EQUITY RESEARCH REPORT Tulip Telecom Ltd. NSE: TULIP; BSE: 532691 ISIN: INE122H01027; Reuters: TULP.BO; Bloomberg Ticker: TTSL:IN Target Price: Rs. 170 by June 2013 Potential Upside: 48%+ in 1 year; Rating: Buy Originally Prepared on May 23rd 2012 Quote: Rs. 70 Updated on July 20th 2012, Current Market Price: Rs. 115 Century Partners For Queries Kindly Write To: [email protected]

Tulip Telecom May 23rd 2012 CP

Oct 26, 2014

Research Report

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

EQUITY RESEARCH REPORT

Tulip Telecom Ltd.NSE: TULIP; BSE: 532691

ISIN: INE122H01027; Reuters: TULP.BO; Bloomberg Ticker: TTSL:IN

Target Price: Rs. 170 by June 2013 Potential Upside: 48%+ in 1 year; Rating: Buy

Originally Prepared on May 23rd 2012 Quote: Rs. 70Updated on July 20th 2012, Current Market Price: Rs. 115

Century PartnersFor Queries Kindly Write To: [email protected]

Tulip Telecom (BSE: 532691) Century Partners; MNSector: Telecommunications- ServicePrepared on: May 23rd 2012, Quote: Rs. 70; Rating: BuyUpdated on Jul 20th 2012, Current Market Price: Rs. 115; Re-Rating: Buy

Head Office: New Delhi, India; Established: 1992

Recommendation: Buy, Target Price: Rs. 170 by June 2013

● We believe considering the Margin Of Safety of 48%, present price per share of Tulip Telecom Ltd. at Rs. 115 (Jul 20th, 2012) is undervalued by a considerable margin to it's Intrinsic Value of Rs. 170.

● We think in an emerging market like India there is lot of room for growth in the Enterprise Data Services (EDS) segment just to come at par with the global benchmark. Tulip Telecom's able management has positioned itself well to take advantage of this growth opportunity.

Conversions: $1 = Rs. 55; Rs. 1 Crore = $181,000; 1Cr = 10 million, 1 Lakh = 100,000

Intrinsic Value (from DCF Analysis): Rs. 170

Margin of Safety: 48% Risk: Low Current Price: Rs. 115

Avg. Daily Volume: $1mm+ 52 Week Range: Rs. 70 - Rs. 167

Market Cap: Rs. 1730 Cr ($314million)

Revenues 2011: Rs. 2350Cr ($427mm)

EPS: Rs. 21.74 P/B: 1.13 P/E: 5.5 (Avg. P/E of Last 6 years: 10)

EV/EBITDA: 4.9 (Avg. EV/EBITDA of Last 6 years: 7)

Margins (EBITDA: 29%, PAT: 13%)

Debt/Equity: 1.44 EBITDA 5Yr. Avg.: 15%

ROE: 26% Div & Yield: Rs. 1.54 (1.34%)

Total Income 5Yr. Growth Rate: 18%

Current Ratio: 2.04 Quick Ratio: 3.63 Book Value/Share: Rs.105

ROCE: 20% Share Holding:Promoters Holdings: 69.9%

Institutional: 20.3%

INVESTMENT THESIS

We think that Tulip Telecom has placed itself into a leading position by becoming a Enterprise Data Services provider from Enterprise Data Connectivity provider. Tulip Telecom being the Asia's largest Data Center and owning the largest fiber last mile network (4,000 kms) in the country provides the company a big competitive advantage over it's competitors. Managements drive to shift product mix to Data Connectivity with Fiber Optics has helped the company in improving EBITDA Margins. Acquisition of Data Center (0.9million sqft) in Bengaluru during Feb 2012 is going to improve margins when operating close to its peak Capacity Utilization by next year. In the Connectivity Segment Company's Business Model is to purchase bandwidth in bulk at a lower per unit cost, deploy Economies of Scale as more customers opts for connection on Fiber Optics and hence improve their margins. Tulip Telcom has diverse but well balanced product mix which is visible from company's recent quarters financials, Data Connectivity formed ~ 64% of total revenues, Managed Services (including Data Center) formed ~ 27% whereas Network Integration contributed ~ 9% to total revenues. On valuation front company is selling at a significant lower multiples relative to it's historic average and peers. Both the undervalued part combined with high growth opportunity in this space makes it a good investment opportunity for investors.

