Tune Ins (TIH MK) 24 May 2013 See important disclosures at the end of this report 1 Tune Ins (TIH MK) Neutral (Maintained) Financial - Insurance Target Price: MYR2.15 Market Cap: USD506m Price: MYR2.04 Casting The Net Macro ¡¡¡ Risks ¡¡ Growth ¡¡¡ Value ¡ From TIH’s analyst briefing last Thursday, we identified a new catalyst for its online travel insurance business – managing the international travel protection needs of leading Filipino low-cost carrier, Cebu Pacific. In view of the carrier’s regional expansion and AirAsia's expectations of rising contribution from the Philippines, we raise our FY14 earnings forecast by 8.2%. Our new MYR2.15 FV is pegged to 20x FY14 EPS. i Widens travel protection to other airlines. Tune Ins Holdings (TIH) has secured an exclusive five-year partnership with leading Filipino non-life insurer, Malayan Insurance Co (MICO), which manages the domestic travel protection needs of Cebu Pacific Air (CEB). Management guided that the earnings accretion from this deal will not be significant for FY13 as it will only cover the airlines’ flights into the Philippines. CEB current operates mostly domestic flights despite flying to 22 international destinations. That said, TIH is looking to secure more partnerships to extend its services to other airlines, including AirAsia India. i No other foreseeable catalysts. Aside from its tie-up with CEB and its sister company Philippines AirAsia’s tie-up with Zest Air, we do not foresee other catalysts. TIH has carried out plans to rebrand and market its travel insurance products via Google and social media in an effort to boost their take-up rate. We remain neutral on this aspect. Meanwhile, it has identified target acquirees in Thailand, but the plans are still too preliminary at this juncture. Moreover, it prefers to focus first on completing the acquisition of a 70% stake in Indonesian insurer PT Batavia Mitratama Insurance (BMI). i TIMB’s top-line growth flat as expected. Its subsidiary, Tune Insurance Malaysia (TIMB), saw net earned premiums (NEP) fall MYR5.5m to MYR30m in 1QFY13, accounting for 24% of our segmental forecast and in line with our estimates. It did not retain MYR4m in NEP due to the 25% motor quota sharing with Swiss Re. Nonetheless, TIMB’s net profit surged 182% y-o-y, bolstered by positive progress in its business realignment. i Adjusting FV. We see the MICO tie-up as a major catalyst. We adjust our FY14 earnings forecast higher by 8.2% and lift its FV to MYR2.15. We also adjust our management expense ratio higher to 20% vs 18% previously as we think its expenses could continue to remain high. 87 99 110 122 134 145 1.1 1.3 1.5 1.7 1.9 2.1 2.3 Tune Insurance Holdings (TIH MK) Price Close Relative to FTSE Bursa Malaysia KLCI Index (RHS) 20 40 60 80 100 120 Feb-13 Mar-13 Mar-13 Apr-13 Apr-13 May-13 Vol m Source: Bloomberg Avg Turnover (MYR/USD) 2.59m/0.85m Cons. Upside (%) 5.4 Upside (%) 5.2 52-wk Price low/high (MYR) 1.28 - 2.14 Free float (%) 28 Shareholders (%) Tune Money SB 55.9 AirAsia 16.2 Shariah compliant The Research Team +603 9207 7620 [email protected] Forecasts and Valuations Dec-10 Dec-11 Dec-12 Dec-13F Dec-14F Net premium revenue (MYRm) 165 211 217 225 268 Net income to ord equity (MYRm) 30 49 39 61 79 Net profit growth (%) 59.2 66.1 (20.4) 56.1 29.3 Recurrent net profit (MYRm) 30 49 47 61 79 Consensus EPS (MYR) 0.04 0.07 0.06 0.08 0.10 EPS (MYR) 0.04 0.07 0.06 0.08 0.11 DPS (MYR) 0.00 0.00 0.00 0.03 0.04 Dividend Yield (%) - - - 1.5 2.0 Return on average equity (%) - - - 17.8 20.4 Return on average assets (%) - - - 6.7 7.2 P/E (x) 54.3 32.7 33.9 26.3 20.4 P/B (x) - - 14.9 4.4 3.9 P/NTA (x) - - 20.7 4.8 4.2 Source: Company data, RHB Estimates

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Tune Ins (TIH MK) 24 May 2013

See important disclosures at the end of this report 1

Tune Ins (TIH MK) Neutral (Maintained)Financial - Insurance Target Price: MYR2.15

Market Cap: USD506m Price: MYR2.04

Casting The Net

Macro

Risks

Growth

Value

From TIH’s analyst briefing last Thursday, we identified a new catalyst for its online travel insurance business – managing the international travel protection needs of leading Filipino low-cost carrier, Cebu Pacific. In view of the carrier’s regional expansion and AirAsia's expectations of rising contribution from the Philippines, we raise our FY14 earnings forecast by 8.2%. Our new MYR2.15 FV is pegged to 20x FY14 EPS.

