Training Material: Introduction to Accounting of Transactions — With Specific Reference to MGNREGA Scheme A JOINT INITIATIVE OF Ministry of Rural Development, Government of India & Professional Development Committee of the ICAI Professional Development Committee The Institute of Chartered Accountants of India (Set up by an Act of Parliament) New Delhi

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Training Material: Introduction to Accounting of

Transactions — With Specific Reference to MGNREGA Scheme

A JOINT INITIATIVE OF Ministry of Rural Development, Government of India & Professional Development Committee of the ICAI

Professional Development Committee

The Institute of Chartered Accountants of India (Set up by an Act of Parliament)

New Delhi

© The Institute of Chartered Accountants of India

All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form, or by any means, electronic, mechanical, photocopying, recording, or otherwise, without prior permission, in writing from the publisher.

Edition : September, 2014

Department : Professional Development Committee

ISBN : 978-81-8441-733-3

Price : ` 200/- (including CD)

Published by : The Publication Department on behalf of The Institute of Chartered Accountants of India, ICAI Bhawan, Post Box No. 7100, Indraprastha Marg, New Delhi-110 002.

Printed by : Sahitya Bhawan Publications, Hospital Road, Agra 282 003. September/2014/1,000 Copies (Updated)

Foreword

The Mahatma Gandhi National Rural Employment Guarantee Act, 2005 (MGNREGA), notified in 2005, mandated to provide 100 days of guaranteed wage employment in a financial year to every household whose adult members volunteer to do unskilled manual work. Taking the forward steps, ICAI approached the Ministry of Rural Development (MoRD) to provide support in guidance for accounting and auditing of the transactions under MGNREGA. The Training Material on Accounting of the transactions under the scheme of MGNREGA has been prepared.

As you all are aware, MGNREGA is a powerful instrument for inclusive growth in rural India through its impact on social protection, livelihood security and democratic empowerment. Any shortcoming in implementation will always need to be closely looked into and rectified.

Implementation of the MGNREGA involves roles and responsibilities of a large number of stakeholders from the village to the national level. The key stakeholders are Wage seekers, Gram Sabha (GS), Three-tier Panchayati Raj Institutions (PRIs), the Gram Panchayat (GP), Block Panchayat, Zilla Panchayat, Programme Officer (PO) at the Block level, District Programme Coordinator (DPC), State Government, Civil Society, and Other stakeholders [viz. line departments, convergence departments, Self-Help Groups (SHGs), etc.].

The nodal Ministry in the Government of India for MGNREGA is Ministry of Rural Development (MoRD), who has issued the guidance to all the States to conduct the training programme. The Ministry ensures timely and adequate resource support to the States and also undertakes review, monitoring and evaluation of processes and outcomes.

I am happy to note that the Professional Development Committee (PDC) of ICAI has brought Background Training Material on accounting of the transactions under MGNREGA. After training on accounting, the accounts under the said scheme could be prepared more systematically to facilitate the audit of the accounts by the members of ICAI and various reporting requirement to the sanction/disbursing authorities.

I would like to thank Chairman, PDC, CA. Shyam Lal Agarwal and his dynamic team for bringing out Background training material on accounting of transactions under MGNREGA. I am sure this background material would of great value addition and use for all the participants.

Date: 1st July, 2014 CA. K. Raghu Place: New Delhi President, ICAI

PREFACE

A meeting with the Ministry of Rural Development, Government of India with representatives of State Governments was held at Krishi Bhawan, New Delhi in June, 2012 to discuss the arrangement for engaging CA firms for audit of MGNREGA Accounts at Gram Panchayat (GP) Level.

A circular on Framework for Certification of Accounts and Financial Audit of MGNREGA accounts at GP Level by Chartered Accountants was released by Ministry of Rural Development in June 2012,wherein, they had mentioned that pursuant to the provisions of 24(1) of MGNREGA Act and with the objective of bringing in more transparency and accountability in management and deployment of MGNREGA funds at the GP level, Ministry of Rural Development, Government of India proposed to get GP accounts of the schemes formulated by the States under Section 4 of MGNREGA and to be audited and certified by the Chartered Accountants in accordance with the guidelines.

Various meetings were held with the officials of the MoRD, GoI for having the proper accounting and reporting of the transactions under MGNREGA and therefore to have the training programmes in the States.

In the last meeting held on 4th March,2014 with the officials of MoRD, it was discussed to direct the States to conduct the training programmes under the guidance and programmes of accountants at Gram Panchayat level to be organised through ICAI and in the matter to incur/bear expenses on such training programs it was approved that such expenses may be incurred out of 6% administrative cost allowed out of MGNREGA funds. The letter bearing such sanction has also been issued by MoRD.

The PDC of ICAI has already issued the letters to all the State Governments for conducting the training programmes and the meetings are also being held from time to time. It is expected that the first training program of its kind would be held shortly.

It was precise that Professional Development Committee comes out with a training module for such programs. I am thankful to CA Dinesh Kumar Garg and CA. Ravi Mansaka for preparation and their valuable contribution by providing deep insight into the intricacies of the same. I am also thankful to the Secretary PDC and PDC secretariat and particularly CA. Anuj Kaushik for putting all efforts for the same.

I hope this training material will provide the basic guidance for accounting the transaction in a manner to facilitate not only smooth audit but also to the various reporting requirements to control and monitor the scheme.

Date: 1st July, 2014 (CA. Shyam Lal Agarwal)

Place: New Delhi Chairman, Professional Development Committee

Contents

Chapter Page

Part A: Introduction to Accounting of Transactions 1

1. Introduction to Accounting 3

2 Financial Statements- Classification & Terminology 10

3 Fundamentals and Principles of Accounting 17

4 Basic Accounting Procedures-I 22

Double Entry System of Book-Keeping

5 Basic Accounting Procedures-II 30

Journal

6 Basic Accounting Procedures-III 46

Ledger

7 Subsidiary Books-I 55

Special Purpose Books

8 Subsidiary Books-II 65

Cash Book

9 Subsidiary Books-III 72

Petty Cash Book

10 Bank Reconciliation Statement 76

11 Trial Balance and Rectification of Error 87

12 Capital and Revenue Transactions 100

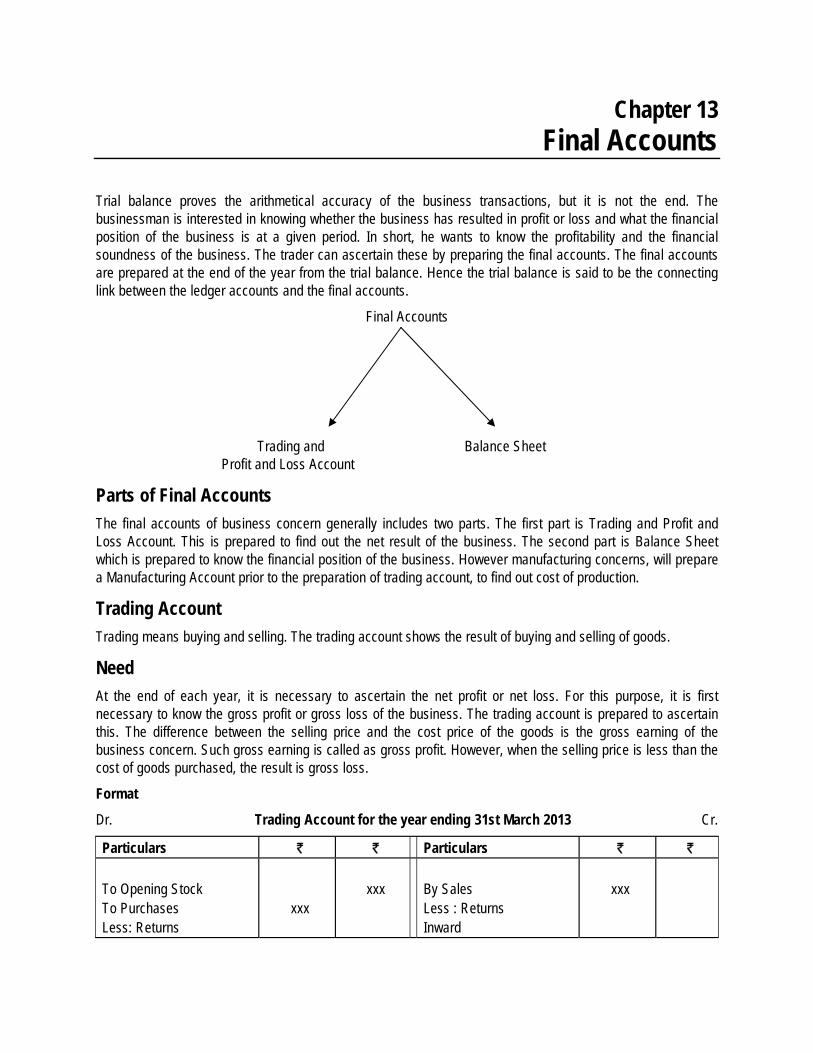

13 Final Accounts 105

14 Not for Profit Organisation 118

15 Preparation of Receipt & Payment Account and Income and Expenditure Account 119

Part B: Formats of Mandatory Registers Maintained under MGNREGA scheme with description 131

Part A Introduction to Accounting of Transactions

Chapter 1 Introduction to Accounting

“Accounting is as old as money itself”. Since in early ages commercial activities were based on barter system, record keeping was not a necessity. The Industrial Revolution of 19th century along with rapid rise in population, paved way for the development of commercial activities, mass production and credit terms. Thus recording of business transaction has become an important feature. In recent years with the change of technologies and marketing along with stiff competition, accounting system has undergone remarkable changes.

