L L e e a a r r n n e e r r G G u u i i d d e e Primary Agriculture T T h h e e b b a a s s i i c c l l a a y y o o u u t t o o f f f f i i n n a a n n c c i i a a l l s s t t a a t t e e m m e e n n t t s s My name: . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Company: . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Commodity: . . . . . . . . . . . . . . . . . . . . Date: . . . . . . . . . . . . . . . NQF Level: 2 US No: 116083 The availability of this product is due to the financial support of the National Department of Agriculture and the AgriSETA. Terms and conditions apply.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

LLeeaarrnneerr GGuuiiddee PPrriimmaarryy AAggrriiccuullttuurree

TThhee bbaassiicc llaayyoouutt ooff ffiinnaanncciiaall

ssttaatteemmeennttss

My name: . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Company: . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Commodity: . . . . . . . . . . . . . . . . . . . . Date: . . . . . . . . . . . . . . .

NQF Level: 2 US No: 116083

The availability of this product is due to the financial support of the National Department of Agriculture and the AgriSETA. Terms and conditions apply.

Illustrate and understand the basic lay-out of financial statements

Primary Agriculture NQF Level 2 Unit Standard No: 116083 22

Version: 01 Version Date: July 2006

BBeeffoorree wwee ssttaarrtt…… Dear Learner - This Learner Guide contains all the information to acquire all the knowledge and skills leading to the unit standard:

Title: Illustrate and understand the basic lay-out of financial statements

US No: 116083 NQF Level: 2 Credits: 2

The full unit standard will be handed to you by your facilitator. Please read the unit standard at your own time. Whilst reading the unit standard, make a note of your questions and aspects that you do not understand, and discuss it with your facilitator.

This unit standard is one of the building blocks in the qualifications listed below. Please mark the qualification you are currently doing:

Title ID Number NQF Level Credits Mark

National Certificate in Animal Production 48976 2 120

National Certificate in Mixed Farming Systems 48977 2 120

National Certificate in Plant Production 48975 2 120

This Learner Guide contains all the information, and more, as well as the activities that you will be expected to do during the course of your study. Please keep the activities that you have completed and include it in your Portfolio of Evidence. Your PoE will be required during your final assessment.

This Learner Guide contains all the information, and more, as well as the activities that you will be expected to do during the course of your study. Please keep the activities that you have completed and include it in your Portfolio of Evidence. Your PoE will be required during your final assessment.

WWhhaatt iiss aasssseessssmmeenntt aallll aabboouutt?? You will be assessed during the course of your study. This is called formative assessment. You will also be assessed on completion of this unit standard. This is called summative assessment. Before your assessment, your assessor will discuss the unit standard with you.

Are you enrolled in a: Y N

Learnership?

Skills Program?

Short Course?

Please mark the learning program you are enrolled in:

Your facilitator should explain the above concepts to you.

Illustrate and understand the basic lay-out of financial statements

Primary Agriculture NQF Level 2 Unit Standard No: 116083 33

Version: 01 Version Date: July 2006

Assessment takes place at different intervals of the learning process and includes various activities. Some activities will be done before the commencement of the program whilst others will be done during programme delivery and other after completion of the program.

The assessment experience should be user friendly, transparent and fair. Should you feel that you have been treated unfairly, you have the right to appeal. Please ask your facilitator about the appeals process and make your own notes.

HHooww ttoo uussee tthhee aaccttiivviittyy sshheeeettss…… Your activities must be handed in from time to time on request of the facilitator for the following purposes:

The activities that follow are designed to help you gain the skills, knowledge and attitudes that you need in order to become competent in this learning module.

It is important that you complete all the activities and worksheets, as directed in the learner guide and at the time indicated by the facilitator.

It is important that you ask questions and participate as much as possible in order to play an active roll in reaching competence.

When you have completed all the activities and worksheets, hand this workbook in to the assessor who will mark it and guide you in areas where additional learning might be required.

You should not move on to the next step in the assessment process until this step is completed, marked and you have received feedback from the assessor.

Sources of information to complete these activities should be identified by your facilitator.

Please note that all completed activities, tasks and other items on which you were assessed must be kept in good order as it becomes part of your Portfolio of Evidence for final assessment.

EEnnjjooyy tthhiiss lleeaarrnniinngg eexxppeerriieennccee!!

Illustrate and understand the basic lay-out of financial statements

Primary Agriculture NQF Level 2 Unit Standard No: 116083 44

Version: 01 Version Date: July 2006

HHooww ttoo uussee tthhiiss gguuiiddee …… Throughout this guide, you will come across certain re-occurring “boxes”. These boxes each represent a certain aspect of the learning process, containing information, which would help you with the identification and understanding of these aspects. The following is a list of these boxes and what they represent:

MMyy NNootteess …… You can use this box to jot down questions you might have, words that you do not understand,

instructions given by the facilitator or explanations given by the facilitator or any other remarks that

will help you to understand the work better.

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

What does it mean? Each learning field is characterized by unique terms and definitions – it is important to know and use these terms and definitions correctly. These terms and definitions are highlighted throughout the guide in this manner.

You will be requested to complete activities, which could be group activities, or individual activities. Please remember to complete the activities, as the facilitator will assess it and these will become part of your portfolio of evidence. Activities, whether group or individual activities, will be described in this box.

Examples of certain concepts or principles to help you contextualise them easier, will be shown in this box.

The following box indicates a summary of concepts that we have covered, and offers you an opportunity to ask questions to your facilitator if you are still feeling unsure of the concepts listed.

Illustrate and understand the basic lay-out of financial statements

Primary Agriculture NQF Level 2 Unit Standard No: 116083 55

Version: 01 Version Date: July 2006

WWhhaatt aarree wwee ggooiinngg ttoo lleeaarrnn??

What will I be able to do? .....................................................……………………… 6

Learning outcomes …………………………………………………………………………… 6

What do I need to know? .................................................…..……………………… 6

Introduction …………………………………………………………………………………… 7

Session 1 Gross margin Statements.................……………………………….. 8

Session 2 The income Statement......................………………………………. 16

Session 3 The balance sheet............................……………………………….. 23

Session 4 The cash flow Budget and Statement………………………….. 31

Session 5 The Financial legal Responsibilities of an agri-business…….. 40

Am I ready for my test? ........................................................... 45

Checklist for Practical assessment.......................................... 46

Paperwork to be done.............................................................. 47

Bibliography............................................................................. 48

Terms and conditions…………………………………………………… 48

Acknowledgements.................................................................. 49

SAQA Unit Standard

Illustrate and understand the basic lay-out of financial statements

Primary Agriculture NQF Level 2 Unit Standard No: 116083 66

Version: 01 Version Date: July 2006

WWhhaatt wwiillll II bbee aabbllee ttoo ddoo?? When you have achieved this unit standard, you will be able to:

Define and illustrate the gross margin statement, income statement, balance sheet and cash flow budget as well as the different cost aspects that one can find in a business.

Extend their learning and practice into other areas of costing and basic financial statements.

Strive towards professional standards and practices at higher levels.

Know if the business is making a profit or a loss, and how to generate basic but effective managerial information from it.

LLeeaarrnniinngg OOuuttccoommeess At the end of this learning module, you must be able to demonstrate a basic knowledge and understanding of:

Gross margin analysis.

Production costs.

Income statement.

Balance sheet.

Cash flow budget and statement.

Statutory/legal requirements, rules and principles.

WWhhaatt ddoo II nneeeedd ttoo kknnooww?? It is expected of the learner attempting this unit standard to demonstrate competence against the unit standard:

NQF 1: Identify the need for capital and understand the need for the recording of the income and different costs in an agri-business.

Illustrate and understand the basic lay-out of financial statements

Primary Agriculture NQF Level 2 Unit Standard No: 116083 77

Version: 01 Version Date: July 2006

IInnttrroodduuccttiioonn The farmer should set up a business plan or project outline of how much produce or crop he would like to calculate. It is important to know what size of field he/she would like to cultivate or for example how big his poultry farm would be. It is necessary that the farmer can identify the infrastructure needed for this purpose and what inputs are needed, financially and support services. The extent of labour needed to do the job is important in the planning phase of the project, since the workforce or labour is responsible for spraying, weeding, cultivating, dipping, feeding etc.

MMyy NNootteess ……

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Illustrate and understand the basic lay-out of financial statements

Primary Agriculture NQF Level 2 Unit Standard No: 116083 88

Version: 01 Version Date: July 2006

SSeessssiioonn 11

GGrroossss mmaarrggiinn ssttaatteemmeennttss

After completing this session, you should be able to: SO 1: Define and understand the gross margin statement and distinguish between direct and indirect costs, as well as fixed and variable costs.

In this session we explore the following concepts:

Fixed costs.

Variable costs.

Indirect costs

Direct costs

In order to run a farm enterprise one has to incur costs i.e. one has to buy farming requirements, and also pay for services rendered. Costs can be classified as direct costs, indirect costs, fixed and variable costs.

FFiixxeedd ccoossttss

Fixed costs are those costs, which cannot easily be allocated to the different enterprises or parts that make up the whole of the farm. These costs include transport, the monthly electricity account and rental or purchase payments. These costs are relevant to the farm as a whole. Fixed costs do not change if the size of the farming enterprise changes. Fixed costs will have to be paid continuously even if no production occurs.

