TRANSACTION trends The Official Publication of the Electronic Transactions Association | October 2011 ALSO INSIDE: The Latest on EMV in the U.S. Startup Focuses on Community Banks Learn how companies stack up in our first- ever mobile commerce providers guide in Mobile Payments Who’s Who

Transaction Trends

Mar 17, 2016

The Official Publication of the Electronic Transactions Association

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

TransacTiontrends

The Official Publication of the Electronic Transactions Association | October 2011

ALSO INSIDE:The Latest on EMV in the U.S.

Startup Focuses on Community Banks

Learn how companies stack up in our first-ever mobile commerce providers guide

in MobilePayments

Who’s Who

TransacTion trends | October 2011 3

The Official Publication of the Electronic Transactions Association Vol. 16 | No. 10

TransacTion trends

cover story

8 sPecIAL: Who’s Who in Mobile Payments By Bryan Ochalla The mobile payments market is ripe with opportunity, but does your company have a strategy for cashing in? Our first-ever Mobile Commerce Providers Guide takes the guess work out of finding key players to partner with in this growing market.

18 steady race to eMv Adoption By Julie Ritzer Ross From Visa’s moves to accelerate EMV technology to two top-10 banks issuing chip cards, EMV adoption in the United States is happening, but industry consensus and investment for migration remain unsettled.

FeAtUres

dePArtMents

4 President’s Message Insights from ETA’s elected leader

6 Industry news Trends, strategies, and news in the payments business

26 neW! etA new Member Listing

23 sPecIAL serIes startup stories: Art of the deal By John Manasso A former artist and founder of Acuity Payment Services applied lessons he learned in his past occupation—fulfilling promises, leveraging niches, and hiring an experienced staff—and watched his business thrive.

27 Ad Index

28 Industry Insider ControlScan helps small- and mid-sized merchants get compliant.

6

8

18

4 October 2011 | TransacTion trends

Electronic Transactions Association1101 16th Street NW, Suite 402Washington, DC 20036202/828.2635www.electran.org

ETA Chief Executive Officer Carla Balakgie

ETA Director, Communications & PR Thomas Goldsmith

Transaction TrendsPublishing office: Stratton Publishing & Marketing Inc.5285 Shawnee Road, Suite 510Alexandria, VA 22312703/914.9200

PublisherDebra Stratton

EditorJosephine Rossi

Contributing EditorAngela Hickman Brady

Editorial/Production AssistantTeresa Tobat

Art DirectorJanelle Welch

Contributing WritersJohn Manasso, Brian Ochalla, Julie Ritzer Ross

Advertising SalesSteve Schwanz or Fox Associates (800/440.0232; [email protected])

Fox Associates Offices Chicago 312/644.3888 New York 212/725.2106Atlanta 770/977.3225 Detroit 248/626.0511Los Angeles 805/522.0501 Phoenix 480/538.5021

Editorial Policy: The Electronic Transactions Association, founded in 1990, is a not-for-profit organization representing entities who provide transaction services between

merchants and settlement banks and others involved in the electronic transactions industry. Our purpose is to provide leadership in the industry through education, advocacy, and the exchange of information.

The magazine acts as a moderator without approving, disapproving, or guaranteeing the validity or accuracy of any data, claim, or opinion appearing under a byline or obtained or quoted from an acknowledged source. The opinions expressed do not necessarily reflect the official view of the Electronic Transactions Association. Also, appearance of advertisements and new product or service information does not constitute an endorsement of products or services featured by the Association. This publication is designed to provide accurate and authoritative information in regard to the subject matter covered. It is provided and disseminated with the understanding that the publisher is not engaged in rendering legal or other professional services. If legal advice and other expert assistance are required, the services of a competent professional should be sought.

Transaction Trends (ISSN 1939-1595) is the official publication, published monthly, of the Electronic Transactions Association, 1101 16th St. N.W., Suite 402, Washington, DC 20036; 800/695-5509 or 202/828-2635; 202/828-2639 fax. Postage paid at Pittsburgh, Pennsylvania, and additional mailing offices. POSTMASTER: Send address changes to the address noted above.

Copyright © 2011 The Electronic Transactions Association. All Rights Reserved, including World Rights and Electronic Rights. No part of this publication may be reproduced without permission from the publisher, nor may any part of this publication be reproduced, stored in a retrieval system, or copied by mechanical photocopying, recording, or other means, now or hereafter invented, without permission of the publisher. Nonmembers, government agencies, $150 per year; single copy, $20. Subscriptions are available for 12-month periods only, at the quoted rates.

Volunteers: ETA’s Lifeblood

Next month, many of you will receive a letter from ETA confirming your place on one of the dozen or so ETA standing committees and task forces for 2012.

As I said when I began my term as president of ETA, volunteers are the backbone of the association. Those who serve on the committees are the core of ETA’s volun-teers. They provide their time and their expertise to ETA and expect nothing in the way of what we normally think of as compensation. That doesn’t mean they’re not rewarded; the benefits of giving, however intangible, often exceed the cost.

Committee members are a window on the industry for ETA’s staff. They generate new ideas, provide valuable services to ETA’s membership, and much more. They contribute much of the content and structure at ETA’s meetings. They provide the analysis and insight that is the foundation for our advocacy efforts, and they keep the entire membership of ETA informed about the trends afoot in areas like technology

and risk management. Those who will take up new committee assignments in

2012 have the gratitude and admiration of ETA’s board, officers, and staff. They will be the core of ETA’s community for the next year and be a big part of ETA’s success in 2012. They have a task before them: To keep the momentum from this year alive and take it to a new level, at a time when the payments indus-try faces many challenges in adapting to new technology, new government regulation, and a changing competitive landscape.

In return for engaging as a volunteer, ETA’s committee members will have the opportunity to forge new and lasting friendships and professional relationships, to grow personally and professionally, and to earn the respect and admiration of every-one in the ETA community.

So if you answered the call to be part of an ETA committee this time around, thank you. And if you haven’t considered doing so, please make a commitment to do so next year. It’s critical that ETA has a continual influx of new ideas and new energy so it can evolve and serve today’s members as well as tomorrow’s. The world of pay-ments is constantly challenging us to keep up. We can’t do it without you.

This issue of Transaction Trends will be distributed at ETA’s Strategic Leadership Forum and the associated Mobile Commerce Summit, so if you’re reading this in Chicago, welcome. Be sure to make the most of what the SLF has to offer. It’s a great opportunity to look down the road a bit further than we normally do and as quickly as our business is changing, that can be a tremendous advantage. I look forward to seeing you in Chicago.

Sincerely, Rick PylantRick Pylant is President of ETAand Chairman & CEO of Strategic Payment Systems Inc.

President’s Message

Las Vegas

an event by

BE PARTOF THE SMART SECURITYAND ADVANCED PAYMENTS EVENTDiscover new technologies and develop your business

CARTES

in North Ame

rica

Expo &Confer

ence

PAYMENT

MOBILITY

CONTACTLES

S

DIGITAL SEC

URITY

IDENTIFICAT

ION

SMART TEC

HNOLOGIES

AUTHENTICA

TION

More event news and information to exhibit, to speak or to attend on

www.cartes-NorthAmerica.com

MARCH 5-7,

2012

THE MIRAGE

HOTEL•LAS V

EGAS,NEVAD

A•USA

/3266

Annonce CARTES-209,5x276,2-v4:Mise en page 1 26/07/11 12:08 Page 1

6 October 2011 | TransacTion trends

inDusTrYnews

The first generation of NFC-enabled smartphones start hitting the market later this year, but the radio-chip maker Broadcom has announced that it’s ready to start production of a new chip that’s smaller, faster, more powerful, and uses less power than those now available.

The development is significant not for its direct impact on payments, but for its potential to spur adoption of NFC-enabled smart-phones and other devices by offering consumers new ways to use them for nonpayment functions. For example, NFC can be used to authenticate a device more easily and more securely than a Bluetooth pairing, making smartphones better for authentication purposes. It also could make phone-to-phone transfers of large files more feasible. And making it easier to connect the phone to other networks securely and easily could enable a host of new applications, some of which are still on the drawing boards.

Of course, once consumers buy smartphones—for whatever reason—con-verting them to mobile payments users will be much easier. Craig Ochikubo, vice president of the business unit that oversees NFC at Broadcom, says the company is excited about these new potential applications for NFC, but adds that Broadcom “can’t ignore mobile payments,” given that carriers, banks, and credit card companies all are going after the revenue stream involved.

New Chip Could Speed Adoption of NFC Smartphones

Compliance Now Drives EncryptionMeeting the requirements of PCI Data Secu-rity Standard and data security regulations in many states is now the number one reason that organizations of all sizes are investing heavily in encryption technology, according to the Ponemon Institute’s annual “U.S. Enter-prise Encryption Trends Report.”

Compliance concerns were cited by 69 per-cent of the 964 IT executives who responded to the Ponemon survey, up 5 percent from one year ago. The survey also found that 84 percent of respondents have either fully ex-ecuted or are in the process of implementing encryption, a two-point increase from 2009 and a five-point increase from 2008.

