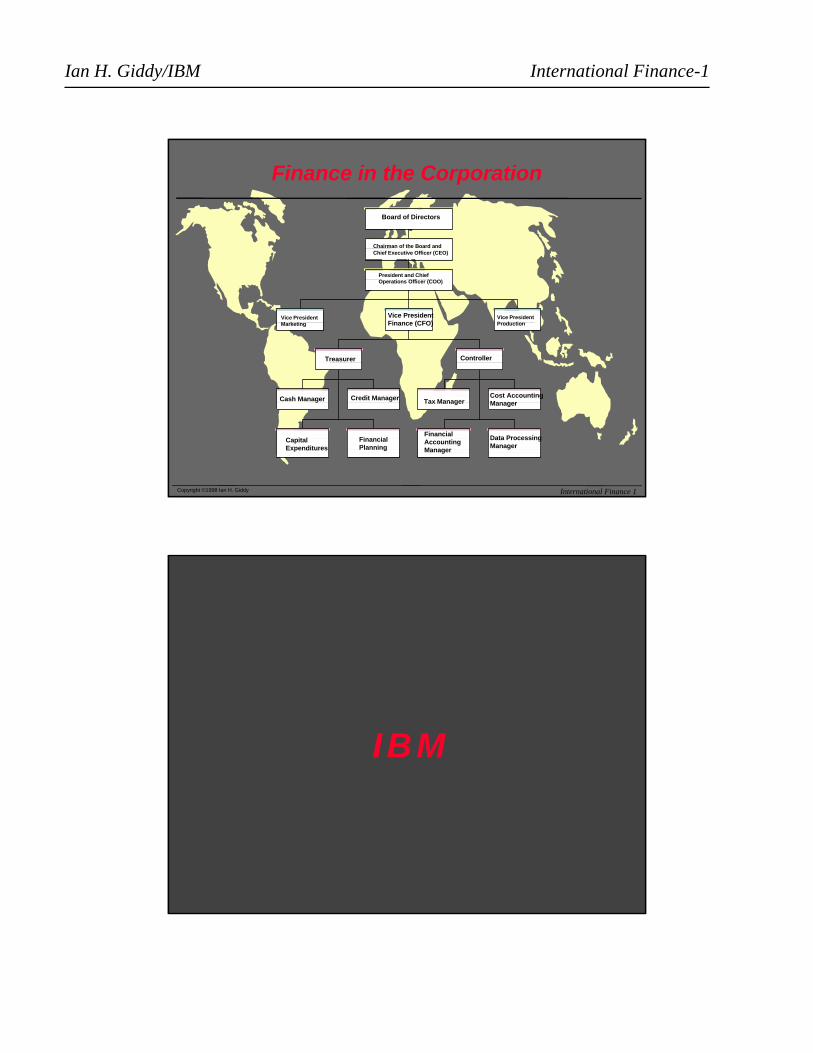

Ian H. Giddy/IBM International Finance-1 Copyright ©1998 Ian H. Giddy International Finance 1 Finance in the Corporation Chairman of the Board and Chief Executive Officer (CEO) Board of Directors President and Chief Operations Officer (COO) Vice President Marketing Vice President Finance (CFO) Vice President Production Treasurer Controller Cash Manager Credit Manager Tax Manager Cost Accounting Manager Capital Expenditures Financial Planning Financial Accounting Manager Data Processing Manager IBM

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Ian H. Giddy/IBM International Finance-1

Copyright ©1998 Ian H. Giddy International Finance 1

Finance in the Corporation

Chairman of the Board andChief Executive Officer (CEO)

Board of Directors

President and ChiefOperations Officer (COO)

Vice PresidentMarketing

Vice PresidentFinance (CFO)

Vice PresidentProduction

Treasurer Controller

Cash Manager Credit Manager Tax ManagerCost AccountingManager

CapitalExpenditures

FinancialPlanning

FinancialAccountingManager

Data ProcessingManager

IBM

Ian H. Giddy/IBM International Finance-2

Prof. I an G iddyNew Y ork University

InternationalFinance

IBM

Copyright ©1998 Ian H. Giddy International Finance 4

International Financial Markets

l Foreign exchangel The Eurocurrency marketl Cost of international borrowing

Ian H. Giddy/IBM International Finance-3

Copyright ©1998 Ian H. Giddy International Finance 5

Exchange Rates

CurrencyHowquoted

Spot(2 businessdays)

Forward(90 days)

Britishpounds(GBP)

US$perGBP

1.632 1.617

Japaneseyen (JPY)

Yen perUS$

117.5 116.3

Copyright ©1998 Ian H. Giddy International Finance 6

A Typical Forward Contract

l We agree today to pay a certain pricefor a currency in the future

SonySony B of AB of A

JPY

Ian H. Giddy/IBM International Finance-4

Copyright ©1998 Ian H. Giddy International Finance 7

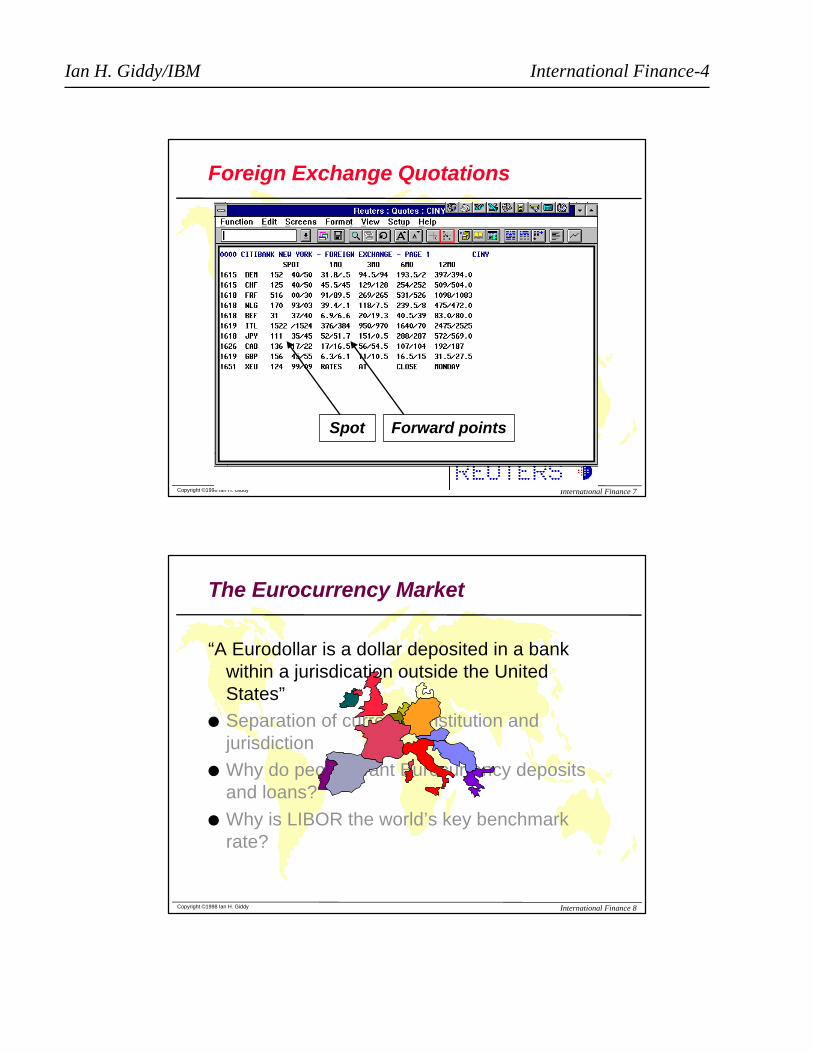

Foreign Exchange Quotations

Spot Forward points

Copyright ©1998 Ian H. Giddy International Finance 8

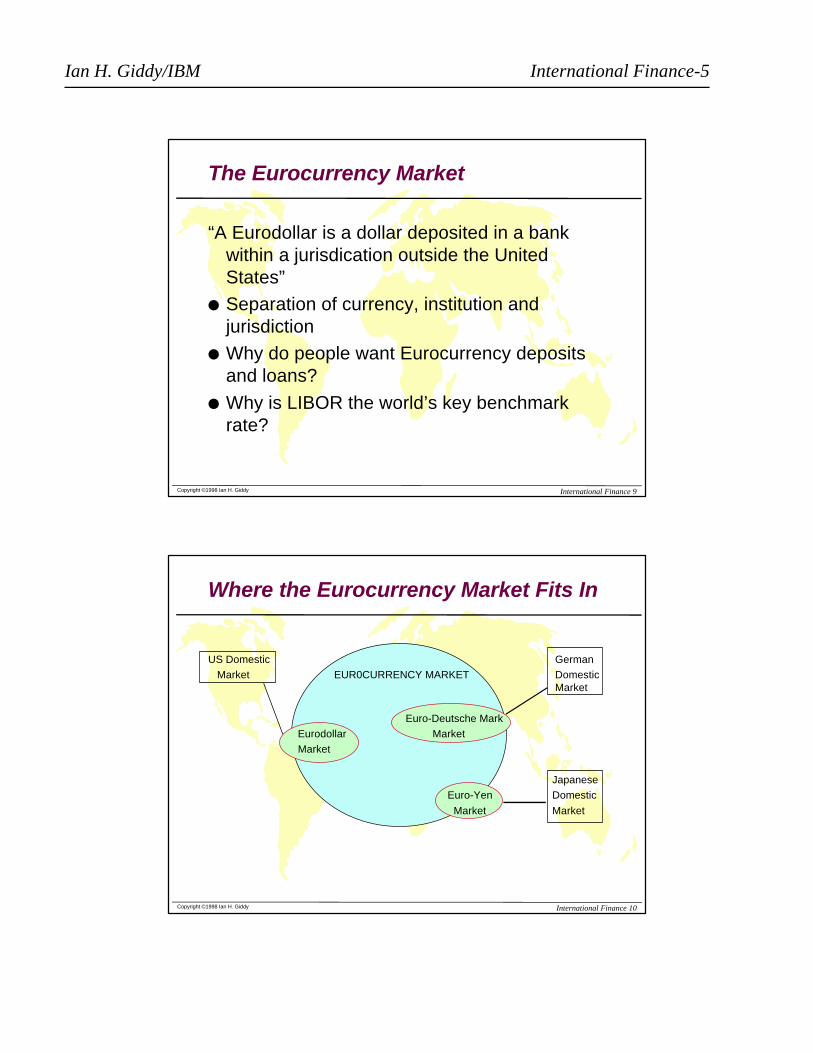

“A Eurodollar is a dollar deposited in a bankwithin a jurisdication outside the UnitedStates”

l Separation of currency, institution andjurisdiction

l Why do people want Eurocurrency depositsand loans?

l Why is LIBOR the world’s key benchmarkrate?

