TRADE FINANCE: TRADE FINANCE: INSTRUMENTS, INSTRUMENTS, TECHNIQUES AND TECHNIQUES AND PROVIDERS PROVIDERS Summary description This section introduces the basics of trade finance. It discusses how traditional techniques of pre- and post-shipment finance relate to financing forms such as forfaiting, countertrade, structured finance, islamic finance, securitization, etc.; all of these techniques are all discussed in greater detail in separate chapters. Trade finance is available from different sources - from suppliers to banks and institutional investors. These various sources are discussed in some detail in the following section. In the final sections, the principles of loan syndication, and issues related to lines of credit are discussed.

TRADE FINANCE: INSTRUMENTS, TECHNIQUES AND PROVIDERS Summary description This section introduces the basics of trade finance. It discusses how traditional.

Dec 22, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

TRADE FINANCE:TRADE FINANCE: INSTRUMENTS, INSTRUMENTS,

TECHNIQUES ANDTECHNIQUES ANDPROVIDERSPROVIDERS

Summary description

This section introduces the basics of trade finance. It discusses how traditional techniques of pre- and post-shipment finance relate to financing forms such as forfaiting, countertrade, structured finance, islamic finance, securitization, etc.; all of these techniques are all discussed in greater detail in separate chapters.

Trade finance is available from different sources - from suppliers to banks and institutional investors. These various sources are discussed in some detail in the following section.

In the final sections, the principles of loan syndication, and issues related to lines of credit are discussed.

2

Table of ContentsTable of ContentsI. IntroductionII. Trade finance and trade paymentsIII. Tools of trade financeIV. Forms of trade financeV. Sources of trade financeVI. Loan syndicationVII. Examples on simple trade financing trade

to more structured trade finance mechanisms

Click here for "GENERAL GUIDELINES FOR

REDUCING THE RISKS OF TRADE FINANCE"

Click here for " BANKS' BASIC LENDING BANK

RATIONALES"

3

Trade finance is the provision of any form of financing that enables a trading activity to take place.

Trade financing can be given directly to the supplier, to enable him procure items for immediate sale and/or for storage for future activities. It could also be provided to the buyer, to enable him meet contract obligations. Or it could be given to a trader, for on-lending to his suppliers.

This training program focuses on international commodity trade finance.

4

The Transaction Chain

Flow of Goods Flow of Goods

Producer

Trader

Consumer

BANK

Bridge Financing

Pre-shipment FinancingPost-shipment Financing Import Financing

Typical forms of international trade Typical forms of international trade & commodity financefinance

Trade finance requirements can be divided into two types: pre-shipment finance and post-shipment finance. Depending on the length of credit required, financing facilities are offered for short-, medium- or long-term period. Commodity trading normally require short-term finance which is provided for up to one year. However, commodities' producers and traders may require medium-term (between one and five years) or long-term (five years or longer) financing facilities for investment or installation projects and also for working capital issues.

5

Evolution

Banks have been involved in international trade since, at least, medieval times. At that time, the services provided aimed at circumventing risks, reducing costs and effecting payment in the required currency.

This basic service has undergone remarkable changes leading to banks now providing a wide range of trade and project finance services to their customers, using a range of financing instruments.

Much of this change has been due to economic events such as crises in developing countries and the bankruptcy of major trading firms. These have, in recent times, precipitated the need for financiers to adopt innovative, structured financing techniques to mitigate their risk of losses.

A separate chapter will emphasize the role of structured finance and will explain the various forms of structured finance, using different approaches.

6

II. International trade finance and trade paymentsInternational trade requires international payments, and more specifically, trade payment systems that make such payments safer for the transaction and for both buyer and seller consequently. This is discussed extensively in the chapter on trade payment systems. Such payment systems, including sales on Open account, Cash in advance, Cash Against Documents (CAD) and Letters of Credit (L/Cs) (also called documentary credits) are not in themselves financing instruments However, they can and often are used as an element in and supports to trade financing transactions.

For example, cash in advancecash in advance may be considered a payment mechanism that provide credit to the exporter since the exporter will receive part of payment prior to shipment, which will enable him to produce. Moreover, sales on open accountopen account may be considered as a payment mechanism that facilitate the financing of the transaction. On one side, the buyer is receiving the goods from the seller before making payment, which gives him time to to resell the goods and make payment. On the other side, the open account lead to trade bills – invoices sent by the seller and confirmed by the buyer, with a guarantee by the buyer’s bank. These trade bills can be used to generate finance to the seller in several ways. Similarly, CADsCADs result in confirmations of the buyer that they will pay once they receive certain documents.

L/CsL/Cs generally show an irrevocable promise to pay by a buyer once the seller has performed as stipulated in the L/C, and banks may feel this is sufficient comfort for them to extend a credit to a seller enabling him to finance his local operations prior to exports. L/C can also be a simple way for importer to obtain short-term finance where the bank can pay the buyer and keep the documents until full repayment of the loan by importer. Letters of credit are discussed further in several sections:

1. Documentary credits as a trade payment system2. Types of Letters of Credit 3. Rules and regulations governing Documentary credit 4. Letters of Credit as transferable instruments 5. How to use letters of credit as a financing support 6. Documents used in Documentary Credit7. Guidelines to avoid discrepancies when using Documentary Credit8. Standby LC

Letters of credit are discussed further in several sections:1. Documentary credits as a trade payment system2. Types of Letters of Credit 3. Rules and regulations governing Documentary credit 4. Letters of Credit as transferable instruments 5. How to use letters of credit as a financing support 6. Documents used in Documentary Credit7. Guidelines to avoid discrepancies when using Documentary Credit8. Standby LC

7

III. Tools of international trade financeIn general terms, trade financetrade finance can be separated into pre-shipment and post-shipment finance. Pre-shipment finance is for the financing of one or more of the stages in the commodity chain before the actual export of the commodity (for e.g. financing required to cover the installation of plant and equipment as well as the cost of production, packing, storage and transportation of goods to the port of shipment). Post-shipment finance is for the financing of the stages after the good has been shipped for international transport while awaiting payment.

