IFD377 May 1999 1(1 DISCUSSION PAPER Trends in Private Investimentin Developing ountries Statistics for 1970-97 (This issue includes the resultsof a worldwide survey of obstacles to dioing business as perceived by executives in 74 countries) Guy P.Pfeffermann Gregory V. Kisunko Mariusz A.Sumlinski INTERNATIONAL FINANCE CORPORATION Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

IFD377May 1999 1(1

DISCUSSION PAPER

Trends in PrivateInvestiment in Developing

ountriesStatistics for 1970-97

(This issue includes the results of a worldwide survey of obstaclesto dioing business as perceived by executives in 74 countries)

Guy P. PfeffermannGregory V. Kisunko

Mariusz A. Sumlinski

INTERNATIONALFINANCE

CORPORATION

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

IFC Discussion Papers

No. 1 Private Business in Deceloping Countries: ImprovedProspects. Guy P. Pfeffermann

No. 2 Debt-Eqzaiy Sraps and Foreign Direct lnvestment in ,LauinAmenca Joel Bergsmanand Wayne Edisis

No. 3 ProspectsfortheBuinessSeetorinDeveopingCounties. Economics Department, IFC

No. 4 Strengthening Heath Servvesin Defeloping Countries through the Private SItor.Charles C. Griffin

No. 5 TheDevelopmentConribution of IFCOperaions. Economics Department, IFC

No. 6 TrendstnPPrxwteJnu%smentin Thiy DevffelopingCountri. Guy P. Pfeffermannand Andrea Madarassy

No. 7 Automotive Industry Trends and Prospctsfor Investment in Developing Countries.Yannis Karmokolias

No. 8 Exportingto Industrial Counties. ProspectsforB isies in Developing Countries.Economics Department, IFC

No.9 AfricanEntrepre s--PoneersofDer,lopment. Keith Marsden

No. 10 Privatizing Teonunm ansSysteyu: Buans Opp ortunities in DevelopingCountries.William W. Ambrose, Paul R. Hennemeyer, and Jean-Paul Chapon

No. 11 Trends in Private Investment in Developing Countries, 1990-91 Edition. Guy P. Pfeffermannand Andrea Madarassy

No. 12 FinangingCorporateGrowYthintheDewelopingWorld Economics Department, IFC

No.13 VentureCapiLessonsfromtheDevelopedWorldfortheDevelopingMarkets. Silvia B. Sagariwith Gabriela Guidotti

No. 14 Trends in Priate Investment in Developing Countries, 1992 edition. Guy P. Pfeffermannand Andrea Madarassy

No. 15 Private Sector Elermi&y in Developing Countries: Supply andDemnd Jack D. Glen

No. 16 Trends in Priwae Invetment in Developing Countries 1993: Statisticsfor 1970-91.Guy P. Pfeffermann and Andrea Madarassy

No. 17 How FirmsinDevelopingCoumtries,ManageRisk. Jack D. Glen

No. 18 Coping smit/ Capitalism: TheNew Polish Entrepreneurs. Bohdan Wyznikiewicz, Brian Pinto,and Maciej Grabowski

No. 19 IntelltProperty Protectin, Foreign Direct Inestment, and Technology Transfer.Edwin Mansfield

No. 20 Trends in Private Investmentin Developing Countries 1994: Statisticsfor 1970-92. Robert Millerand Mariusz Sumlinski

(Continued on the inside back covr)

INTERNATIONALFINANCE

____._L__ CORPORATION

DISCUSSION PAPER NUMBER 37

Trends in Privateinvestment in Developing

ountriesStatistics for 1970-97

Guy P. PfeffermannGregory V. Kisunko

Mariusz A. Sumlinski

The World BankWashington, D.C.

Copyright © 1999The World Bank and

International Finance Corporation1818 H Street, N.W.Washington, D.C. 20433, U.S.A.

All rights reservedManufactured in the United States of AmericaFirst printing May 1999

The Intemational Finance Corporation (IFC), an affiliate to the World Bank, promotes the economicdevelopment of its member countries through investment in the private sector. It is the world's largest multilateralorganization providing financial assistance directly in the form of loan and equity to private enterprises indeveloping countries.

To present the results of research with the least possible delay, the typescript of this paper has not been preparedin accordance with the procedures appropriate to formal printed texts, and the IFC and the World Bank accept noresponsibility for errors. The findings, interpretations, and conclusions expressed in this paper are entirely those ofthe author(s) and should not be attributed in any manner to the IFC or the World Bank or to members of theirBoard of Executive Directors or the countries they represent. The World Bank does not guarantee the accuracy ofthe data included in this publication and accepts no responsibility for any consequence of their use. Some sourcescited in this paper may be informal documents that are not readily available.

The material in this publication is copyrighted. The World Bank encourages dissemination of its work and willnormally grant permission promptly.

Permission to photocopy items for internal or personal use, for the internal or personal use of specific clients, orfor educational classroom use is granted by the World Bank, provided that the appropriate fee is paid directly toCopyright Clearance Center, Inc., 222 Rosewood Drive, Danvers, MA 01923, U.S.A., telephone 978-750-8400, fax978-750-4470. Please contact the Copyright Clearance Center before photocopying items.

For permission to reprint individual articles or chapters, please fax your request with complete information tothe Republication Department, Copyright Clearance Center, fax 978-750-4470.

All other queries on rights and licenses should be addressed to the World Bank at the address above or faxed to202-522-2422.

ISSN (IFC Discussion Papers): 1012-8069ISSN (Trends in Private Investment in Developing Countries): 1018-208XISBN 0-8213-4475-7

Guy P. Pfeffermann is director, Economnics Department, IFC, and economic adviser to the Corporation. Gregory V.Kisunko is country officer in the World Bank's Europe and Central Asia Regional Office. Mariusz A. Sumlinski is aresearch analyst in the Economics Department, IFC.

The first edition of this serial publication was cataloged by the Library of Congress as follows:

Library of Congress Cataloging-in-Publication Data

Pfeffermann, Guy Pierre.Trends in private investment in thirty developing countries / Guy

Pfeffermann, Andrea Madarassy.p. cm. - (Discussion paper / International Finance

Corporation; no. 6)Includes bibliographical references.ISBN 0-8213-1352-51. Investments-Developing countries. II. Madarassy, Andrea,1964- . II. Title. III. Series: Discussion paper (InternationalFinance Corporation) ; no. 6.HG5993.P48 1989332.6'7314'091724-dc2O 89-22588

CIP

Contents

Foreword ..... v

Abstract ... ; vii

Chapter I - Private and Public Investment Trends ......................................................... 1

Chapter II - Perceived Obstacles to Doing Business: Worldwide Survey Results .............5

The survey ..................................................... 5

Number of obstacles .................................................... 6

The nature of obstacles .................................................... 12

Country-specific responses ........................................................ 13

The dog that didn't bark ........................................................ 15

Obstacles and levels of private investment-econometric results .......................... 20

Appendix 1 - Methods and Sources ........................................................ 25

Appendix 2 - Statistics ........................................................ 27

Sub-Saharan Africa ........................................................ 29

Latin America and the Caribbean ........................................................ 33

Middle East and North Africa ........................................................ 37

Transition Countries ........................................................ 39

East Asia ........................................................ 41

South Asia ........................................................ 45

Table - Investment as a share of GDP ........................................................ 47

iii

Foreword

This is the tenth annual edition of "Trends in Private Investment in DevelopingCountries". In order to mark the anniversary, the discussion paper includes figures foreach of the countries for which data are available as well as the first country-specificresults of a worldwide survey of obstacles to doing business perceived by executives in74 countries (including several industrial countries for comparison). The rationale for thispublication is that standard UN national accounts do not break investment down betweenpublic and private; rather, they distinguish between central government and all otherinvestment, and the latter includes investments by state-owned enterprises. The IFCdiscussion papers pull together information provided by national organizations, WorldBank, and IMF economists in order to estimate levels of private investment.

Guy PfeffermannDirector, Economics Department

& Economic Adviser of the Corporation

v

Abstract

The first part of the discussion paper documents trends in private and public fixedinvestment. On average for the 47 countries covered (including, for the first time in thisseries, China), 1997 was a record year for private investment, which rose from a low of11.2 percent of GDP in 1985 to 14.3 percent in 1997, the last year for which data exist.Public investment declined to 7.2 percent of GDP, its lowest level since 1975. The largest1997 increases in private investment were in two transition countries where levels remainlow (Bulgaria and Romania) followed by Panama, CMte d'Ivoire, Bolivia, Argentina andChina. Ratios of private investment to GDP were highest in Papua New Guinea,Malaysia, the Republic of Korea, Thailand, and Indonesia, before the full effects of theAsian crisis were felt.

The second part presents country-specific results of a 1996/97 worldwide surveyof business executives. The discussion focuses on obstacles to doing business in each ofthe 74 countries covered (including industrial economies) and their relationship to levelsof private investment. A few factors emerge as being of particular importance to privateinvestment decisions: the real exchange rate, the rule of law, predictability of judiciarysystems, and the extent to which financing is available to enterprises.

vii

Chapter IPrivate and Public Investment Trends

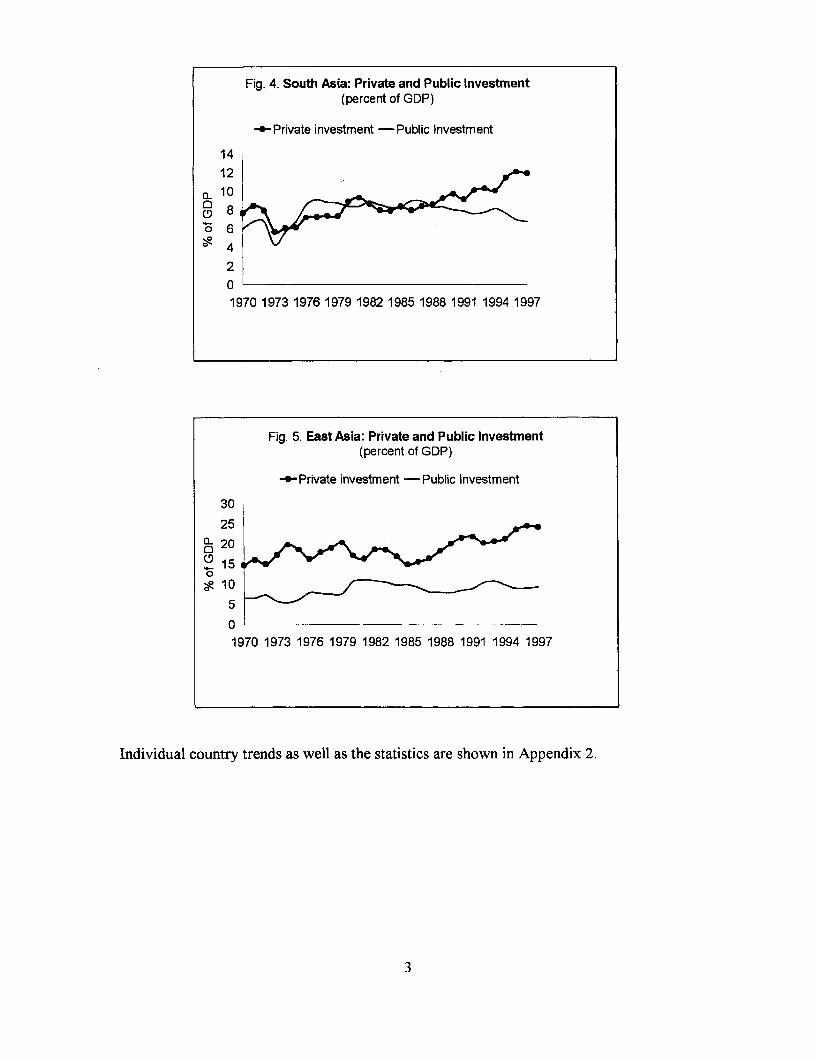

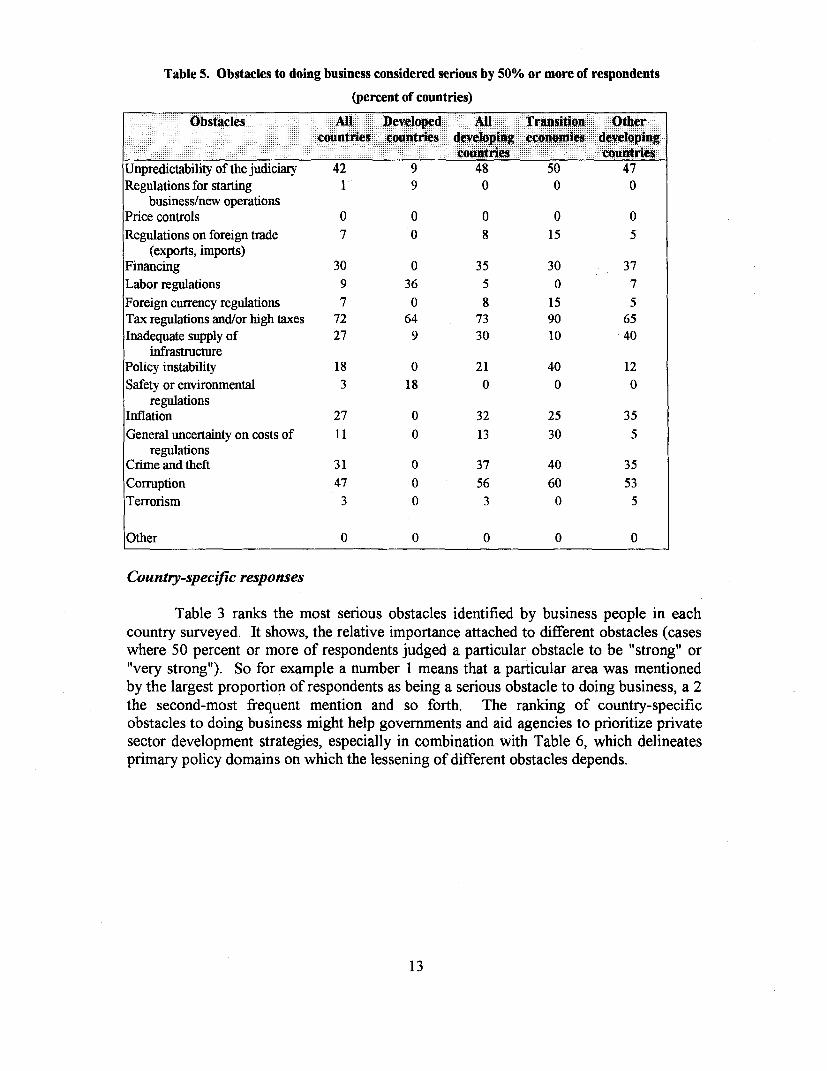

In 1997, the latest year for which the data exist, private investment continued torise and public investment to decline on average in line with recent trends in the 47countries covered this year (see Figure 1). The data do not reflect the worsened economicconditions of many developing countries in the wake of the Asian crisis. "Investment"refers to gross domestic fixed capital and encompasses national as well as foreign directinvestment.