These costs include:

Depreciation in the value of vehicles and machinery Insurance premiums on fixed assets such as buildings and machinery Licenses Permanent labour Monthly payments for the property if money is still owed. Others

VVaarriiaabbllee ccoossttss

Variable costs are costs, which can be allocated to each individual section of the farming enterprise. These are costs that are needed for production, and will only be incurred when production takes place. Variable costs will change as the size of farming enterprise is changes.

Illustrate and understand the basic lay-out of financial statements

Primary Agriculture NQF Level 2 Unit Standard No: 116083 99

Version: 01 Version Date: July 2006

Variable costs are costs that vary with the extent of production of outputs. When output increases, more labour is needed, more irrigation may be required and more fertilizer will be used. If the enterprise reduces, production costs will also reduce. The total variable costs increases as output increases and falls as output decreases.

Variable costs include, but are not limited to the following:

Seed to plant crops purchases such as fertilizers, chemicals marketing costs such as packaging, materials casual labour transport Irrigation costs for field crops

IInnddiirreecctt ccoossttss

Indirect costs are those costs that are essential for the daily running of a business. They are also known as overheads or fixed costs as they remain the same irrespective of the extent of production. Included in these costs are rent, interest payments, electricity and water, municipal rates and taxes, communication costs and management costs.

DDiirreecctt ccoossttss

Direct costs are those costs that are directly linked with the production of a crop. They are also called variable costs as they vary with the output. They would include materials (fertilizer, seed) and wages paid to temporary labour.

IInnccoommee ssoouurrcceess

Income sources refer to the various obvious markets that you supply your product to. Income sources could also include homeowners that purchase things like manure from a chicken farmer or spent bark mix for compost. An income source thus is not limited to those sources that you purchase your core products from. The money you would receive for your produce should be known to you in order to set up a budget.

MMaatteerriiaall ccoossttss

Material costs are costs for items that are used for production and may include costs for fertilizer, pesticides, herbicides, etc.

PPrroodduuccttiioonn ccoossttss

Production costs entail all the costs involved in producing as well as the costs associated with delivering the product to the market. It will therefore include the costs associated with the field production, as well as the packaging and transport associated with marketing.

Illustrate and understand the basic lay-out of financial statements

Primary Agriculture NQF Level 2 Unit Standard No: 116083 1100

Version: 01 Version Date: July 2006

FFoorreeiiggnn ffaaccttoorr ccoossttss

Foreign factor costs are costs that are totally unforeseen at the beginning of the season, when the production budget is prepared. Such costs could include a new levy for training that is implemented by the government.

The Gross margin The Gross margin is defined as the amount that can be calculated by the difference between enterprise gross value of the product (Gross income) and the directly allocated variable costs.

• A financial budget for cotton can be calculated if the following is known: • Field size of the crop (cotton), the estimated yield and the crop value per ton or per

kg. If one assumes that you would get R3.10 per kg seed cotton, and all input costs adds up to a total of R5.561, then the Gross income would be R9300 @ 300kg per ha, (calculated at the above price of R3.10 per kg) and the Gross margin would be the difference between the Gross income and the input costs.

• In this case an amount of R3 739.00.

Please complete Activity 1 at the end of this session.

MMyy NNootteess …… . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

MMyy NNootteess ……

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Illustrate and understand the basic lay-out of financial statements

Primary Agriculture NQF Level 2 Unit Standard No: 116083 1111

Version: 01 Version Date: July 2006

Concept (SO 1) I understand this concept

Questions that I still would like to ask

The ability is demonstrated to explain and define fixed and variable costs.

The ability is demonstrated to identify and quantify the fixed and variable costs.

The ability is demonstrated to identify and explain the various income sources.

The ability is demonstrated to list and quantify the various income sources.

Material cost, labour cost and overhead costs are defined and explained.

All possible material costs, labour, direct and indirect costs for a specific agri-business are listed.

An understanding of the gross margin concept and its application within agriculture is demonstrated.

The ability to complete a template, show and calculate the production costs and gross margin is demonstrated.

Illustrate and understand the basic lay-out of financial statements

Primary Agriculture NQF Level 2 Unit Standard No: 116083 1122

Version: 01 Version Date: July 2006

1. Complete the template for Gross margin statement and explain what the following terms mean? – Fixed costs, variable costs, sources of income, material costs, labour costs, direct and indirect costs mean.

2. Explain why Gross margin statement is so important to agriculture?

IInnssttrruuccttiioonnss ttoo tthhee lleeaarrnneerr::

You have been provided with two templates.

The first is an example of a gross margin statement that describes the production of potatoes under intensive irrigation.

The second template is a blank template that you need to complete. Use figures relating the production cycle of the crop you are involved with.

If you get stuck on a point ask the group or the facilitator to help you.

Note: Remember that this is just an exercise and you can research exact figures when you get back to your workplace.

Before you fill in the blank template you need to have worked through the points above. This will help that the blank template makes sense to you and is essential for you to be able to complete the summative assessment.

After having worked through the above points you need to record the fixed and variable costs as well as the various income sources.

Ensure that you gather all the possible material and labour costs that will occur in the production cycle of your crop, and place them into the blank template provided. You are required to provide the total production cost compared to the gross margin and indicate the gross profit you could expect from your crop.

Instructions: Group Activity 11

SSOO 11 AACC 11--88 My Name:

. . . . . . . . . . . . . . . . . . My Workplace: . . . . . . . . . . . . . . . . . . My ID Number:

. . . . . . . . . . . . . . . . . . .

Illustrate and understand the basic lay-out of financial statements

Primary Agriculture NQF Level 2 Unit Standard No: 116083 1133

Version: 01 Version Date: July 2006

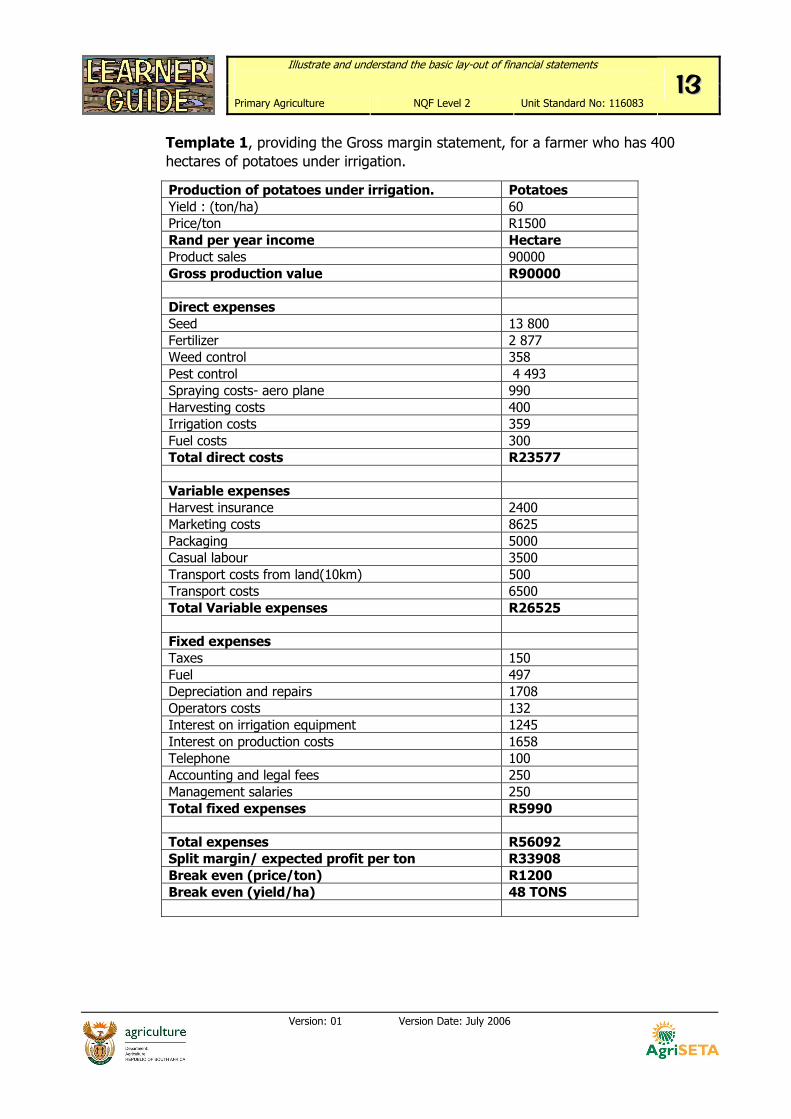

Template 1, providing the Gross margin statement, for a farmer who has 400 hectares of potatoes under irrigation.

Production of potatoes under irrigation. Potatoes Yield : (ton/ha) 60 Price/ton R1500 Rand per year income Hectare Product sales 90000 Gross production value R90000 Direct expenses Seed 13 800 Fertilizer 2 877 Weed control 358 Pest control 4 493 Spraying costs- aero plane 990 Harvesting costs 400 Irrigation costs 359 Fuel costs 300 Total direct costs R23577 Variable expenses Harvest insurance 2400 Marketing costs 8625 Packaging 5000 Casual labour 3500 Transport costs from land(10km) 500 Transport costs 6500 Total Variable expenses R26525 Fixed expenses Taxes 150 Fuel 497 Depreciation and repairs 1708 Operators costs 132 Interest on irrigation equipment 1245 Interest on production costs 1658 Telephone 100 Accounting and legal fees 250 Management salaries 250 Total fixed expenses R5990 Total expenses R56092 Split margin/ expected profit per ton R33908 Break even (price/ton) R1200 Break even (yield/ha) 48 TONS

Illustrate and understand the basic lay-out of financial statements

Primary Agriculture NQF Level 2 Unit Standard No: 116083 1144

Version: 01 Version Date: July 2006

3. Discuss, in your group, why a farmer needs to have an understanding of the gross margin concept and its value in agriculture.

