Travel & Tourism investment in the Americas Will the region’s infrastructure and investment constrain or support future industry growth? September 2014

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Travel & Tourism investment in the Americas

Will the region’s infrastructure and investment constrain or support future industry growth?

September 2014

chapter 1

chapter 2

chapter 3

The importance of investment in supporting the Americas’ Travel & Tourism industry

1.1 The role of investment in the Travel & Tourism industry

1.2 The strong link between Travel & Tourism investment, infrastructure and industry performance

The lagging state of Travel & Tourism infrastructure in the Americas and the need for future investment

2.1 The current state of the Americas’ Travel & Tourism infrastructure

2.2 The outlook for the Americas’ Travel & Tourism investment spending

2.3 Are the Americas on track to invest enough to address current infrastructure deficiencies and realise the Travel & Tourism industry’s future demand and growth potential?

Summary - Putting Travel & Tourism investment on the agenda

Table of Contents

Introduction

Countries in the Americas

September 2014

6

7

8

11

11

12

14

16

Travel & Tourism investment in the Americas: Will the region’s infrastructure and investment constrain or support future industry growth?

4

Countries in the Americas

North America

CanadaMexicoUnited States

Latin America

ArgentinaBelizeBoliviaBrazilChileColombiaCosta RicaEl SalvadorEcuadorGuatemalaGuyanaHondurasNicaraguaPanamaParaguayPeruSurinameUruguayVenezuela

Caribbean

AnguillaAntigua & BarbudaArubaBahamasBarbadosBermudaBritish Virgin IslandsCayman IslandsCubaDominicaDominican RepublicGrenadaGuadeloupeHaitiJamaicaMartiniqueNetherlands AntillesPuerto RicoSt. Kitts & GrenadinesTrinidad and TobagoUS Virgin Islands

September 2014

5

Introduction

1 www.weforum.org/reports/travel-tourism-competitiveness-report-2013

The World Travel & Tourism Council (WTTC)is the forum for business leaders in the Travel & Tourism industry. With Chief Executives of over one hundred of the world’s leading Travel & Tourism companies as its Members, WTTC has a unique mandate and overview on all matters related to Travel & Tourism.

Understanding and addressing the challenges inhibiting the sustainable growth of our sector is paramount for all industry stakeholders. Together with our research partner, Oxford Economics, and to coincide with the WTTC Americas Summit in Lima, Peru, in September 2014, WTTC has produced this report on Travel & Tourism investment in the Americas. The report draws on data from WTTC’s annual Travel & Tourism Economic Impact Research 2014 and the World Economic Forum’s Travel & Tourism Competitiveness Report 20131 , and seeks to understand whether and where the region’s infrastructure and investment will constrain or support future industry growth.

WTTC has forecast that there will be US$3.6 trillion worth of Travel & Tourism investment made in the Americas over the next decade. However, with the industry forecast to grow by an average of 3.7% per annum, and the lagging state of much infrastructure today, it is of critical importance that our baseline forecasts of Travel & Tourism investment are enough to sustain and support future demand.

The analysis produced here shows that a strong and positive relationship exists between Travel & Tourism investment and Travel & Tourism demand. Not surprisingly, given the size and diversity of the Americas, there are huge disparities in the state of Travel & Tourism infrastructure across the countries. Taking the region as a whole, however, Travel & Tourism infrastructure lags behind much of the world. Weaknesses in the current state of the Americas’ Travel & Tourism related infrastructure therefore threaten the growth potential of the sector within the region in the medium term.

Countries across the region need the right business, political and regulatory frameworks in place now to foster necessary infrastructure and investment opportunities. Improving their competitive positions through better infrastructure will help countries ensure that Travel & Tourism will continue to create quality jobs and contribute strongly to their economies well into the future.

Travel & Tourism investment in the Americas: Will the region’s infrastructure and investment constrain or support future industry growth?