Over the years accountancy has made tremendous progress in the field of commerce and industry. Accounting can be described as being concerned with measurement and management. Measurement of recording transactions and management with the use of data for making decisions are the two fundamental aspects.

Definition of Accounting:-

“Accounting is the art of recording, classifying and summarising in a significant manner and in terms of money, transactions and events, which are, in part atleast, of a financial character, and interpreting the result thereof.” — American Institute of Certified Public Accountants

Accounting Process starts with recording of business transactions in the journal or subsidiary books and passing through the ledger and trial balance. It results in the preparation of finals accounts i.e., Trading & Profit and Loss A/c and Balance Sheet.

ACCOUNTING CYCLE/ACCOUNTING PROCESS

Recording of Transaction

Journal

LedgerTrial Balance

Trading & Profit and Loss A/c

Training Material: Introduction to Accounting of Transactions — With Specific Reference to MGNREGA Scheme

4

Book-keeping Book-keeping is that branch of knowledge which tells us how to keep a record of business transactions. It is often routine and clerical in nature. It is important to note that only those transactions related to business which can be expressed in terms of money are recorded. The activities of book-keeping include recording in the journal, posting to the ledger and balancing of accounts.

Accounting

Book-keeping does not present a clear financial picture of the state of affairs of a business. When one has to make a judgement regarding the financial position of the firm, the information contained in these books of accounts has to be analysed and interpreted. It is with the purpose of giving such information that accounting came into being.

Accounting is considered as a system which collects and processes financial information of a business. These information are reported to the users to enable them to make appropriate decisions.

Accounting, as an information system is the process of identifying, measuring and communicating the economic information of an organization to its users who need the information for decision making. It identifies transactions and events of a specific entity. A transaction is an exchange in which each participant receives or sacrifices value. An event (whether internal or external) is a happening of consequence to an entity. An entity means an economic unit that performs economic activities.

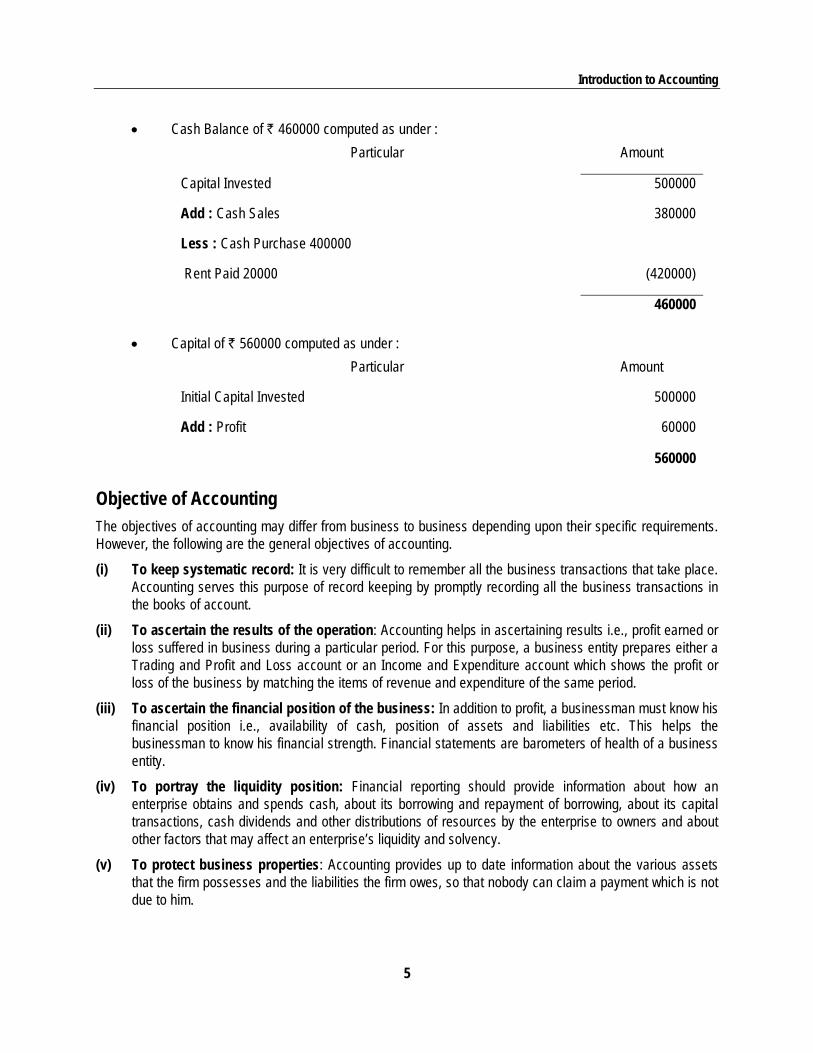

For example: Sachin started business with a capital of ` 500000. He purchases goods of ` 400000 for cash and sells ¾ goods for ` 380000. He also pays a rent of ` 20000.The following results can be drawn from the above:

1. Transaction are :

Investment of ` 500000

Purchasing of goods ` 400000

Cash Sales of ` 380000

Rent Paid ` 20000

2. Events are :

Profit of ` 60000 computed as under :

Particular Amount

Sales Cost of Purchase (3/4 of ` 400000) 300000 Add: Rent 20000 Profit

380000

(320000)

60000

Closing Inventory of ` 100000 computed as under :

Particular Amount

¼ of ` 400000 100000

Introduction to Accounting

5

Cash Balance of ` 460000 computed as under :

Particular Amount

Capital Invested

Add : Cash Sales

Less : Cash Purchase 400000

Rent Paid 20000

500000

380000

(420000)

460000

Capital of ` 560000 computed as under :

Particular Amount

Initial Capital Invested

Add : Profit

500000

60000

560000

Objective of Accounting The objectives of accounting may differ from business to business depending upon their specific requirements. However, the following are the general objectives of accounting.

(i) To keep systematic record: It is very difficult to remember all the business transactions that take place. Accounting serves this purpose of record keeping by promptly recording all the business transactions in the books of account.

(ii) To ascertain the results of the operation: Accounting helps in ascertaining results i.e., profit earned or loss suffered in business during a particular period. For this purpose, a business entity prepares either a Trading and Profit and Loss account or an Income and Expenditure account which shows the profit or loss of the business by matching the items of revenue and expenditure of the same period.

(iii) To ascertain the financial position of the business: In addition to profit, a businessman must know his financial position i.e., availability of cash, position of assets and liabilities etc. This helps the businessman to know his financial strength. Financial statements are barometers of health of a business entity.

(iv) To portray the liquidity position: Financial reporting should provide information about how an enterprise obtains and spends cash, about its borrowing and repayment of borrowing, about its capital transactions, cash dividends and other distributions of resources by the enterprise to owners and about other factors that may affect an enterprise’s liquidity and solvency.

(v) To protect business properties: Accounting provides up to date information about the various assets that the firm possesses and the liabilities the firm owes, so that nobody can claim a payment which is not due to him.

Training Material: Introduction to Accounting of Transactions — With Specific Reference to MGNREGA Scheme

6

Functions of Accounting In order to accomplish its main objective of communicating information to the users, accounting embraces the following functions.

1. Identifying: Identifying the business transactions from the source documents.

2. Recording: The next function of accounting is to keep a systematic record of all business transactions, which are identified in an orderly manner, soon after their occurrence in the journal or subsidiary books.

3. Classifying: This is concerned with the classification of the recorded business transactions so as to group the transactions of similar type at one place. i.e., in ledger accounts. In order to verify the arithmetical accuracy of the accounts, trial balance is prepared.

4. Summarising: The classified information available from the trial balance is used to prepare profit and loss account and balance sheet in a manner useful to the users of accounting information.

5. Analysing: It establishes the relationship between the items of the profit and loss account and the balance sheet. The purpose of analysing is to identify the financial strength and weakness of the business. It provides the basis for interpretation.

6. Interpreting: It is concerned with explaining the meaning and significance of the relationship so established by the analysis. Interpretation should be useful to the users, so as to enable them to take correct decisions.

7. Communicating: The results obtained from the summarised, analysed and interpreted information are communicated to the interested parties.

Importance of Accounting: The “users” of accounting information We have been talking about accounting and its purpose of providing information to users for decision-making. But, who exactly are these "users of financial statements"? Also, what information do they need and what decisions do they make?

The following are the different users of accounting information and their specific information needs:

1. Owners and Investors Stockholders of corporations need financial information to help them make decisions on what to do with their investments (shares of stock), i.e. hold, sell, or buy more. Prospective investors need information to assess the company's potential for success and profitability. In the same way, small business owners need financial information to determine if the business is profitable and whether to continue, improve or drop it.

2. Management In small businesses, management may include the owners. In huge organizations, however, management is usually made up of hired professionals who are entrusted with the responsibility of operating the business or a part of the business. They act as agents of the owners. The managers, whether owners or hired, regularly face economic decisions –

How much supplies will we purchase?

Do we have enough cash?

Introduction to Accounting

7

How much did we make last year?

Did we meet our targets?

All those, and many other decisions, require analysis of accounting information.

3. Lenders

Lenders of funds such as banks and other financial institutions are interested in the company’s ability to pay liabilities upon maturity (solvency).

4. Trade creditors or suppliers

Like lenders, trade creditors or suppliers are interested in the company’s ability to pay obligations when they become due. They are nonetheless especially interested in the company's liquidity -- its ability to pay short-term obligations.

5. Government

Governing bodies of the state, especially the tax authorities, are interested in an entity's financial information for taxation and regulatory purposes. Taxes are computed based on the results of operations and other tax bases. In general, the state would like to know how much the taxpayer is making to determine the tax due thereon.