The study points out that the threat of stiff penalties for breaches where an organization is not in compliance has caught the attention of a large number of IT professionals working where sensitive data is handled.

info graph

ROAM Data has named Ken Paull executive vice president, a new position at the company. ControlScan, a provider of PCI compliance and security solutions for small merchants and acquirers, has entered into a referral partner agree-ment with Convey Compliance Systems, a provider of tax information reporting services and software. CHARGE Anywhere, provider of secure mobile payment and pay-ment gateway solutions, has won PA-DSS certification for version 2.0.0.17 of the CHARGE Anywhere Payment Ap-plication for Windows Mobile. First American Payment Systems, a merchant services acquirer, has expanded its recruiting team with the hire of Greg Carr as manager of strategic partnerships. Payment Alliance International has been named a 2011 Hot Dozen company by Greater Louisville Inc.’s EnterpriseCorp. Rick Pylant, chairman and president, and Jon Stevens, vice president, resigned their positions and separated from CoCard Marketing Group to start Strategic Payment Systems Inc., a new ISO. SunTrust Merchant Services has announced that it has selected SecurityMetrics’ new TIN Matching Service to streamline the matching process for a majority of its merchants.

AROUND THE HORN

Attrition risk

Portfolio-repricing efforts

Pricing transparency

Systems development

New product offering opportunities

Resource consumption

No/minimal impact

New customer acquisitions

Merchant Acquirers Assess Impact of Durbin Amendment

(Multiple responses per respondent)

61%

56%

33%

28%

22%

11%

11%

6% Source: Aite Group

transaction_trends_protection.indd 2 7/1/11 2:47 PM

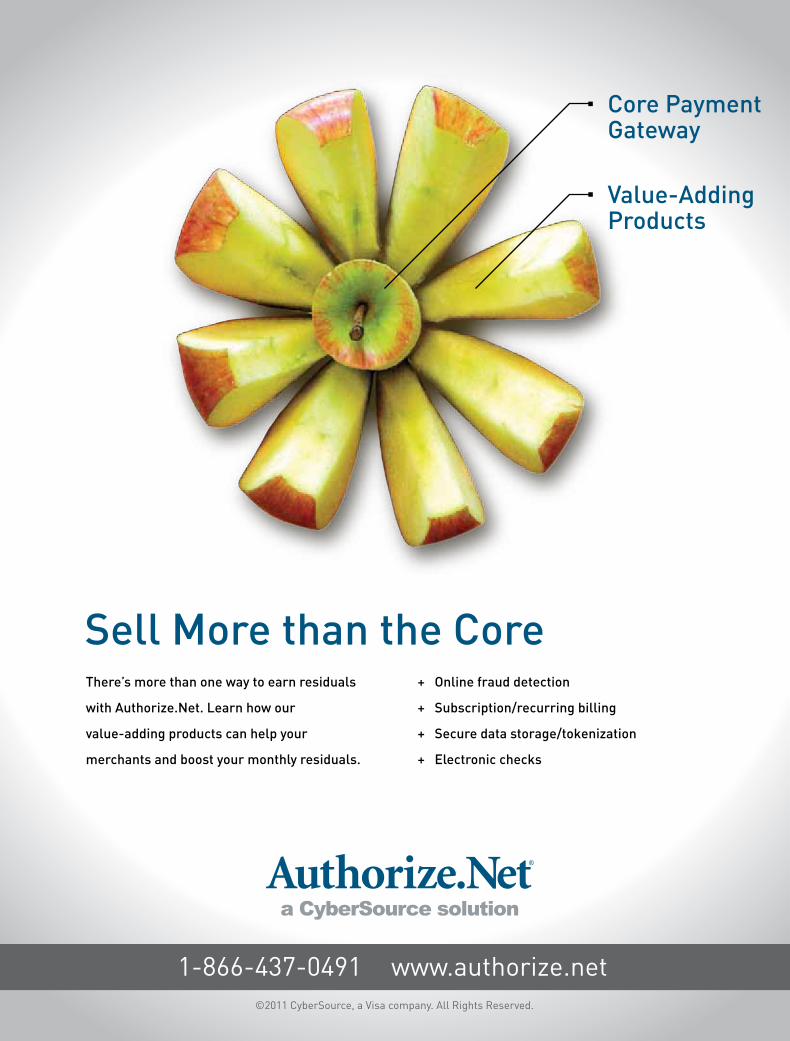

8 October 2011 | TransacTion trends

The mobile commerce market—elec-tronic payments initiated or accept-ed via mobile phone—is red hot. And by most expert accounts, this trend will only continue, consider-

ing that more consumers around the world own and use smartphones than ever before.

In the second quarter of this year, global sales of smartphones rose 74 percent year-over-year and accounted for 25 percent of overall sales (up from 17 percent in the same quarter of 2010), according to recent information from Stamford, Connecticut-based research firm Gartner Inc.

Even the current decline in credit card usage and ownership hasn’t stopped all of the major pay-ments players from implementing a mobile strat-egy, and retailers continue to invest in mobile apps and other solutions.

Should smaller players continue to follow suit? “I think every company involved in payments should have a mobile strategy at this point,” says Todd Ablowitz, president of Denver-based consultancy Double Diamond Group LLC. Those who don’t, he adds, “do so at their own peril.

“There will be winners and losers and con-solidation as we continue to see market up-take, just as there are with any other technol-

ogy rollout,” Ablowitz says, adding, “There’s going to be lots of chaos that will eventually turn into order.”

To that end, the staff at Transaction Trends com-piled this first-ever Mobile Commerce Providers Guide to offer readers a better understanding of the players in this space who provide opportuni-ties for business partnerships. For quick reference, we’ve classified each company’s products and services in up to six categories: mobile payments, mobile acceptance, mobile wallets, handsets, pre-paid and promotion (includes loyalty offerings), and person-to-person payments. These categories are designated by icons in each listing. We’ve also included basic contact information and details on how each company plans to get its mobile com-merce solution to market—via ISOs, directly to merchants, etc.

Aside from conducting internal research, we also reached out to the payments community, ask-ing mobile commerce providers to supply more information on their mobile products and services. But despite our best efforts, it is possible that our information is incomplete. We expect this resource, much like the mobile market itself, will evolve over time. In the meantime, we hope this guide will help you capitalize on this burgeoning market now. TT

By Bryan Ochalla

Who’s Who[ Mobile CoMMerCe Providers Guide ]

in Mobile PaymentsFrom mobile acceptance to mobile wallets, our first-ever

Mobile Commerce Providers Guide makes sense of who is providing technologies and services

10 October 2011 | TransacTion trends

BUSINESS NAME BUSINESS DESCRIPTION

Alpha Card Services

Headquarters: Huntingdon Valley, PennsylvaniaWebsite: alphacardservices.comYear founded: 2000

Alpha Card Services offers businesses the mobility, security, and convenience of accepting credit cards through popular smartphones, such as the iPhone, Android, and BlackBerry. The company’s QwickPAY product can turn a merchant’s smartphone into a mobile processing terminal in a matter of minutes thanks to a free placement reader and downloadable software app.

QwickPAY is sold to merchants through an ISO sales force and various financial institution partnerships.

American Express

Headquarters: New York, New YorkWebsite: americanexpress.comYear founded: 1850

In late March, American Express unveiled Serve, a digital payment and commerce platform that the company says will provide consumers “a new way to spend, send, and receive money, with services that go beyond the existing global payment networks.” Serve allows people to make purchases and person-to-person payments using their mobile phones. Serve accounts can be funded from a bank account, debit, credit, or charge card, or by receiving money from another Serve account, and can be accessed using Serve Apple iOS and Android applications.

Serve is offered directly to consumers and merchants.

AnywhereCommerce

Headquarters: Montreal, CanadaWebsite: anywherecommerce.comYear founded: 2006

AnywhereCommerce is a global e-commerce and m-commerce payments technology engineering and solutions provider with patented and proprietary suites of hardware and software services for secure online and mobile card-present credit card, PIN debit, NFC, and EMV transactions. The company’s universal “aCommerce” platform can be used for e-commerce, m-commerce, P2P, and retail line-busting as well as traditional field services such as home repairs, delivery, or taxi services.

The aCommerce platform is sold via distributors, ISOs, OEMs, and VARs.

AppNinjas

Headquarters: Dublin, OhioWebsite: appninjas.comYear founded: 2009

With the Swipe mobile payment application from AppNinjas, anyone who conducts business outside a traditional office or retail setting can accept credit card payments on their iPhone, iPad, or iPod touch. The simple-to-use app makes it possible for businesses and nonprofits to accept credit cards anywhere.

AppNinjas’ Swipe app is available to the public for download through Apple’s App Store for $0.99.

Apriva

Headquarters: Scottsdale, ArizonaWebsite: apriva.comYear founded: 1999

AprivaPay is a full-featured payment application designed for both smartphones (Windows Mobile, iPhone, BlackBerry, and Android) and browser-capable mobile phones, and it offers integration with optional printers/readers as well as other functionalities that enable merchants to better serve customers. Apriva’s Payment Gateway connects merchants (from single-person entities to enterprises), processors, and card brands to ensure the integrity of the transaction ecosystem.

Apriva’s mobile solutions are available through merchant acquirers and processors.

Charge Anywhere

Headquarters: South Plainfield, New JerseyWebsite: chargeanywhere.comYear founded: 2004

Charge Anywhere’s Mobile Payment Solution enables merchants to accept payment from any mobile device. The solution, which is compatible with all major payment processors, also allows them to securely complete transactions in seconds by swiping credit cards and printing receipts with optional peripherals, such as a Bluetooth card reader/receipt printer or audio jack card reader.

Charge Anywhere’s Mobile Payment Solution is provided to merchants through acquiring banks, ISOs, MSPs, and processors.