Widens travel protection to other airlines. Tune Ins Holdings (TIH) has secured an exclusive five-year partnership with leading Filipino non-life insurer, Malayan Insurance Co (MICO), which manages the domestic travel protection needs of Cebu Pacific Air (CEB). Management guided that the earnings accretion from this deal will not be significant for FY13 as it will only cover the airlines’ flights into the Philippines. CEB current operates mostly domestic flights despite flying to 22 international destinations. That said, TIH is looking to secure more partnerships to extend its services to other airlines, including AirAsia India.

No other foreseeable catalysts. Aside from its tie-up with CEB and its sister company Philippines AirAsia’s tie-up with Zest Air, we do not foresee other catalysts. TIH has carried out plans to rebrand and market its travel insurance products via Google and social media in an effort to boost their take-up rate. We remain neutral on this aspect. Meanwhile, it has identified target acquirees in Thailand, but the plans are still too preliminary at this juncture. Moreover, it prefers to focus first on completing the acquisition of a 70% stake in Indonesian insurer PT Batavia Mitratama Insurance (BMI).

TIMB’s top-line growth flat as expected. Its subsidiary, Tune Insurance Malaysia (TIMB), saw net earned premiums (NEP) fall MYR5.5m to MYR30m in 1QFY13, accounting for 24% of our segmental forecast and in line with our estimates. It did not retain MYR4m in NEP due to the 25% motor quota sharing with Swiss Re. Nonetheless, TIMB’s net profit surged 182% y-o-y, bolstered by positive progress in its business realignment.

Adjusting FV. We see the MICO tie-up as a major catalyst. We adjust our FY14 earnings forecast higher by 8.2% and lift its FV to MYR2.15. We also adjust our management expense ratio higher to 20% vs 18% previously as we think its expenses could continue to remain high.

87

99

110

122

134

145

1.1

1.3

1.5

1.7

1.9

2.1

2.3

Tune Insurance Holdings (TIH MK)

Price Close Relative to FTSE Bursa Malaysia KLCI Index (RHS)

20

40

60

80

100

120

Fe

b-1

3

Ma

r-1

3

Ma

r-1

3

Apr-

13

Apr-

13

Ma

y-1

3

Vol

m

Source: Bloomberg

Avg Turnover (MYR/USD) 2.59m/0.85m

Cons. Upside (%) 5.4

Upside (%) 5.2

52-wk Price low/high (MYR) 1.28 - 2.14

Free float (%) 28

Shareholders (%)

Tune Money SB 55.9

AirAsia 16.2

Shariah compliant

The Research Team +603 9207 7620 [email protected]

Forecasts and Valuations Dec-10 Dec-11 Dec-12 Dec-13F Dec-14F

Net premium revenue (MYRm) 165 211 217 225 268

Net income to ord equity (MYRm) 30 49 39 61 79

Net profit growth (%) 59.2 66.1 (20.4) 56.1 29.3

Recurrent net profit (MYRm) 30 49 47 61 79

Consensus EPS (MYR) 0.04 0.07 0.06 0.08 0.10

EPS (MYR) 0.04 0.07 0.06 0.08 0.11

DPS (MYR) 0.00 0.00 0.00 0.03 0.04

Dividend Yield (%) - - - 1.5 2.0

Return on average equity (%) - - - 17.8 20.4

Return on average assets (%) - - - 6.7 7.2

P/E (x) 54.3 32.7 33.9 26.3 20.4

P/B (x) - - 14.9 4.4 3.9

P/NTA (x) - - 20.7 4.8 4.2 Source: Company data, RHB Estimates

Tune Ins (TIH MK) 24 May 2013

See important disclosures at the end of this report 2

Updates From Analyst Briefing, 23 May 2013

CEB partnership

A major catalyst. The five-year tie up with MICO for Cebu Pacific Air (CEB) marks its first major airline coverage after AirAsia (BUY, FV: MYR3.94). The agreement only covers international flights into Philippines from any of the 15 countries TIH has operations in. CEB currently has flights to 22 international destinations in total. TIH has operations in >10 of these destinations, including Bali, Bangkok, Guangzhou, Hanoi, Ho Chi Minh, Hong Kong, Jakarta, Kota Kinabalu, Kuala Lumpur, Macau, Osaka, Phuket, Shanghai, Singapore and Siem Reap. MICO is CEB’s exclusive partner and it will continue to underwrite insurance for CEB’s domestic flights.