Illustrate and understand the basic lay-out of financial statements

Primary Agriculture NQF Level 2 Unit Standard No: 116083 1155

Version: 01 Version Date: July 2006

Now, complete Template 2 below:

Template 2. This is a gross margin statement for a generic production cycle. Complete this template as an example.

Yield : (ton/ha) Price/ton Rand per year income Hectare Product sales Other sources of revenue Other sources of revenue Gross production value Direct expenses Total direct costs Variable expenses Total Variable expenses Fixed expenses Total fixed expenses Total expenses Split margin/ expected per kg/ton? Gross margin. Break even (price/ton) Break even (yield/ha)

Facilitator comments: Assessment:

Illustrate and understand the basic lay-out of financial statements

Primary Agriculture NQF Level 2 Unit Standard No: 116083 1166

Version: 01 Version Date: July 2006

SSeessssiioonn 22

TThhee iinnccoommee ssttaatteemmeenntt

After completing this session, you should be able to: SO 2: Define and understand the income statement.

In this session we explore the following concepts:

Elements of an income statement.

22..11 EElleemmeennttss ooff aann iinnccoommee ssttaatteemmeenntt FFaarrmm IInnccoommee

Refers to those items that represent the income to the farm business.

FFaarrmm EExxppeennddiittuurree

Refers to the costs of operating a farm business. Some of the items can be allocated to the specific production enterprise and some cannot. Allocated costs include seeds, fertilizers, feeds, labour costs etc… Non-allocated costs (overhead costs) include permanent labour wage, telephone, fuel, repairs, electricity etc.

NNeett FFaarrmm IInnccoommee

The net farm income is the income the farm generates after overheads have been deducted. It is calculated by deducting overheads from the total farm gross margin.

Net farm income provides a measure of performance and factors of production including management, capital and land.

FFaarrmm PPrrooffiitt

This is the income that remains after all costs have been deducted.

This is calculated by deducting external factor costs from the net farm income. The farm profit is a measurement of the return or reward to the owner, management, capital and land.

Illustrate and understand the basic lay-out of financial statements

Primary Agriculture NQF Level 2 Unit Standard No: 116083 1177

Version: 01 Version Date: July 2006

SCHEMATIC DIAGRAM OF INFORMATION FLOW IN A FARM INCOME STATEMENT

Over head costs

Including payment to management, interest on capital and lease or rental on land; electricity, water,

Variable costs

Fuel, oil, and lubricants Repairs and spares for vehicle and machinery Variable costs in respect of sundry farm income Others

Fixed costs

Depreciation on vehicle and machinery Insurance on fixed improvement, vehicle and machinery Licenses Regular labour, Repairs for fixed improvements. Others

Net Farm Income

External Factor cost

Farm Profit

Please complete Activity 2 at the end of this session.

MMyy NNootteess …… . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

TOTAL FARM MARGIN

Illustrate and understand the basic lay-out of financial statements

Primary Agriculture NQF Level 2 Unit Standard No: 116083 1188

Version: 01 Version Date: July 2006

Concept (SO 2) I understand this concept

Questions that I still would like to ask

Ability is demonstrated to understand, distinguish between and quantify all possible fixed and variable costs such as marketing, personnel and admin costs, as well as foreign factors costs.

The ability to provide inputs to an income statement, which reflects production costs, income, foreign cost and profits or losses, is demonstrated.

The ability to generate managerial information from the income statement is demonstrated.

MMyy NNootteess …… . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Illustrate and understand the basic lay-out of financial statements

Primary Agriculture NQF Level 2 Unit Standard No: 116083 1199

Version: 01 Version Date: July 2006

After having completed activity one, you will be familiar with the terminology and as a group complete this activity. The activity deals with income statements.

Go through the example that provides information on the production of potatoes under dry land conditions (template 2.1).

In this example there are fixed, variable and foreign costs that have been omitted. As a group, identify the costs to be omitted. Report back to the bigger group. It is important that all the information is documented, as it will help you to prepare for the completion of a generic income statement (template 2.2).

After the group session you may complete template 2.2 on any other crop or produce than potatoes. The completed generic income statement (template 2.2) must reflect the production cycle of the crop you are involved with. (Use any amounts just to complete the example).

Once you have completed your income statement decide whether you have made a profit or a loss. It is vital to record all information from the feed back sessions, as it will help you in the summative assessment.

Instructions: Group Activity 22

SSOO 22 AACC 11--33 My Name:

. . . . . . . . . . . . . . . . . . My Workplace: . . . . . . . . . . . . . . . . . . My ID Number:

. . . . . . . . . . . . . . . . . . .

MMyy NNootteess ……

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Illustrate and understand the basic lay-out of financial statements

Primary Agriculture NQF Level 2 Unit Standard No: 116083 2200

Version: 01 Version Date: July 2006

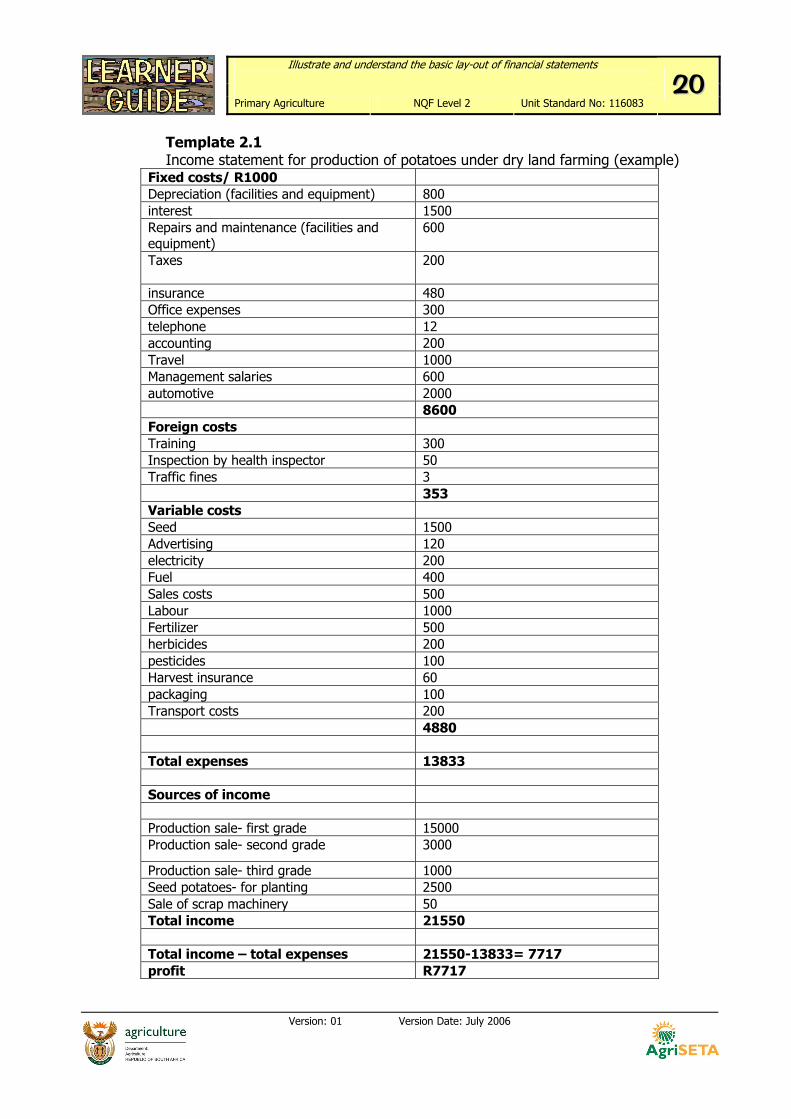

Template 2.1 Income statement for production of potatoes under dry land farming (example)

Fixed costs/ R1000 Depreciation (facilities and equipment) 800 interest 1500 Repairs and maintenance (facilities and equipment)

600

Taxes

200

insurance 480 Office expenses 300 telephone 12 accounting 200 Travel 1000 Management salaries 600 automotive 2000 8600 Foreign costs Training 300 Inspection by health inspector 50 Traffic fines 3 353 Variable costs Seed 1500 Advertising 120 electricity 200 Fuel 400 Sales costs 500 Labour 1000 Fertilizer 500 herbicides 200 pesticides 100 Harvest insurance 60 packaging 100 Transport costs 200 4880 Total expenses 13833 Sources of income Production sale- first grade 15000 Production sale- second grade 3000

Production sale- third grade 1000 Seed potatoes- for planting 2500 Sale of scrap machinery 50 Total income 21550 Total income – total expenses 21550-13833= 7717 profit R7717