The Eurocurrency Market

Ian H. Giddy/IBM International Finance-5

Copyright ©1998 Ian H. Giddy International Finance 9

The Eurocurrency Market

“A Eurodollar is a dollar deposited in a bankwithin a jurisdication outside the UnitedStates”

l Separation of currency, institution andjurisdiction

l Why do people want Eurocurrency depositsand loans?

l Why is LIBOR the world’s key benchmarkrate?

Copyright ©1998 Ian H. Giddy International Finance 10

US Domestic German

Market EUR0CURRENCY MARKET Domestic Market

Euro-Deutsche Mark

Eurodollar Market

Market

Japanese

Euro-Yen Domestic

Market Market

Where the Eurocurrency Market Fits In

Ian H. Giddy/IBM International Finance-6

Copyright ©1998 Ian H. Giddy International Finance 11

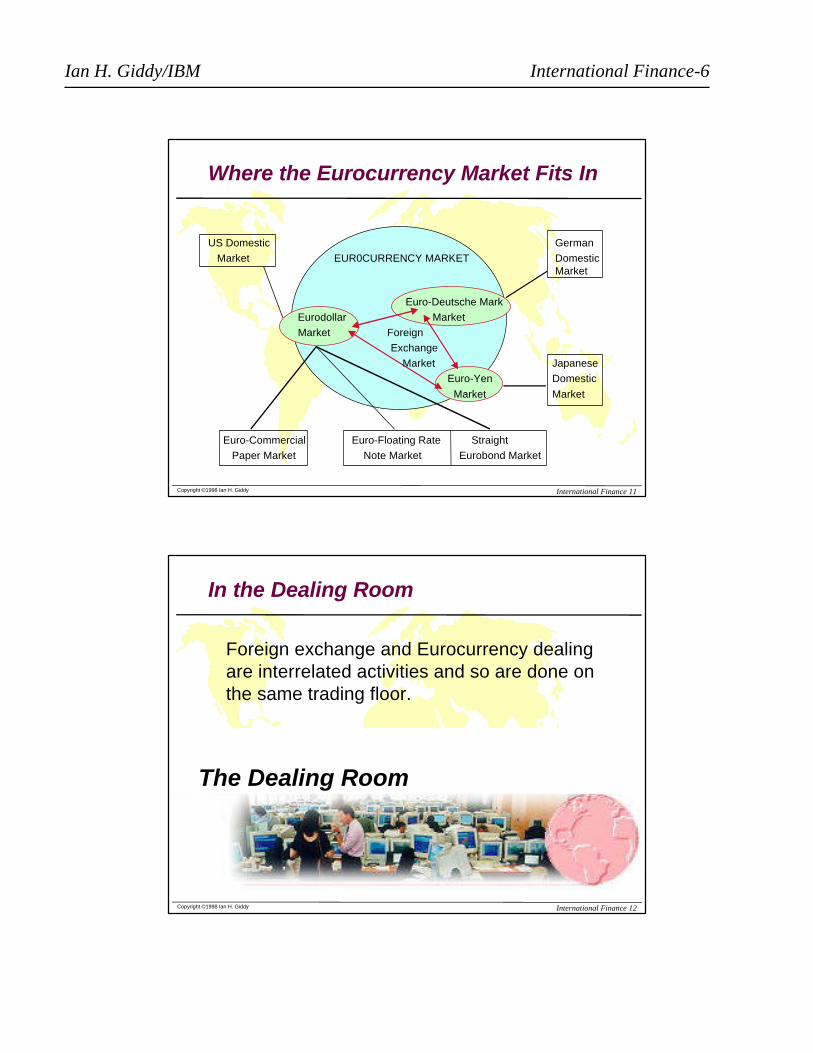

Where the Eurocurrency Market Fits In

US Domestic German

Market EUR0CURRENCY MARKET Domestic Market

Euro-Deutsche Mark

Eurodollar Market

Market Foreign

Exchange

Market Japanese

Euro-Yen Domestic

Market Market

Euro-Commercial Euro-Floating Rate Straight

Paper Market Note Market Eurobond Market

Copyright ©1998 Ian H. Giddy International Finance 12

Foreign exchange and Eurocurrency dealingare interrelated activities and so are done onthe same trading floor.

The Dealing Room

CUS- FOR- Foreign

TOMER SPOT WARD Exchange Dealing

Money

FUNDING EUROCURRENCY Market

Dealing

In the Dealing Room

The Dealing Room

Ian H. Giddy/IBM International Finance-7

Copyright ©1998 Ian H. Giddy International Finance 13

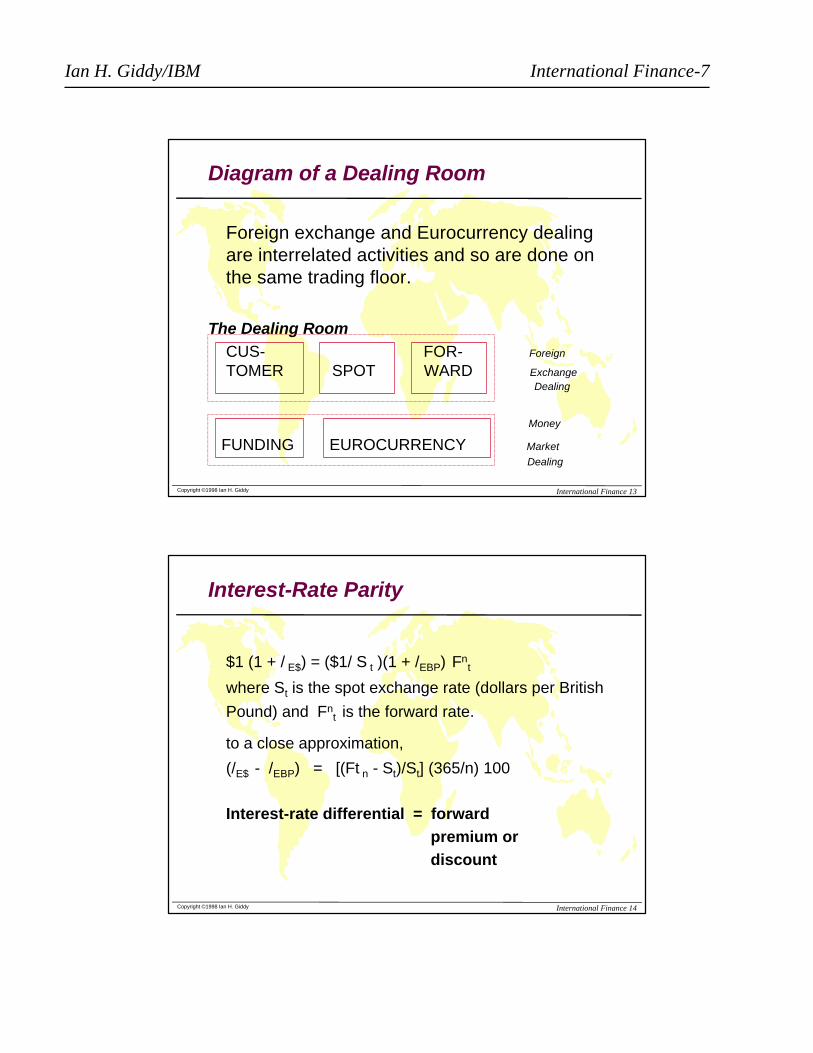

Foreign exchange and Eurocurrency dealingare interrelated activities and so are done onthe same trading floor.

The Dealing Room

CUS- FOR- Foreign

TOMER SPOT WARD Exchange Dealing

Money

FUNDING EUROCURRENCY Market

Dealing

Diagram of a Dealing Room

Copyright ©1998 Ian H. Giddy International Finance 14

Interest-Rate Parity

$1 (1 + / E$) = ($1/ S t )(1 + /EBP) Fnt

where St is the spot exchange rate (dollars per British

Pound) and Fnt is the forward rate.