Further tie-ups are possible. TIH is also in talks with other airlines. Although no specific airline was mentioned, Management is of the opinion that many airlines, especially those with multiple operations (eg + hotel operations) will see greater need for insurance partnerships. The agreements will largely be similar to its current agreement with AirAsia, ie it pays commission of about 30% of gross premiums or more to the airline partner if there are no existing regulations on commission expenses.

Average premiums in line with other markets. Based on the CEB’s current travel insurance product called TravelSure, provided by MICO, a passenger subscribing for the insurance will be charged PHP250.00 for a one-way trip and PHP325 for a round trip (with a maximum coverage period of 30 days). This worked out to be about MYR18 for one-way and MYR24 for return, almost consistent with TIH’s product pricing in the markets it operates in, except Australia. We understand that the plan rates for the international routes will be altered to be consistent with TIH’s plan rates, as the insurance plans will be underwritten based on the country of departure. However we believe the transition should not affect customer perception given the similarities in pricing already in place. TravelSure’s insurance benefits are also consistent with TIH’s existing travel products, covering accidents and medical services, recovery of lost travel documents, loss/delay/damage to checked-in baggage, strikes and hijacking, flight delay, trip curtailment and cancellation for medical or legal emergency.

Details on CEB. CEB is a leading low-cost carrier (LCC) in the Philippines and boasts of having the youngest fleet (average of 3.87 years) and the most extensive route network in the country. It launched its Manila-Bali route in March 2013 and is scheduled to launch its direct Manila-Phuket route in Aug 2013. The carrier is looking to fly to more international routes. It has secured air traffic rights to fly to Saudi Arabia, Kuwait and Australia. Although TIH will not able to underwrite travel protection plans for departures from countries it has no operations in, we think CEB’s regional route expansion still bodes well for its business.

Leveraging on the Philippines’ consumer growth. We are positive on this partnership as we believe CEB and TIH are well positioned to gain from the growth potential of the Filipino consumer spending. Although CEB controls nearly half of the domestic market, TIH will not gain from this strength, as its agreement with MICO is only for flights into the country. Meanwhile, the airline’s international passenger numbers are still relatively small, at slightly above 20% of its overall passengers, but growth had been strong and we continue to see promising numbers from this segment. In 1QFY13, CEB’s international passenger growth rates were strong in Brunei (43%), South Korea (34%), Malaysia (18%), China (15%) and Indonesia (13%), due to increased flight frequencies and promotion packages. We also believe that CEB may have benefited from the sizeable Overseas Filipino Workers (OFWs) market, especially those working in Asean and hence need to travel frequently. We noted that CEB frequently launches campaigns to lure OFWs to fly with it to and fro popular destinations such as Hong Kong.

TIH has widened its reach to other airlines, mitigating the risks of over-reliance on sister company AirAsia

Premiums pricing similar with TIH’s other Asean markets.

CEB is a leading LCC in the Philippines. It boasts of having the youngest fleet and the most extensive route network in the country.

CEB’s international reach, albeit relatively small, is poised for strong growth. And TIH stands to benefit from that expansion. We believe tourists and OFWs play a part in promoting growth in this segment.

Tune Ins (TIH MK) 24 May 2013

See important disclosures at the end of this report 3

Figure 1: Cebu Pacific Air’s passenger growth

Source: Cebu Pacific Air

Figure 2: FY12 comparison of Cebu Pacific Air (CEB), Philippines AirAsia and selected airlines

Source: Cebu Pacific Air

Figure 3: CEB’s fleet expansion plan

Source: Cebu Pacific Air

Tune Ins (TIH MK) 24 May 2013

See important disclosures at the end of this report 4

Figure 4: CEB’s main website

Source: Cebu Pacific Air

Tune Ins (TIH MK) 24 May 2013

See important disclosures at the end of this report 5

Diversifying income streams

Online biz getting more regional. To date, about 54% of TIH’s online business is sourced from foreign markets. Viewing it from a geographical perspective, the online premium portfolio is now more diversified (FY12: 47% of premium portfolio). This is consistent with AirAsia’s regional expansion, on which TIH is able to leverage to introduce its travel products into new markets.

