This booklet consists of two separate documents: INVESTMENT ADVISER’S LETTER TO SHAREHOLDERS - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - ANNUAL REPORT Tweedy, Browne Global Value Fund Tweedy, Browne Value Fund Tweedy, Browne Worldwide High DividendYield Value Fund MARCH 31, 2008 TWEEDY, BROWNE FUND INC.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

This booklet consists of two separate documents:

INVESTMENT ADVISER’S LETTERTO SHAREHOLDERS

- - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - -

ANNUAL REPORT

Tweedy, Browne Global Value FundTweedy, Browne Value Fund

Tweedy, Browne Worldwide High Dividend Yield Value Fund

MARCH 31, 2008

TWEEDY, BROWNE FUND INC.

TWEEDY, BROWNE FUND INC.

Investment Adviser’s Letter to Shareholders . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . I-1

Annual Report . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . II-1

Tweedy, Browne Fund Inc.Investment Adviser’s Note . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . II-2Expense Information . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . II-5

Tweedy, Browne Global Value FundPortfolio Highlights . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . II-6Perspective on Assessing Investment Results . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . II-7Portfolio of Investments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . II-8Sector Diversification . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . II-11Portfolio Composition . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . II-11Schedule of Forward Exchange Contracts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . II-12

Tweedy, Browne Value FundPortfolio Highlights . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . II-13Perspective on Assessing Investment Results . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . II-14Portfolio of Investments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . II-15Sector Diversification . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . II-16Portfolio Composition . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . II-16Schedule of Forward Exchange Contracts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . II-17

Tweedy, Browne Worldwide High Dividend Yield Value FundPortfolio Highlights . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . II-18Perspective on Assessing Investment Results . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . II-19Portfolio of Investments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . II-20Sector Diversification . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . II-21Portfolio Composition . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . II-21

Tweedy, Browne Fund Inc.Statements of Assets and Liabilities. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . II-22Statements of Operations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . II-23Statements of Changes in Net Assets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . II-24Financial Highlights . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . II-25Notes to Financial Statements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . II-27Investment in the Fund by the Investment Adviser and Related Parties . . . . . . . . . . . . . . . . . . . . . . . II-29Report of PricewaterhouseCoopers LLP, Independent Registered Public Accounting Firm . . . . . . . . . II-31Other Information . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . II-32

TWEEDY, BROWNE FUND INC.

Tweedy, Browne Global Value FundTweedy, Browne Value FundTweedy, Browne Worldwide High Dividend Yield Value Fund

INVESTMENT ADVISER’S LETTERTO SHAREHOLDERS

March 31, 2008

I-1

TWEEDY, BROWNE FUND INC.

Investment Adviser’s Letter

I-2

To Our Shareholders:We are pleased to present the Investment Adviser’s Letter

to Shareholders for the Tweedy, Browne Global Value Fund,Tweedy, Browne Value Fund and Tweedy, Browne WorldwideHigh Dividend Yield Value Fund for the year ended March 31,2008. Investment results* for the past six months and the lastone, three, five and ten years, and results since inception ofeach Fund are presented in the tables below:

Tweedy, Browne MSCI EAFE MSCI EAFE Period Ended Global Value Index Hedged Index3/31/08 Fund to US$(1)(2) in US$(1)(2)

6 Months -11.03% -17.55% -10.50%

1 Year -6.35 -14.05 -2.70

3 Years 9.32 10.07 13.32

5 Years 17.36 15.35 21.40

10 Years 8.68 3.63 6.18

Since Inception (6/15/93)(3) 11.86 6.76 7.35

Total Annual Fund Operating Expense Ratio as of 3/31/07 was 1.37%†

Total Annual Fund Operating Expense Ratio as of 3/31/08 was 1.37%†

MSCI WorldPeriod Ended Tweedy, Browne Index Hedged 3/31/08 Value Fund to US$(1)(4) S&P 500(1)(5)

6 Months -9.98% -14.57% -12.46%

1 Year -5.41 -9.22 -5.08

3 Years 4.01 N/A 5.84

5 Years 9.15 N/A 11.30

10 Years 3.93 N/A 3.50

Since Inception (12/8/93)(3) 9.52 N/A 9.53

Total Annual Fund Operating Expense Ratio as of 3/31/07 was 1.38%†

Total Annual Fund Operating Expense Ratio as of 3/31/08 was 1.37%†

Tweedy, Browne MSCI World Period Ended Worldwide High Dividend Index3/31/08 Yield Value Fund in US$(1)(4)

6 Months -3.85% -11.26%

Since Inception (9/5/07)(3) -2.69 -6.72

30-Day Standardized Yield as of 3/31/08: 2.90%

Gross Annual Operating Expense Ratio for current fiscal year ending

3/31/08 was 1.86%†‡

Net Annual Operating Expense Ratio for current fiscal year ending

3/31/08 was 1.37%†‡

* The preceding performance data represents past performance andis not a guarantee of future results. Total return and principalvalue of an investment will fluctuate so that an investor’s shares,when redeemed, may be worth more or less than their original cost.The returns shown do not reflect the deduction of taxes that ashareholder would pay on Fund distributions or the redemption ofFund shares. Current performance may be lower or higher thanthe performance data shown. Please visit www.tweedy.com toobtain performance data, which is current to the most recentmonth end. See pages I-9 and I-10 for footnotes 1 through 5,which describe the indices and inception dates of each Fund.Results are annualized for all periods greater than one year.

† The Funds do not impose any front-end or deferred sales charge.However, the Global Value Fund and the Worldwide HighDividend Yield Value Fund impose a 2% redemption fee onproceeds from redemptions or exchanges made within 60 days ofpurchase.

‡ The Adviser has contractually agreed to waive its investmentadvisory fee and/or to reimburse expenses of the WorldwideHigh Dividend Yield Value Fund to the extent necessary tomaintain the total annual fund operating expenses(excluding brokerage, interest, taxes and extraordinaryexpenses) at no more than 1.37%. This arrangement willcontinue at least through March 31, 2009. In thisarrangement, the Worldwide High Dividend Yield Value

Left to right: Will Browne, Bob Wyckoff, Chris Browne, Tom Shrager and John Spears.

I-3

Fund has agreed, during the two-year period following anywaiver or reimbursement by the Adviser, to repay suchamount to the extent that after giving effect to suchrepayment such adjusted total annual fund operatingexpenses would not exceed 1.37% on an annualized basis.The performance data shown above would be lower had feesand expenses not been waived and/or reimbursed.

The five-year old global bull market across virtually allasset classes came to a grinding halt last summer when two BearStearns-sponsored hedge funds that were invested in subprimemortgages collapsed, and Bear refused to come to the rescue.That, metaphorically, was the day the music died. The collapseof these funds signaled to financial markets that there wereserious problems in the mortgage markets, and ever since wehave all been reading the post mortems on how this allhappened, how extensive the damage might be, and who is toblame. Failure, of course, has a lot of fathers, and we are nodoubt about to see the start of the paternity suits in pursuit ofthe guilty. We are not in the business of finding guilty parties.We would rather focus on how we might benefit from thecurrent mess. What has been underestimated, in our judgment,is the magnitude of the bad credit, the ripple effect on othermarkets and the resulting crisis of confidence and uncertainty.This uncertainty has led to an unwillingness to provideliquidity at the old price levels, kicking off a series of problemsin leveraged balance sheets and portfolios – read Bear Stearnsand Peloton Partners among others. Leverage, as we all know,is great on the upside and deadly on the downside, and thecommon denominator in the markets’ troubles today is theunhappy combination of leverage and greed coupled with WallStreet’s ever-enabling creativity in packaging questionablecredits. The result has been an enormous financial super fundsite.

In previous letters, we warned of a “worrisome degree ofconfidence and complacency among investors fueled by cheapcredit, which in turn led to dramatic rises in many assetcategories and rampant speculation in stocks, bonds, real estateand commodities.” Major participants included banks,mortgage banks, investment banks, hedge funds and privateequity groups, many of which used large amounts of leverage(borrowed money) to supercharge their returns. Figurativelyspeaking, it was a veritable banquet of debt. A passingfamiliarity with margin account arithmetic should have beenadequate to make most funds leave the table. In fact, we thinkmost people probably knew in their hearts or heads it couldn’tlast, the only question being when the music would stop. Thereturns, it seems, were just simply too good to resist. We wouldnot make any predictions about when the music was going tostop and will not make a prediction as to when the music willresume, although we are confident that we will look back onthis period as an opportunity to buy into some good businessesat very attractive prices. We just tried to stay away from thetable. Now, of course, we are inundated with opinions whichrange from talk of a new depression to “I see the light at the endof the tunnel.” We will leave the timing to others and makejust one economic observation based upon our reading ofeconomic history, and that is the depression was not caused bythe 1929 market crash but rather by the economic policies of

the Hoover Administration. There seems to be fairly broadagreement that the people in charge of policy today areextremely capable and working hard to help unwind the mess.When thinking about investing, we happen to believe thatmarkets are not formulas. They are financial town hallmeetings with real people, some rational, others irrational, andmost, from time to time, emotional. The trick is to figure out away to separate yourself from the roar of the crowd and try tobe rational. We believe Ben Graham had a pretty good processfor doing that.

