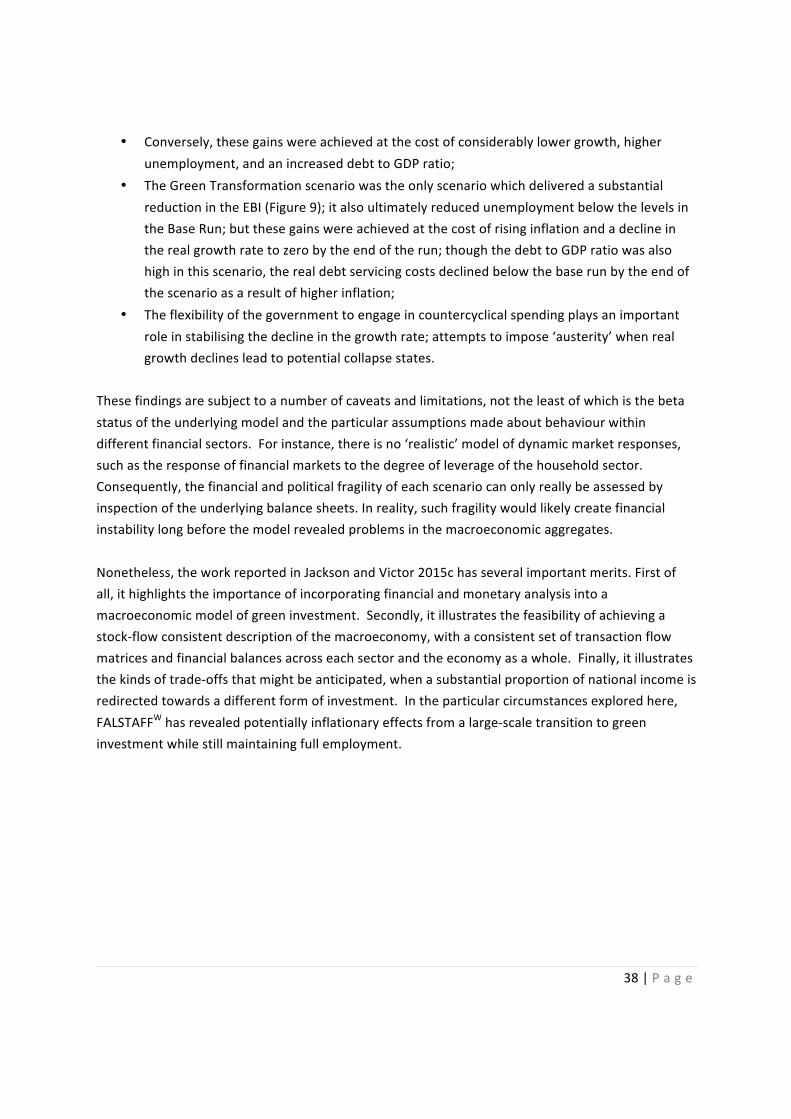

PASSAGE Working Paper Series 15-02 ISSN: 2056-6255 Tim Jackson, Peter Victor and Ali Asjad Naqvi Towards a Stock-Flow Consistent Ecological Macroeconomics For further information on the research programme and the PASSAGE working paper series, please visit the PASSAGE website: www.prosperitas.org.uk

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

PASSAGE Working Paper Series

15-02

ISSN: 2056-6255

Tim Jackson, Peter Victor and Ali Asjad Naqvi

Towards a Stock-Flow Consistent Ecological Macroeconomics

For further information on the research programme and the PASSAGE working paper series, please visit the PASSAGE website: www.prosperitas.org.uk

Prosperity and Sustainability in the Green Economy (PASSAGE) is a Professorial Fellowship held by Prof Tim Jackson at the University of Surrey and funded by the Economic and Social Research Council (Grant no: ES/J023329/1).

The overall aim of PASSAGE is to explore the relationship between prosperity and sustainability and to promote and develop research on the green economy.

The research aims of the fellowship are directed towards three principal tasks:1) Foundations for sustainable living: to synthesise findings from a decade of research on sustainable consumption and sustainable living;2) Ecological Macroeconomics: to develop a new programme of work around the macroeconomics of the transition to a green economy.3) Transforming Finance; to work with a variety of partners to develop a financial system fit for purpose to deliver sustainable investment.

During the course of the fellowship, Prof Jackson and the team will engage closely with stakeholders across government, civil society, business, the media and academia in debates about the green economy.PASSAGE also seeks to build capacity in new economic thinking by providing a new focus of attention on ecological macroeconomics for postgraduates and young research fellows.

© Tim Jackson, 2015The views expressed in this document are those of the authors and not of the ESRC or the University of Surrey. Reasonable efforts have been made to publish reliable data and information, but the authors and the publisher cannot assume responsibility for the validity of all materials. This publication and its contents may be reproduced as long as the reference source is cited.

PublicationJackson, T., Victor, P. and A. Asjad Naqvi. Towards a Stock-Flow Consistent Ecological Macroeconomics. PASSAGE Working Paper 15/02. Guildford: University of Surrey. Online at: www.prosperitas.org.uk/publications.html

Contact details: Tim Jackson, Centre for Environmental Strategy (D3), University of Surrey, Guildford, GU2 7XH, UKEmail: [email protected]

AcknowledgementsThe financial support of the Economic and Social Research Council for the PASSAGE programme (ESRC grant no: ES/J023329/1) is gratefully acknowledged.

|P a g e

1

Abstract

Modernwesterneconomies(intheEurozoneandelsewhere)faceanumberofchallengesoverthecomingdecades.Achievingfullemployment,meetingclimatechangeandotherkeyenvironmentaltargets,andreducinginequalityrankamongstthehighestofthese.Theconventionalroutetoachievingthesegoalshasbeentopursueeconomicgrowth.Butthisroutehascreatedtwocriticalproblemsformoderneconomies.Thefirstisthathighergrowthleads(ceterisparabis)tohigherenvironmentalimpact.Thesecondisthatfragilityinfinancialbalanceshasaccompaniedrelentlessdemandexpansion.

Theprevailingglobalresponsetothefirstproblemhasbeentoencourageadecouplingofoutputfromimpactsbyinvestingingreentechnologies(greengrowth).Butthisresponserunstheriskofexacerbatingproblemsassociatedwiththeover-leveragingofhouseholds,firmsandgovernmentsandplacesundueconfidenceinunprovenandimaginedtechnologies.Analternativeapproachistoreducethepaceofgrowthandtorestructureeconomiesaroundgreenservices(post-growth).Butthepotentialdangersofdeclininggrowthrateslieinincreasedinequalityandinrisingunemployment.Somemorefundamentalargumentshavealsobeenmadeagainstthefeasibilityofinterest-bearingdebtwithinapost-growtheconomy.

Theworkdescribedinthispaperwasmotivatedbytheneedtoaddressthesefundamentaldilemmasandtoinformthedebatethathasemergedinrecentyearsabouttherelativemeritsofgreengrowthandpost-growthscenarios.InpursuitofthisaimwehavedevelopedasuiteofmacroeconomicmodelsbasedonthemethodologyofPost-KeynesianStockFlowConsistent(SFC)systemdynamics.Takentogetherthesemodelsrepresentthefirststepsinconstructinganewmacroeconomicsynthesiscapableofexploringtheeconomicandfinancialdimensionsofaneconomyconfrontingresourceorenvironmentalconstraints.SuchanecologicalmacroeconomicsincludesanaccountofbasicmacroeconomicvariablessuchastheGDP,consumption,investment,saving,publicspending,employment,andproductivity.Italsoaccountsfortheperformanceoftheeconomyintermsoffinancialbalances,netlendingpositions,moneysupply,distributionalequityandfinancialstability.

Thisreportillustratestheutilityofthisnewapproachthroughanumberofspecificanalysesandscenarioexplorations.TheseincludeanassessmentofthePikettyhypothesis(thatslowgrowthincreasesinequality),ananalysisofthe‘growthimperative’hypothesis(thatinterestbearingdebtrequireseconomicgrowthforstability),andananalysisofthefinancialandmonetaryimplicationsofgreeninvestmentpolicies.Theworkalsoassessesthescopeforfiscalpolicytoimprovesocialandenvironmentaloutcomes.

|P a g e

2

1 Introduction

TheWWWforEuropeprojectisalarge-scalecollaborativeprojectwithacommoninterestinthesocio-economictransitiontosustainability.TheoverallobjectiveofWorkPackage205istodevelopmodelstosupportaquantitativeunderstandingofthesocio-economictransitiontowardssustainability.

Milestone38(Jacksonetal2014)outlinedthedevelopmentoftwoseparatestrandsofmodellingwork,oneusingaDynamicStochasticGeneralEquilibrium(DSGE)approachandtheotherusingaStock-FlowConsistent(SFC)systemdynamicsapproach.Milestone39(Kratenaetal2015)reportsonthefindingsfromthefirstapproach.TheaimofMilestone40istoreportontheoutcomesfromtheSFCmodellingstrand.

Section2ofthereportelaboratesonthemotivationforthemodellingapproach.Itsetsoutthechallengesassociatedwithmodellingthetransitiontosustainabilityandarticulatestheneedforan‘ecologicalmacroeconomics’.

Section3describesthebroadprinciplesofSFCmodelling,drawingonthepioneeringworkofWynneGodleyandhiscollaborators.ThoughincreasinglyemployedwithinthePost-Keynesianeconomicparadigm,SFCmodellingisnotparticularlywell-knownbeyondthatfieldandhasonlyrecentlybeguntobeusedtomodelsocialorecologicalaspectsoftheeconomy.Thismilestoneaimstodemonstratethevalueoftheapproachinunderstandingthetransitiontoasustainableeconomy.

Sections4to7describefourdistinctmodellingexercisesundertakenbytheauthorsofthisreportusinganSFCframework.Thefirstoftheseexplorestheso-called‘Pikettyhypothesis’thatdeclininggrowthratesleadtorisinginequality.Thesecondexaminesthequestionwhetherornottheexistenceofinterest-bearingdebtnecessarilycreatesa‘growthimperative’.Thethirdmodelexploresthefinancialandmonetaryimplicationsofalarge-scalegreeninvestmentprogramme.Thefourthmodeldevelopsthecombinedchallengeofsubstitutingforfossilfuelsinthecontextofsocialandeconomicgoals.

Section8summarisesthefindingsfromtheoverallworkprogrammeanddiscussestheimplicationsfordebatesaboutgreengrowthandpost-growtheconomies.

|P a g e

3

2 MotivatingaStock-FlowConsistentEcologicalMacroeconomics

OneoftheclearestlessonsfromthefinancialcrisisisthatanarrowfocusonrealeconomyindicatorsandpolicieswasinsufficienttoavertthepotentiallydisastrousconsequencestriggeredbyweaknessesintheUShousingmarket,theproliferationoffinancialderivatives,andthesubsequentcollapseofLehmanbrothersinSeptember2008.Thefragilityinstilledwithinthefinancialsystemasaresultofover-heatedassetmarkets,over-leveragedbalancesheets,andover-complexfinancialinstrumentswentlargelyunnoticedinapolicyenvironmentfocusedprimarilyonaggregateindicatorssuchastheGDP,employmentrates,inflationandconsumerspending.Thefailureofalmostallmainstreameconomiststoforeseetheglobalfinancialcrisisof2008/9representsaremarkablefailureoffinancialgovernance(Bezemer2010).JustayearbeforetheonsetofthegreatrecessionthethenchairmanoftheU.S.FederalReserveBenBernankereportedtotheU.S.HouseofRepresentatives(Bernanke,2007)that‘theU.S.economyappearslikelytoexpandatamoderatepaceoverthesecondhalfof2007,withgrowththenstrengtheningabitin2008toarateclosetotheeconomy'sunderlyingtrend.’Globalfinancialinstitutionswerealsotakenunawares.InAugust2007,theIMFwasabletoarguethat‘notwithstandingrecentfinancialmarketnervousness,theglobaleconomyremainsontrackforcontinuedrobustgrowthin2007and2008,althoughatasomewhatmoremoderatepacethan2006.Moreover,downsideriskstotheeconomicoutlookseemlessthreateningthanatthetimeoftheSeptember2006WorldEconomicOutlook.’(IMF,2007).Theseoversightsamounttoasystematicfailuretointegrateacoherentdescriptionofthefinancialeconomyintomodelsandpolicyprescriptionsfortherealeconomy(Keen2011).Thecrisisrevealedpainfullythattheapparenteconomicsuccessofthe‘greatmoderation’waslargelybuiltonagrowingfragilityinthebalancesheetsoffirms,householdsandnationstates(BarwellandBurrows2011,Koo2011).Buttheserisksremainedinvisibletomosteconomistsandunpredictedbythemajorityofeconomicmodels.Inthewakeofthecrisis,economistshavethereforeplacedarenewedimportanceonthetaskofunderstandingthebehaviour(andinparticularthestabilityorinstability)ofthefinancialeconomyandintegratingthisunderstandingintotheworkingsoftherealeconomy.Ahostofnewresearchinitiativesandthere-emergenceofsomeearlierschoolsofthoughtbearswitnesstothisnewturnineconomics(Keen2011,Minsky1994,Turner2013,Wray2012).Anothernotableshortcomingoftraditionaleconomicmodelsisthefailuretoaccountproperlyforthestocksandflowsofnaturalresourcesonwhicheconomicactivityultimatelydepends.Theperiodofthegreatmoderationalsowitnessedaprogressivedeclineinenvironmentalqualityacrosstheworld:inparticular,inrelationtoglobalclimatechange,biodiversityloss,thedeforestationanddesertificationofsemi-aridregions,theeutrophicationofwatersuppliesandtheover-exploitationofmineralresources(MEA2005,MGI2013,Rockströmetal2009,Steffenetal2015,TEEB2010,IPCC2014,Wiedmannetal2013).Theselimitationsarewell-rehearsedintheliteraturefromecologicaleconomics(Daly1972,Meadowsetal1972,Costanza1989,Daly1996,Costanzaetal1997).Butattemptstoredressthemhavebeenpartialatbest.

|P a g e

4

Oneofthereasonsforthisisafundamentaldilemmawhichhauntsdebatesaboutasustainableeconomy.Conventionalformulationsforachievingprosperityrelyonacontinualexpansionofconsumerdemand.Moreisdeemedbetterinthereceivedwisdom,evenwhenthewellbeingoutcomesfromincreasinglymateriallivesaretenuous.Butexpandingconsumerdemandincreasestheglobalthroughputofmaterialsandtheconsumptionoffossilfuelsandthreatensthesustainabilityoftheecosystemsonwhichprosperitydepends.Continuedgrowthofthekindseenhithertoispatentlyunsustainable.Ontheotherhand,slowingdown,orreversingeconomicgrowthappearsunpalatabletoo.Incomegrowthisclearlystillneededinthepoorestcountriesatleast,whereitishighlycorrelatedwithrealwellbeingoutcomes.Evenintherichesteconomies,growthinGDPisoftenregardedasthesinglemostimportantpolicyindicatorofprogress.Whengrowthfalters,asitdidinthecrisisof2008/9incomesfall,high-streetspendingisreducedandproductionoutputfalls.Businesseshavelesstoinvest,governmentshavelowertaxrevenues,socialinvestmentiswithdrawn,peoplelosetheirjobsandtheeconomybeginstofallintoaspiralofrecession.Inshort,growthmaybeunsustainable,butde-growthappearstobeunstable.Respondingtothedilemmaofremainingwithinthe‘safeoperatingspace’(Rockström2009,Steffenetal2015)ofafiniteplanetinagrowth-basedeconomyhasoftenbeenconstruedbyeconomistsprimarilyasamicroeconomictask—onethatgovernmentscanaddresswithconventionalfiscalinstrumentsoftaxandsubsidy.The‘external’costsassociatedwitheconomicactivitiesshouldbe‘internalized’inmarketprices,accordingtofamiliaraxioms(Pigou1920,Pearceetal1989,PearceandTurner1990,Ekins1992).Incorporating‘shadowprices’forenvironmentalgoodsintomarketpriceswillsendaclearsignaltoconsumersandinvestorsabouttherealcostsofresourceconsumptionandecologicaldamage,andincentivizeinvestmentinalternatives,accordingtothisconventionalwisdom.Butthisprescriptionhasbeenhardtoimplementoverthelastdecades.Fearsofdamagingeconomicgrowthhaveledpoliticianstoshyawayfrombothecologicaltaxationandgreeninvestment.Recentattemptstoovercomethisfearhavelargelyfocusedonarguingthattheimpactsofgreeninvestmentwillbeeithernegligibleorevenpositiveintermsofstimulatinggrowth(NCE2014).Butitremainsanuncomfortablefactthatfragileprivateandpublicsectorbalancesheetshavesloweddowninvestmentintherealeconomygenerally,letalonetheadditional(andlessfamiliar)investmentneededtomakeatransitiontoasustainableeconomy.Conventionalresponseshavefocussedinsteadoncuttingpublicspending(austerity)andstimulatingconsumptiongrowth(consumerspending)asthebasisforeconomicrecovery.Unfortunately,theseresponsestendtoignorethestructuralproblemsoftheconventionalparadigmanddelayfurthertheinvestmentneededtomakethetransitiontoasustainablegreeneconomy.Thistransitiondemandsaquitespecificinvestmentportfoliowhichisquantitativelyandqualitativelydifferentfromtheinvestmentportfoliothathascharacterisedtheprevailingeconomicsystem.Existinginvestmentpracticestendtobedominatedbyspeculationonassetpricesontheonehandandbytheextractionanddepletionofnaturalresourcesontheother.Easyreturnsinthefirst

|P a g e 5

categoryaregainedatthecostofunstableassetpricesandrisinginequality(CreditSuisse2014,nef2015).Easyreturnsinthesecondareachievedonlyattheexpenseofresourcedepletionandenvironmentaldegradation(UNEP2014).Astheseeasyreturnsbegintodissipate,thedominanceofextractiveinvestmentsleadstoportfoliosweakenedbystrandedassets(HSBC2012)withpotentiallydestabilisingeffectsonfuturefinancialmarkets.

