CHAPTER – 1 INTRODUCTION 1.1 BACKGROUND OF STUDY United Bank of Pakistan is one of the leading and first government recognized bank in Pakistan. Aimed to be the pre-eminent financial institution in Pakistan and achieve market recognition both in the quality and delivery of service as well as the range of product offering. The reason of its development was that the UBL in addition to being a commercial bank in the public sector at a time when all other commercial banks were in the private sector, also came to acquire certain characteristics which to this day set it part from other commercial banks of the country. The establishment of UBL thus signaled the achievement of another milestone in the development of the banking industry in Pakistan. 1.2 OBJECTIVE OF THE STUDY For getting the Master degree of Business Administration, each student is required to spend at least two months as an internee in a recognized organization. The students are required to work in Internship Report on UBL, Main Branch, Bannu 1

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

CHAPTER – 1

INTRODUCTION

1.1 BACKGROUND OF STUDY

United Bank of Pakistan is one of the leading and first government

recognized bank in Pakistan. Aimed to be the pre-eminent financial institution in

Pakistan and achieve market recognition both in the quality and delivery of service as

well as the range of product offering.

The reason of its development was that the UBL in addition to being a

commercial bank in the public sector at a time when all other commercial

banks were in the private sector, also came to acquire certain characteristics

which to this day set it part from other commercial banks of the country.

The establishment of UBL thus signaled the achievement of another

milestone in the development of the banking industry in Pakistan.

1.2 OBJECTIVE OF THE STUDY

For getting the Master degree of Business Administration, each student

is required to spend at least two months as an internee in a recognized

organization. The students are required to work in their own field in which they

have done their specialization.

Main purpose of this program is to make students familiar with the

practical work, as there is great difference between what they have learnt

during their M.B.A. and how the job is practically done.

Another important aspect of the internship program is that internee is placed in most

of the departments of the organization through job rotation. It provides a glance of

each department, as the period is too short for learning in detail.

Internship Report on UBL, Main Branch, Bannu 1

1.3 SCOPE OF THE STUDY

1. It is a compulsory requirement for the award of Master’s Degree of Business

Administration.

2. It will help the present and prospective students of the department in making

assignments and writing reports on the UBL, evolution of banking, importance

of banking and different operations.

3. It can also provide help to UBL’s management in identifying their Strengths,

Weaknesses, Opportunities and Threats.

4. It can also provide assistance to students seeking financial data for analysis.

1.4 IMPORTANCE OF STUDY

Banks play a central and very important role in the economic life of a

country, that’s why they are considered as the lifeblood of modern economy.

Today no one can deny the importance of banking in the economy. They

facilitate and expedite trade and commerce and provide a variety of services

that one can’t imagine with out banks.

I have chosen the United Bank Limited Pine View Road branch for my

internship because it has all the departments a bank could have.

Besides this, UBL plays an important role in the economic development

of Pakistan.

1.5 RESEARCH METHODOLOGY

The methodology that I adopted for this research project is based on

both the primary as well as secondary data.

The sources of primary data were:

1. Formally arranged interview/ discussions with Management, Director

and Joint Directors.

2. Personal observations.

The sources of secondary data were:

Internship Report on UBL, Main Branch, Bannu 2

1. Annual reports

2. Over view of the UBL

3. Relevant books.

4. The web sit of UBL

During the research project, I observed that enough written material

regarding the Bank is not available, so I had count on my personal observation

and interviews with manager. I spent eight weeks in the local branch and

collected information about different departments of the bank from discussion

and interview with manager, so most of the data of this report is primary .I also

availed assistance from few relevant books.

1.6 LIMITATION OF THE REPORT

There were however some limitations and that is the two months

durations of internship are nothing to gain entire knowledge of banking.

Moreover the bank does not want to provide data particularly about the

rightsizing of employees and stuck-up loans due to various reasons, so the

reader must also keep this in mind.

1.7 SCHEME OF THE REPORT

The report has been divided into ten chapters.

Chapter 1 is about the introduction of the report. In this chapter it is

discussed that how the internship is important and what a student can learn

from it. Light is also thrown on the way in which the research has been

conducted.

Chapter 2 of the report is about evolution of banking. This chapter

contains detailed information that what role the banks play in the economic

development of a country. In this chapter the bank is defined. Growth of the

banking globally as well as in Pakistan is pointed here. As well as it is about

the historical background of UBL. The circumstances in which UBL was

established and its growth is discussed here.

Internship Report on UBL, Main Branch, Bannu 3

Chapter 3: This chapter also gives the information about various

services offered by the UBL.

Chapter 4 of the report is about the organizational structure of UBL.

Hierarchy of staff and various positions of seniority are shown and discussed

through a Chart.

Chapter 5 covers various departments of UBL. Each department is

separately given due consideration. Various functions performed by different

departments are highlighted.

Chapter 6 this chapter is about different banking efforts like commercial,

consumer and corporate banking, throws light on various financial products

UBL offers to its customers.

Chapter 7 of the report consists of SWOT analysis.

Chapter 8 is about Financial statement analysis; analyzed horizontally

and vertically. Also the performance of the bank has been shown through ratio

analysis and trend analysis.

Chapter 9 is consists of Findings and Recommendation of UBL.

Internship Report on UBL, Main Branch, Bannu 4

CHAPTER – 2

EVOLUTION OF BANKING

2.1 INTRODUCTION

The word bank is derived from Latin word “Bancs” or “Banque”, which

means a bench. The explanation of this origin is attributed to the fact that the

Jews in Lombardy transected the business of money exchange on benches in

the market place. When the business failed, the people destroy the bench.

Incidentally the word bankrupt is said to have been evolved from this practice.

The opponents of this opinion argue that if it was so, then how is it that

the Italian money changers were never called Banchierei in the middle ages

Other authorities hold the opinion that Bank is derived from German

word back which mean joint stock fund. Later on, when the German occupied

major part of Italy, the Back was italicized into Bank.

2.2 DEVELOPMENT OF MODERN BANKING

Despite the classical origin, banking in its modern form and structure

started in Britain when many of the Lambordary merchants came to England in

the fourteen century and settled in the part of the London now called Lombard

street.

They were so resourceful that even the kings had to depend on them for

loans despite the fact that the church was firmly against usury. They dealt with

not only keeping the money in safe custody but also changed money for the

travelers or merchants engaged in foreign trade.

The business of changing money was so lucrative that King Edward III

established the office of Royal Exchanger for changing foreign money at a

profit for the benefit of the crown.

The discovery of America brought riches to England and gave a

tremendous boost to foreign trade. The merchants now began to hold part of

Internship Report on UBL, Main Branch, Bannu 5

their riches in cash. These transactions, however, received a big setback in

1640, when King Charles I seized 130,000 Pounds and bullion left for safe

custody with the city merchants at the Royal Mint.

This shook the confidence of the merchants in the Royal Exchanger and

Royal Mint. Consequently this business was taken over by the gold smiths,

who, up to that time, were dealing only in gold and silver. Since these gold

smiths required strong safes for the purpose of their own business, they

introduce necessary facilities of safe keeping of the valuables and the cash of

their customers. These goldsmiths issued receipts or note to their depositors in

respect of the cash or articles left with them. These were called gold smith

notes, and carried an undertaking to return the money and articles to depositors

or bearers on demand. There were a considerable number of such notes on

circulation among various classes of merchants and thus they can be aptly

called Bank Notes in their earliest form.

Over a period of time, these goldsmiths discovered that large sums of

money were left in their custody for long periods. Therefore, they started the

use of this cash to advance loans to other persons for a fixed period of time and

at considerably at a higher rate of interest. Moreover they further encourage

cash deposits by their customers by offering them a part of their profit earned

on the money. Thus began the issue and deposit banking of modern times.

Some of the enterprise goldsmiths issued checkbooks for the attraction of their

customers; and thus another important step in the evolution of banking was

taken.

In 1672, however, English banking faced a great crisis when Charles II

borrowed huge sum of money from the goldsmith bankers formed themselves

into a Corporation in 1695, known as the Bank of England. This bank lent

1,200,000 pounds at 8% interest to William III, who in return, allowed a

number of privileges to the bank, specially the right to issue Notes payable to

bearer on demand unto the amount of this loan. This was known as fiduciary

Internship Report on UBL, Main Branch, Bannu 6

issue, not covered by gold. This new bank became a very serious competitor to

the comparatively smaller private banks run by the London goldsmiths.

By the year 1700, the Bank of England was not only issuing Notes but

also conducting accounts for customers. Being a joint stock bank by charter, its

directors were conducting the business like that of limited companies. The

Bank of England was the only joint stock company which was given the

monopoly of issuing the Bank Notes.

In 1708 the privilege to issue Notes in England was withdrawn from

joint stock banks and confined to the private banks with not more then 6

partners.