Fig. 1. Trends in Private and Public Investment(prcent of GDP)

-Pivate investment -Public investnent

1614121010

4201970 1973 1976 1979 1982 1985 1988 1991 1994 1997

Overall trends of the past few years mirror those in the four major regions shownin Figures 2 to 5. In all cases except most recently in East Asia trends in private andpublic investment clearly diverge. The drop in public investment is particularlypronounced in Africa.

1

Fig. 2. Latin America: Private and Public Investment(percent of GDP)

-0-Private investment -Public Investment

1614

12

1970 1973 1976 1979 1982 1985 1988 1991 1994 1997

Fig. 3. Sub-Saharan Africa: Private and Public Investrnent(percent of GOP)

-0Private investment -Public Investment

16

0 46

14

2

01970 1973 1976 1979 1982 1985 1988 1991 1994 1997

2

Fig. 4. South Asia: Private and Public Investment(percent of GDP)

-Private investment -Public Investment

14

121 10

06

201970 1973 1976 1979 1982 1985 1988 1991 1994 1997

Fig. 5. East Asia: Private and Public Investment(percent of GDP)

---Private investment -Public Investment

30

25

EL20

0~10

5

01970 1973 1976 1979 1982 1985 1988 1991 1994 1997

Individual country trends as well as the statistics are shown in Appendix 2.

3

The following table shows 1997 private investment ratios in descending order.

T-b- et. 1iJ$va%e Investment in 199 Unt of; GDP

Papua New Guinea 31.5 Belize 12.8Maaysia 30.9 South Africa 12.7Korea Rep. of* 27.1 Tunisia 12.4Thailalnd000 0 j30 :00 ::24j1 El Salvador 12.1Indonesia 22.1 Egypt 12.1tPanama 0 di :0:t0E ::t22.0 Kenya 11.3Peru 21.0 Cote d'Ivoire 11.2Philippines 2.9 Guatmal 11.1Dominican Republic 20.5 Benin 11.0Turkey000 0 0 0000 0 0 ji 4 ;;j0i$00020.5 0Morocco 11.Chile 20.4 Bangladesh 10.8Maur 4000 0 0004 0 000000titius :000 0 00020.0 P:land 10.3Nicaragua 19.8 Bolivia 10.3Argentina 18.4 Colombia 10.0India 16.1 Guinea-Bissau 9.2Mexico00 000 M16.0 Pakistan 8 9China 15.8 Mauritania 8.6Brazil : 15.8 i Uru i I:guay .8.6Paraguay 15.4 Venezuela 7.4Costa Rica00000000 t :: 0 15.0m Romani a R6.2Iran 13.8 Madagascar 5.5Ecuador00 ttttt 0 000 j0;13.31 Malawi 5.1Namibia 12.9 Bulgaria 4 8* 1996

Table 2 shows changes in ratios of private investment to GDP between 1990 and 1997.

Table I Chaae aiwPrivate luvestnient Ras )ent)

Bulgaria 443 Chile 11Romania 344 Philippines 11Panama 196 Guinea-Bissau 9C6te dIvoire....h i i 1128 El Salvadorf 9Bolivia 108 Guatemala 8Argentina :i: 95 Ecuadori 8China 92 Kenya 3Benm.j 1 lX|j;jl0)|i;00 lt ;l; 8-ti000lS3000 : ::Naminbia 2Nicaragua 77 Mauritius IPeru 72 Tunisia IBangladesh 68 Pakistan 0fakii04g:t0Si tggl66 South Africa -.2Papua New Guinea 57 Colombia -2Venezuela ; ;;j;000;00000 0 tttt 0 50 Mauitaia-7Malaysia 48 Korea Rep. of -9Turkey 31 Brazil -10Poland 21 Paraguay -15Mexicotit t4000000000 ti it0 :i017|;:; 0 ti ;00 Costa Rica -15India 16 Madagascar -21Indonesia i M Morocco -25Dominican Republic 12 Egypt -28l3elize:;000000 i3fi i$iiiX;T: >12 Thailand -30Uruguay 12 Malawi -56

4

Chapter IIPerceived Obstacles to Doing Business: Worldwide Survey Results

The survey

Why is investment, especially private investment, so low in some developingcountries and so high in others? Levels of investment and how efficiently it is being usedare affected by many factors, most of which can be grouped into (a) macroeconomicpolicies; (b) microeconomic incentives; and (c) institutional factors.

An earlier IFC Discussion Paper' as well as other publications2 draw on the viewsexpressed by CEOs or managers of businesses in groups of developing and, for purposesof benchmarking, mature industrialized economies. The present paper uses the samedata, which were collected under the aegis of the World Bank's 1997 World DevelopmentReport3 as well as additional ones gathered by researchers at the University of Basel (forBrazil, Hong Kong, China, Korea, Singapore, and Thailand).

The survey covers 3,951 firms in 74 countries, mostly in manufacturing andservices (about half each) plus some agricultural firms.4 The survey covers large andsmall firms with and without foreign participation. Interviews were conducted in thecountries where firms operate.

This paper addresses the question: which obstacles to doing business areconsidered to be most serious by private sector managers in particular countries?The answer might help to identify policy domains (macroeconomic, institutional)most relevant in each country and levels of national authority (central, local) mostappropriate to reduce obstacles to doing business.

Managers were asked to judge on a six points scale how problematic variousobstacles are for doing business. The six points range from "no obstacle" and "moderateobstacles," to "strong" and "very strong" obstacles.5 The areas listed are:

* Regulations for starting business/new operations

How Businesses See Government: Responses from Private Sector Surveys in 69 Countries. AymoBrunetti, Gregory Kisunko, and Beatrice Weder, IFC Discussion Paper No. 33, 1998.

2 Institutions in transition: reliability of rules and economic performance in former socialist countries.Aymo Brunetti, Gregory Kisunko, Beatrice Weder, Policy Research Working Paper No. 1809, 1997;Credibility of rules and economic growth: evidence from a worldwide survey of the private sector.Aymo Brunetti, Gregory Kisunko, Beatrice Weder, Policy Research Working Paper No. 1760, 1997;Institutional obstacles to doing business: Region-by-region results from a worldwide survey of theprivate sector. Aymo Brunetti, Gregory Kisunko and Beatrice Weder, Policy Research Working Paper,No. 1759, 1997.

3 The State in a Changing World, Oxford University Press, 1997.

4 The average number of respondents per country is 54 (ranging from 13 in Chad to 124 in Togo), themedian 49 and the standard deviation 29.

Each respondent was limited to checking no more than five "very strong" obstacles.

5

* Price controls* Foreign trade regulations (exports, imports)* Financing* Labor regulations* Foreign currency regulations* Tax regulations and/or high taxes* Infrastructure* Policy instability* Safety or environmental regulations. Inflation* General uncertainty regarding costs of regulations* Crime and theft* Corruption* Terrorism* As well as an open-ended category: "Other."

The discussion also draws on responses to a separate question: "Unpredictabilityof the judiciary presents a major problem for my business operations" for which the sixpoints scale ranges from "fully agree" to "strongly disagree." In order to integratejudiciary unpredictability issues with the other obstacles listed above, we equate "fullyagree" to "very strong obstacles" and "agree in most cases" to "strong obstacles."Throughout this paper, "obstacles" are drawn from the list above (includingunpredictability of the judiciary).

Number of obstacles

The bottom line on Table 3 shows the number of areas which 50 percent or moreof respondents considered to be serious ("strong" and "very strong" responses). It isimportant to bear in mind that the table reflects judgements on the part of businesspeople; the apparent absence of serious problems may mean that the items listed in thequestionnaire do not hinder businesses, and/or that business people have learned to getaround them. Furthermore, comparisons between countries are not straightforwardbecause it is quite possible that the "propensity to complain" varies from country tocountry.

6

Table 3. Reported obstadles to doing business--total number and ranking

Obstacles IIiiiI~~1Iiuaik4Unpredictability of the judiciary 2 ... .4 3 1 10 1 4 4 3Regulations for starting business/niew 3

operationsPnice controlsRegulations on foreign trade (exports, 6 5

imports)Financing 2 8 5 7 5 2 4Labor regulations1Foreign currency regulations 2 .4Tax regulations and/orhigh taxes .. 1 2 1 1 2 4 .. 2 3 1 2 1 1 1 Inadequate supply of infrastructure I .. ... .. . 2 . 9 1 .. 2 8 3Policy instability 3 2 .4 .. ... 6Safety or enviromnmental regulations 3Infation 6 4 1General uncertainty on costs of.. .. .5 . . 3

regulationsCrine and theft 4 4 .. 4 1 I 4Corruption 3 2. 1 5. 74. 23 2. 2Terrorism ... 4

Other

Total number ofsexious obstacles 4 1 4 4 7 4 5 0 10 5 1 4 8 6 2 5

per countr

(continued)

Table 3 (continued)

. .. i..i..i...iII.I.Unpredictability of the judiciary 1 4 1 2Regulations for starting business/new

operationsPrice controlsRegulations on foreign trade (exports,.

imnports)Financing 2 ... 2Labor regulations 4 1. ... 2Foreign currency regulations 4Tax regulations and/or high taxes I 2 2 1 1 4 1 2 1 1..Inadequate supply of infrastructure . .... 3.. . I 3 3Policy instability .

Safety or environmental regulationsnflation I .. .. .. I 2 .. . 2General uncertainty on costs of 4

regulationsCrime and theft 3 .. .. .... .. . ICorruption 2 3 ... 2 2 .4...4Terrorism

Other

Total number of serious obstades 2 4 0 6 2 2 1 2 4 2 0 2 2 1 3 4per county

8

Unpredictability of the judiciary .. 3 2 . 2 .1 1 .2 4 1Regulations for starting business/new .

operationsPrice controls. . . ... ...Regulations on foreign trade (exports, 7 . ...

imports)Financing 5 2 . 2 8 .. . 4 5Labor regulations . .. ..Foreign currency regulationsTax regulations and/or high taxes I114. 1 1111I 2 3 1.Inadequate supply of infrastruture 1.5 1.3Policy instability 4. 4.4Safety or environmental regulations Inflation 6 3General uncertainty on costs of .. .4 . ..

regulationsCrime and theft 6 62. 4 . . 72.5 3.Corruption 2 22. 3 3 3. 3.1 22Terrorism

Other

Total number of serious obstadles 1 7 5 0 4 4 3 2 8 3 0 2 0 5 5 3per countr

(continued)

9

Table 3 (continued)

Unpredictability of thle judiciary 1 1 3 1 3 1 3Regulations for starting business/new

operationsPrice controlsRegulations on foreign trade (exports,

imports)Financing 4 3 5 . .3

Labor regulations'...3 Foreign currency regulations . ... 5Tax regulations and/or high taxes 5 2 1 1 2 1 2Inadequate supply of infrastructure 3.2Policy instability .. 5 3 .. 2 3Safety or enviromnental regulationsInflation 3 1 5.5 .. 2General uncertainty on costs of 7. . 2 . . .

regulationsCrimieand theft 1 3 3 .4 .Corruption 2 1 2.2 4 4Terrorism .. 5

Other

Total number of serious obstacles 5 7 4 2 6 1 4 2 0 3 5 1 0 5 1 3

er countr

1 0

Obtces

Unpredictability of the judcir 32 1 3 1 42

Regulations for starting business/new.11operations

Price controls..0 0

Regulations on foreign trade (exports, . 5 . 2 5 7

imnports)Financing .. 3 3. . . 2 22 30

Labor regulations 5 7 9

Foreign currency regulations. .. . 4. .. 5 7

Tax regulations and/or high taxes .. I 1 1 1 6 4 4 1 53 72

Inadequate supply of infrastructure. . ... . . . . 1 5 4 20 27

Policy instabihity I 2 4 1 3 1 8

Safety or environmnental regulations.2.2 3

Inflation 2.3 2 1 2 20 27

General uncertainty on costs of.5.8 1 1

regulationsCrime and theft 4 7 2 23 3 1

Corruption 2 . 6 3 2 3 35 47

Terrorism . .. .. 2 3

Other 0 0

Total number of serious obstacles 3 3 0 5 2 6 7 4 5 4per country _______________________________

The number of problematic areas ranges from zero (in 9 countries, 7 developingplus Switzerland and the UK) 6 to 7 and more (in seven countries). The surveys werecarried out in 1996/97; conditions may have changed since then. An updated survey ofbusiness conditions is being planned for 1999, which may make it possible to identifysuch changes. The average number of serious obstacles to doing buisiness is 3.7 in thedeveloping and transition countries and 1.5 in advanced industrial countries.

Table 4 shows the sensitivity of results to using a more restrictive definition ofwhat constitutes a serious problem area, lowering the bar from 50 percent or more ofrespondents to, respectively, 60, 70 and 75 percent. The average number of seriousobstacles changes as follows:

6 Korean, Malaysian, and Thai mianagers did not perceive "strong" obstacles to doing business in 1997; thismay reflect the fact that the survey was undertaken prior to the worst of the East Asian crisis, but mayalso reflect long-term fundamental strengths.

Table 4. Average number of serious obstacles to doing business per country

Number obfseiu btcepeconr-Percentageshare of repondents who view prblesa

serious50% or more 60% orme 70% omre75%or or

Average for developing and transition 3.7 2.2 1.2 0.7countries (63 countries)

Average for advanced developed 1.5 0.5 0.3 0.3countries (I11 countries)

Ratio of averages for developing/ 2.7 4.4 4 2.3transition and advanced developed,countries

The nature of obstacles

The last columns of Table 3 show obstacles to doing business in order offrequency in the countries where firms were surveyed. Using the 50 percent cut-offpoint, the table suggests that taxes are by far the most prevalent perceived obstacle todoing business (72 percent of the countries). The finding is ambivalent, however,because the question combines tax regulations and "high taxes." More meaningful is thefrequency of corruption and the unpredictability of the judiciary, which are perceived in47 and 42 percent respectively of the 74 countries to be a serious obstacle to doingbusiness. Next come, neck-and-neck, crime and theft (31 percent of countries), lack offinancing (30 percent), inadequate infrastructure (27 percent) and inflation (27 percent).In none of the countries were "other" obstacles to doing business considered to beserious, suggesting that the list of possible problem areas was quite comprehensive.

