1 TOWARDS A MODEL OF MARKET DISTRUPTION (WORKING TITLE – 12/07/2010) Gökçe Sargut Assistant Professor College of Business and Public Administration Governors State University 1 University Parkway University Park, IL 60484 [email protected] (708)534-4944 Rita Gunther McGrath Associate Professor Columbia Business School 4 th Floor, Armstrong Hall 2880 Broadway New York, NY 10025 (212) 854-6155

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

TOWARDS A MODEL OF MARKET DISTRUPTION

(WORKING TITLE – 12/07/2010)

Gökçe Sargut Assistant Professor

College of Business and Public Administration Governors State University

1 University Parkway University Park, IL 60484

[email protected] (708)534-4944

Rita Gunther McGrath Associate Professor

Columbia Business School 4th Floor, Armstrong Hall

2880 Broadway New York, NY 10025

(212) 854-6155

2

INTRODUCTION

Our aim in this chapter is to lay the foundation of a theory of market disruption that sheds new

light on our understanding of the types of disruption that occur in product-markets. In doing so,

we also explore the entrepreneurial conditions and factors that help bring about such disruption.

As such, the preliminary model that is proposed here represents two aspects of market disruption.

First, we propose a classification scheme based on the severity of disruption caused by

newcomers in industry incumbents’ markets. Second, we recognize that disruptive activity is

entrepreneurial in its essence. Over the past three decades, research in strategic management and

organization theory has uncovered insights into the factors that provide advantageous contexts

for entrepreneurs in launching new ventures. Based on these insights, our model also explores

factors that are likely to be important in entrepreneurs’ creation of disruptive business models.

As a concept, ‘market disruption’ immediately harkens research in two areas that have

enjoyed significant contribution over the years—technology and innovation. Because disruption

almost always conveys new ideas or new ways of doing things, it is almost impossible to talk

about market disruption without delving into research in disruptive innovations or disruptive

technology. This is why we would like to begin our exploration with a few words of caution.

Despite valuable research in the area, a great deal of conceptual confusion remains as to the

characteristics, types, and hierarchical locus of innovation (Gatignon et al., 2002). A good

example is disruptive innovation (Christensen, 1997), which is immediately relevant for any

discussion of market disruption. As we explain later in the chapter, many disruptive innovations

can indeed result in market disruption. However, researchers have yet to clarify whether and to

what extent disruptive innovations are different than, say architectural innovations (see Gatignon

et al., 2002). Our proposed solution is to take a more general perspective on disruption so as not

3

to add to this prevailing confusion. However, doing so requires a brief review of extant research

in disruptive innovation so that our own position can be clarified.

Disruptive Innovation: An Overview

The theory of disruptive innovation introduced by Clayton Christensen (Bower & Christensen,

1995; Christensen, 1997) offers an explanation for the displacement of industry leaders by

smaller competitors (almost always new entrants) who initially enter into incumbents’ markets

with seemingly inferior products or services. These products often provide valuable capabilities

to a niche of customers that might be seen as insignificant by industry leaders (Smith, 2007). The

theory’s explanatory power comes from the notion that industry incumbents and new entrants

follow different technology trajectories. Industry leaders tend to focus on sustaining innovations

that continuously improve their flagship products, increasing overall performance in attributes

that are perceived as being important for their existing customer base. Over time, the

performance increases achieved through sustaining innovations begin overshooting the needs of

the best customers who pay the highest prices, whereas the new entrants’ disruptive products

become good enough to meet the needs of the dominant incumbents’ customers. It is usually too

late by the time the latter notices this dynamic.

Christensen identified a number of industries where the pattern of disruption closely fits

with this theory. These include computer hard disk drives, desktop computers, retailing, and

general hospitals, among many others. The value of Christensen’s findings and insights are

accentuated by the fact that there have been very few companies that were able to effectively

manage disruptive change in the long run. IBM, for example, was the only major computer

company to survive from the 1960s. This was mostly due to the fact that it was able to create

4

new entities for its emerging minicomputer and personal computer businesses in order to protect

them from the inertia of their core mainframe business model and its value networks (see

Christensen, 2003[1997]). In a similar vein, de Kluyver & Pearce (2006) identify General

Electric as one of the few companies that have been able to reinvent itself continuously over the

past few decades:

In every major transformation in the last 30 years, GE succeeded by setting up or

acquiring new disruptive business units and selling off or shutting down ones that had

reached the end of their economic lives. It never attempted to transform the business

model of an existing business unit as a way of “catching up” to the new basis for

competition imposed by disruptive innovations. (p. 101)

Gillette is another company that has successfully built dominance against its competitors

“[t]hrough a series of major new product launches, driven by technology and branding

innovations” (D’Aveni, 1999: 127). However, D’Aveni (1999) argues that if we were to examine

the beginnings of the Bic-Gillette competition in the 1970s, a different picture would have

emerged. Early on, Bic was able to shift the dominant value proposition in this market to one of

low-cost convenience through its substitution of disposable razors against Gilette’s cartridge

system. The new rules of competition introduced by Bic at the time were so foreign to Gilette

executives that they admitted to having been left wondering “why anybody would compromise

their shave to save a little money” (Thomas, 1996; quoted in D’Aveni, 1999). As such, Gilette’s

successful turnaround in its battle with Bic is a good example of how a higher end product can

strike back to dominate the market in spite of the disruptive technology dynamic discussed by

Christensen.

Christensen was extremely successful in recognizing a specific pattern of disruption and

cogently outlining its mechanics. Any social scientist can appreciate the value of research that

successfully combines inductive and deductive processes, which is arguably one of the most

5

promising approaches to advancing theory—and this is precisely what Christensen was able to

accomplish1. Despite its elegance and power, Christensen’s theory of disruption has certain

limitations—partly because the model is evolving as new evidence is being incorporated (see

Christensen, 2006), but also because of the fact that it is not clear whether useful insights can be

gained using the same approach at different levels of competitive analysis.

As an example, consider the relationship between technological evolution and product

development. Disruptive innovation can be easier to observe in cases where the natural trajectory

of evolution of a technology can be understood within the confines of a “technological

regime”—a term introduced by Nelson & Winter (1982). As these authors have observed,

technology regimes relate to “technicians’ beliefs about what is feasible or at least worth

attempting” (p. 258-9). As such, regimes provide engineers insights on performance barriers

related to major components of a given technology. In other words, once a regime is established,

engineers quickly start gaining insights as to the extent to which various extensions of the related

technology can be exploited until it is superseded by another technological regime.

It is relatively easy to apply Christensen’s theory to those situations where natural

trajectories of product development can be observed under a given technological regime. Under

such cases, data can be used to track the market leaders’ ongoing exploitation of a dominant

technology. Data can be collected on various performance dimensions in order to accurately and

objectively examine the various technology trajectories in a given industry—as Christensen has

done in his groundbreaking study. Researchers can then look for evidence of disruptive

innovations across technological regimes and examine the eventual—or even potential—success

of disruptive innovations.