Figure 5: TIH’s online business - 1.7m policies sold in 1QFY13 Figure 6: TIH’s online business - 1.3m policies sold in FY12

Malaysia, 46%

Thailand, 21%

Indonesia, 15%

Singapore, 5%

China, 7%Others,

6%

Malaysia, 53%Thailand,

22%

Indonesia, 11%

Singapore, 7%

China, 4% Others, 3%

Source: Company Source: Company

TIMB’s premiums portfolio now more balanced. TIMB had realigned its focus to improve bottomline profitability, starting by encouraging its agents to enhance sales of its non-motor business. Therefore, while its agent base has not deviate much in size – from 1,023 in 2012 to the current 1,078 – its 1QFY13 results demonstrated significant progress, thanks to its business realignment. TIMB’s motor portfolio had shrunk from 48.2% to 27% within the quarter, faster than our expectations. The current general insurance (GI) portfolio mix looks well-balanced, leaving TIMB plenty of room to expand its motor portfolio again in the future if needed. We believe this had also helped improve TIMB’s capital adequacy ratio (CAR) to 240%.

Figure 7: TIMB’s premiums portfolio in 1QFY13 Figure 8: TIMB’s premiums portfolio in FY12

Motor, 27%

Fire, 22%

Marine, 12%

PA & Health,

22%

Misc, 17%

Motor, 48%

Fire, 9%

Marine, 25%

PA & Health,

11%

Misc, 7%

Source: Company Source: Company

Malaysia’s contribution is now reduced to 46% from 53% in FY12. The company is demonstrating geographical diversification.

TIMB had reduced its motor portfolio at a rate that is faster than our expectations.

Tune Ins (TIH MK) 24 May 2013

See important disclosures at the end of this report 6

Claims continued improving. Claims ratio continued to improve to 41.8% (vs 45.9% in FY12 proforma). By segment, the online claims ratio was slightly higher at 3.9%, while TIMB’s claims ratio was at 68.9%. This was due to improved claims management, a more balanced GI premium mix with more low-claim products, and the 25% motor quota sharing agreement with Swiss Re. This was despite recognition of MYR1.95m for Malaysian Motor and Insurance Pool (MMIP) losses. If TIMB continues to improve its claims ratios, and if the online business grows more in proportion to TIH’s total business, we expect claims ratio to improve significantly.

More MMIP provision expected. Management guided that the MMIP provision of MYR1.9m is short of its FY13 provision of MYR2.4m (FY12: MYR7.8m). Therefore we expect another MYR0.5m of MMIP provision to be recognized in 2QFY13. However, Management shared that the company will be entitled to a double tax relief that may amount to >MYR2m.

Management expenses remained high. 1Q13 Group management expense (ME) ratio was high at 22.2%, with online ME ratio at 16.2%, a surge from 10.9% in FY12. TIH incurred MYR1.4m in ME due to additional personnel and marketing expenses. It also incurred some expenses for the due diligence of its proposed acquisition of Indonesia’s BMI and for RAM Rating’s assessment. TIMB’s ME ratio also spiked to 21.9% from 19.4% in FY12 due to a few personnel changes in the Management team and the reduction in NEP. While we expect the NEP to pick up pace, partly due to the strong growth potential of its low-claims online business, we are increasing our ME ratio assumption from 18% to 20% for FY13 and FY14 as expenses may likely remain high. Hence, we think the ME ratio should normalize to our new assumption.

Claims ratios improved, despite a recognition of MYR1.95m for MMIP losses

An additional MYR0.5m MMIP provision may be expected in 2QFY13

ME was high in 1QFY13. The ME ratio is expected to normalize once NEP growth catches up

Tune Ins (TIH MK) 24 May 2013

See important disclosures at the end of this report 7

Financial Exhibits

Profit & Loss (MYRm) Dec-10 Dec-11 Dec-12 Dec-13F Dec-14F

Premium income from insurance policies 288 301 322 357 400

Reinsurance ceded (122) (90) (105) (132) (132)

Net premium revenue 165 211 217 225 268

Total insurance premium revenue 165 211 217 225 268

Gain on securities and other fin assets 16 24 26 30 34

Net investment income 16 24 26 30 34

Total operating income 182 235 244 255 301

Claims, maturities & surrenders (94) (110) (100) (78) (78)

Agents' comissions (23) (30) (31) (34) (44)

Management fees (23) (24) (41) (45) (54)

Other operating costs 0 (2) (4) (2) (2)

Cash operating costs (139) (166) (175) (159) (178)

Total costs (139) (166) (175) (159) (178)

Operating profit 42 69 68 95 123

Other exceptional items 0 0 (10) 0 0

Non recurring items 0 0 (10) 0 0

Pre-tax profit 42 69 58 95 123

Taxation (6) (9) (10) (19) (25)