[ Mobile CoMMerCe Providers Guide ]

mobile payments mobile wallets prepaid and promotion

mobile acceptance handsets person-to-person payments

2011 WinnerShark Tank Innovation Awardmidwestacquirers.com

2011 WinnerTechnology Innovation Awardelectran.org

Paycloud is a registered trademark of SparkBase, Inc. iPhone is a registered trademark of Apple, Inc. SparkBase has no commercial association with Apple, Inc. or its products.

Simple. Secure. Integrated.

The only mobile wallet that works with your existing terminals and extends your gift and loyalty programs to more than 50 million smartphone users.

Don’t wait for NFC. Paycloud will be available nationwide beginning Q4 2011.

View a demo at sparkbase.com/paycloud or call 877-797-7275 to learn more.

®

12 October 2011 | TransacTion trends

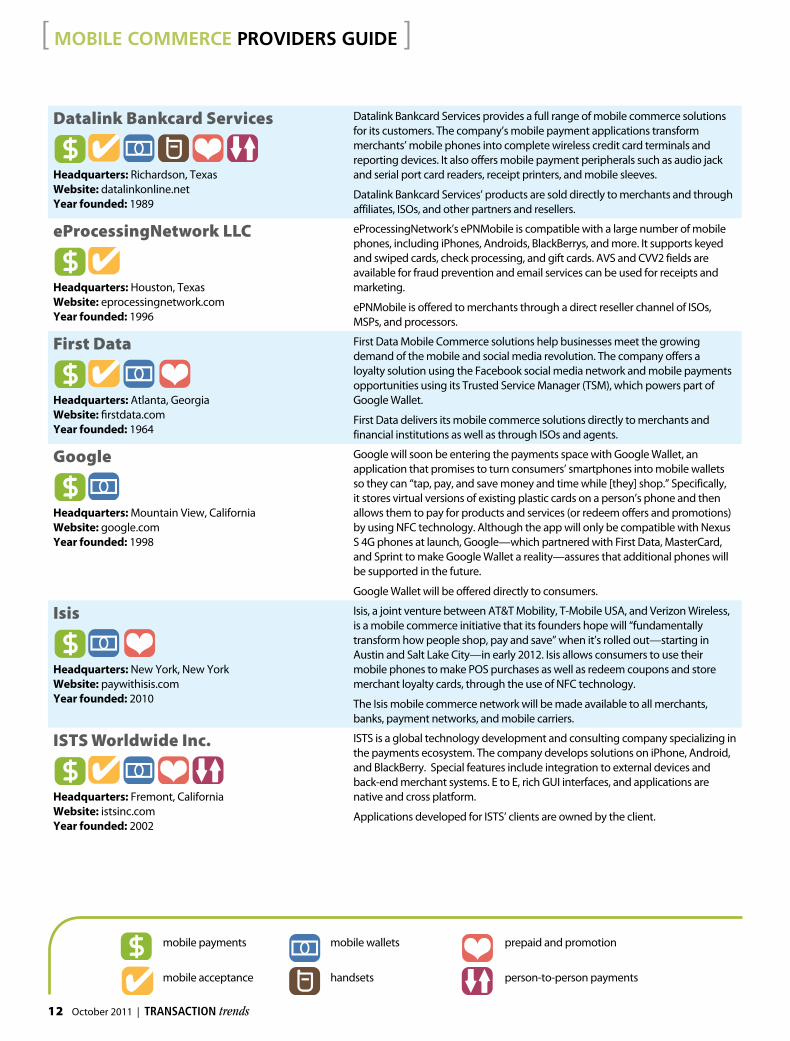

Datalink Bankcard Services

Headquarters: Richardson, TexasWebsite: datalinkonline.netYear founded: 1989

Datalink Bankcard Services provides a full range of mobile commerce solutions for its customers. The company’s mobile payment applications transform merchants’ mobile phones into complete wireless credit card terminals and reporting devices. It also offers mobile payment peripherals such as audio jack and serial port card readers, receipt printers, and mobile sleeves.

Datalink Bankcard Services’ products are sold directly to merchants and through affiliates, ISOs, and other partners and resellers.

eProcessingNetwork LLC

Headquarters: Houston, TexasWebsite: eprocessingnetwork.comYear founded: 1996

eProcessingNetwork’s ePNMobile is compatible with a large number of mobile phones, including iPhones, Androids, BlackBerrys, and more. It supports keyed and swiped cards, check processing, and gift cards. AVS and CVV2 fields are available for fraud prevention and email services can be used for receipts and marketing.

ePNMobile is offered to merchants through a direct reseller channel of ISOs, MSPs, and processors.

First Data

Headquarters: Atlanta, GeorgiaWebsite: firstdata.comYear founded: 1964

First Data Mobile Commerce solutions help businesses meet the growing demand of the mobile and social media revolution. The company offers a loyalty solution using the Facebook social media network and mobile payments opportunities using its Trusted Service Manager (TSM), which powers part of Google Wallet.

First Data delivers its mobile commerce solutions directly to merchants and financial institutions as well as through ISOs and agents.

Headquarters: Mountain View, CaliforniaWebsite: google.comYear founded: 1998

Google will soon be entering the payments space with Google Wallet, an application that promises to turn consumers’ smartphones into mobile wallets so they can “tap, pay, and save money and time while [they] shop.” Specifically, it stores virtual versions of existing plastic cards on a person’s phone and then allows them to pay for products and services (or redeem offers and promotions) by using NFC technology. Although the app will only be compatible with Nexus S 4G phones at launch, Google—which partnered with First Data, MasterCard, and Sprint to make Google Wallet a reality—assures that additional phones will be supported in the future.

Google Wallet will be offered directly to consumers.

Isis

Headquarters: New York, New YorkWebsite: paywithisis.comYear founded: 2010

Isis, a joint venture between AT&T Mobility, T-Mobile USA, and Verizon Wireless, is a mobile commerce initiative that its founders hope will “fundamentally transform how people shop, pay and save” when it’s rolled out—starting in Austin and Salt Lake City—in early 2012. Isis allows consumers to use their mobile phones to make POS purchases as well as redeem coupons and store merchant loyalty cards, through the use of NFC technology.

The Isis mobile commerce network will be made available to all merchants, banks, payment networks, and mobile carriers.

ISTS Worldwide Inc.

Headquarters: Fremont, CaliforniaWebsite: istsinc.comYear founded: 2002

ISTS is a global technology development and consulting company specializing in the payments ecosystem. The company develops solutions on iPhone, Android, and BlackBerry. Special features include integration to external devices and back-end merchant systems. E to E, rich GUI interfaces, and applications are native and cross platform.

Applications developed for ISTS’ clients are owned by the client.

mobile payments mobile wallets prepaid and promotion

mobile acceptance handsets person-to-person payments

[ Mobile CoMMerCe Providers Guide ]

© 2011 DFS Services LLC.

Agency Approvals: INITIALS DATE

Proofreader _______ _______

Copywriter _______ _______

Art Director _______ _______

Creative Director _______ _______

Account Exec. _______ _______

Supervisors: INITIALS DATE

Project Mgr. _______ _______

Acct. Sup. _______ _______

Prod. Mgr. _______ _______

Client Approval: INITIALS DATE

_______ _______

A0303-1 • Discover Network Dupe from A0115 by: jm

Path: Production 1:Discover Network:Jobs:A_ Proof #2

Trim: 8.25"w x 10.875"h Bleed: 8.5"w x 11.125"h Live: 7.75"w x 10.375"h

Page 1 of 1 Date: 8/24/11

Inks: 4/C Revised by: jm CPS CheckOut: _________

DiscoverNetwork.com

Around the corner and around the world, more cardmembers are making their card purchases on the Discover® network. With an expanding global reach and more acceptance partners than any other network, see how Discover can be your gateway to new business.

From St. Louis to St. Lucia.

JOB #: A0303

TITLE: ST. LOUIS

PRINT PRODUCER: MATT

PROJECT MANAGER: JENNIFER BECK

ACCOUNT MANAGER: WARREN

ART DIRECTOR: CIMA

SHIP: 8/26/11

PUBLICATION & INSERTION DATE:

ISO & Agent 10/1/11

A0303-1_8.25x10.875St.Louis.indd 1 8/25/11 3:10 PM

14 October 2011 | TransacTion trends

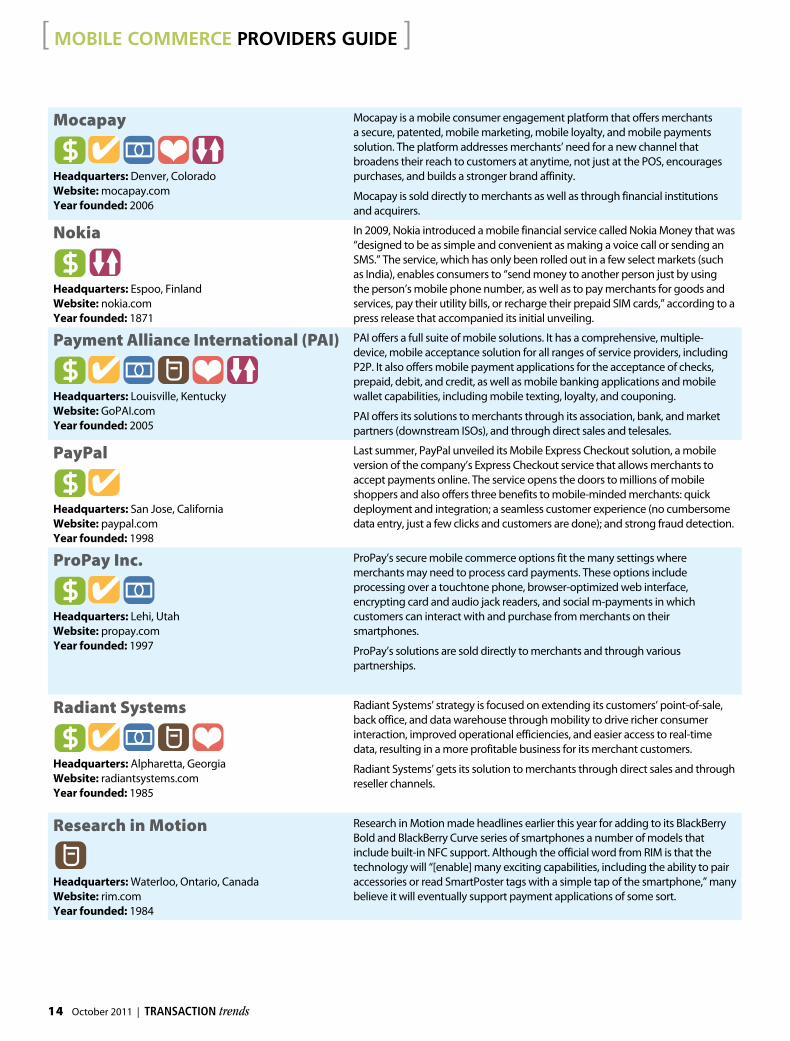

Mocapay

Headquarters: Denver, ColoradoWebsite: mocapay.comYear founded: 2006

Mocapay is a mobile consumer engagement platform that offers merchants a secure, patented, mobile marketing, mobile loyalty, and mobile payments solution. The platform addresses merchants’ need for a new channel that broadens their reach to customers at anytime, not just at the POS, encourages purchases, and builds a stronger brand affinity.

Mocapay is sold directly to merchants as well as through financial institutions and acquirers.

Nokia

Headquarters: Espoo, FinlandWebsite: nokia.comYear founded: 1871

In 2009, Nokia introduced a mobile financial service called Nokia Money that was “designed to be as simple and convenient as making a voice call or sending an SMS.” The service, which has only been rolled out in a few select markets (such as India), enables consumers to “send money to another person just by using the person’s mobile phone number, as well as to pay merchants for goods and services, pay their utility bills, or recharge their prepaid SIM cards,” according to a press release that accompanied its initial unveiling.

Payment Alliance International (PAI)

Headquarters: Louisville, KentuckyWebsite: GoPAI.comYear founded: 2005

PAI offers a full suite of mobile solutions. It has a comprehensive, multiple-device, mobile acceptance solution for all ranges of service providers, including P2P. It also offers mobile payment applications for the acceptance of checks, prepaid, debit, and credit, as well as mobile banking applications and mobile wallet capabilities, including mobile texting, loyalty, and couponing.

PAI offers its solutions to merchants through its association, bank, and market partners (downstream ISOs), and through direct sales and telesales.

PayPal

Headquarters: San Jose, CaliforniaWebsite: paypal.comYear founded: 1998

Last summer, PayPal unveiled its Mobile Express Checkout solution, a mobile version of the company’s Express Checkout service that allows merchants to accept payments online. The service opens the doors to millions of mobile shoppers and also offers three benefits to mobile-minded merchants: quick deployment and integration; a seamless customer experience (no cumbersome data entry, just a few clicks and customers are done); and strong fraud detection.

ProPay Inc.

Headquarters: Lehi, UtahWebsite: propay.comYear founded: 1997

ProPay’s secure mobile commerce options fit the many settings where merchants may need to process card payments. These options include processing over a touchtone phone, browser-optimized web interface, encrypting card and audio jack readers, and social m-payments in which customers can interact with and purchase from merchants on their smartphones.

ProPay’s solutions are sold directly to merchants and through various partnerships.

Radiant Systems

Headquarters: Alpharetta, GeorgiaWebsite: radiantsystems.comYear founded: 1985

Radiant Systems’ strategy is focused on extending its customers’ point-of-sale, back office, and data warehouse through mobility to drive richer consumer interaction, improved operational efficiencies, and easier access to real-time data, resulting in a more profitable business for its merchant customers.

Radiant Systems’ gets its solution to merchants through direct sales and through reseller channels.

Research in Motion

Headquarters: Waterloo, Ontario, CanadaWebsite: rim.comYear founded: 1984

Research in Motion made headlines earlier this year for adding to its BlackBerry Bold and BlackBerry Curve series of smartphones a number of models that include built-in NFC support. Although the official word from RIM is that the technology will “[enable] many exciting capabilities, including the ability to pair accessories or read SmartPoster tags with a simple tap of the smartphone,” many believe it will eventually support payment applications of some sort.

[ Mobile CoMMerCe Providers Guide ]

TransacTion trends | October 2011 15

SparkBase

Headquarters: Cleveland, OhioWebsite: sparkbase.comYear founded: 2004

SparkBase’s Paycloud transforms merchants’ iPhones or Android smartphones into mobile wallets that enable loyalty rewards, deliver merchant coupons, and process payments. Paycloud is built on the SparkBase technology platform that supports thousands of merchant loyalty programs in eight countries.

SparkBase works with its ISO partners to promote Paycloud and to train their merchants to use and promote the Paycloud network.

Square

Headquarters: San Francisco, CaliforniaWebsite: squareup.comYear founded: 2009

The Square card reader allows anyone to accept credit cards anywhere on their mobile device, while the Square card case enables individuals to discover local businesses, browse menus, open a tab, and pay with their name.

Square’s solutions are offered directly to merchants.

Street Savings

Headquarters: Orange, CaliforniaWebsite: streetsavings.comYear founded: 2006

Street Savings provides mobile marketing solutions for merchants, acquiring banks, and ISOs by mobilizing their gift and loyalty programs. The company’s Mobile Rewards and Mobile Coupons products utilize mobile text messaging in coordination with existing payment networks, credit card terminals, and POS systems to enable merchants to market directly to customers’ mobile devices via text marketing campaigns.

Street Savings’ products are made available to small- to medium-sized merchants and businesses through agents and resellers.

TF Payments Inc.

Headquarters: Irvine, CaliforniaWebsite: focuspay.comYear founded: 2009

TF Payments offers FocusPay, which helps large and small businesses get paid for goods and services using their Apple, Android, and BlackBerry smartphones and tablets instead of cash registers and other traditional credit and debit card readers.

Businesses that accept payments remotely are the primary target of FocusPay, which is made available through authorized resellers/retailers and dealers.

TrustCommerce

Headquarters: Irvine, CaliforniaWebsite: trustcommerce.comYear founded: 2000

TrustCommerce Mobile Payment Solution is a proprietary mobile solution for merchants to accept credit cards, PIN-less debit, and ACH in the field. Available through popular mobile devices, merchants can securely capture payments in card-present or card-not-present environments.

TrustCommerce Mobile Payment Solution is sold directly to merchants.

TSYS

Headquarters: Columbus, GeorgiaWebsite: tsys.com/acquiringYear founded: 1983

TSYS’ Mobile Payment Acceptance is a smartphone-based payments application that allows on-the-move merchants to accept and process card payments anywhere they have mobile service. Mobile Payment Acceptance is supported on iPhone and BlackBerry phones and can be paired with a portable card reader/receipt printer to qualify for card-present interchange rates.

Mobile Payment Acceptance is brought to market (i.e., merchants) through merchant acquirers and ISOs.

USA ePay

Headquarters: Los Angeles, CaliforniaWebsite: usaepay.comYear founded: 1998

USA ePay’s Wireless ePay solution allows retail and swipe merchants to accept credit card payments through their existing mobile device on any cellular service provider. Merchants are able to view detailed reports, as well as graphs and charts, of all transactions for the life of the account. Merchants also can email, download, and export their transaction reports. All transactions processed through the Wireless ePay software pass through a secure socket layer (SSL) for data encryption.

USA ePay’s Wireless ePay is offered to merchants through a number of resellers.

mobile payments mobile wallets prepaid and promotion

mobile acceptance handsets person-to-person payments

16 October 2011 | TransacTion trends

VeriFone Systems Inc.

Headquarters: San Jose, CaliforniaWebsite: verifone.comYear founded: 1981

VeriFone’s NFC payment solutions build loyalty, deliver precisely targeted coupons, and provide product information or sign up subscribers. VeriFone’s PAYMEDIA Solutions, launched earlier this year, is a subscription-based offering that provides merchants with payment-enabled media at checkout, including digital couponing, loyalty, location-based social media, and value-added services. PAYMEDIA builds on VeriFone’s PAYware Connect gateway services to integrate traditional payment authorization with nontraditional payment-enabled media and services that accommodate consumer mobile phones.

Acquirers and ISOs help bring VeriFone’s mobile commerce solutions to market.

Visa

Headquarters: San Francisco, CaliforniaWebsite: visa.comYear founded: 1970

Visa is busy prepping what it is calling a “digital wallet and services platform” it expects to launch in Canada and in the United States later this year. The digital wallet—which is being readied with the help of leading payments card issuers, community banks, credit unions, acquirers, payments processors, and merchants—will store Visa and nonVisa payments accounts, support NFC payments through the Visa payWave application, and deliver a wide range of transaction services to accommodate multiple commerce scenarios—including e-commerce, mobile commerce, micropayments, social networks, and person-to-person payments.

Visa’s digital wallet service will be offered directly to consumers/merchants.

ViVOtech Inc.