1 See Christensen’s (2006) notes on theory building, particularly in relation to his work on disruptive innovations.

6

Unfortunately, dynamics of competition in many industries is not so clear-cut—even

when certain patterns in product evolution clearly bear resemblance to the kind of disruptive

innovation outlined by Christensen. Consider product substitution in general and the creation of

new product categories in particular. Although substitution can arise in relation to disruptive

technologies, it encompasses a broader area, including “technological threats from above (as

opposed to below)” (Ghemawat, 2006: 106). According to Ghemawat (2006), a typical example

of this is the first two decades of the videogame market where the market leader was displaced

with each new generation of gaming consoles. In the current generation, with the Wii, Nintendo

launched a product that was in many ways technologically inferior to Sony’s Playstation 3 and

Microsoft’s XBOX 360. It was far behind its competition in both speed and graphics processing

power—the most critical areas of performance by any standard in this industry.

Despite the fact that the Wii was deemed inferior by the majority of hardcore gamers (an

important target market for gaming console manufacturers due to their loyalty to various gaming

genres and franchises), it was able to consistently outsell its competitors following its launch. As

such, Nintendo’s offering represented the characteristics of a disruptive innovation. Using

Christensen’s (1997) terminology, one argument could be that the package of performance

attributes that Nintendo brought into the mix were not valued by the high end customers who

represented the mainstream for market leaders in the industry. However, Nintendo brought other

value propositions into their product offering. As it turns out, Wii’s motion sensing technology—

which was originally seen as a simple gimmick by both the competitors and the core customer

base—was very useful in convincing non-gamers to buy the Wii. In the end, ease-of-use and

simplicity in core mechanics won over those customers who would normally stay away from

video gaming.

7

A new disruptive product is “…usually simpler, more convenient, and more affordable,

[enabling] the participation of a new set of customers who were previously ignored by the

market or shut out completely” (Hwang & Christensen, 2008: 1330). The Wii’s introduction

certainly corresponds to this dynamic. However, Nintendo did not achieve their dominance in the

current generation through gradual improvements in an otherwise inferior product offering.

Rather, they were successful in attracting a new customer segment into the industry. These

customers were not buying the Wii to replace their old gaming systems; the Wii became a

substitute for other leisurely activities the new adopters would otherwise be involved in.

Moreover, for many video-gamers, the Wii was not even a substitute but a second purchase—the

alternative they turned to when they felt like playing lighthearted games with their family and

friends.

In other words, despite the fact that certain aspects of Wii’s introduction supports the

theory of disruptive innovation, Nintendo’s disruption is not simply a story about a previously-

inferior technology that brought low-end customers into the market. Rather, it is part of a

complex business model that created market disruption in various ways2.

One could argue that the theory of disruptive innovation crosses too many levels and tries

to explain too many instances of competitive dynamics. For example, the term disruptive is used

in the context of innovation, technology, product, and business model by various authors—and

even interchangeably across these contexts. Alternatively, the problem could be seen as one of

epistemology. In other words, the problem is not simply a matter of gathering more evidence, but

rather stems from difficulties inherent in building theories based on socially complex

2 This is precisely why Zipcar presents such a formidable challenge to car rental companies. We will discuss the

Zipcar example at some length later in the chapter.

8

phenomena. For example, the limitations in Christensen’s theory are consistent with Weick’s

(1979) insights based on Thorngate’s (1976) postulate of commensurate complexity. Essentially,

the postulate states that any theory of human behavior cannot be general, simple, and accurate at

the same time. The theory advanced in The Innovator’s Dilemma is simple and accurate.

Constructs such as sustaining and disruptive innovation are precise and well-articulated. By

definition, the theory’s weakness comes from its lack of generalizability.

In this chapter, we take a different approach and present a model of market disruption

that is simple and general. Admittedly, unlike Christensen’s model, ours suffers from a lack of

accuracy. As a matter of convenience, we would argue that the best way for practitioners and

researchers to go about studying disruption would be to apply different theoretical models based

on a given context, as well as the level of analysis that is salient in that context.

Elaborating on the meaning and types of disruptive technologies, Keller and Shanklin

(2007) suggested that “for the purposes of crafting strategies, the nomenclature is too imprecise

because it brushes over consequential distinctions” (p. 37). These and other authors have argued

that it is in fact a convergence of a number of circumstances that cause a disruption (Keller &

Shanklin, 2005; Papp & Katz, 2004). Some of the examples we refer to in this chapter can

potentially be labeled as disruptive technologies (or, business models that incorporate disruptive

technologies in their offering). In fact, we refer to them as such in various places throughout the

text. However, we do not formally incorporate the term disruptive technology in our model,

because we do not want to add to the confusion in the area as to what specifically entails a

disruptive technology.

9

Beyond our decision to take a generalist approach, the ongoing confusion among

academics on the meaning of the term is yet another reason why we decided to look at

‘disruption’ from a market perspective. In other words, as long as we can observe that a new

business model has the capability of causing disruption in one or more product markets, we

consider the issue of whether disruptive technologies had a role to play in the said disruption as

secondary. Naturally, we agree that disruptive technologies represent important phenomena that

are deserving of researchers’ ongoing scrutiny. Nevertheless, in this chapter we concentrate on

the types of market disruption based on the impact on incumbents’ markets, as well as the factors

that facilitate the creation of business models that lead to such disruption.