Minority interests (7) (11) (9) (15) (20)

Profit after tax & minorities 30 49 39 61 79

Net income to ord equity 30 49 39 61 79

Recurring net profit 30 49 47 61 79 Source: Company data, RHB Estimates

Key Ratios Dec-10 Dec-11 Dec-12 Dec-13F Dec-14F

Reinsurance ratio (%) 42.5 30.0 32.5 37.8 34.0

Retention ratio (%) 57.5 70.0 67.5 62.2 66.0

Claims ratio (%) 56.6 52.1 45.9 36.2 30.6

Commission ratio (%) 13.6 14.1 14.2 15.3 16.5

Expense ratio (%) 14.0 12.4 20.5 18.9 18.8

Combined ratio (%) 84.3 78.6 80.6 70.4 65.9

Underwriting margin (%) 15.7 21.4 19.4 29.6 34.1

Investment yield (%) 0.0 0.0 5.5 0.1 0.1

Liquidity ratio (%) 0.0 0.0 9.8 0.8 0.7

Return on average equity (%) 0.0 0.0 0.0 17.8 20.4

Return on average assets (%) 0.0 0.0 0.0 6.7 7.2

EPS growth (%) 59.2 66.1 (20.4) 56.3 29.4

Bv per share growth (%) 0.0 0.0 0.0 237.9 13.1

Operating profit growth (%) 64.1 63.7 (1.0) 39.5 29.4 Source: Company data, RHB Estimates

We believe the Group's top-line growth will continue to be driven by the strong latent potential of online premiums. We believe that TIMB's top-line growth is not likely to pick up yet, as Management is more focused on boosting bottomline growth.

We expect Group claims ratio to be better than the industry’s as we project an increase in the proportion of low-claims online travel insurance premiums to total premiums. The online claims ratio was historically at

3.6%

Tune Ins (TIH MK) 24 May 2013

See important disclosures at the end of this report 8

Financial Exhibits

Balance Sheet (MYRm) Dec-10 Dec-11 Dec-12 Dec-13F Dec-14F

Cash at bank - - 23 93 102

Total current assets - - 23 93 102

Total investments - - 477 529 592

Tangible fixed assets - - 10 10 10

Intangible assets - - 30 30 30

Premiums receivable - - 76 84 94

Debtors & prepayments - - 37 94 139

Other assets - - 160 178 199

Total other assets - - 273 356 432

Total assets - - 813 1,019 1,166

Total current liabilities - - 231 117 139

Technical provisions - - 440 488 546

Long term insurance liabilities - - 440 488 546

Total non-current liabilities - - 2 2 3

Total liabilities - - 673 608 688

Share premium account - - 0 199 199

Revaluation reserve - - (0) 5 5

Other reserves - - (28) (14) (14)

