TSG14/02 General Excise Duties (Tobacco, Alcohol, Betting and Others) Introduction 1. This paper examines the area of general excise duties which apply in the State. It outlines the rates that have applied and the revenue yielded from excise duties in recent years. It also examines trends in consumption of excisable products. It considers both new and ongoing social, economic and political issues which may affect excise yields or consumption of the products on which excise duties apply. The paper also puts forward revenue raising options from excise duties. Finally the paper considers new potential excise duties which may be considered to fulfil a social or economic role. The paper is divided in to four sections: A. Tobacco Products Tax B. Alcohol Products Tax C. Betting Duty D. Sugar-Sweetened Drinks Tax Policy Approach to Excise Duties 2. Excise duties are taxes levied on specific goods and products. Following the widespread adoption of VAT in the 1970s and 1980s, many excise duties were abolished in Western Europe, with tobacco, alcohol and energy products remaining as the subjects of excise taxation. The move to complete the Single Market in the early 1990s led to the adoption of a number of Directives, some of which have since been updated, to govern the structure and rates of excise duty on certain excisable products throughout what is now the European Union. As such, Ireland’s excise duties in relation to tobacco, alcohol and energy products most comply with EU Directives in those areas, as well as with the Directive 2008/118/EC, which covers general arrangements for excise duty. 3. While the primary aim of excise duties is to raise revenue for the Exchequer, there are also ancillary objectives, including the deterrence of the consumption of harmful products, and the reflection of the external cost placed on society resulting from the consumption of such products. For example, tobacco consumption places significant current and future costs on the health services, while the abusive consumption of alcohol is linked to public order offences and negative health outcomes. Recent Developments Tobacco 4. Successive excise increases have been imposed on tobacco products over the past number of years. Since 2009 €1.39 has been added to a packet of 20 cigarettes in the most popular price category (MPPC) in excise and VAT. Smoking prevalence in Ireland has reduced by 7 percentage points since 2003. Fewer people are smoking than ten years ago and those that smoke are smoking less. The rates of non-Irish duty paid

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

TSG14/02

General Excise Duties

(Tobacco, Alcohol, Betting and Others)

Introduction

1. This paper examines the area of general excise duties which apply in the State. It

outlines the rates that have applied and the revenue yielded from excise duties in recent

years. It also examines trends in consumption of excisable products. It considers both

new and ongoing social, economic and political issues which may affect excise yields

or consumption of the products on which excise duties apply. The paper also puts

forward revenue raising options from excise duties. Finally the paper considers new

potential excise duties which may be considered to fulfil a social or economic role. The

paper is divided in to four sections:

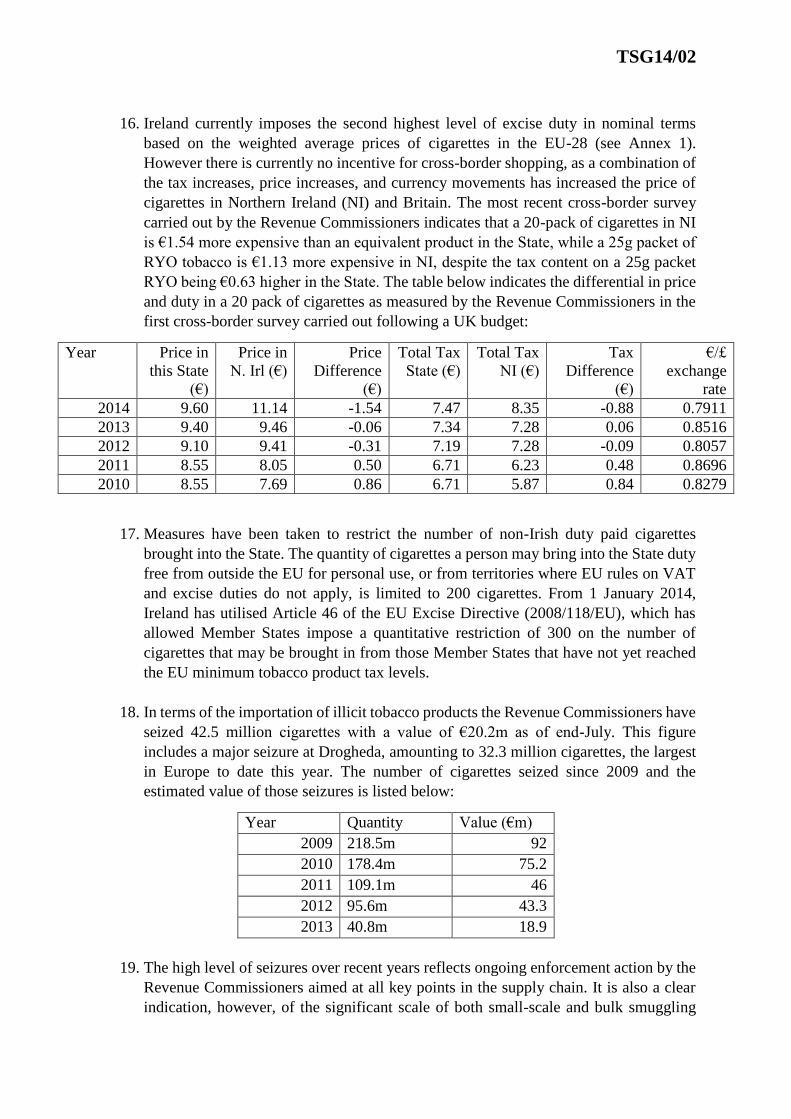

A. Tobacco Products Tax

B. Alcohol Products Tax

C. Betting Duty

D. Sugar-Sweetened Drinks Tax

Policy Approach to Excise Duties

2. Excise duties are taxes levied on specific goods and products. Following the widespread

adoption of VAT in the 1970s and 1980s, many excise duties were abolished in Western

Europe, with tobacco, alcohol and energy products remaining as the subjects of excise

taxation. The move to complete the Single Market in the early 1990s led to the adoption

of a number of Directives, some of which have since been updated, to govern the

structure and rates of excise duty on certain excisable products throughout what is now

the European Union. As such, Ireland’s excise duties in relation to tobacco, alcohol and

energy products most comply with EU Directives in those areas, as well as with the

Directive 2008/118/EC, which covers general arrangements for excise duty.

3. While the primary aim of excise duties is to raise revenue for the Exchequer, there are

also ancillary objectives, including the deterrence of the consumption of harmful

products, and the reflection of the external cost placed on society resulting from the

consumption of such products. For example, tobacco consumption places significant

current and future costs on the health services, while the abusive consumption of

alcohol is linked to public order offences and negative health outcomes.

Recent Developments

Tobacco

4. Successive excise increases have been imposed on tobacco products over the past

number of years. Since 2009 €1.39 has been added to a packet of 20 cigarettes in the

most popular price category (MPPC) in excise and VAT. Smoking prevalence in

Ireland has reduced by 7 percentage points since 2003. Fewer people are smoking than

ten years ago and those that smoke are smoking less. The rates of non-Irish duty paid

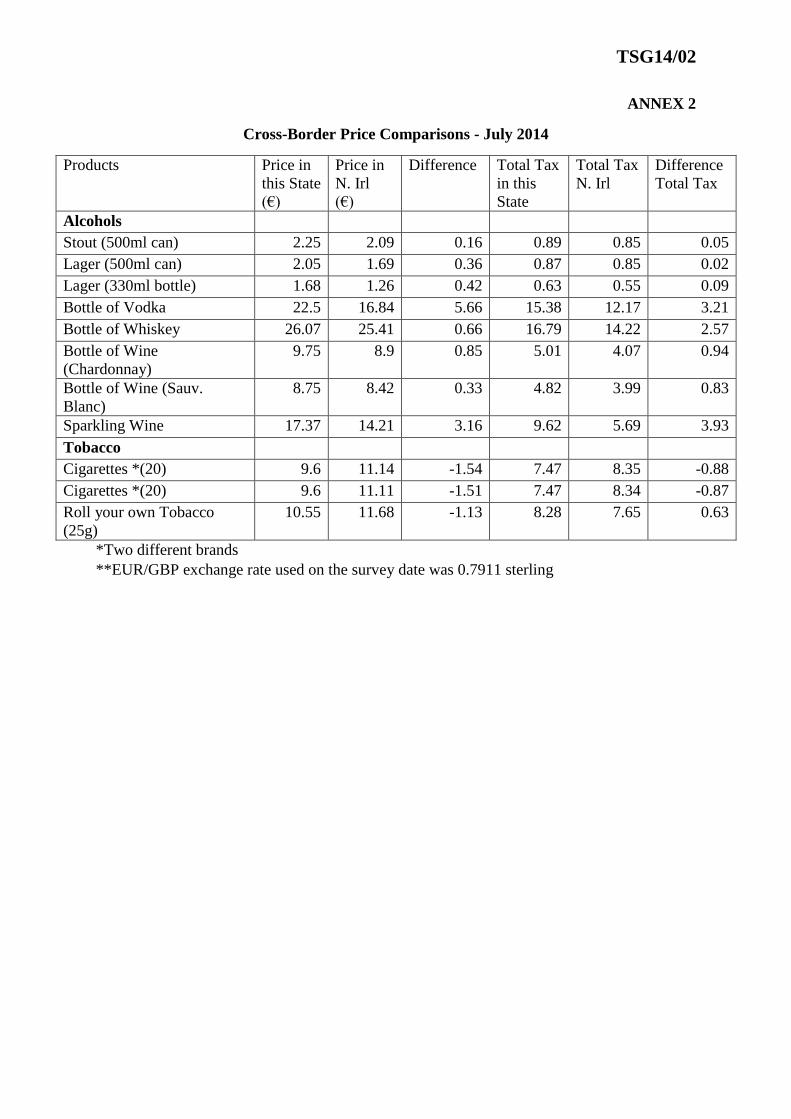

TSG14/02

and illicit cigarettes consumed in the country has reduced from 20% in 2009 to 16% in

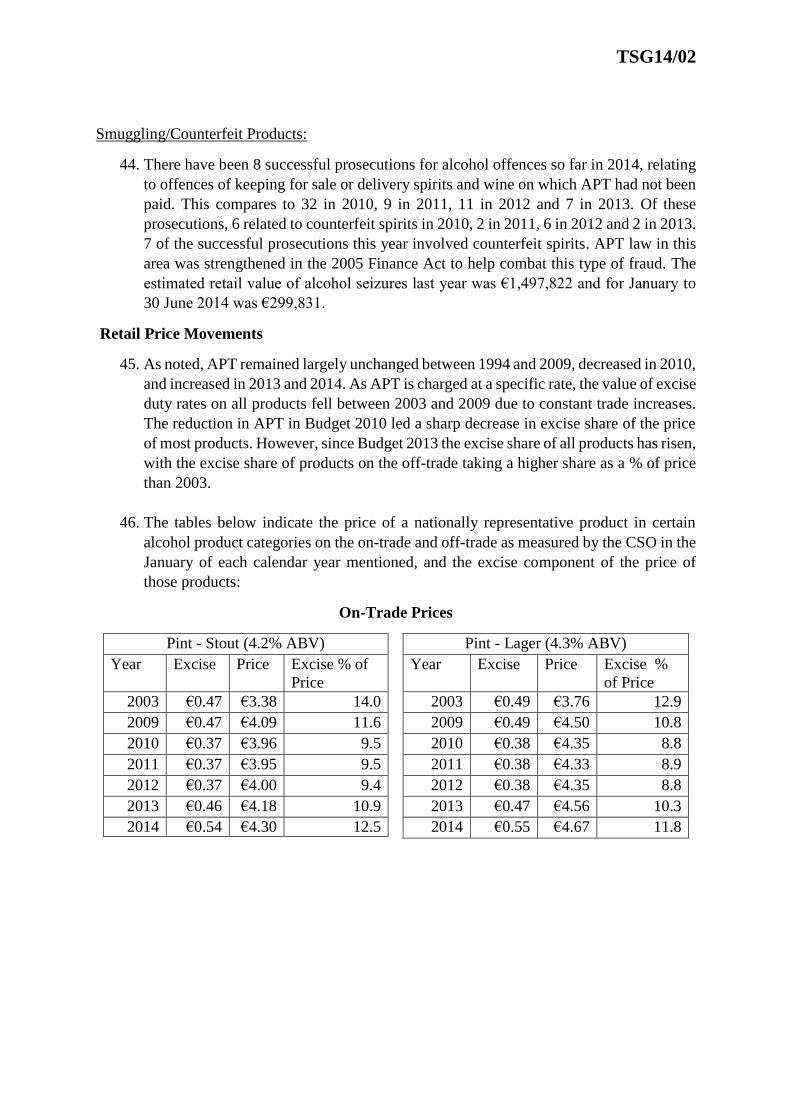

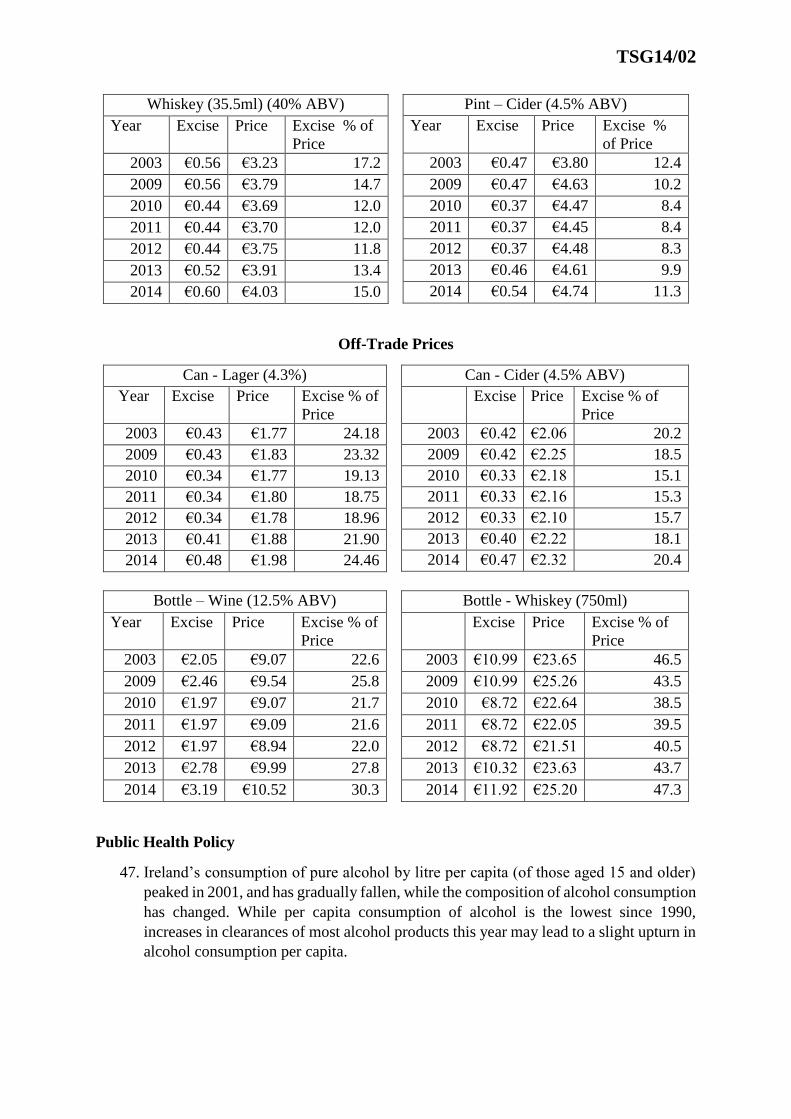

2013. Ireland currently imposes the second highest level of excise duty in nominal

terms in the EU-28, only the UK has higher excises on tobacco.