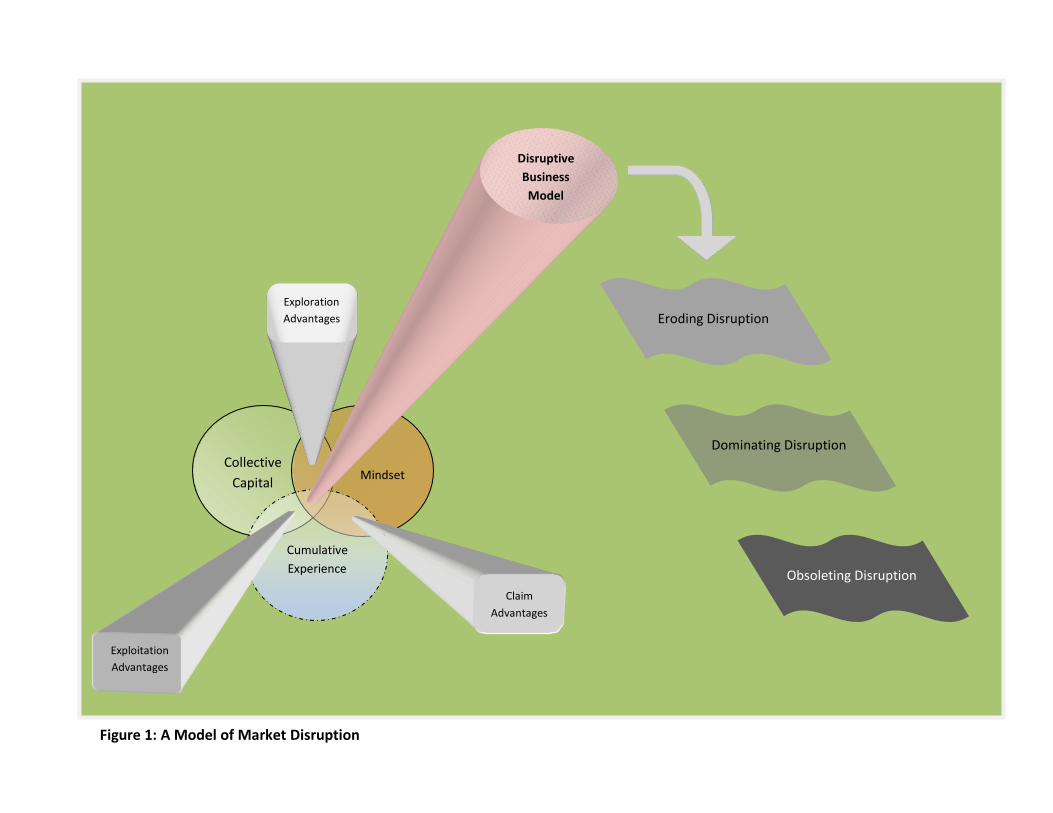

A MODEL OF MARKET DISRUPTION

Figure 1 summarizes the model that will be presented in the remainder of the chapter. We argue

that the creation of a potentially disruptive business model depends on a synergistic combination

of three factors that are critical in entrepreneurial activity—namely, the mindset, cumulative

experience, and collective capital. Collectively, we refer to these as ‘entrepreneurial factors’. The

mindset encompasses the overarching theme or core concept that drives a new product or service.

Cumulative experience refers to the diverse set of experiences and knowledge that entrepreneurs

bring into a new venture—including those gained in their previous jobs or industries. Collective

capital encompasses various forms of capital entrepreneurs possess, including human, cultural,

financial, and social capital.

----------------------------------------------------------

Insert Figure 1 about here

----------------------------------------------------------

10

By their very nature, the mindset, cumulative experience, and collective capital cannot be

thought of as mutually exclusive. As suggested in the graphical representation, these factors all

overlap, and their successful synthesis helps in creating a robust business model that can have the

potential for market disruption. To help explain how this occurs, we identified three sets of

potential advantages where pairs of factors overlap. The first of these is an exploration

advantage, which occurs through the successful synthesis of collective capital and mindset.

Another point of potential synergy is what we refer to as the claim advantage. This becomes

evident in the shaping of the value proposition based on the matching of unique ideas with

entrepreneurs’ experience driven insights on ‘what is doable’. Exploitation advantage is the third

point of synthesis, and it is relevant for the execution of the value proposition. Obviously, this is

important both in planning the strategic implementation, and later, successfully executing the

implementation strategy. We discuss entrepreneurial factors in more detail later in the chapter.

The second half of the figure represents the types of market disruption that can come

about through the successful execution of a disruptive business model. Market incumbents

experience different levels of disruption based on intensity. The severity of disruption increases

as the nature of the threat goes from eroding to dominating. Erosion applies to contexts where

newcomers have slowly started carving out a niche in incumbents’ markets. In our definition, we

also include those cases where a potential threat is recognized by analysts—even if erosion is yet

to occur. This is necessary as the time it takes between the recognition of a potential threat to its

materialization can be of great significance, especially in turbulent environments. The most

severe form of disruption is obsoleting, where a whole category product or service becomes

obsolete in the eyes of the customers in a given market. We will further elaborate these concepts

in the following sections.

11

The Three Types of Market Disruption

We define market disruption as a case where a new entrant gains a significant share in

incumbents’ product or service3 markets through a unique or superior business model. We

differentiate between three types of successful market disruption: eroding, dominating, and

obsoleting. A market disruption can occur in three ways.

The first of these is when a new product dominates a sub-category in a product-market and

then starts eroding the main category4. There are, in turn, two different ways in which such

erosion can occur. The product can create its own category within a given product-market and

proceed to dominate that category. Alternatively, it can enter one of the existing sub-categories

as new entrant and dominate it. A good example for this is Apple Inc.’s iPhone, which was

introduced in 2007. iPhone is technically a smart phone. But it was such a successful product that

it almost instantly started eroding the market share of Research In Motion, a company whose

Blackberry line of smart phones were the category leaders at the time. However, despite causing

considerable erosion in incumbents’ market shares, the iPhone has a relatively small share of the

significantly larger world mobile phone market, which is dominated by companies such as

Samsung and Nokia.

Market disruption can also occur when a new product directly enters incumbents’ main

product-market and immediately starts eroding their market share. In some cases, the new entrant

can completely dominate the category. The success and eventual dominance of Netflix in the

video rental market is a good example of this process. Netflix was able to attack and dominate

market leader Blockbuster through the use of a radically different business model that relied on

3 From here on, we will use the term ‘product’ to refer to both products and services.

4 It is important to remember that a ‘category’ is a fluid construct. Product categories can expand to include other

products that were previously considered to be outside a focal industry’s domain. Also, new product categories can

emerge out of the combination of existing ones (‘nutraceuticals’ is a very good example of this).

12

mail delivery and internet technology (more on this in the next section). Another example is

Apple Inc.’s success with iPod. The iPod was initially released into a market where there were a

number of alternative portable media players (PMPs). Although it is still one of many PMPs in

the market, it remains the dominant product in this market.

The third way in which market disruption can occur is when incumbents’ offerings become

completely obsolete. Disruptive technologies as described by Christensen and colleagues can in

fact provide one explanation for this outcome (see Bower & Christensen, 1995; Christensen,

1997; Christensen & Raynor, 2003; Christensen, Anthony, & Roth, 2004). However, there are

many cases where development of disruptive technology is neither necessary nor sufficient. For

example, there were a number of reasons for nearly complete obsolescence of music retailers

during the past decade. In the end, it was not just new technology but also the way in which

entrepreneurs were able to maneuver a complex social landscape that decided the outcome. New

entrants found ways to make the music-downloading technology cheaper, more convenient, and

legal—providing solutions that satisfied both the consumers and music publishers.