A brief history on how we got to where we are, while itmight be boring, may be instructive. The entire mess beganwith the lowly mortgage. Large numbers of people (estimatesrun into the millions) with limited financial resources werepersuaded to borrow too much money to either buy orrefinance a house with a low initial interest rate. Nobody, itseems, was too concerned about how high that rate might go ina few years. Maybe it was too far in the future to consider. Sowas born the subprime borrower. The oxygen for this was cheapmoney. Responding to deflationary fears following 9/11, theFederal Reserve lowered interest rates to unprecedented levels,and with cheap money, residential real estate skyrocketed.With escalating house prices, mortgages seemed like a low riskbet. The problem in all of this, in our humble opinion, was two-fold. Lenders no longer cared whether the loan was good ornot. They took a fee for originating the loan and sold it on toanother who packaged the loans, the packagers then in turntook a fee and sold it on to another financial firm who slicedthe loans up into CDOs (collateralized debt obligations), tooka fee, and sold them to investors. Rating agencies broughtmagic to the process by converting pools of subprime mortgagesinto investment grade paper. As we sometimes say, no one hadany real skin in the game. The fees drove the process; the creditwas going to be someone else’s problem. The process turnedreally toxic when the buyers – banks, investment banks, hedgefunds – borrowed large amounts of money on a short-term basisto buy the CDOs on which they received a higher rate ofinterest. They used the CDOs as collateral to borrow moremoney to buy more CDOs. It isn’t too hard to see howproblems might develop. Layered on top of this are creditdefault swaps (CDSs). We won’t say too much about theseinstruments. They were originally created to provide insuranceagainst debt defaults, albeit without any reserves, whichprobably wasn’t a good idea to begin with. With the help ofhedge funds and proprietary trading desks, CDSs mutated intoa mechanism to speculate on these new debt instruments withthe nominal value of the swaps today exceeding the value ofthe underlying instruments by a factor of roughly eight times,by some estimates. Today we have trillions of dollars of theseCDOs, CMOs, CDSs, etc. in the financial system with fewbuyers and a weakening housing market. Our view is that it willtake time to unwind the debt and there will be plenty ofvolatility, and no doubt very gloomy predictions in the process.We believe the most rational way to behave is to look for theoccasional baby that gets thrown out with the bath water, andto focus on identifying a good business with strong financialand competitive characteristics at attractive prices. In the notso long run, the economics should win out to our benefit.

I-4

Performance: Results and Attribution

So how have our Funds weathered this turbulent period?While all three of our Funds were not immune to the downturnover the last year, all three significantly outperformed theirrespective benchmarks as the credit crisis unfolded. TheTweedy, Browne Global Value Fund finished this roller coasterperiod down 6.35% while the MSCI EAFE Index hedged backinto U.S. dollars was down 14.05% during the period. TheTweedy, Browne Value Fund marginally underperformed theS&P 500 for the year, but held up very well against the MSCIWorld Index hedged back into U.S. dollars, declining 5.41%versus 9.22% for the index. The Value Fund now hasapproximately 35% of its net assets invested in non-U.S.companies. The new Tweedy, Browne Worldwide HighDividend Yield Value Fund, which began operations onSeptember 5th of last year, has also gotten off to a good relativestart, declining since its inception 2.69% versus a decline of6.72% for the MSCI World Index. While negative results arenothing to boast about, we were gratified that the Funds heldup fairly well during perhaps one of the most volatile periodsthat we have experienced in our 30 plus years of investing.

The subprime mortgage crisis has spawned anunprecedented level of equity market volatility over the lasteight months. Since the bursting of the credit bubble back inAugust, the MSCI EAFE Index has had 17 days of gains orlosses in excess of 2%. In contrast, in the first half of the 2007calendar year, there were only three such days, and in thecombined years of 2005 and 2006 there were a total of just sixsuch days. This increased volatility was not confined to theinternational markets. The S&P 500 also had 26 days duringthe last eight months with gains or losses in excess of 2%. Thiscompares to two days in the first half of 2007, and only twosuch days for the combined years 2005 and 2006. Needless tosay, this kind of market churn generally produces pricingopportunities for value investors such as ourselves.

Ebullient markets such as we had over the last five yearsjust prior to the inception of the credit crisis are generally notthe kind of environment in which value investing shines, atleast not on a relative basis, and this proved to be the caseparticularly in our Value Fund. For the one, three and five-yearannualized periods ending June 30, 2007 for instance, ourValue Fund underperformed the S&P 500 and the MSCIWorld Index hedged to U.S. dollars despite generating solidabsolute returns. During rapidly rising markets, we and othervalue investors often have a hard time finding undervaluedstocks, which leads to rising cash positions, which in turn dragdown portfolio returns. As you will recall, we closed our doorsto new investors in early 2005, preferring not to dilute ourexisting shareholders’ returns by taking on new money that webelieved could not effectively be put to work. With the recentmarket downturn, our Value Fund is now starting to gainconsiderable ground on its benchmark indices.

Over the long term, we believe that how one performs indifficult environments is as important, or perhaps even moreimportant than how one performs in the bull market phase, andin that respect, we believe we have more than held our own.Looking back over the last 14 plus years, the MSCI EAFEIndex hedged to U.S. dollars and the S&P 500 had four and

three down market years, respectively. As you can see from thefollowing chart, our Global Value Fund and Value Fundoutperformed these indices in each of those down periods,producing a cumulative net loss of 1.76% and 2.70%,respectively, versus a cumulative loss of 42.55% and 37.61% forthe MSCI EAFE Index hedged to U.S. dollars and the S&P500, respectively.(6)

Performance in Down Market Years

The most recent downturn over the last nine months is noexception. While we have faced declines in our Funds, thesehave not been as significant as the declines in the broad marketindices. Between June 30, 2007 and March 31, 2008, whenmost of the carnage occurred, the MSCI EAFE Index (Hedgedto U.S. dollars), the MSCI World Index (Hedged to U.S.dollars), and the S&P 500 declined 19.23%, 14.54% and10.68%, respectively. In contrast, our Global Value and ValueFunds finished this same period down an estimated 11.60% and10.05%, respectively. The Worldwide High Dividend YieldValue Fund also held up well during this period declining2.69% since its inception on September 5, 2007 versus adecline of 6.72% for the MSCI World Index in U.S. dollars.(6)

The downturn in our Funds was muted, at least in part,due to the fact that we have had modest direct exposure to thesubprime problem. With the exception of our holdings in AIG,HSBC and Bank of America, which, we believe, havemanageable amounts of capital invested in subprime mortgagesand have many other compensating competitive advantages,we have had very little investment in those areas of the marketthat were the most affected.(7)

The returns for our portfolios over the last year werefueled, in large part, by solid returns in our food, beverage, andindustrial holdings, and continued strength in our Finnish,Dutch, Mexican and South Korean stocks. Our significantunderweighting in Japan also held us in good stead, as thismarket has been under pressure over the last year or so. Ourfinancial stocks, which were down in double digits, still faredbetter than their index counterparts. Our lack of anymeaningful exposure to energy stocks, aside from those in ourhigh dividend yield portfolios, was a drag on our relative results.Those energy stocks that we did own in the Worldwide HighDividend Yield Value Fund underperformed their peers. Oursignificant weighting in media stocks also did not serve us wellduring this period.

Among the most significant individual contributors toportfolio returns over the last year were stocks such as ABNAMRO (Global Value and Value), Kone OYJ (Global Value),Nestle (Global Value and Value), Coca-Cola Femsa (Global

05

-5

10

-10

20

-20

15

-15

30

-30

25

-25

35

-35

TB Global Value Fund MSCI EAFE (Hedged) TB Value Fund S&P 500

4.36

1994 2000 2001 2002

12.39

-4.38

14.45

-9.13-4.67

-15.87

-0.09

-11.88 -12.14

-27.37

-14.91-22.09

TB Value Fund

-1.67

All returns are after the deduction of fees and expenses.

I-5

Value), Samsung SDI (Global Value), Leucadia National(Value), Kimberly-Clark (Worldwide High Dividend YieldValue), AKZO Nobel (Global Value and Worldwide HighDividend Yield Value), and Grolsch (Global Value). As youmay recall, ABN AMRO was acquired by the Royal Bank ofScotland consortium in late October, after a long andcontentious battle with Barclays. When we first purchasedABN AMRO, we believed it was cheap on a fundamental basis,selling at approximately 10 times earnings with a dividend yieldof over 5%. Moreover, while the performance of the bankoverall was below average, our research indicated that they hadseveral very valuable businesses within the bank which wouldbe attractive to competitors. Our return on the investment wasapproximately 130% in local currency in the Global ValueFund, and 125% for the Value Fund, including dividends forboth Funds, during the roughly six year period that we ownedit, with much of our return being realized when it was acquiredby the consortium, which split up the various pieces amongthemselves. As is frequently the case, getting in at a cheap pricewas the key to getting a good return on our investment.