6. Employees

Employees are interested in the company’s profitability and stability. They are after the ability of the company to pay salaries and provide employee benefits. They may also be interested in its financial position and performance to assess the possibility of company expansion and career opportunities.

7. Customers When there is a long-term involvement or contract between the company and its customers, the customers may be interested in the company’s ability to continue its existence and its stability of operations. This need is also heightened in cases where the customers depend upon the entity. For example, a distributor (reseller), the customer in this case, is dependent upon the manufacturing company from which it purchases the items it resells.

8. General Public Anyone outside the company such as researchers, students, analysts and others are interested in the financial statements of a company for some valid reason.

9. Research Scholars Accounting information, being a mirror of the financial performance of a business organization, is of immense value to the research scholar who wants to make a study into the financial operations of a particular firm. To make a study into the financial operations of a particular firm, the research scholar needs detailed accounting information relating to purchases, sales, expenses, cost of materials used, current assets, current liabilities, fixed assets, long-term liabilities and share-holders funds which is available in the accounting records maintained by the firm.

Training Material: Introduction to Accounting of Transactions — With Specific Reference to MGNREGA Scheme

8

Internal and External Users The users may be classified into internal and external users.

Internal users refer to managers who use accounting information in making decisions related to the company's operations.

External users, on the other hand, are not involved in the operations of the company but hold some financial interest. The external users may be classified further into users withdirect financial interest – owners, investors, creditors; and users with indirect financial interest – government, employees, customers and the others.

Advantages of Accounting The following are the advantages of accounting to a business:

1. It helps in having complete record of business transactions.

2. It gives information about the profit or loss made by the business at the end of a financial year and its financial conditions. The basic function of accounting is to supply meaningful information about the financial activities of the business to the owners and the managers.

3. It provides useful information for taking economic decisions.

4. It facilitates comparative study of current year’s profit, sales, expenses etc., with those of the previous years.

5. It supplies information useful in judging the management’s ability to utilise enterprise resources effectively in achieving primary enterprise goals.

6. It provides users with factual and interpretive information about transactions and other events which are useful for predicting, comparing and evaluation the enterprise’s earning power.

7. It helps in complying with certain legal formalities like filing of income- tax and sales-tax returns etc.. If the accounts are properly maintained, the assessment of taxes is greatly facilitated.

Limitations of Accounting 1. Accounting is historical in nature. It does not reflect the current financial position or worth of a business.

2. Transactions of non-monetary nature do not find place in accounting. Accounting is limited to monetary transactions only. It excludes qualitative elements like management, reputation, employee morale, labour strike etc.

3. Facts recorded in financial statements are greatly influenced by accounting conventions and personal judgements of the Accountant or Management. Valuation of inventory, provision for doubtful debts and assumption about useful life of an asset may, therefore, differ from one business house to another.

4. Accounting principles are not static or unchanging-alternative accounting procedures are often equally acceptable. Therefore, accounting statements do not always present comparable data.

5. Cost concept is found in accounting. Price changes are not considered. Money value is bound to change often from time to time. This is a strong limitation of accounting.

Introduction to Accounting

9

Distinction between Book-keeping and Accounting In general the following are the differences between book-keeping and accounting.

S. No.

Basis of Distinction

Book-keeping Accounting

1 Scope Recording and maintenance of books of accounts.

It is not only recording and maintenance of books of accounts but also includes analysis, interpreting and communicating the information.

2 Stage Primary stage. Secondary stage. 3 Objective To maintain systematic records of

business transactions. To ascertain the net result of the business operation.

4 Nature Often routine and clerical in nature. Analytical and executive in nature. 5 Responsibility A book-keeper is responsible for

recording business transactions. An accountant is also responsible for the work of a book-keeper.

6 Supervision The book-keeper does not supervise and check the work of an Accountant.

An accountant supervises and checks the work of the book-keeper.

7 Staff involved Work is done by the junior staff of the organisation.

Senior staff performs the accounting work.

Relationship between Accountancy, Accounting and Book-keeping Book-keeping provides the basis for accounting and it is complementary to accounting process. Accounting begins where book-keeping ends. Accountancy includes accounting and book-keeping. The terms Accounting and Accountancy are used synonymously.

Training Material: Introduction to Accounting of Transactions — With Specific Reference to MGNREGA Scheme

10

USERS OF ACCOUNTING INFORMATION

Accounting

Information

Owners

Researchers

Employees and Trade

Unions

Creditors, Banks & Lending

Institutions

Present Investors

Potential Investors

Government and Tax

Authorities

Regulatory Agencies

Management

Chapter 2 Financial Statements – Classification & Terminology

Terminology Used in Accounting System Account – A formal record of a particular type of transaction expressed in money or other unit of measurement and kept in a recorded form. In accounting separate record of each individual, asset, liability, expenses or income is kept. The place where such a record is maintained is termed as ‘Account’. Such as the Account of Ranbir, the Account of Ram, the Account of Machinery, the Account of Salary, the Account of Rent and likewise. All transactions entered into with Ranbir will be recorded in the Account of Ranbir.

All accounts are divided into two sides.

The left side of an account is arbitrarily or traditionally called Debit side and the right side of an account is called Credit side.

In the abbreviated form, Debit is written as Dr. and Credit is written as Cr.

Accounting Entry – A record of financial transaction in the books of account like journal, ledger, cash book, etc.

Account Payable – Amount owed by an enterprise on account of goods purchased or services received or in respect of contractual obligations. Also termed as Creditor.

Accounting Period – The period of time for which financial statements are customarily prepared.

Accounting Principle – The principles and procedures under which the accounts of an organization are maintained/ to be maintained are called accounting principles. An accounting principle is an adaptation or special application of a principle necessary to meet the peculiarities of an organization or the needs of its management. Thus, principles are required for the computation of depreciation, the recognition of capital expenditures etc.

Account Receivable – Persons from whom amounts are due for goods sold or services rendered or in respect of contractual obligations. Also termed as debtor. The words ‘Receivables’ and ‘Debtors’ are used interchangeably.

Accounting Unit – An accounting unit shall be defined as a department, branch, office identified by the enterprise/as a unit for maintenance of separate accounting records.

Accounting Year – Accounting year means a year commencing on the first day of the accounting period. Generally, in case of a business enterprise /educational body, it would refer to the period from 1st April of a year to 31st March next year.

Accrual – Recognition of revenues and costs as they are earned or incurred (and not as money is received or paid). It includes recognition of transactions relating to assets and liabilities as they occur irrespective of the actual receipts or payments.

Accrual Basis of Accounting – The basis of accounting under which transactions and other events are recognized when they occur (and not only when cash or its equivalent is received or paid). Therefore, the transactions and events are recorded in the accounting records and recognized in the financial statements of the periods to which they relate. The elements recognized under accrual accounting are assets, liabilities, revenue and expenses.

Training Material: Introduction to Accounting of Transactions — With Specific Reference to MGNREGA Scheme

12

Accrued & Due – In respect to an asset (or a liability) it means a claim which has become enforceable, which arises from the sale/ rendering (purchase) of goods/ services or otherwise and has become receivable (payable). In respect to an income (or an expense) it means the amount earned (incurred) in an accounting period, for which a claim has become enforceable, and it arises from the sale/rendering (purchase) of goods/services or otherwise and has become receivable (payable).

Accrued But Not Due – In respect to an asset (or a liability) it means a claim which has not yet become enforceable, which accumulates with the passage of time or arises from the sale/ rendering (purchase) of goods/ services which, on the date of period-end, have been partly performed and are not yet receivable (payable). In respect to an income (or an expense) it means the amount earned (incurred) in an accounting period, but for which no enforceable claim has become due in that period. It accumulates with the passage of time or arises from the sale/ rendering (purchase) of goods/services goods which, at the date of accounting, have been partly performed and are not yet receivable (payable).

Accumulated Depreciation – The total to date of the periodic depreciation charges on depreciable assets.

Advance – Payment made on account of, but before completion of, a contract, or before acquisition of goods or receipt of services.

Amortisation – The gradual and systematic writing off of an asset or an account over an appropriate period. The amount on which amortisation is provided is referred to as amortisable amount. Depreciation accounting is a form of amortisation applied to depreciable assets. Depletion accounting is another form of amortisation applied to wasting assets. Amortisation also refers to gradual extinction or provision for extinction of a debt by gradual redemption or sinking fund payments or the gradual writing off to revenue of miscellaneous expenditure carried forward.

Annual Report – Any report prepared at yearly intervals. A statement of the financial condition and operating results of a business enterprise/institute, prepared yearly for submission to interested parties; summarising its operations for the preceding year and including a balance sheet, income & expenditure statement, often a receipts & payment statement, and the auditor's report, together with comments by the Manager/ Officer of the business enterprise / institute on the year's operations.

Assets – “Any thing which is in the possession or is the property of business enterprises including the amount due to it from others, is called an Asset.” Assets are tangible objects or intangible rights owned by an business enterprise/ and carrying probable future benefits. Assets provide the means to achieve their objectives. Assets that are used to deliver goods and services in accordance with an organisation’s objectives but which do not directly generate net cash inflows are often described as embodying “service potential”. Assets that are used to generate net cash inflows are often described as embodying “future economic benefits”.

Bad Debts – Debts owed to the business enterprises, which are considered to be irrecoverable, e.g., arrears of taxes, fees and other revenue left uncollected and considered to be irrecoverable. It is a business loss debited to Profit and Loss A/c as expense.