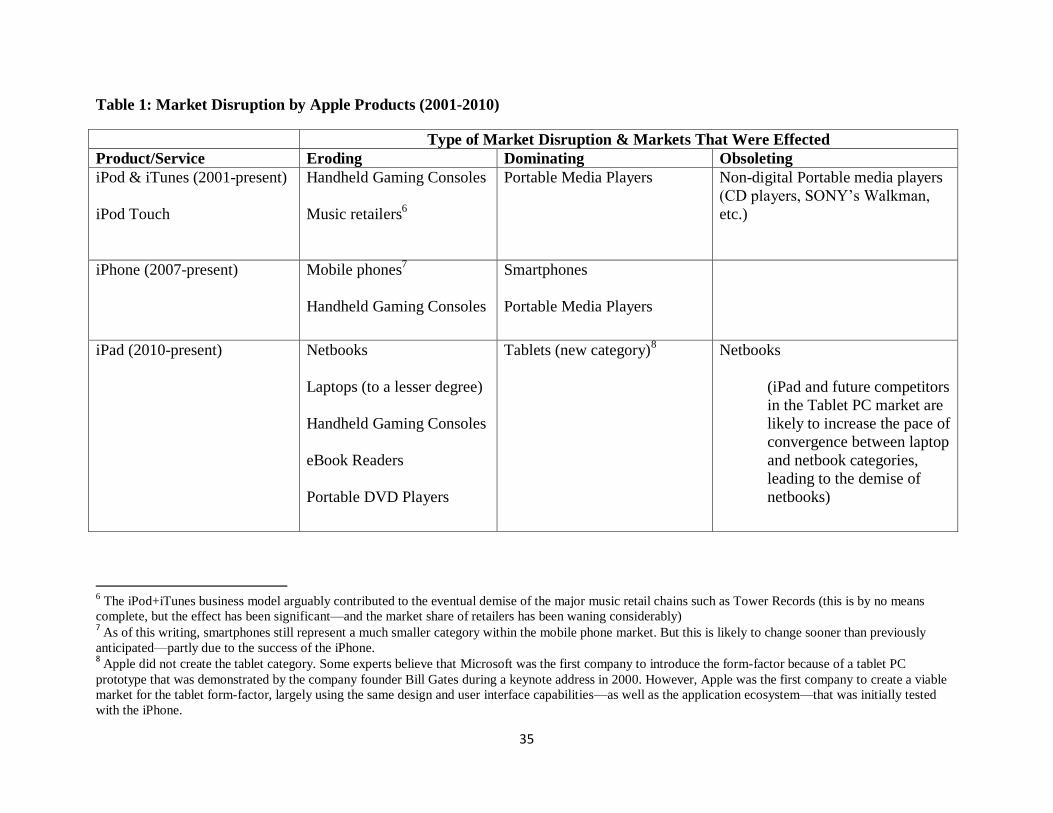

Table 1 uses Apple products as examples in demonstrating the three types of market

disruption outlined in our model.

---------------------------------------------------------------

Insert Table 1 about here

---------------------------------------------------------------

Examples of Market Disruption

Disruption in the Early Movie Industry (1894-1914). The early evolution of the movie industry

presents a very rich context where sources of disruption can be observed at multiple levels.

13

During its initial period of growth, the movie industry as a whole incited a number of disruptions

that first obsoleted Vaudeville, and then significantly eroded the Theatre audience.

The origins of movie industry go back to 1891, when Thomas Edison applied for the

patents of a movie camera, as well as the apparatus for exhibiting moving objects (Fulton, 1985).

In reality, the first cameras to record moving images were discovered by three different groups of

inventors on two different continents. One of these men, William Kennedy Laurie Dickson, was

employed under Edison, and was tasked with putting the invention together based on a number

of existing designs by other inventors. Dickson invented two machines. The Kinetograph was

used for shooting moving images, while the Kinetoscope displayed images through a peephole to

an individual viewer. On April 14, 1894, the first Kinetoscope parlor was opened in New York

City in a converted shoe shop at 1155 Broadway. The shop had ten Kinetoscope machines, a

ticketing booth, and a gold painted bust of Edison at the entrance. April 14th

was a Saturday, and

the owners had gotten the shop ready to open on Monday morning. At around two o’clock, one

of the owners suggested that they let in some customers “to pay for our dinner tonight”

(Hendricks, 1985). They thought it would be a good joke, but the joke was on them, it turned

out, because they had no time to go to dinner that night. The movie business had officially taken

off, and it never looked back.

It took only a year for parlor machines to be replaced by projectors that could project

images on the walls of nickelodeons that acted as makeshift theaters. Despite being a successful

businessman, Thomas Edison seems initially to have been blinded by his inventor alter ego.

There is considerable evidence to suggest that he saw the original Kinetoscope as merely a

novelty, and only after much persuasion did he start providing short film content to be displayed

in nickelodeons that soon started lining up the streets in New York City. But he still saw “the

14

camera” as the product and his main concern was in protecting his patents. A short while later,

Edison, Biograph, and Vitagraph (collectively referred as the ‘Trust’) were all shooting and

distributing 15 minute one-reelers through exchanges that had opened up all over the US in order

to provide local nickelodeons and theaters a steady supply of film. But even then, it is clear that

the Trust was working its way from upstream to downstream—devoting great energy and

resources to protecting their camera patents, the supply of film, and control of sale prices to film

exchanges. The local entrepreneurs who owned the exhibition outlets—small nickelodeons at

first, and then larger movie theaters—had a different perspective on how things were shaping out

for the newly minted movie industry. They realized that they were not selling a product, but an

experience. Being close to their customers daily made them notice two important trends. First,

middle-class customers were increasingly being attracted to movies—so there was a lot of room

for growth in the movie business. Second, it was important to get access not only to more

content, but also diverse, differentiated content in order to fulfill rising demand and keep

audiences interested.

The first owners of nickelodeons had gained access to public exhibition outlets by

creating makeshift viewing spaces. They created a hybrid approach by mixing 15 minute one-

reel films with musical and vaudeville acts5. Newly-immigrant working families were their

initial clientele, and their first establishments were in relatively poor neighborhoods. They

increasingly dominated the exhibition industry by expanding their businesses and opening larger

theaters in more respectable neighborhoods that served the middle class. By 1914, the

nickelodeon business had become so effective in drawing masses of customers that even

legitimate theaters began to offer movies in order to survive the competition. In Boston, one of

5 This section is based on Merritt‘s (1985) highly informative study of Boston’s nickelodeons (1905-1914).

15

the first legitimate theaters to cave in to the onslaught was the Globe Theater owned by the

Shuberts:

Two nearby legitimate theaters—the Shubert at 265 Tremont and the Boston at 539

Washington—were constantly complaining to the New York Dramatic Mirror about the

cheap competition luring away their theater regulars. To meet the threat, the Shuberts

began to show ten-cent movies at their Globe Theatre during the slow 1909 summer

months—an unheard-of practice among Boston’s expensive legitimate houses and one

that created a bitter nickelodeon price war at the Eliot Street corner of Washington Street

(Merritt, 1985: 92).

Within a very short time frame, the film industry had first co-opted and then obsoleted

Vaudeville as the favorite popular pastime of the masses. It then turned into an eroding

disruption for legitimate theater. Despite their modest beginnings, the ‘moguls’ who created the

‘Hollywood Studio System’ (Schatz, 1988), would be victorious. In 1929, during the last wave of

wide-scale industry rivalry, William Fox’s and Warner Brothers’ success in developing and

implementing sound technology brought an end to two decades of ebb and flow, solidifying the

dominance of a handful of firms that we still refer to as Hollywood Studios today.