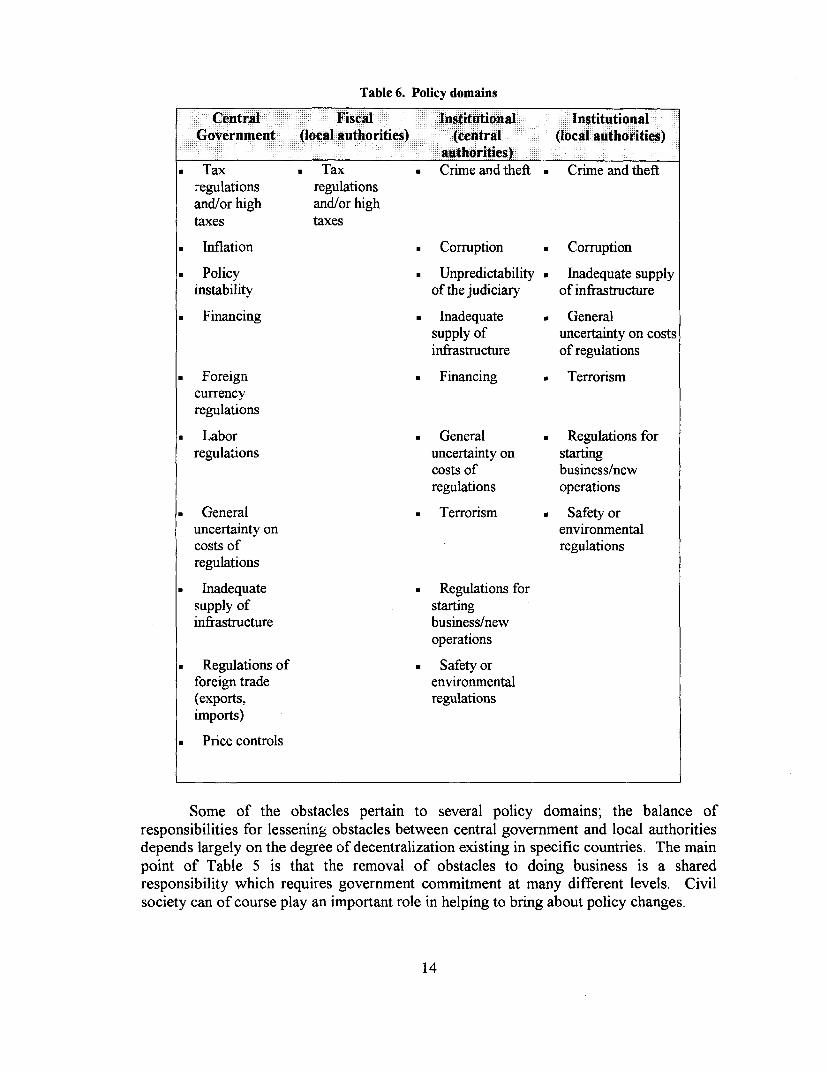

Table 5 compares the perceived seriousness of obstacles in developed anddeveloping countries. Labor regulations and safety and environment regulationsobstacles are considered to be serious obstacles to doing business in a number ofdeveloped countries, but do not loom large in developing economies. Taxes, as noted,are the most prevalent perceived obstacle for all countries (in 90 percent of transitioneconomies and in 64 and 65 percent, respectively, of developed and other developingcountries). Inflation is considered to be a serious obstacle in 35 percent of non-transitiondeveloping countries and 25 percent of transition economies. Infrastructure is considereda problem in 9 percent of developed, 10 percent of transition and 40 percent of othersurveyed developing economies. Obstacles related to political instability and generaluncertainty in the cost of regulations are much more prevalent in transition then in otherdeveloping economies (40 versus 12, and 30 versus 5 percent respectively). Lastly,regulations related to foreign economic activities are more of an obstacle in transitioncountries.

12

Table 5. Obstacles to doing business considered serious by 50% or more of respondents

(percent of countries)

Obstacles All Developed All_ Transition Othercountries :countries deing ies dev-eloping

. --- ~~~~~~~countries - --- countries:Unpredictability of the judiciary 42 9 48 50 47Regulations for starting 1 9 0 0 0

business/new operationsPrice controls 0 0 0 0 0Regulations on foreign trade 7 0 8 15 5

(exports, imports)Financing 30 0 35 30 37Labor regulations 9 36 5 0 7

Foreign currency regulations 7 0 8 15 5Tax regulations and/or high taxes 72 64 73 90 65Inadequate supply of 27 9 30 10 40

infrastructurePolicy instability 18 0 21 40 12Safety or environmental 3 18 0 0 0

regulationsInflation 27 0 32 25 35

General uncertainty on costs of 11 0 13 30 5regulations

Crimeandtheft 31 0 37 40 35

Corruption 47 0 56 60 53Terrorism 3 0 3 0 5

Other 0 0 0 0 0

Count,y-specific responses

Table 3 ranks the most serious obstacles identified by business people in each

country surveyed. It shows, the relative importance attached to different obstacles (caseswhere 50 percent or more of respondents judged a particular obstacle to be "strong" or

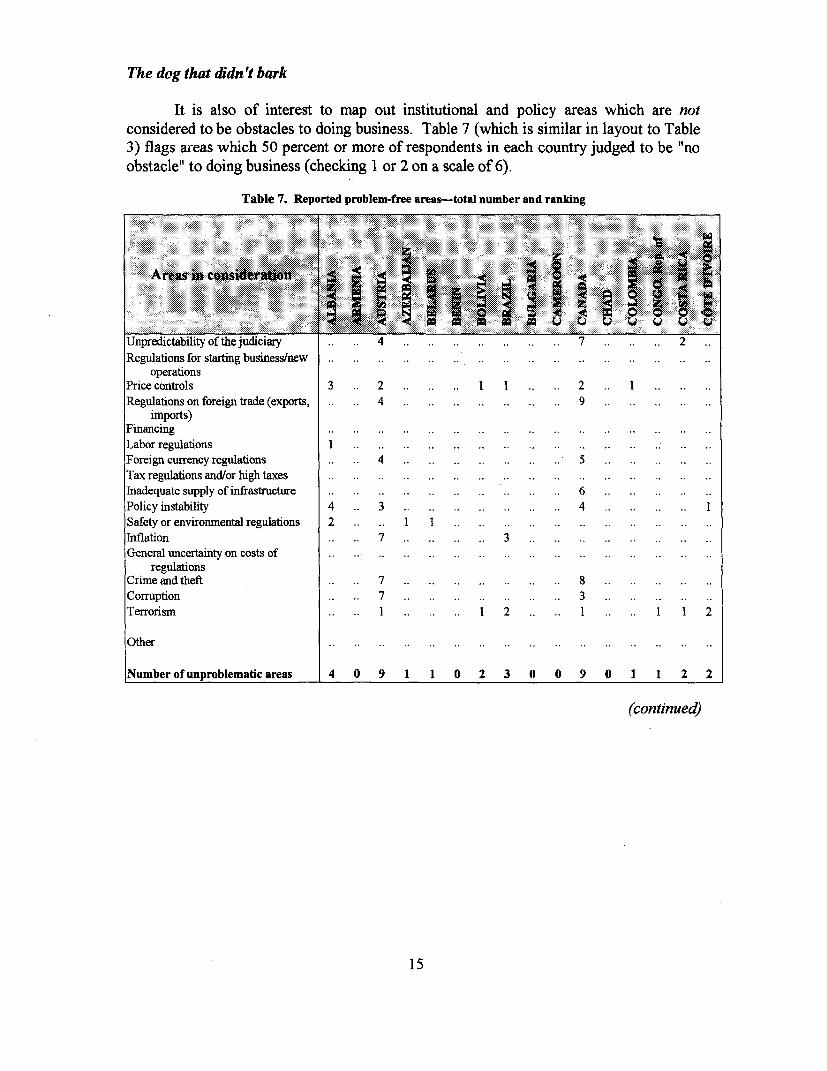

"very strong"). So for example a number 1 means that a particular area was mentionedby the largest proportion of respondents as being a serious obstacle to doing business, a 2the second-most frequent mention and so forth. The ranking of country-specificobstacles to doing business might help governments and aid agencies to prioritize privatesector development strategies, especially in combination with Table 6, which delineatesprimary policy domains on which the lessening of different obstacles depends.

13

Table 6. Policy domains

CentratFiscal XInstitutional InstitutionalGo000Evernment0 0 (1cal fauthorities) (00itral (local autharities)

aut :(iiii:; ialuthoraities)

. Tax . Tax . Crime and theft . Crime and theft.egulations regulationsand/or high and/or hightaxes taxes

. Inflation . Corruption . Corruption

. Policy . Unpredictability . Inadequate supplyinstability of the judiciary of infrastructure

. Financing . Inadequate . Generalsupply of uncertainty on costsinfrastructure of regulations

. Foreign . Financing . Terrorismcurrencyregulations

. Labor . General . Regulations forregulations uncertainty on starting

costs of business/newregulations operations

. General . Terrorism . Safety oruncertainty on environmentalcosts of regulationsregulations

. Inadequate . Regulations forsupply of startinginfrastructure business/new

operations

. Regulations of . Safety orforeign trade environmental(exports, regulationsimports)

. Price controls

Some of the obstacles pertain to several policy domains; the balance ofresponsibilities for lessening obstacles between central government and local authoritiesdepends largely on the degree of decentralization existing in specific countries. The mainpoint of Table 5 is that the removal of obstacles to doing business is a sharedresponsibility which requires government commitment at many different levels. Civilsociety can of course play an important role in helping to bring about policy changes.

14

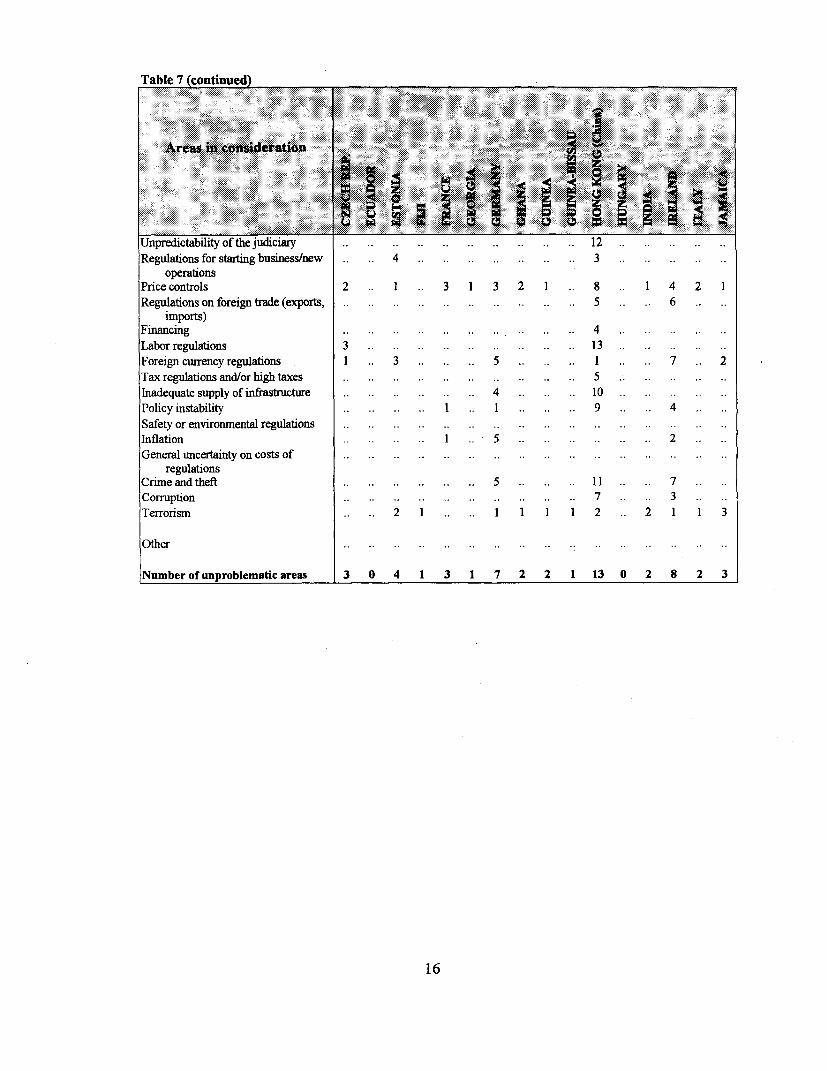

The dog that didn't bark

It is also of interest to map out institutional and policy areas which are notconsidered to be obstacles to doing business. Table 7 (which is similar in layout to Table3) flags ar-eas which 50 percent or more of respondents in each country judged to be "noobstacle" to doing business (checking 1 or 2 on a scale of 6).

Table 7. Reported problem-free areas--total number and ranking

d~ ~~

Areas in M .....de.at.o

Unpredictability of the judiciary 4 7 2

Regulations for starting business/newoperations

Price controls 3 2 121IRegulations on foreign trade (exports, 4 9

imports)FinancingLabor regulations I .. .. ..Foreign currency regulations 4 .. .. . 5Tax regulations and/or high taxesInadequate supply of infrastructure .. . .. .. .. . 6

Policy instability 4 3. 3 .. .. . 4Safety or environmental regulations 2 1 1 . ..Infation 7 .. .... . 3General uncertainty on costs of

regulationsCrime and theft 7 .8Corruption 7 3Terrorism I .1 2 . 1 1 1 2

Other -.... .

Number of unproblematic areas .14 0 9 1 1 0 2 3 0 0 9 0 1 1 2 2

(continued)

1 5

Table 7 (continued)

Unpredictability of the judiciary .. 12Regulations for starting business/new 4 3

operationsPrice controls 2 1 3 13 21 8 1 42 1Regulations on foreign trade (exports. .. .. .5 6

imports)Financing . . . . . . ... 4Labor regulations 3. .. .. 13 . .. . .. .Foreign currency regulations 1 3 .. ... 5.. . 1 . 7 .. 2Tax regulations and/or high taxes. .... 5hinadequate supply of infrastruture. . . . . .4. .. 10Policy instability I 1. .9 4Safety or environmental regulationshiflation 1 5. . .2General uncertainty on costs of

regulationsCrime and theft 5 .. . 1.I1 7Corruption . .... 7 3Terrorism.21 . 1 I 1 1 2. 2 1 1 3

Other

Number of unprobtematic areas 3 0 4 1 3 1 7 2 2 1 13 0 2 8 2 3

1 6

Unpredictability of the judiciary.Regulations for stating business/new ..

operationsPrice controls 3 .. 3 .. .. 2 3Regulations on foreign trade (exports, .. 3

imports)Financing ... 4 . . . . .Labor regulationsForeip currency regulations 1 2.6 .. 2Tax regulations and/or high taxeshinadequate supply of infrastructurePolicy irnstability..2.2Safety or environmnental regulations.I3Inflation.2General uncertainty on costs of

regulationsCrime and theft 2.4.2Corruption..Terrorism 1. 2 1. 1 2 1. 111

Other

Number of unproblematic areas 2 0 3 1 1 2 2 2 0 4 6 1 2 0 0 3

(continued)

17

Table 7!continued)

Unpredictability of the judiciary 6 6Regulations for starting business/new 10

operationsPrice controls I 1 2 6 7 2Regulations on foreign trade (exports, 10

imports)Financing . . . . . . . . . 12.Labor regulationsForeign currency regulations ... .2. . . 9 .. ... 8Tax regulations and/or high taxesInadequate supply of infrastructure. . . . . . . .6 . .4Policy instabiity. .. .. 2 2 .. ... 2 . ..Safety or environmental regulations .. . .. .... . . .. 5Inflation 2 .. 5Generaluncertainty on costs of. .. .. .1 . ..

regulationsCrime and theft. . . . . . . . 1 . .9 . . .Corruption . .. .. 2 .. ... 3 . ..Terrorism 1. . . I 1 2 .. 1..

Other.. . .. . .. . .. . .. .