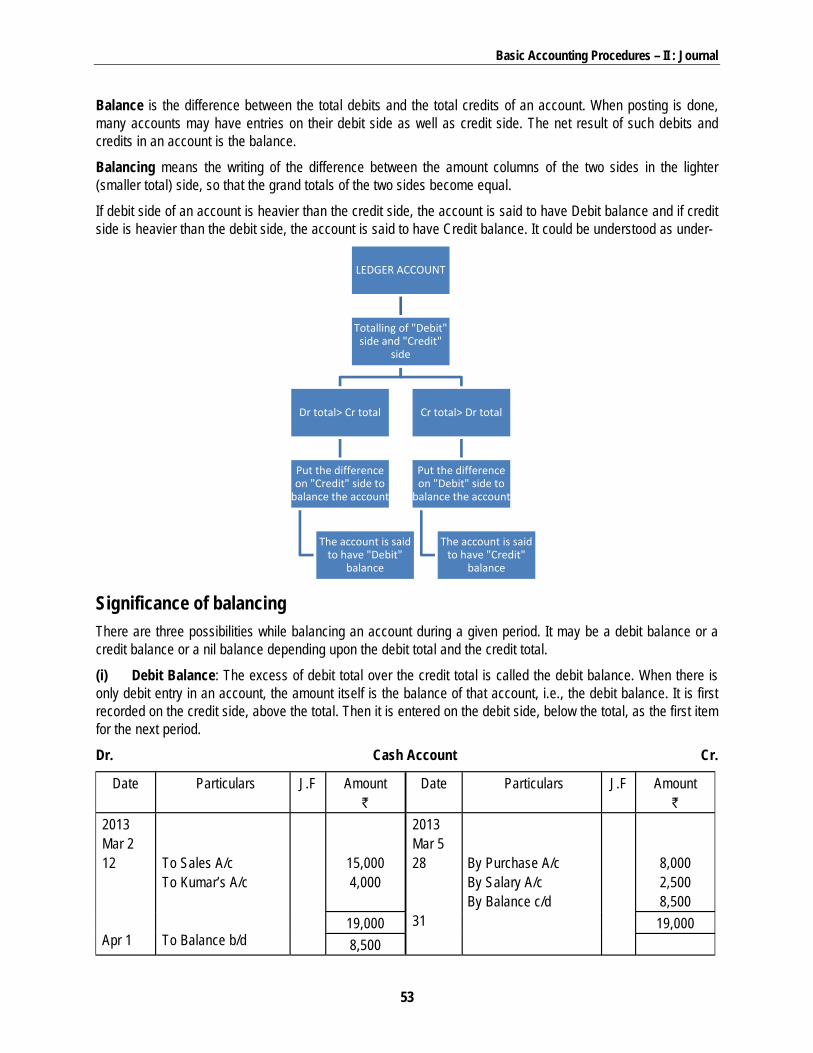

Balancing- It means writing of the difference that exists between the amount columns of the two sides, namely debit and credit in the smaller side so that the totals of the two sides are equalized.

Balance Sheet – A statement of the financial position of an business enterprise/ as at a given date, which exhibits its assets, liabilities, capital, reserve and other account balances at their respective book values.

Bank Reconciliation Statement – A statement, which reflects the nature and amount of transaction (s) not responded either by the business enterprise or the bank as on a particular date. Such statement may also reflect errors/ omission in the recording of transaction inter-se between the business enterprise and the Bank.

Books of Original Entry – A record book, recognised by law in which transactions are successively recorded, and which is the source of postings to ledgers; a journal. Books of original entry include general and special journals, such as cash books.

Financial Statements – Classification & Terminology

13

Budget – Budget is a financial plan, an expression of financial intent. It sets forth the expenditures that bodies are expected to incur during the year on various programmes and the means of financing them. A budget thus provides both, the authorization of, and limitations on, the amounts that may be spent for particular purposes.

Capitalisation – An expenditure for a fixed asset or addition thereto that has the effect of enlarging physical dimensions, increasing productivity, lengthening future life, or lowering future costs.

Capital Expenditure – An expenditure which is incurred in acquiring or increasing the value of Fixed Assets and this expenditure yields (give) benefits for more than one year. The term is generally restricted to expenditure that adds fixed asset units or that has the effect of improving the capacity, efficiency, life span or economy of operations of an existing asset. It is written in Balance Sheet on Assets Side.

Cash Book – A book of original entry maintained on daily basis for cash receipts and disbursement in its chronological order.

Chart of Accounts – A systematically arranged list of accounts applicable to a specific concern, giving account names and numbers, if any.

Contingent Liability – An obligation relating to an existing condition or situation which may arise in future depending on the occurrence or non-occurrence of one or more uncertain future events. No accounting entry needs to be passed for a contingent liability. However, disclosure is required in the Balance Sheet.

Contra Entry – An item on one side of an account which offsets fully or in part one or more items on the opposite side of the same account.

Cost – The amount of expenditure incurred on or attributable to a specified article, product or activity.

Cost of Acquisition – The cost of acquisition of a Fixed Asset comprises its purchase price and includes import duties and other non-refundable taxes or levies and any directly attributable cost of bringing the asset to its working condition for its intended use; any trade discounts and rebates are deducted in arriving at the purchase price.

Credit – A book-keeping entry recording the reduction or elimination of an asset or an expense, or the creation of or addition to a liability or item of net worth or revenue; the amount so recorded.

Current Assets – Cash and other assets that are expected to be converted into cash or consumed in rendering of services in the normal course of operations of the business enterprise/institution.

Current Liability – Liability including loans, deposits, expenses and bank overdrafts which fall due for payment in a relatively short period, normally not more than twelve months.

Debit – The goods or benefit received from a transaction; a book-keeping entry recording the creation of or addition to an asset or an expense, or the reduction or elimination of a liability, or item of net worth or revenue; the amount so recorded.

Deficit – The excess of expenditure over income for an Accounting Period under consideration.

Depreciable Amount – The historical cost or other amount substituted for historical cost of a depreciable asset in the financial statements, less the estimated residual value.

Depreciation – A measure of the wearing out, consumption or other loss of value of a depreciable asset arising from use, efflux ion of time or obsolescence through technology and market changes. It is allocated so as to charge a fair proportion in each accounting period during the useful life of the asset. It includes amortisation of assets whose useful life is predetermined and depletion of wasting assets.

Depreciation Method – The arithmetic procedure followed in determining a provision for depreciation (an expense) and maintaining the accumulated balance.

Training Material: Introduction to Accounting of Transactions — With Specific Reference to MGNREGA Scheme

14

Depreciation Rate – A percentage which when applied to the depreciable amount will yield depreciation expense for a year.

Disclosure – Process of divulging accounting information so that the content of Financial Statements is understood.

Discount – It is a rebate and allowance given by the seller to buyer.

Double-Entry Bookkeeping – It is a system of accounting in which both debit and credit aspects of each transaction is recorded. It affects at least two accounts.

You've probably heard the saying, "Money doesn't grow on trees." It means that money must come from somewhere---it doesn't just "appear." Double-entry accounting is a method of record-keeping that lets you track just where your money comes from and where it goes. Using double-entry means that money is neither gained nor lost---it is always transferred from somewhere (a source account) to somewhere else (a destination account). This transfer is known as a transaction, and each transaction requires at least two accounts.

Earmarked Funds – Funds representing Special Funds to be utilised for specific purposes.

Expenses – A cost relating to the operations of an accounting period or to the revenue earned during the period or the benefits of which do not extend beyond that period.

Fair Market Value – Price at which property would change hands between a buyer and a seller without any compulsion to buy or sell, and both having reasonable knowledge of the relevant facts.

Financial Statement – A balance sheet, income statement (income and expenditure), receipts & payment statement or any other supporting statement or other presentation of financial data derived from accounting records.

Fixed Asset – Asset held for the purpose of providing services and that is not held for resale in the normal course of operations of the business enterprise.

Fixed Deposit – Deposit for a specified period and at specified rate of interest.

Fund – The term fund refers to the amount set aside for a general or specific purpose, whether represented by specifically earmarked assets or not.

Grants – Grants are assistance by State Government and/ or Central Government in cash or kind to an organisation for past or future compliance with certain conditions.

Gross Block – The total cost of acquisition/ purchase of all the Fixed Assets of the business enterprise.

Income – Money or money equivalent earned or accrued during an accounting period, increasing the total of previously existing net assets, and arising from provision of any type of services and rentals.

Income and Expenditure Statement – A financial statement, prepared by institutions in double entry accounting system on accrual basis to present their revenues and expenses for an accounting period and to show the excess of revenues over expenses (or vice-versa) for that period. It is similar to Profit and Loss Statement and is also called revenue and expense statement.

Interest – The service charge for the use of money or capital, paid at agreed intervals by the user, and commonly expressed as an annual percentage of outstanding principal.

Internal Control – The plan of organization and all the methods and procedures adopted by the management of a Body to assist in achieving management’s objective of ensuring, as far as practicable, the orderly and efficient conduct of its business, including adherence to management policies, the safeguarding of assets, prevention and detection of fraud and error, the accuracy and completeness of the accounting records, and the timely preparation of reliable financial information.

Financial Statements – Classification & Terminology

15

Investments – Assets held not for operational purposes or for rendering services, i.e., assets other than fixed assets or current assets (e.g. securities, shares, debentures, immovable properties).

Inventory – The values of those goods which are lying unsold at the end of accounting year. It also known as ‘Stock.’

Inter unit transactions – Transactions between one and more accounting units of the business enterprise.

Infrastructure Assets – Those assets with the characteristics of being, a part of a system or network, specialised in nature and do not have alternative uses, immovable, and subject to constraints on disposal.

Journal Book – The book of original entry in which the ‘dual aspect’ of transactions other than those involving cash and/ or bank, along with explanations, is recorded in their chronological order , from which a posting is done in the relevant ledger.

Journal Entry – Recording of transaction other than those involving cash and/ or bank by dividing into its debit and credit aspects.