Illustrate and understand the basic lay-out of financial statements

Primary Agriculture NQF Level 2 Unit Standard No: 116083 2211

Version: 01 Version Date: July 2006

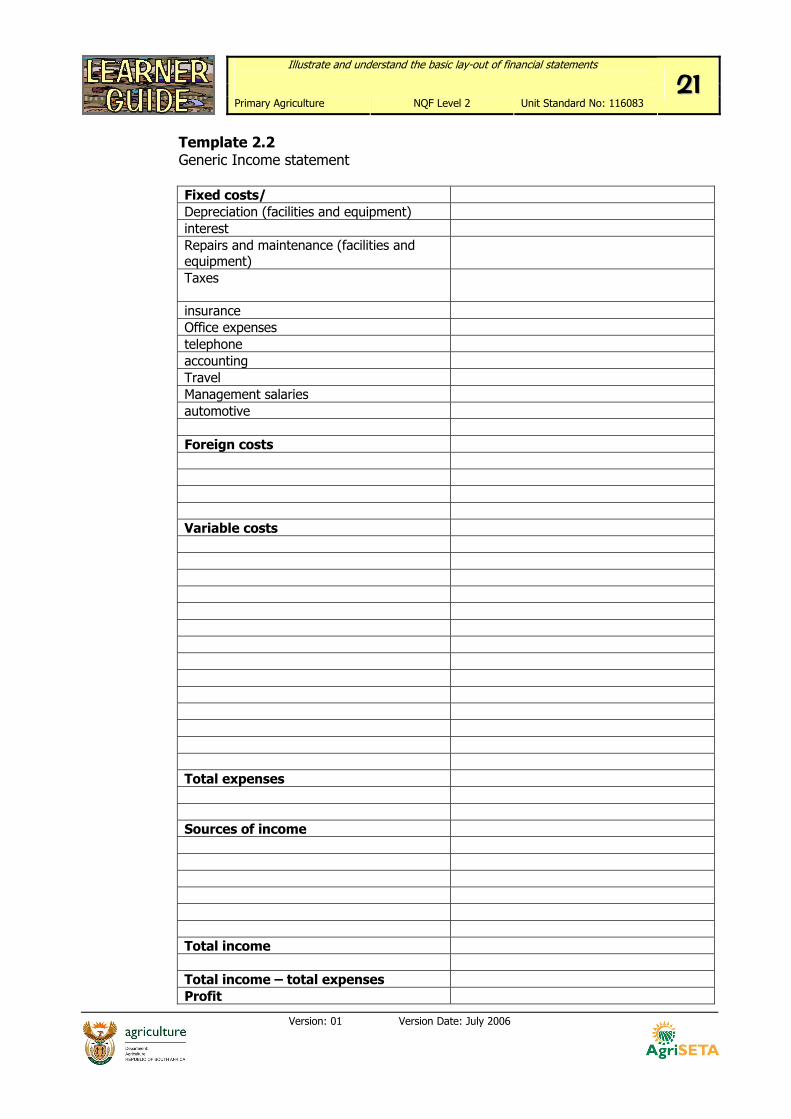

Template 2.2 Generic Income statement

Fixed costs/ Depreciation (facilities and equipment) interest Repairs and maintenance (facilities and equipment)

Taxes

insurance Office expenses telephone accounting Travel Management salaries automotive Foreign costs Variable costs Total expenses Sources of income Total income Total income – total expenses Profit

Illustrate and understand the basic lay-out of financial statements

Primary Agriculture NQF Level 2 Unit Standard No: 116083 2222

Version: 01 Version Date: July 2006

Record all information / notes

Facilitator comments: Assessment:

Illustrate and understand the basic lay-out of financial statements

Primary Agriculture NQF Level 2 Unit Standard No: 116083 2233

Version: 01 Version Date: July 2006

SSeessssiioonn 33

TThhee bbaallaannccee sshheeeett

After completing this session, you should be able to: SO 3: Define and understand the balance sheet.

In this session we explore the following concepts:

Elements of balance sheet.

Balance sheet analysis.

33..11 IInnttrroodduuccttiioonn A balance sheet is a statement summarizing the assets and liabilities of a business at a particular point in time. This time is usually at the end of the financial year. The primary function of a balance sheet is to measure the financial solvency of a business as it indicates the extent to which the assets match to the liability.

33..22 EElleemmeennttss ooff bbaallaannccee sshheeeett A balance sheet is made up of three aspects: capital, assets and liabilities. These three are related to one another as shown in the equation below:

Capital = assets – liability

Or

Assets = capital + liability

It is important to recognize that assets and liabilities are usually grouped according to their lifespan as follows:

Short-term/current Medium term Long-term

They have a strong impact on the results of financial analyses of a business.

Illustrate and understand the basic lay-out of financial statements

Primary Agriculture NQF Level 2 Unit Standard No: 116083 2244

Version: 01 Version Date: July 2006

33..33 BBaallaannccee sshheeeett aannaallyyssiiss Balance sheets are used to establish the financial strength or weakness of the business concern. Furthermore they are used to establish trends from historical information contained in the balance sheet.

Financial Ratio Analysis is used to gain overall financial view of a farm business as well as indicating financial progress.

Financial ratios are classified according to the following:

Solvency Liquidity Growth

Solvency Solvency refers to the business’s ability to meet its long-term obligations if it does not go bankrupt.

Liquidity Liquidity measures the business’s ability to continuously generate sufficient cash to meet its financial commitments. A decrease in liquidity will render the farm business unable to meet its short-term requirements, continue operations and expand. A business’s cash in the bank is referred to as a liquid asset.

Growth Growth of a business or farming venture is measured by the change in value of the business from one financial period to the next.

Assets - are economic resources that can provide potential service in the future. These are divided into non-concurrent assets that would include property, plant and equipment. In addition there will be current assets, sometimes referred to as liquid assets, which includes the debtors and other receivables payments, bank balances and cash.

Short-term assets -current assets that management could convert to cash within the year (cash, receivables, stock)

Medium term assets – intermediate assets that would take longer than a year, but shorter than five years to convert to cash. Includes investments that have a set time frame to them - policies or actual intellectual property (work that can be patented but takes time).

Illustrate and understand the basic lay-out of financial statements

Primary Agriculture NQF Level 2 Unit Standard No: 116083 2255

Version: 01 Version Date: July 2006

Long-term assets - fixed assets like machinery, land, buildings, motor vehicles, computers, furniture and fixtures.

Liabilities - are obligations that the owner must pay to other parties such as creditors, employees

Short term liabilities - current liabilities- these are amounts that must be paid within a year. - Salaries and wages, taxes, short-term loans, money owed to suppliers of goods and services.

Medium term liabilities - are amounts owed on contract work carried out on research that does not have a specified time limit, but will be paid for when the project is complete.

Long-term liabilities - these are debts that are due on long-term (more than one year) loans (mortgage) from the Land Bank. These are bank bonds on farmland and infrastructure, machinery and plants that are paid off over twenty years.

Owners’ equity is the amount owed to the owner after the liabilities have been deducted. - For example, if the owner of a farm is worth R30 000 000 and owes the bank R20 000 000, you would subtract the amount owed on the farm from the owner’s capital worthiness. This renders the owners equity which would be R10 000 000. If the farm is a closed-corporation, the amount owing to the members’ share after all amounts are deducted which is owed on the farm and other liabilities , is called the employees’ own.

Please complete Activity 3 at the end of this session.

MMyy NNootteess …… . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

MMyy NNootteess …… . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Illustrate and understand the basic lay-out of financial statements

Primary Agriculture NQF Level 2 Unit Standard No: 116083 2266

Version: 01 Version Date: July 2006

Concept (SO 3) I understand this concept

Questions that I still would like to ask

An ability is demonstrated to identify and quantify the components of short-term assets.

Ability is demonstrated to identify and quantify the components of short-term liabilities.

Ability is demonstrated to identify and quantify the components of medium term assets.

Ability is demonstrated to identify and quantify the components of medium term liabilities.

An ability is demonstrated to identify and quantify the components of long-term assets.

An ability is demonstrated to identify and quantify the components of long-term liabilities.

An understanding of owner`s equity and what it consists of is demonstrated.

The ability to complete a balance sheet when the template is given is demonstrated.

MMyy NNootteess …… . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Illustrate and understand the basic lay-out of financial statements

Primary Agriculture NQF Level 2 Unit Standard No: 116083 2277

Version: 01 Version Date: July 2006

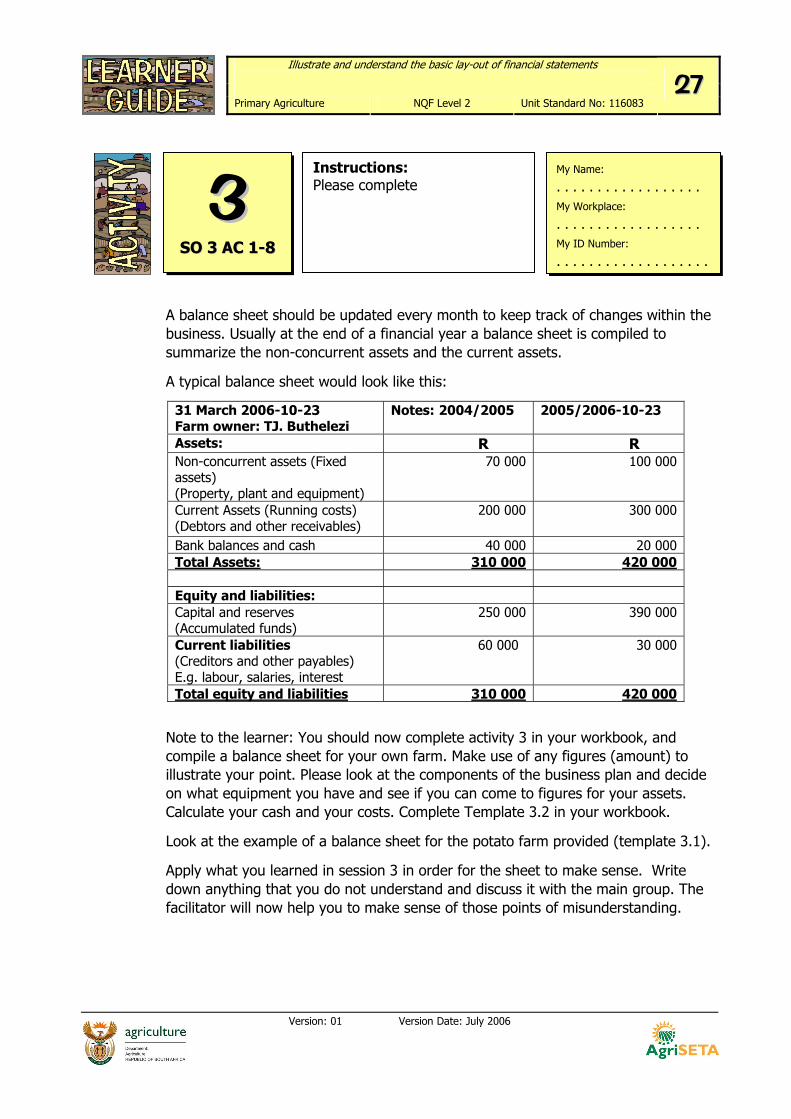

A balance sheet should be updated every month to keep track of changes within the business. Usually at the end of a financial year a balance sheet is compiled to summarize the non-concurrent assets and the current assets.

