ValueGuide January 2018 Intelligent Investing Market Outlook Stock Updates Sector Updates Viewpoints Regular Features Report Card Earnings Guide Products & Services PMS Top Picks MF Picks Advisory Trader’s Edge Technical View Currencies F&O Insights For Private Circulation only www.sharekhan.com Twists and turns ahead

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

ValueGuideJanuary 2018

Intelligent Investing

Market OutlookStock Updates

Sector UpdatesViewpoints

Regular Features

Report CardEarnings Guide

Products & Services

PMSTop PicksMF PicksAdvisory

Trader’s Edge

Technical ViewCurrencies

F&O Insights

For Private Circulation only www.sharekhan.com

Twists and turns ahead

TradeTiger better and faster

every quarter

What’s new in the latest version of TradeTiger

Registered Office: Sharekhan Limited, 10th Floor, Beta Building, Lodha iThink Techno Campus, Off. JVLR, Opp. Kanjurmarg Railway Station, Kanjurmarg (East), Mumbai – 400042, Maharashtra. Tel: 022 - 61150000. Sharekhan Ltd.: SEBI Regn. Nos.: BSE: INB/INF011073351 / BSE-CD ; NSE: INB/INF/INE231073330 ; MSEI: INB/INF261073333 / INE261073330 ; DP: NSDL-IN-DP-NSDL-233-2003 ; CDSL-IN-DP-CDSL-271-2004 ; PMS-INP000005786 ; Mutual Fund-ARN 20669 ; Research Analyst: INH000000370 ; For any complaints email at [email protected] ; Disclaimer: Client should read the Risk Disclosure Document issued by SEBI & relevant exchanges and the T & C on www.sharekhan.com before investing.

Disclaimer: Investment in securities market are subject to market risks, read all the related documents carefully before investing. read more

[email protected] 1800227500

Marketwatch with sectors: Bifurcate stocks according to sectors and track performance easily

Minimum margin display: Say good bye to punching orders repeatedly asrequired margin is now available upfront

Draw on charts: Do free hand drawing or marking on any part of the chart for better analysis

Ichimoku on scanner: The most reliable indicator, Ichimoku is now available on Stock scanner, go ahead make those technical calls!

Net rupee change on HeatMap: You can now get both percentage as well as Net Rupee change on the HeatMap

`%

Dynamic OCF with moneyness filter: With moneyness (ITM, ATM, OTM) filter, option traders can now identify the moneyness of scanned contracts

CONTENTS

3January 2018 Sharekhan ValueGuide3June 2017 Sharekhan ValueGuide

disclaimer

DISCLAIMER: This document has been prepared by Sharekhan Ltd. (SHAREKHAN) and is intended for use only by the person or entity to which it is addressed to. This Document may contain confiden-

tial and/or privileged material and is not for any type of circulation and any review, retransmission, or any other use is strictly prohibited. This Document is subject to changes without prior notice. This

document does not constitute an offer to sell or solicitation for the purchase or sale of any financial instrument or as an official confirmation of any transaction. Though disseminated to all customers

who are due to receive the same, not all customers may receive this report at the same time. SHAREKHAN will not treat recipients as customers by virtue of their receiving this report.

The information contained herein is obtained from publicly available data or other sources believed to be reliable and SHAREKHAN has not independently verified the accuracy and completeness of

the said data and hence it should not be relied upon as such. While we would endeavour to update the information herein on reasonable basis, SHAREKHAN, its subsidiaries and associated compa-

nies, their directors and employees (“SHAREKHAN and affiliates”) are under no obligation to update or keep the information current. Also, there may be regulatory, compliance, or other reasons that

may prevent SHAREKHAN and affiliates from doing so. This document is prepared for assistance only and is not intended to be and must not alone be taken as the basis for an investment decision.

Recipients of this report should also be aware that past performance is not necessarily a guide to future performance and value of investments can go down as well. The user assumes the entire risk

of any use made of this information. Each recipient of this document should make such investigations as it deems necessary to arrive at an independent evaluation of an investment in the securities of

companies referred to in this document (including the merits and risks involved), and should consult its own advisors to determine the merits and risks of such an investment. The investment discussed

or views expressed may not be suitable for all investors. We do not undertake to advise you as to any change of our views. Affiliates of Sharekhan may have issued other reports that are inconsistent

with and reach different conclusions from the information presented in this report.

This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution,

publication, availability or use would be contrary to law, regulation or which would subject SHAREKHAN and affiliates to any registration or licencing requirement within such jurisdiction. The securities

described herein may or may not be eligible for sale in all jurisdictions or to certain category of investors. Persons in whose possession this document may come are required to inform themselves of

and to observe such restriction.

The analyst certifies that the analyst has not dealt or traded directly or indirectly in securities of the company and that all of the views expressed in this document accurately reflect his or her personal

views about the subject company or companies and its or their securities and do not necessarily reflect those of SHAREKHAN. The analyst further certifies that neither he nor his relatives has any

direct or indirect financial interest nor have actual or beneficial ownership of 1% or more in the securities of the company nor have any material conflict of interest nor has served as officer, director or

employee or engaged in market making activity of the company. Further, the analyst has also not been a part of the team which has managed or co-managed the public offerings of the company and

no part of the analyst’s compensation was, is or will be, directly or indirectly related to specific recommendations or views expressed in this document.

Either SHAREKHAN or its affiliates or its directors or employees / representatives / clients or their relatives may have position(s), make market, act as principal or engage in transactions of purchase or

sell of securities, from time to time or may be materially interested in any of the securities or related securities referred to in this report and they may have used the information set forth herein before

publication. SHAREKHAN may from time to time solicit from, or perform investment banking, or other services for, any company mentioned herein. Without limiting any of the foregoing, in no event shall

SHAREKHAN, any of its affiliates or any third party involved in, or related to, computing or compiling the information have any liability for any damages of any kind.

Compliance Officer: Mr. Joby John Meledan; Tel: 022-61150000; For any queries or grievances kindly email

[email protected] or contact: [email protected]

Registered Office: Sharekhan Limited, 10th Floor, Beta Building, Lodha iThink Techno Campus, Off. JVLR, Opp. Kanjurmarg Railway Station, Kanjurmarg (East), Mumbai – 400042, Maharashtra. Tel: 022 - 61150000. Sharekhan Ltd.: SEBI Regn. Nos.: BSE: INB/INF011073351 / BSE-CD; NSE: INB/INF/INE231073330 ; MSEI: INB/INF261073333 / INE261073330 ; DP: NSDL-IN-DP-NSDL-233-2003 ; CDSL-IN-DP-CDSL-271-2004; PMS-INP000005786 ; Mutual Fund-ARN 20669 ; Research Analyst: INH000000370; For any complaints email at [email protected] ; Disclaimer: Client should read the Risk Disclosure Document issued by SEBI & relevant exchanges and the T & C on www.sharekhan.com ; Investment in securities market are subject to market risks, read all the related documents carefully before investing.

In December, the

markets continued

to rise, braving firm

interest rates, the

continued spike in

inflation, concerns of

fiscal slippages an its

fallout on bond yields and financial markets....

From the Editor’s Desk EQUITY

06

RESEARCH-BASED EQUITY PRODUCTS

PMS DESKWealthOptimizer PMS 30

ProPrime - Diversified Equity 31

ProTech - Index Futures Fund 32

ProTech - Trailing Stops 33

FUNDAMENTALS

TECHNICALS DERIVATIVES

Nifty 26 View 27

ADVISORY DESK DERIVATIVES

MID Trades 34 Derivatives Ideas 34

CURRENCY

FUNDAMENTALS USD-INR 28 GBP-INR 28

EUR-INR 28 JPY-INR 28

TECHNICALS

USD-INR 29 GBP-INR 29

EUR-INR 29 JPY-INR 29

MUTUAL FUND DESK

Top MF Picks (equity) 35

Top SIP Fund Picks 36

Market Outlook 07

Top Picks Basket 11

REGULAR FEATURES

Stock Update 16 Report Card 4

Sector Update 25 Earnings Guide 37

EQUITY FUNDAMENTALSREPORT CARD

4January 2018 Sharekhan ValueGuide

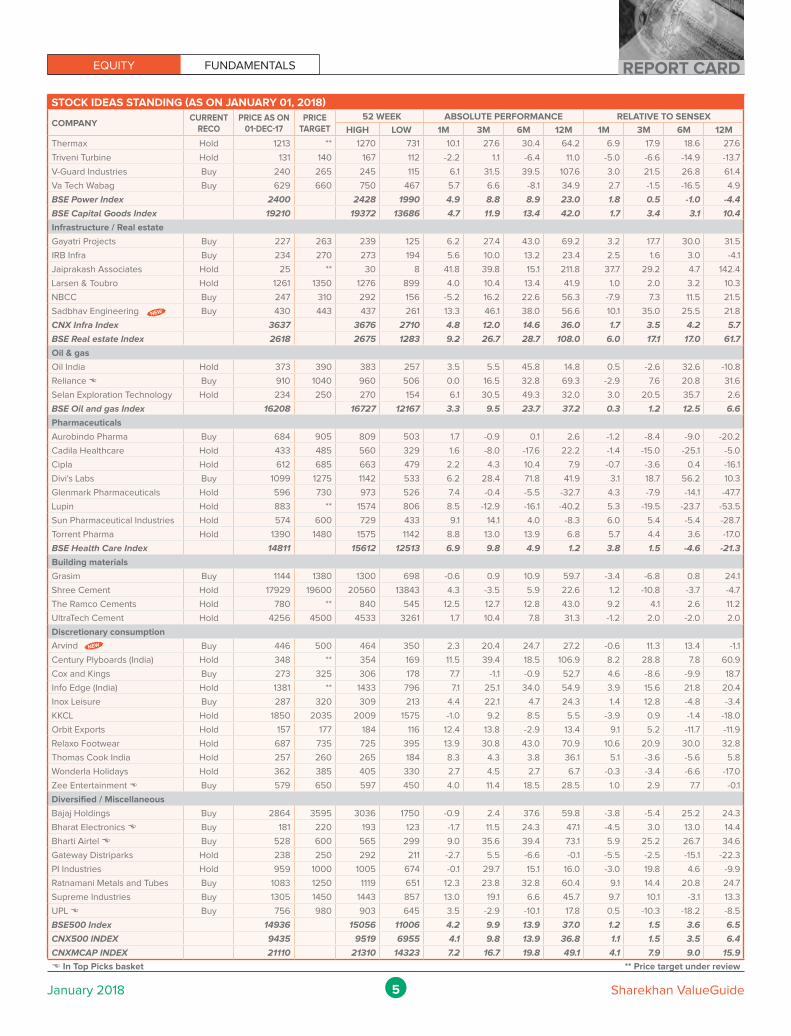

STOCK IDEAS STANDING (AS ON JANUARY 01, 2018)