Catalyst: Qualcomm’s BWA venture (in which Tulip holds 13% stake) has been allotted Spectrum. This will help to bring in an operator partner to roll-out the network & enable stake sale in the venture by Tulip. So possibility of unlocking value in Qualcomm venture and ability to bring in a strategic partner at the Data Centre level can act as a trigger.

With an experienced management and company's strong & diverse revenue streams and present undervalued status leads us to provide a Buy Rating on Tulip Telecom Ltd. with a one year time horizon.

RISKSIf India's economy slowed down that may lead to reduced customer spending and can affect company's revenues in the short run.

The management is in advance stage of deal closures with the bankers and is confident to raise funds for the Aug 2012 redemption of FCCB. Ability of the company to get the debt at reasonable rate is going to be of importance in avoiding higher interest rate cost and maintaining a stable capital structure.

TULIP TELECOM QUALIFIES ON OUR BASIC VALUATION CRITERIA

● Valuation of a company primarily involves Earnings, Growth Rate and Cost of Capital● Price = Avg. Earnings (Last 5yrs)/(Cost of Capital - Growth Rate) = Rs. 12/ (13 - 6) = Rs. 171● Sales & Earnings Growth (last 5yrs) > 15%, Low PEG Ratio, High Earnings/PBV Ratio● Return on Retained Earnings > 15%; Initial Rate of Return > 20%● Market Capital close to Book value, Return On Equity > 20%, Return On Asset > 15%,● Return On Invested Capital > 15%, Earnings Yield > 15%, Current Ratio > 2, Debt/Equity ~ 1● Present P/E < 0.75 * Historical P/E (Average of last 5 years)● Good Credit Rating, Insider Share Buybacks, Stable Capital Structure, Stable Inventory Turnover

Tulip Telecom qualifies well on our above mentioned basic criteria to find undervalued & growing companies.

Expected Value from DCF of Rs. 170 in 1 year provides us a ROR of well over 30%+ It also qualifies the Hurdle Rate > 2 * Long Term Govt. Bond Yield (7.5%) of 15%. Book Value of Tulip Telecom is on continuous rise which will ensure that the Intrinsic Value of Rs. 170 should be reached soon.

FINAL CHECKLIST FOR TULIP TELECOM

● Business: Understandable, Economic Moat, Growth Potential, No Catastrophic Risk● Customers: Stickiness to The Company, Loyalty● Suppliers: Relationship With The Company● Management: Intellect, Initiative and Integrity (3I's)● Board of Directors: Background of The Members● Financial: ROE, ROIC and Other Ratios, Capital Structure● Value: Earnings vs. Value, Margin Of Safety

Tulip Telecom does very well on all of the above mentioned Valuation and Final Checklist Criteria, hence we issue a Buy Rating on Tulip Telecom Limited.