A typical balance sheet would look like this:

31 March 2006-10-23 Farm owner: TJ. Buthelezi

Notes: 2004/2005 2005/2006-10-23

Assets: R R Non-concurrent assets (Fixed assets) (Property, plant and equipment)

70 000 100 000

Current Assets (Running costs) (Debtors and other receivables)

200 000 300 000

Bank balances and cash 40 000 20 000Total Assets: 310 000 420 000 Equity and liabilities: Capital and reserves (Accumulated funds)

250 000 390 000

Current liabilities (Creditors and other payables) E.g. labour, salaries, interest

60 000 30 000

Total equity and liabilities 310 000 420 000

Note to the learner: You should now complete activity 3 in your workbook, and compile a balance sheet for your own farm. Make use of any figures (amount) to illustrate your point. Please look at the components of the business plan and decide on what equipment you have and see if you can come to figures for your assets. Calculate your cash and your costs. Complete Template 3.2 in your workbook.

Look at the example of a balance sheet for the potato farm provided (template 3.1).

Apply what you learned in session 3 in order for the sheet to make sense. Write down anything that you do not understand and discuss it with the main group. The facilitator will now help you to make sense of those points of misunderstanding.

Instructions: Please complete 33

SSOO 33 AACC 11--88 My Name:

. . . . . . . . . . . . . . . . . . My Workplace: . . . . . . . . . . . . . . . . . . My ID Number:

. . . . . . . . . . . . . . . . . . .

Illustrate and understand the basic lay-out of financial statements

Primary Agriculture NQF Level 2 Unit Standard No: 116083 2288

Version: 01 Version Date: July 2006

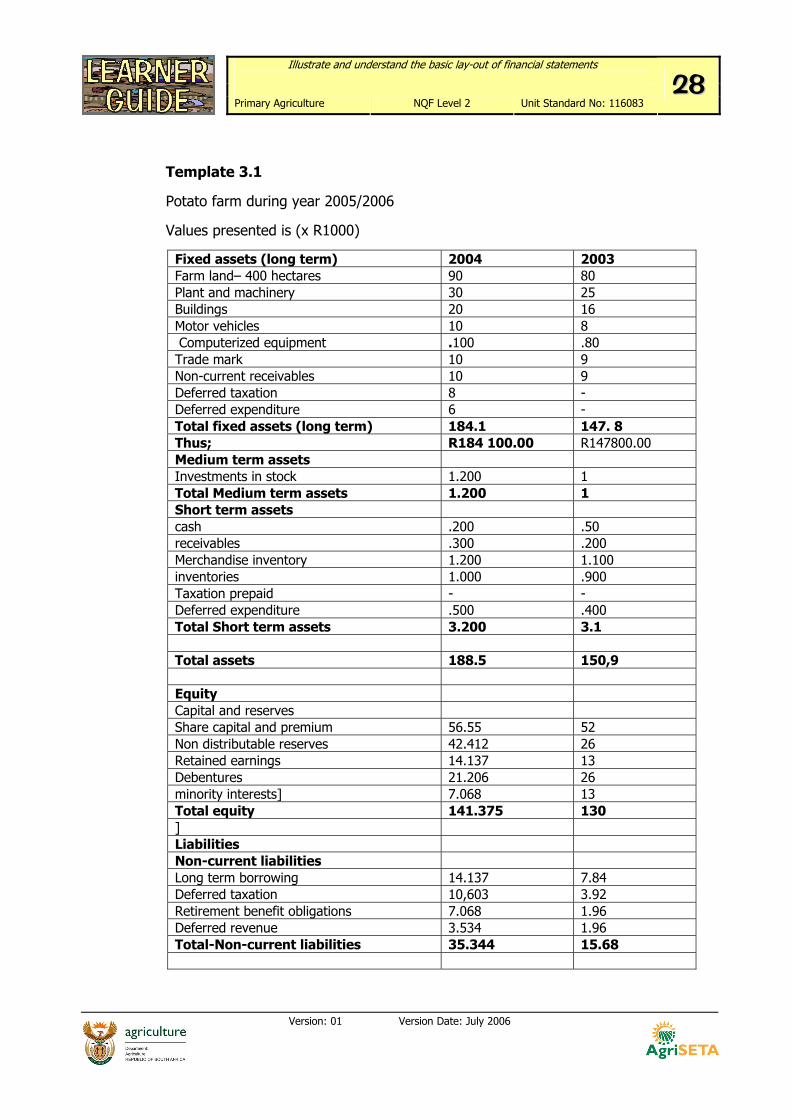

Template 3.1

Potato farm during year 2005/2006

Values presented is (x R1000)

Fixed assets (long term) 2004 2003 Farm land– 400 hectares 90 80 Plant and machinery 30 25 Buildings 20 16 Motor vehicles 10 8 Computerized equipment .100 .80 Trade mark 10 9 Non-current receivables 10 9 Deferred taxation 8 - Deferred expenditure 6 - Total fixed assets (long term) 184.1 147. 8 Thus; R184 100.00 R147800.00 Medium term assets Investments in stock 1.200 1 Total Medium term assets 1.200 1 Short term assets cash .200 .50 receivables .300 .200 Merchandise inventory 1.200 1.100 inventories 1.000 .900 Taxation prepaid - - Deferred expenditure .500 .400 Total Short term assets 3.200 3.1 Total assets 188.5 150,9 Equity Capital and reserves Share capital and premium 56.55 52 Non distributable reserves 42.412 26 Retained earnings 14.137 13 Debentures 21.206 26 minority interests] 7.068 13 Total equity 141.375 130 ] Liabilities Non-current liabilities Long term borrowing 14.137 7.84 Deferred taxation 10,603 3.92 Retirement benefit obligations 7.068 1.96 Deferred revenue 3.534 1.96 Total-Non-current liabilities 35.344 15.68

Illustrate and understand the basic lay-out of financial statements

Primary Agriculture NQF Level 2 Unit Standard No: 116083 2299

Version: 01 Version Date: July 2006

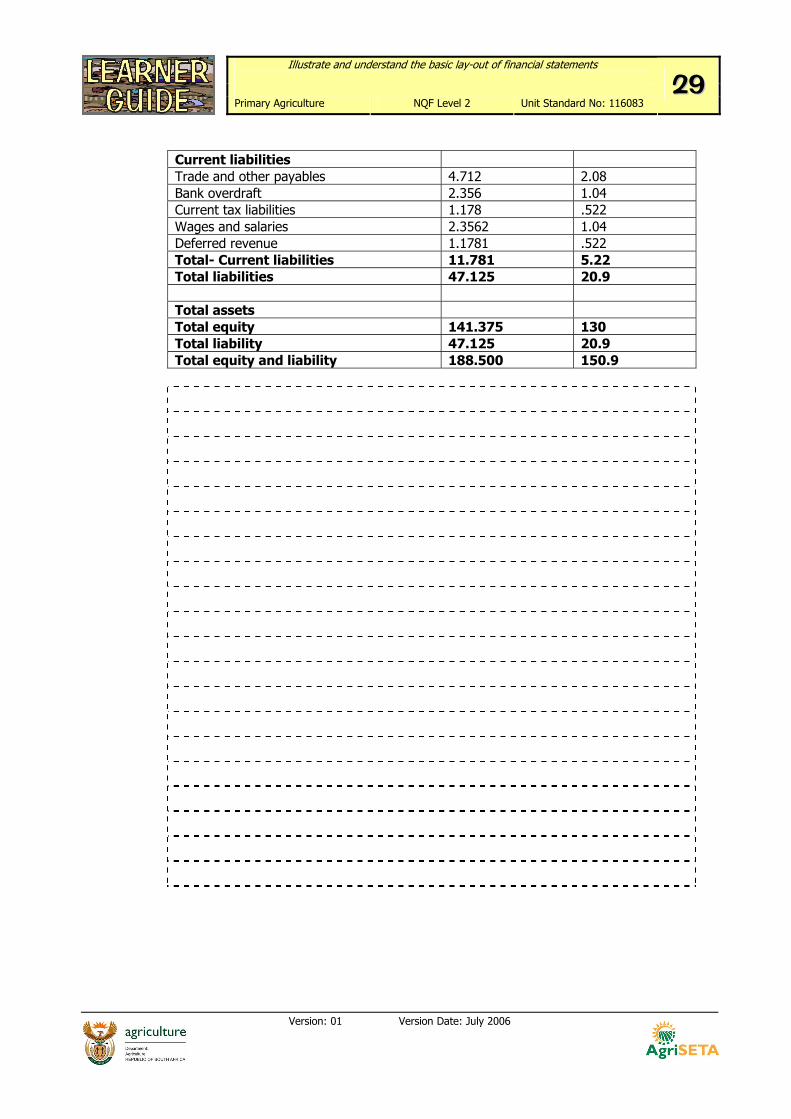

Current liabilities Trade and other payables 4.712 2.08 Bank overdraft 2.356 1.04 Current tax liabilities 1.178 .522 Wages and salaries 2.3562 1.04 Deferred revenue 1.1781 .522 Total- Current liabilities 11.781 5.22 Total liabilities 47.125 20.9 Total assets Total equity 141.375 130 Total liability 47.125 20.9 Total equity and liability 188.500 150.9