COMPANYCURRENT

RECOPRICE AS ON

01-DEC-17PRICE

TARGET

52 WEEK ABSOLUTE PERFORMANCE RELATIVE TO SENSEX

HIGH LOW 1M 3M 6M 12M 1M 3M 6M 12M

Automobiles

Apollo Tyres Hold 269 292 288 172 10.1 9.4 11.7 47.2 6.9 1.1 1.6 14.4

Ashok Leyland Buy 119 130 134 79 -1.2 -3.6 28.3 50.3 -4.0 -11.0 16.7 16.9

Bajaj Auto Buy 3289 3625 3385 2552 2.2 5.8 20.2 27.5 -0.7 -2.3 9.3 -0.9

Gabriel India Buy 202 222 223 107 8.4 2.6 34.8 89.0 5.3 -5.2 22.6 46.9

Hero MotoCorp Buy 3749 4200 4200 2963 4.0 -0.7 1.3 26.2 1.0 -8.2 -7.9 -1.9

M&M Buy 745 788 786 585 5.7 18.7 11.5 26.9 2.6 9.7 1.4 -1.3

Maruti Suzuki E Buy 9652 10170 10000 5268 12.1 21.0 35.0 83.2 8.9 11.8 22.8 42.4

Rico Auto Industries Buy 102 130 111 44 7.6 10.4 88.7 89.8 4.4 2.0 71.6 47.5

TVS Motor Buy 766 825 795 355 5.8 17.0 40.0 113.8 2.7 8.1 27.3 66.2

BSE Auto Index 26543 27031 20179 6.4 9.8 14.1 32.3 3.3 1.4 3.8 2.8

Banks & Finance

Axis Bank Hold 566 UR 570 424 5.9 11.1 10.4 26.9 2.9 2.6 0.4 -1.3

Bajaj Finance Buy 1726 2050 1989 842 0.8 -6.1 26.0 105.4 -2.1 -13.3 14.6 59.7

Bajaj Finserv Buy 5172 6050 5835 2859 1.4 0.3 25.6 78.7 -1.5 -7.3 14.2 38.9

Bank of Baroda Buy 162 220 207 134 -3.6 17.4 -0.1 6.0 -6.4 8.4 -9.2 -17.6

Bank of India Hold 170 215 217 106 -9.3 23.5 21.6 58.4 -11.9 14.1 10.6 23.1

Capital First Buy 695 880 839 564 -0.2 -5.3 4.2 21.6 -3.1 -12.5 -5.3 -5.5

Federal Bank Buy 109 145 128 66 0.2 -3.5 -2.9 63.9 -2.7 -10.8 -11.7 27.4

HDFC Buy 1684 1900 1805 1197 1.5 -3.4 5.2 34.9 -1.4 -10.7 -4.3 4.8

HDFC Bank E Buy 1855 2100 1905 1182 0.3 2.7 12.3 54.8 -2.6 -5.1 2.1 20.3

ICICI Bank Buy 310 340 332 226 1.7 12.2 6.9 34.7 -1.3 3.6 -2.8 4.7

LIC Housing Finance Buy 566 750 794 513 -0.9 -9.8 -23.1 2.0 -3.8 -16.7 -30.1 -20.7

Max Financial Buy 597 660 684 512 9.1 1.0 -5.4 8.8 6.0 -6.6 -14.0 -15.4

PTC India Financial Services Buy 38 45 51 34 3.3 2.2 -0.2 4.7 0.3 -5.6 -9.3 -18.6

Punjab National Bank Buy 170 240 232 113 -1.0 31.5 23.6 47.0 -3.9 21.5 12.4 14.3

SBI Buy 307 370 352 241 -1.8 21.0 12.2 23.8 -4.7 11.8 2.0 -3.7

Union Bank of India Hold 145 210 205 122 -8.3 14.4 -1.7 17.7 -10.9 5.7 -10.6 -8.5

Yes Bank Hold 313 350 383 226 1.9 -10.7 6.8 36.3 -1.1 -17.5 -2.9 5.9

BSE Bank Index 28639 29510 20358 0.7 6.0 9.2 38.9 -2.2 -2.1 -0.7 8.0

Consumer goods

Britannia Buy 4738 5500 4964 2830 -1.4 9.1 29.1 65.1 -4.3 0.8 17.4 28.3

Emami Buy 1336 1355 1352 942 2.4 22.1 24.8 41.3 -0.5 12.8 13.5 9.8

GSK Consumers Hold 6477 ** 6699 4851 6.5 29.1 22.5 31.1 3.4 19.3 11.4 1.9

Godrej Consumer Products Buy 986 1102 1084 746 1.1 7.4 2.1 31.8 -1.8 -0.8 -7.2 2.5

Hindustan Unilever Hold 1345 1350 1384 817 7.5 15.3 25.3 65.2 4.4 6.5 14.0 28.5

ITC Hold 262 325 368 239 2.8 1.5 -19.0 10.2 -0.2 -6.2 -26.3 -14.4

Jyothy Laboratories Hold 378 420 443 325 -1.8 -6.5 8.1 13.6 -4.7 -13.6 -1.7 -11.7

Marico Buy 321 365 349 252 3.3 3.8 2.6 24.7 0.3 -4.1 -6.7 -3.0

Zydus Wellness Hold 1042 ** 1072 809 12.5 16.0 22.7 21.2 9.3 7.1 11.6 -5.8

BSE FMCG Index 10664 10936 8084 3.7 9.3 2.6 32.9 0.7 1.0 -6.7 3.3

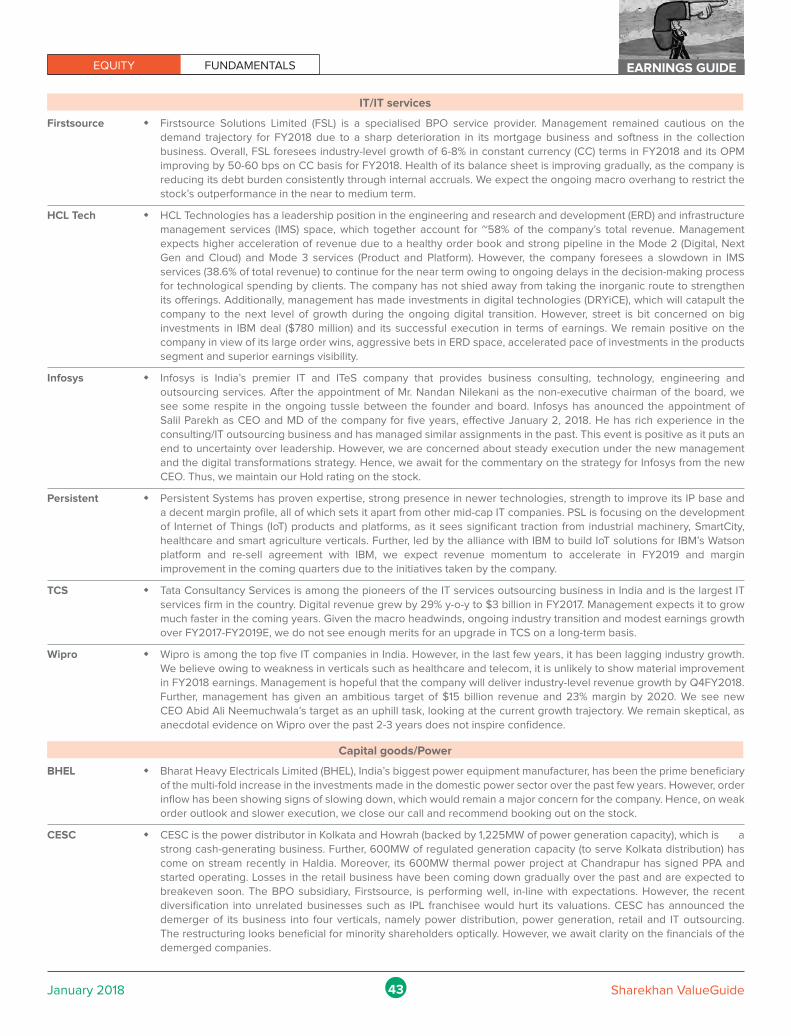

IT / IT services

Firstsource Solution Hold 41 45 49 30 0.4 -1.6 20.1 8.3 -2.5 -9.1 9.2 -15.8

HCL Technologies Buy 879 965 944 778 5.9 0.7 3.7 8.2 2.8 -7.0 -5.7 -15.9

Infosys Hold 1034 ** 1049 860 7.8 16.5 12.0 5.3 4.7 7.6 1.9 -18.2

Persistent Systems Hold 712 720 726 558 8.8 6.3 4.8 17.2 5.6 -1.8 -4.7 -8.9

Tata Consultancy Services Hold 2646 2700 2777 2153 0.6 8.9 12.6 14.0 -2.3 0.6 2.4 -11.3

Wipro Reduce 317 290 324 223 9.4 13.0 22.5 34.0 6.2 4.4 11.4 4.2

BSE IT Index 11216 11307 9357 5.9 13.5 15.1 12.7 2.8 4.9 4.7 -12.4

Capital goods / Power

CESC Buy 1064 1165 1080 636 6.8 7.8 22.5 68.6 3.7 -0.4 11.4 31.1

Crompton Greaves Hold 93 ** 97 59 10.5 17.8 13.0 56.5 7.3 8.9 2.8 21.7

Finolex Cable Hold 702 ** 732 400 5.0 29.6 54.8 70.8 2.0 19.8 40.8 32.8

Greaves Cotton Hold 140 ** 179 112 19.4 2.8 -12.6 19.0 15.9 -5.0 -20.5 -7.5

Kalpataru Power Transmission Hold 471 510 504 247 7.1 27.9 45.6 90.5 4.0 18.2 32.4 48.1

KEC International E Buy 383 ** 392 138 21.8 24.8 49.5 174.3 18.3 15.3 35.9 113.2

PTC India Hold 120 130 130 73 4.2 -2.5 27.1 67.1 1.2 -9.9 15.6 29.9

Skipper Hold 267 280 293 133 0.6 26.5 32.0 93.7 -2.3 16.9 20.0 50.6

NEW

EQUITY FUNDAMENTALS REPORT CARD

5January 2018 Sharekhan ValueGuide

STOCK IDEAS STANDING (AS ON JANUARY 01, 2018)

COMPANYCURRENT

RECOPRICE AS ON

01-DEC-17PRICE

TARGET

52 WEEK ABSOLUTE PERFORMANCE RELATIVE TO SENSEX

HIGH LOW 1M 3M 6M 12M 1M 3M 6M 12M

Thermax Hold 1213 ** 1270 731 10.1 27.6 30.4 64.2 6.9 17.9 18.6 27.6

Triveni Turbine Hold 131 140 167 112 -2.2 1.1 -6.4 11.0 -5.0 -6.6 -14.9 -13.7

V-Guard Industries Buy 240 265 245 115 6.1 31.5 39.5 107.6 3.0 21.5 26.8 61.4

Va Tech Wabag Buy 629 660 750 467 5.7 6.6 -8.1 34.9 2.7 -1.5 -16.5 4.9

BSE Power Index 2400 2428 1990 4.9 8.8 8.9 23.0 1.8 0.5 -1.0 -4.4

BSE Capital Goods Index 19210 19372 13686 4.7 11.9 13.4 42.0 1.7 3.4 3.1 10.4

Infrastructure / Real estate

Gayatri Projects Buy 227 263 239 125 6.2 27.4 43.0 69.2 3.2 17.7 30.0 31.5

IRB Infra Buy 234 270 273 194 5.6 10.0 13.2 23.4 2.5 1.6 3.0 -4.1

Jaiprakash Associates Hold 25 ** 30 8 41.8 39.8 15.1 211.8 37.7 29.2 4.7 142.4

Larsen & Toubro Hold 1261 1350 1276 899 4.0 10.4 13.4 41.9 1.0 2.0 3.2 10.3

NBCC Buy 247 310 292 156 -5.2 16.2 22.6 56.3 -7.9 7.3 11.5 21.5

Sadbhav Engineering Buy 430 443 437 261 13.3 46.1 38.0 56.6 10.1 35.0 25.5 21.8

CNX Infra Index 3637 3676 2710 4.8 12.0 14.6 36.0 1.7 3.5 4.2 5.7

BSE Real estate Index 2618 2675 1283 9.2 26.7 28.7 108.0 6.0 17.1 17.0 61.7

Oil & gas

Oil India Hold 373 390 383 257 3.5 5.5 45.8 14.8 0.5 -2.6 32.6 -10.8

Reliance E Buy 910 1040 960 506 0.0 16.5 32.8 69.3 -2.9 7.6 20.8 31.6

Selan Exploration Technology Hold 234 250 270 154 6.1 30.5 49.3 32.0 3.0 20.5 35.7 2.6

BSE Oil and gas Index 16208 16727 12167 3.3 9.5 23.7 37.2 0.3 1.2 12.5 6.6

Pharmaceuticals

Aurobindo Pharma Buy 684 905 809 503 1.7 -0.9 0.1 2.6 -1.2 -8.4 -9.0 -20.2

Cadila Healthcare Hold 433 485 560 329 1.6 -8.0 -17.6 22.2 -1.4 -15.0 -25.1 -5.0

Cipla Hold 612 685 663 479 2.2 4.3 10.4 7.9 -0.7 -3.6 0.4 -16.1

Divi's Labs Buy 1099 1275 1142 533 6.2 28.4 71.8 41.9 3.1 18.7 56.2 10.3

Glenmark Pharmaceuticals Hold 596 730 973 526 7.4 -0.4 -5.5 -32.7 4.3 -7.9 -14.1 -47.7

Lupin Hold 883 ** 1574 806 8.5 -12.9 -16.1 -40.2 5.3 -19.5 -23.7 -53.5

Sun Pharmaceutical Industries Hold 574 600 729 433 9.1 14.1 4.0 -8.3 6.0 5.4 -5.4 -28.7