6

chapter 1The importance of investment in supporting

the Americas’ Travel & Tourism industry

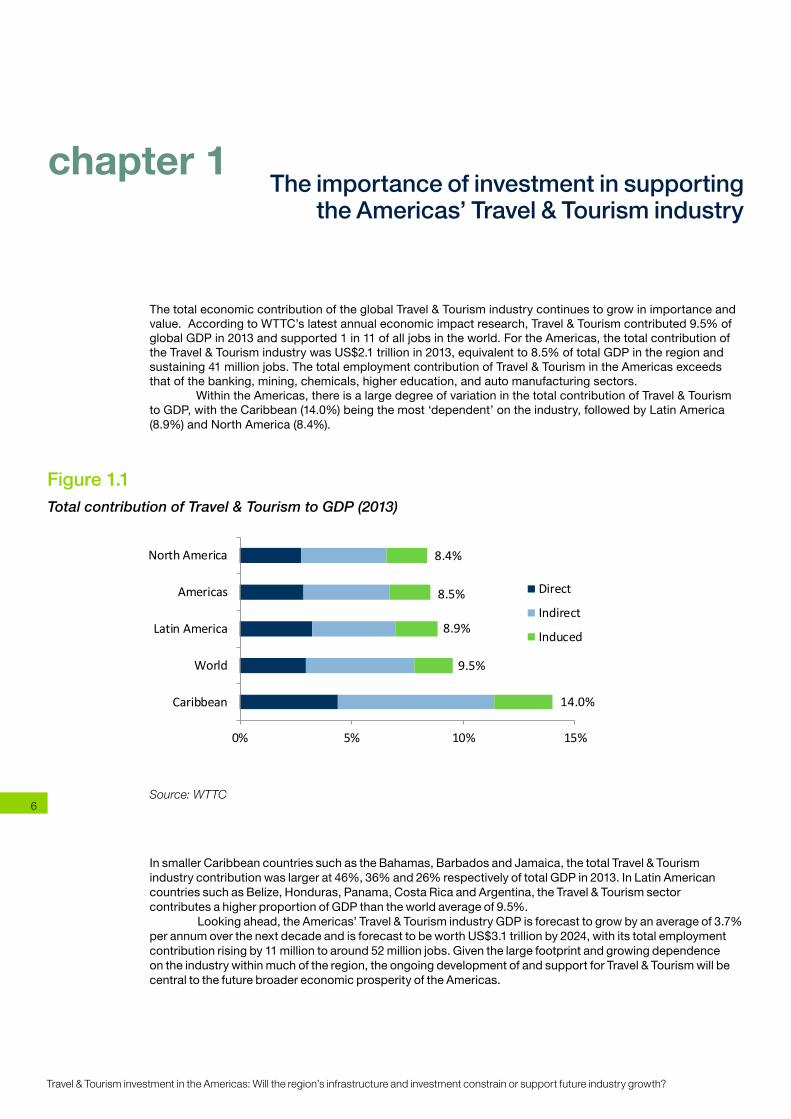

The total economic contribution of the global Travel & Tourism industry continues to grow in importance and value. According to WTTC’s latest annual economic impact research, Travel & Tourism contributed 9.5% of global GDP in 2013 and supported 1 in 11 of all jobs in the world. For the Americas, the total contribution of the Travel & Tourism industry was US$2.1 trillion in 2013, equivalent to 8.5% of total GDP in the region and sustaining 41 million jobs. The total employment contribution of Travel & Tourism in the Americas exceeds that of the banking, mining, chemicals, higher education, and auto manufacturing sectors.

Within the Americas, there is a large degree of variation in the total contribution of Travel & Tourism to GDP, with the Caribbean (14.0%) being the most ‘dependent’ on the industry, followed by Latin America (8.9%) and North America (8.4%).

In smaller Caribbean countries such as the Bahamas, Barbados and Jamaica, the total Travel & Tourism industry contribution was larger at 46%, 36% and 26% respectively of total GDP in 2013. In Latin American countries such as Belize, Honduras, Panama, Costa Rica and Argentina, the Travel & Tourism sector contributes a higher proportion of GDP than the world average of 9.5%.

Looking ahead, the Americas’ Travel & Tourism industry GDP is forecast to grow by an average of 3.7% per annum over the next decade and is forecast to be worth US$3.1 trillion by 2024, with its total employment contribution rising by 11 million to around 52 million jobs. Given the large footprint and growing dependence on the industry within much of the region, the ongoing development of and support for Travel & Tourism will be central to the future broader economic prosperity of the Americas.

Figure 1.1Total contribution of Travel & Tourism to GDP (2013)

Source: WTTC6

0% 5% 10% 15%

Caribbean

World

Latin America

Americas

North America

% Whole economy GDP

Direct

Indirect

Induced

Figure 1.1: Total contribution of Travel & Tourism to GDP (2013)

Sources: WTTC, Oxford Economics

8.4%

8.5%

8.9%

9.5%

14.0%

September 2014

7

1.1 The role of investment in the Travel & Tourism industry

Against the backdrop of strong demand growth prospects and an increasingly competitive marketplace, investment in Travel & Tourism infrastructure is essential for destinations to maintain and grow their market share of visitors and to appeal to an ever-growing and diverse group of travellers. In this report, and consistent with the definitions used in WTTC’s annual economic impact research (which are aligned with the UNWTO TSA Recommended Methodological Framework 2008), Travel & Tourism investment is made up of two components:

Both of these forms of investment are essential in supporting the ongoing growth and development of the Travel & Tourism industry within the Americas for the following reasons:

• Expanding capacity: In order to support higher demand and a greater volume of tourists, investment is required to, for example, build more visitor accommodation, increase airport capacity and expand tourist facilities. Insufficient capacity can lead to supply-side bottlenecks and a limit on growth, as well as upward pressure on prices which affects competitiveness.