Bycontrast,theinvestmentportfolioforasustainableeconomyconsistsinbuildinglong-termassetsinlowcarbontechnologyandinfrastructure,inresource-efficientmanufacturing,inserviceprovision,inhealthcare,ineducation,inpublicspacesandsocialgoods,andintheprotectionandrestorationofhabitats,forests,wetlands,soilsandothernaturalassets.Someoftheseassettypesmayofferveryconventionalbenefitswithratesofreturncomparabletoexistingportfolios.Othershoweverwillimposeconsiderablechallengesonexistinginstitutionalstructuresandfinancialarchitecturesbecausetheirveryrealenvironmentalandsocialbenefitsarenotreflectedinmarketpricesandfinancialreturns.

Thescaleandnatureofthisdilemmasuggestthatthecombinedchallengesofclimatechange,environmentalpressure,andresourcescarcityrequiremacroeconomicaswellasmicroeconomicresponses.Infact,thereisaneedtodevelopafullyconsistentecologicalmacroeconomicsinwhichitispossibletomaintainfinancialstability,ensurehighlevelsofemployment,improvethedistributionofincomeandwealthandyetremainwithintheecologicalconstraintsandresourcelimitsofafiniteplanet.

Inshort,itisclearthatanapproachtomacroeconomicsconfiguredonlyby‘realeconomy’aggregatessuchasoutput,productivity,employment,consumptionandpublicspending,isinsufficienttoensureeconomicsustainability,letalonesocialorenvironmentalsustainability.Norisitsufficientformonetarypolicytoconsistlargelyinlaissezfaireregulationoffinancialmarketscombinedwithcentralbankinterestratepolicyaimedsolelyat‘inflationtargeting’.Theseformsofmonetarypolicywereplainlydeficientinavertingthecrisisandinsufficienttoproviderecoveryfromit.Fortwodecadebeforethecrisis,thissamearchitecturesignallyfailedtoprovideafinanciallandscapeamenabletotheinvestmentneedsofanenvironmentallysustainableandsociallyequitableeconomy.Buildingamoreappropriatefinancialsystemneedstostartfromaclearunderstandingoftheinvestmentneedsassociatedwiththetransitiontosustainableeconomy.

Numerousquestionsemergeasaresultofthisanalysis.Theseincludequestions:abouttheorganisationandstructureofassetportfolios;aboutthebalancebetweenpublicandprivatefinance;aboutthebalancebetweenequityanddebt;aboutthestructureanddistributionofassetownership;abouttheimpactsofelevatedinvestmentsonprices,onwagesandonconsumerdemand;andabouttheappropriateformsofhorizontalandverticalmoney.Clearly,addressingthesequestionsdemandsattentiontoboththerealandthefinancialeconomy.Explicitly,italsorequiresaframeworkthatintegratesbothoftheseaspectsoftheeconomy–inthecontextofecologicalandresourceconstraints.Theaimofthispaperisdescribeseveralapproachestothisover-archingproblem,buildingonthetheoreticalframeworkofstock-flowconsistent(SFC)macroeconomicmodelling.

|P a g e

6

3 AStock-FlowConsistentSystemDynamicsFramework

TheintellectualfoundationforthemodellingworkreportedinthisMilestonederivefromaviewofmacroeconomicsdevelopedwithinpost-Keynesianeconomictheory.WedrawinparticularfromtheStock-FlowConsistent(SFC)approachtomacro-economics,pioneeredbyCopeland(1949)anddevelopedextensivelybyWynneGodleyandothersoverthelastdecades(GodleyandLavoie2007,LavoieandGodley2001,LavoieandZezza2012).2

TheoverallrationaleoftheSFCapproachistoaccountconsistentlyforallmonetaryflowsbetweenagentsandsectorsacrosstheeconomy.Thisrationalecanbecapturedinthreebroadaxioms:firstthateachexpenditurefromagivenactor(orsector)isalsotheincometoanotheractor(orsector);second,thateachsector’sfinancialassetscorrespondtofinancialliabilitiesofatleastoneothersector,withthesumofallassetsandliabilitiesacrossallsectorsequallingzero;andfinally,thatchangesinstocksoffinancialassetsareconsistentlyrelatedtoflowswithinandbetweeneconomicsectors.

Thesesimpleunderstandingsleadtoasetofaccountingprincipleswithimplicationsforactorsinboththerealandfinancialeconomywhichcanbeusedtotestanyeconomicmodelorscenariopredictionforconsistencyasapossiblesolutionintherealworld.Theapproachhascometotheforeinthewakeofthefinancialcrisis,preciselybecauseoftheseconsistentaccountingprinciplesandthetransparencytheybringtoanunderstandingnotjustofconventionalmacroeconomicaggregatesliketheGDPbutalsooftheunderlyingbalancesheets.ItisnotablethatGodley(1999)wasoneofthefeweconomistswhopredictedthecrisisbeforeithappened.

TheapproachisbroadlyKeynesianinthesensethatSFCmodelstendtobedemand-driven,andtheeconomyisarticulatedintermsofanumberofinter-relatedfinancialsectoraccounts:households,firms,banks,government,centralbankandthe‘restoftheworld’(orforeignsector).Theaccountsoffirmsandbanksareusuallyfurthersubdividedintocurrentandcapitalaccountsinlinewithnationalaccountingpractices.Itisalsosometimesusefultosubdivideindividualsectorsfurther.Forinstance,thehouseholdsectorcanbesubdividedintotwosectors(seeSection4below)inordertotestthedistributionalaspectsofchangesintherealorfinancialeconomy.

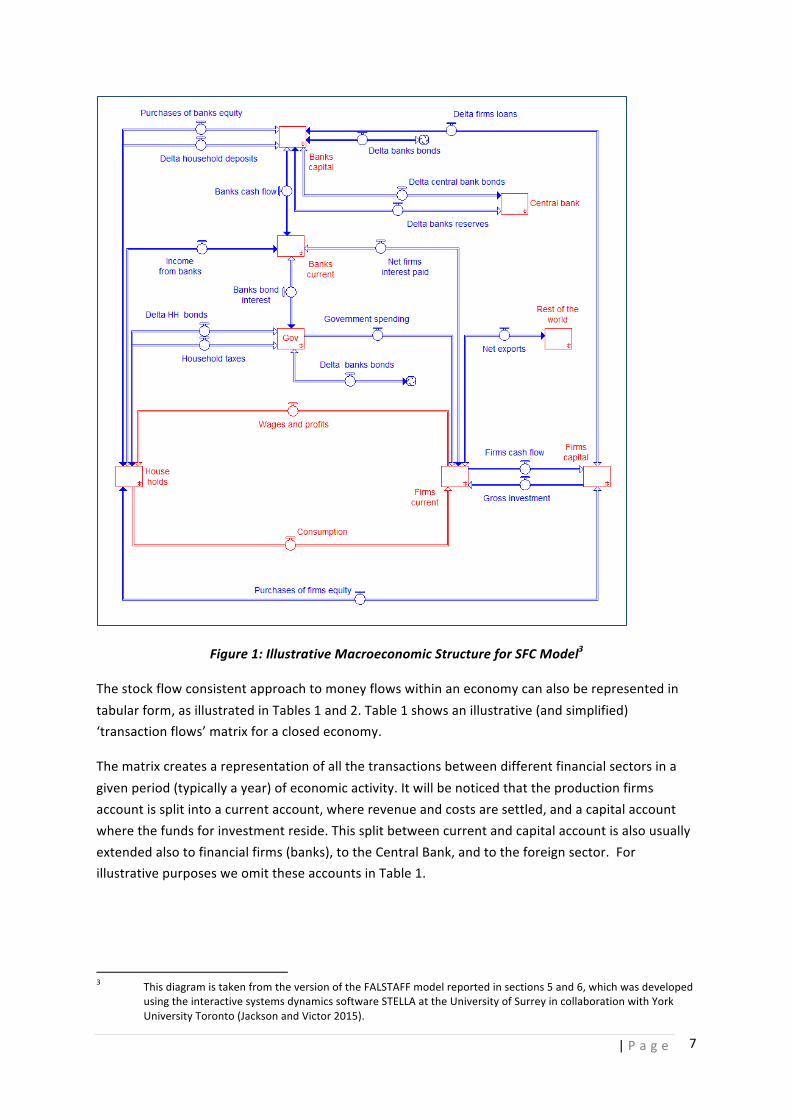

Figure1illustratesatypicalmodelstructureforanSFCmodelwiththefamiliar‘circularflow’oftheeconomyvisible(inred)towardsthebottomleftofthediagram.Therathermorecomplexstructureshown(partially)aboveandaroundthecircularflowrepresentsfinancialflowsofthemonetaryeconomyinthebanking,governmentandforeignsectors.

Ifthemodelisstock-flowconsistent,thefinancialflowsintoandoutofeachfinancialsectorconsistentlysumtozeroateachpointoftimealongthemodelrun.So,forinstance,theincomesofhouseholds(consistingofwagesandprofits)mustbeexactlyequaltotheoutgoingsofhouseholds(includingtaxes,netinterestpayments,consumptionandinvestmentspending,andnetacquisitionsoffinancialassets).Likewise,foreachothersectorinthemodel.

2 ForanoverviewoftheliteratureonSFCmacroeconomicmodelling,seeCaverzasiandGodin2015.

|P a g e 7

Figure1:IllustrativeMacroeconomicStructureforSFCModel3

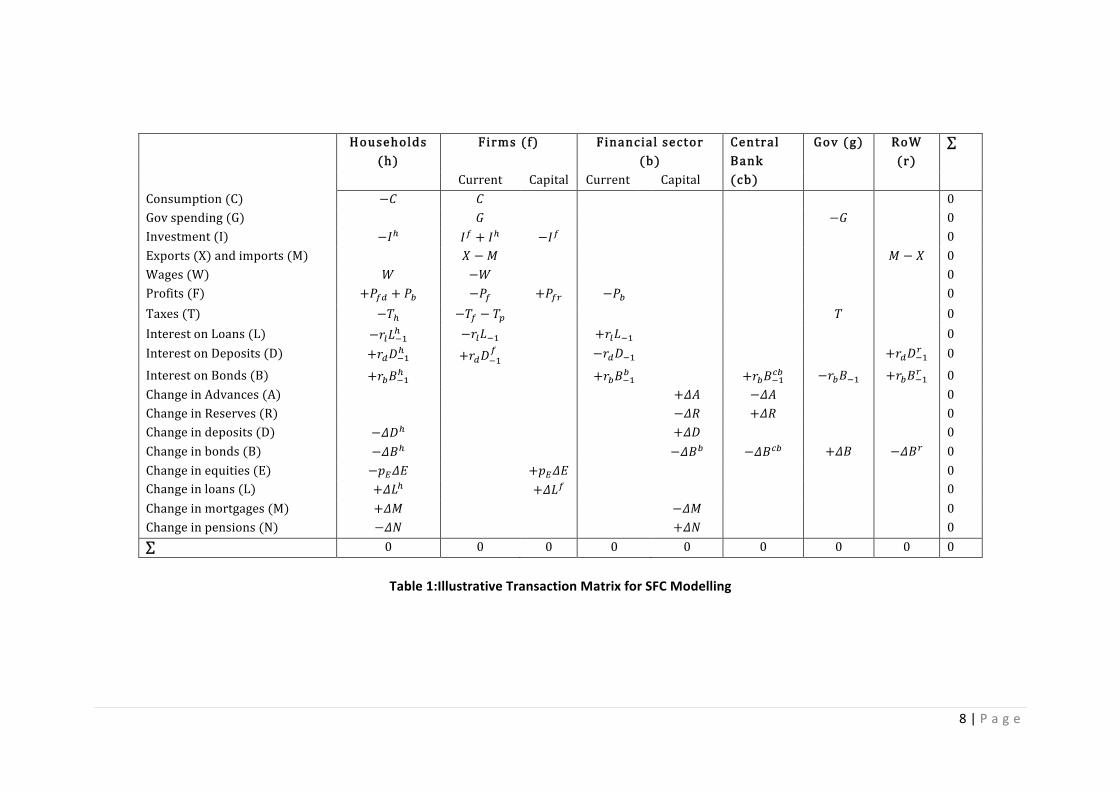

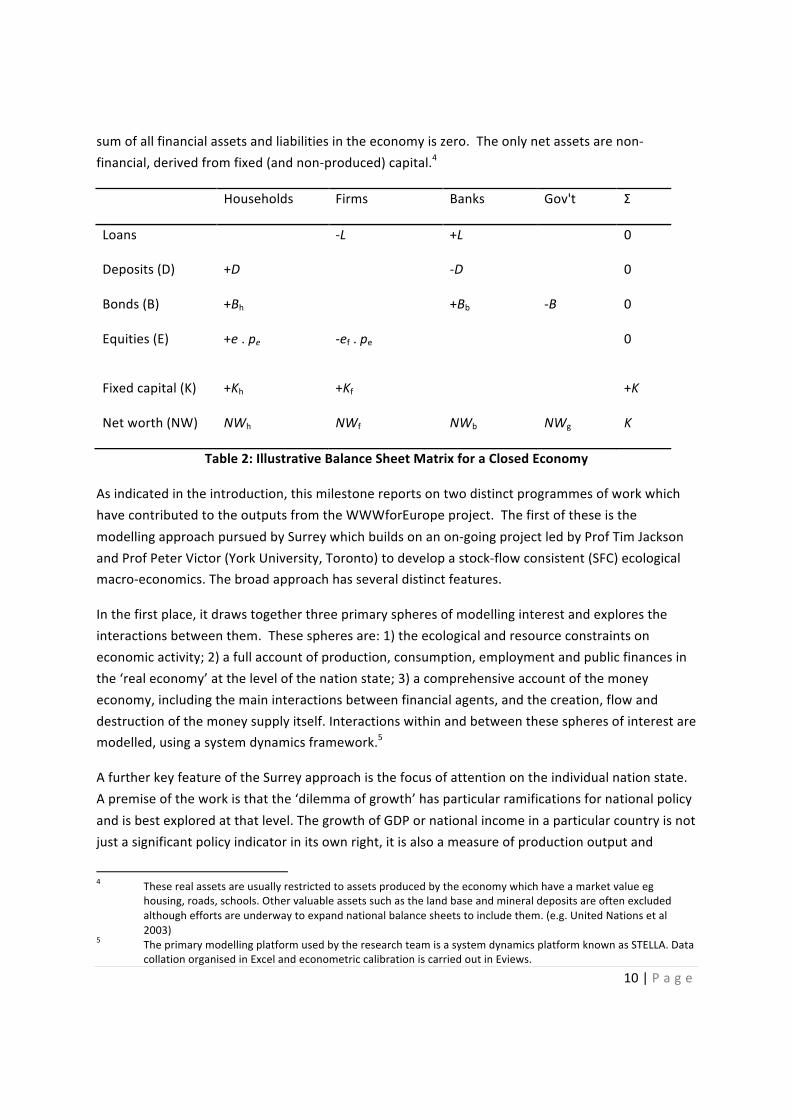

Thestockflowconsistentapproachtomoneyflowswithinaneconomycanalsoberepresentedintabularform,asillustratedinTables1and2.Table1showsanillustrative(andsimplified)‘transactionflows’matrixforaclosedeconomy.