to a close approximation,

(/E$ - /EBP) = [(Ft n - St)/St] (365/n) 100

Interest-rate differential = forward

premium or

discount

Ian H. Giddy/IBM International Finance-8

Copyright ©1998 Ian H. Giddy International Finance 15

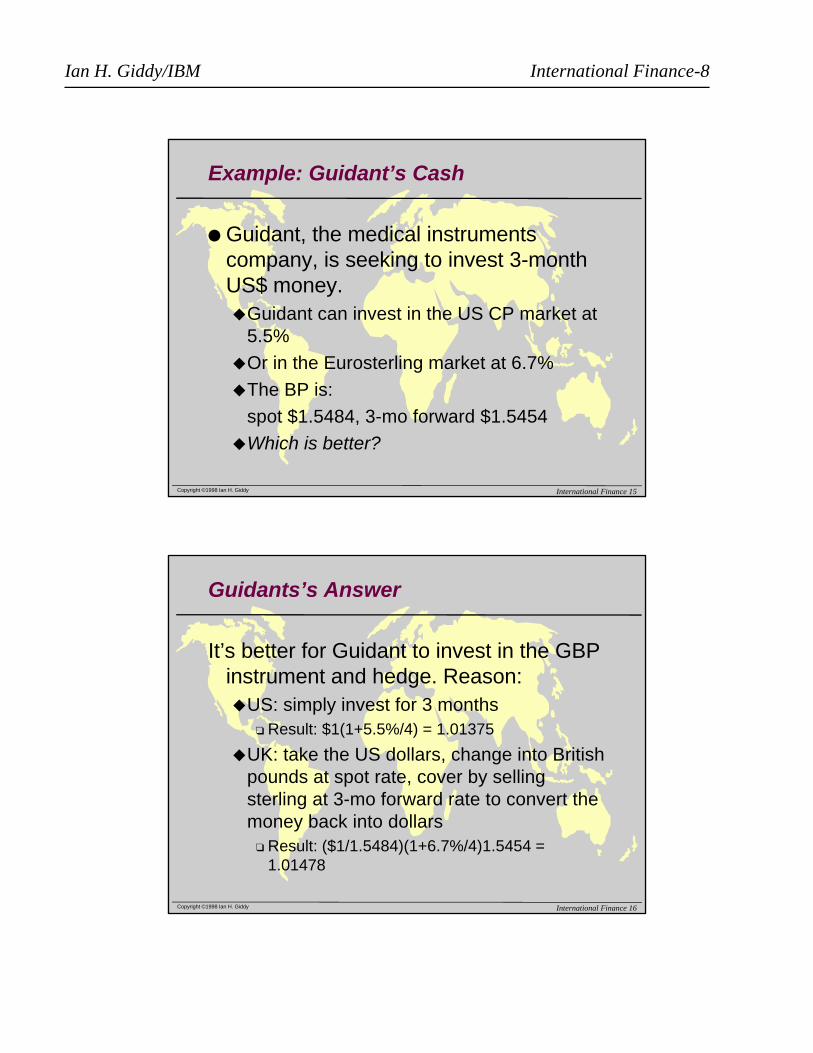

Example: Guidant’s Cash

l Guidant, the medical instrumentscompany, is seeking to invest 3-monthUS$ money.uGuidant can invest in the US CP market at

5.5%

uOr in the Eurosterling market at 6.7%

uThe BP is:

spot $1.5484, 3-mo forward $1.5454

uWhich is better?

Copyright ©1998 Ian H. Giddy International Finance 16

Guidants’s Answer

It’s better for Guidant to invest in the GBPinstrument and hedge. Reason:uUS: simply invest for 3 months

q Result: $1(1+5.5%/4) = 1.01375

uUK: take the US dollars, change into Britishpounds at spot rate, cover by sellingsterling at 3-mo forward rate to convert themoney back into dollars

q Result: ($1/1.5484)(1+6.7%/4)1.5454 =1.01478

Ian H. Giddy/IBM International Finance-9

Copyright ©1998 Ian H. Giddy International Finance 17

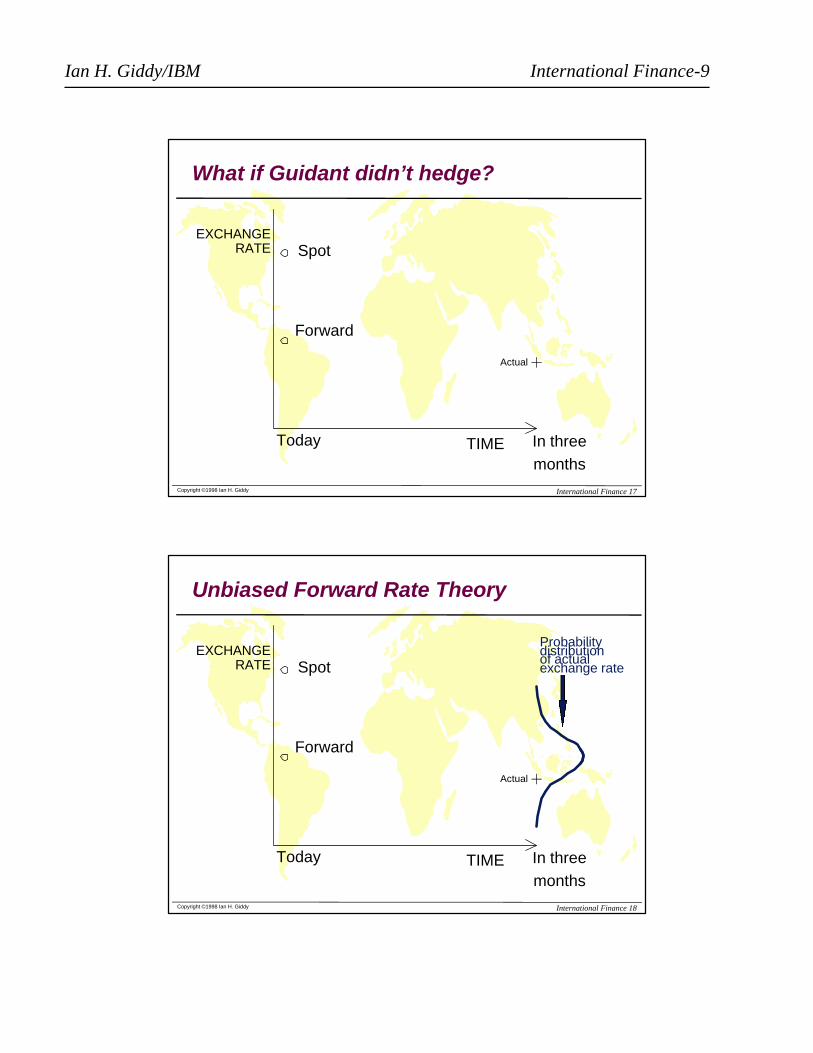

TIME

EXCHANGERATE Spot

Forward

Actual

Today In threemonths

What if Guidant didn’t hedge?

Copyright ©1998 Ian H. Giddy International Finance 18

TIME

EXCHANGERATE Spot

Forward

Actual

Probabilitydistributionof actualexchange rate

Today In threemonths

Unbiased Forward Rate Theory

Ian H. Giddy/IBM International Finance-10

Copyright ©1998 Ian H. Giddy International Finance 19

Questions on a MNC’s FinancialStructure and Cost of Capital

l Debt vs. equityuSubs

uParent

uWhole firm

l What kind of debt?uCurrency

uForm, location, ...

l Whose debt?uSub/parent/affil/guarantee

Copyright ©1998 Ian H. Giddy International Finance 20

Optimal Capital Structure?

DEBT

EQUITY

PARENTASSETS

SUB 1

SUB 2

ASSETS

WEIGHTED

AVERAGE

COST

OF

CAPITAL

LEVERAGE

Ian H. Giddy/IBM International Finance-11

Copyright ©1998 Ian H. Giddy International Finance 21

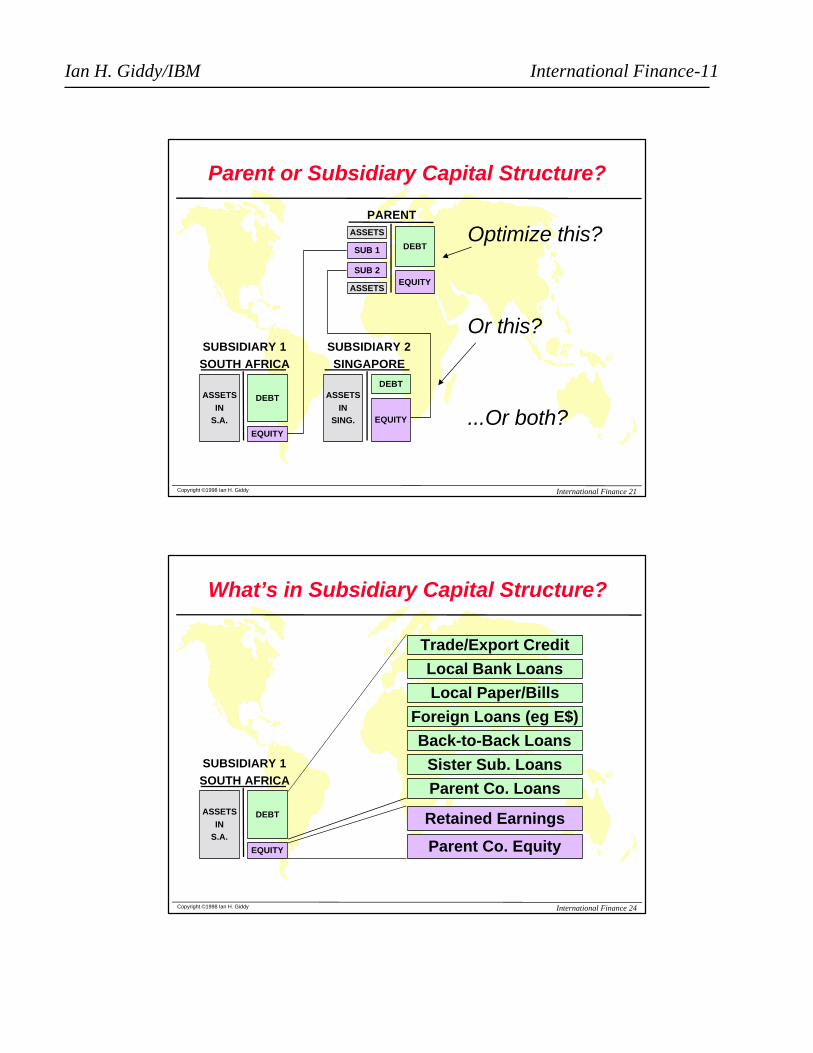

Parent or Subsidiary Capital Structure?

DEBT

EQUITY

PARENTASSETS

SUB 1

SUB 2

ASSETS

DEBT

EQUITY

SUBSIDIARY 1

SOUTH AFRICA

ASSETS

IN

S.A.

DEBT

EQUITY

SUBSIDIARY 2

SINGAPORE

ASSETS

IN

SING.

Optimize this?

Or this?

...Or both?

Copyright ©1998 Ian H. Giddy International Finance 24

What’s in Subsidiary Capital Structure?