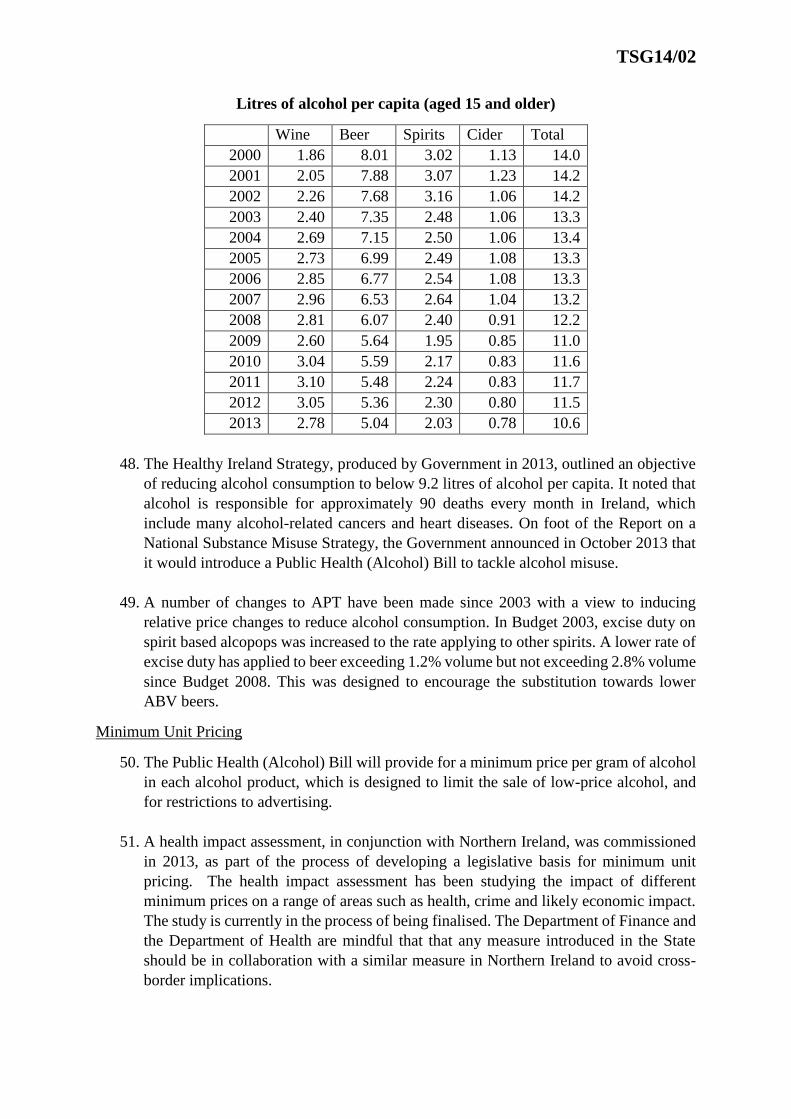

Alcohol

5. Excise duty on alcohol products was increased in Budgets 2013 and 2014. Excise duty

on alcohol products has remained largely unchanged between 1994 and 2010. However,

in Budget 2010, excise duty on all alcohol products was reduced by 20% (including

VAT). Alcohol consumption per capita has reduced significantly in recent years from

14.0 litres in 2000 to 10.6 litres in 2013. There has also been a shift in the type of

alcohol products consumed per capita. There has been a large increase (+79%) in the

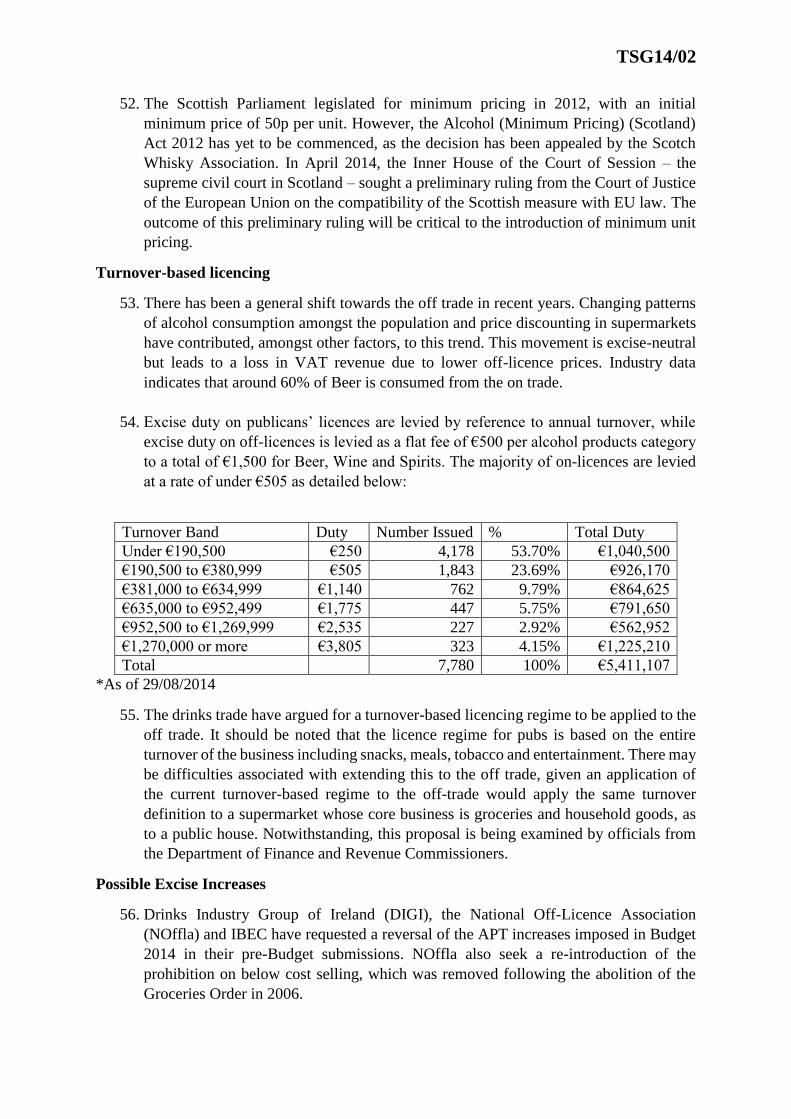

litres of wine cleared for consumption since 2000. There has also been a significant

decrease in the litres of beer cleared for consumption (-24%) over the same period.

Betting

6. Betting duty on bets placed with a traditional bookmaker has remained at 1% since

2006. The new Betting (Amendment) Bill 2013, currently going through the Houses

of the Oireachtas, seeks to bring all remote bookmakers and betting intermediaries,

otherwise known as betting exchanges, into the licensing and taxation regime regardless

of their location. It is estimated that the taxation of this new cohort will yield €20

million in a full year.

Sugar-Sweetened Drinks

7. Recently there have been calls from a number of quarters, particularly the Irish Heart

Foundation (IHF), to introduce a tax on sugar-sweetened drinks to kerb the obesity

problem in Ireland, particularly among the young. France and Hungary have recently

introduced a type of tax on sugar drink products. There may be significant difficulties

introducing a tax of this type as an excise duty in Ireland, and may give rise to

significant administrative costs and overheads for both business and Revenue.

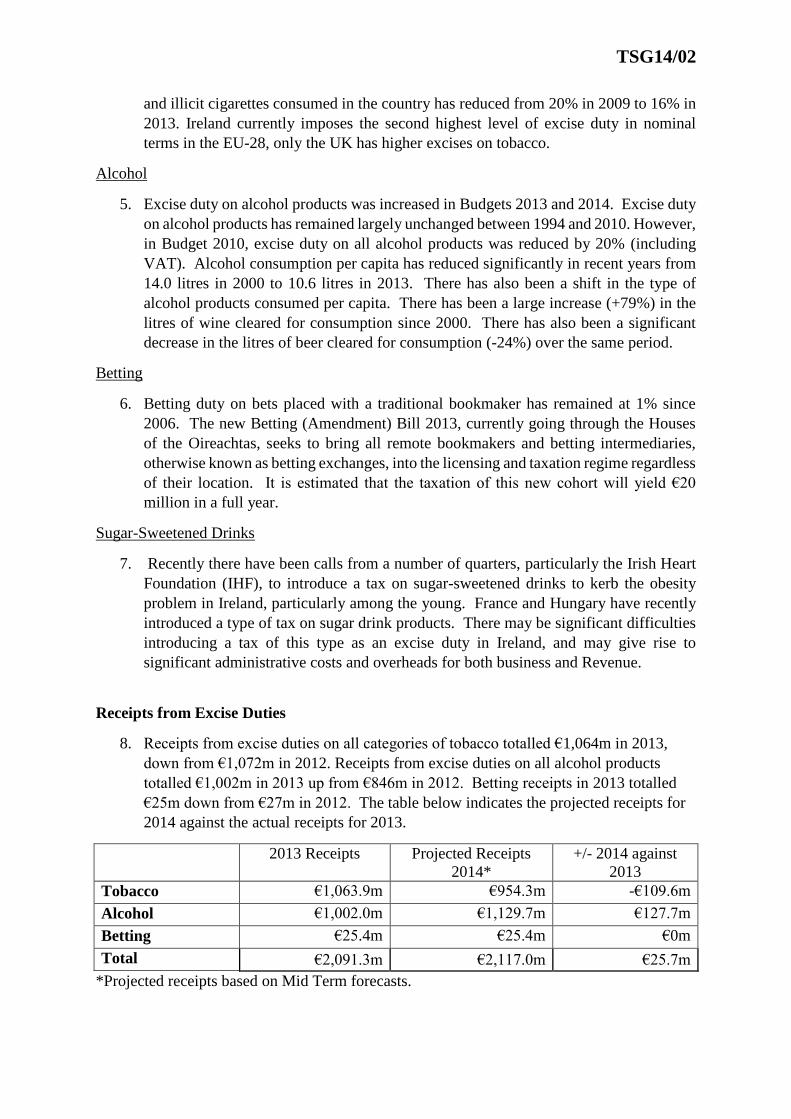

Receipts from Excise Duties

8. Receipts from excise duties on all categories of tobacco totalled €1,064m in 2013,

down from €1,072m in 2012. Receipts from excise duties on all alcohol products

totalled €1,002m in 2013 up from €846m in 2012. Betting receipts in 2013 totalled

€25m down from €27m in 2012. The table below indicates the projected receipts for

2014 against the actual receipts for 2013.

2013 Receipts Projected Receipts

2014*

+/- 2014 against

2013

Tobacco €1,063.9m €954.3m -€109.6m

Alcohol €1,002.0m €1,129.7m €127.7m

Betting €25.4m €25.4m €0m

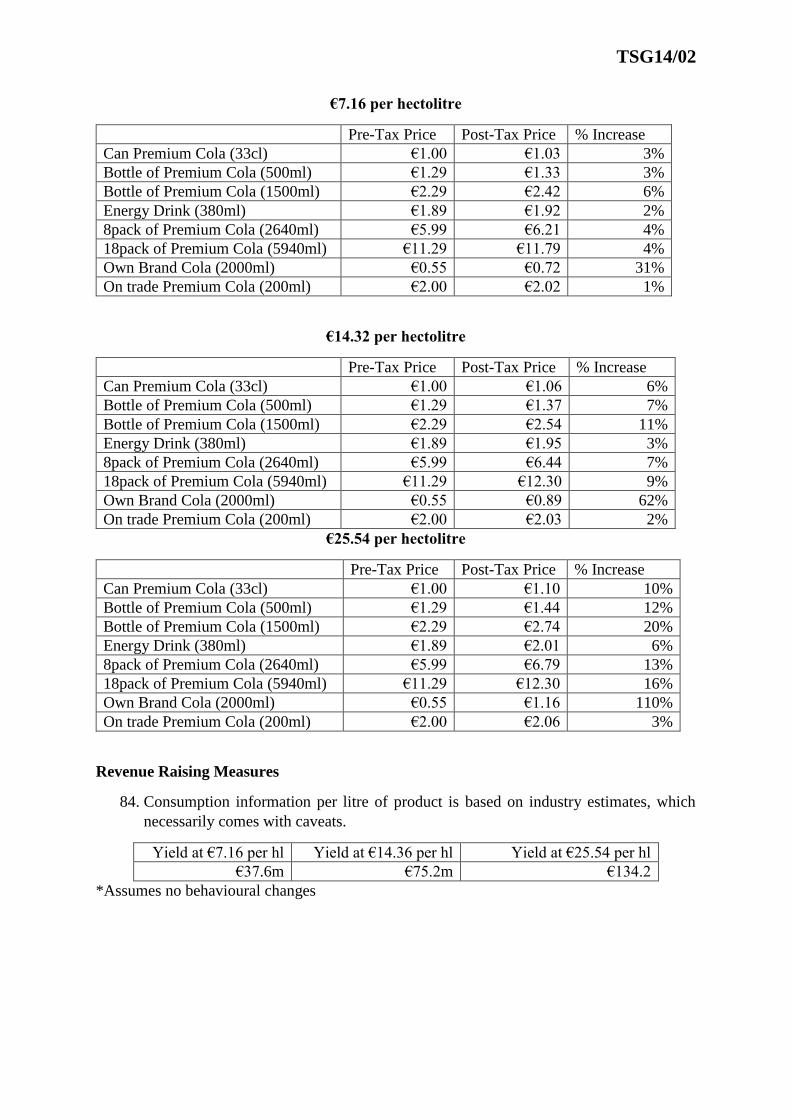

Total €2,091.3m €2,117.0m €25.7m

*Projected receipts based on Mid Term forecasts.