Total reserves - - 47 266 266

Shareholders' equity - - 108 364 411

Minority interests - - 32 47 67

Total equity - - 140 411 478 Source: Company data, RHB Estimates

Key Ratios (MYR) Dec-10 Dec-11 Dec-12 Dec-13F Dec-14F

Operating profit growth (%) 64.1 63.7 (1.0) 39.5 29.4

Net profit growth (%) 59.2 66.1 (20.4) 56.3 29.4

EPS growth (%) 59.2 66.1 (3.6) 28.9 29.4

Bv per share growth (%) 0.0 0.0 0.0 237.9 13.1

Return on average assets (%) - - - 6.7 7.2

Return on average equity (%) - - - 17.8 20.4

DPS 0.00 0.00 0.00 0.03 0.04 Source: Company data, RHB Estimates

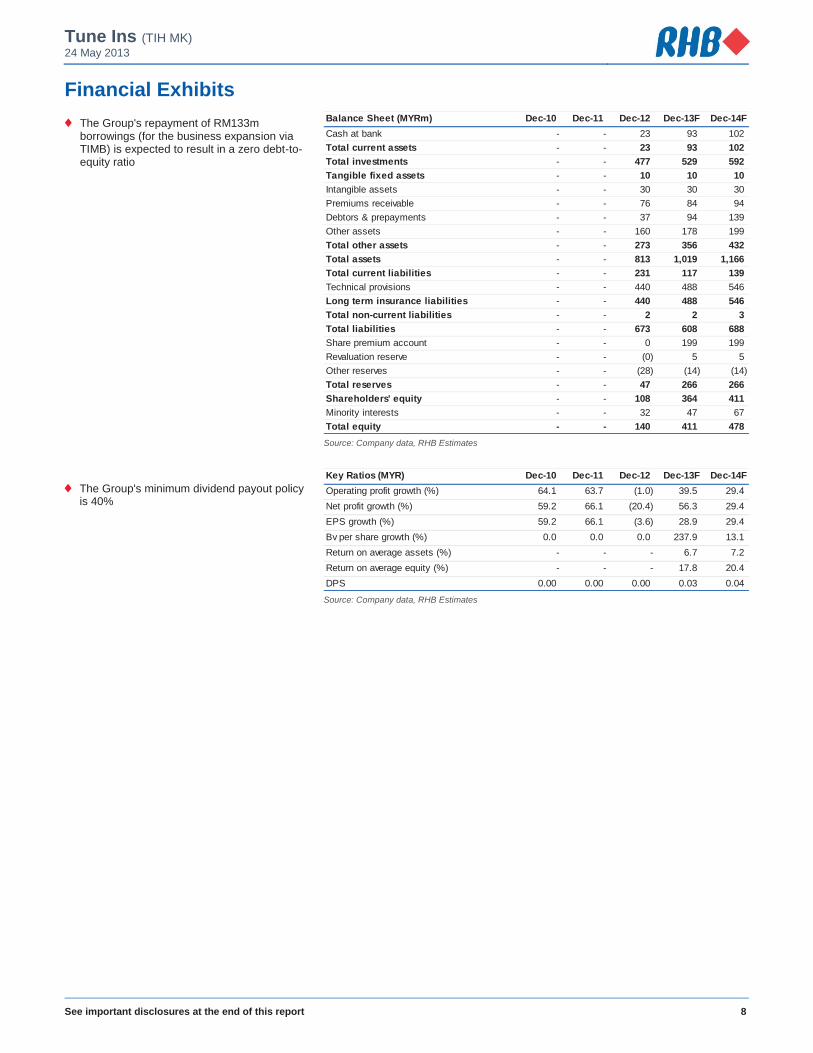

The Group's repayment of RM133m borrowings (for the business expansion via TIMB) is expected to result in a zero debt-to- equity ratio

The Group's minimum dividend payout policy is 40%

Tune Ins (TIH MK) 24 May 2013

See important disclosures at the end of this report 9

SWOT Analysis

Growing its highly profitable online insurance business segment

Embarking on key strategies to improve the efficiency and underwriting profitability of TIMB

Improving capital adequacy ratios at the TIMB level

Competition will intensify in tandem with liberalisation and detariffication

Regulatory changes could affect agency and other operating costs

Natural calamities and severe pandemic i.e. SARS could affect air travel and TIH's take-up rate

Opportunities to expand into new markets via M&As and through AirAsia's expansion

Opportunities to improve take-up rates

Expansion into other distribution channels

Small market share within the total general insurance market and total agency force

Highly dependent on the quality of service, both of its own and that of AirAsia

Claims expenses could be volatile

Figure 9 Figure 10

-30%

-18%

-6%

7%

19%

31%

43%

56%

68%

80%

0

10

20

30

40

50

60

70

80

90

Jan

-10

Jan

-11

Jan

-12

Jan

-13

Jan

-14

P/E (x) vs EPS growth

P/E (x) (lhs) EPS growth (rhs)

0

20

40

60

80

100

120

140

160

180

Jan

-10

Jan

-11

Jan

-12

Jan

-13

Jan

-14

P/BV (x) vs ROAE

P/B (x) (lhs) Return on average equity (rhs)

Source: Company data, RHB Estimates Source: Company data, RHB Estimates

Company Profile Tune Ins Holdings, an investment holding company, engages in the provision of various general and life insurance products in Asia Pacific. The company offers a range of online insurance products, including travel, lifestyle protection, and guest personal accident insurance products.

Re-rating catalysts:-

Higher than expected take-up rate for the online business

Higher than expected improvement in general insurance (GI) claims ratio

Higher than expected growth in GI premiums with controlled levels of expenses and claims