For both pre-shipment and post-shipment finance, banks (and other financiers) have a number of financing tools in their toolkit. Some forms of finance are fairly standardized and well-known by banks and clients alike, others require a more creative, tailor-made use of the various tools.

In this section, some of these tools are described - this is not an exhaustive description, but just describes some of the key terminology and building blocks for trade finance. The next section then describes how these tools are used in various forms of trade finance.

Goods not produced yet

Producer signs export contract

Goods in up-country warehouses

Goods being processed locally

Goods in local transit

Goods in export warehouses

Pre-shipment financePre-shipment finance

Goods in transit through 3rd country

Goods stored in transit port

Goods at sea

Goods in import warehouses

Goods in overland transport to buyer

Goods processed by buyer

Goods already sold by buyer

Post-shipment financePost-shipment finance

8

Goods not produced yet

Producer signs export contract

Goods in up-country warehouses

Goods being processed locally

Goods in local transit

Goods in export warehouses

Pre-shipment financePre-shipment finance

Goods in transit through 3rd country

Goods stored in transit port

Goods at sea

Goods in import warehouses

Goods in overland transport to buyer

Goods received by buyer

Goods processed by buyer

Goods already sold by buyer

Post-shipment financePost-shipment finance

Once an export contract has been signed,

this contract itself can becomean instrument for a financing.

If it is evidenced by, in particular, a letter of Credit which guaranteespayment if certain conditions are

met, a bank can then decide to providepre-export finance to enable

the seller to meet theseconditions.

When goods are loaded for

international shipment, the transport agent issuesa “railway bill”, a “bill of

lading”or a similar document.This document acts as a title

document: one normallyneeds it to receive the goodsfrom the transport agent on

discharge. A financiercan thus use it

for security to provide post-shipment

financing.

All these phasescan result in documents

which can supporta financing.

Moreover, if the producer (or processor) has a convincing track record in

finding overseas buyers, a financier may decide that this is sufficient basis to give him an overdraft. Or one could assign all future receivables to the bank or a “Special Purpose Vehicle” to

create a longer-term financing.

9

Goods not produced yet

Producer signs export contract

Goods in up-country warehouses

Goods being processed locally

Goods in local transit

Goods in export warehouses

Pre-shipment financePre-shipment finance

Goods in transit through 3rd country

Goods stored in transit port

Goods at sea

Goods in import warehouses

Goods in overland transport to buyer

Goods received by buyer

Goods processed by buyer

Goods already sold by buyer

Post-shipment financePost-shipment finance

When goods are in a warehouse, warehouse

receipts can be issued as evidenceof their existence. The goods can

also be inspected to ensure that they meet the requirements of the

contract. Moreover, the warehouse receipts can be

pledged or transferred(sold) to the financier,

as security.

Depending on the details of the

sales contract, in any of these phases the goods

need to be paid by the buyer.The payments due from

the buyer are called“accounts receivable”,

and can be assignedto secure afinancing.

By committing proceeds from future sale to reimbursement,

buyers can obtain finance.

10

Goods not produced yet

Producer signs export contract

Goods in up-country warehouses

Goods being processed locally

Goods in local transit

Goods in export warehouses

Pre-shipment financePre-shipment finance

Goods in transit through 3rd country

Goods stored in transit port

Goods at sea

Goods in import warehouses

Goods in overland transport to buyer

Goods received by buyer

Goods processed by buyer

Goods already sold by buyer

Post-shipment financePost-shipment finance

Both exporterand importer can

assign their portfolio of account receivables to a

financier, in return for up-frontcash (invoice discounting -

Factoring). Or they could just discount or sell the receivables

of specific contracts (bill discounting -

Forfaiting).

Banks canfinance processing, using

so-called trust receiptsunder which the

processor basically acts as agent for

the bank.

11

IV. Forms of international trade financeThis section describes in brief the traditional forms of pre-shipment and post-shipment finance, before discussing how other forms of financing can help address particular problems/risks in these traditional financing forms.

Pre-shipment finance

Pre-shipment finance is meant to enable the exporter the preparation of goods for export. Banks can provide:

• Bank overdrafts (it it’s the provision of instant credit by a lending institution, i.e. the amount by which withdrawals exceed deposits, or the extension of credit by a lending institution to allow for such a situation) click here for further description.

• Term loans – direct credit facilities (a business loan with a final maturity of more than one year – but normally for less than 180 days, payable according to a specified schedule), click here for further description.

• Credit lines (a line of credit is an agreement between a financial institution and a borrower allowing the latter to access credit up to an agreed amount), click here for further description.

• Foreign currency denominated trade facility also referred to as 'off-shore', although provided locally. By borrowing in the export invoice currency, the exporter creates a natural hedge i.e. the export proceeds and the loan are in the same currency and therefore there is no currency risk and no need for forward cover. However, this availability requires guarantee.

14

For example, the same international bank as above extended in 1995 a US$10 million line of credit directly to South Africa Sugar Association at a price of LIBOR + 0.875% (excluding commitment fees).