TSG14/02

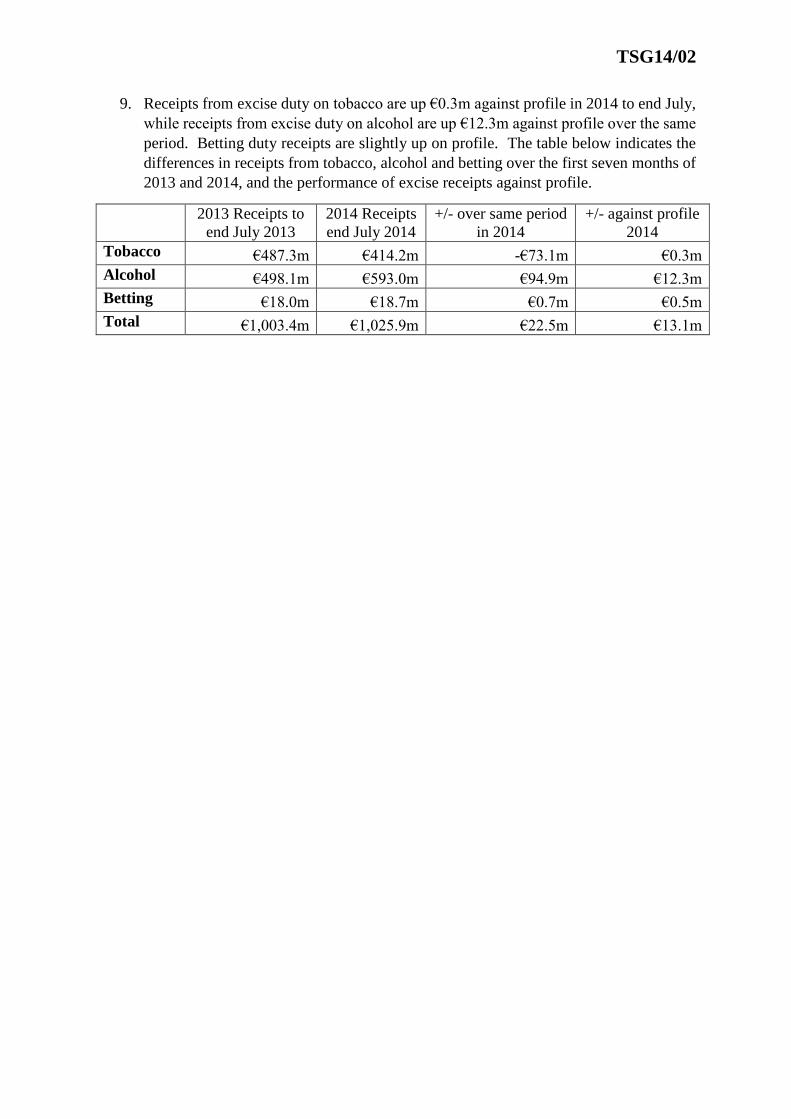

9. Receipts from excise duty on tobacco are up €0.3m against profile in 2014 to end July,

while receipts from excise duty on alcohol are up €12.3m against profile over the same

period. Betting duty receipts are slightly up on profile. The table below indicates the

differences in receipts from tobacco, alcohol and betting over the first seven months of

2013 and 2014, and the performance of excise receipts against profile.

2013 Receipts to

end July 2013

2014 Receipts

end July 2014

+/- over same period

in 2014

+/- against profile

2014

Tobacco €487.3m €414.2m -€73.1m €0.3m

Alcohol €498.1m €593.0m €94.9m €12.3m

Betting €18.0m €18.7m €0.7m €0.5m

Total €1,003.4m €1,025.9m €22.5m €13.1m

TSG14/02

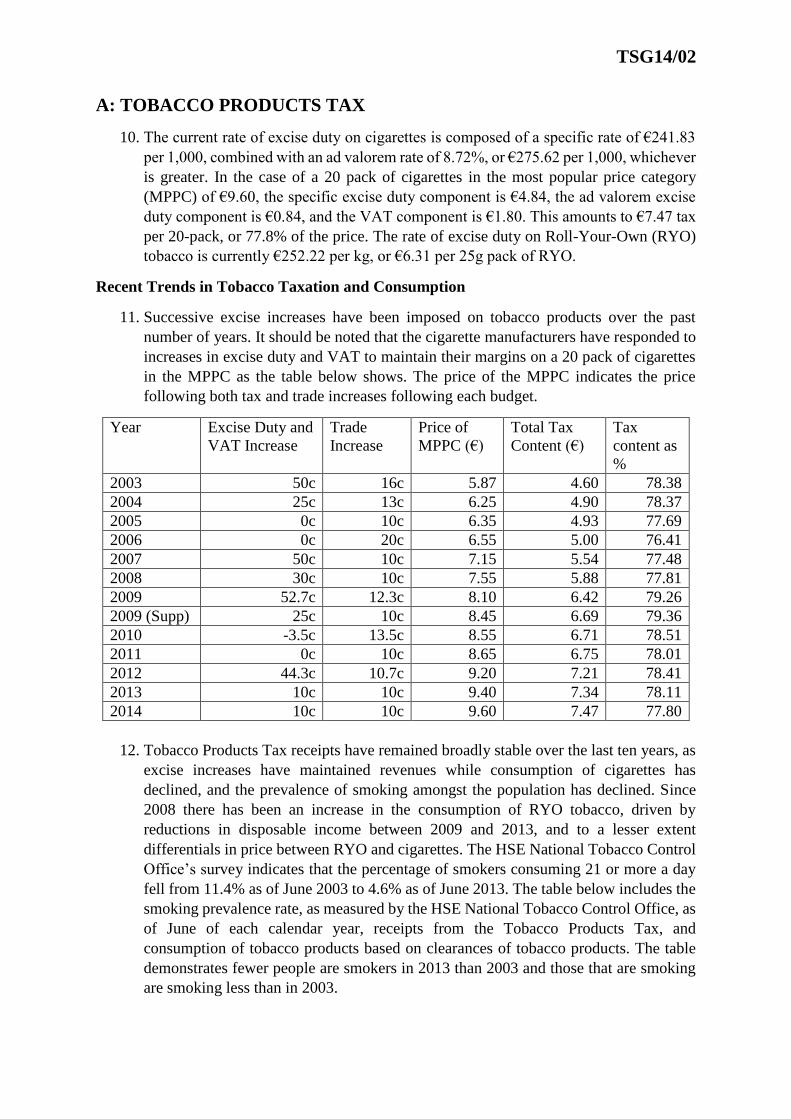

A: TOBACCO PRODUCTS TAX

10. The current rate of excise duty on cigarettes is composed of a specific rate of €241.83

per 1,000, combined with an ad valorem rate of 8.72%, or €275.62 per 1,000, whichever

is greater. In the case of a 20 pack of cigarettes in the most popular price category

(MPPC) of €9.60, the specific excise duty component is €4.84, the ad valorem excise

duty component is €0.84, and the VAT component is €1.80. This amounts to €7.47 tax

per 20-pack, or 77.8% of the price. The rate of excise duty on Roll-Your-Own (RYO)

tobacco is currently €252.22 per kg, or €6.31 per 25g pack of RYO.

Recent Trends in Tobacco Taxation and Consumption

11. Successive excise increases have been imposed on tobacco products over the past

number of years. It should be noted that the cigarette manufacturers have responded to

increases in excise duty and VAT to maintain their margins on a 20 pack of cigarettes

in the MPPC as the table below shows. The price of the MPPC indicates the price

following both tax and trade increases following each budget.

Year Excise Duty and

VAT Increase

Trade

Increase

Price of

MPPC (€)

Total Tax

Content (€)

Tax

content as

%

2003 50c 16c 5.87 4.60 78.38

2004 25c 13c 6.25 4.90 78.37

2005 0c 10c 6.35 4.93 77.69

2006 0c 20c 6.55 5.00 76.41

2007 50c 10c 7.15 5.54 77.48

2008 30c 10c 7.55 5.88 77.81

2009 52.7c 12.3c 8.10 6.42 79.26

2009 (Supp) 25c 10c 8.45 6.69 79.36

2010 -3.5c 13.5c 8.55 6.71 78.51

2011 0c 10c 8.65 6.75 78.01

2012 44.3c 10.7c 9.20 7.21 78.41

2013 10c 10c 9.40 7.34 78.11

2014 10c 10c 9.60 7.47 77.80

12. Tobacco Products Tax receipts have remained broadly stable over the last ten years, as

excise increases have maintained revenues while consumption of cigarettes has

declined, and the prevalence of smoking amongst the population has declined. Since

2008 there has been an increase in the consumption of RYO tobacco, driven by

reductions in disposable income between 2009 and 2013, and to a lesser extent

differentials in price between RYO and cigarettes. The HSE National Tobacco Control

Office’s survey indicates that the percentage of smokers consuming 21 or more a day

fell from 11.4% as of June 2003 to 4.6% as of June 2013. The table below includes the

smoking prevalence rate, as measured by the HSE National Tobacco Control Office, as

of June of each calendar year, receipts from the Tobacco Products Tax, and

consumption of tobacco products based on clearances of tobacco products. The table

demonstrates fewer people are smokers in 2013 than 2003 and those that are smoking

are smoking less than in 2003.

TSG14/02

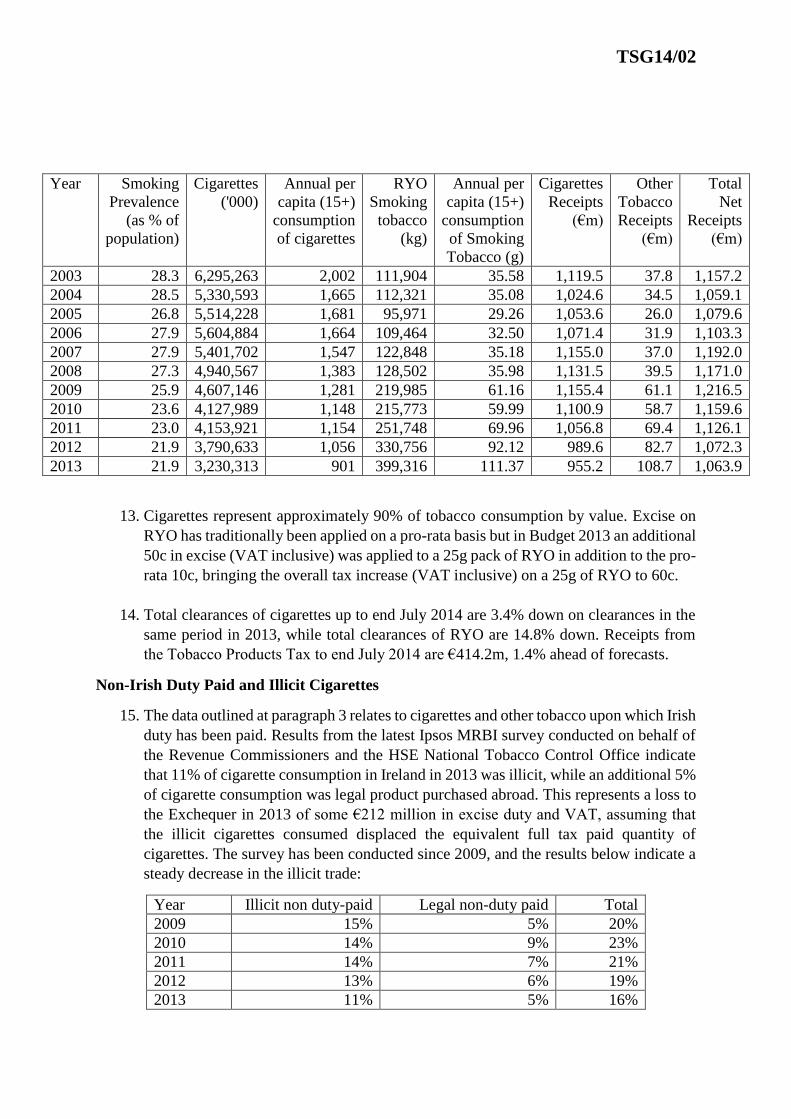

13. Cigarettes represent approximately 90% of tobacco consumption by value. Excise on

RYO has traditionally been applied on a pro-rata basis but in Budget 2013 an additional

50c in excise (VAT inclusive) was applied to a 25g pack of RYO in addition to the pro-

rata 10c, bringing the overall tax increase (VAT inclusive) on a 25g of RYO to 60c.

14. Total clearances of cigarettes up to end July 2014 are 3.4% down on clearances in the

same period in 2013, while total clearances of RYO are 14.8% down. Receipts from

the Tobacco Products Tax to end July 2014 are €414.2m, 1.4% ahead of forecasts.

Non-Irish Duty Paid and Illicit Cigarettes

15. The data outlined at paragraph 3 relates to cigarettes and other tobacco upon which Irish

duty has been paid. Results from the latest Ipsos MRBI survey conducted on behalf of

the Revenue Commissioners and the HSE National Tobacco Control Office indicate

that 11% of cigarette consumption in Ireland in 2013 was illicit, while an additional 5%

of cigarette consumption was legal product purchased abroad. This represents a loss to

the Exchequer in 2013 of some €212 million in excise duty and VAT, assuming that

the illicit cigarettes consumed displaced the equivalent full tax paid quantity of

cigarettes. The survey has been conducted since 2009, and the results below indicate a

steady decrease in the illicit trade:

Year Illicit non duty-paid Legal non-duty paid Total

2009 15% 5% 20%

2010 14% 9% 23%

2011 14% 7% 21%

2012 13% 6% 19%

2013 11% 5% 16%

Year Smoking

Prevalence

(as % of

population)

Cigarettes

('000)

Annual per

capita (15+)

consumption

of cigarettes

RYO

Smoking

tobacco

(kg)

Annual per

capita (15+)

consumption

of Smoking

Tobacco (g)

Cigarettes

Receipts

(€m)

Other

Tobacco

Receipts

(€m)

Total

Net

Receipts

(€m)

2003 28.3 6,295,263 2,002 111,904 35.58 1,119.5 37.8 1,157.2

2004 28.5 5,330,593 1,665 112,321 35.08 1,024.6 34.5 1,059.1

2005 26.8 5,514,228 1,681 95,971 29.26 1,053.6 26.0 1,079.6

2006 27.9 5,604,884 1,664 109,464 32.50 1,071.4 31.9 1,103.3

2007 27.9 5,401,702 1,547 122,848 35.18 1,155.0 37.0 1,192.0

2008 27.3 4,940,567 1,383 128,502 35.98 1,131.5 39.5 1,171.0

2009 25.9 4,607,146 1,281 219,985 61.16 1,155.4 61.1 1,216.5

2010 23.6 4,127,989 1,148 215,773 59.99 1,100.9 58.7 1,159.6

2011 23.0 4,153,921 1,154 251,748 69.96 1,056.8 69.4 1,126.1

2012 21.9 3,790,633 1,056 330,756 92.12 989.6 82.7 1,072.3

2013 21.9 3,230,313 901 399,316 111.37 955.2 108.7 1,063.9

TSG14/02

16. Ireland currently imposes the second highest level of excise duty in nominal terms

based on the weighted average prices of cigarettes in the EU-28 (see Annex 1).