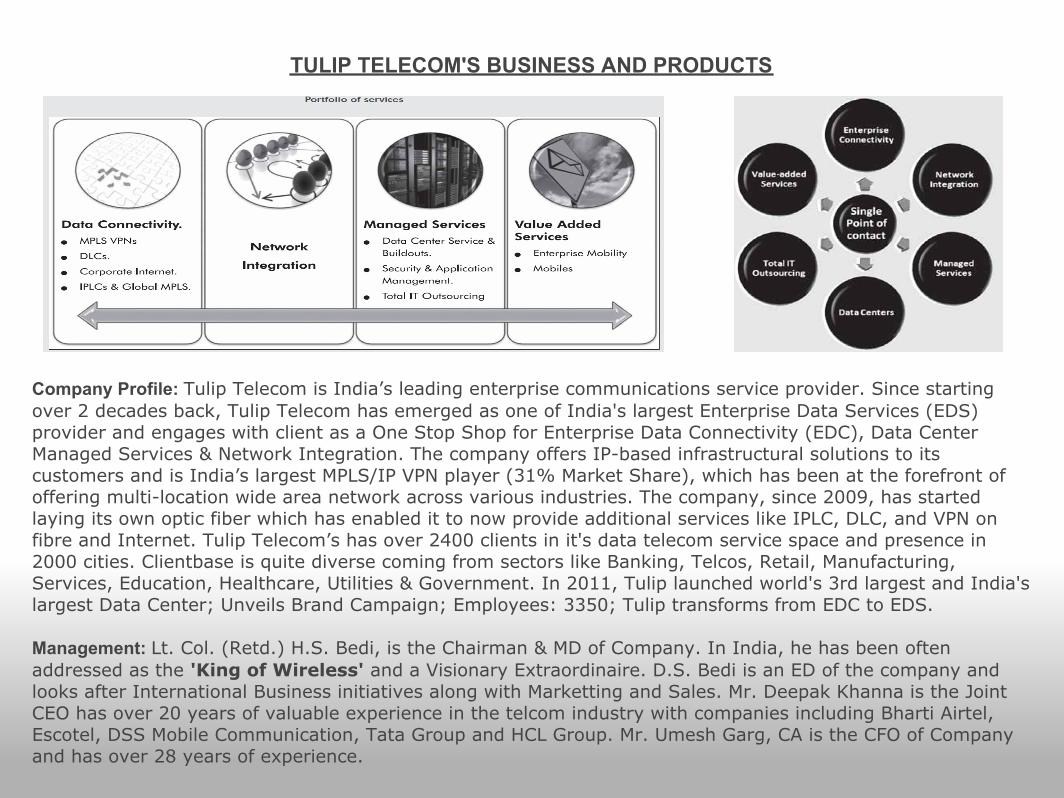

TULIP TELECOM'S BUSINESS AND PRODUCTS

Company Profile: Tulip Telecom is India’s leading enterprise communications service provider. Since starting over 2 decades back, Tulip Telecom has emerged as one of India's largest Enterprise Data Services (EDS) provider and engages with client as a One Stop Shop for Enterprise Data Connectivity (EDC), Data Center Managed Services & Network Integration. The company offers IP-based infrastructural solutions to its customers and is India’s largest MPLS/IP VPN player (31% Market Share), which has been at the forefront of offering multi-location wide area network across various industries. The company, since 2009, has started laying its own optic fiber which has enabled it to now provide additional services like IPLC, DLC, and VPN on fibre and Internet. Tulip Telecom’s has over 2400 clients in it's data telecom service space and presence in 2000 cities. Clientbase is quite diverse coming from sectors like Banking, Telcos, Retail, Manufacturing, Services, Education, Healthcare, Utilities & Government. In 2011, Tulip launched world's 3rd largest and India's largest Data Center; Unveils Brand Campaign; Employees: 3350; Tulip transforms from EDC to EDS.

Management: Lt. Col. (Retd.) H.S. Bedi, is the Chairman & MD of Company. In India, he has been often addressed as the 'King of Wireless' and a Visionary Extraordinaire. D.S. Bedi is an ED of the company and looks after International Business initiatives along with Marketting and Sales. Mr. Deepak Khanna is the Joint CEO has over 20 years of valuable experience in the telcom industry with companies including Bharti Airtel, Escotel, DSS Mobile Communication, Tata Group and HCL Group. Mr. Umesh Garg, CA is the CFO of Company and has over 28 years of experience.