Similarly, in our Global Value Fund, Grolsch, the Dutchbeer brewer, has been acquired by SABMiller PLC, and was uproughly 190% over our original cost at the time we tenderedour shares. Again, we’ve held this stock since March 1999, andmost of our return occurred in a concentrated burstimmediately after the takeover bid was announced.

Another stock that contributed significantly to last year’sresults was Nestle, the large Swiss food company. This is a stockthat has been a core holding in many of our portfolios for thelast seventeen years. Many of our clients may think that thebulk of our returns over the long term are attributable to oursmaller and medium capitalization holdings. That is not alwaysthe case. Nestle, which we first purchased for the Global ValueFund and the Value Fund back in 1993, has compounded at anaverage annualized return of 12.5% and 12.7% per yearincluding dividends, for the Global Value Fund and the ValueFund, respectively, over the last fifteen years. We believe thatNestle is well managed, has a diversified array of over 100different branded products sold on a worldwide basis, producessteady and consistent growth in earnings, and affords investorsa relatively safe way to participate in the growth of emergingmarkets around the globe.

The increase in Nestle’s stock price has been significant since Tweedy, Browne began buying it

in 1993

Larger capitalization securities such as Nestle now accountfor roughly two-thirds of net assets in the Global Value Fundversus one-third in smaller and medium capitalizationcompanies. Five years ago, the reverse was the case withsmaller and medium capitalization companies accounting fortwo-thirds of net assets. This change in composition has comeabout simply because there is more value to be found today inlarger companies. We sold a number of our smaller companiesas they surged in price over the last five years.

Another segment of our Funds’ portfolios that producedattractive returns over the last year were our South Koreanstocks. The values we have been able to uncover in this mostdeveloped of developing nations have been nothing less thanextraordinary. Even in the short run, value has been borne outby rapidly advancing stock prices. Stocks such as Samsung SDI,Dongah Tire & Rubber, Taeyoung Engineering, Hanil Cementand Youngone Corporation, among others, produced attractivereturns for our Global Value Fund.

Despite these gains, a number of the stocks in our Fundswere dragged down in price during the year, not surprisinglysome of our financial, retail and media-related holdings. Stockssuch as Comcast (Value), Axel Springer (Global Value),Mediaset (Global Value, Value and Worldwide High DividendYield Value), Mondadori (Global Value, Value and WorldwideHigh Dividend Yield Value), Home Depot (Value andWorldwide High Dividend Yield Value), and AIG (GlobalValue and Value) all finished the year in negative territory,despite what we feel are very attractive long-term fundamentalsfor each of them.

Currency Hedging and Its Impact on Recent Returnsand Peer Group Comparisons

As you know, over 14 years ago when we established theGlobal Value Fund, we decided to try to eliminate currency riskfrom our non-U.S. investments by hedging our foreigncurrency exposure back into the U.S. dollar. By doing this, webelieved we would be able to earn our returns in the stocks andnot the currencies. After all, we had gone abroad looking forcheap stocks, not to speculate in foreign currencies. From ourpoint of view, valuing a stock was one thing, valuing a currencywas something entirely different. We knew we couldn’t do it,and quite frankly, we were not at all confident that anyone elsecould either, at least on a reasonably consistent basis.

It was also comforting to know that we could eliminatewhat we felt to be an undesirable element of internationalinvesting at a de minimis cost over the long term.(8) Study afterstudy had indicated that over long measurement periods,currency was generally a wash in terms of its impact on returns,and whether you hedged or didn’t hedge, you tended to comeout in roughly the same place in terms of performance. We alsofound added reassurance in a paper written by André Perold,the noted Harvard Business School professor entitled, The FreeLunch in Currency Hedging,a where he found that hedgingcurrency exposure greatly enhanced the diversificationpotential of foreign investments. He went on to find thatoutside of transaction costs associated with hedging, whichappeared to be minimal, it was hard to make the case thatcurrency hedging reduced long-run expected returns.

0

100

200

300

400

500

600

6/30/1

993

6/30/1

994

6/30/1

995

6/30/1

996

6/30/1

997

6/30/1

998

6/30/1

999

6/30/2

000

6/30/2

001

6/30/2

002

6/30/2

003

6/30/2

004

6/30/2

005

6/30/2

006

TB Global Value Fund6/24/93 - 3/31/08Cumulative Return:Annualized Return:

465.5%12.5%

TB Value Fund12/9/93 - 3/31/08Cumulative Return:Annualized Return:

457.2%12.7%

Including the return from dividends, $10,000 investedin June and December 1993 would be valued at

$56,500 and $55,700 at March 31, 2008, respectively.

Split

-Adj

uste

d Pr

ice

Source: Bloomberg

I-6

So how did the theory hold up in reality over the last 14plus years? Surprisingly well. In fact, back in September of lastyear, had you gone to our website and looked at the annualizedreturns since the inception of our Fund for the EAFE Index,both hedged and unhedged, you would have found only a onebasis point difference between EAFE Hedged and EAFEUnhedged over a 14 plus year period. During that period theU.S. dollar strengthened in seven of the calendar year periodsand weakened in the other seven. The theory, indeed, hadproven out at least for that period.

That said, in the shorter term, hedged and unhedgedreturns can diverge dramatically. For example, the U.S. dollarhas declined vis-à-vis the Euro in four out of the last five years,giving a large currency boost to the returns of unhedgedinternational investors. This is one of the main reasons whydespite having beaten the hedged MSCI EAFE Index in sevenout of the last eight years, in recent years the Tweedy, BrowneGlobal Value Fund has trailed many of the funds to which weare closely compared, as they are for the most part unhedged.

We don’t know when the U.S. dollar will strengthen, butif the past is indeed prologue, it will strengthen at some point,and when it does, our portfolios will be protected from thedilutive impact of weakening foreign currencies, and our peergroup performance comparisons should reverse.

When we opened the Global Value Fund in 1993, thedollar had been under pressure for most of the previous eightplus years. We had record twin deficits, and there were nodollar bulls to be found. Many investors, when learning of ourFund, liked our investment approach, but didn’t like ourhedging policy. Well, we all know what happened over thenext eight plus years. The Federal budget fell into balance andthe dollar strengthened. During this period, our forwardhedging contracts protected our Fund to a great degree from thedilutive impact of declining foreign currencies relative to thedollar. Again, theory became reality.

While we would prefer not to go through periods when ourpeer group comparisons suffer due to our hedging policy, we areconfident — based on empirical data and our own experience— that it will correct itself over time, and currency will onceagain prove to be a wash in terms of its impact on internationalinvestment returns.

We’d like to make one more point regarding our hedgingprocess. We hedge what we believe to be our perceived non-U.S.currency exposure back into the dollar. What do we mean byperceived exposure? Some big multinational corporations thatare domiciled in a foreign country and whose shares aredenominated in a foreign currency earn a substantial amount oftheir profits in U.S. dollars through the sale of products to U.S.consumers. For example, Nestle, which is headquartered inSwitzerland and whose shares are denominated in Swiss Francs,earns as much as 40% of its annual profits in U.S. dollars. Thismeans we are already somewhat hedged with respect to theSwiss franc exposure of our Nestle shares without having toenter into a forward hedging contract. If the dollar strengthens,we feel that we are somewhat protected from the decline inSwiss franc-denominated Nestle by the fact that Nestle’s stockshould benefit from the currency translation profits theyreceive from their U.S. sales. Because of this fact, we onlypartially hedge our position in Nestle back into the dollar. In

essence, we are only hedging our perceived exposure to the Swissfranc as best as we can determine, which is the non-U.S. profitcomponent of Nestle. As a matter of policy, we only partiallyhedge the nominal currency exposure of companies who earnwhat in our analysis is a material or significant portion of theirprofits in U.S. dollars. As of March 31, 2008, our hedge ratio,or the value of our forward contracts versus our total nominalnon-U.S. currency exposure, was approximately 70%. Theother 30% was implicitly hedged by the U.S. profits of thesecompanies.

We intend to continue, absent extraordinarycircumstances, to hedge the perceived foreign currencyexposure inherent in our non-U.S. equity investments backinto the U.S. dollar. Remember, we believe that we neithermake money nor do we lose money over the long term onforeign currency in the overall portfolio by hedging. When yousee losses in our hedging contracts, they are generally offset bycorresponding currency translation gains in the shares of ournon-U.S. holdings. We are simply attempting to set aside whatwe believe to be the unmanageable and speculative componentof the return that results when one invests in a stockdenominated in a currency other than the U.S. dollar. Thetheory suggests that aside from transaction expenses which arede minimis, there is virtually no cost in doing this over the longterm, and our experience over the last 14 years, we believe, hasborne this out.