However there is currently no incentive for cross-border shopping, as a combination of

the tax increases, price increases, and currency movements has increased the price of

cigarettes in Northern Ireland (NI) and Britain. The most recent cross-border survey

carried out by the Revenue Commissioners indicates that a 20-pack of cigarettes in NI

is €1.54 more expensive than an equivalent product in the State, while a 25g packet of

RYO tobacco is €1.13 more expensive in NI, despite the tax content on a 25g packet

RYO being €0.63 higher in the State. The table below indicates the differential in price

and duty in a 20 pack of cigarettes as measured by the Revenue Commissioners in the

first cross-border survey carried out following a UK budget:

Year Price in

this State

(€)

Price in

N. Irl (€)

Price

Difference

(€)

Total Tax

State (€)

Total Tax

NI (€)

Tax

Difference

(€)

€/£

exchange

rate

2014 9.60 11.14 -1.54 7.47 8.35 -0.88 0.7911

2013 9.40 9.46 -0.06 7.34 7.28 0.06 0.8516

2012 9.10 9.41 -0.31 7.19 7.28 -0.09 0.8057

2011 8.55 8.05 0.50 6.71 6.23 0.48 0.8696

2010 8.55 7.69 0.86 6.71 5.87 0.84 0.8279

17. Measures have been taken to restrict the number of non-Irish duty paid cigarettes

brought into the State. The quantity of cigarettes a person may bring into the State duty

free from outside the EU for personal use, or from territories where EU rules on VAT

and excise duties do not apply, is limited to 200 cigarettes. From 1 January 2014,

Ireland has utilised Article 46 of the EU Excise Directive (2008/118/EU), which has

allowed Member States impose a quantitative restriction of 300 on the number of

cigarettes that may be brought in from those Member States that have not yet reached

the EU minimum tobacco product tax levels.

18. In terms of the importation of illicit tobacco products the Revenue Commissioners have

seized 42.5 million cigarettes with a value of €20.2m as of end-July. This figure

includes a major seizure at Drogheda, amounting to 32.3 million cigarettes, the largest

in Europe to date this year. The number of cigarettes seized since 2009 and the

estimated value of those seizures is listed below:

Year Quantity Value (€m)

2009 218.5m 92

2010 178.4m 75.2

2011 109.1m 46

2012 95.6m 43.3

2013 40.8m 18.9

19. The high level of seizures over recent years reflects ongoing enforcement action by the

Revenue Commissioners aimed at all key points in the supply chain. It is also a clear

indication, however, of the significant scale of both small-scale and bulk smuggling

TSG14/02

activity. Legislative action has been taken over recent years to further strengthen

Revenue’s powers to respond effectively to the problem of the illegal tobacco trade:

The Finance Act 2012 clarified the legal basis for Revenue officers to open and

examine the contents of postal and courier packets that are reasonably believed

to contain untaxed excise products.

The Finance Act 2013 introduced new offence and forfeiture measures relating

to the illicit production of tobacco and also strengthened the offence provisions

relating to the sale or delivery of unstamped tobacco products.

The Finance (No. 2) Act 2013 provided that a person suspected of an offence of

dealing in, or with, unstamped tobacco products must provide information to a

Revenue Officer or a Garda and may be required to present any tobacco product

concerned for examination, and makes provision for search by a Revenue

Officer or Garda of any bag or other receptacle that he or she reasonably

believes to contain tobacco products that are concerned in the offence.

Public Health Policy: Tobacco Control Policies and Standardised Packaging

20. Smoking is the leading cause of preventable death in Ireland, accounting for at nearly

19% (or 5,200) of deaths annually. It is estimated that one out of every two long-term

smokers will die of a disease related to their tobacco use. In March 2013 the

Government published Healthy Ireland, a Framework document outlining public health

objectives out to 2025. The Framework outlined a preliminary objective of reducing

smoking prevalence and smoking initiation by 1 percentage point per annum. In

October 2013 the Department of Health published Tobacco Free Ireland, a Report of

the Tobacco Policy Review Group, confirming a target of less than 5% smoking

prevalence by 2025, which implies a 77% reduction in the numbers smoking between

2013 and 2025.

21. In Tobacco Free Ireland, the Department of Health made a number of recommendations

in relation to fiscal policy, including raising excise duty on tobacco products over a five

year period and reducing the price differential between RYO and cigarettes.

22. Increasing excise duty on tobacco products is only one of a number of measures that

contributes to the overall strategy to reducing tobacco consumption and smoking

prevalence. As part of tobacco control policy a range of initiatives have been introduced

over the past number of years, including a prohibition on tobacco advertising, a

prohibition on sponsorship, the smoking ban in January 2004, a prohibition on the sale

of cigarettes in packs of less than 20 in May 2007 and in July 2009 a ban on the

advertising and display of tobacco products in retail outlets.

Standardised Packaging

23. Regulations to introduce combined text and photo warnings on tobacco products came

into force on 1 February 2013. In June 2014 the Government approved the Public

Health (Standardised Packaging of Tobacco) Bill 2014, which will remove all forms of

branding including trademarks, logo, colours and graphics from packs, except for the

brand and variant name which will be presented in a uniform typeface. It is expected

that the measures will come into force in 2016. It is estimated that 80% of smokers start

TSG14/02

when they are children, and standardised packaging legislation is designed to reduce

smoking initiation rates.

24. Australia introduced standardised packaging in December 2012, while in April 2014

the British government announced it plans to legislate for the introduction of

standardised packaging. The tobacco industry has been strongly opposed to the

introduction of standardised packaging, and has threatened legal action against the

State, based on the argument that standardised packaging amounts to an expropriation

of their intellectual property. Indonesia, Cuba, the Dominican Republic, Honduras and

Ukraine have all challenged Australia’s standardised packaging through the World

Trade Organisation’s (WTO) dispute resolution mechanism.

25. The Revenue Commissioners are satisfied that the proposed standardised packaging of

tobacco products will not damage their work to tackle the illicit tobacco trade. Revenue

relies on the tax stamp to identify tax paid tobacco products, and the standardised

packaging legislation will accommodate the stamp. The tax stamp contains a range of

features designed to minimise the risk of counterfeiting.

EU Context – Directive 2011/64/EU

26. Directive 2011/64/EU has codified previous Directives regulating the structure of

duties imposed on tobacco products. The Directive requires the tax imposed on

cigarettes to be composed of both a specific and ad valorem component, and imposes a

ceiling such that the specific component may be no more than 76.5% of the total tax

take (i.e. excise and VAT) based on the Weighted Average Retail Selling Price (WAP).

Ireland rebalanced its rates in Finance Act 2012, so that the specific component is

currently 66% of the total tax based on the WAP. There have been calls from the Irish

Heart Foundation and Irish Cancer Society to extend the specific element to a higher

percentage of the total tax take, but while a higher specific element provides greater

security of revenue in the event of price decreases, it would mean the Exchequer taking

a lower yield from any trade increases.

27. The tobacco market in Ireland is characterised by a high market share (nearly 75%) for

cigarettes which occupy the higher price points in the market. Given the Directive

provides that manufacturers and importers are free to determine the maximum retail

selling price of cigarettes placed on the market in a Member State, the tobacco industry

can mitigate any attempt to reduce their share of the price of cigarettes. As the table

under paragraph 2 displays, the tobacco industry have maintained the trade share of the

price of a 20 pack of cigarettes in the MPPC.

Reducing the ad valorem rate would also prevent the Exchequer taking a share of any

trade increase. For example, the Budget 2014 tax increase of 10c raised the price of a

pack of 20 cigarettes in the MPPC to €9.50. A subsequent trade increase in June 2014

increased this to €9.60. This 10 cent trade increase resulted in an additional tax take of

3 cent (1 cent TPT and 2 cent VAT). If the tax structure was based on a maximum

specific component and a minimum ad valorem component, a similar increase in the

TSG14/02

retail selling price would result in a VAT increase of 2 cents but virtually no additional

excise duty.

Minimum Excise Duty

28. Directive 2011/64/EU also contained a provision allowing for application of a

minimum excise duty (MED) on cigarettes, provided the mixed structure of the tax (that is,

the combination of specific and ad valorem elements) and the specific element parameters are

respected. On 1 May 2012 a minimum amount of duty was introduced that has to be paid

irrespective of the price at which cigarettes are sold. The current minimum amount is

€275.62 per thousand in respect of cigarettes sold by retail where the rate of tax would

be less than that rate had the rate been calculated to the specific and ad valorem formula.

The current MED represents the excise duty payable on a packet of 20 cigarettes priced

at €7.75.

29. It may be prudent to increase the MED to €276.71 per thousand, which represents the

excise duty payable on a packet of 20 cigarettes priced at €8.00. This will provide

greater security of revenue if the tobacco industry introduces a brand of cigarettes at a

lower price point than €8.00.

Relative Rates of Tobacco Duty on Different Tobacco Products

30. The consumption of RYO has nearly tripled since 2008, although it still represents a

relatively small portion of the tobacco market. As noted, excise duty on a 25g pack of

RYO was increased by 60c (VAT included) in Budget 2013, against a 10c increase in

cigarettes in the same budget.

31. Given the differences in product characteristics and tax bases, comparisons of the tax

levels applicable to cigarettes and RYO are difficult and inexact. However, if it is

assumed that a kilogram of RYO tobacco yields 1,320 commercially-produced

cigarettes, the tax applicable (excluding VAT) to a kilogram of tobacco (based on a

price of €9.60 per pack of 20 cigarettes) can be estimated to be €374.47, while the tax

levied on a kilogram of RYO tobacco is €252.22. The comparison can provide only a

general indication, but it is reasonable to conclude that the tax burden on RYO tobacco

is substantially less than that on cigarettes.

Possible Excise Increases

32. The Irish Heart Foundation (IHF) and Irish Cancer Society (ICS) have recommended,

in their pre-Budget submission, the introduction of a tobacco price escalator of CPI +

5%, and the increase in the level of specific excise duty levied on tobacco products to

the maximum permissible level of 76.5% of the WAP. The IHF and ICS have also

recommended that the tax applied to RYO be increased by CPI + 15% until such a time

as the price of RYO is equalised with cigarettes.

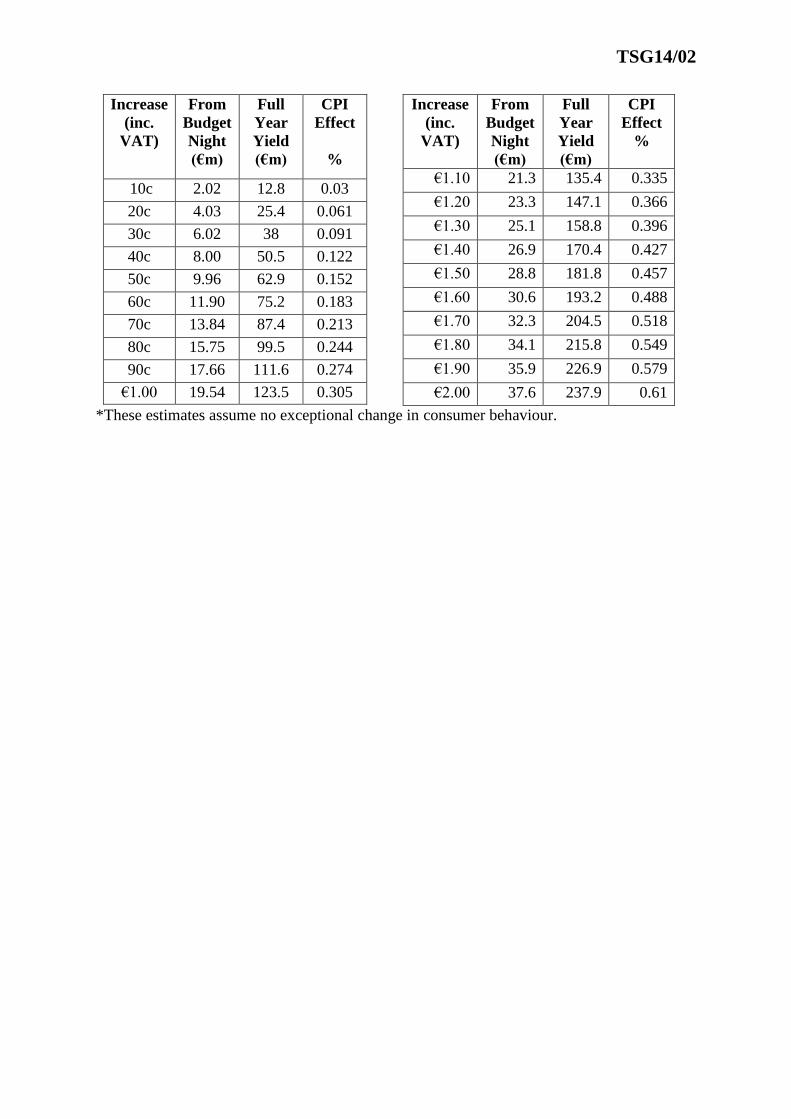

33. The table below indicates the effects of increasing various levels of increased duty (on

cigarettes, with pro rata increases on other tobacco products – calculated on the basis

of maintaining specific duty at 65% of total tax).

TSG14/02

Increase

(inc.

VAT)

From

Budget

Night

(€m)

Full

Year

Yield

(€m)

CPI

Effect

%

10c 2.02 12.8 0.03

20c 4.03 25.4 0.061

30c 6.02 38 0.091

40c 8.00 50.5 0.122

50c 9.96 62.9 0.152

60c 11.90 75.2 0.183

70c 13.84 87.4 0.213

80c 15.75 99.5 0.244

90c 17.66 111.6 0.274

€1.00 19.54 123.5 0.305

Increase

(inc.