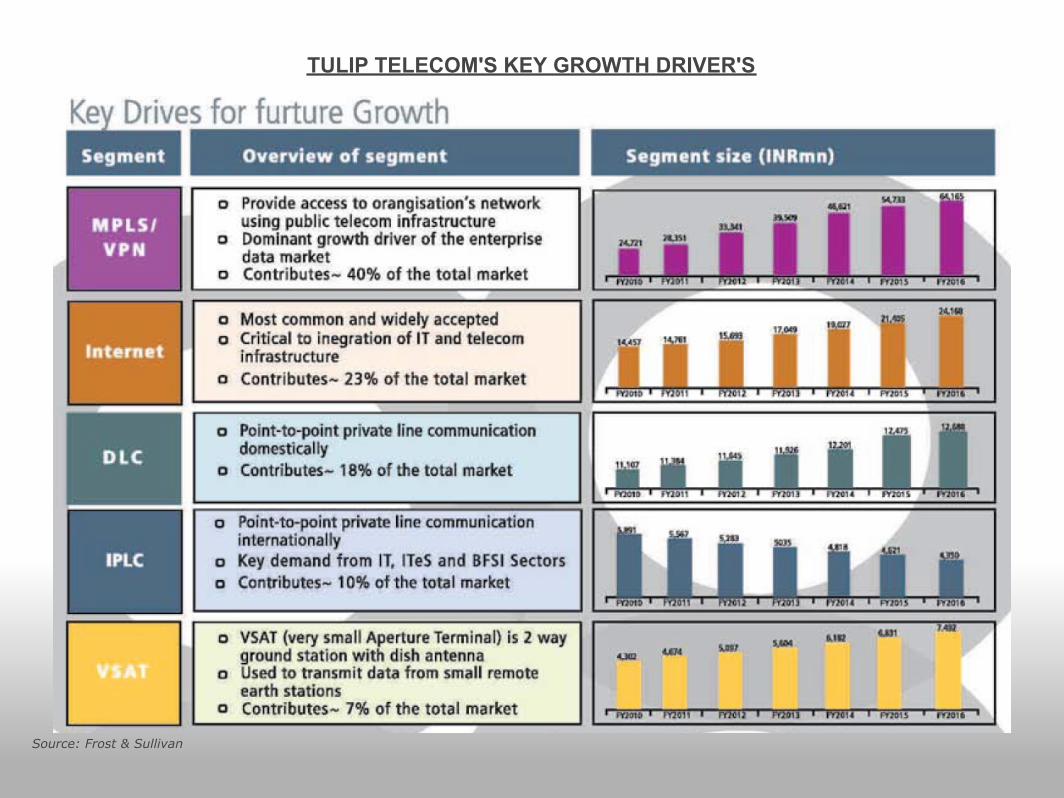

TULIP TELECOM'S KEY GROWTH DRIVER'S

Source: Frost & Sullivan

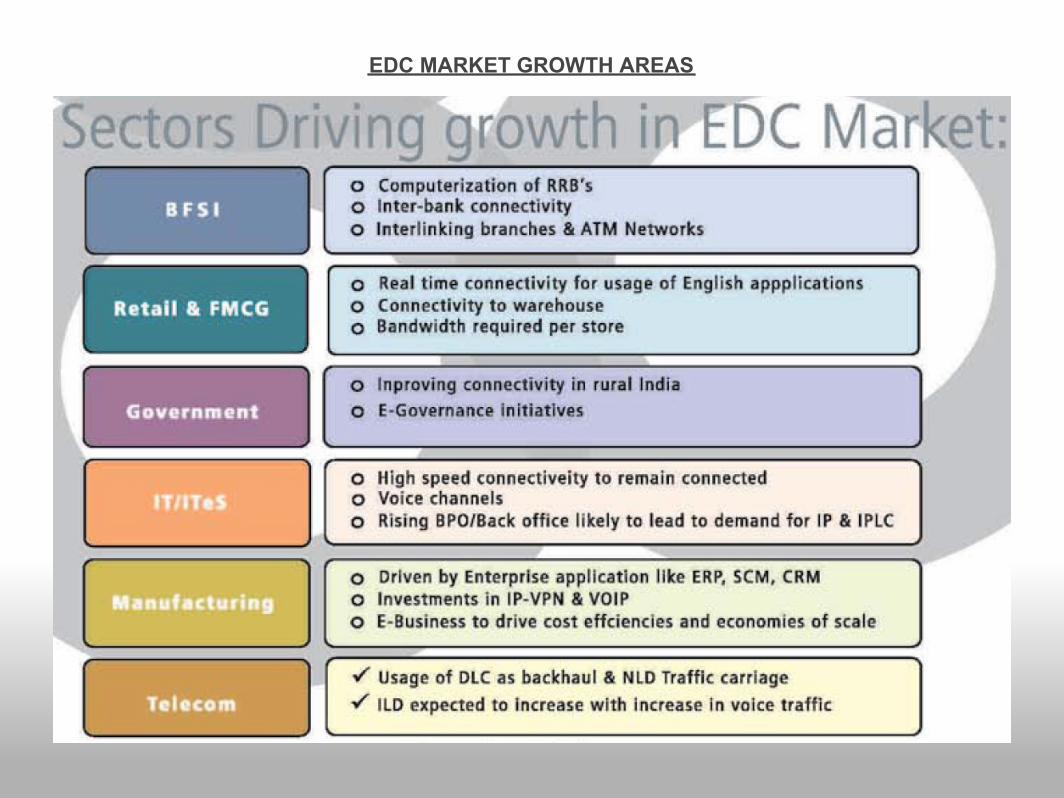

EDC MARKET GROWTH AREAS

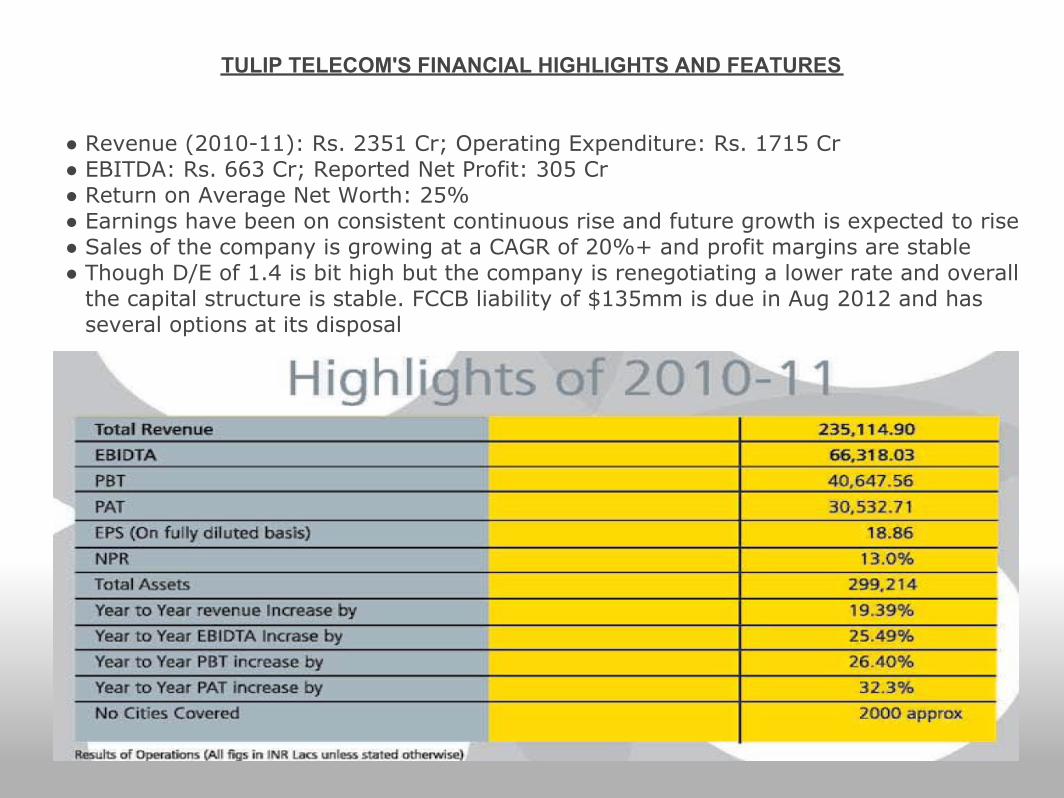

TULIP TELECOM'S FINANCIAL HIGHLIGHTS AND FEATURES

● Revenue (2010-11): Rs. 2351 Cr; Operating Expenditure: Rs. 1715 Cr● EBITDA: Rs. 663 Cr; Reported Net Profit: 305 Cr● Return on Average Net Worth: 25%● Earnings have been on consistent continuous rise and future growth is expected to rise● Sales of the company is growing at a CAGR of 20%+ and profit margins are stable● Though D/E of 1.4 is bit high but the company is renegotiating a lower rate and overall

the capital structure is stable. FCCB liability of $135mm is due in Aug 2012 and has several options at its disposal