New OpportunitiesThe silver lining in our current rather grim investment

environment is that we believe that we are in the process ofbeing presented with an unusual opportunity to buy trulyundervalued businesses on our terms. While broad marketindices have declined roughly 15% since the credit bubbleburst in August of last year, there has been heightenedvolatility in certain sectors, industry groups and countries, andsome stocks are beginning to offer what appear to becompelling values.

Perhaps the segment of the stock market that has causedthe most anxiety of late, aside from housing stocks, is financialstocks. As a group, these stocks are down approximately 34%from their highs in the face of large and serious markdowns,which for many has caused considerable damage to theirbalance sheets. One must tread cautiously here, but there aresome very good companies that we feel are “being thrown outwith the bathwater,” companies such as Lloyds TSB, AmericanExpress, AIG and U.S. Bancorporation. We have been addingto our positions in these companies. While there might befurther markdowns in financial stocks to come, given the levelof uncertainty in the stock market, at current prices, adiversified group of financials such as these should proverewarding looking beyond the current environment.

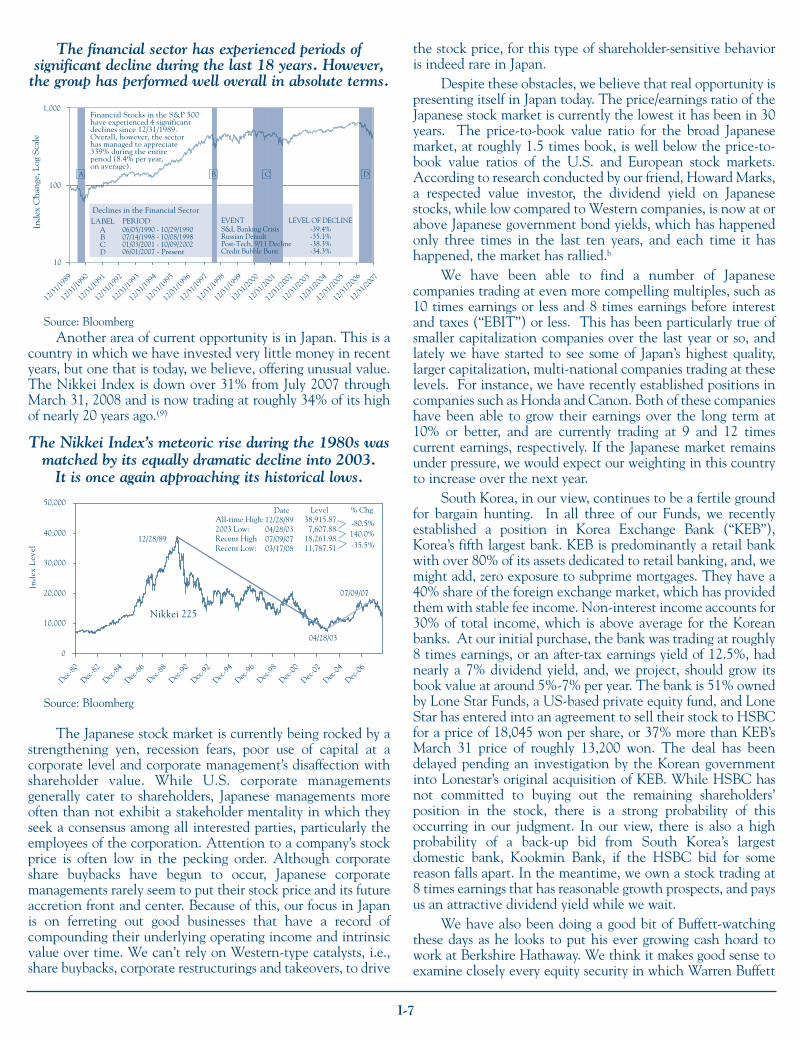

While the past performance of any stock or industry sectoris not necessarily indicative of future returns in general, or ourFunds in particular, over the last 18 years, there have been fourtimes when financial stocks corrected by as much as 30% ormore. Yet over this entire period, a buy and hold investor wouldhave made a cumulative return of 339% or roughly 8.40% peryear on average. If you include estimated dividends during thisperiod, your return would have been approximately 10% to11% annualized. Not bad for such a turbulent period.

I-7

The financial sector has experienced periods of significant decline during the last 18 years. However,

the group has performed well overall in absolute terms.

Another area of current opportunity is in Japan. This is acountry in which we have invested very little money in recentyears, but one that is today, we believe, offering unusual value.The Nikkei Index is down over 31% from July 2007 throughMarch 31, 2008 and is now trading at roughly 34% of its highof nearly 20 years ago.(9)

The Nikkei Index’s meteoric rise during the 1980s wasmatched by its equally dramatic decline into 2003.

It is once again approaching its historical lows.

The Japanese stock market is currently being rocked by astrengthening yen, recession fears, poor use of capital at acorporate level and corporate management’s disaffection withshareholder value. While U.S. corporate managementsgenerally cater to shareholders, Japanese managements moreoften than not exhibit a stakeholder mentality in which theyseek a consensus among all interested parties, particularly theemployees of the corporation. Attention to a company’s stockprice is often low in the pecking order. Although corporateshare buybacks have begun to occur, Japanese corporatemanagements rarely seem to put their stock price and its futureaccretion front and center. Because of this, our focus in Japanis on ferreting out good businesses that have a record ofcompounding their underlying operating income and intrinsicvalue over time. We can’t rely on Western-type catalysts, i.e.,share buybacks, corporate restructurings and takeovers, to drive

the stock price, for this type of shareholder-sensitive behavioris indeed rare in Japan.

Despite these obstacles, we believe that real opportunity ispresenting itself in Japan today. The price/earnings ratio of theJapanese stock market is currently the lowest it has been in 30years. The price-to-book value ratio for the broad Japanesemarket, at roughly 1.5 times book, is well below the price-to-book value ratios of the U.S. and European stock markets.According to research conducted by our friend, Howard Marks,a respected value investor, the dividend yield on Japanesestocks, while low compared to Western companies, is now at orabove Japanese government bond yields, which has happenedonly three times in the last ten years, and each time it hashappened, the market has rallied.b

We have been able to find a number of Japanesecompanies trading at even more compelling multiples, such as10 times earnings or less and 8 times earnings before interestand taxes (“EBIT”) or less. This has been particularly true ofsmaller capitalization companies over the last year or so, andlately we have started to see some of Japan’s highest quality,larger capitalization, multi-national companies trading at theselevels. For instance, we have recently established positions incompanies such as Honda and Canon. Both of these companieshave been able to grow their earnings over the long term at10% or better, and are currently trading at 9 and 12 timescurrent earnings, respectively. If the Japanese market remainsunder pressure, we would expect our weighting in this countryto increase over the next year.

South Korea, in our view, continues to be a fertile groundfor bargain hunting. In all three of our Funds, we recentlyestablished a position in Korea Exchange Bank (“KEB”),Korea’s fifth largest bank. KEB is predominantly a retail bankwith over 80% of its assets dedicated to retail banking, and, wemight add, zero exposure to subprime mortgages. They have a40% share of the foreign exchange market, which has providedthem with stable fee income. Non-interest income accounts for30% of total income, which is above average for the Koreanbanks. At our initial purchase, the bank was trading at roughly8 times earnings, or an after-tax earnings yield of 12.5%, hadnearly a 7% dividend yield, and, we project, should grow itsbook value at around 5%-7% per year. The bank is 51% ownedby Lone Star Funds, a US-based private equity fund, and LoneStar has entered into an agreement to sell their stock to HSBCfor a price of 18,045 won per share, or 37% more than KEB’sMarch 31 price of roughly 13,200 won. The deal has beendelayed pending an investigation by the Korean governmentinto Lonestar’s original acquisition of KEB. While HSBC hasnot committed to buying out the remaining shareholders’position in the stock, there is a strong probability of thisoccurring in our judgment. In our view, there is also a highprobability of a back-up bid from South Korea’s largestdomestic bank, Kookmin Bank, if the HSBC bid for somereason falls apart. In the meantime, we own a stock trading at8 times earnings that has reasonable growth prospects, and paysus an attractive dividend yield while we wait.

We have also been doing a good bit of Buffett-watchingthese days as he looks to put his ever growing cash hoard towork at Berkshire Hathaway. We think it makes good sense toexamine closely every equity security in which Warren Buffett

10

100

1,000

12/31

/1989

12/31

/1990

12/31

/1991

12/31

/1992

12/31

/1993

12/31

/1994

12/31

/1995

12/31

/1996

12/31

/1997

12/31

/1998

12/31

/1999

12/31

/2000

12/31

/2001

12/31

/2002

12/31

/2003

12/31

/2004

12/31

/2005

12/31

/2006

12/31

/2007

A B C D

Inde

x C

han

ge, L

og S

cale

Financial Stocks in the S&P 500have experienced 4 significantdeclines since 12/31/1989.Overall, however, the sectorhas managed to appreciate339% during the entireperiod (8.4% per year,on average).

