currently or formerly associated with us in any number of activities or circumstances, including third parties, the use and protection of data and systems, satisfaction of client expectations, and regulatory compliance. Damage to our reputation could affect the confidence of our clients, rating agencies, regulators, stockholders, and third parties in transactions that are important to our business adversely effecting our business, financial condition, and operating results.

Revenues from commission arrangements may fluctuate due to many factors, including cyclical or permanent changes in the insurance and reinsurance markets outside of our control.

Revenues from commission arrangements have historically been affected by significant fluctuations arising from uncertainties and changes in the industries in which we operate. A significant portion of our revenue consists of commissions paid to us out of the premiums that insurers and reinsurers charge our clients for coverage. We have no control over premium rates, and our revenues and profitability are subject to change to the extent that premium rates fluctuate or trend in a particular direction. The potential for changes in premium rates is significant, due to pricing cyclicality in the commercial insurance and reinsurance markets.

In addition to movements in premium rates, our ability to generate premium-based commission revenue may be challenged by:

• the growing availability of alternative methods for clients to meet their risk-protection needs, including a greater willingness on the part of corporations to “self-insure,” the use of so-called “captive” insurers, and the development of capital markets-based solutions and other alternative capital sources for traditional insurance and reinsurance needs that increase market capacity, increase competition and put pressure on pricing;

• fluctuation in the need for insurance;• the level of compensation, as a percentage of premium, that insurance carriers are willing to compensate brokers for

placement activity;• the growing desire of clients to move away from variable commission rates and instead compensate brokers based upon

flat fees, which can negatively impact us as fees are not generally indexed for inflation and do not automatically increase with premium as does commission-based compensation; and

• competition from insurers seeking to sell their products directly to consumers, including online sales, without the involvement of an insurance broker.

9

The profitability of our consulting engagements with clients may not meet our expectations due to unexpected costs, cost overruns, early contract terminations, unrealized assumptions used in our contract bidding process or the inability to maintain our prices.

Our profitability with respect to consulting engagements is highly dependent upon our ability to control our costs and improve our efficiency. As we adapt to changes in our business, adapt to the regulatory environment, enter into new engagements, acquire additional businesses, and take on new employees in new locations, we may not be able to manage our large, diverse and changing workforce, control our costs, or improve our efficiency.

Our profit margin, and therefore our profitability, is largely a function of the rates we are able to charge for our services and the staffing costs for our personnel. Accordingly, if we are not able to maintain the rates we charge for our services or appropriately manage the staffing costs of our personnel, we may not be able to sustain our profit margin and our profitability will suffer. The prices we are able to charge for our services are affected by a number of factors, including competitive factors, the extent of ongoing clients’ perception of our ability to add value through our services, and general economic conditions. If we cannot drive suitable cost efficiencies, our profit margins will suffer. Our cost efficiencies may also be impacted by factors such as our ability to transition consultants from completed projects to new assignments, our ability to secure new consulting engagements, our ability to forecast demand for consulting services (and, consequently, appropriately manage the size and location of our workforce), employee attrition, and the need to devote time and resources to training and professional and business development.

In our investment consulting business, we advise or act on behalf of clients regarding their investments. The results of these investments are uncertain and subject to numerous factors, some of which are within our control and some which are not. Clients that experience losses or lower than expected investment returns may leave us for competitors and/or assert claims against us.

Our investment consulting business provides advice to clients on: investment strategy, which can include advice on setting investment objectives, asset allocation, and hedging strategies; selection (or removal) of investment managers; the investment in different investment instruments and products; and the selection of other investment service providers such as custodians and transition managers. For some clients, we are responsible for making decisions on these matters and we may implement such decisions in a fiduciary or agency capacity without assuming title or custody over the underlying funds or assets invested. Asset classes may experience poor absolute performance and third parties we recommend or select, such as investment managers, may underperform their benchmarks due to poor market performance, negligence, or other reasons, resulting in poor investment returns or losses. These losses may be attributable in whole or in part to failures on our part or to events entirely outside of our control, including but not limited to uncertainty in financial markets due to economic, political, and regulatory conditions. Regardless of the cause, clients experiencing losses or clients that allege that we overcharge for such fiduciary services have in the past asserted claims against us, and we anticipate future similar claims, which could be for significant amounts. Defending against these claims can involve potentially significant costs, including legal defense costs, as well as cause substantial distraction and diversion of other resources. Furthermore, our ability to limit our potential liability is restricted in certain jurisdictions and in connection with claims involving breaches of fiduciary or agency duties or other alleged errors or omissions. Additionally, clients experiencing losses or lower than expected investment returns may leave us for our competitors.

Financial Risks

We are exposed to fluctuations in currency exchange rates that could negatively impact our financial results and cash flows.