Short-term "export" loans and lines of credit

Exporters are more likely than importers to obtain clean line of credit to finance their marketing cycle. Short-term lines of credit would cover post-shipment or pre-shipment financing needs. But otherwise the same comments apply as in the case of importers.

Short-term foreign exchange lines of credit can be granted by local banks. [1] The financing can also be directly between the international bank and the local commodity company. [2]

For example, the Zambian subsidiary of an international bank granted in 1996 a US$1.5 mn cotton input facility to a local cotton producer at LIBOR +1.5% (excluding arrangement fees).

Short-Term “import” loans and lines of credit

An importer’s line of credit is an arrangement to finance one or more contracts to be subsequently entered into by the same importer and accepted by the bank as eligible.

Lines of credit would typically be granted by local banks which would in turn obtain financing from an international bank. The latter could be a correspondent bank, sometimes part of the same banking group than the local bank, and would establish a line of credit available for the local bank to draw on for general purpose or for a specific loan.

Clean lines of credit are difficult to obtain for commodity importers located in developing countries. Clean financing is generally limited to borrowers that can be regarded as “good credits” and, in any case, can be more expensive than structured finance. When the creditworthiness of the borrower is fair or poor, local banks would only lend on a secured basis and traditional security (e.g., mortgage on fixed assets) are typically onerous in more than one respect (for example a mortgage has to be registered or up-date for each new short-term financing, which is in any case difficult and costly).

16

Pre-shipment finance can also provide:

• Open local or international letters of credit to the benefit of the borrower’s local or international suppliers;

• Leasing or hire/purchase arrangements (e.g., to finance processing equipment - Lease Purchase is a term which is used to describe a type of hire purchase which includes a final or "balloon" payments at the end of an agreement, thus reducing monthly rental/repayments).

• Can, in several ways, provide advances against future export receivables, or can provide

• Guarantees.

Pre-shipment finance is normally disbursed in stages. The bank evaluates the borrower’s production (or procurement, or processing) operations, and fits its financing around the seasonality of these operations. Each tranche of financing is only disbursed when the borrower has undertaken certain activities.

Banks prefer to structure pre-shipment finance in such a way that:

they can be sure that the funds that they advance are indeed used for preparing goods for export; and

the liquidation of the facility is semi-automatic, from export proceeds, or through conversion to post-shipment finance.

17

Pre-shipment finance – with or without letters of credit/confirmed export orders

Generally, pre-shipment finance involves the opening of a L/C, or at least, an export order that the bank is able to verify (and coming from a buyer whose credit standing he can verify). There are then several ways to build pre-shipment finance on the basis of the L/C – e.g., it can be as a security to receive pre-financing arrangement (usually up to 80-85% of the sales value) or through red or green clauses incorporated in the L/C. The various forms are discussed in the section on How to use letters of credit as a financing support.

Banks may also give pre-shipment finance on the basis of a company’s past export performance. This is called a “running account facility”. They can be given in the form of an overdraft or a direct credit (as has been described previously).

Several of the main forms of Islamic finance have, as an objective, the provision of pre-export finance, e.g., packing credit to enable an exporter to assemble sufficient goods for export, or credits to finance local pre-export processing operations.

One structured finance application that is typically used for pre-shipment finance is pre-payment, in which a bank operates through an international trader to finance the procurement, processing, transport and storage of commodities at origin, prior to exports.

In order to stimulate exports, many governments have programmes that either provide direct pre-export finance to incumbent exporters, or that provide credit guarantees to banks that provide credits.

18

Post-shipment finance

Post-shipment finance can be given to the buyer or the exporter:

It can be given to the buyer who then can promptly pay the seller (“buyer’s credit”). It therefore allows the buyer not to commit his own funds to pay for the goods until some time after they have been shipped - preferably, until after he has already sold the goods.

Exporter operate in a very competitive buyer's market and in order to conclude an export sale, it is critical to offer attractive credit terms to the overseas buyer. Thus, Post-shipment finance can be given to the seller so that he can sell on deferred payment terms to the buyer (this is “seller’s credit”).

• Post-shipment finance is generally provided against shipping documents, as proof that the shipment has indeed been made. As the buyer normally takes possession of the goods before he reimburses the credit, the shipping documents only provide security to the bank for a limited period, basically while the goods are in international transit.

• Post-shipment finance is normally for a short- to medium-term period.

