Towards a New Paradigm for Monetary Economics Bank Negara January, 2005 Joseph E. Stiglitz

Towards a New Paradigm for Monetary Economics Bank Negara January, 2005 Joseph E. Stiglitz.

Dec 28, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Towards a New Paradigm for Monetary Economics

Bank Negara

January, 2005

Joseph E. Stiglitz

Outline

1. Failure of Traditional Monetary Theory

2. Financial Markets Differ from Ordinary Markets

3. Modeling an Ideal Competitive Banking System

4. Differences Between Ideal and Current

5. Applications of the New Paradigm

Failings of the Traditional Theory of Money

1. Because of new technologies, “money” is interest bearing, with differences between t-bill rate & “CMA” accounts rate small (determined by transactions costs, unrelated to economic activity)

• 2. With new technologies, money is not required for transactions—only credit

• 3. Most transactions not income generating—simply exchanges of assets; ratio of exchange of assets to income is not stable

4. Velocity has not been stable, relatively little of the changes in velocity are explained by changes in interest rates

5. Real Interest Rate Does Not Seem to Play Pivotal Role Assumed by Theory:

A. For many investment regressions, nominal interest rates, instead of, or as well as, real interest rates matter

In recent U.S. recession, major effect was through mortgage refinancing, spurring consumption boom

B. For long periods of time, real interest rate did not vary much at all; can’t explain economic

variability by a constant

• For long term investments, it is long term interest rate that should matter; But then why should changes in monetary conditions today have significant effect on long term interest rate?

6. Hard to Reconcile Cyclical Movements in Real Interest Rates with Standard Theories

In a recession, marginal productivity theory predicts, as labor input goes down, the

marginal productivity of capital decreases => real interest rate should decrease

Credit Should Be at the Center of Monetary Theory

1. Providing credit entails assessing credit-worthiness, ie. probability of repaying loan

2. Based on information

3. Information is highly specific and not easily transferable

4. Credit is not allocated by an auction market (to highest bidder)

5. There may be credit rationing– Because of adverse selection and incentive effects, increasing

interest rate beyond a certain level may lead to a reduction in expected return (i.e. Probability of default increases faster than nominal return)

Key to Understanding the Supply of Credit Is Understanding Bank Behavior1. Banks are firms that certify creditworthiness, screen and monitor

loan applicants

2. Issuing loans is risky, since there is probability of not being repaid

3. Banks, like other firms, act in a risk averse mannerA. “Constraints” in the issuance of equity imply limited ability to diversify out of risk

– Empirical evidence: firms finance little of new investment through issuing new equity

– When firms issue new equity, share price typically declines markedly

– Explained by theories of adverse selection and adverse incentives

IMPLICATIONS OF RISK AVERSE BANK

A. With equity constraints, if banks want to increase lending, they must borrow—fixed obligations, with uncertain returns

B. The more firms borrow, the higher the probability of bankruptcy

C. With significant costs of bankruptcy, banks will limit borrowing and lending—acting as if they are risk averse

Modeling an Ideal Competitive Banking System

• Government Insured Deposits

• Government Imposed Reserve Requirements, which Acts as a Tax on Deposits

• No Transactions Costs

• High Degree of Competition So

Deposit Rate = T-Bill Rate

The Bank’s Objectives

• There are two alternative ways of modeling bank behavior. They both yield similar results, namely, that the bank acts in a risk-averse manner

• The first is based on the assumption that the bank is risk neutral, provided it does not go bankrupt, but there is a high cost to bankruptcy, so it naturally wishes to avert bankruptcy.

• The second is based on the standard mean variance model

• They both yield the same basic result

Basic ModelBank maximizes expected value of terminal wealth

net of bankruptcy cost, i.e.Max E{at+1} – cF

Where at+1 = Max {Y + M(1 + ) - (1 + )(N + M + e – at) , 0}

Where

At = Wealth at Time T,

Y = Income,

c = Cost of Bankruptcy

F = Probability of Bankruptcy

N = Amount Lent

M = Amount Borrowed by the Bank

e = Expenditures on Screening

and Where

r1 = interest rate charged

Θ = state of the business cycle, representing the undiversifiable risk of the banks’ portfolio.