• Maintaining and enhancing current infrastructure: Continued investment in existing infrastructure plays a central role in maintaining and improving its functionality and quality through refurbishment and upgrading. Capital expenditure on existing infrastructure is also essential for adapting infrastructure to account for the evolution in consumer tastes over time.

• Stimulating demand: Visitor attraction capital projects can be used as a means of generating additional demand and to gain or retain market share from competitors. These projects aim to enhance the appeal of destinations through improving their product offering.

1) Government Public Travel & Tourism Investment

2) Private Travel & Tourism Investment

• Defintion: Public capital spending, directly related to Travel & Tourism, on items such as equipment, land, buildings and infrastructure.

• Examples: Government spending on the construction of visitor centres, tourist information offices, publicly funded airports and government contributions to large resort-based investments.

• Note: The estimates of Government Travel & Tourism investment do not include government investment in multi-use infrastructure such as roads or public transport, even though this may be used for Travel & Tourism as well as for other uses.

• Definition: Private sector capital expenditure, directly related to the Travel & Tourism industry.

• Examples: Residential structures such as vacation houses and non-residential structures such as hotels, and convention centres. Travel & Tourism equipment such as airplanes, cruise ships, and rental cars.

Travel & Tourism investment in the Americas: Will the region’s infrastructure and investment constrain or support future industry growth?

8

1.2 The strong link between Travel & Tourism investment, infrastructure and industry

performance

Statistical analysis shows that there is a strong link between the quality and capacity of a country’s Travel & Tourism related infrastructure, and the contribution that the Travel & Tourism industry makes to the economy.

Specifically, when the quality and capacity of Travel & Tourism related infrastructure is measured according to the average of a country’s scores in the air transport infrastructure, ground transport infrastructure and tourism infrastructure pillars of the World Economic Forum (WEF) Travel & Tourism Competitiveness Index, and is compared to the direct contribution of Travel & Tourism to total GDP, a strong, positive correlation is evident (see Figure 1.2).

This relationship is to be expected given that in order to support a relatively large and advanced Travel & Tourism sector, an appropriate quality and capacity of Travel & Tourism infrastructure is required.

Box 1

The relationship between quality and capacity of Travel & Tourism infrastructure and industry performance

This relationship can be exemplified through two extreme cases. At one end of the spectrum is Barbados, which has a very high Travel & Tourism infrastructure rating and a very large Travel & Tourism industry in relative terms. By contrast, Paraguay has a very poor Travel & Tourism infrastructure rating and a very small Travel & Tourism industry in relative terms.

R² = 0.4742

0%

2%

4%

6%

8%

10%

12%

0.00 1.00 2.00 3.00 4.00 5.00 6.00

Dire

ct T

rave

l & T

ouris

m G

DP

(% t

otal

GD

P)

WEF composite infrastructure score

Barbados

Jamaica

Puerto Rico

Sources: WTTC, Oxford EconomicsNote: US and Canada are excluded from this analysis due to their distorting effect. Countries not included in the WEF Travel & Tourism Competitiveness Index are also excluded

Figure 1.2: WEF composite Travel & Tourism infrastructure score and Travel & Tourism direct GDP contribution (2013)

Haiti

Increasing infrastructure quality

Paraguay

Figure 1.2WEF composite Travel & Tourism infrastructure score and Travel & Tourism direct GDP contribution (2013)

Sources: WTTC, World Economic Forum, Oxford EconomicsNote: US and Canada are excluded from this analysis due to their distorting effect. These nations both have very high WEF composite infrastructure scores despite direct Travel & Tourism GDP making a relatively small contribuition to total GDP. Countries not included in the WEF Travel & Tourism Competitiveness index are also excluded from this analysis.