Illustrate and understand the basic lay-out of financial statements

Primary Agriculture NQF Level 2 Unit Standard No: 116083 3300

Version: 01 Version Date: July 2006

At the end of the group session, complete the blank balance sheet provided (Template 3.2). Use the example as a guide and ask the group and facilitator for help if you get stuck. Complete the template for the crop you are involved with. Keep notes of proceedings during the activities.

Template 3.2

Balance sheet your enterprise

Fixed assets-long term 2004/2005 2005/2006

Non-concurrent assets (Long-term & Medium term assets)

Current assets (Short term assets)

Total assets

Equity

Capital and reserves

Total equity

Liabilities:

Current liabilities

Total liabilities

Total assets

Total equity

Total liability

Total Equity and liabilities

Facilitator comments: Assessment:

Illustrate and understand the basic lay-out of financial statements

Primary Agriculture NQF Level 2 Unit Standard No: 116083 3311

Version: 01 Version Date: July 2006

SSeessssiioonn 44

TThhee ccaasshh ffllooww BBuuddggeett aanndd SSttaatteemmeenntt

After completing this session, you should be able to: SO 4: Define and understand the structure of a cash-flow budget and statement.

In this session we explore the following concepts:

Cash flow budget.

The need for the 12-month cash flow budget.

44..11 IInnttrroodduuccttiioonn ttoo ccaasshh ffllooww bbuuddggeett Cash flow is the money needed to run your company on a day-to-day basis. This is the money available after all the expected expenses have been covered, for unexpected expenses.

Cash flow statements are a tool that reflects the sources from which funds are generated during the accounting period as well as the purpose for which these were used.

The cash flow statements must be compiled for one year or at least until positive cash flow is achieved if not attained within the first year.

The most important feature of a cash flow budget is that only cash expenses and cash income are indicated at the estimated time of payment or receipt.

The cash flow statement reflects the source from which funds were generated during the accounting period. Cash flow is an important consideration when it comes to financing a business. The bank and monthly bank balance are important elements of a cash flow statement. A cash flow statement consists of three components: income, expenditure and bank balance.

Income consists of operating income, capital income and cash income.

Expenditure is classified as operating expenditure, capital expenditure and debt repayment.

Shortfall/surplus is calculated by deducting total expenditure from the total income.

Illustrate and understand the basic lay-out of financial statements

Primary Agriculture NQF Level 2 Unit Standard No: 116083 3322

Version: 01 Version Date: July 2006

The various components of a cash flow budget statement are:

Farm Income Capital income

Opening cash balance

Non farm Income Fertilizers Leases or rental Sprays Wages

Farm Operating Expenses

Repairs Machinery Capital expenditure Livestock Income statement Other expenditures Living wages Interest Redemption Total cash outflow

Scheduled debt payment

Closing cash balance

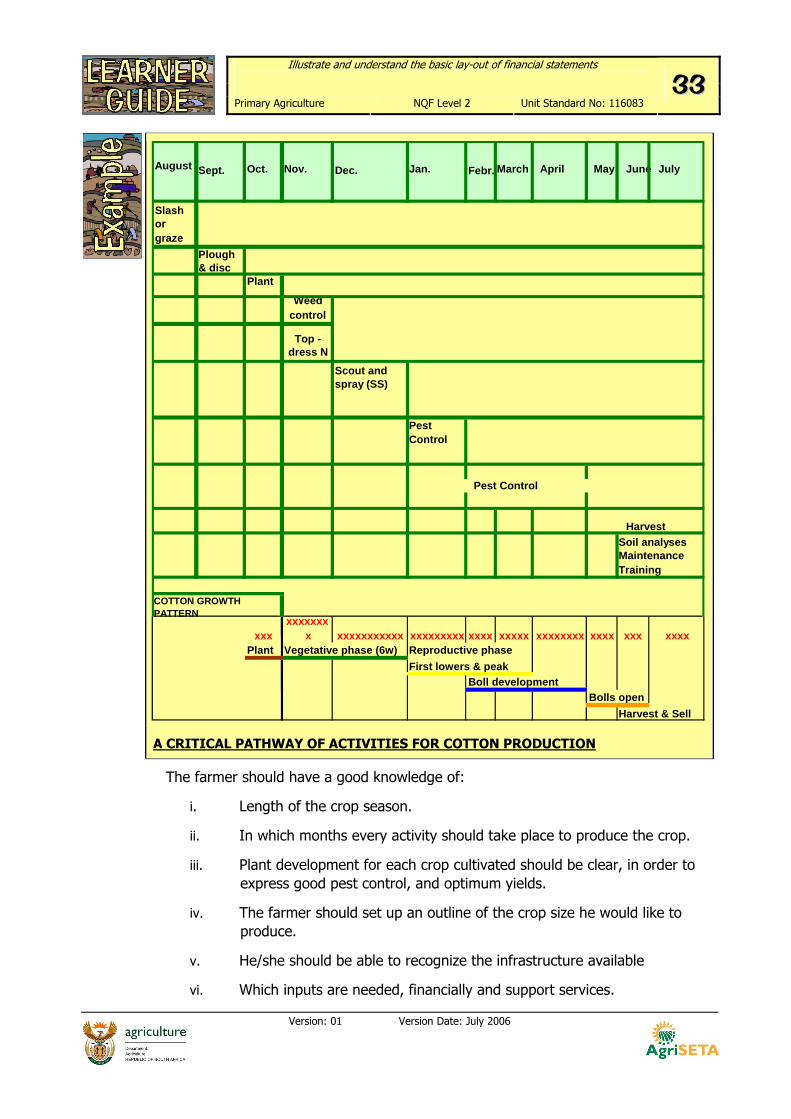

44..22 TThhee nneeeedd ffoorr tthhee ttwweellvvee mmoonntthh ccaasshh ffllooww bbuuddggeett

In order to understand a cash flow budget it is necessary for a farmer to understand which activities take place during the season, and the associated costs to complete these activities successful. For example, cotton is a cash crop. In order to set up a cash flow budget the farmer must have a cultivation programme in place as the crop will need attention (insecticides, fertilizers, picking, ext.) at different growing stages, and therefore, cash must be available for every event according to the programme arranged beforehand.

Illustrate and understand the basic lay-out of financial statements

Primary Agriculture NQF Level 2 Unit Standard No: 116083 3333

Version: 01 Version Date: July 2006

A CRITICAL PATHWAY OF ACTIVITIES FOR COTTON PRODUCTION

The farmer should have a good knowledge of:

i. Length of the crop season.

ii. In which months every activity should take place to produce the crop.

iii. Plant development for each crop cultivated should be clear, in order to express good pest control, and optimum yields.

iv. The farmer should set up an outline of the crop size he would like to produce.

v. He/she should be able to recognize the infrastructure available

vi. Which inputs are needed, financially and support services.

August

Sept. Oct. Nov.

Dec. Febr. March April May June July

Slash or graze

Plough & disc

Plant Weed

control

Top - dress N

xxx xxxxxxx

x xxxxxxxxxxx xxxxxxxxx xxxx xxxxx xxxxxxxx xxxx xxx xxxxPlant

First lowers & peakVegetative phase (6w) Reproductive phase

Harvest

Boll developmentBolls open

Harvest & Sell

COTTON GROWTH PATTERN

Soil analysesMaintenanceTraining

Pest Control

Pest Control

Scout and spray (SS)

Jan.

Illustrate and understand the basic lay-out of financial statements

Primary Agriculture NQF Level 2 Unit Standard No: 116083 3344

Version: 01 Version Date: July 2006

vii. Have a clear comprehension of the available workforce (labour)

viii. When a critical programme has been drawn up as above, the learner can compile cash flow statements. These are probably the most important aspect of the financial management of a farming business. Many farming based businesses currently experience cash flow related problems. A 12-month cash flow budget predicts an estimate of cash needed for a year.