Zipcar versus Traditional Car Rental (1999-present). Zipcar was established in 1999 by a team

of entrepreneurs with the goal of combating congestion and pollution by reducing the number of

cars on the road. Their business model was based on offering car-sharing services, and their

initial growth came from word-of-mouth advertising from like-minded environmentally

conscious individuals. As Zipcar grew, however, it started becoming clear that their time-sharing

model was going to be a potential threat to the traditional car-rental industry. This was confirmed

in 2008, when Hertz Corporation, the market leader in the rental industry, started ‘Connect by

Hertz’—a new service offering that is remarkably similar to Zipcar’s.

It is apparent that, at least initially, none of Zipcar’s founders saw their service as a threat

to—or much less a direct competitor of—car rental companies. As such, the case of Zipcar is an

16

interesting example for disruptive business models that could potentially blindside industry

incumbents because new entrants originate in seemingly non-overlapping markets (see

Markman, Gianiodis, & Buchholtz, 2009). It is also interesting to note that Zipcar is the product

of a completely different mindset that is associated with environmental consciousness and a

green lifestyle, backed by a philosophy that goes against excessive waste and redundancy.

It remains to be seen whether Zipcar is going to move from being an eroding disruptor to

a position of dominance. However, the community that developed around the company is a good

example of how collective capital can form the basis of a disruptive business model. Because

Zipcar sees its members’ lifestyle choices as a resource, its more traditional competition is forced

to deal with a new entrant whose business model includes tacit factors such as belief in

conservation, even ideology. It will be interesting to see if incumbents such as Avis and National

are going to be able to successfully defend their position against such a challenging disruptor—

especially during a difficult economic period.

Entrepreneurial Factors

According to one of the simplest yet most elegant definitions found in research, entrepreneurship

is the process of discovering new ways of combining resources (Sobel, 2008). Entrepreneurs

clearly accomplish much more than that, but resources—in the form of knowledge, business

processes, interpersonal relationships, or finances—are always at the locus of entrepreneurial

activity. As such, entrepreneurs are routinely faced with the enormous task of transforming

bundles of resources into viable business models. Naturally, success of a business model can

never be guaranteed. However, thanks to ongoing work, researchers are increasingly more aware

of some of the factors that are important components of success.

17

Regardless of their level of visibility, leaders of innovative teams, such as Apple’s CEO

Steve Jobs, rarely create new products or unique business models on their own. Any

entrepreneurial team includes individuals who bring their unique background, training, and

previous experience into the mix. For this reason, the entrepreneurial factors discussed in our

model should be considered from either an individual or group perspective, depending on the

makeup of the entrepreneurial team. Depending on the context, the factors can apply to an

individual entrepreneur and how she combines and synthesizes various types of diverse resources

related to capital, experience, and mindset. Alternatively, the focus can be on a team of

entrepreneurs who bring with them a diverse set of resources stemming from individual

differences in their background, training, relationships, industry experience, and so on. As such,

‘cumulative experience’ can either refer to accumulated experience of an individual

entrepreneur, or a group of entrepreneurs, as dictated by the context.

Furthermore, the use of resources such as social capital necessarily involves skillfully

managing relationships among many individuals—even in the case of a single entrepreneur. In a

study of Inc. 500 companies, Bhide (2003) found that the individual entrepreneurs who started a

significant number of successful companies “…don’t have verifiable human capital or objective

business experience” (p. 36). Obviously, even the most successful individual entrepreneurs do

not achieve results on their own—an observation that further emphasizes the importance of

social capital—a point which we return to later in the chapter.

In this section we discuss three types of advantage that are important in creating the

context for a potentially disruptive business plan. We refer to these as the claim, exploration, and

exploitation advantages. Social capital, which is a part of collective capital in our model, (see

18

Figure 1) has important implications for both exploration and exploitation advantages.

Consequently, exploration and exploitation will be discussed in tandem.

Claim Advantage

As shown in Figure 1, we argue that claim advantage comes about through the effective

synthesis between mindset and cumulative experience. Experience is one of the most salient

resources for a group of newcomers who want to create a viable business model. Research in

entrepreneurship can offer clues as to why this may be the case. Particularly, entrepreneurs often

reproduce existing forms of knowledge they acquired previously in organizational settings

(Aldrich, 1999). More specifically, founding team members’ past company affiliations, as well

as their relationships, play an important role in determining firm strategy and action (Beckman,

2006; Boeker, 1988). Positive organizational experiences in various settings help shape potential

entrepreneurs and prepare them for ventures they are likely to initiate in the future. They also

help in the transmission of rules, norms, and knowledge within and between generations of

organizations.

When looking at potential impact on business models, claim advantage is closely related

to a value proposition—that is, “a product that helps customers do more effectively,

conveniently, and affordably a job they have been trying to do” (Hwang & Christensen, 2008).

What is worth stressing here is the fact that our approach emphasizes the required synthesis

between different forces that may at times oppose each other, presenting significant challenge for

new entrepreneurial ventures.

Consider Japanese automakers’ early success into the US market during the 1970s. While

the Japanese mindset was based on the notions of ‘compact, cheap, and fuel-efficient’, their large

19

American counterparts were still basing their offering around designs configurations that

emphasized ‘big and powerful’. As far as cumulative experience goes, Japanese companies such

as Honda had a significantly different approach to the supply and configuration of car

components because of their significant expertise in building motorcycles. Not only can

cumulative experience have an influence on mindset, companies (especially established ones)

can have face considerable difficulty in changing their business processes in order to create and

offer a better value proposition to their customers.

As the examples demonstrate, cumulative experience can be both enabling and disabling.

The important point to remember is that enrepreneurial action is not based on isolated events, but

rather, is socially embedded (Granovetter, 1985). As Fombrun observed (1986), “[t]he

entrepreneurial founder of an organization, coworkers, managers, and employees are all drawn

from an institutional context that powerfully shapes beliefs and cognitions” (p. 405).

Furthermore, this ‘institutional context’ need not be limited to the confines of a single

organization. The experience gained in one industry or market can lead to market disruption in

another industry. Consider the following account of the founders of MGM, Fox, and

Paramount—the three largest film distribution companies during the classical Hollywood era

(1930-1950):

It is no coincidence that men who had been in the garment industry were able to survive

in the film business. Samuel Goldfish had been a glove salesman before he became

Samuel Goldwyn, motion picture producer. Both Adolph Zukor and Marcus Loew had

been furriers. The same kind of tenacity, hard-sell techniques, and inventiveness were the

prerequisites of both industries. With similar, extremely narrow margins for error and

cutthroat competition, Fox, Zukor, and Goldwyn were able to carve out empires where

none had been before (Solomon, 1988: 2).