20

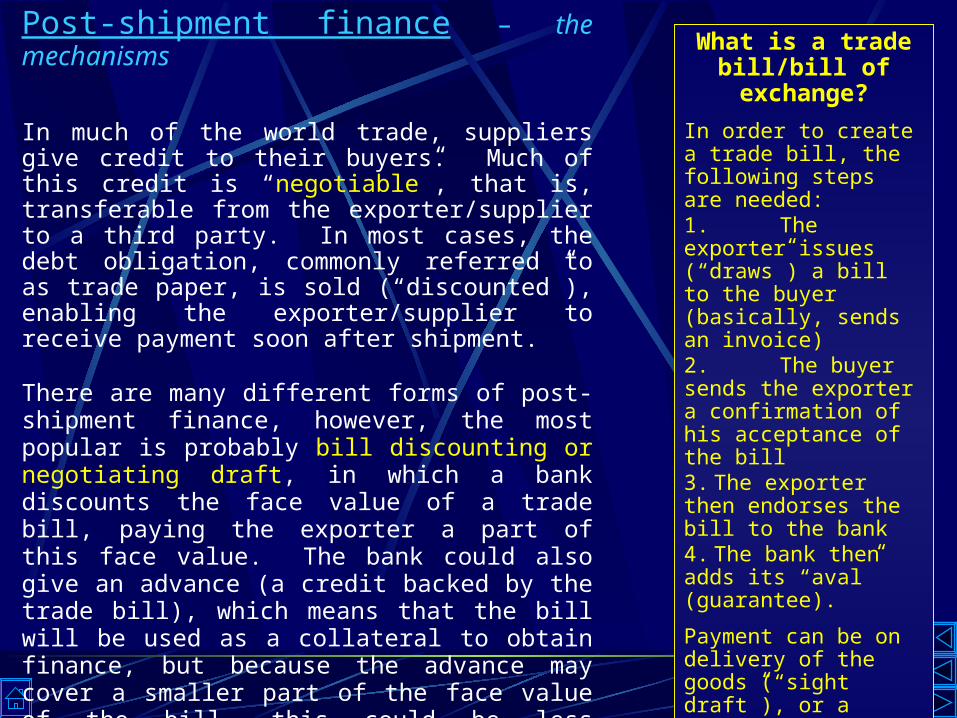

Post-shipment finance – the mechanisms

In much of the world trade, suppliers give credit to their buyers. Much of this credit is “negotiable”, that is, transferable from the exporter/supplier to a third party. In most cases, the debt obligation, commonly referred to as trade paper, is sold (“discounted”), enabling the exporter/supplier to receive payment soon after shipment.

There are many different forms of post-shipment finance, however, the most popular is probably bill discounting or negotiating draft, in which a bank discounts the face value of a trade bill, paying the exporter a part of this face value. The bank could also give an advance (a credit backed by the trade bill), which means that the bill will be used as a collateral to obtain finance, but because the advance may cover a smaller part of the face value of the bill, this could be less popular.

What is a trade bill/bill of exchange?

In order to create a trade bill, the following steps are needed:1. The exporter issues (“draws”) a bill to the buyer (basically, sends an invoice)2. The buyer sends the exporter a confirmation of his acceptance of the bill3. The exporter then endorses the bill to the bank4. The bank then adds its “aval” (guarantee).

Payment can be on delivery of the goods (“sight draft”), or a certain number of days after delivery (“term draft”).

21

Post-shipment finance – Bill discounting

Bill discountingBill discounting can be possible both when the exports were executed under a letter of credit, and when they were made under a documentary collection;

In the case of L/Cs, the bank will ensure that the shipping documents that have been delivered indeed conform to the requirements of the L/C. Then, assuming that the payment obligations under the L/C are by a reliable bank from a country for which they have a credit line, the bank will simply discount the face value of the L/C, applying its standard discount rate for the time until maturity. Note: Documentary Letters of Credit whether payable upon presentation of shipping documents or up to 360 days thereafter and other clearly defined terms, are among the most common negotiable term debt instruments and hold a critical function in international trade financing.

In the case of documentary collections, the bank will confirm that the export orders are indeed firm, and that the buyer has a good credit standing. If such is the case, they will then discount the bill. In documentary collections as with L/Cs, the bank has recourse to the exporter in case the buyer does not pay.

But there are also other post-shipment finance mechanisms, which may provide the exporter with non-recourse finance (in other words, the financier bears the risk of non-payment by the buyer). The exporter could resort to factoring, which does not involve drafts/bills of exchange; instead, the exporter hands over the full management of his debtor book to a factoring company, which in turn gives him an advance (i.e. discounting his account receivables). Or he could use the forfaiting market, for individual transactions/bills. In addition to L/C, and other negotiable debt instrument, forfaiting includes bank guarantees, bills of exchange, promissory notes.

Click here for more

22

Post-shipment finance – Bill discounting in in the absence of L/C

Without the use of an L/C, the exporter (beneficiary) can also grant extended payment terms directly to the importer and generally would issue bills of exchange addressed to, and accepted by, the importer (drawee and acceptor) who commits to pay on demand, or at a fixed or determinable future time, a certain sum to the exporter (drawer and, generally, payee).

Note: Bills of exchange are similar to invoices - the exporter issues a demand for payment to an importer (or to a guarantor). This is a trade bill, drawn by one commercial party on another. Once it has been accepted or endorsed by the importer, it becomes a trade acceptance, which, with a bank guarantee, becomes negotiable.

The claim may also be supported by promissory notes issued by the importer (or buyer) once the commodity has been accepted. Promissory notes are issued by the importer directly to the exporter, usually with a guarantee or “aval” from his bank. Such an “aval” is generally essential for making the notes negotiable. The importer pays for this guarantee, but its cost is in many cases more than offset by the lower interest rates on this form of credit.

Once an exporter has issued term drafts/bills of exchange or have accepted promissory notes issued by an importer/buyer, all of which guarantee a payment at some time in the future from the importer/buyer, he or she can negotiate or discount (sell for less than the face value) these instruments against cash. In other words, rather than providing credit to importers out of their own financial resources, exporters do so after having obtained refinancing from banks or other “discounters”.

23

Post-shipment finance – Negotiable instruments

There are three major types of such “trade paper” that can be used as a credit instrument : bills of exchange, promissory notes and bankers' bills of exchange, promissory notes and bankers' acceptanceacceptance. In the case of bankers' acceptance, the exporter can ask his bank to discount the trade paper, in which case it becomes a “bankers acceptance” (B/A). (Bankers' acceptance are explained separately in sub-chapter).

How to qualify as a negotiable instrument?