VAT)

From

Budget

Night

(€m)

Full

Year

Yield

(€m)

CPI

Effect

%

€1.10 21.3 135.4 0.335

€1.20 23.3 147.1 0.366

€1.30 25.1 158.8 0.396

€1.40 26.9 170.4 0.427

€1.50 28.8 181.8 0.457

€1.60 30.6 193.2 0.488

€1.70 32.3 204.5 0.518

€1.80 34.1 215.8 0.549

€1.90 35.9 226.9 0.579

€2.00 37.6 237.9 0.61

*These estimates assume no exceptional change in consumer behaviour.

TSG14/02

B: ALCOHOL PRODUCTS TAX

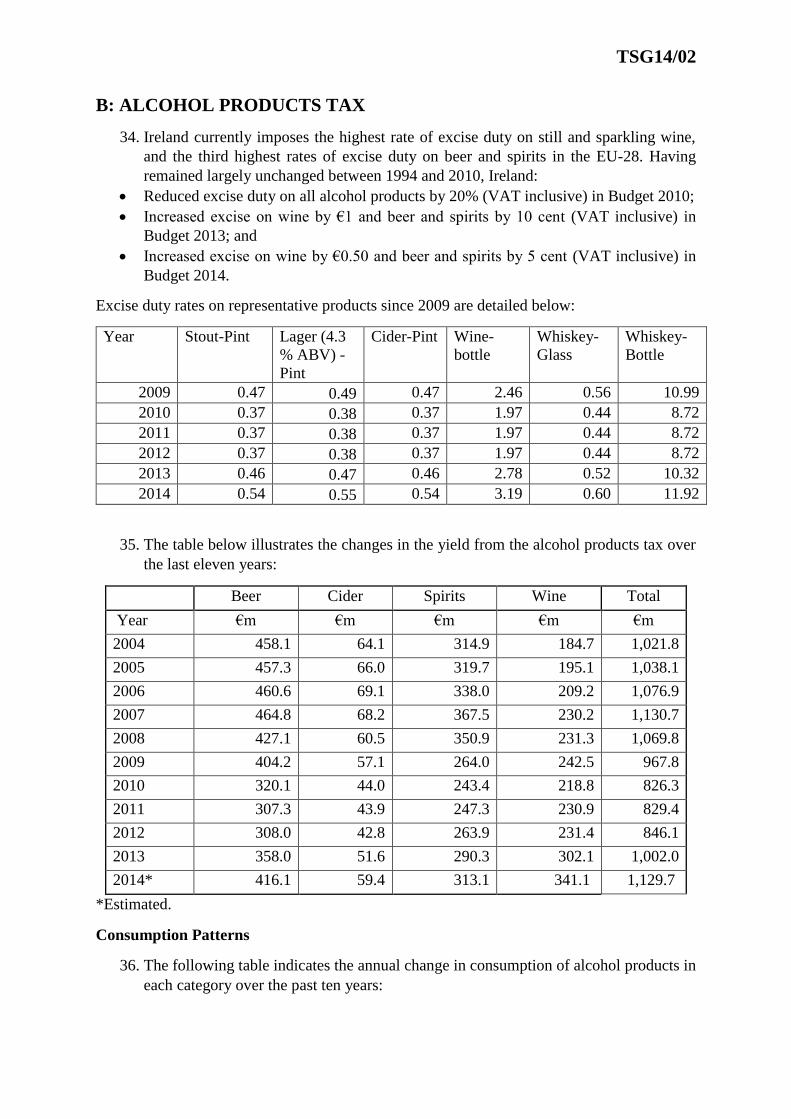

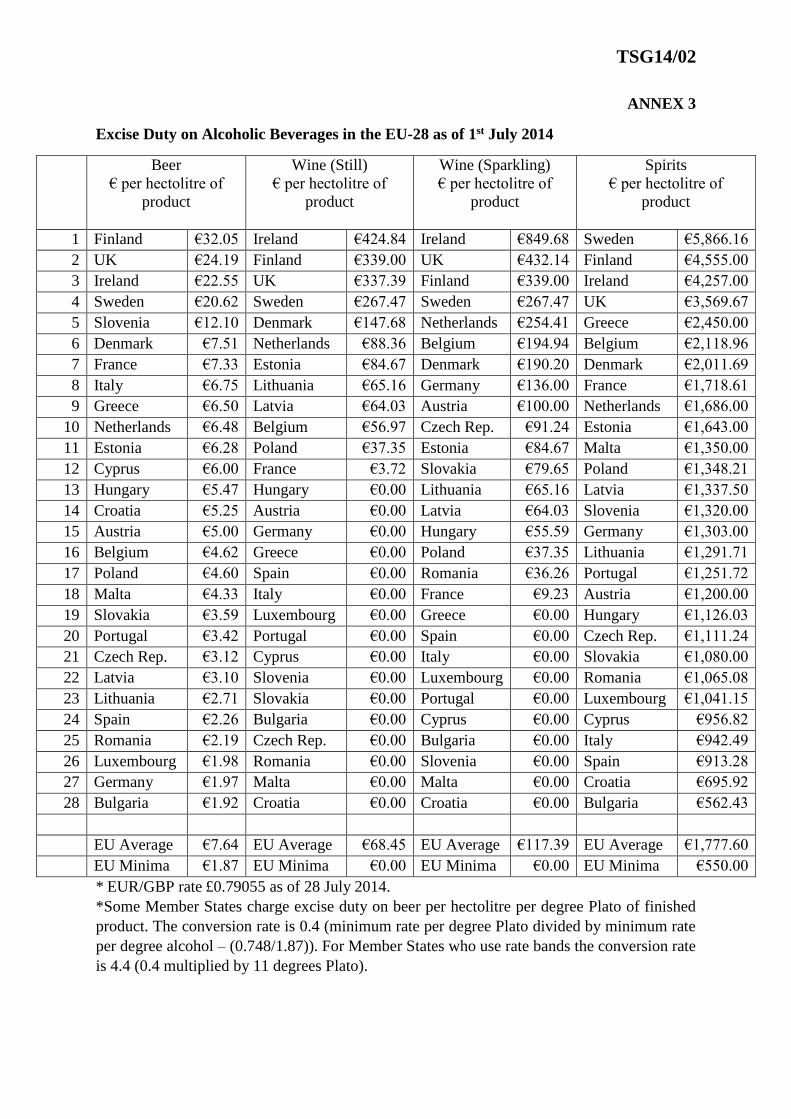

34. Ireland currently imposes the highest rate of excise duty on still and sparkling wine,

and the third highest rates of excise duty on beer and spirits in the EU-28. Having

remained largely unchanged between 1994 and 2010, Ireland:

Reduced excise duty on all alcohol products by 20% (VAT inclusive) in Budget 2010;

Increased excise on wine by €1 and beer and spirits by 10 cent (VAT inclusive) in

Budget 2013; and

Increased excise on wine by €0.50 and beer and spirits by 5 cent (VAT inclusive) in

Budget 2014.

Excise duty rates on representative products since 2009 are detailed below:

Year Stout-Pint Lager (4.3

% ABV) -

Pint

Cider-Pint Wine-

bottle

Whiskey-

Glass

Whiskey-

Bottle

2009 0.47 0.49 0.47 2.46 0.56 10.99

2010 0.37 0.38 0.37 1.97 0.44 8.72

2011 0.37 0.38 0.37 1.97 0.44 8.72

2012 0.37 0.38 0.37 1.97 0.44 8.72

2013 0.46 0.47 0.46 2.78 0.52 10.32

2014 0.54 0.55 0.54 3.19 0.60 11.92

35. The table below illustrates the changes in the yield from the alcohol products tax over

the last eleven years:

Beer Cider Spirits Wine Total

Year €m €m €m €m €m

2004 458.1 64.1 314.9 184.7 1,021.8

2005 457.3 66.0 319.7 195.1 1,038.1

2006 460.6 69.1 338.0 209.2 1,076.9

2007 464.8 68.2 367.5 230.2 1,130.7

2008 427.1 60.5 350.9 231.3 1,069.8

2009 404.2 57.1 264.0 242.5 967.8

2010 320.1 44.0 243.4 218.8 826.3

2011 307.3 43.9 247.3 230.9 829.4

2012 308.0 42.8 263.9 231.4 846.1

2013 358.0 51.6 290.3 302.1 1,002.0

2014* 416.1 59.4 313.1 341.1 1,129.7

*Estimated.

Consumption Patterns

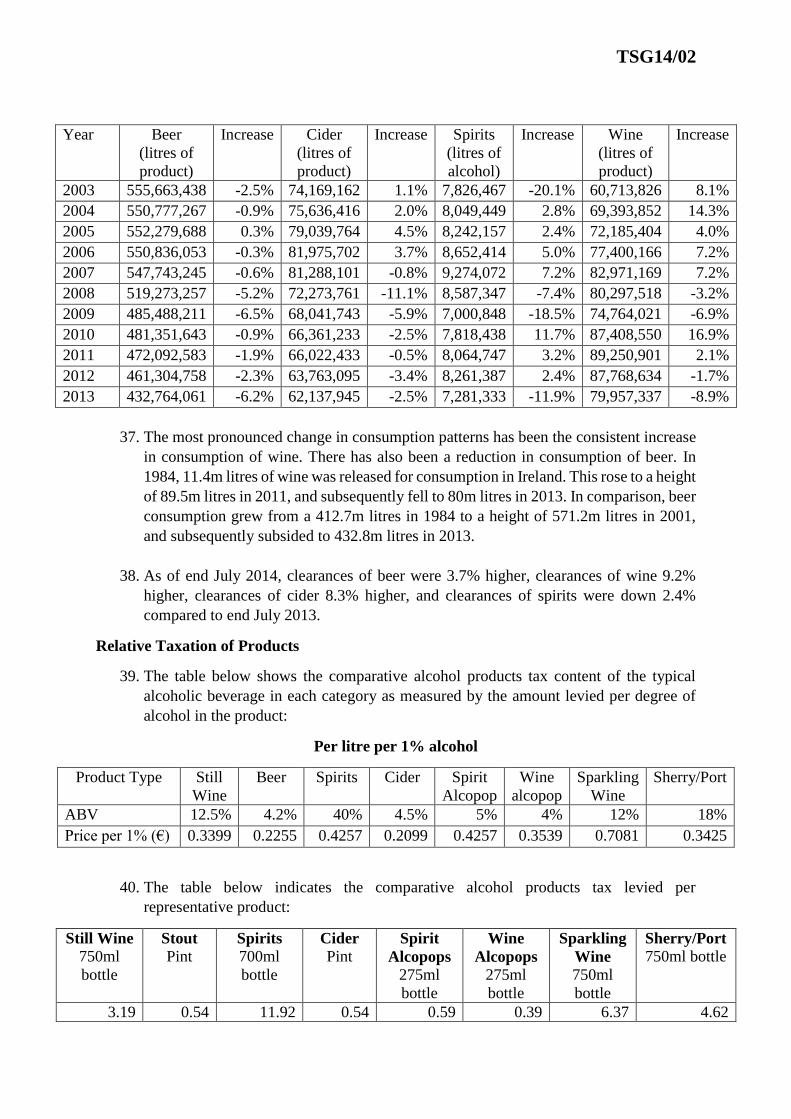

36. The following table indicates the annual change in consumption of alcohol products in

each category over the past ten years:

TSG14/02

Year Beer

(litres of

product)

Increase Cider

(litres of

product)

Increase Spirits

(litres of

alcohol)

Increase Wine

(litres of

product)

Increase

2003 555,663,438 -2.5% 74,169,162 1.1% 7,826,467 -20.1% 60,713,826 8.1%

2004 550,777,267 -0.9% 75,636,416 2.0% 8,049,449 2.8% 69,393,852 14.3%

2005 552,279,688 0.3% 79,039,764 4.5% 8,242,157 2.4% 72,185,404 4.0%

2006 550,836,053 -0.3% 81,975,702 3.7% 8,652,414 5.0% 77,400,166 7.2%

2007 547,743,245 -0.6% 81,288,101 -0.8% 9,274,072 7.2% 82,971,169 7.2%

2008 519,273,257 -5.2% 72,273,761 -11.1% 8,587,347 -7.4% 80,297,518 -3.2%

2009 485,488,211 -6.5% 68,041,743 -5.9% 7,000,848 -18.5% 74,764,021 -6.9%

2010 481,351,643 -0.9% 66,361,233 -2.5% 7,818,438 11.7% 87,408,550 16.9%

2011 472,092,583 -1.9% 66,022,433 -0.5% 8,064,747 3.2% 89,250,901 2.1%

2012 461,304,758 -2.3% 63,763,095 -3.4% 8,261,387 2.4% 87,768,634 -1.7%

2013 432,764,061 -6.2% 62,137,945 -2.5% 7,281,333 -11.9% 79,957,337 -8.9%

37. The most pronounced change in consumption patterns has been the consistent increase

in consumption of wine. There has also been a reduction in consumption of beer. In

1984, 11.4m litres of wine was released for consumption in Ireland. This rose to a height

of 89.5m litres in 2011, and subsequently fell to 80m litres in 2013. In comparison, beer

consumption grew from a 412.7m litres in 1984 to a height of 571.2m litres in 2001,

and subsequently subsided to 432.8m litres in 2013.

38. As of end July 2014, clearances of beer were 3.7% higher, clearances of wine 9.2%

higher, clearances of cider 8.3% higher, and clearances of spirits were down 2.4%

compared to end July 2013.

Relative Taxation of Products

39. The table below shows the comparative alcohol products tax content of the typical

alcoholic beverage in each category as measured by the amount levied per degree of

alcohol in the product:

Per litre per 1% alcohol

Product Type Still

Wine

Beer Spirits Cider Spirit

Alcopop

Wine

alcopop

Sparkling

Wine

Sherry/Port

ABV 12.5% 4.2% 40% 4.5% 5% 4% 12% 18%

Price per 1% (€) 0.3399 0.2255 0.4257 0.2099 0.4257 0.3539 0.7081 0.3425

40. The table below indicates the comparative alcohol products tax levied per

representative product:

Still Wine

750ml

bottle

Stout

Pint Spirits

700ml

bottle

Cider

Pint Spirit

Alcopops

275ml

bottle

Wine

Alcopops

275ml

bottle

Sparkling

Wine

750ml

bottle

Sherry/Port

750ml bottle

3.19 0.54 11.92 0.54 0.59 0.39 6.37 4.62

TSG14/02

41. A relief, of 50% of the APT paid, applies to tax paid at the rate applicable to beer

exceeding 2.8% alcohol by volume, which is produced in microbreweries – defined as

a brewery in which not more than 20,000 hectolitres of beer is brewed - located within

the European Union. In 2013, 25 microbreweries availed of this relief at a cost of just

over €970,000.