20

All three of these men got their start in the fast-paced garment industries in New York and

Chicago. Not only were they able to create successful businesses, they redefined and restructured

the film production business, even succeeding in overthrowing the ‘Trust’ cartel headed by

Thomas Edison. The key to their success was not the similarity in product, but rather the

dynamics of competition between the two industries. In other words, garments and motion

pictures were ‘nonoverlapping’ product-markets (see Markman et al., 2009)—yet the degree of

rivalry in the former ended up having a profound influence in disrupting the latter. In this sense,

the sources of disruption were based on neither product-market nor factor-market rivalry, but

something more tacit that manifested itself in the mindset of the newcomers.

The Hollywood moguls adapted their experience in the fast-paced garment industry to an

entirely new setting where they grew their business with a similar mindset based on rapid

reaction to customer demand, variety in products, and a very disciplined production process.

Their fast, adaptive style, combined with their proximity with customers (by virtue of their being

at the exhibition end of the value chain), allowed them to discover new opportunities that the

then-powerful producers such as Edison were blinded to. Starting with their modest roots in

exhibition, MGM, Fox, and Paramount became large vertically integrated companies. They had

complete control over virtually every aspect of the movie business value chain from the training

and signing of new talent, to securing intellectual copyrights, and organizing film production,

distribution, and exhibition.

Exploration and Exploitation Advantages

Synergy between collective capital and mindset plays an important role in exposing

entrepreneurs to diverse ideas and solutions through their personal and social resources (see

21

Figure 1). On the other hand, synergy between collective capital and cumulative experience is

crucial in guiding entrepreneurs in their search for trustful partners who will help apply their

existing experience and resources in useful ways. Drawing on March’s (1991) research, we refer

to these points of synergy as exploration and exploitation advantages respectively.

Exploration and exploitation advantages also mirror Burt's (2005) insights on social

capital and social networks. These relate to advantages gained from brokerage and closure

respectively. In our model, where brokerage opportunities arise, they do so at the intersection of

mindset and social capital, leading to exploration advantages. Not only do brokerage

opportunities expose entrepreneurs to new relationships, but they also introduce variation in

ideas and diversity of perspectives. This is precisely why exploration advantages arise at the

intersection of collective capital and mindset. To reemphasize the point, our claim is not that

social capital is unequivocally more important than human, cultural, or financial capital. Rather,

as demonstrated in the case of entrepreneurs such as Mike Burnett (see below), having access to

these latter types of capital may not be sufficient, or even necessary (see Bhide, 2003) in many

cases.

Closure is the other side of the coin in that it ensures successful execution. Advantages of

closure include high levels of trust and coordination. According to Burt (2005), brokerage is

about introducing variation into group opinion and behavior. Closure, on the other hand, is

essential in building an effective team once the variety is absorbed through the bridges created

by brokerage. As Burt explains (2005):

Where third parties close the network around bridge relations, reputation pressures

encourage the trust and collaboration needed to deliver the value of bridges […], creating

a social capital advantage defined in terms of closure across structural holes, especially at

extreme levels of closure coordinating across extensive bridge relations as in a

22

skunkworks or crisis team… [s]ocial capital of closure is about the advantages of driving

variation out of group behavior or opinion (p. 224-225).

A good example of the brokerage advantage of social capital can be seen in the story of how

Mark Burnett, the creator of the television series Survivor and Apprentice, successfully disrupted

television programming. Through an innovative combination of game show and reality TV

elements, Survivor resurrected the CBS network at the top of the Nielsen Ratings. More

importantly, it created a new sub-genre, a new category of programming that TV producers have

emulated since.

There are two points in Burnett’s story that demonstrate how he was in the right place at

the right time to bridge structural holes. The first of these is when he crossed paths with Doug

Herzog, the chief programmer for MTV through his race partner after he joined an extreme

cross-country race called the Raid Gauloises (Ross & Holland, 2006). It should be noted that

Burnett had absolutely no experience in television. It was probably his background (especially

his training as a paratrooper) that was influential in his decision to enter an extreme cross-

country race which led to him meeting his race partner in the first place.

Being at the right place at the right time obviously helps, but it is only half the story.

There is a point at which entrepreneurs’ individual skills and experience have to come into play.

A case in point: Burnett was not even the first to come up with the idea of a show that would

follow the Survivor format. Two other entrepreneurs from England had come up with a similar

idea almost a decade before him, but were not successful at getting US producers to finance it. In

1998, Burnett struck a deal with them for the U.S. rights for the show and successfully pitched it

to CBS. This was the second critical point at which Burnett made the brokerage opportunities of

social capital work for him.

23

While the brokerage view is more important in the initial stages of entrepreneurial

activity (e.g., the recognition of opportunities), acting on those opportunities while executing a

potentially disruptive business model requires discipline and focus—which requires more

emphasis on closure. In looking at research that examines venture-capitalists’ investment

networks, Burt (2005) concluded that “[t]he social capital of bridging structural holes is more of

an advantage in more uncertain ventures” (p. 157). In other words, despite the fact that

entrepreneurial opportunities (especially the potentially disruptive ones) exist primarily in

uncertain business environments (Covin & Slevin, 2002; Ireland et al., 2003; McGrath &

MacMillan, 2000), successful execution requires cohesion between members of the

entrepreneurial team that is involved in bringing the new business model to life.

The management of exploitation advantages can continue to have important implications

long after initial success in disrupting a market. After the successful launch of their service in

1999, Netflix found itself in a potentially disadvantageous position, due to the fact that

Blockbuster decided to respond by not exactly matching their mail distribution services, but also

complementing it with in-store video rentals and drop-off. Some analysts at the time declared

that this would be the end of Netflix’s brief success in the video rental market. According to one

financial analyst, Netflix was no longer a viable business. How could they succeed against a

competitor that offered the same exact service and a bricks-and-mortar component? (Stross,

2010). But it took Blockbuster three years to integrate their online services with their bricks-and-

mortar operation. Even then, it proved too costly and inefficient, because Netflix had already

widened the experience gap when it came to running a mail-based operation. As it turns out,

24

[S]everal years earlier, Netflix’s engineers [had] modified industry-standard bar-code

sorting machines to handle the odd-shaped envelopes used for DVDs. The machines read

the DVD bar code that peeks through the window on the envelope, print the address, then

send the envelope to the appropriate ZIP code bin for bulk mailing—dashing through

5000 envelopes an hour. The modifications of the machines were done secretly[…]

(Stross, 2010).

Apparently, no one in the outside world knew about Netflix’s modifications. After Blockbuster

finally managed to integrate its systems, the company still had to sharply raise subscription

prices for their unlimited-exchange plans in order to make up for their lack of efficiency.

The success of disruptors such as Netflix partly depends on their ability to strike a

balance between exploration, exploitation, and claim advantages and remain flexible in

modifying and evolving their business models. At its initial introduction in 1999, Netflix’s

business model was not different from their established brick-and-mortar counterparts (see

McGrath & MacMillan, 2009). Yet the company was able to quickly change course when

alternative opportunities presented themselves. By the end of 2010, Netflix had completed yet

another transformation that had successfully repositioned the firm as primarily an internet video-

streaming service.