Headquarters: Santa Clara, California Website: vivotech.comYear founded: 2001

ViVOtech is a NFC software and systems company, enabling rich mobile commerce solutions for in-store payment, loyalty, marketing, and merchandising. ViVOtech’s end-to-end solutions enable over-the-air (OTA) card issuance, card management, and contactless POS card acceptance at merchant locations. Consumers can download their credit, debit, prepaid, or loyalty cards securely to their mobile phones and use them to shop, receive and redeem offers, earn loyalty points, and make payments.

ViVOtech’s solutions are available to vendors directly and through ISOs.

[ Mobile CoMMerCe Providers Guide ]

18 October 2011 | TransacTion trends

As Visa, Walmart, and others speed toward EMV adoption, U.S. players’ support for the global Europay/

MasterCard/Visa standard surges

[ feature ]

Steady Race to EMV Adoption

Few issues in the electronic payments industry have been more widely debated than when the United States will see mainstream adoption of the EMV (Europay/MasterCard/Visa) global standard for interoperation of integrated circuit cards (IC cards or “chip” cards) and IC-enabled POS terminals.

Overseen by EMVCo LLC—jointly owned by American Express Co., JCB International Credit Card Co., MasterCard, and Visa—the standard was rolled out in the United Kingdom in May 1997 and has garnered world-wide acceptance even in North America, with the exception of the U.S. That is, until now.

“Comments from many U.S.-based organizations over the past few years have been along the lines of, ‘We will bypass EMV; we don’t need it,’ ‘It will come, but when we are ready,’ and, ‘It’s too expensive to do now,’” comments Kishalay Kumar Anal of ISTS Worldwide, a retail and payment technology provider with U.S. headquarters in Fremont, California.

EMV will “come to the U.S. now sooner, rather than later,” he says, for several reasons. One is the increased incidence of credit card fraud, which EMV effectively quashes because it relies on two factors (a chip and a PIN or, less commonly, a chip and a signature), rather than a single fac-tor, for cardholder authentication. A growing desire for worldwide payment technology interoperability also is pushing the envelope, as is consumer backlash resulting from the refusal of fraud-wary merchants abroad to accept magnetic stripe cards.

Ignition PointOn August 9, Visa revealed plans to accelerate adoption of contact and contactless chip technology via three initiatives:

• For starters, the issuer is expanding its Technology

KE Y NOTES8 Visa’s moves to accelerate adoption of contact and contactless chip technology via three major initiatives—including PCI DSS deferments—could spur further development in the EMV realm.

8 Some believe a single EMV implementation “road map” that reflects a consensus of industry groups is needed in order for widespread migration to occur.

8 Some experts predict merchants will balk at the significant investment in hardware, integration, and testing needed to execute a conversion to EMV-enabled card readers and POS kiosks. Some estimates put the tab at $35 billion.

8 Even with the best road map in hand and major obstacles overcome, U.S. deployment could take up to 10 years.

By Julie Ritzer Ross

TransacTion trends | October 2011 19

Innovation Program (TIP) to U.S. merchants. Made available to international merchants effective March 31, TIP recognizes the se-curity benefits of dynamic authentication enabled by EMV chip and offers tangible benefits to merchants that update their POS technology to accept chip cards. Effective Oct. 1, 2012, Visa will expand TIP by elimi-nating the requirement for eligible U.S. mer-chants to annually validate their compliance with PCI DSS for any year in which at least 75 percent of their Visa transactions origi-nate from chip-enabled terminals. The latter must support both contact and contactless

chip acceptance, including mobile contact-less payments that leverage NFC technology.

• Visa has instituted a mandate that by April 1, 2013, U.S. acquirer processors and sub processors must be able to support merchant acceptance of chip transactions. This will require service providers to carry and process additional data encompassed in such transactions, including the crypto-graphic message that renders each transac-tion unique.

• Visa will implement what it deems a “U.S. liability shift” for domestic and cross-border counterfeit card-present POS trans-actions, effective Oct. 1, 2015 (or, for mer-chants that sell fuel through automated fuel dispensers, Oct. 1, 2017). Counterfeit card-present fraud is presently absorbed by card issuers. However, under the umbrella of the liability shift, if a contact chip card is pre-sented to a merchant that has not adopted, at minimum, contact chip terminals, liability for counterfeit fraud may shift to the mer-chant’s acquirer.

“Other developments are going to play a part in getting EMV to where it really should be here, but the Visa initiatives re-ally represent the necessary ‘ignition point’

to spark a migration to the technology,” says Randy Vanderhoof, executive direc-

tor of the Smart Card Alliance. “I think some of the delay on merchants’ part stems from the fact that they were waiting for a road map from card companies as to what technolo-gies to invest in. Now that Visa has signaled that the future will include contact chips and mobile contactless payments, they know what the next generation of payments will look like.”

The initiatives will truly fuel issuers’ EMV fire and accelerate the migra-tion trajectory, agrees Chris Cox, vice presi-dent, product de-velopment, in the mobile solutions group at First Data. “This is

truly a watershed event; the incentives are very compelling for stakeholders across the board,” he says. “The prospect of bypassing PCI compliance validation is attractive,” and the liability shift should be a major boon to chip adoption because any “chip-on-chip” transaction or chip card read by a chip ter-minal provides the dynamic authentication data that helps to better protect all parties. The U.S. is the only country in the world that has not committed to either a domestic or cross-border liability shift associated with chip payments, Cox points out.

Banks and Merchants Join the Race But EMV’s progress in the U.S. isn’t limited to issuer initiatives. In mid-April, two top-10 U.S. banks—spurred by a push to accom-modate frequent travelers who had made clear their displeasure at experiencing diffi-culty in executing transactions abroad with magnetic stripe cards—announced plans to issue smart cards based on the EMV chip card standard. The first such issuer, JPMorgan Chase & Co., shortly thereafter introduced a chip-and-signature technol-ogy to holders of its high-end Palladium credit card. Chip-and-signature cards were made available to individuals holding the J.P. Morgan Select Visa Signature card. Both cards also have magnetic stripes, enabling them to be used wherever magnetic strip cards are accepted.

Wells Fargo & Co., the second issuer, be-gan in mid-summer to issue chip cards to 15,000 credit card customers who frequent-ly travel abroad.

The moves by JPMorgan Chase and Wells Fargo follow on the heels of forays into EMV by North Carolina’s State Employees Credit Union, the nation’s second-largest credit union, and the 88,000-member, $3.1 billion United Nations Federal Credit Union (UNFCU) in Long Island City, New York. State Employees Credit Union is currently replacing its one million traditional magnet-ic stripe cards with EMV cards; the project is slated to wrap up by year-end. UNFCU has already completed the transition, which it reportedly made in part as a response to negative feedback from customers whose magnetic stripe cards had been rejected

20 October 2011 | TransacTion trends

abroad, especially for offline transactions executed at unattended kiosks and in taxis.

Fierce competition will likely spur many more initiatives. “For cardholders, it’s embarrassing to be at the head of a queue in a store, only to be told that that store doesn’t accept cards without chips and asked to pay cash or in some other way,” Anal says. “Who will get the blame? The bank that issued the card—and cardholders not only won’t use it in the future; they will be more likely to move to an issuer that provides chip-based EMV cards. We expect to see—and it’s already started—U.S. issuers go to EMV technology before they lose too many customers they will potentially never recover.”

Initiatives are brewing in the merchant sector as well. A handful of players were already charting EMV waters before Visa revealed its plans for the expansion of TIP to the U.S.

On the “pure” retail side, Walmart Stores Inc. has equipped its more than 4,000 U.S. stores with chip-and-PIN EMV-enabled POS terminals, Jamie Henry, the chain’s senior director of payments services, reported at the Smart Card Alliance’s 2011 conference in April 2011.

In part, Walmart made the move to chip-and-PIN to offer cus-tomers the “most secure environment” through which to pay for merchandise; patrons like the assurance that by inputting a PIN number for each transaction, they eliminate the transmission of unsecured data and, in turn, the risks of sharing personal infor-mation with merchants, banks, and e-commerce sites, Henry told Smart Card Alliance attendees. Additionally, the retailer likes the fact that the heightened fraud protection afforded by EMV re-duces or wipes out unnecessary fraud-related expenditures, for instance, PCI compliance costs.

Walmart would prefer magnetic stripe cards go the way of the dinosaur, with chip-and-PIN cards taking their place. “We want to eliminate the fraud-prone mag stripe,” Henry says. “It has served its purpose.” The chain is “encouraged” by banks’ recent initiatives to issue EMV cards to U.S. customers, but prefers the industry move beyond such limited issuance. Walmart in May became one of several technical associates—and the sole retailer—to take a seat on EMVCo’s Board of Advisors.

Target and Nordstrom are among other retailers that have dem-onstrated support of EMV. “Visa’s plan to encourage this adoption and lay the groundwork (for EMV) and mobile payments is a posi-tive development,” says Kevin Knight, executive vice president of Nordstrom Inc.

EMV activity is heating up in the hospitality subsector, too. McDonald’s Corp., which has already rolled out contactless chip terminals in its U.S. restaurants, intends to go a step further to take advantage of “the security benefits of EMV chip and dynamic authentication,” says Dave Weick, McDonald’s chief information officer and senior vice president, shared services.

These examples are only the tip of the iceberg. “Although nothing will happen at lightning speed or anything approach-ing it, merchants will, in an effort to prevent themselves from becoming easy targets of fraud as their (competitors) shore up with EMV, get on board,” suggests Scott Goldthwaite, senior vice president, product management and marketing, of processor Planet Payment in Long Beach, New York.