We face exposure to adverse movements in exchange rates of currencies other than our reporting currency, the U.S. dollar, as a significant portion of our business is located outside of the U.S. These exposures may change over time, and they could have a material adverse impact on our financial results and cash flows. Approximately 57% of our consolidated revenue is non-U.S., attributed on the basis of where the services are performed, and the exposures created can have significant currency volatility. These currency exchange fluctuations create risk in both the translation of the financial results of our global subsidiaries into U.S. dollars for our consolidated financial statements, as well as in those of our operations that receive revenue and incur expenses other than in their respective local currencies, which can reduce the profitability of our operations based on the direction the respective currencies’ exchange rates move. A decrease in the value of certain currencies relative to other currencies could place us at a competitive disadvantage compared to our competitors that benefit to a greater degree from a specific exchange rate move and can, as a result, deliver services at a lower cost or receive greater revenues from such a transaction. Although we use various derivative financial instruments to help protect against adverse foreign exchange rate fluctuations, we cannot eliminate such risks, and, as a result, changes in exchange rates may adversely affect our results. For example, the strengthening of the value of the U.S. dollar versus other currencies might adversely affect the value of our products and services when translated to U.S. dollar, even if the value of such products and services has not changed in their original currency.

Changes in interest rates and deterioration of credit quality could reduce the value of our cash balances and investment portfolios and adversely affect our financial condition or results.

10

Operating funds available for corporate use were $828 million at December 31, 2018 and are reported in Cash and cash equivalents and Short-term investments. Funds held on behalf of clients and insurers were $3.9 billion at December 31, 2018 and are reported in Fiduciary assets. We also carry an investment portfolio of other long-term investments. As of December 31, 2018, these long-term investments had a carrying value of $54 million. Adverse changes in interest rates, performance, and counterparty credit quality, including default, could reduce the value of these funds and investments, thereby adversely affecting our financial condition or results. We may experience reduced investment earnings on our cash and short-term investments of fiduciary and operating funds if the yields on investments deemed to be low risk remain at or near their current low levels, or if negative yields on deposits or investments are experienced, as we have experienced in Japan and certain jurisdictions in the European Union. On the other hand, higher interest rates could result in a higher discount rate used by investors to value our future cash flows thereby resulting in a lower valuation of the Company. In addition, during times of stress in the banking industry, counterparty risk can quickly escalate, potentially resulting in substantial losses for us as a result of our cash or other investments with such counterparties, as well as substantial losses for our clients and the insurance companies with which we work.