September 2014

9

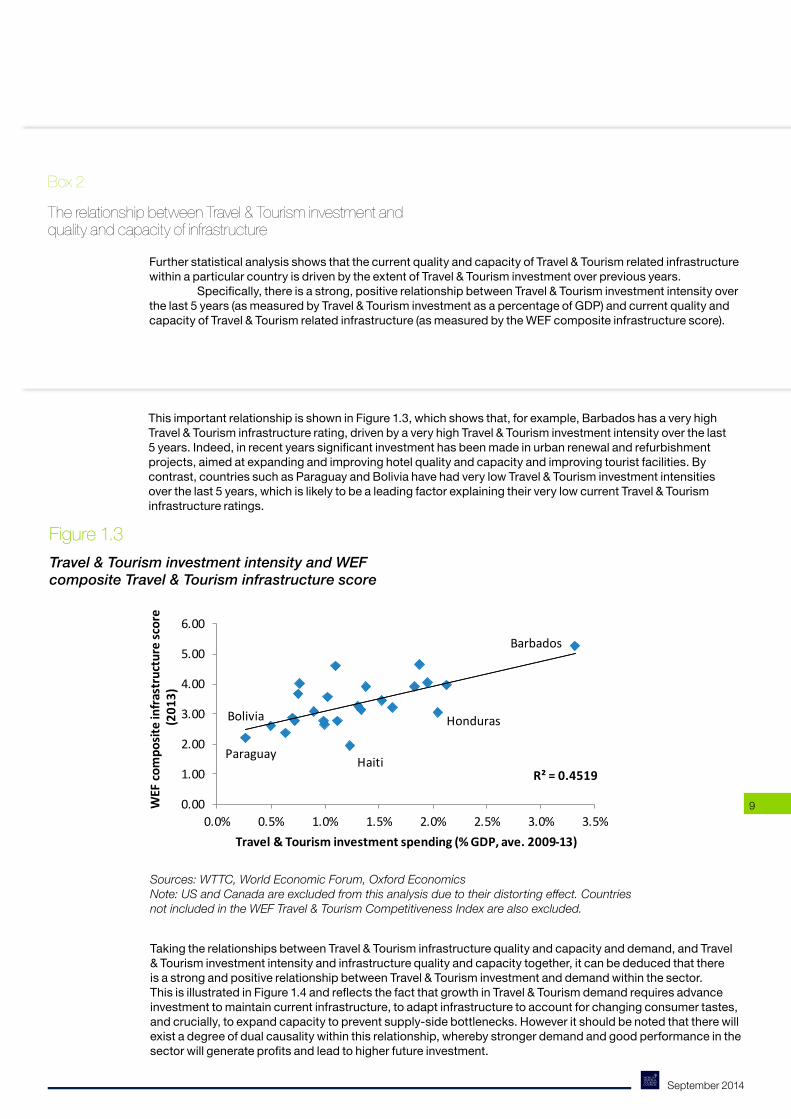

Further statistical analysis shows that the current quality and capacity of Travel & Tourism related infrastructure within a particular country is driven by the extent of Travel & Tourism investment over previous years.

Specifically, there is a strong, positive relationship between Travel & Tourism investment intensity over the last 5 years (as measured by Travel & Tourism investment as a percentage of GDP) and current quality and capacity of Travel & Tourism related infrastructure (as measured by the WEF composite infrastructure score).

Box 2

The relationship between Travel & Tourism investment and quality and capacity of infrastructure

This important relationship is shown in Figure 1.3, which shows that, for example, Barbados has a very high Travel & Tourism infrastructure rating, driven by a very high Travel & Tourism investment intensity over the last 5 years. Indeed, in recent years significant investment has been made in urban renewal and refurbishment projects, aimed at expanding and improving hotel quality and capacity and improving tourist facilities. By contrast, countries such as Paraguay and Bolivia have had very low Travel & Tourism investment intensities over the last 5 years, which is likely to be a leading factor explaining their very low current Travel & Tourism infrastructure ratings.

Taking the relationships between Travel & Tourism infrastructure quality and capacity and demand, and Travel & Tourism investment intensity and infrastructure quality and capacity together, it can be deduced that there is a strong and positive relationship between Travel & Tourism investment and demand within the sector. This is illustrated in Figure 1.4 and reflects the fact that growth in Travel & Tourism demand requires advance investment to maintain current infrastructure, to adapt infrastructure to account for changing consumer tastes, and crucially, to expand capacity to prevent supply-side bottlenecks. However it should be noted that there will exist a degree of dual causality within this relationship, whereby stronger demand and good performance in the sector will generate profits and lead to higher future investment.