Number of unproblematic areas 1 0 1 2 2 2 0 2 10 0 0 0 12 2 0 0

1 8

Unpredictability of the judiciary .. .. .. .. .. .. .. .. .. .. 6 8Regulations for starting business/new .. .. .. .. .. .. .. 3 4

operationsPrice controls 1 5 . .5 1 1 33 45Regulations on foreign trade (exports, . .. 5.... .. 7 9

imports)Financing ...... 3 4Labor regulations ....... 3 4Foreign currency regulations 1 2 .. .I I 19 26Tax regulations and/or high taxes .. .. . . . . . I IInadequate supply of infrastructure .. 7 .. . . .. .. 6 8Policy instability . ...... 13 18Safety or environmental regulations .. .. .. .... .. 4 7 9Inflation 1 .. .. .. .. .. .. 9 12Generaluncertaintyon costs of 2 .... .. 2 3

regulationsCrime and theft .... 2 11 15Corruption 2 ...... 7 9Terrorism 2 I I 1 2 3 2 43 58

Other 0 0

Number of unproblematic areas 1 2 7 1 1 1 0 5 3 2

Table 8 aggregates countries by groups, as in Table 5. It suggests that in 58percent of the surveyed countries (73 percent of developed, 65 percent of developing and35 percent of transition countries) terrorism is not perceived to be a serious problem bybusiness people, nor are price controls, which are not considered to be a serious problemin 45 percent of the countries (73 percent of developed, 44 percent of developing and 30percent of transition countries, respectively).

19

Table 8. Reported problem-free areas (percent of countries)

............. .. .. .- eveloped eAl l Transition i thert000Ares i consideratin tk ll .cFountries40 Coun0. itrie devel0oping eco4;nomie eeloping0i^^}i

iEEi;i .i Ei; cou,ntries countnresUnpredictability of the 8 27 5 0 7

judiciaryRegulations for starting 4 0 5 5 5

business/new operationsPrice controls 45 73 40 30 44Regulations on foreign trade 9 45 3 0 5

(exports, imports)Financing 4 9 3 0 5Labor regulations 4 0 5 10 2Foreign currency regulations 26 55 21 15 23Tax regulations and/or high 1 0 2 0 2

taxesInadequate supply of 8 36 3 0 5

infrastructurePolicy instability 18 55 11 5 14Safety or environmental 9 0 11 20 7

regulationsInflation 12 64 3 5 2General uncertainty on costs of 3 18 0 0 0

regulationsCrime and theft 15 45 10 0 14Corruption 9 45 3 0 5Terrorism 58 73 56 35 65

Other 0 0 0 0 0

Looked at together with problem areas in Table 3 it seems that neither pricecontrols, foreign trade controls or foreign exchange regulations were considered in1996-97 to be serious obstacles to doing business except in a handful countries (Belarus,Bulgaria, Republic of Congo, Fiji, Kazakhstan, Ukraine, Uzbekistan, West Bank andGaza, and South Africa). Regulations for starting a new business were found to be anobstacle in only one of the surveyed countries, surprisingly a developed one (Austria).These results are indicative of the depth and breadth of liberalization which has takenplace over the last decades.

Obstacles and levels ofprivate investment-econometric results

Econometric calculations presented in Table 97 show that, unsurprisingly, in manycases a definite link exists between 1996 private investment and problems (or lack of

7 The specifications we tested have the following form:Private Inv./GDP96 = aO + al LN(GDP/Const. 87 PPP,90) + a2 LN(Sec school enrol., 1990)+ a3 OBST +

u. Private Inv./GDP96 is a ratio of private investment to GDP in 1996. LN(GDP/Const. 87 PPP,90) isthe logarithm of 1990 GDP per capita calculated at PPP in 1987 prices from a World Barik data base.LN(Sec school enrol., 1990) is the logarithm of growth secondary school enrollment in 1990 also takenfrom a World Bank data base. OBST is an additional variable drawn from the set of 16 obstacles (weran separate tests for "problem" and "problem-free" values of the variable).

20

them) in policy areas relevant to doing business. In some cases the share of businessexecutives reporting that a particular policy area is problematic is significant, in somecases the share of problem-free responses and in other areas both responses are relatedsignificantly to investment. These results are to be treated as preliminary, if only becauseof the small number of countries (23) common to both data sets. Nevertheless, out of 16policy areas 7 are significant for private investment levels when there is a perceivedserious problem in these areas. At the same time, 9 out of the 16 policy areas aresignificant to levels of private investment when they are problem-free. And 4 areas outof 16 (financing, labor regulations, foreign currency regulations, and crime and theft) aresignificant in both cases.

Table 9. Summary regression output (dependent variable-private investment/GDP, 1996, numberof observations - 23)

Variables:- . ..... . . - . .... --. . .... .. ,, , 1 : :

Intercept 3.841 14.488: 0.265 0.7941 -15.346 17.4 . -0.878 0.391

LN(GDP/Const. 87 PPP,90) 1.312 2.5931 0.506 0.619 2.102 3.161 0.665 0.514

LN(Sec school enrol., 1990) 2.291 2.870 0.798 0.435 2.108 3.524 0.598 0.557

Unpredictability of the -0.169 0.049 -3.425 0.003 0.175 0.138 1.273 0.219Audiciary ___

Adjusted R Squarem__ 0.410 0.121

Intercept -9.852 17.537 -0.562 0.581 -25.294 21.662 -1.168 0.257

LN(GDP/Const. 87 PPP,90) 2.026 3.266 0.620 0.542 3.483 3.462 1.006 0.327

LN(Sec school enrol., 1990) 2.750 3.625 0.759 0.4571 1.838 3.591 0.512 0.615

Regulations for starting -0.091 0.157 -0.581 0.568 0.118 0.103 1.147 0.265business/new operations_________

Adjusted R Square 0.063 0.108-

Intercept -8.974 16.706 -0.537 0.597 -19.122 15.915 -1.202 0.2441

LN(GDP/Const. 87 PPP,90) 2.710 3.147 0.861 0.400 1.665 2.878 0.579 0.570

LN(Sec school enrol., 1990) 1.605 3.504 0.458 0.652 3.819 3.229 1.183 0.252

Pric controls -0.277 0.181 -1.529 0.143 0.274 0.113 2.419 0.026

Adjusted R Squarem__ 0.151 0.271

Intercept -5.776 18.1621 -0.318 0.754 -12.543 14.724 -0.852 0.405LN(GDP/Const. 87 PPP,90) 1 .172 3.234 0.610 0.549 0.987 2.752 0.359 0.724

LN(Sec school enrol., 1990) 2.295 3.606 0.636 0.532 3.580 3.050 1.174 0.255

Regulationson foreigntrade -0.154 0.189 -0.814 0.426 0.338 0.116 2.918 0.009(exports, imports)_

(continued)

2 1

Table 9 (continued)

Var iables o _

Adjusted R Square ___0.079 0.342

Intercept 9.462 15.217 0.622 0.541 -23.107 13.767 -1.678 0.110

LN(GDP/Const. 87 PPP,90) 0.229 2.661 0.086 0.932 2.446 2.483 0.985 0.337

LN(Sec school enrol., 1990) 3.687 2.9161 1.265 0.2211 2.908 2.7511 1.057 0.3041

Financing -0.250 0.075 -3.335 0.003 . 0.430 0.113 3.801 0.001

Adjusted R Square 0.399 ___0.458

Intercept -22.060 16.532 -1.334 0.198 -12.652 16.404 -0.771 0.450

LN(GDP/Const. 87 PPP,90) 4.099 3.0681 1.336 0.197 1.386 3.053 0.454 0.655

LN(Sec school enrol., 1990) 3.056 3.238 0.944 0.3571 2.938 3.375 0.870 0.395

Labor regulations -0.223 0.098 -2.282 0.034 ** 0.177 0.098 1.806 0.087*

Adjusted R Square 0.252 0.186

Intercept -4.065 16.680 -0.244 0.810 -0.554 15.148 -0.037 0.971

LN(GDP/Const. 87 PPP,90) 1.909 3.040 0.628 0.537 -0.7891 2.906 -0.271 0.789

LN(Sec school enrol., 1990) 2.118 3.382 0.626 0.539 4.7671 3.141 1.518 0.146,

Foreign currency -0.185 0.102 -1.802 0.087 * 0.389~ 0.136 2.865 0.010*regulations

Adjusted R Square 0.186 _ 0.334

hitercept 12.237 16.957 0.722 0.479 -5.639 16.924 -0.333 0.743

LN(GDPfConst. 87 PPP,90) -0.677 2.930 -0.231 0.820 0.893 3.172 0.282 0.781

LN(Sec school enrol., 1990) 4.901 3.189 1.537 0.141 2.770 3.442 0.805 0.431

Tax regulations and/or high -0.195 0.070 -2.771 0.012 ** 0.234 0.152 1.539 0.140taxes

Adjusted R Square 0.321 ___0.1521

Intercept 5.447 24.151 0.226 0.824 -15.085 17.846 -0.845 0.408LN(G-DP/Const. 87 PPP,90) 0.183 3.729 0.049 0.961 2.227 3.211 0.694 0.496

LN(Sec school enrol., 1990) 3.078 3.607 0.853 0.4041 2.859 3.554, 0.804 0.431

Inadequate supply of -0.081 0.8 0900.369 0.076 0.072 1.054 0.305infrastructure

22

-- ~~~~~g N --aiA d0 a1t Va4riables

Adjusted R Square _ ____ __ 0.087 0.099

Intercept -10.993 16.568 -0.663 0.515 -2.567 17.874 -0.144 0.887LN(GDP/Const. 87 PPP,90) 2.294 3.088 0.743 0.467 1.301 3.185 0.409 0.687LN(Sec school enrol., 1990) 3.183 3.433 0.927 0.365 3.259 3.529 0.923 0.3671Policy instability -0.128 0.078 -1.638 0.118 -0.250 0.191 -1.311 0.206

Adjusted R Square 0.164 0.126

Intercept -28.823 19.750 -1.459 0.161_ -11.125 16.947 -0.656 0.519LN(GDP/Const. 87 PPP,90) 1.197 3.088 0.388 0.703 2.037 3.149 0.647 0.526LN(Sec school enrol., 1990) 6.538 4.093 1.597 0.127 2.096 3.512 0.597 0.558Safety or environmental 0.389 0.226 1.719 0.102 0.123 0.093 1.322 0.202

regulations _ _

Adjusted R Square 0.175 0.127

Intercept -7.608 17.031 -0.447 0.660 -14.764 14.311 -1.032 0.315LN(GDP/Const. 87 PPP,90) 3.118 3.278 0.951 0.353 1.719 2.648 0.649 0.524LN(Sec school enrol., 1990) 0.322 3.897 0.083 0.935 2.260 2.938 0.769 0.451Inflation -0.109 0.082 -1.319 0.203 0.499 0.155 3.215 0.005

Adjusted R Square 0.126 0.382

Intercept -9.577 16.992 -0.564 0.580 -12.319 15.190 -0.811 0.427LN(GDP/Const. 87PPP,90) 2.288 3.173 0.721 0.480 2.403 2.826 0.850 0.406LN(Sec school enrol., 1990) 2.588 3.504 0.739 0.469 1.043 3.184 0.328 0.7471General uncertainty on costs -0.154 0.122 -1.265 0.221 0.211 0.081 2.617 0.017 *

of regulations

Adjusted R Square 0.121 0.299

Intercept -1.461 16.043 -0.091 0.928 -6.562 16.445 -0.399 0.694LN(GDP/Const. 87 PPP,90) 2.291 2.908 0.788 0.441- 1.157 3.066 0.377 0.710LN(Sec school enrol., 1990) 0.697 3.323 0.210 0.836 = 2.340 3.372 0.694 0.496Crime and theft -0.128 0.055 -2.323 0.031 ** 0.320 0.177 1.813 0.086 *

(continued)

23

Table 9(cVntinued

XM MlE:.i. j :2E E

.1;.~~~~~~~~~~~~~~~~~;

i . Ei.ij20ijjjj j jgtjjjEi.gi0i .............. -E ..lg iif. 1i2 :ff;4 .id............ ji00i. .ii; i#SS t :0 0ti: : , I 0: : f d: :tf j:0 .....................:::..j ....Ei

Adjusted R Square 0.257 0.187

Intercept 9.878 17.925 0.551 0.588 -15.458 17.453 -0.886 0.387LN(GDP/Const. 87 PPP,90) 0.795 2.954 0.269 0.791 1.457 3.172 0.459 0.651LN(Sec school enrol., I1990) 2.202 3.236 0.6811 0.504 3.777 3.610 1.046 0.309

Corruption -0.190 0.083 -2.286 0.034 ** 0.089 0.069 1.301 0.209

Adjusted R Square 0.252 0.124

Intercept -9.088 17.106 -0.531 0.601 -6.765 16.493 -0.410 0.686LN(GDP/Const. 87 PPP,90) 1.727 3.182 0.543 0.594 1.623 3.052 0.532 0.601LN(Sec school enrol., 1990) 3.295 3.574 0.922 0.368 2.047 3.395 0.603 0.554Terrorism -0.139 0.119 -1.167 0.258 0.330 0.186 1.770 0.093 =

Adjusted R Square I0.11 0.181

* Significant on the 10 percent confidence level.** Significant on the 5 percent confidence level.

IntecepSignificant on the 1 percenit confidence level.

Source for private n vestment data: Jack Glen and Ma5usz A. Sunlinsl, "Trends in Prvate Investment in DevelopingCountriestatistics for 1970-96," IFC Discussion Papr 34, Wash=2igton, D.C., 1998.

The highest statistical significance for depressing private investment (on the 1

percent confidence level) is for unpredictability of the judiciary and lack of financing.Where financing is not a serious problem this is very positively associated to levels ofprivate investment (significance on the 1 percent confidence level). In contrast, lack ofserious problems with the judiciary are not related significantly to high levels of privateinvestment. The same asymmetrical relationship seems to characterize tax regulationsand corruption-where these are serious problems they depress private investment, butlow taxes and lack of corruption do not by themselves stimulate private investment.

24

Appendix IMethods and Sources

1. Fixed Investment Data

National accounts normally do not break down gross domestic investment into itsprivate and public sector components. Private investment is defined in this publication asthe difference between total gross domestic investment (from national accounts) andconsolidated public investment. Consolidated public investment data for each countrywere compiled mainly from World Bank Country Economic Memoranda, PublicInvestment Reviews, Public Expenditure Reviews, and other World Bank countryreports. They reflect efforts by World Bank missions to compile public sector data.Where World Bank data are not available, country data were used.

The countries included in this edition represent all the developing countries forwhich the relevant data are available. Minor changes were made in the last two or threeyears for most countries as a result of revisions in their national accounts data. Updatesare not available (at the time of this writing) through 1997 for Korea.

Table 1 presents investment figures for each country, including total fixedinvestment (GDFIIGDP); private fixed investment (PRIVATE I/GDP); and public fixedinvestment (Public I/GDP). The ratios are computed using local currency units at currentprices.