Without loss of generality, we assume that YΘ > 0.

Basic Model

and where

where

r1 = interest rate charged

Θ = state of the business cycle, representing the undiversifiable risk of the banks’ portfolio.

Without loss of generality, we assume that YΘ > 0.

e, ,r Y(N, Y 1

Basic Model

0,)a-eMτ)(Nρ(1-ρ)M(1Y t

the bank goes bankrupt if:

i.e., there exists a critical value of Θ, , such that the bank goes bankrupt if Θ , and not otherwise.

ˆ

Let be the probability that Θ , i.e., the probability that the bank goes bankrupt,

and let c be the cost of bankruptcy

(c will normally be a function of the scale of the bank; bankruptcy costs will be larger the larger the bank, e.g., measured by the value of assets or liabilities).

F ˆ

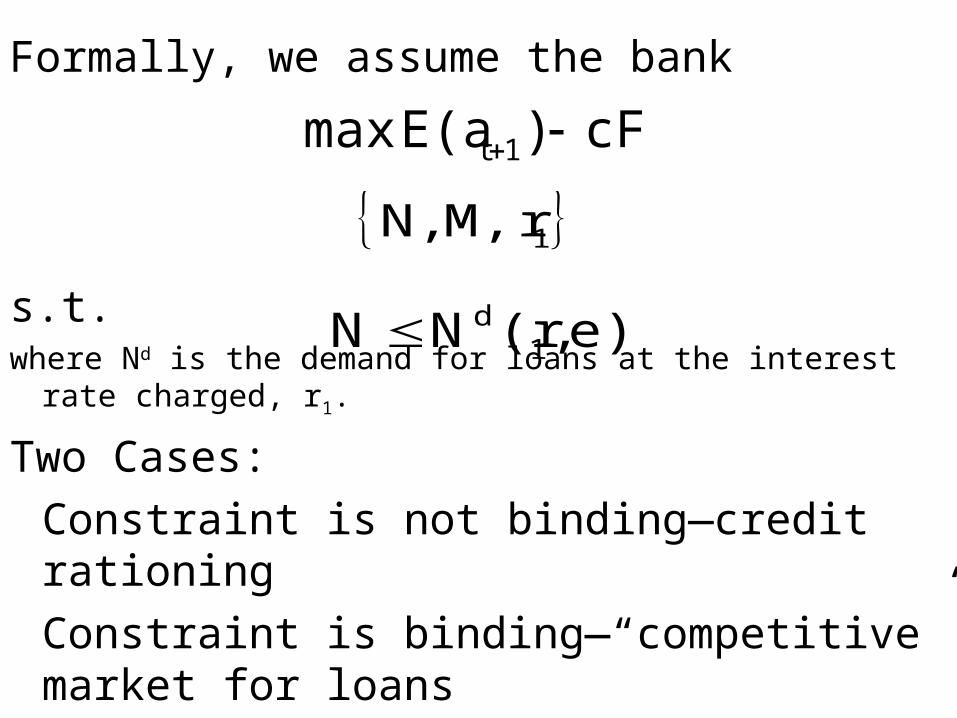

Formally, we assume the bank

s.t.where Nd is the demand for loans at the interest rate charged, r1.

Two Cases:

Constraint is not binding—credit rationing

Constraint is binding—“competitive” market for loans

cF)E(amax 1t

1rM,N,

e),,(rNN 1d

Alternative Formulation—Mean Variance

The Bank Maximizes

U = U(,)

where

and

for most of the analysis we assume constant returns, so that. . .

e) r, N,μμ

e) r, N,σσ

= N*(r,e)

= N*(r,e)

which in turn means thatY = N* + M - (1 + ) (N + M + e - at)

for N + M + e - at > 0

Y = N* + M

for N + M + e - at 0

and

Y = N*

Comparative Statics

• What happens if there is a decrease in bank net worth?

• What happens if there is an increase in the riskiness of the environment

Proposition 1. A Decrease in Bank’s Net Worth Leads to a Decrease in Bank Lending

Optimal behavior of bank is described by

ρEYN

where ø is the marginal bankruptcy cost

0.NcF/

under mild restrictions, it can be shown that

Implication: With lower net worth, marginal bankruptcy curve shifts up at any level of lending.