Torrent Pharma Hold 1390 1480 1575 1142 8.8 13.0 13.9 6.8 5.7 4.4 3.6 -17.0

BSE Health Care Index 14811 15612 12513 6.9 9.8 4.9 1.2 3.8 1.5 -4.6 -21.3

Building materials

Grasim Buy 1144 1380 1300 698 -0.6 0.9 10.9 59.7 -3.4 -6.8 0.8 24.1

Shree Cement Hold 17929 19600 20560 13843 4.3 -3.5 5.9 22.6 1.2 -10.8 -3.7 -4.7

The Ramco Cements Hold 780 ** 840 545 12.5 12.7 12.8 43.0 9.2 4.1 2.6 11.2

UltraTech Cement Hold 4256 4500 4533 3261 1.7 10.4 7.8 31.3 -1.2 2.0 -2.0 2.0

Discretionary consumption

Arvind Buy 446 500 464 350 2.3 20.4 24.7 27.2 -0.6 11.3 13.4 -1.1

Century Plyboards (India) Hold 348 ** 354 169 11.5 39.4 18.5 106.9 8.2 28.8 7.8 60.9

Cox and Kings Buy 273 325 306 178 7.7 -1.1 -0.9 52.7 4.6 -8.6 -9.9 18.7

Info Edge (India) Hold 1381 ** 1433 796 7.1 25.1 34.0 54.9 3.9 15.6 21.8 20.4

Inox Leisure Buy 287 320 309 213 4.4 22.1 4.7 24.3 1.4 12.8 -4.8 -3.4

KKCL Hold 1850 2035 2009 1575 -1.0 9.2 8.5 5.5 -3.9 0.9 -1.4 -18.0

Orbit Exports Hold 157 177 184 116 12.4 13.8 -2.9 13.4 9.1 5.2 -11.7 -11.9

Relaxo Footwear Hold 687 735 725 395 13.9 30.8 43.0 70.9 10.6 20.9 30.0 32.8

Thomas Cook India Hold 257 260 265 184 8.3 4.3 3.8 36.1 5.1 -3.6 -5.6 5.8

Wonderla Holidays Hold 362 385 405 330 2.7 4.5 2.7 6.7 -0.3 -3.4 -6.6 -17.0

Zee Entertainment E Buy 579 650 597 450 4.0 11.4 18.5 28.5 1.0 2.9 7.7 -0.1

Diversified / Miscellaneous

Bajaj Holdings Buy 2864 3595 3036 1750 -0.9 2.4 37.6 59.8 -3.8 -5.4 25.2 24.3

Bharat Electronics E Buy 181 220 193 123 -1.7 11.5 24.3 47.1 -4.5 3.0 13.0 14.4

Bharti Airtel E Buy 528 600 565 299 9.0 35.6 39.4 73.1 5.9 25.2 26.7 34.6

Gateway Distriparks Hold 238 250 292 211 -2.7 5.5 -6.6 -0.1 -5.5 -2.5 -15.1 -22.3

PI Industries Hold 959 1000 1005 674 -0.1 29.7 15.1 16.0 -3.0 19.8 4.6 -9.9

Ratnamani Metals and Tubes Buy 1083 1250 1119 651 12.3 23.8 32.8 60.4 9.1 14.4 20.8 24.7

Supreme Industries Buy 1305 1450 1443 857 13.0 19.1 6.6 45.7 9.7 10.1 -3.1 13.3

UPL E Buy 756 980 903 645 3.5 -2.9 -10.1 17.8 0.5 -10.3 -18.2 -8.5

BSE500 Index 14936 15056 11006 4.2 9.9 13.9 37.0 1.2 1.5 3.6 6.5

CNX500 INDEX 9435 9519 6955 4.1 9.8 13.9 36.8 1.1 1.5 3.5 6.4

CNXMCAP INDEX 21110 21310 14323 7.2 16.7 19.8 49.1 4.1 7.9 9.0 15.9

E In Top Picks basket ** Price target under review

NEW

NEW

6January 2018 Sharekhan ValueGuide

Twists and turns ahead

In December, the markets continued to rise, braving firm interest rates, the continued spike in inflation, concerns of fiscal slippages an its fallout on bond yields and financial markets. The Sensex and Nifty ended the month and year at all-time highs above 34000 and 10500, respectively, riding on the BJP’s electoral wins and positive macroeconomic data such as a rise in core sector output and a higher reading on the Nikkei Manufacturing Purchasing Manager’s Index (PMI).

For the whole of 2017, the benchmark indices gained 29-30% in their best run since 2014. Major movers and shakers were the onset of the Goods and Services Tax (GST) regime, upgrades from Moody’s and World Bank, a stellar series of initial public offers, bank recapitalisation and the amendment to the Insolvency and Bankruptcy Code. Steady investments by domestic institutional investors added the liquidity push. A gradual revival in GDP growth and corporate earnings, as effects of demonetisation and GST fades away also supported markets.

After a happy ending to 2017, the new-year has also begun on an optimistic note. Equity markets continue to scale new heights in the initial days itself. The street is hoping for better times ahead. And rightly so, the domestic policy driven disruption is behind us, the corporate earnings revival could finally materialise in 2018 and finally, the global environment is also expected to remain supportive in 2018.

The US economy is expected to build on the recovery of 2017 and the US Federal Reserve expects the economy to grow by 2.5% in 2018. In fact, the World Manufacturing PMI is surging and promises 2018 to be one of the strongest growth years in the last one decade. On the other hand, the liquidity conditions are comfortable and bond yields of many countries are yielding negative returns. No wonder, the leading global markets are at all time high levels.

But all is not well. There are challenges ahead. Domestically, the government has to play a difficult balancing act in the forthcoming Union Budget. On one hand, there is a need to make higher allocations to ease rural stress and continue to scale up public spending in infrastructure development to support the economy. On the other hand, the revenue collections post implementation of GST continues to remain weak. Thus, it would be a challenge to stick within the prescribed target on fiscal deficit under the FRBM Act. It would be difficult for the government to resist populist measures given the fact that 2018 would see elections in many important states like Rajasthan, Madhya Pradesh, Chhattisgarh and Karnataka. Lastly, the rising crude oil prices would put additional pressure on government’s fiscal position.

Globally, the US Federal Reserve’s planned rate hikes, geopolitical tensions and the movement in crude oil prices will be key factors to keep an eye on. Rate hikes by the US Federal Reserve may make FII inflows unpredictable, though domestic inflows are likely to remain healthy due to lack of better investment opportunities.

Overall, the research team believes that the returns could be much sober in 2018 and the volatility could increase in the second half of the year. However, the year would offer many money making opportunities including the resurgence of some of the lagging stocks and/or sectors/pockets of stocks. Stay tuned to our research recommendations and subscribe to our investment products to make the best of your investments in 2018. Wish you a happy and a profitable New Year!

To read our Market Outlook for 2018, turn to page 7.Fro

m t

he

Ed

ito

r’s

De

skFrom the Editor’s Desk

EQUITY FUNDAMENTALS MARKET OUTLOOK

7January 2018 Sharekhan ValueGuide

5

10

15

20

Dec

-07

Dec

-08

Dec

-09

Dec

-10

Dec

-11

Dec

-12

Dec

-13

Dec

-14

Dec

-15

Dec

-16

Dec

-17

Sensex PE 10 Year average

Market Outlook December 26, 2017

Winds of changeReturns to sober down in 2018, expect some of the laggards to lead the rally

Happy ending to 2017: Benchmark indices are set to close 2017 at their all-time high levels. This is sort of a complete turnaround from the cautious atmosphere resulting from the aftermath of demonetisation at the beginning of the year. Indian equities rode on the tide of unabated equity rally globally. However, from India’s point of view, the underlying theme was the strong retail inflow into equity markets that not only absorbed the selling pressure from foreign investors but also pushed indices to a new peak. From a macro perspective, the government with bold reforms to curb black money implemented Goods and Services Tax (GST) and is looking at addressing the issue of recapitalisation of ailing public sector banks. No wonder, the rupee snapped the six-year trend of weakness and appreciated in 2017 despite weak industrial production and slowdown in exports.

Key expectations from 2018: Earnings growth to pan out finally; Laggards to rise from ashes1. Revival of earnings growth in India

2. Underperforming sectors/pockets of stocks and certain companies to outperform indices

Earnings – Revival in demand and normalisation of earnings from a low base: Benchmark indices are already trading at premium to long-term average valuation (PE) multiples. Thus, it is high time the baton shifts from expansion in PE multiples to earnings growth to drive the rally ahead. The revival in earnings growth is based on three pillars of pickup in consumer demand (both urban and rural as GST impact eases out and the government takes policy measures to ease rural stress), improvement in exports (driven by revival in global economic growth outlook) and normalisation of earnings across key sectors from a low base. Earnings growth would normalise in some of the heavyweight sectors such as banks (especially corporate lenders such as ICICI Bank, Axis Bank, SBI and BoB), telecom, energy (high crude oil realisations) and auto (two-wheelers and farm equipment) along with continued uptrend in consumer goods, metals and other commodity stocks.

Laggards to rise from ashes; Emergence of new drivers of the rally: Year 2018 would be different than the past couple of years in terms of much better growth outlook for the global economy, expectations of a healthy revival in India’s economic growth and earnings (from a low base) and the largely stable commodity prices. Changing macro environment and business conditions would result in emergence of new leaders of the rally in the Indian equity market. Though we continue to retain our faith in investment themes with multi-year growth story such as financialisation and formalisation

(extensively documented in our Market Outlook reports), we expect new leaders to emerge and outperform in 2018. Some of these leaders are as follows:

- Three large-cap index stocks that are witnessing significant improvement in their fortunes and would outperform the benchmark indices are: Bharti Airtel, ONGC and SBI

- Rural and semi-urban demand-driven companies

- Midcap infra/construction companies

Dark clouds on the horizonThere are issues on the global and domestic front that could derail the rally. Globally, the Bitcoin bubble (that has grown to unexpectedly high proportions) could burst and have its ripple effects on financial markets. Moreover, there are geopolitical risks in the form of growing political instability in Spain and continued threats by North Korea. Lastly, valuations are turning out to be a concern for equity investors globally in general and particularly in India due to absence of the much-promised meaningful revival in corporate earnings.

Valuation – Limited scope for PE expansion; Expect returns in line with earnings growthOverall, the Sensex is trading at 18x-18.5x times its one-year forward earnings and is clearly not cheap anymore. Thus, the scope for further PE expansion is limited. More so, bond yields (risk premium) have also hardened and it clearly has an impact on PE multiples in equities. However, equities are expected to still give healthy double-digit returns in 2018 on account of healthy revival in earnings growth coupled with continued inflows into equities. Though foreign inflows tend to be unpredictable and erratic at times, domestic inflows are likely to remain healthy due to lack of better investment opportunities. Sensex PE band (based on one-year forward earnings)

Source: Bloomberg, Sharekhan Research

EQUITY FUNDAMENTALSMARKET OUTLOOK

8January 2018 Sharekhan ValueGuide

The Indian markets scale new all time high...

Despite weakness in IIP data & slowdown in exports...

...but Indian markets weren’t alone, we were part of a Global rally

Rupee has snapped its 6-yr weakening trend

Participation (across sector & size) has been broad based FIIs yet to fully join the party

Happy ending to 2017

05000

10000150002000025000300003500040000

Dec

-06

Dec

-07

Dec

-08

Dec

-09

Dec

-10

Dec

-11

Dec

-12

Dec

-13

Dec

-14

Dec

-15

Dec

-16

Dec

-17

Sensex crosses 34K !