Ledger – A compilation of all accounts used for accounting purposes.

Performa of Ledger

LEDGER

Group – Head Ledger Account

Date Particulars C.B. Folio

Debit Credit Dr. or Cr.

Balance

` P. ` P. ` P.

Lease – A lease is an agreement whereby the less or conveys to the lessee in return for a payment or series of payments the right to use an asset for an agreed period. A lease agreement also includes a Hire Purchase agreement. A lease is classified as a finance lease if it transfers substantially the entire risks and rewards incident to ownership. All other leases are classified as operating leases.

Liability – An amount owing by one person to another, payable in money, or in goods or services: the consequence of an asset or service received or a loss incurred or accrued; particularly, any debt (a) due or past due (current liability), (b) due at a specified time in the future (e.g. funded debt, accrued liability), or (c) due only on failure to perform a future act (contingent liability).

Training Material: Introduction to Accounting of Transactions — With Specific Reference to MGNREGA Scheme

16

Long term investments – Any investment falling outside the ambit of current investments are treated as long-term investments.

Mortgage – A lien on land, buildings, machinery, equipment, and other property, fixed or movable, given by a borrower to the lender as security for his loan; sometimes called a deed of trust.

Narration – A brief description written below an Accounting Entry. It explains as to why the entry has been recorded and other related aspects of the entry.

Net Assets – The excess of the book value of the assets of a Body over its external liabilities.

Net Block – Gross Block less Accumulated Depreciation of all the Fixed Assets of the business enterprise.

Period End – The last day of any Accounting Period, e.g., quarter, half-year or year-end.

Prepaid Expense – Payment for expense in an accounting period, the benefit for which will accrue in the subsequent accounting period(s).

Purchase – The goods which are purchased in which business deals or for resale purpose are known as ‘Purchase.’

Purchase Return – When purchase goods are returned to suppliers these are known as ‘Purchase Return’ or ‘ Return Outward.’

Ratio Analysis – Analysis of relationship worked out among various accounting data which are mutually interdependent and which influence each other in a significant manner, arises from the fact that often absolute figures standing alone convey no meaning. They become significant only when considered with other figures. It also helps in comparing the actual or projected data for a particular business enterprise to the data of that business enterprise or any other business enterprises in order to analyse trends or relationship.

Receipt – A written acknowledgement of something acquired; hence, an accounting document recording the physical receipt of cash/ cheques.

Receipts & Payments Statement – A financial statement prepared for an accounting period to depict the changes in the financial position and to present the cash received in and paid out in whatever form (cash, cheques, etc.) under certain headings. All non-cash related transactions are ignored while preparing this Statement.

Reconciliation – It means identifying the difference between two items (i.e. amounts, balances, accounts or statements) so that the figures agree.

Revenue Expenditure – It means outlay benefiting only the current year. It is treated as an expense to be matched against revenue.

Sale – It means transfer of ownership of goods and services to customer. The term ‘sales’ is used only for the sales of those goods which are purchased for resale purpose. It includes both cash sales and credit sales.

Sales Return – When sold goods are received back from customers then it is known as ‘Sales Return’ or ‘return outward.’

Special Fund – An amount set aside for a specific purpose represented by specifically earmarked assets.

Straight Line Method (SLM) – The method under which the periodic charge for depreciation is computed by dividing the depreciable amount of a depreciable asset by the estimated number of years of its useful life. It also known as Fixed Installment Method or Original Cost Method.

Surplus – The excess of income over expenditure of the business enterprise for an Accounting Period under consideration.

Financial Statements – Classification & Terminology

17

Trial Balance – A list or abstract of the balances or of total debits and total credits of the accounts in a ledger, the purpose being to determine the equality of posted debits and credits and to establish a basic summary for financial statements. Its main objective is to check the Arithmetical Accuracy of the business transactions.

Useful Life – The period over which a depreciable asset is expected to be used by the enterprise; or (ii) the number of production or similar units expected to be obtained from the use of the asset by the enterprise.

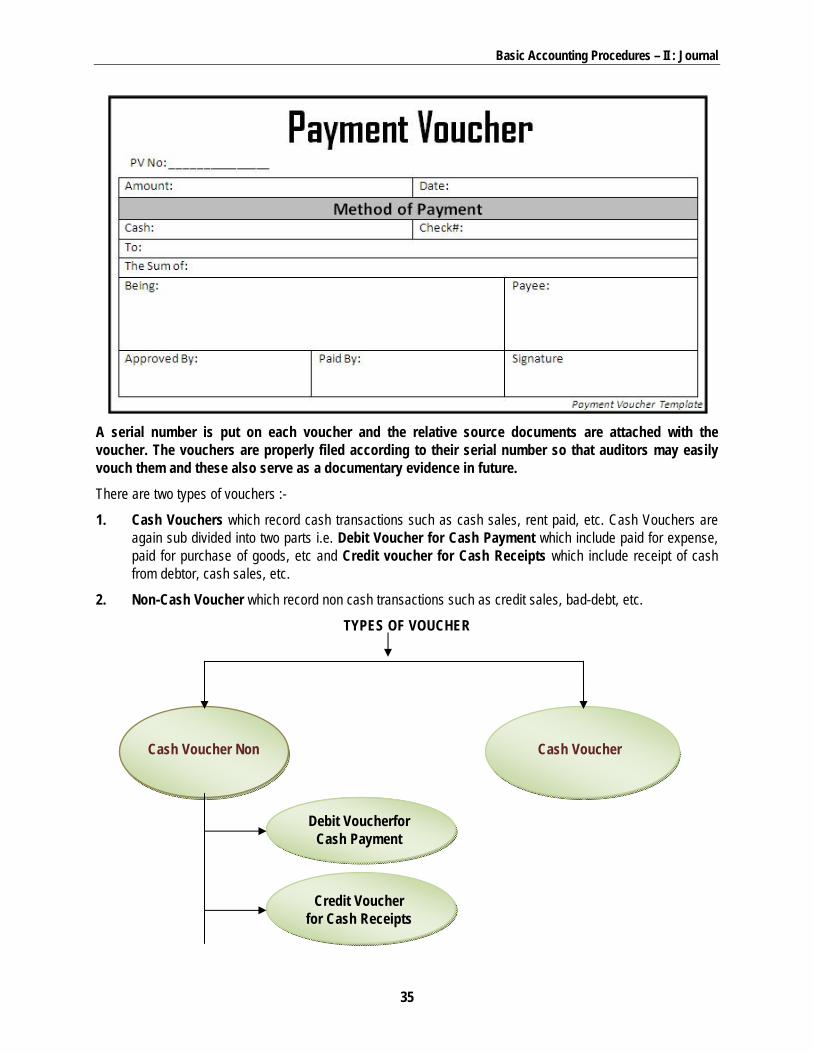

Voucher – A document which serves as an authorisation for any financial transaction and forms the basis for recording the accounting entry for the transaction in the books of original entry, e.g., Cash Receipt Voucher, Bank Receipt Voucher, Journal Voucher, Payment Voucher, etc.

Written Down Value (WDV) – Written Down Value in respect of an asset, means its cost of acquisition or substituted value less accumulated depreciation.

Written Down Value (WDV) Method – A method under which the periodic charge for depreciation of an asset is computed by applying a fixed percentage to its historical cost or substituted amount less accumulated depreciation (net book value). This is also referred to as “Diminishing Balance Method”.

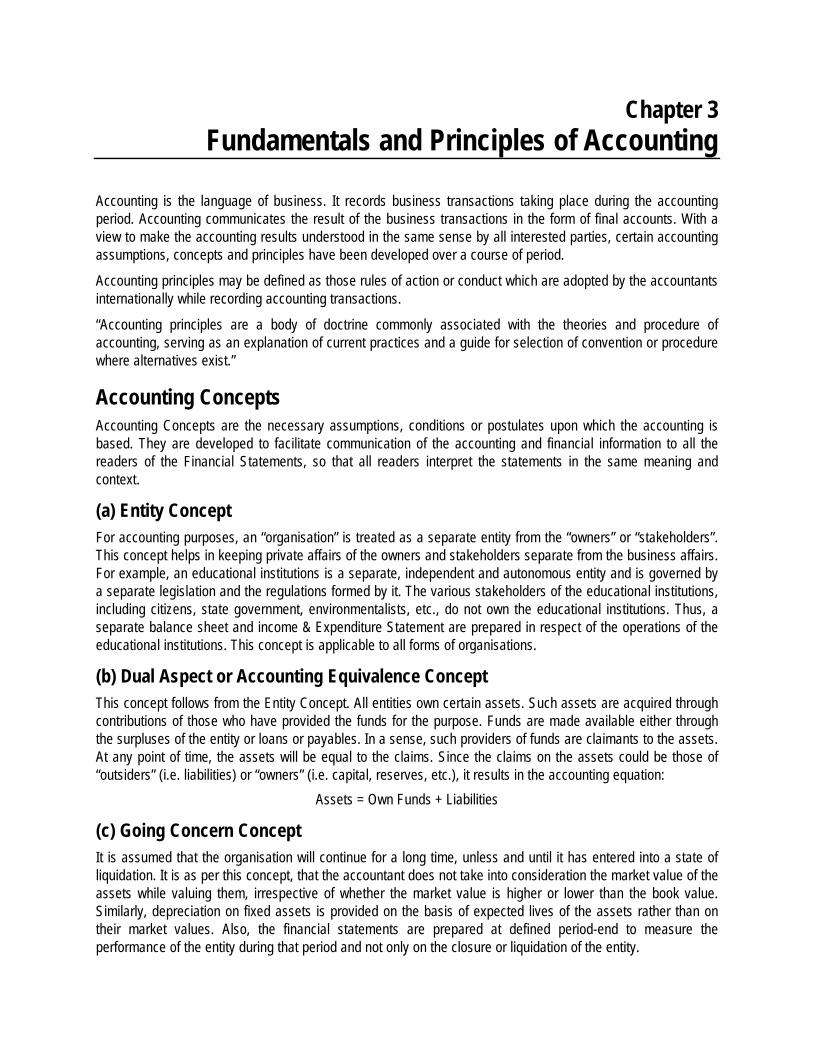

Chapter 3 Fundamentals and Principles of Accounting

Accounting is the language of business. It records business transactions taking place during the accounting period. Accounting communicates the result of the business transactions in the form of final accounts. With a view to make the accounting results understood in the same sense by all interested parties, certain accounting assumptions, concepts and principles have been developed over a course of period.