Declines in the Financial SectorLABEL

ABCD

PERIOD06/05/1990 - 10/29/199007/14/1998 - 10/08/199801/03/2001 - 10/09/200206/01/2007 - Present

EVENTS&L Banking CrisisRussian DefaultPost-Tech, 9/11 DeclineCredit Bubble Burst

LEVEL OF DECLINE-39.4%-35.1%-38.3%-34.3%

Source: Bloomberg

0

10,000

20,000

30,000

40,000

50,000

Dec-80

Dec-82

Dec-84

Dec-86

Dec-88

Dec-90

Dec-92

Dec-94

Dec-96

Dec-98

Dec-00

Dec-02

Dec-04

Dec-06

Nikkei 225

Date12/28/8904/28/0307/09/0703/17/08

All-time High:2003 Low:Recent HighRecent Low:

Level 38,915.877,607.88

18,261.9811,787.51

% Chg

-80.5%140.0%-35.5%

Inde

x L

evel

12/28/89

04/28/03

07/09/07

Source: Bloomberg

I-8

invests. He is, after all, arguably the investment world’s greatestsecurities analyst.

Over the last year, Warren Buffett’s Berkshire Hathawaytook positions in a number of railroad stocks, includingBurlington Northern, Norfolk Southern, and Union Pacificrailroads. One of our analysts, David Browne, who is the thirdgeneration of Brownes to grace the halls of Tweedy, Browne,studied the railroads intensely, and found what we believe to bea growing competitive advantage for the railroads over thetrucking industry in the face of higher oil prices. In addition,railroad consolidation, which has lead to a decline in trackmiles in conjunction with a highway system operating at fullcapacity and moderate future growth in freight transportation,should enable the railroads to raise prices. We establishedpositions in Burlington Northern and Norfolk Southern in theValue Fund at prices we felt were at or near the price thatWarren Buffett paid, and both were trading at roughly 12 to 14times estimated earnings.

We believe another area of current opportunity is highdividend yield stocks. As stock prices have come down overthe last eight months, dividend yields are up and are in manyinstances more than competitive with high quality bond yields.We find it somewhat interesting that an investor currentlyreceives approximately 2.5% to 3.0% yield on a certificate ofdeposit issued by Bank of America that is taxed at ordinaryincome tax rates for an average taxpayer, while an investmentin the common stock of Bank of America currently yieldsapproximately 6.5%, which is currently generally taxed at aFederal rate of 15%. While the principal invested in the formermay be insured by the FDIC, and the latter exposes the investorto a potential for loss of principal inherent in equity investing,we feel the common stock, trading at less than 9 times earnings,with a retail deposit base of over $800 billion in what we thinkis likely to be a rising yield curve environment, should prove tobe a profitable investment.

The Tweedy, Browne Worldwide High Dividend YieldValue Fund, as of March 31st, had a weighted average dividendyield of 4.9% and traded at a weighted average price/earningsratio of roughly 11 to 12 times forward earnings. (Please notethat the weighted average dividend yield is not representative of theFund’s yield, nor does it represent the Fund’s performance. Thefigure solely represents the average weighted dividend yield of thecommon stocks held in the Fund’s portfolio. Please refer to the 30-Day Standardized SEC Yield in the performance chart on page I-2for the Fund’s yield.) This compares to the MSCI World Index,which currently has a yield of 2.7%, and trades at 14 timesearnings. We have mentioned before that there is significantevidence that higher dividend yield portfolios produce higherrates of return than lower dividend yield portfolios over thelong term. Furthermore, the studies show that the differentialincreases in down-market environments. Our focus in the Fundis on companies that we believe are undervalued, that havesteady and relatively predictable earnings, and that have a longhistory of paying consistently growing dividends. For example,U.S. Bancorporation and General Electric, two holdings in theWorldwide High Dividend Yield Value Fund, have paid anincreasing dividend for 36 and 34 consecutive years,respectively. In the last 10 years, their dividends have growneach year on average 19.4% and 12.4%, respectively. Earlier

this year, Genuine Parts, another one of our holdings, increasedits dividend by 6.85%, which marks the 52nd straight year ofincreasing dividends for the company.

It’s Déjà Vu All Over Again — Yogi BerraSo where does all the current turmoil in our capital

markets leave us? We certainly don’t want to appear overlysanguine about this mess, but we’ve been here before and wewill revisit times like this again if we are fortunate to liveanother 10 or 20 years.

That said, if the next year or so in global equity marketscould be fraught with rampant volatility and the possibility offurther erosion in stock prices, why shouldn’t one simply retreatto cash until the dust settles and a more promisingenvironment presents itself? We wish it were that simple. Firstof all, selling your stocks after many years of gains would, formost taxable investors, create a windfall for the tax man.Secondly, trying to call the bottom of a stock market cycle canbe hazardous to wealth-building. A study of the history ofequity returns reveals that the bulk of an equity investor’sreturn occurs in short bursts. We believe that if you are notinvested during these rather brief upswings, your long-termcompounded return can suffer dramatically.

In a recent paper entitled, Black Monday and Black Swans,cJack Bogle, the former chairman of Vanguard, illustrated thefolly of trying to time markets. He cited a study which indicatedthat the S&P 500 had risen from 17 in 1950 to roughly 1540 inOctober 2007 (some 57 years later). If you deducted the 40 daysof highest returns out of these 14,528 trading days, the Indexwould have increased to only 276, some 70% less. In a similarstudy, Laszlo Birinyi, the noted quantitative investmentanalyst, examined the performance of the S&P 500 between1966 and 2001, a period of 35 years. $1 invested in the S&P500 in 1966 would have grown to $11.71 in 2001. If youdeducted the returns from the five best trading days in each ofthese 35 years, the $1 would actually have declined to $0.15.This is pretty humbling data.

Third, this is precisely the kind of market environmentthat generally produces unusually attractive opportunities forvalue investors. Lewis Sanders of the value investment firm,AllianceBernstein, once described difficult markets as the“domain of progressive discouragement.”d He went on to pointout that value opportunities often present themselves in highanxiety environments; and that “...anxiety-producing assets –those framed in the domain of potential losses – will be pricedto offer returns that are meaningfully higher than the returnsjustified by the actual risks taken.” In our judgement, today isone of those market environments, and we are being presentedwith potential pricing opportunities. It is our job to have thebehavioral temperament to take advantage of them.

What allows us to do this while many investors panic andflee in the face of overwhelming uncertainty? We’re not quitesure, but perhaps with the tools that Ben Graham gave us, weare able to make a rather clear distinction between the dailyprice fluctuations in the stock market and the underlyingeconomics of the businesses we own. It is this core belief, i.e.,that it is the economics of the business that wins out in the longrun and is eventually reflected in stock prices, that has allowedour Funds to survive and prosper in Sanders’ domain of

progressive discouragement.In a recent interview discussing his new book entitled,

Your Money and Your Brain,e Jason Zweig opined that thebiggest key to the investment success of Warren Buffett andBenjamin Graham was that they were “inversely emotional.”They have an ability, as Warren Buffett has described, to begreedy when others are fearful and fearful when others aregreedy. Zweig went on to say that great investors seem to sharea quality that goes beyond calm, “a certain imperturbability orimplacability,” and used a classical Greek term, “ataraxia,” todescribe the state of not being bothered by the things thatbother most people. However one may describe it, perhaps weshare the affliction, because in a perverse sort of way, despitethe head winds we face near term, we are beginning to getexcited by the opportunities that appear to be headed our way.

We would remind our shareholders that over the last 50years, the stock market has endured some pretty grim news.From the rise and fall of the “Nifty Fifty” and the rampaginginflation of the 1970s, to the double digit interest rates of theearly 1980s, to the crash of 1987, to the banking and Savings& Loan crisis of the early 1990s, the Asian crisis and theRussian default of 1998, the Y2K systems threat of 1999, to thebursting of the technology bubble and the Presidential electioncrisis of 2000, followed by the terrorist attacks of September 11,2001 and the year-end collapse of Enron, all leading up totoday’s housing and credit conflagration – through all theseconfidence-shattering events, our Funds have survived andprospered.

In closing, perhaps Lew Sanders said it best:The principal dynamics in the world’s capital marketsrevolve around a tug-of-war between feeling secure andmaking money. In the end, the feelings generally win out.A substantial amount of money can thus be made if avalue investment manager is willing to spend the bulk ofhis or her professional life feeling depressed, isolated, andafraid, waiting for the forces of mean reversion to relievethe stress, at which point the manager will sell and use theproceeds to rebuild anxiety. Is it worth it? This question,of course, is philosophical, but the money on the table isconsiderable, and the question deserves serious thought.