EXPENDITURE/CASH OUTFLOW Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Total

Office lease 1 500 1 500 1 500 1 500 1 500 1 500 1 500 1 500 1 500 1 500 1 500 1 500 18 000

Traveling expenses - 5 000 - - - - - - - - - - 5 000

Training Equipments - 3 500 - - - - - - - - - - 3 500

Vehicle costs 30 000 - - - - - - - - - - 30 000

Stationery 1 200 - - - - 1 200 - - - - - - 2 400

Admin costs 100 50 30 40 30 50 40 30 20 40 50 30 510

Telephone cost 500 450 300 250 500 250 200 250 100 250 150 100 3 300

Electricity 150 200 250 180 150 280 200 250 150 200 100 250 2 360

TOTAL EXPENDITURE 33 450 10 700 2 080 1 970 2 180 3 280 1 940 2 030 1 770 1 990 1 800 1 880

65 070

ACCUMULATED DEFICIT 33 450 10 700 2 080 1 970 2 180 3 280 1 940 2 030 1 770 1 990 1 800 1 880

65 070

A Cash flow budget is a budget that breaks the yearly cash flow into twelve-month segments. This allows for greater control of the flow of cash.

A cash flow statement presents the source and use of the funds of the enterprise according to operating activities, investing activities and financing activities.

Operating activities describes the cash received for the product and cash payments made for production costs.

Investing activities describes the purchasing of new equipment or expanding the operation.

Financing activities describes the repayment of long-term loans.

Illustrate and understand the basic lay-out of financial statements

Primary Agriculture NQF Level 2 Unit Standard No: 116083 3355

Version: 01 Version Date: July 2006

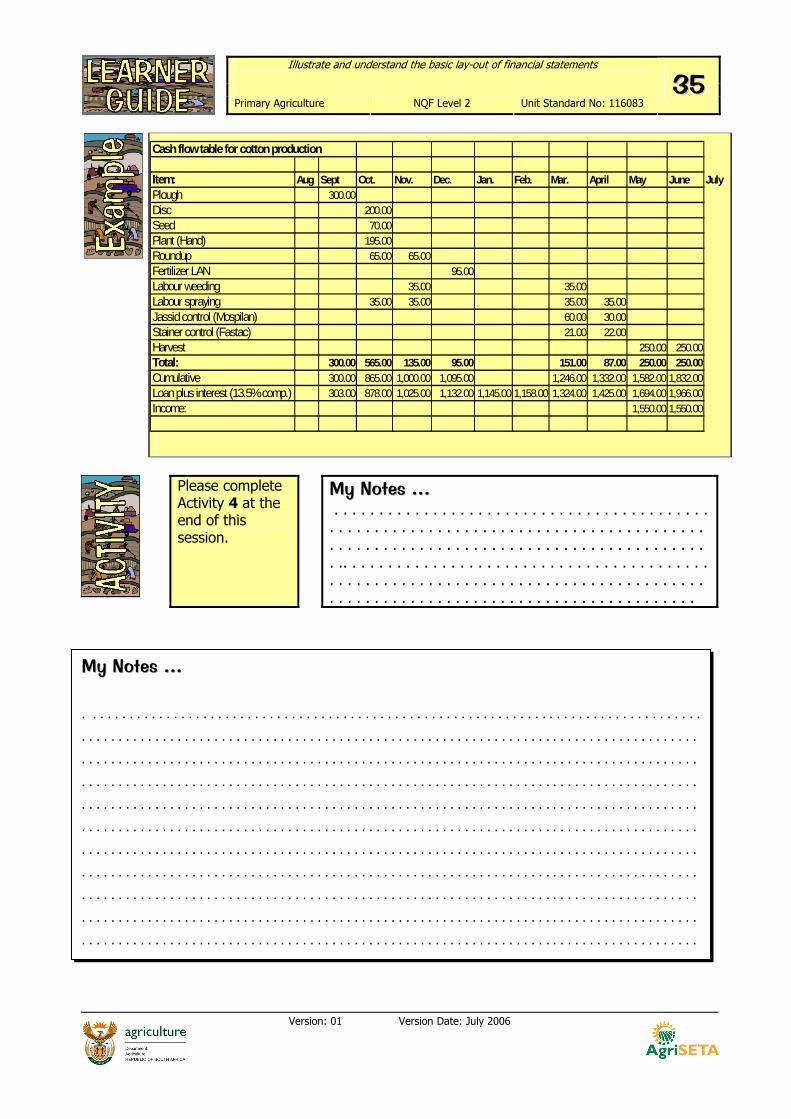

Please complete Activity 4 at the end of this session.

MMyy NNootteess …… . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Cash flow table for cotton production

Item: Aug Sept Oct. Nov. Dec. Jan. Feb. Mar. April May June JulyPlough 300.00Disc 200.00Seed 70.00Plant (Hand) 195.00Roundup 65.00 65.00Fertilizer LAN 95.00Labour weeding 35.00 35.00Labour spraying 35.00 35.00 35.00 35.00Jassid control (Mospilan) 60.00 30.00Stainer control (Fastac) 21.00 22.00Harvest 250.00 250.00Total: 300.00 565.00 135.00 95.00 151.00 87.00 250.00 250.00Cumulative 300.00 865.00 1,000.00 1,095.00 1,246.00 1,332.00 1,582.00 1,832.00Loan plus interest (13.5% comp.) 303.00 878.00 1,025.00 1,132.00 1,145.00 1,158.00 1,324.00 1,425.00 1,694.00 1,966.00Income: 1,550.00 1,550.00

MMyy NNootteess ……

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Illustrate and understand the basic lay-out of financial statements

Primary Agriculture NQF Level 2 Unit Standard No: 116083 3366

Version: 01 Version Date: July 2006

Concept (SO 4) I understand this concept

Questions that I still would like to ask

The ability to source various financial data for the cash-flow budget and statement is demonstrated.

The ability to fill in the template of a cash flow budget and/or statement is demonstrated.

An understanding of the need for a twelve-month budget is demonstrated.

An understanding of the various components of a cash flow budget and statement is demonstrated.

The ability to transfer the month-end balance to the next month`s opening balance is demonstrated.

An understanding of the influence interest rates on the budget and statement is demonstrated.

The ability to interpret basic results of the budget and statement is demonstrated.

An understanding of how the cash-flow budget/statement links up with the income statement is demonstrated.

An understanding and ability to use the cash-flow budget in a cash-flow statement is demonstrated.

Illustrate and understand the basic lay-out of financial statements

Primary Agriculture NQF Level 2 Unit Standard No: 116083 3377

Version: 01 Version Date: July 2006

In this activity an example of a month-to-month budget and statement for cash flow of an operation is provided (Template 1). The example only provides information for two of the twelve months.

Additional Information:

Budget statements are often presented on two separate sheets. To simplify the process we will use only one combined statement.

Brainstorm in your groups: Why it is necessary to have a twelve-month budget and not only an annual budget? This is applicable to agricultural businesses where income and expenses vary over the twelve months. It is also important to notice that an agricultural operation often owes money to various entities, and the repayment of the interest needs to be budgeted for. It could happen that in some months a loss may be budgeted.

The gross margin statement, income statement and the balance sheet provided as an example in the Learner Guide, contain sufficient data for you to complete the blank copy of the cash flow statement (Template 4.2). (You can use any figures to complete this exercise).

Before you start this exercise, you need to go through the example copy to get an idea of what is expected of you to consummate the blank copy. An important point, you must determine how to transfer the one-month’s end balance to the next month’s opening balance.

Once you have completed the input of required data into the blank statement you need to look for important results that are highlighted, such as whether the cash flow is positive or negative. Also determine whether and how you could improve the flow of cash.

It is advisable to ask the group and the facilitator for guidance as this section can get confusing and complicated.

At the end of this exercise you must be able to link the cash flow budget/ statement to the income statement.

Instructions: Group Activity 44

SSOO 44 AACC 11--99 My Name:

. . . . . . . . . . . . . . . . . . My Workplace: . . . . . . . . . . . . . . . . . . My ID Number:

. . . . . . . . . . . . . . . . . . .

Illustrate and understand the basic lay-out of financial statements

Primary Agriculture NQF Level 2 Unit Standard No: 116083 3388

Version: 01 Version Date: July 2006

Template 4.1

Mark activities (with an X) when they are scheduled to take place (you could adapt the months and activities to suit the crop).

Activity table for crop production

Item: Aug Sept Oct. Nov. Dec. Jan. Feb. Mar. April May June July

Plough

Disc

Seed

Plant (Hand)

Roundup

Fertilizer LAN

Labour weeding

Labour spraying

Early Pest control

Mid-season Pest control

Late-season Pest control

Harvest

Total:

Illustrate and understand the basic lay-out of financial statements

Primary Agriculture NQF Level 2 Unit Standard No: 116083 3399

Version: 01 Version Date: July 2006

Template 4.2.

Cash flow budget /statement (values in brackets are negative). Use the example in the Learner Guide and complete the table below. Check Template 4.1 to see which months you have already scheduled which tasks.

Cash flow table for crop production

Item: Aug Sept Oct. Nov. Dec. Jan. Feb. Mar. April May June July

Plough

Disc

Seed

Plant (Hand)

Roundup

Fertilizer LAN

Labour weeding

Labour spraying

Early Pest Control

Mid season Pest Control

Late season Pest Control

Harvest

Total:

Cumulative (budget) Budget carried over from previous month

Loan plus interest (13.5% comp.)

Gross Income:

Gross margin (expenditure)

Net Profit (negative number in brackets)

Facilitator comments: Assessment:

Illustrate and understand the basic lay-out of financial statements

Primary Agriculture NQF Level 2 Unit Standard No: 116083 4400

Version: 01 Version Date: July 2006

SSeessssiioonn 55

TThhee FFiinnaanncciiaall lleeggaall RReessppoonnssiibbiilliittiieess ooff aann aaggrrii--bbuussiinneessss

After completing this session, you should be able to: SO 5: Demonstrate an understanding of the legal responsibilities of an agri-business owner.