DEBT

EQUITY

SUBSIDIARY 1

SOUTH AFRICA

ASSETS

IN

S.A.

Trade/Export Credit

Local Bank Loans

Local Paper/Bills

Foreign Loans (eg E$)

Back-to-Back Loans

Sister Sub. Loans

Parent Co. Loans

Retained Earnings

Parent Co. Equity

Ian H. Giddy/IBM International Finance-12

Copyright ©1998 Ian H. Giddy International Finance 25

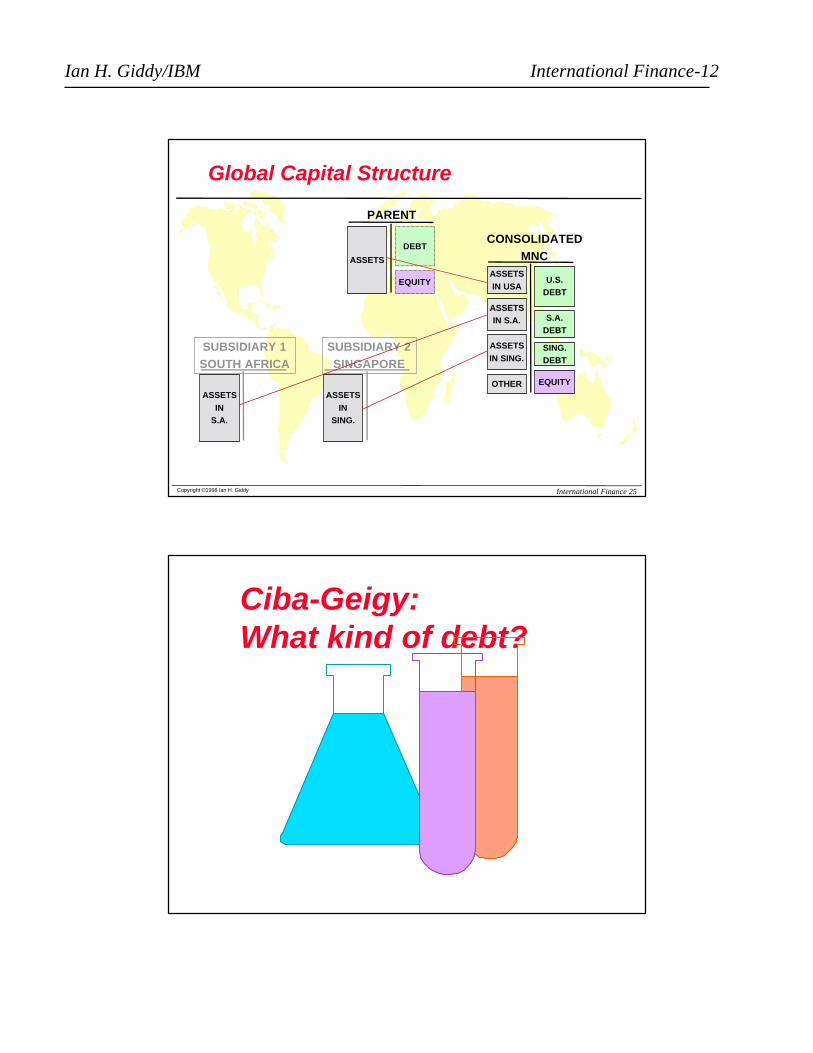

Global Capital Structure

DEBT

EQUITY

PARENT

ASSETS

S.A.

DEBT

SUBSIDIARY 1

SOUTH AFRICA

ASSETS

IN

S.A.

SING.

DEBT

SUBSIDIARY 2

SINGAPORE

ASSETS

IN

SING.

U.S.

DEBT

EQUITY

CONSOLIDATED

MNC

ASSETS

IN USA

OTHER

ASSETS

IN S.A.

ASSETS

IN SING.

Ciba-Geigy:What kind of debt?

Ian H. Giddy/IBM International Finance-13

Copyright ©1998 Ian H. Giddy International Finance 27

Short Term or Long Term?

l In 1992, Ciba had fixed assets ofSF13.9 billion and capitalexpenditures of SF1.9 billion.

l Yet the majority of Ciba's debt is in theshort-term commercial paper, bankdebt, and suppliers-credit markets.

l This suggests that if the proportion ofdebt financing as a whole isincreased, much of it should be in theform of long-term debt.

Copyright ©1998 Ian H. Giddy International Finance 28

l Geographic location of sales and capitalassets.

l Currency distribution of sales.l Nature of the company's businesses

Currency of Denomination of Ciba'sDebt? What Should It Be?

Ian H. Giddy/IBM International Finance-14

Copyright ©1998 Ian H. Giddy International Finance 29

Currency of Ciba’s Assets and Debt

Geographic distributionof

Currencydistribution

of sales Remarks on economic exposure

Estimatedcurrency

distribution ofdebt

Fixedassets Sales

Switzerland 41%

A 43%

2.4% Net short position because much ofproduction, but little of sales, here

9%

U.K.

A 27%

5.4% Part of sales effectively U.S. dollardenominated

7%

OtherEurope

34.6% 21%

U.S. andCanada

23% 32% 41.3% 54%

LatinAmerica

4% 7% 5.3% Most of sales effectively dollardenominated

2%

Asia 4% 13% 10.9% Part of sales effectively U.S. dollardenominated

6%

Rest of theworld

1% 5% Most of sales effectively dollardenominated

1%

Geographic distributionof

Currencydistribution

of sales Remarks on economic exposure

Estimatedcurrency

distribution ofdebt

Fixedassets Sales

Switzerland 41%

A

2.4% Net short position because much ofproduction, but little of sales, here

9%

U.K.

A 27%

5.4% Part of sales effectively U.S. dollardenominated

7%

OtherEurope

34.6% 21%

U.S. andCanada

23% 32% 41.3% 54%

LatinAmerica

4% 7% 5.3% Most of sales effectively dollardenominated

2%

Asia 4% 13% 10.9% Part of sales effectively U.S. dollardenominated

6%

Rest of theworld

1% 5% Most of sales effectively dollardenominated

1%

Copyright ©1998 Ian H. Giddy International Finance 30

Guidelines for Financing

l Liabilities to match assets: economicexposure of the firm determines basefinancing choices.

l Decision on whether or not to fullymatch depends on company's viewrelative to the view implied by marketprices.

l When strategy is chosen, use thefinancing/hedging techniques that offerthe lowest effective cost.

Ian H. Giddy/IBM International Finance-15

Copyright ©1998 Ian H. Giddy International Finance 31

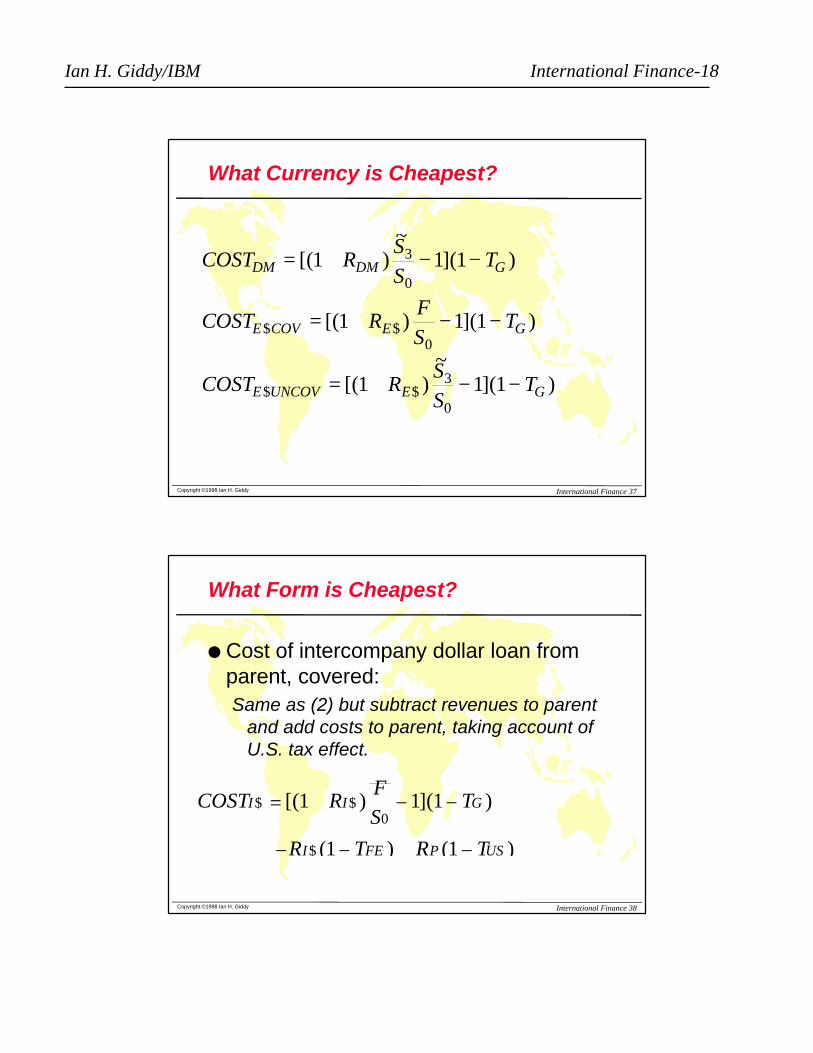

What Currency is Cheapest?

l Local currency debtl Foreign currency, hedgedl Foreign currency, unhedgedl Intercompany loan

Copyright ©1998 Ian H. Giddy International Finance 32

Case Study: Guidant Corp., Germany

l The German subsidiary of an American company,Guidant, has the following types of financing choices toobtain DM2.5 million for 3-month working capital needs:u Borrow in DM (domestic or Euro)u Borrow in a foreign currency (uncovered or covered)u Borrow through another legal entity of the company

l The following factors may affect the effective borrowingcost:u Interest ratesu Expected future spot exchange rate, oru Forward exchange rateu Taxes in Germanyu Taxes in USA