As your Fund manager, we feel that we have an obligationto try to put anxiety in perspective and to behave rationally, sothat we can capture for you some of the rewards which we areconfident will come in the future. We hope in some small way,through our actions and our words, that we are able to do justthat. We would encourage you to keep the faith. 2008 could bea terrific year for planting the seeds from which attractivefuture returns will grow.

Thank you for investing alongside us, and for yourcontinued confidence.

Very truly yours,

TWEEDY, BROWNE COMPANY LLCChristopher H. BrowneWilliam H. BrowneJohn D. SpearsThomas H. ShragerRobert Q. Wyckoff, Jr.Managing Directors

April 24, 2008

Notes:

(1)Indexes are unmanaged, and the figures for the indexesshown include reinvestment of dividends and capitalgains distributions and do not reflect any fees orexpenses. Investors cannot invest directly in an index.We strongly recommend that these factors beconsidered before an investment decision is made.

(2)MSCI EAFE Index US$ is an unmanagedcapitalization-weighted index of companiesrepresenting the stock markets of Europe, Australasia and the Far East. MSCI EAFE IndexHedged consists of the results of the MSCI EAFEIndex hedged 100% back into US dollars and accountsfor interest rate differentials in forward currencyexchange rates. Results for both indexes are inclusiveof dividends and net of foreign withholding taxes.

(3)Inception dates for the Global Value Fund, Value Fundand Worldwide High Dividend Yield Value Fund wereJune 15, 1993, December 8, 1993, and September 5,2007, respectively. Information with respect to MSCIEAFE indexes used is available at month end only;therefore the closest month end to the Global ValueFund’s inception date, May 31, 1993, was used.

(4)The MSCI World Index is a free float-adjusted marketcapitalization weighted index that is designed tomeasure the equity market performance of developedmarkets. As of March 2008, the MSCI World Indexconsisted of the following 23 developed marketcountry indices: Australia, Austria, Belgium, Canada,Denmark, Finland, France, Germany, Greece, HongKong, Ireland, Italy, Japan, the Netherlands, NewZealand, Norway, Portugal, Singapore, Spain, Sweden,Switzerland, the United Kingdom, and the UnitedStates. The MSCI World Index (US$) reflects thereturn of this index for a US dollar investor. MSCIWorld Index (Hedged to US$) consists of the results ofthe MSCI World Index with its foreign currencyexposure hedged 100% back into US dollars. The

I-9

I-10

index accounts for interest rate differentials in forwardcurrency exchange rates. Results for this index areinclusive of dividends and net of foreign withholdingtaxes.

(5)S&P 500 Index is an unmanaged capitalization-weighted index composed of 500 widely held commonstocks listed on the New York Stock Exchange,American Stock Exchange and over-the-countermarket and includes the reinvestment of dividends.

(6)Returns shown are for a specific time period where theFunds outperformed their relevant indexes. While theFunds outperformed the relevant indexes for theperiod shown, there have been previous periods whenthe Funds underperformed these indices. Since pastperformance is not indicative of future results, therecan be no guarantee that the Funds will outperformtheir relevant indexes in the future. Please refer to pageI-2 of the letter for the Funds’ standardizedperformance results.

(7)As of March 31, 2008, Tweedy, Browne Global ValueFund, Tweedy, Browne Value Fund, and Tweedy,Browne Worldwide High Dividend Yield Value Fundhad invested the following percentages of its net assets,respectively, in the following portfolio holdings: AIG(2.8%, 3.5%, 0.0%); HSBC (1.3%, 0.0%, 1.7%); Bankof America (0.0%, 2.0%, 1.6%); ABN AMRO (0.0%,0.0%, 0.0%); Kone OYJ (5.8%, 0.0%, 0.0%); Nestle(6.6%, 9.2%, 0.0%); Coca-Cola Femsa (1.6%, 0.0%,0.0%); Samsung SDI (1.0%, 0.0%, 0.0%); LeucadiaNational (0.0%, 3.9%, 0.0%); Kimberly-Clark (0.0%,0.0%, 3.3%); AKZO Nobel(2.5%, 0.0%, 2.2%);Grolsch (0.0%, 0.0%, 0.0%); Royal Bank of Scotland(0.0%, 0.0%, 0.0%); Barclays (0.0%, 0.0%, 0.0%);SABMiller PLC (0.0%, 0.0%, 0.0%); Dongah Tire &Rubber (0.0%, 0.0%, 0.0%); Taeyoung Engineering(0.0%, 0.0%, 0.0%); Hanil Cement (0.4%, 0.0%,0.0%); Youngone Corporation (0.3%, 0.0%, 0.0%);Comcast (0.0%, 4.0%, 0.0%); Axel Springer (2.9%,0.0%, 0.0%); Mediaset (2.2%, 0.6%, 3.0%);Mondadori (1.5%, 0.5%, 1.9%); Home Depot (0.0%,4.1%, 0.9%); Lloyds TSB (2.1%, 1.1%, 2.5%);American Express (2.0%, 4.3%, 0.0%); U.S.Bancorporation (0.0%, 0.0%, 2.6%); Honda (0.7%,0.0%, 0.0%); Canon (1.1%, 0.0%, 0.0%); KoreaExchange Bank (1.6%, 1.0%, 2.6%); BurlingtonNorthern (0.0%, 1.2%, 0.0%); Norfolk Southern(0.0%, 1.3%, 0.0%); Union Pacific (0.0%, 0.0%,0.0%); General Electric (0.0%, 0.0%, 4.4%); andGenuine Parts (0.0%, 0.0%, 2.9%).

(8)Although hedging against currency exchange ratechanges reduces the risk of loss from exchange ratemovements, it also reduces the ability of the Funds togain from favorable exchange rate movements whenthe U.S. dollar declines against the currencies inwhich the Funds’ investments are denominated and insome interest rate environments may impose out-of-pocket costs on the Funds.

(9)The Nikkei 225 Index is an unmanaged price-weighted average of 225 Japanese companies listed inthe First-Section of the Tokyo Stock Exchange.

Investing in foreign securities involves additional risks beyondthe risks of investing in U.S. securities markets. These risksinclude currency fluctuations; political uncertainty; differentaccounting and financial standards; different regulatoryenvironments; and different market and economic factors invarious non-U.S. countries. In addition, the securities of small,less well-known companies may be more volatile than those oflarger companies. Investors should refer to the Funds’prospectus for a description of risk factors associated withinvestments in securities held by the Funds.

This letter contains opinions and statements on investmenttechniques, economics, market conditions and other matters.Of course there is no guarantee that these opinions andstatements will prove to be correct, and some of them areinherently speculative. None of them should be relied upon asstatements of fact.

Tweedy, Browne Global Value Fund, Tweedy, Browne ValueFund, and Tweedy, Browne Worldwide High Dividend YieldValue Fund are distributed by Tweedy, Browne Company LLC.

This material must be preceded or accompanied by a prospectusfor Tweedy, Browne Fund Inc.

REFERENCESa. André Perold and Evan C. Schulman, “The Free

Lunch in Currency Hedging: Implications forInvestment Policy and Performance Standards,”Financial Analysts Journal, May-June 1988, p. 45.

b. Howard Marks, “OCM Japan Opportunities Fund,”client letter, January 18, 2008.

c. Jack Bogle, “Black Monday and Black Swans,” speechbefore the Risk Management Association, Boca RatonFlorida, October 11, 2007.

d. Lewis A. Sanders, “The Advantage to ValueInvesting,” Association for Investment Managementand Research, 1995.

e. Zweig, Jason, “Mind Games - Jason Zweig Talks AboutNew Book on the Brain Science of Money.”Welling@Weeden – A Journal of IndependentResearch, Analysis and Opinion, May 11, 2007.

II-1

TWEEDY, BROWNE FUND INC.

Tweedy, Browne Global Value FundTweedy, Browne Value FundTweedy, Browne Worldwide High Dividend Yield Value Fund

ANNUAL REPORT

March 31, 2008

TWEEDY, BROWNE FUND INC.

