TRENDS IN MIGRATION AND REMITTANCES OCTOBER 2016 WORLD BANK GROUP ON THE GLOBAL MIGRATION AGENDA Four areas that the World Bank Group and International financial Institutions can contribute to: Financing migration programs Addressing fundamental drivers of migration Maximizing the benefits and managing the risks of migration in sending and receiving countries Providing knowledge for informed policy making and improving public perceptions 1 2 3 4 ($ billion) 800 700 600 500 400 300 200 100 0 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016f 2018f REMITTANCE FLOWS ARE MORE THAN THREE TIMES LARGER THAN OFFICIAL DEVELOPMENT ASSISTANCE (ODA) FDI Remittances Pvt debt & port. equity ODA Sources: World Development Indicators and World Bank Development Prospects Group • Weak growth in remittance sending countries • Low oil price and labor market ‘nationalization’ in Gulf Cooperation Council countries • Exchange rates controls and de-risking Remittance Growth Rate, 2016 What are the reasons for slow growth? 2.1% –4.0% 6.3% 1.5% –2.3% –0.5% REMITTANCES TO DEVELOPING COUNTRIES TO GROW AT WEAK PACE IN 2016 Remittances to low and middle income countries are expected to increase only slightly by 0.8 percent to $442 billion in 2016. Source: World Bank Data

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

TRENDS IN MIGRATION AND REMITTANCESOCTOBER 2016

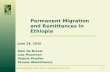

WORLD BANK GROUP ON THE GLOBAL MIGRATION AGENDAFour areas that the World Bank Group and International financial Institutions can contribute to:

Financing migration programs

Addressing fundamental drivers

of migration

Maximizing the benefits and

managing the risks of migration in sending

and receiving countries

Providing knowledge for informed policy

making and improving public perceptions

1 2 3 4

($ billion)800

700

600

500

400

300

200

100

0

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

f

2018

fREMITTANCE FLOWS ARE MORE THAN THREE TIMES LARGER THAN OFFICIAL DEVELOPMENT ASSISTANCE (ODA)

FDI

Remittances

Pvt debt & port. equity

ODA

Sources: World Development Indicators and World Bank Development Prospects Group

• Weak growth in remittance sending countries

• Low oil price and labor market ‘nationalization’ in Gulf Cooperation Council countries

• Exchange rates controls and de-risking

Remittance Growth Rate, 2016

What are the reasons for slow growth?

2.1%

–4.0%

6.3%

1.5%

–2.3%–0.5%

REMITTANCES TO DEVELOPING COUNTRIES TO GROW AT WEAK PACE IN 2016Remittances to low and middle income countries are expected to increase only slightly by 0.8 percent to $442 billion in 2016.

Source: World Bank Data

Related Documents