Sensex

0%10%20%30%40%50%60%70%

BS

E S

mal

l Cap

BS

E C

onsu

mer

D

iscr

etio

nary

BS

E M

idC

ap

BS

E M

etal

BS

E B

anke

x

BSE

Cap

Goo

ds

BS

E O

il &

Gas

BS

E F

MC

G

BS

E A

uto

BS

E P

ower

BS

E IT

Sen

sex

1 Year Sectoral Indices performance (%)

-40000

0

40000

80000

120000

160000

CY11 CY12 CY13 CY14 CY15 CY16 CY17

FII Inflow into Equities (Rs Cr)

-4-202468

10121416

Apr

-12

Oct

-12

Apr

-13

Oct

-13

Apr

-14

Oct

-14

Apr

-15

Oct

-15

Apr

-16

Oct

-16

Apr

-17

Oct

-17

IIP growth 3Month Moving Average

3.3%

-16.8%

-4.0%

-13.3%

-2.3%-4.2%

-2.4%

5.5%

Dec-10 Dec-11 Dec-12 Dec-13 Dec-14 Dec-15 Dec-16 Dec-17

INR strengthens (against USD)

Source: Bloomberg, Sharekhan Research

Source: Bloomberg, Sharekhan Research

Source: Bloomberg, Sharekhan Research

Source: Bloomberg, Sharekhan Research

Source: Bloomberg, Sharekhan Research

Source: Bloomberg, Sharekhan Research

0.0%

10.0%

20.0%

30.0%

40.0%

Han

g S

eng

Sen

sex

IBO

VE

SP

A

Dow

Jon

es

FTS

E-J

SE

KO

SP

I

Nik

kei

DA

X

CA

C

SH

AN

GH

AI C

OM

P

1 Year Return Global Indices

EQUITY FUNDAMENTALS MARKET OUTLOOK

9January 2018 Sharekhan ValueGuide

State elections results set priorities for Union Budget:

Results of Gujarat state elections saw BJP maintaining

its citadel. The margin of victory has, however, left alarm

bells ringing. The show is likely to compel the NDA

Government to deliver faster and more visible results on

the growth and employment front (since jobless growth is

the key niggle). Hence, intuitively, one expects political

expediency in determining economic policy direction

and higher public spending. The FY2018-FY2019 Union

Budget is likely to be pro-growth and employment with

special focus on rural and middle income groups with

greater focus on things such as doubling of farm and rural

income, job creation, boosting of disposable income and

housing for all. We opine that the government’s stance is

likely to continue till 2019 General Elections. Moreover,

we believe there is less probability of disruptive reforms

coming up in 2019, as the government may look to

consolidate on its earlier initiatives.

Fiscal deficit – Slippage not a big concern if done

for the right reason: As subsequent elections loom

over the horizon, the spectre of farm loan waivers and

implementation of Pay Commission recommendations

may skew the fiscal discipline going forward. Moreover,

measures such as UDAY, PSU Bank Recapitalisation

and GST slab reductions are likely to impact the fiscal

consolidation roadmap.

FY2017A FY2018E

FISCAL DEFICIT TARGET (as % of

GVA)

3.50 3.20

TILL APR-AUG (as % of GVA) 2.67 3.08

Source: Sharekhan Research

While acknowledging that fiscal deficit financing fiscal

slippage generally comes with its share of negative

externalities, we believe, in the present context of India,

some amount of deficit financing, as counter cyclical

measures could support recovery, will not only be

welcomed but crucial to support growth. Notably, the

deficit will be due to higher capital expenditure rather

than due to revenue shortfall, which should be growth

supportive in the long term.

US Fed hike finally arrives, indicates growing strength

of the US economy: With the recent Federal Reserve

rate hike (increased by 25 bps) for the U.S., the U.S.

Fed has indicated that the U.S. economy has not only

improved, it is also in line with its planned trajectory. The

move in the U.S. will most likely create an environment

where probability of further rate cuts by the Reserve

Bank of India (RBI) decreases as the hike puts a kind of

floor for Indian interest rates in the near term. The Indian

markets (especially debt and equity) are in a different

risk category with respect to developed economies

(especially the U.S.). Hence, we believe there should

be minimal impact on Indian markets due to the rate

hike. Significant capital flow between disparate risk

baskets, especially equities, while is possible, has a low

probability in our view.

Nonetheless, with the hike, U.S. treasuries will become

attractive and will strengthen the U.S. dollar. Hence,

India’s exports may benefit with a weaker rupee, though

imports may become dearer.

Easy liquidity regime to continue with stable EU and

Japan improving marginally: Manufacturing in the

Eurozone is growing at its fastest pace since at least

2014. Demand for metals in Europe is picking up on

account of rising demand from the construction and

automotive sectors.

Japanese inflation unexpectedly sped up in November

2017 to 0.9% (better than estimates) even though the rate

is less than ~2% rate targeted by central bank. However,

the unemployment rate fell to 2.7%, while household

spending increased 1.7% from a year ago. The job-to-

applicant ratio rose to 1.56, the highest since mid-1970s.

LME price chart of key commodities

Source: Bloomberg, Sharekhan Research

2000

3000

4000

5000

6000

7000

8000

Dec

-16

Jan-

17

Feb-

17

Mar

-17

Apr

-17

May

-17

Jun-

17

Jul-1

7

Aug

-17

Sep

-17

Oct

-17

Nov

-17

Dec

-17

AL ($/2MT) CU ($/MT) Zinc ($/2MT)

EQUITY FUNDAMENTALSMARKET OUTLOOK

10January 2018 Sharekhan ValueGuide

Sharekhan Limited, its analyst or dependant(s) of the analyst might be holding or having a position in the companies mentioned in the article.

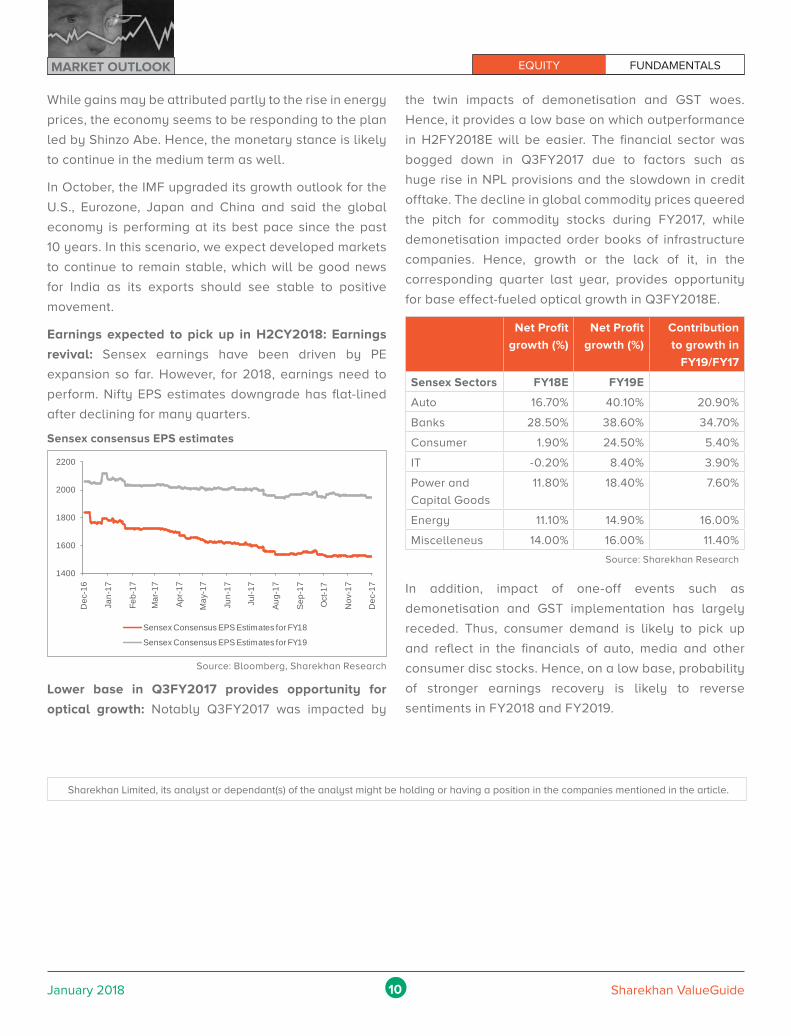

Sensex consensus EPS estimates

1400

1600

1800

2000

2200

Dec

-16

Jan-

17

Feb-

17

Mar

-17

Apr

-17

May

-17

Jun-

17

Jul -1

7

Aug

-17

Sep

-17

Oct

-17

Nov

-17

Dec

-17

Sensex Consensus EPS Estimates for FY18

Sensex Consensus EPS Estimates for FY19

Source: Bloomberg, Sharekhan Research

While gains may be attributed partly to the rise in energy

prices, the economy seems to be responding to the plan

led by Shinzo Abe. Hence, the monetary stance is likely

to continue in the medium term as well.

In October, the IMF upgraded its growth outlook for the

U.S., Eurozone, Japan and China and said the global

economy is performing at its best pace since the past

10 years. In this scenario, we expect developed markets

to continue to remain stable, which will be good news

for India as its exports should see stable to positive

movement.

Earnings expected to pick up in H2CY2018: Earnings

revival: Sensex earnings have been driven by PE

expansion so far. However, for 2018, earnings need to

perform. Nifty EPS estimates downgrade has flat-lined

after declining for many quarters.

the twin impacts of demonetisation and GST woes.

Hence, it provides a low base on which outperformance

in H2FY2018E will be easier. The financial sector was

bogged down in Q3FY2017 due to factors such as

huge rise in NPL provisions and the slowdown in credit

offtake. The decline in global commodity prices queered

the pitch for commodity stocks during FY2017, while

demonetisation impacted order books of infrastructure

companies. Hence, growth or the lack of it, in the

corresponding quarter last year, provides opportunity

for base effect-fueled optical growth in Q3FY2018E.

Net Profit

growth (%)

Net Profit

growth (%)

Contribution

to growth in

FY19/FY17

Sensex Sectors FY18E FY19E

Auto 16.70% 40.10% 20.90%

Banks 28.50% 38.60% 34.70%

Consumer 1.90% 24.50% 5.40%

IT -0.20% 8.40% 3.90%

Power and

Capital Goods

11.80% 18.40% 7.60%

Energy 11.10% 14.90% 16.00%

Miscelleneus 14.00% 16.00% 11.40%

Source: Sharekhan Research

In addition, impact of one-off events such as

demonetisation and GST implementation has largely

receded. Thus, consumer demand is likely to pick up

and reflect in the financials of auto, media and other

consumer disc stocks. Hence, on a low base, probability

of stronger earnings recovery is likely to reverse

sentiments in FY2018 and FY2019.

Lower base in Q3FY2017 provides opportunity for

optical growth: Notably Q3FY2017 was impacted by

EQUITY FUNDAMENTALS Sharekhan Top Picks

11January 2018 Sharekhan ValueGuide

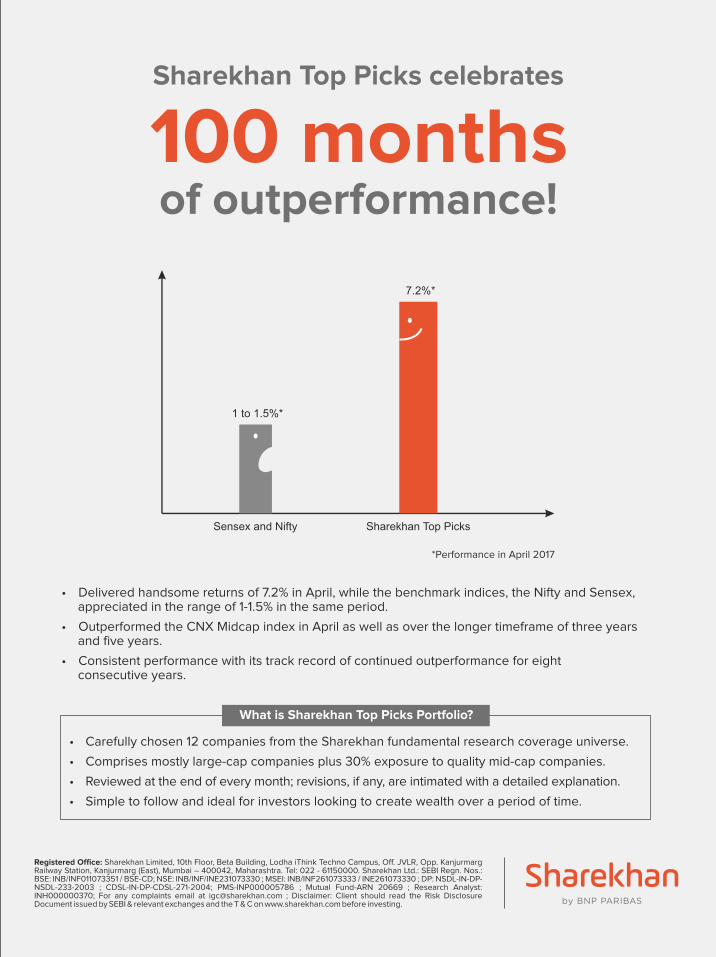

Sharekhan Top Picks9-in-9! Yes, the money invested in the Top Picks portfolio would have gone up by nine times over nine years, since its inception in January 2009. This works out to annualised average returns of 27.6% for the last nine years; as compared to returns of 14.5-15% in the Sensex/Nifty over the same period.