R² = 0.4519

0.00

1.00

2.00

3.00

4.00

5.00

6.00

0.0% 0.5% 1.0% 1.5% 2.0% 2.5% 3.0% 3.5%

WEF

com

posi

te in

fras

truc

ture

scor

e(2

013)

Travel & Tourism investment spending (% GDP, ave. 2009-13)

Barbados

Haiti

Honduras

Figure 1.3: Travel & Tourism investment intensity and WEF composite Travel & Tourism infrastructure score

Sources: WTTC, Oxford EconomicsNote: US and Canada are excluded from this analysis due to their distorting effect. Countries not included in the WEF Travel & Tourism Competitiveness Index are also excluded

Paraguay

Bolivia

Figure 1.3Travel & Tourism investment intensity and WEF composite Travel & Tourism infrastructure score

Sources: WTTC, World Economic Forum, Oxford EconomicsNote: US and Canada are excluded from this analysis due to their distorting effect. Countries not included in the WEF Travel & Tourism Competitiveness Index are also excluded.

Travel & Tourism investment in the Americas: Will the region’s infrastructure and investment constrain or support future industry growth?

10

0

50

100

150

200

250

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 2022 2024

Inde

x: 2

000=

100

T&T investment

T&T demand

Forecast

Sources: WTTC, Oxford Economics

Figure 1.4: Americas Travel & Tourism investment spending and demand

Investment boom

Investment recovery lags behind demand

Although there is a strong link between Travel & Tourism investment and Travel & Tourism demand, the variables do not always move exactly in line and in time with one another. This is due to the even more cyclical nature of investment and its link to wider economic performance, confidence and other issues such as access to finance and the state of public finances. Within the Americas between 2003 and 2008, with annual average growth of 10.5%, Travel & Tourism investment boomed and far outpaced Travel & Tourism growth of 3.0% during this period. After the onset of the global economic slowdown in 2008/09, Travel & Tourism investment fell sharply and did not recover until 2012. By contrast, Travel & Tourism demand fell by much less and began to recover much earlier in 2010. Nonetheless, the strong and positive relationship remains over a longer period and it is evident that sufficient Travel & Tourism investment will be central to sustaining and supporting future demand growth within the sector in the Americas over the next decade. If sufficient investment is not made, there is a strong possibility that some countries within the Americas may struggle to realise current Travel & Tourism demand projections, costing the region heavily in GDP and employment terms.

Figure 1.4Americas Travel & Tourism investment spending and demand

Sources: WTTC, Oxford Economics

Figure 1.5Americas Travel & Tourism investment spending and demand growth

Source: WTTC

10.5%

-2.6%

4.6%

3.4%

3.0%

0.9%

3.9%

2.6%

-4% -2% 0% 2% 4% 6% 8% 10% 12%

2003-08

2008-13

2014-24

2000-24

Annual average growth rate

T&T demand

T&T investment

Sources: WTTC, Oxford Economics

Figure 1.5: Americas Travel & Tourism investment and demand growth

Significant over-investment

September 2014

11

chapter 2The lagging state of Travel & Tourism

infrastructure in the Americas and the need for future investment

2.1 The current state of the Americas’ Travel & Tourism infrastructure

Shortcomings in the current state of its Travel & Tourism related infrastructure is a considerable threat to realising the growth potential of the Travel & Tourism industry within the Americas. According to the WEF Travel & Tourism Competitiveness Index 2 and compared to other world regions, the Americas Travel & Tourism related infrastructure lags behind that of much of the rest of the world. In fact, when measured as the equally weighted scores of the air transport infrastructure, ground transport infrastructure and tourism infrastructure pillars - it rated only better than that of Africa across all world regions. This should be a significant concern if the region wants to remain competitive on the world stage and be able to sustain the strong rate of Travel & Tourism demand growth forecast. Interestingly, the Americas’ best WEF rating is for its tourism specific infrastructure, while its ratings for air transport and ground transport infrastructure are less favourable. This suggests that most investment is required in ‘tourism supporting’ infrastructure, which plays an essential role in transporting tourists into and within the region.

There is however a large degree of variation within the Americas in terms of Travel & Tourism infrastructure quality and capacity. For example, the United States, Canada and Barbados have world class ratings across each of the 3 infrastructure types. By contrast, in 5 of the 27 Americas countries covered by the WEF Travel & Tourism Competitiveness Index, Travel & Tourism infrastructure is rated as worse than the African average. These countries are Bolivia, Guatemala, Guyana, Haiti and Paraguay and the future infrastructure and investment challenges facing these nations are significant.