To qualify as a negotiable instrument, the trade paper must meet at least three conditions: First, the obligation that the buyer has to repay the debt to the exporter/supplier is absolute, that is without regard to performance of the underlying commercial transaction on the part of the exporter (or supplier). Nevertheless, the bank which originally accepts the trade paper will want assurance that the exporter/supplier will meet, or has met, his or her obligations under the commercial contract, and will generally disburse funds only after shipment. Second, the trade paper must be endorsed as “non-recourse” by each successive holder, meaning that the obligor remains the importer/buyer and that neither the exporter/supplier nor the previous holder(s) of the debt is(are) responsible for effecting repayment at maturity. Third and last, if the importer/buyer is not widely accepted as a highly creditworthy counterparty, then a guarantee must be provided by a third party, usually a solid bank with a record in international trade.

NOTE: Trade paper which is provided by highly creditworthy counterparties, or which has been guaranteed by reputable banks, is actively traded in a market which has as participants banks, traders (who provide much of the liquidity) and investors (individuals as well as investment funds). Banks and other investors often prefer trade paper over other debt instruments because it is seen as self liquidating. The market where trade paper is traded is thus both large and liquid, and is commonly referred to as the forfaiting market (explained in a separate chapter) Moreover, as the value of trade paper is based on single, real transactions, it is quite stable, much more so than other debt instruments.

NOTE: Trade paper which is provided by highly creditworthy counterparties, or which has been guaranteed by reputable banks, is actively traded in a market which has as participants banks, traders (who provide much of the liquidity) and investors (individuals as well as investment funds). Banks and other investors often prefer trade paper over other debt instruments because it is seen as self liquidating. The market where trade paper is traded is thus both large and liquid, and is commonly referred to as the forfaiting market (explained in a separate chapter) Moreover, as the value of trade paper is based on single, real transactions, it is quite stable, much more so than other debt instruments.

24

Post-shipment finance – Discounting based on documentary collections, risks for the bank

At times, post-shipment finance is on a “documents against payment” (DP) basis – that is, the buyer pays, and then receives the shipping documents. But as this mainly covers the financing of the goods in transit, “documents against acceptance” (DA) is more common. Here, the bank has to hand over the shipping documents to the buyer before he receives the payment. The bank receives a draft from the buyer committing to payment at maturity of the draft. There is, therefore, a risk of non-payment by the buyer (an example is given in the Banco Santander vs. Banque Paribas case using discounting deferred payment LC).

To mitigate this risk, banks generally take out export credit insurance (which, however, generally only covers up to 90% of eventual losses), or can discount the bills without recourse (e.g., on the forfaiting market).

How can an exporter receive post-shipment finance if he sells his goods on consignment?

Commodities such as fruits and vegetables are often sold under consignment – implying that they will only be sold once they have arrived at destination. However, exporters can still obtain bank financing for the commodity during international transport and storage in the destination country. They will let the bank handle the shipping documents after shipment, and then, in order to be able to take delivery at destination, sign Trust Receipts or undertakings with the bank in which they commit themselves to deliver the sales proceeds to the bank by a specified time.

document against payment - the exporter will release the documents only if the importer makes immediate payment; also known as sight draft or accept the draft.

document against acceptance - the exporter will release the documents only if the importer accept the accompanying draft, thereby taking the obligation to pay over a designated period of time, i.e. 30 days or 90 days; also known as term draft.

26

In SUMMARY, Pre- and Post- shipment Finance Compared

Pre-shipment FinancePre-shipment FinanceFinance is disbursed prior to shipment to enable collection of materials for export.

Involves both performance and payment risk of the exporter and buyer respectively.

Source of repayment is proceeds of the contract.

Relatively a higher risk with higher costs.

Post-shipment FinancePost-shipment FinanceFinance is disbursed after shipment to keep exporter in funds pending payment by buyers.

Involves mainly payment risk of the buyer

Repayment comes from proceeds of exports

Risk is lower, especially if buyer is well known, hence financing cost is lower.

27

Integrating pre- and post-shipment finance Some forms of finance can be used both for pre-shipment and for post-shipment finance. Banker’s Acceptances are an example – while they are mostly used for post-shipment finance (allowing a company active in international trade to refinance its export receivables or the goods it has received from imports), it can also be used to finance goods in a warehouse awaiting shipment.

Banks often accept to roll pre-shipment finance into post-shipment finance on presentation of the proper shipping documents. But there are other ways to link the two.

For example, warehouse receipt finance is based on the security of goods in stock, whether in the importing or exporting country. If export- and import-warehouses are linked through a door-to-door letter of credit and the transporter provides appropriate guarantees, than a warehouse receipt financing structure can integrate both the pre- and the post-shipment phase.

Various structured finance tools link imports and exports. This is explicitly so for countertrade, but also applies to many forms of structured finance which lend against a client’s “borrowing base” – a discounted sum of its account receivables, due from overseas buyers, and the goods in stock awaiting shipment.

Furthermore, not only banks can provide trade finance. Securitization permits access to the market of institutional investors – most easily for post-shipment finance (refinancing a portfolio of export receivables), but use for financing domestic crops and for pre-shipment finance is also possible.

Click here foran explanationand examplesof the use of

Banker’s Acceptances

Click here foran example of

using trade paperfor grain financing

in Zimbabwe

28

Using trade paper to finance domestic grain trade:the case of Zimbabwe

Until political problems caused the collapse of its agricultural sector, Zimbabwe was a large cereals producer (primarily growing maize), able to export in many years. Although grain trade continues being in the hands of a government entity (the Grain Marketing Board, GMB), trade has been financed, since the 1980s, by the private sector. The mechanism used is the issuance of trade bills: several times a year, the GMB issues trade bills, which are tendered to the highest bidders (in the 1980s, the trade bills, with a bank aval, were also discounted in the international market for Bankers’ Acceptances, but the declining international reputation of Zimbabwe has put a stop to this).