The unmatched and consistent track record clearly highlights the importance of making the right sector allocations along with superior stock selection to build a portfolio. Moreover, it bursts the myth that wealth creation or handsome returns can only be earned by dabbling into risky stocks and unknown companies. With a portfolio of large-sized quality companies in the Top Picks basket, we have shown that it is possible to earn handsome returns that are far higher than not only the Sensex/Nifty but also the CNX Midcap 100 index.

This month again, the Top Picks portfolio has given healthy returns of 4.2%, far ahead of 2.7% and 3.0% gains in Sensex and Nifty respectively. For the full year CY2017, the top picks portfolio

has appreciated by 58% much ahead of 28% and 29% gains in Sensex and Nifty respectively, during the same period.

We are suggesting two changes in the portfolio this month. We are replacing Bajaj Finserv and Powergrid Corp with Bharti Airtel and ONGC. The changes are in line with our views (as stated in the Market Outlook report, “Winds of Change”) that some of the laggards would lead the rally this year. For both ONGC and Bharti Airtel, the conditions are turning supportive of the growth of their businesses and the outlook appears much promising now.

Last month, we highlighted the fact that it is necessary to follow the monthly revisions in the Top Picks portfolio in a disciplined manner to harness the true potential of this superior investment product. And soon we would be graduating the product to an investment advisory platform, where a team of experience relationship managers would assist you with execution and other product-related clarifications. Watch out for more details on it soon. Wish you a Happy and a profitable New Year.

Consistent outperformance (absolute returns; not annualised) (%)

(%) 1 month 3 months 6 months 1 year 3 years 5 yearsSharekhan Top Picks 4.2 10.0 16.2 58.0 68.4 285.5Sensex 2.7 9.0 10.3 28.0 12.1 80.1Nifty 3.0 8.0 10.9 29.0 15.2 84.4CNX MIDCAP 100 6.2 17.8 19.2 47.3 40.9 180.3

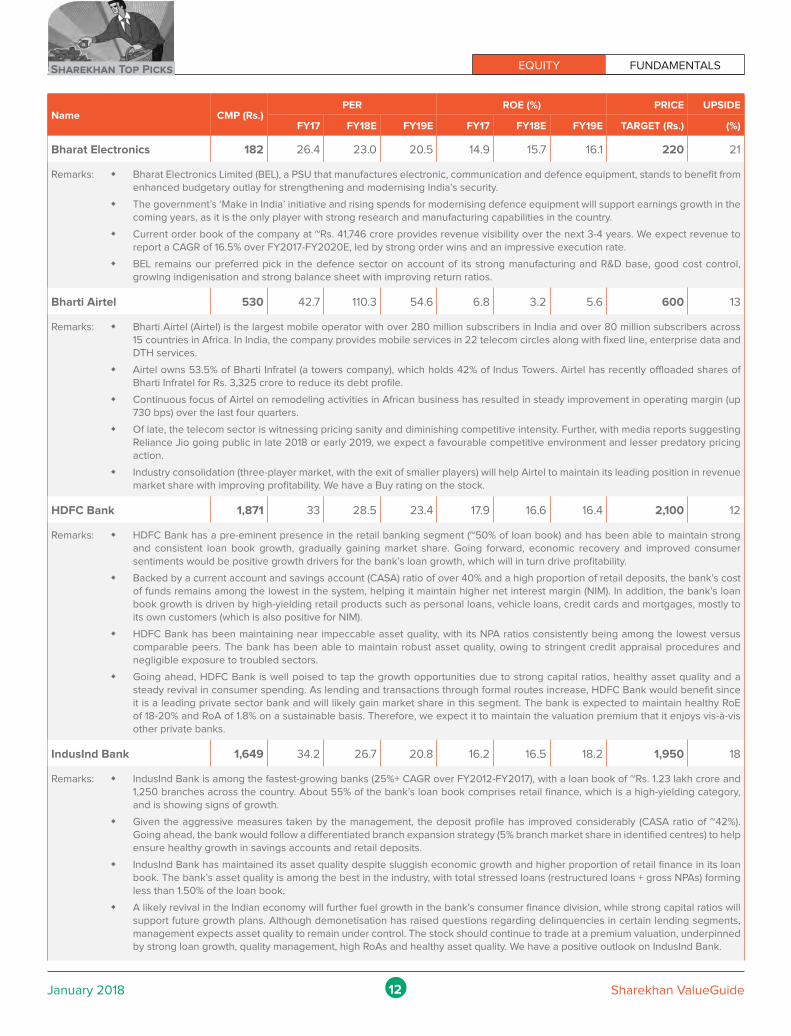

NameCMP*

(Rs)PER (x) RoE (%) Price

target (Rs)#Upside

(%)FY17 FY18E FY19E FY17 FY18E FY19E

Bharat Electronics 182 26.4 23.0 20.5 14.9 15.7 16.1 220 21

Bharti Airtel 530 42.7 110.3 54.6 6.8 3.2 5.6 600 13

HDFC Bank 1,871 33 28.5 23.4 17.9 16.6 16.4 2,100 12

IndusInd Bank 1,649 34.2 26.7 20.8 16.2 16.5 18.2 1,950 18

Jubilant FoodWorks 1,752 152.3 79.6 59.8 9.2 15.9 18.2 1,914 9

KEC International 384 32.3 23.6 18.4 21.2 23.3 24.2 ** -

Maruti Suzuki 9,731 40.1 34.0 28.3 21.0 20.7 20.6 ** -

ONGC Ltd 195 12.6 10.1 8.7 9.5 11.0 12.1 221 14

Reliance Industries 921 18.3 16.6 13.7 11.2 10.9 11.8 1,040 13

Sundram Fasteners 584 36.0 30.4 25.8 27.6 27.1 26.6 674 15

UPL Limited 762 21.3 18.8 15.2 27.2 25.0 25.4 980 29

ZEE Entertainment 586 46.1 42.4 32.4 18.3 17.3 19.4 650 11

*CMP as on December 29, 2017 # Price target for next 12 months ** Under review

Absolute returns (Top Picks Vs Benchmark indices) (%)

Sharekhan (Top Picks)

Sensex Nifty CNX Mid-cap 100

CY2017 58.0 28.0 29.0 47.3

CY2016 8.8 1.8 3.2 7.1

CY2015 13.9 -5.1 -4.1 6.5

CY2014 63.6 29.9 30.9 55.1

CY2013 12.4 8.5 6.4 -5.6

CY2012 35.1 26.2 29.0 36.0

CY2011 -20.5 -21.2 -21.7 -25.0

CY2010 16.8 11.5 12.9 11.5

CY2009 116.1 76.1 72.0 114.0

Constantly beating Nifty and Sensex (cumulative returns since April 2009)

Please note the returns are based on the assumption that at the beginning of each month an equal amount was invested in each stock of the Top Picks basket

100200300400500600700800900

1000

Apr-0

9Au

g-09

Nov

-09

Mar

-10

Jul-1

0N

ov-1

0M

ar-1

1Ju

l-11

Oct

-11

Feb-

12Ju

n-12

Oct

-12

Feb-

13Ju

n-13

Oct

-13

Jan-

14M

ay-1

4Se

p-14

Jan-

15M

ay-1

5Se

p-15

Dec

-15

Apr-1

6Au

g-16

Dec

-16

Apr-1

7Au

g-17

Dec

-17

Sharekhan Sensex Nifty

Sharekhan Top Picks EQUITY FUNDAMENTALS

12January 2018 Sharekhan ValueGuide

Name CMP (Rs.)PER ROE (%) PRICE UPSIDE

FY17 FY18E FY19E FY17 FY18E FY19E TARGET (Rs.) (%)

Bharat Electronics 182 26.4 23.0 20.5 14.9 15.7 16.1 220 21

Remarks: � Bharat Electronics Limited (BEL), a PSU that manufactures electronic, communication and defence equipment, stands to benefit from enhanced budgetary outlay for strengthening and modernising India’s security.

� The government’s ‘Make in India’ initiative and rising spends for modernising defence equipment will support earnings growth in the coming years, as it is the only player with strong research and manufacturing capabilities in the country.

� Current order book of the company at ~Rs. 41,746 crore provides revenue visibility over the next 3-4 years. We expect revenue to report a CAGR of 16.5% over FY2017-FY2020E, led by strong order wins and an impressive execution rate.

� BEL remains our preferred pick in the defence sector on account of its strong manufacturing and R&D base, good cost control, growing indigenisation and strong balance sheet with improving return ratios.

Bharti Airtel 530 42.7 110.3 54.6 6.8 3.2 5.6 600 13

Remarks: � Bharti Airtel (Airtel) is the largest mobile operator with over 280 million subscribers in India and over 80 million subscribers across 15 countries in Africa. In India, the company provides mobile services in 22 telecom circles along with fixed line, enterprise data and DTH services.

� Airtel owns 53.5% of Bharti Infratel (a towers company), which holds 42% of Indus Towers. Airtel has recently offloaded shares of Bharti Infratel for Rs. 3,325 crore to reduce its debt profile.

� Continuous focus of Airtel on remodeling activities in African business has resulted in steady improvement in operating margin (up 730 bps) over the last four quarters.

� Of late, the telecom sector is witnessing pricing sanity and diminishing competitive intensity. Further, with media reports suggesting Reliance Jio going public in late 2018 or early 2019, we expect a favourable competitive environment and lesser predatory pricing action.

� Industry consolidation (three-player market, with the exit of smaller players) will help Airtel to maintain its leading position in revenue market share with improving profitability. We have a Buy rating on the stock.

HDFC Bank 1,871 33 28.5 23.4 17.9 16.6 16.4 2,100 12

Remarks: � HDFC Bank has a pre-eminent presence in the retail banking segment (~50% of loan book) and has been able to maintain strong and consistent loan book growth, gradually gaining market share. Going forward, economic recovery and improved consumer sentiments would be positive growth drivers for the bank’s loan growth, which will in turn drive profitability.

� Backed by a current account and savings account (CASA) ratio of over 40% and a high proportion of retail deposits, the bank’s cost of funds remains among the lowest in the system, helping it maintain higher net interest margin (NIM). In addition, the bank’s loan book growth is driven by high-yielding retail products such as personal loans, vehicle loans, credit cards and mortgages, mostly to its own customers (which is also positive for NIM).

� HDFC Bank has been maintaining near impeccable asset quality, with its NPA ratios consistently being among the lowest versus comparable peers. The bank has been able to maintain robust asset quality, owing to stringent credit appraisal procedures and negligible exposure to troubled sectors.

� Going ahead, HDFC Bank is well poised to tap the growth opportunities due to strong capital ratios, healthy asset quality and a steady revival in consumer spending. As lending and transactions through formal routes increase, HDFC Bank would benefit since it is a leading private sector bank and will likely gain market share in this segment. The bank is expected to maintain healthy RoE of 18-20% and RoA of 1.8% on a sustainable basis. Therefore, we expect it to maintain the valuation premium that it enjoys vis-à-vis other private banks.

IndusInd Bank 1,649 34.2 26.7 20.8 16.2 16.5 18.2 1,950 18

Remarks: � IndusInd Bank is among the fastest-growing banks (25%+ CAGR over FY2012-FY2017), with a loan book of ~Rs. 1.23 lakh crore and 1,250 branches across the country. About 55% of the bank’s loan book comprises retail finance, which is a high-yielding category, and is showing signs of growth.

� Given the aggressive measures taken by the management, the deposit profile has improved considerably (CASA ratio of ~42%). Going ahead, the bank would follow a differentiated branch expansion strategy (5% branch market share in identified centres) to help ensure healthy growth in savings accounts and retail deposits.

� IndusInd Bank has maintained its asset quality despite sluggish economic growth and higher proportion of retail finance in its loan book. The bank’s asset quality is among the best in the industry, with total stressed loans (restructured loans + gross NPAs) forming less than 1.50% of the loan book.