Up to 1813 or there about in England, the main profit of banks was

derived from the circulation of notes and for many years after that, deposits

were treated as very minor matters

2.3 GROWTHS AND HISTORY OF UBL

Commercial banks play a role of vital importance in the economic

growth of a country. Banks mobilize idle savings of public and provide finance

to various sectors of economy. In spite of vital importance, there was shortage

of branches of commercial banks in the areas of sub-continents, which now

constitute Pakistan. When Pakistan got independence, there were only 487

branches of commercial banks, which were further reduced to 195 as at

30/09/47 due to shifting of a number of branches to India or U.K. The Reserve

Bank of India, which was made responsible to exercise control over banking

sector in both the dominions, did not perform its duties properly in Pakistan.

The State Bank of Pakistan was established on 01/07/1948. After the

establishment of State Bank of Pakistan, banking expansion got momentum but

real progress was not achieved until 1959, when a dynamic banker Mr. Agha

Hassan Abedi conceived the idea of opening a bank different from others. His

dream was translated into reality on November 07/1959 when first branch of

Internship Report on UBL, Main Branch, Bannu 7

UBL was opened at McLeod Road Karachi (now known as I.I. Chundrigar

Road).

This achievement was secured after passing through many problems and

after completion of a lot of legal formalities. UBL was established on 24-07-59

as a public limited company with registered office at I.I. Chandrigar road

Karachi. The authorized capital was RS. 20,000,000 issued, subscribed and

paid up capital was. RS. 10,000,000 divided into 1,000,000 shares of RS.

10each.

I. LOCATION

WITH an integrated network of over 1000 branches in Pakistan as well

as 15 Overseas branches, UBL gives you direct access to a comprehensive

range of better banking facilities to help you monitor your business locally as

well as internationally.

II. TREASURY

The UBL Treasury & Capital Markets (TCM) has developed a

reputation as a proven market leader in converting innovative ideas into

profitable ventures for the bank and for its customers. Today the UBL TCM is

a frontrunner in providing:

The narrowest bid/ask spreads and the fastest quotes

Dynamic risk-reducing hedging strategies for its customers

The best relationships with institutional, corporate and retail clients Year

2003 was a highly lucrative year for the bank with net profits in excess of PKR

4 billion. Treasury and Capital Markets contributed to over 65% of UBL’s total

returns. This was due to Government Bond Trading, Equity Trading, Structured

Products/Financial Engineering, Corporate Debt trading, and double-Count of

revenues.

Under the new management, the TCM expedited the launch of

Pakistan’s first derivative money market product-the FRA (forward rate

Internship Report on UBL, Main Branch, Bannu 8

agreement) with Quetta Textile Mills Ltd. in August 2003, and has further

closed several similar transactions thereafter.

UBL TCM is a market maker in both the domestic money market as

well as the foreign exchange market. Being one of 11 primary dealers (PD),

UBL has one of the largest balance sheets amongst banks in Pakistan, and

hence our Foreign Exchange Exposure Limit (FEEL), as imposed by the State

Bank of Pakistan, is the highest in the industry.

UBL was the first local bank to establish a Corporate Treasury team in

the Treasury dealing room. The Global Corporate Treasury Business is globally

responsible for sales of all structured and derivative products for UBL. The

bank’s trade volumes and revenues have grown significantly since the

introduction of the corporate treasury business.

Equities are responsible for managing the bank’s trading and badla

portfolio, and to eventually develop a global equity trading activity for UBL.

Structured Products is responsible for developing and packaging plain vanilla

derivatives as well as more exotic customer specific products, and pipeline

products.

The Strategic Planning and Balance Sheet Management responsibilities

include:

Liquidity Management for the domestic balance sheet - This unit is the

focal point for all branch-related liquidity issues and will also be responsible

for day-to-day management of liquidity for UBL.

Overseas Branches Treasury and Capital Markets - we plan to integrate

the treasury activities for all overseas branches, to develop synergies

amongst our various treasuries. As our core business in these markets

continues to develop, we expect significant opportunities to arise in the

trading, funding and gapping areas.

Research - providing market research for internal and external clients in

order to support the sales and trading effort.

Internship Report on UBL, Main Branch, Bannu 9

2.4 THE FIRST BOARD OF GOVERNORS OF UBL CONSISTED OF THE FOLLOWING MEMBERS

TABLE – 1

1 Mr. Ismail Ibrahim Chandrighar Chairman

2 Mr. Muhammad Shafiq Saigol Managing Director

3 Mr. Muhammad Rafiq Saigol Director

4 Mr. M.Bashir saigol Director

5 Mr. A. Razaq Dada Director

6 Mr. Mian M.Yahya Director

7 Mr. M. Saeed Saigol Director

8 Mr. Agha Hassan Abidi Director and General ManagerSource: Hassan Raza, Internship Report on UBL, 2002.

Presently UBL is managed by a board of directors including one

president, 4 directors from UBL, 1 from Pakistan Banking Council and one

from ministry of finance.

The names and designations of present top management include;

TABLE – 2

1 Mr. Shaikh Nahayan Mubarak Al Nahayan Chairman

2 Mr. Afzal H.Mufti Director

3 Mr. Iltaf M. Saleem Director

4 Mr. Iftikhar Allahwala Director

5 Mr. Munnawar Hameed Director

6 Mr. Syed Shamsul Haq Director

7 Mr. Afaq Tiwana Director

8 Mr. Abdul Ghafoor Corporate Secretary

Source: www.ubl.com.pk

Since inception, UBL provides personalized, efficient and courteous

services to its customers and has achieved dynamic progress in a short span of

time. UBL has achieved the distinction of earning profit in very first year of its

operation. UBL also introduced many remunerative schemes for its depositors

and introduced computer services for the first time in the banking history of

Internship Report on UBL, Main Branch, Bannu 10

Pakistan. UBL gives advance finances to small, medium and large industries,

commercial establishments, agriculturists, construction companies and other

needy persons. UBL offers computerized services to intending Hajis free of

cost. UBL collects Electricity, Gas and Telephone bills from public and issues

TV licenses on behalf of Pakistan Television Corporation. It also offers

evening banking and lockers facilities at its selected branches. Over 100

branches deal in foreign exchange where facilities to importers, exporters,

travelers and other persons are being given.

UBL arranges prompt payment of inward remittances. Similarly for

issues of outward remittances minimum time is taken. Other auxiliary services

such as unicorn, inland travelers checks, school banking and collection of

checks and other documentary bills drawn on its station drawees are offered.