Composite rank Composite score(0-7)

Tourism infrastructure rank

Air transport infrastructure rank

Ground transport infrastructure rank

Europe 1 4.8 1 1 1Middle East 2 4.0 2 3 3Asia-Pacific 3 3.8 4 2 2Americas 4 3.5 3 4 4Africa 5 2.7 5 5 5

Sources: World Economic Forum, WTTC, Oxford EconomicsNote: The composite score is calculated as an equally weighted average of the 3 separate infrastructure scoresRanks and ratings are shaded using a colour scale, where green signifies strong performance and red signifies bad performance

Table 2.1: WEF infrastructure ratings by world region by type (2013)

Sources: World Economic Forum, WTTC, Oxford EconomicsNote: The composite is calculated as an equally weighted average of the 3 separate infrastructure scoresRanks and ratings are shaded using a colour scale, where green signifies strong performance and red signifies weak performance

2 It should be noted that many small Caribbean countries are not included in the WEF Travel & Tourism Competitiveness Index

Travel & Tourism investment in the Americas: Will the region’s infrastructure and investment constrain or support future industry growth?

12

The Travel & Tourism infrastructure within the United States, Canada and to a lesser extent, Barbados, can be considered as amongst the best in the world and fares well against that of advanced economies such as Singapore, Australia and Japan. Interestingly, the United States and Canada have extremely high ratings for tourism and air transport infrastructure, but rank much less favourably in terms of ground transport infrastructure, which serves to highlight the key area where improvement is required for these countries. By contrast, Travel & Tourism infrastructure standards in parts of Latin America, such as Colombia, Peru and Argentina are poor and rate below the likes of India and South Africa.

Composite rank Composite score(0-7)

Tourism infrastructure rank

Air transport infrastructure rank

Ground transport infrastructure rank

France 1 5.9 2 5 2United States 2 5.8 1 2 6Canada 3 5.7 4 1 7United Arab Emirates 4 5.6 5 3 5Singapore 5 5.5 8 6 1Australia 6 5.3 3 4 9Barbados 7 5.3 6 10 4Japan 8 5.1 12 8 3Thailand 9 4.5 7 7 13Turkey 10 4.4 10 9 11Russian Federation 11 4.1 9 11 17South Africa 12 4.1 13 14 14Chile 13 4.0 11 17 12Mexico 14 3.9 16 15 15India 15 3.8 20 13 8China 16 3.6 21 12 10Brazil 17 3.6 15 15 21Argentina 18 3.4 14 19 19Peru 19 3.3 17 21 19Egypt 20 3.1 18 18 18Kenya 21 2.8 22 22 16Colombia 22 2.8 19 20 22

Sources: World Economic Forum, WTTC, Oxford EconomicsNote: Countries from the Americas are shaded in blueRanks and ratings are shaded using a colour scale, where green signifies strong performance and red signifies bad performance

Table 2.2: WEF infrastructure ratings by selected country by type (2013)

2.2 The outlook for the Americas’ Travel & Tourism investment spending

Given the relatively poor current state of Travel & Tourism related infrastructure within the Americas, the importance of the Travel & Tourism industry to the Americas and the link between infrastructure quality and the success of the Travel & Tourism sector, forecasts of Travel & Tourism investment should be of particular interest to industry stakeholders within the Americas.

WTTC forecasts that there will be US$3.6 trillion worth of Travel & Tourism investment made in the Americas over the next decade, which represents 28% of total world Travel & Tourism investment growth over the same period. As shown in Figure 2.3, within the Americas, the vast majority of the investment growth is expected to come from North America (70%), with Latin America and the Caribbean accounting for 28% and 2% of the growth in investment respectively.

Sources: World Economic Forum, WTTC, Oxford EconomicsNote: Countries from the Americas are shaded in blueRanks and ratings are shaded using a colour scale, where green signifies strong performance and red signifies weak performance

September 2014

13

Africa3%

Asia51%

Middle East3% Europe

15%

North America

70%

Latin America

28%

Caribbean2%

Americas28%

Figure 2.3: Source of future global and Americas Travel & Tourism investment spending growth (2014-24)

Sources: WTTC, Oxford Economics

When analysing projected Travel & Tourism investment spending growth, it is also important to consider the extent to which Travel & Tourism investment is ‘prioritised’ within a country’s overall investment, i.e. Travel & Tourism’s projected share of economy-wide investment. This analysis is strongly correlated with the contribution that the Travel & Tourism industry makes to the economy as a whole. It therefore comes as no surprise that for the Caribbean, where the industry makes a very high contribution to total economy GDP, Travel & Tourism investment is expected to make up a high relative share of total investment compared to the world average. In fact, all Americas’ sub-regions are forecast to have higher than world average relative shares of Travel & Tourism investment over the next decade.