Thematrixcreatesarepresentationofallthetransactionsbetweendifferentfinancialsectorsinagivenperiod(typicallyayear)ofeconomicactivity.Itwillbenoticedthattheproductionfirmsaccountissplitintoacurrentaccount,whererevenueandcostsaresettled,andacapitalaccountwherethefundsforinvestmentreside.Thissplitbetweencurrentandcapitalaccountisalsousuallyextendedalsotofinancialfirms(banks),totheCentralBank,andtotheforeignsector.ForillustrativepurposesweomittheseaccountsinTable1.

3 ThisdiagramistakenfromtheversionoftheFALSTAFFmodelreportedinsections5and6,whichwasdevelopedusingtheinteractivesystemsdynamicssoftwareSTELLAattheUniversityofSurreyincollaborationwithYorkUniversityToronto(JacksonandVictor2015).

8|P a g e

Households (h)

Firms (f) Financial sector (b)

Central Bank

Gov (g) RoW (r)

∑

Current Capital Current Capital (cb) Consumption (C) −𝐶 𝐶 0 Gov spending (G) 𝐺 −𝐺 0 Investment (I) −𝐼! 𝐼! + 𝐼! −𝐼! 0 Exports (X) and imports (M) 𝑋 −𝑀 𝑀 − 𝑋 0 Wages (W) 𝑊 −𝑊 0 Profits (F) +𝑃!" + 𝑃! −𝑃! +𝑃!" −𝑃! 0 Taxes (T) −𝑇! −𝑇! − 𝑇! 𝑇 0 Interest on Loans (L) −𝑟!𝐿!!! −𝑟!𝐿!! +𝑟!𝐿!! 0 Interest on Deposits (D) +𝑟!𝐷!!! +𝑟!𝐷!!

! −𝑟!𝐷!! +𝑟!𝐷!!! 0

Interest on Bonds (B) +𝑟!𝐵!!! +𝑟!𝐵!!! +𝑟!𝐵!!!" −𝑟!𝐵!! +𝑟!𝐵!!! 0 Change in Advances (A) +𝛥𝐴 −𝛥𝐴 0 Change in Reserves (R) −𝛥𝑅 +𝛥𝑅 0 Change in deposits (D) −𝛥𝐷! +𝛥𝐷 0 Change in bonds (B) −𝛥𝐵! −𝛥𝐵! −𝛥𝐵!" +𝛥𝐵 −𝛥𝐵! 0 Change in equities (E) −𝑝!𝛥𝐸 +𝑝!𝛥𝐸 0 Change in loans (L) +𝛥𝐿! +𝛥𝐿! 0 Change in mortgages (M) +𝛥𝑀 −𝛥𝑀 0 Change in pensions (N) −𝛥𝑁 +𝛥𝑁 0 ∑ 0 0 0 0 0 0 0 0 0

Table1:IllustrativeTransactionMatrixforSFCModelling

9|P a g e

Thetransactionmatrixincorporatesanaccountoftheincomesandexpendituresinthenationaleconomy,reflectingdirectlythestructureofthesystemofnationalaccounts.ThusthefirsttenrowsinTable1illustratetheflowaccountsofeachsector.Intermsofthehouseholdsector,forexample,itcanbeseenthathouseholdsreceivemoneyintheformofwagesanddistributedprofitsfromproductionfirms,whilespendingmoneyonconsumptionandtaxes.

ItistobeobservedthatthefirstsixrowsoftheFirmssector(column3inTable1)presentasimplifiedformoftheconventionalGDPaccountingidentity:

𝐶 + 𝐺 + 𝐼 = 𝐺𝐷𝑃𝑒 = 𝐺𝐷𝑃𝑖 = 𝑊 + 𝑃 1)

where𝐺𝐷𝑃! representstheexpenditure-basedformulationoftheGrossDomesticProductand 𝐺𝐷𝑃! representstheincomebasedGDPformulation.

ThelowerportionofTable1showsthechangesinfinancialassetsandliabilitiesbetweensectors.Soforexamplethenetlendingofthehouseholdssector(thesumofrows1to10incolumn2ofTable1)isdistributedamongstfourdifferentkindsoffinancialassetsinthisillustration:deposits,governmentbondsandequities.NotethatthisTableisforillustrativepurposesonly.ActualallocationsinFALSTAFFincludeotheroptions,includingthetakingofloansandmortgagesbyhouseholds.

Akeyfeatureofthetransactionmatrix,indeedthecoreprincipleattheheartofSFCmodelling,isthateachoftherowsandeachofthecolumnsmustalwayssumtozero.Ifthemodeliscorrectlyconstructed,thesezerobalancesshouldnotchangeovertimeasthesimulationprogress.TheaccountingidentitiesshowninTable1thereforeallowforaconsistencycheck,toensurethatthesimulationsactuallyrepresentpossiblestatesofthemonetaryeconomy.

AssociatedwiththetransactionsillustratedinthebottomfiverowsofTable1arechangesinthecapitalaccountsofeacheconomicsector.Foreachtransactioninfinancialassetsbetweentwosectorsoftheeconomythereisanassociatedchangeinthebalancesheetofthesametwosectors.Forinstance,adecisionbythehouseholdsectortoincreasedepositsatbankswillincreasethedepositassetsofhouseholdswhilesimultaneouslyincreasingdepositliabilitiesatbanks.

Thebalancesheetofaneconomy(Table2below)maybethoughtofasprovidingarecordofallprevioustransactionsuponwhichthetransactionsinthecurrentperiodareadded.Changesinthebalancesheetfromtheendofperiodt-1totheendofperiodtarethereforetheresultoftransactionsoccurringinperiodt.Typicallybalancesheetdataarecollatedandreportedonanannualbasisinthenationalaccounts.OneofthekeyfinancialaxiomsillustratedinTable2isthatthe

10|P a g e

sumofallfinancialassetsandliabilitiesintheeconomyiszero.Theonlynetassetsarenon-financial,derivedfromfixed(andnon-produced)capital.4

Households Firms Banks Gov't Σ

Loans

-L +L

0

Deposits(D) +D

-D

0

Bonds(B) +Bh

+Bb -B 0

Equities(E) +e.pe -ef.pe

0

Fixedcapital(K) +Kh +Kf

+K

Networth(NW) NWh NWf NWb NWg K

Table2:IllustrativeBalanceSheetMatrixforaClosedEconomy

Asindicatedintheintroduction,thismilestonereportsontwodistinctprogrammesofworkwhichhavecontributedtotheoutputsfromtheWWWforEuropeproject.ThefirstoftheseisthemodellingapproachpursuedbySurreywhichbuildsonanon-goingprojectledbyProfTimJacksonandProfPeterVictor(YorkUniversity,Toronto)todevelopastock-flowconsistent(SFC)ecologicalmacro-economics.Thebroadapproachhasseveraldistinctfeatures.

Inthefirstplace,itdrawstogetherthreeprimaryspheresofmodellinginterestandexplorestheinteractionsbetweenthem.Thesespheresare:1)theecologicalandresourceconstraintsoneconomicactivity;2)afullaccountofproduction,consumption,employmentandpublicfinancesinthe‘realeconomy’atthelevelofthenationstate;3)acomprehensiveaccountofthemoneyeconomy,includingthemaininteractionsbetweenfinancialagents,andthecreation,flowanddestructionofthemoneysupplyitself.Interactionswithinandbetweenthesespheresofinterestaremodelled,usingasystemdynamicsframework.5

AfurtherkeyfeatureoftheSurreyapproachisthefocusofattentionontheindividualnationstate.Apremiseoftheworkisthatthe‘dilemmaofgrowth’hasparticularramificationsfornationalpolicyandisbestexploredatthatlevel.ThegrowthofGDPornationalincomeinaparticularcountryisnotjustasignificantpolicyindicatorinitsownright,itisalsoameasureofproductionoutputand

4 Theserealassetsareusuallyrestrictedtoassetsproducedbytheeconomywhichhaveamarketvalueeg

housing,roads,schools.Othervaluableassetssuchasthelandbaseandmineraldepositsareoftenexcludedalthougheffortsareunderwaytoexpandnationalbalancesheetstoincludethem.(e.g.UnitedNationsetal2003)

5 TheprimarymodellingplatformusedbytheresearchteamisasystemdynamicsplatformknownasSTELLA.DatacollationorganisedinExcelandeconometriccalibrationiscarriedoutinEviews.

11|P a g e

consumptionpossibilities,aswellasbeingrelatedtoacountry’sabilitytoprovidecitizenswithwork,financeitssocialinvestment,andcompeteinglobalmarkets.Admittedly,allofthesequestionscouldalsobe(andoftenare)askedatsupra-nationalorsub-nationallevel.SincethedevelopmentofaunifiedSystemofNationalAccounts(UN1993,2008),however,themostcomprehensive,reliableandconsistentdatasetstendtobeavailableatcountryandnationallevel.

TheworkledbySurreyhassofardevelopedthreerelatedmacro-economicmodels.TheSIGMAmodel(Section4)employsasomewhatsimplifiedversionofthebroadermodellingstructuretoexploretherelationshipbetweensavings,inequalityandgrowthinamacroeconomicframework.WeaddressinparticularthehypothesisadvancedbyThomasPikettythatdeclininggrowthratesleadinevitablytowardsrisingsocialinequality.

TheFALSTAFFmodel(Sections5and6)isamoreextensiverepresentationofthemacro-economyincorporatingawidervarietyoffinancialassetsandliabilitiesinastock-flowconsistentframework.WeillustratetheuseofFALSTAFFbyexploring(Section5)theso-called‘growthimperative’whichissupposed(Binswanger2009eg)toarisefromthecreationofmoneyalongsideinterest-bearingdebt,andalso(Section6)thefinancialandmonetaryimplicationsoflarge-scalegreeninvestmentscenarios.

Finally,theGEMMAmodel(whichisstillunderdevelopment–seeSection8)buildsontheFALSTAFFframeworktoincludegreaterinter-industrystructureandmoreextendedbehaviouraldynamics–includingforinstanceaneconometricallyestimatedportfolioallocationfunctionforhouseholdassetsandliabilities.

ThesecondstrandofworkhasbeendevelopedindependentlythroughtheUniversityofVienna.TheECOGROmodel(Section7)isastock-flowconsistentmodelcalibratedtotheleveloftheEUasawhole.Itincorporatestwospecificenvironmentalextensionstotheconventionalstock-flowconsistentframework.Oneoftheseexpandsthestructureofnonfinancialfirmstoincorporateaseparateenergysector.Theotherincorporatesanenvironmentaldamagefunctionwhichimpactsonthecapitalstock.

Thefollowingsectionsofthepaperprovideanoverviewofthedifferentapproachestakenandreportinthefindings.Furtherdetailsoneachapproacharetobefoundinthereferences.

12|P a g e

4 Doesslowgrowthleadtorisinginequality?

TheFrencheconomist,ThomasPiketty(2014),hasreceivedwidespreadacclaimforhisbookCapitalinthe21stCentury.Buildingonover700pagesofpainstakingstatisticalanalysis,thecentralthesisofthebookisnonethelessrelativelystraightforwardtodescribe.Pikettyarguesthattheincreaseininequalitywitnessedinrecentdecadesisadirectresultoftheslowingdownofeconomicgrowthinmoderncapitalisteconomies.Undercircumstancesinwhichgrowthratesdeclinefurther,hesuggests,thischallengewouldbeexacerbated.Pikettyadvanceshisargumentthroughtheformulationoftwo‘fundamentallaws’ofcapitalism.Thefirstofthese(Piketty2014:52etseq)relatesthecapitalstock(morepreciselythecapitaltoincomeratio𝛽)totheshareofincomeαflowingtotheownersofcapital.Specifically,thefirstfundamentallawofcapitalismsaysthat:6

𝛼 = 𝑟𝛽, (1)whereristherateofreturnoncapital.Since𝛽 isdefinedasK/YwhereKiscapitalandYisincome,itiseasytoseethatthis‘law’is,asPikettyacknowledges,anaccountingidentity:

𝛼𝑌 = 𝑟𝐾. (2)Formallyspeaking,theincomeaccruingtocapitalequalsthetotalcapitalmultipliedbytherateofreturnonthatcapital.Thoughthis‘law’onitsowndoesnotforcetheeconomyinonedirectionoranother,itprovidesthefoundationfromwhichtoexploretheevolutionofhistoricalrelationshipsbetweencapital,incomeandratesofreturn.Inparticular,itcanbeseenfromthisidentitythatforanygivenrateofreturnrtheshareofincomeaccruingtotheownersofcapitalrisesasthecapitaltoincomeratiorises.7ItisthesecondofPiketty’s‘fundamentallawsofcapitalism’(opcit:168etseq;seealsoPiketty2010)thatgeneratesparticularconcerninthecontextofdeclininggrowthrates.Thislawstatesthatinthelongrun,thecapitaltoincomeratioβtendstowardstheratioofthesavingsratestothegrowthrateg,ie:

6 Inwhatfollows,wesuppressspecificreferencetotime-dependencyofvariablesexceptwhereabsolutely

necessary.Thusallvariablesshouldbereadastimedependentunlessspecificallydenominatedwithasubscriptedsuffix0.Occasionally,wewillhavereasontousethesubscriptedsuffix(-1)todenotethefirstlagofatime-dependentvariable.

7 Wewillseelaterthattheceterisparibusclauserelatingtoconstantrhereisimportant.Infact,therateofreturnwilltypicallychangeasthecapitaltoincomeratiorises;andtotheextentthatthisratiodeclineswithincreasingβ,itcanpotentiallymitigatetheaccumulationofthecapitalshareofincome.

13|P a g e

𝛽 → !!

𝑎𝑠 𝑡 → ∞. (3)

Thisasymptoticlawsuggeststhat,asgrowthratesfalltowardszero,thecapitaltoincomeratiowilltendtorisedramatically–dependingofcourseonwhathappenstosavingsrates.Takentogetherwiththefirstlaw,equation(3)suggeststhatoverthelongterm,capital’sshareofincomeisgovernedbythefollowingrelationship:

𝛼 → 𝑟 !!