25

Appendix 2Statistics

27

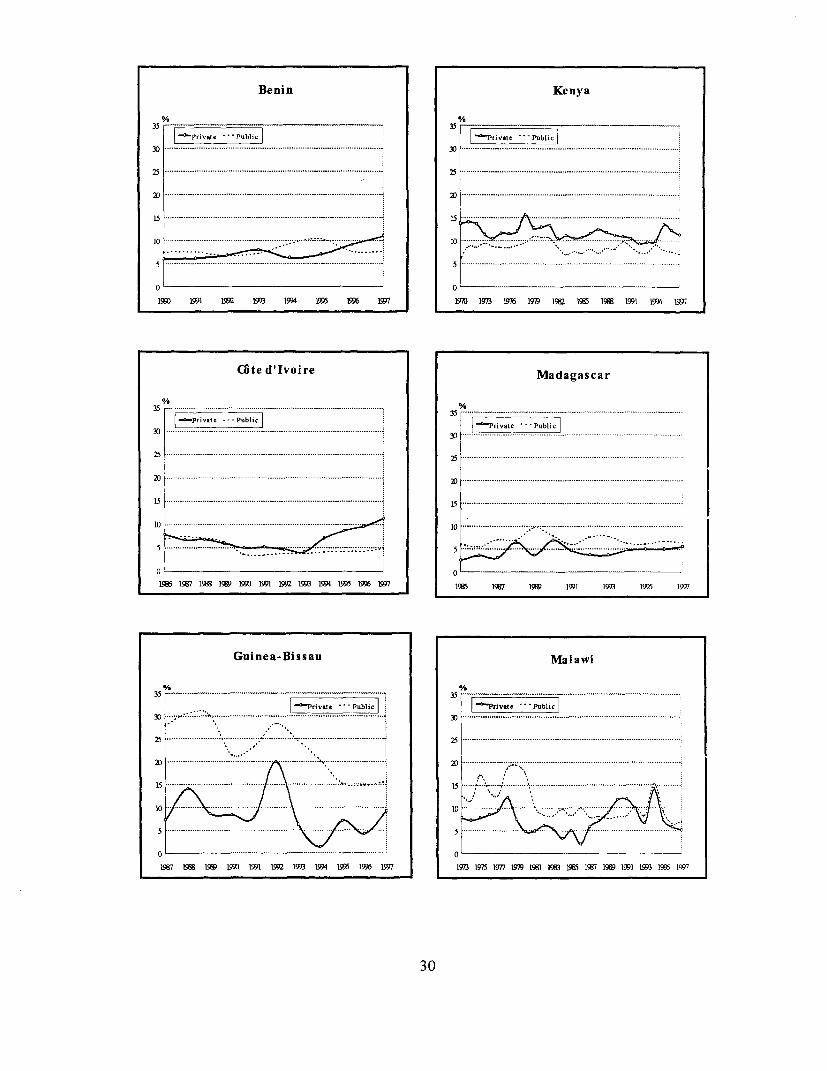

Sub-Saharan Africa

Benin

C6te d'Ivoire

Guinea-Bissau

Kenya

Madagascar

Malawi

Mauritania

Mauritius

Namibia

South Africa

29

Benin Kenya

35 35tPia. ... Publc[ I tj7 bi

15. ........... 15.............

10 *.10 . -..

0 0

C6te dIlvoire Madagascar

35 ...... .......... .................................... ... 5

30 P...... ... .... I. ...... ......P....b....i....... ........ e Pu li33~~~~~~~ ~~~~~~~~~~~~~~~~~~~~~~~0............................. ........ ....

25 ...... . ....... .. .. . ........ .. .... .. ....... ........

5 ........ .........

0 0

]9ff 1967 1 9 l 1 1971 1992 1973 1ON 1975 w 199717 7 19M 1971 1993 1975 1977

Guinea-Bissau Malawi

--------- Privt e ... ubh1i-cit Mt~ ~ 17i33 . .... .~~~~~~~~~~~~~~~~~~~~~~.. ~~~~~ 30 .....................

25.

............ 10 .........

30

966 f661 Z661 (t 05t I¶ 966 Z66 X1

-0

.- ~ - -w .*. * 01;b-- - -

......... ..................................................................... ...........................O

.............. tA Ji

,..._..........._... _..._..._..._.._.1,_,.... 01

:.. .............................. ............. . ......

Sl ~~~~~~~............................................. .......................... :.'.: ' 5

, w~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~In . s. . jv Ap ,

1661 1661 1661 R661 6661 Z661 6161 9161 £161 0161 1661~~~~~~~fi Wb 96 1 6661 66 £66 Z661 T66 9661

06.~~~~~~~~~~~~~~~~~~~06

,~~~'J , , OS , S!UU

, ............ .... + . .* . OE ... ~~~~~~~~~~~~~~~~~~... ,^........................................... ........... ...... --................ .. .........

.. _w_o ... _ _ _ _ _ _ _.,_ .. _ _ _ _ _ _._ .. _ SE .... :_ _._._._ ......... _.,_ .. _, _ _ _.,._............._._ ...... ... _.SE

ea!ltlllos e!ue!sneyV~~~~~~~~~~~~.......................................................s

Latin America and the Caribbean

Argentina

Belize

Bolivia

Brazil

Chile

Colombia

Costa Rica

Dominican Republic

Ecuador

El Salvador

Guatemala

Mexico

Nicaragua

Panama

Paraguay

Peru

Uruguay

Venezuela

33

L661 r661 Lff61

£651 6661 1661 891 SW1 ME 666! 9L6 £6h 61 066

0

C..~~~~~~~~~~~~~~~............

.~~~~~~~~~~~~~~~01

........ .............. ~.................... o

¾ ~ ~ ~ ~ ~ ~~~~........................................ --- -... .. .. .. .. ... .. .. .. .. ... .- .. .. .. ... .. .. .. .. ... .. .. .. .. .... .. .. ¾

~ ~~~~~IzU Jg w ui;u~~~~~~~~~~........... ........ ..............................v

.91

169 P60 M M M M &O Wg M M~~1~q15.-. 9

L661 M M M M ZZI 6661 9LO EL61 OL6~~~~~~~~~~~~1:

0.............................

.91.191~~~~...................... ..........

................................ 0 .. ...

.... . . ....... .... .. .... .......

1611 1611 1611 ~~~1 ~~1 Z~ 9161 9161 £161 £661 £611 t611 ~~~~~ ~1 16..1....91.6.............0.61

. 91.~~~~~~~~~~~~~~~~~~~~~~~~~~~~~...... ..... ............... 91

............... .......................................... CZ

...........................................................

9£

L661561 S0i t66 Ka i M 61 166 055 dl MK ¢lV SNS SW Pil L651 M6 166 MI5 SSi D15 6l6 916 E;!61 f6l

',. ~~~~~~~~~~~~~~~~~~~~~~~~~~~~~............... ...,S' ,;\;-;; --"

. ............ .e 46 + + .6.iE......... .... .... .... . ........ 6. . .......... . ... ....... . ,. . ........

, I allQnd,., 9le^IJd__ I t I allqtld ~~~~~~~~~~~~~~~~.......................................................................... ~M S E.. _ *.E6.>..................... ......w. ........................... SE

...... ........................................................... ........................... 51 .......................... ......... ..... ............

................... ............................................. ... ...... s ..................... ......... ......... .. sz. .............. ..........................

.............. , ^ ...................................... OE ....... , . .6. .,,,,, + .. e+ ..................... I.............. OE

Tlid. .. | d v!lqnd ... aluA!ld_ S.,, , , ,. S~~~~~~~~~~~~~~~~~E . . .d. *, .....

L62 t61 1661l 1W 6F ZR5I S^1 9 E851W lRil aR61 S< 651 m il1i 2661 %166 OSS1

: .......... _ O , .... ~~~~~ ~ ~ ~~~~~~~~~~~~....................... . ......... : .::... ..... . : . :.: ...................... .. .. vS..... ............... ......... . . . ........ 5

,~~~~~~~~~~~~~~~~~~~~~~~0 ... ........... '..'..''............................ 0_w 1

.* 66* .- * , 6++ * , , S~~~~~~~~~~~Z ....... ... ...... -. ....... .................. ....... ............ . ... 5Z

......... ................... ..................,.,...........OE....... ... ............... .. ..... .... .. . OE

I O lnlq ,, e 'I 3tlmi d ,, sal

L6~~~~~~~~~~51 91, _,6,_ _S661 K _ M _ ba- 9661 -w-s6--es-51 E 1 Z 61 05

nsaa enSese3!N~~~~~~0

Middle East and North Africa

Egypt

Iran

Morocco

Tunisia

Turkey

37

Egypt Tunisia

.................................... ~.-...-..-.....-........-.20.. .......... 2 3.......... .. ..... ..........................

25 .................. ............. 5 .......

0 ~~~~~~~~~~~~~~~~~~~~~~~~0

Iran Turkey

35 ----- . . . .. 35 . ------ --- . .... ......

5..0.- . . ....... S...... ................

C C-

Mo ro cco

Pri--P ubi,305............................... ......................

25 ...................................... ..........

15 . ... .....I. .............. ..... ; .......

10 .......... .... ...

S....................................... .........

0

1975 197g 91 I(M IM IM M 7 IM 1MI 1M IM 15

38

Transition Countries

Bulgaria

Poland

Romania

39

0t7

Ob~~~~~~~V

L651 9661 Sit 161 6661

0

_ .. ~~~~~~~......... ''..::.L:.:.'.'.'.:................ . ,...... .................................

