Uganda’s tax treaties: a legal and historical analysis Martin Hearson, London School of Economics Jalia Kangave, East African School of Taxation International Centre for Tax and Development annual meeting Arusha, December 2014

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Uganda’s tax treaties: a legal and historical analysisMartin Hearson, London School of EconomicsJalia Kangave, East African School of Taxation

International Centre for Tax and Development annual meetingArusha, December 2014

Presentation outline

1. Context: tax treaties in sub Saharan Africa

2. Uganda’s treaties past

3. Uganda’s treaties present

4. Uganda’s treaties future

Tax treaties signed by sub Saharan countries (and in force in 2013)

Source: IBFD

Countries having signed six or more treaties with sub-Saharan African countries

1952

2012

Year signed

Source: IBFD

“Double taxation treaties”: a misnomer?

“it is scarcely necessary to stress the importance of removing the obstacles that double taxation presents to the development of economic relations between countries”

- introduction to the OECD model tax treaty

“In the absence of an agreement there is no question of United Kingdom investors being doubly taxed and the main cash benefit for the investor is matching credit for pioneer reliefs... An acceptable double taxation agreement will normally ensure that United Kingdom investors are treated no worse than overseas competitors”

- UK govt unpublished review of double tax relief, 1976

So why sign?

Proponents say that treatieso mop up outstanding double taxationo standardise definitionso guarantee tax stabilityo result in lower (single) taxationo create a framework for cooperation/dispute resolutiono send a signal that a country is open for business

Opponents say that tax treatieso Transfer the burden of double tax relief from residence to

source countrieso Bind developing countries into disadvantageous legal

concepts and mechanisms

Tax treaties and foreign direct investment

The evidence that tax treaties attract new FDI into developing countries is inconclusive at best(problems include: poor data, endogeneity, robustness to treaty shopping, competition effects).

Most African negotiators interviewed agree. For example:

“Most of the time developing countries are disadvantaged by treaties. Treaties do not attract investment. It is other factors.”

“I know there’s empirical evidence that it [a treaty] has no effect on investment, but the reality country-to-country is that there’s a bluff goes on, and countries don’t want to take the risk of losing big investments.”

A long tradition of treaty scepticism

“The present system of tax agreements creates the anomaly of aid in reverse— from poor to rich countries.” – Charles Irish, 1974

“In treaties between developing and developed countries…re-allocating tax revenues means regressive redistribution-to the benefit of the developed countries at the expense of the developing ones.” – Tsilly Dagan, 2000

“When you sign an OECD model treaty, you say there is no withholding, or hardly any withholding, on outflows of cash to multinationals. Now why in hell do you want to sign that?” – Lee Sheppard, 2013

Contribution of this case study

Most of the academic literature on tax treaties and developing countries consists of:• Econometric papers often making herculean assumptions• Legal papers that do not always consider realities ‘on the

ground’

An historical and legal case study helps to ground the debate:• What were the actual objectives of treatymaking?• Were they achieved?• Are they still relevant?• How significant are the current costs and benefits?

Data source: interviews with govt officials and private sector tax advisers in Kampala September 2014, combined with analysis of official documents (negotiation minutes, budget speeches) from UK and Uganda.

The Uganda treaty review

All negotiations currently frozen while policy is developed.

Treaty with China remains unratified.

Motivations for review:

• “When I go to negotiate, all I have is my own judgement…We thought that cabinet should express itself.”

• Oil industry: taxation of technical services provided by consultant professionals

• Treaty with China is notably worse than any Ugandan treaty in force.

Presentation outline

1. Context: tax treaties in sub Saharan Africa

2. Uganda’s treaties past

3. Uganda’s treaties present

4. Uganda’s treaties future

Motivation 1: tax sparing

Unfruitful negotiations with (at least) the UK in 1970s and 1980s. Uganda insistent on high WHTs.

1991: Investment Code Act

1993: Finance Minister Mr J. Mayanja Nkangi: “negotiating double taxation agreements with identified major trading partners” because “in the absence of any complementary tax holidays with the home countries of foreign investors, the revenue foregone by reducing a company’s tax liability in Uganda represents a revenue gain by the Ministry of Finance in the home country.”

Treaties with UK (1992), South Africa (1997), Italy (2000) and Mauritius (2003) contain tax sparing provisions.

BUT by 2014, UK, South Africa & Italy exempt overseas equity FDI income, so tax sparing redundant.

Motivation 2:double tax relief

From 2001, successive finance ministers justified treaties to parliament on the grounds of double tax relief and investment promotion. Eg:

“to protect taxpayers against double taxation, and to ensure that the tax system does not discourage direct foreign investment” - Mr G Ssendula, 2001

Treaties signed with Norway (1999), Denmark (2000), the Netherlands (2004), India (2004) and Belgium (2007).

BUT all these countries relieve double taxation unilaterally. So where double taxation exists it is not on what Dagan calls an “heroic” level

Motivation 3:Tax treaty = tax incentive?

If most treaty partners exempt overseas FDI income from tax, many treaty concessions accrue directly to the investor as a lower effective tax rate.