Apple Revisited. We can apply these insights in examining Apple Inc.’s recent success in

disrupting several markets with their products. Apple is certainly not a newcomer in the

computer industry. As researchers such as Christensen (1997) would predict, the size and scale

of Apple’s operations requires that it continue to command a large enough share in the markets

they were successfully able to penetrate. Sure enough, after having established a dominant

design, the company’s product development strategy in each of its new product lines went into

an incremental innovation stage. This has been in much the same way that was observed with

Sony’s Walkman—another market disruptor that revolutionized music consumption at the time it

25

was introduced. Just like the Walkman two decades prior, the iPod became the dominant design

of its generation of products. However, iPod’s success went much further than that simple

analogy would suggest. Unlike Sony’s portable cassette player, iPod was not the first digital

player that was introduced into the market. Yet because of its integration with the iTunes music

service, its impact was much more pronounced. With the addition of iTunes, Apple’s evolving

business model shifted to a software platform supported with an ecosystem of content and

applications. Another strong component of success was the tight integration of software design

and hardware engineering capability.

By the winter of 2001, major music publishers such as Columbia and EMI were

increasingly feeling the damage inflicted by digital music piracy. Yet they were seemingly

incapable of coming up with realistic solutions to their rapidly shrinking market woes. Neither

were they able to converge upon a model of digital music distribution that received support from

all major players. Apple entered into this remarkably disjointed arena and offered its services as

middleman. Using its software design capabilities, Apple was able to create Fairplay, an easy-to-

implement digital rights management technology that required no effort on the part of music

publishers. The result was a unique combination of product and service, supported by an

effective synthesis of hardware and software design. On the one hand, customers could search,

buy, and organize reasonably priced, legally protected digital music using Apple’s iTunes

software. On the other, they could download their library of up to thousands of songs into their

meticulously engineered small-form-factor iPod music players to carry around with them. Thus,

it was the business model that combined the product with the service that caused an impact that

was far greater than the sum of its parts.

26

In the end, Apple’s success with the business model (which extended to iPhone and iPad)

was based primarily on the mindset (digital, small, convenient access, and ease-of-use) and

cumulative experience (i.e. in engineering components and software design). The hardest part, of

course was in the seamless integration of these factors into a viable business model. This is why

exploitation advantages are very important.

Notwithstanding popular magazine articles that give oversimplified accounts of Apple’s

success based on a couple of themes (e.g., obsessive secrecy, elaborate public relations

campaigns, or the supposedly dictatorial management style of CEO Steve Jobs) it should be clear

that Burt’s insights on an ideal equilibrium between the perspectives on social capital definitely

seem to be valid in Apple’s case. A big component of Apple’s success lies in their ability to

create the kind of skunkworks operation Burt (2005) has alluded to. What is perhaps more

fascinating is the fact that Apple’s leadership has been able to effectively create and sustain such

a successful operation within an organization of Apple’s size. Students of organizations are all-

too-familiar with the difficulties inherent in accomplishing this (see, for example, Ch. 8 in

Christensen, 1997).

27

CONCLUSION

In this chapter, our goal was to lay out the beginnings of a blueprint for research on market

disruption. We defined market disruption as occurring in three different ways, based on the

intensity of competition and threat experienced by market incumbents. We labeled these as

eroding, dominating, and obsoleting, in the order of lower to higher intensity. We also argued

that mindset, collective capital, and cumulative experience were three factors that are essential

for the creation of a business model that can have the potential to be disruptive. We contend that

through the synthesis of these ‘entrepreneurial factors’, entrepreneurs can gain valuable

exploration, exploitation, and claim advantages that will contribute to the creation of disruptive

business models.

As is true with most early attempts, our model has important limitations. We talked about

perhaps the most obvious of these in our introduction. In its current form, the model is simply

too general to have much explanatory power. However, we also see this as a strength—especially

in leading the way to further theory development and empirical research which we hope will

shed more light on the disruption process based on the general outline presented here.

Despite its shortcomings, the three-tiered typology of market disruption has the

advantage of being intuitively appealing. It offers a useful point of departure for researchers who

would like to delve further into the phenomenon of market disruption. We encourage other

researchers to look at how the three types of disruption are manifested in industries and markets

with which they have strong familiarity. Empirical research will also be valuable in developing

new metrics and meaningful measures that can increase the explanatory power of the blueprint

provided in this chapter.

28

Perhaps not surprisingly, our model did not have much to add in terms what really makes

a successful disruptive business model. To create a model with such predictive power is no doubt

a significant undertaking. Alas, the black box is still black at the end of the day. However, we

remain confident that the entrepreneurial factors that were outlined in the model hold the keys to

start coloring that box and unearthing new insights into the process of market disruption. As is so

often the case, it is time for us to turn to our colleagues and look forward to their contributions.

29

REFERENCES

Aldrich, H. 1999. Organizations Evolving, London: Sage Publications.

Beckman, C. M. 2006. The Influence of Founding Team Company Affiliations on Firm

Behavior. Academy of Management Journal, 49(4): 741-758.

Bhide, A. 2003. The Origin and Evolution of New Businesses, New York: Oxford University

Press.

Boeker, W. 1988. Organizational Origins: Entrepreneurial and Environmental Imprinting at the

Time of Founding. In G. R. Carroll (Ed.), Ecological Models of Organization: 33-51,

Cambridge, MA: Ballinger.

Bower, J. L., & Christensen, C. M. 1995. Disruptive Technologies: Catching the Wave. Harvard

Business Review, (January-February): 43-53.

Burt, R. S. 1997. The Contingent Value of Social Capital. Administrative Science Quarterly, 42:

339-365.

Burt, R. S. 2005. Brokerage and Closure: An Introduction to Social Capital, New York:

Oxford University Press.

Christensen, C. M. 1997. The Innovator's Dilemma: When New Technologies Cause Great

Firms to Fail, Boston: Harvard Business School Press.

Christensen, C. M. 2006. The Ongoing Process of Building a Theory of Disruption. The Journal

of Product Innovation Management, 23: 39-55.

Christensen, C. M., Anthony, S. D., & Roth, E. A. 2004. Seeing What's Next: Using the

Theories of Innovation to Predict Industry Change, Boston, MA: Harvard Business

School Press.

Christensen, C. M., & Raynor, M. E. 2003. The Innovator's Solution, Boston, MA: Harvard

Business School Press.

30

Covin, J. G., & Slevin, D. P. 2002. The Entrepreneurial Imperatives of Strategic Leadership. In

M. A. Hitt, R. D. Ireland, S. M. Camp, & D. L. Sexton (Eds.), Strategic

Entrepreneurship: Creating a New Mindset: 309-327, Oxford: Blackwell.

D'Aveni, R. A. 1999. Strategic Supremacy through Disruption and Dominance. Sloan

Management Review, 40(3): 127-135.

Fombrun, C. J. 1986. Structural Dynamics Within and Between Organizations. Administrative

Science Quarterly, 31(3): 403-421.