Ian H. Giddy/IBM International Finance-16

Copyright ©1998 Ian H. Giddy International Finance 33

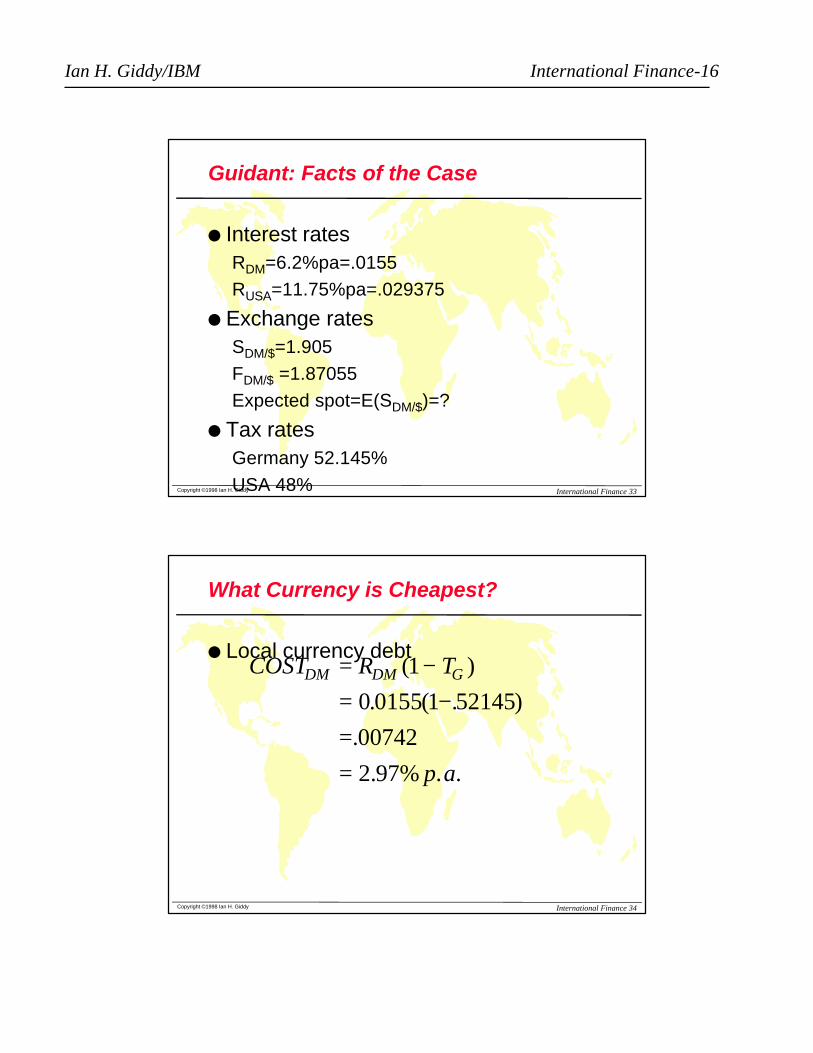

Guidant: Facts of the Case

l Interest ratesRDM=6.2%pa=.0155

RUSA=11.75%pa=.029375

l Exchange ratesSDM/$=1.905

FDM/$ =1.87055

Expected spot=E(SDM/$)=?

l Tax ratesGermany 52.145%

USA 48%

Copyright ©1998 Ian H. Giddy International Finance 34

What Currency is Cheapest?

l Local currency debtCOST R T

p a

DM DM G= −= −==

( )

. ( . )

.

. .

1

0 0155 1 52145

00742

2.97%

Ian H. Giddy/IBM International Finance-17

Copyright ©1998 Ian H. Giddy International Finance 35

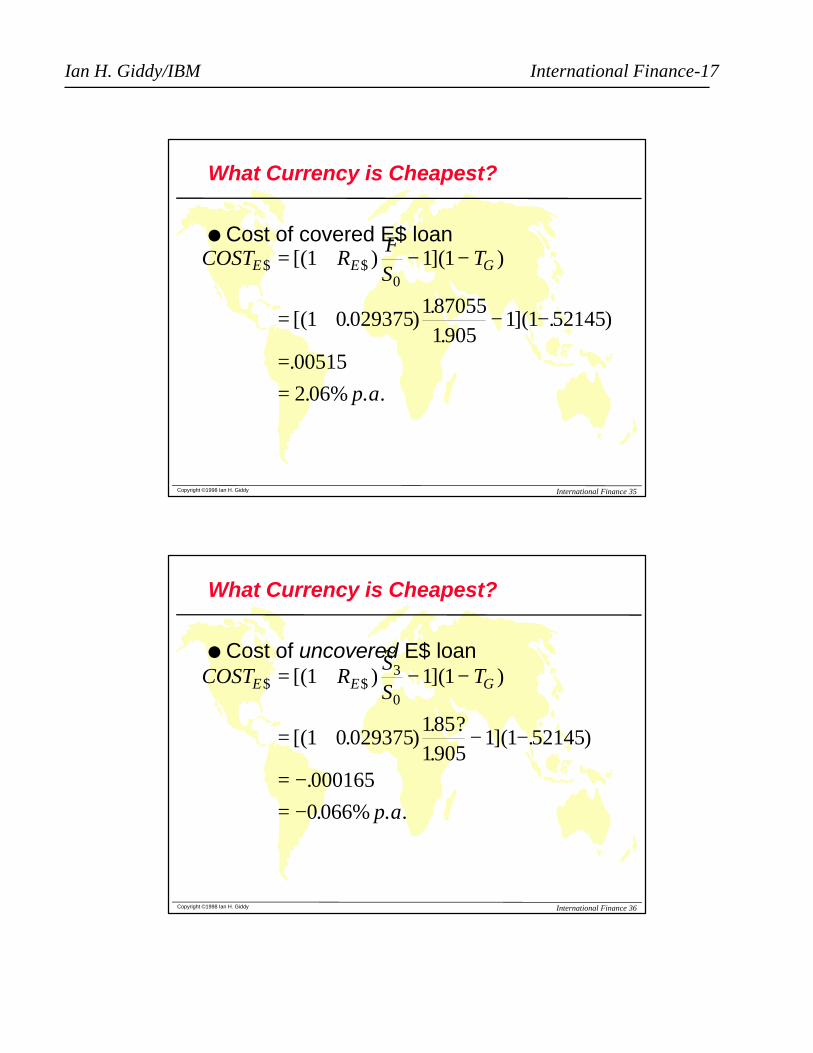

What Currency is Cheapest?

l Cost of covered E$ loanCOST R

FS

T

p a

E E G$ $[( ) ]( )

[( . )..

]( . )

.

. . .

= + − −

= + − −

==

1 1 1

1 0 0293751870551905

1 1 52145

00515

2 06%

0

Copyright ©1998 Ian H. Giddy International Finance 36

What Currency is Cheapest?

l Cost of uncovered E$ loanCOST R

SS

T

p a

E E G$ $[( )~

]( )

[( . ). ?.

]( . )

.

. . .

= + − −

= + − −

= −= −

1 1 1

1 0 0293751851905

1 1 52145

000165

0 066%

3

0

Ian H. Giddy/IBM International Finance-18

Copyright ©1998 Ian H. Giddy International Finance 37

What Currency is Cheapest?

COST RSS

T

COST RFS

T

COST RSS

T

DM DM G

E COV E G

E UNCOV E G

= + − −

= + − −

= + − −

[( )~

]( )

[( ) ]( )

[( )~

]( )

$ $

$ $

1 1 1

1 1 1

1 1 1

3

0

0

3

0

Copyright ©1998 Ian H. Giddy International Finance 38

What Form is Cheapest?

l Cost of intercompany dollar loan fromparent, covered:Same as (2) but subtract revenues to parent

and add costs to parent, taking account ofU.S. tax effect.

COST RFS

T

R T R T

I I G

I FE P US

$ $

$

[( ) ]( )

( ) ( )

= + − −

− − + −

1 1 1

1 1

0

Ian H. Giddy/IBM International Finance-19

Copyright ©1998 Ian H. Giddy International Finance 39

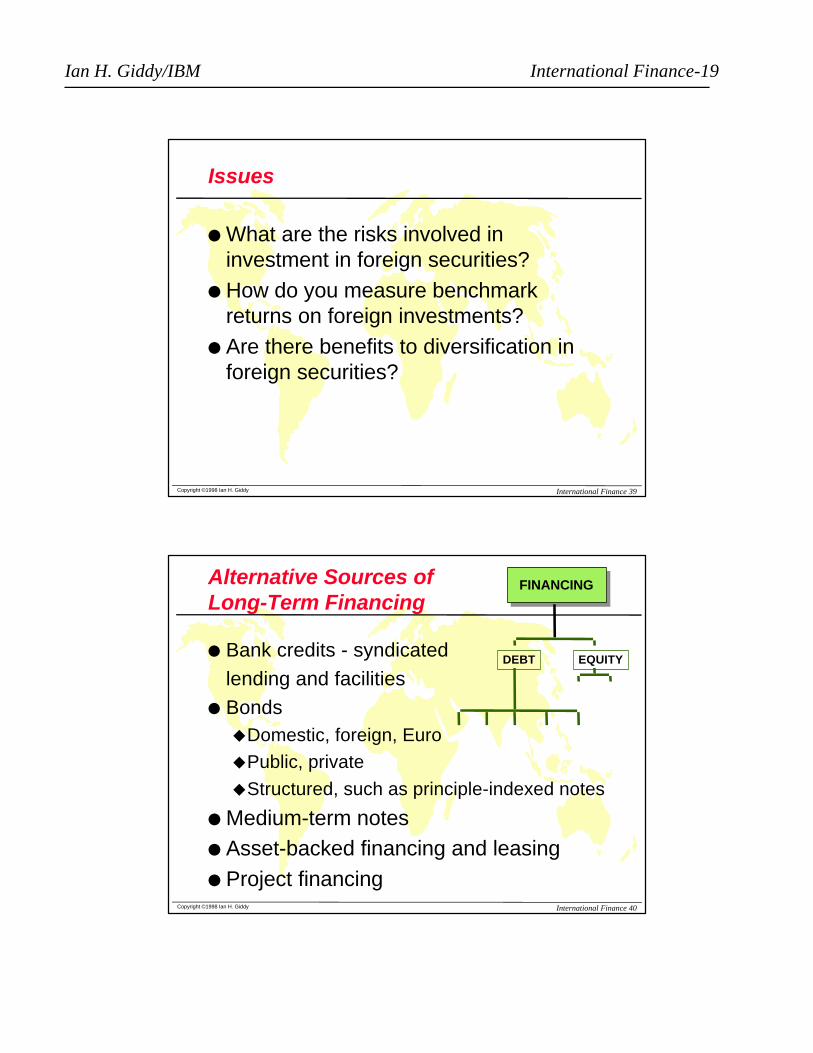

Issues

l What are the risks involved ininvestment in foreign securities?

l How do you measure benchmarkreturns on foreign investments?

l Are there benefits to diversification inforeign securities?