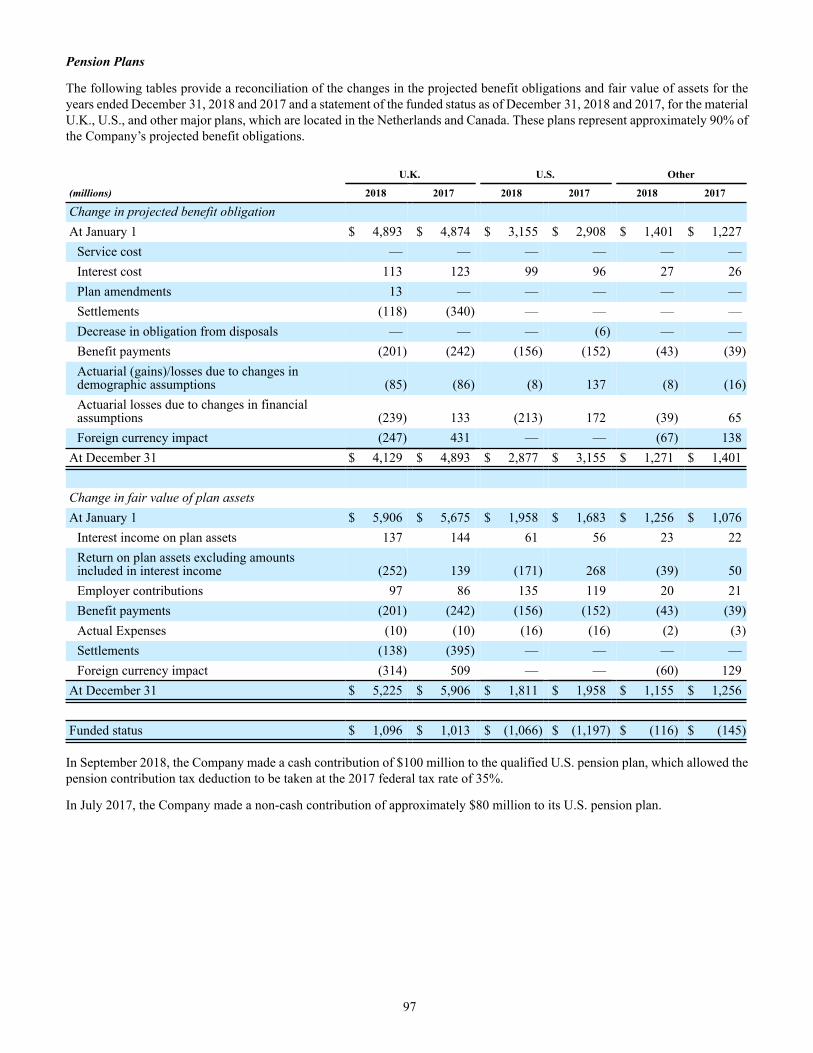

Our pension obligations and value of our pension assets could adversely affect our shareholders’ equity, net income, cash flow and liquidity.

To the extent that the pension obligations associated with our pension plans continue to exceed the fair value of the assets supporting those obligations, our financial position and results of operations may be adversely affected. In particular, lower interest rates and investment returns could result in the present value of plan liabilities increasing at a greater rate than the value of plan assets, resulting in higher unfunded positions in our pension plans. In addition, the periodic revision of pension assumptions or variances of actual results from our assumptions can materially change the present value of expected future benefits, and therefore the funded status of the plans and resulting net periodic pension expense. As a result, we may experience future changes in the funded status of our plans that could require us to make additional cash contributions beyond those that have been estimated and which could adversely affect shareholders’ equity, net income, cash flow and liquidity.

Our worldwide pension plans are significant, and therefore our pension contributions and expense are sensitive to various market, demographic, and other factors. These factors include equity and bond market returns, fair value of pension assets, the assumed interest rates we use to discount our pension liabilities, foreign exchange rates, rates of inflation, mortality assumptions, potential regulatory and legal changes or developments and counterparty exposure from various investments and derivative contracts, including annuities. Variations or developments in connection with any of these factors could cause significant changes to our financial position and results of operations from year to year. In addition, contributions are generally based on statutory requirements and local funding practices, which may differ from measurements under International Financial Reporting Standards as endorsed by the European Union (“IFRS”).

We have debt outstanding that could adversely affect our financial flexibility.

As of December 31, 2018, we had total consolidated debt outstanding of approximately $6.2 billion. The level of debt outstanding could adversely affect our financial flexibility by reducing our ability to use cash from operations for other purposes, including working capital, dividends to shareholders, share repurchases, acquisitions, capital expenditures and general corporate purposes. We also are subject to risks that, at the time any of our outstanding debt matures, we will not be able to retire or refinance the debt on terms that are acceptable to us, or at all.

As of December 31, 2018, we had two committed credit facilities outstanding. Each of these facilities is intended to support our commercial paper obligations and our general working capital needs. In addition, each of these facilities included customary representations, warranties, and covenants, including financial covenants that require us to maintain specified ratios of adjusted consolidated earnings before interest, taxes, depreciation, and amortization (“EBITDA”) to consolidated interest expense and consolidated debt to adjusted consolidated EBITDA, tested quarterly.

A substantial portion of our outstanding debt, including certain intercompany debt obligations, contains financial and other covenants. The terms of these covenants may limit our ability to obtain, or increase the costs of obtaining, additional financing to fund working capital, capital expenditures, acquisitions, or general corporate requirements. This in turn may have the impact of reducing our flexibility to respond to changing business and economic conditions, thereby placing us at a relative disadvantage compared to competitors that have less indebtedness, or fewer or less onerous covenants associated with such indebtedness, and making us more vulnerable to general adverse economic and industry conditions.

If we cannot service our indebtedness, we may have to take actions such as selling assets, seeking additional equity, or reducing or delaying capital expenditures, strategic acquisitions, investments, and alliances, any of which could impede the implementation of our business strategy or prevent us from entering into transactions that would otherwise benefit our business. Additionally, we may not be able to effect such actions or refinance any of our debt, if necessary, on commercially reasonable terms, or at all.

11

A decline in the credit ratings of our senior debt and commercial paper may adversely affect our borrowing costs, access to capital, and financial flexibility.

A downgrade in the credit ratings of our senior debt and commercial paper could increase our borrowing costs, reduce or eliminate our access to capital, reduce our financial flexibility, and limit our ability to implement on corporate strategy. Our senior debt ratings at December 31, 2018 were A- with a stable outlook (Standard & Poor’s, or “S&P”), BBB+ with a stable outlook (Fitch, Inc., or “Fitch”), and Baa2 with a stable outlook (Moody’s Investor Services, or “Moody’s”). Our commercial paper ratings were A-2 (S&P), F-2 (Fitch) and P-2 (Moody’s).