Non-Irish Duty Paid Alcohol: Cross-border purchases and counterfeit alcohol

Cross-Border Purchases

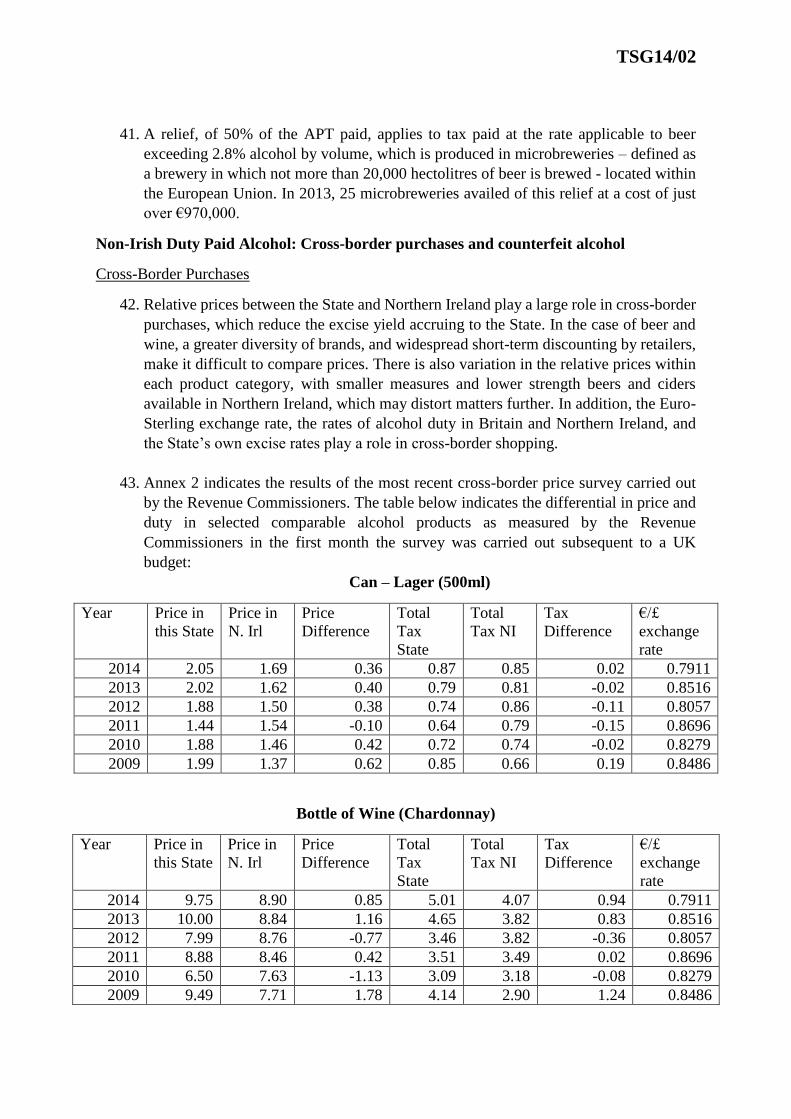

42. Relative prices between the State and Northern Ireland play a large role in cross-border

purchases, which reduce the excise yield accruing to the State. In the case of beer and

wine, a greater diversity of brands, and widespread short-term discounting by retailers,

make it difficult to compare prices. There is also variation in the relative prices within

each product category, with smaller measures and lower strength beers and ciders

available in Northern Ireland, which may distort matters further. In addition, the Euro-

Sterling exchange rate, the rates of alcohol duty in Britain and Northern Ireland, and

the State’s own excise rates play a role in cross-border shopping.

43. Annex 2 indicates the results of the most recent cross-border price survey carried out

by the Revenue Commissioners. The table below indicates the differential in price and

duty in selected comparable alcohol products as measured by the Revenue

Commissioners in the first month the survey was carried out subsequent to a UK

budget:

Can – Lager (500ml)

Year Price in

this State

Price in

N. Irl

Price

Difference

Total

Tax

State

Total

Tax NI

Tax

Difference

€/£

exchange

rate

2014 2.05 1.69 0.36 0.87 0.85 0.02 0.7911

2013 2.02 1.62 0.40 0.79 0.81 -0.02 0.8516

2012 1.88 1.50 0.38 0.74 0.86 -0.11 0.8057

2011 1.44 1.54 -0.10 0.64 0.79 -0.15 0.8696

2010 1.88 1.46 0.42 0.72 0.74 -0.02 0.8279

2009 1.99 1.37 0.62 0.85 0.66 0.19 0.8486

Bottle of Wine (Chardonnay)

Year Price in

this State

Price in

N. Irl

Price

Difference

Total

Tax

State

Total

Tax NI

Tax

Difference

€/£

exchange

rate

2014 9.75 8.90 0.85 5.01 4.07 0.94 0.7911

2013 10.00 8.84 1.16 4.65 3.82 0.83 0.8516

2012 7.99 8.76 -0.77 3.46 3.82 -0.36 0.8057

2011 8.88 8.46 0.42 3.51 3.49 0.02 0.8696

2010 6.50 7.63 -1.13 3.09 3.18 -0.08 0.8279

2009 9.49 7.71 1.78 4.14 2.90 1.24 0.8486

TSG14/02

Smuggling/Counterfeit Products:

44. There have been 8 successful prosecutions for alcohol offences so far in 2014, relating

to offences of keeping for sale or delivery spirits and wine on which APT had not been

paid. This compares to 32 in 2010, 9 in 2011, 11 in 2012 and 7 in 2013. Of these

prosecutions, 6 related to counterfeit spirits in 2010, 2 in 2011, 6 in 2012 and 2 in 2013.

7 of the successful prosecutions this year involved counterfeit spirits. APT law in this

area was strengthened in the 2005 Finance Act to help combat this type of fraud. The

estimated retail value of alcohol seizures last year was €1,497,822 and for January to

30 June 2014 was €299,831.

Retail Price Movements

45. As noted, APT remained largely unchanged between 1994 and 2009, decreased in 2010,

and increased in 2013 and 2014. As APT is charged at a specific rate, the value of excise

duty rates on all products fell between 2003 and 2009 due to constant trade increases.

The reduction in APT in Budget 2010 led a sharp decrease in excise share of the price

of most products. However, since Budget 2013 the excise share of all products has risen,

with the excise share of products on the off-trade taking a higher share as a % of price

than 2003.

46. The tables below indicate the price of a nationally representative product in certain

alcohol product categories on the on-trade and off-trade as measured by the CSO in the

January of each calendar year mentioned, and the excise component of the price of

those products:

On-Trade Prices

Pint - Stout (4.2% ABV)

Year Excise Price Excise % of

Price

2003 €0.47 €3.38 14.0

2009 €0.47 €4.09 11.6

2010 €0.37 €3.96 9.5

2011 €0.37 €3.95 9.5

2012 €0.37 €4.00 9.4

2013 €0.46 €4.18 10.9

2014 €0.54 €4.30 12.5

Pint - Lager (4.3% ABV)

Year Excise Price Excise %

of Price

2003 €0.49 €3.76 12.9

2009 €0.49 €4.50 10.8

2010 €0.38 €4.35 8.8

2011 €0.38 €4.33 8.9

2012 €0.38 €4.35 8.8

2013 €0.47 €4.56 10.3

2014 €0.55 €4.67 11.8

TSG14/02

Whiskey (35.5ml) (40% ABV)

Year Excise Price Excise % of

Price

2003 €0.56 €3.23 17.2

2009 €0.56 €3.79 14.7

2010 €0.44 €3.69 12.0

2011 €0.44 €3.70 12.0

2012 €0.44 €3.75 11.8

2013 €0.52 €3.91 13.4

2014 €0.60 €4.03 15.0

Pint – Cider (4.5% ABV)

Year Excise Price Excise %

of Price

2003 €0.47 €3.80 12.4

2009 €0.47 €4.63 10.2

2010 €0.37 €4.47 8.4

2011 €0.37 €4.45 8.4

2012 €0.37 €4.48 8.3

2013 €0.46 €4.61 9.9

2014 €0.54 €4.74 11.3

Off-Trade Prices

Can - Lager (4.3%)

Year Excise Price Excise % of

Price

2003 €0.43 €1.77 24.18

2009 €0.43 €1.83 23.32

2010 €0.34 €1.77 19.13

2011 €0.34 €1.80 18.75

2012 €0.34 €1.78 18.96

2013 €0.41 €1.88 21.90

2014 €0.48 €1.98 24.46

Can - Cider (4.5% ABV)

Excise Price Excise % of

Price

2003 €0.42 €2.06 20.2

2009 €0.42 €2.25 18.5

2010 €0.33 €2.18 15.1

2011 €0.33 €2.16 15.3

2012 €0.33 €2.10 15.7

2013 €0.40 €2.22 18.1

2014 €0.47 €2.32 20.4

Bottle – Wine (12.5% ABV)

Year Excise Price Excise % of

Price

2003 €2.05 €9.07 22.6

2009 €2.46 €9.54 25.8

2010 €1.97 €9.07 21.7

2011 €1.97 €9.09 21.6

2012 €1.97 €8.94 22.0

2013 €2.78 €9.99 27.8

2014 €3.19 €10.52 30.3

Bottle - Whiskey (750ml)

Excise Price Excise % of

Price

2003 €10.99 €23.65 46.5

2009 €10.99 €25.26 43.5

2010 €8.72 €22.64 38.5

2011 €8.72 €22.05 39.5

2012 €8.72 €21.51 40.5

2013 €10.32 €23.63 43.7

2014 €11.92 €25.20 47.3

Public Health Policy

47. Ireland’s consumption of pure alcohol by litre per capita (of those aged 15 and older)

peaked in 2001, and has gradually fallen, while the composition of alcohol consumption

has changed. While per capita consumption of alcohol is the lowest since 1990,

increases in clearances of most alcohol products this year may lead to a slight upturn in

alcohol consumption per capita.

TSG14/02

Litres of alcohol per capita (aged 15 and older)

Wine Beer Spirits Cider Total

2000 1.86 8.01 3.02 1.13 14.0

2001 2.05 7.88 3.07 1.23 14.2

2002 2.26 7.68 3.16 1.06 14.2

2003 2.40 7.35 2.48 1.06 13.3

2004 2.69 7.15 2.50 1.06 13.4

2005 2.73 6.99 2.49 1.08 13.3

2006 2.85 6.77 2.54 1.08 13.3

2007 2.96 6.53 2.64 1.04 13.2

2008 2.81 6.07 2.40 0.91 12.2

2009 2.60 5.64 1.95 0.85 11.0

2010 3.04 5.59 2.17 0.83 11.6

2011 3.10 5.48 2.24 0.83 11.7

2012 3.05 5.36 2.30 0.80 11.5

2013 2.78 5.04 2.03 0.78 10.6

48. The Healthy Ireland Strategy, produced by Government in 2013, outlined an objective

of reducing alcohol consumption to below 9.2 litres of alcohol per capita. It noted that

alcohol is responsible for approximately 90 deaths every month in Ireland, which

include many alcohol-related cancers and heart diseases. On foot of the Report on a

National Substance Misuse Strategy, the Government announced in October 2013 that

it would introduce a Public Health (Alcohol) Bill to tackle alcohol misuse.

49. A number of changes to APT have been made since 2003 with a view to inducing

relative price changes to reduce alcohol consumption. In Budget 2003, excise duty on

spirit based alcopops was increased to the rate applying to other spirits. A lower rate of

excise duty has applied to beer exceeding 1.2% volume but not exceeding 2.8% volume

since Budget 2008. This was designed to encourage the substitution towards lower

ABV beers.

Minimum Unit Pricing

50. The Public Health (Alcohol) Bill will provide for a minimum price per gram of alcohol

in each alcohol product, which is designed to limit the sale of low-price alcohol, and

for restrictions to advertising.

51. A health impact assessment, in conjunction with Northern Ireland, was commissioned

in 2013, as part of the process of developing a legislative basis for minimum unit

pricing. The health impact assessment has been studying the impact of different

minimum prices on a range of areas such as health, crime and likely economic impact.

The study is currently in the process of being finalised. The Department of Finance and

the Department of Health are mindful that that any measure introduced in the State

should be in collaboration with a similar measure in Northern Ireland to avoid cross-

border implications.

TSG14/02

52. The Scottish Parliament legislated for minimum pricing in 2012, with an initial

minimum price of 50p per unit. However, the Alcohol (Minimum Pricing) (Scotland)

Act 2012 has yet to be commenced, as the decision has been appealed by the Scotch

Whisky Association. In April 2014, the Inner House of the Court of Session – the

supreme civil court in Scotland – sought a preliminary ruling from the Court of Justice

of the European Union on the compatibility of the Scottish measure with EU law. The

outcome of this preliminary ruling will be critical to the introduction of minimum unit

pricing.

Turnover-based licencing

53. There has been a general shift towards the off trade in recent years. Changing patterns

of alcohol consumption amongst the population and price discounting in supermarkets

have contributed, amongst other factors, to this trend. This movement is excise-neutral

but leads to a loss in VAT revenue due to lower off-licence prices. Industry data

indicates that around 60% of Beer is consumed from the on trade.

54. Excise duty on publicans’ licences are levied by reference to annual turnover, while

excise duty on off-licences is levied as a flat fee of €500 per alcohol products category

to a total of €1,500 for Beer, Wine and Spirits. The majority of on-licences are levied

at a rate of under €505 as detailed below:

Turnover Band Duty Number Issued % Total Duty

Under €190,500 €250 4,178 53.70% €1,040,500

€190,500 to €380,999 €505 1,843 23.69% €926,170

€381,000 to €634,999 €1,140 762 9.79% €864,625

€635,000 to €952,499 €1,775 447 5.75% €791,650

€952,500 to €1,269,999 €2,535 227 2.92% €562,952

€1,270,000 or more €3,805 323 4.15% €1,225,210

Total 7,780 100% €5,411,107

*As of 29/08/2014

55. The drinks trade have argued for a turnover-based licencing regime to be applied to the

off trade. It should be noted that the licence regime for pubs is based on the entire

turnover of the business including snacks, meals, tobacco and entertainment. There may

be difficulties associated with extending this to the off trade, given an application of

the current turnover-based regime to the off-trade would apply the same turnover

definition to a supermarket whose core business is groceries and household goods, as

to a public house. Notwithstanding, this proposal is being examined by officials from

the Department of Finance and Revenue Commissioners.