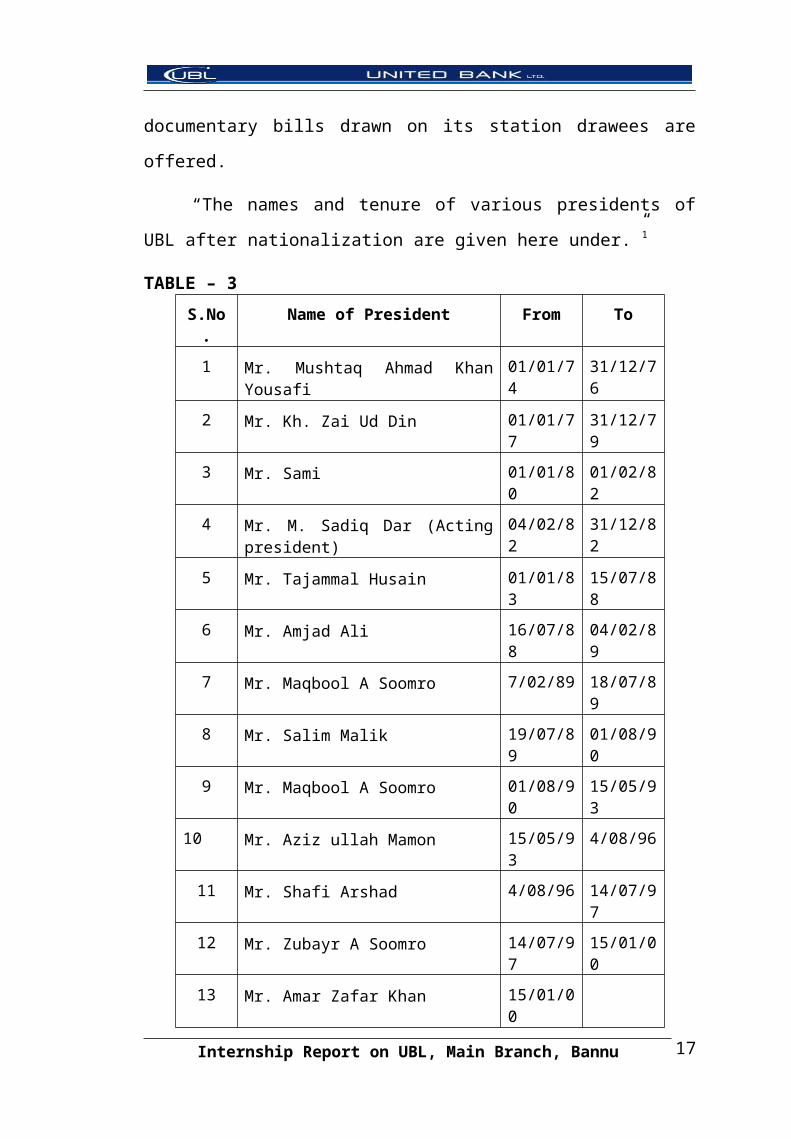

“The names and tenure of various presidents of UBL after

nationalization are given here under.”1

TABLE – 3

S.No. Name of President From To

1 Mr. Mushtaq Ahmad Khan Yousafi 01/01/74 31/12/76

2 Mr. Kh. Zai Ud Din 01/01/77 31/12/79

3 Mr. Sami 01/01/80 01/02/82

4 Mr. M. Sadiq Dar (Acting president) 04/02/82 31/12/82

5 Mr. Tajammal Husain 01/01/83 15/07/88

6 Mr. Amjad Ali 16/07/88 04/02/89

7 Mr. Maqbool A Soomro 7/02/89 18/07/89

8 Mr. Salim Malik 19/07/89 01/08/90

9 Mr. Maqbool A Soomro 01/08/90 15/05/93

10 Mr. Aziz ullah Mamon 15/05/93 4/08/96

11 Mr. Shafi Arshad 4/08/96 14/07/97

12 Mr. Zubayr A Soomro 14/07/97 15/01/00

13 Mr. Amar Zafar Khan 15/01/00

Internship Report on UBL, Main Branch, Bannu 11

2.4 NUMBER OF BRANCHES

UBL has a large network of branches, which extends to the remotest

areas of the country. In December 1983, there were 1417 branches whereas in

1974 it had only 1238 branches and in December 1999 there were 1623

branches and in December 2003 there were 1821 branches. Presently there are

1056 domestic branches and 15 overseas branches.

I. OVERSEAS BRANCHES

UBL, with an integrated network of over 1000 branches globally, with

15 overseas locations, gives their customers direct access to a

comprehensive range of better banking facilities to help them monitor

their business internationally.

They have branches in:

United States of America

Qatar

UAE

United Kingdom

Bahrain

Republic of Yemen

Zurich

Off Shore banking Unit

II. SUBSIDIARIES

UBL has two subsidiaries, namely,

United Bank of Lebanon & Pakistan

United bank A. G. Zurich.

United bank of Lebanon and Pakistan was established in 1968, 1st had a

paid up capital of dollars 379,000, deposits of dollars 125,978, advances

of dollars 1983,313 and six branches as on December 31, 1983.

Internship Report on UBL, Main Branch, Bannu 12

United Bank A.G. Zurich also was established in 1968 and had a paid –

up capital of dollars 2722 thousand, deposits of dollars 5827 thousand

and advances of dollars 5538 thousand as on December 31, 1962.

2.5 JOINT VENTURE

UBL has two ventures, Commercial Bank of Oman limited, established

in 1975. It had a paid up capital of dollars 8,700 million, deposits of dollars

7,333 million, advances of dollars 73.993 million and 11 branches as on

December 31, 1962. And United Saudi Commercial Bank Limited (Saudi

Arabia), established in 1982.

2.6 ROLE OF UBL IN N.W.F.P.

The role of UBL has developed largely; through out the country in very

short period of forty seven years. The bank is operating in the entire country

and has branches all over the country and overseas. In N.W.F.P, UBL is

operating successfully. The number of branches of UBL in Peshawar region is

156 up to dec.2001 i.e. there are total 14 Hub Branches in Peshawar region and

under these Hub branches, there are 142 spokes branches. These 156 branches

come under the Peshawar Region , for which there is a Regional head Quarter

(RHQ) in Peshawar.

The list of hub branches come under the Peshawar Region is as under.

1. Peshawar 6. Haripur 11. Mardan2. Bannu 7. D.I. Khan 12. Swabi3. Mansehra 8. Mingora 13. Kohat4. Timergara 9. Nowshera 14. Abbotabad5. Hangu 10. Bathela

2.7 MISSION STATEMENT OF UBL

“We shall dominate Pakistan’s financial markets and be the leading

bank of Pakistan in term of quality of customer services, assets, profits and

reserves. we shall consistently try to be among banks in the Pakistan.

Comparing over selves to international standards. We shall be a modern

universal bank. Our employees will be efficient, motivated and have corporate

pride”

Internship Report on UBL, Main Branch, Bannu 13

2.8 OBJECTIVES OF UBL

Objectives mean the end towards which an activity is aimed. An

organization without objective is like a person who is wandering with no

purpose. All the activities of an organization are due to its objectives and goals.

And for the attainment of those objectives, various types of financial products

and plans are developed. UBL has also some objectives, which are as under.

To ensure growth and development of the bank.

To use resources of the bank efficiently.

To get more deposits.

To participate in development of the country.

Paying special attention to the areas, which are under developed.

To develop SME’S.

To increase industrialization in the country.

To provide financial help to the farmers.

To provide employment opportunities.

To make people more of mind to have saving habits.

Internship Report on UBL, Main Branch, Bannu 14

REFERENCES

www.ubl.com

Hassan Raza, Internship Report on UBL, 2002.

UBL Annual Report, 2005.

Internship Report on UBL, Main Branch, Bannu 15

CHAPTER – 3

SERVICES OFFERED BY UNITED BANK LIMITED

3.1 CONSUMER BANKING

United Bank limited aspires to be the leading provider of consumer

baking services in the country besides the fact that UBL was the Last entrant in

the consumer products of the new age but Not The Least. The bank’s operating

strategy in this regard has been aligned with the core customer needs of highest

value and expert services. The bankers in general are facing challenging time

today as bankers; as they should be more than just custodians of client’s funds.

Rather they should devise safe and prudent methods of maximizing the returns

on hard earned savings and investments of their customers. These corporate

values are evident in United Bank’s diversified product portfolio which

includes Current a/c, Pls saving, Business Partner a/c, Term Finance

Certificate, UBL Profit certificate of deposit, Monthly income, Foreign

currency a/c, Rupee travelers’ check, Money gram, Safe deposits, Car finance,

Credit card, Personal loans, Housing finance, Business Loans and Running

Finance.

In the arena of consumer banking the bank has carved a niche in the

market place, with products like car finance, rupee travelers’ checks homes and

car loans for U.A.E based non-resident Pakistanis. It has set up strong internal

control mechanisms to monitor and measure risks arising out of consumer

banking products. The bank is developing electronic, automated and

computerized environment to give impetus to their efforts in consumer banking

area.

3.2 CORPORATE BANKING

Systems and operations have to be aligned so that they support the

performance of the Organization’s product offering. Consequently, business

process re-engineering and quality control are on the main maxims of corporate

Internship Report on UBL, Main Branch, Bannu 16

philosophy. United Bank Limited has the Corporate Banking Group (CBG)

which enhanced the image of UBL in the corporate world and also increased

the advances, revenues and profit of the bank to the new heights.

United Bank’s product line-up fulfills and satisfies the banking

requirements of not just the conventional consumer, but the demanding

financial needs of the corporate sector as well. Corporate product includes

current deposits, foreign deposits, over draft, term loans, project financing etc.

The bank is continuously setting new standards of services in the industry and

is becoming reliable financial ally of all the customers.

3.3 INVESTMENT BANKING

Investment Banking Group of UBL (IBG) continues its leadership

position in providing innovative and unique financial solution to its clients by

anticipating their changing requirements and developing new products &

services.

IBG concludes more transactions, both number and volume than any

other local and foreign financial institution, including banks, investment banks,

and brokerage houses.

More specifically, while IBG maintained its leading status in the

traditional business of loan syndication and debt capital markets, major strides

were achieved in the newer value-added business areas of projects and

structured finance, equity & advisory services and private equity solutions.

Nowadays IBG is focusing on the fast emerging Technology, Media and

Telecom sector where it concluded several unique high-profile transactions.

Most significantly UBL is the only major financial institution based in Pakistan

to be engaged by a reputable local group to act as financial advisor for the

cellular license auction bidding in April 2004.

3.4 AUTOMATED BANKING

Technology and automation play a pivotal role in the progressive

development of any organization. It has become impossible to control the

Internship Report on UBL, Main Branch, Bannu 17

operations of a bank effectively in real time situation without the latest

technology. The bank continues to invest heavily into the progressive

automation and computerization of all banking activities. Its aim is to achieve

total connectivity between branches. The objectives are to achieve efficiency in

services and to control costs. UBL has recently installed the New-state-of-the-

art ATM machines in UAE.

United Bank Ltd provides:

ATM/ UBL Wallet Debit Card

Online Banking/ Uni Remote

Telephone banking

UBL Business Partner ( In 500 branches and 250 cities)

3.5 ISLAMIC BANKING

UBL has played an important role in Islamic banking and successful

operation of Non- interest based system of banking.