Implies a cut back in lending

0,a

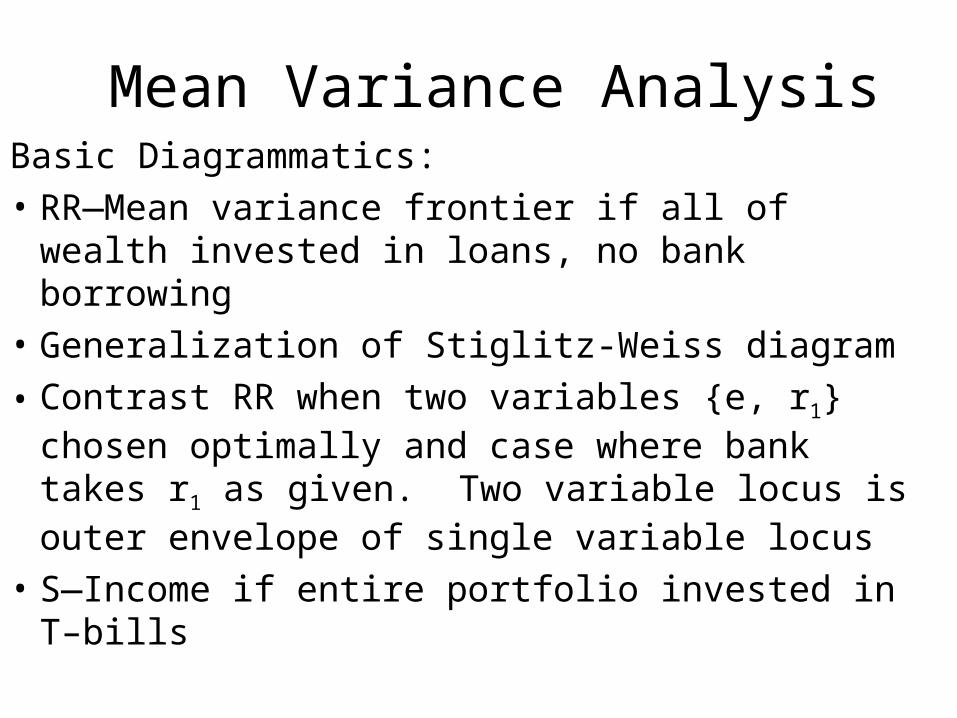

Mean Variance AnalysisBasic Diagrammatics:

• RR—Mean variance frontier if all of wealth invested in loans, no bank borrowing

• Generalization of Stiglitz-Weiss diagram

• Contrast RR when two variables {e, r1} chosen optimally and case where bank takes r1 as given. Two variable locus is outer envelope of single variable locus

• S—Income if entire portfolio invested in T–bills

• Total Portfolio—SPP’L

• SP—Mixture of T-Bills and loans

• PP’—All loan portfolio

• P’L—Bank borrows, putting extra proceeds (beyond “tax”) into risky assets (loans)

• Implication—When there is credit rationing, a risk averse bank chooses a lower interest rate than a risk neutral lender

• A bank that accepts deposits charges a higher interest rate than an “investment” bank (interest rate at P’ higher than at P)

• With lower wealth, entire opportunity locus shifts in proportionately.

• In central case, lending reduced proportionate to the reduction in wealth

• With decreasing relative risk aversion, reduction in lending somewhat smaller

Effect of an increase in uncertainty

• Proposition 2: a Mean Preserving Increase in Risk Reduces Lending Activity

• Implications:In a recession bank net worth declinesAnd risk increases, so supply of funds is reducedContributing to economic downturnCan lead to increase in spread between deposit rate

and lending rate

Policy analysis

• What is the effect of an increase in reserve requirements

• What is the effect of an increase in t bill rate

• What is the effect of a tightening of capital adequacy regulatons

Proposition 3: An Increase in Reserve Requirements Leads to Reduced Lending

Proposition 4: An Increase in the Rate of Interest on T-Bills Leads to Less Lending for Banks that Accept Deposits