Real or anticipated changes in our credit ratings will generally affect any trading market for, or trading value of, our securities. Such changes could result from any number of factors, including the modification by a credit rating agency of the criteria or methodology it applies to particular issuers, a change in the agency’s view of us or our industry, or as a consequence of actions we take to implement our corporate strategies. A change in our credit rating could adversely limit our access to capital and our competitive position.

U.S. federal income tax reform could create uncertainty and adversely affect our business and financial condition.

On December 22, 2017, U.S. federal tax legislation, commonly referred to as the Tax Cuts and Jobs Act (the “Tax Reform Act”), was signed into law, significantly changing the U.S. Internal Revenue Code. These changes include, among other things, lowering the corporate income tax rate, subjecting certain future foreign subsidiary earnings, whether or not distributed, to U.S. tax under a Global Intangible Low-Taxed Income provision, imposing a new alternative “Base Erosion and Anti-Abuse Tax” on U.S. corporations that limits deductions for certain deductible amounts payable to foreign affiliates, imposing significant additional limitations on the deductibility of interest payable to related and unrelated lenders, further limiting deductible executive compensation, and imposing a one-time repatriation tax on deemed repatriated earnings of foreign subsidiaries accumulations through the end of 2017. The new provisions have been the subject of proposed regulations and other guidance that, if and when issued in final form, could materially affect the application of the new statutory provisions. In many cases, the proposed regulations and other guidance proposed to apply retroactively to the date of enactment of the Tax Reform Act. The government could also further modify the rules when they are issued in final form. We continue to analyze how the Tax Reform Act, and any regulations or other governmental action with respect thereto, may impact our business and results of operations. The changes effected pursuant to the Tax Reform Act, and the regulations or other governmental action thereunder, may have an adverse or volatile effect on our tax rate in fiscal years 2019 and beyond, thereby affecting our results of operations. Additionally, the resulting uncertainty with respect to the interpretation and application of the new provisions, and the risk that regulations or other governmental guidance, including revisions to any such regulations or other governmental action that may change the application of the new statutory provisions, may affect our assessment of the effect of the Tax Reform Act on our business and operations as we continue to analyze it.

Our global effective tax rate is subject to a variety of different factors, which could create volatility in that tax rate, expose us to greater than anticipated tax liabilities or cause us to adjust previously recognized tax assets and liabilities.

We are subject to income taxes in the U.K., U.S. and many other jurisdictions. As a result, our global effective tax rate from period to period can be affected by many factors, including changes in tax legislation or regulations, such as the enactment of the U.S. Tax Reform Act detailed above, the continuing development of regulations and other governmental action that affect the application of such legislation, our global mix of earnings, the use of global funding structures, the tax characteristics of our income, the effect of complying with transfer pricing requirements under laws of many different countries on our revenues and costs, the consequences of acquisitions and dispositions of businesses and business segments, and the portion of the income of non-U.S. subsidiaries that may be subject to U.S. tax, or the portion of the income of non-U.K subsidiaries that may be subject to U.K. tax, whether or not distributed to the respective U.S. or U.K. shareholders. In addition, we could be subject to increased taxation as a result of changes in eligibility for the benefits of current income tax treaties between and among the U.K., the U.S., and other countries, including any future amendments to the current income tax treaties between the U.K. and other jurisdictions (including the U.S.), or any new statutory or regulatory provisions that might limit our ability to take advantage of any such treaties. Significant judgment is required in determining our worldwide provision for income taxes, and our determination of the amount of our tax liability is always subject to review by applicable tax authorities. Our actual global tax rate may vary from our expectation and that variance may be material.

We are subject to tax audits conducted by U.S., U.K., and other tax authorities, and the resolution of such audits could impact our tax rate in future periods, as would any reclassification or other changes (such as those in applicable accounting rules) that increases the amounts we have provided for income taxes in our consolidated financial statements. There can be no assurance that we would be successful in attempting to mitigate the adverse impacts resulting from any changes in law, audits and other matters. Our inability to mitigate the negative consequences of any changes in the law, audits and other matters could cause our global tax rate to increase, our use of cash to increase and our financial condition and results of operations to suffer.

12

Changes in our accounting estimates and assumptions could negatively affect our financial position and results of operations.

We prepare our consolidated financial statements in accordance with IFRS. IFRS require us to make estimates and assumptions that affect the reported amounts of assets and liabilities, and the disclosure of contingent assets and liabilities at the date of our financial statements. We are also required to make certain judgments that affect the reported amounts of revenues and expenses during each reporting period. We periodically evaluate our estimates and assumptions including, but not limited to, those relating to revenue recognition, restructuring, pensions, recoverability of assets including customer receivables, valuation of goodwill and intangibles, contingencies, share-based payments, and income taxes. We base our estimates on historical experience and various assumptions that we believe to be reasonable based on specific circumstances. These assumptions and estimates involve the exercise of judgment and discretion, which may evolve over time in light of operational experience, regulatory direction, developments or changes in accounting principles or standards, and other factors. Actual results could differ from these estimates, or changes in assumptions, estimates, policies, or developments in the business may change our initial estimates, which could materially affect the Consolidated Statements of Income, Comprehensive Income, Financial Position, Shareholders’ Equity, and Cash Flows.