, St

..... .......... ...............................I ............................... OE

|~~~~~~~~~ - --------- *IAd

00

....... ........ I..... . .................... ._. ..... _.___........... ~._.... _(

........ %

....................... ..................... ............................................... / S

~~~~~~~~~~~~~~~........................................................................ ,.... ,S

..................................................... . ............... ............... , ,

...................................... ................................................. . O...........,5

|1 auijndg «78da|S

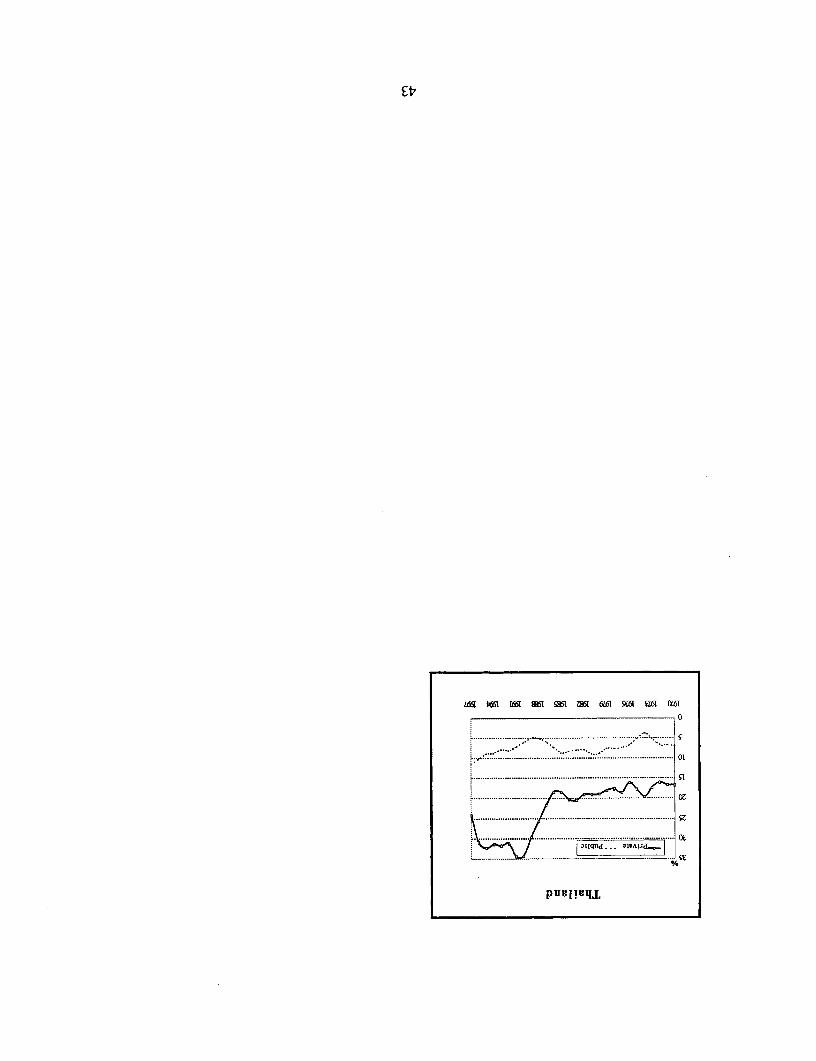

East Asia

China

Indonesia

Korea

Malaysia

Papua New Guinea

Philippines

Thailand

41

ztl~~~~~~~~~~~~~~~~~~~*U

L661 9%1i E661 16t;1 6fti LSS Sib EF 1F 6l6 U616 SUil i651 Z661 taI Z9il U61 ZC6

0 0

..... .

................ w... .. ,I ;i..01.. ..... ............... ;: ' .:.::.:.......... ol ............. 0 1

~i~qt o ............. 9L1 ...... .... .;. .S1

................................ o...................................... ........ a 9 O

..................................................................... ................ ...... g............... 5E.. ... .. ... ...... yS

......................................................... .................... -------- s. +OE ......... ..... O

........................................ I l= d - ] <Id- SE. E

sauddUl!qd c nouXd DS 3qWdaH

_l 5 _661 E661 51_ _ _6_1 _ l S1 ER51 lRIl L661 v661 1661 i ESS1 1951

~t~qfO . O

................... - ....... S .............. ... .. ..~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~................ ... ,,'0 . ............. .... :.:. ... '..__0

;. ..... . .... ............ , .............................

/ ~ ~ ~ ~~~~~~~~~~~~~~~~~~~~~~o ............ ....... ........ OE..,............

DI[qlid,, SIBAISd,

b~~~~~~~~~~~~~~~~~~

. .

.. ................ e;&..... ............... ..............._.......

.. ~~~~~~~~~~~~~~~~ J

. . ....... ...... . . .... ........... ....... ........................................... 0

........ ... ....................................,

South Asia

Bangladesh

India

Pakistan

45

Bangladesh

35 - ____l_.

30 . ...... ., ...

25 . ............... ..

is ....... ................................. ..................10.

05

1973 1975 1977 1919 1511 19 1E5 1907 19 1991 13 1995 1907

India

35

Z rvate* -Pubic :{0 1........ ........................................25 ......................... ........ .....................................................

A) .................................................................. I............

10 .........

* b......................................... ............................................

0

I91 IM L76 L9XIg9 Ig ISS IRE Ml9 1994 MW7

Pakistan

35

| v Pil^e -Public.I30 M - ... P bi ................................................

25 .... .......... ... ......... .... ................. ........... ....................

U5 .......................... ............. ............... .......... ......... ...........

10 --------- .. .....5 ......................................... ........

19 I1510 19B5 SEX 19; 5

46

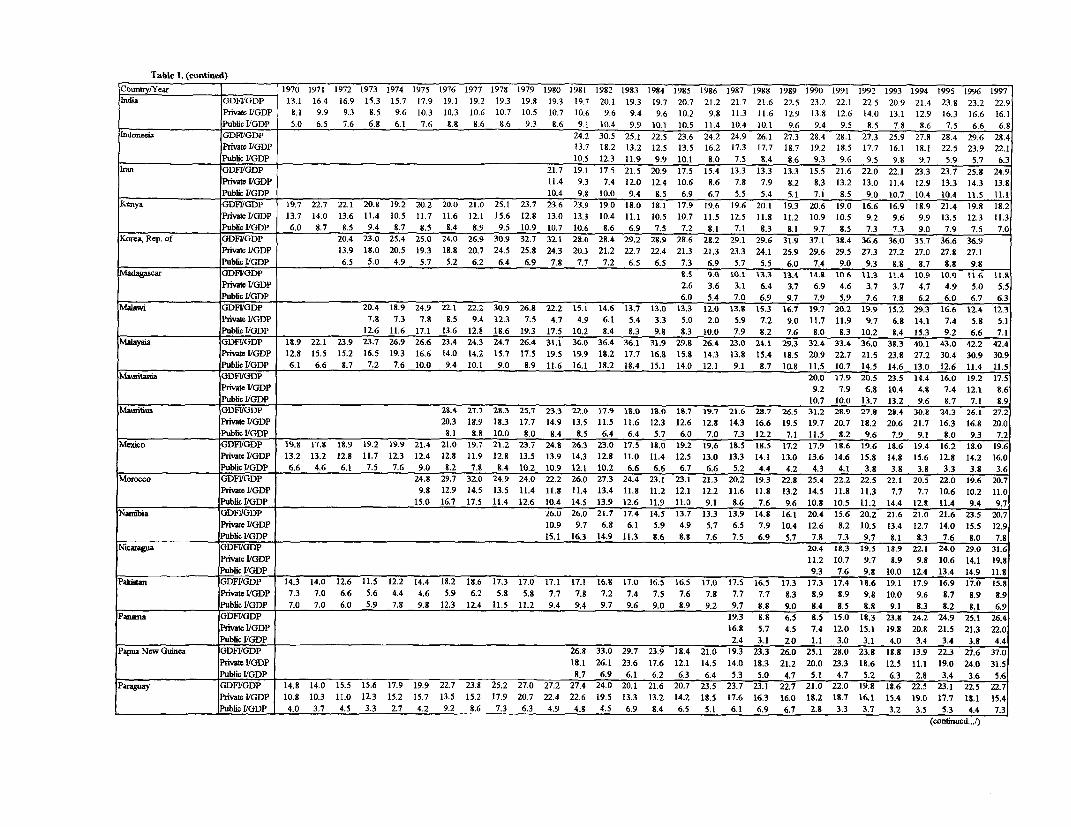

Table I. Investmerit as a share of GDP (in %)Country/Year 1970 1971 1972 1973 1974 1975 1976 1977 1978 1979 1980 1981 1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997

Argentina GDIJGDP 21.2 20-.9 20.7- 18.2 19.3 25.9 26.8 27.2 24. 22.7 25.3 22.7 21.8 20.9 20.0 17.6 17.5 19.6 18.6 15.5 14.0 14.6 16.7 182 19.9 18.3 18.5 20.1

Private I/GDP 13.1 12.8 12.5 11.6 12.5 16.1 15.1 15.0 13.4 14.1 19.2 16.9 16.6 14.8 14.9 12.5 13.2 15.7 14.4 12.2 9.4 12.7 14.9 166 18.1 16.6 16.8 18.4

____________________Public IIGDP 8.1 8.1 8.2 6.6 6.8 9.8 11.7 12.2 11.0 8.6 6.1 5.8 5.2 6.1 5.0 5.1 4.3 3.9 4.3 3.3 4.6 1.9 1.8 1.7 1.8 1.7 1.7 1.7

Bargladesh GDl/GDP 3.0 7.1 6.3 9.9 11.1 11.8 11.3 15.3 16.2 15.5 13.4 12.4 12.9 12.5 12.9 12.4 12.9 12.8 11.5 12.1 14.3 15.4 16.6 17.0 17.3

Privatve 1GDP 2.9 4.2 3.4 5.4 4.9 5.6 5.7 8.2 9.6 9.1 7.2 6.7 7.4 6.3 6.2 6.4 6.5 6.4 5.8 6.6 7.8 7.8 9.4 10.7 10.8

Public I/GDP 0.1 2.9 2.9 4.6 6.2 6.2 5.6 7.1 6.7 6.4 6.2 5.7 5.6 6.3 6.7 6.0 6.4 6.4 5.7 5.5 6.4 7.6 7.2 6.3 6.5

Belize GDFI/GDP 26.2 23.5 27.1 25.3 28.7 28.0 28.5 26.6 22.7 24.8 22.5 18.9 20.3 17.4 17.4 21.5 25.7 27.4 25.6 28.5 29.3 29.8 24.1 20.6 18.8 23.3

Private /GDP 17.8 15.2 14.8 16.6 18.5 16.1 11.7 9.8 11.1 13.5 9.8 8.5 11.8 8.7 8.4 13.8 17.1 17.4 11.4 8.1 10.0 16.3 13.0 12.7 12.2 12.8

Public I/GDP 8.4 8.3 12.3 8.7 10.2 11.9 16.8 16.8 11.5 11.3 12.7 10.4 8.6 8.7 9.0 7.7 8.6 10.0 14.2 20.4 19.3 13.5 11.1 7.9 6.6 10.5

Bernin CiD1IGDP 13.4 13.5 13.3 1ISfI 35.5 17.3 16.6 1S. 5

Private I/GDP 6.0 6.1 6.7 7.9 6.2 6.9 9.1 11.0

Public 1/GDP 1.4 7.4 6.6 7.1 9.3 10.4 7.5 7.5

BolMia c3DFIGDP 12.1 12.7 12.0 12.6 14.5 16.3 16.3 14.8 15.5 15.8 17.2

Private I/GDP 5.9 4.0 3.6 5.0 5.8 6.6 7.4 6.4 7.6 8.4 10.3

Public I/GDP 6.2 8.1 8.4 7.6 8.7 9.7 8.9 8.4 8.0 7.5 6.9

Brazil GDFI/GDP 18.8 19.7 20.2 21.4 22.8 24.4 22.5 21.3 21.8 22.8 23.6 24.3 23.0 19.9 18.9 18.0 20.0 23.2 24.3 26.9 22.9 19.6 19.6 20.4 20.7 20.5 19.1 19.6

PrivaleI/GDP 12.8 14.2 14.4 16.2 15.8 16.9 14.2 14.7 14.1 12.5 17.0 16.6 16.0 13.8 13.7 12.9 14.4 16.8 17.9 21.1 17.6 14.4 13.9 155 15.8 16.8 15.3 15.8

Public I/GDP 6.0 5.5 5.8 5.2 7.0 7.5 8.3 6.6 7.7 10.3 6.6 7.7 7.0 6.1 5.2 5.1 5.6 6.4 6.4 5.8 5.3 5.2 5.7 4.9 4.9 3.7 3.9 3.8

Bulgaria GDFI/GOP 24.4 18.2 16.2 13.0 13.8 15.3 13.6 11.3

Private 1/CIDP 0.9 0.5 0.3 2.9 5.4 6.8 5.3 4.8

Public I/GDP 23.5 17.7 15.9 10.0 8.4 8.5 8.4 6.5

Chile GDFI/CiODP 16.4 14.5 12.2 7.9 21.2 13.9 12.8 14.5 17.8 17.8 16.6 18.6 14.2 12.0 12.4 16.8 17.1 19.4 20.3 23.0 23.1 19.9 22.4 24.9 23.3 23.9 24.8 25.2

Private I/GDP 9.5 6.5 4.5 0.5 9.2 3.2 4.8 7.6 11.4 12.6 11.2 13.4 9.5 7.4 6.4 14.1 13.6 13.1 14.4 18.2 18.4 15.0 16.7 18.9 18.0 19.9 19.6 20.4

Public 1/GDP 6.9 8.0 7.7- 7.4 12.0 10.7 8.0 6.9 6.4 5.2 5.4 5.2 4.7 4.7 6.0 2.8 3.5 6.4 5.9 4.8 4.8 4.9 5.8 6.0 5.3 3.9 5.2 4.8

China GDFIIGDP 20.2 19.8 23.2 24.1 25.6 28.4 30.6 31.7 31.8 26.1 24.4 25.9) 30.3 37.7 36.4 34.2 33.8 33.4

Private IKIDP 3.7 6.0 7.3 8.1 9.0 9.6 10.2 11.2 11.6 9.5 8.3 8.7 9.7 14.9 15.9 15.6 16.1 15.8

Public I/GDP 16.5 13.7 16.0 16.0 16.5 18.7 20.4 20.5 20.2 16.6 16.1 17.2 20.6 22.9 20.6 18.6 17.7 17.5

Colombia GDFI/GDP 18.0 17.5 16.1 15.8 16.4 15.3 15.9 14.3 15.4 15.4 16.8 17.7 17.5 17.2 17.0 17.5 17.7 17.4 19.5 18.1 16.6 14.6 15.6 18.8 20.5 19.7 17.2 16.9

Private I/GDP 12.4 11.6 9.8 10.1 11,5 9.9 10.3 7.9 9.9 10.0 9.8 10.3 9.4 9.7 8.5 8.4 9.2 10.2 11.5 10.2 10.2 8.3 8.6 10.8 13.3 12.0 8.2 10.0

Public JYGDP 5.6 6.0 6.3 5.7 4.9 5.4 5.6 6.6 5.5 5.4 7.0 7.3 8.1 7.5 8.5 9.2 8.5 7.3 8.0 7.8 6.4 6.3 7.0 8.0 7.1 7.7 8.9 6.9

Costa Rica GDFI/GDP 19.4 22.1 21.9 20.5 21.3 20.7 23.5 22.4 23.0 26.2 23.9 24.1 20.3 18.0 20.0 19.3 18.7 19.8 18.9 20.5 22.4 19.7 20.8 23.2 19.8 19.3 18.4 19.5

Private IIGDP 15.0 16.4 15.1 14.7 15.8 14.4 15.1 14.2 15.6 17.3 14.7 15.2 13.1 11.6 13.7 12.3 12.8 15.4 14.8 16.0 17.7 15.5 16.6 18.3 15.0 14.8 14.0 15.0

__________________ Public IIGDP 4.4 5.7 6.8 5.8 5.5 6.3 8.4 8.2 7.4 8.9 9.2 8.9 7.2 6.4 6.4 7.0 5.8 4.4 4.1 4.5 4.7 4.2 4.1 4.9 4.9 4.4 4.4 4.5

M6e d¶lvoiee GDFI/GDP 14.8 14.1 13.8 12.2 8.5 8.6 8.5 7.8 11.1 12.9 13.9 16.0

Private I/GDP 7.9 6.7 6.8 5.9 4.9 5.1 4.7 4.1 7.0 8.7 9.6 11.2

__________________Public I/GDP 6.9 7.4 7.0 6.3 3.6 3.4 3.8 3.7 4.1 4.2 4.3 4.8

Domirica Republic GDFI/GDP 19.1 17.9 19.8 22.2 23.3 24.5 22.3 21.7 21.0 23.9 23.9 22.8 18.7 20.3 21.0 18.3 20.6 26.0 27.1 28.2 24.9 21.6 22.2 26.4 25.9 23.9 24.2 24.7

Private I/GDP 14.0 12.4 12.2 15.1 15.9 16.5 16.0 15.6 14.8 18.8 16.3 16.1 14.3 15.6 17.6 12.9 16.0 16.2 16.8 18.1 18.2 15.3 15.1 17.9 17.3 16.8 17.1 20.5

____________________PubIicI/GDP 5.1 5.5 7.6 7.1 7.4 8.0 6.3 6.1 6.2 5.1 7.6 6.7 4.4 4.7 3.4 5.4 4.6 9.7 10.3 10.2 6.7 6.3 7.1 8.5 8.6 7.1 7.1 4.2

Ecuador GDFI/GDP 16.7 21.8 18.0 17.6 18.2 23.2 22.2 23.6 26.2 23.7 23.6 22.3 22.7 16.6 15.4 16.1 -18.8 22.7 21.3 20.7 18.4 19.7 19.5 19.9 18.8 18.6 17.8 19.0

Private I/GDP 10.0 14.7 11.4 10.8 10.2 14.5 13.0 13.4 16.8 14.5 14.1 11.7 13.0 8.6 9.0 9.5 9.6 13.4 12.7 11.6 12.4 12.6 12.4 13.2 12.8 13.1 11.7 13.3

Public IIGDP 6.7 7.1 6.6 6.8 8.0 8.7 9.2 10.2 9.4 9.2 9.5 10.6 9.7 8.0 6.4 6.6 9.2 9.3 8.6 9.2 6.1 7.0 7.1 6.7 6.0 5.5 6.1 5.7

Egypt GDFI/GDP 30.1 34.2 32.1 32.1 34.4 27.4 34.5 30.6 26.9 22.2 19.1 16.2 16.6 16.2 16.0 17.6

Private I/GDP 9.1 13.9 13.1 12.7 13.2 10.1 13.3 16.0 16.7 13.1 10.5 9.2 10.5 10.7 10.5 12.1