Proposition 5. An increase in capital adequacy

requirements leads to less lending

Important point: prudential regulations have macro-economic effects

Reconstructing Standard Monetary Economics

• Models provide basis for a new “IS-LM” equilibrium analysis

• At each level of Y (national output) construct demand and supply curve for funds

Key Differences• Focus on lending rate

• Equilibrium lending rate may not equate demand and supply of funds (may be credit rationing)

• Need to solve simultaneously for deposit rate –interest rate spread (in IS curve, investment depends on lending rate, savings depends on deposit rate)

• Supply of funds depends not just on monetary stance, but on:

• Bank capital

• Firm capital (affects probability of default on loans, indirectly bank’s net worth)

• Major difference with standard model—LM curve stable over business cycle, IS curve shifts

• Here, LM curve shifts as well

• Implication: movements in real interest rates over cycle indeterminate

• Model suggests raising interest rates may have larger and more prolonged effects under certain circumstances than previously thought—destroys firm and bank capital

• Model explains why changes in nominal interest

rates matter, even when real interest rates do not

change, if loan contracts are not fully indexed

• Model suggests why changing the institutional

structure of the banking system—e.g. increasing

competition—may alter efficacy of monetary policy• Eliminates seignorage effects, with associated wealth effects

• Forces greater reliance on substitution effects

• Because of credit rationing, investment may be

affected even when interest rates are not.

Towards a General Equilibrium Theory of Credit

• Banks are at center of financial system

• But there are large credit interlinkages (trade credit)

• As important in transmitting disturbances throughout the economy as goods/services interlinkages

• Can give rise to credit crises

Applications of the New Paradigm

I. Monetary Policy

II. Regulatory Policy

III. Financial Market Liberalization

IV. Regional Downturns and Development and Monetary Policy

V. The East Asia Crisis

VI. The 1991 U.S. Recession and Recovery

VII. Concluding Remarks

I. Monetary Policy(i) What affects the level of economic activity is terms

at which credit is made available, and quantity of credit, not the quantity of money itself nor the interest rate on T-bills.

(ii) Relationship between the terms at which credit is available (e.g. the loan rate) and the T-bill (or deposit) rate may change markedly over time.

(iii) Similarly, the supply of credit may not change in tandem with the money supply; and changes in the relationship between money and credit may be particularly marked in periods of crisis further reason to reject monetarist approach

(iv) The terms and quantity at which credit is made available are determined by banks; their ability and willingness to lend are affected by the T-bill interest rate, but in ways which depend on economic conditions; changes in interest rates affect the net worth of the firm, and the opportunity set of the bank.

---in some extreme circumstances, there may even be a liquidity trap, in which easing of monetary policy has no significant effect on lending.

(v) - Monetary authorities can affect bank behavior not only through changes in the T-bill rate, but also by altering constraints (e.g. reserve requirements, capital adequacy standards) and incentives;

- impacts on bank behavior are likely to be greater when constraints (e.g. reserve requirements) are binding than when they are not (there is “excess liquidity”);

(vi) Monetary policy affects economic activity not only through its effect on demand (e.g. for investment) but also on supply (e.g. when there is credit rationing, it is impacts on the supply of credit that matter);

- impacts on aggregate supply and on aggregate demand are often intertwined.

(vii)While the immediate impact of monetary policy is typically on the banking system, its full effects are distributed through the economy as a result of the network of credit interlinkages.

(viii)Changes in interest rates can affect the economy through many channels, - a reduction of interest rates can lead to mortgage refinancing stimulating consumption (this may be very institutional specific)

– An increase in the interest rate (T bill) reduces the value of the bank’s assets, both directly, and indirectly, through increased probability of default of the loans, with potentially severe consequences, especially if there is a mismatch between maturity of assets and liabilities. The supply of loans will be affected

--Adverse effects of interest rate increase on lending increased by uncertainty--effects on any particular firm, bank may be uncertain

• Leads to reduced supply of lending

• Effects are likely to be persistent, i.e. last long after interest rates are lowered

(ix)Changes in institutional arrangements can affect effectiveness of monetary policy. Increases in the competitiveness of the banking system, eliminating or significantly reducing seignorage, is also likely to reduce the effectiveness of monetary policy.