Copyright ©1998 Ian H. Giddy International Finance 40

Alternative Sources ofLong-Term Financing

FINANCINGFINANCING

DEBT EQUITYl Bank credits - syndicated

lending and facilities

l BondsuDomestic, foreign, Euro

uPublic, private

uStructured, such as principle-indexed notes

l Medium-term notesl Asset-backed financing and leasingl Project financing

Ian H. Giddy/IBM International Finance-20

Copyright ©1998 Ian H. Giddy International Finance 41

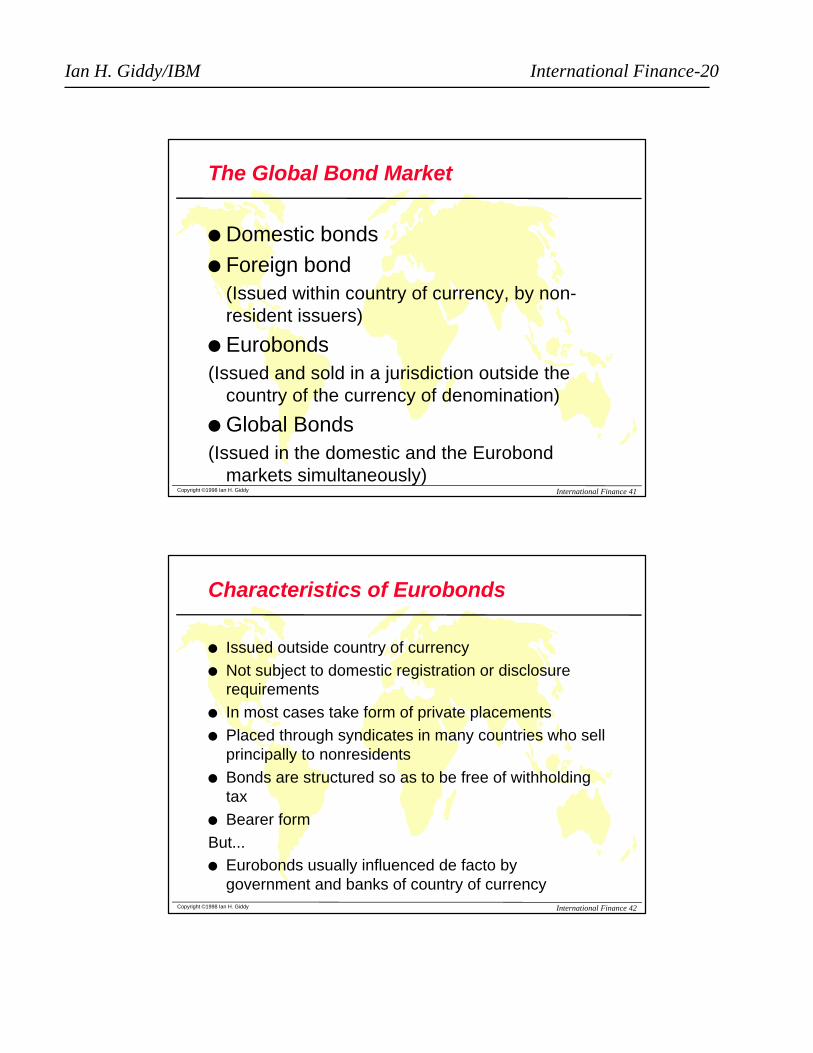

The Global Bond Market

l Domestic bondsl Foreign bond

(Issued within country of currency, by non-resident issuers)

l Eurobonds(Issued and sold in a jurisdiction outside the

country of the currency of denomination)

l Global Bonds(Issued in the domestic and the Eurobond

markets simultaneously)

Copyright ©1998 Ian H. Giddy International Finance 42

Characteristics of Eurobonds

l Issued outside country of currencyl Not subject to domestic registration or disclosure

requirementsl In most cases take form of private placementsl Placed through syndicates in many countries who sell

principally to nonresidentsl Bonds are structured so as to be free of withholding

taxl Bearer formBut...l Eurobonds usually influenced de facto by

government and banks of country of currency

Ian H. Giddy/IBM International Finance-21

Copyright ©1998 Ian H. Giddy International Finance 43

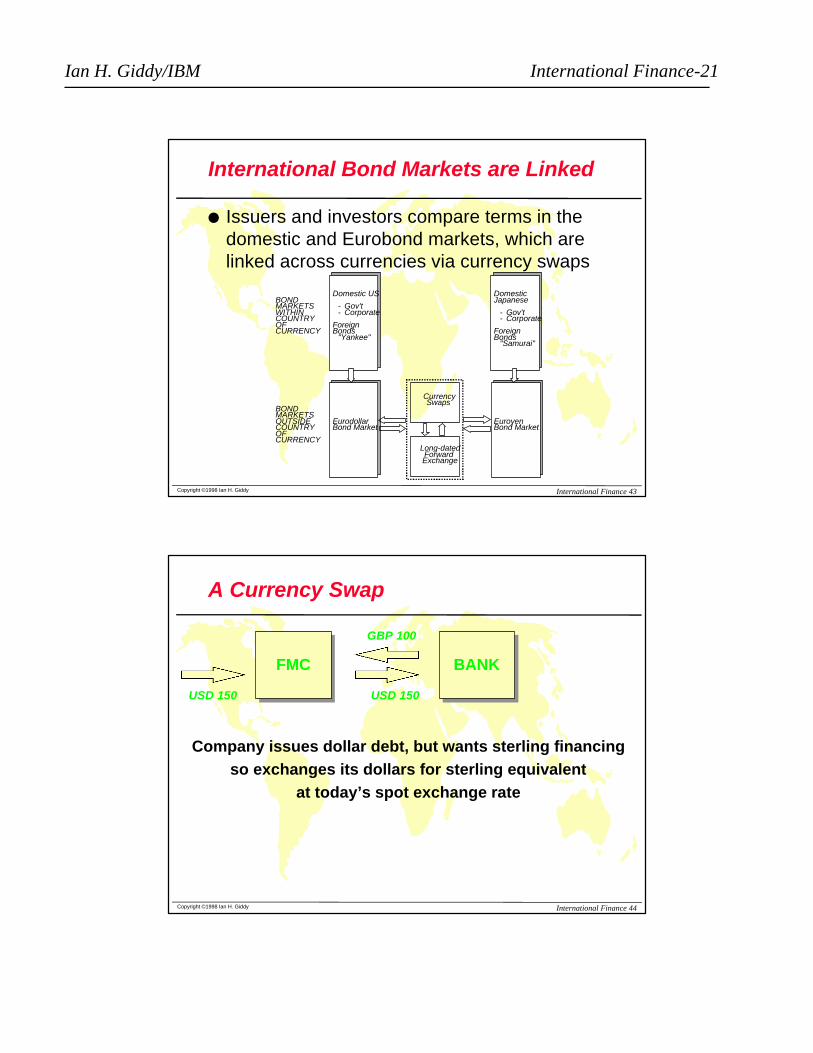

International Bond Markets are Linked

l Issuers and investors compare terms in thedomestic and Eurobond markets, which arelinked across currencies via currency swaps

BONDMARKETSWITHINCOUNTRYOFCURRENCY

BONDMARKETSOUTSIDECOUNTRYOFCURRENCY

CurrencySwaps

Long-datedForwardExchange

Domestic US

- Gov't- Corporate

ForeignBonds

"Yankee"

DomesticJapanese

- Gov't- Corporate

ForeignBonds

"Samurai"