We may be required to record goodwill or other long-lived asset impairment charges, which could result in a significant charge to earnings.

Under IFRS, we review our long-lived assets for impairment when events or changes in circumstances indicate the carrying value may not be recoverable. Goodwill is assessed for impairment at least annually. Factors that may be considered in assessing whether goodwill or other long-lived assets may not be recoverable include a decline in our share price or market capitalization, reduced estimates of future cash flows and slower growth rates in our industry. We may experience unforeseen circumstances that adversely affect the value of our goodwill or other long-lived assets and trigger an evaluation of the recoverability of the recorded goodwill and other long-lived intangible assets. Future goodwill or other long-lived asset impairment charges could materially impact our consolidated financial statements.

We are a holding company and, therefore, may not be able to receive dividends or other payments in needed amounts from our subsidiaries.

The Company is organized as a holding company, a legal entity separate and distinct from our operating entities. As a holding company without significant operations of its own, our principal assets are the shares of capital stock of our subsidiaries. We rely on dividends, interest, and other payments from these subsidiaries to meet our obligations for paying principal and interest on outstanding debt, paying dividends to shareholders, repurchasing ordinary shares, and corporate expenses. Certain of our subsidiaries are subject to regulatory requirements of the jurisdictions in which they operate or other restrictions that may limit the amounts that subsidiaries can pay in dividends or other payments to us. No assurance can be given that there will not be further changes in law, regulatory actions, or other circumstances that could restrict the ability of our subsidiaries to pay dividends or otherwise make payments to us. Furthermore, no assurance can be given that our subsidiaries may be able to make timely payments to us in order for us to meet our obligations.

Legal and Regulatory Risks

We are subject to E&O claims against us as well as other contingencies and legal proceedings, some of which, if determined unfavorably to us, could have a material adverse effect on the financial condition or results of operations of a business line or the Company as a whole.

We assist our clients with various matters, including placing insurance and reinsurance coverage and handling related claims, consulting on various human resources matters, and providing actuarial, investment consulting, and asset management services. E&O claims against us may allege our potential liability for damages arising from these services. E&O claims could include, for example, the failure of our employees or sub-agents, whether negligently or intentionally, to place coverage correctly or notify carriers of claims on behalf of clients, to provide insurance carriers with complete and accurate information relating to the risks being insured, or the failure to give error-free consulting or investment advice. It is not always possible to prevent and detect E&O, and the precautions we take may not be effective in all cases. In addition, we are subject to other types of claims, litigation, and proceedings in the ordinary course of business, which along with E&O claims, may seek damages, including punitive damages, in amounts that could, if awarded, have a material adverse impact on the Company’s financial position, earnings, and cash flows. In addition to potential liability for monetary damages, such claims or outcomes could harm our reputation or divert management resources away from operating our business.

We have historically purchased, and intend to continue to purchase, insurance to cover E&O claims and other insurance to provide protection against certain losses that arise in such matters. However, we have exhausted or materially depleted our coverage under some of the policies that protect us for certain years and, consequently, are self-insured or materially self-insured for some historical claims. Additionally, parts or all of an E&O claim could fall within insurance deductibles, self-insured retentions, or policy exclusions. Accruals for these exposures, and related insurance receivables, when applicable, have been provided to the

13

extent that losses are deemed probable and are reasonably estimable. These accruals and receivables are adjusted from time to time as developments warrant and may also be adversely affected by disputes we may have with our insurers over coverage. Amounts related to settlement provisions are recorded in Other general expenses in the Consolidated Statements of Income. Discussion of some of these claims, lawsuits, and proceedings are contained in the Notes to Consolidated Financial Statements.

In addition, we provide a variety of guarantees and indemnifications to our customers and others. In the event of a default, Aon’s potential exposure is equal to the amount of the guarantee or indemnification.

The ultimate outcome of claims, lawsuits, proceedings, guarantees and indemnifications cannot be ascertained, and liabilities in indeterminate amounts may be imposed on us. It is possible that future results of operations or cash flows for any particular annual period could be materially affected by an unfavorable resolution of these matters.

Our businesses are subject to extensive governmental regulation, which could reduce our profitability, limit our growth, or increase competition.