� A likely revival in the Indian economy will further fuel growth in the bank’s consumer finance division, while strong capital ratios will support future growth plans. Although demonetisation has raised questions regarding delinquencies in certain lending segments, management expects asset quality to remain under control. The stock should continue to trade at a premium valuation, underpinned by strong loan growth, quality management, high RoAs and healthy asset quality. We have a positive outlook on IndusInd Bank.

EQUITY FUNDAMENTALS Sharekhan Top Picks

13January 2018 Sharekhan ValueGuide

Name CMP (Rs.)PER ROE (%) PRICE UPSIDE

FY17 FY18E FY19E FY17 FY18E FY19E TARGET (Rs.) (%)

Jubilant Food- Works 1,752 152.3 79.6 59.8 9.2 15.9 18.2 1914 9

Remarks: � Jubilant FoodWorks Limited (JFL), India’s largest food service company, shifted its focus to customer satisfaction from store additions

to improve its store fundamentals over the long run.

� Post the induction of Mr. Pratik Pota as the CEO, the company refreshed its menu by launching new items and improving the quality of

its pizzas with better offerings. The company gained good traction and posted same-store-sales growth (SSSG) of 5.5% in Q2FY2018

(6.5% in Q1FY2018), as against a decline in SSSG in earlier quarters.

� Operating profit margin (OPM) improved by 440 bps in Q2FY2018 to 14% (highest in the last 14 quarters). JFL is also focusing on

reducing losses of Dunkin Donuts by shutting non-profitable stores and introducing value product portfolio to improve store sales in

the coming quarters. We expect standalone OPM to improve to ~14% in FY2020 from 9.7% in FY2017.

� With negative working capital, the company’s balance sheet remained lean amid slowing SSSG and sustained store additions.

� JFL would be one of the key beneficiaries of improvement in the discretionary environment in the domestic market. With a redefined

strategy, revenue and earnings of JFL are expected to report CAGRs of 12% and 47%, respectively, over FY2017-FY2020.

KEC International 384 32.3 23.6 18.4 21.2 23.3 24.2 ** -

Remarks: � KEC International (KEC) is a global power transmission infrastructure EPC major. The company is present in verticals such as power

transmission and distribution (T&D), cables, railways, water, renewable (solar energy) and civil.

� Globally, the company has powered infrastructure development in more than 61 countries. KEC is a leader in power transmission EPC

projects and has more than seven decades of experience.

� Management sounded very confident of delivering growth across all verticals such as T&D, railways, solar and cables. Management

is banking on state transmission companies, private sector under tariff-based competitive bidding (TBCB) route and overseas

geographies for growth in the T&D segment.

� Management expects the railway business to grow ~80% y-o-y to ~Rs. 800 crore and solar EPC business to grow by over 3x to ~Rs.

500 crore in FY2018. KEC is witnessing improved revenue mix with the execution of extra high voltage (EHV) cables, which have

better profitability.

� Over the years, KEC has grown through the organic as well as inorganic route. Going forward, we estimate the company’s OPM to

expand to 10% compared to 9.5% currently. Debt/equity (D/E) ratio is expected to improve to 0.4:1 by the end of FY2020E from 1.3:1

in FY2017.

� We expect earnings to report a CAGR of 29% during FY2017E-FY2020E, with strong cash flows and a leaner balance sheet. Thus,

we retain our positive outlook on the stock.

Maruti Suzuki 9,731 40.1 34.0 28.3 21.0 20.7 20.6 ** -

Remarks: � Maruti Suzuki India Limited (MSIL) is India’s largest passenger vehicle (PV) manufacturer with a strong 47% market share. Over the

past two years, the company has been able to gain market share due to new product launches, a vast distribution network (with

increased focus on rural markets) and a shift in consumer preference to petrol models from diesel models.

� The recently launched premium hatchback, Baleno, Ignis and upgrade of Dzire have received strong response, which will help MSIL

to expand its market share in the segment. MSIL is likely to continue outpacing industry growth as four of its models (Baleno, Brezza,

Ignis and Dzire), which form 37% of its vehicle portfolio, command a waiting period of 2-5 months.

� The parent company of MSIL, Suzuki Motor Corporation, commissioned its Greenfield plant in Gujarat in February 2017. Maruti Suzuki

India Limited (MSIL) is ramping capacity in Gujarat, with production expected to double to 20,000 units per month by Q4FY2018

as against the current rate of 10,000 units per month. With capacity for the first line expected to be reached by the end of FY2018,

MSIL has commenced work on operating the second line, which has installed capacity of 2.5 lakh units. MSIL expects to reach the

full capacity of 7.5 lakh units at Gujarat by 2020. Enhanced production in Gujarat will ease capacity constraints and help MSIL to

reduce waiting periods for its models. we expect MSIL to outpace the industry and expect volumes to post a 12% CAGR over FY2018-

FY2020 as against industry growth of about 10%.

� MSIL has recently announced price hikes of up to 2% to tide over input cost increases, effective January 2018. Moreover, increased

sales of products having robust waiting period coupled with planned launches would result in lower discounting for MSIL, which

would augment margins. Further a favorable currency position would aid margin improvement. We believe the above factors will

offset the margin impact on account of increased proportion of traded products and would enable MSIL to sustain higher margins

of 15-16%.

� We have introduced FY2020 estimates in this note. A better-than expected industry growth will justify premium multiples for MSIL.

We retain our Buy rating on the stock.

Sharekhan Top Picks EQUITY FUNDAMENTALS

14January 2018 Sharekhan ValueGuide

Name CMP (Rs.)PER ROE (%) PRICE UPSIDE

FY17 FY18E FY19E FY17 FY18E FY19E TARGET (Rs.) (%)

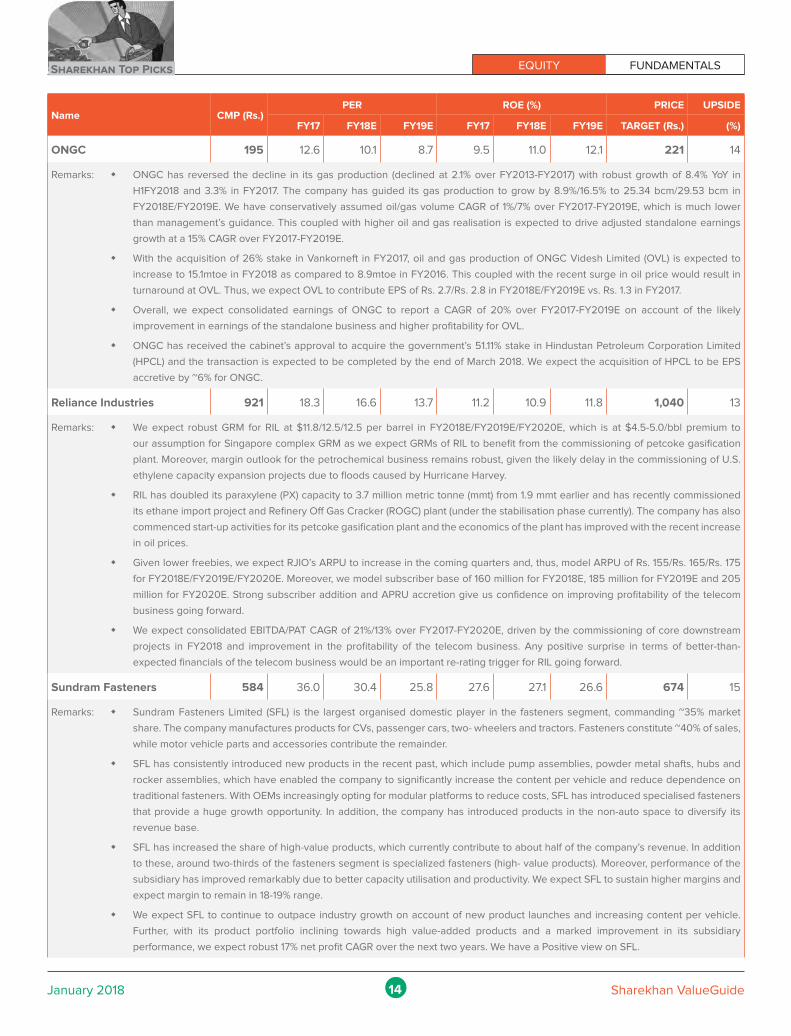

ONGC 195 12.6 10.1 8.7 9.5 11.0 12.1 221 14

Remarks: � ONGC has reversed the decline in its gas production (declined at 2.1% over FY2013-FY2017) with robust growth of 8.4% YoY in

H1FY2018 and 3.3% in FY2017. The company has guided its gas production to grow by 8.9%/16.5% to 25.34 bcm/29.53 bcm in

FY2018E/FY2019E. We have conservatively assumed oil/gas volume CAGR of 1%/7% over FY2017-FY2019E, which is much lower

than management’s guidance. This coupled with higher oil and gas realisation is expected to drive adjusted standalone earnings

growth at a 15% CAGR over FY2017-FY2019E.

� With the acquisition of 26% stake in Vankorneft in FY2017, oil and gas production of ONGC Videsh Limited (OVL) is expected to

increase to 15.1mtoe in FY2018 as compared to 8.9mtoe in FY2016. This coupled with the recent surge in oil price would result in

turnaround at OVL. Thus, we expect OVL to contribute EPS of Rs. 2.7/Rs. 2.8 in FY2018E/FY2019E vs. Rs. 1.3 in FY2017.

� Overall, we expect consolidated earnings of ONGC to report a CAGR of 20% over FY2017-FY2019E on account of the likely

improvement in earnings of the standalone business and higher profitability for OVL.

� ONGC has received the cabinet’s approval to acquire the government’s 51.11% stake in Hindustan Petroleum Corporation Limited

(HPCL) and the transaction is expected to be completed by the end of March 2018. We expect the acquisition of HPCL to be EPS

accretive by ~6% for ONGC.

Reliance Industries 921 18.3 16.6 13.7 11.2 10.9 11.8 1,040 13

Remarks: � We expect robust GRM for RIL at $11.8/12.5/12.5 per barrel in FY2018E/FY2019E/FY2020E, which is at $4.5-5.0/bbl premium to

our assumption for Singapore complex GRM as we expect GRMs of RIL to benefit from the commissioning of petcoke gasification

plant. Moreover, margin outlook for the petrochemical business remains robust, given the likely delay in the commissioning of U.S.

ethylene capacity expansion projects due to floods caused by Hurricane Harvey.

� RIL has doubled its paraxylene (PX) capacity to 3.7 million metric tonne (mmt) from 1.9 mmt earlier and has recently commissioned

its ethane import project and Refinery Off Gas Cracker (ROGC) plant (under the stabilisation phase currently). The company has also

commenced start-up activities for its petcoke gasification plant and the economics of the plant has improved with the recent increase

in oil prices.

� Given lower freebies, we expect RJIO’s ARPU to increase in the coming quarters and, thus, model ARPU of Rs. 155/Rs. 165/Rs. 175

for FY2018E/FY2019E/FY2020E. Moreover, we model subscriber base of 160 million for FY2018E, 185 million for FY2019E and 205

million for FY2020E. Strong subscriber addition and APRU accretion give us confidence on improving profitability of the telecom

business going forward.

� We expect consolidated EBITDA/PAT CAGR of 21%/13% over FY2017-FY2020E, driven by the commissioning of core downstream

projects in FY2018 and improvement in the profitability of the telecom business. Any positive surprise in terms of better-than-

expected financials of the telecom business would be an important re-rating trigger for RIL going forward.

Sundram Fasteners 584 36.0 30.4 25.8 27.6 27.1 26.6 674 15

Remarks: � Sundram Fasteners Limited (SFL) is the largest organised domestic player in the fasteners segment, commanding ~35% market

share. The company manufactures products for CVs, passenger cars, two- wheelers and tractors. Fasteners constitute ~40% of sales,

while motor vehicle parts and accessories contribute the remainder.

� SFL has consistently introduced new products in the recent past, which include pump assemblies, powder metal shafts, hubs and

rocker assemblies, which have enabled the company to significantly increase the content per vehicle and reduce dependence on

traditional fasteners. With OEMs increasingly opting for modular platforms to reduce costs, SFL has introduced specialised fasteners

that provide a huge growth opportunity. In addition, the company has introduced products in the non-auto space to diversify its

revenue base.