GMB Agent bank Investors

Government

Guarantee

Trade billsTender of trade bills

Secondary trade

The basic mechanism for issuing the bills is as follows:

29

GMB Agent bank Investors

Government

Guarantee

Trade billsTender of trade bills

Secondary trade

Zimbabwe’s grain bills

After 180 days, bills are claimed at face value

After 180 days, bills are claimed at face value

The bills are issued by the GMB 3-4 times a year, in tranches of 4 to 5 billion Z$ (70-90 million US$, at the official exchange rate of late 2001, and 13-16 million US$ at the parallel market rate). The government provides a guarantee (which has never been called upon). Agent banks are selected each year, in principle through a tendering process – banks generally form syndicates to bid on the tender. The winning agent banks are then responsible for placing the trade bills with investors, including other banks, pension funds and other institutional investors, and individual investors (the bills are tendered with a face value of 1 million Z$, less than 2,000 US$ at the official rate). The bills are placed with the best bidders in the tender – there are no private placements – and are then actively traded on the secondary market. Demand for the trade bills is normally very strong.

30

Zimbabwe’s grain bills

GMB Agent bank Investors

Government

Guarantee

Trade billsTender of trade bills

Secondary trade

Farmers

Traders

Z$

Z$grain

grain

After 180 days, bills are claimed at face value

After 180 days, bills are claimed at face value

The GMB uses the proceeds from the bills to buy grain from farmers. The 180-day maturity of the bills is meant to coincide with the average time it takes GMB to sell these cereals and obtain the proceeds from these sales, on the domestic or export market.

The effective interest rate on the issues is close to treasury bill rates, and far below banks’ prime rates. The bills are not collateralized – in the late 1980s, warehouse receipts and inspection services were used to ensure the proper use of the funds, but after several years, financiers had built up sufficient trust in the system to do without. It remains to be seen what will be the effects of the GMB’s problems in 2001.

At the bills’ maturity, those holding them claim the face value with the agent bank, which in turn claims the bills with the GMB.

31

V. Sources of Trade Finance

Traders (importers and exporters) have over the years relied on banks to provide them with short or medium term finance for their operations. Often times though, when banks are not able to support them due to portfolio or other constraints, there are other sources of finance available. These other sources are becoming more prominent in recent times due to the use of modern financing techniques in trade financing which enhances the risk quality of loans, thus enabling them meet the risk appetite of many financiers. The various sources of trade finance are discussed in the following slides.

32

Suppliers`credit

Banks

Buyers’ Credit

Multilateralfinancial

institutions

Governments

Investmentmanagementcompanies

Export CreditAgencies

33

A supplier may grant a buyer credit for items supplied. This is possible especially in circumstances where both parties have had satisfactory transactions over a reasonable period and developed some form of mutual trust. Such arrangement, apart from lifting the buyer from the financial limitations, provide the seller with opportunity to keep his productive capacity engaged optimally.

1.1. Suppliers' CreditSuppliers' Credit1.1. Suppliers' CreditSuppliers' Credit

34

Much of trade finance comes from the banks either in the form of direct advances to the traders or through issuing and/or advising of L/Cs especially when they are not cash collateralized. Banks may also discount bills or drafts held by suppliers, thus providing them with funding prior to maturity of their instruments.

Banks have to provision against their loans - that is to say, they have to keep a certain percentage of their loan portfolio in safe assets which may, however, pay little or no interest rates (e.g., deposits with the Central Bank). Under the Basel agreement, banks now have to provision 8 percent of their outstanding loan portfolio. Under the new Basel 2 agreement, which will become operational in 2005, provisioning rules will be more tailored to the riskiness of individual loans. Banks may then have to provision as much as 50 percent of their loans to non-investment grade countries. This implies, of course, that the interest rates they need to charge on such loans will increase strongly - unless if they find ways to mitigate the risks.

2.2. Banks (local and international)Banks (local and international)2.2. Banks (local and international)Banks (local and international)

35

It is not unusual for traders to request their customers to make deposits for goods deliverable at future dates. This is mostly for items scarce in supply or those supplied by monopolies. Such deposits made by customers enable the trader meet urgent working capital needs.

A buyer may also grant direct advance to an exporter to enable him obtain materials for processing and export for his favor. Such arrangement is operated under a prepayment arrangement and may involve a lender providing funds to an exporter on the buyer’s behalf. The funds enable the exporter to gather stocks for processing and export to the buyer, who then makes direct payment to the lender up to the limit of the loan and associated interest charges. While the facility is in place, the lender takes a charge over the stock at the exporter’s place.

3.3. Buyer's CreditBuyer's Credit3.3. Buyer's CreditBuyer's Credit

36

Export Credit Agencies (ECAs) are also very instrumental to credit availability since they provide necessary guarantees and bonds that enable financiers to make funds available for trade. The role of ECAs are much more relevant in the developing economies where unstable governments tend to erode the confidence of lenders to expose themselves to such markets. Export credit guarantees do not involve the actual provision of funds to exporters but are instruments offered by government agencies to safeguard export-financing banks against losses resulting from the export transactions they finance. In this way they facilitate exporters' access to credit and are thus powerful incentives for exporting. By providing guarantees, ECAs encourage local exporters to venture into difficult environments with the hope that if payment defaults arise, they would not lose money. ECAs are owned by governments who use them as instruments to encourage exports and hence boosting local productive capacities. Notable ECAs include the US - based Overseas Private Investment Corporation (OPIC) and Multilateral Investment Guarantee Agency (MIGA), and also Export Credit Guarantee Department (ECGD) of the United Kingdom, and COFACE of France.