Our businesses are subject to extensive legal and regulatory oversight throughout the world, including the U.K. Companies Act and the rules and regulations promulgated by the FCA, the U.S. securities laws, rules, and regulations, and a variety of other laws, rules, and regulations addressing, among other things, licensing, data privacy and protection, trade restriction and export controls, anti-money laundering, wage-and-hour standards, employment and labor relations, anti-competition, anti-corruption, currency, reserves, government contracting, and the amount of local investment with respect to our operations in certain countries. This legal and regulatory oversight could reduce our profitability or limit our growth by: increasing the costs of legal and regulatory compliance; limiting or restricting the products or services we sell, the markets we serve or enter, the methods by which we sell our products and services, the prices we can charge for our services, or the form of compensation we can accept from our clients, carriers, and third parties; or by subjecting our businesses to the possibility of legal and regulatory actions, proceedings, or fines.

The global nature of our operations increases the complexity and cost of compliance with laws and regulations adding to our cost of doing business. In addition, many of these laws and regulations may have differing or conflicting legal standards across jurisdictions, increasing the complexity and cost of compliance. In emerging markets and other jurisdictions with less developed legal systems, local laws and regulations may not be established with sufficiently clear and reliable guidance to provide us adequate assurance that we are operating our business in a compliant manner with all required licenses or that our rights are otherwise protected. In addition, certain laws and regulations, such as the Foreign Corrupt Practices Act (“FCPA”) and the Foreign Account Tax Compliance provisions of the Hiring Incentives to Restore Employment Act (“FATCA”) in the U.S., and the Bribery Act of 2010 (“U.K. Bribery Act”) in the U.K., impact our operations outside of the legislating country by imposing requirements for the conduct of overseas operations, and in several cases, requiring compliance by foreign subsidiaries.

In addition to the complexity of the laws and regulations themselves, the development of new laws and regulations or changes in application or interpretation of current laws and regulations also increases our legal and regulatory compliance complexity. Additionally, our acquisitions of new businesses and our continued operational changes and entry into new jurisdictions and new service offerings increases our legal and regulatory compliance complexity, as well as the type of governmental oversight to which we may be subject. Changes in laws and regulations could mandate significant and costly changes to the way we implement our services and solutions, could impose additional licensure requirements or costs to our operations and services, or even cause us to cease offering certain services or solutions. Furthermore, as we enter new jurisdictions or businesses and further develop and expand our services, we may become subject to additional types of laws and policies and governmental oversight and supervision, such as those applicable to the financial lending or other service institutions. New regulatory developments that could result in changes that adversely affect us or cause us to change our business or operations include: additional requirements respecting data privacy, data security, and data usage in jurisdictions in which we operate that may increase our costs of compliance and potentially reduce the manner in which we can use data; additional changes in tax regulations in the jurisdictions in which we operate; changes in accounting standards; regulatory actions or changes that require us to change our compensation model; or additional regulations promulgated by the FCA in the U.K., or other regulatory bodies in jurisdictions in which we operate.

In all jurisdictions, the applicable laws and regulations are subject to amendment or interpretation by regulatory authorities. Generally, such authorities are vested with relatively broad discretion to grant, renew, and revoke licenses and approvals and to implement regulations. Accordingly, we may have a license revoked or be unable to obtain new licenses and therefore be precluded or temporarily suspended from carrying on or developing some or all of our activities or otherwise fined or penalized in a given jurisdiction. No assurances can be given that our business can further develop or continue to be conducted in any given jurisdiction in the future as it has been conducted in the past.

Changes in the regulatory scheme, or even changes in how existing regulations are interpreted, could have an adverse impact on our results of operations by limiting revenue streams or increasing costs of compliance. For instance, The General Data Protection Regulation (“GDPR”), which became effective in May 2018, created a range of new compliance obligations, increased financial penalties for non-compliance, and extended the scope of the European Union data protection law to all companies processing data

14

of European Union residents, wherever the company’s location. We have incurred substantial operational costs to bring our practices into compliance with GDPR and where other jurisdictions enact privacy and data protection regulations, we will incur further expenses to bring our practices in compliance with those regulations, which may differ from GDPR.

Our business’ regulatory oversight also includes licensing of insurance brokers and agents, managing general agency or general underwriting operations, and the regulation of the handling and investment of client funds held in a fiduciary capacity. Our continuing ability to provide insurance broking in the jurisdictions in which we operate depends on our compliance with the rules and regulations promulgated by the regulatory authorities in each of these jurisdictions. Also, we can be affected indirectly by the governmental regulation and supervision of insurance companies. For instance, if we are providing or managing general underwriting services for an insurer, we may have to contend with regulations affecting our client.