𝑎𝑠 𝑡 → ∞. (4)

Inotherwords,asgrowthdeclines,therisingcapitaltoincomeratio𝛽leadstoanincreasingshareofincomegoingtocapitalandadecliningshareofincomegoingtolabour.Itisimportanttostressthattherelationships(3)and(4)arelong-termequilibriatowhichtheeconomyevolves,providedthatthesavingsratesandthegrowthrategstayconstant.AsPikettypointsout,‘theaccumulationofwealthtakestime:itwilltakeseveraldecadesforthelawβ=s/gtobecometrue’(opcit:168).Inanyrealeconomy,thegrowthrategandthesavingsratesarelikelytobechangingcontinually,sothatatanypointintime,theeconomyisstrivingtowards,butmayneverinfactachieve,theasymptoticresult.Piketty’shypothesisposesaparticularchallengetothoseeconomistswhohavebeencriticalofsociety’s‘GDPfetish’(Stiglitzetal2009)andsoughttoestablishalternativeapproaches(Daly1996,Victor2008,Jackson2009,Rezaietal2012,d’Alisaetal2014)inwhichsocio-economicgoalsareachievedwithoutassumingcontinualthroughputgrowth.Certainly,theprospectsfor‘prosperitywithoutgrowth’(Jackson2009)wouldappearslimatbestifPiketty’sthesiswereunconditionallytrue.ThePikettyhypothesisisalsoproblematicinthefaceofapotential‘secularstagnation’(Gordon2012),inwhichdeclininggrowthratesareafeatureofthenationalorglobalmacro-economy.InordertoexplorefurtherthePikettyhypothesis,JacksonandVictor(2014,2015)developedaclosed,SFC,demand-drivenmodelofSavings,InvestmentandGrowthinaMacroeconomicframework(SIGMA).SIGMAwasusedtotestfortheimplicationsofaslowdownofgrowthona)capital’sshareofincomeandb)thedistributionofincomesintheeconomy.Policyoptionstoreduceinequalitywerealsoexamined.SIGMAhasfourfinancialsectors:households,government,firmsandbanks.Firms’andbanks’accountsaredividedbetweencurrentandcapitalaccountsandthehouseholdssectorisfurthersubdividedintotwosubsectors(whichwedenominateas‘workers’and‘capitalists’)inordertoexplorepotentialinequalitiesinthedistributionofincomesandofwealth.Byaddingagovernmentsectortothemodel,weareabletoexplorethepotentialtomitigateregressiveimpactsthrougha

14|P a g e

progressivetaxationsystem.Theinclusionofabankingsectorallowsustoestablishclearrelationshipsbetweentherealandthefinancialeconomyanddiscussquestionsofhouseholdwealth.BeforedescribingSIGMAinmoredetail,wefirstsummarisePiketty’sargument.ThemodelitselfisbuiltusingthesystemdynamicssoftwareSTELLA.Thiskindofsoftwareprovidesausefulplatformforexploringeconomicsystemsforseveralreasons,nottheleastofwhichistheeaseofundertakingcollaborative,interactiveworkinavisual(iconographic)environment.Furtheradvantagesarethetransparencywithwhichonecanmodelfullydynamicrelationshipsandmirrorthestock-flowconsistencythatunderliesourapproachtomacroeconomicmodelling.FollowingmuchoftheSFCliterature,themodelisbroadlyKeynesianinthesensethatitisdemand-driven.Ourapproachistoestablishalevelofoveralldemandthroughanexogenousgrowthrate,𝑔,andtogeneratethelevelofinvestmentthroughanexogenoussavingsrate,𝑠.Wethenexploretheimpactsofchangesinthesevariablesovertimeontheincomesharesfromcapitalandlabourthroughanendogenousrateofreturn,𝑟,oncapital.Toachievethisweemployaconstantelasticityofsubstitution(CES)productionfunction,nottodriveoutputasinaconventionalneoclassicalmodel,buttoderivethemarginalproductivity𝑟! ofcapital𝐾andalsotoestablishthelabouremploymentassociatedwithagivenlevelofaggregatedemand.8Toillustrateourargumentswithoutunnecessarycomplications,weworkwithasimplifiedversionofthemorecomplexstructurethatwehavedevelopedelsewhere.First,asnoted,theSIGMAeconomyisclosedwithrespecttooverseastrade.Next,weassumethatgovernmentalwaysbalancesthefiscalbudgetandholdsnooutstandingdebt,sothatgovernmentspending,𝐺,isequaltotaxes,𝑇,leviedonlyonhouseholds.Finally,weemployarathersimplebalancesheetstructure,sufficientonlytogetahandleonchangesinhouseholdwealthunderdifferentpatternsofownershipofcapital.Householdsassetsareheldeitherasdeposits,𝐷,inbanksorasequities,𝐸,infirms.Theonlyotheritemonthebalancesheetisloans,𝐿,madebybankstonon-financialfirms.Thebankingsectorplaysarelativelystraightforwardroleasafinancialintermediary,providingdepositfacilitiesforhouseholdsandloanstofirms.Clearlynoneoftheseassumptionsisaccurateasafulldescriptionofamoderncapitalisteconomy,butallofthemcanberelaxedinmoresophisticatedversionsofourframeworkandnoneofthemobstructsourpurposesinthisstudy.

8 Weareawareofcourseofthelimitationsofusingabroadlyneoclassicalproductionfunction(Cohenand

Harcourt2003,Robinson1953).However,retainingthisaspectofPiketty’sanalysisallowsustocompareourfindingsmoredirectlywithhis.

15|P a g e

Householdsavingsaredistributedbetweennewbankdeposits,𝛥𝐷,andthepurchaseofequities,𝛥𝐸,fromfirms.Itisassumedforsimplicitythatthedemandfornewequitiesbyhouseholdsisequaltothesupplyofnewequitiesbyfirmsandthattheseintheirturnaredeterminedviaadesireddebttoequityratioinfirms.9Thedistributionofequitypurchasesbetweencapitalistandworkerhouseholdsisdeemedtobeinthesameproportionasthenetsavingsofeachsector.Changesindepositsarethencalculatedasaresidualfromnetsavings.InordertomodeltheevolutionoftheSIGMAeconomyovertime,wefollowPikettybydefiningtheevolutionofthenetnationalincome𝑁𝐼accordingtoan(exogenous)growthrate𝑔suchthat:

𝑁𝐼 = 1 + 𝑔 ∗ 𝑁𝐼(!!) (4)

where𝑁𝐼(!!)isthevalueinthepreviousperiod(iethefirstlag)ofthevariable𝑁𝐼.Insome

scenarios𝑔willtakeafixedvalue𝑔!throughouttheperiod𝜏ofthescenario,10whileinothers𝑔willdeclineuniformlyfrom𝑔!tozeroovertimet.TestingPiketty’shypothesisrequiresthatweestablishtherateofreturntocapital,𝑟,whichinturnallowsustodeterminethesplitbetweenwagesandfirmsprofitsinthenetnationalincome.AlongwithPiketty(2014a:213-214),weassume(fornow)thatthereturntocapitalisgivenbythemarginalproductivityofcapital,whichwedenoteby𝑟!.Thisassumptiononlyworksundermarketconditionsinwhichtherearenostructuralfeatureswhichmightleadeithercapitalorlabourtoextortmorethantheir‘fair’shareoftheoutputfromproduction.Inasense,thisassumptionisaconservativeoneforus,totheextentthatconclusionsaboutinequalityarestrongerinimperfectmarketdynamics.Underconditionsofduress,inwhichtheownersofcapitalreceivearateofreturn𝑟greaterthanthemarginalproductivityofcapital𝑟!,ourconclusionsaboutanyinequalitywhichresultsfromdeclininggrowthrateswillbereinforced.Conversely,ofcourse,wemustbewareofmakingtoostrongassumptionsaboutthepotentialtomitigateinequality,inanysituationinwhichtheownersofcapitalhavegreaterbargainingpowerthanwagelabour.TheresultsofouranalysisaredescribedindetailinJacksonandVictor(2015a)andsummarisedinFigures2and3.Theanalysisconfirmsthat,undercertainconditions,itisindeedpossibleforbothcapital’sshareofincomeandincomeinequalitytorisesubstantiallyasgrowthratesdecline.

9 Incontrasttoourtreatmentelsewhere(JacksonandVictor2015),thismeansthatthereisnospeculative

purchasingofequitiesthatmightleadtocapitalgainsandlosses.10 Inthispaperwetake𝜏 = 100,iethescenariosrunover100years.

16|P a g e

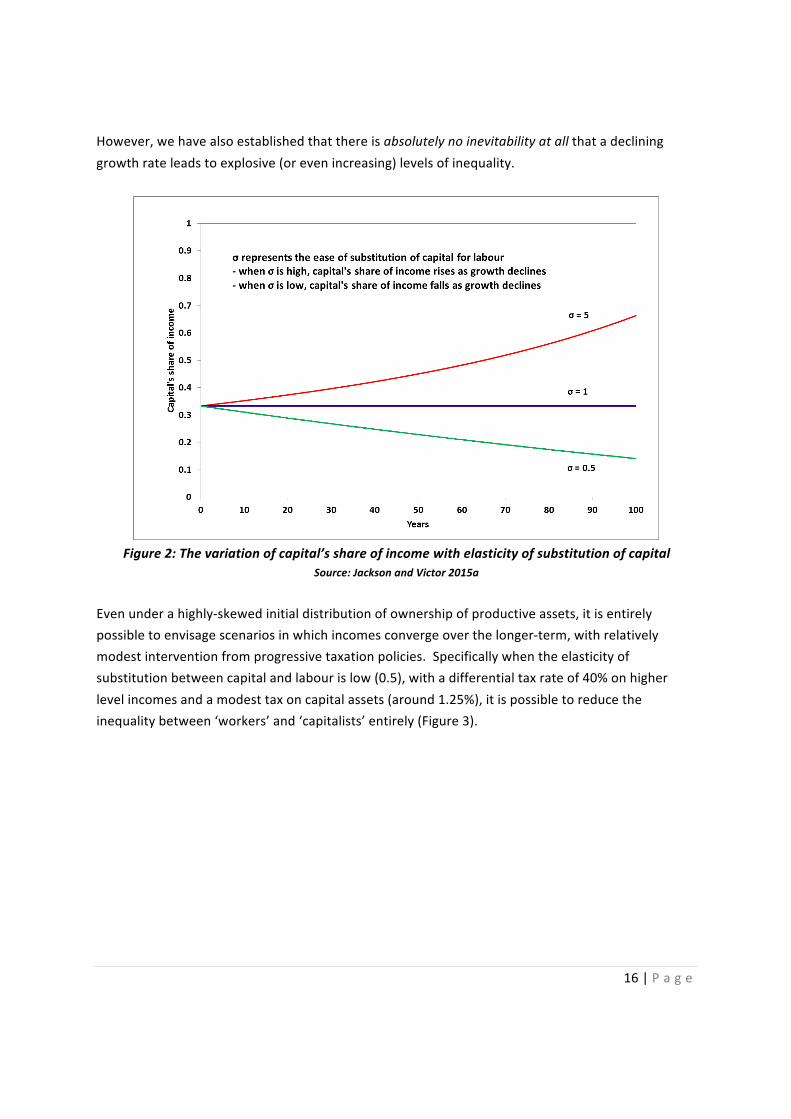

However,wehavealsoestablishedthatthereisabsolutelynoinevitabilityatallthatadeclininggrowthrateleadstoexplosive(orevenincreasing)levelsofinequality.

Figure2:Thevariationofcapital’sshareofincomewithelasticityofsubstitutionofcapital

Source:JacksonandVictor2015a

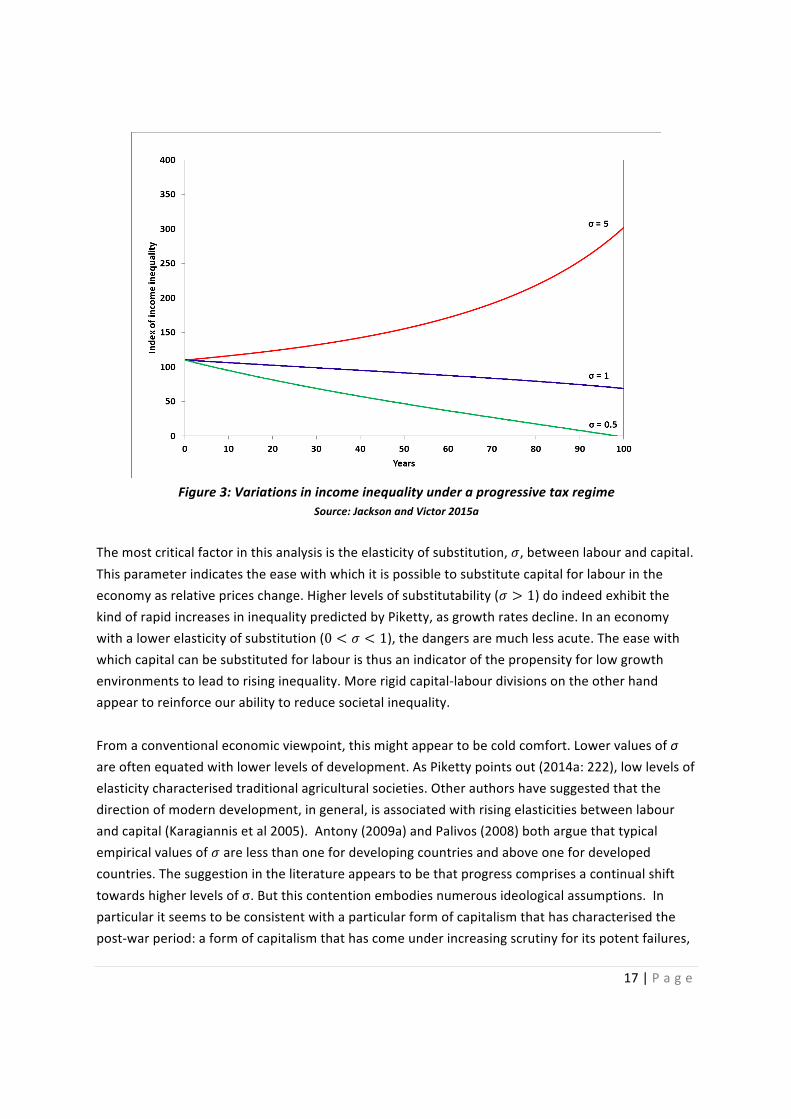

Evenunderahighly-skewedinitialdistributionofownershipofproductiveassets,itisentirelypossibletoenvisagescenariosinwhichincomesconvergeoverthelonger-term,withrelativelymodestinterventionfromprogressivetaxationpolicies.Specificallywhentheelasticityofsubstitutionbetweencapitalandlabourislow(0.5),withadifferentialtaxrateof40%onhigherlevelincomesandamodesttaxoncapitalassets(around1.25%),itispossibletoreducetheinequalitybetween‘workers’and‘capitalists’entirely(Figure3).