Help your merchants reach their global potentialPlanet Payment’s multi-currency payment solutions can help your merchants increase global sales while significantly growing the profitability of your portfolio. Talk to us and discover our robust FX revenue-sharing program and opportunities in the US & Canada.

To get started, call Planet Payment at (800) 489-0174 or visit us at www.planetpayment.com/ETA2011

Planet Payment thanks you for another successful ETA!

One Partner.One Platform.

60+ CURRENCIES1 MERCHANT ACCOUNT0 HASSLES

pp-eta-transaction-trends-postETA-3.5x9.5-FINAL.ai 1 4/26/2011 11:26:20 AM

TransacTion trends | October 2011 21

In the hotel subsector, Goldthwaite notes, EMV deployment will begin with operators that cater to chip card-bearing travelers from abroad. However, as hoteliers refresh their POS and property management systems and deal with PCI compliance, the number of operators making a switch to EMV will ex-pand by leaps and bounds, he says.

“It’s not just the rising volume of fraud, and the fact that the U.S. has become low-hanging fruit for fraudsters because other parts of the world have moved to EMV, that will drive merchants forward,” adds Vander-hoof. “Merchants’ increased unhappiness with the high cost of meeting strict PCI compliance standards is also a factor.”

Detours AheadWhile recent developments indicate that EMV is moving closer to the mainstream, both short- and long-term uncertainties and obstacles remain.

Logistics pose significant questions and challenges. Notably, MasterCard, American Express, and Discover remain noncommit-tal about their plans to follow Visa down the EMV path. For MasterCard, neither con-sumer demand nor market economics have justified boarding the EMV bandwagon yet, says Seth Eisen, a spokesperson for the as-sociation. MasterCard is currently assisting its customers in understanding “what the implications of EMV and other technolo-gies in the U.S. would be,” Eisen continues. “Any migration must take into account all customer and consumer interests if a col-lective effort is to be successful. Obviously, Visa’s decision will impact market direc-tion, and we will continue to consider our actions accordingly.”

For its part, American Express reveals only that it does issue chip cards in some markets, like the United Kingdom, but has not received a large number of requests for EMV-enabled cards from cardmembers in the U.S. “While we cannot comment on any future plans, we are always looking to best serve our cardmembers and anticipate their needs,” says spokesperson Elizabeth Crosta.

Unless MasterCard, American Express, and Discover introduce EMV adoption programs similar to Visa’s, merchants will be forced to validate PCI compliance to these other card brands each year, warned Avivah Litan, a vice president and distinguished analyst for Gartner Research, in an August 9 blog entry.

Most Level 1 and the majority of Level 2 and 3 merchants are already PCI compliant, Litan asserts. Accordingly, while they may eventu-ally save about $30,000 to $55,000 on the annual cost of PCI audits and assessments if MasterCard and American Express adopt EMV, they will incur expenditures of $30 per payment terminal upgrade to enable chip payments, plus unpublished activation, in-stallation, and maintenance fees. For a ma-jority of large merchants, Litan contends, the price of upgrades alone “will almost surely” surpass yearly PCI audit fees.

Litan adds that because at least 75 per-cent of their Visa transactions must originate from chip-enabled terminals if they are to skip PCI compliance validation as permit-ted under terms of the incentive, “merchants won’t stand a chance of gaining the benefit of not having to validate PCI compliance an-nually until at least 2016 or later.” This, she emphasizes, is “well after most will have spent all the money on terminal upgrades and years of annual PCI audits.”

Moreover, some observers believe a sin-gle EMV implementation “road map” that reflects a consensus of industry groups is

needed in order for widespread migration to occur. The road map must address sev-eral key questions, including whether cards will be chip-and-PIN, chip-and-signature, or a combination thereof and whether all EMV-enabled systems will incorporate mobile ca-pabilities, suggests David Hogan, executive technology advisor for the National Retail Federation. A timeline for banks to begin is-suing EMV-enabled cards constitutes anoth-er key component of the road map, Hogan says, as do methodologies for authenticat-ing cards (i.e., online, off-line, or both), and a “go-forward” strategy for card-not-present transactions.

Visa and MasterCard have released stan-dards for using EMV cards to support the latter; these encompass the Visa Dynamic Authentication Password (DPA) scheme and the MasterCard Chip Authentication Program (CAP)/EMV-CAP. However, other card brands have not yet followed suit, a fac-tor some industry pundits consider a fairly significant roadblock to EMV adoption.

On the technology front, experts predict many merchants will balk at the significant investment in hardware, integration, and

As widespread EMV technology adoption moves ever closer to becoming a reality in the U.S., many have questioned whether EMV and NFC technology can co-exist. The answer seems to be a resounding “yes.”

EMV and NFC are complementary technologies that round out and enhance each other, sources say. “EMV can authenticate a card, verify the identity of a cardholder, and protect cardholder data through the life of a transaction, while NFC is a fast, secure means of transmitting data between adjacent devices,” says Dale Laszig of Castles Technology Co.

In fact, Visa considers EMV deployment a step in preparing the U.S. payments infra-structure for the arrival of NFC-based mobile payments by creating the building blocks needed to accept and process chip transactions that support either a signature or PIN at the point of sale.

“NFC is an extension of EMV,” concurs Kishalay Kumar Anal of ISTS Worldwide. He notes that steps are being taken by vendors to bolster the co-existence of EMV and NFC. In August, he says, NFC software and systems vendor ViVOtech of Santa Clara, California, rolled out the ViVOpay 8100 terminal. The hardware can handle transactions executed via magnetic stripe, contact and contactless chip cards, and NFC-enabled mobile devices.

EMV + NFC = A Happy Marriage

22 October 2011 | TransacTion trends

testing needed to execute a conversion to EMV-enabled card read-ers and POS kiosks. By most estimates, the tab for U.S. merchants to get the job done will exceed $35 billion.

Walmart, whose net income reportedly totaled $17 billion for the fiscal year ending Jan. 31, 2011, “may, along with other large retailers, have the financial resources to go forward with EMV now,” says the director of information technology for one Tier 3 merchant. “But not all of us can say the same, and that is going to create some sort of bottleneck on the road to implementation.”

Beyond technology investments at the retail level, processing hosts will require updating in order to support EMV messaging formats. Acquirers and ISOs will need to update Tier 1 and Tier 2 support teams to manage the added complexity of EMV and the customized host interfaces maintained by card brand and payment networks as well as hardware manufacturers, cautions Dale Laszig, senior vice president, sales, Castles Technology Co. Ltd. in Hones-dale, Pennsylvania.

Although updating legacy infrastructure constitutes no small task, Laszig adds, the endeavor may not be as difficult as it could conceivably be because there’s the opportunity to learn from and

emulate the steps taken by players in nations that have already im-plemented EMV, among them Canada and the United Kingdom. “We also have a latecomer’s advantage of stepping into a mature, highly developed environment that includes EMV-certified equipment and host interfaces that are tested, proven, and ready to deploy,” Laszig says. “And although dealing with a large base of non-compliant POS products may seem like an obstacle, it is also a huge opportunity for terminal manufacturers” and, by extension, ISOs, to improve their product arsenals by refreshing product options and replacing outdated equipment.

Then, there’s the matter of time. Deployment of EMV in Canada took seven years. Even with the best road map in hand and ma-jor obstacles overcome, the U.S. presents a larger, more complex scenario by virtue of the higher number of merchants, financial institutions, and other players involved. Deployment in the U.S. could take 10 years, say Hogan and others.

Still, the challenges associated with embracing EMV will serve as a “refreshing” change after so much time and energy has been de-voted to “patching” legacy host systems, says Laszig. “We’re going to see a lot of new activity and excitement here in the U.S. payments industry” as EMV makes its mark, she concludes. TT

Julie Ritzer Ross is a contributing writer to Transaction Trends. Reach her at [email protected].

“Although dealing with a large base of non-compliant POS products may seem like an obstacle, it is also a huge opportunity for terminal manufacturers.” —Dale Laszig, Castles Technology Co.

TransacTion trends | October 2011 23

Startup Stories:»

Austin Center’s path to running an ISO was hardly orthodox. The son of a successful Chattanooga, Tennes-

see, businessman, Center majored in art at the College of Charleston. Then he moved to New York City where he both taught art and practiced as an artist.

After relocating back down South, Center began working for a merchant services company that his father and a partner had founded, helping to process health-care claims, so that he would have, in his words, “something else in my toolbox” in terms of job skills. About four years ago, Center went from one of four people running the ISO to doing it all himself. Now, he is the president of Acuity Payment Services.

“I was basically thrown to the wolves,” he says. “Basically, not knowing much about it, I started from scratch.”

Drawing on ExperienceCenter fell back on an art management minor, as well as the practical education earned while working at his father’s company, Cenco Inc., a manufacturer of chemical products and an industrial maintenance company. He accompanied his dad on business trips when he was as young as 8-years-old, and later, at 12, started helping out with filing and other simple tasks. As he got older, Center worked in the back of the warehouse, stacking boxes, helping out with shipping, and labeling bottles using a silk screen.

Perhaps, surprisingly, he also applied what he had learned as an artist. Ceramics, in particular, taught him about process, which he then applied to business. He said it took him about a year and a half to wrap his arms around the payments business.