Accounting principles may be defined as those rules of action or conduct which are adopted by the accountants internationally while recording accounting transactions.

“Accounting principles are a body of doctrine commonly associated with the theories and procedure of accounting, serving as an explanation of current practices and a guide for selection of convention or procedure where alternatives exist.”

Accounting Concepts Accounting Concepts are the necessary assumptions, conditions or postulates upon which the accounting is based. They are developed to facilitate communication of the accounting and financial information to all the readers of the Financial Statements, so that all readers interpret the statements in the same meaning and context.

(a) Entity Concept For accounting purposes, an “organisation” is treated as a separate entity from the “owners” or “stakeholders”. This concept helps in keeping private affairs of the owners and stakeholders separate from the business affairs. For example, an educational institutions is a separate, independent and autonomous entity and is governed by a separate legislation and the regulations formed by it. The various stakeholders of the educational institutions, including citizens, state government, environmentalists, etc., do not own the educational institutions. Thus, a separate balance sheet and income & Expenditure Statement are prepared in respect of the operations of the educational institutions. This concept is applicable to all forms of organisations.

(b) Dual Aspect or Accounting Equivalence Concept This concept follows from the Entity Concept. All entities own certain assets. Such assets are acquired through contributions of those who have provided the funds for the purpose. Funds are made available either through the surpluses of the entity or loans or payables. In a sense, such providers of funds are claimants to the assets. At any point of time, the assets will be equal to the claims. Since the claims on the assets could be those of “outsiders” (i.e. liabilities) or “owners” (i.e. capital, reserves, etc.), it results in the accounting equation:

Assets = Own Funds + Liabilities

(c) Going Concern Concept It is assumed that the organisation will continue for a long time, unless and until it has entered into a state of liquidation. It is as per this concept, that the accountant does not take into consideration the market value of the assets while valuing them, irrespective of whether the market value is higher or lower than the book value. Similarly, depreciation on fixed assets is provided on the basis of expected lives of the assets rather than on their market values. Also, the financial statements are prepared at defined period-end to measure the performance of the entity during that period and not only on the closure or liquidation of the entity.

Fundamentals and Principles of Accounting

19

(d) Money Measurement Concept

In accounting, every transaction is recorded in terms of money. Events or transactions that cannot be expressed in terms of money are not recorded in the books of accounts. Receipt of income, payment of expenses, purchase and sale of assets, etc., are monetary transactions that are recorded in the books of accounts. For example, the event of a machinery breakdown is not recorded as it does not have a monetary value. However, the expenditure incurred for the repair of the machinery can be measured in monetary value and hence is recorded.

(e) Cost Concept

As per this concept, an asset is ordinarily recorded at the price paid to acquire it, i.e., at its cost and this cost is the basis for all subsequent accounting for the asset. The cost concept does not mean that the asset will always be shown at cost. This basically signifies that each time the financial statements are prepared; the fixed assets need not be revised and recorded at its realisable or replacement or market value. The assets recorded at cost at the time of purchase may systematically be reduced through depreciation.

(f) Accounting Period Concept

An accounting period is the interval of time at the end of which the financial statements are prepared to ascertain the financial performance of the organisation. Although the “going concern” concept stresses the continuing nature of the entity, it is necessary for an organisation to review how it is performing. The preparation of financial statements at periodic intervals helps in taking timely corrective actions and developing appropriate strategies. The accounting period is normally considered to be of twelve months.

(g) Accrual Concept

Under the cash system of accounting, the revenues and expenses are recorded only if they are actually received or paid in cash, irrespective of the accounting period to which they belong. But under the accrual concept, occurrence of claims and obligations in respect of incomes or expenditures, assets or liabilities based on happening of any event, passage of time, rendering of services, fulfilment (partially or fully) of contracts, diminution in values, etc., are recorded even though actual receipts or payments of money may not have taken place. In respect of an accounting period, the outstanding expenses and the prepaid expenses and similarly the income receivable and the income received in advance are shown separately in the books of accounts under the accrual method.

(h) Periodic Matching of Cost and Revenue Concept

To ascertain the surplus or deficit made by the entity during an accounting period, it is necessary that the costs incurred are matched with the revenue earned by the entity during that accounting period. The matching concept is a corollary drawn from the accrual concept. To ascertain the correct surplus or deficit, it is necessary to make adjustments for all outstanding expenses, prepaid expenses, income receivable and income received in advance to correctly depict and match the income and expenditure relating to that accounting period.

(i) Realization Concept

According to this concept, revenue should be accounted for only when it is actually realised or it has become certain that the revenue will be realised. This signifies that revenue should be recognised only when the services are rendered or the sale is affected. However, in order to recognise revenue, actual receipt of cash is not necessary. What is important is that the organisation should be legally entitled to receive the amount for the services rendered or the sale affected.

Training Material: Introduction to Accounting of Transactions — With Specific Reference to MGNREGA Scheme

20

Accounting Conventions The term "accounting conventions" refer to the customs or traditions, which are used as a guide in the preparation of meaningful financial records in the form of the income statement (Profit and Loss Account) and the position statement (Balance Sheet).

(a) Convention of Disclosure

The term “disclosure” implies that there must be a sufficient revelation of information which is of material interest to owners, creditors, lenders, investors, citizens and other stakeholders. The accounts and the financial statements of an entity should disclose full and fair information to the beneficiaries in order to enable them to form a correct opinion on the performance of such entity, which in turn would allow them to take correct decisions. For example, the Accounting Principles that have been followed for preparation of the Financial Statements should be disclosed along with the Financial Statements for proper understanding and interpretation of the same.

(b) Convention of Materiality

An item should be regarded as material, if there is a sufficient reason to believe that knowledge of it would influence the decision of informed creditors, lenders, investors, citizens and other stakeholders. The accounts and the financial statements should impart importance to all material information so that true and fair view of the state of affairs of the entity is given to its beneficiaries. Hence, keeping the convention of materiality in view, unimportant items are not disclosed separately and are merged with other items. For example, the expenditure incurred on repairs and maintenance of a certain asset, which are small, may not be disclosed separately in respect of each such small item but may be grouped together and shown as a single item of expenditure.

(c) Convention of Consistency

The convention of consistency facilitates comparison of financial performance of an entity from one accounting period to another. This means that the accounting principles followed by an entity should be consistently applied by it over the years. For example, an organisation should not change its method of depreciation every year, i.e., from Straight Line Method to Written Down Value Method or vice-versa. Similarly, the method adopted for valuation of stocks, viz., First in First Out (FIFO) or Weighted Average should be consistently followed. In case a change is made, it should be disclosed.

(d) Convention of Conservatism

As per this convention, the anticipated profits should be ignored but all anticipated losses should be provided for in the books of accounts of an entity. This means that all prospective losses are taken into consideration, however, no doubtful income is taken into consideration in recording of transactions by an entity. For example, while provision for doubtful debts and discount is made on debtors or Accounts Receivables, no provision is made for likely discount receivable from creditors or Accounts Payables. Similarly, provision is made for diminution in value of investments; however, no provision is made for any appreciation in value of investments.

The Accounting Cycle: 9-Step Accounting Process The accounting cycle, also commonly referred to as accounting process, is a series of procedures in the collection, processing, and communication of financial information.

As defined earlier, accounting involves recording, classifying, summarizing, and interpreting financial information. Financial information is presented in reports called financial statements. But before they can be

Fundamentals and Principles of Accounting

21

prepared, accountants need to gather information about business transactions, record and collate them to come up with the values to be presented in these reports. The cycle does not end with the presentation of financial statements. Several steps are needed to be done to prepare the accounting system for the next cycle.

Though a detailed study of each of these accounting steps is incorporated later in this material, yet a brief overview about each of them is as under:

Accounting cycle steps:

1. Identifying and Analyzing Business Transactions

The accounting process starts with identifying and analyzing business transactions and events. Not all transactions and events are entered into the accounting system. Only those that pertain to the business entity are included in the process. For example, a loan made by the owner in his name that does not have anything to do with the entity is not accounted for. The transactions identified are then analyzed to determine the accounts affected and the amounts to be recorded. The first step includes the preparation of business documents, or source documents. A business document serves as basis for recording a transaction.

2. Recording in the Journals

A journal is a book – paper or electronic – in which transactions are recorded. Business transactions are recorded using the double-entry bookkeeping system. They are recorded in journal entries containing at least two accounts (one debited and one credited). To simplify the recording process, special journals are often used for transactions that recur frequently such as sales, purchases, cash receipts, and cash disbursements. A general journal is used to record those that cannot be entered in the special books. Transactions are recorded in chronological order and as they occur. Hence, journals are also known as Books of Original Entry.

3. Posting to the Ledger

Also known as Books of Final Entry, a ledger is a collection of accounts that shows the changes made to each account as a result of past transactions, and their current balances. This is the core of the classifying phase. After the posting process, the balances of each account can now be determined. For example, all journal entries made to Cash would be transferred into the Cash account in the ledger. Increases and decreases in cash will be entered into one ledger account. Thus, the ending balance of Cash can be determined.