(x)Aggregate money or credit numbers (or free reserve numbers) may be highly misleading; credit entails highly specific information about specific borrowers inside specific lending institutions. Funds may not flow freely from banks with excess free reserves to banks with capital shortages

Why Monetary Policy?

• Advantages:– Imposes lower information costs—banks do

screening of projects– At times, there may be large and predictable

multipliers—increasing bank net worth through seignorage may lead to multiple increase in lending activity

Why Monetary Policy?• Disadvantages:

– May be ineffective—liquidity trap– Impact distortionary—largest impact through banking

system– Different sectors rely differentially on banking sector– With credit rationing, certain categories of risk may be

excluded from market– Impacts are especially large on small and medium size

enterprises that do not have access to commercial paper market; large international markets can access capital anywhere in world

– Effects may not be predictable, e.g. when structure of banking system changing or when shocks affect net worth of banking system

– Adverse effects may be particularly significant in economies with high volatility—heavy reliance on interest rate policies induces low debt-equity ratio, forcing reliance on retained earnings, with adverse effects on growth

– Some of the adverse effects may be offset by targeted lending programs

• Reduce efficacy of monetary policy

• Argument that such interventions are “distortionary” based on naïve, wrong model of capital market

Exchange Rate Policy• Using interest rate policy to maintain exchange

rates particularly questionable– Often entails very high interest rates– High interest rates occur when economy is going into

recession (pro-cyclical monetary policy)– Empirical evidence is that they are often ineffective– Standard model ignores bankruptcy probability; high

interest rates increase bankruptcy• Confidence not restored

• Encourages capital flight

Won’t a Decrease in Exchange Rate Also Have Adverse Effects?

• Increase in interest rates often ineffective: lose-lose situation

• Risk averse firms should have cover (e.g. exporters implicitly “covered” by increased value of exports in domestic currency)

• Protecting firms that do not have cover exacerbates moral hazard problem

Regulatory Policy and the New Paradigm

• Deregulation has played a large role in recent increases in economic instability

• Underlying problem—with implicit or explicit deposit insurance, banks do not bear all the costs of the risks that they undertake

--but important not to draw wrong conclusion monitoring banks is a public good, not best done by

individuals or firms

and deposit insurance is important in promoting stability

• Key question: what kind of regulatory system• answer requires theory of banks • excessive reliance on capital adequacy

standards misguided• need portfolio approach• general approach helps us understand some

common problems with financial and capital market liberalization

• Sole reliance on capital adequacy standards misguided– Not based on modern finance—looks at assets in

isolation– Often have focused on credit risks– Recent problems have entailed interactions between

credit and market risk– Pareto efficiency requires using in addition other

regulatory instruments– Increasing capital adequacy standards may even lead

to less prudential behavior, because of decrease in franchise value (value as an ongoing enterprise)

– With imperfect risk adjustments, banks may shift portfolio to riskiest assets within any asset class

• With imperfect risk adjustments and failure to mark to market, banks have an incentive to sell off assets that have increased in value, and retain assets that have decreased (deteriorating information content of asset numbers)

• Worse, under same conditions, banks have incentive to invest in high risk activities; maximize above “option” value

• Risk weighting encouraged short term foreign lending, probably contributing to East Asia crisis

Alternative Approach—Portfolio Approach to Regulation

• Recognizes the government can only imperfectly control the actions of banks– Banks must know more about to whom they are

lending than regulator

• Government needs to take variety of actions that affect bank incentives and constraints

Examples of Constraints

• Categories of loans—real estate

• Insider lending

• Bank exposure (e.g. foreign exchange risk, mismatch of maturity structure)

• Speed limits

• Interest rate restrictions

Incentives

• Increase franchise value

• Put others at risk—subordinated debt

• Individual incentives as well as organizational incentives

• Key question: How does changing regulation affect the behavior of the bank—its choices

Financial and Capital Market Liberalization

• Analysis based on false analogy between markets for ordinary goods and services and financial, capital markets