Possible Excise Increases

56. Drinks Industry Group of Ireland (DIGI), the National Off-Licence Association

(NOffla) and IBEC have requested a reversal of the APT increases imposed in Budget

2014 in their pre-Budget submissions. NOffla also seek a re-introduction of the

prohibition on below cost selling, which was removed following the abolition of the

Groceries Order in 2006.

TSG14/02

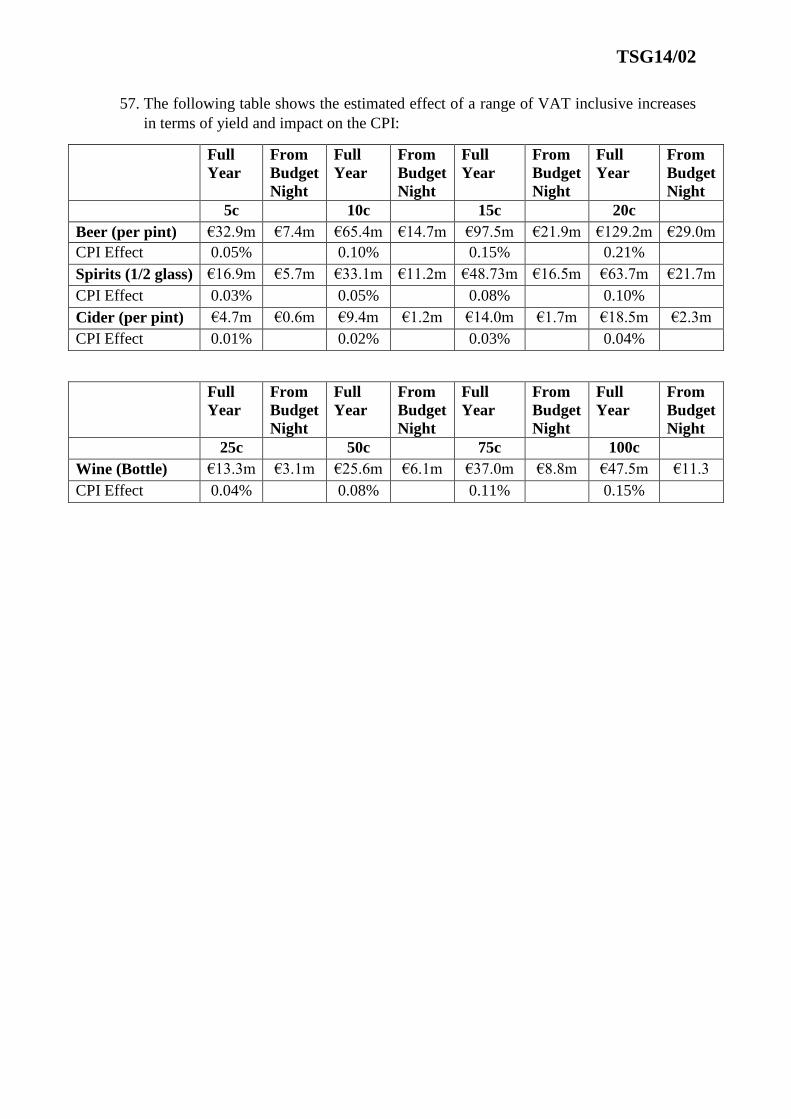

57. The following table shows the estimated effect of a range of VAT inclusive increases

in terms of yield and impact on the CPI:

Full

Year

From

Budget

Night

Full

Year

From

Budget

Night

Full

Year

From

Budget

Night

Full

Year

From

Budget

Night

5c 10c 15c 20c

Beer (per pint) €32.9m €7.4m €65.4m €14.7m €97.5m €21.9m €129.2m €29.0m

CPI Effect 0.05% 0.10% 0.15% 0.21%

Spirits (1/2 glass) €16.9m €5.7m €33.1m €11.2m €48.73m €16.5m €63.7m €21.7m

CPI Effect 0.03% 0.05% 0.08% 0.10%

Cider (per pint) €4.7m €0.6m €9.4m €1.2m €14.0m €1.7m €18.5m €2.3m

CPI Effect 0.01% 0.02% 0.03% 0.04%

Full

Year

From

Budget

Night

Full

Year

From

Budget

Night

Full

Year

From

Budget

Night

Full

Year

From

Budget

Night

25c 50c 75c 100c

Wine (Bottle) €13.3m €3.1m €25.6m €6.1m €37.0m €8.8m €47.5m €11.3

CPI Effect 0.04% 0.08% 0.11% 0.15%

TSG14/02

C: BETTING DUTY

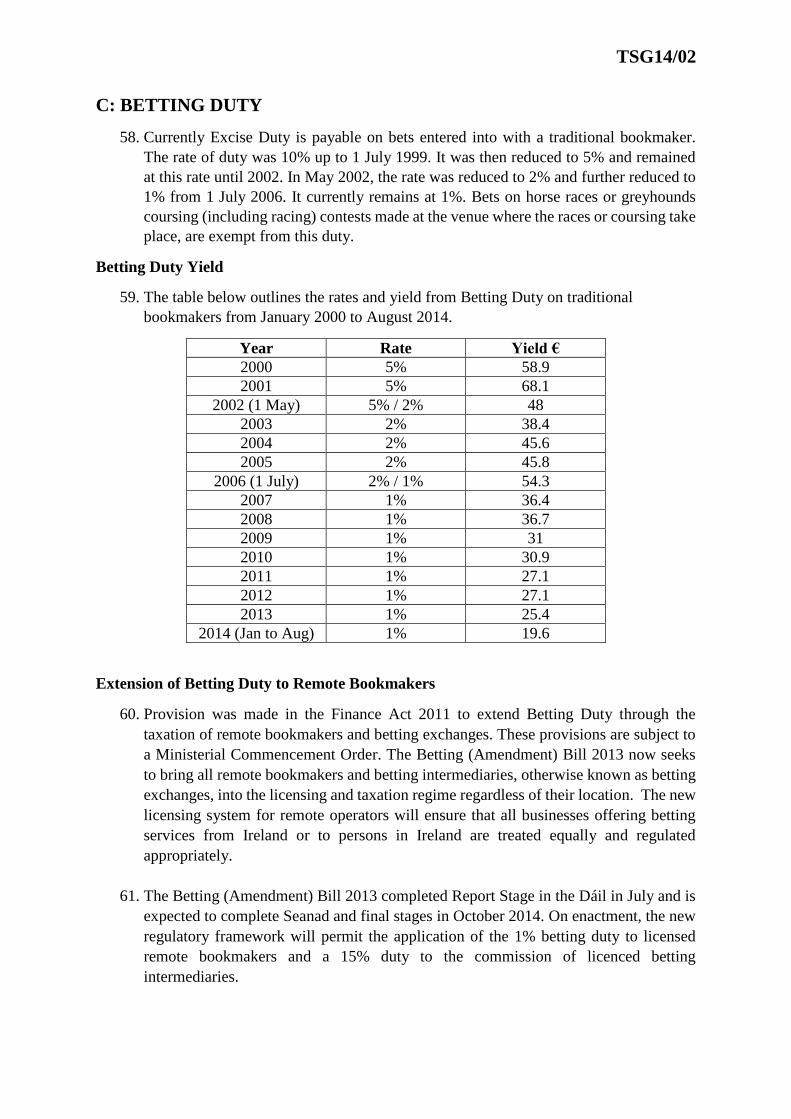

58. Currently Excise Duty is payable on bets entered into with a traditional bookmaker.

The rate of duty was 10% up to 1 July 1999. It was then reduced to 5% and remained

at this rate until 2002. In May 2002, the rate was reduced to 2% and further reduced to

1% from 1 July 2006. It currently remains at 1%. Bets on horse races or greyhounds

coursing (including racing) contests made at the venue where the races or coursing take

place, are exempt from this duty.

Betting Duty Yield

59. The table below outlines the rates and yield from Betting Duty on traditional

bookmakers from January 2000 to August 2014.

Year Rate Yield €

2000 5% 58.9

2001 5% 68.1

2002 (1 May) 5% / 2% 48

2003 2% 38.4

2004 2% 45.6

2005 2% 45.8

2006 (1 July) 2% / 1% 54.3

2007 1% 36.4

2008 1% 36.7

2009 1% 31

2010 1% 30.9

2011 1% 27.1

2012 1% 27.1

2013 1% 25.4

2014 (Jan to Aug) 1% 19.6

Extension of Betting Duty to Remote Bookmakers

60. Provision was made in the Finance Act 2011 to extend Betting Duty through the

taxation of remote bookmakers and betting exchanges. These provisions are subject to

a Ministerial Commencement Order. The Betting (Amendment) Bill 2013 now seeks

to bring all remote bookmakers and betting intermediaries, otherwise known as betting

exchanges, into the licensing and taxation regime regardless of their location. The new

licensing system for remote operators will ensure that all businesses offering betting

services from Ireland or to persons in Ireland are treated equally and regulated

appropriately.

61. The Betting (Amendment) Bill 2013 completed Report Stage in the Dáil in July and is

expected to complete Seanad and final stages in October 2014. On enactment, the new

regulatory framework will permit the application of the 1% betting duty to licensed

remote bookmakers and a 15% duty to the commission of licenced betting

intermediaries.

TSG14/02

Revenue Raising Options

62. The current relatively low rate of betting duty, at 1%, is a function of the changes that

have taken place in the bookmaking industry over the past number of years and in

particular the increase in activity in the remote or online sector. The explosion in the

use of mobile phones, laptops and other electronic communication devices has greatly

facilitated the migration of punters to the remote sector. Accordingly, until such time

as the playing field for the traditional and remote bookmaker has been levelled, in so

far as taxation is concerned, the rate had to be kept at low levels.

63. Once a regulatory and licencing regime for the remote sector is in place, all other

options around the level and type of tax involved in the betting industry can be

considered and reviewed.

64. In 2013, betting duty receipts from traditional bookmakers amounted to €25.4m. The

most up to date figure for the 8-month period to the end August 2014 is approximately

€19.6m. In addition, a working estimate of some €20m is anticipated from the

application of Betting Duty to the remote sector.

65. While it is considered prudent to wait until the new regime has bedded in before

considering changes to the rate, for illustrative purposes, revenue yield from modest

increases in the rate are examined below. These figures presume no other changes to

the structure or nature of the duty.

a) Increase Betting Duty Rate to 2% - It is estimated that an increase in the rate of

duty from 1% to 2% may yield an additional €35m per annum.

b) Increase Betting Duty Rate to 3% - It is estimated that an increase in the rate of

duty from 1% to 3% may yield an additional €70m approximately per annum.

It should be borne in mind that increases in Betting Duty may result in some customers

reducing their gambling expenditure and others diverting their expenditure to other

gambling products or to unlicensed operators.

Further Considerations – Introducing a Tax on Winnings

66. It is considered that any tax on winnings, however small, would be very difficult to

enforce in terms of internet and phone betting. Punters that bet via remote means are

highly price sensitive and a tax on winnings would incentivise tax avoidance. Policing

such a large group of people would be far more onerous than policing the betting firms.

67. All betting firms including betting exchanges share the above view and would prefer

that the tax liability remains with the firms. The fact that the companies would prefer

to bear the tax is a clear indication of how challenging it will be to enforce the tax.

TSG14/02

D: TAX ON SUGAR SWEETENED DRINKS

68. The Irish Heart Foundation (IHF) has sought, as part of its pre-Budget submission, the

introduction of a tax on sugar sweetened drinks (SSD) which increases the price of such

products by at least 20% to curb obesity amongst children and younger people. The IHF

believe that such a tax could raise between €58m and €71m per annum. This projection

is based on the household expenditures measured by the Household Budget Survey

carried out by the CSO.

69. ICTU have called for a tax on saturated fat, added sugar and added salt. However, this

approach may impose significant compliance cost on firms, particularly smaller firms.

For example, a tax on saturated fat would place significant compliance costs on

butchers and cheesemongers, who would have to price their products according to the

content of saturated fat. Denmark withdrew their ‘fat tax’ after a year in operation. An

excise-type tax on a specifically defined product is simpler to administer and places

less compliance burdens on businesses.

70. Ireland historically levied a form of excise duty on ‘table waters’, which included most

categories now considered sugar sweetened drinks. The tax operated between 1916 and

1992. It also became increasingly important in the context of an increasing Exchequer

shortfall in 1979/1980. The excise on table waters was levied at £0.10 a gallon from

1975 to 1979, but was sharply increased to £0.37 per gallon in Budget 1980. As the

Minister for Finance of the day put it, this was equivalent to putting 2.2p on a 33cl can

of Coca-Cola. This had the effect of raising the VAT-included price of a can of Coca-

Cola by over 10% in 1980. The table waters tax was abolished in November 1992 as

part of the reform of the tax code undertaken in anticipation of the full application of

Single Market rules on 1 January 1993.

71. France, Hungary and Finland all impose volumetric taxes on SSD. A volumetric tax is

imposed as a specific amount per litre of product, as opposed to an ad valorem rate

imposed on the final retail price of product. As such, it is easier to administer and

impose. France introduced its tax on SSD at a rate of €7.16 per hectolitre of SSD in

2012. After amendments by the National Assembly, the tax applied to all SSD, whether

diet or full sugar. The tax yielded €351m in 2013 and is expected to yield €373m in

2014. An analysis conducted by economists based in the Banque de France found that

after 6 months, the tax was fully shifted to soda prices while the pass-through to prices

of fruit drinks and flavoured waters was not complete.

72. The European Commission has not, thus far, indicated that it considers the French,

Hungarian or Finnish SSD duties contrary to the European Treaties. Given SSD are not

defined as a product under the general excise directive. This does not negate the need

to design an excise on SSD in such a way as to comply with the Treaties, in particularly

Article 110 of the TFEU and its associated case-law, which prohibits internal

discriminatory taxation which has the effect of imposing taxes on products from other

Member States in such a way as to provide indirect protection to similar domestic

products. Given the tax will fall on all SSD, it would be difficult to argue that such a

tax would be discriminating between similar products under Article 110 TFEU.