Potential acquisition opportunities

New customer segment

TIMB posting better than expected profitability

Higher dividend payouts

Tune Ins (TIH MK) 24 May 2013

See important disclosures at the end of this report 10

Recommendation Chart

1.2

1.3

1.4

1.5

1.6

1.7

1.8

1.9

2.0

2.1

Feb-13 Mar-13 Apr-13 May-13

Price Close

NR

1.75

1.7

5

2.0

5 Recommendations & Target Price

Buy Neutral Sell Trading Buy Take Profit Not Rated

Source: RHB Estimates, Bloomberg

Date Recommendation Target Price Price

2013-05-23 Neutral 2.15 2.04

2013-05-22 Buy 2.05 2.08

2013-05-20 Neutral 2.05 2.06

2013-05-08 Buy 2.05 1.73

2013-05-02 Buy 1.75 1.48

2013-04-02 Buy 1.75 1.45 Source : RHB Estimates, Bloomberg

11

RHB Guide to Investment Ratings Buy: Share price may exceed 10% over the next 12 months Trading Buy: Share price may exceed 15% over the next 3 months, however longer-term outlook remains uncertain Neutral: Share price may fall within the range of +/- 10% over the next 12 months Take Profit: Target price has been attained. Look to accumulate at lower levels Sell: Share price may fall by more than 10% over the next 12 months Not Rated: Stock is not within regular research coverage Disclosure & Disclaimer All research is based on material compiled from data considered to be reliable at the time of writing, but RHB does not make any representation or warranty, express or implied, as to its accuracy, completeness or correctness. No part of this report is to be construed as an offer or solicitation of an offer to transact any securities or financial instruments whether referred to herein or otherwise. This report is general in nature and has been prepared for information purposes only. It is intended for circulation to the clients of RHB and its related companies. Any recommendation contained in this report does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. This report is for the information of addressees only and is not to be taken in substitution for the exercise of judgment by addressees, who should obtain separate legal or financial advice to independently evaluate the particular investments and strategies. RHB, its affiliates and related companies, their respective directors, associates, connected parties and/or employees may own or have positions in securities of the company(ies) covered in this research report or any securities related thereto, and may from time to time add to, or dispose off, or may be materially interested in any such securities. Further, RHB, its affiliates and related companies do and seek to do business with the company(ies) covered in this research report and may from time to time act as market maker or have assumed an underwriting commitment in securities of such company(ies), may sell them or buy them from customers on a principal basis and may also perform or seek to perform significant investment banking, advisory or underwriting services for or relating to such company(ies), as well as solicit such investment, advisory or other services from any entity mentioned in this research report. RHB and its employees and/or agents do not accept any liability, be it directly, indirectly or consequential losses, loss of profits or damages that may arise from any reliance based on this report or further communication given in relation to this report, including where such losses, loss of profits or damages are alleged to have arisen due to the contents of such report or communication being perceived as defamatory in nature. The term “RHB” shall denote where applicable, the relevant entity distributing the report in the particular jurisdiction mentioned specifically herein below and shall refer to RHB Research Institute Sdn Bhd, its holding company, affiliates, subsidiaries and related companies. All Rights Reserved. This report is for the use of intended recipients only and may not be reproduced, distributed or published for any purpose without prior consent of RHB and RHB accepts no liability whatsoever for the actions of third parties in this respect. Malaysia This report is published and distributed in Malaysia by RHB Research Institute Sdn Bhd (233327-M), Level 11, Tower One, RHB Centre, Jalan Tun Razak, 50400 Kuala Lumpur, a wholly-owned subsidiary of RHB Investment Bank Berhad (RHBIB), which in turn is a wholly-owned subsidiary of RHB Capital Berhad. Singapore This report is published and distributed in Singapore by DMG & Partners Research Pte Ltd (Reg. No. 200808705N), a wholly-owned subsidiary of DMG & Partners Securities Pte Ltd, a joint venture between Deutsche Asia Pacific Holdings Pte Ltd (a subsidiary of Deutsche Bank Group) and OSK Investment Bank Berhad, Malaysia which have since merged into RHB Investment Bank Berhad (the merged entity is referred to as “RHBIB”, which in turn is a wholly-owned subsidiary of RHB Capital Berhad). DMG & Partners Securities Pte Ltd is a Member of the Singapore Exchange Securities Trading Limited. DMG & Partners Securities Pte Ltd may have received compensation from the company covered in this report for its corporate finance or its dealing activities; this report is therefore classified as a non-independent report. As of 23 May 2013, DMG & Partners Securities Pte Ltd and its subsidiaries, including DMG & Partners Research Pte Ltd do not have proprietary positions in the securities covered in this report, except for: a) - As of 23 May 2013, none of the analysts who covered the securities in this report has an interest in such securities, except for: a) Tune Ins Holdings Bhd Special Distribution by RHB Where the research report is produced by an RHB entity (excluding DMG & Partners Research Pte Ltd) and distributed in Singapore, it is only distributed to "Institutional Investors", "Expert Investors" or "Accredited Investors" as defined in the Securities and Futures Act, CAP. 289 of Singapore. If you are not an "Institutional Investor", "Expert Investor" or "Accredited Investor", this research report is not intended for you and you should disregard this research report in its entirety. In respect of any matters arising from, or in connection with this research report, you are to contact our Singapore Office, DMG & Partners Securities Pte Ltd. Hong Kong This report is published and distributed in Hong Kong by RHB OSK Securities Hong Kong Limited (“RHBSHK”) (formerly known as OSK Securities Hong Kong Limited), a subsidiary of OSK Investment Bank Berhad, Malaysia which have since merged into RHB Investment Bank Berhad (the merged entity is referred to as “RHBIB”), which in turn is a wholly-owned subsidiary of RHB Capital Berhad. RHBSHK, RHBIB and/or other affiliates may beneficially own a total of 1% or more of any class of common equity securities of the subject company. RHBSHK, RHBIB and/or other affiliates may, within the past 12 months, have received compensation and/or within the next 3 months seek to obtain compensation for investment banking services from the subject company.