17|P a g e

Figure3:Variationsinincomeinequalityunderaprogressivetaxregime

Source:JacksonandVictor2015a

Themostcriticalfactorinthisanalysisistheelasticityofsubstitution,𝜎,betweenlabourandcapital.Thisparameterindicatestheeasewithwhichitispossibletosubstitutecapitalforlabourintheeconomyasrelativepriceschange.Higherlevelsofsubstitutability(𝜎 > 1)doindeedexhibitthekindofrapidincreasesininequalitypredictedbyPiketty,asgrowthratesdecline.Inaneconomywithalowerelasticityofsubstitution(0 < 𝜎 < 1),thedangersaremuchlessacute.Theeasewithwhichcapitalcanbesubstitutedforlabouristhusanindicatorofthepropensityforlowgrowthenvironmentstoleadtorisinginequality.Morerigidcapital-labourdivisionsontheotherhandappeartoreinforceourabilitytoreducesocietalinequality.Fromaconventionaleconomicviewpoint,thismightappeartobecoldcomfort.Lowervaluesofσareoftenequatedwithlowerlevelsofdevelopment.AsPikettypointsout(2014a:222),lowlevelsofelasticitycharacterisedtraditionalagriculturalsocieties.Otherauthorshavesuggestedthatthedirectionofmoderndevelopment,ingeneral,isassociatedwithrisingelasticitiesbetweenlabourandcapital(Karagiannisetal2005).Antony(2009a)andPalivos(2008)botharguethattypicalempiricalvaluesof𝜎arelessthanonefordevelopingcountriesandaboveonefordevelopedcountries.Thesuggestionintheliteratureappearstobethatprogresscomprisesacontinualshifttowardshigherlevelsofσ.Butthiscontentionembodiesnumerousideologicalassumptions.Inparticularitseemstobeconsistentwithaparticularformofcapitalismthathascharacterisedthepost-warperiod:aformofcapitalismthathascomeunderincreasingscrutinyforitspotentfailures,

18|P a g e

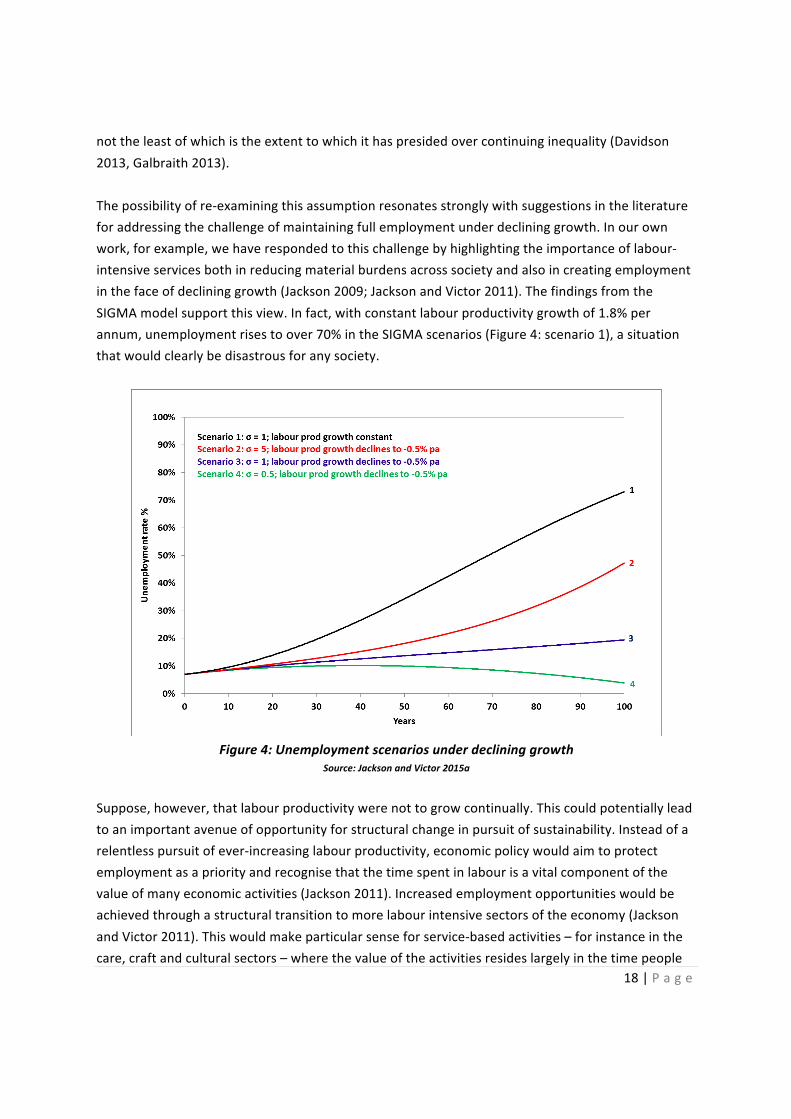

nottheleastofwhichistheextenttowhichithaspresidedovercontinuinginequality(Davidson2013,Galbraith2013).Thepossibilityofre-examiningthisassumptionresonatesstronglywithsuggestionsintheliteratureforaddressingthechallengeofmaintainingfullemploymentunderdeclininggrowth.Inourownwork,forexample,wehaverespondedtothischallengebyhighlightingtheimportanceoflabour-intensiveservicesbothinreducingmaterialburdensacrosssocietyandalsoincreatingemploymentinthefaceofdeclininggrowth(Jackson2009;JacksonandVictor2011).ThefindingsfromtheSIGMAmodelsupportthisview.Infact,withconstantlabourproductivitygrowthof1.8%perannum,unemploymentrisestoover70%intheSIGMAscenarios(Figure4:scenario1),asituationthatwouldclearlybedisastrousforanysociety.

Figure4:Unemploymentscenariosunderdeclininggrowth

Source:JacksonandVictor2015a

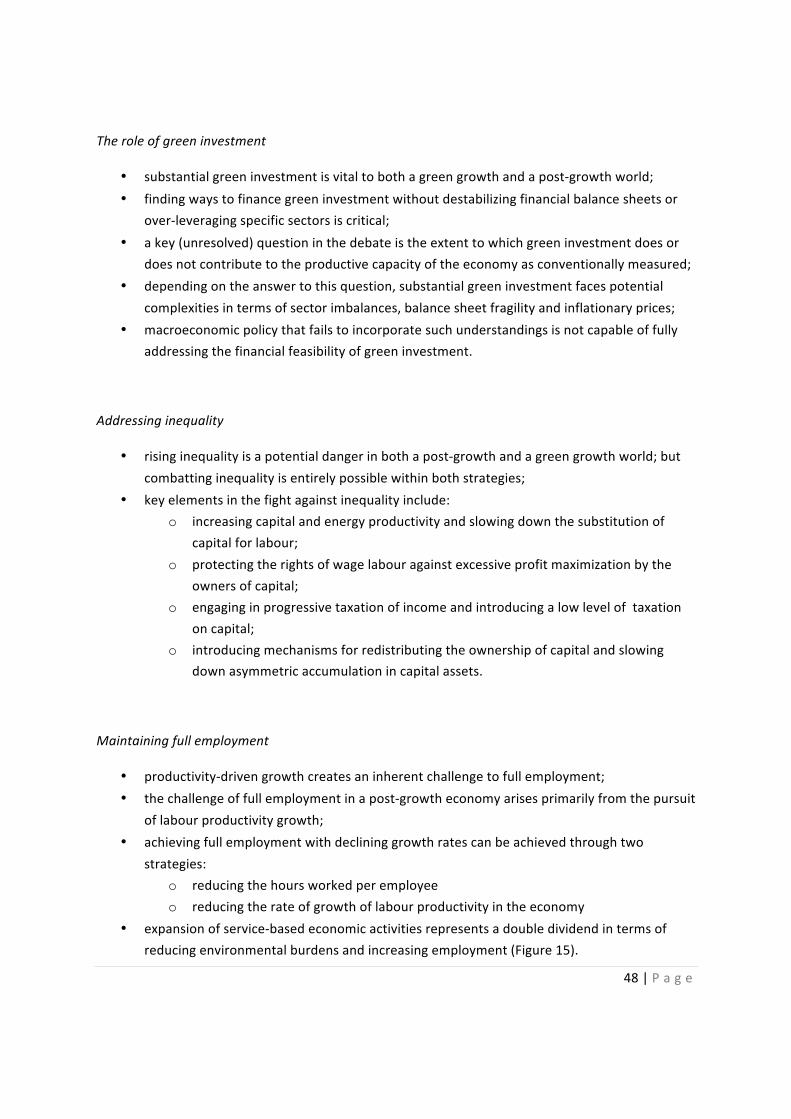

Suppose,however,thatlabourproductivitywerenottogrowcontinually.Thiscouldpotentiallyleadtoanimportantavenueofopportunityforstructuralchangeinpursuitofsustainability.Insteadofarelentlesspursuitofever-increasinglabourproductivity,economicpolicywouldaimtoprotectemploymentasapriorityandrecognisethatthetimespentinlabourisavitalcomponentofthevalueofmanyeconomicactivities(Jackson2011).Increasedemploymentopportunitieswouldbeachievedthroughastructuraltransitiontomorelabourintensivesectorsoftheeconomy(JacksonandVictor2011).Thiswouldmakeparticularsenseforservice-basedactivities–forinstanceinthecare,craftandculturalsectors–wherethevalueoftheactivitiesresideslargelyinthetimepeople

19|P a g e

devotetothem.Inpolicyterms,suchatransitionwouldinvolveprotectingthequalityandintensityofpeople’stimeintheworkplacefromtheinterestsofaggressivecapital.SuchaproposalisnotamillionmilesfromMinsky’s(1986)suggestionthatgovernmentshouldactas‘employeroflastresort’instabilisinganunstableeconomy.Scenarios2to4inFigure4alldescribeasituationinwhichbytheendoftherun,labourproductivitygrowthhasdeclinedtoapointwhereitisslightlynegative.Bytheendofthescenario,labourproductivityitselfisdecliningintheeconomy–productionoutputisbecomingmorelabourintensive.Figure4revealsthatthisdeclineinlabourproductivitygrowthisnotinitselfsufficienttoensureacceptablelevelsofunemployment.Forhighervaluesofσ,unemploymentisstillrunningdangerouslyhigh.Butforlowervaluesofσitispossiblenotonlytomaintainbuteventoimprovethelevelofemploymentintheeconomy,inspiteofadeclineinthegrowthratetozero.Thereishoweveratantalisingsuggestioninherentinthisanalysisthatchangingtheelasticityofsubstitutionbetweenlabourandcapitaloffersanotherpotentialavenuetowardsamoresustainablemacro-economy,andinparticularawayofmitigatingtheperniciousimpactsofinequalityandunemploymentinalowgrowtheconomy.Exploringthatsuggestionfullyisbeyondthescopeofthispaper,butiscertainlyworthflagginghere.Weshouldalsorecallhereourassumptionthattherateofreturntocapitalisequaltothemarginalproductivityofcapital.Asweremarkedearlier,thisassumptiononlyholdsinmarketsconditionswherecapitalisunabletouseitspowertocommandahighershareofincome.Clearly,insomeofthescenarioswehaveenvisaged,thisassumptionmaynolongerhold.Wherepoliticalpoweraccumulatesalongsidetheaccumulationofcapital,thedangerofrisinginequalityisparticularlysevereandisnolongeroffsetsimplybychangesintheeconomicstructure.Thisquestionalsowarrantsfurtheranalysis.Insummary,theSIGMAmodelexplorestherelationshipbetweengrowth,savingsandincomeinequality,underavarietyofassumptionsaboutthenatureandstructureoftheeconomy.Ourprincipalfindingisthatrisinginequalityisbynomeansinevitable,eveninthecontextofdeclininggrowthrates.Akeypolicyconclusionconcernstheneedtoprotectwagelabouragainstaggressivecost-reducingstrategiestofavourtheinterestsofcapital.Thismeasurewouldhavetheadditionalbenefitofmaintaininghighemployment,eveninalow-ordegrowtheconomy.

20|P a g e

5 FALSTAFFPart1–Creditcreationandthe‘growthimperative’

Ithasbeenarguedthatcapitalismhasaninherent‘growthimperative’:inotherwords,thattherearecertainfeaturesofcapitalismwhichareinimicaltoastationarystate11oftherealeconomy.ThisargumenthasitsrootsinthewritingsofKarlMarx(1848)andRosaLuxemburg(1913)andtherearegoodreasonstotakeitseriously.Forinstance,undercertainconditions,thedesireofentrepreneurstomaximiseprofitswillleadtothepursuitoflabourproductivitygainsinproduction.Unlesstheeconomygrowsovertime,aggregatelabourdemandwillfall,leadingtoa‘productivitytrap’(JacksonandVictor2011)inwhichhigherandhigherlevelsofunemploymentcanonlybeoffsetbycontinuedeconomicgrowth.Ourconcerninthissectionistoaddressoneparticularaspectofthegrowthimperative:namely,thequestionofinterest-bearingdebt.Avarietyofauthorshavesuggestedthatwhenmoneyiscreatedinparallelwithinterest-bearingdebtitinevitablycreatesagrowthimperative.Tosome,thechargingofinterestondebtisitselfanunderlyingdriverforeconomicgrowth.Intheabsenceofgrowth,itisargued,itwouldbeimpossibletoserviceinterestpaymentsandrepaydebts,whichwouldthereforeaccumulateunsustainably.Thisclaimwasmade,forinstance,byRichardDouthwaite(1990,2006).InTheEcologyofMoney,Douthwaite(2006)suggeststhatthe‘fundamentalproblemwiththedebtmethodofcreatingmoneyisthat,becauseinteresthastobepaidonalmostallofit,theeconomymustgrowcontinuouslyifitisnottocollapse.’Thisviewhasbeeninfluentialamongstarangeofeconomistscriticalofcapitalism,andinparticularthosecriticalofthesystemofcreationofmoneythroughinterest-bearingdebt.Eisenstein(2012)maintainsthat‘ourpresentmoneysystemcanonlyfunctioninagrowingeconomy.Moneyiscreatedasinterest-bearingdebt:itonlycomesintobeingwhensomeonepromisestopaybackevenmoreofit’.Insimilarvein,Farleyetal(2013)claimthatthe‘currentinterest-bearing,debt-basedsystemofmoneycreationstimulatestheunsustainablegrowtheconomy’(opcit:2803).Thesameauthorsseektoidentifypoliciesthat‘wouldlimitthegrowthimperativecreatedbyaninterest-basedcreditcreationsystem’(opcit:2823).Thepopularunderstandingthatdebt-basedmoneyasaformofgrowthimperativeisintuitivelyappealing,buthasbeensubjecttoremarkablylittlein-deptheconomicscrutiny.AnotableexceptionisalandmarkpaperbyMathiasBinswanger(2009),whosetouttoprovidean‘explanationforagrowthimperativeinmoderncapitalisteconomies,whicharealsocreditmoneyeconomies’(opcit:

11 WeusethetermstationarystatetodescribezerogrowthintheGrossDomesticProduct(GDP).Wepreferhere

stationarytosteadystate,whichisalsowidelyused(Daly2014eg),fortworeasons.First,thetermsteadystateisemployedinthepost-Keynesianliterature(GodleyandLavoie2007)todescribeastateoftheeconomyinwhichflowsareconstant;butthismaystillentailgrowth.Astationarystateisusedtodescribeastateinwhichbothflowsandstocksareconstant,inwhichcasethereisnogrowth.Second,thisterminologyharksbacktoearlyclassicaleconomistssuchasMill(1848),emphasisingthepedigreeoftheideaofanon-growth-basedeconomy.

21|P a g e

707).Asaresultoftheabilityofcommercialbankstocreatemoneythroughtheexpansionofcredit,heclaims(opcit:724),‘azerogrowthrateisnotfeasibleinthelongrun’.Byhisownadmission,however,Binswanger’spaper‘doesnotaimtogiveafulldescriptionofamoderncapitalisteconomy’.Inparticular,henotes(opcit:711)thathismodel‘shouldbedistinguishedfromsomerecentmodelingattemptsinthePostKeynesiantradition’whichsetouttoprovide‘comprehensive,fullyarticulated,theoreticalmodels’thatcouldserveasa‘blueprintforanempiricalrepresentationofawholeeconomicsystem’(Godley1999:394).ArecentsymposiumonthegrowthimperativehascontributedseveralnewperspectivesonBinswanger’soriginalhypothesis,butthesepapersalsofallshortofprovidingafullanalysisofthiskind(Binswanger2015,Rosenblum2015).Ouraiminthissectionistoaddressthislimitation,inthecontextofastock-flowconsistentmodel,calibratedwithempiricallyplausibledata.Tothisend,wehavedevelopedamacroeconomicmodelofFinancialAssetsandLiabilitiesinaStockandFlowconsistentFramework(FALSTAFF),calibratedatthelevelofthenationaleconomy(JacksonandVictor2015b).AswiththeSIGMAmodel(Section4),theapproachisbroadlypost-Keynesianinthesensethatthemodelisdemand-drivenandincorporatesaconsistentaccountofallmonetaryflows.ThefullFALSTAFFmodelisarticulatedintermsofsixinter-relatedfinancialsectoraccounts:households,firms,banks,government,centralbankandthe‘restoftheworld’(foreignsector).Theaccountsoffirmsandbanksarefurthersubdividedintocurrentandcapitalaccountsinlinewithnationalaccountingpractices.Thehouseholdsectorcanbefurthersubdividedintotwosectorsinordertotestthedistributionalaspectsofchangesintherealorfinancialeconomy.12Forthepurposesofthisanalysis,wehavesimplifiedtheFALSTAFFstructure(denotedhereasFALSTAFFS)inordertofocusspecificallyonthequestionofinterest-bearingmoney.Forinstance,weassumebalancedtradeandrestrictthenumberofcategoriesofassetsandliabilitiestoincludeonlyloans,deposits,equitiesandgovernmentbonds.ThebroadstructureoftheFALSTAFFSmodelisasfollows.Aggregatedemandiscomposedofhouseholdspending,governmentspending,andtheinvestmentexpenditureoffirms.13Theallocationofgrossincomeissplitbetweenthedepreciationoffixedcapital(whichisassumedtoberetainedbyfirms),thereturntolabour(thewagebill)andthereturntocapital(profits,dividendsandinterestpayments).Households’propensitytoconsumeisdependentbothonincomeandonfinancialwealth(GodleyandLavoie2007).Themodelalsoincorporatesthepossibilityofexploringtwokindsofexogenous

12 WehaveusedthissubdivisiontoexploretheimplicationsofPiketty’s(2014)hypothesisthatinequalityincreases

asthegrowthratedeclines(JacksonandVictor2015b).13 Forsimplicity,weassumeforthepurposesofthispaperabalancedtradepositioninwhichexportsareequalto

importsandnettradeiszero.