“For any project that I did with art, there was a definite beginning, middle, and end,” Center explains. “I’ve brought that into anything I do, but the main part, if you think about it with this industry, there’s a process—whether it’s signing a merchant, whether its courting a bank, whether it’s dealing with sales agents and associates. Any

merchant you sign, there’s a definite process and along the way, you have to make sure that each step in the process is taken care of to make sure that that account is processed, and that task is complete.”

Acuity Senior Vice President Cheryl Cockrell is a long-time veteran of the industry who worked at both Payment Alliance International and Payment Transac-tion Solutions. She brings the practical knowledge to what Center might lack, but she’s impressed by his business acumen.

“When he was talking about being self-taught in business, it was born into him,” she says.

Leveraging a NicheAcuity’s strategy is mainly to work with small community banks to sign up accounts. Austin Center’s father Morton and Nelson Bowers, an owner of automobile dealerships in the Chattanooga area, are two of the company’s owners. Both had extensive contacts in the community banking business. Cockrell got her start almost 20 years ago working at Mississippi’s People Bank, which happened to have an in-house merchant program. In working with community banks, Acuity not only has a strategy but also a business ethos.

“From my father’s industry and Nelson Bowers’ industries, the main thing they told me is, ‘It’s customer first,’ and, ‘Take care of the customer,’” Austin Center says. “And that’s the main thing, especially for the merchant service industry. You’re going to have things hap-pen, but as long as you’re on top of it and you build the relationship with the customer and you build the relationship with the bank, that’s what they want to see.”

Cockrell works a time zone and a six-hour car ride away in Missis-sippi, rather than in Acuity’s Chattanooga headquarters. Operating out of a small town there, she helps to stay in touch with the needs of small-town and rural merchants.

“There is not a lot of support out there,” she says. “It doesn’t seem that the companies actually support community banks. They will give them an 800 number, and you will call and fill out an applica-tion over the phone or online, and then you get a terminal in the mail and you plug it up. There’s not a lot of those companies out there today that still have those personal relationships and in these

Former artist paints a bright future for Acuity PaymentBy John Manasso

Art of the Deal

Acuity Payment Services

Acuity Payment Services

Chattanooga, TN

Founded: 2006

Portfolio size: 500 merchants

Transaction volume: $60

million annually

LET US PROFILE YOUR ISOIs your company a successful ISO? Let us tell your story. Email [email protected] for more information.

24 October 2011 | TransacTion trends

small towns in the South—in Georgia, Mis-sissippi, and Tennessee—that really gives you an edge above the competitor.”

Building a MasterpiecePart of the reason that Acuity has gone through fits and starts is a change in the company’s executive management. Earlier this year, Acuity joined ETA as a member. Steve Demaree also was a veteran of Pay-ment Alliance International who had served in the past as a director of ETA. He was a part owner with Morton Center and Bowers and also served as CEO, but departed the com-pany earlier this year.

“The idea is you need to be knowledge-able about the industry,” Center says. “With all the regulations and all that’s going on, you need to get your hands around what’s going on in the industry and build relationships. There’s so much going on in this industry, there’s always change.”

Center’s goal with Acuity is to achieve manageable growth. Right now, Acuity is processing between 30 and 40 accounts per month. Center says that while the company has the capability to sign up many more new accounts, it is trying not

to bite off more than it can chew. The idea is to deliver on all of its promises to customers.

“The key is having good people—peo-ple that I know are genuine—and when we build a relationship with a community bank they know the people they’re dealing with,” he says. “With community banks, there is such a loyalty and we try to cater our ser-

vices. Being small, we’re able to do what the community banks and financial institutions need. That enables us to give them the best support and services, and support their cus-tomers how they want them supported.” TT

John Manasso is a contributing writer to Transaction Trends. Reach him at [email protected].

WORDSTOTHEWISEBe in it for the long haul and act ethically. “There are so many ISOs, so many companies out there, and we went through a segment of time where people made their money through equipment and they would sell a $200 piece of equipment for $1,200,” says Acuity Senior Vice President Cheryl Cockrell.

Not all companies are ethical, she says. “Some are there to make a buck today and this is not how this business works. It’s not a get-rich-quick business. It’s about building relationships with these community banks and partnering with them.”

Follow through on what you tell your customers. “If you say you’re going to do something, then do it,” says Acuity President Austin Center. “That’s my main thing that I harp on with sales agents.”

Surround yourself with experienced people. “Ask people who have done it before,” Center says. “A lot of people want to tell you ‘the right way’ and ‘this way,’ but the fact is that you’ve got to find the people who have done it before.”

Startup Stories:» Acuity Payment Services

October 25 - 27, 2011 • Palmer House Hilton • Chicago

Electronic Transactions Association

3 DAYS. 3 EVENTS. 1 LOCATION.Every day brings a new entry into the payments landscape. Who will cause baseline changes to the existing value chain? How can you adapt to capitalize on new ways of transacting?

This fall, 3 EVENTS will come together for 3 DAYS to feature an unprecedented line-up of mobile, security, technology, and top-level payments experts all in 1 LOCATION to address the trends that will change what your customers demand!

Save these dates: Mobile Commerce Summit

Tuesday, Oct. 25 NEW!

Strategic Leadership ForumTuesday, Oct. 25 - Thursday, Oct. 27

Compliance Day Thursday, Oct. 27

www.electran.org

TF0608_ISS_Digital_Transactions_ISO_Ad_MECH_OUTLINE.indd 1 8/17/11 2:25 PM

26 October 2011 | TransacTion trends

1 Card At A Time LLCNew York, NY 10018212/981.2541Contact: Luigi Ceneri

A-AAccess OnLine Payment Systems Inc.Decatur, GA 30033404/499.9944Contact: Nelda Mays

ACT CanadaAjax, Ontario CanadaContact: Diane Eskesen-Power

Activant SolutionsLivermore, CA 94526925/518.1444Contact: Matt Mullen

Acuity Payment Services LLCGermantown, TN 38139901/218.6414Contact: Steve Demaree

Adaptive Payments Inc.Fort Lauderdale, FL 33301954/756.1603Contact: Shashi Kapur

AlertPay.comMontreal, Quebec Canada514/748.1441 x703Contact: Mohammad Hashemi

Alpha Card ServicesHuntingdon Valley, PA 19006215/494.0200 x13Contact: Lazaros Kalemis

AltchargeLas Vegas, NV 89119866/967.8306Contact: David Long

Ascent Processing Inc.Boulder, CO 80301303/543.0378Contact: DeAnna Constant

B2 Processing Solutions Inc.Toronto, Ontario Canada416/730.9827 x1Contact: Bruce Murray

Bank of America Merchant ServicesContact: Scott Calliham

BankCard USAWestlake Village, CA 91362818/540.3500Contact: Shawn Skelton

Beacon Processing SolutionsOrlando, FL 32803866/430-2322 x108Contact: Sean Reed

The Electronic Transactions Association is pleased to welcome the following companies to its membership. To inquire about a membership with ETA, please contact Del Baker Robinson, director of membership and marketing, at [email protected].

Mobile

eCommerceRetail

eProcessing Network’s PA-DSS compliant application lets you:

• Maintain existing processor relationships• Transact directly through QuickBooks®• Eliminate double-entry of transactions• Simplify back offi ce & accounting procedures

The ePN QuickBooks® Solution allows you to be everywhere you need to be to manage your business!

ProcessingNetwork

TheeverywhereProcessingNetworkSM

eProcessingNetwork.com (800) 296-4810

[ NEW MEMBERS ]