12

Risk Disclosure Statements The prices of securities fluctuate, sometimes dramatically. The price of a security may move up or down, and may become valueless. It is as likely that losses will be incurred rather than profit made as a result of buying and selling securities. Past performance is not a guide to future performance. RHBSHK does not maintain a predetermined schedule for publication of research and will not necessarily update this report Indonesia This report is published and distributed in Indonesia by PT RHB OSK Securities Indonesia (formerly known as PT OSK Nusadana Securities Indonesia), a subsidiary of OSK Investment Bank Berhad, Malaysia, which have since merged into RHB Investment Bank Berhad, which in turn is a wholly-owned subsidiary of RHB Capital Berhad. Thailand This report is published and distributed in Thailand by RHB OSK Securities (Thailand) PCL (formerly known as OSK Securities (Thailand) PCL), a subsidiary of OSK Investment Bank Berhad, Malaysia, which have since merged into RHB Investment Bank Berhad, which in turn is a wholly-owned subsidiary of RHB Capital Berhad. Other Jurisdictions In any other jurisdictions, this report is intended to be distributed to qualified, accredited and professional investors, in compliance with the law and regulations of the jurisdictions.

Kuala Lumpur Hong Kong Singapore

Malaysia Research Office

RHB Research Institute Sdn Bhd Level 11, Tower One, RHB Centre

Jalan Tun Razak Kuala Lumpur

Malaysia Tel : +(60) 3 9280 2185 Fax : +(60) 3 9284 8693

RHB OSK Securities Hong Kong Ltd.

(formerly known as OSK Securities Hong Kong Ltd.) 12th Floor

World-Wide House 19 Des Voeux Road Central, Hong Kong

Tel : +(852) 2525 1118 Fax : +(852) 2810 0908

DMG & Partners

Securities Pte. Ltd. 10 Collyer Quay

#09-08 Ocean Financial Centre Singapore 049315

Tel : +(65) 6533 1818 Fax : +(65) 6532 6211

Jakarta Shanghai Phnom Penh

PT RHB OSK Securities Indonesia

(formerly known as PT OSK Nusadana Securities Indonesia)

Plaza CIMB Niaga 14th Floor

Jl. Jend. Sudirman Kav.25 Jakarta Selatan 12920, Indonesia

Tel : +(6221) 2598 6888 Fax : +(6221) 2598 6777

RHB OSK (China) Investment Advisory Co. Ltd.

(formerly known as OSK (China) Investment Advisory Co. Ltd.)

Suite 4005, CITIC Square 1168 Nanjing West Road

Shanghai 20041 China

Tel : +(8621) 6288 9611 Fax : +(8621) 6288 9633

RHB OSK Indochina Securities Limited

(formerly known as OSK Indochina Securities Limited) No. 1-3, Street 271

Sangkat Toeuk Thla, Khan Sen Sok Phnom Penh

Cambodia Tel: +(855) 23 969 161 Fax: +(855) 23 969 171

Bangkok

RHB OSK Securities (Thailand) PCL

(formerly known as OSK Securities (Thailand) PCL) 10th Floor, Sathorn Square Office Tower

98, North Sathorn Road,Silom Bangrak, Bangkok 10500

Thailand Tel: +(66) 862 9999 Fax : +(66) 108 0999

This area is for use by EFA and will not be shown when printed Neutral Neutral Maintained| NO RHB Estimates 2.15

Related Documents

![[ TOPIC ] Introduction to Real Estate Investment Trust ...ir.chartnexus.com/sunwayreit/docs/presentation/Market Chat(Apr 2012... · Introduction to Real Estate Investment Trust ...](https://static.cupdf.com/doc/110x72/5ae948df7f8b9aee07909e05/-topic-introduction-to-real-estate-investment-trust-ir-chatapr-2012introduction.jpg)