__________________Public I/GDP 21.0 20.3 19.0 19.4 21.3 17.3 21.2 14.6 10.2 9.2 8.5 7.1 6.1 5.5 5.5 5.6

El Sahlvaor GDIGP 10.7 11.2 14.1 12.4 14.2 23.0 20.1 21.2 21.4 17.6 13.6 13.6 12.6 11.6 11.5 12.0 13.1 13.6 12.6 13.3 13.7 15.2 17.2 17.8 18.5 18.7 15.8 15.7

PGrDivFate G/DGPDP 8.4 8.3 10.1 8.8 9.5 15.0 13.9 13.9 15.6 11.5 6.4 6.2 6.5 7.0 7.6 8.7 10.6 10.7 9.5 9.8 11.2 12.3 13.2 13.7 14.7 15.1 11.6 12.1

Public IIGDP 2.3 2.9 4.0 3.6 4.7 8.0 6.2 7.3 5.8 6.1 7.1 7.3 6.1 4.6 3.9 3.3 2.5 2.9 3.1 3.5 2.5 2.8 4.0 4.0 3.7 3.6 4.1- 3.6

Guatemala GDIIGDP 12.6 13.3 13.0 13.9 14.8 15.6 20.6 18.9 20.0 18.7 16.4 16.8 15.0 10.5 9.6 11.0 10. 1 12.4 13.4 13.7 13.0 12.2 15.6 16.1 14.2 14.5 13.3 13.9

Private IGDP 10.2 10.4 9.8 10.5 11.9 12.1 14.0 13.0 14.4 12.4 t0.5 8.9 8.9 6.6 6.7 8.8 8.1 9.7 10.5 10.6 10.3 9.8 13.2 13.3 11.8 12.2 10.9 11.1

___________________Public L'GDP 2.4 2.9 3.2- 3.4 2.9 3.5 6.6 5.9 -5.6 6.3 5.9- 7.8 6.1 3.9 2.9 2.1 1.9 2.7 2.9 3.2 2.7 2.4 2.4 2.7 2.4 2.3 2.4 2.8

Guinea-B3inaa GDFI/GDP 35.2 44.7 39.0 29.9 31.0 48.3 30.9 21.8 22.3 18.9 24.8

Private ItGDP 7.3 14.1 8.7 8.4 7.8 20.0 6.3 1.4 7.1 4.2 9.2

__________________ Public 1/GDP 27.9 30.6 30.3 21.5 23.2 28.3 24.6 20.4 15.2 14.8 15.6(continued.. .i)

Table 1. (contiued)

Cpimtry/Year- - 1970 1971 1972 1973 1974 1975 1976 1977 1979 1979 1980 1991 1982 1993 1984 1985 1986 1997 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997

India GDFVGDP 13.1 16.4 16.9 15.3 15.7 17.9 19.1 19.2 19.3 19.8 193 19.7 20.1 19.3 19.7 20.7 21.2 21.7 21.6 22.5 23.2 22.1 22.5 20.9 21.4 23.8 23.2 22.9

Private I/GDP 8.1 9.9 9.3 8.5 9.6 10.3 10.3 10.6 10.7 10.5 10.7 10.6 9.6 9.4 9.6 10.2 9.9 11.3 11.6 12.9 13.8 12.6 14.0 13.1 12.9 16.3 16.6 16.1

Pubhc FGDP 5.0 6.5 7.6 6.8 6A 7.6 9.8 8.6 8.6 9.3 9.6 9.1 10.4 9.9 10.1 10.5 11.4 10.4 10.1 9.6 9.4 9.5 8.5 7.8 9.6 7.5 6.6 6.8

Indonesia GDFVGDP 24.2 30.5 25.1 22.5 23.6 24.2 24.9 26.1 3 28.4 28.1 27.3 25.9 27.8 28.4 29.6 28.4

Privato IIGDP 13.7 18.2 13.2 12.5 13.5 16.2 17.3 17.7 18.7 19.2 19.5 17.7 16.1 18.1 22.5 23.9 22.1

Pubfiv I/GDP 10.5 12.3 IL9 9�9 10.1 8.0 7.5 8.4 8.6 9.3 9.6 9.5 9.8 9.7 5.9 5.7 6.3

GDFVGDP 21.7 19.1 17.5 21.5 20.9 17.5 15.4 13.3 13.3 13.3 15.5 21.6 22.0 22.1 23.3 23.7 25.8 24.9

Private I/GDP 11.4 9.3 7.4 12.0 12.4 10.6 9.6 7.8 7.9 8.2 8.3 13.2 13.0 11.4 I2.9 13.3 14.3 13.8

Pubfic IIGDP 10.4 9.8 10.0 9.4 8.5 6.9 6.7 5.5 -5.4 5.1 7A 8.5 9.0 10�7 10.4 10.4 11.5 11.1

Ktnya GDFVGDP 19.7 22.7 22.1 20.8 19.2 20.2 20.0 21.0 25.1 23.7 23-6 23.9 19.0 18.0 19-1 17.9 19.6 19-6 20.1 19.3 20.6 19.0 16�6 16.9 I&9 21A 19�8 1&2

Pri%,21c I/GDP 13.7 14.0 13.6 11.4 10.5 11.7 11.6 12,1 15.6 12.8 13.0 13.3 10.4 11.1 10.5 10.7 11.5 12.5 11.9 11.2 10.9 10.5 9.2 9.6 9.9 13.5 12.3 11.3

Pubho l/GDP 6.0 8.7 8.5 9.4 9.7 8.5 9.4 8.9 9.5 10.9 10.7 10.6 8.6 6.9 7.5 7.2 9.1 7.1 8.3 9.1 9.7 8.5 7.3 73 9.0 7.9 7.5 7.0

Koma, Rep. of GDFJ/GDP 20.4 23.0 25.4 25.0 24.0 26.9 30.9 32.7 32.1 29.0 29.4 29.2 28.9 29.6 29.2 29A 29A 31-9 37.1 39.4 36.6 36.0 35-7 36.6 36.9

Pxivato 11GDP 13.9 18.0 20.5 19.3 18.8 20.7 24.5 25.8 24.3 20.3 21.2 22.7 22.4 21.3 21.3 23.3 24.1 25.9 29.6 29.5 27.3 27.2 27.0 27.8 27.1

Pubfic I/GDP 6.5 5.0 4.9 5.7 5.2 6.2 6.4 6.9 7.8 7.7 7.2 6.5 6.5 7.3 6.9 5.7 5.5 6.0 7.4 9.0 9.3 8.8 8.7 8.8 9.9

Madag- GDFI/GDP 9.5 9.0 10.1 13.3 13.4 14.2 10.6 II.S 11.4 10-9 10 9 11.6 IT.5t

Privato l/GDP 2.6 3.6 3.1 6.4 3.7 6.9 4.6 3.7 3,7 4.7 4.9 5.0 5.5

Pubfic I/GDP 6.0 5.4 7.0 6.9 9.7 7.9 5.9 7.6 7.8 6.2 &O 6.7 6.3

Malawt GDFI`GDP 20A I&9 2C9 21 1 22.2 30.9 26.9 22.2 15.1 14.6 13.7 13.0 13.3 12.0 13.9 15.3 16.7 19.7 20.2 19.9 15.2 29.3 16.6 12.4 12.3

Private VGDP 7.8 7.3 7.8 8.5 9.4 12.3 7.5 4.7 4.9 6.1 5.4 3.3 5.0 2.0 5.9 7.2 9.0 11.7 11.9 9.7 6.8 14.1 7.4 5.8 5.1

Pubhe I/GDP 12.6 11.6 17.1 13.6 12.8 18.6 19.3 17.5 10.2 8.4 8.3 9.9 8.3 10.0 7.9 8.2 7.6 8.0 8.3 10.2 9.4 15.3 9.2 6.6 7.1

Malaysia GDFI(GDP 18.9 22.1 23.9 23.7 26.9 26.6 23.4 24.3 24.7 26.4 31.1 36.0 36.4 36.1 31.9 29.9 26.4 23.0 24.1 29.3 32.4 33.4 36.0 38.3 40.1 43.0 42.2 42.4

Private l(GDP 12.8 15.5 15.2 16.5 19.3 16,6 14.0 14.2 15.7 17.5 19.5 19.9 18.2 17.7 16.8 15.8 14.3 13.8 15.4 18.5 20.9 22.7 21.5 23.8 27.2 30.4 30.9 30.9

Pubho l(GDP 6.1 6.6 8.7 7.2 7.6 10.0 9.4 10.1 9.0 8.9 11.6 16.1 18.2 18.4 15.1 14.0 12.1 9.1 8.7 10.9 11.5 10.7 14.5 14.6 13.0 12.6 11.4 11.5

Mauritwua C3DFYC3DP 20.0 17.9 20.5 23.5 14.4 16.0 19.2 17.5

Pfi"te I/GDP 9.2 7.9 6.9 10A 4.8 7.4 12.1 8.6

Pubbe l(GDP 10.7 10.0 13.7 13.2 9.6 8.7 7.1 8.9

Mauritius GDFVUUP 28.4 27.7 29.3 25.7 23.3 22.0 17.9 18.0 18.0 18.7 19.7 21.6 28.7 26.5 31.2 29.9 27.8 29.4 30.8 24.3 2 W.-1 27.2

Private IIGDP 20.3 19.9 18.3 17.7 14.9 13.5 11.5 11.6 12.3 12.6 12.8 14.3 16.6 19.5 19.7 20.7 19.2 20.6 21.7 16.3 16A 20.0

Public. I(GDP 8.1 8.8 10.0 8.0 8.4 8.5 6.4 6.4 5.7 6.0 7.0 7.3 12.2 7.1 11.5 8.2 9.6 7.9 9.1 8.0 9.3 7.2

mmdco GDFI/GDP 19.8 17.8 18.9 19.2 19.9 21.4 21.0 19.7 21.2 23.7 24,8 26.3 23.0 17.5 18.0 19.2 19.6 18.5 19.5 17.2 17.9 19.6 19.6 19.6 19.4 16.2 19.0 19.6

Private I/GDP 13.2 13.2 12.8 11.7 12.3 12.4 12.8 11.9 12.8 13.5 13.9 14.3 12.8 11.0 11.4 12.5 13.0 13.3 14.1 13.0 13.6 14.6 15.8 14.8 15.6 12.8 14.2 16.0

Pubhc FGDP 6.6 4.6 6.1 7,5 7.6 9.0 8.2 7.8 8.4 10.2 10.9 12.1 10.2 6.6 6.6 6.7 6.6 5.2 4.4 4.2 4.3 4.1 3.8 3.8 3.8 3.3 3.9 3.6

Morocco GDFl1GDP 24.8 29.7 32.0 24.9 24.0 22.2 26.0 27.3 24.4 23.1 23.1 21.3 20.2 19.3 22.8 25.4 22.2 22.5 22.1 20.5 22. 19.6 20.7

Private I/GDP 9.8 12.9 14.5 13.5 11.4 11.9 11.4 13.4 11.9 11.2 12.1 12.2 11.6 11.9 13.2 14.5 11.8 11.3 7.7 7.7 10.6 10.2 11.0

Public I/GDP 15.0 16.7 17.5 11.4 12.6 10.4 14.5 13.9 12.6 11.9 11.0 9.1 8.6 7.6 9.6 10.8 10.5 11,2 14.4 12.8 11.4 9.4 9.7

Nambia GDFVGD? 26.0 26.0 21.7 17.4 14.5 13.7 13.3 13.9 14.9 16.1 20.4 15.6 20.2 21.6 21.0 21.6 23.5 20.7

Private ItGDP 10.9 9.7 6.9 6.1 5.9 4.9 5.7 6.5 7.9 10.4 12.6 8.2 10.5 13.4 12.7 14.0 15.5 12.9

Pubfic. I/GDP 15.1 16.3 14.9 11.3 9.6 9.9 7.6 7.5 6.9 5.7 7.8 7.3 9.7 8.1 8.3 7.6 9.0 7.8

GDFLIGDP 20.4 19.3 19.5 18,9 22.1 24.0 29.0 31.6

Privatc VGDP 11.2 10.7 9.7 8.9 9.8 10.6 14.1 19.8

Public VGDP 9.3 7.6 9.8 10.0 12.4 13.4 14.9 11.8

Paldstan GDFI/GDP 14.3 14.0 12.6 11.5 12.2 I4.4 18.2 19.6 17.3 17.0 17.1 17.1 16.8 17.0 16.5 16.5 17.0 17.5 16.5 17.3 17.3 17.4 18.6 19.1 17.9 16.9 17.0 15.8

Private I/GDP 7.3 7.0 6.6 5.6 4.4 4.6 5.9 6.2 5.8 5.8 7.7 7.8 7.2 7.4 7.5 7.6 7.8 7.7 7.7 8.3 8.9 9.9 9.8 10.0 9.6 9.7 8.9 8.9

Public I/GDP 7.0 7.0 6.0 5.9 7.9 9.8 12.3 12.4 11.5 11.2 9.4 9.4 9.7 9.6 9.0 9.9 9.2 9.7 8.8 9.0 8.4 8.5 8.8 9.1 9.3 8.2 8.1 6.9

Panarna GDF1/GDP 19.3 9.8 6,5 8.5 15.0 19.3 23.8 24.2 24.9 25.1 26.4

Private VGDP 16.8 5.7 4.5 7.4 12.0 15.1 19.9 20.8 21.5 21.3 22.0

Pubfic VGDP 2.4 3.1 2.0 1.1 3.0 3.1 4.0 3.4 3.4 3.8 4.4

Papua New Guinea GDFI/GDP 26.9 33.0 29.7 23.9 18.4 21.0 19.3 23.3 26.0 25.1 28.0 23.8 19.8 13.9 22.3 27.6 37.0

Privatt IIGDP 18.1 26.1 23.6 17.6 12.1 14.5 14.0 18.3 21.2 20.0 23.3 18.6 12.5 11.1 19.0 24.0 31.5

Pubfic VGDP 8.7 6.9 6.1 6.2 6.3 6A 5.3 5.0 43 5.1 4.7 5.2 6.3 2.9 3.4 3.6 5.6

Paraguay GDFI/GDP 14,8 14.0 15.5 15.6 17.9 19.9 22.7 23.8 25.2 27.0 27.2 27.4 24.0 20.1 21.6 20.7 23.5 23.7 23.1 22.7 21.0 22.0 19.8 19.6 22.5 23.1 22.5 22.7

Pfivate LIGDP 10.8 10.3 11.0 12.3 15.2 15.7 13.5 15.2 17.9 20.7 22.4 216 19.5 13.3 13.2 14.2 18.5 17.6 16.3 16.0 18.2 18.7 16.1 15.4 19.0 17.7 19.1 15.4

Public I/GDP 4.0 3.7 4.5 3.3 2.7 4.2 9.2 8.6 73 6.3 C9 CS C5 6.9 9.4 6.5 5.1 6.1 6.9 6.7 2.9 3.3 3.7 3.2 3.5 5.3 4.4 7.3

(confmued /)

Table 1. (contlued)

country/Yewr 1970 1971 1972 1973 1974 1975 1976 1977 1978 1979 1980 1981 1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997

Peru GDFI/GDP 28.8 29.5 23.7 20.2 18.2 18.5 17.8 19.7 16.6 14.7 14.5 15.2 16.8 21.0 23.5 23.5 24.8

PTivate VIGDP 21.5 20.8 15.1 12.1 12.0 13.2 13.4 15.5 13.1 12.2 11.7 12.0 13.4 16.9 19.5 19.6 21.0

Public 1/GDP 7.3 8.7 8.7 8.1 6.1 5.4 4.4 4.2 3.5 2.5 2.7 3.1 3.4 4.0 4.0 3.9 3.9

Philippines GDFI/GDP 24.7 26.4 25.1 25.2 27.5 27.2 27.8 27.5 29.8 24.5 17.5 16.8 16.5 17.8 20.8 23.1 20.0 20.9 23.8 23.6 22.2 23.4 24.5Private I/GDP 20.6 16.1 17.9 18.2 20.1 18.8 16.8 20.0 23.7 19.1 13.7 14.0 13.7 14.9 17.3 18.9 15.9 16.0 18.8 18.7 17.6 18.8 20.9Pubhic lGDt' 4.1 10.3 7.2 7.0 7.4 8.5 10.9 7.5 6.1 3.4 3.7 2.8 2.8 2.9 3.6 4.2 4.1 4.9 3.0 4.9 4.6 4.6 3.6

Poland GDFV/GDP 16.0 20.7 20..8 17.5 15.8 16.1 19.3 17.0 19.3

Privat I/GDP 2,7 8.5 12.3 7.7 6.8 7.1 6.8 7.8 10.3Pubiic 1/GDP 13.3 12.1 8.5 9.8 9.1 9.0 12.5 9.2 9.0

Romania GDFI/GDP 14.2 14.7 14.1 16.1 18.0 19.3 15.4Privat I/GDP 1.4 2.8 4.3 6.7 8.5 9.4 6.2

