UK - Actuarial Advisory Firm of the Year UK - Pensions Advisor of the Year January 2015

UK - Actuarial Advisory Firm of the Year UK - Pensions Advisor of the Year January 2015.

Dec 18, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

UK - Actuarial Advisory Firm of the YearUK - Pensions Advisor of the Year

January 2015

Agenda

Changes to DC pensions

Product innovation

Engagement innovation

Global lessons

Market structure changes

2

Benefit access from 6 April 2015

Income drawdown (flexi-access drawdown)

Taking a single or series of lump sums from uncrystallised funds (UFPLS)

Buying a lifetime annuity

Scheme pension

3

Previous DC investment focus

4

Growth phaseInvestment choice and engagement

focused here

Protection phaseCommon destination point of

purchasing an annuity

Growth phaseMay need to simplify choice in the growth phase so that more of the

governance budget can be re-directed to the protection phase

DC investment focus now

5

Protection phaseGovernance budget focused on

designing strategies based on how members are expected to retire

Protection phase – in reality

6

Growth phaseMay need to simplify choice in the growth phase so that more of the

governance budget can be re-directed to the protection phase

Protection phaseGovernance budget focused on

designing strategies based on how members are expected to retire

Investment framework

7

Drawdown innovation – wish list

8

Provides sustainable level of income

Provides inflation protection

Growth-seeking but with a capital preservation focus

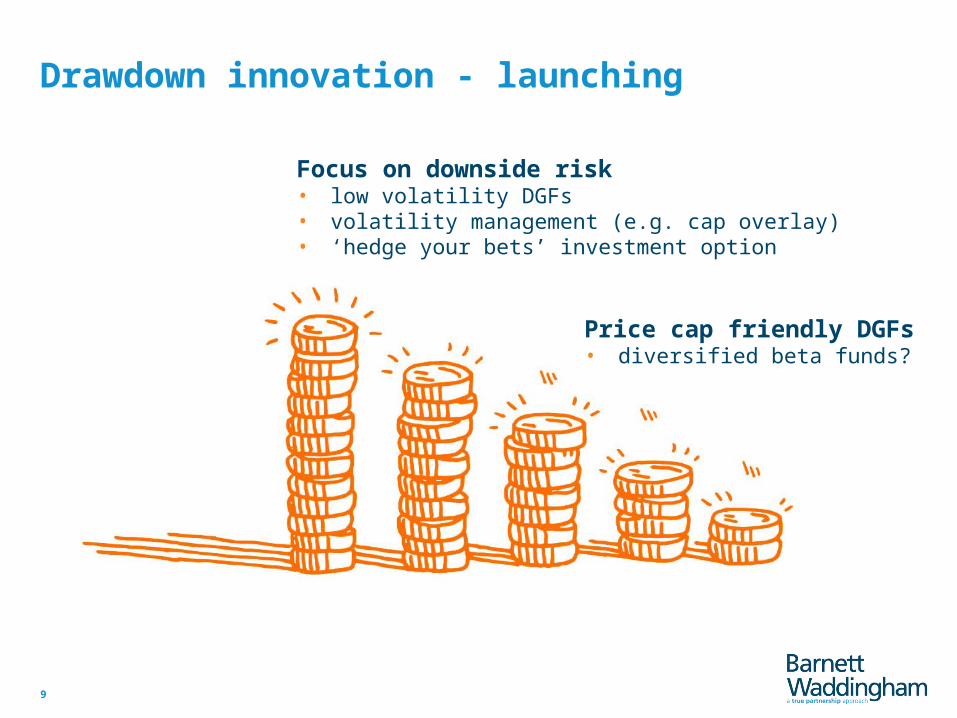

Drawdown innovation - launching

9

Price cap friendly DGFs• diversified beta funds?

Focus on downside risk• low volatility DGFs• volatility management (e.g. cap overlay)• ‘hedge your bets’ investment option

Developments in the annuity market

10

Biggest unknown is life expectancy

Consistently underestimated

Biggest risk is running out of

money

•Annuities benefit from the pooling of longevity risk allowing for health status

•Deferred annuities? Temporary annuities? Variable annuities?