4. Unadjusted Trial Balance

A trial balance is prepared to test the equality of the debits and credits. All account balances are extracted from the ledger and arranged in one report. Afterwards, all debit balances are added. All credit balances are also added. Total debits should be equal to total credits. When errors are discovered, correcting entries are made to rectify them or reverse their effect. Take note however that the purpose of a trial balance is only test the

Training Material: Introduction to Accounting of Transactions — With Specific Reference to MGNREGA Scheme

22

equality of total debits and total credits and not to determine the correctness of accounting records. Some errors could exist even if debits are equal to credits, such as double posting or failure to record a transaction.

5. Adjusting Entries

Adjusting entries are prepared as an application of the accrual basis of accounting. At the end of the accounting period, some expenses may have been incurred but not yet recorded in the journals. Some income may have been earned but not entered in the books. Adjusting entries are prepared to have the accounts updated before they are summarized into the financial statements. Adjusting entries are made for accrual of income, accrual of expenses, deferrals (income method or liability method), prepayments (asset method or expense method), depreciation, and allowances.

6. Adjusted Trial Balance

An adjusted trial balance may be prepared after adjusting entries are made and before the financial statements are prepared. This is to test if the debits are equal to credits after adjusting entries are made.

7. Financial Statements

When the accounts are already up-to-date and equality between the debits and credits have been tested, the financial statements can now be prepared. The financial statements are the end-products of an accounting system. A complete set of financial statements is made up of:

(1) Statement of Comprehensive Income (Income Statement and Other Comprehensive Income),

(2) Statement of Changes in Equity,

(3) Statement of Financial Position or Balance Sheet,

(4) Statement of Cash Flows, and

(5) Notes to Financial Statements.

8. Closing Entries

Temporary or nominal accounts, i.e. income statement accounts, are closed to prepare the system for the next accounting period. Temporary accounts include income, expense, and withdrawal accounts. These items are measured periodically. The accounts are closed to a summary account (often, Income Summary) and then closed further to the appropriate capital account. Take note that closing entries are made only for temporary accounts. Real or permanent accounts, i.e. balance sheet accounts, are not closed.

9. Post-Closing Trial Balance

In the accounting cycle, the last step is to prepare a post-closing trial balance. It is prepared to test the equality of debits and credits after closing entries are made. Since temporary accounts are already closed at this point, the post-closing trial balance contains real accounts only.

*Reversing Entries: Optional step at the beginning of the new accounting period

Reversing entries are optional. They are prepared at the beginning of the new accounting period to facilitate a smoother and more consistent recording process.

In this step, the adjusting entries made for accrual of income, accrual of expenses, deferrals under the income method, and prepayments under the expense method are reversed.

Chapter 4 Basic Accounting Procedures – I

Double Entry System of Book Keeping

Recording of business transactions has been in vogue in all countries of the world. In India, maintenance of accounts was practised not in such a developed form as we have today. Kautilya’s famous Arthasastra not only relates to Politics and Economics, but also explains the art of account keeping in a separate chapter. Written in 4th century BC, the book gives details about account keeping, methods of supervising and checking of accounts and also about the distinction between capital and revenue, income and expenses etc.

Double entry system was introduced to the business world by an Italian merchant named Lucas Pacioli in 1494 A.D. Though the system of recording business transactions in a systematic manner has originated in Italy, it was perfected in England and other European countries during the 18th century only i.e., after the Industrial Revolution. Many countries have adopted this system today.

Double Entry Accounting System Double Entry Accounting System recognizes that every transaction has a dual effect. There are two sides of every transaction. If one account is debited, any other account must be credited. Every transaction affects at least two accounts in opposite directions. It may, however be noted, that the double entry does not mean that a transaction is recorded twice. But it means that at least two accounts are affected by a transaction one account receiving a benefit and other account yielding a benefit. It is because of dual aspect principle that the two sides of the Balance Sheet are always equal and the following accounting equation will always hold good at any point of time.

Assets = Liabilities + Capital (or Net Worth)

Or

Capital (or Net Worth) = Assets – Liabilities

Whenever a transaction is to be recorded, it has to be recorded in two or more accounts to balance the equation. If a transaction affects (increases or decreases) one side of equation, it will also affect (increase or decrease) the other side of equation or increase one account and decrease another account on the same side of equation. Equation remains balanced whenever a transaction takes place. E.g. Mr. A commences a business with ` 5 Lacs in cash and takes a loan of ` 1 Lacs from bank, and this ` 6 Lacs are used in buying some assets say plant & machinery,

The equation will be as follows:

Assets = Liabilities + Capital

` 6 Lakh = ` 1 Lakh + ` 5 Lakh

S. No.

Transaction Accounts affected

Assets Liabilities & Capital

1 Capital brought in Cash increases Capital increases

2 Purchase Goods for Cash Cash decreases Stock increases

Training Material: Introduction to Accounting of Transactions — With Specific Reference to MGNREGA Scheme

24

3 Purchase Goods on Credit Stock increases Creditors increase

4 Purchase Furniture for Cash Furniture increases Cash decreases

5 Paid Rent Cash decreases Rent = Expenses Therefore Capital decreases

6 Received Interest Cash Increases Interest = Income Therefore Capital increases

7 Sold Goods on Credit for ` 40,000 costing ` 30,000

Debtors increase by ` 40,000 Stock decreases by ` 30,000

Capital increases by ` 40,000 – 30,000 = ` 10,000

8 Paid to Creditors Cash decreases Creditors decrease

Account

An account is a record of all business transactions relating to a particular person or item. In accounting, separate record of each individual, asset, liability, expenses or income is kept.

It is stated that ‘an account is a summary of relevant transactions at one place relating to a particular head’.

All accounts are divided into two sides. The left side of an account is arbitrarily or traditionally called Debit side and the right side of an account is called the Credit side.

The terms originated from the Latin terms "debere" or "debitum" which means "what is due"; and "credere" or "creditum" which means "something entrusted or loaned". Every transaction has two aspects and each aspect has an account.

Different Accounting Systems and Basis of Accounting

Cash Based Double Entry Accounting System is rarely followed. Hence, we shall concentrate on understanding the basic difference between Cash Based Single Entry Accounting and Accrual Based Double Entry Accounting:

Single Entry Accounting

Cash Based

Double Entry Accounting

Cash based Accrual based

Basic Accounting Procedures – I : Double Entry System of Book Keeping

25

Basis of Distinction Cash Based Single Entry Accounting

Accrual Based Double Entry Accounting

Nature of Transaction All receipts and payments during the Accounting period are recorded whether or not the transactions actually belong to that accounting period.

All income and expenses relating to the Accounting period are recorded, whether or not received or paid actually.

Accounts Only personal accounts and Cash Book are opened.

Personal, Real and Nominal accounts are opened.

Accuracy of results Accuracy of transactions cannot be verified since all transactions are recorded on single entry basis and no trial balance is prepared.

All transactions are recorded based on double entry book keeping, a trial balance is prepared to check the arithmetical accuracy of the transactions.

Financial Performance Only receipt and payment account is prepared, hence financial performance cannot be ascertained as Income and Expenditure Account is not prepared.

Financial performance of an entity can be ascertained by preparing the Income and Expenditure Statement.

Financial Position Only a Statement of Affairs is prepared which does not give the true and fair statement of affairs.

A balance sheet is prepared on going concern basis which gives a true and fair state of affairs.

Authenticity This system is not considered authentic by the Financial Institutions, lending agencies and other outside bodies.

This system of accounting is well accepted by Financial Institutions, lending agencies and all outside bodies.

Double Entry Accrual Based Accounting

Receipt

Receipt Voucher

Cash Book

Payment

Payment Voucher

Cash Book

Deposit Withdrawal

Contra Voucher

Cash Book

Non cash Transactions

Journal Voucher

Journal

Training Material: Introduction to Accounting of Transactions — With Specific Reference to MGNREGA Scheme

26

Classification of Accounts

Transactions can be divided into three categories.

Transactions relating to individuals and firms

Transactions relating to properties, goods or cash

Transactions relating to expenses or losses and incomes or gains.

Therefore, accounts can also be classified into Personal, Real and Nominal. The classification may be illustrated as follows:

Accounts

Personal Impersonal

Natural Artificial Representative Real Nominal

Tangible Intangible

I. Personal Accounts: The accounts which relate to persons. Personal accounts include the following.

(i) Natural Persons: Accounts which relate to individuals. For example, Mohan’s A/c, Shyam’s A/c etc.

(ii) Artificial persons: Accounts which relate to a group of persons or firms or institutions. For example, HMT Ltd., Indian Overseas Bank, Life Insurance Corporation of India, Cosmopolitan club etc.

Representative Persons: Accounts which represent a particular person or group of persons. For example, outstanding salary account, prepaid insurance account, etc.

A business concern may keep business relations with all the above personal accounts, because of buying goods from them or selling goods to them or borrowing from them or lending to them. Thus they become either Debtors or Creditors.

The proprietor being an individual, his capital account and his drawings account are also personal accounts.

II. Impersonal Accounts: All those accounts which are not personal accounts. This is further divided into two types viz. Real and Nominal accounts.

(i) Real Accounts: Accounts relating to properties and assets which are owned by the business concern. Real accounts include tangible and intangible accounts. For example, Land, Building, Goodwill, Purchases, etc.

(ii) Nominal Accounts: These accounts do not have any existence, form or shape. They relate to incomes and expenses and gains and losses of a business concern. For example, Salary Account, Dividend Account, etc.