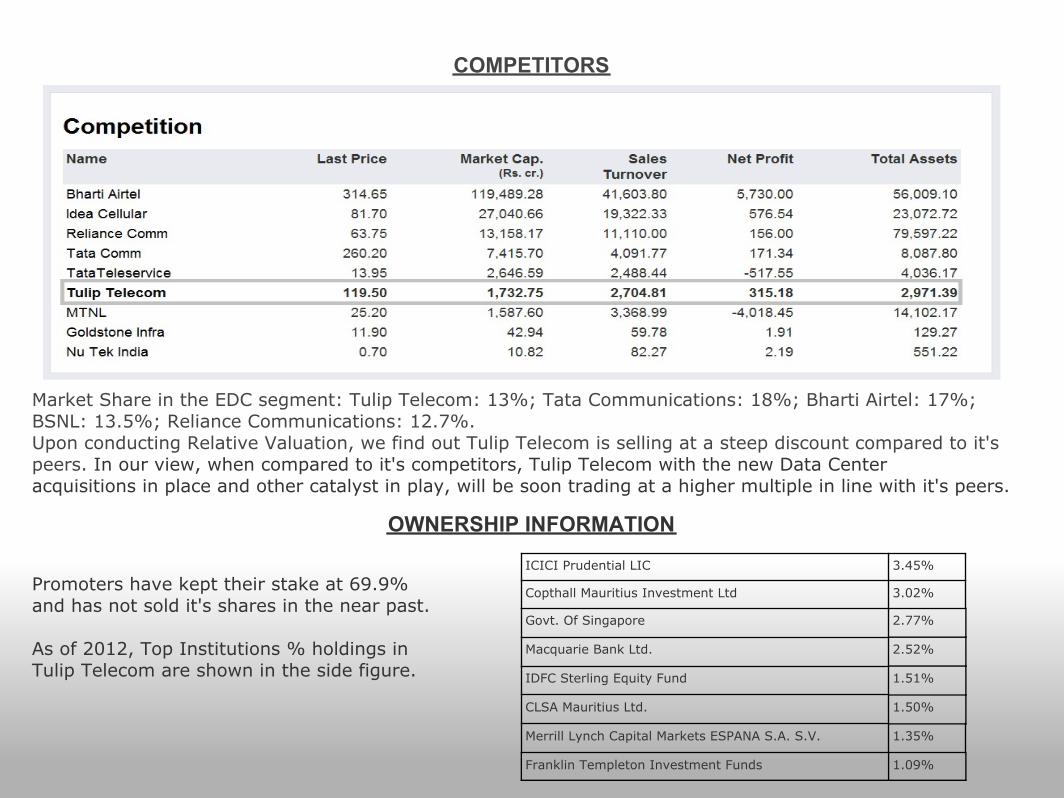

COMPETITORS

Market Share in the EDC segment: Tulip Telecom: 13%; Tata Communications: 18%; Bharti Airtel: 17%; BSNL: 13.5%; Reliance Communications: 12.7%.Upon conducting Relative Valuation, we find out Tulip Telecom is selling at a steep discount compared to it's peers. In our view, when compared to it's competitors, Tulip Telecom with the new Data Center acquisitions in place and other catalyst in play, will be soon trading at a higher multiple in line with it's peers.

OWNERSHIP INFORMATION

Promoters have kept their stake at 69.9% and has not sold it's shares in the near past.

As of 2012, Top Institutions % holdings in Tulip Telecom are shown in the side figure.