No ‘default’ default

Membership specific

Pot size specific

Analysis needs to evolve with the membership

Needs of those retiring now different vs those retiring in 15 years

11

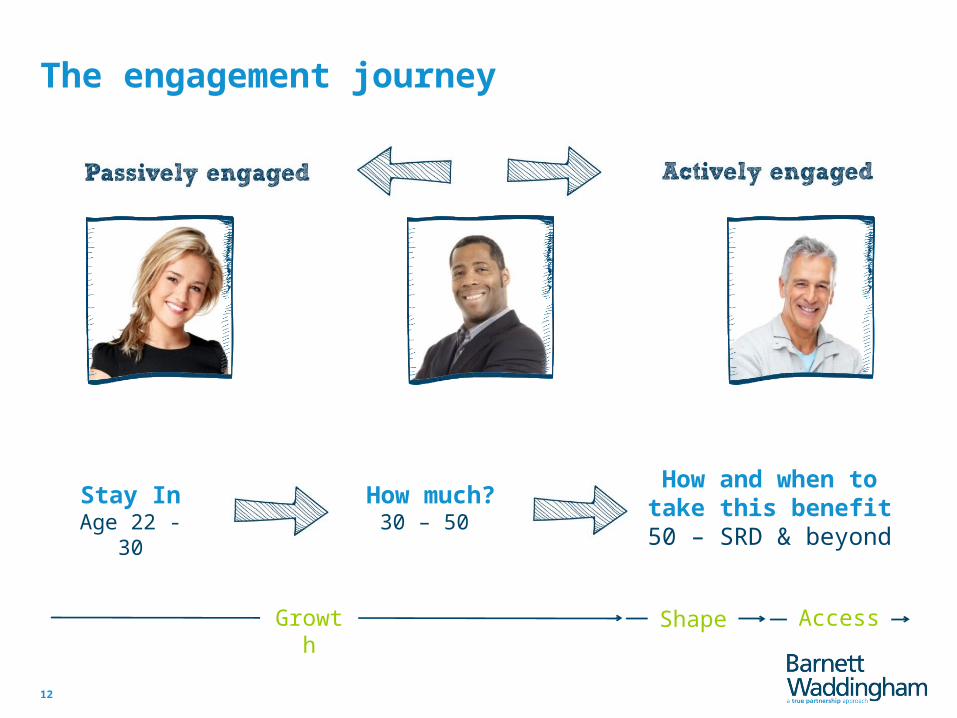

The engagement journey

12

Key messages:

Stay InAge 22 - 30

How much?30 – 50

How and when to take this benefit

50 – SRD & beyond

Growth Shape Access

Innovation in communication

Good member communications need to accompany innovative investment products

13

Key challenges

Administration systems

Legacy issues

Pressure applied by ‘all’ schemes trying to be ready by April

Communication issues (e.g. double defaulters)

Investment strategy agreed now will need to change (mitigated somewhat by future-proofing)

14

What can we learn from others?

15

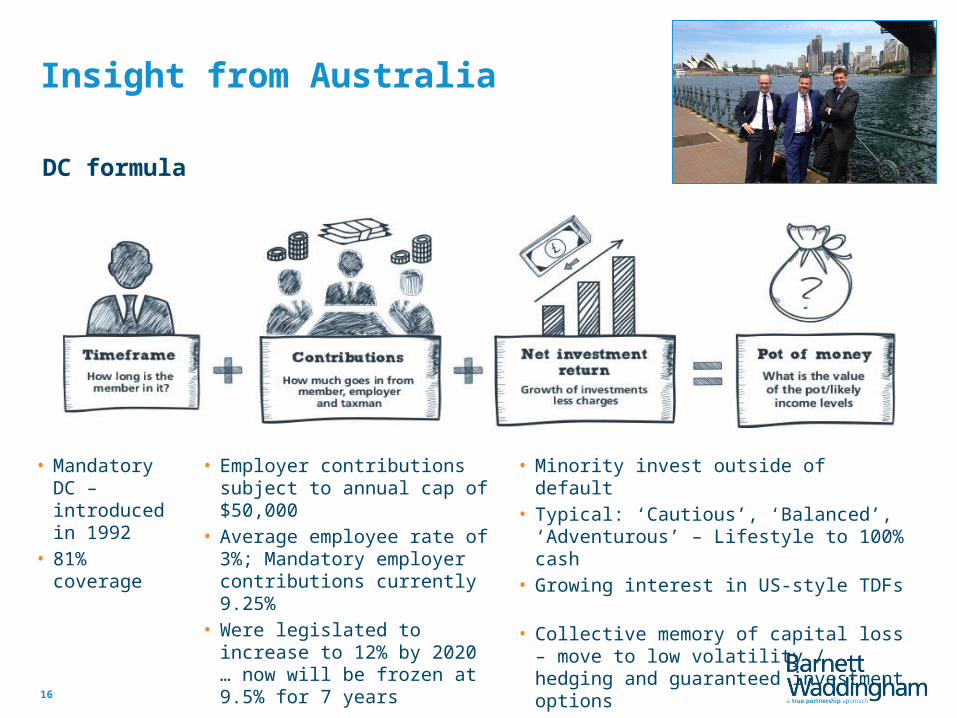

Insight from Australia

16

• Mandatory DC – introduced in 1992

• 81% coverage

• Employer contributions subject to annual cap of $50,000

• Average employee rate of 3%; Mandatory employer contributions currently 9.25%

• Were legislated to increase to 12% by 2020 … now will be frozen at 9.5% for 7 years

• Minority invest outside of default • Typical: ‘Cautious’, ‘Balanced’, ‘Adventurous’

– Lifestyle to 100% cash • Growing interest in US-style TDFs • Collective memory of capital loss – move to

low volatility / hedging and guaranteed investment options

DC formula

DC 2020

17

Master TrustTrust

Contract

Summary

Step-change in DC pensions

DC innovation requires more than just clever investment products

Some early innovation; more to come

No immediate need to appoint first movers

18

Regulatory Information

The information in this presentation is based on our understanding of current taxation law, proposed legislation and HM Revenue & Customs practice, which may be subject to future variation.

This presentation is not intended to provide and must not be construed as regulated investment advice. Returns are not guaranteed and the value of investments may go down as well as up.

Barnett Waddingham LLP is a limited liability partnership registered in England and Wales.

Registered Number OC307678.

Registered Office: Cheapside House, 138 Cheapside, London, EC2V 6BW

Barnett Waddingham LLP is authorised and regulated by the Financial Conduct Authority and is licensed by the Institute and Faculty of Actuaries for a range of investment business activities.

19

Related Documents