Fulton, A. R. 1985. The Machine. In T. Balio (Ed.), The American Film Industry: 27-42,

Madison, WI: The University of Wisconsin Press.

Gatignon, H., Tushman, M. L., Smith, W., & Anderson, P. 2002. A Structural Approach to

Assessing Innovation: Construct Development of Innovation Locus, Type, and

Characteristics. Management Science, 48(9): 1103-1122.

Ghemawat, P. 2006. Strategy and the Business Landscape (2nd ed.), Upper Saddle River, NJ:

Pearson Prentice Hall.

Granovetter, M. 1985. Economic Action and Social Structure: The Problem of Embeddedness.

American Journal of Sociology, 91(3): 481-510.

Hendricks, G. 1985. The History of the Kinetoscope. In T. Balio (Ed.), The American Film

Industry: 43-56, Madison, WI: The University of Wisconsin Press.

Hwang, J., & Christensen, C. M. 2008. Disruptive Innovation in Health Care Delivery: A

Framework For Business-Model Innovation. Health Affairs, 27(5): 1329-1335.

Ireland, R. D., Hitt, M. A., & Sirmon, D. G. 2003. A Model of Strategic Entrepreneurship: The

Construct and its Dimensions. Journal of Management, 29(6): 963-989.

Johnson, S. 2005. Everything Bad Is Good for You: How Today's Popular Culture Is Actually

31

Making Us Smarter, NY: Riverhead.

Keller, E. W., & Shanklin, W. L. 2005. The Perfect Storm for Disruptive Technologies. The

Marketing Management Journal, (Spring): 172-178.

Keller, E. W., & Shanklin, W. L. 2007. Canaries in the High-Tech Mine. Marketing

Management, (May/June): 37-41.

Kids in the U.S. Eyeing Big-Ticket Tech This Holiday Season | Nielsen Wire. 2010. nielsenwire,

http://blog.nielsen.com/nielsenwire/consumer/kids-in-the-u-s-eyeing-big-ticket-tech-this-

holiday-season/, November 28, 2010.

de Kluyver, C. A., & Pearce, J. A. 2006. Strategy: A View From the Top (2nd ed.), Upper

Saddle River, NJ: Pearson Prentice Hall.

March, J. G. 1991. Exploration and Exploitation in Organizational Learning. Organization

Science, 2(1): 71-87.

Markman, G. D., Gianiodis, P. T., & Buchholtz, A. K. 2009. Factor-Market Rivalry. The

Academy of Management Review, 34(3): 423-441.

McGrath, R. G., & MacMillan, I. C. 2000. The Entrepreneurial Mindset, Boston, MA: Harvard

Business School Press.

McGrath, R. G., & MacMillan, I. C. 2009. Discovery-Driven Growth: A Breakthrough Process

to Reduce Risk and Seize Opportunity, Boston, MA: Harvard Business School Press.

Merritt, R. 1985. Nickelodeon Theaters, 1905-1914: Building an Audience for the Movies. In T.

Balio (Ed.), The American Film Industry: 83-102, Madison, WI: The University of

Wisconsin Press.

Nelson, R. R., & Winter, S. G. 1982. An Evolutionary Theory of Economic Change,

Cambridge, MA: Belknap Press.

32

Page, S. E. 2007. The Difference: How the Power of Diversity Creates Better Groups, Firms,

Schools, and Societies, Princeton, NJ: Princeton University Press.

Papp, J., & Katz, R. 2004. Anticipating Disruptive Innovation. Research Technology

Management, (September-October): 13-22.

Ross, E., & Holland, A. 2006. 100 Great Businesses and the Minds Behind Them, Naperville,

IL: Sourcebooks, Inc.

Schatz, T. 1988. The Genius of the System: Hollywood Film-making in the Studio Era,

London: Faber and Faber.

Smith, R. 2007. The Disruptive Potential of Game Technologies. Research Technology

Management, 50(2): 57-64.

Sobel, R. S. 2008. Entrepreneurship. In D. R. Henderson (Ed.), The Concise Encyclopedia of

Economics: 154-157, Indianapolis: Liberty Fund.

Solomon, A. 1988. Twentieth-Century Fox: A Corporate and Financial History, Metuchen,

NJ: Scarecrow.

Stross, R. 2010, September 19. Why Bricks and Clicks Don't Always Mix. The New York

Times, New York.

Thomas, L. G. 1996. The Two Faces of Competition. Organization Science, 7(May-June): 221-

242.

Thorngate, W. 1976. "In General" vs. "it depends": Some comments on the Gergen-Schlenker

debate. Personality and Social Psychology Bulletin, 2: 404-410.

Wakabayashi, D. 2009, November 11. Apple Emerges as Nintendo's Game Rival - WSJ.com.

WSJ.com,

http://online.wsj.com/article/SB10001424052748704402404574527572534809890.html?

33

ru=yahoo&mod=yahoo_hs, November 28, 2010.

Weick, K. E. 1979. The Social Psychology of Organizing (2nd ed.), Reading, MA: Addison-

Wesley.

34

TABLES AND FIGURES

35

Table 1: Market Disruption by Apple Products (2001-2010)

Type of Market Disruption & Markets That Were Effected

Product/Service Eroding Dominating Obsoleting

iPod & iTunes (2001-present)

iPod Touch

Handheld Gaming Consoles

Music retailers6

Portable Media Players Non-digital Portable media players

(CD players, SONY’s Walkman,

etc.)

iPhone (2007-present) Mobile phones7

Handheld Gaming Consoles

Smartphones

Portable Media Players

iPad (2010-present) Netbooks

Laptops (to a lesser degree)

Handheld Gaming Consoles

eBook Readers

Portable DVD Players

Tablets (new category)8 Netbooks

(iPad and future competitors

in the Tablet PC market are

likely to increase the pace of

convergence between laptop

and netbook categories,

leading to the demise of

netbooks)

6 The iPod+iTunes business model arguably contributed to the eventual demise of the major music retail chains such as Tower Records (this is by no means

complete, but the effect has been significant—and the market share of retailers has been waning considerably) 7 As of this writing, smartphones still represent a much smaller category within the mobile phone market. But this is likely to change sooner than previously

anticipated—partly due to the success of the iPhone. 8 Apple did not create the tablet category. Some experts believe that Microsoft was the first company to introduce the form-factor because of a tablet PC

prototype that was demonstrated by the company founder Bill Gates during a keynote address in 2000. However, Apple was the first company to create a viable

market for the tablet form-factor, largely using the same design and user interface capabilities—as well as the application ecosystem—that was initially tested

with the iPhone.

36

Cumulative

Experience

Collective

Capital

Mindset

Disruptive

Business

Model

Eroding Disruption

Dominating Disruption

Obsoleting Disruption

Exploration

Advantages

Exploitation

Advantages

Claim

Advantages

Figure 1: A Model of Market Disruption

Related Documents