Figure 2.3Source of future global and Americas Travel & Tourism investment spending growth (2014-24)

Source: WTTC

Figure 2.4Travel & Tourism investment share of total investment

Source: WTTC

12.0%6.8%

5.7%5.1%

4.8%4.7%4.7%

4.3%4.3%

0.0% 5.0% 10.0% 15.0%

CaribbeanLatin America

AfricaAmericas

EuropeNorth America

WorldMiddle East

Asia

Travel & Tourism investment spending (% total investment, ave. 2014-24)Sources: WTTC, Oxford Economics

Figure 2.4: Travel & Tourism investment share of total investment

Travel & Tourism investment in the Americas: Will the region’s infrastructure and investment constrain or support future industry growth?

14

The Americas’ forecast annual average growth of Travel & Tourism investment over the next decade (4.6%) is expected to lag behind the world average (5.1%). Within the Americas’ sub-regions, the slowest growth is forecast for the Caribbean (3.5%), followed by 4.4% annual average growth in North America and 5.2% growth in Latin America. Therefore, only Asia and the Middle East are ahead of Latin America in terms of expected Travel & Tourism investment growth to 2024, and indeed North America’s growth is forecast to be stronger than that of Europe, one of its key competitors in the industry. However, the forecast for the Caribbean is comparatively weak and may be considered a cause for concern, given the crucial contribution to GDP and employment that the industry makes in the region.

Figure 2.5Travel & Tourism investment spend outlook

Source: WTTC

2.3 Are the Americas on track to invest enough to address current infrastructure deficiencies

and realise the Travel & Tourism industry’s future demand and growth potential?

By analysing the projected growth in Travel & Tourism demand, the growth in Travel & Tourism related investment and the current quality of Travel & Tourism related infrastructure within individual countries in the Americas, it is possible to classify countries into typologies. This is useful to highlight specific threats and opportunities faced by individual countries. Figure 2.6 classifies countries into 5 distinct groups as described below:

Infrastructure constrained: With already poor quality and low capacity Travel & Tourism infrastructure and relatively slow investment growth forecast over the next decade compared to demand forecasts, these countries are at risk of not having the necessary quality and capacity of infrastructure to meet forecast demand projections. Consequently, the Travel & Tourism industries within these countries are likely to create less GDP and create fewer jobs than current forecasts predict.

6.4%5.5%

5.2%5.1%

4.6%4.4%4.4%

3.5%3.5%

0.0% 2.0% 4.0% 6.0% 8.0%

AsiaMiddle East

Latin AmericaWorld

AmericasAfrica

North AmericaEurope

Caribbean

Annual average growth in Travel & Tourism investment (2014-24)Sources: WTTC, Oxford Economics

Figure 2.5: Travel & Tourism investment spend outlook

September 2014

15

Improving infrastructure and growth prospects: Travel & Tourism infrastructure within these countries is currently relatively weak. However, with strong Travel & Tourism investment forecast over the next decade, these countries are likely to have the resources required to support and sustain projected demand, and improve the quality of their current Travel & Tourism infrastructure. This means that the Travel & Tourism industries within these countries are likely to realise current growth predictions and could perform more positively.

Balanced markets: Based on an analysis of current Travel & Tourism infrastructure, the outlook for Travel & Tourism investment and the outlook for Travel & Tourism demand, these countries are expected to strike an appropriate balance between supply-side quality and capacity and demand-side growth, meaning that these countries should be well placed to realise current Travel & Tourism growth forecasts.

At risk of complacency: Travel & Tourism infrastructure within these countries at present is of comparatively high quality and capacity. However, given the outlooks for Travel & Tourism investment and demand over the next decade, these countries are at risk of complacency and may see infrastructure quality decline in future (at least in relative terms), which could adversely impact upon the sector’s growth potential.

Stars or over-investors?: These countries currently possess a comparatively high quality of Travel & Tourism infrastructure, accompanied by strong forecast growth in Travel & Tourism investment over the next decade. The forecast scale of future investment will enable them to fully support and sustain projected levels of future demand, and maintain their high quality infrastructure. However, a downside risk is that over-investment could result in excess capacity and disappointing returns on investment.

Figure 2.6Country typologies

Greater current Travel & Tourism infrastructure quality

Sources: WTTC, Oxford Economics

Mor

e fa

vour

able

inve

stm

ent t

o de

man

d gr

owth

bal

ance

Improving infrastructure and growth prospects

Stars or over-investors?

Infrastructure constrained At risk of complacency

Balanced markets

Argentina,Bolivia,Brazil,Dominican Republic,Ecuador,

Chile,Mexico,Paraguay,Trinidad & Tobago

Barbados,Costa RicaPanama,Puerto Rico

Colombia, El Salvador,Guatemala,Guyana,Haiti,

Nicaragua,Peru,Uruguay,Venezuela

Canada,United States

Honduras,Jamaica,Suriname

Travel & Tourism investment in the Americas: Will the region’s infrastructure and investment constrain or support future industry growth?