Services provided in our Health Solutions and Retirement Solutions revenue lines are also the subject of ever-evolving government regulation, either because the services provided to our clients are regulated directly or because third parties upon whom we rely to provide services to clients are regulated, thereby indirectly affecting the manner in which we provide services to those clients. In particular, our health care exchange business depends upon the private sector of the U.S. insurance system and its role in financing health care delivery, and insurance carriers’ use and payment of commissions to agents, brokers, and other organizations to market and sell individual and family health insurance products and plans. Uncertainty regarding, or any changes to, state or federal law, or the interpretation of such law by applicable regulatory agencies, including the effects of health care reform by the U.S. government, could delay client adoption of our health care exchanges, impair our ability to retain clients who have adopted our health care exchanges, or cause insurance carriers to alter or eliminate the products and plans that they offer or attempt to move members into new products or plans for which we receive lower commissions. In addition, changes in laws, government regulations, or the way those regulations are interpreted in the jurisdictions in which we operate could affect the viability, value, use, or delivery of benefits and human resources programs, including changes in regulations relating to health and welfare plans (such as medical), defined contribution plans (such as 401(k)), or defined benefit plans (such as pension), may adversely affect the demand for, or profitability of, our services.

If we violate the laws and regulations to which we are subject, we could be subject to fines, penalties, or criminal sanctions and could be prohibited from conducting business in one or more countries. There can be no assurance that our employees, contractors, or agents will not violate these laws and regulations, causing an adverse effect on our operations and financial condition.

Heightened regulatory oversight and scrutiny may lead to additional regulatory investigations, increased government involvement, or enforcement actions. For instance, increased scrutiny by competition authorities may increase our costs of doing business or force us to change the way we conduct business or refrain from or otherwise alter the way we engage in certain activities. Additionally, we operate in many different business lines, which may occasionally intersect with each other, such as placing both insurance and reinsurance or providing both investment consultancy and fiduciary management services. If we fail to control possible resulting conflicts of interest, we could be subject to civil litigation, fines, penalties, and criminal sanctions and could be prohibited from participating in one or more lines of business. As regulators and other government agencies continue to examine our operations, there is no assurance that consent orders or other enforcement actions will not be issued by them in the future. These and other initiatives from national, state, and local officials may subject us to judgments, settlements, fines, or penalties, or cause us to be required to restructure or divest operations and activities, all of which could lead to reputational issues, higher operational costs, business disruption or loss, thereby adversely affecting our business, financial condition, or operating results.

Failure to protect our intellectual property rights, or allegations that we have infringed on the intellectual property rights of others, could harm our reputation, ability to compete effectively, and financial condition.

To protect our intellectual property rights, we rely on a combination of trademark laws, copyright laws, patent laws, trade secret protection, confidentiality agreements, and other contractual arrangements with our affiliates, employees, clients, strategic partners, and others. However, the protective steps that we take may be inadequate to deter misappropriation of our proprietary information. In addition, we may be unable to detect the unauthorized use of, or take appropriate steps to enforce, our intellectual property rights. Further, effective trademark, copyright, patent, and trade secret protection may not be available in every country in which we offer our services or competitors may develop products similar to our products that do not conflict with our related intellectual property rights. Failure to protect our intellectual property adequately could harm our reputation and affect our ability to compete effectively.

In addition, to protect or enforce our intellectual property rights, we may initiate litigation against third parties, such as infringement suits or interference proceedings. Third parties may assert intellectual property rights claims against us, which may be costly to defend, could require the payment of damages, and could limit our ability to use or offer certain technologies, products or other intellectual property. Any intellectual property claims, with or without merit, could be expensive, take significant time and divert management’s attention from other business concerns. Successful challenges against us could require us to modify or discontinue our use of technology or business processes where such use is found to infringe or violate the rights of others, or

15

require us to purchase licenses from third parties, any of which could adversely affect our business, financial condition, and operating results.

We have less flexibility as a public limited company incorporated under the laws of England and Wales with respect to certain aspects of capital management.

English law imposes additional restrictions on certain corporate actions. For example, English law provides that a board of directors may only allot securities with the prior authorization of shareholders, with such authorization specifying a maximum amount of shares that may be allotted under it, and lasting for a maximum period of five years, each as specified in the articles of association or relevant shareholder resolution. The current authorization is effective until the earlier of our next annual general meeting or August 31, 2019. This authorization will need to be renewed by our shareholders periodically and we intend to renew this authorization at each annual general meeting.

English law also generally provides shareholders with preemptive rights when new shares are issued for cash; however, it is possible for the articles of association, or shareholders in general meeting, to exclude preemptive rights. Such an exclusion of preemptive rights may be for a maximum period of up to five years as specified in the articles of association or relevant shareholder resolution. The current exclusion is effective until the earlier of our next annual general meeting or August 31, 2019. This exclusion would need to be renewed by our shareholders periodically and we intend to renew this exclusion at each annual general meeting.