22|P a g e

‘shocks’tohouseholdspending.Inthefirst,arandomadjustmentismadetohouseholdspendingthroughouttherun,withinarangeofplusorminus2.5%fromthepredictedvalue.Inthesecond,aone-offshockeitherreducesorincreasesspendingby5%overtwoconsecutiveperiodsearlyintherun.Weusetheseexogenousshockstotestthestabilityofthestationarystateunderourdefaultassumptions.Householdsavingsmayinprinciplebedistributedbetweengovernmentbonds,firmsequities,banksequities,bankdepositsandloans.14Householddemandforbondsisassumedheretobeequaltotheexcesssupplyofbondsfromgovernment,oncebanks’demandsforbondsaremet.Householddemandforequitiesisassumedtobeequaltotheissuanceofequitiesfromfirmsandbanks.Thus,householdsarethesoleownersofequityinthismodelandthereturnonequitiesislimitedtodividendsreceived,sincetherearenocapitalgainsinthemodel.15Thebalanceofhouseholdsavings,oncebondandequitypurchaseshavebeenmade,isallocatedtopayingdownloansorbuildingupdeposits.Ifsavingsarenegative,householdsmayalsoborrowfrombankstofinancespending.Firmsareassumedtoproducegoodsandservicesondemandforhouseholds,governmentsandtomeetthedemandforgrossfixedcapitalinvestment.Investmentdecisionsarebasedonaflexibleacceleratorfunction(Jorgenson1963,GodleyandLavoie2007)inwhichnetinvestmentisassumedtobeafixedproportionofthedifferencebetweencapitalstockinthepreviousperiod,andatargetcapitalstockdeterminedbyexpecteddemandandanassumedcapital-to-outputratio.Aproportionofgrossprofitsequaltothedepreciationofthecapitalstockoverthepreviousperiodisassumedtoberetainedbyfirmsforinvestment,withnet(additional)investmentfinancedthroughamixtureofnewloansfrombanksandtheissuanceofequitiestohouseholds,accordingtoadesireddebt-to-equityratio.Governmentreceivesincomefromtaxationandpurchasesgoodsandservices(forthebenefitofthepublic)fromthefirmssector.Taxationisonlyleviedonhouseholdsinthisversionofthemodel,ataratewhichprovidesforaninitiallybalancedbudgetunderthedefaultvaluesforaggregatedemand.Usingtheseassumptions,JacksonandVictor(2015b)explorethreegovernmentspendingscenarios:oneinwhichgovernmentspendingremainsconstantthroughouttherun,oneinwhichgovernmentspendingplusbondinterestisequaltotaxreceipts(ieastrict‘austerity’policyinwhichgovernmentbalancesthefiscalbudget),andoneinwhichgovernmentengagesina‘countercyclical’spending

14 InthefullFALSTAFFframework,householdsavingsareallocatedbetweenarangeoffinancialassets(and

liabilities)includingbankdeposits,equities,pensionfunds,governmentbonds(andmortgageandloans),usinganeconometrically-estimatedportfolioallocationmodelbasedontheframeworkoriginallyproposedbyBrainardandTobin(1968).

15 ThisassumptionisrelaxedinthefullFALSTAFFmodel,inwhichbothequitypricesandhousingvaryaccordingtosupplyanddemand.Theseassetsarethereforesubjecttocapitalgainsinthefullmodel.

23|P a g e

policy,increasingspendingwhenaggregatedemandfallsanddecreasingitwhenaggregatedemandrises.Governmentbondsareissuedtocoverdeficitspending.Banksacceptdepositsandprovideloanstohouseholdsandtofirms,asdemanded.Bankprofitsaregeneratedfromtheinterestratespreadbetweendepositsandloans,plusinterestpaidonanygovernmentbondstheyhold.Profitsaredistributedtohouseholdsasdividends,exceptforanyretainedearningsthatmayberequiredtomeetthecapitalaccount‘financingrequirement’.Thisfinancingrequirementisthedifferencebetweendeposits(inflowsintothecapitalaccount)andthesumofloans,bondpurchasesandincreasesincentralbankreserves(outgoingsfromthecapitalaccount).ThecentralbankplaysaverysimpleroleinthestationarystateversionofFALSTAFF,providingliquidityondemand(intheformofcentralbankreserves)tocommercialbanksinexchangeforgovernmentbonds.FALSTAFFSprovidesfortworegulatorypoliciesthatmightreasonablybeimposedonbanks.First,themodelcanimposea‘capitaladequacy’requirementinwhichbanksarerequiredtoholdenough‘capital’tocoveragivenproportionofriskyassets.Second,banksmaybesubjecttoacentralbank‘reserveratio’inwhichreservesareheldatthecentralbankuptoagivenproportionofdepositsheldonaccount.Fewdevelopedcountriesretainformalreserveratiosthesedays,leavingituptothebanksthemselvestodecidewhatreservestohold.However,wehaveincludedadefaultreserveratioof5%inordertotestBinswanger’shypothesisthatsuchrequirementsmightleadtoagrowthimperative.Thecapitaladequacyrequirementissupposedtoprovideresilienceinthefaceofdefaultingloans,asrequiredforinstanceundertheBaselIIIframework(BIS2011).Infact,weadoptasourstartingpointtheBaselIIIrequirementthatbanks’‘capital’(thebookvalueofequityinthebanks’balancesheet)shouldbeequalto8%ofrisk-weightedassets(loanstohouseholdsandfirms).Tomeetthisrequirement,banksinFALSTAFFSissueequitiestohouseholds,whichhastheeffectofshiftingdepositstoequityontheliabilitysideofthebalancesheetandincreasingtheratioofcapitaltoloans.Tobalancethebalancesheet,bankspurchasegovernmentbonds(conventionallydeemedrisk-free)whichtogetherwithcentralbankreserves(alsorisk-free)provideforacertainproportionof‘safe’capitaltobalanceagainstriskyassets.Theprincipalaimoftheanalysisistoidentifythepotentialforastationarystateeconomy,eveninthepresenceofdebt-basedmoney.Infact,itmaybenotedthattheFALSTAFFeconomyisalmostentirelyacreditmoneyeconomy.Nophysicalcashchangeshands,andtransactionsarealldeemedtobeelectronictransactionsthroughthebankaccountsoffirms,householdandgovernment(andthroughthereserveaccountofthecentralbank).Forthepurposesoftestingtheroleofcreditcreationinthegrowthimperative,thissimplificationisclearlyrobust.Wehavealsoincorporated

24|P a g e

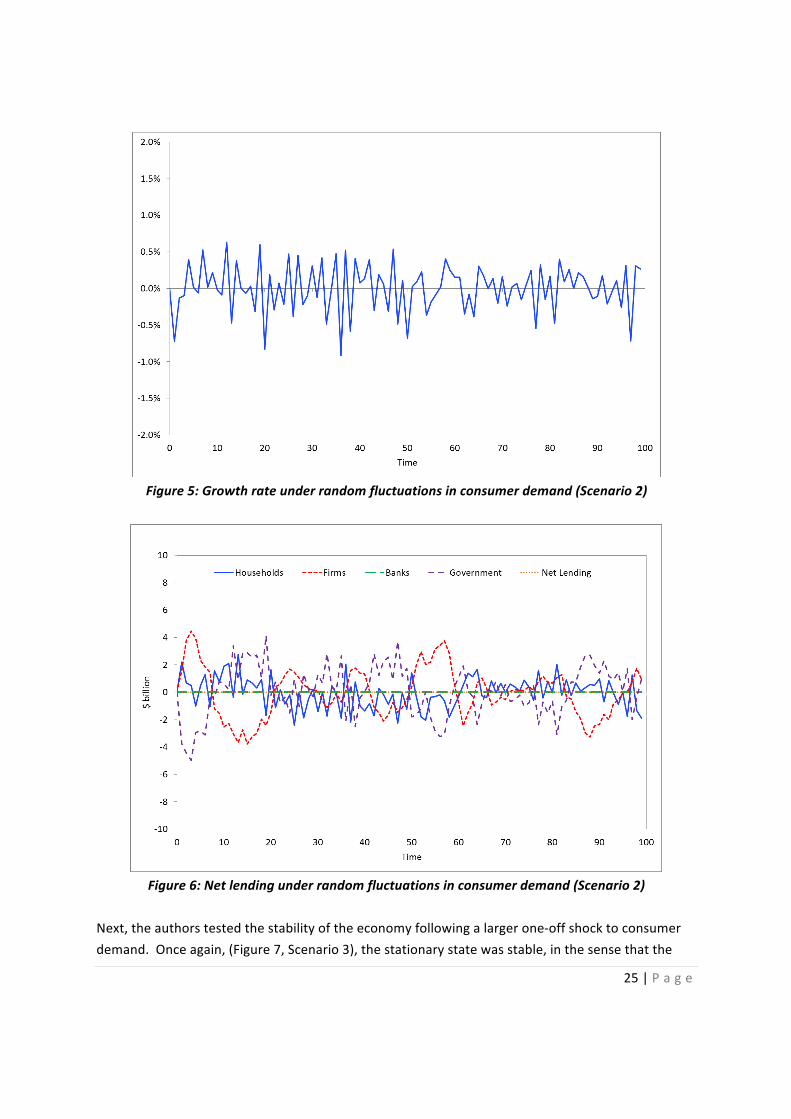

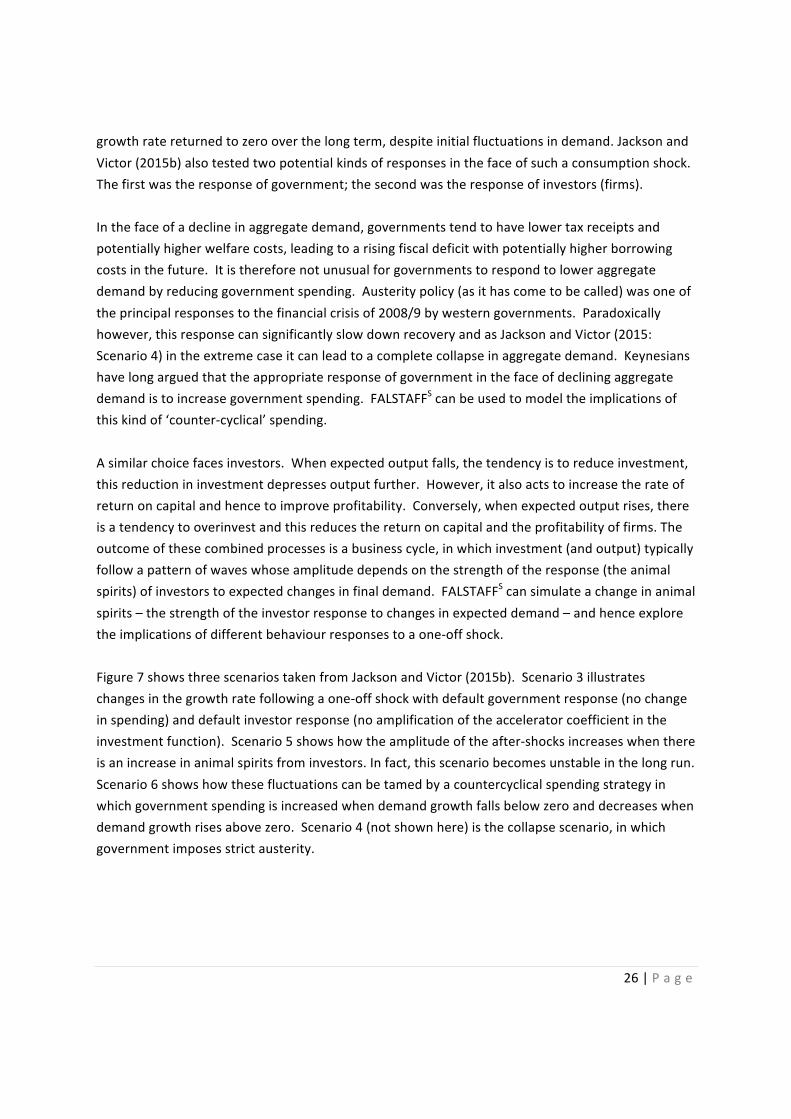

conditionsoncommercialbanksappropriateforthetestingoftheoverallhypothesisthatinterest-bearingdebtleadstogrowth.TheresultsoftheanalysisarediscussedindetailinJacksonandVictor(2015b)wheretheauthorspresentavarietyofscenarios,thefirstofthesedemonstratesclearlythepotentialforastationarystate:insuchascenario(whichwastestedunderarangeofvaluesfortheinterestrateondeposits,loansandgovernmentbonds)therearenochangesinanyoftherealeconomyaggregates,netlendingiszeroacrossallsectorsandtherearenochangesinthestocksofassetsandliabilities.Thoughnotparticularlyrepresentativeofaneconomyintherealworld,thissolutiondoeshoweverrefutethe‘growthimperative’hypothesis.Severalsensitivityanalyseswerethencarriedouttotesttherobustnessofthisfinding.First,theauthorsintroducedarandomvariationinconsumerdemandtotestwhetherthestationarystatewasstable.Figures5and6illustratetheresultsofthisanalysis.AlthoughFigure5showsconsiderablevariationintheshorttermgrowthrate(withinarangeoflessthan±1%)itisclearthatthelong-rungrowthrateisstillaroundzero.Certainlythereisnoobvioussystematicexpansionoftheeconomy,eventhoughthenetlendingpositionsofthedifferentsectors(Figure6)varyconsiderablyovertherun.Again,variationsindeposit,loan,andbondrates,andinthecapitaladequacyrequirementandthereserveratiomakenoappreciabledifferencetothislong-termtrend,orindeedtotheamplitudeofthevariationsaroundit.WecoulddescribetheeconomyillustratedinFigures5and6asaquasi-stationary-stateeconomywithalong-runaveragegrowthrateofzero.Noticethatthesumofnetlending,remainszeroacrosstherun,inspiteofthevariationinnetlendinginindividualsectors.Thisisanindicationthatthemodelisworkingconsistently,andreflectingcorrectlytheaccountingidentitiesthatmustholdinanyrealeconomy.Thoughthepatternlooksratherdramatic,noticethattheamplitudeofthevariationsinnetlendingisnothigh–lessthan0.5%oftheGDPinmostcases.