In this session we explore the following concepts:

Legal responsibilities of an agri-business owner.

There are many South African agricultural laws and Acts that govern the way in which a farmer operates on a farm. In groups of four, discuss these laws and provide your understanding of why they are in place. These laws and Acts include:

Labour laws that refer to the following Acts;

Taxes: PAYE and income tax.

Types of crops produced: Restrictions on the production of certain products (cannabis/dagga) or certain animals.

Environmental legislation: The control of activities that concern the environment.

Health and safety: Storage and dealing with livestock.

Export and import: Certain crops and animals are not allowed to be imported or exported.

Labour and industrial relations: These are laws that cover the relationship between employers and employees and the state.

Basic conditions of employment Act of 1983.

Occupational health and safety Act, 1993.

Wages Act.

Workmen’s compensation Act.

Unemployment insurance Act.

Labour relations Act of 1995.

Employment equity Act of 1998.

Skills development levies Act of 1998.

Illustrate and understand the basic lay-out of financial statements

Primary Agriculture NQF Level 2 Unit Standard No: 116083 4411

Version: 01 Version Date: July 2006

SSkkiillllss ddeevveellooppmmeenntt AAcctt ooff 11999988

Income tax: A tax levied by a government on the income of individuals and business firms. Taxes on personal income and business profits are major revenue sources for South Africa. These taxes are applied to repair roads and infrastructure, pays for government hospitals and clinics, government services (policy, military), training subsidies, housing etc. Discuss your personal feelings about taxes

Value added tax - it is the law of the country that tax must be included in the price of goods and services, commonly referred to as VAT-

Workmen’s compensation - this is an Act that forces employers to insure their employees against disablement or death caused by accidents while they are on duty or illness caused as a result of the kind of work that they do.

Skills levy payments - this is a levy imposed by the government on all businesses and government institutions in the country. This levy is set up to accelerate the training and development of skills in all areas of the workforce and to ensure that South Africa becomes a world-trading competitor.

Please complete Activity 5 at the end of this session.

MMyy NNootteess …… . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

MMyy NNootteess …… . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Illustrate and understand the basic lay-out of financial statements

Primary Agriculture NQF Level 2 Unit Standard No: 116083 4422

Version: 01 Version Date: July 2006

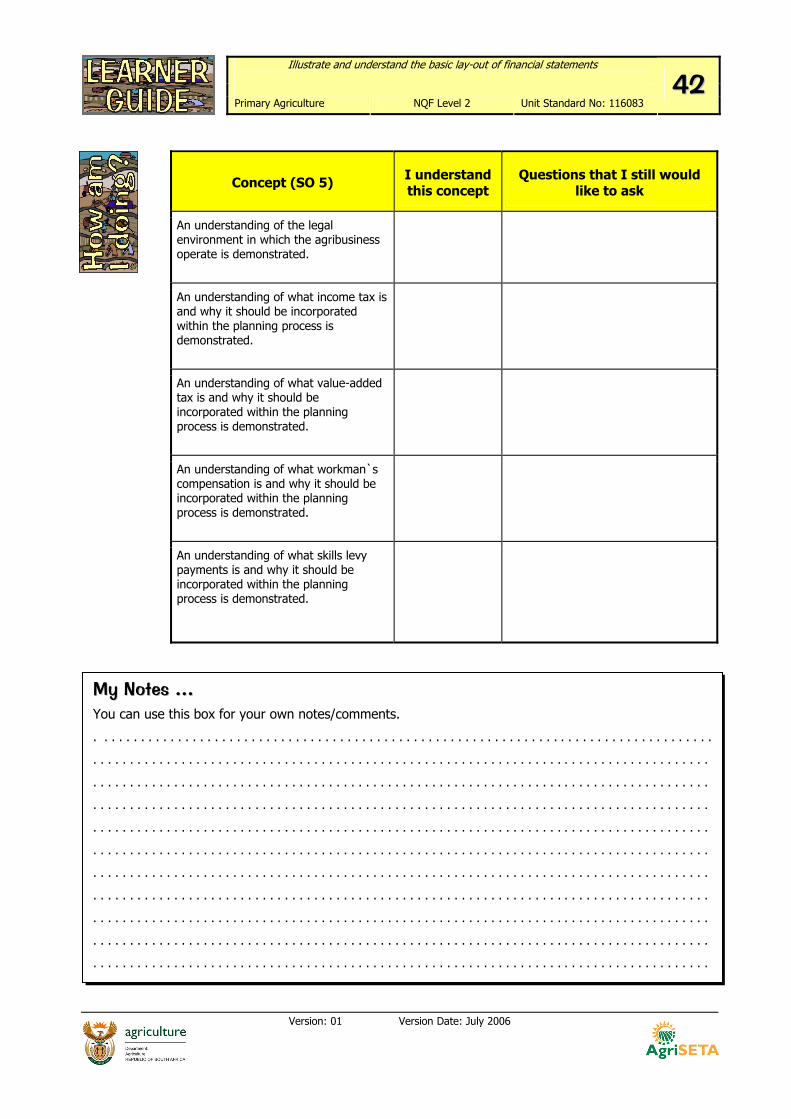

Concept (SO 5) I understand this concept

Questions that I still would like to ask

An understanding of the legal environment in which the agribusiness operate is demonstrated.

An understanding of what income tax is and why it should be incorporated within the planning process is demonstrated.

An understanding of what value-added tax is and why it should be incorporated within the planning process is demonstrated.

An understanding of what workman`s compensation is and why it should be incorporated within the planning process is demonstrated.

An understanding of what skills levy payments is and why it should be incorporated within the planning process is demonstrated.

MMyy NNootteess …… You can use this box for your own notes/comments.

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Illustrate and understand the basic lay-out of financial statements

Primary Agriculture NQF Level 2 Unit Standard No: 116083 4433

Version: 01 Version Date: July 2006

1. Give a brief understanding why there is a need for legislation covering every aspect of agri-business (from the environment to labour relations)?

Instructions: Group Activity 55

SSOO 55 AACC 55 My Name:

. . . . . . . . . . . . . . . . . . My Workplace: . . . . . . . . . . . . . . . . . . My ID Number:

. . . . . . . . . . . . . . . . . . .

Illustrate and understand the basic lay-out of financial statements

Primary Agriculture NQF Level 2 Unit Standard No: 116083 4444

Version: 01 Version Date: July 2006

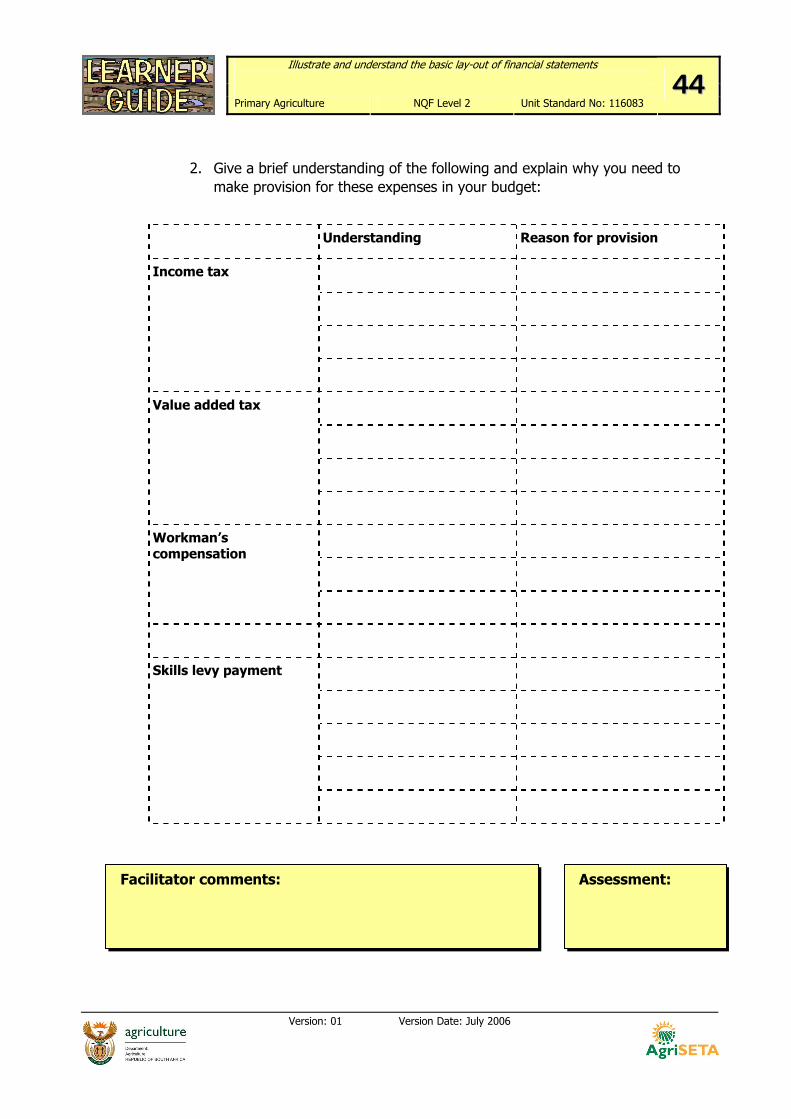

2. Give a brief understanding of the following and explain why you need to make provision for these expenses in your budget:

Understanding Reason for provision

Income tax

Value added tax

Workman’s compensation

Skills levy payment

Facilitator comments: Assessment:

Illustrate and understand the basic lay-out of financial statements