EurodollarBond Market

EuroyenBond Market

Copyright ©1998 Ian H. Giddy International Finance 44

A Currency Swap

FMCFMC BANKBANK

GBP 100

USD 150

Company issues dollar debt, but wants sterling financing

so exchanges its dollars for sterling equivalent

at today’s spot exchange rate

USD 150

Ian H. Giddy/IBM International Finance-22

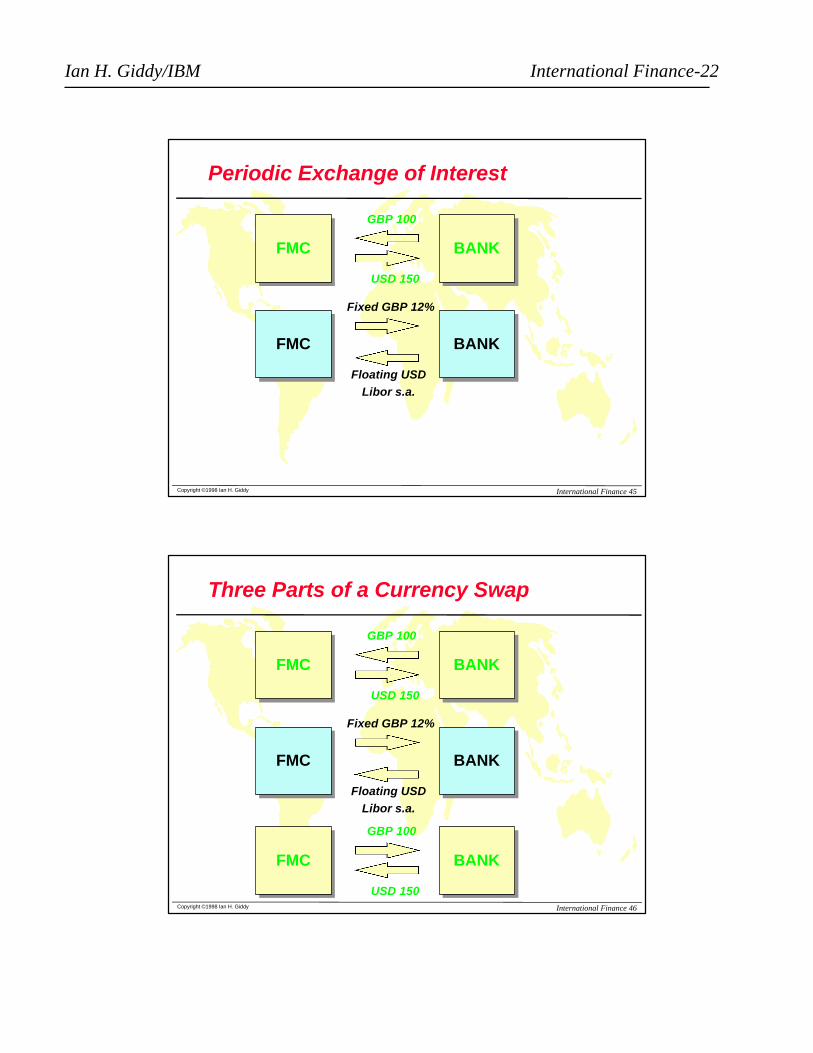

Copyright ©1998 Ian H. Giddy International Finance 45

Periodic Exchange of Interest

FMCFMC BANKBANK

GBP 100

USD 150

FMCFMC BANKBANK

Fixed GBP 12%

Floating USD

Libor s.a.

Copyright ©1998 Ian H. Giddy International Finance 46

Three Parts of a Currency Swap

FMCFMC BANKBANK

GBP 100

USD 150

FMCFMC BANKBANK

Fixed GBP 12%

Floating USD

Libor s.a.

FMCFMC BANKBANK

GBP 100

USD 150

Ian H. Giddy/IBM International Finance-23

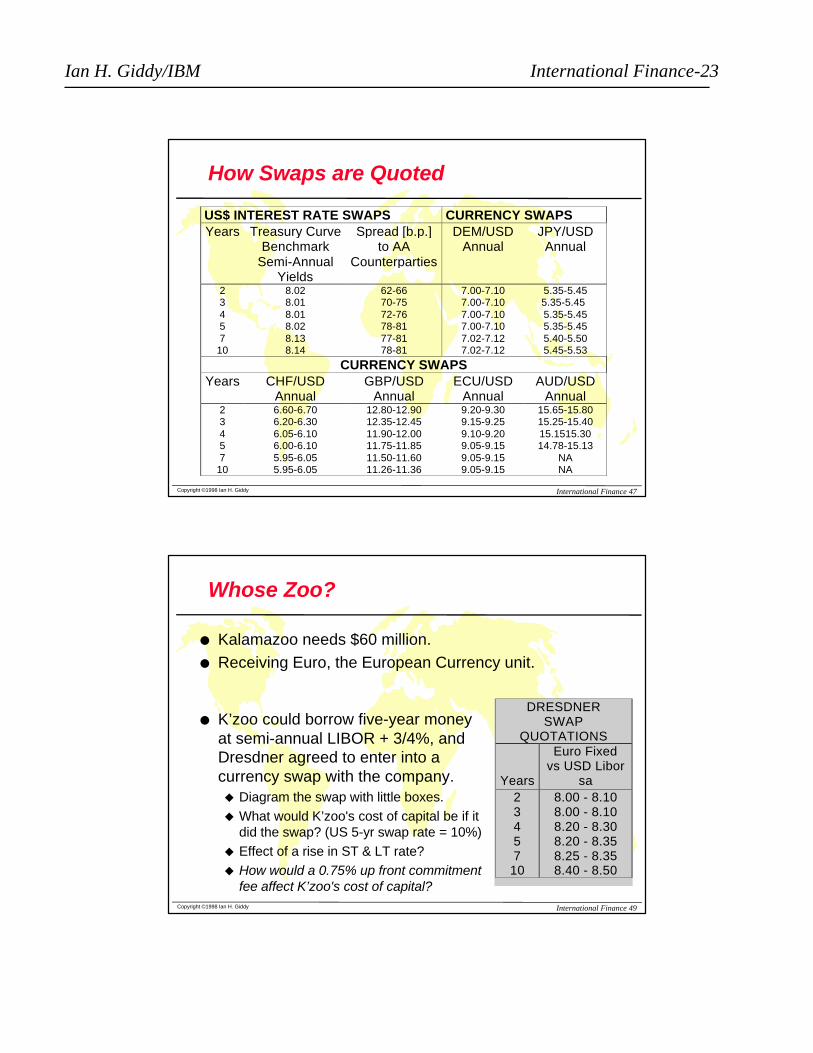

Copyright ©1998 Ian H. Giddy International Finance 47

How Swaps are Quoted

US$ INTEREST RATE SWAPS CURRENCY SWAPSYears Treasury Curve

BenchmarkSemi-Annual

Yields

Spread [b.p.]to AA

Counterparties

DEM/USDAnnual

JPY/USDAnnual

23457

10

8.028.018.018.028.138.14

62-6670-7572-7678-8177-8178-81

7.00-7.107.00-7.107.00-7.107.00-7.107.02-7.127.02-7.12

5.35-5.455.35-5.455.35-5.455.35-5.455.40-5.505.45-5.53

CURRENCY SWAPSYears CHF/USD

AnnualGBP/USD

AnnualECU/USD

AnnualAUD/USD

Annual23457

10

6.60-6.706.20-6.306.05-6.106.00-6.105.95-6.055.95-6.05

12.80-12.9012.35-12.4511.90-12.0011.75-11.8511.50-11.6011.26-11.36

9.20-9.309.15-9.259.10-9.209.05-9.159.05-9.159.05-9.15

15.65-15.8015.25-15.4015.1515.3014.78-15.13

NANA

Copyright ©1998 Ian H. Giddy International Finance 49

l Kalamazoo needs $60 million.l Receiving Euro, the European Currency unit.

Whose Zoo?

l K’zoo could borrow five-year moneyat semi-annual LIBOR + 3/4%, andDresdner agreed to enter into acurrency swap with the company.u Diagram the swap with little boxes.u What would K’zoo's cost of capital be if it

did the swap? (US 5-yr swap rate = 10%)u Effect of a rise in ST & LT rate?u How would a 0.75% up front commitment

fee affect K’zoo's cost of capital?

DRESDNERSWAP

QUOTATIONS

Years

Euro Fixedvs USD Libor

sa2345710

8.00 - 8.108.00 - 8.108.20 - 8.308.20 - 8.358.25 - 8.358.40 - 8.50

Ian H. Giddy/IBM International Finance-24

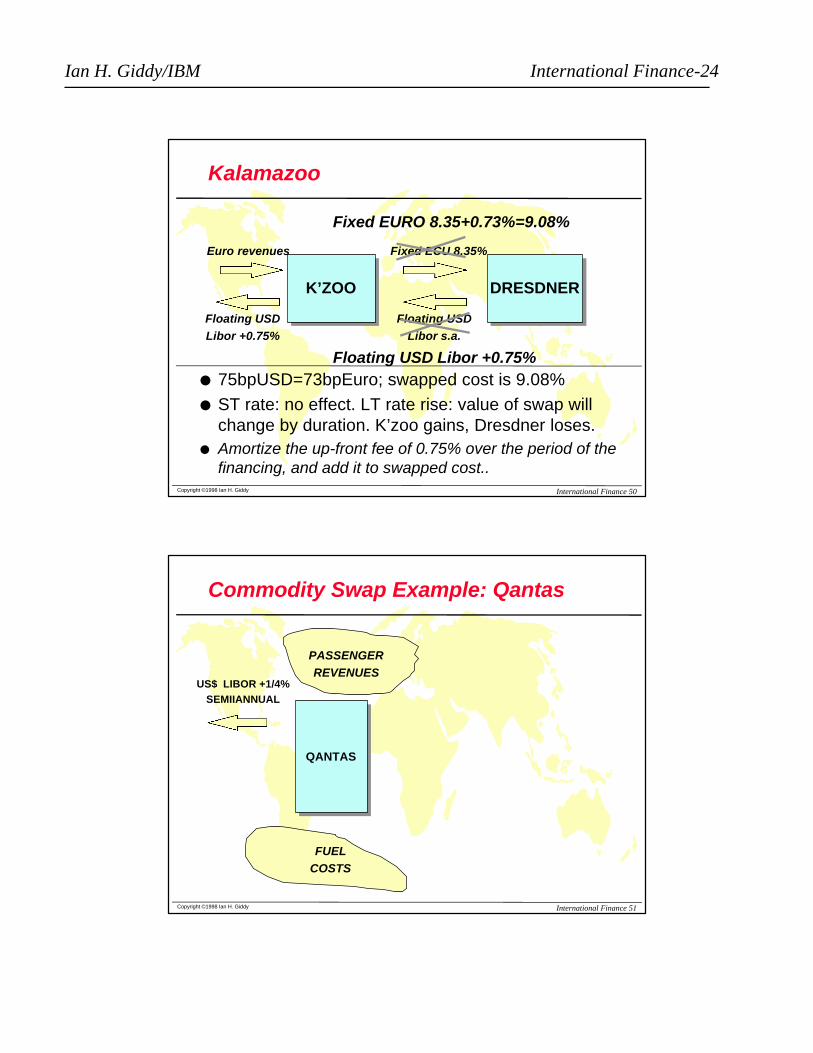

Copyright ©1998 Ian H. Giddy International Finance 50

Kalamazoo

K’ZOOK’ZOO DRESDNERDRESDNER

Fixed ECU 8.35%

Floating USD

Libor s.a.