25|P a g e

Figure5:Growthrateunderrandomfluctuationsinconsumerdemand(Scenario2)

Figure6:Netlendingunderrandomfluctuationsinconsumerdemand(Scenario2)

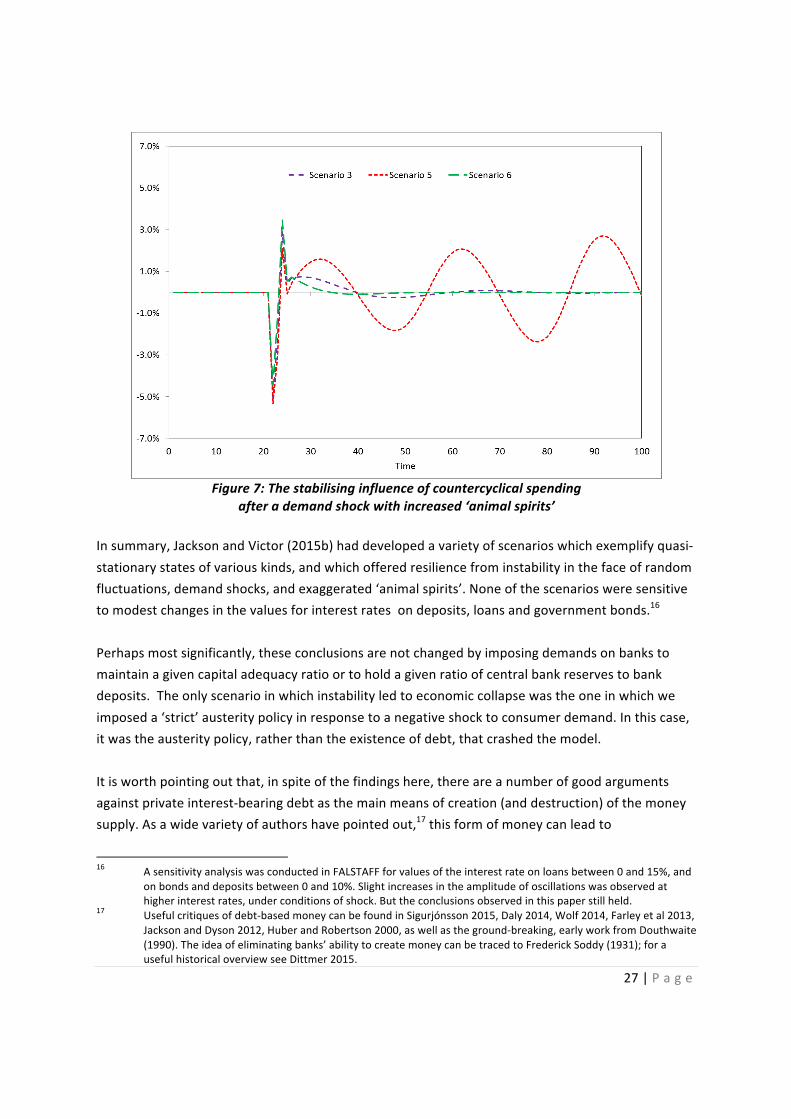

Next,theauthorstestedthestabilityoftheeconomyfollowingalargerone-offshocktoconsumerdemand.Onceagain,(Figure7,Scenario3),thestationarystatewasstable,inthesensethatthe

26|P a g e

growthratereturnedtozerooverthelongterm,despiteinitialfluctuationsindemand.JacksonandVictor(2015b)alsotestedtwopotentialkindsofresponsesinthefaceofsuchaconsumptionshock.Thefirstwastheresponseofgovernment;thesecondwastheresponseofinvestors(firms).Inthefaceofadeclineinaggregatedemand,governmentstendtohavelowertaxreceiptsandpotentiallyhigherwelfarecosts,leadingtoarisingfiscaldeficitwithpotentiallyhigherborrowingcostsinthefuture.Itisthereforenotunusualforgovernmentstorespondtoloweraggregatedemandbyreducinggovernmentspending.Austeritypolicy(asithascometobecalled)wasoneoftheprincipalresponsestothefinancialcrisisof2008/9bywesterngovernments.Paradoxicallyhowever,thisresponsecansignificantlyslowdownrecoveryandasJacksonandVictor(2015:Scenario4)intheextremecaseitcanleadtoacompletecollapseinaggregatedemand.Keynesianshavelongarguedthattheappropriateresponseofgovernmentinthefaceofdecliningaggregatedemandistoincreasegovernmentspending.FALSTAFFScanbeusedtomodeltheimplicationsofthiskindof‘counter-cyclical’spending.Asimilarchoicefacesinvestors.Whenexpectedoutputfalls,thetendencyistoreduceinvestment,thisreductionininvestmentdepressesoutputfurther.However,italsoactstoincreasetherateofreturnoncapitalandhencetoimproveprofitability.Conversely,whenexpectedoutputrises,thereisatendencytooverinvestandthisreducesthereturnoncapitalandtheprofitabilityoffirms.Theoutcomeofthesecombinedprocessesisabusinesscycle,inwhichinvestment(andoutput)typicallyfollowapatternofwaveswhoseamplitudedependsonthestrengthoftheresponse(theanimalspirits)ofinvestorstoexpectedchangesinfinaldemand.FALSTAFFScansimulateachangeinanimalspirits–thestrengthoftheinvestorresponsetochangesinexpecteddemand–andhenceexploretheimplicationsofdifferentbehaviourresponsestoaone-offshock.Figure7showsthreescenariostakenfromJacksonandVictor(2015b).Scenario3illustrateschangesinthegrowthratefollowingaone-offshockwithdefaultgovernmentresponse(nochangeinspending)anddefaultinvestorresponse(noamplificationoftheacceleratorcoefficientintheinvestmentfunction).Scenario5showshowtheamplitudeoftheafter-shocksincreaseswhenthereisanincreaseinanimalspiritsfrominvestors.Infact,thisscenariobecomesunstableinthelongrun.Scenario6showshowthesefluctuationscanbetamedbyacountercyclicalspendingstrategyinwhichgovernmentspendingisincreasedwhendemandgrowthfallsbelowzeroanddecreaseswhendemandgrowthrisesabovezero.Scenario4(notshownhere)isthecollapsescenario,inwhichgovernmentimposesstrictausterity.

27|P a g e

Figure7:Thestabilisinginfluenceofcountercyclicalspending

afterademandshockwithincreased‘animalspirits’Insummary,JacksonandVictor(2015b)haddevelopedavarietyofscenarioswhichexemplifyquasi-stationarystatesofvariouskinds,andwhichofferedresiliencefrominstabilityinthefaceofrandomfluctuations,demandshocks,andexaggerated‘animalspirits’.Noneofthescenariosweresensitivetomodestchangesinthevaluesforinterestratesondeposits,loansandgovernmentbonds.16Perhapsmostsignificantly,theseconclusionsarenotchangedbyimposingdemandsonbankstomaintainagivencapitaladequacyratioortoholdagivenratioofcentralbankreservestobankdeposits.Theonlyscenarioinwhichinstabilityledtoeconomiccollapsewastheoneinwhichweimposeda‘strict’austeritypolicyinresponsetoanegativeshocktoconsumerdemand.Inthiscase,itwastheausteritypolicy,ratherthantheexistenceofdebt,thatcrashedthemodel.Itisworthpointingoutthat,inspiteofthefindingshere,thereareanumberofgoodargumentsagainstprivateinterest-bearingdebtasthemainmeansofcreation(anddestruction)ofthemoneysupply.Asawidevarietyofauthorshavepointedout,17thisformofmoneycanleadto

16 AsensitivityanalysiswasconductedinFALSTAFFforvaluesoftheinterestrateonloansbetween0and15%,and

onbondsanddepositsbetween0and10%.Slightincreasesintheamplitudeofoscillationswasobservedathigherinterestrates,underconditionsofshock.Buttheconclusionsobservedinthispaperstillheld.

17 Usefulcritiquesofdebt-basedmoneycanbefoundinSigurjónsson2015,Daly2014,Wolf2014,Farleyetal2013,JacksonandDyson2012,HuberandRobertson2000,aswellastheground-breaking,earlyworkfromDouthwaite(1990).Theideaofeliminatingbanks’abilitytocreatemoneycanbetracedtoFrederickSoddy(1931);forausefulhistoricaloverviewseeDittmer2015.

28|P a g e

unsustainablelevelsofpublicandprivatedebt,increasedpriceandfiscalinstability,speculativebehaviourinrelationtoenvironmentalresources,greaterinequalityinincomesandinwealth,andalossofsovereigncontrolofthemoneysystem.Wearethereforefirmlyoftheopinionthatmonetaryreformisanessentialcomponentofasustainableeconomy.Weregardthecurrentstudyasanimportantwayofdistinguishingwhereeffortshouldbeplacedintransformingthissystem.Specifically,theresultsinthispapersuggestthatitisnotnecessarytoeliminateinterest-bearingdebtperse,ifthegoalistoachievearesilient,stationaryorquasi-stationarystateoftheeconomy.Itisalsoworthreiteratingthat,asidefromthequestionofinterest-bearingmoney,thereexistsanumberofotherincentivestowardsgrowthwithinthearchitectureofthecapitalisteconomy.Wehaveelucidatedsomeoftheseincentiveselsewhere(Jackson2009,Victor2008,JacksonandVictor2011).Theymustbetakentoinclude,forinstance:profitmaximisation(andinparticularthepursuitoflabourproductivitygrowth)byfirms,assetpricespeculationandconsumeraspirationsforincreasedincomeandwealth.Someofthesemechanismsalsoleadtopotentialinstabilitiesinthecapitalisteconomy.Manyofthemarereliantontheexistenceofcredit-basedmoneysystems.Minsky(1994),perhapsmostfamously,hasshownhowcyclesofinvestmentandspeculation,builtarounddebt-basedmoney,canleadtoendemicinstability.Butthislogicdoesnotentailthatinterest-bearingmoney,inandofitself,createsagrowthimperative.

29|P a g e

6 FALSTAFFPart2:GreenInvestmentandPortfolioAllocation

InadditiontotheworkdescribedinSection5,theFALSTAFFframeworkhasbeenusedtoillustratetheimportanceofassessingbothrealandfinancialaspectsofthetransitiontoalow-carboneconomy.IllustrativeresultsfromanexpandedversionofthemodelwerepresentedataworkshopconvenedbytheUNEPFinanceInitiativeinWaterloo,CanadainDecember2014(JacksonandVictor2015c).TheWaterlooversionofFALSTAFF–denotedhereasFALSTAFFWforeaseofreference-includedseveraladditionsandvariationstothemodeldescribedintheprevioussection.Thesecomprised:aneconometricallyestimatedinvestmentfunction,aneconometricallyestimatedportfolioallocationmodeltodescribehouseholdssavingsbehaviour,anadditionalsectortoaccountfortrade(andcapitaltransactions)withtherestoftheworld,andanexpandedbalancesheetincludingdebt,equity,bonds,housing,mortgages,loansandpensionfunds.InthissectionweprovideanoverviewofthestructureoftheexpandedFALSTAFFWmodelandpresentsomeoftheillustrativeresultspresentedattheWaterloomeeting.HouseholdsmakethreekindsofdecisionsinFALSTAFFW.Firsttheydecidehowmuchtospendandhowmuchtosave.Second,theydecidehowmuchtoinvestinfixedcapitalassets(housing).Finallytheydecidehowtoallocatesavings/borrowingtodifferentassetclasses.Inrelationtothefirstdecision,themodelallowstheusertochoosebetweenasimplesavingsratiobasedonaproportionofdisposableincome,oramoresophisticatedconsumptionfunctionoftheformfavouredbypost-KeynesianSFCtheorists,inwhichhouseholdconsumptionCisgivenbyafunctionoftheform: 𝐶 = 𝛼!𝑌!"#$ + 𝛼!𝑁𝑊! 5)

whereYdispisthedisposableincomeofhouseholdsandNWhistheirnetworth.Thisformofconsumptionfunctionthusincorporatesbothpropensitiestoconsumefromdisposableincomeandalsopropensitiestoconsumefromhouseholdwealth(asdoesthemodelinSection5).Inthelongrunthisdependencyofconsumptiononhouseholdwealthprovidesalinkbetweenbehaviourintherealeconomyandthehealthofthefinancialeconomy(GodleyandLavoie,2007),althoughitshouldbenotedthatthesefeedbacksaremuchslowerthanthoseprovidedviastock-marketsignalsonconsumerconfidence,forinstance.Valuesforα1andα2wereestimatedusingquarterlynationalaccountsdatabetween1991and2013,publishedbyforCanadabyStatisticsCanadaandfortheUKbytheOfficeforNationalStatistics.18

18 TheStatCandatabase(http://www5.statcan.gc.ca/cansim/)isoneofthemostuser-friendlynationalaccounts

databasesofanycountryintheworldandoneofthereasonswedecidedtocalibrateFALSTAFFfirstagainstCanadiandata.

30|P a g e

HousinginvestmentinFALSTAFFWisdrivenpartlybypopulationgrowth,19andpartlybyanexogenouslydefinedhousinggrowthparametertoreflectchangesinhouseholdsizeandcomposition.Thepriceofhousingisdeterminedbythebalancebetweensupplyofhousing(investment)andthedesireforhousing,whichflowsfromhouseholdssavingsdecision.ThesesavingsdecisionsareakeyelementintheestablishmentofSFCmonetaryflowsandaremodelledinFALSTAFFWusinganeconometricallyestimatedPortfolioAllocationModulebasedonaframeworkoriginallydevelopedbyBrainardandTobin(1968)–partoftheworkforwhichTobinlaterreceivedaNobelprize.Theapproachwaslateradopted(andadapted)byGodleyandLavoie(2007)asakeyelementwithinapost-KeynesianSFCapproach.Thebroadthrustoftheapproachistosupposethatthedesiredholdingsofaparticularassetdependbothontherateofreturnonthatassetandalsoontheratesofreturn(orinterestrates)onotherassets(orliabilities).Soforexample,iftherateofreturnonequitiesrises(orisexpectedtorise),householdstendtoallocatemoreoftheirsavingstoequitiesthan,say,governmentbonds.Converselyifthereturnonequityfalls(orisexpectedtofall),householdswouldtendtosellequitiesinfavourofsomeotherasset.Thereareseveraldistinctwaysofrepresentingthiskindofallocationprocess.Forexample,onecanproceed(seeGodleyandLavoie,2007)bydeterminingforeachassetAiatargetproportionofhouseholdnetworth,𝑎!!,occupiedbythatasset,givenby:

𝑎!! = 𝜆!! + 𝜆!"𝑟!! + 𝜆!!!!!!"

6)

wheretherjaretheratesofreturn(orinterest)onthevariousassets(orliabilities)andtheλijareconstantcoefficients,tobederivedfroma(constrained)econometricanalysisofpasttrends.20InthisversionofFALSTAFF,weestimatethesetargetproportionsusingdataforsevendistinctasset/liabilityclasses:deposits,bonds,equities,housingwealth,mortgages,loansandpensions.WhenweestimatedtheserelationshipsusingtheeconometricsoftwareEviewsandquarterlyfinancialaccountsdataforCanadaandtheUKfrom1991to2013,wefoundahighdegreeofdependencyon𝑎!!(−1),thefirstlagof𝑎!!.Inotherwords,itseemsasthoughhouseholds’portfolioallocationsarerelatively“sticky”onaggregate.Toimprovetheestimationwemadetwochangestoequation6).ThefirstwastouseYddirectlyratherthantheratioYd/NWasadependentvariableontherighthandsideoftheequation.Thesecondwastoincludethelaggedvariable𝑎!(−1)–theactualvalueofassetAiasaproportionofnetworthinthepreviousperiod–asanadditional

19Weassumeanexogenouslyvariable0.5%annualgrowthrateforpopulation.20Inorderforthisproceduretoworkcorrectly,itshouldbenotedthatliabilities(mortgagesandloans)mustbecountedina

negativesensewithintheframework.