Investment Adviser’s Note

II-2

To Our Shareholders:We are pleased to present the Annual Report to

Shareholders for the Tweedy, Browne Global Value Fund,Tweedy, Browne Value Fund and Tweedy, Browne WorldwideHigh Dividend Yield Value Fund for the year ended March 31,2008. Investment results* for the past six months and the lastone, three, five and ten years, and results since inception ofeach Fund are presented in the tables below:

Tweedy, Browne MSCI EAFE MSCI EAFE Period Ended Global Value Index Hedged Index3/31/08 Fund to US$(1)(2) in US$(1)(2)

6 Months -11.03% -17.55% -10.50%

1 Year -6.35 -14.05 -2.70

3 Years 9.32 10.07 13.32

5 Years 17.36 15.35 21.40

10 Years 8.68 3.63 6.18

Since Inception (6/15/93)(3) 11.86 6.76 7.35

Total Annual Fund Operating Expense Ratio as of 3/31/07 was 1.37%†

Total Annual Fund Operating Expense Ratio as of 3/31/08 was 1.37%†

MSCI WorldPeriod Ended Tweedy, Browne Index Hedged3/31/08 Value Fund to US$(1)(4) S&P 500(1)(5)

6 Months -9.98% -14.57% -12.46%

1 Year -5.41 -9.22 -5.08

3 Years 4.01 N/A 5.84

5 Years 9.15 N/A 11.30

10 Years 3.93 N/A 3.50

Since Inception (12/8/93)(3) 9.52 N/A 9.53

Total Annual Fund Operating Expense Ratio as of 3/31/07 was 1.38%†

Total Annual Fund Operating Expense Ratio as of 3/31/08 was 1.37%†

Tweedy, Browne MSCI World Period Ended Worldwide High Dividend Index3/31/08 Yield Value Fund in US$(1)(4)

6 Months -3.85% -11.26%

Since Inception (9/5/07)(3) -2.69 -6.72

30-Day Standardized Yield as of 3/31/08: 2.90%

Gross Annual Operating Expense Ratio for current fiscal year ending

3/31/08 was 1.86%†‡

Net Annual Operating Expense Ratio for current fiscal year ending

3/31/08 was 1.37%†‡

* The preceding performance data represents past performance andis not a guarantee of future results. Total return and principalvalue of an investment will fluctuate so that an investor’s shares,when redeemed, may be worth more or less than their original cost.The returns shown do not reflect the deduction of taxes that ashareholder would pay on Fund distributions or the redemption ofFund shares. Current performance may be lower or higher thanthe performance data shown. Please visit www.tweedy.com to

obtain performance data, which is current to the most recentmonth end. See page II-4 for footnotes 1 through 5, which describethe indices and inception dates of each Fund. Results areannualized for all periods greater than one year.

† The Funds do not impose any front-end or deferred sales charge.However, the Global Value Fund and the Worldwide HighDividend Yield Value Fund impose a 2% redemption fee onproceeds from redemptions or exchanges made within 60 days ofpurchase.

‡ The Adviser has contractually agreed to waive its investmentadvisory fee and/or to reimburse expenses of the WorldwideHigh Dividend Yield Value Fund to the extent necessary tomaintain the total annual fund operating expenses(excluding brokerage, interest, taxes and extraordinaryexpenses) at no more than 1.37%. This arrangement willcontinue at least through March 31, 2009. In thisarrangement, the Worldwide High Dividend Yield ValueFund has agreed, during the two-year period following anywaiver or reimbursement by the Adviser, to repay suchamount to the extent that after giving effect to suchrepayment such adjusted total annual fund operatingexpenses would not exceed 1.37% on an annualized basis.The performance data shown above would be lower had feesand expenses not been waived and/or reimbursed.

Performance: Results and AttributionWhile all three of our Funds were not immune to the

downturn over the last year, all three significantlyoutperformed their respective benchmarks as the credit crisisunfolded. The Tweedy, Browne Global Value Fund finishedthis roller coaster period down 6.35% while the MSCI EAFEIndex hedged back into U.S. dollars was down 14.05% duringthe period. The Tweedy, Browne Value Fund marginallyunderperformed the S&P 500 for the year, but held up very wellagainst the MSCI World Index hedged back into U.S. dollars,declining 5.41% versus 9.22% for the index. The Value Fundnow has approximately 35% of its net assets invested in non-U.S. companies. The new Tweedy, Browne Worldwide HighDividend Yield Value Fund which began operations onSeptember 5th of last year has also gotten off to a good relativestart, declining since its inception 2.69% versus a decline of6.72% for the MSCI World Index. While negative results arenothing to boast about, we were gratified that the Funds heldup fairly well during perhaps one of the most volatile periodsthat we have experienced in our 30 plus years of investing.

The subprime mortgage crisis has spawned anunprecedented level of equity market volatility over the lasteight months. Since the bursting of the credit bubble back inAugust, the MSCI EAFE Index has had 17 days of gains orlosses in excess of 2%. In contrast, in the first half of the 2007calendar year, there were only three such days, and in thecombined years of 2005 and 2006 there were a total of just sixsuch days. This increased volatility was not confined to the

II-3

international markets. The S&P 500 also had 26 days duringthe last eight months with gains or losses in excess of 2%. Thiscompares to two days in the first half of 2007, and only twosuch days for the combined years 2005 and 2006. Needless tosay, this kind of market churn generally produces pricingopportunities for value investors such as ourselves.

Ebullient markets such as we had over the last five yearsjust prior to the inception of the credit crisis are generally notthe kind of environment in which value investing shines, atleast not on a relative basis, and this proved to be the caseparticularly in our Value Fund. For the one, three and five-yearannualized periods ending June 30, 2007 for instance, ourValue Fund underperformed the S&P 500 and the MSCIWorld Index hedged to U.S. dollars despite generating solidabsolute returns. During rapidly rising markets, we and othervalue investors often have a hard time finding undervaluedstocks, which leads to rising cash positions, which in turn dragdown portfolio returns. As you will recall, we closed our doorsto new investors in early 2005, preferring not to dilute ourexisting shareholders’ returns by taking on new money that webelieved could not effectively be put to work. With the recentmarket downturn, our Value Fund is now starting to gainconsiderable ground on its benchmark indices.

Over the long term, we believe that how one performs indifficult environments is as important, or perhaps even moreimportant than how one performs in the bull market phase, andin that respect, we believe we have more than held our own.The most recent downturn over the last nine months is noexception. While we have faced declines in our Funds, thesehave not been as significant as the declines in the broad marketindices. Between June 30, 2007 and March 31, 2008, whenmost of the carnage occurred, the MSCI EAFE Index (Hedgedto U.S. dollars), the MSCI World Index (Hedged to U.S.dollars), and the S&P 500 declined 19.23%, 14.54% and10.68%, respectively. In contrast, our Global Value and ValueFunds finished this same period down an estimated 11.60% and10.05%, respectively. The Worldwide High Dividend YieldValue Fund also held up well during this period declining2.69% since its inception on September 5, 2007 versus adecline of 6.72% for the MSCI World Index in U.S. dollars.(6)

The downturn in our Funds was muted, at least in part,due to the fact that we have had modest direct exposure to thesubprime problem. With the exception of our holdings in AIG,HSBC and Bank of America, which, we believe, havemanageable amounts of capital invested in subprime mortgagesand have many other compensating competitive advantages,we have had very little investment in those areas of the marketthat were the most affected.(7)

The returns for our portfolios over the last year werefueled, in large part, by solid returns in our food, beverage, andindustrial holdings, and continued strength in our Finnish,Dutch, Mexican and South Korean stocks. Our significantunderweighting in Japan also held us in good stead, as thismarket has been under pressure over the last year or so. Ourfinancial stocks, which were down in double digits, still faredbetter than their index counterparts. Our lack of anymeaningful exposure to energy stocks, aside from those in ourhigh dividend yield portfolios, was a drag on our relative results.Those energy stocks that we did own in the Worldwide High

Dividend Yield Value Fund underperformed their peers. Oursignificant weighting in media stocks also did not serve us wellduring this period.

Larger capitalization securities now account for roughlytwo-thirds of net assets in the Global Value Fund versus one-third in smaller and medium capitalization companies. Fiveyears ago, the reverse was the case with smaller and mediumcapitalization companies accounting for two-thirds of netassets. This change in composition has come about simplybecause there is more value to be found today in largercompanies. We sold a number of our smaller companies as theysurged in price over the last five years.

Another segment of our Funds’ portfolios that producedattractive returns over the last year were our South Koreanstocks. The values we have been able to uncover in this mostdeveloped of developing nations have been nothing less thanextraordinary. Even in the short run, value has been borne outby rapidly advancing stock prices. Stocks such as Samsung SDI,Dongah Tire & Rubber, Taeyoung Engineering, Hanil Cementand Youngone Corporation, among others, produced attractivereturns for our Global Value Fund.

Despite these gains, a number of the stocks in our Fundswere dragged down in price during the year, not surprisinglysome of our financial, retail and media-related holdings. Stockssuch as Comcast (Value), Axel Springer (Global Value),Mediaset (Global Value, Value and Worldwide High DividendYield Value), Mondadori (Global Value, Value and WorldwideHigh Dividend Yield Value), Home Depot (Value andWorldwide High Dividend Yield Value), and AIG (GlobalValue and Value) all finished the year in negative territory,despite what we feel are very attractive long-term fundamentalsfor each of them.

Thank you for investing alongside us, and for yourcontinued confidence.