The interest free banking system was introduced on January I, 1981.

Since then, UBL has played an important role in the successful operation of

this system. For this purpose, it has established a special division, “The Islamic

Banking Cell”.

The sincere efforts of UBL as making Islamic Banking successful is

proved by the fact that it declared the highest rates of profit for PLS deposits

for the first half year of 1983. This has been due to a sound planning of all its

Islamic Banking efforts.

The bank has provided capital to businessmen and industrialists on the

basis of “Mudaraba and Musharika”. Additionally the bank has started interest-

free hire purchase and lease schemes for financing purchase of buses, trucks

and industrial machinery on installments. The bank also provides “Qarz-e-

Hasna” to needy and deserving students.

Internship Report on UBL, Main Branch, Bannu 18

3.6 AGRICULTURE

UBL has contributed in full measures to the development of agriculture.

It has always exceeded, by a considerable margin, the targets given by the State

Bank of Pakistan. UBL has also provided loans for a variety of agricultural

activities including tractors, tube-wells, fertilizers, insecticides, poultry

farming, bio-gas plants etc. The bank officers who are qualified agricultural

graduates not only provide loans at the doorsteps of the farmers, but also render

technical assistance to them. To maintain constant liaison with the farmers, the

bank officers have been provided with motorcycles.

Financing of Small Business to meet the goals of social justice, the bank

has zealously participated in the small loans scheme. It has always tried to

exceed the targets fixed by the state Bank. A full- fledged department catering

to the needs of small businessmen is functioning. To improve its operations, the

bank has made arrangements for overseas training of its staff.

The bank is also participating in the dollars 30 million IDA credit,

which will be provided to small industrialists.

For training its staff, a staff collage was established at Karachi in 1994.

Now there are three such colleges at Karachi, Lahore and Rawalpindi, where

the officers and staff are provided extensive training. Furthermore for training

senior officers, a UBL school of Banking has been set up at Karachi. Senior

bankers and management experts provide training to the executives and senior

officers of the bank.

3.7 RESEARCH DEPARTMENT

UBL was the first commercial bank in the private sector to establish a

full- fledged Research Department. Prominent economists of the country have

been acclaimed both at home and abroad. Not only does this research provides

useful and cogent studies of economic development in Pakistan and abroad, it

also assists in the managerial decision making process.

Internship Report on UBL, Main Branch, Bannu 19

The Research Department is publishing “Economic Matters” every

month since 1967. It was recently upgraded to “UBL Economic Journal”. In

addition, the department also brings out the “UBL Home Journal”.

3.8 COMPUTER SERVICES

UBL was the first bank to introduce computers. The Computer Division

was established in 1968. Presently, UBL has Computer Department at Karachi,

Lahore and Rawalpindi. Many branches have been fully equipped with

computers. The Computer Division prepares weekly, monthly, quarterly, bi-

annual and annual reports for top services to many Government, Semi

Government and private institutions.

3.9 SERVICE TO HAJJIS

For providing prompt and efficient services to the intending Hajis who

come to UBL every year, the bank has introduced the most modern system of

electronic banking which permits all formalities to be completed within a short

time. This year 2005, UBL received the greatest number of applications from

customers for Hajj, which shows the customers faith in UBL.

3.10 AUXILIARY BANKING SERVICE

Bank provides a number of auxiliary services such as credit cards,

travelers checks and school banking.

3.11 COLLECTION OF UTILITY BILLS

UBL also collects electricity, gas, and telephone bills from the public on

behalf of the respective organizations. The bank also introduced the bills

collection facilities in selected branches in the evening hours for the

convenience of general public. And now selected UBL branches are collecting

the utility bills through online banking.

3.12 ISSUANCE OF TV LICENSE

UBL also collects TV License fee on behalf of Pakistan Television

Corporation and issues TV Licenses to the general public.

Internship Report on UBL, Main Branch, Bannu 20

Sports

UBL was one of the first banks to patronize sports. Senior executives at

the highest level supervise the sports activities.

The bank has established a special department to organize its various

sports activities. It has provided patronage to leading sportsmen. Many

outstanding players and national players have been included in its teams.

The bank has won United States of America trophies in hockey, cricket,

badminton, table tennis, rifle shooting, etc.

Development of Data Base Management System (DBMS)

United bank is the only bank in Pakistan, which is making use of its own

data base management system (DBMS) since 1971. The VIS was used

in the three main branches of Karachi. After years of deducted efforts on

its work, it succeeded in loping UNI Bank Plus.

Internship Report on UBL, Main Branch, Bannu 21

CHAPTER – 4

ORGANIZATIONAL STRUCTURE

Organizational structure of a firm provides boundaries for authority of

persons and clarifies individual responsibility and authority. It shows who is

responsible to whom, and who has the authority to give orders to someone. An

organization having dual authority or vague structure would not have clear

direction and will face hurdles in getting its goals and objectives. Therefore, it

is very important for any organization to have a well-established structure of

responsibility and authority. An organization structure should be so designated

to clarify the environment so that everyone knows his duty and who is

responsible for what. It results to remove obstacle to performance caused by

confusion and uncertainty of tasks and to furnish a decision making

communication network reflecting and supporting enterprise objectives.

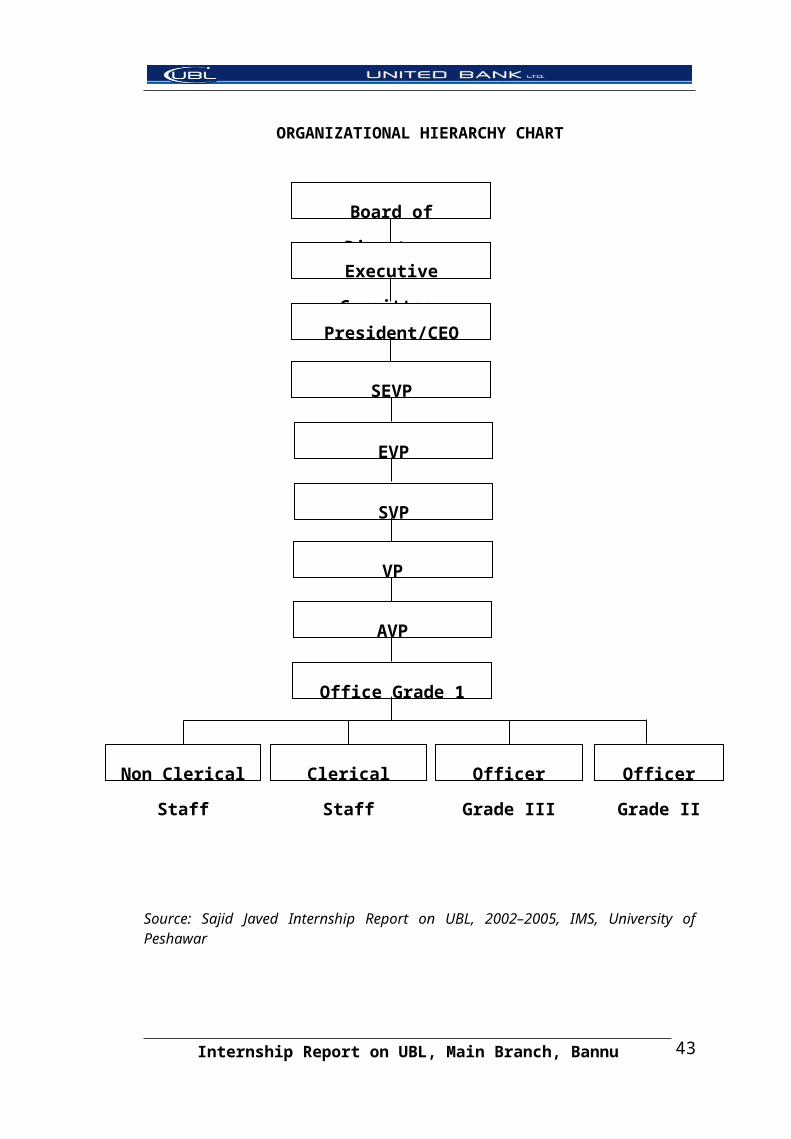

4.1 UBL ORGANIZATIONAL STRUCTURE:

UBL also has a well defined formal organizational structure. UBL is a

very vast organization. In the organization set up of UBL, the highest authority

rests with Board of Directors which consists of Chairman, Deputy Chairman,

President & CEO and the directors. In which four directors are from UBL, one

from Pakistan Banking Council, one from Ministry of Finance and one who is

also the secretary of the board. So the Board of Directors is an eight member

team, and is responsible for policy formulation and making important strategic

decisions.