• Allowing entry has benefits from increased competition

• But increased competition erodes wealth, franchise value

• May lead to less prudential behavior

• Information base of new, foreign banks different from information base of domestic banks

• May lead to less lending to SME’s, more lending to large, international firms

• Net effect may be to impede efficient allocation of resources

• Problems may be able to be partially addressed through lending (CRA) requirements

Regional Downturns and Development and Monetary Policy

• Increasing globalization of world economy, increasing importance of capital flows

• Question: will they eventually undermine role of monetary policy

• Parallel question: within a single country (like U.S.), single currency, no barriers to flow of capital, is there scope for “regional monetary policy”

Perspective of This Book• Information is local (regional)

• Regional banks have more information about their own region, lend to their own region– Shocks to their region affect their net

worth, their ability and willingness to lend– Regional credit interlinkages exacerbate

regional downturns—extend impacts beyond non-traded sectors to traded goods produced within the region

– Statistical studies confirm the effect in the U.S.

Underlying Problem:

• Capital and financial market liberalization without adequate regulatory oversight

• Leading to large ratios of short term debt relative to reserves

• Sudden change in investor sentiment led to crisis—change in flows amounted to 14% of GDP for Thailand, 9% for Korea, 10% for region as a whole

East Asia Crisis

Two Issues

• Interest rate policy

• Dealing with weak banks

Interest Rate Policy• IMF theory—raise interest rates, higher

interest rates attract more capital, exchange rate stabilized, confidence restored, interest rates can be brought down

• In practice—total package, billions of dollars plus raising interest rates—did not stabilize exchange rate, stem flow of capital out of country

• Key mistake—ignored probability of bankruptcy (default)

• Mistake surprising—worries about default were at root of problem, explained why banks refused to roll over loan

• Policies increased probability of default, so much so that expected returns were lowered

• At beginning of crisis economies were in rough economic balance (some problems of excess capacity)

• Fall in stock market, real estate prices would have been expected to reduce investment, induce recession– High interest rates and fiscal contraction only

exacerbated problem– Effects on economy exercised not only through

aggregate demand but also aggregate supply as credit became less available

• Reduction in “supply” by one firm becomes a

• Problem of “demand” for its suppliers. Demand and supply problems intertwined

– Exports did not increase to extent expected, even with large devaluations

– Higher probability of default affects demand—firms become unreliable suppliers

– Supply constraints from lack of credit– Regional interdependence, downward spiral

caused by “beggar thy-self policies”

• Not only were foreign investors not attracted back in, domestic investors were induced to leave—higher risk at home, highly correlated with returns on human capital

• Consequence: confidence was undermined, not restored

• (In fact, hard to reconcile argument that temporary increase in interest rate will have a permanent effect on beliefs with any theory of rational expectations; if anything, high interest rate policy “signaled” adverse information concerning monetary authorities—that they did not understand situation)

• Adverse effects of high interest rates persist after interest rates are reduced– Firms in distress– Depleted net worth of firms– Weakened financial institutions

Restructuring BanksKey issue from perspective of this lecture:• Banks embody specific information about the

creditworthiness of particular borrowers• Closing banks destroys this informational capital• Borrowers (especially SME’s) depend on one or

two banks• In a recession, banks contract lending• Borrowers whose banks close will find it difficult

or impossible to find alternative sources of credit• Credit interlinkages are important, and can

exacerbate negative effects

Policy Implication• In face of systemic problem, try to maintain credit flows• Recapitalize, merge banks• Need some degree of forebearance

– Impact of strict enforcement of capital adequacy standards different when problem is systemic

– banks will find it difficult to find additional capital in a recession

– Accordingly, to restore capital adequacy, have to cut back on loans

– As each bank cuts back on loans, more firms are forced into distress, number of non-performing loans increase

– Health of banking system as a whole may be weakened

Policies Pursued Sometimes Ignored These Principles

• Worries about moral hazard (forward looking) dominated concerns about maintaining credit flow

• In Indonesia—closed 16 private banks, announced more might be closed, depositors would not be protected—induced run on private banks, weakening banking system