Very truly yours,

TWEEDY, BROWNE COMPANY LLCChristopher H. BrowneWilliam H. BrowneJohn D. SpearsThomas H. ShragerRobert Q. Wyckoff, Jr.Managing Directors

April 24, 2008

II-4

Notes:(1)Indexes are unmanaged, and the figures for the indexes

shown include reinvestment of dividends and capitalgains distributions and do not reflect any fees orexpenses. Investors cannot invest directly in an index.We strongly recommend that these factors beconsidered before an investment decision is made.

(2)MSCI EAFE Index US$ is an unmanagedcapitalization-weighted index of companiesrepresenting the stock markets of Europe, Australasiaand the Far East. MSCI EAFE Index Hedged consistsof the results of the MSCI EAFE Index hedged 100%back into US dollars and accounts for interest ratedifferentials in forward currency exchange rates.Results for both indexes are inclusive of dividends andnet of foreign withholding taxes.

(3)Inception dates for the Global Value Fund, Value Fundand Worldwide High Dividend Yield Value Fund wereJune 15, 1993, December 8, 1993, and September 5,2007, respectively. Information with respect to MSCIEAFE indexes used is available at month end only;therefore the closest month end to the Global ValueFund’s inception date, May 31, 1993, was used.

(4)The MSCI World Index is a free float-adjusted marketcapitalization weighted index that is designed tomeasure the equity market performance of developedmarkets. As of March 2008, the MSCI World Indexconsisted of the following 23 developed marketcountry indices: Australia, Austria, Belgium, Canada,Denmark, Finland, France, Germany, Greece, HongKong, Ireland, Italy, Japan, the Netherlands, NewZealand, Norway, Portugal, Singapore, Spain, Sweden,Switzerland, the United Kingdom, and the UnitedStates. The MSCI World Index (US$) reflects thereturn of this index for a US dollar investor. MSCIWorld Index (Hedged to US$) consists of the results ofthe MSCI World Index with its foreign currencyexposure hedged 100% back into U.S. dollars. Theindex accounts for interest rate differentials in forwardcurrency exchange rates. Results for this index areinclusive of dividends and net of foreign withholdingtaxes.

(5)S&P 500 Index is an unmanaged capitalizationweighted index composed of 500 widely held commonstocks listed on the New York Stock Exchange,American Stock Exchange and over-the-countermarket and includes the reinvestment of dividends.

(6)Returns shown are for a specific time period where theFunds outperformed their relevant indexes. While theFunds outperformed the relevant indexes for theperiod shown, there have been previous periods whenthe Funds underperformed these indices. Since pastperformance is not indicative of future results, therecan be no guarantee that the Funds will outperformtheir relevant indexes in the future. Please refer to page2 of the letter for the Funds’ standardized performanceresults.

(7)As of March 31, 2008, Tweedy, Browne Global ValueFund, Tweedy, Browne Value Fund, and Tweedy,Browne Worldwide High Dividend Yield Value Fundhad invested the following percentages of its net assets,respectively, in the following portfolio holdings: AIG(2.8%, 3.5%, 0.0%); HSBC (1.3%, 0.0%, 1.7%); Bankof America (0.0%, 2.0%, 1.6%); Samsung SDI (1.0%,0.0%, 0.0%); Dongah Tire & Rubber (0.0%, 0.0%,0.0%); Taeyoung Engineering (0.0%, 0.0%, 0.0%);Hanil Cement (0.4%, 0.0%, 0.0%); YoungoneCorporation (0.3%, 0.0%, 0.0%); Comcast (0.0%,4.0%, 0.0%); Axel Springer (2.9%, 0.0%, 0.0%);Mediaset (2.2%, 0.6%, 3.0%); Mondadori (1.5%,0.5%, 1.9%); Home Depot (0.0%, 4.1%, 0.9%).

Investing in foreign securities involves additional risks beyondthe risks of investing in US securities markets. These risksinclude currency fluctuations; political uncertainty; differentaccounting and financial standards; different regulatoryenvironments; and different market and economic factors invarious non-U.S. countries. In addition, the securities of small,less well-known companies may be more volatile than those oflarger companies. Investors should refer to the Funds’prospectus for a description of risk factors associated withinvestments in securities held by the Funds.

Tweedy, Browne Global Value Fund, Tweedy, Browne ValueFund, and Tweedy, Browne Worldwide High Dividend YieldValue Fund are distributed by Tweedy, Browne Company LLC.

This material must be preceded or accompanied by a prospectusfor Tweedy, Browne Fund Inc.

TWEEDY, BROWNE FUND INC.

Expense Information

II-5II-5

Hypothetical ExpensesActual Expenses (5% Return Before Expenses)

Expenses Expenses Beginning Ending Paid During Beginning Ending Paid During Account Account Period* Account Account Period*

Value Value 10/1/07 – Value Value 10/1/07 – Expense10/1/07 3/31/08 3/31/08 10/1/07 3/31/08 3/31/08 Ratio

Global Value Fund $1,000 $890 $6.47 $1,000 $1,018 $6.91 1.37%Value Fund $1,000 $900 $6.51 $1,000 $1,018 $6.91 1.37%Worldwide High Dividend

Yield Value Fund (†) $1,000 $962 $6.72 $1,000 $1,018 $6.91 1.37%

(†) The Tweedy, Browne Worldwide High Dividend Yield Value Fund commenced operations on September 5, 2007.

* Expenses are equal to each Fund’s annualized expense ratio, multiplied by the average account value over the period, multiplied by the number of days in the period, divided by 366 (to reflect the one-half year period).

A shareholder of the Global Value Fund, Value Fund orWorldwide High Dividend Yield Value Fund (collectively, the“Funds”) incurs two types of costs: (1) transaction costs and (2)ongoing costs, including management fees and other Fundexpenses. The Example below is intended to help a shareholderunderstand their ongoing costs (in U.S. dollars) of investing inthe Funds and to compare these costs with the ongoing costs ofinvesting in other mutual funds.

The Example is based on an investment of $1,000 investedat the beginning of the period and held for the entire period ofOctober 1, 2007 to March 31, 2008.

Actual Expenses The first part of the table presentedbelow, under the heading “Actual Expenses”, providesinformation about actual account values and actual expenses.The information in this line may be used with the amount ashareholder invested to estimate the expenses that were paid bythe shareholder over the period. Simply divide theshareholder’s account value by $1,000 (for example, an $8,600account value divided by $1,000 = 8.6), then multiply theresult by the number in the first line under the heading entitled“Expenses Paid During Period” to estimate the expenses paidduring this period.

Hypothetical Example for Comparison Purposes Thesecond part of the table presented below, under the heading“Hypothetical Expenses”, provides information about

hypothetical account values and hypothetical expenses basedon each Fund’s actual expense ratio and an assumed rate ofreturn of 5% per year before expenses, which is not each Fund’sactual return. The hypothetical account values and expensesmay not be used to estimate the actual ending account balanceor expenses paid by the shareholder of the Funds for the period.This information may be used to compare the ongoing costs ofinvesting in the Funds and other funds. To do so, compare this5% hypothetical example with the 5% hypothetical examplesthat appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table below aremeant to highlight a shareholder’s ongoing costs only and donot reflect redemption fees. Redemptions from the GlobalValue Fund and the Worldwide High Dividend Yield ValueFund, including exchange redemptions, within 60 days ofpurchase are subject to a redemption fee equal to 2% of theredemption proceeds, which will be retained by the Funds.There are no other transactional expenses associated with thepurchase and sale of shares charged by the Funds, such ascommissions, sales loads and/or redemption fees on shares heldlonger than 60 days. Other mutual funds may have suchtransactional charges. Therefore, the second part of the table isuseful in comparing ongoing costs only, and will not help ashareholder determine the relative total costs of owningdifferent funds. In addition, if redemption fees were included, ashareholder’s costs would have been higher.

TWEEDY, BROWNE GLOBAL VALUE FUND

Portfolio Highlights (Unaudited)

SEE NOTES TO FINANCIAL STATEMENTS

II-6

March 31, 2008Hypothetical Illustration of $10,000 Invested in

Tweedy, Browne Global Value Fund vs. Morgan Stanley Capital International (“MSCI”) Europe, Australasia and Far East (“EAFE”)

Index (in US Dollars and Hedged)6/15/93 through 3/31/08

________________________________________________________________________________________________________________________________________________________________________________________________________________

MSCI EAFE Index represents the change in market capitalizations of Europe, Australasia and the Far East (EAFE), including dividends reinvested monthly, net after foreign withholding taxes.

Index and Average information is available at month end only; therefore, the closest month end to inception date of the Fund, May 31, 1993, has been used.

$52,473

$26,423$28,757

Tweedy, Browne Global Value Fund*Index: MSCI EAFE Index (in US Dollars)*Index: MSCI EAFE Index (Hedged)*

Jun 19

93

Sep 1

993

Mar

1994

Sep 1

994

Mar

1995

Sep 1

995

Mar

1996

Sep 1

996

Mar

1997

Sep 1

997

Mar

1998

Sep 1