ICICI Prudential LIC 3.45%

Copthall Mauritius Investment Ltd 3.02%

Govt. Of Singapore 2.77%

Macquarie Bank Ltd. 2.52%

IDFC Sterling Equity Fund 1.51%

CLSA Mauritius Ltd. 1.50%

Merrill Lynch Capital Markets ESPANA S.A. S.V. 1.35%

Franklin Templeton Investment Funds 1.09%

ECONOMIC MOATS

In recent years Tulip Telecom has established itself as a one stop shop for all the EDS related needs. That acts as a huge entry barrier for the competitors and economic deterrent for the present customer to switch to another service provider. Tulip Telecom has constructive sales growth, increased ROIC, ROE and it’s economic moat was maintained even during the economic downturn and shows lot of future potential.

MANAGEMENT EFFECTIVENESS AND CORPORATE GOVERNANCE

Tulip Telecom is run by highly entrepreneurial, experienced and qualified industry leaders.Management is very dynamic and work relentlessly towards providing customers a one stop shop solution.Professional culture and good academic background of its managers and over 20+ years of experience helped Tulip Telecom faced the downturn effectively.Low dividend policies are suitable seeing the higher future growth prospects and current expansions.Management is focused on transparency while operating and keep investors interest first.Tulip's Management is very particular about being the best in their league and making the company state of art operations.

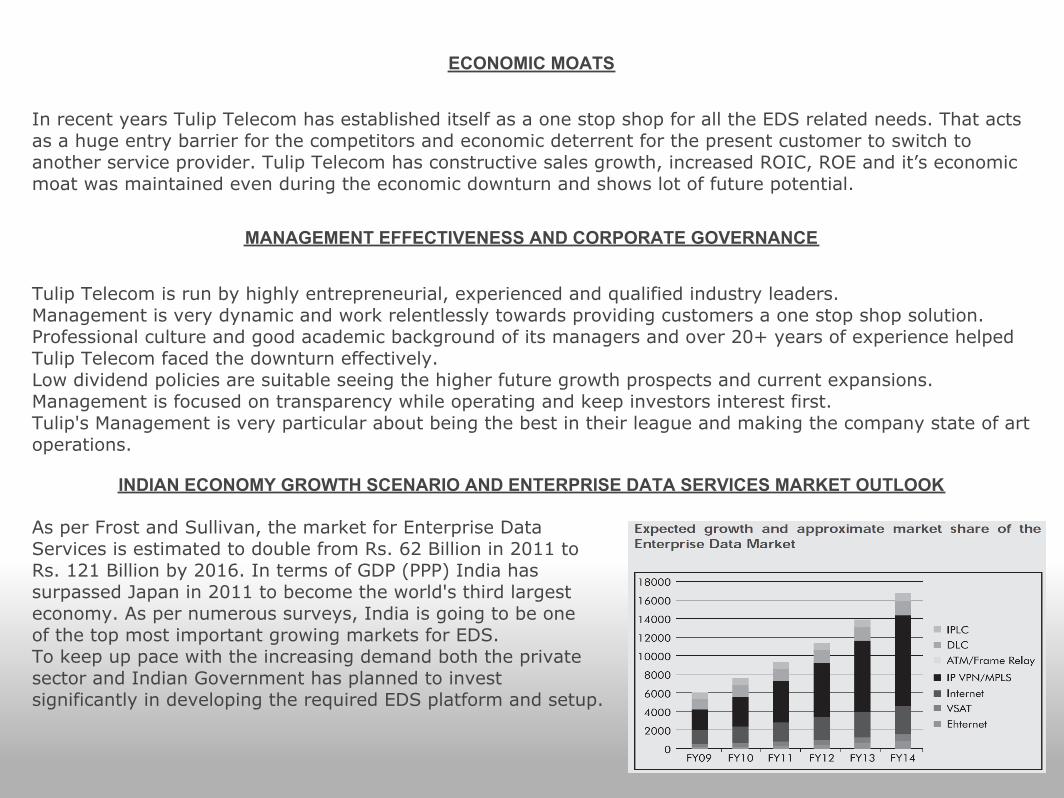

INDIAN ECONOMY GROWTH SCENARIO AND ENTERPRISE DATA SERVICES MARKET OUTLOOK

As per Frost and Sullivan, the market for Enterprise Data Services is estimated to double from Rs. 62 Billion in 2011 to Rs. 121 Billion by 2016. In terms of GDP (PPP) India has surpassed Japan in 2011 to become the world's third largest economy. As per numerous surveys, India is going to be one of the top most important growing markets for EDS. To keep up pace with the increasing demand both the private sector and Indian Government has planned to invest significantly in developing the required EDS platform and setup.