• While funds flowed into other banks, information is specific—customers of weakened or closed private banks lost access to credit

• Throughout region, controversy over degree of forbearance

The 1991 U.S. Recession and Recovery

• Both recession and recovery linked to banking system– Recession to weaknesses– Recovery to unanticipated strengthening

History

• Huge increases in interest rates under Volcker in 1979-1982 weakened financial system, especially S&L’s– Long term assets (mortgages)– Had to pay higher interest rates for deposits

• To forestall closing of S&Ls, accounting rules changed; at same time deregulation allowed S&Ls to enter new lines of business, reduced supervisory oversight

• Banks with negative net worth—given new opportunities for risk taking—“gambled on resurrection.” – Because of deposit insurance, had no problem

attracting funds

• 1989 issue came to head– Gambles had not paid off– S & L’s had to be bailed out– Regulatory standards tightened

• As U.S. went into recession, Fed failed to recognize the changed state of banking system (especially S&Ls)

• Fed lowered interest rates in accord with standard IS-LM model

• Predicted effects did not occur

• Did not realize key issue—banks’ willingness and ability to lend, given weakened net worth and tighter regulatory standards

• Some in Fed recognized, but dominant view stuck to traditional “model.”

• Only in 1993, at end of recession, was due recognition taken of financial system problems

Recovery• Standard explanation: deficit reduction allowed

interest rates to come down, and that spurred investment

• Two problems:– Fed should be able to maintain economy at “NAIRU”

with higher deficit, higher interest rate, but output/employment should be same

– Fed thought NAIRU was 6.0- 6.2%. Why did Fed allow unemployment to fall so far below NAIRU? Models predicted inflation would result. Given widespread belief within Fed that one should mount “pre-emptive” attacks against inflation, why did they not do so? Did they not believe their models?

Answer:Recovery was due to deficit reduction, plus two

mistakes by Fed (mistakes do not always work against you)

• In 1989 Fed had resisted using appropriate risk adjustments in capital adequacy standards, did not treat long term bonds as risky– Provided incentives for banks to put more of their capital into

long term bonds– High interest rates reflected market judgments that capital

values might fall (e.g. if inflation increased, and future short term interest rates increased). Risk ignored by regulators; banks “recapitalized” as long term interest rates exceeded short term (what they had to pay depositors).

– Risk meant that if deficits grew faster, interest rates increased, banks could have found their capital value greatly diminished

• Deficit reduction: barely got through Congress, led to lowering of long term interest rates, increases in value of long term bonds. Banks, in effect, were recapitalized– Led to increased supply of loans

Fed failed to anticipate strength of recovery, again because relied on standard models, did not focus on banks and financial markets

• Quicker than anticipated recovery led to lower unemployment rates but no inflation—demonstrating that estimates of NAIRU were also faulty.

• Good news was that Fed took pragmatic line—allowed unemployment to continue to fall so long as inflation did not increase.

Concluding Remarks

• New paradigm focused on the central role of credit and banks in a monetary economy

• Some final thoughts about implications of the role of monetary policy in the future

• And the conduct of monetary policy in developing countries

• Credit is based on highly specific information• Such information is widely dispersed within a

market economy• New technologies are changing rapidly access to

information, and the speed with which information can be transmitted

• Information that a credit card company judges an individual “credit worthy” (up to some limit) can be transmitted instantaneously around the world

• It is still the case that much of the relevant information for judging creditworthiness will remain highly concentrated and banks continue to play a key role in the processing of such information and in forming judgments about creditworthiness

• New technologies and increased competition may affect the efficiency with which they perform those tasks

• But these changes may, at the same time, impair the efficacy of monetary policy.

• Will this herald in a new era of economic instability?

• Or will changes elsewhere in the economy enable the market economy to have less need for monetary authorities to perform their traditional roles in stabilization?

Some final thoughts on the conduct of monetary policy in developing

countries• Fads like monetarism and inflation targeting may

do far more damage in developing countries than in developed

• Banks are likely to remain even more important in developing economies than in developed economies– Attention needs to focus on flow of credit to all

segments of economy– And stability of credit flow in the face of an economic

downturn

Related Documents