_________________Public I/GDP 12.9 11.9 9.8 9.4 9.6- 9.9 9.2

south Africa GDFI/GDP 24.7 26.2 26.9 25.4 25.1 29.4 30.1 28.0 26.4 26.2 26.2 27.8 27.9 26.8 24.4 23.3 20.2 18.5 19.8 20.6 19.6 17.8 16.6 15.5 16.1 16.9 17.2 17.4Private I/GDP 14.1 14.5 14.0 13.5 13.4 14.8 14.7 13.7 13.0 12.7 13.3 15.5 15.9 15.6 14.6 13.1 11.6 11.2 13. 2 13.2 12.9 11.9 11.4 10.8 11.7 12.6 12.6 12.7

Public I/GDP 10.6 11.7 12.8_ 11.9 11.7 14.6 15.5 14.3 13.4 13.5 12.9 12.3 12.0 11.2 9.9 10.2 8.6 7.3 6.7 7.4 6.8 5.9 5.2 4.7 4.4 4.3 4.6 4.7

Thailand GDFIIGDP 23.8 23.3 22.7 22.4 23.3 22.9 22.9 26.0 25.3 25.6 27.8 28.0 26.9 28.5 28.6 27.2 25.8 27.6 30.7 34.6 40.4 41.6 39.3 39.5 40.0 41.1 41.1 35.6

Private IfGDP 16.7 16.6 16.0 17.3 19.6 17.7 16.1 18.6 17.6 18.0 18.9 19.0 19.1 20.5 20.3 18.5 15.4 21.7 25.6 29.6 34.2 34.4 31.1 31.6 31.3 32.2 30.8 24.1Public ItGDP 7.1 6.7 6.7 5.1 3.7 5.2 6.8 7.4 7.7 7.6 8.8 8.9 7.9 8.0 8.3 8.7 7.4 6.0 5.0 5.0 6.1 7.2 8.1 7.9 8.7 8.9 10.2 11.5

Tunisia GDFI/GDP 20.4 19.8 19.8 20.5 20.8 25.7 29.0 30.7 30.9 30.5 28.3 31.0 34.0 31.8 32.1 28.1 25.0 21.6 20.5 22.5 24.4 24.1 24.6 25.5 24.9 24.2 23.2 24.5

PrivateIVGDP 8.5 7.7 8.8 10.7 10.5 12.3 11.6 10.9 11.7 12.0 13.3 14.8 15.4 15.9 15.7 14.5 12.1 11.1 11.3 12.4 12.3 12.7 13.2 12.7 13.1 12.3 11.8 12.4

__________________Public I/GDP 11.9 12.1 11.0 9.8 10.3 13.4 17.4 19.8 19.2 18.5 15.0 16.2 18.6 16.0 16.4 13.7 12.8 10.5 9.3 10.1 12.0 11.4 11.4 12.8 11.8 11.9 11.4 12.1

Turkey GDF1/IDP 22.5 20.2 21.7 21.4 19.9 22.1 24.4 25.7 23.1 21.9 22.1 20.1 19.4 20.1 19.5 20.3 22.8 24.7 26.1 22.8 22.9 23.8 23.6 26.5 24.6 23.8 25.0 26.1

Privat 1/GDP 12.6 11.6 13.0 12.9 11.3 11.7 13.2 13.2 12.4 10.7 13.3 11.0 11.1 11.4 11.4 11.1 12.6 14.7 17.2 15.2 15.6 16.2 16.2 19.3 18.9 19.9 20.3 20.5_________________Public I/GDP 9.9 8.6 8.7 8.5 8.6 10.4 11.2 12.5 10.7 11.2 8.8 9.2 8.3 8.7 8.1 9.2 10.2 10.0 8.9 7.6 7.3 7.6 7.4 7.3 5.7 3.9 4.7 5.6

ruguay GDFIIGDP 11.8 11.5 9.8 9.0 10.3 13.3 15.5 15.2 16.0 16.2 16.7 15.7 15.1 13.7 10.9 9.6 9.9 11.4 1 1.9 11.6 10.8 11.9 12.5 13.8 12.8 11.5 11.8 12.0

Private I/GDP 8.8 8.3 7.5 7.1 7.7 8.7 9.0 8.2 8.0 9.7 11.4 10.7 7.9 8.6 6.4 6.1 6.2 7.4 7.9 7.2 7.7 7.8 9.0 9.5 8.3 8.2 8.4 8.6Public, l/GDP 3.0 3.2 2.3 1.9 2.6 4.6 6.5 7.0 8.0 6.5 5.3 5.0 7.2 5.1 4.5 3.5 3.7 4.0 4.0 4.3 3.1 4.1 3.4 4.3 4.5 3.3 3.4 3.3

Venemuela GDFI/CGDP 16.0 17.3 20.4 21.2 22.8 16,9 14.1 18.2 21.1 20.0 17.6 16.1 14.8 16.9

Private I/GDP 10.5 11.1 10.9 12.1 12.3 7.2 4.9 7.6 8.9 9.0 8.2 6.7 5.1 7.4__________________Public I/GDP 5.5 6.2 9.5 9.1 10.5 9.7 9.2 10.6 12.2 11.0 9.4 9.4 9.7 9.5

East Asia GDFIIGDP 21.3 22.7 22.3 23.0 25.2 24.8 24.2 25.6 26.5 28.0 27.7 27.2 29.4 28.9 26.5 24.8 24.7 24.6 26.2 28.0 30.1 30.8 30.6 31.4 31.1 32.6 33.5 33.5

Pri-a,eL/GDP 14.8 16.1 15.0 17.3 19.8 18.6 16.3 17.9 19.0 20.4 17.0 16.3 18.6 18.5 16.8 14.9 15.6 16.4 18.2 20.1 21.6 21.9 20.3 20.7 21.3 23.6 24.5 24.2

Public YGrDP 6.6 6.7 7.3 5.8 5.4 6.2 7.9 7.7 7.5 7.7 10.7 10.9 10.8 10.4 9.7 9.8 9.1 8.1 8.0 7.9 8.5 8.9 10.3 10.8 9.8 9.0 9.0 9.3

South Asia GDFIIGDP 13.7 15.2 14.8 9.9 11.7 12.9 15.7 16.3 16.1 16.0 17.2 17.7 17.5 16.5 16.2 16.7 16.9 17.3 16.9 17.6 17.8 17.0 17.7 18.1 18.2 19.1 19.1 18.7

Private IIGDP 7.7 8.5 8.0 5.7 6.1 6.1 7.2 7.2 7.4 7.3 8.9 9.3 8.6 8.0 7.9 8.4 8.0 8.4 8.6 9.2 9.7 9.1 10.1 10.3 10.1 11.5 12.1 11.9

Publicll/GDP 6.0 6.8 6.8 4.3 5.6 6.8 8.6 9.1 8.8 8.7 8.4 8.4 8.8 8.6 8.3 8.3 8.9 8.9 8.3 8.3 8.0 7.9 7.6 7.8 8.1 7.6 7.0 6.7

LAC GDF7/GDP 16.6 16.9 17.4 16.7 19.0 20.5 21.1 20.9 21.7 21.7 21.2 21.8 20.0 17.2 16.9 16.6 17.5 18.8 18.8 18.3 17.5 17.7 18.9 20.1 20.0 19.6 19.3 20.5

Private I/GDP 11.5 11.6 11.5 11.1 12.5 13.2 13.1 12.8 13.6 13.6 13.7 14.1 12.7 10.8 10.9 11.0 11.9 13.0 12.7 12.3 12.0 11.8 12.7 14.0 14.2 14.2 13.7 15.0

Public IIGDP 5.1 5.3 6.0 5.6 6.5 7.3 8.0 8.1 8.1 8.1 7.5- 7.7 7.3 6.4 6.0 5.6 5.7 5.8 6.1 5.9 5.4 5.9 6.3 6.1 5.8 5.4 5.7 5.5

SSAFR GDFTIGDP 22.2 24.4 24.5 22.2 21.1 24.8 25.2 24.7 27.7 25.6 24.3 23.0 20.2 18.8 17.6 15.9 15.5 18.3 21.3 20.5 19.8 18.3 20.3 18.6 19.0 18.0 17.9 18.4

Private I/GDP 13.9 14.2 13.8 10.9 10.4 11.4 13.8 13.5 14.8 12.7 11. 11.4 10.2 10.0 9.3 8.2 7.9 8.4 10.5 10.2 10.3 9.5 10.1 9.4 9.4 9.9 10.3 10.7

PubliCL/GDP 8.3 10.2 10.7 -11.3 10.7 13.4 11.4 11.2 12.9 12.9 12.9 11.6 10.1 8.8 8.3 7.7 7.7 9.9 10.8 10.3 9.5 8.8 10.2 9.3 9.6 8.1 7.6 7.7

Total GDFIIGDP 17.8 18.3 18.8 17.7 19.2 21.2 22.3 22.6 23.2 23.0 22.7 23.0 22.6 21.2 20.1 19.1 19.3 19.9 20.9 20.8 20.8 20.3 21.1 21.3 21.3 21.3 21.3 21.6

Total Private l/tDP 11.6 11.8 11.8 11.2 12.2 12.8 12.9 13.1 13.7 13.5 13.2 13.4 13.0 12.4 11.9 11.2 11.5 12.1 12.8 12.9 12.8 12.4 12.5 13.0 13.3 14.0 14.1 14.4

Total Public /GDP 6.2 6.6 7.0 6.5 7.0 8.4 9.4 9.6 9.4 9.5 9.5 9.6 9.6 8.8 8.2 7.9 7.8 7.8 8.1 7.9 8.0 8.0 8.6 8.3 8.0 7.4 7.2 7.1

Note: UnLless otherwise noted the sources are: national authonitie & World BankfIMF staff estansates

Data for 1996/97 are prelainernay/estimates,Chass- private investment uincludes: mnvestment by collectrv-owned units, joint-owned uniits, share-holding uniits,

foreigri-fianded iunts, Hong KongMacao-Tawn-funded units and by individuals.

Brazi - source 1990-1997: FIBU, C;entro de Escudos de Econoinia and Governo/IBRE/FGV, previous yearn World Bank.

1990-9? - privsce irvesrteent mncludes investment by enteiprises controlled by state and local rmuncipalities.

Republic ofKorea - public inestmnent = capital expenditur of consolidated nonfmancia public sector

Mexico - I S88-97 data based 008a new INGI methodology.

Morocco - up to 1990 public inrestmuent are estimtated by investment of 1 4 higgest public companies; 1990-1997 data for the whole economy.

Poland - 1 995-97 GDP includes estimates of "the gey economy"

South Africa - Source: Quarterly Bulletin of South African Reserve Bank.

Distributors ofWorld Bank Group Publications

Prirs and mitemsn aryfrom CECHREPUBLIC I1NDI EulyeooPubishinWgCo., Ltd. PERU SWEDENcountlry to countOy. Coesult your USIS. HIS Prodejn A eoPublishes Ltd. 46-. Susong-Dong Editoral Desaroltlo SA Wetnergren-Wiltoo ABlocal distrlbutor beore placing an Haveolkva 22 751 Mount Road Jegro-Gu Apartado 3824. Ica 242 OF. 106 P 0. Box 1305order. 130 00 Pgue 3 Madras - 600002 Seoul Urma1 5-171 25 Solna

Tel: (420 2) 2423 1486 Tel: (82 2) 734-3515 Tel: (SI 14) 285380 Tel: (46 8) 705-97-50ARGENTINA Fax: (420 2) 2423 114 Fax: (91 44)852-0649 Fau: (822) 732-0154 Fax: (51 14) 286628 Fax: (468) 27-00-71World Pt 877ons SA URL: http vww .ns.caV INDONESIA LEBANON PHILIPPINES E-mail: [email protected] Cua d te Buenos Aires DENMARK Pt. Indira Umited Libraine du Liban Intemationa' Booksource Center Inc. SWITZERLANDTel: (3411) 481541S6 SamfurndsLitteratur Jalan Borobudur 20 P.O. Bo 11-9232 1127-A Antipolo St, BarangaY. Ubraide Payot Service InstitubonnelFae: (54 11)48158156 RosenoemsAtel11 P.O. Box 181 Beirut Venezueb C(trres-de-Montbenon30E-mail: wpboeelrirfovia.com.ar DK-1970 Fredenksberg C Jukarta 10320 Tel:)(961 9)217944 Makabti City 1 02LausanneTel: (4535)351942 Tel: (6221) 390-4290 Fax (9619)217 434 Tel (63 2) 896 6501 6505 6507 Tel: (41 21)341-3220AUSTALIA, FIJI, PAPUJA NEW For: (45 35) 357822 Fax: (62 21) 390-4289 C-maO: hsayeghrSibrairie-du- Fax: (63 2)9896 1741 Fax (41 211 341-3235GUINEA. SOLOMON ISLANDS, URL: http:l)www.sl.cbs.dk IRAN litaincom.lb n-VANUATU, AND SAMOA iUon corn/w l 1b aiecu POLAND AD0C0 Vae DiemrenD.A. lnformabon Services ECUADOR Ketab Sara Co. Publishers Intemabonal Publishing Service EditConsTecnriqes648 Whitehorse Road Libn Mundi Khaled Eslamboli Ave., 61h Street libuncornlb Ul. Piekn 31/37 Ch. de Lacuez 41Mltcham 3132. Victona Libreda lntemacional Delafnooz Alley No. 8 MALAYSIA 00-677 Warzawa CH1807 BlonayTel: (61) 3 9210 7777 P.O. Box 17-01-3029 P0 BoX 15745-733 University of Malaya Cooperative Tel: (48 2) 628-6089 Tel: (41 21M 943 2673FPx: 161) 3 9210 7788 Joan Leon Mera 851 Tehran 15117 Bookshop, Limited FPx: (48 2) 621-7255 Fax: (41 21) 943 3605E-mail: [email protected] Qulto Tel: (98 21) 8717819:8716194 P.O. Boo 1127 C-mail. books%ipo@*ikp.atrn.esm.pi THAILANDURL: htp:l/www.dadireci.com au Tn(593 2) 521-606 (593 2) 544- Fax: (98 21) 8712479 Jalan Pantai Barnu URL: Conlrol Books SistHibUN01 E-mail: ketab-sararieda.ret.ir 59700 KuoAa Lumpur htIp://ww.ipscg.waw.plIps/exporl 3Ceal BooksDstribue onAUS'roIA Far (593 2) 504-209 Kowkab Publishem Tel (60 3) 756-5t00 PORTUGAL Sangkok 10500Gerold aind Co. E-mail librnliffiinriouid.cornec PO Box 19575-511 Funa (603) 755-4424 Livnria Portugal Tel: (66 2) 2336930-9-tiOt osem - Tehnn . et.my Apartado 2681 Rua Do Carm Fax. (66 2) 237-8321