� SFL has increased the share of high-value products, which currently contribute to about half of the company’s revenue. In addition

to these, around two-thirds of the fasteners segment is specialized fasteners (high- value products). Moreover, performance of the

subsidiary has improved remarkably due to better capacity utilisation and productivity. We expect SFL to sustain higher margins and

expect margin to remain in 18-19% range.

� We expect SFL to continue to outpace industry growth on account of new product launches and increasing content per vehicle.

Further, with its product portfolio inclining towards high value-added products and a marked improvement in its subsidiary

performance, we expect robust 17% net profit CAGR over the next two years. We have a Positive view on SFL.

EQUITY FUNDAMENTALS Sharekhan Top Picks

15January 2018 Sharekhan ValueGuide

Name CMP (Rs.)PER ROE (%) PRICE UPSIDE

FY17 FY18E FY19E FY17 FY18E FY19E TARGET (Rs.) (%)

UPL Limited 762 21.3 18.8 15.2 27.2 25.0 25.4 980 29

Remarks: � United Phosphorous Limited (UPL) is a global generic crop protection chemicals and seeds company. UPL is the largest producer

of agrochemicals in India. The company is among the top five post-patent agrochemical manufacturers in the world. UPL has ~23

manufacturing sites, including nine in India, four in France and two in Spain. The company operates in every continent and has a

customer base in 123 countries with its own subsidiary offices.

� Management of UPL is confident of the long-term growth prospects such as 1) introduction of new products, at least two per year; 2)

improving innovation turnover index; 3) partnership with Bayer in Brazil; and 4) strong distribution network. However, FY2018E seems

to be on the softer side than anticipated earlier owing to the increase in inventory situation in Brazil, currency fluctuation and erratic

weather conditions. These will not have a major impact on long-term prospects.

� Management has guided for 8-12% growth in overall revenue on a reported basis. Constant currency growth will be still 12-15% along

with a 50-75 bps expansion in EBITDA margin in FY2018. Management also expects acceleration in growth in H2FY2018 versus

H1FY2018, owing to a late season pickup in Latin America.

� Owing to continuous product launches, UPL has managed to increase its innovation rate from 5% in FY2015 to 15% in FY2017 (it was

14% in FY2016).

� A positive outlook for geographies such as India, Europe and Latin America would also drive revenue growth going ahead. Further,

patent expiry of significant agrochemicals, the value of which is pegged at ~$4 billion over the next three years, augurs well for UPL

to leverage the opportunity.

� We see concerns around growth are overdone and believe management’s guidance for FY2018 topline growth can be comfortably

achieved on account of its strong product portfolio, new product introductions and improved demand outlook. We maintain our Buy

rating on the stock.

ZEE Entertainment 586 46.1 42.4 32.4 18.3 17.3 19.4 650 11

Remarks: � Zee Entertainment Enterprises Limited (ZEEL) continues to lead the broadcasting industry in terms of growth in advertising revenue.

ZEEL is one of the leading players in television broadcasting with a bouquet of 34+ TV channels across genres.

� ZEEL expects domestic subscriptions to grow at a low-teen CAGR for the next 3-4 years. However, the ongoing litigation on TRAI’s

tariff order is causing a delay in contract renewal negotiations with distributors.

� ZEEL expects advertisement revenue growth to be in mid-teens during H2FY2018E, as it expects clients across sectors to spend

more on advertising. Programming hours in its flagship channel, Zee TV, have reached 30 hours with new slot opening on weekends.

� ZEEL will unveil its OTT 2.0 ZEE5 (replace its current advertising video-on-demand (AVOD)-based OZEE and subscription video-

on-demand (SVOD)-based Ditto TV) in the next three months. Management expects margins to remain at around 30%+, even after

increasing programming cost in digital content.

� We continue to remain positive on ZEEL, as it is a structural India consumption theme. Moreover, the company continues to invest

across the media spectrum, including movies, music, events, digital and international markets, to maintain its high-growth trajectory.

We maintain our Buy rating on the stock.

EQUITY FUNDAMENTALSStock Update

16January 2018 Sharekhan ValueGuide

Date Company Report TypeRecommendation

Reco PricePrice Target/ Upside (%)

Latest Chg Latest Chg

Dec 01, 2017 Infosys Stock Update HOLD 1 959 1,000 1

Summary

• Infosys has kicked off the buyback of up to 11.3 crore equity shares (4.9% of its outstanding share) at Rs. 1,150 per share. It closes

on December 14, 2017.

• Rs. 13,000 crore share buyback represents 31% of the company’s Rs. 41,392 crore cash balance (Q2FY2018) and around 18%

of the net worth (Q2FY2018).

• The entitlement ratio for reserved shareholders stands at 23 shares out of 81 shares held as on record date i.e., November 1,

2017, implies 28.4%.

• We advise investors to tender their shares in the buyback offer owing to lack of clarity on CEO appointment and absence of any

growth triggers in the near-to-medium term.

Report link: http://old.sharekhan.com/Upload/NewsLetter/Infosys-Dec01_17.pdf

Dec 01, 2017 Carborundum Universal Limited Viewpoint POSITIVENew

Initiation380 15-18% -

Summary

• Ramping up of capacity and new product launch to drive volumes of Carborundum Universal Limited (CUMI).

• Operating leverage to play out post stabilisation of all capacities.

• Strong balance sheet and steady positive free cash flow to enable CUMI generate healthy return ratios going ahead.

• We initiate a Positive viewpoint on CUMI with 15-18% upside in the next 12-15 months.

Report link: http://old.sharekhan.com/Upload/NewsLetter/Carborundum-Dec01_17.pdf

Dec 04, 2017 Persistent Systems Stock Update HOLD 1 653 720 1

Summary

• Management of Persistent Systems’ (PSL) demonstrates its digital competencies through multiple live demos/sessions.

• Though the IBM IoT product is doing well, the management acknowledged that the IBM IoT product deal has failed to deliver

the desired results given higher complexity. It expects the recent reseller agreement will drive growth in FY2019.

• PSL is hopeful the newly launched products likely gain traction among customers and the repeat sales of its in-house digital

solutions would improve profitability.

• Given lack of any medium-term triggers for margin recoveries, we maintain our Hold rating on the stock with price target (PT)

of Rs.720.

Report link: http://old.sharekhan.com/Upload/NewsLetter/Persistentsyst-Dec04_17.pdf

Dec 04, 2017 Biocon Limited Viewpoint POSITIVE 1 514 10-12% h

Summary

• USFDA approves first biosimilar trastuzumab (the first biosimilar from the joint portfolio of Biocon and Mylan), which led to a

sharp jump in the stock price of Biocon.

• We expect Biocon to report sales and profit CAGR of 18.5% and 25%, respectively, over the next four years.

• We maintain our Positive view on the stock with additional upside of 10-12% returns over the next six months, as Biocon and

Mylan will have first-mover advantage.

Report link: http://old.sharekhan.com/Upload/NewsLetter/Biocon-Dec04_17.pdf

� Upgrade � No change � Downgrade

� Note: The arrow indicates change in call and price target, if any, vis-à-vis the previous report

EQUITY FUNDAMENTALS Stock Update

17January 2018 Sharekhan ValueGuide

Date Company Report TypeRecommendation

Reco PricePrice Target/ Upside (%)

Latest Chg Latest Chg

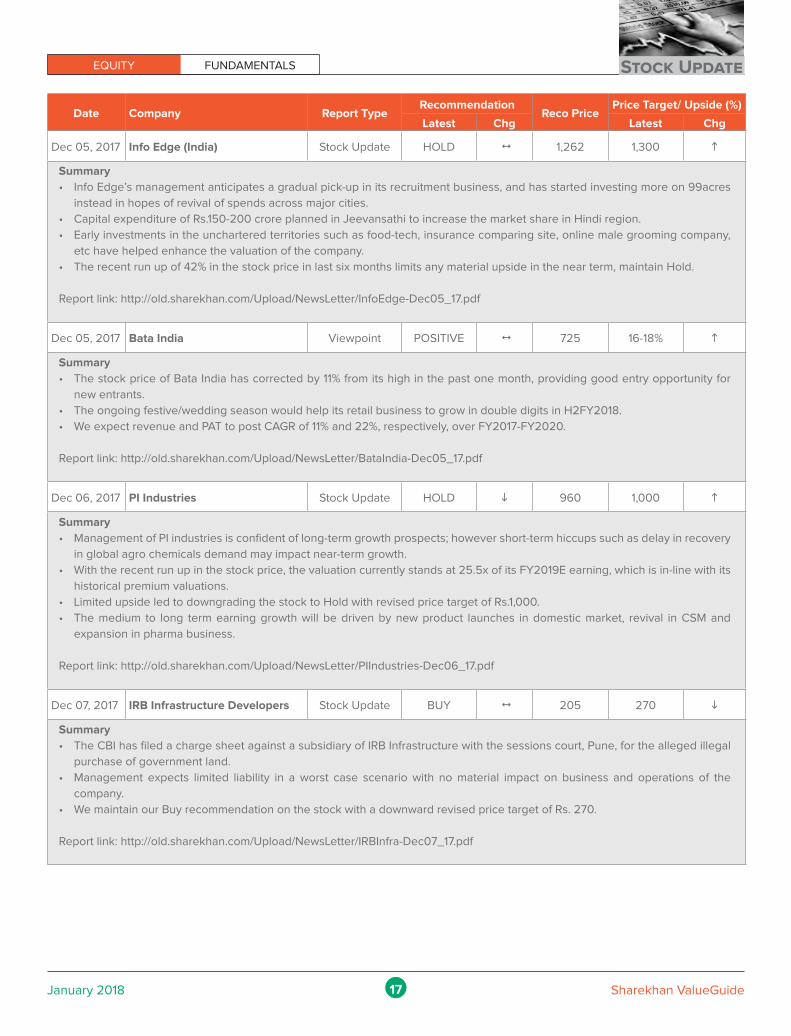

Dec 05, 2017 Info Edge (India) Stock Update HOLD 1 1,262 1,300 h

Summary

• Info Edge’s management anticipates a gradual pick-up in its recruitment business, and has started investing more on 99acres

instead in hopes of revival of spends across major cities.

• Capital expenditure of Rs.150-200 crore planned in Jeevansathi to increase the market share in Hindi region.

• Early investments in the unchartered territories such as food-tech, insurance comparing site, online male grooming company,

etc have helped enhance the valuation of the company.

• The recent run up of 42% in the stock price in last six months limits any material upside in the near term, maintain Hold.

Report link: http://old.sharekhan.com/Upload/NewsLetter/InfoEdge-Dec05_17.pdf

Dec 05, 2017 Bata India Viewpoint POSITIVE 1 725 16-18% h

Summary

• The stock price of Bata India has corrected by 11% from its high in the past one month, providing good entry opportunity for

new entrants.

• The ongoing festive/wedding season would help its retail business to grow in double digits in H2FY2018.

• We expect revenue and PAT to post CAGR of 11% and 22%, respectively, over FY2017-FY2020.

Report link: http://old.sharekhan.com/Upload/NewsLetter/BataIndia-Dec05_17.pdf

Dec 06, 2017 PI Industries Stock Update HOLD i 960 1,000 h

Summary

• Management of PI industries is confident of long-term growth prospects; however short-term hiccups such as delay in recovery

in global agro chemicals demand may impact near-term growth.

• With the recent run up in the stock price, the valuation currently stands at 25.5x of its FY2019E earning, which is in-line with its

historical premium valuations.

• Limited upside led to downgrading the stock to Hold with revised price target of Rs.1,000.

• The medium to long term earning growth will be driven by new product launches in domestic market, revival in CSM and

expansion in pharma business.

Report link: http://old.sharekhan.com/Upload/NewsLetter/PIIndustries-Dec06_17.pdf

Dec 07, 2017 IRB Infrastructure Developers Stock Update BUY 1 205 270 i

Summary

• The CBI has filed a charge sheet against a subsidiary of IRB Infrastructure with the sessions court, Pune, for the alleged illegal

purchase of government land.

• Management expects limited liability in a worst case scenario with no material impact on business and operations of the

company.

• We maintain our Buy recommendation on the stock with a downward revised price target of Rs. 270.

Report link: http://old.sharekhan.com/Upload/NewsLetter/IRBInfra-Dec07_17.pdf

EQUITY FUNDAMENTALSStock Update

18January 2018 Sharekhan ValueGuide

Date Company Report TypeRecommendation

Reco PricePrice Target/ Upside (%)

Latest Chg Latest Chg

Dec 07, 2017 ION Exchange Viewpoint POSITIVENew

Initiation420 15-20% -

Summary

• Execution begins on sizeable water supply project of Rs. 1250 crore by the engineering division of ION Exchange.