Treaty is a tax incentive?

BUT few tax professionals in Uganda believe treaties influence their clients’ investment decisions, and the UIA doesn’t even mention them on promotional literature.

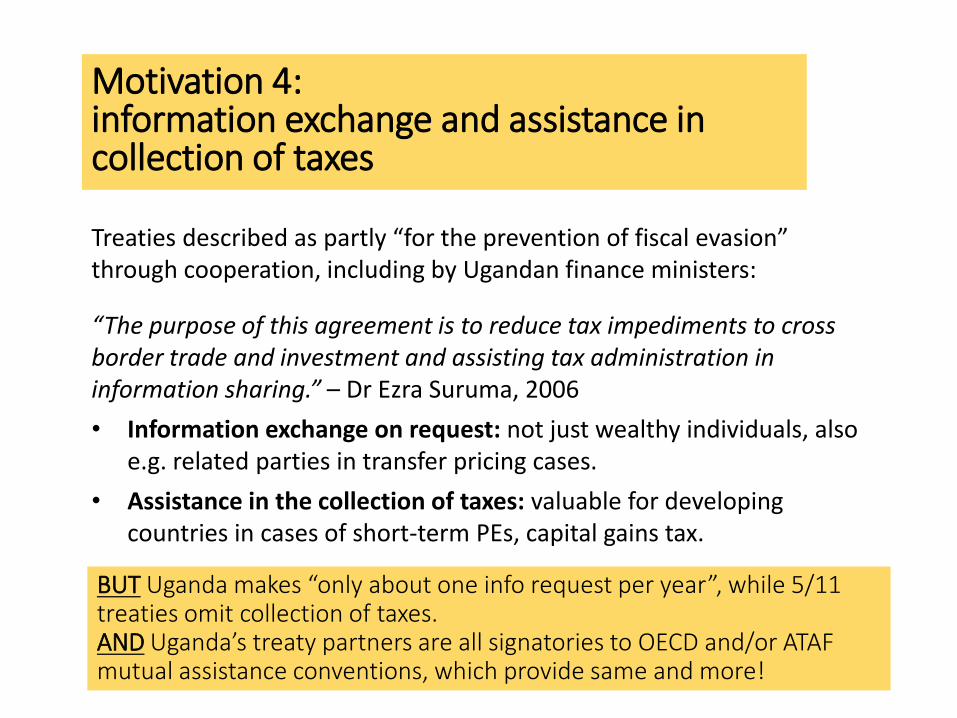

Motivation 4:information exchange and assistance in collection of taxes

Treaties described as partly “for the prevention of fiscal evasion” through cooperation, including by Ugandan finance ministers:

“The purpose of this agreement is to reduce tax impediments to cross border trade and investment and assisting tax administration in information sharing.” – Dr Ezra Suruma, 2006

• Information exchange on request: not just wealthy individuals, also e.g. related parties in transfer pricing cases.

• Assistance in the collection of taxes: valuable for developing countries in cases of short-term PEs, capital gains tax.

BUT Uganda makes “only about one info request per year”, while 5/11 treaties omit collection of taxes.AND Uganda’s treaty partners are all signatories to OECD and/or ATAF mutual assistance conventions, which provide same and more!

Presentation outline

1. Context: tax treaties in sub Saharan Africa

2. Uganda’s treaties past

3. Uganda’s treaties present

4. Uganda’s treaties future

Uganda’s treaties are less generous than the UN model

Officials say Ugandan position is UN+WHT on management fees. But…

UN ArticleDescription (domestic law in parenthesis)

In how many UG treaties? (10 total)

5(3)(a) Construction PE (90 days) All (@ 183 days)5(3)(a) Supervisory activities (yes) 85(3)(b) Service PE (90 days) 4 (@ 4 or 6 months)

10 WHT on FDI dividend (15%)Mostly @ 10% or 15%

Except NL (0), BE (5), CN (7.5)

11 WHT on interest (15%) Mostly @ 10%

12 WHT on royalties (15%) Mostly @ 10%

12a WHT on management fees (15%) 8 (mostly @ 10%)13(4) Capital gains – ‘property rich’ (yes) 2

21(3) Source taxation of other income 3

Uganda’s treaties are vulnerable to preventable treaty abuse

“The ones claiming [reduced taxation] under the DTAs are many, about one per day. The worst culprits are Mauritius, Netherlands. There is a lot of treaty shopping. A lot of companies trading in Uganda have their HQs in Mauritius.” –URA official

Examples of investments structured through treaty havens:• Total oil (from France via Netherlands)• Bahti Airtel (from India via Netherlands)• MTN (from South Africa via Mauitius)

Zain capital gains case revolves round an indirect transfer, no protection from this in UG-NL treaty.

Most treaty SAARs are rarely included in Ugandan treaties (eg dependent agent maintaining stock, limited force of attraction, indirect transfers)

Domestic treaty override provision s88(5) is untested in the courts.