Fixed EURO 8.35+0.73%=9.08%

Floating USD Libor +0.75%

Floating USD

Libor +0.75%

l 75bpUSD=73bpEuro; swapped cost is 9.08%l ST rate: no effect. LT rate rise: value of swap will

change by duration. K’zoo gains, Dresdner loses.l Amortize the up-front fee of 0.75% over the period of the

financing, and add it to swapped cost..

Euro revenues

Copyright ©1998 Ian H. Giddy International Finance 51

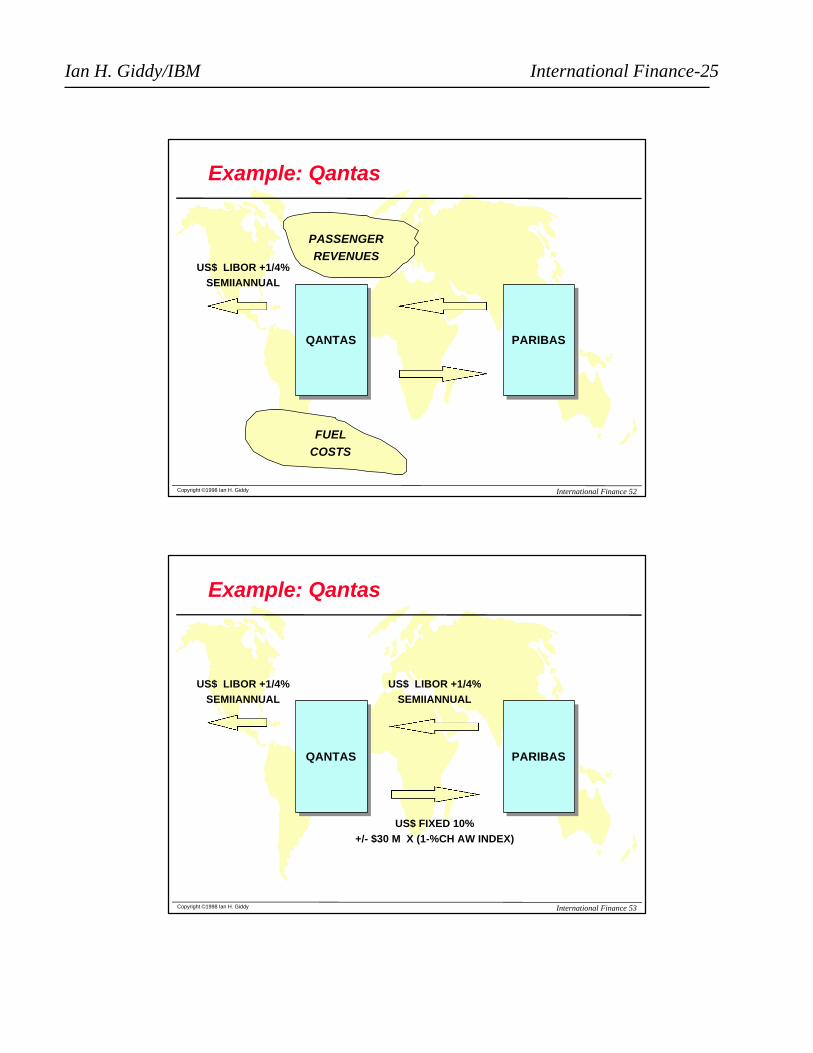

Commodity Swap Example: Qantas

QANTASQANTAS

US$ LIBOR +1/4%

SEMIIANNUAL

PASSENGER

REVENUES

FUEL

COSTS

Ian H. Giddy/IBM International Finance-25

Copyright ©1998 Ian H. Giddy International Finance 52

Example: Qantas

QANTASQANTAS PARIBASPARIBAS

US$ LIBOR +1/4%

SEMIIANNUAL

PASSENGER

REVENUES

FUEL

COSTS

Copyright ©1998 Ian H. Giddy International Finance 53

Example: Qantas

QANTASQANTAS PARIBASPARIBAS

US$ LIBOR +1/4%

SEMIIANNUAL

US$ FIXED 10%

+/- $30 M X (1-%CH AW INDEX)

US$ LIBOR +1/4%

SEMIIANNUAL

Ian H. Giddy/IBM International Finance-26

Copyright ©1998 Ian H. Giddy International Finance 54

Anatomy of a Deal

Copyright ©1998 Ian H. Giddy International Finance 55

Anatomy of a Deal

Issuer:uLooking for large amounts of floating-rate

USD and DEM funding for its loan porfolio.

uWants low-cost funds: target CP-.10

uIs not too concerned about specific timingof issue, amount or maturity

uIs willing to consider hybrid structures.

Ian H. Giddy/IBM International Finance-27

Copyright ©1998 Ian H. Giddy International Finance 56

Anatomy of a Deal

Investor:uHas distinctive preference for high grade

investments

uLooking for investments that will improveportfolio returns relative to relevant indexes

uInvests in both floating rate and fixed ratesterling and dollar securities

uCan buy options to hedge portfolio butcannot sell options

Copyright ©1998 Ian H. Giddy International Finance 57

Anatomy of a Deal

Intermediary:uHas experience and technical and legal

background in structure finance

uHas active swap and option trading andpositioning capabilities

uHas clients looking for caps and otherforms of interest rate protection.

Ian H. Giddy/IBM International Finance-28

Copyright ©1998 Ian H. Giddy International Finance 58

The Deal

1 Initiate medium term note programme for theborrower, allowing for a variety of currencies,maturities and special structures

2 Structuring a MTN in such a way as to meetthe investor’s needs and constraints

3 Line up all potential counterparties andnegociate numbers acceptable to all sides

4 Upon issuer’s and investor’s approval, placethe securities

Copyright ©1998 Ian H. Giddy International Finance 59

The Deal / 2

5 For the issuer, swap and strip the issue intothe form of funding that he requires

6 Offer a degree of liquidity to the issuer bystanding willing to buy back the securities at alater date.

Ian H. Giddy/IBM International Finance-29

Copyright ©1998 Ian H. Giddy International Finance 60

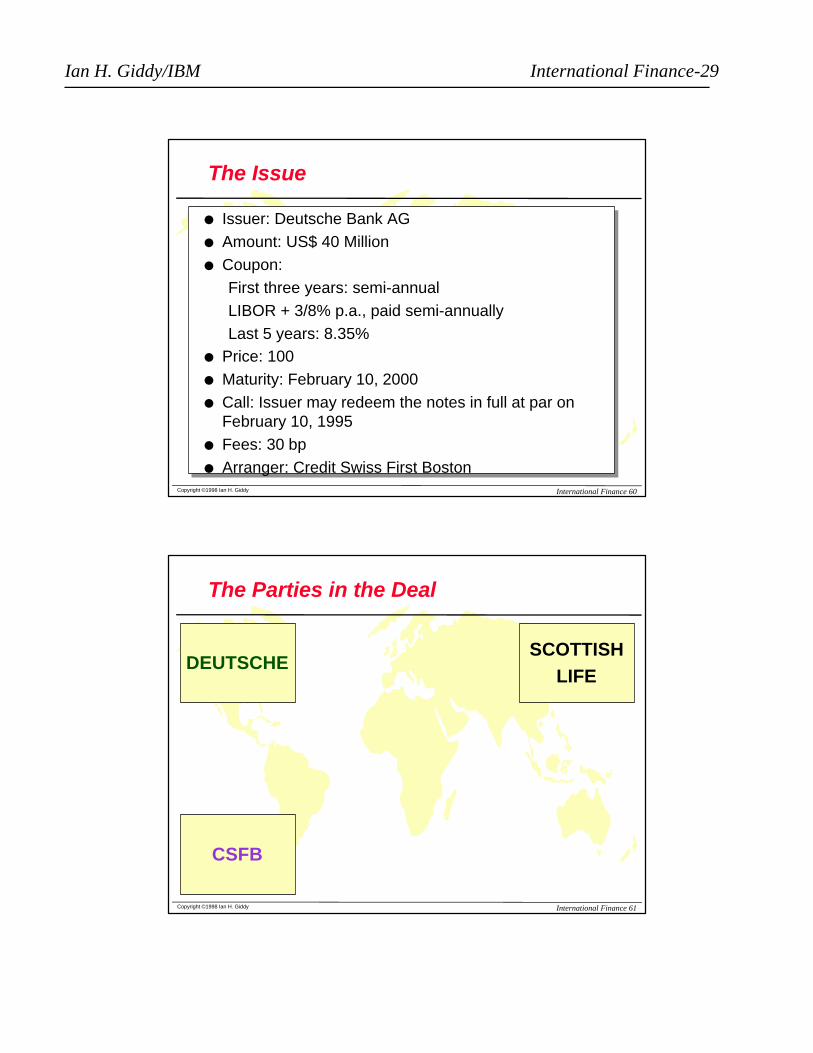

The Issue

l Issuer: Deutsche Bank AGl Amount: US$ 40 Millionl Coupon:

First three years: semi-annualLIBOR + 3/8% p.a., paid semi-annuallyLast 5 years: 8.35%

l Price: 100l Maturity: February 10, 2000l Call: Issuer may redeem the notes in full at par on

February 10, 1995l Fees: 30 bpl Arranger: Credit Swiss First Boston

Copyright ©1998 Ian H. Giddy International Finance 61

The Parties in the Deal

SCOTTISH

LIFE

CSFB

DEUTSCHE

Ian H. Giddy/IBM International Finance-30

Copyright ©1998 Ian H. Giddy International Finance 66

What’s Really Going On?

Note:l Issuer has agreed to pay an above-market

rate on both the floating rate note and thefixed rate bond segment of the issue

FRN portion: .75 % above normal cost

Fixed portion: .50% above normal cost

l Issuer has in effect purchased the right to paya fixed rate of 8.35% on a five-year bond tobe issued in three years time.

Related Documents