THE NAMES OF THE BOARD OF DIRECTORS ARE AS FOLLOWS:

Chairman

H.H Sheikh Nahayan Mabarak Al Nahayan

Deputy Chairman

Sir Muhammad Anwar Pervez, OBE, HPK

Internship Report on UBL, Main Branch, Bannu 22

President & CEO

Atif R. Bokhari

Director

Zameer M. Choudrey

Director

Omar Z. Al Askari

Director

Muhammad Tehsin Khan Iqbal

Director

Ahmad Waqar

Director

Javed Sadiq Malik

The authority, which is second highest, lies with executive committee. It

consists of seven members, including the president and secretaries are in charge

of divisions. The members are Senior Executive Vice President (SEVP) of

UBL. There are twenty divisions, which have their own Senior Executive Vice

President (SEVT). Executive Vice President (EVP), or Senior Vice President

(SVP), the

SEVP to international divisions manages the operations of foreign

countries branches. The rest of the divisions work along their functional lines

as shown in the organizational chart.

At the National level, UBL has a network of branches spread allover the

country and its field operations are one of the most extensive among the

leading banks in Pakistan. At provincial level the bank is managed by SEVP,

who is assisted by General Manager (OM), who is EVP or SEVP. The OM is

responsible for either a number of regional areas or in charge of various

provincial departments such as Administration, General Recovery, Loans,

Inspection, etc. The complexity and extensiveness of the operations in a given

Internship Report on UBL, Main Branch, Bannu 23

province determine the number of OMs. OMs are assisted by circles executives

who are of the rank of SEVP or VP.

The entire country is divided into Circles which are further divided into

Zones.

The circles are administered by circle executive. Each zone is comprised

of a number of branches, which are managed by branch managers who are

mostly Grade I or Grade II officers. Some large sized branches are also

managed by AVPs.

4.2 CONCEPT OF HUB AND SPOKES BRANCHES:

The concept of HUB and Spoke branches was introduced by ANZ Grind

lays Bank (now renamed Standard Chattered Bank). The bank couldn’t get the

desired benefits and withdrew form it. Another bank which adopted the concept

was National Bank of Pakistan (NBP), which also couldn’t get the desired

results so both the banks disbanded it. Recently UBL has implemented this

scheme with high hopes. Under the concept big branches of a zone are given

the status of Hub branches. The Hub branches monitor the activities of spokes

branches. The number of branches under a Hub branch depends upon the

resources of Hub branch and the location of the spokes branches e.g. in

Peshawar there are two hub branches one is Peshawar Cantt branch and the

other one is Khyber Bazaar branch. All the spoke and Hub branches work

under the concerned area manager. He is responsible for the performance of

these branches. He sits in the Hub branch and is assisted by a Vice President. In

UBL this new concept of banking has shown tremendous results and is quite

successful here. Unlike ANZ and NBP, UBL is getting benefits from it, and has

improved its performance quite well.

Internship Report on UBL, Main Branch, Bannu 24

4.3 DIVISION OF UBL’S OFFICE

Basically there are two types of offices in UBL

1. Head Office

2. Regional Head quarters

1. Head Office

Head office of UBL is in Karachi. It exercises overall control over the

bank. The head office (HQ) has various functions.

It formulates polices and ensures its implementation.

To supervise and control the operations of the regional offices.

To formulate policies and ensure its implementation by the field offices.

To deal/liaison with foreign donors like IBRD (World Bank), Asian

Development Bank, Islamic Development Bank, KFW (German Bank),

FMO Netherlands etc.

To deal with Ministry of Finance.

To supervise RHQs.

To sanction loan applications received from the branches.

To deal with ministry of finance.

2. Regional Head Quarters

There are Eleven Regional Offices of UBL which fully cooperate with

the Head Office. UBL Regional Offices performance with reference to

sanctions, disbursement, recoveries, and deposit mobilization is of vital

importance to the bank operations. The functions are as follows:

To implement the policies formulated by the Head Office.

To extend the credit facilities by keeping in view all the prescribed

conditions.

Internship Report on UBL, Main Branch, Bannu 25

To recover/collect the existing long-term credits extended by the bank as

per schedule.

To assist customers in the process of development by advancing loans

for viable financial projects.

All the 1056 UBL branches are the representatives of the bank. These

branches provide commercial as well as non-commercial banking facilities.

Various structures involved in the organization of UBL are given below.

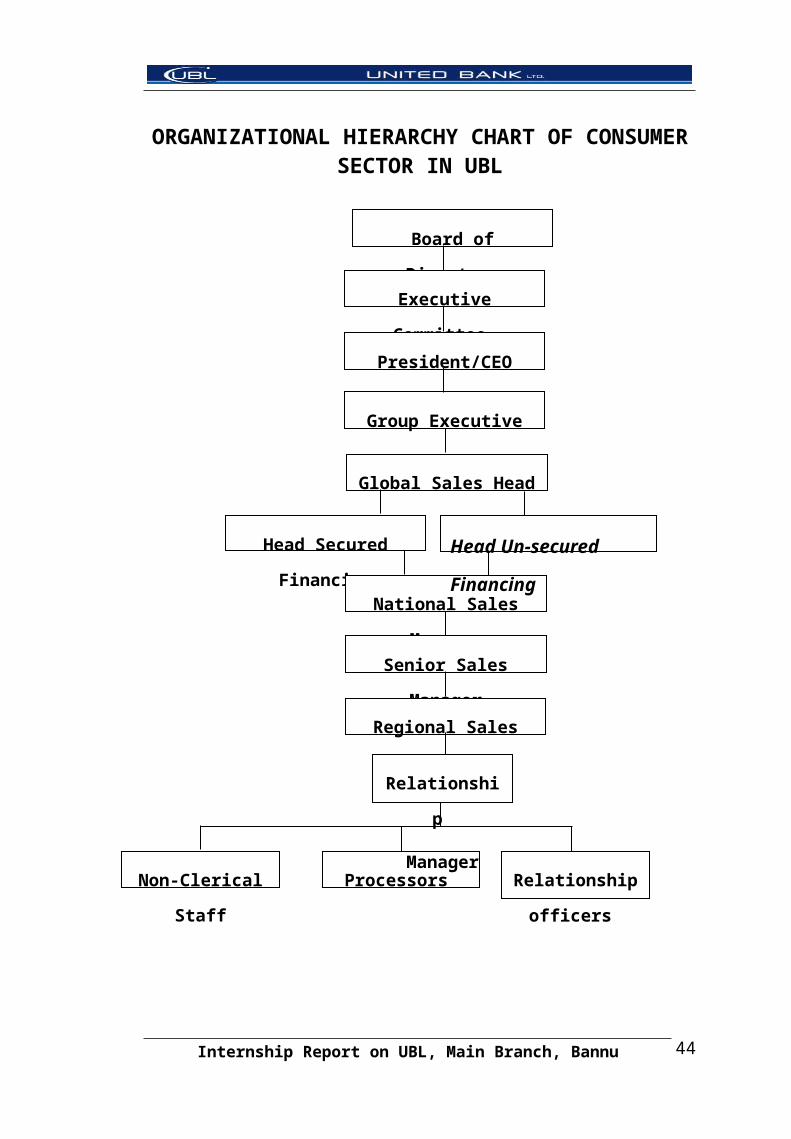

4.4 CONCEPT OF CONSUMER ASSETS CENTERS:

As the UBL was privatized the management started thinking about the

consumer products as well the commercial products. For this purpose the

management started hiring from all over the world in order to collect the cream,

and make a world class team without any doubt.

The management took the consumer head from the bank which is

consider as the pioneer in the consumer sector “Citi Bank”, and then he joined

hands management and made all the possible ways to make UBL a World

Class Bank on the Consumer Side as well in the Commercial Sector. They

made collectively the plans to make Consumer Assets Centers in all over the

country which was introduced first time in Pakistan.

The UBL’s Consumer Assets Centers are the state-of-the-art in the main

cities like Karachi, Lahore, Islamabad and Peshawar. The Consumer Assets

Centers are divided in main Head Office, Regional Centers and New Cities. At

the time of launch the regions were 10 in the country but now it has been

increased to 14.

In Consumer Assets centers the products are divided in to two types:

The Secured, and Un-secured Products. The Secured include UBL Autos, UBL

Address, and Credit Card while the UBL Money and UBL Cashline comes

under the canopy of Un-secured Products.

Internship Report on UBL, Main Branch, Bannu 26

There is a Group Executive, a Global Sales Head, Head Secured

Financing, Head Un-secured Financing, National Sales Managers, Regional

Sales Managers, Relationship Managers and the Relationship Officers.

4.5 TOP MANAGEMENT AT THE HEAD OFFICE:

I. Board of Directors

The executive authority for the general direction and supervision of the

Bank operations or the conduct of business of UBL vests in Board of

Directors. The board consists of a Chairman and seven other Directors.

The chairman of the Board of Directors is the “Managing Director”. All

the members of the Board of Directors, as well as the Managing

Directors are appointed by the government of Pakistan.