4.4. Export Credit AgenciesExport Credit Agencies4.4. Export Credit AgenciesExport Credit Agencies

37

4.4. Export Credit Agencies (cont'd)Export Credit Agencies (cont'd)4.4. Export Credit Agencies (cont'd)Export Credit Agencies (cont'd)

The OECD provides links to all the export credit agencies of OECD countries.

Export credit insurance : A policy to cover one of the riskier areas faced by exporters i.e. the non payment either due to insolvency of the importer (commercial risk) or political events (political risk). Export credit insurance is frequently mentioned in connection with export credit guarantees. However, while guarantees cover bank export loans, insurance policies are issued in favour of exporters. In many developing countries, this type of insurance is not available or too expensive. Several types of export credit insurance are available; they differ from country to country according to the needs of the business community.

38

The most widely used types of export credit insurance are the following:

Short-term export credit insurance : Generally covers periods not exceeding 180 days. Pre-shipment and post-shipment export stages are covered, and protection can be provided against political and commercial risks. Medium- and long-term export credit insurance : This type of insurance is issued for credits extending for long periods - up to three years (medium-term) or longer. It provides cover for financing exports of capital goods and services or construction costs in foreign countries. Investment insurance : Under this type of policy, insurance is offered to exporters investing in foreign countries. The Multilateral Investment Guarantee Agency (MIGA), affiliated to the World Bank, offers this type of insurance. External trade insurance : This type of credit insurance applies to goods not shipped from the originating country and is not available in many developing countries. Exchange risk insurance : This type of insurance covers losses arising from the fluctuation in the respective exchange rates of the importer's and exporter's national currencies over a determined period of time.

4.4. Export Credit Agencies (cont'd)Export Credit Agencies (cont'd)4.4. Export Credit Agencies (cont'd)Export Credit Agencies (cont'd)

39

Multilateral financial institutions also play a major role financing trade especially where such financing advances their mandates of poverty alleviation and common good of the people. The world bank world balance of payments support facilities provide the necessary financing window for many countries thereby enabling trading activities between such countries and the rest of the world.

5.5. Multilateral Financial InstitutionsMultilateral Financial Institutions5.5. Multilateral Financial InstitutionsMultilateral Financial Institutions

40

Government involvement in trade sometimes go further than providing the enabling environment for trade to outright advances for import purposes especially where such imports are export generative in nature. In some other instances, imports of essential items such as food and medicines receive direct government support in the form of advances and/or guarantees.

6.6. Governments Governments6.6. Governments Governments

41

Certain institutions managing portfolios of varying sizes and tenor occasionally inject some funds into the trade finance market. Such institutions like insurance companies and pension fund managers take advantage of instruments like commercial papers to earn quick yields.

Under the Basel agreement, Banks are faced with increasingly stringent rules on lending to “risky” countries and clients. In contrast, institutional investors are not limited by any rules on provisioning, or unduly restrained by country credit lines. It is therefore likely that the role of investors in trade finance will increase.

7.7. Investment Management CompaniesInvestment Management Companies7.7. Investment Management CompaniesInvestment Management Companies

42

Syndication is a process involving the coming together of various banks and/or other financiers for the purpose of providing finance to a single entity. It is also known as club deal. In this arrangement, the leader of the team (the Arranger) divides the entire facility sum into bits (tickets) and stratifies them in descending order for the purpose of apportioning fees due to participants in the transaction. Participants in descending order may include all or some of lead arrangers, senior co-arrangers, co-arrangers, senior lead managers, lead managers and managers. Fees paid to these members of the syndicate vary according to their respective tickets.

Club deals have become increasingly important in present day financing, enabling the banks to share in risks across continents. The arranging bank in most instances is the facility agents with the responsibility to manage the reimbursement from the borrower and then to the funding participants. The members of the syndicate are bound by an agreement (participation agreement).

VI. Loan Syndication

43

Types of Syndication

Syndication could be under disclosure or non-disclosure basis

Disclosure: In this arrangement the identity of all the participants are disclosed to the borrower while the participants also know the full terms and conditions of the facility. This arrangement is preferred by banks because it has some promotional appeal.

Non-Disclosure: In this arrangement, the identity of participants are not made known to the borrower. The participants in this case sign a sub-participation agreement.

44

Advantages of Syndication

It enables the creation of a sizeable pool of funds within a short time.

It helps in the sharing of risks and moreover, it makes room for both big and small banks to share in the same mandate through the availability of tickets of various sizes.

It enables banks with relatively poor structuring capabilities to study those of the transactions they are participating in and learn therefrom.

Syndication make for constant interaction between and among bankers and therefore aids in information flow on events in the market place.

Syndication encourage the distribution of wealth since it enables developed country banks to participate in funding developing country entities.

It can bring down pricing. This is very true for mandates that have over a long time or those that are over subscribed. The borrower may cash in on his strength to negotiate for better pricing; e.g. Ghana Cocobod syndication whose margin has gone down by over 50bp since its debut.