Presentation outline

1. Context: tax treaties in sub Saharan Africa

2. Uganda’s treaties past

3. Uganda’s treaties present

4. Uganda’s treaties future

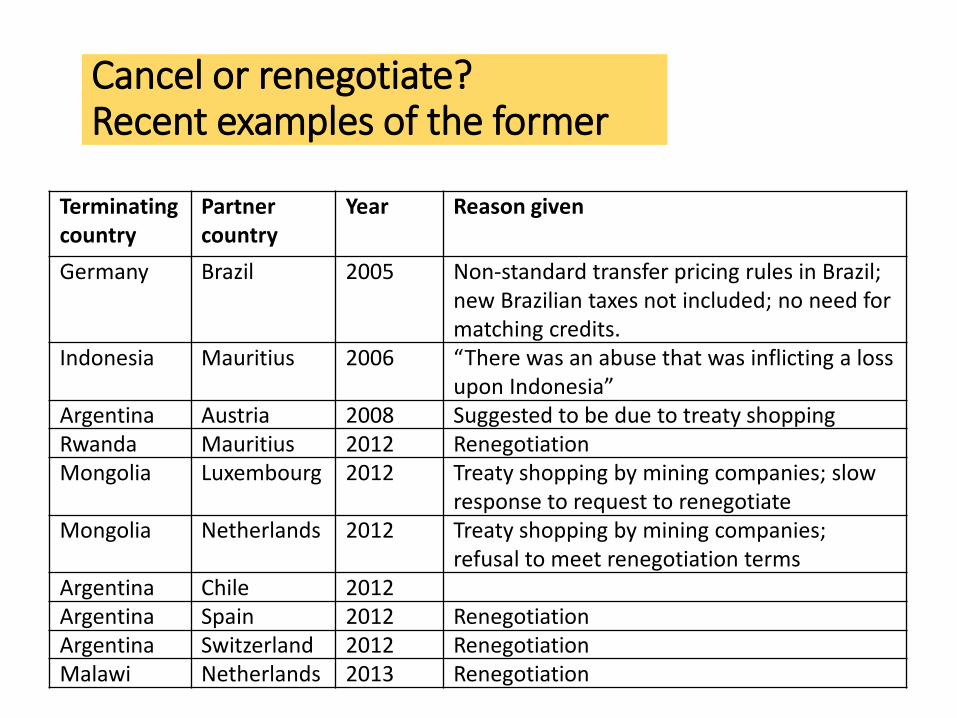

Cancel or renegotiate?Recent examples of the former

Terminating country

Partner country

Year Reason given

Germany Brazil 2005 Non-standard transfer pricing rules in Brazil; new Brazilian taxes not included; no need for matching credits.

Indonesia Mauritius 2006 “There was an abuse that was inflicting a loss upon Indonesia”

Argentina Austria 2008 Suggested to be due to treaty shoppingRwanda Mauritius 2012 RenegotiationMongolia Luxembourg 2012 Treaty shopping by mining companies; slow

response to request to renegotiateMongolia Netherlands 2012 Treaty shopping by mining companies;

refusal to meet renegotiation termsArgentina Chile 2012Argentina Spain 2012 RenegotiationArgentina Switzerland 2012 RenegotiationMalawi Netherlands 2013 Renegotiation

Cancel or renegotiate?

Cancellation has reputation costs, but is a viable option. A clear treaty policy can help identify priority treaties for reconsideration:

• Why does Uganda need treaties? No clear answer to this from officials at present.

• Cost-benefit analysis. No systematic assessment of even the easiest-to-measure WHT costs (which could be included within tax expenditure reporting)

• Treaty abuse risk assessment.

• Negotiating red lines.

Which model to use?

UN: Uganda has not attended annual session since 2004, nor submitted written comments, and does not coordinate with African committee members.

OECD: Uganda has not entered “observations” (from Africa, Ivory Coast, Gabon and DRC have done).

EAC: has some strengths (management fees WHT, LOB clause), but in other areas weaker source taxation than the UN model and some Ugandan treaties. Also, why MFN clause in WHT articles?

COMESA: has some strengths (main purpose test in WHT articles) but weaker than UN, EAC and some Ugandan treaties. Uganda has some reservations, esp for management fees WHT.

A ‘best available’ model as Uganda’s opening position

Could be:

1. PE: UN model definition, + 90 day construction and service PEs as per Ugandan law.

2. WHT: 15% across-the-board, including on technical service fees, as per Uganda’s treaty with the UK and its domestic legislation, + main purpose tests for passive income as per the COMESA model.

3. Capital gains: All provisions from the UN model.

4. Anti-abuse: Limitation of Benefits clause from the EAC model or the forthcoming new OECD provision.

5. Exchange of information and collection of taxes provisions from the UN and EAC models.

An holistic approach to international taxation

Not enough to consider treaties in isolation, when policy objectives may be undermined by:

• Tax incentives and production sharing agreements (eg Tullow case)

• Bilateral Investment Treaties (eg Uganda-Netherlands does not carve out taxation matters)

• Income Tax Act (eg definitions of PE, immovable property)

Thankyou

For more discussion of the issues covered in this presentation: http://martinhearson.wordpress.com

Related Documents