TULIP TELECOM’S VALUATION

● For this study, 2-Stage aggregate free cash flow model has been used, which is growing well over 50%, even if we take a conservative growth rate of 10% for the next 5 years and 7.5% for the 5 years thereafter, our intrinsic value calculation of Rs. 170 shows a MOS of 48% from the present day price of Rs. 115.

● Taking a range gives us a valuation of Rs. 150 to Rs. 190 market value for earnings multiple of 7X and 9X respectively. The multiples used are reasonable given the excellent growth rate the company exemplifies.

● DCF Model approach value of Rs. 170 lies in between this Earnings Multiple range of Rs. 150 - Rs. 190.

● The main reason for the low valuation of Tulip Telecom is due to increase in capital expenditure for strategic acquisitions, has put pressure on it's earnings and market players with short term interest are not very keen. For long term investors with one to two years investment horizon, Tulip Telecom is attractive at these valuations.

● Comparing the present P/E and P/B ratio to it’s historic average and it's competitors figures, tells us that the company is trading at a lower multiple.

● Debt to equity = 1.4 (overall stable capital structure). Company has moderate debt considering the major expansion to become a strategic player in the EDS segment and become a one stop shop.

● Credit Rating and Information Services of India Limited (CRISIL) has provided good rating to Tulip Telecom.

VALUATION METHOD

Method used here is 2 Stage Discount cash flow valuation with an aim to find the intrinsic value of Tulip Telecom based on the present cash flow, growth and risk. Assuming the life of the assets, here 20 years, to estimate Free cash flows, and Discount rate (r) to apply to get the present value. Free cash flow = Cash from operating activities – Capital Expenditure

Future Free cash flow growth based on past revenue growth rate of Tulip Telecom from 2008- 09 (Rs. 93.37 Cr) to 2010 - 11 (Rs. 213.61 Cr) ~ 51%.

Taking a conservative approach due to rising lending rates and expecting a modest free cash flow growth of: Year 1- 5, growth rate – 10%, Year 6-10, Growth Rate – 7.5%.

Perpetuity value (Year 11- 20) = FCFn+1/(r-gn), FCFn+1 = FCFn * (1+ gn )/(r- gn), where n = 10 years, Perpetuity Growth (gn) = growth of Indian economy in future (Historic avg. of Indian economy last decade: 6%), Cost of Equity (COE) = r = Risk free rate + Beta* Risk premium

Tulip Telecom has good credit rating from CRISIL, so enjoys lower credit cost. Risk free rate = 7.5 % (Average Indian Government Bond Yield for 10 Year Notes Rate)Beta = 0.75 for Tulip Telecom ; Risk premium = 7.5% (Average Indian Historic implied equity risk premium) Therefore COE (r) = 7.5% + 0.75 *7.5% ~ 13%

Free cash flow (year 1-20) = Free cash flow (year 1- 5) at 10% + Free cash flow (year 6- 10) at 7.5% + Perpetuity value (Year 11- 20). All the three values are discounted at COE.

Net value = DCF Estimate (Rs. 277) + Present (Cash-Debt) (- Rs. 107) Using the above values and steps Tulip Telecom's Per share value is coming out to be Rs. 170 This value is based on Discounted Free Cash Flow Analysis. Present value of Rs. 115 (As of Jul 20th, 2012) shows a Margin of Safety of 48%.

Disclaimer: This Report is for information purpose only and express our views about the company, not an offer to buy or sell. Risks involved in investing is not suitable for all kinds of investors. Seek professional advice if this research is suitable for you.

DCF ANALYSIS SHEET

Related Documents