45

Click for some Examples on simple trade financing and

more structured trade finance mechanisms

Exporter/Seller(Country X)

EXAMPLE I:EXAMPLE I: Short-term Pre-shipment Financing (L/C-Based)

1. Purpose: Financing to start production for US$50 million worth contracts signed.

2. Exporter: A credit worthy company in country X.

3. Importer: Various credit-worthy buyers in safe country.

4. Lender: XYZ Bank.

5. Amount to be financed: 85% of the signed contracts value (i.e. US$ 42.5 million).

6. Tenor: 6 months, representing shipment period.

7. Documentation: - Confirmed copies of the L/Cs;- Assignment of proceeds by the exporter to the

bank;- Notification of assignment proceeds by the

exporter to the issuing bank as well as advising bank;

- Acknowledgment of assignment by the issuing bank.

L/C Opening BankAdvising/

Negotiating Bank

XYZ Bank

Request to open a sight L/C

Acknowledgement of assignment

Assignment of L/Cs proceeds

Pre-shipment financing

Sales Contract

Notification of Assignment of

Proceeds

Issuing Sight L/C

Notification of Assignment of Proceeds

Buyers

This is a simple pre-finance transaction where an L/C is issued from a reliable bank in a safe country and the tenor of the finance is limited to the shipment period only. The proceeds of the L/C are assigned to the financing bank.

Advising of Sight L/C Proceeds

This is a simple medium-term, pre-shipment finance transaction where the borrower (the exporter) issues P-notes to the lending bank and payment is done automatically to the bank from the importer through the escrow account. No country nor business risk implication.

Seller (Country X)

XYZ Bank

Sales Contract

BuyerLetter of Notification

Letter of Acknowledgment

Letter of Assignment of Rights and Benefits

Issuing P-note and Loan Agreement

Pre-shipment financing

EXAMPLE II: EXAMPLE II: Medium-term Pre-shipment Financing with no Bank Guarantee (Contract-Based)

1. Purpose: To secure short-term financing at a lower cost than the in local market. (The total amount of contract is approximately US$60 million signed to be delivered over 5 years)

2. Exporter: A credit worthy company in country X.

3. Importer: A well-known company.

4. Lender: XYZ Bank.

5. Amount to be financed: US$7.5 million, repayable in 6 half-yearly installments (final maturity of three years).

6. Tenor: 3 years.

7. Documentation: - Promissory notes issued by the exporter for US$7.5

million (P-Note is a financing instrument that states the terms of the underlying obligation, is signed by its maker and is negotiable/transferable to a third party);

- Confirmed copies of the Contract stipulating: i) quantity ii) quality iii) delivery schedule, and iv) take-or pay provision (a contractual term whereby the buyer is unconditionally obligated to take any product or service that he is offered - and pay the corresponding purchase price-, or to pay a specified amount if he refuses to take the product or service);

- Letter of Assignment of rights and benefits by exporter to bank;

- Letter of Acknowledgment by importer to bank, confirming that any payment of goods received under this contract can only be affected to the escrow account maintained by exporter with bank;

- Charge over bank account;- Legal opinion from the exporting country.

Exporter/ Company A(Country X)

EXAMPLE III:EXAMPLE III: Construction financing for overseas plants in combination with an ECA

1. Purpose: 100% finance for a project in country Y.

2. Exporter: Company A in country X.

3. Importer: Company B in country Y.

4. Lender: XYZ Bank.

5. Amount to be financed: 100% of the total finance, i.e. US$ 42 million.

6. Construction period: Over 2 years.

7. Repayment terms: In 4 half-yearly installments starting 2 years after the signing of the loan agreement (i.e, 2 year grace and a total of 4 years the final maturity).

8. Documentation: Two separate loans agreements and guarantees; one for ECA and one for the forfaitor.

GovernmentCountry Y

ECA

XYZ Bank

Providing a guarantee for the whole projectProviding a guarantee

for the construction Material

Loan Agreement for the portion not covered by ECA

Financing

Sales ContractImporter/

Company B(Country Y)

This example represents two separate financing agreements one with ECA and one with government.

Request of Guarantee

Financing

Exporter

EXAMPLE IV:EXAMPLE IV: Account Receivable-Based Financing

1. Underlying transaction: To trade naphtha and crude oil.

2. Lender: XYZ Bank.

3. Facility Amount: US$ 50 million for credit facility.

4. Exporter: Major oil company in Kuwait.

5. Trader: Korea trading company in Singapore.

6. Importers: Major oil refineries worldwide.

7. Tenor: 30-90 days from B/L date.

8. Collateral: Outstanding account receivables.

9. Facility Period: 1 year.

10. Each transaction amount: Over US$5 million.

Trader(Singapore)

XYZ Bank

Sales/Purchase Contract

Payment after 30-90 days from

B/L date

Letter of Undertaking (remedial procedures in case of non-performance)

Shipment Buyers (Oil Refineries)

This financing is given to the exporter once goods are shipped and repayment is done automatically by importer through an escrow account.

Letter of Acknowledgment

Sales/Purchase Contract

Payment at shipment

Aluminum Billet Producer/

Borrower (Korea)

EXAMPLE V:EXAMPLE V: Structured Commodity Financing

1. Underlying transaction: Aluminum billet.

2. Lender: XYZ Bank

3. Borrower/Exporter: Aluminum billet producer, Korea.

4. Trader: Non-ferrous metal trader.

5. Tenor: 60 days.

6. Security: • 100% performance guarantee by the

borrower.• Assignment of receivables• Payment into Escrow account

Bank XYZ / Escrow account

Raw material supplier

Non-Ferrous Metal Trader

Structured finance mechanism through which the supplier is paid from the bank for the raw material sold to the exporter and repayment is made automatically by the importer to the bank through an escrow account

2. Loan($)

3. Aluminum Ingot

4. Aluminum Billet

1. Performance Guarantee

5. Payment

Related Documents