II. Executive Committee

Executive committee of UBL consists of seven members. With the

expectation of the president, and secretary all other members serves as

Incharge of many divisions. These members are Senior Executive Vice

President (SEVP), or consultants hired on contract basis. The Division

Heads that work under SEVP or consultants are either Senior Vice

President (SVP), Executive Vice President (EVP) or Vice President

(VP). The members of the executive committee other than the M.D.

shall hold office for such period as may be determined by the Board.

The decisions of the executive committee, other than those, which relate

to matters specified by the board in this behalf, shall be laid before the

board

Functions of Executive Committee

The members of the executive committee other than the M.D. shall hold

office for such period as may be determined by the Board of Directors.

Internship Report on UBL, Main Branch, Bannu 27

The decisions of the executive committee, other than those, which relate

to matters specified by the board in this behalf, shall be laid before the

board for approval.

Subject to the general or special direction of the board, The Executive

Committee may deal with any matter within the competence of the

board.

Managing Director

The Managing Director is responsible for the efficient working of the

organization. He performs his duty according to the policies formulated

by the Board of Directors and is directly answerable to it.

The Federal Government on such salary and on terms and conditions,

shall appoint the MD as it might deem fit.

The MD shall hold office for term of three years, which the government

may extend from time to time.

The MD shall be the Chief Executive of the organization and shall

perform such functions as required by the Ordinance and the rules and

regulations made for the past.

Internship Report on UBL, Main Branch, Bannu 28

ORGANIZATIONAL HIERARCHY CHART

Source: Sajid Javed Internship Report on UBL, 2002–2005, IMS, University of Peshawar

Internship Report on UBL, Main Branch, Bannu 29

Board of Directors

Executive Committee

President/CEO

SEVP

EVP

SVP

VP

AVP

Office Grade 1

Non Clerical Staff Clerical Staff Officer Grade

III

Officer Grade

II

ORGANIZATIONAL HIERARCHY CHART OF CONSUMER SECTOR IN UBL

Internship Report on UBL, Main Branch, Bannu 30

Board of Directors

Executive Committee

President/CEO

Group Executive

Global Sales Head

Head Secured Financing

National Sales Manager

Senior Sales Manager

Regional Sales Manager

Non-Clerical Staff Processors Relationship

officers

Relationship

Manager

Head Un-secured

Financing

LOCATION MAP

WITH an integrated network of over 1000 branches in Pakistan as well

as Overseas, UBL gives you direct access to a comprehensive range of better

banking facilities to help you monitor your business locally as well as

internationally.

www.ubl.com.pk

Internship Report on UBL, Main Branch, Bannu 31

CHAPTER – 5

DEPARTMENTATION

5.1 ACCOUNTS DEPARTMENT

This department deals with the internal accounts of the bank. The only

Book maintained here is the cashbook. The summary book and main ledger are

maintained.

The function of cashbook is to balance the daily transactions. At the end

of the day this department receives cash position from the cashier. This

position shows opening and closing balance.

TYPES OF ACCOUNTS

There are three types of accounts:

Current Accounts

Saving Accounts

Fixed Accounts

5.2 REMITTANCES DEPARTMENT

This dept is concerned with transfer of money from one place to another

place. Remittance can take place in three different ways.

a. Mail Transfer

When a customer requests the bank to transfer his money from this bank

to any other bank or the branch of the same bank in the city/ outside the

city or outside the country, the first thing he has to do is to fill an

application form in which he states that I want to transfer the money

from this bank to another bank. If the customer is the account bolder of

bank, then the bank will debit his account. The concerned office will fill

the different forms to make the mail transfer complete. Three forms used

for this purpose are listed below;

Internship Report on UBL, Main Branch, Bannu 32

Debit voucher

Credit voucher

Mail transfer register

If the customer is not the account holder of bank, then firstly he has to

deposit the money and then the above said procedure will be adopted to

transfer his money.

b. Telegraphic Transfer

This type of transfer is simple. After filling the application form, the

concerned officer fills the telegraphic form. This telegram is sent to the

required bank. Which on receiving it immediately makes the payment to

the customer and afterwards the vouchers are sent to the bank by

ordinary mail.

c. Demand Draft

DD is just a check and is issued when the customer wants to take the

draft personally. The idea behind it is that as the cash is not safe to be

kept along and a check in the shape of a draft is safer and one can easily

get cash by presenting it in the bank, on whose favor it has been made.

Draft is only issued when the customer is known to the bank and the

bank has the confidence that the customer will not do anything wrong

with the draft. For the preparation of a draft, first of all customer has to

fill an application form, then the concerned officer fills the following

before delivering the draft to the customer. The forms filled for this

purpose are as follows;

Demand draft register

Credit vouchers

Internship Report on UBL, Main Branch, Bannu 33

5.3 DEPOSITS DEPARTMENT

The main economic function of the commercial bank is to receive

surplus balances of individuals, firms, public institutions and to honor check

drawn up to it. The funds deposited with the commercial banks are classified

under four main heads.

a. Current or Demand Deposits

In this type of deposits, the depositor at any time by presenting a check

can draw his money from the bank. People keep some of their deposits

in current account in order to have ready command over money. No

interest is given on current deposits, because it is subject to transfer or

cashing by check at sight. The bank charges commission on the account,

which is called bank charges.

b. Saving Deposits

This deposit refers to the deposits, which are kept to meet the customer

and unexpected outlay or to safeguard financial respectability. The bank

undertakes to repay the money on demand up to a certain limit fixed by

the rules of the bank. The bank pays interest to the customers on saving

deposits. The customer has to give a notice to the bank about two weeks

in advance for withdrawal of large amounts.

c. Fixed Deposits

Fixed deposits are those, which are repayable only after the expiry of the

stipulated period i.e. from three months up to sixty months. The rate of

interest depends upon the length of the period. The rate of interest on

fixed deposits is higher than saving account, because the bank can safely

utilize these deposits for a certain period. Customer is allowed to borrow

the required amount, which should not exceed his fixed deposit. The

bank charges one or two percent higher rate of interest than the profit

allowed to him at his fixed deposit. The bank issues a receipt against the

fixed disposition stating the amount and the time of expiry to the

Internship Report on UBL, Main Branch, Bannu 34

customer. There is no paying book or passbook or checkbook issued to

the depositor.

Call Deposits

It is a type of bank guarantee on behalf of the depositor given at call. In

this case, Security Deposit Receipt (SDR) is issued by the bank at the

instructions of the depositor, confirming that amount of the SDR is held

by the bank, to be paid whenever called upon to do so by the beneficiary

named in the SDR.

5.4 ADVANCES DEPARTMENT

It is the loan function, which produces the major portion of banks’

income, and as such it is one of the major areas of professional bankers’

concerns and attention.

A bank generally deals in following areas;

Agricultural finance

Commercial finance

Industrial finance

Export finance

Import finance

In addition to the above-mentioned broad areas, there are loans available

to small size businessmen, construction companies etc.

In UBL, advances department is responsible to deal with following

cases;

1. Handle all the cases of short and long term loans.

2. To process all the cases concerned.

3. To forward the cases for approval and consideration to the higher authorities.

4. To deal with the borrower directly.

5. To implement the disbursement of the loan.

6. To give feed back to higher authorities in advance.

Internship Report on UBL, Main Branch, Bannu 35

UBL advances loans in the following manners:

a. By Cash Credit

In this form of lending, the bank lends money to the borrower against a

tangible security. The total amount of the loan, which is given, is not

paid in one installment. The borrower has to pay interest on the amount

borrowed. Cash credit is the favorite loan for large commercial and

industrial concerns, on account that the customers need not to borrow at

once the whole amount he is likely to require, but can draw such amount

as and when required.

b. By Discounting Bills of Exchange

It is another method of advancing loans to borrowers. The holder of bills

is paid an amount equal to the face value of the bill after deducting

interest at the market rate for the period the bill has to mature. Interest in

this type of loan can be charged as running finance and demand finance.

c. By Over Drafting

This facility is given to regular, reliable and well- established customers.

The bank charges interest on the extra money, which the borrower takes.

When a customer requires temporary accommodation, he may be

allowed to overdraw his current account usually against collateral

security. From the customers point of view this agreement like cash

credit is advantageous, as he is required to pay interest on the amount

actually used by him.

5.5 FOREIGN EXCHANGE DEPARTMENT

In modern banking system, foreign exchange department plays very

crucial and important role from every aspect. It is parallel banking with general

banking with an additional function of import and export business controlled

by State Bank of Pakistan. Rules and regulations are framed by state Bank of

Pakistan in the form of manuals. Foreign exchange department under SBP

Internship Report on UBL, Main Branch, Bannu 36

regulations also carries out international banking of UBL. Foreign exchange is

being controlled by SBP. No transaction can be affected without permission of

SBP, under foreign exchange regulations Act 1947 and notification issued there

under. Exchange control department of State Bank of Pakistan is responsible

for day-to-day administration of exchange control.