31|P a g e

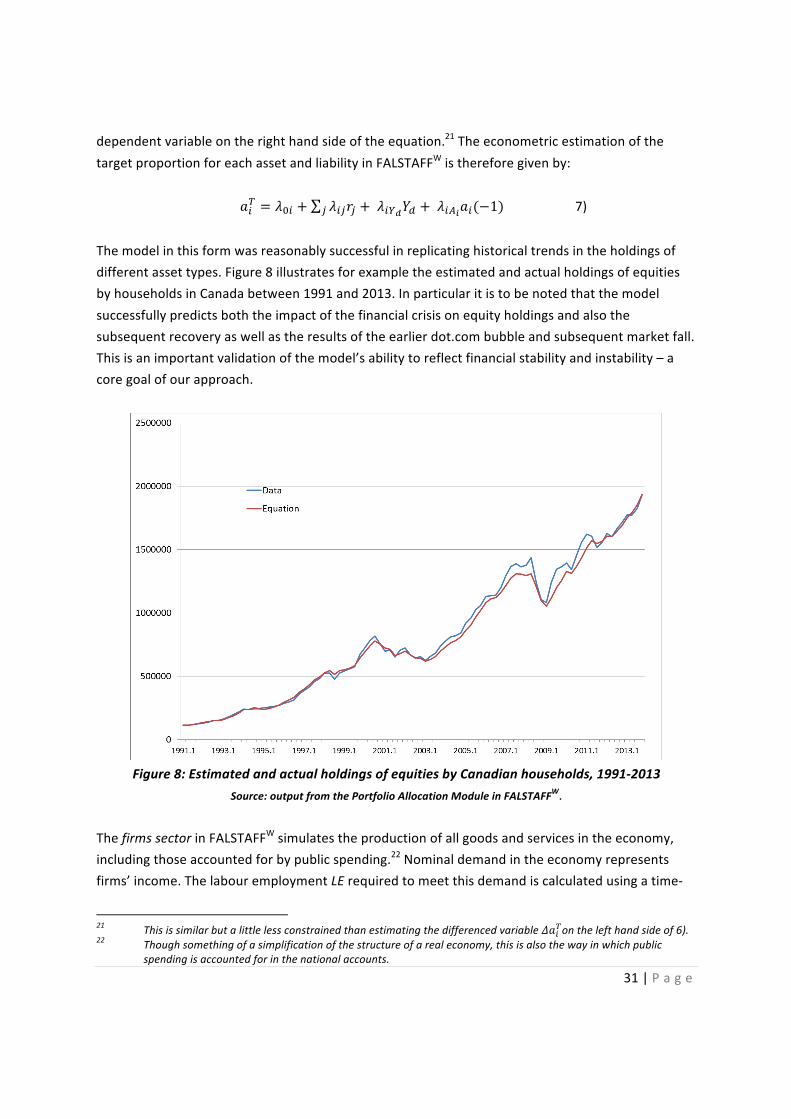

dependentvariableontherighthandsideoftheequation.21TheeconometricestimationofthetargetproportionforeachassetandliabilityinFALSTAFFWisthereforegivenby: 𝑎!! = 𝜆!! + 𝜆!"𝑟!! + 𝜆!!!𝑌! + 𝜆!!!𝑎!(−1) 7)

Themodelinthisformwasreasonablysuccessfulinreplicatinghistoricaltrendsintheholdingsofdifferentassettypes.Figure8illustratesforexampletheestimatedandactualholdingsofequitiesbyhouseholdsinCanadabetween1991and2013.Inparticularitistobenotedthatthemodelsuccessfullypredictsboththeimpactofthefinancialcrisisonequityholdingsandalsothesubsequentrecoveryaswellastheresultsoftheearlierdot.combubbleandsubsequentmarketfall.Thisisanimportantvalidationofthemodel’sabilitytoreflectfinancialstabilityandinstability–acoregoalofourapproach.

Figure8:EstimatedandactualholdingsofequitiesbyCanadianhouseholds,1991-2013

Source:outputfromthePortfolioAllocationModuleinFALSTAFFW.ThefirmssectorinFALSTAFFWsimulatestheproductionofallgoodsandservicesintheeconomy,includingthoseaccountedforbypublicspending.22Nominaldemandintheeconomyrepresentsfirms’income.ThelabouremploymentLErequiredtomeetthisdemandiscalculatedusingatime-

21 Thisissimilarbutalittlelessconstrainedthanestimatingthedifferencedvariable𝛥𝑎!!onthelefthandsideof6).22 Thoughsomethingofasimplificationofthestructureofarealeconomy,thisisalsothewayinwhichpublic

spendingisaccountedforinthenationalaccounts.

32|P a g e

varyinglabourproductivityfunctionLPwhichvariesovertimeaccordingtoaneconometricallyestimatedreallabourproductivitygrowthrate,lpgaccordingto: 𝐿𝑃 = 𝐿𝑃!(1 + 𝑙𝑝𝑔)!!!"#! 8a)

𝐿𝐸 = !"#!"#!.!"

8b)

wherepispriceandGDPnomisthenominaldemand.Itshouldbeclearthatnominaldemandcannotalwaysbemetbydomesticproduction,particularlygiventhatlabourisconstrainedbytheavailablelabourforcewhichthereforedeterminesasupplyconstraintonthedomesticeconomy.Firms’costsincludetaxesonproductionandonproducts(determinedinthegovernmentsector),interestpaymentsonloans,andwages.Thewagebilliscalculatedviaatime-varyingwagerateWRwhichalsodeterminespriceinthemodel.Twofactorsaredeemedtochangethewagerateinthemodel.Initiallyweassumethatlabourproductivityimprovementsarepassedontoworkers,sothattheunadjustedwagerateWRisgivenby:

𝑊𝑅 = 𝑊𝑅!(1 + 𝑙𝑝𝑔)!!!"#! 9)AninflationadjustedwagerateWR’isthenestimatedbyusingasimplifiedPhillipscurvethatinflatesthewageratewhenunemploymentislowanddeflatesitwhenunemploymentishigh.23ThepriceofdomesticallyproducedgoodsinthemodelisdeterminedbytheratiooftheinflationadjustedwagerateWR’totheunadjustedwagerateWR.FirmshavetomakethreeotherkindsofdecisionsinFALSTAFFW:howmuchoftheirnetprofitsFtodistributeasdividends;howmuchtoinvestinproduction;andhowtofinancethisinvestment.ThedividenddistributionFDcanbedecidedeitherviaanexogenouslydetermined“retainedearningsratio”orelsethroughanequationoftheform:

𝐹! = 𝐹! −1 + 𝜂𝐹(−1) 10)whereF(-1)denotesprofitsinthepreviousperiod(i.e.thefirstlagofprofits)andηisaneconometricallyestimatedcoefficient.Theinvestmentdecisionisdeterminedintwoparts.Oneofourintentionsinthemodelistobeabletounderstandtheimplicationsofgreeninvestmentontheperformanceoftheeconomy.Wethereforeseparatefirms’investmentintoaconventionalcomponent,predictedeconometricallyin

23 OurPhillipscurveissimilartotheoneusedbyKeen(2011)withaflatsectionaroundnormalemploymentrates,a

risingadjustmentforlowunemployment,adeclining(butflatter)lineformediumunemploymentandaflatdownwardsadjustmentofthewageforhighunemployment.

33|P a g e

themodelandagreencomponentwhichisdeterminedexogenously.Fortheconventionalcomponent,weuseaninvestmentfunctionproposedbyLavoieandGodley(2001).Firms’investmentIisestimatedwithacapitalaccumulationrategwhichisdeemedtobedependentontherateofcashflowrcf(calculatedfromtheratioofretainedearningstocapital),therateofinterestrLfonfirmsloans(moderatedbyaleverageratio,l),Tobin’sqratio24andtheraterCUofcapacityutilisation: 𝑔 = 𝛾!𝑟!" + 𝛾!𝑟!"𝑙 + 𝛾!𝑞 + 𝛾!𝑟!" 11)

Broadlyspeaking,thisfunctionmeansthatconventionalinvestmentisexpectedtoincreasewithincreasingcashflow,todeclinewithincreasinginterestrates,toriseasTobin’sqrises(becausethevalueofequityishighinrelationtocapital),andtoincreasewiththecapacityutilisationrate.Thislastfactorreflectstheimpactofrisingdemandoninvestment.Asdemandrises,sparecapacitydiminishes,encouragingnewinvestment.Conventionalinvestmentisthengivenby: 𝐼 = 𝑔𝐾!(−1) 11)

WhereKf(-1)isthelagoffirms’productivecapitalstockKf.AlthoughtheinvestmentinproductivecapitalstockisendogenousinFALSTAFFW,greeninvestmentisdeterminedexogenously.Itisassumedfirstthatoverthecourseoftherun,arisingproportionofGDP(startingfromzero)willbeallocatedtogreeninvestment.Theuserdecidesonthefinaltargetproportionandalsoselectsthesectorsinwhichthisinvestmentismade(firms,housing,government).Themodelthencalculatesthegreeninvestmentineachsectorovereachyearoftherunassumingthesameproportionsofgreeninvestmentineachsectoraspredictedforconventionalinvestment.Theimpactontheeconomyofthisgreeninvestmentdependsontwofurtherparameters.Thefirstistheextenttowhichitisdeemedtobeadditionaltoorsimplytosubstituteforpredictedinvestment.Thesecondistheextenttowhichbothadditionalandnonadditionalgreeninvestmentsareproductive–inthesensethattheyaddtotheproductivestockoftheeconomy.25Bothoftheseparameterscanbeselectedbytheuser.Thedefaultpositionassumesthatgreeninvestmentswillbenon-additional,sothattherewillbeagradualshiftawayfrom“browninvestment”towardsgreeninvestmentwithinthesameinvestmentarchitecturepredictedbythemodel.Itshouldbenotedthatproductiveadditionalinvestmentaddstotheproductivecapacityoftheeconomy,whereasnon-productive,non-additionalinvestmentssubtractfromtheproductivecapacityoftheeconomy.Non-productive,additionalinvestmentsaddtonominaldemandinthe24 Tobin’sq(firstproposedbyNobelLaureateJamesTobin)isaparameterthatmeasurestheratioofthevalueof

equitytothevalueofthecapitalstock.25 Weusetheterm“productive”hereintheratherconventionalsensethatanincreaseintheproductivecapital

stockincreasestheimmediatecapacityoftheeconomytoproducegoodsandservices.Clearly,thisdoesnotalwayscoincidewiththelong-termsustainabilityofthatproduction,whichmightbebetterprotectedbytheso-called“non-productive”investmentsdesignedtoprotectenvironmentalresources.

34|P a g e

economy,butdonotchangetheproductivecapitalstock.Themodelaccountsseparatelyfornon-productivecapitalstocks.Thefinancialandmonetaryimportanceofthisdistinctionconcernsthesupplyconstraintsondomesticproductionofgoodsandservices.Justassupplyissometimesconstrainedbyavailablelabour,itmayalsobeconstrainedbyavailablecapital.Weassumehereaconstantcapitaloutputratio(calibratedagainsthistoricaldata)todetermineafurtherlimitonmaximumreal(andhencenominal)demandsuppliedbythedomesticeconomy.TheoveralllimitonGDPisthentheminimumofthemaximadeterminedthroughlabourandthroughcapitalconstraints.Oncesupplyconstraintsarereached,additionalnominaldemandcreatedbytheexogenousinvestmentstrategycanonlybemetintwoways:firstbyincreasingimportedfinaldemandfromtheoverseassector;orintheabsenceofthispossibilitybyanincreaseinprices.BothavenueswouldtendtodepressrealGDPgrowth.Thefinaldecisiontobemadebyfirmsishowtofinancetheoverallinvestmentneeds(includingbothconventionalandgreeninvestments).InFALSTAFF,firmsinvestmentscanbefundedthroughretainedearnings(profitsminusdividends),throughissuingnewequitiesandthroughtakingoutnewbankloans.Oncefirms’retainedearningsareexhaustedweassumethatadditionalfinancingneedsaremetthroughamixtureofloansandequitiesaccordingtoanexogenouslyvariabledebttoequityratio,whichismoderatedtosome(variable)degreebytherateofinterestonfirms’loans.26ThebankssectorinFALSTAFFisasimplifiedaccountingsectorwithtwomainfunctions.Itsprofitandlossaccountsimplycollatestheinterestpaymentsonloans(includinghouseholdmortgages)andpaysouttheinterestdueondeposits.Grossprofitsarethedifferencebetweenthesetwo.27Bankspaytaxestothegovernmentontheseearningsandnetprofitsaredividedbetweenretainedearningsanddividends.Banks’dividendsarecalculatedasaresidual.Retainedearningsdecisionsdependonthefinancingrequirementsofbanks,whichareintheirturndependonwhatishappeninginthecapitalaccount.ThisisthesecondfunctionallocatedtobanksinFALSTAFFandrelatestotheprovisionofcapitalfacilities(depositsandloans)forothersectors.Therearetwomaincapitalaccountdecisionstobemadebybanks.Thefirstishowmuchmoneytoholdasreserveswiththecentralbank.Forthepurposesofthisversionofthemodel,thisisallocatedthroughanexogenouslyvariablereserveratio,withadefaultvalueinwhichreservesconstitute1%ofdepositsheldwiththebank.Theseconddecisioninvolvesbankscapitaladequacyrequirements.

26 Currentlythismoderationofthedebttoequityratioisdeterminedbyasmallexogenouslysetadjustmenttothe

debttoequitypreference.Infuturedevelopmentswewilllookforwaystoendogenizethedebttoequityratiofurthertodependonmarketconditions.

27 Wedonot,forinstance,includebankswagesinthebankingsector.Theyareassumedtobeaccountedforviathefirmssector.

35|P a g e

BaselIIIrequiresbankstoholdaminimumof8%oftheirrisk-adjustedcapitalintheformofrisk-freecapital.Weinterpretthisrequirementtomeanthatthesumofbanksreservesplustheirholdingsofsovereignbondsmustbe8%oftheirtotalprivatesectorlending.28Thiscapitaladequacyrequirementthendeterminesbanksneedforgovernmentbonds,andalso(inconjunctionwiththechangesindepositsandlending)determinestheirneedforretainedearnings.Specifically,thetransactionmatrixrevealsthatbanks’undistributedprofitsFUfaregivenby:

𝐹𝑈! = 𝛥𝐷 + 𝛥𝑃 − 𝛥𝐿 − 𝛥𝑀 − 𝛥𝑅 − 𝛥𝐵 12)

WhereDrepresentsdeposits,Pispensions,Lisloanstohouseholdsandfirms,Mismortgagesagainstpropertypurchases,RiscentralbankreservesandBisgovernmentbonds.Intheeventthatthisfundingrequirementexceedstotalnetprofits,bankscanalsomeettheirfundingrequirementbytakingoutloans(advances)fromthecentralbank.ThegovernmentsectorinFALSTAFFWallowsforavarietyofgovernmentspendingstrategiesandsetsthetaxratesonhouseholdincome,firms’incomeand(indirectly)onproducts.SpendingdecisionsbythegovernmentcanbedeterminedinthreeseparateModesinthemodel.InMode1,asimpleexogenouslyvariedgrowthrateisappliedtobothconsumptionspendingandinvestmentspending.Thedefaultvalueinthebaserun(describedinmoredetailinthenextsection)is2%perannum.InMode2,thegovernmentcanoperateabalancedbudgetpolicyinwhichspendingisstrictlyconstrainedbytaxreceipts.Finally,inMode3,itcanoperateacounter-cyclicaladjustmenttotheexogenousgrowthrateinwhichgovernmentspendingrises(byupto20%)ifunemploymentishighandfalls(byuptothesameamount)whenunemploymentislow.Ineachofthesemodes,itisalsoassumedthatgovernmentswilltendtoreducedeficits(orsurpluses)throughadjustmentstobothspendingandthetaxrates,whenthedebttoGDPratiorisesabove(orfallsbelow)certainlevels.GovernmentborrowingisfundedthroughtheissuanceofbondswhichareconceptualisedinFALSTAFFWassimpleloanswithanendogenouslyvaryinginterestrate.Threeothersectorscreateanendogenousdemandforloans.Householdspurchasebondsinresponsetotheirassetallocationpreferences(equation4)above).Banksholdbondsinordertomeettheircapitaladequacyrequirements.Centralbanksholdbonds(seebelow)inexchangeforliquidityprovidedtocommercialbanksintheformofreserves.Thegapbetweenthesupplyofbonds(governmentborrowing)andthedemandforbondsisassumedtobemetbybondpurchases/salesfromtheforeignsector.29

28 Sovereignbondsaretypicallyratedatzerorisk.Thehistoricaldatasupportacloseto8%capitaladequacyratioin

Canada.Thisratecanbevariedinthemodel.29 Amoresophisticatedendogenizationofthepriceofbondsthroughcapitalgains/losses(iechangesinbondyields)

isunderdevelopment.

36|P a g e