16

chapter 3Summary - putting Travel & Tourism

investment on the agenda

• Travel & Tourism investment intensity over previous years drives current quality and capacity of Travel & Tourism related infrastructure;

• The quality and capacity of Travel & Tourism infrastructure is strongly correlated with industry performance; and

• Taking these two key relationships together, it can be deduced that there is a strong and positive relationship between Travel & Tourism investment and industry performance.

Investment in Travel & Tourism infrastructure is essential for the ongoing development and growth of the Travel & Tourism industry within the Americas. Indeed, statistical analysis shows that:

Given the relatively poor current state of Travel & Tourism related infrastructure within the Americas, the importance of the Travel & Tourism sector to the Americas and the link between infrastructure quality and capacity and the success of the Travel & Tourism sector, forecasts of Travel & Tourism investment should be of particular interest to industry stakeholders.

WTTC forecasts that there will be US$3.6 trillion worth of Travel & Tourism investment made in the Americas over the next decade. However, with the sector forecast to grow by an average of 3.7% per annum, and the lagging state of infrastructure today, it is of critical importance to determine whether baseline forecasts of Travel & Tourism investment will be enough to sustain and support future demand.

Across the region:

At a global macroeconomic level, it is expected that one of key trends over the next decade will be strong growth of economy-wide investment as normalisation of the beleaguered financial sector continues. Indeed, with large cash reserves, and confidence gradually being restored, investors and corporates from all over the world will be looking for opportunities to invest. This presents a crucial opportunity for the Americas to attract much needed investment for its Travel & Tourism infrastructure.

Governments within the region should act to ensure that they are an attractive location for this investment and that their countries do not fail to realise the economic benefits associated with Travel & Tourism growth due to a lack of infrastructure investment and poor quality and low capacity infrastructure. With many countries in other parts of the world waking up to the opportunities to be gained from Travel & Tourism, countries in the Americas need to act now ensure they increase their competitiveness for the future.

• In North America, Travel & Tourism infrastructure is of a generally high standard as compared to the world average and the rest of the Americas. However, certain aspects of its infrastructure, particularly its ground transport infrastructure, are less impressive when compared to other advanced economies and tourism competitors within developed Asia and continental Europe. Therefore, these nations need to be wary of complacency if they are to achieve the projected levels of demand growth over the next decade and maintain their current industry competitiveness ranking.

• For the Caribbean, where Travel & Tourism accounts for a larger share of the economy than any other sub-region in the Americas, significant Travel & Tourism investment will be essential in delivering and maintaining the infrastructure required to support projected growth. Certain parts of the Caribbean have poor current standards of Travel & Tourism related infrastructure and forecast investment spending within the industry over the next decade is unlikely to be sufficient to realise growth potential, while other parts need to pay attention to the threat of over-investment.

• In Latin America, much of the region has comparatively poor Travel & Tourism related infrastructure and together with investment versus demand forecasts, there is a strong possibility that other supply-side constraints such as lack of credit, availability of labour and availability of technology, may limit the sector’s growth within parts of the region over the next decade.

THE WORLD TRAVEL & TOURISM COUNCIL IS THE FORUM FOR BUSINESS LEADERS IN THE

TRAVEL & TOURISM INDUSTRY.

With the Chairs and Chief Executives of more than 100 of the foremost Travel & Tourism

companies as its Members, WTTC has a unique mandate and overview on all matters related to

Travel & Tourism.

WTTC works to raise awareness of Travel & Tourism as one of the world’s largest sectors,

supporting over 266 million jobs and generating 9.5% of global GDP in 2013.

WTTC produces comprehensive reports on an annual basis – to quantify, compare and forecast the economic impact of

Travel & Tourism on 184 economies around the world. Our reports highlight global trends, as well as focus on regions, sub-regions and economic and geographic groups. Further research

reports include those that benchmark the economic and employment contribution from

Travel & Tourism against a number of other industry sectors across 25 countries and others that look in detail at important

policy areas facing the sector.

The WTTC Americas’ Summit 2014 was held in Lima, Peru from 10-11 September 2014 with the theme of

“Facing Challenges, Finding Opportunities”.

To download reports and find out more, visit www.wttc.org

Harlequin Building65 Southwark Street

London, SE1 0HRUnited Kingdom

Telephone: +44 (0)20 7481 8007Fax: +44 (0)20 7488 1008Email: [email protected]

www.wttc.org

Related Documents