English law also requires us to have available “distributable reserves” to make share repurchases or pay dividends to shareholders. Distributable reserves may be created through the earnings of the U.K. parent company (the “Parent Company”) or other actions. As of December 31, 2018, we had distributable reserves in excess of $3.7 billion. While it is our intention to maintain a sufficient level of distributable reserves in order to pay dividends on our ordinary shares and make share repurchases, there is no assurance that the Parent Company level will maintain the necessary level of distributable reserves to do so. If at any time we do not have sufficient distributable reserves to declare and pay dividends, we may undertake a reduction in capital of the Company to reduce the amount of our share capital and non-distributable reserves and to create a corresponding increase in our distributable reserves out of which future distributions to shareholders could be made.

English law also generally prohibits a company from repurchasing its own shares by way of “off-market purchases” without the prior approval of our shareholders. Such approval lasts for a maximum period of up to five years. Our shares are traded on the New York Stock Exchange (“NYSE”), which is not a recognized investment exchange in the U.K. Consequently, any repurchase of our shares is currently considered an “off market purchase.” The current authorization expires on June 22, 2023. Renewal of this authorization will be sought periodically.

The enforcement of civil liabilities against us may be more difficult.

Because we are a public limited company incorporated under the laws of England and Wales, investors could experience more difficulty enforcing judgments obtained against us in U.S. courts than would have been the case for a U.S. company. In addition, it may be more difficult (or impossible) to bring some types of claims against us in courts in England than it would be to bring similar claims against a U.S. company in a U.S. court.

We are a public limited company incorporated under the laws of England and Wales. Therefore, it may not be possible to effect service of process upon us within the U.S. in order to enforce judgments of U.S. courts against us based on the civil liability provisions of the U.S. federal securities laws.

There is doubt as to the enforceability in England and Wales, in original actions or in actions for enforcement of judgments of U.S. courts, of civil liabilities solely based on the U.S. federal securities laws. The English courts will, however, treat any amount payable by us under U.S. judgment as a debt and new proceedings can be commenced in the English courts to enforce this debt against us. The following criteria must be satisfied in order for the English court to enforce the debt created by the U.S. judgment:

• the U.S. court having had jurisdiction over the original proceedings according to English conflicts of laws principles and rules of English private international law at the time when proceedings were initiated;

• the U.S. proceedings not having been brought in breach of a jurisdiction or arbitration clause except with the agreement of the defendant or the defendant’s subsequent submission to the jurisdiction of the court;

• the U.S. judgment being final and conclusive on the merits in the sense of being final and unalterable in the court which pronounced it and being for a definite sum of money;

• the recognition or enforcement, as the case may be, of the U.S. judgment not contravening English public policy in a sufficiently significant way or contravening the Human Rights Act 1998 (or any subordinate legislation made thereunder, to the extent applicable);

• the U.S. judgment not being for a sum payable in respect of taxes, or other charges of a like nature, or in respect of a penalty or fine, or otherwise based on a U.S. law that an English court considers to be a penal or revenue law;

16

• the U.S. judgment not having been arrived at by doubling, trebling or otherwise multiplying a sum assessed as compensation for the loss or damages sustained, and not otherwise being a judgment contrary to section 5 of the Protection of Trading Interests Act 1980 or is a judgment based on measures designated by the Secretary of State under Section 1 of that Act;

• the U.S. judgment not having been obtained by fraud or in breach of English principles of natural justice; • the U.S. judgment not being a judgment on a matter previously determined by an English court, or another court whose

judgment is entitled to recognition (or enforcement as the case may be) in England, in proceedings involving the same parties which conflicts with an earlier judgment of such court;

• the party seeking enforcement (being a party who is not ordinarily resident in some part of the U.K. or resident in an EU Member State) providing security for costs, if ordered to do so by the English courts; and

• the English enforcement proceedings being commenced within the relevant limitation period.

If an English court gives judgment for the sum payable under a U.S. judgment, the English judgment will be enforceable by methods generally available for this purpose. These methods generally permit the English court discretion to prescribe the manner of enforcement. Also note that, in any enforcement proceedings, the judgment debtor may raise any counterclaim that could have been brought if the action had been originally brought in England unless the subject of the counterclaim was in issue and denied in the U.S. proceedings.

Operational Risks

The economic and political conditions of the countries and regions in which we operate, including the U.K.’s expected withdrawal from the European Union, could have an adverse impact on our business, financial condition, operating results, liquidity, and prospects for growth.

Our operations in countries undergoing political change or experiencing economic instability are subject to uncertainty and risks that could materially adversely affect our business. These risks include, particularly in emerging markets, the possibility we would be subject to undeveloped or evolving legal systems, unstable governments and economies, and potential governmental actions affecting the flow of goods, services, and currency.