All the transactions shall be done at rate authorized by SBP. For this

purpose, US dollar has been fixed by SBP and the rates of other currencies are

calculated in accordance with the formula approved by SBP and as published

daily by the Foreign Exchange Rate Committee in Karachi. Head office ensures

that the branches receive the rates published by Foreign Exchange Rate

Committee on the same day.

The foreign exchange department provides the following services;

1. Foreign Currency Accounts

Foreign currency in UBL can be opened in 4 major currencies of the

world i.e. US dollar $, Japanese Yen, German Mark, DM and Pound

Sterling. Only authorized branches of UBL can deal in foreign currency

account.

Pakistani citizens and foreigners both can open foreign currency account

by introduction and following the procedure required for general

accounts with one exception for foreigners that they will have to submit

a copy of their passport. The account may be personal or joint.

Amount deposited in foreign currency account must be in four

currencies, which were mentioned earlier. When the customer will

withdraw the money he will receive the amount in the same foreign

currency. Profit will also be in the same currency. There are two types

of foreign currency account;

a. Current account

b. Saving account

Internship Report on UBL, Main Branch, Bannu 37

a. Current Account

On current account, no profit is given to the account holder. This

account is exempted from zakat, income tax and wealth tax. Worldwide

remittances (inside and outside) facility is given to customer. Cash travel

checks, foreign exchange bearer certificate, and coming for customer

can be deposited in his account.

Similarly account holder can shift the amount or any part thereof to

foreign countries through exchange remittances service.

b. Saving Account

On saving account, a handsome profit is paid to the account holder. On

saving account, profit is paid to the customer in the same currency in

which he had opened the account. This account is also exempted from

zakat, income tax and wealth tax etc.

Saving account can be opened with an amount of $ 100 equivalent in

other three currencies. The facility of inward and outward remittance is

also granted to the customer. Profit is paid on monthly product basis.

2. Sale and Purchase of Foreign Currency

UBL is an authorized dealer of State Bank of Pakistan. It can sell and

purchase foreign currency. UBL usually involves sale and purchase of

US dollars, Japanese yen, Pound Sterling, German Mark, Saudi Riyal,

and UAE Durham.

Daily exchange rate by SBP from ANZ Grind lays Bank Karachi is sent

to all the branches authorized in foreign exchange. Daily sale and

purchase of foreign currencies is done according to that rate sheet issued

by SBP on daily basis. Sale and purchase rates of foreign currency are

different.

The purchase of coins is avoided, only notes are purchased. Only those

foreign currencies are purchased for which resale to customer is

possible. And only those persons, who have passport, can sell and

Internship Report on UBL, Main Branch, Bannu 38

purchase foreign currency to or from UBL. Foreigners can also sell

foreign currencies by showing their passport.

There are 5 rates of foreign currencies:

1. For import

2. Cash purchase

3. Cash sale

4. Travel check purchases

5. Foreign currency

It is the policy of UBL to involve only in the sale of hard currencies i.e.

those, which are easily accepted. Head office of UBL has given certain

limits to each authorized branch about the custody of foreign currency.

If the amount exceeds this limit, the branch must transfer the cash to

feeding branch or SBP.

All the authorized branches of UBL must submit following reports about

foreign exchange business;

1. Report to general manager office

2. Monthly business report to SBP

3. Monthly report to head office

3. Remittances in Foreign Exchange

As we know that the money of one country is not legal tender in other

countries. The monetary device, which has been evolved, for all international

payments is the foreign exchange from the exporter and others who have it for

sale and sell foreign currency to importers and others who need it in their own

countries. A transfer from a bank account in the debtor’s country to the

creditor’s country affects the international payments.

Two branches of the same bank or of different banks involve in foreign

remittance. One is called remitting branch or bank and the other is called

receiving branch or bank. In foreign currency, SBP has given general

permission to authorized dealers in foreign exchange including UBL to affect

Internship Report on UBL, Main Branch, Bannu 39

remittances for specific purposes without referring it to (SBP) for approval i.e.

remittance on account of education subscription, books and periodical of

technical nature. Remittance can be done in following ways;

1. Telegraphic Transfer (TT)

2. Mail Transfer (MT)

3. Foreign Demand Draft (FDD)

Internship Report on UBL, Main Branch, Bannu 40

REFERENCES

1. S.A.HAQ (1980), practice and Law of Banking in Pakistan 6 th Edition,

Royal Book Company Karachikpp1-19.

2. UBL Annual Report (2003-2005).

3. Sajid Javed (2002-2005) Internship Report on UBL, IMS P (36-38)

4. UBL annual report (2003-2005)

5. Ibid.

Internship Report on UBL, Main Branch, Bannu 41

CHAPTER – 6

BANKING EFFORTS

6.1 COMMERCIAL BANKING

If you have a small or medium-sized business, UBL can assist you with

the right mix of banking services that will help you manage and grow your

business. Our experts will facilitate you in the varied financial situations that

you come across. We will respond to your needs promptly because we

understand how many your customers, your employees and you depend on us.

6.2 CONSUMER BANKING

You as an individual can gain and benefit the most through UBL

Consumer Banking. In UBL you get friendly, efficient and attentive

personalized banking services - a unique banking relationship experienced by

each UBL client. You can utilize the following services

UBL Cash line

UBL Address

UBL Drive

PLS Term Deposits

PLS Savings Accounts

Uni-Saver

Remittances

6.3 CORPORATE BANKING

Our mission is to serve all your corporate needs and ensure your full

satisfaction through product innovation, personalized banking, and top notch

service.

The CBG department of UBL defines corporate banking in Pakistan.

Amongst the local banks UBL CBG is the pioneer in providing innovative

Internship Report on UBL, Main Branch, Bannu 42

solutions to its diversified and satisfied customer base. UBL CBG is considered

to be a major player in the financial market of Pakistan.

The Corporate Banking Group focuses on attracting and servicing large

portfolio customers. Our effort is providing exemplary customer service using

the "Single Window" concept and product superiority. The Relationship

Management team managed by highly qualified individuals from the industry

has steadily expanded our customer base and continues to enhance our cordial

relations with our esteemed clients.

Despite the sluggish economic growth in recent years, UBL

outperformed all the other local banks in the corporate banking sector primarily

due to CBG's emphasis on establishing and enhancing relationships with

foreign/local blue chip and middle market customers thereby capturing

significant market share.

UBL's appetite for large exposures coupled with dedicated Structured

Finance Unit, and an innovative team of professionals having extensive

experience of Corporate Banking gives it the right platform to succeed in

todays competitive and a demanding environment.

The success of CBG has been established from the fact that UBL

received the 'No.1Euromoney 2000' Best Local Bank award and recognized it

to have out performed all other banks. In year 2000, UBL was also voted as the

best Corporate Bank by the customers of a major foreign bank in a survey.

Aggressive marketing combined with professionalism has led to an increase in

UBL's market share with top corporate customers and in some cases replacing

Foreign Banks.

Internship Report on UBL, Main Branch, Bannu 43

FINANCIAL PRODUCTS

6.4 UNI CASH

Nowadays carrying cash while going out of your home is very risky.

Every body wants maximum security while keeping his money in his pocket.

People make use of TC and various credit cards for this purpose. UBL provides

such facility through UNI CASH. The management of UNI CASH is carried

out in the following way.

I. Personal Identification Number

When a Uni-Cash card is issued to a customer, a unique number known

as Personal Identification Number (PIN) is also allotted to him/her. This

is 4 digits confidential number which when used in conjunction with the

Uni-Cash card enables the customer to avail the cash point service. To

keep it secret even from the bank staff, the PIN is generated and printed

in a special manner by the computer on pre-sealed, tamper proof PIN

millers. These PIN millers are designed in such a way that the PIN is

only visible after the envelope is opened by the customer.

II. Card serial number

The customer will notice that some numbers and alphabets are embossed

on his Uni-Cash card. The first line obtains UNICASH CARD SERIAL

NUMBER while the other line has customer’s name, account number

and card expiry Month/ Year.

III. Weekly withdrawal limits

The Uni-Cash card issued to customer carries a weekly withdrawal limit,

which applies to cash withdrawal, made from any of the cash point. This

limit is equal to initial amount deposited by him at the time of applying

for his card.

IV. Cash points

For customer’s convenience, a number of cash points are available in the

country. These machines are at customer’s service round the clock on all

Internship Report on UBL, Main Branch, Bannu 44

days of the year. Uni-Cash card can be used in these machines. Besides

cash withdrawal, cash points would provide the following facilities;

Balance Inquiry Mini Statement

Pin Change

V. Card Captures

Cash points will automatically capture card that have been duly reported

as lost or have been cancelled or have expired. Similarly if one fails to

key-in his correct PIN, in three repeated attempts, the card will be

captured.