TSG14/02

Public Health Rationale

73. The Department of Health has been concerned about the impact of obesity on the cost

of health services for some time. The Report of the National Taskforce on Obesity

(2005) recommended an examination of the impact of fiscal measures on obesity. In,

2009 a Special Action Group on Obesity was established by the Department of Health

to work on an interdepartmental basis to review the 2009 report. In 2011 the Department

of Health sent a memo to Government on the idea of an SSD tax. In 2012, the

Department of Health commissioned a Health Impact Assessment (HIA) under the

aegis of the Institute of Public Health. The resulting HIA formed the basis of the

Department of Health’s SSD tax proposal before Budget 2013.

74. The HIA noted that there was a positive relationship between SSD consumption and

measures of weight gain. The National Adult Nutrition Survey conducted between 2008

and 2010 indicates that 53% of all adults are overweight, and 24.5% are obese. The

modelling in the HIA indicated that, assuming an own-price elasticity of 0.9 in relation

to SSD, a 10% increase in the price of SSD would lead to a 1.25% reduction in obesity

amongst adults.

Applying an SSD in Ireland

75. Given the difficulties in applying an SSD at an ad valorem rate it would not be prudent

to implement it in Ireland. A volumetric rate imposed at a specific amount per hectolitre

would be easier to impose and administer, and have a greater price impact on

multipacks, large volume SSD bottles and cheaper ‘own-brand’ SSD products. As such,

the SSD would function much like an excise, or indeed much as the old table waters

tax operated.

76. France has applied its SSD tax on SSD to CN code 2009, encompassing fruit juices,

and CN code 2202 which is categorised as ‘waters, including mineral waters and

aerated waters, containing added sugar or other sweetening matter or flavoured, and

other non-alcoholic beverages’ under Council Regulation 2658/87/EEC . CN codes are

used by customs and tax authorities to identify products, and manufactures, processors

and importers must declare which CN code their products fall under. Excise duty is

collected at the earliest point of distribution; in this case this suggests that one of

manufacturers, processors or importers of SSD would be liable for a SSD tax. While

there are a number of sophisticated suppliers within the market, such as large soft-drink

producers, with the capacity to comply with an SSD tax, there are also a number of

producers operating at a ‘cottage industry’ level, who may find it difficult and costly to

comply with an SSD.

77. It is generally accepted that, in order have a non-trivial effect on consumption and

thereby impact on obesity levels and health related issues, the price shift induced by the

level of taxation should be high, typically over 10%.

TSG14/02

Issues of Concern

78. As with any consumption tax, it is difficult to predict with certainty the effect a tax on

sugar-sweetened drinks will have on the behaviour of individuals. While a number of

countries have recently introduced a tax which targets similar products, it is too early

to affirm whether these countries are now experiencing a positive effect on obesity

levels as a direct result of the tax.

79. The measure outlined above is not exactly that intended by the IHF. Notably, it does

not differentiate between sugar-sweetened and artificially-sweetened drinks. It involves

fruit juices. There is no incentive in the measure to move towards the sugar free soft

drink offerings on the market.

80. It is also necessary to consider the impact of such a measure on small businesses such

as retailers and domestic soft drinks producers. A reduction in the consumption of soft

drinks would obviously have an impact in this area. It may also act as a disincentive

for large soft drink multinationals to locate in the State.

81. The State should guard against introducing a tax that cannot be fully collected or that

costs more to collect than it raises. While it is presumed that the Revenue

Commissioners would be the collection agent if such a duty was introduced there are

risks associated with introducing a tax on sugar-sweetened drinks as an excise when

the products themselves are not currently treated like our other excisable products. For

example, the system for controlling the movement of alcohol and tobacco products is

subject to tight supervision, and both alcohol and tobacco products are kept in

warehouses and factories specifically constructed for the storage of tobacco and alcohol

products, facilitating the control and subsequent taxation of those products. No such

system currently exists for the movement of soft drinks.

82. It is evident, therefore, that any consideration of a new tax on sugar-sweetened drinks

would require adequate deliberation to assess the practical and administrative cost

implications for both business and Revenue.

Impact on Retail Prices of Various Rates

83. The tables below indicate the effects of a number of rates on the retail prices of existing

products. Projected effects of rates of €7.16 per hectolitre, €14.32 per hectolitre, €25.54

per hectolitre on representative products are displayed below.

TSG14/02

€7.16 per hectolitre

Pre-Tax Price Post-Tax Price % Increase

Can Premium Cola (33cl) €1.00 €1.03 3%

Bottle of Premium Cola (500ml) €1.29 €1.33 3%

Bottle of Premium Cola (1500ml) €2.29 €2.42 6%

Energy Drink (380ml) €1.89 €1.92 2%

8pack of Premium Cola (2640ml) €5.99 €6.21 4%

18pack of Premium Cola (5940ml) €11.29 €11.79 4%

Own Brand Cola (2000ml) €0.55 €0.72 31%

On trade Premium Cola (200ml) €2.00 €2.02 1%

€14.32 per hectolitre

Pre-Tax Price Post-Tax Price % Increase

Can Premium Cola (33cl) €1.00 €1.06 6%

Bottle of Premium Cola (500ml) €1.29 €1.37 7%

Bottle of Premium Cola (1500ml) €2.29 €2.54 11%

Energy Drink (380ml) €1.89 €1.95 3%

8pack of Premium Cola (2640ml) €5.99 €6.44 7%

18pack of Premium Cola (5940ml) €11.29 €12.30 9%

Own Brand Cola (2000ml) €0.55 €0.89 62%

On trade Premium Cola (200ml) €2.00 €2.03 2%

€25.54 per hectolitre

Pre-Tax Price Post-Tax Price % Increase

Can Premium Cola (33cl) €1.00 €1.10 10%

Bottle of Premium Cola (500ml) €1.29 €1.44 12%

Bottle of Premium Cola (1500ml) €2.29 €2.74 20%

Energy Drink (380ml) €1.89 €2.01 6%

8pack of Premium Cola (2640ml) €5.99 €6.79 13%

18pack of Premium Cola (5940ml) €11.29 €12.30 16%

Own Brand Cola (2000ml) €0.55 €1.16 110%

On trade Premium Cola (200ml) €2.00 €2.06 3%

Revenue Raising Measures

84. Consumption information per litre of product is based on industry estimates, which

necessarily comes with caveats.

Yield at €7.16 per hl Yield at €14.36 per hl Yield at €25.54 per hl

€37.6m €75.2m €134.2

*Assumes no behavioural changes

TSG14/02

ANNEX 1

Specific, Ad Valorem and Minimum Excise Duty Rates per 1,000 Cigarettes in the EU

Member State WAP/

1000

Specific

Excise /

1000

Specific

Excise as

a % of

Total Tax

(including

VAT)

Ad

valorem

as a % of

WAP

Minimum

Excise as

a % of

WAP

Total

excise

duty***

Total

tax as

% of

WAP

Ireland €454.50 €241.83 65.99% 8.72% 60.64% €281.46 80.6%

UK** €443.05 €232.71 61.30% 16.50% 69.02% €305.81 85.7%

France €325.00 €48.75 18.43% 49.70% 64.70% €210.27 81.4%

Netherlands €291.91 €173.97 76.50% 0.95% 60.55% €176.75 77.9%

Sweden €286.96 €163.33 73.05% 1.00% 57.92% €166.20 77.9%

Denmark €271.88 €158.55 73.52% 1.00% 59.32% €161.27 79.3%

Germany €254.50 €96.30 50.09% 21.74% 59.58% €152.00 75.6%

Finland €250.41 €28.00 13.55% 52.00% 63.18% €161.50 82.5%

Belgium €244.11 €23.59 12.48% 50.41% 60.07% €148.11 77.4%

Italy €229.00 €13.10 7.50% 52.41% 58.13% €144.65 76.2%

Spain €215.00 €24.10 14.09% 51.00% 62.21% €133.75 79.2%

Austria €208.80 €40.00 24.93% 41.00% 60.16% €125.61 76.8%

Luxembourg €208.51 €17.75 12.21% 48.14% 57.00% €118.12 69.7%

Cyprus €204.00 €55.00 35.04% 34.00% 60.96% €124.36 76.9%

Malta €203.43 €82.50 50.19% 25.00% 66.36% €135.00 80.8%

Portugal €194.88 €87.33 55.73% 17.00% 64.39% €125.50 80.5%

Greece €175.15 €82.50 54.90% 20.00% 67.10% €117.53 85.8%

Hungary €170.60 €42.22 36.38% 31.00% 55.75% €95.11 77.0%

Slovenia €165.50 €67.92 50.00% 23.01% 64.04% €106.00 82.1%

Slovakia €150.11 €59.50 49.98% 23.00% 62.64% €94.03 79.3%

Czech Rep. €143.76 €46.40 42.12% 27.00% 59.28% €87.73 76.6%

Estonia €141.00 €46.50 39.43% 34.00% 66.98% €94.44 83.7%

Romania €140.54 €60.40 52.84% 19.00% 61.98% €81.78 81.3%

Poland €140.04 €48.87 41.05% 31.41% 66.31% €92.86 85.0%

Croatia €134.99 €27.57 26.38% 37.00% 57.43% €78.59 77.4%

Latvia €129.88 €51.80 48.50% 25.00% 64.88% €85.60 82.2%

Lithuania €123.38 €45.47 46.53% 25.00% 61.85% €76.31 79.2%

Bulgaria €118.88 €51.64 52.27% 23.00% 66.44% €78.98 83.1%

*The information contained in this table is based on information provided by each EU Member

State to the European Commission and published in the ‘EU Excise Duty Tables, Ref 1041,

July 2014’. There may be some variations within the figures provided due to rounding or

particular national means of calculating excise duty not evident from these tables.

**EUR/GBP exchange rate 0.7911 of 30 July 2014.

*** MS highlighted in bold have minimum excise duty which is equal to or higher than the

standard rates of excise duty based on WAP.

TSG14/02

ANNEX 2

Cross-Border Price Comparisons - July 2014

Products Price in

this State

(€)

Price in

N. Irl

(€)

Difference Total Tax

in this

State

Total Tax

N. Irl

Difference

Total Tax

Alcohols

Stout (500ml can) 2.25 2.09 0.16 0.89 0.85 0.05

Lager (500ml can) 2.05 1.69 0.36 0.87 0.85 0.02

Lager (330ml bottle) 1.68 1.26 0.42 0.63 0.55 0.09

Bottle of Vodka 22.5 16.84 5.66 15.38 12.17 3.21

Bottle of Whiskey 26.07 25.41 0.66 16.79 14.22 2.57

Bottle of Wine

(Chardonnay)

9.75 8.9 0.85 5.01 4.07 0.94

Bottle of Wine (Sauv.

Blanc)

8.75 8.42 0.33 4.82 3.99 0.83

Sparkling Wine 17.37 14.21 3.16 9.62 5.69 3.93

Tobacco

Cigarettes *(20) 9.6 11.14 -1.54 7.47 8.35 -0.88

Cigarettes *(20) 9.6 11.11 -1.51 7.47 8.34 -0.87

Roll your own Tobacco

(25g)

10.55 11.68 -1.13 8.28 7.65 0.63

*Two different brands

**EUR/GBP exchange rate used on the survey date was 0.7911 sterling

TSG14/02

ANNEX 3

Excise Duty on Alcoholic Beverages in the EU-28 as of 1st July 2014

Beer

€ per hectolitre of

product

Wine (Still)

€ per hectolitre of

product

Wine (Sparkling)

€ per hectolitre of

product

Spirits

€ per hectolitre of

product

1 Finland €32.05 Ireland €424.84 Ireland €849.68 Sweden €5,866.16

2 UK €24.19 Finland €339.00 UK €432.14 Finland €4,555.00

3 Ireland €22.55 UK €337.39 Finland €339.00 Ireland €4,257.00

4 Sweden €20.62 Sweden €267.47 Sweden €267.47 UK €3,569.67

5 Slovenia €12.10 Denmark €147.68 Netherlands €254.41 Greece €2,450.00

6 Denmark €7.51 Netherlands €88.36 Belgium €194.94 Belgium €2,118.96

7 France €7.33 Estonia €84.67 Denmark €190.20 Denmark €2,011.69

8 Italy €6.75 Lithuania €65.16 Germany €136.00 France €1,718.61

9 Greece €6.50 Latvia €64.03 Austria €100.00 Netherlands €1,686.00

10 Netherlands €6.48 Belgium €56.97 Czech Rep. €91.24 Estonia €1,643.00

11 Estonia €6.28 Poland €37.35 Estonia €84.67 Malta €1,350.00

12 Cyprus €6.00 France €3.72 Slovakia €79.65 Poland €1,348.21

13 Hungary €5.47 Hungary €0.00 Lithuania €65.16 Latvia €1,337.50

14 Croatia €5.25 Austria €0.00 Latvia €64.03 Slovenia €1,320.00

15 Austria €5.00 Germany €0.00 Hungary €55.59 Germany €1,303.00

16 Belgium €4.62 Greece €0.00 Poland €37.35 Lithuania €1,291.71

17 Poland €4.60 Spain €0.00 Romania €36.26 Portugal €1,251.72

18 Malta €4.33 Italy €0.00 France €9.23 Austria €1,200.00

19 Slovakia €3.59 Luxembourg €0.00 Greece €0.00 Hungary €1,126.03

20 Portugal €3.42 Portugal €0.00 Spain €0.00 Czech Rep. €1,111.24

21 Czech Rep. €3.12 Cyprus €0.00 Italy €0.00 Slovakia €1,080.00

22 Latvia €3.10 Slovenia €0.00 Luxembourg €0.00 Romania €1,065.08

23 Lithuania €2.71 Slovakia €0.00 Portugal €0.00 Luxembourg €1,041.15

24 Spain €2.26 Bulgaria €0.00 Cyprus €0.00 Cyprus €956.82

25 Romania €2.19 Czech Rep. €0.00 Bulgaria €0.00 Italy €942.49

26 Luxembourg €1.98 Romania €0.00 Slovenia €0.00 Spain €913.28

27 Germany €1.97 Malta €0.00 Malta €0.00 Croatia €695.92

28 Bulgaria €1.92 Croatia €0.00 Croatia €0.00 Bulgaria €562.43

EU Average €7.64 EU Average €68.45 EU Average €117.39 EU Average €1,777.60

EU Minima €1.87 EU Minima €0.00 EU Minima €0.00 EU Minima €550.00

* EUR/GBP rate £0.79055 as of 28 July 2014.

*Some Member States charge excise duty on beer per hectolitre per degree Plato of finished

product. The conversion rate is 0.4 (minimum rate per degree Plato divided by minimum rate

per degree alcohol – (0.748/1.87)). For Member States who use rate bands the conversion rate

is 4.4 (0.4 multiplied by 11 degrees Plato).

Related Documents