• Visible shift from private sector to Municipal projects for providing water management solutions enhances addressable market,

engineering division a clear winner with order book of Rs. 500 crore.

• Earnings expected to compound at 26% over same time-frame. We thus initiate a positive view on the stock and expect a 15-

20% upside over the next 6-8 months.

Report link: http://old.sharekhan.com/Upload/NewsLetter/IONExchange-Dec07_17.pdf

Dec 08, 2017 Federal Bank Stock Update BUY 1 109 145 1

Summary

• A multi-channel business approach to target corporate, SME and retail loans through its existing leads to growth traction in its

loan book . Corporate loan book surges up by 38% yoy.

• The bank plans for a vertical expansion in its operational domain by foraying into the mutual fund and/or microfinance business.

• Federal Bank is also planning to divest 26% stake in its wholly owned subsidiary FedBank Financial Services In an event of

successful divestment, Federal Bank would witness a boost in its capital adequacy, without equity dilution, which will be a

positive.

• Since our last report dated (October 16, 2017) the stock price has corrected by 12.0% which we believe provides a good

opportunity to add for better gains, given the various positives stated above.

Report link: http://old.sharekhan.com/Upload/NewsLetter/FederalBank-Dec08_17.pdf

Dec 11, 2017 Dabur India Viewpoint POSITIVENew

Initiation350 16-18% -

Summary

• Dabur India Ltd (Dabur) is a trusted brand with strong footing in natural healthcare products and presence in low penetrated

categories.

• A pick up in rural demand (contributes ~50% of total revenues) would aid in improving the domestic business volume growth.

• One of the stable balance sheets amongst the peers with healthy dividend payout of ~40%.

• We have positive view on the stock with 16-18% upside from the current levels.

Report link: http://old.sharekhan.com/Upload/NewsLetter/DaburIndia-Dec11_17.pdf

Dec 12, 2017 Sadbhav Engineering Stock Update BUY 1 370 443 h

Summary

• Sadbhav Engineering to benefit as subsidiary Sadbhav Infrastructure Project Ltd (SIPL) has bagged new orders and received

appointed dates to commence construction.

• Company expects order inflow to the tune of Rs. 7,000 crore during FY2018 out of which it has already bagged Rs. 3,500 crore

during H1FY2018.

• The government’s approval for Rs. 7 lakh crore of highway projects is expected to yield significant opportunities for Sadbhav

Engineering.

• We maintain our Buy rating on the stock, with a higher PT of Rs. 443 given the company’s expertise in timely execution, focus

on improving balance sheet and generating higher cash flows.

Report link: http://old.sharekhan.com/Upload/NewsLetter/SadbhavEngg-Dec12_17.pdf

EQUITY FUNDAMENTALS Stock Update

19January 2018 Sharekhan ValueGuide

Date Company Report TypeRecommendation

Reco PricePrice Target/ Upside (%)

Latest Chg Latest Chg

Dec 12, 2017 Rico Auto Industries Stock Update BUY 1 95 130 h

Summary

• Rico Auto has secured project orders worth Rs. 1,900 crore, which is expected to boost topline.

• Margin expansion on cards given a better product mix; Company expects to reach 15% margins in the next 3-4 years .

• We expect PAT to clock a 39% CAGR over FY2018-FY2020.

• We maintain our Buy rating on the stock and raise our PT to Rs. 130.

Report link: http://old.sharekhan.com/Upload/NewsLetter/RicoAuto-Dec12_17.pdf

Dec 13, 2017 Bharti Airtel Stock Update BUY h 517 600 1

Summary

• Warburg Pincus to acquire up to 20% stake in Bharti Telemedia for $350 million.

• At EV of $2.1 billion, the implied valuation stands at 10.5x TTM EV/EBITDA, 9.8x FY2018E EV/EBITDA, 8.6x FY2019E EV/EBITDA

and 7.5x FY2020E EV/EBITDA.

• Continuous focus of Airtel on remodeling activities in African business has resulted in steady improvement in operating margins

(up 730 bps) over the last four quarters.

• Africa could be the trump card for future growth; hence, Airtel is consciously implementing strategies focusing on customer

retention.

• With favourable earnings traction in the African market and supportive sector tailwinds, we upgrade our rating from Hold to Buy

with an unchanged price target (PT) of Rs. 600.

Report link: http://old.sharekhan.com/Upload/NewsLetter/BhartiAirtel-Dec13_17.pdf

Dec 13, 2017 Oil and Natural Gas Corporation Viewpoint POSITIVENew

Initiation184 18-20% -

Summary

• Sharp correction in ONGC stock price in the past one year factors in all negatives.

• Acquisition of HPCL to be EPS accretive.

• Improving gas production, higher oil and gas realisation and turnaround of OVL to drive 20% consolidated earnings CAGR over

FY2017-FY2019E.

• Attractive valuation of 8.2x FY2019E EPS and high dividend yield provide comfort.

• We expect 18-20% upside from current levels.

Report link: http://old.sharekhan.com/Upload/NewsLetter/ONGC-Dec13_17.pdf

Dec 13, 2017 Natco Pharma Viewpoint POSITIVE 1 962 18-20% h

Summary

• Litigation over two US patents of gCopaxone against Mylan Inc, the marketing partner of Natco for in the US has been dropped

by Teva.

• This event reduces risk related to gCopaxone 40 mg and provides greater comfort and confidence in Mylan (thus, Natco’s)

ability to provide complex products as affordable treatment options.

• With this, Natco now has a first-mover advantage and the gCopaxone approval proves its ability to develop complex products.

• Natco sales and profitability are expected to grow at a three year compound annual growth rate (CAGR) of 34% and 45%,

respectively over FY2018-FY2020. Hence, we expect 18-20% upside in the stock over next six months.

Report link: http://old.sharekhan.com/Upload/NewsLetter/NatcoPharma-Dec13_17.pdf

EQUITY FUNDAMENTALSStock Update

20January 2018 Sharekhan ValueGuide

Date Company Report TypeRecommendation

Reco PricePrice Target/ Upside (%)

Latest Chg Latest Chg

Dec 14, 2017 Grasim Industries Stock Update BUY 1 1,141 1,380 i

Summary

• Grasim uses asset-light expansion arrangement for doubling VFY capacity.

• Growth prospects for the VFY business of Grasim have further improved with this proposed expansion.

• We maintain our Buy recommendation on the stock with a revised price target (PT) of Rs. 1,380.

Report link: http://old.sharekhan.com/Upload/NewsLetter/Grasim-Dec14_17.pdf

Dec 15, 2017 Maruti Suzuki Stock Update BUY 1 9,164 10,170 h

Summary

• Maruti Suzuki India Limited (MSIL) is ramping capacity in Gujarat, with production expected to double to 20,000 units per month

by Q4FY2018.

• Price hikes, lower discounting and favourable currency movement to sustain higher margins for MSIL.

• MSIL is set to continue outpacing industry growth.

• We retain our Buy rating on the stock with a price target (PT) of Rs.10,170.

Report link: http://old.sharekhan.com/Upload/NewsLetter/Maruti-Dec15_17.pdf

Dec 15, 2017 UPL Stock Update BUY 1 719 980 1

Summary

• Management is confident of long-term growth prospects such as introduction of new products, improving turnover index and

partnership with Bayer in Brazil.

• We believe management’s revised guidance for FY2018 topline growth can be comfortably achieved with better H2FY2018.

• The stock has corrected close to 15% in the past three months and is currently trading at reasonable valuation at 14.3x of

FY2019E earnings, which provides a good opportunity to invest at current levels. We maintain our Buy rating on the stock with

a PT of Rs.980.

Report link: http://old.sharekhan.com/Upload/NewsLetter/UPL-Dec15_17.pdf

Dec 18, 2017 Relaxo Footwear Stock Update HOLD i 697 735 h

Summary

• 25% run-up in Relaxo Footwear’s stock price (since our last update) on improving discretionary environment and expectation

of better H2FY2018.

• Due to the recent run-up in the stock price, we downgrade our rating from Buy to Hold, with a revised PT of Rs. 735.

• The company’s long-term growth prospects are intact as it will gain benefits from GST shift to branded products and improvement

in the discretionary environment.

Report link: http://old.sharekhan.com/Upload/NewsLetter/Relaxo-Dec18_17.pdf

EQUITY FUNDAMENTALS Stock Update

21January 2018 Sharekhan ValueGuide

Date Company Report TypeRecommendation

Reco PricePrice Target/ Upside (%)

Latest Chg Latest Chg

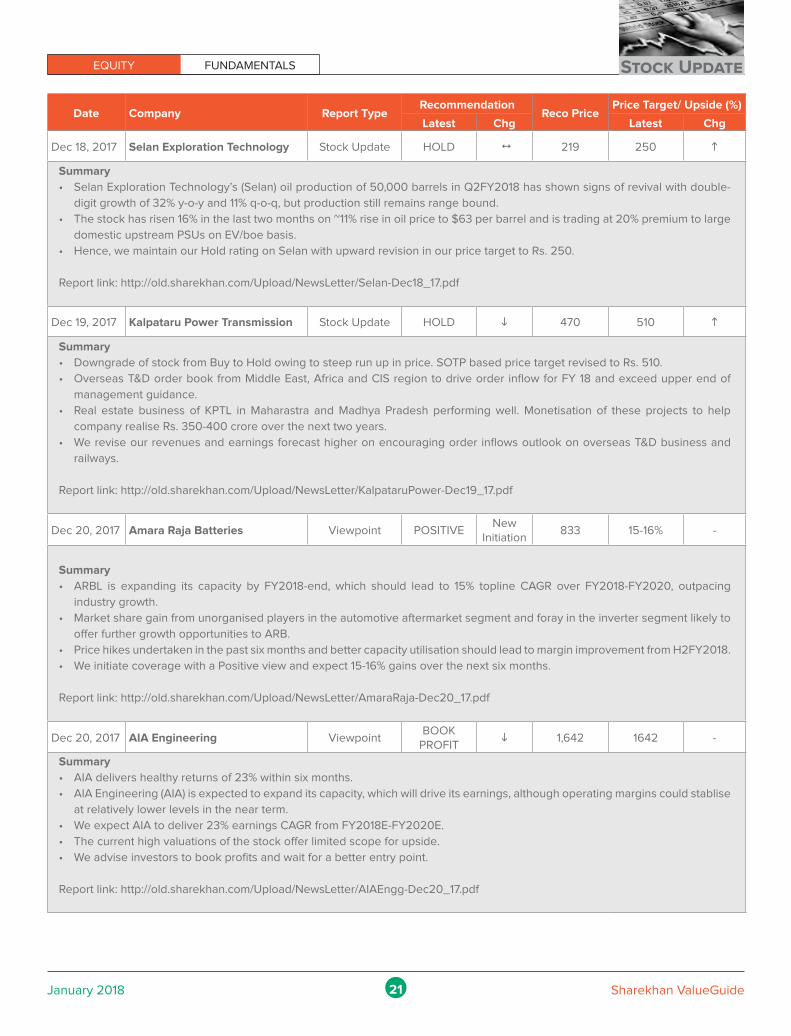

Dec 18, 2017 Selan Exploration Technology Stock Update HOLD 1 219 250 h

Summary

• Selan Exploration Technology’s (Selan) oil production of 50,000 barrels in Q2FY2018 has shown signs of revival with double-

digit growth of 32% y-o-y and 11% q-o-q, but production still remains range bound.

• The stock has risen 16% in the last two months on ~11% rise in oil price to $63 per barrel and is trading at 20% premium to large

domestic upstream PSUs on EV/boe basis.

• Hence, we maintain our Hold rating on Selan with upward revision in our price target to Rs. 250.

Report link: http://old.sharekhan.com/Upload/NewsLetter/Selan-Dec18_17.pdf

Dec 19, 2017 Kalpataru Power Transmission Stock Update HOLD i 470 510 h

Summary

• Downgrade of stock from Buy to Hold owing to steep run up in price. SOTP based price target revised to Rs. 510.

• Overseas T&D order book from Middle East, Africa and CIS region to drive order inflow for FY 18 and exceed upper end of