VI. Loss of Card

In case, customer loses his UNI CASH card or the card is stolen, the

matter should invariably be brought to the notice of the bank personnel.

6.2 UNI SONA

This product has been designed to attract more and more savings. As

inflation in Pakistan is at a very high rate, due to which money has very limited

value.

The features of Uni-Sona are the following;

The amount deposited in the bank becomes triple after seven years.

If person withdraws his money after five years he will get double

amount as compared to its initial deposits.

There is also a facility for partial withdrawal from principle amount. For

example, if a person has deposited Rs.50, 000,000 in January 1993 and he

withdraws Rs.20, 000,000 in January 1995. In 1996 the person has Rs.

30,000,000. This amount will receive the same interest rate and would be

doubled (Rs. 60,000,000) in January 98 and triple (RS. 90,000,000) in January

2000.

Internship Report on UBL, Main Branch, Bannu 45

6.3 UNIZAR

It is a special type of foreign currency account and can be opened in two

currencies i.e. US $ and Pound Sterling. Minimum amount required for

opening of this account is 750 pounds or $ 1000. Profit is paid in the currency

in which the account is opened. Rate of return of 2.25% is paid to the depositor.

A special feature of this account is that withdrawal from the deposits can

be made anywhere in the world in the UBL branch.

6.4 UISAVER

It is a special type of account designed for corporate savers. This

account can be opened with Rs.1 m up to Rs. 10 m. The minimum profit rate is

4% while maximum limit is 8%. Profit is paid on daily product basis. Any one

can open this account.

Internship Report on UBL, Main Branch, Bannu 46

REFERENCES

Thaiman Theo, Scott G. William, Connor E.Partick, Management, “5th

Edition”, Boston USA, Houghton Miffin Company 1985, p. 303.

Ewin B. Flipp, principles of personnel Management, Tokyo McGraw

Hill 1984, p. 275.

www.ubl.com.pk

Internship Report on UBL, Main Branch, Bannu 47

CHAPTER – 7

SWOT ANALYSIS

SWOT analysis helps to find out about the strengths and weaknesses of

an organization, the opportunities that the organization can avail and the threats

that could be harmful. This analysis gives a clear picture about the organization

management and giving a review of the organization’s environments. The

following are the strengths, weaknesses, opportunities and threats of United

Bank Limited:

7.1 STRENGTHS

Product Line

Bank offers a prestigious product line-up that continues to fulfill and

satisfy the banking requirements of not just the conventional consumers but the

demanding financial needs of the corporate sector as well. The product

portfolio has been expanded in response to the customers’ needs, and now

covers a host of services in the areas of corporate banking, consumer banking,

and investment banking. The line-up includes:

Business Line Account

Car financing

Credit cards

Home loans

ATMs and etc.

Running Finances

Rupee traveler’s checks & Money gram

Online banking

Personal Loans

Internship Report on UBL, Main Branch, Bannu 48

QUALITY OF MANAGEMENT

Any banking organization is successful if it has an efficient and effective

management structure. The management of United Bank limited is providing

the best possible services and is trying to push the organization to heights of

success. The management is free from any politics after the privatization. The

structure is designed in such a way that everyone is clear about the assigned

role and responsibilities; the hierarchy is efficient in problem solving and

making decisions. An organization’s success dependent on the efficiency of its

management, and weak management can destroy its image. Planning, staffing,

organizing and leading are the basic functions of any management, the

structure is affiliated with Abu Dhabi consortium, the management style is also

successfully implemented in Pakistan.

RESOURCEFULNESS OF THE SPONSORS

United Bank Limited has been taken over by Abu Dhabi Consortium and

BestWay Group. These sponsors are resourceful, as in the span of three and half years

the bank has launched the consumer loans segments and expanded the regional sales

centers from 10 to 14 from the launch till date and is further expanding. The bank is

planning to add 10 more regions in the years to come.

COMPETITIVENESS AND AGILITY

The bank is one of the top banks of Pakistan. It has a tendency of being

agile in any kind of market condition and can compete with any bank. The

Banks like PICIC, ASKARI, HBL, NBP, Bank Alfalah and UNION

commercial banks are also having a lead in providing better services and

products but United Bank limited still has a cutting edge by providing branded

products. The market of Pakistan is fragile but UBL has the talent to act

accordingly to any situation and take control. The basic philosophy is customer

satisfaction and in order to act on this they are providing new and better

products. The services of UBL as compared with other banks are customer

friendly.

Internship Report on UBL, Main Branch, Bannu 49

FLEXIBILITY IN APPROACH

The bank has a flexible approach towards different kinds of customers

located in different regions of Pakistan. The bank knows where to invest and

lend funds and from where to generate deposits. The branches are located in the

main areas where resources and clientele are readily available. The bank is not

taking any kind of the risk by investing into areas where profit is unpredictable.

EFFICIENT HUMAN RESOURCE MANAGEMENT

UBL has a qualified staff and the bank’s human resource policy is quite

satisfactory. The bank provides formal and on- the job training to its staff

members. Every year the bank is adding young and energetic personnel to its

team. The increments of UBL are merit based. The bank has a separate

department, human resource department that deals with hiring, developing and

retaining staff. The bank places advertisements in the newspapers, giving the

job description specifying the types of personnel required. Performance based

evaluation is done at the year-end.

OFFER INNOVATIVE PRODUCTS

UBL is keeping pace not only with the local market but also with the

global market. New products like credit card and money gram remittance

service have been introduced. Being a big bank by network it has established

reputation in providing all the possible products with attractive package e.g.,

low rates or low entrance fee, no annual and renewal charges etc.

PROMOTING SPORTS

The bank arranges championships and tournaments of Golf and Cricket

in all the provinces of Pakistan.

CREDIT RATINGS

PACRA (Pakistan Credit Rating Agency) an affiliate of IBCA rated

UBL as A1+ for both long term and short-term periods. Both ratings are

investment grade and deficits expectation of credit quality and very low

expectation of credit risk. It is a statutory requirement that every bank will go

Internship Report on UBL, Main Branch, Bannu 50

through an exercise with this rating agency. United Bank limited credit

portfolio was rated on the basis of bad debts, lending to different sectors and

overall credit management.

7.2 WEAKNESSES

Even if an organization is profitable and is having best possible policies

and management, it might be having certain shortcomings, which should be

pinpointed in order to overcome them or minimize their adverse effects.

OVER AMBITIOUSNESS

The bank is over ambitious. In the last three and half years post-

privatization era the bank has not consolidated. Within this short span of time,

the bank has opened 14 regions for granting consumer loans and is planning to

open more which can become very unwieldy. The bank is attempting to

achieve too many things too soon. In doing so it is ignoring the myriad

problems faced by the branches, which can’t keep pace with the high speed.

STAFF OVER WORKED

The bank’s staff is over worked and over loaded with responsibilities.

The bank needs more staff as the existing staff is trying it hard but cannot cope

with both the paper work and customer handling at the same time. Though the

working hours of the bank are from 9 am to 5 pm but the staff has some much

work to handle that they have sit late hours. This frequent late sitting is likely

to erode the employee efficiency/morale.

OVER COMPETITIVENESS

The bank is too concerned about competition. This is affecting the

bank’s profitability. Rates charged on home loans and car finance is too low,

lower than what is being charged by others in the market. In attracting

customers and taking over a large portion of the market share, the bank is

putting its profitability as stake.

Internship Report on UBL, Main Branch, Bannu 51

CONTRACTUAL STAFF

The UBL has hired the Consumer Loans personnel through the

recruiting agencies, who are not treated at par with its regular employees. The

contractual workers work on commission or commission +salary basis. These

employees leave UBL when they get permanent or relatively better job in the

market. Continued use of contract staff creates problems for the UBL

management in the form of employees’ shortage.

TOO CAUTIOUS

The bank is cautious in relation to investment and exploring new

markets. It has invested in all those companies which are already on-going

concerns it is good for the profitability of the bank but it is not beneficial to the

market. The bank also follows a strict lending policy that is ignoring project

financing. The bank is also not taking initiative in introducing new products in

the markets e.g., debit card is a new product and other banks are trying to

concentrate on it, but UBL is not availing it. Leasing and micro finance for the

consumer durables have already been started by other banks, but United Bank

Limited is still waiting for the response from the market, and is delaying the

launch of these products.

SHORTAGE OF CAPITAL ADEQUACY

The bank is suffering from capital inadequacy. The deposit base has

overgrown the equity. As per statutory requirement the bank has to keep 51.6

billion deposits against Rs. 4.13 billion equity, but its deposit of Rs. 51.6

billion are far above the statutory level.

7.3 OPPORTUNITIES

Financial market of Pakistan is a dynamic one and offers a number of

opportunities to the organizations. Due to lack of know-how and initiation on