Basic Accounting Procedures – I : Double Entry System of Book Keeping

27

Illustration:

Classify the following items into Personal, Real and Nominal Accounts.

1. Capital 2. Sales

3. Drawings 4. Outstanding salary

5. Cash 6. Rent

7. Interest paid 8. Indian Bank

9. Discount received 10. Building

11. Bank 12. Chandrasekar

13. Murugan Lending Library 14. Advertisement

15. Purchases

Solution:

1. Personal account 2. Real account

3. Personal account 4. Personal (Representative) account

5. Real account 6. Nominal account

7. Nominal account 8. Personal (Legal Body) account

9. Nominal account 10. Real account

11. Personal account 12. Personal account

13. Personal account 14. Nominal account

15. Real account

Accounting Equation Based Classifications of Accounts

The source document is the origin of a transaction and it initiates the accounting process, whose starting point is the accounting equation.

Accounting equation is based on dual aspect concept (Debit and Credit). It emphasizes on the fact that every transaction has a two sided effect i.e., on the assets and claims on assets. Always the total claims (those of outsiders and of the proprietors) will be equal to the total assets of the business concern. The claims are also known as equities, and are of two types: i.) Owners equity (Capital); ii.) Outsiders’ equity (Liabilities).

The classification of accounts, accounting to ‘Accounting Equation’ approach is given below:

Type of Account Meaning Example

Asset Account These accounts relate to tangible and intangible real assets

Tangible: Land, Building, Machinery, etc. Intangible: Trademarks, Goodwill

Liability Account These accounts relate to the financial obligations of an organization towards outsiders.

Salaries payable, creditors, outstanding expenses, bank overdrafts, short terms/ long term borrowings. etc.

Capital Fund These accounts relate to owners of the organization

Educational Institutions funds

Training Material: Introduction to Accounting of Transactions — With Specific Reference to MGNREGA Scheme

28

Assets = Equities

Assets = Capital + Liabilities (A = C+L)

Capital = Assets – Liabilities (C = A–L)

Liabilities = Assets – Capital (L = A–C)

Effect of Transactions on Accounting Equation:

Illustration

If the capital of a business is ` 3,00,000 and other liabilities are ` 2,00,000 calculate the total assets of the business.

Solution

Assets = Capital + Liabilities

Capital + Liabilities = Assets

` 3,00,000 + ` 2,00,000 = ` 5,00,000

Illustration

If the total assets of a business are ` 3,60,000 and capital is ` 2,00,000, calculate liabilities.

Solution

Assets = Capital + Liabilities

Liabilities = Assets – Capital

Assets – Capital = Liabilities

` 3,60,000 – ` 2,00,000 = ` 1,60,000

Illustration

Transaction 1: Murugan started business with ` 50,000 as capital.

The business unit has received assets totalling ` 50,000 in the form of cash and the claims against the firm are also ` 50,000 in the form of capital. The transaction can be expressed in the form of an accounting equation as follows:

Assets = Capital + Liabilities

Cash = Capital + Liabilities

` 50,000 = ` 50,000 + 0

Transaction 2: Murugan purchased furniture for cash ` 5,000.

The cash is reduced by `,5,000 but a new asset (furniture) of the same amount has been acquired. This transaction decreases one asset (cash) and at the same time increases the other asset (furniture) with the same amount, leaving the total of the assets of the business unchanged. The accounting equation now is as follows:

Assets = Capital + Liabilities Cash + Furniture = Capital + Liabilities

Transaction 1 50,000 + 0 = 50,000 + 0 Transaction 2 (–) 5,000 + 5,000 = 0 + 0

45000 + 5000 = 50000 + 0

Basic Accounting Procedures – I : Double Entry System of Book Keeping

29

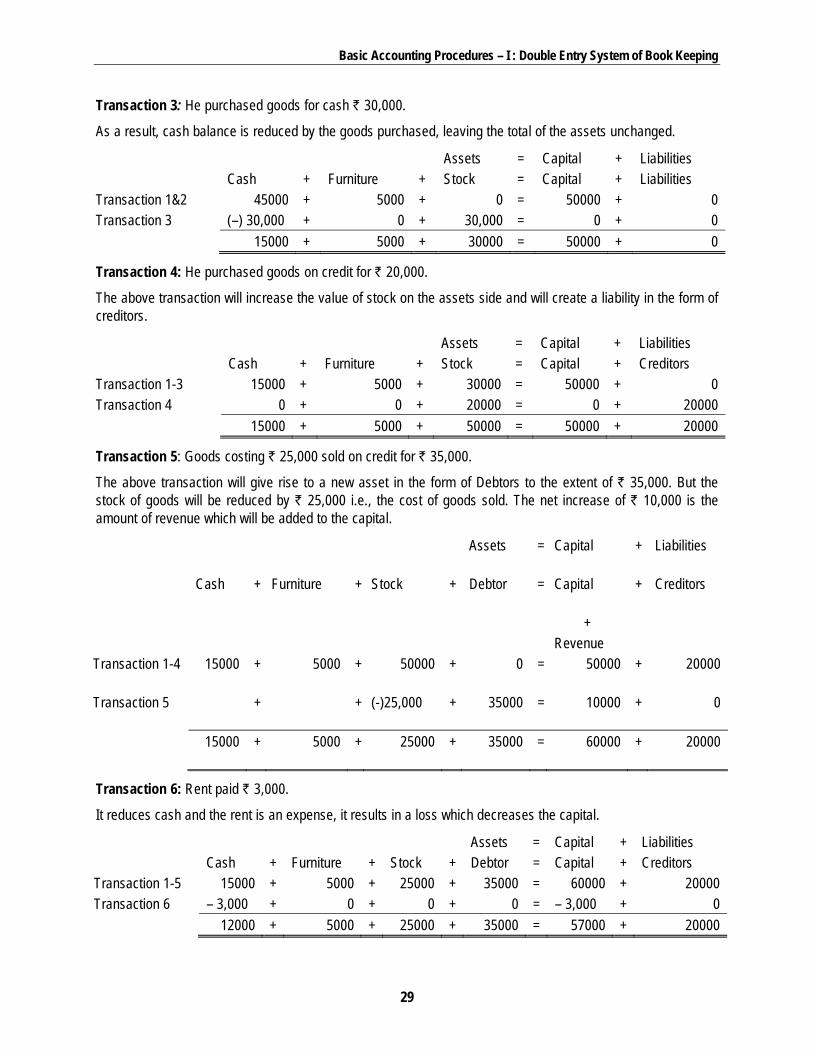

Transaction 3: He purchased goods for cash ` 30,000.

As a result, cash balance is reduced by the goods purchased, leaving the total of the assets unchanged.

Assets = Capital + Liabilities Cash + Furniture + Stock = Capital + Liabilities

Transaction 1&2 45000 + 5000 + 0 = 50000 + 0 Transaction 3 (–) 30,000 + 0 + 30,000 = 0 + 0

15000 + 5000 + 30000 = 50000 + 0

Transaction 4: He purchased goods on credit for ` 20,000.

The above transaction will increase the value of stock on the assets side and will create a liability in the form of creditors.

Assets = Capital + Liabilities Cash + Furniture + Stock = Capital + Creditors

Transaction 1-3 15000 + 5000 + 30000 = 50000 + 0 Transaction 4 0 + 0 + 20000 = 0 + 20000

15000 + 5000 + 50000 = 50000 + 20000

Transaction 5: Goods costing ` 25,000 sold on credit for ` 35,000.

The above transaction will give rise to a new asset in the form of Debtors to the extent of ` 35,000. But the stock of goods will be reduced by ` 25,000 i.e., the cost of goods sold. The net increase of ` 10,000 is the amount of revenue which will be added to the capital.

Assets =

Capital + Liabilities

Cash + Furniture + Stock + Debtor =

Capital + Creditors

+ Revenue Transaction 1-4 15000 + 5000 + 50000 + 0 =

50000 + 20000

Transaction 5 + + (-)25,000 + 35000 =

10000 + 0

15000 + 5000 + 25000 + 35000 =

60000 + 20000

Transaction 6: Rent paid ` 3,000.

It reduces cash and the rent is an expense, it results in a loss which decreases the capital.

Assets = Capital + Liabilities Cash + Furniture + Stock + Debtor = Capital + Creditors

Transaction 1-5 15000 + 5000 + 25000 + 35000 = 60000 + 20000 Transaction 6 – 3,000 + 0 + 0 + 0 = – 3,000 + 0

12000 + 5000 + 25000 + 35000 = 57000 + 20000

Training Material: Introduction to Accounting of Transactions — With Specific Reference to MGNREGA Scheme

30

From the above transactions, it may be concluded that every transaction has a double effect and in each case – Assets = Capital + Liabilities, i.e., ‘Accounting equation is true in all cases’. The last equation appearing in the books of Mr. Murugan may also be presented in the form of a statement called Balance Sheet. It will appear as below:

Balance Sheet of Mr. Murugan as on . . . . . . . . . . . . . .

Liabilities ` Assets `

Capital Creditors

57,000 20,000

Cash Stock Debtors Furniture

12,000 25,000 35,000

5,000

77,000 77,000

Practical Problem Show the Accounting Equation on the basis of the following transactions and prepare a Balance Sheet on the basis of the last equation.

1. Maharajan commenced business with cash 1,00,000

2. Purchased goods for cash 70,000

3. Purchased goods on credit 80,000

4. Purchased furniture for cash 3,000

5. d rent 2,000

6. SolSold goods for cash costing ` 45,000 60,000

7. Paid to creditors 20,000

8. Withdrew cash for private use 10,000

9. Paid salaries 5,000

10. Sold goods on credit (cost price ` 60,000) 80,000

Chapter 5 Basic Accounting Procedures – II

Journal