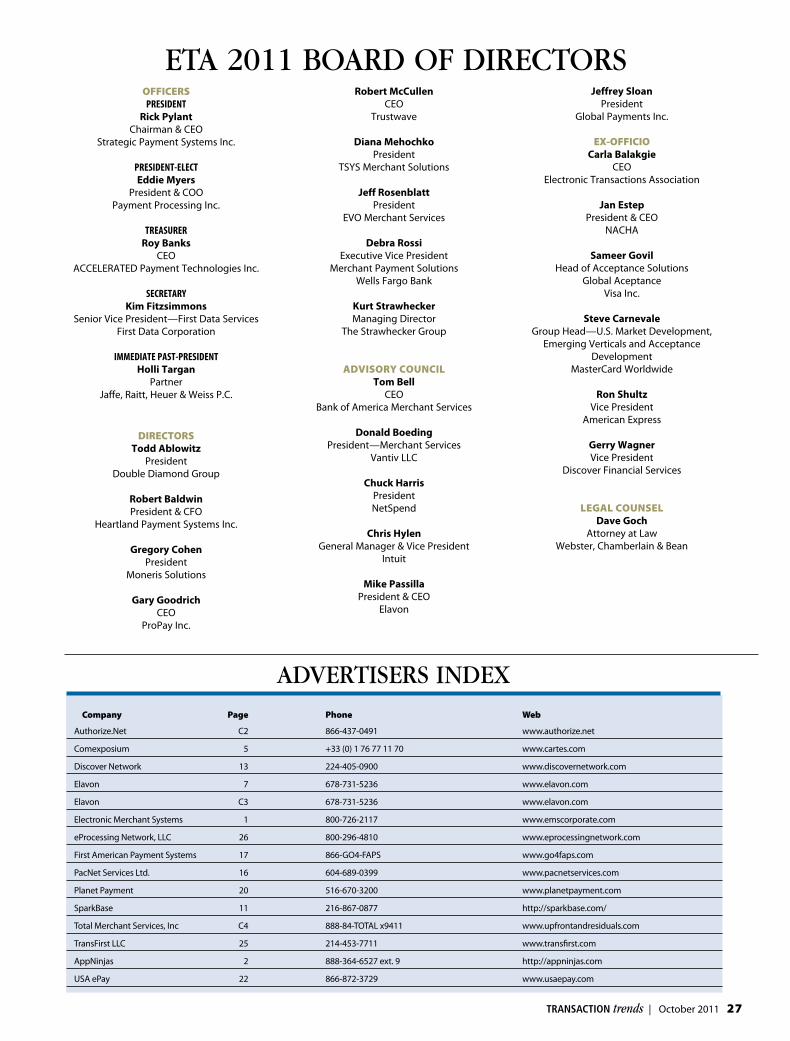

Company Page Phone Web

Authorize.Net C2 866-437-0491 www.authorize.net

Comexposium 5 +33 (0) 1 76 77 11 70 www.cartes.com

Discover Network 13 224-405-0900 www.discovernetwork.com

Elavon 7 678-731-5236 www.elavon.com

Elavon C3 678-731-5236 www.elavon.com

Electronic Merchant Systems 1 800-726-2117 www.emscorporate.com

eProcessing Network, LLC 26 800-296-4810 www.eprocessingnetwork.com

First American Payment Systems 17 866-GO4-FAPS www.go4faps.com

PacNet Services Ltd. 16 604-689-0399 www.pacnetservices.com

Planet Payment 20 516-670-3200 www.planetpayment.com

SparkBase 11 216-867-0877 http://sparkbase.com/

Total Merchant Services, Inc C4 888-84-TOTAL x9411 www.upfrontandresiduals.com

TransFirst LLC 25 214-453-7711 www.transfirst.com

AppNinjas 2 888-364-6527 ext. 9 http://appninjas.com

USA ePay 22 866-872-3729 www.usaepay.com

Advertisers index

etA 2011 BOArd OF direCtOrsOFFICERS

PRESIDENTRick Pylant

Chairman & CEOStrategic Payment Systems Inc.

PRESIDENT-ELECTEddie Myers

President & COOPayment Processing Inc.

TREASURERRoy Banks

CEOACCELERATED Payment Technologies Inc.

SECRETARYKim Fitzsimmons

Senior Vice President—First Data ServicesFirst Data Corporation

IMMEDIATE PAST-PRESIDENTHolli Targan

PartnerJaffe, Raitt, Heuer & Weiss P.C.

DIRECTORSTodd Ablowitz

PresidentDouble Diamond Group

Robert BaldwinPresident & CFO

Heartland Payment Systems Inc.

Gregory CohenPresident

Moneris Solutions

Gary GoodrichCEO

ProPay Inc.

Robert McCullenCEO

Trustwave

Diana MehochkoPresident

TSYS Merchant Solutions

Jeff RosenblattPresident

EVO Merchant Services

Debra RossiExecutive Vice President

Merchant Payment SolutionsWells Fargo Bank

Kurt StrawheckerManaging Director

The Strawhecker Group

ADVISORY COUNCILTom Bell

CEO Bank of America Merchant Services

Donald BoedingPresident—Merchant Services

Vantiv LLC

Chuck HarrisPresidentNetSpend

Chris HylenGeneral Manager & Vice President

Intuit

Mike PassillaPresident & CEO

Elavon

Jeffrey SloanPresident

Global Payments Inc.

EX-OFFICIOCarla Balakgie

CEOElectronic Transactions Association

Jan EstepPresident & CEO

NACHA

Sameer Govil Head of Acceptance Solutions

Global AceptanceVisa Inc.

Steve CarnevaleGroup Head—U.S. Market Development,

Emerging Verticals and Acceptance Development

MasterCard Worldwide

Ron ShultzVice President

American Express

Gerry WagnerVice President

Discover Financial Services

LEGAL COUNSELDave Goch

Attorney at LawWebster, Chamberlain & Bean

TransacTion trends | October 2011 27

“We know that most small- and mid-sized merchants wake up thinking about how they can bring in the next dollar, not

about how they can secure their environment,” says Joan Herbig, CeO of Atlanta-based Controlscan.

this piece of wisdom comes from six years of helping merchants safeguard their data. Founded in 2005 by richard stanton, Controlscan originally got into business by help-ing scan e-commerce websites to uncover vulnerabilities. in 2007, however, the company changed tactics “while remain-ing focused on our core competency of servicing small mer-

chants,” Herbig says, after stanton, a former e-commerce merchant, and his team raised their first round of funding and hired the company’s current management team.

High-Tech ProductsControlscan’s move into the PCi compliance space was prompted by the gradual trickle-down of the PCi data security standard (dss) enforcement, says Herbig. “the first area of focus was, unsurpris-ingly, among larger merchants, but in late 2007 and early 2008 the card brands began to push down the requirement for PCi to smaller

merchants. that created an opportunity for solutions to enter the marketplace.”

Making the switch required Controlscan to change its target audience. the company originally focused directly on merchants as its core customer base. now, it concentrates on “acquirers, banks, and isOs who have portfolios of small- and mid-sized merchants and are looking for ways to guide them through the PCi compliance process,” Herbig explains.

these organizations approach Controlscan primarily for its flagship pair of product offerings: PCi 1-2-3 and PCi dashboard. (the company also offers breach protection, ssL certificates, and, as of May, security consulting services.) PCi 1-2-3 is based around an online merchant-facing portal called myControlscan.com that walks merchants through the complicated PCi compliance process.

“it provides education [in the form of a ‘policy builder’ that automatically generates policy templates based on the way a merchant processes payment cards], and it provides security-awareness training” that satisfies the PCi dss re-quirement, Herbig says. “it also provides the self-Assessment

INduStRy InsIder

On the Straight and NarrowControlScan leads small- and mid-sized merchants down the path to compliance By Bryan Ochalla

Questionnaire in a form and fashion that we believe is easier for small merchants to complete than other options that exist in the marketplace.”

Controlscan also offers quarterly scanning to mer-chants who interact and conduct scans through the my-Controlscan.com portal.

the company’s PCi dashboard product, on the other hand, is a portal that’s aimed at acquirers, banks, and isOs. it “provides them with a great level of detail about the state of compliance of their small- and mid-sized mer-chant portfolios,” according to Herbig.

through this portal, which can be exported for use within any risk-management system an isO or acquirer may employ, “they can assess the overall compliance rate, they can determine where a particular merchant is within the compliance process...they can even drill down and see exactly what kind of communication we’ve had with the merchant over time,” she adds.

High-Touch ServiceControlscan also strives to carve out individual relation-ships with its clients and their customers.

“We have a team of representatives who reach out to merchants to educate them and engage them in the process to begin with and then continue to interact with them as they’re working through it,” Herbig says. “We’ve found that it’s rare for a small merchant to complete the PCi compli-ance process without any questions popping up.”

the company’s unwavering focus on and support of small- and mid-sized merchants is just one thing that Herbig says sets Controlscan apart from its competitors in the pay-ments space. Another is its ability to create and tailor pro-grams to the specific needs of each acquirer, bank, or isO.

“We customize programs to help them deliver PCi solu-tions that are based on the way that they do business with their merchants,” she explains. “We work with some acquirers who have very hands-on relationships with their merchants.” Other companies, however, prefer that Controlscan be the main interface with their merchants regarding compliance.

“the idea,” she adds, “is that we try to understand what an acquirer, bank, or isO is trying to accomplish with the program and then develop something for them that is spe-cific to their needs, as opposed to the kind of cookie-cutter program they might get elsewhere.” TT

Bryan Ochalla is a contributing writer to transaction trends. Reach him at [email protected].

“It’s rare for a small merchant to com-plete the PCI com-pliance process without any ques-tions popping up.”—Joan Herbig, CEO

28 October 2011 | TransacTion trends

VM Mobile

VirtualMerchant

©2011 Elavon, Inc. All Rights Reserved.

transaction_trends_2011_vm_v2.indd 2 7/5/11 4:52 PM

Total Transparency Total Merchant Services protects you and your merchants with total transparency. We take a reasonable approach in disclosing the financial details of our Compliance Program to every new merchant on our Schedule Of Fees in simple, clear language. Easy To SellAll our merchants receive the Compliance Program at no additional charge during the first year of their processing relationship with us and these services may be accessed immediately. On the 13th month of processing, and from that point forward, merchants will be assessed a fee of $4.95 per month. We even offer a $25,000 Compliance Reimbursement Program to make sure our merchants feel good as they are getting something in return.

Honesty is our Everyday PolicyAt Total Merchant Services, you’ll find no compliance fee trickery and zero surprises. We believe in being upfront, honest and ethical in all of our business dealings. We will not use bait and switch tricks or surprises to get over on merchants or sales partners. We know that doing anything less would be a recipe for disaster—not growth.

Still not sure? Want to be convinced?If you’d like help comparing our program, including the true impact of the Compliance Program fees, please give us a call. We’ll show you that chasing a deal that looks better is NOT going to make up for a Compliance Fee Program that destroys your reputation and your business.

We’ve got some better ideas! Take a look:

Who’s going to have happier customers?

You!Who’s going to earn more money?

You!Who’s going to get more referrals?

You!Who’s going to break through in ‘11?

You!

Give us a call or visit our website for more details. (888) 848.6825 x9411 upfrontandresiduals.com

You can have it all! You can still earn an 8x upfront bonus, 50%-65% revenue sharing splits, the best free terminal placement programs in the business, with an honest, transparent, reasonable Compliance Program.

Hidden Compliance Fees? Angry Merchants?Don’t take it anymore!

Related Documents